banco popular - axiomaxiom-ai.com/.../06/banco-popular_axioms-analysis.pdf · banco popular 1. what...

TRANSCRIPT

14/06/2017

1

Banco Popular

1. What were Popular’s problems?

The initial problems

The initial problems of Popular were rather well known, including from the supervisors. They

can be broken down into two issues:

A much too large real estate book (37bn€), a legacy from the financial crisis and the

result of foreclosures on non-performing loans. This book was decently performing:

Popular had set up a dedicated department to wind it down and to optimize sales, had a

partnership with an experienced servicing firm and was selling assets at a 2% premium to

book value. On top of the real estate book, the bank had a large NPL ratio (14.7% in the

latest EBA data – the most reliable source, we believe.) However, in April 2016 the Bank

of Spain introduced a new circular on provisioning, with, in particular, new rules on

appraisals, collateral haircuts, etc. With the limited disclosures available (EBA, company

reports) we had estimated the shortfall at 6.7bn€ and the company booked 5.7bn€ of

provisions at FY2016. In Q1 2017 the bank booked an additional €506m.

A mortgage book that was exposed to the mortgage floor litigation risk following the

ECJ ruling on full retroactivity. This led to a 229m€ provision in Q4 2016 but also put

pressure on the NIM, by far the biggest share of Popular’s earnings.

These problems were mitigated by the following considerations:

The bank had a very successful and very profitable core SME commercial franchise;

The bank had been able to raise equity successfully to compensate for some of the

provisions (including recently in May 2016.)

The crisis

The crisis started to unfold when the bank indicated that its internal audit had uncovered (a) a

provision shortfall and (b) financing granted to clients during the latest capital increase1 for

205m€. This led to media frenzy and speculations that large additional provisions were required

on the real estate book and that the management should envision a new strategy.

The management put on a dismal performance in combining various potential strategies without

giving a clear direction to the market:

1 This in itself is neither illegal nor a wrongdoing but it should lead to CET1 deductions.

14/06/2017

2

The management was very late in announcing that the bank was officially for sale and

instead it sounded interest from local buyers. Foreign banks and investment funds were

effectively shut out from the process.

The management initially rejected a capital increase and then “soft hired” advisors to raise

equity – but this was too little too late. Institutional buyers were struggling to understand

why they should invest equity in a bank when no competitor seemed interested, despite

the huge potential synergies, which they obviously did not have.

The management had no communication strategy and was merely reacting to the news

flow. They were not even able to organize an investor day to present a comprehensive

strategy.

Creditors, such as the large AT1 holders, were totally kept in the dark and were reassured

that it was business as usual. The largest AT1 holder was not able to access management

to discuss strategic options.

As we explain below, the authorities justified the resolution by a liquidity crisis. Hence, the

ultimate downfall of Popular demonstrated another weakness of the bank: despite a high

Liquidity Coverage Ratio (“LCR”) the bank’s deposit base was not granular enough, with several

very large tickets. This is partly explained by the SME franchise of the bank but also, we think, by

some of its political connections. The numbers are not public but it is very likely that, compared

to peers, the bank had a smaller share of guaranteed deposit (i.e. below 100K€.)

2. Why was the decision so shocking to the market?

We believe the market was shocked by different aspects of the crisis which we discuss here.

The swiftness of the SRB’s actions

We believe a lot of investors were shocked by the celerity of the SRB’s decision, especially

outside of a weekend. However, we understood from various conversations we have had with

banks, including Santander, investors and journalists, that the FROB actually took control of

Popular earlier, maybe as soon as Friday night, and organised the sale to Santander on Tuesday

night. This is not unusual for the resolution of a bank that usually takes place over a weekend.

True, the management was still contemplating various capital actions and even the possibility of a

sale, but it seems that liquidity concerns left them without the time they required.

All junior bonds got wiped out with no creditor hierarchy

Some investors have expressed disbelief at the 0 valuation for Tier 2 bonds. It is true that the

provisional valuation, that was made by an independent advisor, in only a few hours we

understand (!), had a very wide range of values, and that the higher bound (-2bn€) was

suspiciously close to the amount that allows the resolution authorities to effectively wipe out

junior creditors. Still we are not that surprised: as long as the bank is declared in resolution,

bondholders have basically two protections:

The valuation of the bank should show that losses to be absorbed are higher than the

amount of the junior bonds available to absorb them.

The no creditor worse off principle implies that creditors should not receive less than

they would have received in a normal bankruptcy.

14/06/2017

3

However, we have always expressed serious doubts on the strength of the protection offered

by these two principles. A Tier 2 or AT1 tranche in a bank’s balance sheet will generally

represent between 1% and 2% of RWA, if not less. Considering an average 40% RWA

density, this means the size of such liabilities is between 0.4% and 0.8% of a generally very

complex balance sheet. In spreadsheet modelling, when you have to value a bank in a

weekend, it is very clear that a number like that is well within the margin of error. The

valuation range for Popular was 6bn€, i.e. 3.8% of total assets. What this means in practice, is

that a zero recovery is a logical and credible scenario both for AT1 and Tier 2, and possibly

non-preferred seniors, unless there is a political will to protect some tranche of the balance

sheet or there is a buyer willing to make whole these investors. In other terms, when it comes

to bank risk, the probability of default is much more important than the loss given default.

Some investors have also been shocked that conversion terms included in the AT1

documentation were not respected (i.e. there was no conversion at the price given in the

prospectus) and that Tier 2 were converted despite no such clause in their prospectus. We

believe this criticism is unmerited: the conversion powers of the resolution authorities are

very clear in the BRRD and the bond prospectuses are largely irrelevant here.

The market believed the PONV was still distant

The exact trigger of a bank’s non-viability remains a grey area in European legislation and the

case of Popular came as big surprise to most investors. True, the CET1 ratio was low, but it was

above the MDA threshold for distribution restriction, the supervisor had allowed for a recent

AT1 coupon payment, and the bank was clearly working (although not very efficiently) on a

strategic plan that included, to the very least, asset sales likely to generate 200bps of CET1.

Potential additional LLPs were being discussed, and rumoured to be below 2bn€, which seemed

manageable for a bank with a pre-provision profit around 1bn€/year and a 10bn€ book value.

Crucially, and unlike many problem banks in Italy or elsewhere, the core franchise of the bank

was very profitable and delivering a good ROE, suggesting that there would be an appetite for

capital raising post dilution.

Moreover, the possibility to convert AT1 bonds, especially the one with a 7% CET1 trigger,

seemed to allow for an additional 1.25bn€ CET1 buffer (i.e. 200bps CET1) should additional

provisions lower the CET1 ratio below 5.125%. Clearly, the most bearish market view was that

the bank was viable, possibly after 2bn€ of additional LLPs and an AT1 conversion, and it seems

that some distressed investors would have been interested by the bank at a low price-to-book

valuation (maybe 0.2x). We can think of a few banks in Europe that have a lower “viability”

(starting with the four Greek banks or the two Venetians) and that have not been put into

resolution by the SRB.

Last but not least, even after taking into account the “abnormal” (see below) provisions taken by

Santander (7.2bn€) the equity of the bank remained positive.

However, the main reason for the resolution, as explicitly stated by the ECB, was the liquidity of

the bank, not its solvency: “The significant deterioration of the liquidity situation of the

bank in recent days led to a determination that the entity would have, in the near future, been unable to pay

its debts or other liabilities as they fell due.” Obviously, this remains a valid ground for determining that

14/06/2017

4

a bank has to be resolved but it came at a surprise to the market as we discuss below into more

details.

Liquidity was not perceived as a substantial risk for Popular

Since 2011, liquidity has become a non-issue for banks. Indeed, authorities have taken successive

decisions that have allowed banks to access almost unlimited amounts of liquidity provided they

are solvent:

The MRO facility of the ECB is now unlimited in amount provided that collateral is

available;

The new LTRO/TLTROs facilities have given banks access to very large amounts of

medium term funding;

New collateral rules have allowed banks to dramatically expand the amount of available

collateral;

Several legislations have allowed banks to issue covered bonds collateralised by a wider

range of assets;

The ECB and national central banks have showed their willingness to provide

emergency liquidity (ELA) even for the most distressed banks (90bn€ for Greek banks!)

with even larger eligibility for collateral;

Governments have granted guarantees on senior bonds, including very recently for

Italian banks, and with the blessing of the European Commission;

Deposit guarantees have been harmonized in the EU and there is now certainty that

deposits under 100k€ are fully protected.

This is probably why most investors felt that liquidity was not a risk for Popular and were

shocked that it turned out to be the sole motivation for the resolution– especially with a very

decent 146% LCR ratio and with a large portfolio of liquid government bonds.

However, it appears that a quite remarkable series of events happened, as reported by the press in

the past few days.

The FROB and ministry of finance disclosed that the bank had lost approximately

18bn€ of deposits in a couple of days.

From the discussions we have had with two of the three largest banks in Spain, we

understand they saw combined inflows of only 1.5bn€…leaving a 15bn€ gap even with

the assumption that the other commercial banks also received similar inflows.

The Spanish press reported that the deposit outflows were largely due to withdrawals

from public clients: local authorities (Canaries allegedly withdrew 600m€), social

security funds (allegedly withdrew several billions), SAREB (allegedly withdrew 600m€),

etc. Allegedly the ICO also had a large deposit balance with Popular and we understand

that it was withdrawn too.

According to the press, the Bank of Spain requested a 90% haircut on the bank’s

collateral. Allegedly, Popular offered 40bn€ of collateral and was offered…only 3.5bn€

in funding in exchange, which is quite extraordinary considering the ECB’s general

documentation where the maximum haircut is 65%.

14/06/2017

5

There have been conflicting reports on the bank’s access to the ELA: according to

official statements the bank had limited access to the ELA, but the press reported that

according to internal sources at Popular, the bank was denied any ELA.

All in all, it seems the liquidity dry up was rather unusual and it is quite possible that the

government did not feel the need to prevent it – or to stop public institutions from withdrawing

their money. Clearly, this demonstrates a couple of important points:

The LCR calculation is somehow flawed because it assumes standard withdrawal

rates on deposits (these rates are different for corporate, retail, etc.) but any coordinated

decision to withdraw very large deposits by a few actors could be enough to destabilize

rapidly the balance sheet of a bank;

A much diversified deposit base is much stronger than a concentrated one. In particular,

we think the share of guaranteed deposit will become an important metric when

assessing the liquidity risk of bank. Obviously not all depositors will act rationally and

some could be influenced and scared by media frenzy, but in a world where deposits

below 100k are fully guaranteed and where the BRRD grants a senior ranking to

guaranteed deposits, we think these deposits should be stickier, even in distressed

situations.

The auction was surprising

Another reason for the market shock was that many global, large, investors were still waiting to

hear from the investment banks mandated by Popular to reach an opinion on a potential

recapitalisation or even an outright sale. Clearly, the feeling was that the new strategy was still a

work in progress. However, we understand from conversations with the banks themselves and

press reports, that only two banks were allowed to submit a bid for Popular and that they had

only 11 hours to do so. Many investors have expressed surprise at such a closed-door auction and

do not understand why they were not consulted. This could also be a consequence of the

management’s actions as it chose to consult only a handful of Spanish banks for a potential

merger. These banks were already in the process of a due diligence and had more information

than the rest of the market.

The procedural requirements set out in the BRRD are rather loosely drafted although the general

principle is that, if a sale is organised, there should be a minimum of competition. Clearly, here, if

the reports are correct, it was the absolute minimum (two banks.)

Again, this demonstrates a few important points for future cases:

During a resolution process, it is very unlikely that institutions without a deep

knowledge of the bank will be able to make a price (for the bank or some of its

portfolios)

In practice, this means that the sale of business tool (or an outright sale) is unlikely to be

the preferred resolution tool, as in most cases there will be no investor with a clear view

on the bank. However, should special circumstances apply, such as the one with

Popular, i.e. an ongoing sale process, then the potential buyers will be in such a strong

14/06/2017

6

position that they are unlikely to make a generous bid and to offer any protection to

shareholders or junior bondholders.

3. Does this crisis show a significant shift in the SRB/EU’s resolution

policy?

Clearly, the first and foremost concern for investors should be the read-across of that resolution

to other banks. This raises two very different questions: (i) has the SRB changed its stance

regarding resolution and (ii) are there any other banks significantly at risk? We deal with the first

question below.

All considered, we think there has been no shift in the EU or the SRB’s stance towards

resolution:

- In terms of valuation, all banks that have been put in resolution have had negative

valuation estimates to justify full or partial write-downs on subordinated debt.

- In terms of burden sharing, since the EC’s decision to change state aid rules, a full

contribution of junior debt (write-down or equity conversion) has been considered a

prerequisite to any state aid and we think it is fair to assume that in most resolutions a

similar approach will apply.

- Popular’s case has been different from other situations where equity conversion had

some value (e.g. Bankia or MPS more recently.) We believe there are two reasons why

this did not apply here

o a buyer for the whole bank was found, taking on board all senior liabilities,

and this was obviously the safest option from a systemic risk point of view.

Based on the (obviously disputable) valuations made by the advisors, this

could even be considered a good deal for Popular’s creditors as any negative

valuation below -2.3bn€ could have justified a haircut on senior debt.

o The main issue (see above) of Popular was a liquidity issue. Converting the

subordinated debt into equity would have not contributed in any way to

restoring liquidity.

- The market focused probably too much on the bail-in tool, but resolution authorities

can use a variety of tools – and have used them in the past! The SRB used the "sale of

business tool" (Article 38), the write-down tool (Article 59) but not the "bail-in" tool

(Article 43) in particular on senior debt (probably because Popular had very little

senior bonds.)

In other terms, we think the SRB has not changed its approach but was confronted with a

situation where the only way to stop a senior debt default was to sell the bank to a larger bank –

at whatever price that bank was willing to accept.

14/06/2017

7

The true and significant shift was in Spain’s approach to the crisis: there was no political will

whatsoever to grant liquidity measures to Popular or to provide capital. In that context,

where there is no time, the resolution authorities, which are independent and have no power to

grant liquidity measures, have basically only two options: a default on senior debt (haircut,

moratorium, etc.) or the sale of the bank.

4. What is the read-across for other banks?

The first and immediate read-across concern is regarding asset quality. Indeed, immediately

following its acquisition for 1€, Santander announced 7.9bn€ of additional provisions, bringing

real-estate loan coverage to 75% and real estate assets coverage to 65%. Non-real estate loans

coverage was increased to 56%. Benchmarking these very high coverage ratios to many of the

smaller Spanish banks – or Italian, Portuguese, Greek and Irish banks for that matter – would

raise considerable capital concerns.

The truth, as always, is more complicated. Indeed, Santander itself acknowledges that these

coverage ratios are very high. They were chosen to allow a full sale of the entire real estate

portfolio within the next 18-36 months to distressed investors looking for a 20% return!

Under IFRS rules, yields used to compute a loan’s coverage ratio should be the loan’s yields, i.e.

rarely above 5%. Even regulatory overlays do not lead to such pharaonic returns.

Moreover, coverage ratios are not arbitrary numbers, they depend, among other things, on the

type of NPE (forborne, past due, NPL, etc.) on the type of debtor (corporate, financial or

household) and on the collateral value.

So the bottom line is that Santander’s choice of coverage ratios should definitely not be

used as benchmarks for other banks.

Still, we believe there is a substantial non-performing asset overhang in the EU - even if this is

certainly not new. We show below the results of the detailed benchmarking analysis of NPE that

we have performed on a wide sample of EU banks with the latest EBA Transparency Data

available (this is the only dataset that includes consistent and harmonized data in the EU.)

14/06/2017

8

Source: Axiom AI, EBA

Apart from the Greek and Cypriot banks, we can see obvious shortfalls for some midcap Spanish

and Italian banks that we think will need to be addressed at some point. Interestingly, in the few

cases where supervisory authorities have forced banks to take extra provisions or where the

banks have decided to do it themselves, our estimates have been very close (e.g. Monte dei Paschi

with 4.9bn€ or Unicredit with 13.2bn€.) Any bank which would see its CET1 ratio go below 9%

(obviously an arbitrary threshold) after taking these extra provisions should only be considered

with caution.

This study does not include other NPAs, i.e. foreclosed real estate, but the situation is very

different for those. Spain has been “penalized” by the quality of its enforcement procedures: in

many EU jurisdictions, banks are struggling to repossess the collateral on their loans and,

logically, own very few real assets. On the contrary, in Spain, NPE have been going down

because banks have been able to write them off against the collateral (which is good) but now

have large real estate books. It is not easy to harmonize the disclosure of all banks on this,

especially smaller ones, but we believe EBA data provides, again, the best disclosure. In this data

set, real estate is booked as NCO, i.e. non-credit obligation. Apart from a few odd cases (e.g. VW

Bank which obviously has many cars…) the 7 banks which have the largest share of RWA in

NCO are all Spanish, as shown below.

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

CY

16

CY

17

CY

18

CY

19

ES4

3

ES4

4

ES4

5

ES4

6

ES4

7

ES4

8

ES4

9

ES5

0

ES5

1

ES5

2

ES5

3

ES5

4

ES5

5

ES5

6

GR

71

GR

72

GR

73

GR

74

IE76

IE77

IE78

IE79

IT80

IT81

IT82

IT83

IT84

IT85

IT86

IT87

IT88

IT89

IT90

IT91

IT92

IT93

IT94

PT

113

PT

114

PT

115

PT

116

PT

117

PT

118

NPE provisioning shortfall as % RWA

14/06/2017

9

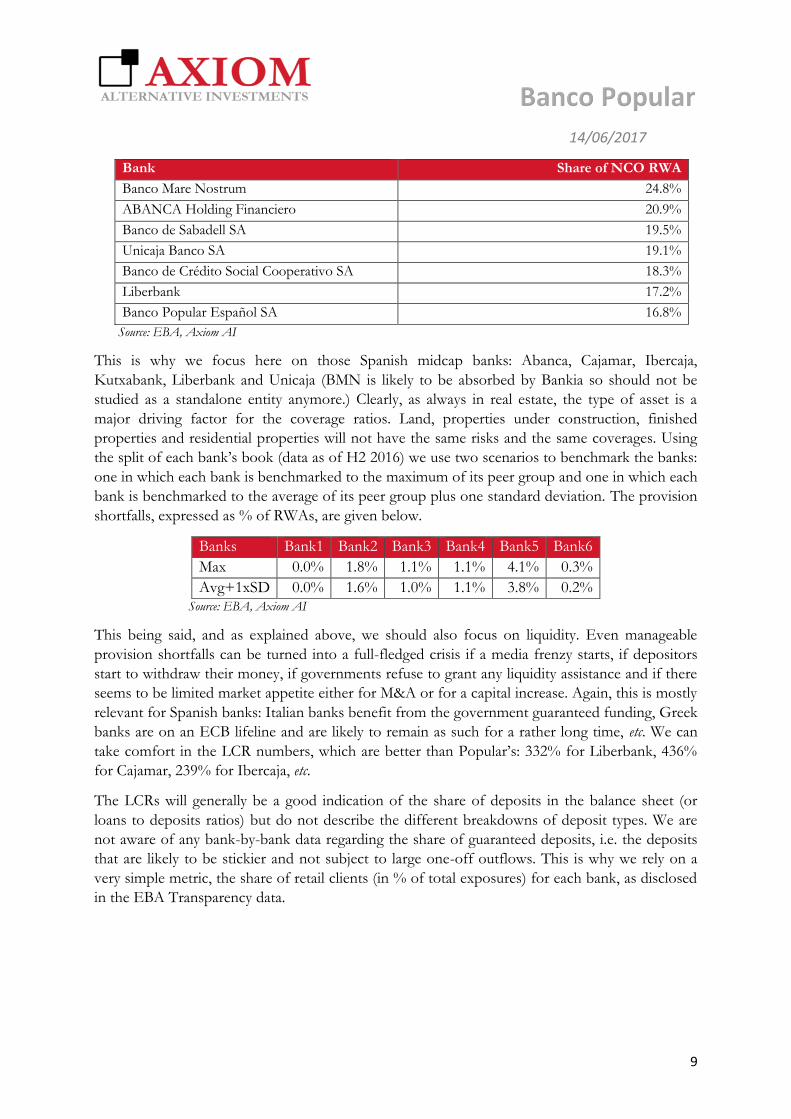

Bank Share of NCO RWA

Banco Mare Nostrum 24.8%

ABANCA Holding Financiero 20.9%

Banco de Sabadell SA 19.5%

Unicaja Banco SA 19.1%

Banco de Crédito Social Cooperativo SA 18.3%

Liberbank 17.2%

Banco Popular Español SA 16.8%

Source: EBA, Axiom AI

This is why we focus here on those Spanish midcap banks: Abanca, Cajamar, Ibercaja,

Kutxabank, Liberbank and Unicaja (BMN is likely to be absorbed by Bankia so should not be

studied as a standalone entity anymore.) Clearly, as always in real estate, the type of asset is a

major driving factor for the coverage ratios. Land, properties under construction, finished

properties and residential properties will not have the same risks and the same coverages. Using

the split of each bank’s book (data as of H2 2016) we use two scenarios to benchmark the banks:

one in which each bank is benchmarked to the maximum of its peer group and one in which each

bank is benchmarked to the average of its peer group plus one standard deviation. The provision

shortfalls, expressed as % of RWAs, are given below.

Banks Bank1 Bank2 Bank3 Bank4 Bank5 Bank6

Max 0.0% 1.8% 1.1% 1.1% 4.1% 0.3%

Avg+1xSD 0.0% 1.6% 1.0% 1.1% 3.8% 0.2% Source: EBA, Axiom AI

This being said, and as explained above, we should also focus on liquidity. Even manageable

provision shortfalls can be turned into a full-fledged crisis if a media frenzy starts, if depositors

start to withdraw their money, if governments refuse to grant any liquidity assistance and if there

seems to be limited market appetite either for M&A or for a capital increase. Again, this is mostly

relevant for Spanish banks: Italian banks benefit from the government guaranteed funding, Greek

banks are on an ECB lifeline and are likely to remain as such for a rather long time, etc. We can

take comfort in the LCR numbers, which are better than Popular’s: 332% for Liberbank, 436%

for Cajamar, 239% for Ibercaja, etc.

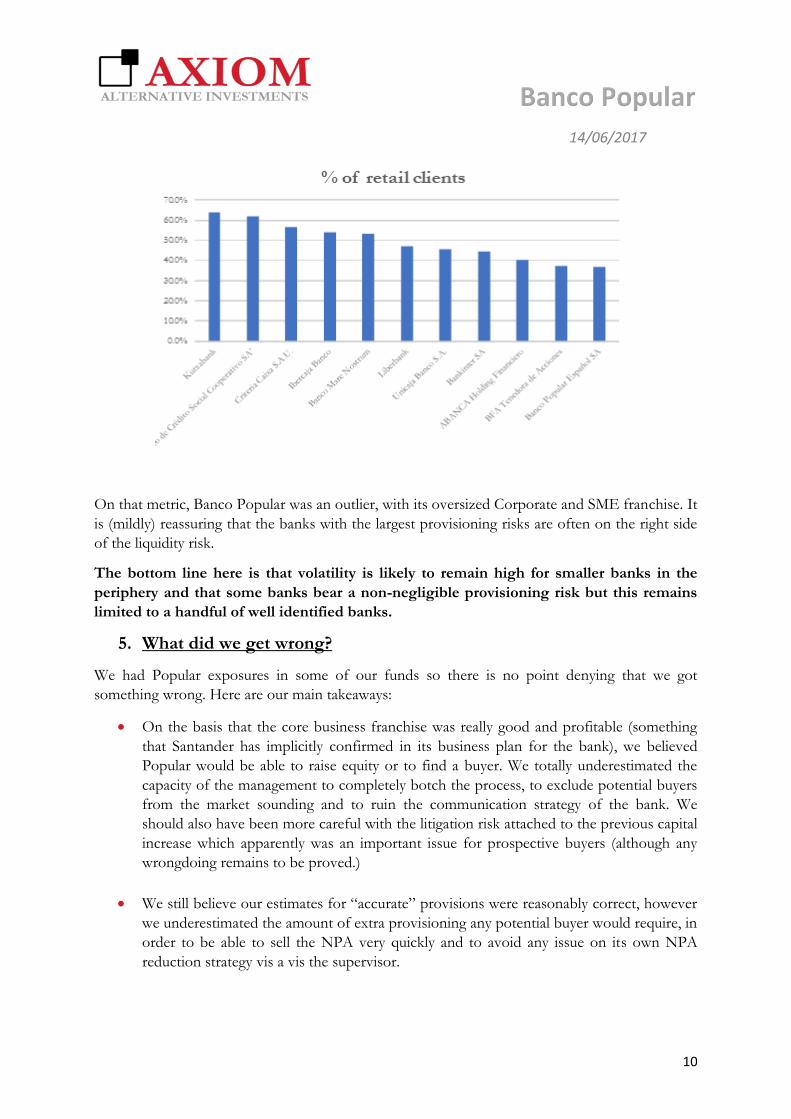

The LCRs will generally be a good indication of the share of deposits in the balance sheet (or

loans to deposits ratios) but do not describe the different breakdowns of deposit types. We are

not aware of any bank-by-bank data regarding the share of guaranteed deposits, i.e. the deposits

that are likely to be stickier and not subject to large one-off outflows. This is why we rely on a

very simple metric, the share of retail clients (in % of total exposures) for each bank, as disclosed

in the EBA Transparency data.

14/06/2017

10

On that metric, Banco Popular was an outlier, with its oversized Corporate and SME franchise. It

is (mildly) reassuring that the banks with the largest provisioning risks are often on the right side

of the liquidity risk.

The bottom line here is that volatility is likely to remain high for smaller banks in the

periphery and that some banks bear a non-negligible provisioning risk but this remains

limited to a handful of well identified banks.

5. What did we get wrong?

We had Popular exposures in some of our funds so there is no point denying that we got

something wrong. Here are our main takeaways:

On the basis that the core business franchise was really good and profitable (something

that Santander has implicitly confirmed in its business plan for the bank), we believed

Popular would be able to raise equity or to find a buyer. We totally underestimated the

capacity of the management to completely botch the process, to exclude potential buyers

from the market sounding and to ruin the communication strategy of the bank. We

should also have been more careful with the litigation risk attached to the previous capital

increase which apparently was an important issue for prospective buyers (although any

wrongdoing remains to be proved.)

We still believe our estimates for “accurate” provisions were reasonably correct, however

we underestimated the amount of extra provisioning any potential buyer would require, in

order to be able to sell the NPA very quickly and to avoid any issue on its own NPA

reduction strategy vis a vis the supervisor.

14/06/2017

11

We underestimated the capacity of Santander, or of any buyer in a resolution, to negotiate

a very strong position, with barely any competitor, in a peculiar auction process.

Paradoxically, it might be more interesting to invest in more distressed banks where no

buyer is available than in less distressed banks where a buyer could show up and take the

whole bank for 1€!

We clearly underestimated the liquidity risk and relied too much on previous situations

where deposits remained fairly sticky (underestimating the large deposit risk) and where

both central banks and governments were ready to facility a change in strategy and capital

raising initiatives with temporary liquidity facilities.

Last but not least, we underestimated the political risk. We were aware that the chances of

a capital injection were very low (“precautionary recapitalisation”), if not zero, because of

the toxic memories of past bailouts in Spain, but also because the government has no

stable majority in Parliament, but we did not realize that this would extend to any kind of

liquidity assistance. On the contrary, press reports, if they are confirmed, point to the fact

that public entities were quick to dry up any liquidity granted to Popular. It is likely that

the solution found was very convenient to a lot of parties, including Spanish ones and

there was no political goodwill to protect bondholders.

6. What is our conclusion?

Our main conclusions are the following:

Post-Popular, the market is likely to refocus on the NPA overhang of some banks, be it

because of their possible future capital needs or because media speculation could lead to

stock market woes and liquidity runs. Based on our in-house analysis we will sharply

decrease our risk appetite for banks where such an overhang exists.

In the world of TLTRO and guaranteed bonds, the market had forgotten what liquidity

risk is about. We will increase the focus on this risk in our analysis, in particular on

deposits.

This crisis has confirmed our long-standing view: in bank credit, the probability of default

matters more than the loss given default. This confirms our sharp bias towards T1 vs.

Tier 2 or non-preferred seniors at current market level (for which we struggle to see any

investment rationale at current prices.) The current market pricing does not reflect this

(and we think it will take time to change) so we expect to continue with our current bias.

More than ever, political risk is an important part of bank risk. Strong jurisdictions (e.g.

France, Germany, Switzerland) continue to offer better protection. In weaker

jurisdictions, the appetite of the government to offer support (recapitalization or liquidity)

remains a key issue, despite all the talk about banking union, common supervision, etc.

14/06/2017

12

The definition of non-viability was voluntarily left discretionary in the BRRD and the

range of tools available to supervisory authorities is wide. On Popular, we think

resolution authorities applied their normal set of rules and policies, albeit in a very

unusual context. This demonstrates that it is crucial to consider all possible options and

outcomes and to avoid an important bias: that the next crisis will be similar to the

previous one.

As we think we have shown above, the case of Popular was quite extraordinary. If press

reports are to be trusted, it seems that public entities largely contributed to the liquidity

crisis and that the management of the bank handled the crisis extremely poorly. We trust

banks’ managements will learn from it and understand that decisive actions are needed

when confidence starts to erode. The way Unicredit handled its strategic turnaround is

probably the best blueprint one can find.