ba 427 – assurance and attestation services lecture 20 the audit: phase i

Post on 21-Dec-2015

218 views

TRANSCRIPT

BA 427 – Assurance and Attestation Services

Lecture 20The Audit: Phase I

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Client acceptance and continuation New clients

Evaluate management’s integrity, reputation, and financial stability.

Evaluate client business risk. Evaluate industry risk. Communicate with predecessor auditor. Understand the services desired by the

client, and evaluate the accounting firm’s desire and ability to deliver those services.

Communications with predecessor auditor Initiated by the successor auditor. Required, under GAAS (SAS 84), prior to

accepting the engagement. Requires permission of the client. Old working papers are normally made

available.

Client acceptance and continuation

Existing clients Ongoing evaluation of management integrity

and the working relationship between the auditors and client management.

Evaluation of trends with regard to client business risk and industry risk.

Ongoing evaluation of the services desired by the client, and the accounting firm’s desire and ability to deliver those services.

Client acceptance and continuation

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Initial Planning Prepare an engagement letter. Select the audit team. Evaluate the client’s internal audit

function, if any. Evaluate the need for outside

specialists.

Prepare an engagement letter and obtain a signed copy from the client. The engagement letter should specify:

Nature of services to be rendered Deadlines for completing the audit Assistance to be provided by client

personnel Fees Limitations on the auditor’s

responsibilities

Initial Planning

Select the audit team According to the first General Standard of

GAAS: “The audit is to be performed by a person or persons having adequate technical training and proficiency as an auditor.”

According to the first Standard of Field Work of GAAS: “The work is to be adequately planned and assistants, if any, are to be properly supervised.”

Initial Planning

Evaluate the internal audit function This evaluation affects the nature, timing

and extent of external audit procedures. The external auditor assesses the

competence and objectivity of the internal audit function.

Initial Planning

Using the work of a specialist Examples include actuaries and appraisers. Auditor must be satisfied with the

qualifications and reputation of the specialist. (The specialist need not be independent of the client.)

The auditor should understand the specialist’s methods and assumptions, consider whether the specialist’s findings support the assertions, and test the data provided by the client.

Initial Planning

Using the work of a specialist The client, auditor and specialist should

document their understanding of the nature of the work to be performed.

The audit report normally does not refer to the work of the specialist.

Initial Planning

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Assess client business risk Client business risk is the risk that the

client will fail to achieve its objectives. Sources of client business risk:

Industry and external environment Business operations and processes Management and governance, objectives

and strategies, measurement and performance

Assess client business risk Industry and external environment

Industry-wide risks (regulation, deregulation, economic trends, competition).

Inherent risks typical for companies in the industry (e.g., inventory obsolescence, regulatory approval).

Accounting issues relevant to the industry.

Assess client business risk Business operations and processes

Key products and associated risks. Key customers and associated risks. Key suppliers and associated risks. Tour the plant and offices. Identify related parties and related party

transactions.

Assess client business risk Management and governance, objectives

and strategies, measurement and performance Review corporate charter and bylaws. Review the company’s code of ethics. Review minutes of meetings. Identify terms of key contracts and legal

obligations. Identify the client’s key performance

measures.

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Preliminary analytical procedures Analytical procedures conducted in the

planning phase of the audit serve the following objectives: Understand the client’s industry and

business Assess going concern Indicate possible misstatements Reduce detailed tests

Preliminary analytical procedures Analytical procedures are defined by

SAS no. 56:“Evaluations of financial information made by a study of plausible relationships among financial and nonfinancial data … involving comparisons of recorded amounts to expectations developed by the auditor.”

Preliminary analytical procedures Types of analytical procedures:

Compare client data to industry data. Compare current period to prior periods. Compare current period to budget. Compare financial data for internal

consistency between accounts. Compare financial data to expected results

based on operational data.

Preliminary analytical procedures Ratios used in analytical procedures:

Cash ratio, quick ratio and current ratio. A/R turnover and A/R days to collect. Inventory turnover and inventory days to

sell. Debt to equity EPS Gross profit percentage ROA and ROE

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Set materiality and overall audit risk

Materiality as defined by the FASB:The magnitude of an omission or misstatement of accounting information that, in the light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the omission or misstatement.

Set materiality and overall audit risk

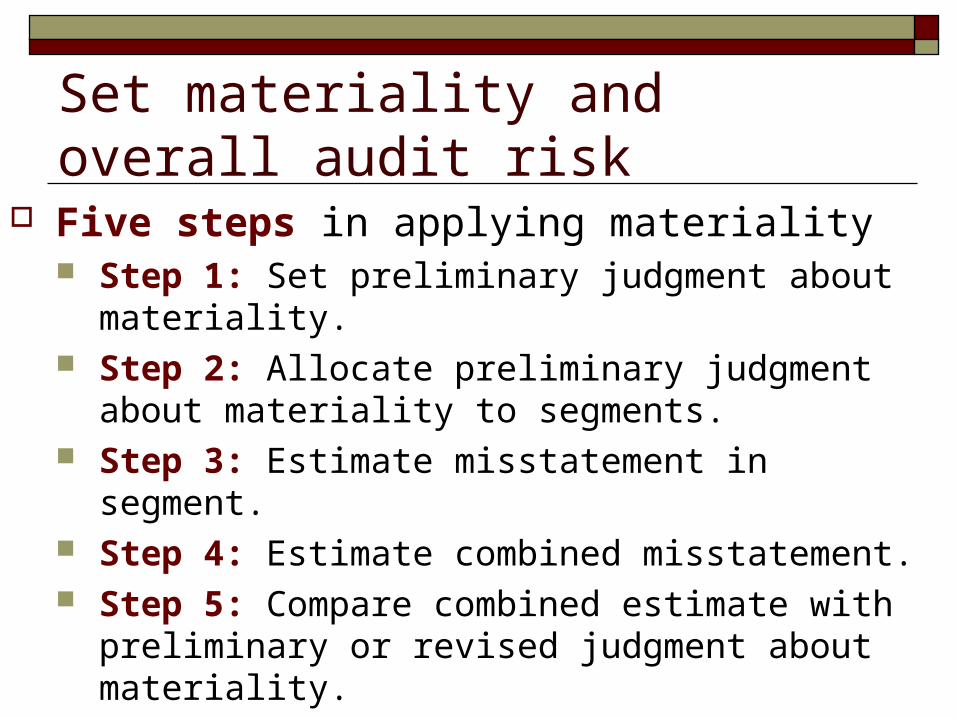

Five steps in applying materiality Step 1: Set preliminary judgment about

materiality. Step 2: Allocate preliminary judgment

about materiality to segments. Step 3: Estimate misstatement in segment. Step 4: Estimate combined misstatement. Step 5: Compare combined estimate with

preliminary or revised judgment about materiality.

Set materiality and overall audit risk

The first two steps are the only steps that occur in the planning phase of the audit. Step 1: Set preliminary judgment about

materiality. Step 2: Allocate preliminary judgment

about materiality to segments.

Set materiality and overall audit risk

Step 1: Set preliminary judgment about materiality. The maximum amount by which the

statements could be misstated and still not affect the decisions of reasonable users.

One of the most important decisions the auditor makes.

Requires considerable professional judgment.

Professional standards do not say 5% or 10!

Set materiality and overall audit risk

Step 1: Quantitative factors in setting materiality. Materiality is a relative concept. Hence, the auditor must identify one or

more bases by which to set materiality. Net income before taxes is a common base. Other bases include: net sales, gross profit,

total assets, current assets, owners’ equity.

Set materiality and overall audit risk

Step 1: Qualitative factors in setting materiality. Misstatements that affect contractual

obligations. Misstatements that affect a trend in

earnings. Misstatements that turn a loss into a profit

(or vice versa). Misstatements arising from irregularities.

Set materiality and overall audit risk

Step 2: Allocate preliminary judgment about materiality to individual accounts. This allocation facilitates planning the audit

of individual balance sheet line-items. This allocation identifies the tolerable

misstatement in each account. The sum of tolerable misstatements can

exceed overall materiality. The allocation must consider the possibility

that a significant misstatement in an individual account might affect F/S users.

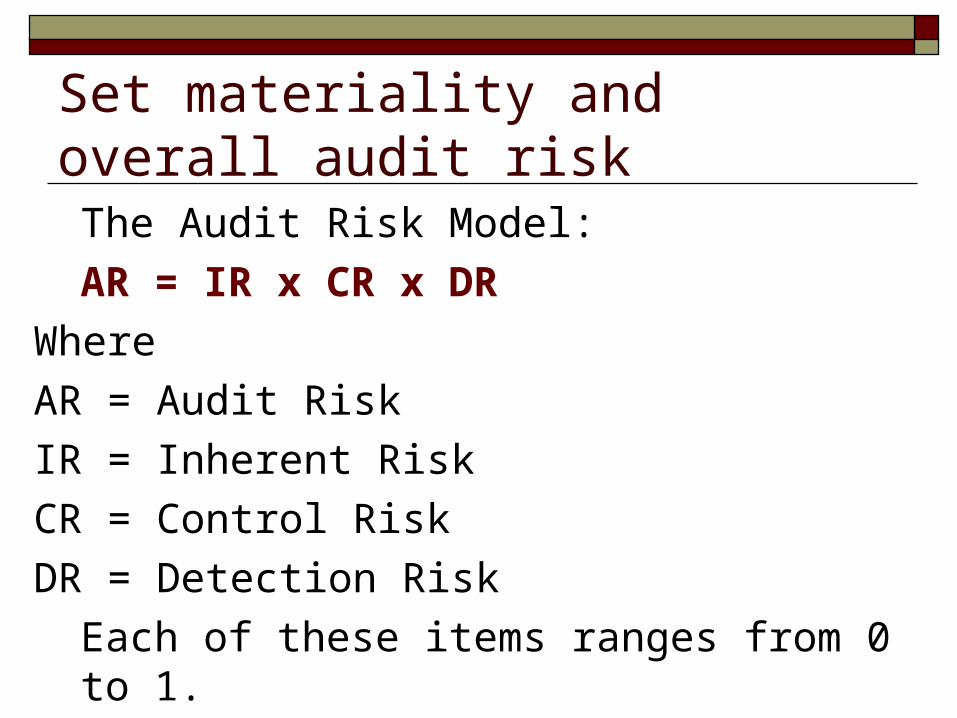

Set materiality and overall audit riskThe Audit Risk Model:

AR = IR x CR x DRWhereAR = Audit Risk IR = Inherent RiskCR = Control RiskDR = Detection Risk

Each of these items ranges from 0 to 1.

Set materiality and overall audit risk

The Audit Risk Model (A.R.M.):AR = IR x CR x DR

Audit Risk: This is the likelihood that the F/S are materially misstated. It is a probability, and a choice variable by the auditor. 5%, 1%, or 1/10 of 1% are common objectives.

The A.R.M. can be applied separately for each balance sheet account. (Even so, the auditor might choose the same level of Audit Risk for each account).

Set materiality and overall audit risk

Engagement risk is the risk the audit firm will suffer a loss arising from the client relationship. Engagement risk is closely related to, but

not synonymous with, client business risk. Auditors disagree about whether

engagement risk should be considered in planning the audit.

In other words, should some audits provide more assurance than others?

Set materiality and overall audit risk

If Engagement Risk Affects Acceptable Audit Risk, then consider: The degree to which external users will rely

on the financial statements. Related factors are client size, distribution of ownership, and nature and amount of liabilities.

The likelihood that the client will experience financial difficulties.

Management integrity.

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Assess Inherent Risk Inherent risk (IR):

The auditor’s assessment of the likelihood that there are material misstatements before considering the effectiveness of controls.

In assessing inherent risk, the auditor considers such factors as: Nature of the client’s business Initial versus repeat engagement Nature of accounting judgments and estimates Non-routine transactions

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Assess control risk Control Risk (CR):

The auditor’s assessment of the likelihood that material misstatements are not prevented or detected by the client’s internal controls.

Hence: CR x IR is the likelihood that the account is materially misstated as presented to the auditors.

To set CR below 1, the auditor will have to understand controls and test controls.

Assess control risk Control Risk (CR):

Therefore, if the auditor does not want to test internal controls, CR must be set at 1, regardless of the actual effectiveness of internal controls.

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Assess fraud risk We discussed this topic in connection

with SAS No. 99.

Lecture 20 – Phase I Client acceptance and continuation Initial planning Assess client business risk Preliminary analytical procedures Set materiality and overall audit risk Assess inherent risk Assess control risk Assess fraud risk Audit evidence and the audit program

Audit evidence and the audit program

Third standard of field work: Sufficient competent evidential matter

is to be obtained through inspection, observation, inquiries, and confirmations to afford a reasonable basis for an opinion regarding the financial statements under audit.

Competence of evidential matter Sufficiency of evidential matter

Audit evidence and the audit program

Competence of evidential matter: Evidence should be Valid (objective and reliable)

Independent sources are better than sources internal to the organization.

Direct evidence (from physical examination, observation, computation and inspection) is more persuasive than indirect evidence.

Relevant (including timely)

Audit evidence and the audit program

Sufficiency of evidential matter Five ways to accumulate evidential matter:

Procedures to obtain an understanding of controls

Tests of controls Substantive tests of transactions Analytical procedures Tests of details of balances

Audit evidence and the audit program

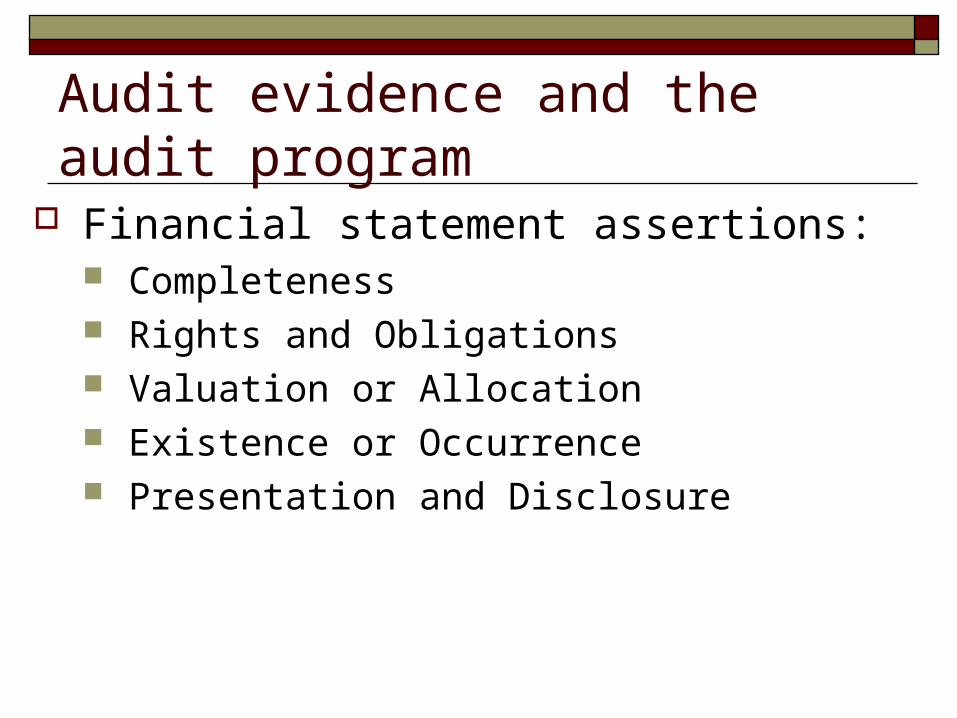

Financial statement assertions: Completeness Rights and Obligations Valuation or Allocation Existence or Occurrence Presentation and Disclosure

Audit evidence and the audit program

Financial statement assertions: Completeness

Whether all transactions and accounts that should be presented in the financial statements are included.

Rights and Obligations Valuation or Allocation Existence or Occurrence Presentation and Disclosure

Audit evidence and the audit program

Financial statement assertions: Completeness Rights and Obligations

Whether, at a given date, all assets are the rights of the entity and all liabilities are the obligations of the entity.

Valuation or Allocation Existence or Occurrence Presentation and Disclosure

Audit evidence and the audit program

Financial statement assertions: Completeness Rights and Obligations Valuation or Allocation

Whether the assets, liabilities, revenues and expenses of an entity have been included in the financial statements at the appropriate amounts, in conformity with GAAP.

Existence or Occurrence Presentation and Disclosure

Audit evidence and the audit program

Financial statement assertions: Completeness Rights and Obligations Valuation or Allocation Existence or Occurrence

Whether assets and liabilities exist at a given date and whether recorded transactions have occurred during a given period.

Presentation and Disclosure

Audit evidence and the audit program

Financial statement assertions: Completeness Rights and Obligations Valuation or Allocation Existence or Occurrence Presentation and Disclosure

Whether financial statement components have been properly classified, described, and disclosed.

Audit evidence and the audit program

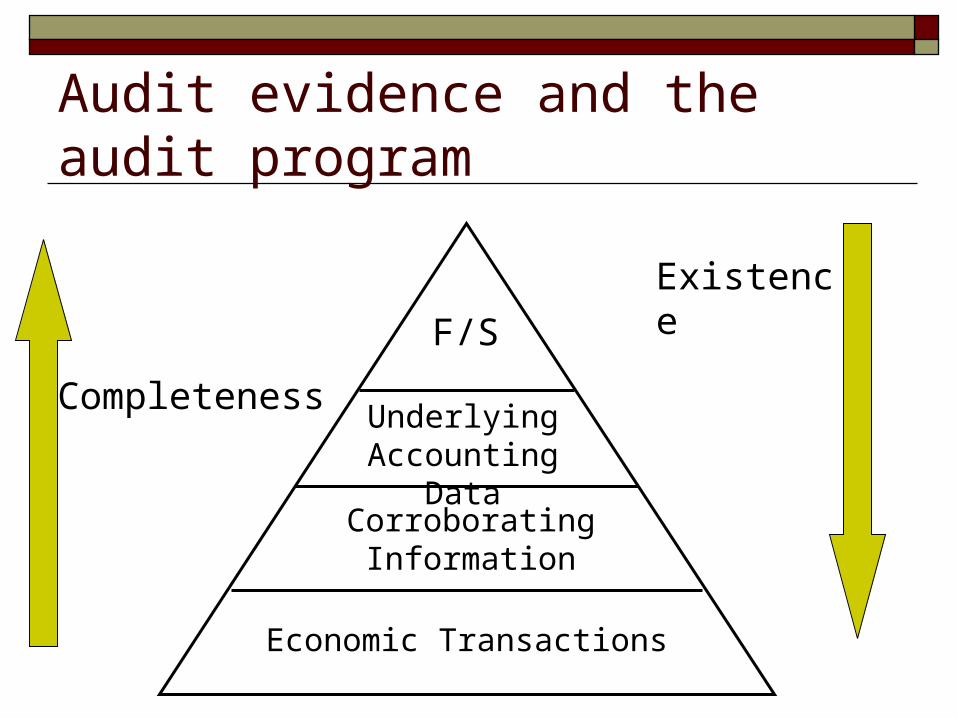

F/S

Underlying Accounting Data

Corroborating Information

Economic Transactions

Existence

Completeness

Audit evidence and the audit program

Types of Evidence Physical evidence of tangible assets Confirmation by a third party Documentation, internal and external Observation to assess certain activities Client inquiry, can be written or oral Reperformance Analytical procedures

Audit evidence and the audit program

Audit workpapers Permanent files (used every year)

Articles of incorporation and bylaws Contracts and debt agreements Organization chart Internal control analyses

Audit evidence and the audit program

Audit workpapers Current files (annual)

The Audit Program Working Trial Balance Lead Schedules Tests of controls Substantive tests

Audit evidence and the audit program

Assets Liabilities & EquityCash

Accounts receivable

Inventory

Prepaid assets

Property, plant and equipment

Other assets

Total

Accounts payable

Other current liabilities

Long-term debt

Shareholders’ equity

Common stock

Retained earnings

Total liabilities and equity

Audit evidence and the audit program

Assets Liabilities & EquityCash

Accounts receivable

Inventory

Prepaid assets

Property, plant and equipment

Other assets

Total

Accounts payable

Other current liabilities

Long-term debt

Shareholders’ equity

Common stock

Retained earnings

Total liabilities and equity

Audit evidence and the audit program

Working Trial Balance

Cash

Accounts receivable

Inventory

Prepaid assets

Property, plant and equipment

Other assets

Total

AccountPrior year

Trial balance

Final balance

Adjusting entries

Reclassifications

Audit evidence and the audit program

Lead Schedule: Cash

Sunwest Bank – general account

Sunwest Bank – Payroll account

First Federal Savings and Loan

Petty cash

Total cash

AccountPrior year

Trial balance

Final balance

Adjusting entries

Reclassifications

Audit evidence and the audit program