banco santander (brasil) · pdf filesource:anfavea top 10 on vehicles industry 4 new car sales...

TRANSCRIPT

Banco Santander (Brasil)

JP Morgan Field Trip

Mar, 2012.

Santander Financiamentos

Felix Cardamone

Head of Consumer Finance Brazil

Mar, 2012.

Agenda

I. Vehicles Market Overview

II. Santander Financiamentos

Loan Portfolio & Restructuring Plan

WebMotors

Risk Management

3

Source:ANFAVEA

Top 10 on Vehicles Industry

4

New Car Sales

China 12,668

USA 11,535

Japan 3,825

Germany 3,137

Brazil 3,096

India 2,567

France 2,406

Russia 2,402

United Kingdom 2,064

Italy 1,794

Vehicles Market

Source:ANFAVEA

2011

Millions

Sourcee: FENABRAVE/CETIP

Vehicles Sales (Units Sold - Million)

+17% +5%

+23%

Vehicles Market in Brazil 5

6

Vehicles Sales

Sourcee: FENABRAVE/CETIP

(Units - Thousand)

New Cars

-23%

0%

Used Cars

Motorcycles

-20%

-2%

-20%

+1%

Agenda

I. Vehicles Market Overview

II. Santander Financiamentos

Loan Portfolio & Restructuring Plan

WebMotors

Risk Management

7

29,1 29,8 30,2 30,8 32,7

35,6

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

Consumer Finance - Breakdown Dec/11

Total Loan Portfolio – Consumer Finance

22.4%

8.8%

R$ billion

Part. (%) – Consumer Finance / Total Loans

Santander Loan Portfolio – Consumer Finance (BR GAAP)

Vehicles & Motorcycles

Trucks

Consumer Credit

18%

82%

Santander

Financiamentos

Source: CFO Financeira (dec/11).

BR GAP: 100% Renault Portfolio

8

Integration of Banco Real and Santander:

Aymoré+Olé =

2008 2009 2010 2011

Restructuring Plan

Aymoré +

competitive

End of the restructuring process

and launch of new brand

Focus on

Profitability

Evolution of Management

Market Share Growth with Profitability

Strategic Pillars

Commercial structure focused on high productivity

Automatic credit analysis response

Redirection of collection to the Bank Risks

Products portfolio and operational processes review, operations and collected vehicles management

Commercial Strategy

Risk Management

Products & Operations

New management model and creation of committees to manage the business

Institucional

Restructuring Plan 9

10

10

Source: - Brazil Central Bank

- Competition: Investors Relationship sites

Loans Portfolio Market Share – Individuals (BR GAAP)

Santander: 100% Renault and Branches Channel

Bank 1

Bank 2

Bank 3

Agenda

I. Vehicles Market Overview

II. Santander Financiamentos

Loan Portfolio & Restructuring Plan

WebMotors

Risk Management

11

Magazines “Quatro Rodas” and “Exame”

www.webmotors.com.br

Website Leader at Brazilian Internet Automotive Sector:

– More than 4 thousand dealers with active packs and, at least, one classified ad published in a month

– 13 million unique visitors per month

“93% of Brazilian research online before buying a car”

12

Top of mind

First Choice

Usage

Source: WebMotors BI and 2010 Research

Santander Financiamentos – Internet Business

Source: WebMotors.

Unique visitors per month New and used car dealers as client

8

13

Jan/10 Dec/11 Jan/10 Dec/11

4.208

2.683

Active auto adds

Jan/10 Dec/11

159

108

13 WebMotors.com.br

(# Millions) (#)

(# Thousand)

Agenda

I. Vehicles Market Overview

II. Santander Financiamentos

Loan Portfolio & Restructuring Plan

WebMotors

Risk Management

14

15

Santander presents growth but

below market

Reference: Febraban

Não inclui canal interno.

Santander inclui Renault 100%, demais Instituições contemplam (Banco Ford, Banco Fiat).

15

Over 90 dpd - Santander vrs Market

Over 30 - mob 3

Vintages Evolution – Santander

New Admission Policy

The new admission process

generates vintages with better

quality

Auto Loan Business – Delinquency Rates

Market (Bacen) Santander Financiamentos

nov/11 dec/11 jan/12

Decreasing the Cost of Credit (%)

2009 2010 1S11 2S11

Increase of almost 40% of the

commercial staff

The improve of credit response time and

automatic decision, impacted positively

the dealer’s satisfaction…

… Even with more conservative Credit

Policy

16 Portfolio Growth with good quality

Reference: Pesquisa anual IBOPE de satisfação intermediário.

Santander Brasil Santander Cards Business

March, 2012

18 18

Agenda

Overview of Brazilian Cards Industry

Santander Cards Issuer

Santander Cards Acquirer

19 Overview of Brazilian Cards Industry Cards industry continues to show substantial growth rates, even considering the competitive scenario consolidation and recent regulation changes

Source: BACEN.

Transactions, # Billion

Transactiosn Growth

Check

Debit

# Cards/Active Economic Population

Cards Penetration Growth

2005 2006 2007 2008 2009 2010

+11%

CAGR

+ 21%

- 10%

+ 17%

Credito

CAGR

Cards transactions have been strongly replacing checks transactions last 10 years

CAGR

6,315,93

5,514,93

4,283,75

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2005 2006 2007 2008 2009 2010

20

97 118 147 173 196 225 247171 187

201217

233249

266

6882

104124

136153

173

336

2005

388

2006

453

2007

628

2010

686

514

2008

565

2009

Credit

Debit

P. Label

+13%

2011

Evolución de la Industria de Meios de Pago en Brasil La industria ha logrado ritmos intensivos de crecimiento desde 2005, tanto en

base de tarjetas cuanto en facturación

67 83 107 129 158197

115142

174215

256

309

386

60 68 8529 36

2009

535

2010

56

200

2005

245

2006

45

302

2008

375

53

2007

444

2011

Credit

Debit

P.Label

+22%

668 R$, Billones

CAGR CAGR

Source: ABECS – Associação Brasileira de Cartões – 2011: Estimated values

# Millones

Number of Cards Total Revenues (R$ Bi)

Card penetration, average ticket and transactions per card are still low in Brazil

Overview of Brazilian Cards Industry

53 53 52 54 57

45 48 51 53 56 58

93 98 100 107 113

5250

46

9186

+4%

P. Label

181

2005

189

2006

194

2007

201

2008

206

2009

216

2010

228

2011

Credit

Debit

Average Ticket (R$, Transaction)

21 21

Agenda

Overview of Brazilian Cards Industry

Santander Cards Issuer

Santander Cards Acquirer

22

Product focus

Specialized

capabilities: risk,

marketing

Direct channels:

Telemkt / Mailings

Specialized

systems

Customers

Traditional

Channels: branches/

agents, call-center,

web pages

Brand

Economies of scale

Cards Specialist Retail Bank

Santander Cards Issuer – our approach Our approach continues to be the world’s best integrated cards specialist within a retail bank (since 2002)…

… Contributing to improve our local banks’ performance

23 Santander Cards Issuer – our model Is based on managing all levers along the product lifecycle …

Activation Retention Balance Building Spending

Portfolio Management

Acquisition

RISK MANAGEMENT

Dep

th o

f card

ho

lder

rela

tio

nsh

ip

VALUE

CHURN

TIME

SERVICING TECHNOLOGY ANALYTICS MULTI-CHANNEL

24

Knowledge Ca

rd

Ca

rd

s

Homogeneous Business Model

Common methodologies

Similar organizational structures

across countries

True best practices sharing

Global specialists and knowledge

initiatives (Forums, Campaigns

Library, Benchmarking, etc.)

Scale Economies

Talent Management: global

opportunities, specialist trainings

Global relationships with key industry

players (Amex, Visa, MasterCard,

Diners)

Global Products and Alliances

(Elavon, FDI, Ferrari, etc.)

Value added to the Group

Santander Cards Issuer – our model …in a absolutely integrated global business model metlhodoly….

25

(1) Source: Internal data

Increase the

profitability by using

the card’s platforms as

a distribution channel

for other banking

products and services

Continuous product

innovation as a growth

lever

Payment Services

Savings

Personal Loan

Insurance

Santander Cards Issuer – our model The Business expansion will be held in two dimensions: Customer Base and Profitability per Account

2010 2011

2010

2011

20%

12%

Net in

co

me

Card Accounts

Δ P

rofita

bili

ty p

er

Acco

un

t

26 Santander Cards Issuer – continuous growth The Credit market continues to show substantial growth rates, even considering the competitive scenario consolidation and recent regulation changes

Total Spend (R$ Bi)

Cards (MM)

Revolving Balance (R$ Bi)

Key Observations

Focus on increase credit card

penetration in client base with

new commercial agreements

(Raizen / Telefonica).

Growth of the customer

relationship stimulate Spend

Financial orientation to

revolving – offering financing

credit card bills (lower rate,

but with longer term)

Market

Note 1: Source Banco Central do Brasil, including +360 days balance

Note 2: Source ABECs – Brazilian Cards Association

173,0153,0

136,0124,0104,0

12,411,59,78,56,8

07 11 10 08 09

364,3313,7

256,0215,0

174,0

50,939,933,326,518,8

11 10 09 08 07

35,729,225,7

22,117,2

4,33,02,52,11,7

07 08 09 10 11

+19%

+14%

+16

+20%

+28%

+20%

+25%

Santander

7%

14%

12%

27 Santander Cards Issuer –performance … generating relevant revenue increase

Net Fee (R$ MM)

1.298

969

785

2011

+34%

2010 2009

+29%

19%

Source: Santander Income Statement – Net Fees IFRS

CAGR

28 28

Agenda

Overview of Brazilian Cards Industry

Santander Cards Issuer

Santander Cards Acquirer

29 Merchant Acquiring - Market Potential

» More than 2 million

establishments » 22% annual

growth

» 50% of all trade

sales

» Large

profitability

margins

» R$ 560 billion in

sales in 2011; volume

is expected to double

in 5 years

» Duopoly until

April, 2010

30

REDECARD

AND

CIELO ACQUIRING

SERVICES

FINANCIAL

SERVICES

BANKS

The 1st bank to combine acquirer and

financial services

Merchant Acquiring - Innovative Value Proposition

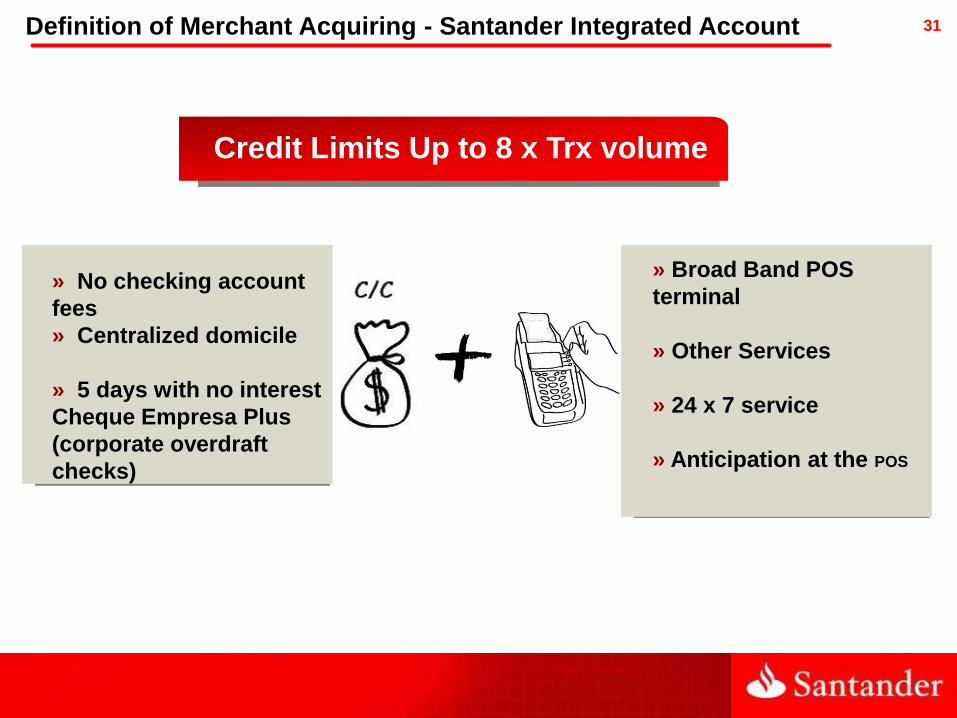

31 Definition of Merchant Acquiring - Santander Integrated Account

» No checking account

fees

» Centralized domicile

» 5 days with no interest

Cheque Empresa Plus

(corporate overdraft

checks)

» Broad Band POS

terminal

» Other Services

» 24 x 7 service

» Anticipation at the POS

Credit Limits Up to 8 x Trx volume

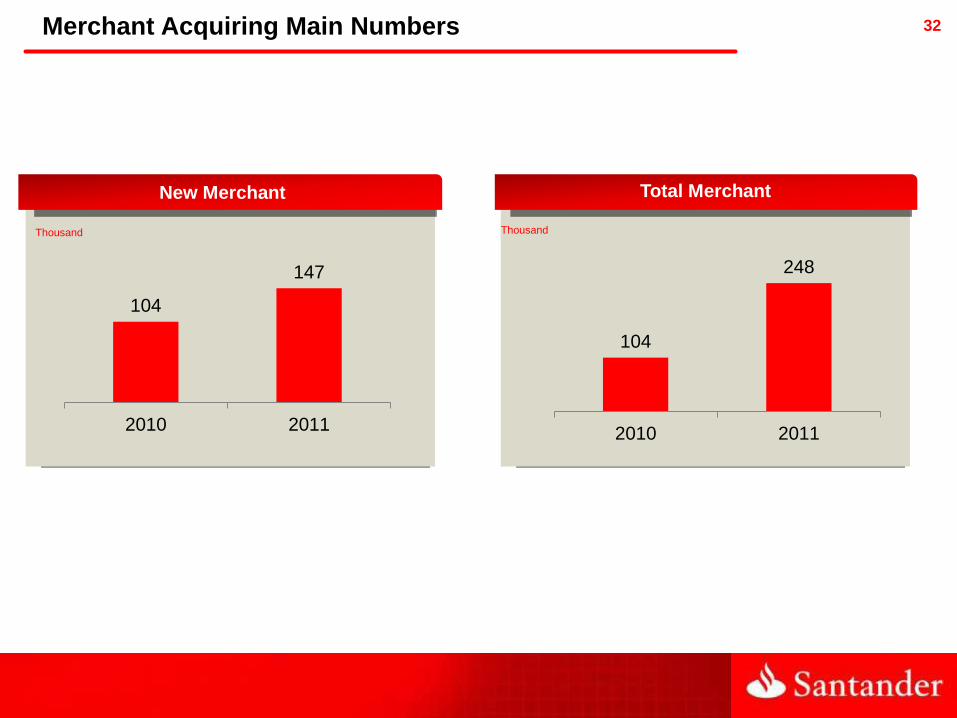

32

New Merchant Total Merchant

Merchant Acquiring Main Numbers

Thousand Thousand

104

147

2010 2011

104

248

2010 2011

33 Merchant Acquiring Revenue: marketing share

Market Share

55,8% 56,9% 56,3% 56,5% 57,0%

43,1% 41,8% 42,0% 41,4% 40,4%

1,0% 1,3% 1,7% 2,1% 2,6%

4Q10 1Q11 2Q11 3Q11 4Q11

ACQ 1 ACQ 2 Santander