baltic countries overview

DESCRIPTION

Baltic countries overviewTRANSCRIPT

Confidential and Proprietary Copyright © 2010 The Nielsen Company

1

May, 2010

Baltic Countries’ Overview

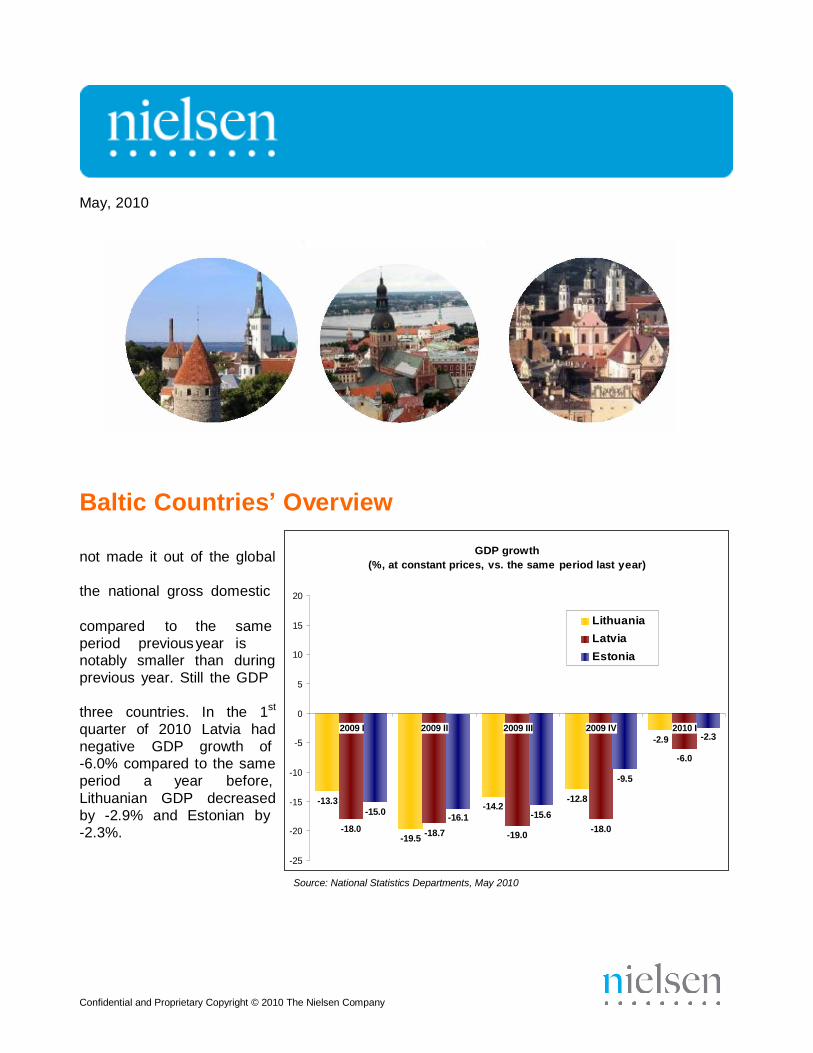

not made it out of the global

the national gross domestic

compared to the same

period previous year is notably smaller than during

previous year. Still the GDP

three countries. In the 1st

quarter of 2010 Latvia had

negative GDP growth of -6.0% compared to the same

period a year before,

Lithuanian GDP decreased

by -2.9% and Estonian by

20

15

10

5

0

-5

-10

-15

-13.3

GDP growth

(%, at constant prices, vs. the same period last year)

Lithuania

Latvia

Estonia

2009 I 2009 II 2009 III 2009 IV 2010 I

-2.9

-6.0

-9.5

-12.8

-15.0 -14.2

-16.1 -15.6

-2.3

-2.3%. -20 -18.0 -19.5

-18.7 -19.0 -18.0

-25

Source: National Statistics Departments, May 2010

Confidential and Proprietary Copyright © 2010 The Nielsen Company

2

-3%

Latv

ia

Lithuania

Esto

nia

Hungary

Czech

Rep.

Irela

nd

Fin

land

Gre

ece

Port

ugal

Sw

itzerland

Neth

erlands

Italy

Slo

vakia

Denm

ark

Spain

Germ

any

Austr

ia

Belg

ium

Fra

nce

UK

Pola

nd

Sw

eden

Norw

ay

Turk

ey

Q1 2010 growth rates per country (versus Q1 2009)

20%

1% 1% 1% 2% 2% 2% 2% 2% 3%

9%

4% 5% 7%

21%

3% -25%% -1% -14%%% 02%% 1%

1% 4%

1% 3% 1% 3% 2% 1% 1% 2% 4%

2% 1% 2% 1% 2%

-0.8% 0% 0% -01%

-3%

0% -32% 1%

-2% 0% -1% 1% -1%

-3.8% -5.4% -3% -3% -6-2%% -7% -4%

-11.0% -4.1%

-12.3%

-4% -3%

-9.5% -11.8%

-16.2%

Unit value change Volume growth Value Growth

Source: Nielsen Growth Reporter, May, maitinimo kedutes

The estimated nominal value growth for total Europe was +4.1% for the 1st quarter of 2010

compared to the same quarter of 2009. The estimated nominal value growth in the FMCG sector

was still negative for all Baltic countries, in Latvia -16.2%, Lithuania -11.8% and the lowest in Estonia -9.5% in the 1st quarter of 2010.

The estimated volume change for Latvia was -12.3%, followed by -11.0% in Lithuania and -4.1%

in Estonia in the 1st quarter of 2010. The volume change in total Europe was +1.3% in 1st quarter

of 2010 compared to same period last year. Volume change for the 4th quarter of 2009 was 1.6%.

In the first half of 2010 the consumer confidence index decreased in Estonia reaching 62 points

(66 in the 2nd half of 2009) and in Lithuania to 46 points (54 points in the 2nd half of 2009). In

Latvia the index grew to 53 points from 49 in the 2nd

half of 2009. The index is based on responses to three questions regarding perceptions of local job prospects, personal finances and whether or not it’s a good time to buy things that people need and want, all over a timeframe of

the next 12 months. For Europe the average consumer confidence index in the 1st half of 2010

was 78 (76 in the 2nd half of 2009). The global average consumer confidence index for the 1st

quarter in 2010 was 92 points which has increased constantly from its lowest point of 77 in the 1st

quarter of 2009.

95% of Latvians and 93% of Lithuanians believe that their country is in recession. 87% of

Estonians also thinks so. All Baltic nations are rather pessimistic about the recession ending

during the next year. 15% of Estonians and 13% of Lithuanians who said that their country is

currently in recession believe that it will be out of the recession in the next 12 months. Just 7% of

Latvians, who answered that their country is in recession, feel the same way.

Confidential and Proprietary Copyright © 2010 The Nielsen Company

3

Lithuania

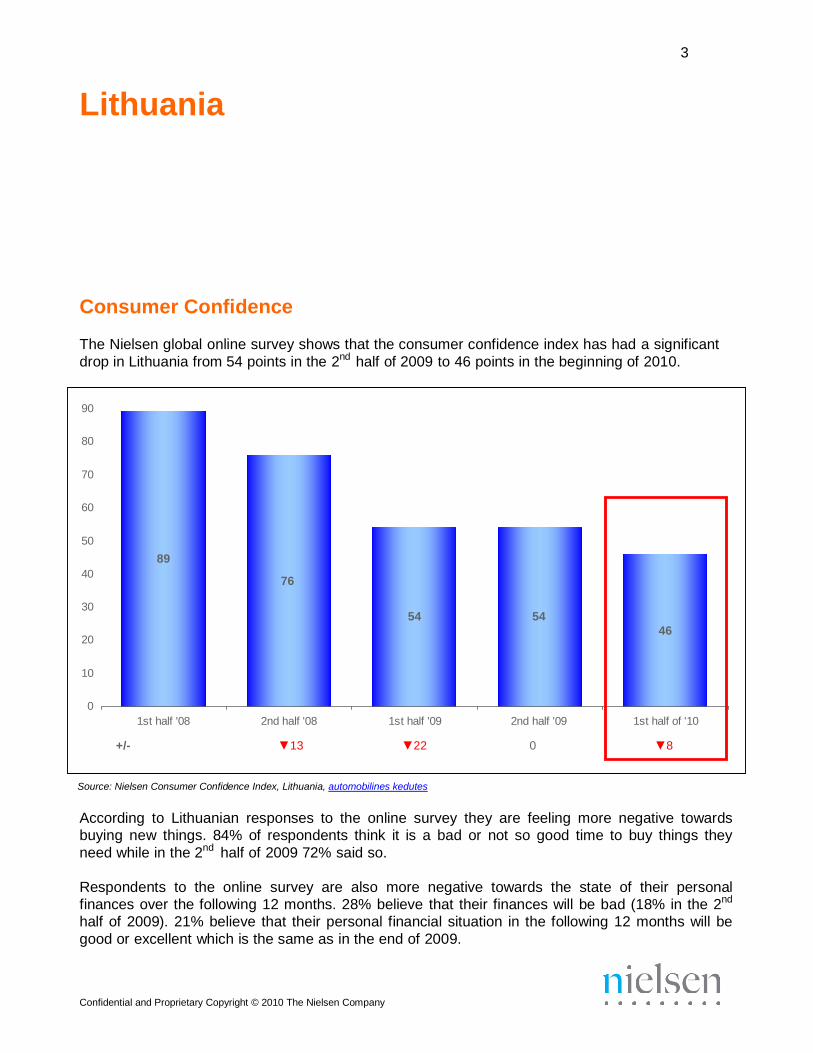

Consumer Confidence

The Nielsen global online survey shows that the consumer confidence index has had a significant

drop in Lithuania from 54 points in the 2nd half of 2009 to 46 points in the beginning of 2010.

90

80

70

60

50

89

40 76

30 54 54

46 20

10

0

1st half '08 2nd half '08 1st half '09 2nd half '09 1st half of '10

+/- ▼13 ▼22 0 ▼8

Source: Nielsen Consumer Confidence Index, Lithuania, automobilines kedutes

According to Lithuanian responses to the online survey they are feeling more negative towards

buying new things. 84% of respondents think it is a bad or not so good time to buy things they

need while in the 2nd half of 2009 72% said so.

Respondents to the online survey are also more negative towards the state of their personal

finances over the following 12 months. 28% believe that their finances will be bad (18% in the 2nd

half of 2009). 21% believe that their personal financial situation in the following 12 months will be

good or excellent which is the same as in the end of 2009.

4

Confidential and Proprietary Copyright © 2010 The Nielsen Company

Lithuanians’ perception of the local job market has slightly improved, but is still very negative in

the 1st

half of 2010 as 93% of respondents think that the prospects of a local job are either bad or

not so good in the following 12 months (in the 2nd

half of 2009 97% said the same). Just 4% think

that their prospects are good.

In the 1st

half of 2010, 93% of respondents think that Lithuania is currently in recession.

Nevertheless, the existence of recession in their country hit Lithuanians later than both Estonians

and Latvians. In the 2nd half of 2008 86% thought the country was in economic recession, while in

Estonia and Latvia 93% of respondents said the same in the corresponding period. The highest

number of Lithuanian respondents believed that the country is in economic recession in the 1st

half of 2009 when 98% of respondents said so, in Estonia and Latvia also the highest number of

people believed that their country is in recession during that period.

At the moment, 13% of respondents who said that Lithuania is currently in recession believe that

the recession will be over in the next 12 months. In the 2nd

half of 2009 11% believe it and in the 1st half of 2009 just 7% said so. Compared to other Baltic countries just 7% of Latvians believe

that their recession will be over in the next 12 months, but 15% of Estonians are that optimistic and think that Estonian economy will recover during the year.

5

Confidential and Proprietary Copyright © 2010 The Nielsen Company

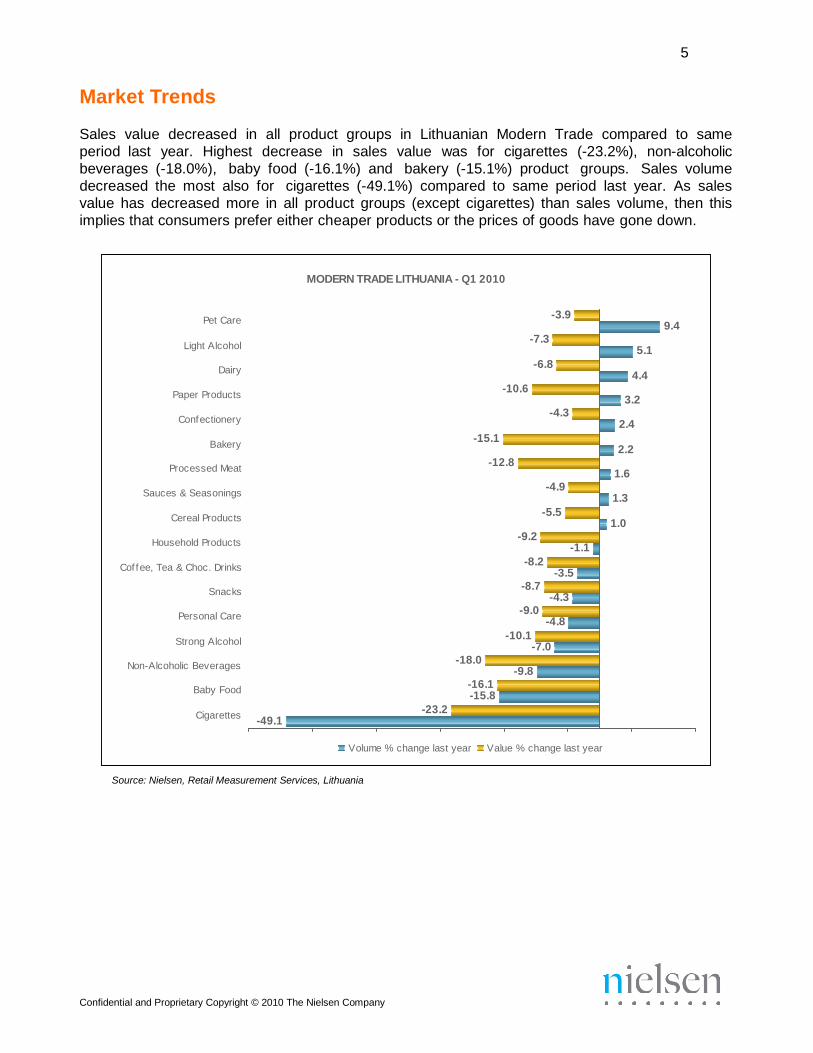

Market Trends Sales value decreased in all product groups in Lithuanian Modern Trade compared to same

period last year. Highest decrease in sales value was for cigarettes (-23.2%), non-alcoholic

beverages (-18.0%), baby food (-16.1%) and bakery (-15.1%) product groups. Sales volume

decreased the most also for cigarettes (-49.1%) compared to same period last year. As sales

value has decreased more in all product groups (except cigarettes) than sales volume, then this

implies that consumers prefer either cheaper products or the prices of goods have gone down.

MODERN TRADE LITHUANIA - Q1 2010

Pet Care

Light Alcohol

-7.3

-3.9

5.1

9.4

Dairy

Paper Products

Conf ectionery

Bakery

-15.1

-10.6

-6.8

-4.3

4.4

3.2 2.4 2.2

Processed Meat

Sauces & Seasonings

Cereal Products

Household Products

-12.8 -9.2

-4.9

-5.5

-1.1

1.6 1.3 1.0

Cof f ee, Tea & Choc. Drinks

Snacks

Personal Care

-8.2

-8.7

-9.0 -10.1

-3.5

-4.3

-4.8

Strong Alcohol

Non-Alcoholic Beverages

Baby Food

Cigarettes

-49.1

-23.2

-18.0

-16.1 -15.8

-7.0

-9.8

Volume % change last year Value % change last year

Source: Nielsen, Retail Measurement Services, Lithuania

6

Confidential and Proprietary Copyright © 2010 The Nielsen Company

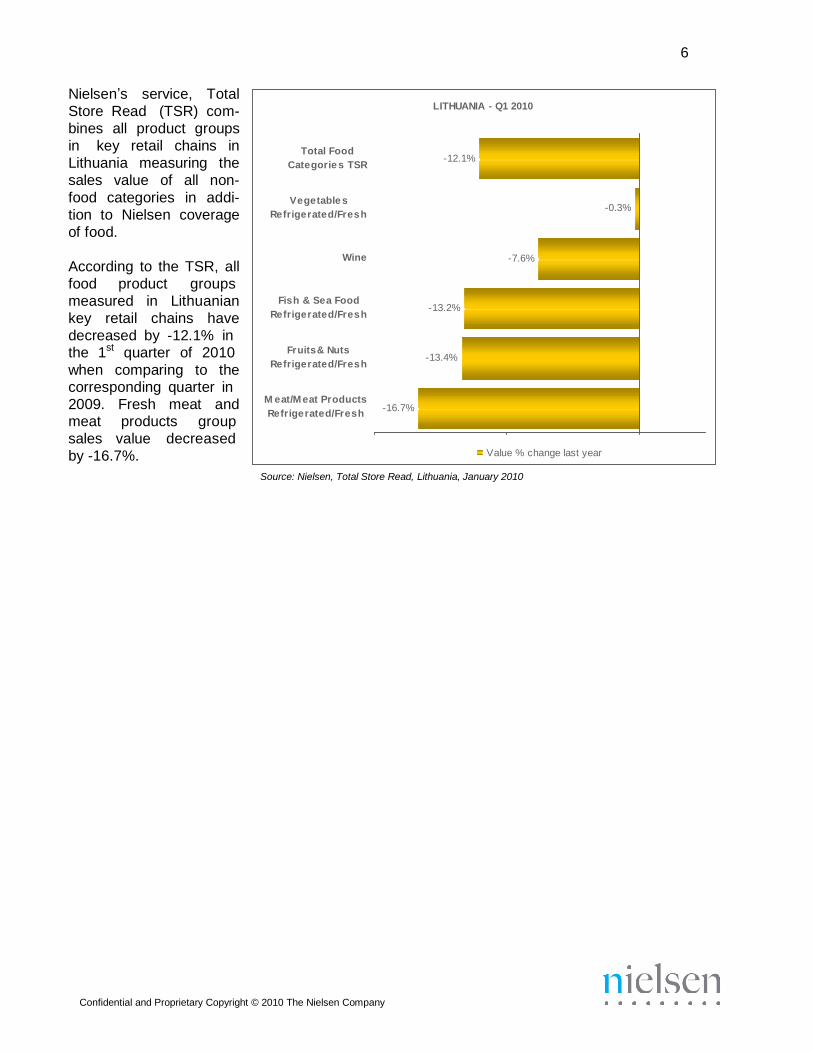

Nielsen’s service, Total

Store Read (TSR) com-

bines all product groups

in key retail chains in

Lithuania measuring the

sales value of all non-

food categories in addi-

tion to Nielsen coverage

of food.

Total Food

Cate gorie s TSR

Ve ge table s

Re frige r ate d/Fr e s h

LITHUANIA - Q1 2010

-12.1%

-0.3%

According to the TSR, all

food product groups

measured in Lithuanian

key retail chains have

decreased by -12.1% in the 1st quarter of 2010

when comparing to the corresponding quarter in

2009. Fresh meat and meat products group

sales value decreased

by -16.7%.

Wine

Fis h & Se a Food

Re frige r ate d/Fr e s h

Fr uits & Nuts

Re frige r ate d/Fr e s h

M e at/M e at Products

Re fr ige rate d/Fre s h

-16.7%

-13.2% -13.4%

-7.6%

Value % change last year

Source: Nielsen, Total Store Read, Lithuania, January 2010

7

Confidential and Proprietary Copyright © 2010 The Nielsen Company

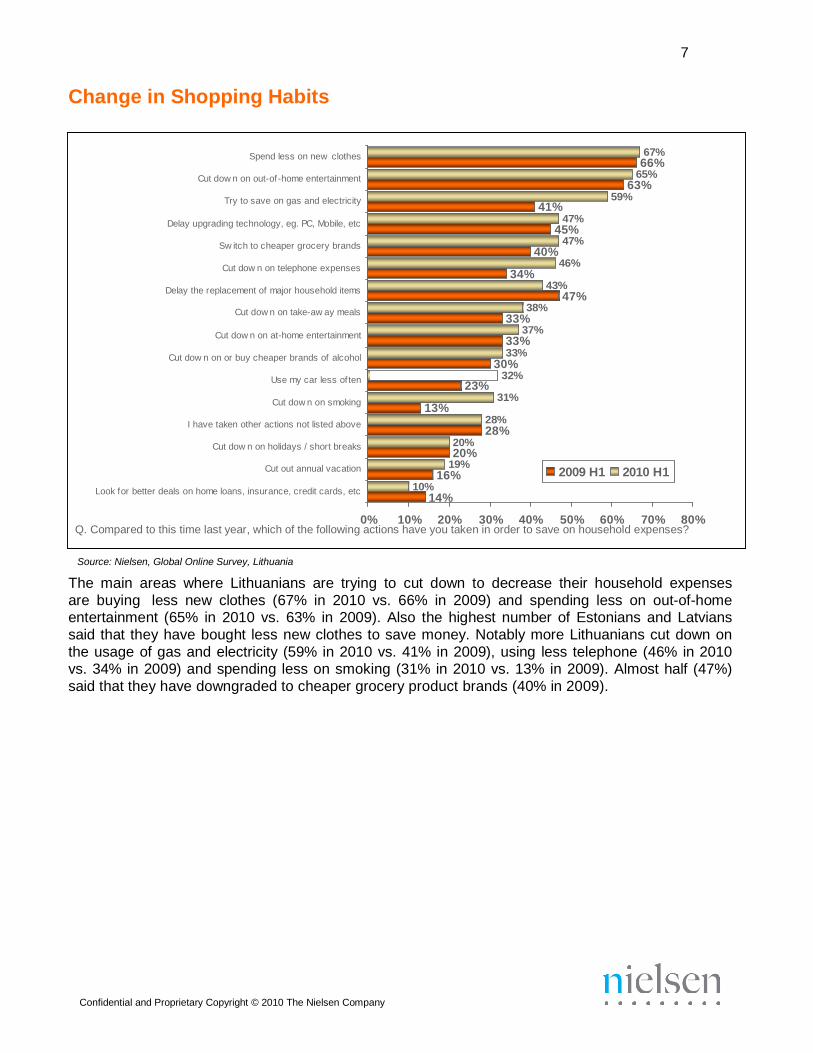

Change in Shopping Habits

Spend less on new clothes

Cut dow n on out-of -home entertainment

Try to save on gas and electricity

Delay upgrading technology, eg. PC, Mobile, etc

Sw itch to cheaper grocery brands

Cut dow n on telephone expenses

Delay the replacement of major household items

41%

47% 45%

47% 40%

46% 34%

43% 47%

67% 66%

65% 63%

59%

Cut dow n on take-aw ay meals

Cut dow n on at-home entertainment

Cut dow n on or buy cheaper brands of alcohol

Use my car less of ten

Cut dow n on smoking

13%

23%

38% 33%

37% 33% 33%

30% 32%

31%

I have taken other actions not listed above

Cut dow n on holidays / short breaks

Cut out annual vacation

Look f or better deals on home loans, insurance, credit cards, etc

10%

20% 20%

19% 16%

28% 28%

2009 H1 2010 H1

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% Q. Compared to this time last year, which of the following actions have you taken in order to save on household expenses?

Source: Nielsen, Global Online Survey, Lithuania

The main areas where Lithuanians are trying to cut down to decrease their household expenses

are buying less new clothes (67% in 2010 vs. 66% in 2009) and spending less on out-of-home entertainment (65% in 2010 vs. 63% in 2009). Also the highest number of Estonians and Latvians

said that they have bought less new clothes to save money. Notably more Lithuanians cut down on

the usage of gas and electricity (59% in 2010 vs. 41% in 2009), using less telephone (46% in 2010 vs. 34% in 2009) and spending less on smoking (31% in 2010 vs. 13% in 2009). Almost half (47%)

said that they have downgraded to cheaper grocery product brands (40% in 2009).

8

Confidential and Proprietary Copyright © 2010 The Nielsen Company

Vo

lum

e %

CH

G L

Y

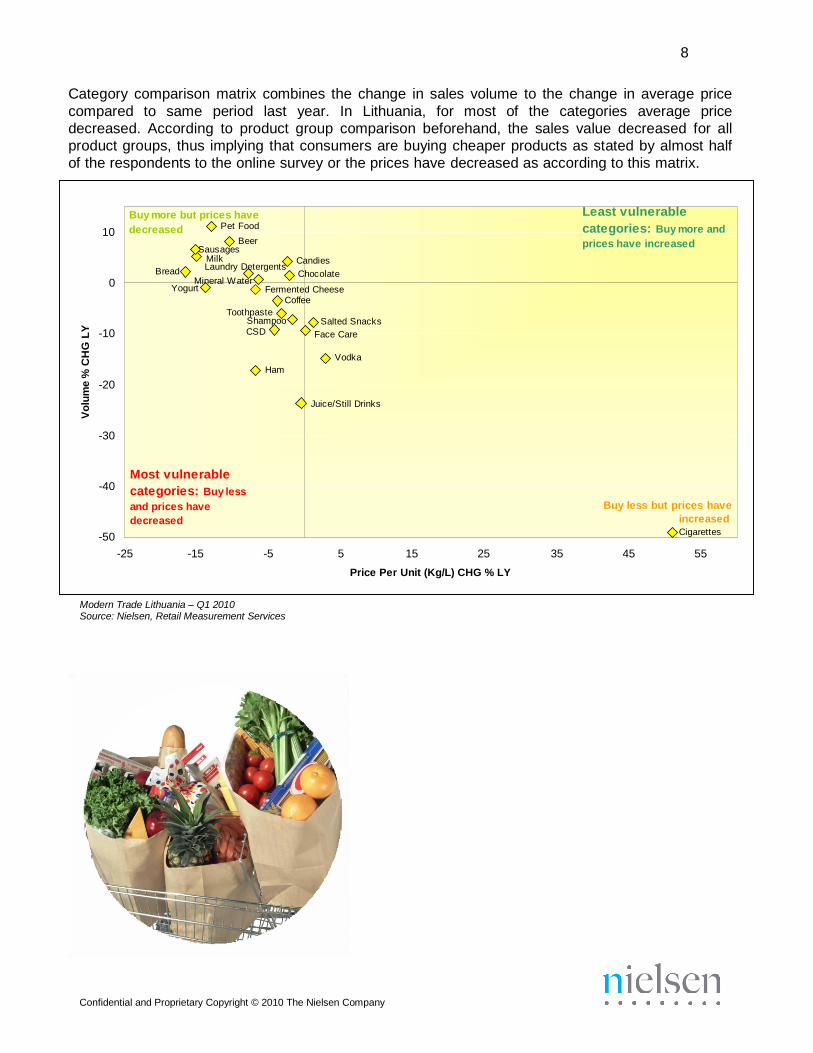

Category comparison matrix combines the change in sales volume to the change in average price

compared to same period last year. In Lithuania, for most of the categories average price

decreased. According to product group comparison beforehand, the sales value decreased for all

product groups, thus implying that consumers are buying cheaper products as stated by almost half

of the respondents to the online survey or the prices have decreased as according to this matrix.

Buy more but prices have Least vulnerable

10 decreased Pet Food

Beer Sausages

Milk Laundry Detergents

Candies

categories: Buy more and

prices have increased

Bread Chocolate

0 Mineral Water Yogurt Fermented Cheese

Coffee

Toothpaste Shampoo Salted Snacks

-10 CSD Face Care

-20

Ham

Vodka

Juice/Still Drinks

-30

-40

-50

Most vulnerable

categories: Buy less

and prices have

decreased

Buy less but prices have

increased

Cigarettes

-25 -15 -5 5 15 25 35 45 55

Price Per Unit (Kg/L) CHG % LY

Modern Trade Lithuania – Q1 2010 Source: Nielsen, Retail Measurement Services

9

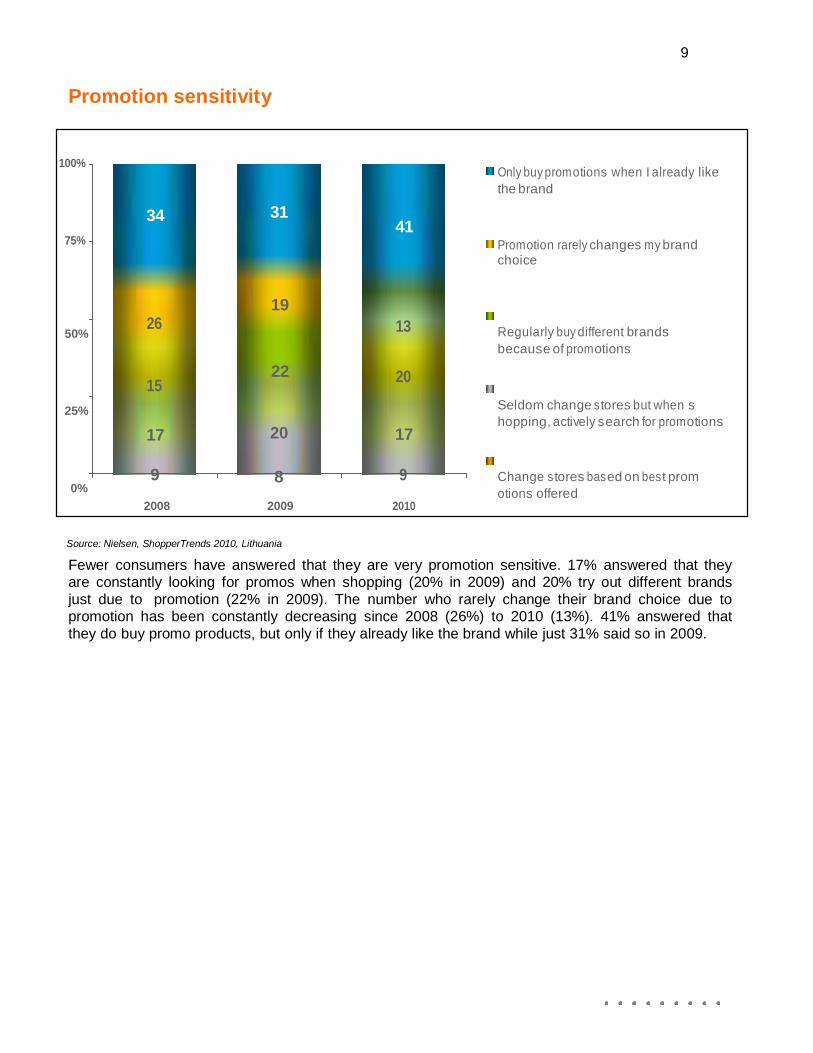

Promotion sensitivity

100%

75%

34 31

Only buy prom otions when I already like

the brand

41

Prom otion rarely changes m y brand choice

26

50%

15

25%

19

13

22 20

Regularly buy different brands

because of prom otions

Seldom change s tores but when s

hopping, actively search for prom otions 17 20 17

9 8 9

0%

2008 2009 2010

Change s tores bas ed on bes t prom

otions offered

Source: Nielsen, ShopperTrends 2010, Lithuania

Fewer consumers have answered that they are very promotion sensitive. 17% answered that they are constantly looking for promos when shopping (20% in 2009) and 20% try out different brands

just due to promotion (22% in 2009). The number who rarely change their brand choice due to promotion has been constantly decreasing since 2008 (26%) to 2010 (13%). 41% answered that

they do buy promo products, but only if they already like the brand while just 31% said so in 2009.

10

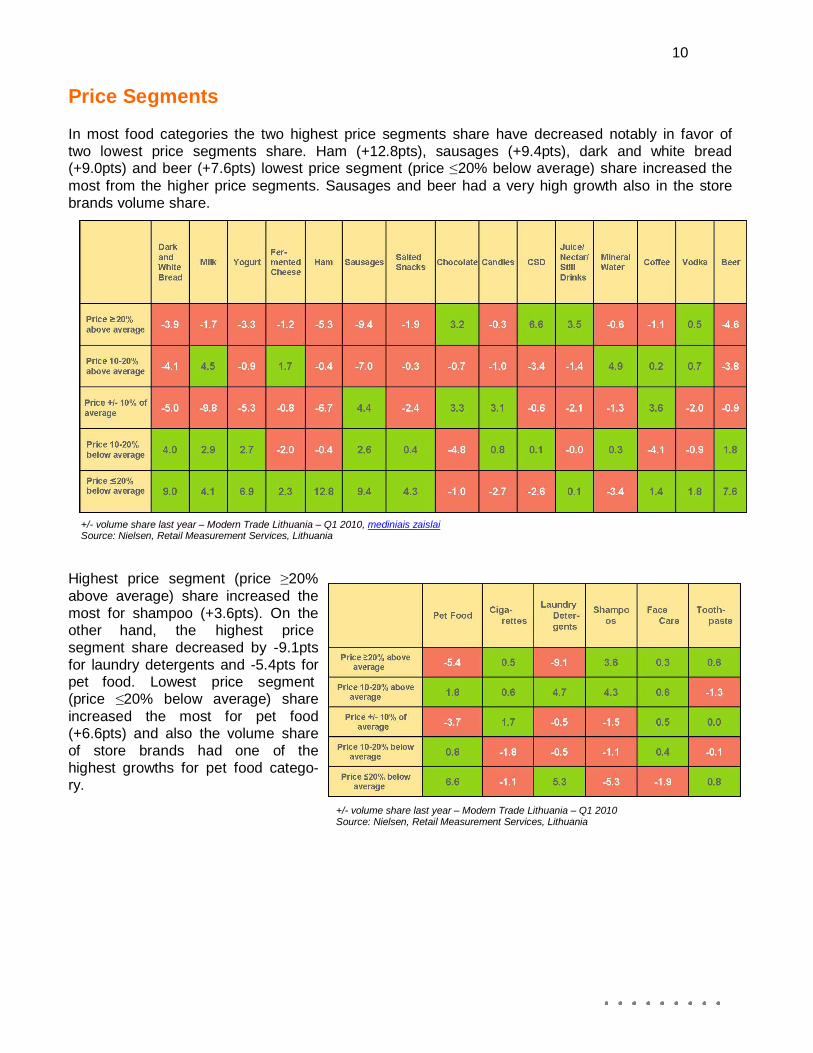

Price Segments In most food categories the two highest price segments share have decreased notably in favor of

two lowest price segments share. Ham (+12.8pts), sausages (+9.4pts), dark and white bread (+9.0pts) and beer (+7.6pts) lowest price segment (price ≤20% below average) share increased the

most from the higher price segments. Sausages and beer had a very high growth also in the store

brands volume share.

+/- volume share last year – Modern Trade Lithuania – Q1 2010, mediniais zaislai Source: Nielsen, Retail Measurement Services, Lithuania

Highest price segment (price ≥20%

above average) share increased the

most for shampoo (+3.6pts). On the other hand, the highest price

segment share decreased by -9.1pts

for laundry detergents and -5.4pts for pet food. Lowest price segment (price ≤20% below average) share

increased the most for pet food (+6.6pts) and also the volume share

of store brands had one of the

highest growths for pet food catego- ry.

+/- volume share last year – Modern Trade Lithuania – Q1 2010 Source: Nielsen, Retail Measurement Services, Lithuania

11

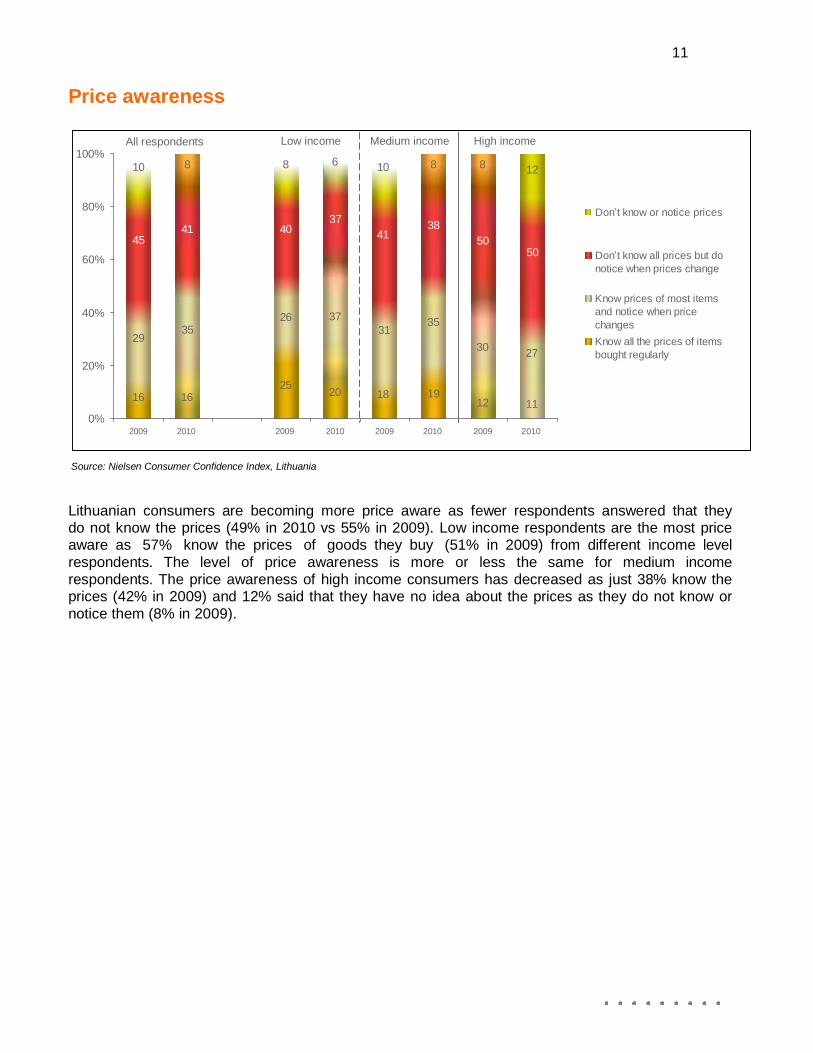

Price awareness

100% All respondents Low income Medium income High income

10 8 8 6 10 8 8 12

80%

45

60%

37

41 40 41

38

50 50

Don’t know or notice prices

Don’t know all prices but do

notice when prices change

40%

35 29

20%

26 37

31 35

30

27

Know prices of most items

and notice when price

changes

Know all the prices of items

bought regularly

16 16

0%

25 20 18 19

12 11

2009 2010 2009 2010 2009 2010 2009 2010

Source: Nielsen Consumer Confidence Index, Lithuania

Lithuanian consumers are becoming more price aware as fewer respondents answered that they do not know the prices (49% in 2010 vs 55% in 2009). Low income respondents are the most price aware as 57% know the prices of goods they buy (51% in 2009) from different income level

respondents. The level of price awareness is more or less the same for medium income

respondents. The price awareness of high income consumers has decreased as just 38% know the prices (42% in 2009) and 12% said that they have no idea about the prices as they do not know or

notice them (8% in 2009).

12

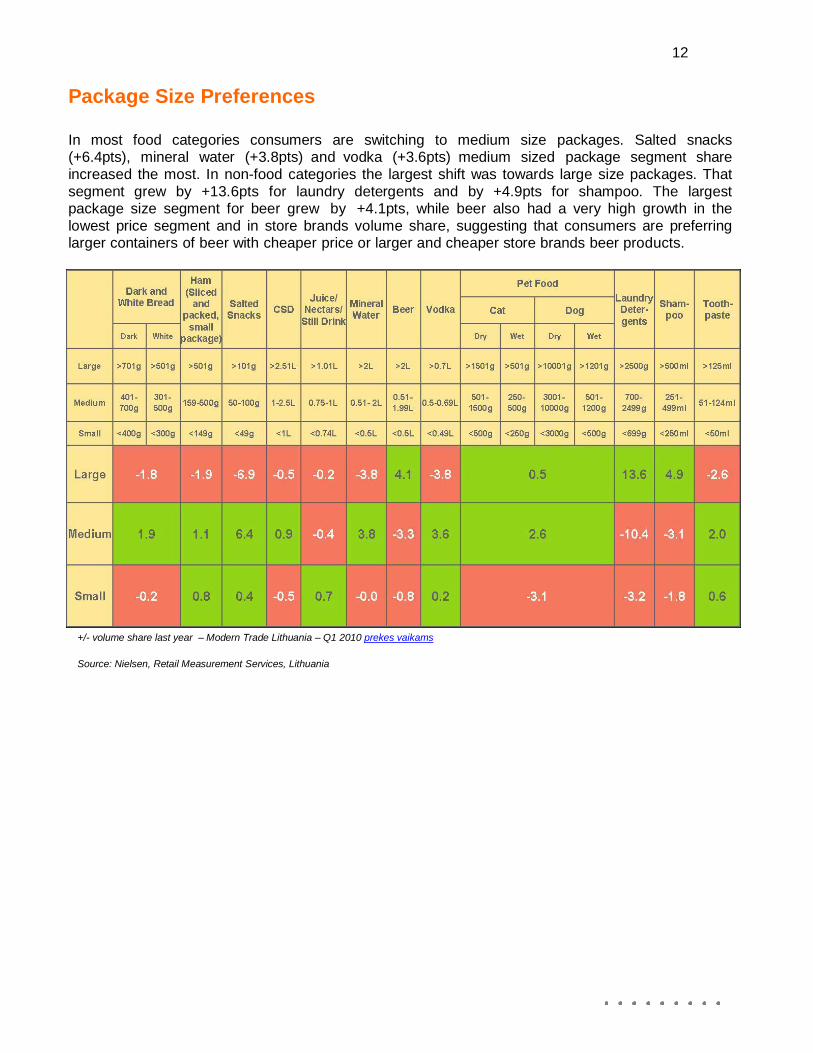

Package Size Preferences

In most food categories consumers are switching to medium size packages. Salted snacks (+6.4pts), mineral water (+3.8pts) and vodka (+3.6pts) medium sized package segment share

increased the most. In non-food categories the largest shift was towards large size packages. That

segment grew by +13.6pts for laundry detergents and by +4.9pts for shampoo. The largest package size segment for beer grew by +4.1pts, while beer also had a very high growth in the

lowest price segment and in store brands volume share, suggesting that consumers are preferring larger containers of beer with cheaper price or larger and cheaper store brands beer products.

+/- volume share last year – Modern Trade Lithuania – Q1 2010 prekes vaikams

Source: Nielsen, Retail Measurement Services, Lithuania

13

DA

RK

AN

D W

HIT

E

BR

EA

DS

MIL

K

FE

RM

EN

TE

D C

HE

ES

E

YO

GU

RT

HA

M

SA

US

AG

ES

SA

LT

ED

SN

AC

KS

CH

OC

OLA

TE

S

CA

ND

Y

CS

D

JU

I CE

/NE

CT

AR

S/ S

TIL

L

DR

INK

S

MIN

ER

AL W

AT

ER

CO

FF

EE

VO

DK

A

BE

ER

PE

T F

OO

D

CIG

AR

ET

TE

S

LA

UN

DR

Y

DE

TE

RG

EN

TS

SH

AM

PO

OS

FA

CE

CA

RE

TO

OT

HP

AS

TE

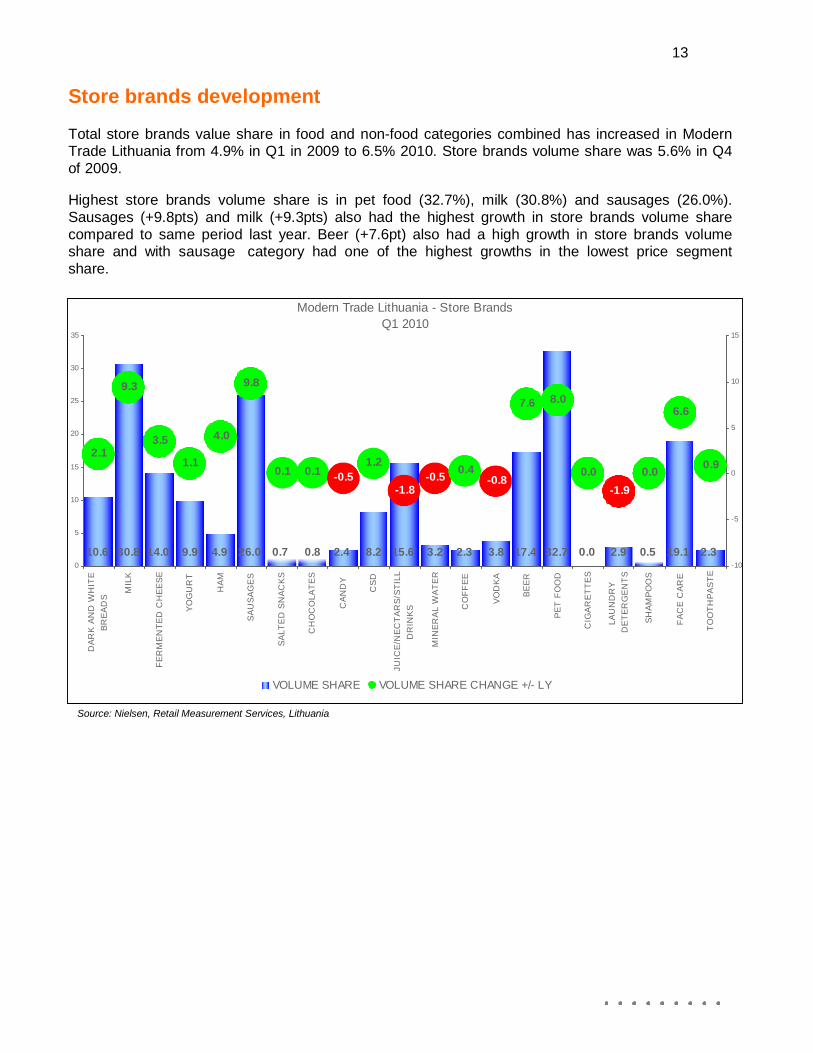

Store brands development Total store brands value share in food and non-food categories combined has increased in Modern Trade Lithuania from 4.9% in Q1 in 2009 to 6.5% 2010. Store brands volume share was 5.6% in Q4

of 2009.

Highest store brands volume share is in pet food (32.7%), milk (30.8%) and sausages (26.0%).

Sausages (+9.8pts) and milk (+9.3pts) also had the highest growth in store brands volume share

compared to same period last year. Beer (+7.6pt) also had a high growth in store brands volume share and with sausage category had one of the highest growths in the lowest price segment

share.

Modern Trade Lithuania - Store Brands

Q1 2010 35 15

30

25

20

2.1 15

10

9.3

3.5 4.0

1.1

9.8

0.1

0.1

1.2

-0.5 -0.5 0.4

-0.8 -1.8

7.6 8.0

0.0

-1.9

0.0

6.6

10

5

0.9

0

5

10.6 30.8 14.0 9.9 4.9 26.0 0.7 0.8 2.4 8.2 15.6 3.2 2.3 3.8 17.4 32.7 0.0 2.9 0.5 19.1 2.3 0

-5

-10

VOLUME SHARE VOLUME SHARE CHANGE +/- LY

Source: Nielsen, Retail Measurement Services, Lithuania

14

Confidential and Proprietary Copyright © 2010 The Nielsen Company

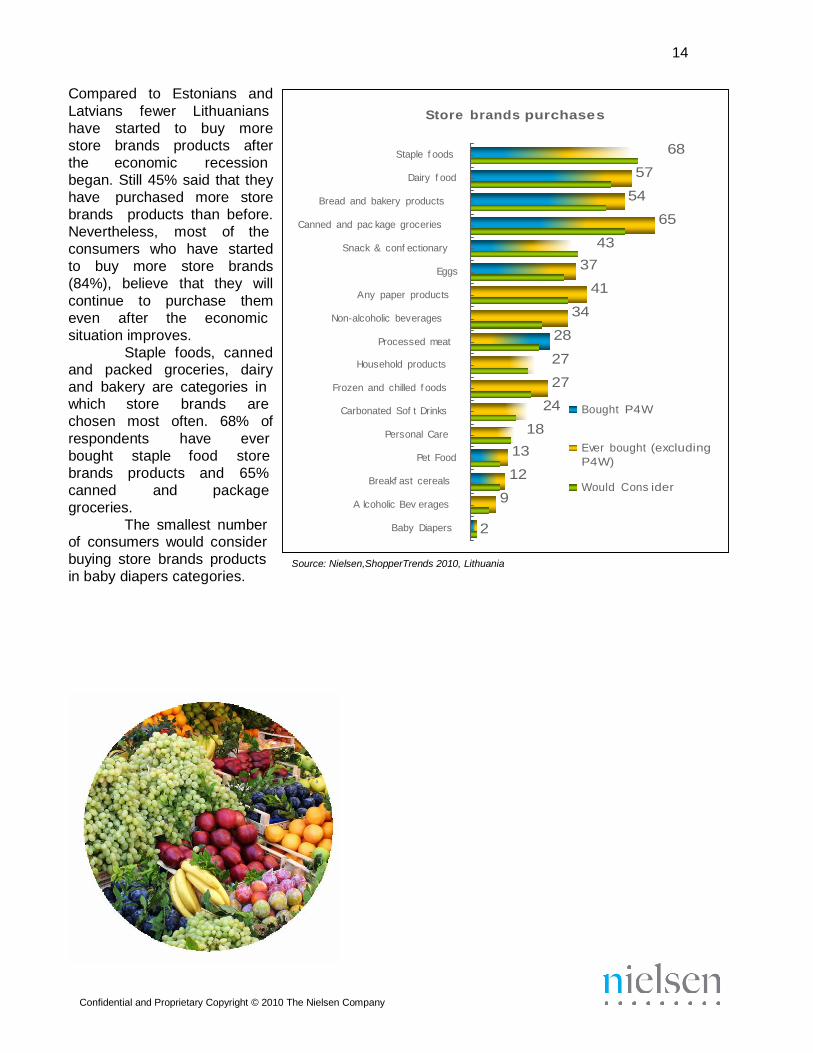

Compared to Estonians and

Latvians fewer Lithuanians

have started to buy more

store brands products after

the economic recession

began. Still 45% said that they

have purchased more store

brands products than before.

Nevertheless, most of the

consumers who have started

to buy more store brands

(84%), believe that they will

continue to purchase them

even after the economic

situation improves.

Staple foods, canned and packed groceries, dairy

and bakery are categories in

Store brands purchase s

Staple f oods 68

Dairy f ood 57

Bread and bakery products 54

Canned and pac kage groceries 65

Snack & conf ectionary 43

Eggs 37

Any paper products 41

Non-alcoholic beverages 34

Processed meat 28

Household products 27

Frozen and chilled f oods 27

which store brands are

chosen most often. 68% of

respondents have ever

bought staple food store

brands products and 65%

canned and package

groceries.

The smallest number of consumers would consider

Carbonated Sof t Drinks 24

Personal Care 18

Pet Food 13

Breakf ast cereals 12

A lcoholic Bev erages 9

Baby Diapers 2

Bought P4W Ever bought (excluding

P4W) Would Cons ider

buying store brands products

in baby diapers categories.

Source: Nielsen,ShopperTrends 2010, Lithuania

15

Confidential and Proprietary Copyright © 2010 The Nielsen Company

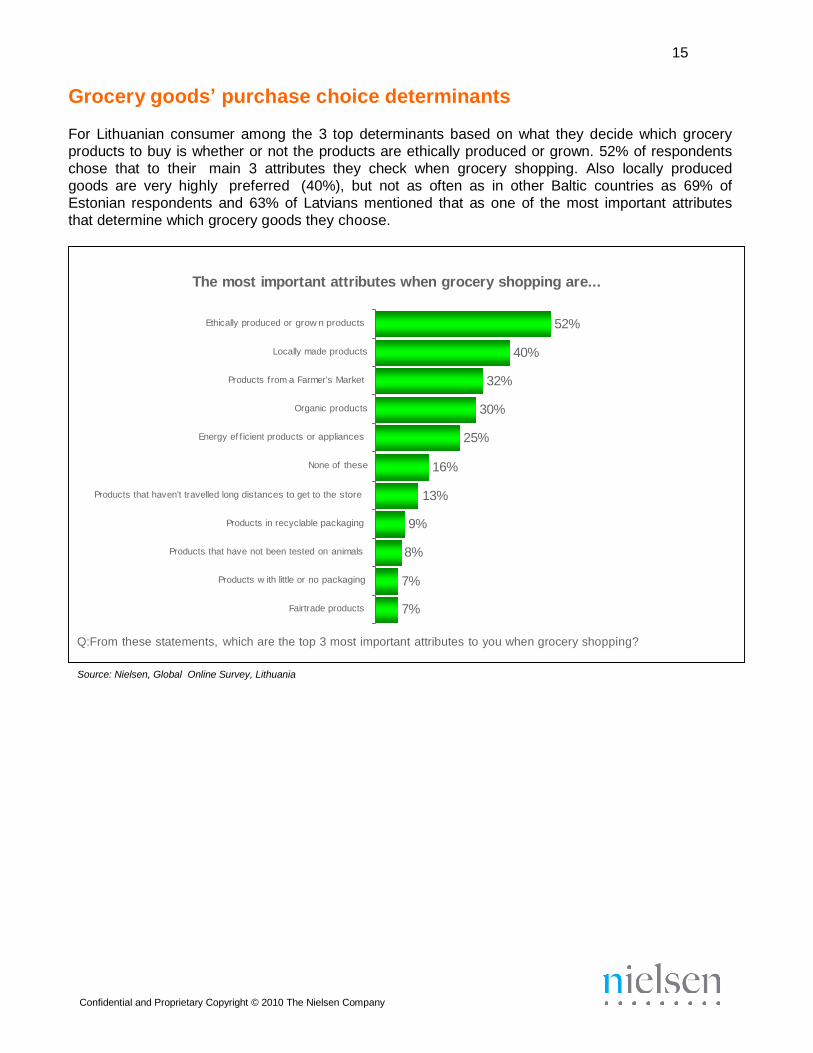

Grocery goods’ purchase choice determinants For Lithuanian consumer among the 3 top determinants based on what they decide which grocery

products to buy is whether or not the products are ethically produced or grown. 52% of respondents

chose that to their main 3 attributes they check when grocery shopping. Also locally produced

goods are very highly preferred (40%), but not as often as in other Baltic countries as 69% of

Estonian respondents and 63% of Latvians mentioned that as one of the most important attributes

that determine which grocery goods they choose.

The most important attributes when grocery shopping are...

Ethically produced or grow n products 52%

Locally made products 40%

Products f rom a Farmer's Market 32%

Organic products 30%

Energy ef f icient products or appliances 25%

None of these 16%

Products that haven't travelled long distances to get to the store 13%

Products in recyclable packaging 9%

Products that have not been tested on animals 8%

Products w ith little or no packaging 7%

Fairtrade products 7%

Q:From these statements, which are the top 3 most important attributes to you when grocery shopping?

Source: Nielsen, Global Online Survey, Lithuania

16

Confidential and Proprietary Copyright © 2010 The Nielsen Company

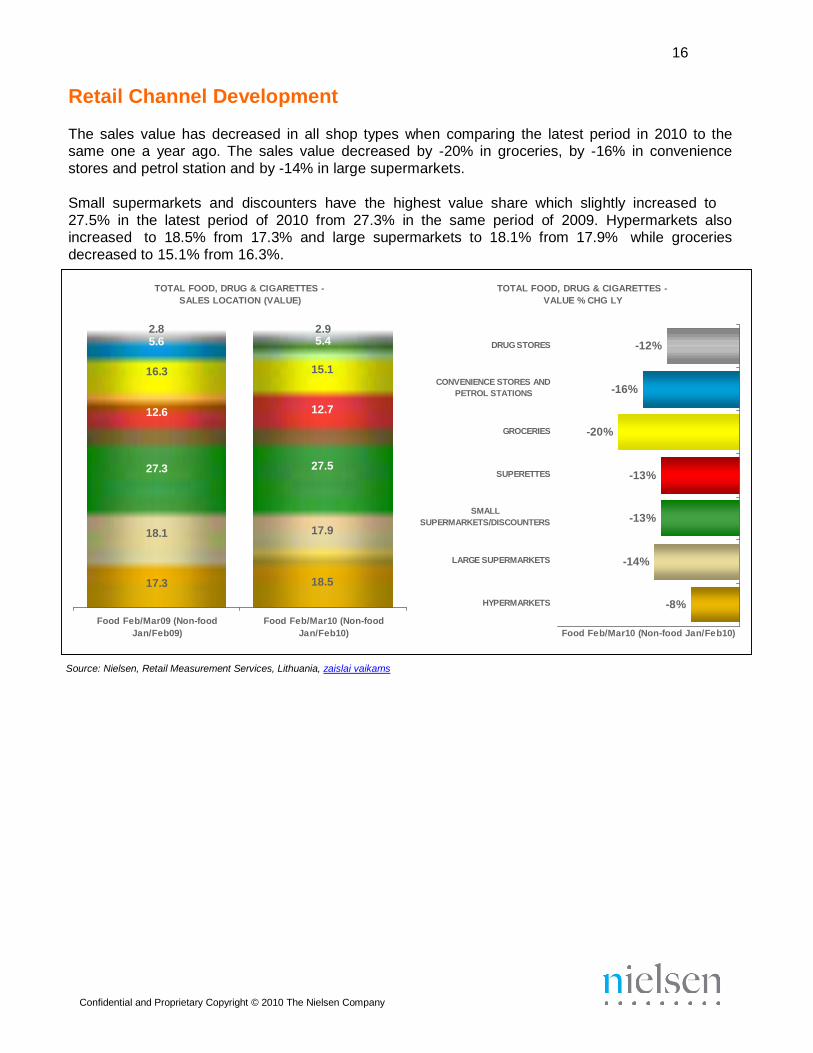

Retail Channel Development

The sales value has decreased in all shop types when comparing the latest period in 2010 to the same one a year ago. The sales value decreased by -20% in groceries, by -16% in convenience

stores and petrol station and by -14% in large supermarkets.

Small supermarkets and discounters have the highest value share which slightly increased to

27.5% in the latest period of 2010 from 27.3% in the same period of 2009. Hypermarkets also increased to 18.5% from 17.3% and large supermarkets to 18.1% from 17.9% while groceries

decreased to 15.1% from 16.3%.

TOTAL FOOD, DRUG & CIGARETTES -

SALES LOCATION (VALUE)

TOTAL FOOD, DRUG & CIGARETTES -

VALUE % CHG LY

2.8 2.9 5.6 5.4

16.3 15.1

12.6 12.7

DRUG STORES

CONVENIENCE STORES AND

PETROL STATIONS

GROCERIES

-12%

-16%

-20%

27.3 27.5

SUPERETTES

-13%

18.1 17.9

SMALL

SUPERMARKETS/DISCOUNTERS

-13%

17.3 18.5

LARGE SUPERMARKETS

HYPERMARKETS

-14%

-8%

Food Feb/Mar09 (Non-food

Jan/Feb09)

Food Feb/Mar10 (Non-food

Ja n/Feb10)

Food Fe b/Mar10 (Non-food Jan/Fe b10)

Source: Nielsen, Retail Measurement Services, Lithuania, zaislai vaikams

17

Confidential and Proprietary Copyright © 2010 The Nielsen Company

+1

Ma

xim

a X

XX

Ma

xim

a X

X

Ma

xim

a X

Iki

Ikiu

ka

s

Ce

nto

Hyp

er

No

rfa

No

rfa X

XL

No

rfa X

L

No

rfa L

No

rfa S

Rim

i H

yp

erm

ark

et

Rim

i

Su

pe

rne

tto

Pri

sm

a

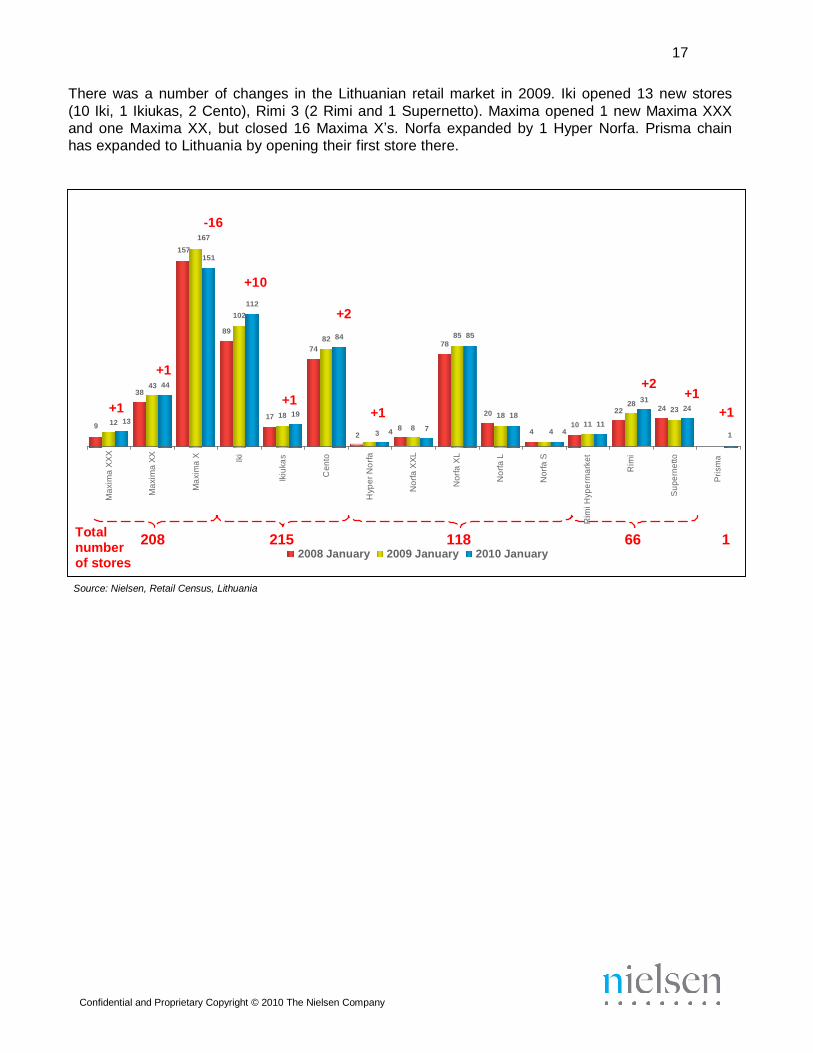

There was a number of changes in the Lithuanian retail market in 2009. Iki opened 13 new stores

(10 Iki, 1 Ikiukas, 2 Cento), Rimi 3 (2 Rimi and 1 Supernetto). Maxima opened 1 new Maxima XXX

and one Maxima XX, but closed 16 Maxima X’s. Norfa expanded by 1 Hyper Norfa. Prisma chain

has expanded to Lithuania by opening their first store there.

157

-16 167

151

+10

+1

43 44 38

112

102 89

+2

82 84

74

85 85

78

+2 +1

+1 +1

17 18 19

9 12 13 8 8

20 18 18

10 11 11

28 31

22

24 23 24 +1

2 3 4 7 4 4 4 1

Total number of stores

208 215 118 66 1 2008 January 2009 January 2010 January

Source: Nielsen, Retail Census, Lithuania

18

Confidential and Proprietary Copyright © 2010 The Nielsen Company

Store Visit Triggers

Most of the Lithuanian shoppers are also triggered simply by habit when shopping. In 2010, slightly more shoppers have stated that they choose where to shop out of habit or just go to the store that

is physically the closest to them. However at the same time, the importance of flyers and coupons

is increasing. More consumers have started to experiment with the choice of store to visit than last year.

HABIT

I shopped at the same store I always do

80%

75%

I just went to the closest store

I shopped at a store that a colleague, friend or relative had

recommended

I checked the newspaper or flyers for coupons and went

to the store with the attractive deals

5%

4%

17%

13%

64%

74%

I chose the store that I'd seen advertised recently

I heard of a new store and decided to try it

I was visiting friends/ family and went to a store that they

8%

5%

6%

5%

18%

2010

2009

usually shop at

I was passing a store that caught my attention and tried it

EXPERIMENTING

11%

14%

9%

Source: Nielsen, ShopperTrends 2010, Lithuania

19

Confidential and Proprietary Copyright © 2010 The Nielsen Company

Methodology and Design

ShopperTrends Research Design

• City Coverage:

– Estonia: Tallinn, Tartu, Pärnu, Narva

– Lavia: Riga, Daugavpils, Liepaja

– Lithuania: Vilnius, Kaunas, Klaipeda, Siauliai, Panevezys

• Target Respondent: Males/females aged 15-65 years, both main grocery

buyers and influencers;

• Interview Methodology: FtF interviews;

• Sampling Method: Random sampling with quotas for age and gender

• Sample Size: Estonia (n=550), Latvian (n=620), Lithuania (n=720)

• Fieldwork Period: 12th January – 12th February 2010

• Questionnaire length: ~60 minutes

• Weighting variables: Data weighted proportional to national ‘main grocery

shopper’ statistics based on age / gender / location

Global Online Survey

• Method and interviewing process: online interviews

• Geography: all areas of Estonia, Latvia and Lithuania – targeted at below

quotas

• Target audience:

– Males and females

– Aged 15+

• Sample size: Estonia (n=501), Latvia (n=501), Lithuania (n=503)

• Data weighted proportionally to total national population

• Timing: 8th

– 26th

of March

Confidential and Proprietary Copyright © 2010 The Nielsen Company

20

Retail Measurement Services

• Markets covered:

o Modern Trade Estonia: Selver, RIMI, Säästumarket, Maxima, Prisma, Kaubamaja, ETK

(hypers, large/small supers, superettes), Stockmann, Comarket, Statoil*,

Olerex*, R-Kiosk*, Watson*, Laminto*, Rosalind*, L’Cosmetics*,

Kaubamaja*, Koduextra*, Apotheca*, ILU* Latvia: Maxima, RIMI, Supernetto, Prisma, IKI, LeaderPrice/Cento, Mego,

Elvi, Nelda, Drogas, Statoil*, Plus Punkts*, Narvessen*, Tabakas Nams*, Kollonna*, Euroaptieka*, SentorPharm*, Multilukss*

Lithuania: Maxima, RIMI, Supernetto, Norfa, Prisma, IKI, LeaderPrice,

Lukoil*, Statoil*, Lietuvos Spauda*, R-kiosk*, Kauno Spauda*, Drogas*,

Sarma*, Kosmada*, Eurovaistines*, Eurokos*, Ermitazas* * not for all categories due to low importance

• Categories covered:

o Baby Food - Infant Milk, Jarred Baby Food, Porridges o Bakery - Dark Bread, White Bread o Cereal Products - Breakfast Cereals, Flakes

o Cigarettes

o Coffee, Tea & Cocoa Drinks

o Confectionery – Assortments, Caramels, Chewing Candies, Chewing Gum, Chocolate Bars, Chocolate Countlines, Pastilles, Small Bites

o Dairy - Butter & Margarine, Fresh and Processed Cheese, Cottage Cheese

(EE,LT), Fermented Cheese, Fresh Cream, Curd Countlines, Kefir, Milk, Milk Desserts, Quark Curd Desserts, Quark Curd Pastes (EE, LV), Sour Cream, Yogurt, Ice Cream

o Frozen Food (EE, LV) - Minced Meat Products, Deep Frozen Potatoes

o Household Products - Laundry Detergents, Dishwashing Detergents, Household Cleaning, Fabric Softeners, Toilet Blocks, Air Fresheners, Laundry

Bleaches, Toilet Cleaners, Water Softeners, Stain Removers, Laundry Bar Soaps

o Light Alcohol – Beer, Beer Cocktails, Ciders and Long Drinks

o Non-Alcoholic Ready-to-drink Beverages - Carbonated Soft Drinks, Energy and Sport Drinks, Ice Tea, Juice, Nectars, Still Drinks, Mineral Water

o Paper Products - Toilet Paper, Baby Diapers, Sanitary Protection, Kitchen Rolls, Serviettes

o Personal Care - Face Skin Care, Shampoos, Toothpaste, Hair Colorants,

Shower Gel, Decorative Cosmetics, Blades, Deodorants, Hair Conditioners, Toothbrushes, Skin Care, Soaps, Razors, Hair Treatments, Depilatories,

o Pet Care - Cat Food, Dog Food, Cat Litter

o Processed Meat – Boiled & Cooked Sausages, Ham, Meat Jellies (EE), Meat Marinade (EE, LV), Pastes (EE), Meal Sausages, Smoked Sausages

o Sauces & Seasonings – Bouillons, Soups, Dehydrated Seasonings, Dressings,

Ketchup, Mayonnaise, Tomato Sauces o Snacks – Sweet Biscuits, Chips & Extruders, Salted Nuts, Salted Biscuits

o Strong Alcohol – Brandy & Cognac (LV, LT), Nastoyka/Nalivka (EE, LT), Sparkling Wine & Champagne (EE, LT), Vermouth, Whisky, Vodka