“back office procedures in debt...

TRANSCRIPT

1

“BACK OFFICE PROCEDURES IN DEBT MANAGEMENT”

BY THEMBA ANDREAS DLAMINI

RESEARCH DEPARTMENT CENTRAL BANK OF SWAZILAND

MENTOR: MR MACDONALD BANDA

DEBT MANAGEMENT SECTION CROWN AGENTS

A TECHNICAL PAPER SUBMITTED IN PARTIAL FULFILMENT

OF THE AWARD OF MEFMI FELLOWSHIP PROGRAMME

JULY 2009

2

Table of Contents List of Acronyms and Abbreviations iv

Acknowledgements v

Executive Summary vi

Section Page

Section 1: Introduction 8

1. Background 8

Section 2: Best practices in Back Office Operations 10 2.1 Legal Framework 11 2.2 Organisational Framework 13 2.3 Procedures 16 2.4 Staffing 18 2.5 Technology 19 2.6 DeMPA Tool Functions on Back Office 21

Section 3: Back Office Operations in sampled MEFMI countries 15

3.1 Legal Framework 25 3.2 Government Policy on Debt 27 3.3 Institutional Arrangements 28 3.4 Procedures 32 3.5 Staffing 36 3.6 Technology 38

Section 4: Back Office functions available in CS-DRMS 40 4.1 Overview 41 4.2 Operational Functions 49 4.3 Exchange Rates and Interest Rates 41 4.4 Reporting Functions 49 4.5 Database Management Functions 50 4.6 Future Plans for CS-DRMS 50

Section 5: Ideal Back Office operations in MEFMI Member States 62 5.1 Overview

5.2 Critical Analysis of DMO Models

5.3 Ideal Back Office Operations in MEFMI members states

Section 6: Recommendations for CS-DRMS

3

Appendices Page

Appendix A: UK Government Securities: gilts 73

Appendix B: Objectives of UK Government Debt Management 75

References 77

4

List of Acronyms and Abbreviations

AfDF - African Development Fund

BADEA - Arab Bank for Economic Development in Africa

BEAD - Budget and Economic Affairs Department of the Ministry of

Finance

BES - Book Entry System

BIS - Bank for International Settlements

CBDMS - Computer Based Debt Management Systems

CBS - Central Bank of Swaziland

ComSec - Commonwealth Secretariat

CS-DRMS - Commonwealth Secretariat Debt Recording and

Management System

CTP - Customized Training Programme

DMFAS - Debt Management Financial and Analysis System

DMO - Debt Management Office

DSA - Debt Sustainability Analysis

EIB - European Investment Bank

FDP - Fellows Development Programme

FMAD - Fiscal and Monetary Affairs Department of the Ministry of

Finance

GDP - Gross Domestic Product

HIPCs - Highly Indebted Poor Countries

IBRD - International Bank for Reconstruction and Development

ICT - Information and Communication Technology

IDA - International Development Association

IFAD - International Fund for Agricultural Development

IMF - International Monetary Fund

LICs - Low Income Countries

MEFMI - Macroeconomic and Financial Management

Institute of Eastern and Southern Africa

OECD - Organization for Economic Co-operation and

Development

UNCTAD - United Nations Conference on Trade and Development

5

ACKNOWLEDGEMENTS

The paper would not have been a success without the guidance of

my mentor, Mr MacDonald Banda of Crown Agents. His continuous

and timely guidance was indeed invaluable. Further accolades go to

MEFMI Secretariat, ComSec Debt Management Section and the UK

Debt Management Office.

6

Executive Summary

Whether centralized or decentralized, the way forward with respect to

enhancing the institutional and coordination structures for debt management

would be to regularly update and implement appropriate legal frameworks

and coordinated policies; review institutional roles and responsibilities as and

when necessary; segregation of duties in debt management and strengthen its

supervision so as to reduce inefficiencies and avoid duplication or gaps;

provide adequate resources; train and retain mass of staff with requisite

expertise and experience; develop, document and implement systems and

procedures that enhance debt office operations and institutional memory and

adapt relevant experiences to individual country circumstances.

Coordinated analysis and implementation of fiscal and monetary policies and

effective debt and aid policies including the development of domestic

financial markets will remain an important aspect of best practice in debt

management. To achieve these outcomes, capacity building initiatives will

continue to play a pivotal role.

Choosing the best Computer Based Debt Management System is also critical.

The support of ICT department is also vital for debt managers especially the

back office. The system should be well maintained, including the local area

network plus the interface this technology now gives with other Integrated

Financial Management Systems that it may be used along with.

It should be noted that use of the system would require a highly performing

hardware to run the very specialized software used with the debt recording

system in use. There is therefore a strong need for Executives to decide on the

choice of the system since it implies a lot of financial resources. Backups,

preferably done by ICT staff, should be run in order to allow for recovery of

information stored in the system in the event of disaster.

7

Section 1: Introduction

1. Background

The institutional perspective of debt management can be broadly categorized

into three functions, namely; Front Office, Middle Office and Back Office. This

paper’s focus would be on the back office procedures in debt management.

Before pursuing that, it may be necessary to highlight that: “the main

objective of public debt management is to ensure that the government

financing needs and its payment obligations are met at the lowest possible cost

over the medium to long run, consistent with a prudent degree of risk”1. Public

debt management cannot be effectively realized if the back office fails to

deliver the necessary information to middle and front offices. It is the back

office’s responsibility to ensure that debt data is accurate, exhaustive,

comprehensive, up-to-date and usable by the other two (front and middle

offices) functional aspects of debt management.

Approaches to debt management differ from country to country, between

developed, emerging economies and developing countries. The size of the debt

management office and/or size of debt portfolio may also provide guidance on

the approach to be used in debt management. Central to this difference is the

structure and role of the back office function.

The objectives of this paper are therefore threefold; firstly, is to research and

describe international best practices in the area of debt management with

particular emphasis on back office procedures. Secondly, is to analyze debt

management functions and the role of back office in selected MEFMI member

countries. Lastly, is to identify weaknesses and recommend ideal back office

procedures for debt management including the use of CS-DRMS that would suit

1 World Bank and IMF, (2001, 2003 and 2007), Guidelines for Public Debt Management, Washington

MEFMI member states. The paper would, therefore, provide practical guidelines

to staff involved in back office operations and recommends best practices for

MEFMI member states.

Section 2: Best practices in Back Office

Operations

2. Best practices in Back Office Operations

2.1 Legal Framework

It is indeed a challenge to establish institutional arrangements that ensure

effective debt management. Best practice would require institutional

arrangements to have: Legal framework; Policy coordination; Transparency and

accountability; Clarity of roles, responsibilities and objectives; Organizational

framework and Management of internal controls.

Sound institutional framework call for clear legislative framework that would

define goals, authorities and accountabilities. There should be well-defined

institutional responsibilities, which clearly specify the mandates and roles of

key stakeholders. A clearer accountability arrangement, which articulates

reporting arrangements, should be in place. To be precise, it is of paramount

importance that the allocation of responsibilities among the ministry of

finance, central bank, or a separate debt management agency, for debt

management policy advice, and for undertaking debt issues, secondary market

arrangements, depository facilities, clearing and settlement arrangements for

trade in government securities, should be publicly disclosed.

An ideal legislative for debt management should address authority to borrow,

borrowing limits, issue and management of guarantees, on-lending and/or

direct lending arrangements. Such would entail separate acts or a single act

governing both foreign and domestic borrowing. Usually, it is the sole

responsibility of the Minister of Finance after Parliament approval to borrow

and issue guarantees. However, for domestic borrowing, like Issuance of

Government Treasury Bills and Bonds, such authority is usually delegated to

central banks. Further, there should be regulations to provide for consultations

with other agencies involved. There should also be establishment of a Debt

Management Office (DMO) in the ministry of finance or as a separate entity. A

high-level debt policy committee should also be established. The committee

should deal with policy issues, which the government will pursue. The primary

objective of the policy is to ensure that borrowing for government financing

needs are met at optimal cost over the medium to-long-term, consistent with a

prudent degree of risk to ensure that the debt remains sustainable. The policy

document should also allow government to pursue a debt strategy consistent

with laid down policy guidelines. In that regard, the debt management strategy

should focus on close monitoring and regular assessment of the debt portfolio.

Sound institutional framework also seeks to ensure that borrowing limits are

specified for both foreign and domestic borrowing. Separate ceilings should

also be set for government guaranteed debt and for unguaranteed debts of

state enterprises. Such legislation should be tightened such that there are no

loopholes to allow certain kinds of borrowings to be unrestricted. It is also

important that the limits be increasingly set within the framework of fiscal

responsibility legislation. Thus, close co-ordination of public debt policy with

monetary and fiscal policies will result in sound public debt management.

In summary, it is fundamental that the Legal Framework for Public Debt

Management consists of three (3) bases. Firstly, it is important that all

borrowings are done through the same entity; e.g. Ministry of Finance.

Secondly, it should be authorized by the highest state authority (Parliament)

with delegation of powers to the entity that actually manages the debt. Lastly,

the debt manager should report on a regular basis to the highest state

authority. These facts should be stated explicitly in law. Reporting to

Parliament increases transparency and strengthens accountability. Debt

statistics reports should be timely, coherent and accessible even to general

public. Further, the Public Debt Law should define; the actors involved in

public debt management, the rules and regulations, their interactions and

responsibilities.

The above requirements for a model debt management operations is essential

since a weak legislative framework would often leads to: unauthorized persons

contracting loans; stipulated borrowing limits contravened; loan funds

misappropriated; no sanctions applied when laws are broken and moreover

leads to fragmented approach to debt management. The impact of the weak

legislative framework would be; unchecked growth in debt, high costs since

debt would often be contracted on poor terms, potential macroeconomic

instability and slow market development.

2.2 Organisational Framework

Institutional arrangements for debt management differ from country to

country. The location of debt office (whether it is at the ministry of finance,

central bank or shared amongst these institutions or even as a separate entity)

depends on the Institutional arrangements that suit a particular country.

Legislation should therefore establish an efficient institutional structure to

manage the debt through any of structures mentioned above, which are further

discussed below.

2.2.1 Setting up Debt Management Office in Ministry of Finance

Setting up a DMO in the Ministry of Finance facilitates the smooth interaction

between the ministry economic and financial forecasting functions and

preparation of borrowing programme. This will also enable all debt transactions

(drawdowns and repayments) to be timely fed in the budget process. Further,

as custodian of public funds, DMO in the Ministry of Finance is good since the

Ministry is in most cases the only entity legally entrusted to contract and

manage public debt on behalf of the government.

2.2.2 Locating the Debt Management Office in Central Bank

Setting of a DMO in the Central Bank may lead to potential conflict of interest

with fiscal authorities. The Central Bank, to control inflation may wish to raise

interest rates and such may not go down well with government in that it will

certainly increase the cost of borrowing in the domestic economy and also lead

to low economic growth since credit would be expensive. To avoid conflict of

interest and allow for segregation of duties, DMO should be removed from the

Central Bank since the Bank cannot fairly continue issuing government

securities and at the same time be responsible for setting interest rates. This

was the main reason for the establishment of the United Kingdom Debt

Management Office.

On the other hand, location of a DMO in the Central Bank may fit if the

institution has human capacities to handle such a task. This will hold true

where Ministries of Finance has no such capacity mostly associated with staff

turnover as a result of poor remuneration associated with civil servants salary

scales. Proper coordination with the Ministry of Finance (being the designated

legal borrowing authority) must under such arrangement be at its best.

2.2.3 Shared debt management responsibilities between Ministry and

Central Bank

Under this set-up, it is crucial that the Ministry of Finance, as custodian of all

public borrowing, is at the forefront in public debt management. However, it

would still be important to specifically define the roles to be played by the

different entities involved in public debt management in order to eliminate

conflict that might arise. For example, the Central Bank may want to increase

interest rates to curb inflation, whilst Ministry of Finance would see that as an

increase to the cost of borrowing in the domestic market. Through proper

coordination, such potential conflicts would be eliminated.

For developing countries, due to the size of the debt offices and the strong need

for consistent co-ordination within the institutions and departments involved in

public debt management such arrangement may hold.

2.2.4 Separate and independent Debt Management Office

Internationally, it is ideal to have a debt office as a separate and independent

entity. That also eliminate staff turnover as a result of poor remuneration

aligned to government salary scales. It allows greater focus on debt management

policy and separates fiscal policy advice from debt management. It also provides

greater operational independence and increases success in obtaining budget

resources.

Managing the government’s public debt requires controls. There are daily

internal controls set in into the DMO activities that are based on segregation of

duties and responsibilities. There are also regular controls within the DMO and

by Internal Auditors. The controls implanted in the DMO activities vary according

to the functions of the different offices namely; front, middle and back offices.

Then, there would be the senior management who would control and monitor

that each one of the offices perform their duties efficiently and in due time.

The controls involved in back office operations, the focus of this paper, include:

the need to have a legally binding and enforceable contract with all

creditors/borrowers and the central government in its capacity as a

borrower/creditor including the issuance of guarantees; quality of debt data

(should be complete and up-to-date) for all central government debt records

including records of holders of government securities; well documented

procedures for settlement of transactions, maintenance of financial records and

for accessing the Computer Based Debt Management Systems (CBDMS) including

the payment systems (ICT specialist therefore should tighten controls access

rights); meet statutory reporting requirements; systems for contracting loans

and issuance of guarantees. The key requirement in these controls is that

someone must ensure that all such are adhered to which can be easily achieved

and/or monitored where the DMO is set as a separate and independent entity.

Finally, the activities in the back office should be subject to scrutiny by national

audit bodies. Standards of external audit practice should be consistent with

international standards.

2.3 Procedures

The tasks of a back office include debt recording and validation, debt

accounting, quality control and debt reporting2. On the other hand, the

objective of the back office is to create and maintain a high quality up-to-date

database; high quality of the debt portfolio that allows timely registration,

disbursements, and servicing as well as to produce accurate statistical

information. The back office functions therefore comprise the administration

of the full cycle of a contract, from loan contracting to its full repayment.

Back office procedures can broadly be categorized into two, namely; the

Recording and the Operating functions. These basic functions of the back office

are critical for the other operational function of the middle and front offices to

be carried out.

2.3.1 Recording function

The recording function is the ‘base’ of all the other functions of debt

management. It involves; collecting, storing, processing and validating:

2 MEFMI, (2005) , Public Debt Management, Procedures Manual, Harare

2.3.1.1 Collecting

Best practice entails that all information of different categories of debt; to

include loan contracts, disbursements, repayments,

cancellations/enhancements, restructuring etc should be collected timely.

2.3.1.2 Storing

The back office, since it is in charge of the implementation and maintenance of

the CS-DRMS would further use the system to electronically store scanned

documents in the system or the information can be physically stored in

classified files.

2.3.1.3 Processing and Validating

Once all the debt data is stored, the system would be used to perform tasks

such as capturing basic loans details, forecasting rules, actual transactions etc.

The data would further need to be validated implying the need for using

internal checks within the system or through reconciliation of debt data

periodically with creditors.

2.3.2 Operating function

The operating function would perform functions such as; triggering of

disbursements in due time, pay without falling into arrears, verify if creditors

claim correct amounts, and notify budget department and treasury through

IFMIS, order debt service etc. The operating function would also produce debt

service and disbursements for the budget department for inclusion in the

incoming financial year’s budget.

Basically, operating functions entails processes that allow the back office to

function. This section looks at the operational aspects of back office;

2.3.2.1 Debt Servicing

Sound practice entails that the institution should have systems and/or

procedures that result in accurate and timely debt servicing. System in place

should also facilitate tracking of payments to establish and analyze

unwarranted discrepancies. There should be a way of monitoring arrears and

penalties. System should also generate debt service payments due such that

debt service obligations are not solely relied upon instruction or bills from

creditors.

2.3.2.2 Debt data dissemination

The dissemination of data by way of reports generation is the final output of all

the recording and validations made. Users of debt statistics would include

international financial institutions, national and foreign users, private users

etc. Over and above statistical bulletins published, posting of the debt

statistics on a website is necessary to reach a wide range of users.

2.4 Staffing

It is a universal problem for governments to attract and retain skilled personnel

for debt management offices. Staff in DMO should have varying educational

background combining; ICT, financial, macroeconomic and public policy skills.

Such a profile is highly demanded in private sector resulting in alarming rate of

staff turnover in DMOs. The poor remuneration of public servants when

compared to private sector also add in ‘facilitating’ these skilled personnel

early exit for greener pastures and retaining them might be an impossible task

to achieve. There is often no career path and skills development in

government structure and capacity building is often ignored until one is faced

with a crisis. Such hinders the proper functioning of a DMO and needs to be

addressed at executive’s level.

The DMO is not the only government department affected by this but other

sectors as well. However, the argument is that DMO deserves special attention

considering that public debt is often a major share of expenditure within the

national budget. The DMO should have regular training programs tailored to the

ever changing global debt management challenges thus covering all the

different aspects of public debt monitoring and management.

2.5 Technology

It is undoubted that computer based debt management systems bring flexibility

and rapidity to the debt data processing and thereby allow debt managers to

review the information that are not otherwise practicable. Within

minutes/seconds, a CBDMS can compute the current balances of hundreds of

loans, sum and print reports by borrower/creditor category, remaining

maturities, economic sector etc. The CBDMS does not operate in isolation

though; it has to be operated by a trained user capturing accurate and complete

debt data to produce reliable information.

Today, it is totally impossible to effectively manage debt without a performing

computerized system. The Executives of an Institution should diligently choose

the right CBDMS considering the costs involved, then the hardware needed

because of the operating and application software, which are complex and

heavy, implying the need for a highly performing hardware to run a very

specialized software. Executives may decide to choose a standard system

developed by one of the international suppliers (e.g. UNCTAD’s DMFAS or

ComSec’s CS-DRMS), a domestic in-house developed system or outsourcing the

development of the system to an external software developer.

Developing an in-house system might be a best strategy since it would be

tailored towards the needs of that institution managing the debt but it comes

with massive costs. These include hiring of highly qualified ICT staff and

retaining them, debt managers capable of drafting and reviewing the

specifications for the ICT team and the time length. Outsourcing the

development of the system is the worse decision. Reasons being: DMO ICT team

is not directly involved which might lead to problems regardless of the

documentation supplied with the system, documentation itself might be

incomplete, contract with supplier is bound to end leaving system obsolete if

DMO ICT fails to fix any emerging deficiencies.

Choosing a Standard Software package, CS-DRMS in my case, is the best option.

This system has been tried and tested – it PERFORMS if used properly! Also,

frequent forums organized by the developers to interact with users have made

the system less vulnerable such that it has fewer operating problems than in-

house developed or outsourced systems. Further, choosing CS-DRMS decreases

the need to maintain a full group of developers within DMO’s ICT departments

since they would only be needed for maintenance of the system and local area

network , database management and security procedures like regular backups.

Use of CS-DRMS also avoids physical hardcopy filing systems since all legal loan

contracts and their annexes could be scanned and filed electronically,

simplifying retrieving. For simplicity, the system come with a full documentation

on how it is structured and operates. There a number of manual detailing

various modules, operating procedures and help functionalities.

To eliminate disaster though, regular and efficient backups and recovery

strategy should be in place. The back office should also test the disaster

recovery strategy in place and all staff should be trained on this. Full backups of

the system should be done at least once a month. A use of a remote service for

the monthly backup or placement of the backup in another place (outside the

building where normal business is conducted), which has to satisfy the same

security and accessibility standards as the original site is vital. Incremental

backups should be done on a daily overnight basis. The media; i.e. another

server, tapes, CD’s to be used should be defined, taking into account cost of

purchasing.

CS-DRMS has evolved significantly over time, progressing from DOS to UNIX to

Windows. It has been continuously tested and improved over the years to meet

creditor practices, user requirements, and evolving technology changes and

harmonized with the External Debt Guide. Likewise, the system functionalities in

terms of data capture, reports, debt analysis, securities issuance and

management have also been improved to conform to best practice guidelines.

2.6 DeMPA Tool Functions on Back Office

The Debt Management Performance Assessment Tool (DeMPA) developed by the

World Bank is a methodology for assessing performance through a

comprehensive set of performance indicators spanning the full range of

government debt management functions. This facilitates the design of plans to

build and augment capacity and institutions tailored to the specific needs of a

country.

2.6.1 Recording and Reports

The DeMPA tool stipulates that sound practice with regard to debt recording

demand that there should be comprehensive debt management systems to

record, monitor, settle and account effectively for all central government debt

and related transactions. The system used should be capable of performing

accurate and consistent handling of a complete debt database consisting of

domestic, external and guaranteed debt. System used to register government

securities holdings should be secure and efficient. It should also provide

accurate and timely information on all holders of government securities,

including classification by residency. CS-DRMS does cater for almost all of the

above debt recording laid down by the DeMPA tool although there is need to

enhance some of the available features e.g. security and authorisation.

On debt reporting, the DeMPA tool stipulates that Governments should report

all public sector debt outstanding and debt related transactions. This includes

obligations to report to international financial institutions. A Debt Statistical

Bulletin covering domestic and external central government debt including

guarantees should be prepared. The statistical bulletin should at least provide

information on central government debt stock, debt flows and debt rations.

This may be in a form of quarterly reviews published by Central Banks or tables

published in government financial accounts. Again, CS-DRMS has a wide range

of in-built standard reports, which cater for almost all of the reports specified

in the DeMPA tool, including data export facility for reporting to World Bank.

2.6.2 Auditing

Accountability by debt management offices can be enhanced and strengthened

by introducing regular internal audits and periodic external auditing. The

audits would help uncover all government debt management activities with

regard to: reliability and integrity of financial information; effectiveness and

efficiency of debt management operations; safeguarding of public funds; and

compliance with laws and regulations.

Ideally, auditors need to have the required skills to audit all debt management

activities, including systems used. There should also be mechanism to adopt

and implement corrective measures as recommended by audit reports.

2.6.3 Security

DeMPA tool advocate that there should be clearly documented authorisation

and controls to access the debt management and payment systems in place.

This would be achieved by active management of individual access permission

and passwords. System should also be able to produce audit trails that indicate

who has accessed the system and at what level.

Back-ups should be frequently done and stored off-site, i.e. outside the

building where the debt database is located. An original copy of loan

agreement should be stored in a secure and fireproof location. All other

correspondences with the lender should also be maintained in a secure filing

system.

Section 3: Back Office Operations in sampled

MEFMI countries

3. Back office operations in sampled MEFMI Countries

3.1 Legal Framework

3.1.1 Swaziland

The main legislation that regulates government borrowings in Swaziland is the

Constitution of the Kingdom of Swaziland Act, 2005. The Act stipulates that

Parliament is the final decision-maker on central government borrowings.

Although it is stated that the Minister of Finance on behalf of Government may

borrow or raise moneys from any reputable source, this is followed by the

important proviso that such borrowing or provision of a guarantee shall be as

authorized by or under an Act of Parliament.

In the case of domestic borrowing, authorization that has been given by

Parliament is in the form of Treasury Bills and Government Stocks Act, 1994,

(Amended) 2003. The Act authorizes the Minister of Finance to borrow against

the issue of treasury bills and stocks. The Minister may appoint a Government

Department or any financial institution licensed by law as agent for the issue,

management, and repayment of any treasury bills or stocks issued under this

Act or for any other matter related thereto. The maximum amount, which may

be borrowed under this Act, may at any point in time not exceed One Billion

Emalangeni (E1 billion). In addition, the Central Bank of Swaziland, through the

provisions of the Central Bank of Swaziland Order, 1974, as agent for

Government, is mandated to undertake issue, placement, and service of any

Government securities, including treasury bills.

All other borrowings, including all foreign borrowings, must be decided by

Parliament, on a loan-by-loan basis. For that, a legal instrument in place

and/or used is the Finance Management and Audit Act, 1967 and Amendments

thereof. The Act empowers Parliament to grant authority to the Minister of

Finance to borrow money to an amount not exceeding the sum specified in that

resolution, to meet current requirements. Further, the Act provides that such

resolution shall not have any effect for any period exceeding twelve months.

The principal and interest of all such advances shall be charged on the

Government Consolidated Fund held at the Central Bank of Swaziland.

3.1.2 Botswana

Governing domestic borrowing in Botswana is the Stocks, Bonds and Treasury

Bills Act, 2005. The Act stipulates that the Minister of Finance is authorized to

appoint an agent to float any government securities. In addition, there is the

Finance and Audit Act, which authorize the Minister for Finance to borrow by

means of a bank overdraft or advances from any bank or any public institution

in Botswana, such moneys, as he may need to meet current requirements. The

total outstanding amount of money that can be borrowed under this Act shall

not at any time exceed 5 percent of the total revenue credited to the

Consolidated Fund in the previous financial year or such higher amount as the

National Assembly may approve by resolution.

There is no law governing foreign borrowing. The practice is that the Minister

of Finance seeks parliament approval on a loan-by-loan basis the sum specified

in the purported loan agreement. Alternatively, the Minister for Finance

request parliament to ratify foreign borrowing that has already been

contracted by the Minister.

Other than central government, there are other key regulators involved in debt

market issues. These include the Capital Market Authority, which provides

supervision to ensure investor confidence. There is also the Botswana Stock

Exchange, which approves new issues and provides a market place for

secondary trading.

3.2 Government Policy on Debt

3.2.1 Swaziland

The Government of Swaziland in 2005, with technical assistance from MEFMI,

formulated a National Public Debt Policy to guide contracting, coordinating,

and managing domestic and external public debt. In a nutshell, the Debt Policy

set out the Government’s policy position on all stages of public debt

management process.

The main objective of the Debt Policy with regard to external and domestic

debt is to ensure that Government’s financing needs are met at the lowest

possible cost over the medium to long-term, consistent with a prudent degree

of risk. The policy is based upon the premise of enabling Government to pursue

developmental objectives whilst at the same time ensuring that debt remains

within sustainable levels.

The policy document further underlines the following requirements to facilitate

achieving the cost and risk objectives and importantly to evolve sound public

debt management:

Debt contracted is only entered into through legally established

structures by the Minister of Finance;

Debt contracted is done through full cooperation and consultation with

line Ministries involved;

Close coordination of public debt policy with monetary and fiscal

policies given the interdependencies of the three macroeconomic policy

areas;

Transparency and accountability to the public with regard to debt

management operations;

Maintaining comprehensive databases on public sector debt including

Government explicit and implicit contingent liabilities; and

Annual audit of debt administration by the Government Auditor

General.

3.2.2 Botswana

The Government of Botswana does not have a formal policy instrument to guide

public external and domestic borrowing and debt management. The line

Ministries tend to initiate project proposals for funding and external creditors

can pick from a poll of proposed projects to fund.

The Ministry of Finance and Development Planning react on a case-by-case

basis. The Ministry then assess these project proposals and their concessionality

in the context of the country’s development priorities, as spelt out in the

country’s Annual National Budget Speeches, Development Plans, National

Strategy for Poverty Reduction and Vision 2016.

Until recently, Botswana had mainly external debt, also underpinned by the

country’s strong international credit rating (A+). There is also no formal debt

strategy and the country total debt levels are guided by the Finance and Audit

Act, which itself, is being reviewed.

3.3 Institutional Arrangements

3.3.1 Swaziland

The institutional framework for public debt management in Swaziland consists

of a number of public institutions in carrying out all duties relating to

contracting and utilization of borrowed funds. Each institution has its specific

roles and responsibilities in the public debt management starting from the

initiation of the project to the financing requirements, contracting of debt, up-

to maturity (public debt cycle). The institutions involved include:

Ministry of Finance (Mof), - which is mandated by the Finance and Audit

Act, 1967 to administer and manage the public sector external debt. The

task is undertaken by the Budget and Economic Affairs Section of the

Ministry. The Ministry of Finance determines financing requirements

from external sources, maintains the overall public debt database,

manages, and monitors the overall public debt portfolio.

Also in existence within the Ministry of Finance is a formal structure for

negotiating and contracting debt. This structure is comprised of

representatives from Mof, Attorney General’s Office, Ministry of

Economic Planning and Development (MEPD) and the implementing

agencies involved for that particular project. There is also an Investment

Committee that oversees the management of government financial

activities. This Committee comprises of representatives from the Central

Bank of Swaziland, Accountant General’s Office, and Mof. The Principal

Secretary, Mof chairs this Committee.

Ministry of Economic Planning and Development (MEPD), - works with

line Ministries, to identify the projects that require external funding and

assess their viability. MEPD also participates in the loan negotiation

processes.

Central Bank of Swaziland (CBS), - is mandated through the provisions

of the Central Bank of Swaziland Order, 1974 to undertake issue,

placement, and service of any Government securities including

maintaining the domestic debt database. To carry out government

treasury bills auctions, a Treasury Bills Auction Committee was

established. Its members comprise of representative from the CBS and

Mof’s Fiscal and Economic Affairs Section. The Bank also advises the

Minister of Finance on contracting and managing domestic debt. The

Bank also monitors private sector external debt. Further, the Bank

externalizes debt services payments on instruction by the Accountant

General after receiving a request from the Mof.

Accountant General’s (AG) Office, - in conjunction with Mof and CBS,

the AG ensures that proper record of all government loans is kept and

the AG prepares a statement of all government loans at the end of each

fiscal year. The AG also ensures that funding for debt servicing is

available for onward transmission to the creditors by CBS.

Attorney General’s Chambers, - is entrusted with the responsibility to

ensure that all legal requirements are met before foreign loans are

contracted and that legal contractual terms are observed throughout the

loan cycle.

Line Ministries, - they identify and prepare project documents in their

respective sectors in line with government’s developmental policies and

partake in loan negotiations involving their departments, projects

implementation, and ensuring that loans are disbursed appropriately.

Public Enterprises, - participate in the negotiation of loans being

contracted to their benefit, monitor and manage the debt.

Auditor General’s Department, - responsible for monitoring compliance

of debt transactions with regulations and procedures governing the

utilization of loan resources and prudent management of the overall

public debt portfolio.

3.3.2 Botswana

The current institutional arrangements for the debt management in Botswana

are shared between the Ministry of Finance and Development Planning (MFDP)

and the Bank of Botswana (BOB). Each of these institutions has specific but

interactive offices handling decisions right from the strategic decision making

level to operational level.

MFDP, - as custodian of all public borrowing, the Ministry administer and

manage all public sector external borrowings. It has delegated domestic debt

management and administration to the BOB.

Bank of Botswana, - it is the fiscal agent of the government and therefore the

operational arm of the MFDP decisions through the Bank’s Financial Markets

Department. The department has a dedicated Open Market Operations Division

that specifically handles the implementation and monitoring in the domestic

market.

Attorney General’s Office, - the MFDP has a legal officer seconded from the

Attorney General’s Office. The legal officer has the responsibility to ensure

that all legal requirements are met before foreign loans are contracted and

consequently advice the Ministry on all legal issues pertaining to debt

management.

Internal Audit Unit, - the MFDP also has an internal auditing unit responsible

for monitoring compliance of debt transactions with regulations and procedures

governing the utilization of loan resources.

3.4 Procedures

3.4.1 Swaziland

Swaziland, with assistance from MEFMI, developed a Debt Management

Operations Manual in 2004. The manual helps build institutional memory that

will enable a new debt officer/manager to understand the operations of a debt

office and the embedded challenges and skill requirements. Thus, the manual

documents the operations and procedures in the functional/operational offices.

The procedures for back office operations in Swaziland are as follows:

Collecting and storing - the Mof’ BEAS, as custodian of public debt,

collects all information of different categories of external debt to include loan

contracts, disbursements and repayments. The information collected is

physically stored by the Mof in filing cabinets. On the other hand, the Bank

collects and stores information on private sector external debt through annual

surveys. Further, the Bank keeps a register of all information pertaining to

issuance of government treasury bills. Government appointed a Fund manager

to issue and register information on treasury bonds issued in 2002, with the last

maturity only falling due in August 2010.

Debt data recording - all external debt data (including guarantees

and private sector debt) is recorded by the Mof’s Budget & Economic Affairs

Department in CS-DRMS. This is done jointly with the Central Bank of

Swaziland, Research Department, Public Finance Section. The recording is done

after reconciliation of the debt data between Mof, Accountant General's Office

and Central Bank of Swaziland (CBS). CBS takes a copy of the debt data and

restore in its site of CS-DRMS since the two CS-DRMS sites in Swaziland; i.e. at

Mof and CBS are not yet electronically linked.

On the other hand, domestic debt recording is captured by the Central Bank of

Swaziland in two (2) systems (IMF Book Entry System and CS-DRMS). The

Investex department of the Bank uses the IMF Book Entry System to conduct

Auctions. After the Auction has been confirmed by the Treasury Bills Auction

Committee, Research Department captures this information manually in the

Domestic Debt Module of CS-DRMS since the IMF Book Entry System is again not

interfaced with CS-DRMS. The Research department also serves as Secretariat

to the Auction Committee and thus get information on allotments made from

primary source.

Disbursements - the contractor, attaching certificates of work done,

lodges a claim through the relevant line Ministry (implementing agency). After

satisfying herself, the implementing agency sends a withdrawal request to the

Mof's Budget & Economic Affairs Section (BEAS). After being approved by the

Mof, the withdrawal request is sent to the creditor. The creditor, depending on

the agreement; pay the sum to government for onward transmission to

contractor, or creditor pay directly to the contractor (direct disbursement), or

alternatively government pay the contractor upon receiving a claim and

forward the claim to the creditor to facilitate reimbursement. When

disbursements have been made, the creditor sends a disbursement statement

to the Mof’s BEAS. The BEAS verifies/checks the disbursed amount against the

withdrawal request, and enters the disbursement into the CS-DRMS.

In respect of treasury bills issuance, settlement is done by the Central Bank of

Swaziland, two business days following the auction date. Settlement is done

against Primary Dealers Accounts held at the Bank. Primary Dealers, who also

submit on behalf of their clients, are responsible to make settlements with

their clients. Non-competitive bidders, including individuals who come directly

to the Bank instead of Primary Dealers deposit their cash/cheque in a Treasury

Bills Disbursement Account at the Central Bank of Swaziland. All competitive

bidders come through Primary Dealers.

Debt service - it is initiated by the creditor who sends a bill to the

Ministry of Finance’s BEAS for any principal, interest, commitment fees or

service fees due. The bill is usually received before the actual due date of the

payment. The Mof having satisfied itself on the correctness of the bill as per

the Loan Agreement then instructs the Treasury Department or Accountant

General’ Office to authorize payment. In this regard, the Mof prepares a Debt

Service Payment Advice which is signed by the Principal Secretary, requesting

the Accountant General to authorize payment as indicated in the Advice form.

The Advice form specifies the payments to be made, that is, principal

payment, interest payment and/or commitment fees payment etc. The foreign

currency amount is specified, details of bank/account to be credited and due

date of payment are all indicated in the Debt Service Payment Advice.

After confirming the validity and accuracy of the payment, the Accountant

General signs the Advice form and instructs the Central Bank to effect payment

which is done through the Investment & Exchange Department (Investex) in CBS

as indicated in the Advice Form. The Investex also state the local currency

equivalent for any foreign debt service made.

After effecting payment, the Investex returns the original Advice Forms to the

Ministry of Finance and other copies sent to Treasury/Accountant General and

the Research Department of the Central Bank of Swaziland – Public Finance

Section. To indicate that debt service payments have been done efficiently,

the Public Finance and External Debt Section of the Research Department in

the Central Bank of Swaziland meets with the Ministry of Finance’s Budget and

Economic Affairs Section on a quarterly basis or as and when necessary to

reconcile debt service payments. This is done after Mof has reconciled with

Accountant General’s Office. This process ensures that there are no errors and

omissions made. The information is then captured in the debt recording

system, i.e. CS-DRMS.

For treasury bills, at maturity, the Central Bank of Swaziland credits the

Primary Dealers Accounts held at the Bank. Primary Dealers are responsible for

settlement with their clients. Where an applicant had applied directly to the

Bank, at maturity she receives a Bank Guaranteed cheque from the Central

Bank of Swaziland, which can be cashed at the Bank or from any commercial

bank.

Debt reporting, - external debt is reported to the World Bank on a yearly basis

using CS-DRMS Data Export Facility – World Bank Bridge. The IMF Article IV

Missions also gets various reports generated from the system. Information on

domestic debt is provided by the Central Bank of Swaziland. Some reports

(both for external and domestic debt) are done using Ms-excel generated

spreadsheets. Further, regional organisations like SADC, COMESA etc also get

debt statistics either from the Bank or Mof as and when required. Various other

reports, either generated from CS-DRMS and/or Excel spreadsheet, are

produced for internal use as and when required, i.e. by management, CBS BOP

Unit, government ministries, private users of debt information etc. The Bank

also publishes debt statistics in Quarterly Reviews and Annual Reports. Such

information is also available in the Bank’s website: www.centralbank.org.sz.

The Minister of Finance, also, on an annual basis, reports to Parliament on

public debt when delivering his Budget Speech.

3.4.2 Botswana

Data collection and storing, - all information on public debt is collected and

stored by the MFDP's Public Debt Service Unit (PDSU). The information is

obtained from the MFDP's Development Programmes Section, Development

Unit, Bank of Botswana's Financial Markets Department and correspondence on

loan agreements, disbursement and debt service that is received from external

creditors is through the office of the Permanent Secretary, MFDP.

Disbursements, - disbursements tracking and recording are the responsibility

of the Development Unit. Disbursements are recorded by this office in the

Government Accounting and Budgeting System (GABS).

Debt service, - the PDSU of the MFDP is responsible for performing the debt

service function in collaboration with the MFDP's Banking and Remittance Units.

All these Units are staffed with officers seconded from the Accountant

General's Department. After getting a bill from creditors, the PDSU initiate the

debt service process. Eventually, such is externalized by the BOB.

Debt recording and reporting, - the PDSU and Cash Flow Unit (CFU) are the

two units of the MFDP responsible for debt recording with the latter also

handling budget execution functions. In addition, the PDSU records lending and

on-lending. The PDSU records debt information that relates to debt contracting

and debt service in GABS whilst the Development Unit records the

disbursements component. The CFU uses GABS information to capture debt

data in CS-DRMS. The PDSU reports debt statistics to World Bank manually

using information generated by GABS. CFU who uses CS-DRMS are not aware of

the Data Export Facility available in CS-DRMS to report to the World Bank.

3.5 Staffing

3.5.1 Swaziland

3.5.1.1 CS-DRMS Users

In Swaziland, CS-DRMS is installed and used in two sites; i.e. Mof and CBS.

There are two officers currently maintaining the CS-DRMS external debt

database in the Mof’s BEAS. These are the same officers who are responsible

for initiating debt service payments after receiving bills from creditors. These

officers perform such a task on “part-time basis” since they are budget officers

and are always busy with budget monitoring. The Director, Budget and

Economic Affairs Section is involved in loan negotiations. Accountant General’s

staff had been previously trained in CS-DRMS, but do not have access to it even

on a view basis.

In the Central Bank of Swaziland, CS-DRMS is installed at the Research

department, where two officers use it. This is mainly the domestic debt

module, since the Bank issues and manages domestic debt (treasury bills) on

behalf of the government. The same officers also support or work together with

the Mof in recording instruments, debt services etc in the External Debt Module

of CS-DRMS maintained by the Mof. Thus, only four people in Swaziland are

familiar with CS-DRMS.

3.5.1.2 System Support Staff

Swaziland has only one (1) CS-DRMS System Support Officer. He is employed by

the Central Bank of Swaziland and also attends to CS-DRMS IT issues at the

Ministry of Finance. Amongst other training attended, the officer has been

previously trained on CS-DRMS Training For New Users, CS-DRMS System

Administration and CS-DRMS Report Writer.

On another note, two (2) ICT staff currently support the IMF Book Entry System

on a trial and error basis since they have not been trained on it.

3.5.2 Botswana

3.5.2.1 CS-DRMS Users

Three (3) officers use the system only for recording both external and domestic

debt. These are officers from the Cash Flow Unit of the Ministry of Finance and

Development Planning. The Bank of Botswana does not use CS-DRMS. In

conducting auctions, the Bank's Financial Markets Department uses Ms-Excel

Spreadsheet. On a rare basis, specifically when calculating the grant element

for loan(s) still being negotiated for possible contracting, the Director

Development Unit who also has the system installed in her office uses CS-DRMS

specifically for that purpose.

3.5.2.2 System Support Staff

The computer system that is used by PDSU, i.e. the Government Accounting

and Budgeting System is technically supported by IT staff from the Government

Department of Information Technology. On the other hand, CS-DRMS which is

used by the Cash Flow Unit is technically supported by Development Unit Staff.

3.6 Technology

3.6.1 Swaziland

The Ministry of Finance and Central Bank of Swaziland use CS-DRMS 2000+ v1.3

for both external and domestic debt recording and management. The Bank, as

an agent for the issuance and management of Government of the Kingdom of

Swaziland’s debt and as an institution with a keen interest in the domestic

financial system also uses the IMF Book Entry System for treasury bills issuance.

Hardware used by these institutions include personal computers; Pentium 2

with a 4.5 giga bytes. The memory is a 128 MB.

CS-DRMS 2000+ is running on Windows 2003, Structured Query Language (SQL)

2000 both client and server and Borland Data Engine (BDE) Administrator.

There is a centralized database architecture. Two (2) users access the database

from their workstations through the Local Area Network (LAN), and the users

are set to have different access profiles depending on the tasks they perform

on the database. Debt Sustainability Module Plus has also been installed.

Over and above this, the Mof is working toward upgrading the existing

hardware and software in support of the CS-DRMS 2000+. This will include the

networking of the system internally and to all agencies involved in debt

management including Treasury or Accountant General' Office.

Further, for conducting auction of treasury bills which are done on a weekly

basis, the Central Bank of Swaziland uses the IMF Book Entry System. This

system is interfaced with the Globus Financial and Accounting System

(Termenos T24) to facilitate settlement and redemption of the treasury bills

issued. The Globus system is inturn interfaced with RTGS.

3.6.2 Botswana

The Ministry of Finance and Development Planning also uses the latest version

of CS-DRMS 2000+, i.e. version 1.3. The installation is similar to Swaziland's,

that is, CS-DRMS 2000+ is running on a Windows 2000 Client-Server Technology.

They also have a centralized database architecture running Microsoft SQL2000

server (MSSQL2000). All the users share one password. Thus, the users access

the database from their workstations through the Local Area Network (LAN),

and all of them are set as system administrators.

The main system used in Botswana for debt recording is the Government

Accounting and Budgeting System. This system is updated on a real time basis

and is mainly used by the Public Debt Service Unit. The Cash Flow Unit uses it

on a view basis to extract the necessary data in order to update CS-DRMS.

Section 4: Back Office functions available

in CS-DRMS

4. Back Office functions available in CS-DRMS

4.1 Overview

CS-DRMS 2000+ is a versatile tool for recording and monitoring of debt

activities. It is designed to capture all activities pertaining to the loan cycle

from the stage of signing the loan agreement till maturity. As such, the system

requires information on several types of debt transactions like disbursements,

debt service payments, enhancements, cancellations and any other debt

restructuring to generate the amount of actual liability.

The current version is Windows based. It is used by government agencies for

monitoring and managing the debt portfolio of the country, including the

government debt. The scope of CS-DRMS has significantly evolved over the

years, undergoing a series of enhancements as earlier discussed.

Described in the sections below are the functionalities currently available in

the system and plans on future development.

4.2 Operational Functions

4.2.1 Recording Functions

The recording functions in CS-DRMS can be broadly categorised into two

modules, i.e. Domestic and External Debt Modules. Filing of Data Entry Sheets

(DES) before specific details are recorded into CS-DRMS is necessary. These DES

are filed when extracting details for array of loan agreements and securities.

4.2.1.1 Data Entry Sheets

Proper recording of loans and/or other debt instruments require one to extract

details from loan agreements and other debt instruments and compile them in

a manner that allows for easy input into CS-DRMS.

The data input screens of CS-DRMS have been revised and updated and new

ones added to represent the requirement of a more comprehensive debt data

by debt managers. All these developments are reflected in data entry sheets

which have been designed to facilitate easy input of loan data into CS-DRMS.

Each input screen in the system has its own DES. In practice, however, it may

not be necessary to complete a whole set of DES for every instrument.

The main data types used and covered in DES include; loan details, forecasting

rules, actual transactions, codes, rates. DES can also be filed for debt

securities like Bonds, Treasury Bills, Promissory Notes etc.

4.2.1.2 Domestic Module

Treasury Bills and Bonds (Zero coupon and Fixed coupon bonds) are the most

common domestic debt instruments issued in MEFMI member states. The

recording of treasury bills and zero coupon bonds is similar in almost all

aspects. Both are issued at a discount, and at maturity, the holder gets the

face value. The interest paid would be the difference between the face value

and the purchase price. The differentiating factor between these two is that

treasury bills are short-term debt instruments issued at a discount for not more

than a year (365 days) and anything with an original maturity of over 12 months

is a treasury bond/note.

The basic principle for recording these follows a standard format where no step

can be skipped even if there was only one bidder. The three (3) steps followed

are the recording of instrument details, tranche details (usually differentiated

by competitive and non-competitive bids) and bid details. The system has

validation checks for these, which are outlined under database management

section below. Similarly, other domestic debt instruments follow the same

format except that one has to define fixed interest in case of a fixed coupon

bond, variable interest in case of floating rate bond, stepped rate for stepped

bonds. These can also be indexed to some other variable that need to be

specified, e.g. indexed to consumer price index.

Once information about instrument details, tranche and bid details have been

recorded, the system will automatically general forecasts. Thus, actual

transactions can be generated simply by clicking processing and generate

actuals. This is based on the assumption that no government can ever default

on domestic debt, thus it is assumed that actuals will always be equal to

forecast. Nevertheless, the system still provides an option to manually capture

actual transactions if they happen to differ from forecasts.

For promissory notes, only the promissory note details are entered. There are

neither any tranches nor bids required. However, depending on the promissory

note details, sometimes you may need to specify the interest rate charged or

penalty interest to be charged in case of default payment.

The practical business processes, which would require checks and

authorisation, is not adequately catered for in CS-DRMS. System administrators

can, however, set users with access rights such as to add, modify, delete or

view basis only. This means that if one user has rights to add, she can add

everything, thus there is almost no segregation of duties observed in the

system. The usual front, middle and back office operations and authorisation

processes as they happen in practice are not robust. Nevertheless, there is an

audit trail facility that can be set on to track as to who did what and when.

As mentioned, currently, the authorisation process is not vigorous as is the case

with the Commonwealth Secretariat Securities Auctioning System. Such

functionalities will, however, be incorporated in future releases to represent

the debt management process as they practically occur within debt

management institutions.

4.2.1.3 External Module

The external module provides the necessary links between various aspects of

the loan cycle, e.g. loan registration, disbursements, debt service and any

restructuring that may occur during the life of an instrument. To avoid

inconsistent debt data for a country, it is necessary that one institution

manages such and network links can be set up for other institutions within the

system for analytical purposes.

Recording of external debt in the system is completely different from capturing

domestic debt instruments. The recording of loans ideally is done immediately

after the signing of the loan agreement. Like in domestic debt module, the first

four digits of the instrument id refer to the year in which the agreement was

signed. All other information concerning basic details is recorded as indicated

below. Most fields under basic details are mandatory. Other fields like title and

reference are optional.

On other details screen, there are fields that are automatically calculated by

the system after all the loan details, including forecasting rules have been

entered and loan having been processed. The fields calculated by the system

include grant element and maturity (i.e. maturity date, original maturity,

remaining maturity and grace period).

Another important screen is for utilization where critical fields like effective

date, terminal date of disbursement, disbursement agency are recorded. Status

screen indicate status of loan at any point in time. Documents screen allows

scanned documents to be stored for future reference.

Forecasting rules is the core function in the recording of external debt

instruments. This is where information such as how disbursements are to be

made, interest is to be paid, principal payments are to be made etc are

captured. Information entered here is the one used by the system when it

generates forecasts. Since disbursements are always tricky to record,

considering that most loan agreements have conditions precedent that need to

be full-filled before the loan can start disbursing, effectively meaning that

disbursements dates are not immediately known to enable recording in system.

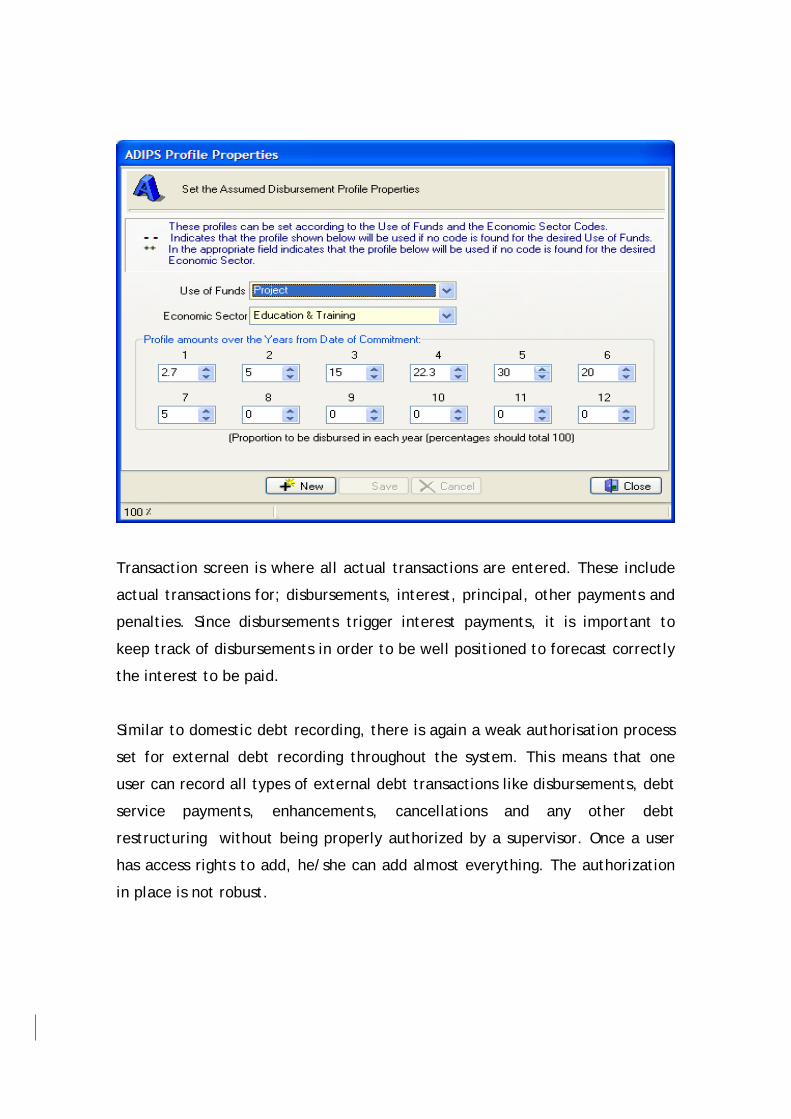

Thus, CS-DRMS has a facility known as Assumend Disbursement Profile (ADIPS),

which allow user to switch it on where disbursements are not known how they

would be made. The ADIPS is based on the economic sector of the project to be

financed. Once switched on (ADIPS), it would make disbursements forecasts for

that particular instrument. There is still an option to amend it if user is not

comfortable with its projections for disbursements. However, users are not

encouraged to use this facility.

Transaction screen is where all actual transactions are entered. These include

actual transactions for; disbursements, interest, principal, other payments and

penalties. Since disbursements trigger interest payments, it is important to

keep track of disbursements in order to be well positioned to forecast correctly

the interest to be paid.

Similar to domestic debt recording, there is again a weak authorisation process

set for external debt recording throughout the system. This means that one

user can record all types of external debt transactions like disbursements, debt

service payments, enhancements, cancellations and any other debt

restructuring without being properly authorized by a supervisor. Once a user

has access rights to add, he/she can add almost everything. The authorization

in place is not robust.

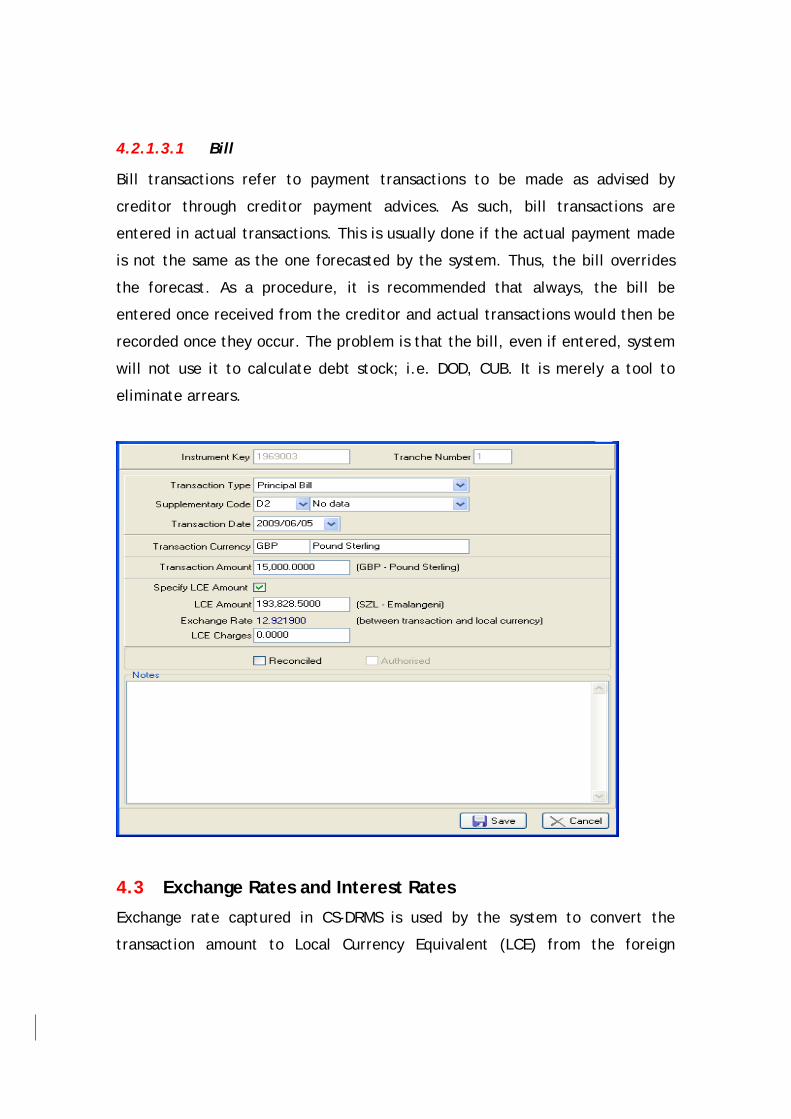

4.2.1.3.1 Bill

Bill transactions refer to payment transactions to be made as advised by

creditor through creditor payment advices. As such, bill transactions are

entered in actual transactions. This is usually done if the actual payment made

is not the same as the one forecasted by the system. Thus, the bill overrides

the forecast. As a procedure, it is recommended that always, the bill be

entered once received from the creditor and actual transactions would then be

recorded once they occur. The problem is that the bill, even if entered, system

will not use it to calculate debt stock; i.e. DOD, CUB. It is merely a tool to

eliminate arrears.

4.3 Exchange Rates and Interest Rates

Exchange rate captured in CS-DRMS is used by the system to convert the

transaction amount to Local Currency Equivalent (LCE) from the foreign

currency amount. The LCE is the most important transaction since all reports

convert amounts to the reporting currency through the LCE amount. Once the

instrument amount has been updated, the LCE can either be converted using

the rate stored in the transaction table or LCE can be specified manual. It is

recommended that users use the ‘Specify LCE Amount’ rather than using the

latest exchange rate stored in then system since such may not have been

updated or may not necessarily corresponds to the resultant LCE.

Likewise, floating/variable interest rates need to be updated frequency since

the the system apply such rates when calculating interest forecast based on

DOD.

The manual recording of rates can be tedious and time consuming and can

easily allow errors to go unnoticed. Current functionalities available in CS-DRMS

do not allow such information to be uploaded from systems where such data is

sourced like Bloomberg and Reuters. Further, there is no proper tool for

validating the rates other than the use of graphs.

4.4 Reporting Functions

There are various in-built standard reports available in the system for both

external and domestic debt. There is currently an effort to increase the array

of domestic debt reports to respond to user needs. System also provides the

report writer facility which enables users to design their own reports based on

the specifications that suit their needs. There is also the data export facility

which is used to report debt information to the World Bank on a calendar year

basis. This facility has been modified to meet the requirement/needs of the

World Bank.

Reports in CS-DRMS are in reference to the cut-off date. All actual transactions

after the cut-off date are not included in the aggregate figures. In order to

incorporate these, it is important for the user to carry out a period end

processing to move the cut-off date after the dates of the actual transactions.

Further to note is that cut-off date is used system wide. It cannot be applied to

a specific instrument or specific components of an instrument.

4.5 Database Management Functions

4.5.1 Validation

Validation checks in recording of treasury bills include the following:

o Instrument Number should start with the year in which the debt

instrument was issued. Other years will not be activated.

o System will not accept as a treasury bill if that instrument has a

maturity of more than 365 days.

o Total of bids amounts cannot exceed tranche amount.

o Total of tranche amounts cannot exceed instrument amount.

o With the exception of the 365 days being the maximum maturity period

for a treasury bill, the above validation checks also hold for zero coupon

bonds.

o For a fixed coupon bond, system will lead you to define the fixed

interest rate.

o The validation checks are similar even for floating (where system would

lead user to define the variable interest rate) and for stepped (to

defined stepped interest) bonds.

Ideally, there is no separate tool for database validation in the system.

However, CS-DRMS does validation in three distinct stages:

A number of checks and validations take place at the time of data

entry. System prompt user to a different stage, provide

warnings/error messages, during this period;

System provides either warnings or validation error messages or both

during processing.; and finally

System has sequenced procedures to be followed when doing an

upgrade.

4.5.2 Use of Graphs

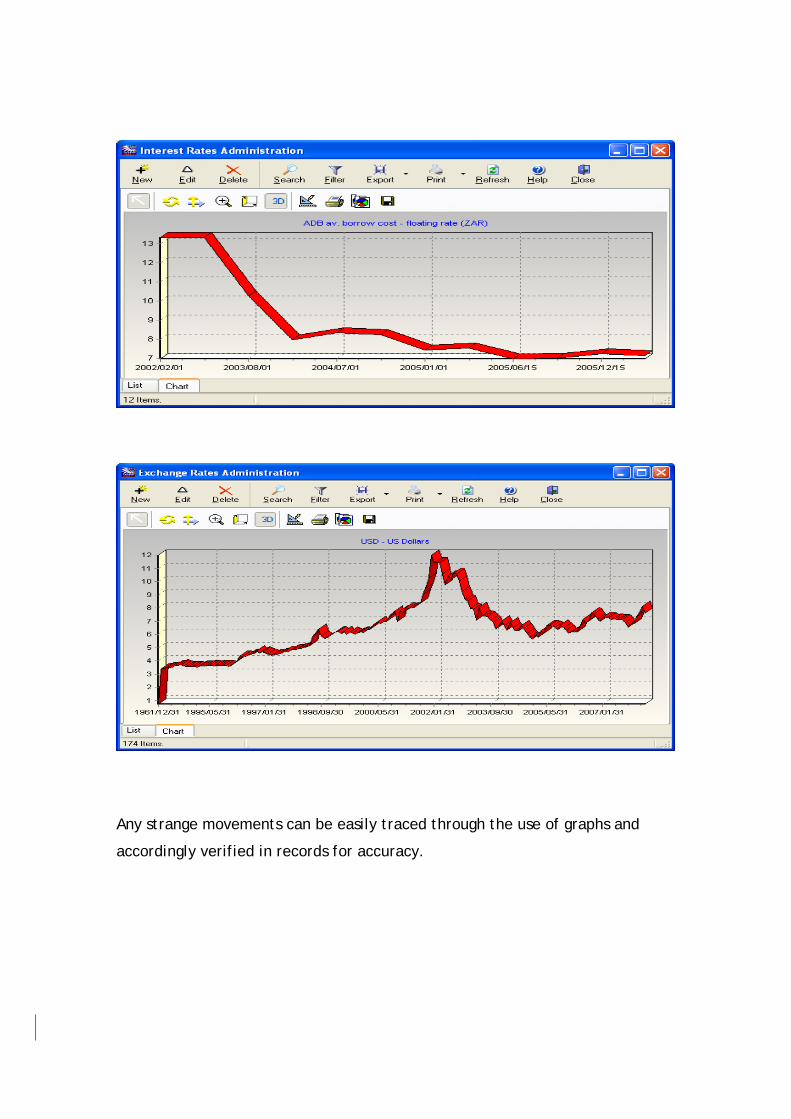

The use of graphs is the only currently available ‘tool’ to enhance validation of

exchange rates and interest rates.

Any strange movements can be easily traced through the use of graphs and

accordingly verified in records for accuracy.

4.5.3 Processing

This refers to the activity where CS-DRMS integrates all the relevant records

pertaining to an instrument to create day- by -day account on the activity of

the instrument. Specifically, during processing, system carries out extensive

validation between instrument details, forecasting rules, actual transactions

and balance record. Any inconsistencies found will either lead to warnings or

error messages or both.

Violation of business principles and any system pre-set limits and criteria will

result to errors. Where a validation error message has been posted, that

instrument will be excluded from any reports generated, which will therefore

result in inaccurate reports. Minor inconsistencies will lead to warnings. Even

though such instruments with validation warnings will be part of the reports,

the reports generated would provide a warning that it contains instruments

which have not been successfully processed.

Processing is one of the critical activities within CS-DRMS and it is only at this

time that all the diverse elements of an instrument are examined together.

All efforts should be made to fix and/or correct all validations warnings and

errors in order to produce accurate reports. The system is user friendly, as it

will also provide user with the validation error messages or warnings for ease of

reference when correcting these.

Once all validation warnings and errors have been cleared, period end

processing may be run. This is basically advancing the cut-off date by one

month. The cut-off date is the reference date which is a common point

between historical and future transactions for all instruments. Transactions

before cut-off date are referred to as historical or actual transactions whilst

those after cut-off date are known as future or forecast transactions. Reason

for having monthly period end processing in CS-DRMS instead of real time is

because the flow of information in debt offices is usually monthly. It also

allows for a month lag for reconciliation of debt figures before they are

actually recorded in the system. This is the view of the system developers’ i.e.

ComSec.

4.5.4 Backup and Restore

This facility is available in the system and is fairly up to users to decide how to

use it. It is a question of establishing right procedures for employees to

perform it and such a facility would work well with good ICT support.

Back up and restore should be done occasionally including testing of disaster

recovery plan in place. Keeping a backup off-site is also vital. Scanning

documents for future reference also help to avoid going though a pile of files

when looking for information on any particular instrument.

4.6 Future Plans for CS-DRMS

4.6.1 Software

The Secretariat intends to move CS-DRMS to a new development platform and

is looking to re-engineer the application software to closely mirror debt

management business processes as they practically occur within debt

management institutions.

The new software will be based on a workflow system to model the flow of

information and authorization procedures as they happen in practice. ComSec,

inturn commissioned a consultant to undertake a study and compare businesses

processes in different countries (a mix of advanced economies, emerging

market economies and developing countries) and come up with a comparative

generic model which captures best practices that can be replicated in the

software.

The scope of the study include a comprehensive documentation for public debt

management which clearly describe business processes, information flow,

authorization process, functions and responsibilities within the different debt

management institutions and units. These include; front office, middle office

and back office as well as between the debt management institutions and

external entities like Accountant General Office and Central Banks. These will

allow different users to have different controls and audit trails. System will

cascade down the different processes in the debt management cycle. The

outcome of the study would be a documentation that would then be used by

ComSec to tailor CS-DRMS to support each step in the debt management chain.

4.6.2 Domestic Debt Module

The Secretariat, to meet user requirement launched a Securities Auctioning

System (SAS). The SAS is interfaced to CS-DRMS thus auction results can be

easily imported from SAS to CS-DRMS Domestic Module. ComSec, still in an

effort to meet user requirements is also exploring having a facility to record

secondary market trading in the system.

On another note, seeing that domestic debt reports are insufficient to satisfy

the diverse needs of CS-DRMS users, the Secretariat is currently pursuing a

project meant to increase the array of reports in the Domestic Module of CS-

DRMS. This on-going process tries to implement and incorporate a number of

reports already identified in the next version of the system. A number of

countries were invited to make an input to this development. The reports

would be categorized into two:

- Operational; and

- Analytical (to include tables and charts).

Below are examples of some of the recommended reports to be incorporated in

the domestic debt module for the next release of CS-DRMS:

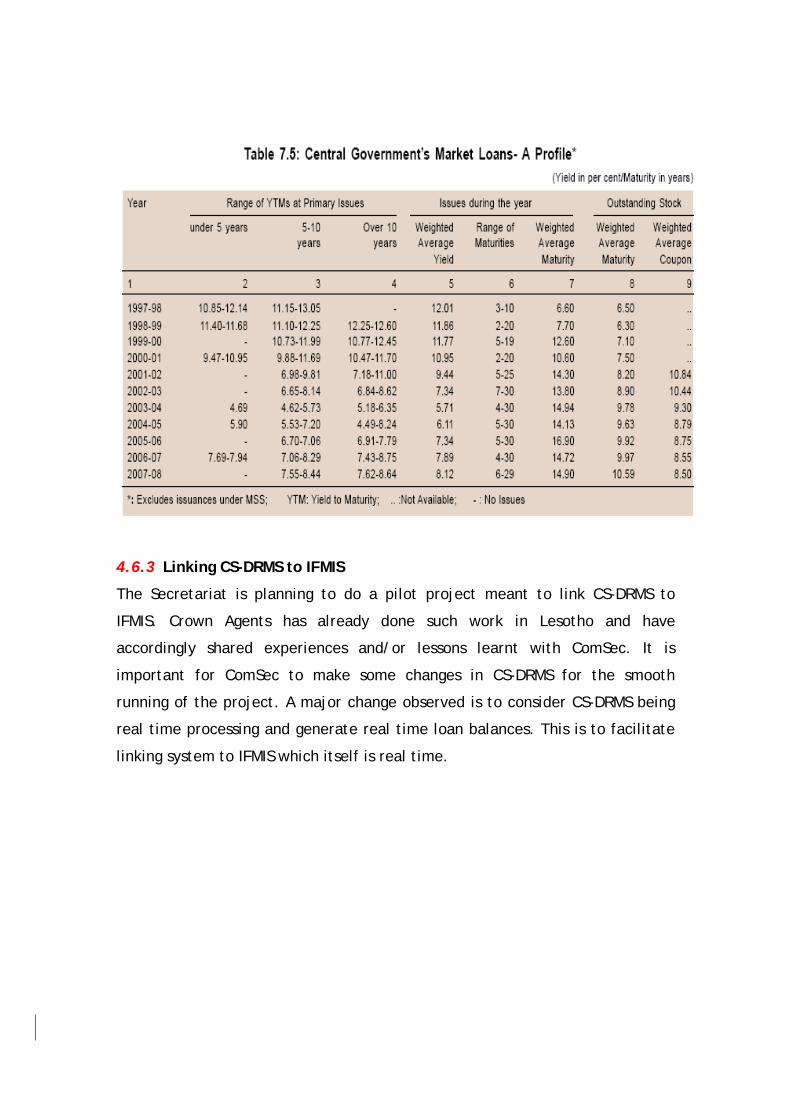

Debt Profile: Risk Indicators – Maturity

4.6.3 Linking CS-DRMS to IFMIS

The Secretariat is planning to do a pilot project meant to link CS-DRMS to

IFMIS. Crown Agents has already done such work in Lesotho and have

accordingly shared experiences and/or lessons learnt with ComSec. It is

important for ComSec to make some changes in CS-DRMS for the smooth

running of the project. A major change observed is to consider CS-DRMS being

real time processing and generate real time loan balances. This is to facilitate

linking system to IFMIS which itself is real time.