background paper international experience … paper international experience with private sector...

TRANSCRIPT

Background Paper

INTERNATIONAL EXPERIENCE WITH PRIVATE SECTOR

PARTICIPATION IN POWER GRIDS TURKEY CASE STUDY

101754P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

ESMAP Mission The Energy Sector Management Assistance Program (ESMAP) is a global knowledge and technical assistance program administered by the World Bank. It provides analytical and advisory services to low‐ and middle‐income countries to increase their know‐how and institutional capacity to achieve environmentally sustainable energy solutions for poverty reduction and economic growth. ESMAP is funded by Australia, Austria, Denmark, Finland, France, Germany, Iceland, Lithuania, the Netherlands, Norway, Sweden, and the United Kingdom, as well as the World Bank.

Copyright © May 2012 The International Bank for Reconstruction And Development / THE WORLD BANK GROUP 1818 H Street, NW | Washington DC 20433 | USA Cover image: ©iStock

Written by Budak Dilli, Independent Consultant For Victor Loksha, Energy Sector Management Assistance Program (P146042) See synthesis report (No. 99009): World Bank. 2015. Private Sector Participation in Electricity Transmission and Distribution: Experiences from Brazil, Peru, the Philippines, and Turkey. Energy Sector Management Assistance Program (ESMAP) Knowledge Series No. 023/15. Washington, DC: World Bank Group. https://hubs.worldbank.org/docs/imagebank/pages/docprofile.aspx?nodeid=24933178 Energy Sector Management Assistance Program (ESMAP) reports are published to communicate the results of ESMAP’s work to the development community. Some sources cited in this report may be informal documents not readily available. The findings, interpretations, and conclusions expressed in this report are entirely those of the author(s) and should not be attributed in any manner to the World Bank, or its affiliated organizations, or to members of its board of executive directors for the countries they represent, or to ESMAP. The World Bank and ESMAP do not guarantee the accuracy of the data included in this publication and accept no responsibility whatsoever for any consequence of their use. The boundaries, colors, denominations, and other information shown on any map in this volume do not imply on the part of the World Bank Group any judgment on the legal status of any territory or the endorsement of acceptance of such boundaries. The text of this publication may be reproduced in whole or in part and in any form for educational or nonprofit uses, without special permission provided acknowledgement of the source is made. Requests for permission to reproduce portions for resale or commercial purposes should be sent to the ESMAP Manager at the address below. ESMAP encourages dissemination of its work and normally gives permission promptly. The ESMAP Manager would appreciate receiving a copy of the publication that uses this publication for its source sent in care of the address above. All images remain the sole property of their source and may not be used for any purpose without written permission from the source.

CONTENTS EXECUTIVE SUMMARY ................................................................................................................................... i

Turkey Case Study ......................................................................................................................................... 1

1. INTRODUCTION ................................................................................................................................. 1

2 GENERAL OVERVIEW AND HISTORICAL BACKGROUND .................................................................... 1

2.1 The Period until 1984 ................................................................................................................ 2

2.2 The Period between 1984 and 2001 ......................................................................................... 3

2.3 The Period after 2001: Creation of a Competitive Liberal Electricity Market .......................... 4

3 PSP MODELS IMPLEMENTED IN T&D ................................................................................................ 7

3.1 PSP Models under Past Concessionary Regime ........................................................................ 7

3.2 PSP Model After 1984 ............................................................................................................... 9

3.3 EXISTING PSP MODELS IN T&D AFTER EML ............................................................................ 13

4 RESULTS OF IMPLEMENTATION ...................................................................................................... 29

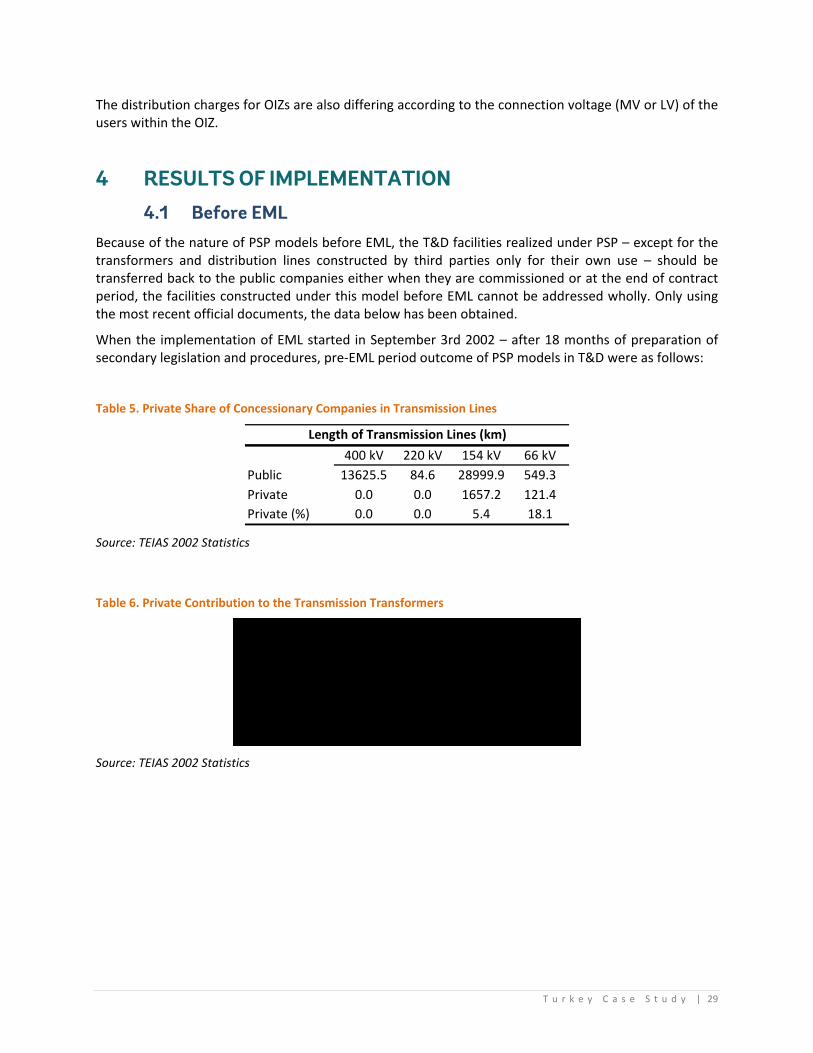

4.1 Before EML .............................................................................................................................. 29

4.2 After EML ................................................................................................................................ 30

5 OPERATIONAL PERFORMANCE OF PRIVATIZED (OR PRIVATELY OPERATED) T&D ASSETS ............. 34

6 PROBLEMS OF IMPLEMENTATION .................................................................................................. 38

7 CONCLUSIONS, LESSONS LEARNED, AND RECOMMENDATIONS .................................................... 40

APPENDIX 1: Transmission System ............................................................................................................. 46

APPENDIX 2: Distribution System ............................................................................................................... 48

T u r k e y C a s e S t u d y | i

EXECUTIVE SUMMARY PSP in Turkish power sector was started almost from the beginning of electricity generation within the country in the first decade of 20th century. Since then, depending on the macroeconomic policies and models preferred by the governments, there had been several distinct periods in which different models are used and for each period, the degree of participation of private sector to T&D activities and investments varied.

It can be said that, except the period up to 1930s, the main players in the field of power generation, transmission and distribution were either municipalities or various state organizations. Up to 1970s the system was fragmented, there was no interconnected transmission grid. The main priority was the electrification of the country, and all electrification programs were carried by public entities. The electrification and interconnected grid construction activities gained pace after consolidation of all activities under a single public authority TEK. PSP was very limited and there were only two vertically integrated regional concessionary companies and only one concessionary distribution company operating in a small region. Pubic companies were also shareholders of these concessionary companies.

In the concessionary regime which was implemented within the period up to the year 1984, the cost of the activity plus a predetermined profit is guaranteed to private participants. The disputes between the private participant and public authorities were to be solved by the State Council. Also concessionary contracts were reviewed by the State Council and should have been revised in accordance with the Council’s comments.

The first major step for liberalization and increasing the level of PSP in power sector was the issuance of the Law 3096 in 1984. The aim of the Law 3096 was to enable PSP in generation, transmission and distribution activities through private law assignment contracts as opposed to concession concept. Build Operate and Transfer and Autoproduction in generation, Transfer of Operating Rights for generation and distribution activities were the models for PSP in power business.

The “assignment” concept was enabling private law contracts, international arbitration for dispute settlement, and no State Council review or approval was needed. However, sometimes after, the Constitutional Court has ruled that, according to Turkish Constitution, the only mean for PSP in a public service is concession and private law cannot be used. As a result, except some BOT generation projects, which were enacted before cancellation, the implementation models brought by the Law 3096 is had to be realized with concession contracts. It was only after 1999, private law contracts and international arbitration was made possible by changing the Constitution. The main reason for this change is to attract private, especially foreign investors to the power sector investments; since administrative law contracts, administrative authorities’ involvement and lack of international arbitration were deemed risky by private investors.

During the period between 1984 and 2001, it was tried to privatize the distribution activities by TOOR method, however upon lawsuit applications of NGOs and labor unions, Council of State decisions, except two regions, all contracts were cancelled. Some of those contracts were private law contracts (enacted after 1999) and after international arbitration proceedings Turkish Government had to pay compensation.

The Turkish electricity market is one of the fastest growing markets throughout the World. The annual average consumption increase was 7.3 % in the last 30 years (1980‐2010), and it is expected that this fast growth will persist in the future. Therefore, there is a need for new generation investments to cope with the demand increase. The transmission and distribution system should also be expanded accordingly. It was necessary to attract local and foreign capital to power business, which was why the first steps have

ii | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

taken after 1984. However, the first steps were without solid legal footing. Rather than resulting from a long‐term restructuring plan; liberalization of the electricity industry stemmed from high demand growth, and a corresponding urgency for investment needs. Lacking of a properly working legal framework, the process has been subjected to interruptions and reversals. The overall outcome of the first phase of reform efforts (1984‐2001) can be summarized as comprising a moderate level of private capital inflow into the generation segment.

The problems encountered in the previous period led to find a different model for attracting private investment. The currently ongoing period of power market was started in March 2001 by the enactment of Electricity Market Law (“EML”) which aims to establish a liberal, competitive energy market and enables PSP in market activities through a licensing mechanism instead of concession. In fact the main policy since 2001 is to carry out all market activities except transmission by private parties instead of public companies and therefore EML basically envisages a private ownership in all market activities except transmission.

In Turkey “integrated transmission business model” is implemented. That is the transmission system operation and transmission grid ownership and operation is under the responsibility of a single transmission company (TEIAS). EML does not foresee a privately owned and operated transmission grid. TEIAS is a state owned company and independent of all supply and trading activities. The rationale for the selection of the integrated model and public ownership is discussed in the report. As a summary, it can be said that; the vital role of transmission for a reliable power system, the importance of independent and impartial transmission system operation for open access and competition, the need for coordinated operation and necessity for a central decision for investment planning were the main reasons for combining TSO and grid ownership under the same company.

Once the integrated model is selected for transmission and State owned company is assigned, the PSP in transmission activities are limited. However, there are two cases defined in the legislation that making possible PSP in transmission system investments such as: Realization or financing of the necessary investments by the generation companies on behalf of TEIAS for the connection of the power plant to the transmission system and construction and operation of a private direct line.

The PSP in distribution however, followed a different track. Rooting from highly politicized municipality ownership time, political interventions in management, price control policies, insufficient budget allocations have resulted in an inefficient operational performance and low quality of service. Furthermore, starting from 1980s, in parallel with liberalization policies in almost all sectors, PSP in distribution was on the agenda.

Distribution companies have two licenses: distribution license and retail license. Under distribution license, companies operate and maintain distribution system in their regions, carry out necessary expansion investments. Under retail license, they are supplier of non‐eligible consumers in their region. They are completely subject to regulation of EMRA.

The main model for PSP in distribution is privatization of the State‐owned regional companies operating the distribution systems, while the assets remain state‐owned. Today, the implementation of this model in Turkey is well underway, there are 21 distribution regional companies and 13 of them are privatized. The privatization model is “TOOR model backed Share Sale” model which is explained in detail in the report.

Other participation means such as participation in grid investments for generator connections or consumer connections also exist and they are described in detail in the report.

Distribution and retail activities in Organized Industrial Zones (OIZ) are also important PSP implementations in Turkish power market. OIZ legal entities can perform distribution and/or generation

T u r k e y C a s e S t u d y | iii

activities within the approved borders in order to meet the demands of their participants upon receiving license from EMRA.

In the scope of PSP in transmission, total estimated cost of the transmission facilities constructed or under construction by private sector is TL818 million (roughly $455 million) for the connection of 281 new power plants in the last 5 years.

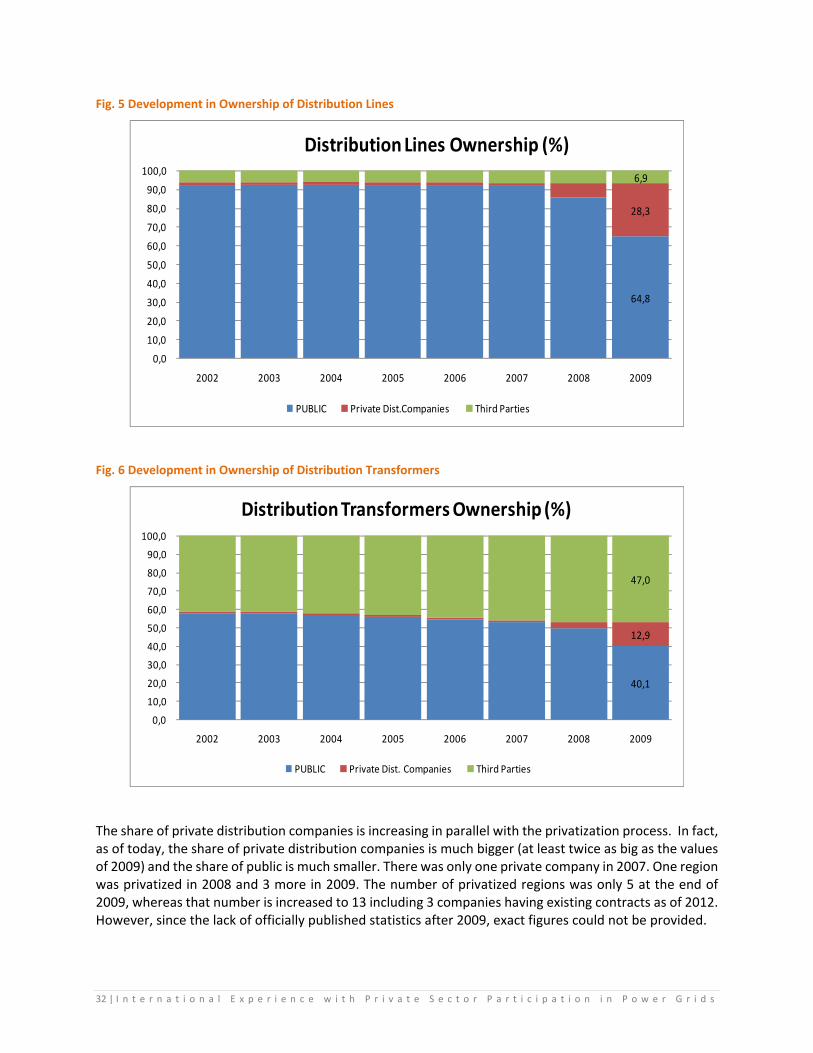

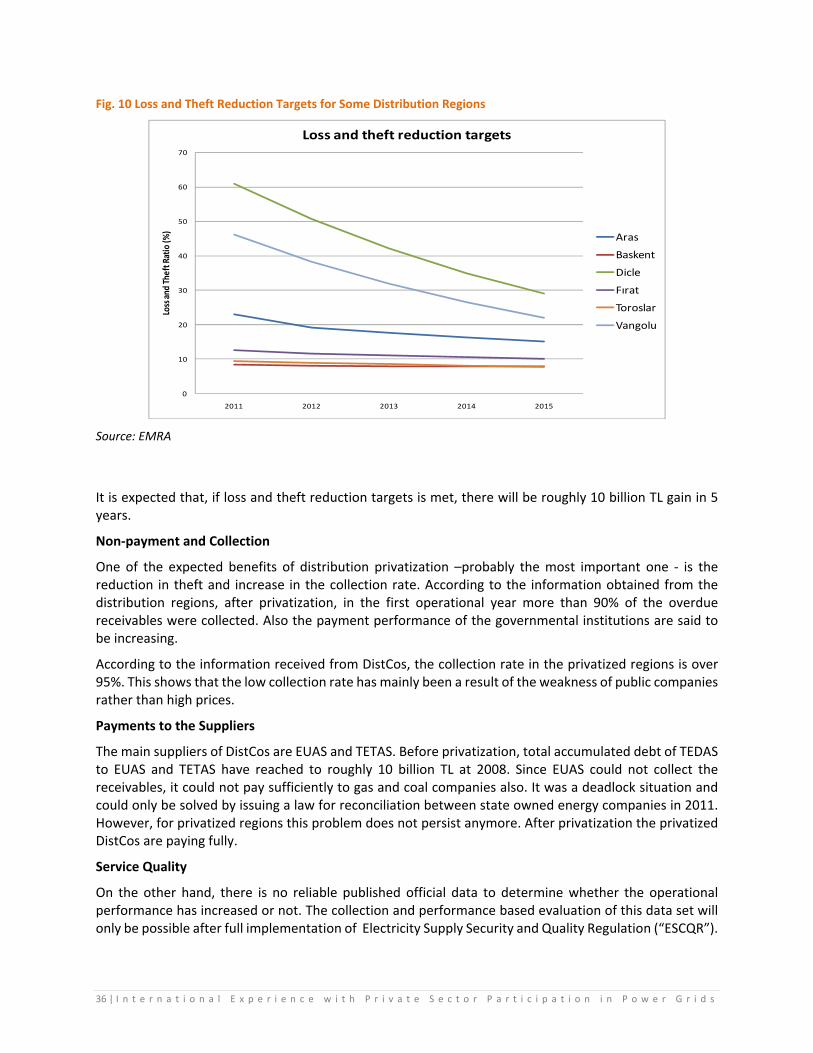

Since the privatization of the distribution business could only start in 2009 (although the process started earlier, due to delays and cancellations actual transfers of the assets started in 2009), and due to gradual transfer process in 2009‐2011 period, a meaningful PSP occurred only in the last two years of this period. Therefore it is not possible to make a general realistic assessment of the gains and/or shortcomings of the privatization. However, the public sector investments reduced by more than 50% after privatization. As opposed to previous payment problems, privatized DistCos are paying fully the cost of energy to the suppliers. Also improvements are reported in collection rates, and in service quality. The loss and theft reduction targets are determined and private DistCos are implementing the systems like Supervisory Control and Data Acquisition (SCADA) systems, Geographic Information Systems (GIS) and they are trying to renew or improve metering, registration and maintenance systems and activities, in order to met the service quality requirements and the loss reduction targets imposed by EMRA.

There are still some lingering problems impeding the successful implementation of the Turkish privatization model in distribution. However, it is expected that these “teething problems” will not persist for too long.

The Turkish experience shows that, first and foremost, a strong and credible judiciary is a necessary condition to employ the regulatory system as a means of securing PSP in the industry. The legal framework should be clearly defined and a consensus of related parties must be reached on the methods with which a “public service” can be provided by private sector.

Also the ownership issue with respect to restructuring and privatization should be solved. Since the assets in T&D grids are used for a public service, and since there is no other alternative, it can be claimed that those assets cannot be subjected in private ownership, like it has been interpreted in Turkey. This interpretation naturally depends on the legal system of countries, however, if interpreted like in Turkey; in order not to cause legal problems, the PSP model like TOOR can be implemented. Although asset ownership increases credibility of the private companies and reduces the risks, a long term operational rights can reduce uncertainty and can be used as a compromise.

The unbundling of distribution activities from retail and careful regulatory oversight for self‐dealing will enhance the effective competition in the market.

The regulatory framework should be prepared by taking into account the future developments and should not be changed frequently. To attract PSP, the regulations should be clear, consistent and simple as much as possible. However, at the same time, the balance between public benefit and incentives should be carefully considered.

If a country plans to liberalize the electricity market, implementing concession or assignment methods or long term contracts inherited from previous regime make the transformation complex and costly. If implementing such models is preferred, as an intermediary step, before liberalization, the related contracts should have an article about full compliance with the further legislative environment.

The unbundling of distribution activities from retail and careful regulatory oversight for self‐dealing will enhance the effective competition in the market. If private ownership is envisaged in transmission, then System Operation should be independent and careful regulatory oversight is needed to ensure non discriminatory transmission service.

iv | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

Cost based pricing is important for attracting PSP and for creating a well functioning market. However, especially for the countries like Turkey, where the demand increase rate is very high and substantial generation, transmission and distribution expansion investments are required, it is necessary to protect low income consumers against price increases.

T u r k e y C a s e S t u d y | 1

TURKEY CASE STUDY

1. INTRODUCTION Development of transmission and distribution (T&D) infrastructure is crucial for the power systems. Regardless of the market models and the ownership structure, they have to be adequate for the continuity of the energy flow, the reliability of the power system and the quality of the energy supply. They have to be developed in parallel with the generation expansion in order to cope with the energy demand and to provide a sustainable service to the users and consumers.

Furthermore, in the liberalized electricity markets, the lack of availability of transmission capacity, occurrence of transmission congestion, transmission pricing, etc. are deeply affecting the ability of the market participants to trade and to enter into the system, and may prevent effective competition in the market.

Private sector participation (PSP) mechanisms can be used in order to remove transmission and distribution bottlenecks without putting burden on public finances; or in order to speed up the transmission and distribution investments.

On the other hand, the T&D grid operations are not competitive activities. Due to their monopolistic nature, those activities should be regulated. Therefore, the dynamics and methods of PSP to T&D are different from PSP in generation and/or trade.

In this study, PSP practices of Turkey in T&D have been investigated. In this respect; a general overview and historical background has been given in Section 2. The structural and regulatory aspects of PSP models in T&D in the past and also after the reform have been explained in Section 3. It should be noted that, the PSP models used before the electricity market reform are also introduced in order to give information about different models. However, emphasis is given to the implementation of the recent PSP models. Results of implementation and problems are explained in sections 4, 5 and 6. Finally, conclusions, lessons learned and recommendations are discussed in Section 7.

2 GENERAL OVERVIEW AND HISTORICAL BACKGROUND PSP in Turkish power sector was started almost from the beginning of electricity generation within the country in the first decade of 20th century. Since then, depending on the macroeconomic policies and models preferred by the governments, there had been several distinct periods in which different models are used and for each period, the degree of participation of private sector to T&D activities and investments varied.

Although including some intermediary stages, the development of Turkish power system and PSP models can be overviewed historically in 3 distinct periods:

Zero point to 1984: From a fragmented system to country‐wide vertically integrated system.

1984 ‐ 2001: First liberalization and restructuring efforts and new models for PSP.

2001 ‐ Today: Competitive Electricity Market.

2 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

2.1 The Period until 1984 When the Turkish Republic was established in 1923, the installed capacity of Turkey was only 33 MW and only Istanbul, Tarsus and Adapazari had been using electricity.

Until the mid of 1930ies, the electricity generation and distribution activities were carried out by private concessionary companies (mostly foreign companies). Kayseri ve Civarı T.A.S. (“Kayseri Co.”), being a fully Turkish company was established at that time (1926). By following Kayseri Co. example, a lot of concessionary companies were established in 1926 – 1929 periods. The 154 kV transmission line from Silahtaraga power plant to Yedikule in Istanbul in the year 1927, and 26 kV transmission line between Visera and Trabzon on Black sea shore in 1929 were constructed by those concessionary companies.

In 1930, the Municipality Law was enacted and municipalities had gained the ability to deal with electricity activities and to make concessions for establishing and operating electricity facilities in their territory.

In 1935, three State‐owned enterprises were established. In this context, village electrification activities were carried out by Iller Bankasi (Bank of Provinces), thermal plants were constructed and operated by ETIBANK and hydropower plants were planned and constructed by Electrical Power Resources Survey and Development Administration (EIE).

In the second half of 1930ies, due to the lack of domestic capital accumulation, the rules had changed towards a centrally planned economy and a nationalization program in line with the other European countries was began to be implemented. As a result of this change, concessionary companies of electricity sector were transferred to municipalities (Ankara in 1938, Istanbul in 1939 and Izmir in 1943).

This period lasted to the first half of 1950’s; and after that, a new wave of private participation by the transfer of operational rights from municipalities to concessioner companies was started.

Turkey had not had a national interconnected grid in 1950ies; so municipalities, public companies and concessionary companies were generating and distributing electricity in their area of authority. The first step towards the construction of interconnected grid was the construction of 288 km, 154 kV transmission line between Zonguldak Catalagzi thermal power plant and Istanbul. The constructor company of the transmission line was Eregli Coal Enterprises (afterwards named as Turkish Hard Coal Enterprises ‐ TTK) which also constructed the Catalagzi hard coal TPP.

The main characteristic of that period is that, the electricity system is fragmented. There was a separated ownership structure that directly effecting the operation of the transmission and distribution systems. Concessionary companies and municipalities had their own rights and responsibilities with respect to execution of electricity generation, transmission and distribution and sale activities. Although there were different public organizations dealing with electrification, generation and development, there was no central planning for electrification, generation and transmission development. Also, there was practically no interconnected transmission grid.

The system was drastically changed again by the establishment of vertically integrated Turkish Electricity Authority (TEK) in 1970. TEK was established to own, operate and develop a national transmission and generation system. After the establishment of TEK, there had been a fast increase in generation and development of interconnected transmission system.

Although, the establishment of TEK helped for the improvement of the interconnection system overall management, the today’s country‐wide interconnection can only be ensured by the transfer of all assets including distribution assets hold by municipalities and Iller Bankasi to TEK in 1983 by after the enactment of Law No. 2705 in September 1982 except the assets of two regional vertically integrated concessionary companies Cukurova Electricity Company (“CEAS”) and Kepez Electricity Company (“KEPEZ”) which were

T u r k e y C a s e S t u d y | 3

established in early 50’s based on the Concession Law. After the transfers of these facilities, TEK became a real vertically integrated entity, carrying generation, transmission and distribution and sale activities in the country except two regions mentioned above.

2.2 The Period between 1984 and 2001 The very high demand growth and a corresponding urgency for investments needed the government to decide on the abolishment of TEK’s monopoly in electricity generation and distribution. In this respect, the enactment of Law No. 3096 in 1984 was started a new era for the liberalization of power sector even before most of the European countries’ experience.

The aim of the Law 3096 was to enable PSP in generation, transmission and distribution activities based on private law through assignment contracts as opposed to concession concept. However, due the general public opinion and the decisions of jurisdictional authorities at that time, Law No. 3096 was also forced to be implemented within the form of concession subjected to administrative jurisdiction by the Council of State. So, Build‐Operate‐Transfer (“BOT”) and Transfer of Operational Rights (“TOOR”) type PSP models of Law No. 3096 were bounded by concession concept. However, the Auto‐production model which was another type of PSP according to Law No. 3096 was implemented successfully without necessitating the concession concept.

Meanwhile, in 1994, TEK was restructured and two State‐owned companies, namely Turkish Electricity Generation and Transmission Company (“TEAS”) and Turkish Electricity Distribution Company (“TEDAS”) were established. This was the first step towards unbundling of the vertically integrated structure.

On the other hand, the Law No. 3996 which was also covered other sectors beside the energy sector enacted in 1994 in order to open the door again for contracts based on private law rather than the concession. Furthermore, through the Law No. 3996, regeneration of the Law No. 3096 was aimed also; but, the Constitutional Court cancelled the desired implementation of the relevant articles in 1995.

In 1997, through the enactment of Law No. 4283, the Build‐Own‐Operate (“BOO”) model is introduced for generation investments based on imported resources (i.e. natural gas) by taking into account the jurisdictional decisions that interrelated the use of domestic natural resources with the concession concept.

And, in 1999, the Parliament realized Constitutional amendments enabling the implementation of private law for BOT and TOOR models and also allowing international arbitration for dispute settlement. Accordingly a set of adjustment laws were enacted in which the international arbitration clauses became possible even for the already contracted projects based on Law No. 3096. However this time, the problem of “project selection” for Treasury Guarantee had occurred between governmental institutions and the expected benefit cannot be ensured. On the contrary, all of those efforts had counterproductive effects and Government struggled against international arbitration cases in the following years.

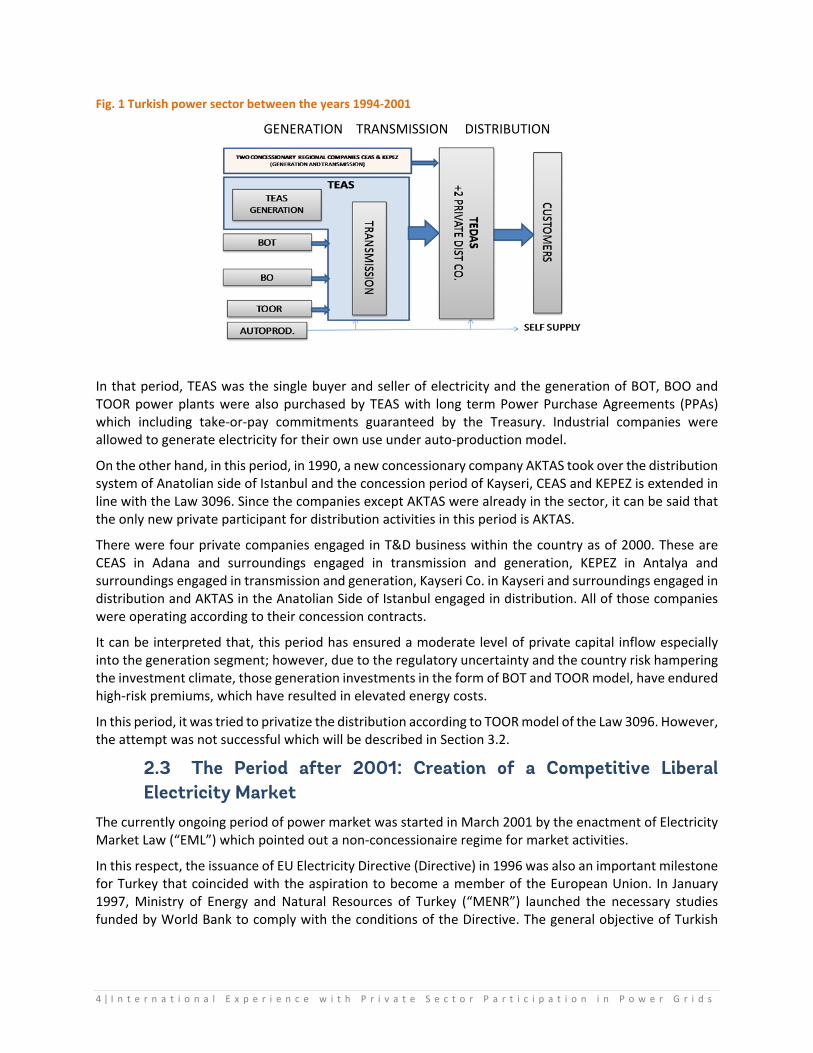

The sector structure occurred at the end of this period is shown in Fig. 1 below.

4 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

Fig. 1 Turkish power sector between the years 1994‐2001

GENERATION TRANSMISSION DISTRIBUTION

In that period, TEAS was the single buyer and seller of electricity and the generation of BOT, BOO and TOOR power plants were also purchased by TEAS with long term Power Purchase Agreements (PPAs) which including take‐or‐pay commitments guaranteed by the Treasury. Industrial companies were allowed to generate electricity for their own use under auto‐production model.

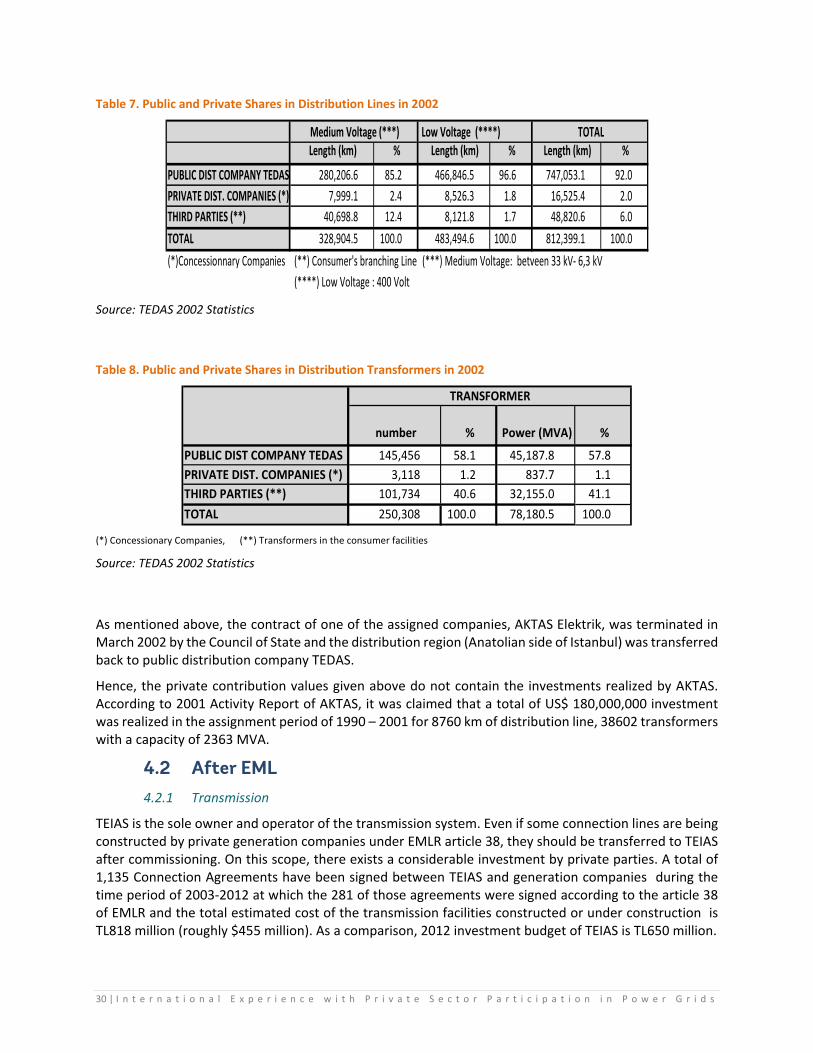

On the other hand, in this period, in 1990, a new concessionary company AKTAS took over the distribution system of Anatolian side of Istanbul and the concession period of Kayseri, CEAS and KEPEZ is extended in line with the Law 3096. Since the companies except AKTAS were already in the sector, it can be said that the only new private participant for distribution activities in this period is AKTAS.

There were four private companies engaged in T&D business within the country as of 2000. These are CEAS in Adana and surroundings engaged in transmission and generation, KEPEZ in Antalya and surroundings engaged in transmission and generation, Kayseri Co. in Kayseri and surroundings engaged in distribution and AKTAS in the Anatolian Side of Istanbul engaged in distribution. All of those companies were operating according to their concession contracts.

It can be interpreted that, this period has ensured a moderate level of private capital inflow especially into the generation segment; however, due to the regulatory uncertainty and the country risk hampering the investment climate, those generation investments in the form of BOT and TOOR model, have endured high‐risk premiums, which have resulted in elevated energy costs.

In this period, it was tried to privatize the distribution according to TOOR model of the Law 3096. However, the attempt was not successful which will be described in Section 3.2.

2.3 The Period after 2001: Creation of a Competitive Liberal Electricity Market

The currently ongoing period of power market was started in March 2001 by the enactment of Electricity Market Law (“EML”) which pointed out a non‐concessionaire regime for market activities.

In this respect, the issuance of EU Electricity Directive (Directive) in 1996 was also an important milestone for Turkey that coincided with the aspiration to become a member of the European Union. In January 1997, Ministry of Energy and Natural Resources of Turkey (“MENR”) launched the necessary studies funded by World Bank to comply with the conditions of the Directive. The general objective of Turkish

T u r k e y C a s e S t u d y | 5

governments for the improvement of economic efficiency and attracting investment into the power sector had also gained pace to the process.

Energy Market Regulatory Authority (“EMRA”) established by EML and became operational on November 2001 was prepared the secondary legislation according to the primary legislation set forth in EML during the Preparatory Period which was ended on 3rd of September 2002. On the other hand, the eligibility concept has been put into operation on 3rd of March 2003 according to EML . There had been many revisions and additions to the secondary legislation since then.

Together with the market reform introduced by EML, sectoral structure and market players are also changed. In this respect, TEAS was restructured to form three State‐owned Public Enterprises namely:

Turkish Electricity Transmission Company (“TEIAS”) for carrying out electricity transmission activities, system and the market operation;

Electricity Generation Company (“EUAS”) for carrying out electricity generation activities until fully privatized;

Turkish Electricity Trading and Contracting Company (“TETAS”) for carrying out electricity wholesale activities in order to undertake the long term PPAs (existing contracts) with BOO, BOT and TOOR companies.

These three companies, together with the Turkish Electricity Distribution Company (“TEDAS”) are the State‐owned players in the market.

In addition to EML and the secondary legislation, High Planning Council of Turkish Government (GoT) published 2004 and 2009 Strategy Papers with the aim to underline the commitment of GoT to the market reform and to constitute a road map for market liberalization, privatization and supply security issues.

On the other hand, by following the enactment of EML, the concession contract of AKTAS was cancelled by MENR upon the decision of the Council of State (DANISTAY), due to misconduct. The concession contracts of CEAS and KEPEZ companies were cancelled also by MENR as those companies did not fulfill the requirements of EML and did not obey the rules and procedures of the market reform introduced by EML even though their contracts oblige them to do so. In addition, Kayseri Co. has abandoned its concession contract and granted by EMRA as a licensed company through the revision of its contract in order to comply with the requirements of EML.

EML does not foresee the privately owned and operated transmission system, (a very important reason for the cancellation of the concession contracts of CEAS and KEPEZ companies was the resistance of those companies for the transferring of the transmission facilities to TEIAS), except private direct transmission lines.

6 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

The main model for PSP in distribution system is privatization. Privatization of distribution business is also an important element of market reform through EML. However, the realization of privatizations is considerably delayed and only 13 of 21 regions are privatized during the 10 year’s time. In principle, the Strategy Papers of GoT suggested the completion of distribution privatizations before privatization of power plants which are still pending. Forms of PSP other than full privatization are also possible for the distribution regions which are not privatized yet. The privatization model and other means for PSP in distribution business will be explained in Section 3.3.2.

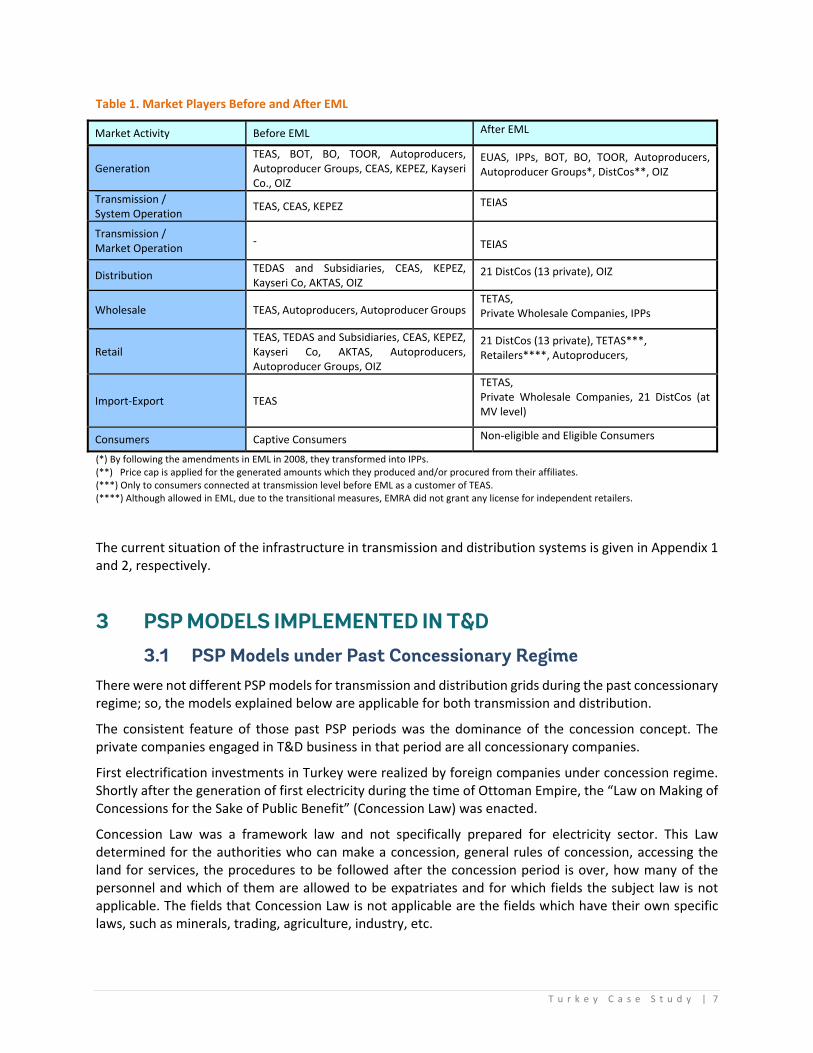

The fields of activities of the market players before and after EML are shown in the Table 1 below.

Box: Transmission Model

From the ownership and operation point of view, transmission business can be separated into two main categories: One is the transmission system control and operation (can also be named as power system operation) and the other is transmission network operation, maintenance and expansion. Both of those functions are vitally important for security of supply, for providing open access and establishment of a well‐functioning electricity market.

There are different models for running of transmission business. One option is to separate the system operation from the transmission network ownership and establish two entities: TSO and Grid Company. The other alternative, which also implemented in Turkey, is to set up a separate company, independent of all supply and trading activities, which combines the ownership of transmission with system operations (integrated model).

There may be different preferences for the selection of the business model; however, the independence of system operation is indispensible. In some countries there are still vertically integrated utilities which own and maintain the transmission grid either nationally or regionally. The general trend is to take the system operation and planning authorization from these utilities and hand over these functions to an independent system operator. However, the integrated company or utility have still the power to keep other competitors out.

The transmission system operation should be independent from generation and trade activities. The system operators have an enormous power to affect competition. Therefore, even if the integrated model is not selected, the transmission ownership should be unbundled from other activities.

Having only one owner and operator of transmission system has following advantages:

1 | Planning and operation of the transmission system by a single entity is much easier; 2 | There is only one entity that is responsible for the quality of electricity, 3 | Monitoring the independency of the single operator is also much easier. 4 | Coordination is easier and there will be no tension between TSO and transmission system

owner.

T u r k e y C a s e S t u d y | 7

Table 1. Market Players Before and After EML

Market Activity Before EML After EML

Generation TEAS, BOT, BO, TOOR, Autoproducers, Autoproducer Groups, CEAS, KEPEZ, Kayseri Co., OIZ

EUAS, IPPs, BOT, BO, TOOR, Autoproducers, Autoproducer Groups*, DistCos**, OIZ

Transmission / System Operation

TEAS, CEAS, KEPEZ TEIAS

Transmission / Market Operation

‐ TEIAS

Distribution TEDAS and Subsidiaries, CEAS, KEPEZ, Kayseri Co, AKTAS, OIZ

21 DistCos (13 private), OIZ

Wholesale TEAS, Autoproducers, Autoproducer Groups TETAS, Private Wholesale Companies, IPPs

Retail TEAS, TEDAS and Subsidiaries, CEAS, KEPEZ, Kayseri Co, AKTAS, Autoproducers, Autoproducer Groups, OIZ

21 DistCos (13 private), TETAS***, Retailers****, Autoproducers,

Import‐Export TEAS

TETAS, Private Wholesale Companies, 21 DistCos (at MV level)

Consumers Captive Consumers Non‐eligible and Eligible Consumers

(*) By following the amendments in EML in 2008, they transformed into IPPs. (**) Price cap is applied for the generated amounts which they produced and/or procured from their affiliates. (***) Only to consumers connected at transmission level before EML as a customer of TEAS. (****) Although allowed in EML, due to the transitional measures, EMRA did not grant any license for independent retailers.

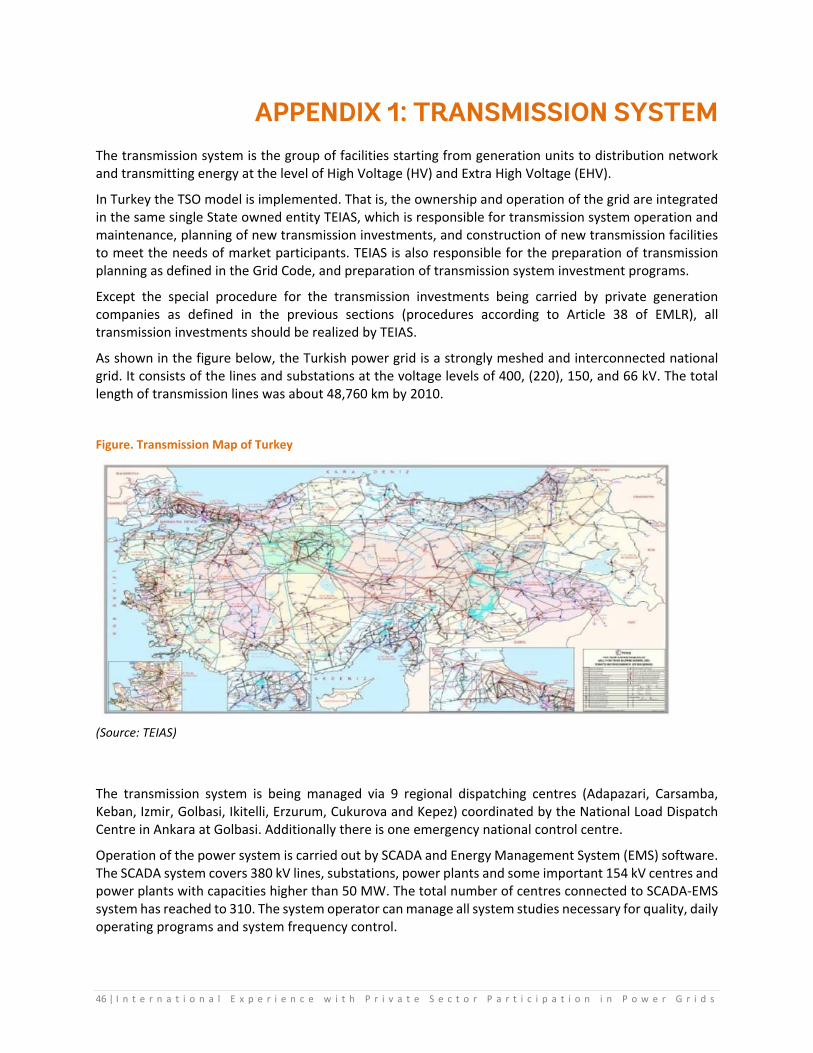

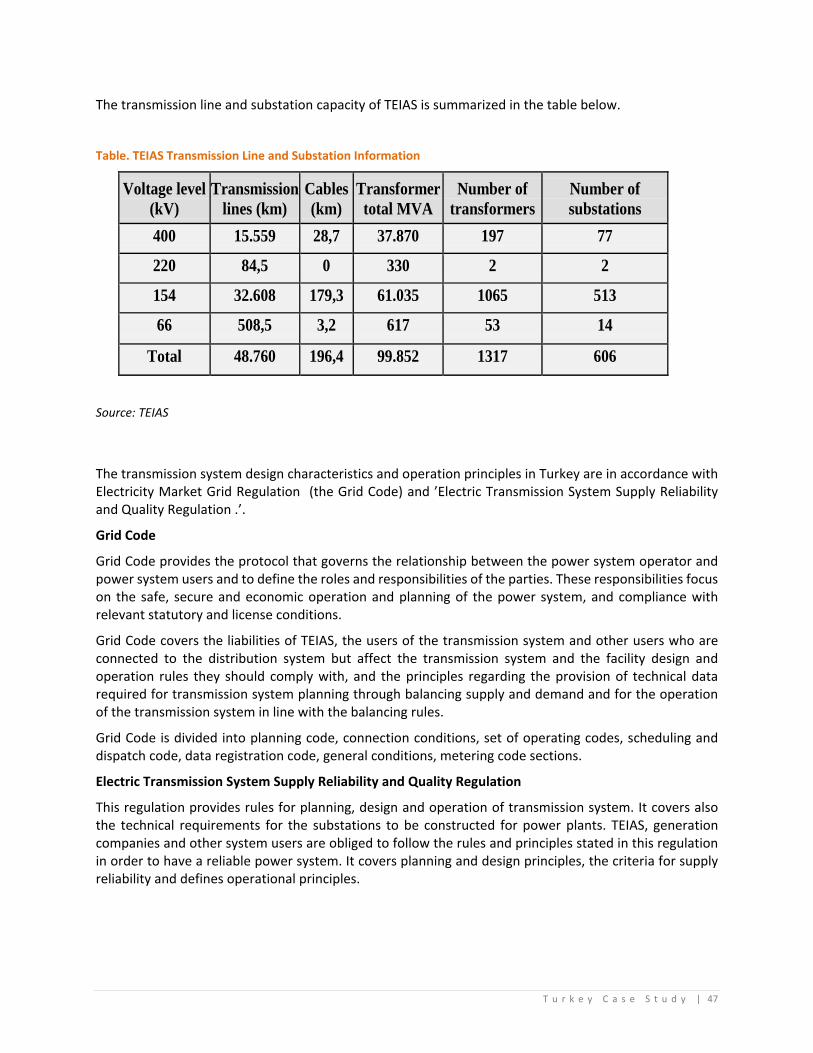

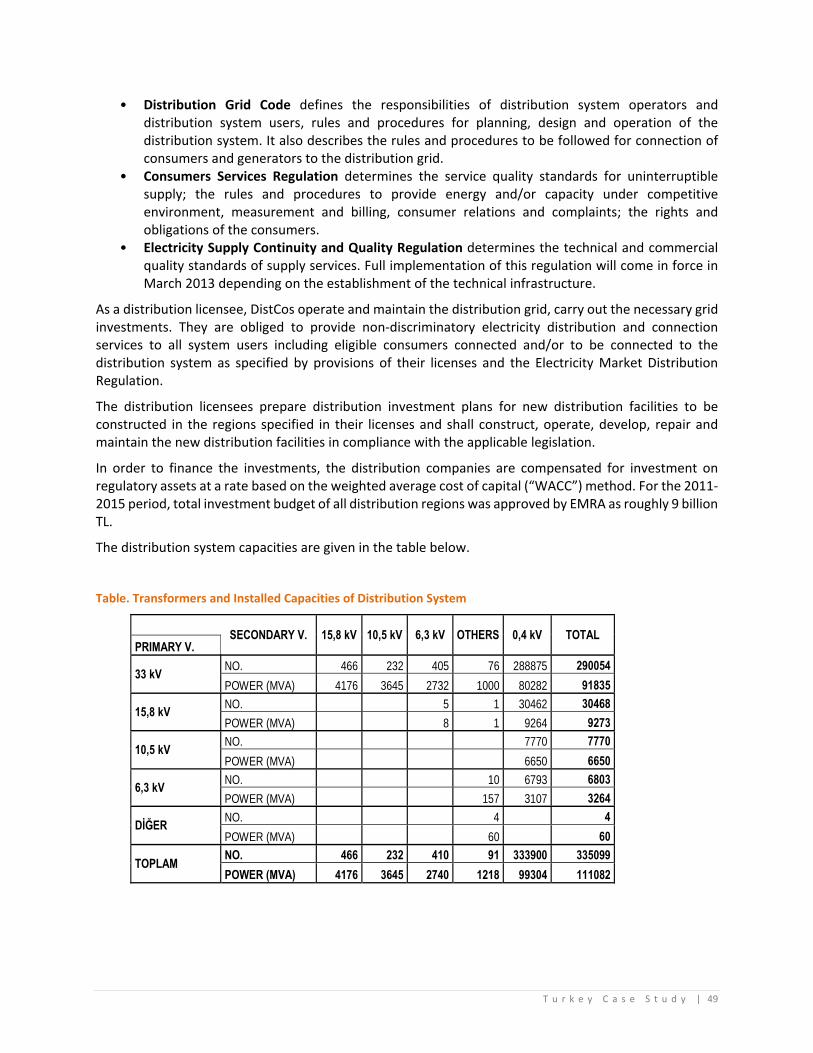

The current situation of the infrastructure in transmission and distribution systems is given in Appendix 1 and 2, respectively.

3 PSP MODELS IMPLEMENTED IN T&D 3.1 PSP Models under Past Concessionary Regime

There were not different PSP models for transmission and distribution grids during the past concessionary regime; so, the models explained below are applicable for both transmission and distribution.

The consistent feature of those past PSP periods was the dominance of the concession concept. The private companies engaged in T&D business in that period are all concessionary companies.

First electrification investments in Turkey were realized by foreign companies under concession regime. Shortly after the generation of first electricity during the time of Ottoman Empire, the “Law on Making of Concessions for the Sake of Public Benefit” (Concession Law) was enacted.

Concession Law was a framework law and not specifically prepared for electricity sector. This Law determined for the authorities who can make a concession, general rules of concession, accessing the land for services, the procedures to be followed after the concession period is over, how many of the personnel and which of them are allowed to be expatriates and for which fields the subject law is not applicable. The fields that Concession Law is not applicable are the fields which have their own specific laws, such as minerals, trading, agriculture, industry, etc.

8 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

The land and assets which are necessary for carrying out activities in the scope of a concession would be purchased by the concessionary company. The land which is necessary for temporary use under the concession would be transferred to the concessionary company by the local authorities after the indemnification, which is calculated in line with the Expropriation Law valuation procedure, was paid by the concessionary. If the required land belongs to public domain and not used for other purposes, subject land is given to the concessionary until the end of concession period free of charge. In any case, any cost incurred is paid by the concessionary and the assets would be transferred to government free of charge at the end of concession period. If it is deemed necessary by the Government, the tools and movables used in the concession activities might also be purchased by Government at the end of concession contract period. Also in the contract, at the end of concession period Government’s right of being a partner would take place.

In case that, new investments which were not existing in the concession contract, are realized with the approval of related ministry in the last 15 years of concession period, after completion of such investments, 1/15th of the cost of those investments would be deducted each year and remaining value would be paid to the concessionary at the end of concession period as an indemnification.

The concession contracts would be the enclosure of concession laws specific to the concessionary and would be reviewed, accepted or rejected by the parliament. The rules on tariff determination, revision and implementation take place in the Concession Law or Council of Ministers’ Decree specific to the concessionary.

It is impossible to assess the definite degree of unbundling during the past PSP periods due to the lack of the data. However, the installed capacity was 2,235 MW and the generation was 8.6 billion kWh in 1970 when TEK was established. And, in the year 1983 when the today’s interconnected system is ensured, the total installed capacity and the total energy generation was nearly 6,640 MW and 26.6 billion kWh respectively. In the same year (1983), the total length of transmission lines was 25,231 km and only 887 km of this total (3.5 %) was owned and operated by private sector.

Box: Concessionary Regime

There are primarily two regimes according to Turkish Constitution for the procurement of public services by private parties. One of them is licensing regime while the other is concession. However, until the constitutional amendment realized in 1999, the jurisdictional decisions did not allow private parties to operate under a regime other than concession in energy sector.

In the concessionary regime which was implemented in the period up to the year 1984, the cost of the activity plus a predetermined profit is guaranteed to private participants. The disputes between the private participant and public authorities were to be solved by the State Council. Also concessionary contracts were reviewed by the State Council and should have been revised in accordance with the Council’s comments.

Although pricing policy seems attractive from the financial point of view, dispute settlement mechanism (no international arbitration) and finalizing the contract draft with the State Council approval did not attract foreign capital investments under this model.

T u r k e y C a s e S t u d y | 9

3.2 PSP Model After 1984 1984 was an important date where the Law on Assigning Private Companies to Electricity Generation, Transmission, Distribution and Trade (Law No. 3096) was enacted to make private participation to power sector much easier.

With the introduction of Law No. 3096, the procedures were intended to be simplified and the related contracts were intended to be governed by private law rather than the concession. In this model, instead of providing concession for the activity, selected companies were “assigned” for carrying out the activity through an assignment contract. Essentially, except the dispute settlement method (in private law international arbitration is possible and no approval by the Council of State is needed; however, concession contracts should be submitted to the Council of State for approval) the main principles of the PSP model are the same.

The assignment regions where a private company will carry out electricity generation, transmission, distribution and trading should first be determined. The law foresees that electricity generation, transmission, distribution and trading authority in assignment regions may be given to private companies by the Council of Ministers upon suggestion of MENR. Before making such a suggestion, MENR is obliged to receive the positive opinion of State Planning Organization (SPO).

Box. Assignment and Concession Contracts in Turkish Case

With the fast increase in the electricity demand and limited capital accumulation of domestic businessmen, Turkey had strongly needed foreign capital inflow to the energy sector. However, being not a well known emerging economy, foreign investors exhibited hesitancy about the flow of payments they are going to receive and how Council of State would solve the disputes of a concessionary contract in case of conflicts.

To overcome such hesitation, an “assignment system” was introduced through Law No. 3096 in 1984. In this system, MENR would be a party of the implementation contract (governed by private law) to a private participant after that participant is assigned by the decree of Council of Ministers. This contract would be subjected to international arbitration in case of disputes and the first contracts had included such international arbitration clauses.

However, the Constitutional Court has decided that assignment is nothing more than making concession with the following reasons:

Any long‐term contract which was executed with a private party in power sector to carry out a public service is an administrative contract;

Supplying any public service by a private entity having all risk and benefits of the service by means of administrative contracts under the supervision of administration is concession;

According to the Constitution and Council of State’s Law, concession contracts should be reviewed and amended by Council of State.

So, the Constitutional Court has decided that assignment is in fact concession considering the nature of the service disregarding the written articles in the related Law. However, in 1999 after changes in Constitution, it was made possible to sign private law contracts instead of concession contracts.

10 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

The assignment process either in BOT or TOOR model was functioning in two ways.

In the first option, a company can submit a proposal to MENR for a market activity in a region. MENR was taking opinion of SPO about the proposal and completed its review and evaluation. If finally agreed and accepted by MENR, a decree of the Council of Ministers was asked by MENR first for the determination of an assignment region where MENR would enter into contract with private parties; and then another decree of the Council of Ministers have been taken for signing of an implementation agreement with a specified company for a specified period.

In the second option, MENR was asking for a decree of the Council of Ministers about determination of a region for assignment. After determination, MENR was making an announcement for assignment and companies were applying to MENR for tendering. The steps that are valid for the first option were followed for the qualified company through tendering process.

After receiving the decree of Council of Ministers, MENR enters into an implementation agreement for up to 99 years with the assigned company. The minimum assignment period is determined by considering the depreciation period of the planned investments. Following the execution of implementation agreement, in the light of implementation agreement articles, the related public companies enter into energy sales agreement and transfer of operational rights contract.

For the field of generation, the assigned company is obliged to utilize the primary energy sources for electricity generation to meet the demand of its assignment region. However, if the sources in the region are not adequate or for achieving generation economy, the assigned company may trade electricity with the public electricity company and/or with other assigned companies.

All the facilities, movable and immovable parts were transferred back to the government without any debt or liabilities at the end of the contract period either in BOT or in TOOR model. In case some assets are left which are not repaid through the tariff, the organization which receives the assets pays the cost of the un‐repaid portion. Also the contracts may be cancelled in case of insolvency or breach of contract conditions.

The tariff is determined on a cost plus basis and approved by MENR. Although the Law No. 3096 enables the assigned company to construct and operate transmission system in the assignment region as well, in some cases only the distribution grid in the region was transferred to the companies and the activity of current companies were limited with distribution.

In case of need of expropriation, MENR expropriates the necessary land and assigned company pays for the cost.

Two different contract types are implemented under TOOR model. First model is used for 2 distribution regions where all the risks were on the energy supplying company TEAS and model guarantees a predetermined profit to the distribution company. Profit was determined as a “reasonable return to the equity”.

At each year, a budget is prepared covering all operational expenses, and investment program. Energy was supplied by TEAS. The sale price of energy is determined through an energy sales agreement (ESA).

The company expenses and profit is transferred to the assigned company by adjusting the energy sale price of TEAS to assigned companies since national tariff is applied country wide. The investment program is prepared by the assigned company in line with the country’s electrification plan and the need of surrounding regions and implemented after the approval of MENR. The assigned company is obliged to include the investments to its investment program which are determined by MENR as well.

T u r k e y C a s e S t u d y | 11

After each year is over, costs and revenues are calculated using the actual values and financial reconciliation is achieved to adjust the income of the assigned company. As a result of the reconciliation process, if the company revenues are over than that of determined in the budget, the excess part is transferred back to TEAS. However, in case the result is negative, i.e. if the company cannot obtain the guaranteed profit, the deficient amount is to be paid back to the company.

Indeed, the reconciliation process created problems and accusations in time. Therefore, after two contracts (Kayseri Co. and AKTAS) the model is revised.

The second model used for the TOOR of distribution regions was realized through a tendering process. The main difference of this model is leaving of some risks to the company and removing the reconciliation process.

According to the model, the distribution regions can be transferred to private companies for operation for a limited time. The ownership of assets is remained owned with the state. The companies have exclusive rights to operate the region and to supply energy to all consumers in the region except the industrial companies supplied by autoproducers.

During the tendering process, each bidder prepared a feasibility report showing their expenses for operation, investments and loss and theft reduction programs, and expected profits for 30 years. They also proposed a transfer fee which will be repaid through tariffs.

Again, the energy sale price was used to ensure the revenues determined in the feasibility report which was the part of the contract. If the real revenue is over than the expected revenue in the feasibility report or the expenses are less, the company would make more profit. On the contrary, if the real expenditures of the company were over than the values determined in the feasibility report, then the company could not get expected profit or even lose. There is no compensation or no reconciliation.

On the other hand, there was no IPP’s and eligible consumer concept before EML. The only private energy producers were autoproducers and autoproducer groups which may decrease the consumption in a distribution region when they supply electricity to their shareholders. For such cases, if the consumption of the distribution region is decreased by at least 5%, energy sale price to the assigned company would have to be re‐determined in order to offset the loss of the distribution company. Also the transfer fees would be paid back through tariffs. Provided that they can keep the loss and theft ratios below the pre‐determined level and their operational expenses do not exceed their assumptions, their revenues are guaranteed.

On such conditions, Turkey had auctioned almost all distribution regions in 1996, but not succeeded to transfer the operational rights of the regions because of annulment of the authorizations of most of the companies by the Council of State, except for two regions, this process could not be finalized as described below.

12 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

It should also be mentioned that the studies and contract negotiations were coincided with the electricity sector restructuring studies and later with drafting of EML, and were not concluded successfully.

3.2.1 PSP for the Connection of Power Plants Build according to Previous BOT and BOO Models

During the planned economy years starting from 1961 when the power plants were constructed by public electricity companies, transmission grid was also planned and constructed by public electricity company

Box: Unsuccessful Distribution Privatization Attempt according to Law No. 3096

In 1995, 29 distribution regions are defined. Except 4 regions which were operated already by private companies at that time, it was decided to transfer the operating rights of 25 regions according to TOOR model defined in the Law No. 3096. Tenders were realized in 1996 and as a result of tenders, 20 companies were determined (for 5 regions the bids were found to be inappropriate). On the other hand, 3 of those 20 successful bidders did not fulfill the bureaucratic requirements and the Ministerial Council Decisions for remaining 17 regions which were necessary for the “assignment” of the companies, were obtained and MENR has been authorized for contractual negotiations. For some of the regions, contract negotiations for the making of concessions were completed and submitted the Council of State for approval since they were deemed as administrative contracts. Upon approval of the Council of State, some concession contracts were signed in 1997‐1999 period. At the same period, some organizations (NGOs and the labor unions) applied to the Council of State and brought suits against the Ministerial Council decisions and asked for cancellation of authorization.

While the cases against concession contracts were continuing, in 1999 Constitution has been changed and signing of implementation contracts (private law) instead of concession contracts became possible. Upon this change, new legislation is prepared and some of companies preferred to renew their concession contracts and applied for signing implementation contracts. MENR renewed the authorization from the Council of Ministers, and started the negotiations. As a result of negotiations a total of 6 implementation contracts were signed in addition to 5 concession contracts. However, new lawsuits were opened against those contracts also.

The cases against the Ministerial Council decisions and contracts took a long time. After 3 years, except 2 regions, the Council of State has cancelled the Ministerial Council Decisions and contracts could not be implemented.

The main reasons for the cancellation of contracts were:

The tendering conditions did not take public interest into consideration,

Investment programs for the regions were not asked from the companies.

The corruption claims against MENR and formal defects about the tendering process were also effective for cancellation decisions.

As a result, except two regions, the privatization process was not successful. After EML, the remaining two regions were renegotiated and their contracts were revised according to the new legislation and the regions were transferred.

The dispute resolution method for the implementation contracts was international arbitration. 4 companies applied to ICC for arbitration claiming for compensation. 1 claim is rejected; however, GoT has paid roughly $ 150 million to 3 companies.

T u r k e y C a s e S t u d y | 13

in parallel to the power plant construction. On the other hand, when the private companies began to be involved in electricity generation activities under BOT and BOO models, the location of the power plants and their commissioning dates were started to be determined by private companies. The speed of construction of power plants by private companies increased the risk of delay in completion of connection facilities by public electricity company. To overcome this difficulty, public electricity companies started to ask the generation companies to construct their connection facilities to distribution or transmission grid. The transmission or distribution facilities which connect the BOO or BOT generation facility to the existing transmission or distribution grid were constructed by the generation companies in accordance with the projects approved by TEAS or TEDAS companies.

The cost of connection facilities were included in the generation companies’ investment cost and hence paid back through energy sale (to the same public electricity companies) price. Such grid connection facilities were constructed by the generation companies on behalf of State‐owned transmission or generation companies and when the facilities are commissioned, the related State‐owned company (TEAS or TEDAS) had the title of connection facilities assets outside the power plant site.

Connection facilities of BOO model generation facilities under the Law No. 4283 were also constructed in a similar way. All BOO generation facilities are connected to the transmission grid and the cost of connection facilities were included in the investment cost of the generation facilities and the title of connection facilities assets outside the power plant site belongs to State‐owned transmission company.

3.2.2 Consumer’s Connection to the Grid

Electricity consumers on the other hand, were obliged to pay to the distribution company a connection contribution charge when they are first connected to the distribution grid. The connection contribution charge was determined by the distribution company for each customer group considering the economic conditions and paid per connection at kW basis. This charge has been changed into connection charge after EML.

On the other hand, some consumers such as agricultural irrigation customers and factories, malls, dwellings etc., may construct, own and operate transformers and connection lines in their property. The basic prerequisite of this implementation is that, the owner of the facilities should be the only user connected to the facilities he owned. If and when other users are connected to such facilities, the commonly used portion of those facilities should be transferred to regional distribution company.

3.3 EXISTING PSP MODELS IN T&D AFTER EML Previous PSP models are no longer in use after the enactment of EML. In line with the establishment of liberalized electricity market, previous PSP methods based on concession and guaranteed models such as BOT and BOO are not used. EML basically envisages a private ownership in all market activities except transmission and suggests competition in generation and trade. However, Turkey still is in a transition stage and there is a mixed ownership. In this section, the models for PSP being used after 2001 will be explained.

3.3.1 PSP in Transmission

The PSP models in transmission are regulated by EML and the secondary legislation issued according to EML.

EML does not foresee a privately owned and operated transmission grid. The rationale for this decision is elaborated in the Section 6. However, there are two cases defined in the legislation that making possible PSP in transmission system investments:

14 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

CASE 1: Realization or financing of the necessary investments by the generation license holder on behalf of TEIAS for the connection of the power plant to the transmission system in accordance with article 38 of Electricity Market Licensing Regulation (“EMLR”);

CASE 2: Construction and operation of a private direct line.

The fundamentals of the above mentioned regulatory cases can be summarized as follows:

The enormously increasing number of private generation projects portfolio and accompanying uncertainties for the connection of those plants to the T&D systems;

The budgetary constraints of TEIAS and accompanying deficiencies in infrastructure;

As a short‐term measure, making contribution to the supply security by solving of the connection problems of generation facilities.

3.3.1.1 CASE 1. Realization of transmission investments necessary for the connection of power plants by generation companies

According to EMLR Article 38 and Grid Code, if the connection point is approved by TEIAS and if new transmission facilities (substation, line) are not in TEIAS’ investment plan, or if the proposed timing of the new investment is not suitable for the investor, TEIAS can ask the market participants to construct the connection lines and the related equipment on behalf of TEIAS or finance their establishment. After the construction is completed and power plant is commissioned, the cost of investment is going to be repaid to the power plant license holder via transmission use of system fee. On the other hand, in 2008, with the amendments to EML aiming to speed up the generation investments in order to overcome tight supply‐demand balance; the repayment period was limited to maximum 10 years for the plants to be commissioned before 2015. Amended Provisional Article 14 and the related communiqué are given below:

EML Provisional Article 14

“Where new transmission facilities and installation of new transmission lines are required for connection of the generation plants to the system until the end of 2015, and if the sufficient financing not being available at TEIAS for the construction of said plants, these may be constructed or financed jointly by the legal entity or entities requesting connection to said plant.

The amount of the investment made shall be repaid within the framework of the plant agreement and the connection and use of system agreements to be signed between the related legal entity or entities and TEIAS. Repayment term shall be maximum ten years. Procedures and principles related with the said subject shall be arranged in a communiqué to be published by EMRA.”

Provisional Article 6th of the Communiqué for the Connection and Use of System in the Electricity Market

“Provided that the conditions in the provisional article 14 of EML have been met, the necessary investments can be realized individually or jointly by the license holder or holders according to the plant agreement signed with TEIAS. The ownership of the realized plant and lines shall belong to TEIAS.

In case of a jointly investment, the total cost of investment can be shared proportionally according to the electrical installed capacity figures of each licensee regulated in their respective licenses. The details of implementation shall be set by TEIAS.

T u r k e y C a s e S t u d y | 15

The total amount to be subjected to the repayment shall be calculated according to the methodology prepared by TEIAS and approved by the Board of EMRA. The payments shall begin in the subsequent year by following the completion of investments. Payments shall be made at the last working day of each month by the deduction of relevant costs for the use of system and the system operation amounts of each licensee by TEIAS. The total time period for repayment shall be 10 years starting with the temporary commissioning date of the plant and facilities by TEIAS. The interim period between the commissioning date and the subsequent implementation period shall be deducted from the 10 years time period. The repayments shall be done in each implementation period in monthly equal installments.”

The Methodology for the Fixation of Repayment Amounts of Realized Investments

“The total amount to be subjected to the repayment shall be calculated according to the occurred minimum total cost of similar investment projects having the same technical characteristics made by TEIAS during the time period between the signing of the Connection Agreement and the date of commissioning. Price difference calculations or escalation shall not be applied while calculating the total amount of investments.”

In this model, the operation of the transmission line is under the responsibility of TEIAS. That is, the generation company builds the transmission line and hand over to TEIAS after commissioning. Since the line is constructed on behalf of TEIAS, the design standards and technical requirements are designed and provided by TEIAS. There is a separate construction agreement between TEIAS and the generation company, describing the responsibilities and technical specifications for the facility to be constructed. These technical requirements are as per the Grid Code and TEIAS technical standards. Also, the land acquisition and expropriation approvals are obtained on behalf of TEIAS.

On the other hand, the substations of power plants generally constructed and operated by the plant owner. However, if this substation is used for the connection of other participants (other generators or consumers); then, the substation equipment which is used for the connections of other parties also, will become a part of the TEIAS transmission system and owned and operated by TEIAS.

3.3.1.2 CASE 2. Private Direct Transmission Line

If an alternative connection point cannot be proposed or the applicant does not accept the proposed connection point, applicant may propose to build a private direct transmission line within the scope of license application between the generation facility and partners and/or its customers. The line can be established on the condition that a transmission control agreement is signed between applicant legal entity and TEIAS.

Box: Private Direct Transmission Line

A transmission line which is not part a of the transmission system and constructed and operated in accordance with the provisions of the transmission control agreement to be signed with TEIAS and in line with the standards applicable for the national transmission network, providing electricity transmission between a generation facility owned by a legal entity holding a generation, auto‐producer or auto‐producer group license and its affiliates, partners and/or customers.

16 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

In addition to those cases, methods used by TEIAS such as outsourcing some of the maintenance work and operation of some substations can also be considered as limited methods for PSP to transmission. The lessons learned from Turkish experience for PSP in transmission is discussed in the last section of the report.

3.3.2 PSP in Distribution

The main model for PSP in distribution system is privatization. Other participation means such as participation in grid investments for generator connections or consumer connections also exist. In this section these models will be explained.

3.3.2.1 Distribution Privatization

As mentioned above, privatization of distribution business was on the agenda even before EML. Privatization of state owned distribution and generation is also accepted as necessary steps of sector reform which is aiming to create a competitive liberal electricity market.

The main differences from the previous regime are: under previous concessionary or assignment model, distribution companies had the exclusive rights in their territories, there was no eligibility concept, and distribution and retail sale was not differentiated as separate activities (no unbundling). Furthermore, that model was ensuring a determined profit. Whereas, in the new regime, the activities are unbundled, there is no exclusive right of the distribution companies to serve all the consumers in their region. Eligible consumers have the right to select their suppliers. Theoretically when the eligibility is enlarged to all consumers including households (full retail competition), the company will compete with other suppliers, otherwise they can only act as a service company for the investments, operation and maintenance of the distribution grid. Distribution privatizations are prioritized by the Strategy Papers of GoT.

The main pillars for the prioritization of distribution privatizations were:

• Improvement of service quality by timely and adequate realization of distribution grid investments;

• Implementation of cost‐reflective pricing without any kind of cross subsidization by the minimization of loss and theft ratios that are exhibiting a big variance in distribution regions;

• Ensuring the creditworthiness of distribution companies for generation investments as they serve a big amount of consumer portfolio;

• Empowering the autonomy of EMRA while setting the regulated tariffs and prices without political influence.

The first Strategy Paper of GoT has been issued on 17th of March 2004 by after long discussions about the execution of EML in all respects. The total number and contents of distribution regions were identified by this Paper and a road map is defined for the realization of distribution privatizations.

The aim and expected gains from market reform and privatizations are listed in the Paper as follows:

Box: Transmission Control Agreements

The bilateral agreements that are signed under the provisions of private law between TEIAS and the licensed legal entities owning or operating private direct transmission lines, and that set forth the minimum terms and conditions for compliance of the private direct transmission lines with the transmission system.

T u r k e y C a s e S t u d y | 17

• Obtaining substantial cost reductions through effective and efficient operation of generation and distribution assets by private parties;

• Ensuring the security of supply as well as the supply quality; • Reduction of technical loss ratios to the average values of OECD countries and termination of

theft; • Continuance of necessary expansion and renovation investments by private parties without

creating burden on state budget and contingent liabilities for the public; • Returning of the gains to the consumers through effective regulation and competition especially

in generation and trade segments of the market.

On the other hand, the model to be used for generation and distribution privatizations was actively discussed. And finally, the Privatization Administration (PA) has asked for the view of the Council of State.

The reasoned decision of the Council of State in March 2004 terminated the discussion and it has been decided that the TOOR model of Law No. 4046 (Privatization Law) will be applied for distribution privatizations. The model of PA is determined as a “TOOR model backed Share Sale model ("TSS model").

In accordance with the determined Road Map, TEDAS and its affiliated companies were restructured. In addition to one already privatized under concessionary regime, 20 State‐owned distribution companies were established. The operational rights of those regions were transferred from TEDAS to the regional companies. To enable this, TOOR Agreements between TEDAS and regional public companies were enacted. These companies are not asset owners, but they have rights to operate those regions.

As a result of privatization, the investor shall attain the shares of the distribution company which holds the operating rights of distribution assets and all related assets (e.g., buildings, vehicles, machine park), and the electricity distribution and retail licenses in a given region.

According to this model, the investor will be the sole owner of the shares of the distribution company which will be the unique licensee for the distribution of electricity in the designated region, but they will not have the ownership of distribution network assets. The ownership of these distribution assets will remain with TEDAS. The investor, through its shares in the distribution company, will be granted the right to operate the distribution assets pursuant to a "TOOR Agreement" with TEDAS.

Box. TOOR Model in Law. No. 4046

Currently implemented DistCo privatization model has been derived from the TOOR model under Law No. 4046 by taking into account the lessons learned with respect to distribution privatization attempts in Turkey. Although Law No. 4046 includes the asset sale model, due to the historical background and the final view of the Council of State, the TSS model has been produced depending on the TOOR model in 4046.

So, the current TOOR concept is completely different than the TOOR model of Law No. 3096.

In this new model, the operating rights were transferred to a public DistCo leaving the title of assets with TEDAŞ. In the privatization process, the shares of that public DistCo was block sold to private parties. These private parties operate distribution regions without any guarantee of profit under the revenue cap regulation model. They are completely subject to regulation of EMRA. The consumers in their region may shift if they are eligible and if they feel that they have more favorable seller

18 | I n t e r n a t i o n a l E x p e r i e n c e w i t h P r i v a t e S e c t o r P a r t i c i p a t i o n i n P o w e r G r i d s

After privatization, the distribution company having the operational rights will still remain as the party of TOOR and only the owner of that company changes. Hence, TOOR also contains articles which mostly are in effect after the public distribution company is privatized by way of share transfer.

In the TSS model, asset ownership of new as well as existing distribution assets belong to TEDAS, while the investor attains the right to operate the distribution network together with the obligation to undertake the necessary investments.

In this respect:

• The ownership of the existing assets and the new assets arising from investments to be carried out by the investor; rests with TEDAS. The legal obligations relating to the asset base before the signing of the TOOR Agreement (for example, expropriation costs) have been assumed by TEDAS.

• All investments shall be realized by the investor and will be recovered through the tariffs. Except for cases of investor misconduct, the part of investments not yet recovered via the tariffs shall be paid by TEDAS to the investor upon the expiry or termination of the contract.

Not only all distribution assets transferred to DistCos belong to TEDAS; but also new assets invested by DistCos will be owned by TEDAS. In order to implement rules of the current legislation, Articles 272 and 327 of Tax Procedure Law numbered 213 was amended to enable DistCos to amortize the investments which are realized after privatization and to reimburse the cost of investments.

Since the DistCos do not have any assets and any depreciation in first tariff implementation period (2006‐2010), EMRA determined an additional income component, named the TOOR Charge component, to the distribution tariff to enable DistCos to finance the required investments. In this period depreciation term was determined as 5 years. In the second tariff implementation period (2011‐2015), since DistCos have adequate depreciation income, the TOOR Charge component was removed and depreciation term increased to 10 years.

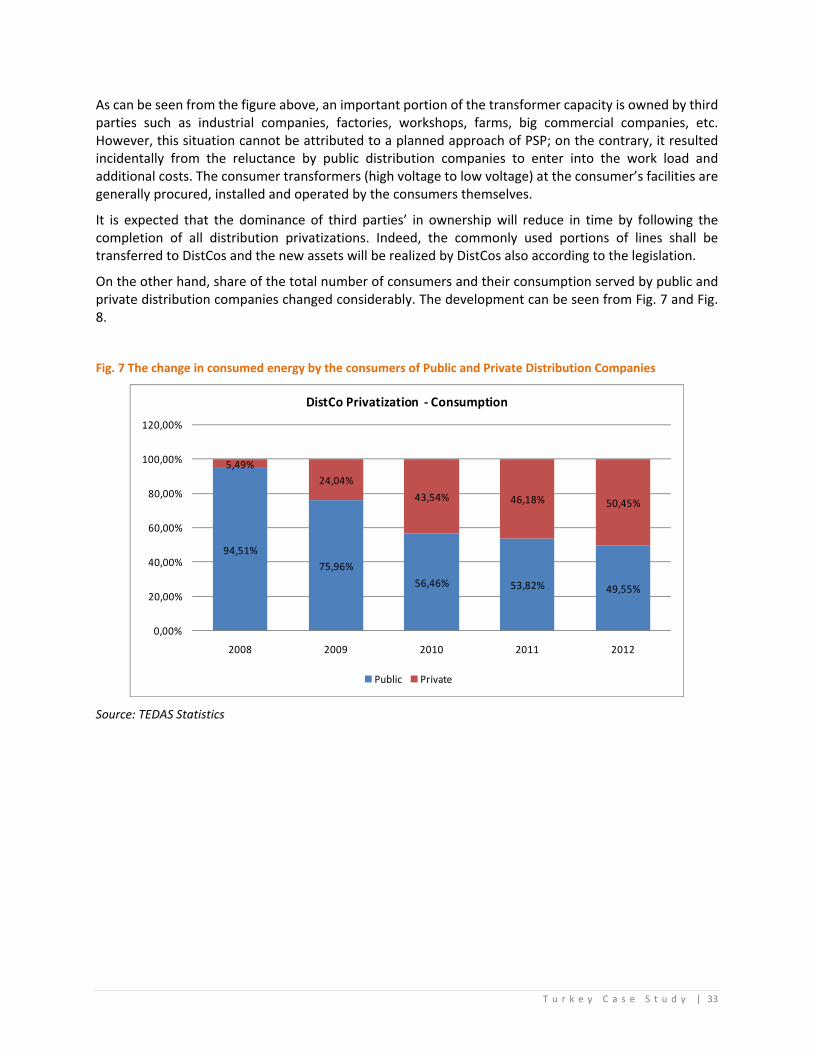

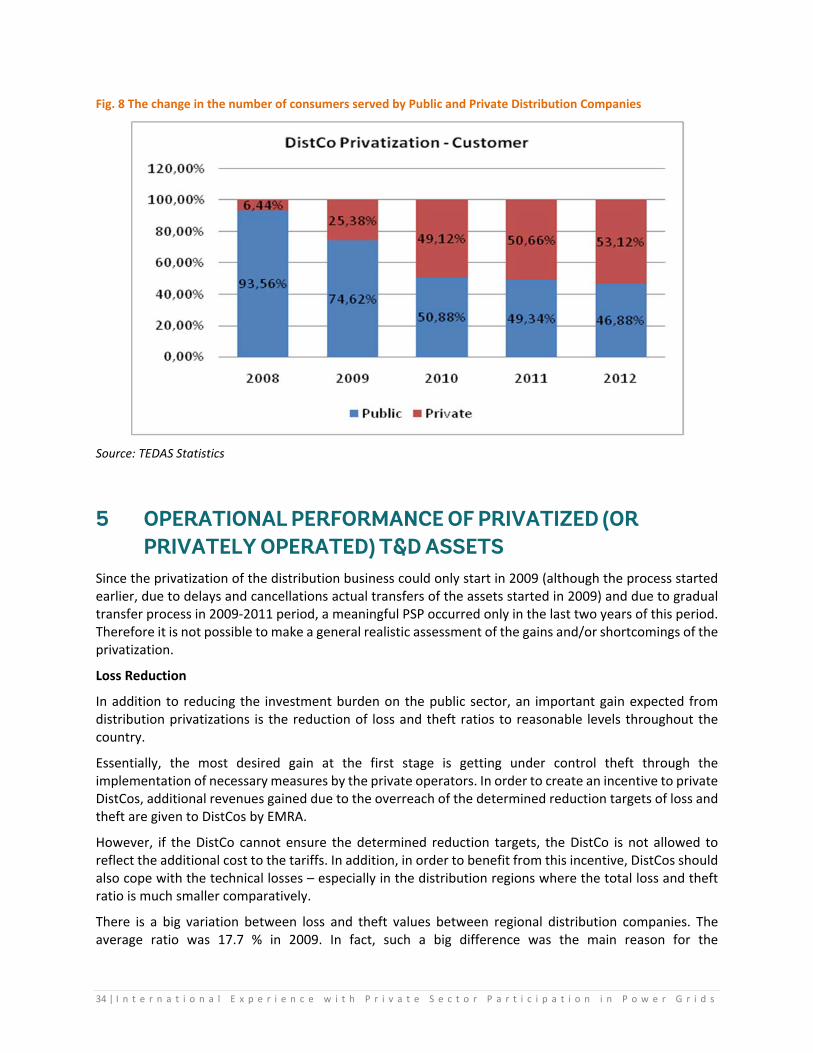

The first Strategy Paper was brought forward the end of 2006 for the completion of distribution privatizations. However, privatizations could only be started in 2008 and the first transfer was realized in January 2009 by the transfer of the shares of Baskent DistCo to EnerjiSa. As of the beginning of 2012, out of 21 distribution regions, 13 regions have been operated by private parties. Those companies distribute around 50% of the electricity consumed as of 2012.

T u r k e y C a s e S t u d y | 19

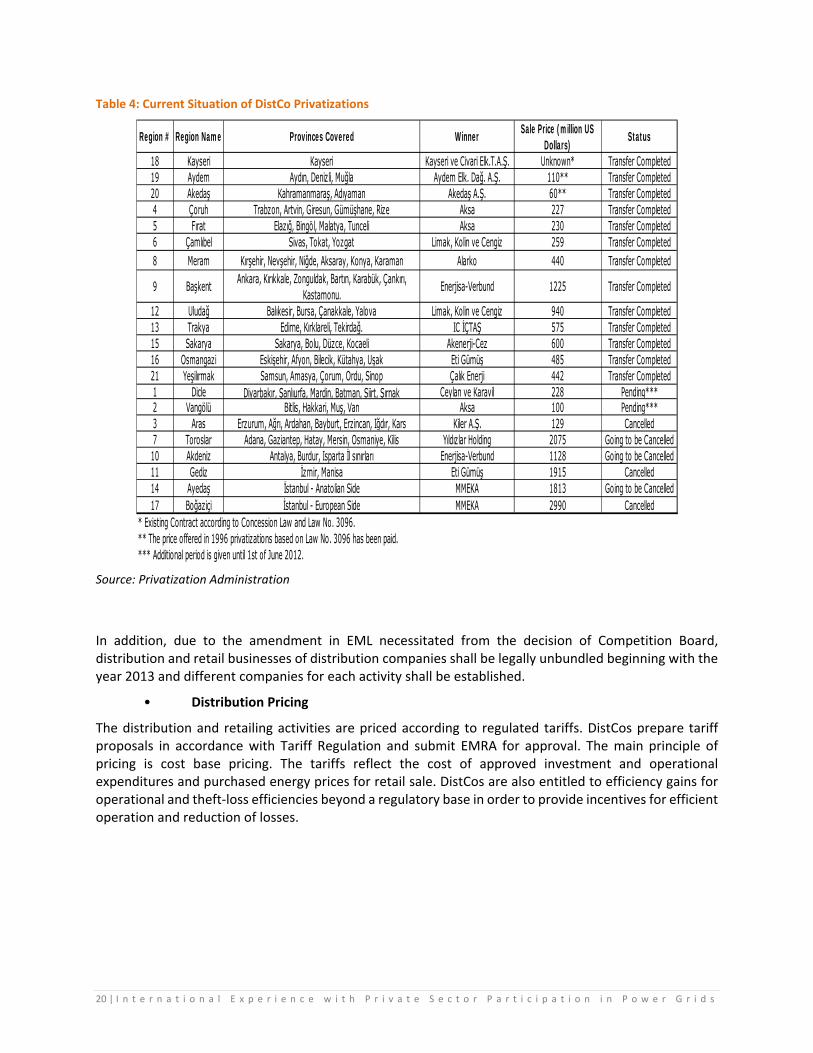

The current situation of distribution privatizations is shown in the table below. As it can be seen, total distribution privatization revenue of GoT is around US $5,700 million.

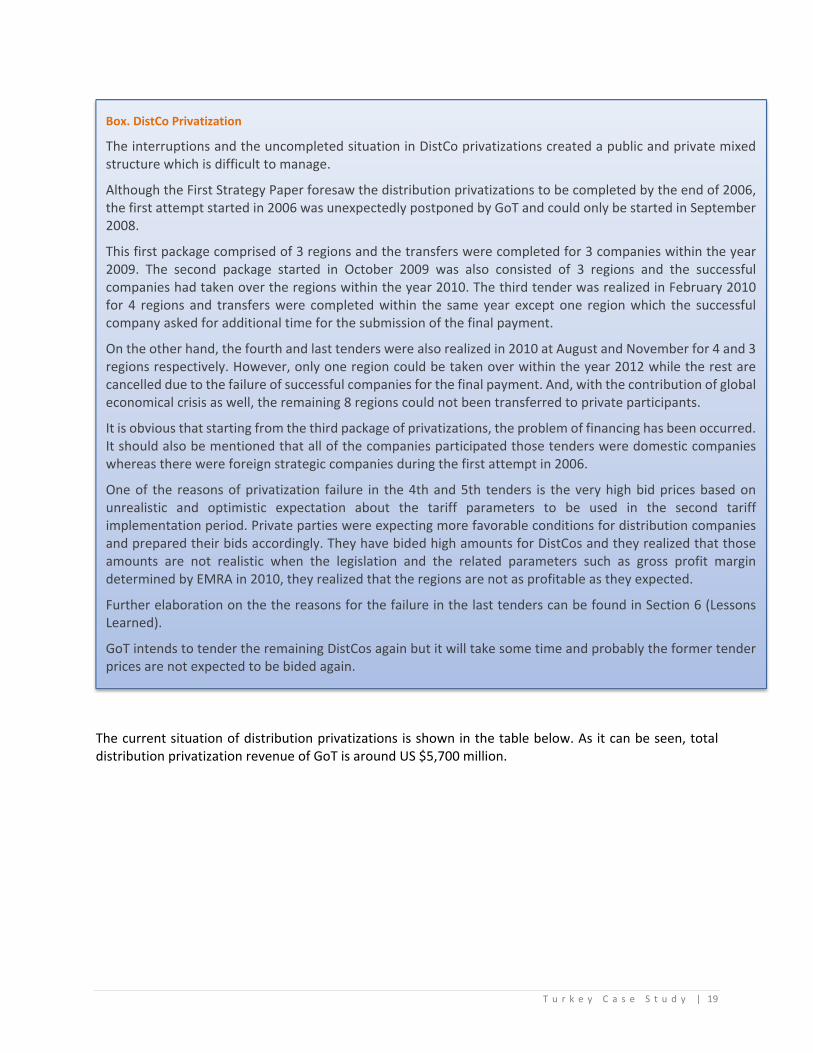

Box. DistCo Privatization

The interruptions and the uncompleted situation in DistCo privatizations created a public and private mixed structure which is difficult to manage.

Although the First Strategy Paper foresaw the distribution privatizations to be completed by the end of 2006, the first attempt started in 2006 was unexpectedly postponed by GoT and could only be started in September 2008.