balancing the balance sheet and resolving other disputes ppt...– elements of the balance sheet...

TRANSCRIPT

© 2016 Morgan, Lewis & Bockius LLP

M&A ACADEMY: BALANCING THE BALANCE SHEET AND RESOLVING DISPUTESKaren Abesamis

Michael Blanchard

December 18, 2018

Overview of Presentation

• Purchase Price Adjustments

• Net Working Capital

– General Overview

– Negotiation and Drafting Best Practices

– Litigation Risk Management Considerations

• Earn-Outs

– General Overview

– Negotiation and Drafting Best Practices

– Litigation Risk Management Considerations

1

Why Have Purchase Price Adjustments?

• Means to ensure the value of the target

• Protection against fluctuations in the value of the target during the period that the target was initially valued and closing

• Minimum level of operating capital

• Means to give the Buyer comfort that the target will conduct business in the ordinary course

• Other options:

– Indemnification

– Walk-away / termination provisions

2

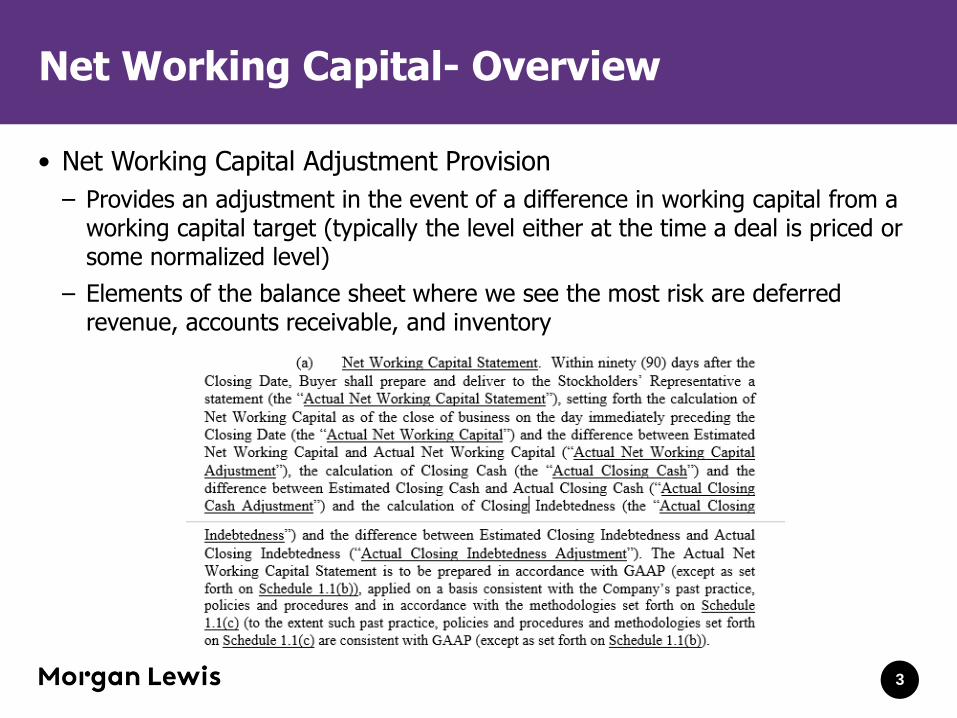

Net Working Capital- Overview

• Net Working Capital Adjustment Provision

– Provides an adjustment in the event of a difference in working capital from a working capital target (typically the level either at the time a deal is priced or some normalized level)

– Elements of the balance sheet where we see the most risk are deferred revenue, accounts receivable, and inventory

3

Net Working Capital Drafting Tips

• Confer with finance and accounting to understand the Company’s past practices and historic positions taken under GAAP

• Specify methodologies for calculations

– Draft with the Company’s balance sheet handy

– Provide illustrations and examples

• Think through the post-closing process

– Consider threshold triggering amounts to avoid disputes over small amounts

– Scope of information exchanges

– Realism about post-closing timeline

4

Net Working Capital– Positioning for Best Possible Litigation Outcome

• An ounce of prevention is worth a pound of cure

• The best litigation outcome is to avoid a dispute entirely

• Precise, contextualized drafting of the agreement will reduce the risk of disputes arising post-closing

• Expressly address impact of Company’s past practices

– Is Buyer and/or arbitrator/referee bound by Seller’s past practices irrespective of appropriateness under GAAP?

– What is implication of pre-closing or benchmark Working Capital example/calculation/target?

5

Net Working Capital– Positioning for Best Possible Litigation Outcome

• Dispute resolution clauses/Arbitration

• Expressly address scope of arbitrator's/referee’s review and authority

– Lawyer . . . or accountant?

• Expressly address scope of review/standard governing Buyer’s document/information production obligations

• Expressly address mechanics of dispute-resolution process

– Written submissions, site/inventory inspections, witness interviews/depositions, evidentiary hearings?

– Timing from start to conclusion?

– Reasoned determination or simple issuance of final binding calculation?

6

Net Working Capital– Positioning for Best Possible Litigation Outcome

• Expressly consider (and address, if desired) dispute resolution risk allocation

– Payment of arbitrator’s/referee’s fees

– Allocation based on success?

– Calculation methodology?

– Prevailing party’s attorney fees/expert-accountant fees

– Encourage reasonableness; resolve de minimis disputes

– Focus on large disputed issues

• Expressly address interest on final working capital amount

– Calculation rate, timing, disputed vs. “undisputed” amounts

7

CLE

DRCJ523Please save this number; you will need this to receive a Certificate of Attendance. You will be contacted within 30-60 days by our CLE administrative team. We will process your credits for other states where this program has been approved.

Please email Chris Chang at [email protected] if you have any questions.

8

Earn-Out Provisions

• Often used to:– Bridge valuation gap

– Motivate Seller to perform in future

– Help early stage companies for which value is better represented by future, not past, performance

• Benefits for Buyer– Reduce initial purchase consideration

– Minimize risk of overpaying

– Incentivize Seller to support business post-closing

• Benefits for Seller– Leverage post-closing synergies and opportunities to increase ultimate purchase

price

– Defer taxes – but beware of employment-related contingencies

• According to the ABA, nearly one-third of private company deals use earn-outs

9

Earn-Out Provisions

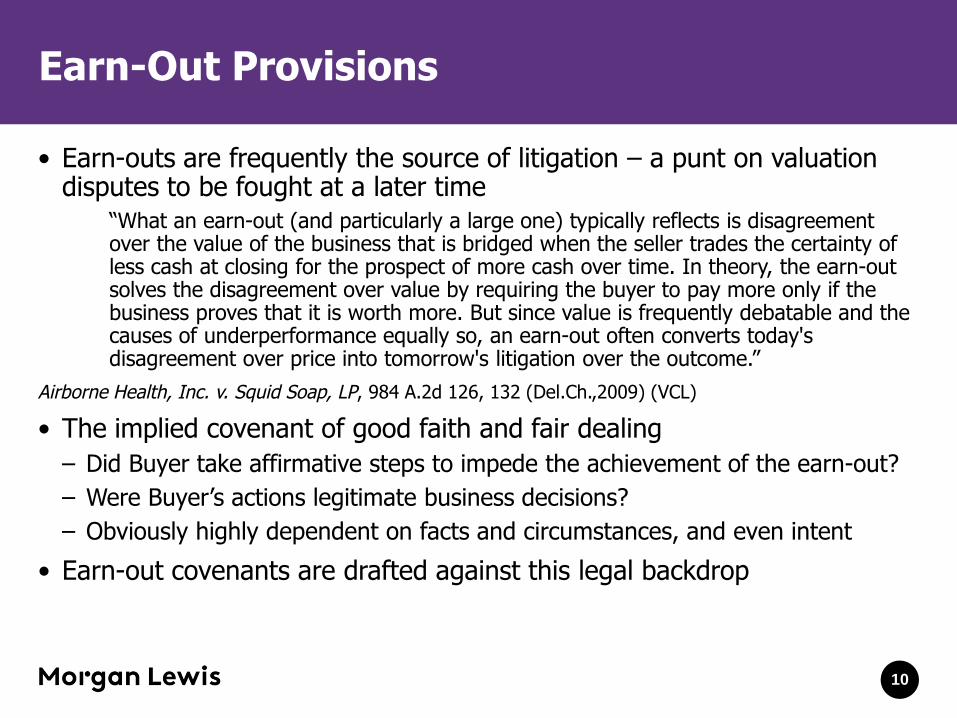

• Earn-outs are frequently the source of litigation – a punt on valuation disputes to be fought at a later time

“What an earn-out (and particularly a large one) typically reflects is disagreement over the value of the business that is bridged when the seller trades the certainty of less cash at closing for the prospect of more cash over time. In theory, the earn-out solves the disagreement over value by requiring the buyer to pay more only if the business proves that it is worth more. But since value is frequently debatable and the causes of underperformance equally so, an earn-out often converts today's disagreement over price into tomorrow's litigation over the outcome.”

Airborne Health, Inc. v. Squid Soap, LP, 984 A.2d 126, 132 (Del.Ch.,2009) (VCL)

• The implied covenant of good faith and fair dealing

– Did Buyer take affirmative steps to impede the achievement of the earn-out?

– Were Buyer’s actions legitimate business decisions?

– Obviously highly dependent on facts and circumstances, and even intent

• Earn-out covenants are drafted against this legal backdrop

10

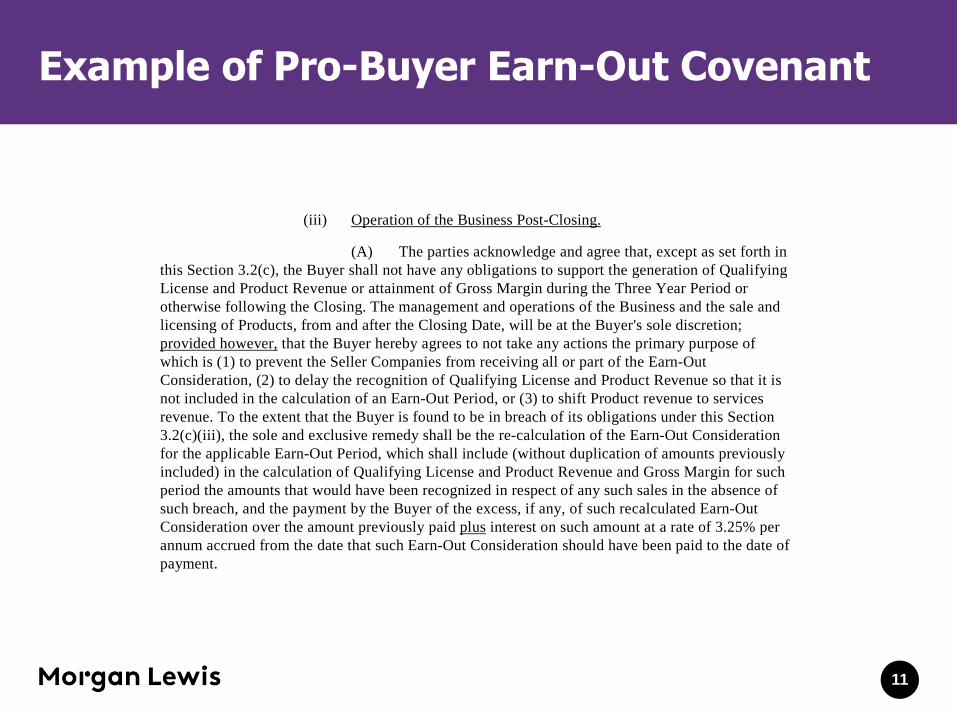

Example of Pro-Buyer Earn-Out Covenant

11

(iii) Operation of the Business Post-Closing.

(A) The parties acknowledge and agree that, except as set forth in this Section 3.2(c), the Buyer shall not have any obligations to support the generation of Qualifying License and Product Revenue or attainment of Gross Margin during the Three Year Period or otherwise following the Closing. The management and operations of the Business and the sale and licensing of Products, from and after the Closing Date, will be at the Buyer's sole discretion; provided however, that the Buyer hereby agrees to not take any actions the primary purpose of which is (1) to prevent the Seller Companies from receiving all or part of the Earn-Out Consideration, (2) to delay the recognition of Qualifying License and Product Revenue so that it is not included in the calculation of an Earn-Out Period, or (3) to shift Product revenue to services revenue. To the extent that the Buyer is found to be in breach of its obligations under this Section 3.2(c)(iii), the sole and exclusive remedy shall be the re-calculation of the Earn-Out Consideration for the applicable Earn-Out Period, which shall include (without duplication of amounts previously included) in the calculation of Qualifying License and Product Revenue and Gross Margin for such period the amounts that would have been recognized in respect of any such sales in the absence of such breach, and the payment by the Buyer of the excess, if any, of such recalculated Earn-Out Consideration over the amount previously paid plus interest on such amount at a rate of 3.25% per annum accrued from the date that such Earn-Out Consideration should have been paid to the date of payment.

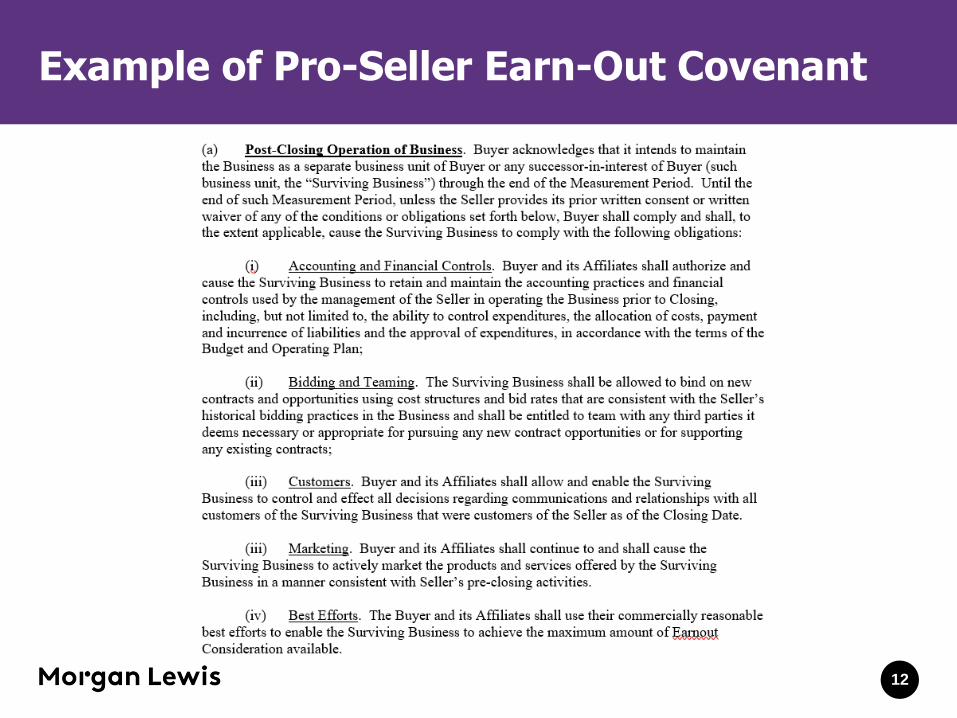

Example of Pro-Seller Earn-Out Covenant

12

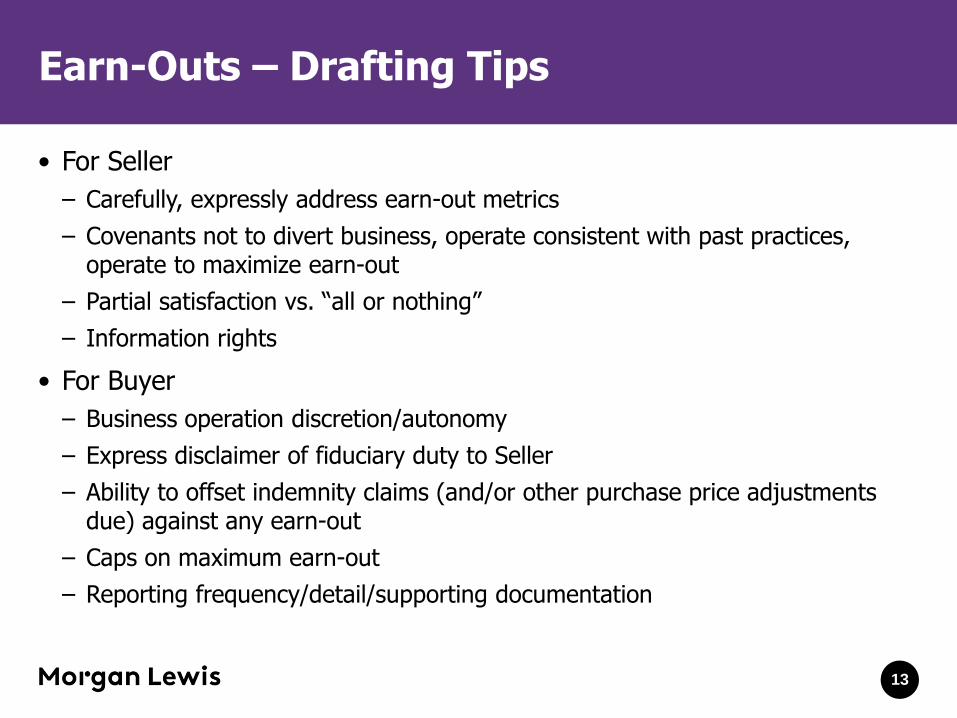

Earn-Outs – Drafting Tips

• For Seller

– Carefully, expressly address earn-out metrics

– Covenants not to divert business, operate consistent with past practices, operate to maximize earn-out

– Partial satisfaction vs. “all or nothing”

– Information rights

• For Buyer

– Business operation discretion/autonomy

– Express disclaimer of fiduciary duty to Seller

– Ability to offset indemnity claims (and/or other purchase price adjustments due) against any earn-out

– Caps on maximum earn-out

– Reporting frequency/detail/supporting documentation

13

Earn-Outs – Positioning for Best Possible Litigated Outcome

• Plan on litigation, beginning at the drafting stage and through performance of the earn-out

• Alternative dispute resolution

– Many of the same considerations as with working capital disputes

• Documenting performance of the earn-out

– Creating the record that demonstrates a breach of the implied covenant (representing Seller) or mere exercise of business judgment (representing Buyer)

• The role of experts

14

Biographies

Karen Abesamis

Partner

Silicon Valley

T +650.843.7277

karen.abesamis@ morganlewis.com

Michael Blanchard

Partner

Boston

T +860.240.2945

michael.blanchard@ morganlewis.com

Karen Abesamis focuses her practice on mergers and acquisitions, private equity, venture capital, securities, and general corporate matters. Karen represents clients that include public and private companies, financial institutions, and venture capital and corporate investors. Karen advises on a variety of transactions, including cross-border and domestic acquisitions, venture capital investments, and capital raises by private and public companies.

15

Michael Blanchard represents clients in all facets of shareholder litigation, class actions, securities enforcement matters, investigations, and business disputes. Michael has obtained numerous dismissals at the pleading stage, including, for example, the dismissal of a 1933 Act class action which Forbes magazine called a “stunning class action victory.” Where dismissal is not achievable, Michael has successfully tried cases to judges and juries alike, and successfully litigated numerous appeals. Michael also counsels clients on litigation avoidance strategies, and is member of Morgan Lewis’s crisis management practice.

Almaty

Astana

Beijing*

Boston

Brussels

Chicago

Dallas

Dubai

Frankfurt

Hartford

Hong Kong*

Houston

London

Los Angeles

Miami

Moscow

New York

Orange County

Paris

Philadelphia

Pittsburgh

Princeton

San Francisco

Santa Monica

Shanghai*

Silicon Valley

Singapore

Tokyo

Washington, DC

Wilmington

*Our Beijing office operates as a representative office of Morgan, Lewis & Bockius LLP. In Shanghai, we operate as a branch of Morgan Lewis Consulting (Beijing) Company Limited, and an application to establish a representative office of the firm is pending before the Ministry of Justice. In Hong Kong, Morgan Lewis has filed an application to become a registered foreign law firm and is seeking approval with The Law Society of Hong Kong to associate with Luk & Partners.

Africa

Asia Pacific

Europe

Latin America

Middle East

North America

Our Global Reach Our Locations

© 2017 Morgan, Lewis & Bockius LLP© 2017 Morgan Lewis Stamford LLC© 2017 Morgan, Lewis & Bockius UK LLP

Morgan, Lewis & Bockius UK LLP is a limited liability partnership registered in England and Wales under number OC378797 and is a law firm authorised and regulated by the Solicitors Regulation Authority. The SRA authorisation number is 615176.

*Our Beijing office operates as a representative office of Morgan, Lewis & Bockius LLP. In Shanghai, we operate as a branch of Morgan Lewis Consulting (Beijing) Company Limited, and an application to establish a representative office of the firm is pending before the Ministry of Justice. In Hong Kong, Morgan Lewis has filed an application to become a registered foreign law firm and is seeking approval with The Law Society of Hong Kong to associate with Luk & Partners.This material is provided for your convenience and does not constitute legal advice or create an attorney-client relationship. Prior results do not guarantee similar outcomes. Attorney Advertising.

17