banjo & matilda investor presentation

TRANSCRIPT

This presentation includes forward-looking statements. Forward-looking statements reflect our current views with respect to, among other things, future events and performance. All statements other than statements of historical facts, including statements regarding our future operating results and financial position, business strategy, and plans and objectives of management for future operations, are forward-looking statements. In many cases, you can identify forward-looking statements by words such as “anticipate,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “project,” “plan,” “potential,” “predict,” “target,” “believe,” “seek,” “continue,” “outlook,” “may,” “might,” “will,” “should,” “can have,” “likely” or the negative version of these words or comparable words. Forward-looking statements speak only as of the date on which they are made and are based on beliefs and assumptions made by management using currently available information.

These statements are only predictions and are not guarantees of future performance, results, actions or events. The issuer expressly disclaims any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

All written and oral forward-looking statements attributable to the Company, or persons acting on are its behalf, expressly qualified in their entirety by the cautionary statements in the preliminary prospectus, including, without limit, those described under the heading “risk factors”, as well as other cautionary statements that are made from time to time in the Company’s public communications. You should evaluate all forward-looking statements made in this presentation in the context of these risks and uncertainties.

This presentation contains certain information that has not been derived in accordance with generally accepted accounting principles (“GAAP”). Reconciliations of such information to the most directly comparable information derived in accordance with GAAP are contained in this presentation. This information should not be considered a substitute for any measures derived in accordance with GAAP.

Disclaimer | Forward Looking Statements

2

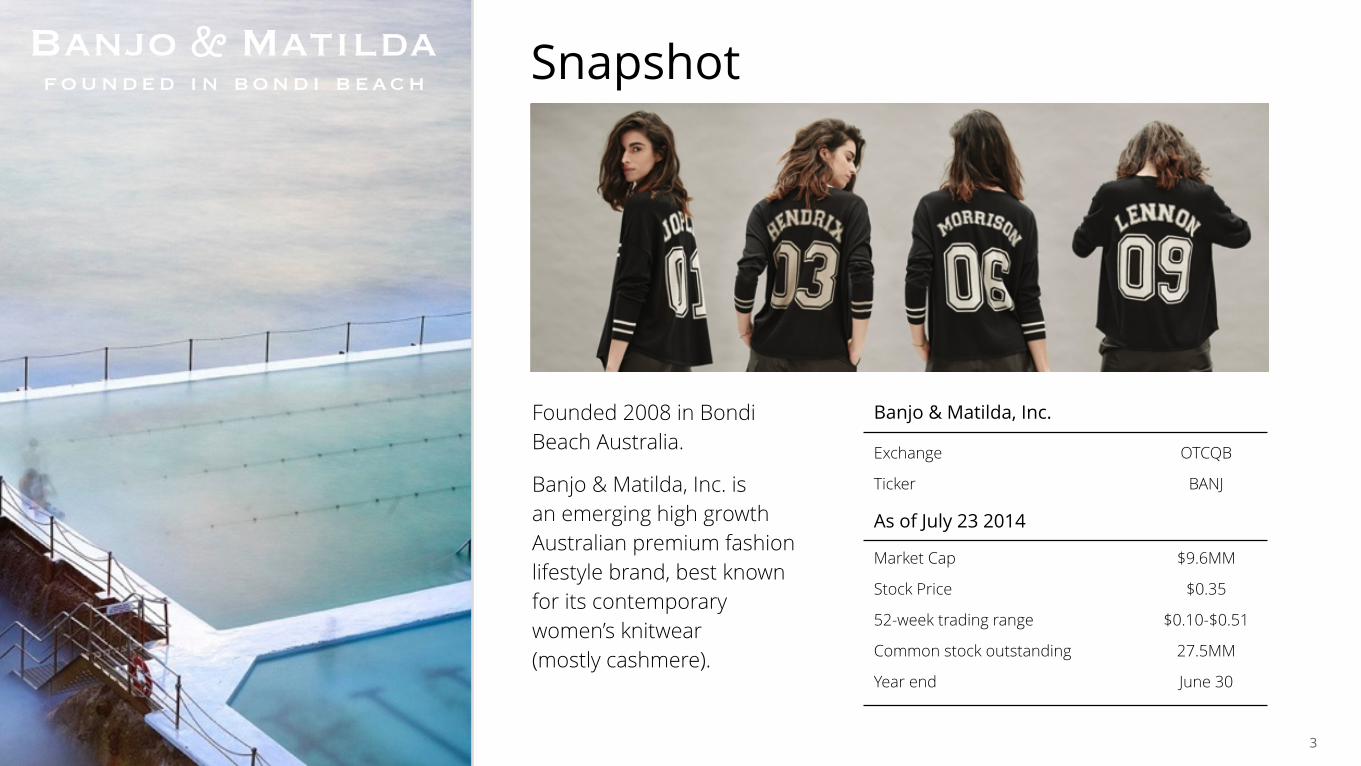

Snapshot

Founded 2008 in Bondi Beach Australia.

Banjo & Matilda, Inc. isan emerging high growth Australian premium fashion lifestyle brand, best known for its contemporary women’s knitwear (mostly cashmere).

Banjo & Matilda, Inc.

Exchange OTCQB

Ticker BANJ

As of July 23 2014

Market Cap $9.6MM

Stock Price $0.35

52-week trading range $0.10-$0.51

Common stock outstanding 27.5MM

Year end June 30

3

Distribution / Where to Buy

Yesterday

Premium contemporary cashmere knitwear collection.

!4 styles - solely women’s sweaters.

Today Tomorrow

4

2008 2014 2015 & beyond

Brand

Brand taking off - media support, celebrity endorsements, & industry jumping on board.

40+ styles per season

Full lifestyle product offering with unique brand position and offer

!Valuable lifestyle brand

Online retail only. Stocked in 100+ retail outlets around the world.

Key retailers including:Net-a-porter, Harvey Nichols, Neiman Marcus, Anthropologie ShopBop, Intermix, Beyman, Revolve, David Jones.

Current growth path will see retail outlets stocking the brand continue to grow quickly and sales continue to double.

!Target 1,000+ outlets

Results

Year 1 - $80k revenue. FY 14’ June 30 Revenue circa $2.5MM.

Online Retail sales keeping pace with Wholesale sales.

Sales more than doubling every 12 months.

FY 15’ June 30 Revenue $4MM+

Raising additional $5m to fast track growth through expanded ranges/ offering =open more doors and expand Revenue per Door.

Liquidity in BANJ public co.

Belynda MacphersonCo-founder & Creative Director

Belynda’s love of knitwear began at an earlyage and continued throughout a successful career in public relations.

Tight knit management team

Ben MacphersonCo-founder & CEO

Ben has started 5 businesses, successfully developing and exiting with 3 of the 5being sold and one resulting in IPO.

Neil LivingstonExternal Chief Financial Officer

Neil is a career finance professional with broad experience in both Financial Services & Fashion for public and private companies.

5

Global Apparel Retail IndustryValue Forecast 2009 - 2014*

Industry opportunity

6* Source: companiesandmarkets.com, Global Apparel Industry - http://www.companiesandmarkets.com/MarketInsight/Textiles-and-Clothing/Global-Apparel-Industry/NI7468

1000

1100

1200

2009 2010 2011 2012 2013 2014

$ Billion

% Growth2.22.5

2.6

2.5

2.3

2.0

Stable single digit growthLow competition entry point to

broader $1.2T market

Womenswear $621

2014 Global Market Segments Apparel Industry*

$ Billion

12% year over year increase

Menswear $40215% increase over 5 year span

Childrenswear $186

Knitwear $20

New luxury sweet spot

New Luxury products are sold at much higher prices than conventional goods and in much higher volumes than Old Luxury goods,

the result is a transformation of the entire category.“ “

Boston Consulting Group

7

Luxury

PremiumFashion

dream

seduction realism

Social imitation & instant

Social elevation & timelessness

Quality / price ratio, investment & performance

Priceless gift

In with the fast crowd…

Lora Piana Hermes Chanel YSL Bally

Gucci Prada Chloe Lanvin Louboutin

ACNE Isabel Marrant Rag & Bone Vince !Equipment Zadig & Voltaire Stella McCartney Chintia & Parker

H&M ZARA J.Crew Mango Top Shop

8

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

December 2008 2009 2010 2011 2012 2013 2014

May 2008Brand & first collection launched Bondi Beach Australia - online only

Banjo & Matilda timeline

Operating Profit(169,400) (280,571) (130,176) (171,287) (18,227) 212,451

Revenue

Doors

Celebrity collaboration program commenced

Wholesale program commenced

Sweater Exchange launched

First retail store opens

Net-a-porter secured. Re-orders within 3 weeks.

GOOP / Gwyneth Paltrow collaboration goes global

$1MM Equity Convertible

APO listing on OTCBB: BANJ

Additional US & UK retailers begin to stock B&M

US based Debtor finance secured

First collection launched - 4 styles

8

1 1 11

18

149,462

200+

200 Doors confirmed Oct 14

$ 000‘s per door82 135 684 836 155 114 26

9

2012 Brand Begins to Take Off

!!+

Own Retail (DTC) (Margin % Expansion)

x Offering

(Revenue Per Door) !

Wholesale “Doors”

= A Global Lifestyle Brand !

10

Retailers jumping on board

USA Net-A-Porter ShopBop Revolve Intermix Neiman Marcus Anthropologie !!!UK Net-A-Porter Harvey Nichols

Germany KaDeWe

Hong Kong Net-a-porter

Australia David Jones

Middle East Boutique1

On radar of..

11

Media & Celebrities fuelling brand growth

12

!Wholesale “Doors”

+ !!x

Offering (Revenue Per Door)

!

Own Retail (DTC) (Margin % Expansion)

= A Global Lifestyle Brand !

13

Consumers diving in

DTC Onlinee-commerce

1 x Sydney Australia store

14

0

35,000

70,000

105,000

140,000

Q1 Q2 Q3 Q4 Q1 Q2

Sales

2013 2014

0

25,000

50,000

75,000

100,000

Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2008 2009 2010 2011 2012 2013 2014

Visitors

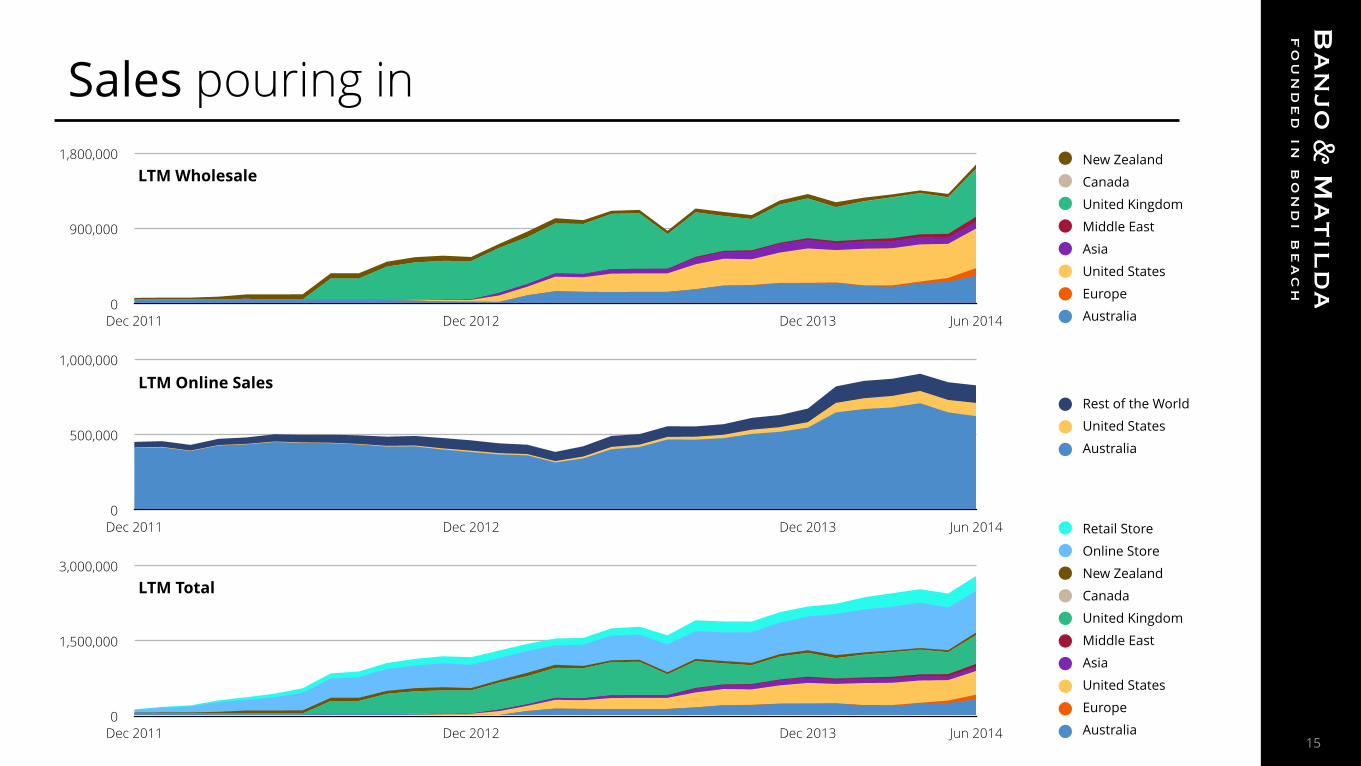

Sales pouring in

0

900,000

1,800,000

Dec 2011 Dec 2012 Dec 2013 Jun 2014

LTM WholesaleNew Zealand

Canada

United Kingdom

Middle East

Asia

United States

Europe

Australia

0

500,000

1,000,000

Dec 2011 Dec 2012 Dec 2013 Jun 2014

LTM Online SalesRest of the World

United States

Australia

0

1,500,000

3,000,000

Dec 2011 Dec 2012 Dec 2013 Jun 2014

LTM Total

Retail Store

Online Store

New Zealand

Canada

United Kingdom

Middle East

Asia

United States

Europe

Australia15

Offering (Revenue Per Door)

!Wholesale “Doors”

+ Own Retail (DTC)

(Margin % Expansion) x !!

= A Global Lifestyle Brand !

16

today

Global Australian Lifestyle

Brand

Simple growth plan

+ +

ExpandRanges

+ Aggressive online US

penetration

Major department

concession roll out +

Key flagship retail stores

Secure new key retailers

Wholesale “Doors” + Retail (DTC) Margin Expansion x Revenue/Offering per door

17

June 30 YE 2014 2015 2016 2017 2018

Revenue $m 2.6 6 11.2 21 37.9

Doors 96 214 310 505 725

Rev/Door$‘000 26 28 36 41 52

FinancialsSummary P&L (ending June 30)* FY12’ FY13’ 9 MONTHS TO MARCH 14’

New Wholesale Revenue $- 0% 147,793 8.3% 272,984 13.6%Existing Wholesale Revenue 269,784 29.3% 1,026,514 57.8% 818,951 42.5%Total Wholesale Revenue 269,784.13 29.3% 1,174,307.11 66.1% 1,091,934 56.1%Total Online Revenue 540,053.85 58.6% 446,286.09 25.1% 549,100 30.6%Total Retail Revenue 111,744 12.1% 154,650.53 8.7% 198,321 11.8%Total Revenue 921,581.98 1,775,243.73 1,839,356

Total Wholesale COGS 191,721 20.8% 727,243.69 41% 672,362 36.7%Total Online COGS (incl. Freight) 384,532.68 41.7% 153,893.5 8.7% 312,173 15.9%Total Retail COGS 79,564.7 8.6% 69,685.82 3.9% 143,491 7.1%Total COGS 655,818.38 71.2% 950,823.01 53.6% 1,128,026 59.7%

Total Wholesale GP 78,063.13 8.5% 447,063.42 25.2% 419,572 19.4%Total Online GP 155,521.17 16.9% 292,392.59 16.5% 236,927 14.7%Total Retail GP 32,179.3 3.5% 84,964.71 4.8% 54,831 4.8%Total GP 265,763.6 28.8% 824,420.72 46.4% 711,329 40.3%

Total Wholesale OPEX 49,270 5.3% 59,678 3.4% 53,919 2.8%Total Online OPEX 143,587 15.6% 89,487 5% 30,965 2.1%Total Retail OPEX 73,010 7.9% 130,385 7.3% 83,482 4.1%Total OPEX (exc. Corporate) 265,867 28.8% 279,550 15.7% 168,366 9%

Total Wholesale Contribution 28,793 3.1% 387,386 21.8% 365,653 16.6%Total Online Contribution 11,934 1.3% 202,906 11.4% 205,962 12.6%Total Retail Contribution (40,831) (4.4%) (45,420) (2.6%) (28,651) (0.6%)Total Contribution -104 0% 544,871 30.7% 542,964 29.4%

Corporate Overhead 184,904 20.1% 325,360 18.3% 594,478 31.3%

Total EBITDA -185,007 (20.1%) 219,511 12.4% -51,514 (0.1%) 18* All financials in AUD and based on Management Accounts. See relevant filings for US and public company results. Excludes financing/interest costs.

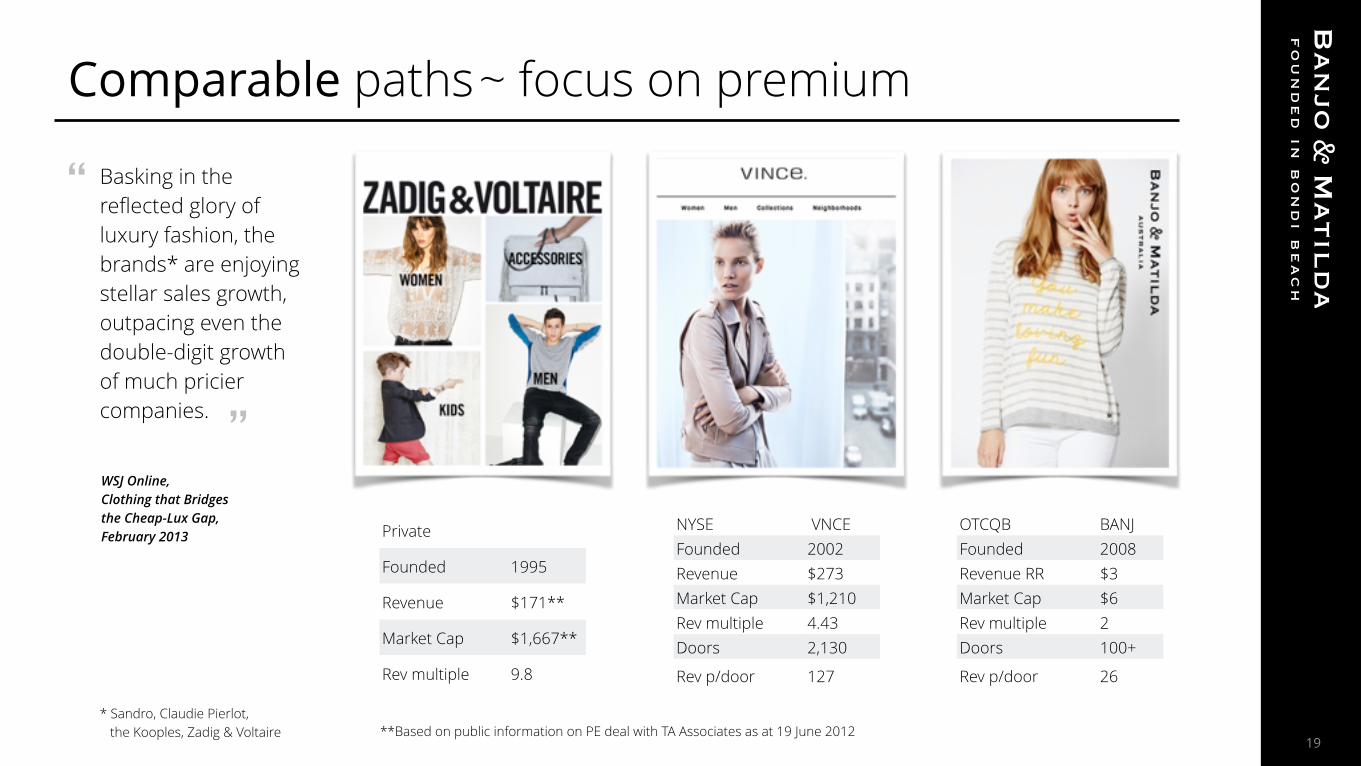

Basking in the reflected glory of luxury fashion, the brands* are enjoying stellar sales growth, outpacing even the double-digit growthof much pricier companies.

“

“

Comparable paths ~ focus on premium

**Based on public information on PE deal with TA Associates as at 19 June 201219

WSJ Online,Clothing that Bridges the Cheap-Lux Gap,February 2013

* Sandro, Claudie Pierlot, the Kooples, Zadig & Voltaire

NYSE VNCEFounded 2002Revenue $273Market Cap $1,210Rev multiple 4.43Doors 2,130

Rev p/door 127

Private

Founded 1995

Revenue $171**

Market Cap $1,667**

Rev multiple 9.8

OTCQB BANJFounded 2008Revenue RR $3Market Cap $6Rev multiple 2Doors 100+

Rev p/door 26

Market Cap *

EBITDA Margins CY 2014

EV / Sales CY 2014

EV / EBITDA CY 2014

Revenues (FY) 2014 * Growth %

Kate Spade & Co US 4,882 12.4% 4.77x NM 1,080 -15%

Vince Holding Corp US 1,342 21.6% 4.35x 20.2x 331 15%

Michael Kors Holdings Ltd Hong Kong 18,083 32.5% 4.30x 13.3x 3,311 -15%

Brunello Cucinelli Spa Italy 1,499 18.2% 3.16x 17.4x 4891 14%

Salvatore Ferragamo Spa Italy 4,778 21.3% 2.66x 12.5x 18,311 10%

Banjo & Matilda Aust/US 7 N/A 1.60x N/A 4 127%

Steven Madden Ltd US 2,186 16% 1.36x 8.5x 1,403 7%

Listed comparables

Low Mean High

12.4% 20.3% 32.5%

1.36x 3.85x 4.77x

12.5x 15.8x 20.2x

4 1,408 3,311

(15%) 20%

127%

* $ million 7 4,682

18,083

20

Investment highlights

21

Started as a Family Business - Growing into an Enterprise. Founded by husband & wife team of CEO, Ben Macpherson and Creative Director, Belynda Macpherson.

Growing Retail Presence. Operates fast growing e-commerce site and is stocked in major key retailers such as Net-a-porter, Harvey Nichols, Neiman Marcus, Anthropologie, ShopBop, Intermix, Beyman, Revolve and David Jones.

Rapid Financial Growth as Brand is Adopted. Reported sales of $86,000 for its first year (2008). Currently, on track to generateover $4 million in sales for FY 15’ ( June 30).

Clear Opportunity & Strategy for Continued Growth Comparable companies $1B+. Its been done before many times.

More wholesale Doors + Higher margin DTC x Full lifestyle product range= global lifestyle brand

Additional Information

At the Company

Ben Macpherson, Chief Executive Officer [email protected]

Aust. +61(0)413 836 633 /US (917) 683-7875

Investor Relations The Equity Group Inc.

Terry Downs, Associate Adam Prior, Senior Vice President [email protected] [email protected]

(212) 836-9615 (212) 836-9606

Market Street

Stan Abiassi, Managing member

[email protected] (281) 940-8889 !

22