balance sheet, t-accounts and the simple ledger the recording process unit 2

TRANSCRIPT

Balance Sheet, T-Accounts and the Simple Ledger

THE RECORDING PROCESS

Unit

2

THE ACCOUNTTHE ACCOUNT

An account is an individual accounting record of increases and decreases in a specific asset, liability, or owner’s equity item.

An account is a page specifically designed to record the changes in each individual item affecting the financial position

Each item will have its own account.

A company will have separate accounts for such items as cash, salaries expense, accounts payable, and so on.

THE LEDGERTHE LEDGER

The entire group of accounts maintained by a company is referred to collectively as the ledger.

A general ledger contains all the assets, liabilities, and owner’s equity accounts.

GENERAL LEDGER

ANALYZING THE ACCOUNTING EQUATION

The alignment of these parts resembles the letter T, and therefore the account form is called a T account.

ACCOUNTS

In its simplest form, an account consists of

1. the title of the account,

2. a left or debit side, and

3. a right or credit side.

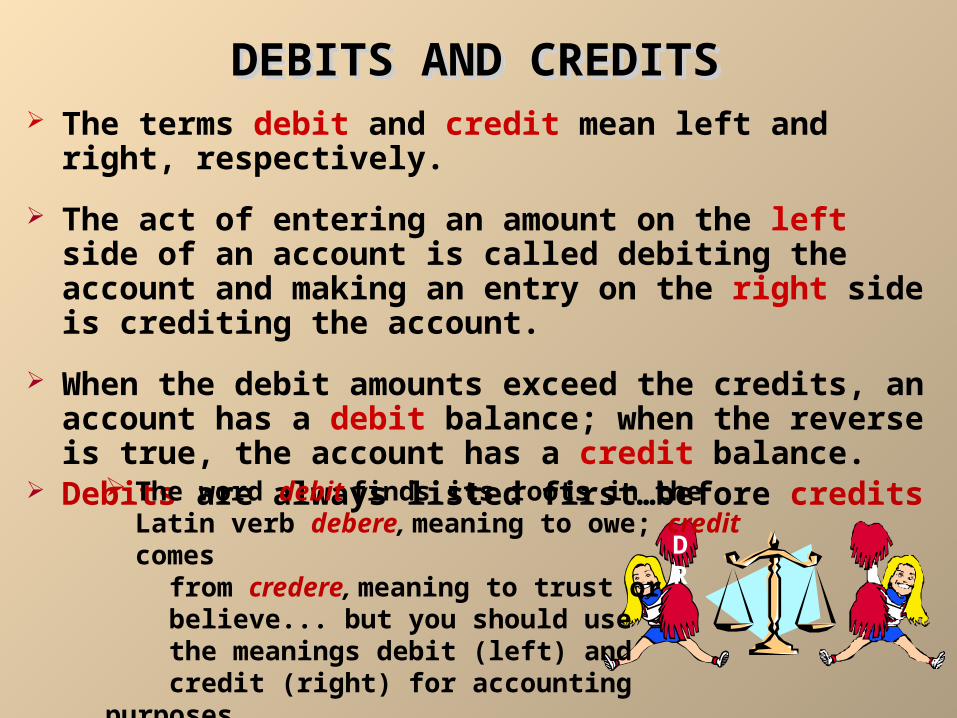

DEBITS AND CREDITSDEBITS AND CREDITS The terms debit and credit mean left and right, respectively.

The act of entering an amount on the left side of an account is called debiting the account and making an entry on the right side is crediting the account.

When the debit amounts exceed the credits, an account has a debit balance; when the reverse is true, the account has a credit balance.

Debits are always listed first…before credits

DR

CR

The word debit finds its roots in the Latin verb debere, meaning to owe; credit comes

from credere, meaning to trust or believe... but you should use the meanings debit (left) and credit (right) for accounting purposes.

NORMAL BALANCENORMAL BALANCE

Every account classification has a normal balance, whether it is a debit or credit.

ACCOUNT BALANCES

INCREASES AND DECREASES IN ACCOUNTS

OPENING THE LEDGEROPENING THE LEDGER The balance sheet shown below can be visualized as a large "T," with the assets on the left and the liabilities and owner's equity on the right.

This will help you remember that asset accounts normally have debit balances (balances shown on the left side of the T-account), while liability and owner's equity accounts have credit balances (balances shown on the right side of the T-account) .

To open accounts in the ledger, these steps should be followed:

• Place the account name in the middle of each account.

• Record the date and opening balance from the balance sheet on the appropriate side in the account.

OPENING THE LEDGEROPENING THE LEDGER

Example: The owner makes an initial investment of $15,000 to start the business. Cash is debited and the owner’s Capital account is credited.

Example: The owner makes an initial investment of $15,000 to start the business. Cash is debited and the owner’s Capital account is credited.

DEBITING AN ACCOUNTDEBITING AN ACCOUNT

15,000 Cash

Example: Monthly rent of $7,000 is paid. Cash is credited and Rent Expense is debited.

Example: Monthly rent of $7,000 is paid. Cash is credited and Rent Expense is debited.

CREDITING AN ACCOUNTCREDITING AN ACCOUNT

7,000 Cash

Example: The owner makes an initial investment of $15,000 to start the business. Cash is debited and the owner’s Capital account is credited.

Example: The owner makes an initial investment of $15,000 to start the business. Cash is debited and the owner’s Capital account is credited.

DEBITING AN ACCOUNTDEBITING AN ACCOUNT

15,000 Cash

Example: Monthly rent of $7,000 is paid. Cash is credited and Rent Expense is debited.

Example: Monthly rent of $7,000 is paid. Cash is credited and Rent Expense is debited.

CREDITING AN ACCOUNTCREDITING AN ACCOUNT

7,000 Cash

DEBITING AND CREDITING AN ACCOUNT

DEBITING AND CREDITING AN ACCOUNT

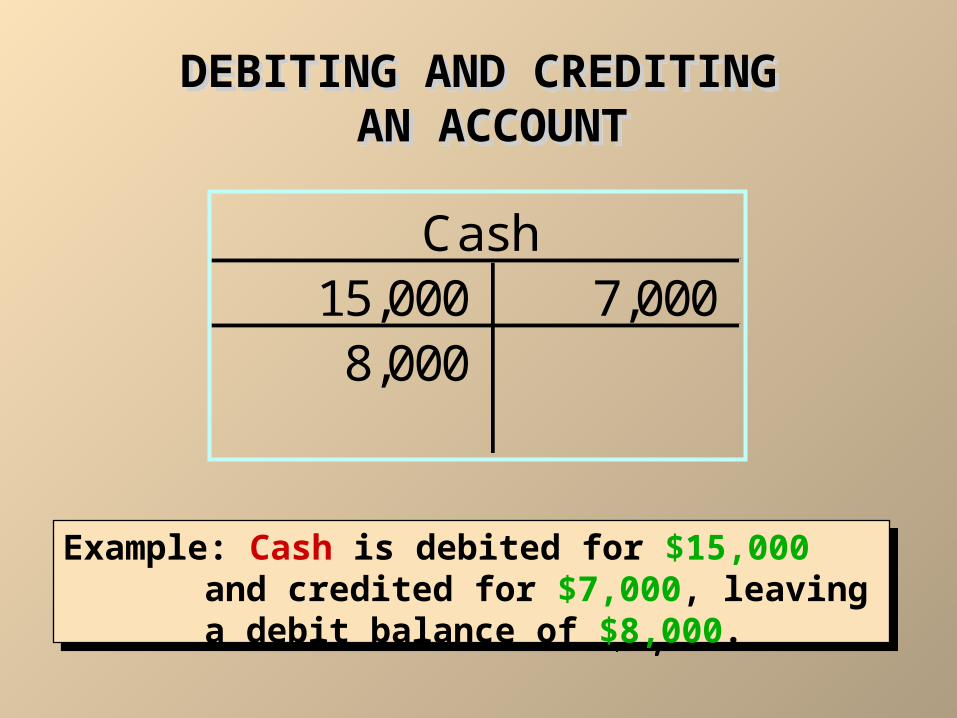

Example: Cash is debited for $15,000 and credited for $7,000, leaving a debit balance of $8,000.

Example: Cash is debited for $15,000 and credited for $7,000, leaving a debit balance of $8,000.

15,000 7,000 8,000

Cash

Calculating New Balances in the Accounts

To determine the new account balance, the following calculations are made for each account:

1. Add up the debit side of the account.2. Add up the credit side of the account.3. Subtract the smaller amount from the larger and place the answer on the larger side of the account. This is the new balance.

Analyzing How Transactions Affect

Accounts

NORMAL BALANCES — ASSETS AND LIABILITIESNORMAL BALANCES — ASSETS AND LIABILITIES

Assets

Increase Decrease Debit Credit

Decrease Increase Debit Credit

Liabilities

Normal Balance

Normal Balance

PAID CASH FOR SUPPLIES

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

August 3. Paid cash for supplies, $275.00.

1 12

3 3

4 4

1. Which accounts are affected?

1. Which accounts are affected?

PAID CASH FOR INSURANCE

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

August 4. Paid cash for insurance, $1,200.00.

1 12

3 3

4 4

BOUGHT SUPPLIES ON ACCOUNT

August 7. Bought supplies on account from Supply Depot, $500.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

1 1

3 3

4 4

2 2

PAID CASH ON ACCOUNT

August 11. Paid cash on account to Supply Depot, $300.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

1 1

3 3

4 4

2 2

DOUBLE-ENTRY SYSTEMDOUBLE-ENTRY SYSTEM

In a double-entry system, equal debits and credits are made in the accounts for each transaction.

Thus, the total debits will always equal the total credits and the accounting equation will always stay in balance.

Assets Liabilities Equity

Analyzing How Transactions Affect Owner’s Equity

Accounts

NORMAL BALANCE — OWNER’S CAPITALNORMAL BALANCE — OWNER’S CAPITAL

Owner’s Capital

Decrease Increase Debit Credit

Normal Balance

RECEIVED CASH FROM SALES

August 12. Received cash from sales, $295.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

1 1

3 3

4 4

2 2

SOLD SERVICES ON ACCOUNT

August 12. Sold services on account to Oakdale School, $350.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

1 1

3 3

4 4

2 2

PAID CASH FOR AN EXPENSE

August 12. Paid cash for rent, $300.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

1

1

4

4

2 2

3

3

3

NORMAL BALANCE — OWNER’S DRAWINGSNORMAL BALANCE — OWNER’S DRAWINGS

Owner’s Drawings

Normal Balance

Increase Decrease Debit Credit

PAID CASH TO OWNER FOR PERSONAL USEAugust 12. Paid cash to owner for personal use, $125.00.

1. Which accounts are affected?

2. How is each account classified?

3. How is each classification changed?

4. How is each amount entered in the accounts?

4

4

2

2

3

3

3

1

1

THE TRIAL BALANCETHE TRIAL BALANCE

A trial balance is a list of accounts and their balances at a given time.

The primary purpose of a trial balance is to prove the mathematical equality of debits and credits after posting.

A trial balance also uncovers errors in journalizing and posting.

The procedures for preparing a trial balance consist of

1. listing the account titles and their balances,

2. totaling the debit and credit columns, and

3. proving the equality of the two columns.

PIONEER ADVERTISING AGENCYTrial Balance

October 31, 2002

Debit CreditCash $ 15,200Advertising Supplies 2,500Prepaid Insurance 600Office Equipment 5,000Notes Payable $ 5,000Accounts Payable 2,500Unearned Revenue 1,200C. R. Byrd, Capital 10,000C. R. Byrd, Drawings 500Service Revenue 10,000Salaries Expense

900$ 28,700 $ 28,700

The total debits must equal the total credits.

The total debits must equal the total credits.

A TRIAL BALANCEA TRIAL BALANCE

Rent Expense4,000

LIMITATIONS OF A TRIAL BALANCE

LIMITATIONS OF A TRIAL BALANCE

A trial balance does not prove that all transactions have been recorded or that the ledger is correct.

Numerous errors may exist even though the trial balance columns agree.

The trial balance may balance even when

1. a transaction is not journalized,2. a correct journal entry is not posted,3. a journal entry is posted twice,4. incorrect accounts are used in journalizing or posting,

5. offsetting errors are made in recording the amount of the transaction.

EXPANDED BASIC EQUATION AND DEBIT/CREDIT RULES AND EFFECTSEXPANDED BASIC EQUATION AND

DEBIT/CREDIT RULES AND EFFECTS

LiabilitiesAssets Owner’s Equity

= + -

+=

+ -

Assets

Dr. Cr.+ -

Liabilities

Dr. Cr.- +

Dr. Cr.

Owner’s Drawings

+ -

Dr. Cr.

Revenues

- +Dr. Cr.

Expenses

+ -

Dr. Cr.

Owner’s Capital

- +

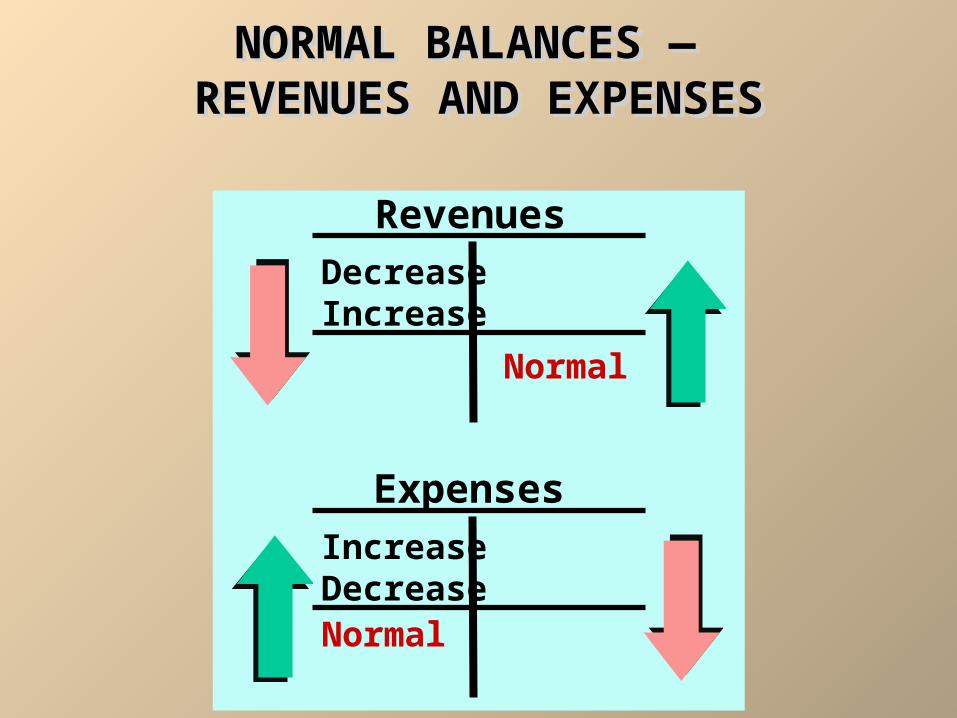

NORMAL BALANCES — REVENUES AND EXPENSES

NORMAL BALANCES — REVENUES AND EXPENSES

Increase Decrease Debit Credit

Expenses

Revenues

Decrease Increase Debit Credit

Normal BalanceNormal

Balance

Summary of Accounting Procedures