banco abc - 2007 apimec presentation

TRANSCRIPT

December 2007

Banco ABC BrasilAPIMEC

22

Summary

Who we are 03

Business Segments 10

Competitive Advantages 16

Financial Overview 22

Our Vision of the Future 26

Contacts and Disclaimer 28

Who we are

4

Leading Credit Provider to Mid-Sized and

Large Companies

Strong focus on providing loans and structured products to Middle and Large-Middle.

Expertise in corporate credit risk analysis with remarkably low historical losses

Unique and wide range of credit products for Middle and Large-Middle segments

High level of customization

Sophisticated products for Large-Middle clients

Winning combination of a strong controlling shareholder and an independent local management

team

Agile decision making process

Access to attractive funding sources

Enhanced rating

Overview

5

Our History

Arab Bank Corporation and Roberto Marinho

Group jointly initiate Banco ABC Roma SA,

acting in the segments of corporate lending,

trade finance and treasury

Current

management starts

running the bank

Arab Banking Corporation

and Local Management

acquire Roberto Marinho

Group´s shares

The bank´s name

changes to

Banco ABC Brasil S/A

The bank structures

its Middle Market

Operations

The bank starts its

payroll deductible

activity

1989 1991 1997 2005 2006 2007

IPO

66

Initial Public Offering July 25 2007

R$ 1,7 Billion

Market Cap

Offering structure

IPO in Brazil with sales effort

abroad via 144A and Reg S

Offering Summary

Shares Offered

Offering price and

size

45,1 million preferred shares,

with 100% tag along (98.4%primary issuance)

R$ 13,50 / share. Total of

R$608.850.000,00

Ownership Structure

Marsau Uruguay

(ABC)

56,0%

Local Management

9,4%

Associates1,4%

Free Float

33,2%

7

Focus in Corporate Credit

1 Including guarantees

-

-

-

100%94% 88,5%

89,8%

86,7%

6%11%

10%

11,7%

0,5%

0,21%

1,6%

2004 2005 2006 9M 2006 9M 2007

2.011

2.605

2.911

2.649

4.251

CAGR = 20.3% CAG

R = 6

0,5%

-

-

-

100%94% 88,5%

89,8%

86,7%

6%11%

10%

11,7%

0,5%

0,21%

1,6%

2004 2005 2006 9M 2006 9M 2007

2.011

2.605

2.911

2.649

4.251

CAGR = 20.3% CAG

R = 6

0,5%

Corporate & Large Middle Middle Market Payroll Deductible

Credit Portfolio1 (R$ million)

CR

ED

IT

Corporate

Loans

Consumer

Large

Corporate &

Large

Middle

Middle

Market

Payroll

Deductible

Segments

Over R$ 250 mi

R$ 30 mi to

R$ 250 mi

Consumer

Annual

Revenues

8

Credit Portfolio

Guarantees % by Sector

Agribusiness 18%

Construction 14%

Financial Inst./Insurance 14%

Whosale Distribution 6%

Electric Energy 5%

Foods 4%

Professional Services 4%

Individuals 3%

Vehicles and Tools 3%

Industry - Machine 3%

Telecommunications 3%

Transport and Logistic 3%

Retail Distribution 3%

Payroll Deductible 2%

Industry - Chemicals 2%

Others 12%

Oth

ers

Sto

cks

Ru

ral P

rom

isso

ry N

ote

Me

rch

an

t P

led

ge

Ma

rke

tab

le S

ecu

ritie

s

Ve

hic

les

Re

al E

sta

te

Gu

ara

nte

es issu

ed

on

be

ha

lf o

f clie

nts

Go

od

s

Re

ce

iva

ble

s

Ch

atte

l M

ort

ga

ge

Cle

an

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

9

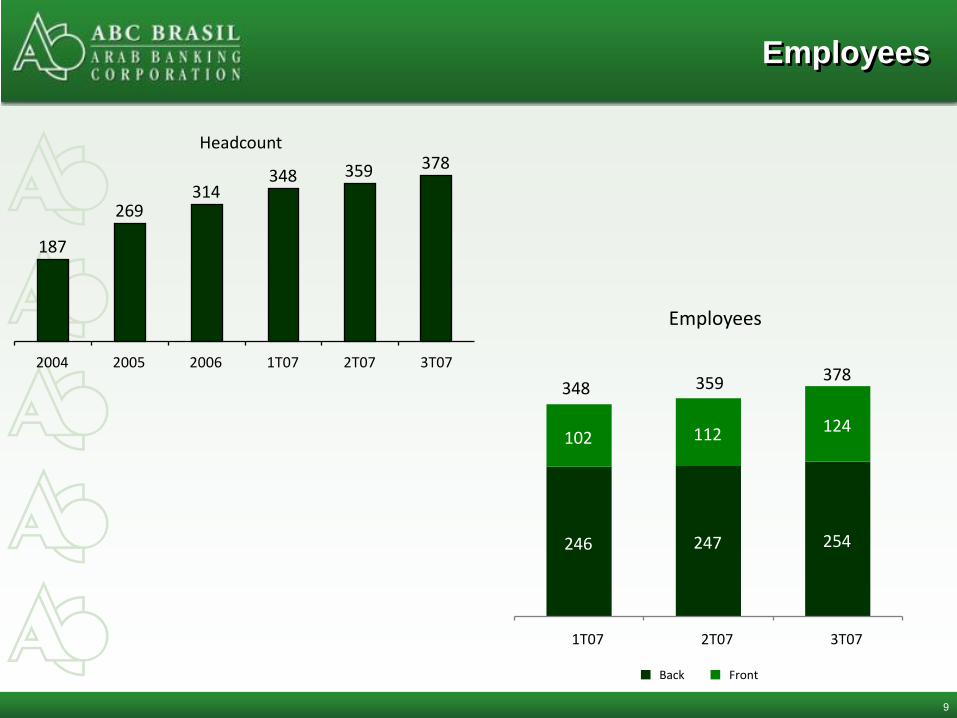

Employees

Headcount

187

269314

348 359 378

2004 2005 2006 1T07 2T07 3T07

Employees

246 247 254

102 112 124

1T07 2T07 3T07

Back Front

348 359 378

Business Segments

11

Large Corporate & Large Middle

Large

Corporate &

Large Middle

Target MarketAverage

Ticket

Companies with annual revenues

over R$ 250 miR$ 8,2mi

# Clients

446

Great SP

38%

SP Countryside and MG

37%

RJ and Northeast

14%

South

11%

Geographical Distribution (% of portfolio)

Large Corporate & Large Middle R$ mi

2.010,7

2.458,22.587,3

3.684,2

2004 2005 2006 9M2007

12

Middle Market

(R$ MM)

Middle Market

Target MarketAverage

Ticket

Companies with annual revenues

ranging from R$ 30 mi to R$ 250 miR$ 1,7mi

# Clients

297

Great SP89,4%

SP Countryside7,3%

MG3,3%

Geographical Distribution (% of portfolio)Middle Market R$ mi

146,4

309,2

498,4

2005 2006 9M2007

Middle Market

2005 2006 9M2007

13

Payroll Deductible

Payroll

Deductible

Target MarketAverage

Ticket

INSS retirees

Civil Servants24.778

# Clients

58R$2.740 24

# Credit

Agents # Agreements

(R$ MM)

Payroll Deductible R$ mi

14,4

67,9

2006 9M2007

50,3%

INSS

49,7%

CCóódigos (% digos (%

OTHERS

50,3%

49,7%

Agreements (% of portfolio)

Originated Loans per Month : R$12

Million

Credit Assigned : Zero

14

Other Activities

Hedge & Derivatives – sophisticated products offered to Clients

Pricing & Asset Liability Management

Proprietary Trading

Brazilian Sovereign Bonds (Local / Offshore)

Interest Rates

FX (USD-BRL)

Brazilian Corporate Bonds (Local / Offshore)

Brazilian Corporate – other instruments (CDS, CLN, Forfaiting)

Average V@R 2006 : US$1 Million

Treasury

15

Other Activities

Capital Markets

Products Offered : FIDCs / Debentures / Structured Trade Finance

Local Mkt (1H2007)

# Transactions : 5

R$ 1,6 Bi

Offshore (1H2007)

# Transactions : 5

US$ 82 Mi

Competitive Advantages

1717

Sophisticated and Diversified Products

Our sophisticated and diversified product portfolio allows us to benefit from an

untapped demand in our market niche

Note:

1 In terms of annual revenues in R$ million

Larg

e

Co

rpo

rate

Larg

e-M

idd

leM

idd

le

Client Size1

2,000+

250-

2,000

30-250

Clients

NeedsHow We See Competition?

Individuals

Co

nsu

mer

# of potential clients

Industry

Supply

Product Sophistication

Products

Onshore / Offshore loansGuaranteesDebt capital marketsFIDC / securitizationStructured trade financeStructured project financeHedge and derivatives

Loans (working capital, revolving credit)Advances on receivablesTrade financeGuarantees

Untapped Demand

Onshore / Offshore loansGuaranteesDebt capital marketsFIDC / securitizationStructured trade financeStructured project financeHedge and derivatives

Payroll deductible loans

LEGEND: High Mid-High Medium Low

1818

Proven Track Record

Growth Despite Adverse Economic Conditions

Mexican Crisis

Growth throughout different economic scenarios

Credit Portfolio

1996 2000 2001 20032002199919981997 2004 2005 2006 9M07

Asian Crisis

Russian Crisis

Devaluation of R$

“Apagão”

September11th

Argentinean Crisis

Presidential Elections of

Lula

Banco Santos Bankruptcy

IPO(R$ million)

0.33% 0.39% 0.10%0.02%0.00% 0.02% 0.06%

0.67%

0.00% 0.02% 0.06%

1.09%

19

AA-C99,3 %

D-H0,7 %

High Quality of

Credit Portfolio

Credit Portfolio

Classification 3Q07

% by

portfolio

AA 510,6 15,2%

A 1.529.6 45,5%

B 1.067.1 31,7%

C 232,7 6,9%

D 8,4 0,2%

E 0,7 0,0%

F 2,8 0,1%

G 2,8 0,1%

H 8,4 0,2%

Total 3.363,1 100,0%

(Em R$ Million)

(Em R$ Million)

2001 2002 2003 2004 2005 2006 2007

Losses/Portfolio (%) 0,1% 0,1% 0,7% 1,2% 0,0% 0,0% 0,1%

Provision/Portfolio (%) 0,5% 1,8% 2,7% 1,6% 1,2% 1,4% 1,1%

AA-C 3.340,0

D-H 23,1

2020

Agile Decision Making & Experienced

Management

Key Management Team

& Shareholders

Fast and secure credit approval is possible due to the 16 years experience of the same

senior management team

Credit Approval Process

Committees meet officially every week or whenever it is necessary

Whole credit approval process takes no longer than 20 days after

client visit

Ability to get credits safely approved within 48 hours

Days

CommercialArea

Credit Risk Area

Credit Risk &Commercial

Credit Committee

Disbursement

Client Visits

Document Requests

ProposalProposal Analysis

Client Due Diligence

Further Client Information

Credit Risk Analysis and Discussions

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10 D11 D12 D13 D14 D20

At least 70% of clients have its credit

analyzed, approved and money disbursed

within 14 daysFast Track – 1 Day Credit Approval

Tito E. da Silva 16 38

Name ABC Banking

Years

Anis Chacur 16 24

José E. C. Laloni 16 23

Gustavo A. Lanhoso 16 23

Sérgio L. Jacob 16 19

Sérgio R. Borejo - 20

21

Controlling

Shareholders

(1S07)

Total Assets: US$ 27,311 Mi.

Equity Shareholders: US$ 2,168 Mi.

ROE: 13,6%

Ratings:

BBB+ A3BBB+

2004 2005 2006 2007

National - Long Term A A AA- AA-

National- Short Term F1 F1 F1+ F1+

International - Long Term - BB- BB BB+

International - Short Term - B B B

The combination of independent management with successful track record and a strong

controlling shareholder helps to support our high rating

High Rating with Strong Sponsor &

Independent Management

Financial Overview

23

Funding

Performance

1.707

2.045

2.472

3.106

2004 2005 2006 9M2007

CAGR = 24,3%

Private

3%

Private

2%

Financial Inst.

32%

BNDES

14%

Corporate

26%

Institutional

23%

Local International

24

Profitability *

Net Profit (R$ mi) - Quarterly

16,2

25,8 23,3

3Q06 2Q07 3Q07

CAGR = 43,8%

41,1

67,5

Jan-Sep/06 Jan-Sep/07

Net Profit (R$mi) – 9 months

CAGR = 64,3%

15,7%

22,0%

10,1%

3Q06 2Q07 3Q07

ROAE (%aa) - Quarterly

13,3% 14,7%

Jan-Sep/06 Jan-Sep/07

ROAE (%aa) – 9 months

*Excluding IPO expenses

25

Indicators

Shareholders Equity (R$ MM) and Basel Index (%)

422 483

1.083

14,0% 13,6%

26,7%

3Q06 2Q07 3Q07

Efficiency Ratio (%)

52,4%41,9%

35,8%

3Q06 2Q07 3Q07

NIM (Quarterly)

6,7% 6,8%5,9%

3Q06 2Q07 3Q07

6,7% 6,8%5,9%

NIM (9 months)

6,3% 6,5%

Jan-Set/06 Jan-Set/07

6,3% 6,5%

Jan-Sep/06 Jan-Sep/07

Our Vision of the Future

27

Diversified Growth Strategy

Banco ABC Brasil is well-positioned to capture growth from different segments within

the industry

Strategic Approach

Opportunistic

Increase average loan per client

Cross-selling of products

Strong focus with long-term approach

Increase average loan per client

Increased product sophistication

Geographic expansion (new offices)

Increase client base

Increase average ticket

Increase client base organically or through acquisition of on-going business

Fo

cu

s

Large-Middle

Large

Corporate

Middle

Payroll

Drivers

# Clients Avg. Loan Spread

28

Contacts and Disclaimer

Investor Relations

Sergio Lulia Jacob – CFO and IRO

Alexandre Sinzato – IR Manager

Eduardo Randich – IR Analyst

Web Site: www.abcbrasil.com.br/ri

Email: [email protected]

Phone: +55 (11) 3170 2186

The material that follows is a presentation of general background information about Banco ABC Brasil S.A. ( “Banco ABC” or the “Bank”) as of the date of the presentation. It is information

in summary form and does not purport to be complete. No representation or warranty, express or implied, is made concerning, and no reliance should be placed on, the accuracy,

fairness, or completeness of this information.

This presentation may contain certain forward-looking statements and information relating to Banco ABC that reflect the current views and/or expectations of the Bank and its

management with respect to its performance, business and future events. Forward looking statements include, without limitation, any statement that may predict, forecast, indicate or imply

future results, performance or achievements, and may contain words like “believe,” “anticipate,” “expect,” “envisages,” “will likely result,” or any other words or phrases of similar meaning.

Such statements are subject to a number of risks, uncertainties and assumptions. We caution you that a number of important factors could cause actual results to differ materially from the

plans, objectives, expectations, estimates and intentions expressed in this presentation. In no event, neither the Bank nor any of its affiliates, directors, officers, agents or employees shall

be liable before any third party (including investors) for any investment or business decision made or action taken in reliance on the information and statements contained in this

presentation or for any consequential, special or similar damages.

Securities may not be offered or sold in the United States unless they are registered or exempt from registration under the United States Securities Act of 1933. Any offering of securities

to be made in the United States will be made solely by means of an offering circular that may be obtained from the placement agents or the underwriters. Such offering circular will

contain, or incorporate by reference, detailed information about Banco ABC and its business and financial results, as well as its financial statements.

This presentation does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase any securities. Neither this presentation nor anything contained herein

shall form the basis of any contract or commitment whatsoever.

The market and competitive position data, including market forecasts, used throughout this presentation was obtained from internal surveys, market research, publicly available

information and industry publications. Although we have no reason to believe that any of this information or these reports are inaccurate in any material respect, we have not

independently verified the competitive position, market share, market size, market growth or other data provided by third parties or by industry or other publications. Banco ABC, the

selling shareholders, the placement agents and the underwriters do not make any representation as to the accuracy of such information.

This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated in whole or in part without Banco ABC’s prior written consent.