bank performance analysis - resources.gabankers.comresources.gabankers.com/event agenda...

TRANSCRIPT

Bank Performance Analysis

The Business of Banking

© 2015 American Bankers Association

Objectives

Explain the ratios used in analyzing the performance of a commercial bank

Calculate the various performance ratios to evaluate the performance of a commercial bank

Recognize the historical experience of the commercial banking industry

Explain the various driver ratios used to explain bank management strategies

© 2015 American Bankers Association

Analyzing Performance

System that decomposes changes in ROA/ROE

Identifies drivers of profitability performance

Illustrates connection between drivers and final performance results

Useful at all levels of performance analysis

– Industry

– Bank

– Line of business

© 2015 American Bankers Association

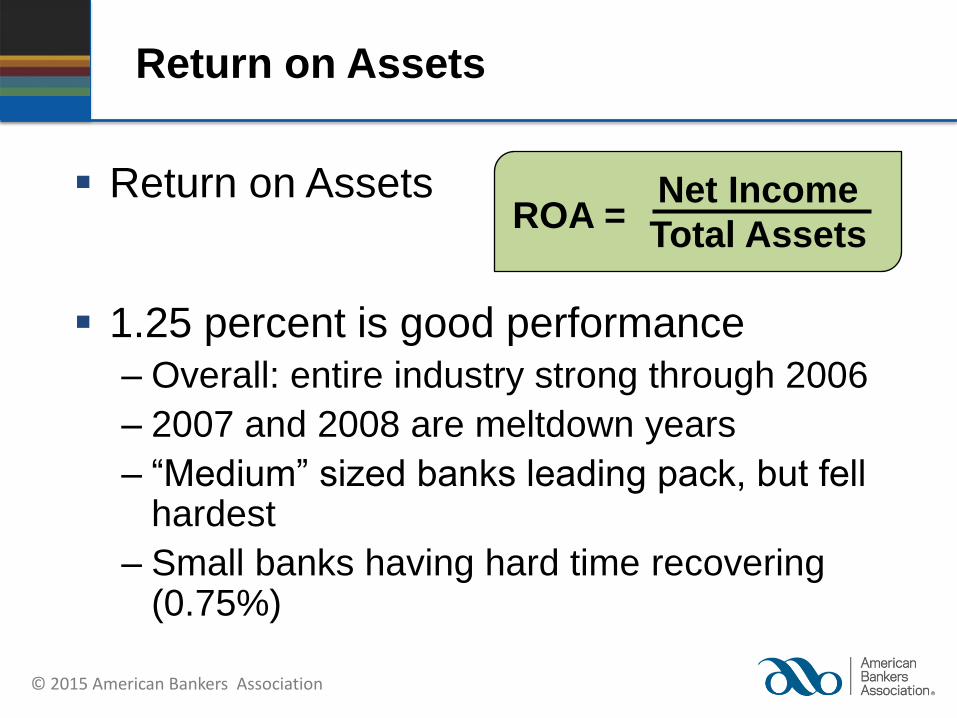

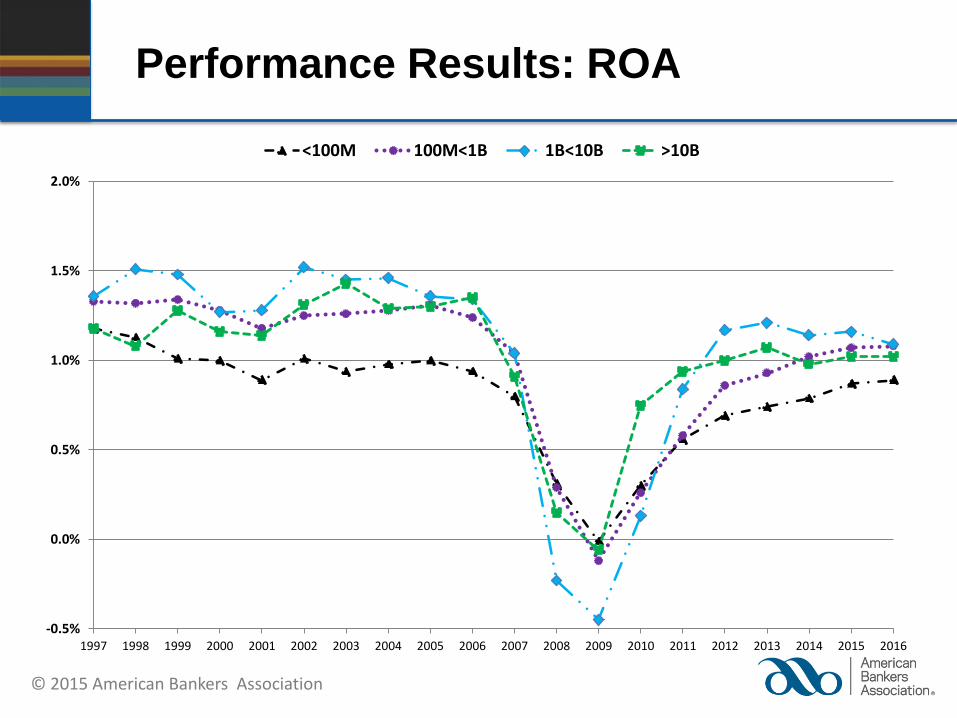

Return on Assets

Return on Assets

1.25 percent is good performance

– Overall: entire industry strong through 2006

– 2007 and 2008 are meltdown years

– “Medium” sized banks leading pack, but fell hardest

– Small banks having hard time recovering (0.75%)

ROA = Net Income

Total Assets

© 2015 American Bankers Association

Performance Results: ROA

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

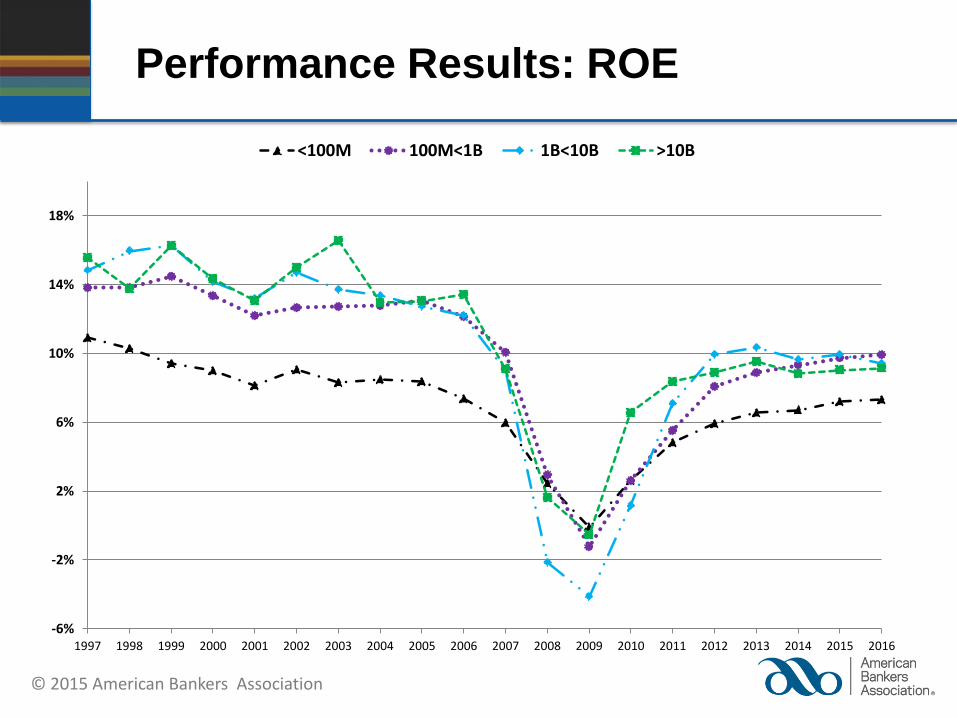

Return on Equity

Return on Equity

Large banks near top

Industry trend flat (to lower) before 2008

How can ROA trend upward and ROE trend flat to downward?

Negative for many banks in 2008

Small banks consistently lower

ROE = Net Income

Equity

© 2015 American Bankers Association

Performance Results: ROE

-6%

-2%

2%

6%

10%

14%

18%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

What Drives ROA and ROE?

Interest Rate Factors

– Yield on Earning Assets

– Cost Rate on Interest Bearing Liabilities

Quality of Assets

Operational Factors

– Non-Interest Income

– Non-Interest Expense

© 2015 American Bankers Association

Performance Driver Ratios

Yield on Earning Assets

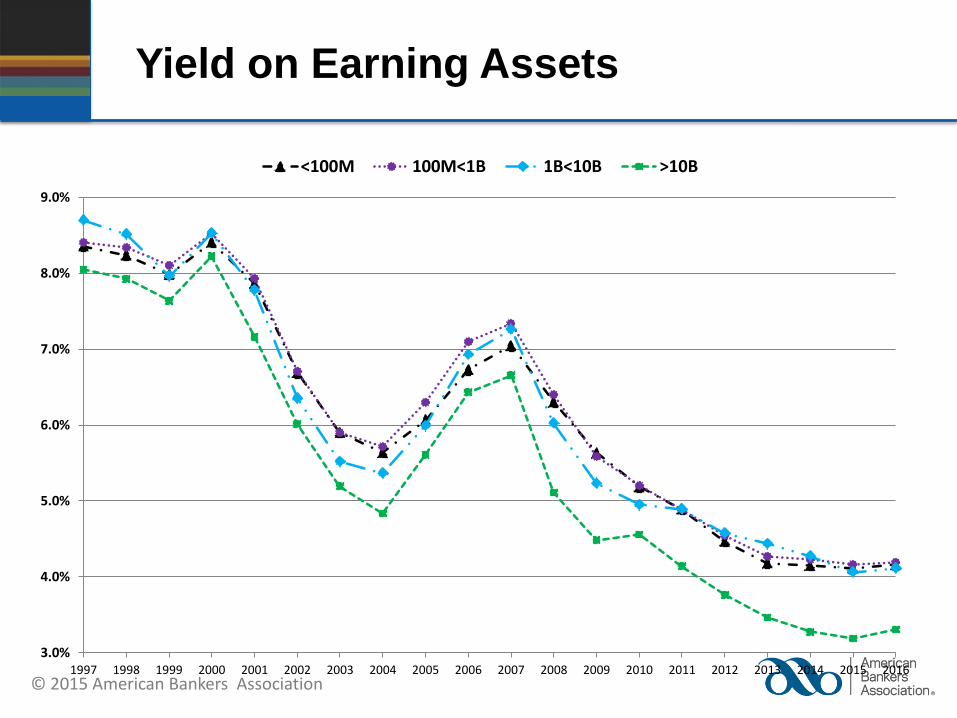

Most banks are tightly bunched together

Large banks are below industry

Smaller banks are leading industry

Note how yields move with changes in interest rates

Yield on Earning Assets = Total Interest Income

Earning Assets

© 2015 American Bankers Association

Yield on Earning Assets

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Driver Ratios

Cost Rate on Interest Bearing Liabilities

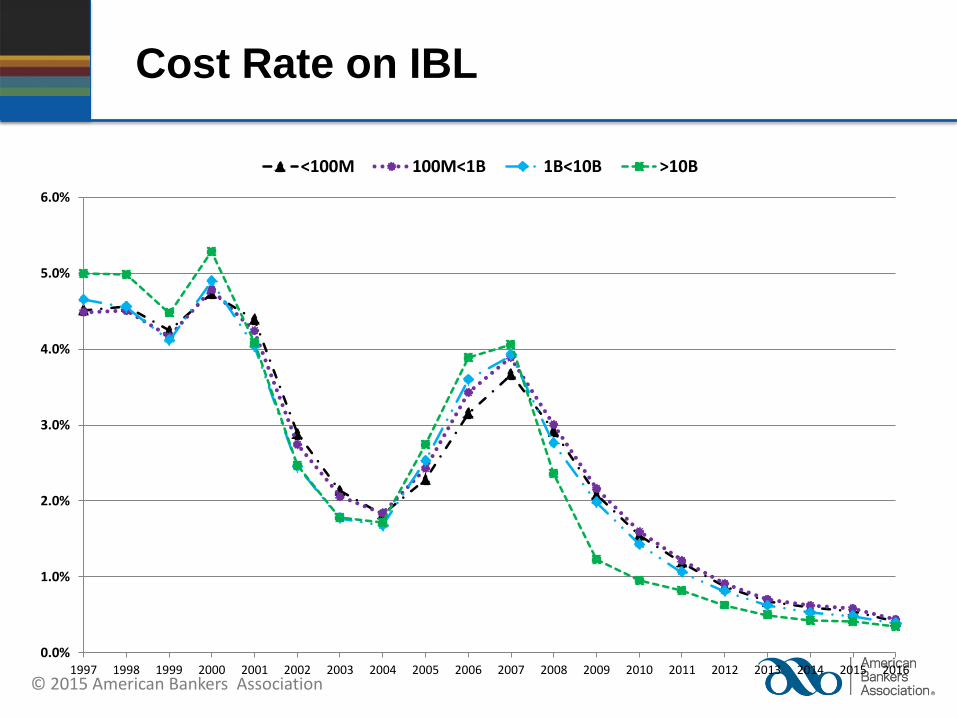

Large banks paid more in 90s

More purchased money, less core deposits

Negotiable CDs, Eurodollar CDs, Fed Funds

Other groups are now following suit

All banks are close together

Cost Rate on IBL = Total Interest Expense

Interest Bearing Liabilities

© 2015 American Bankers Association

Cost Rate on IBL

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

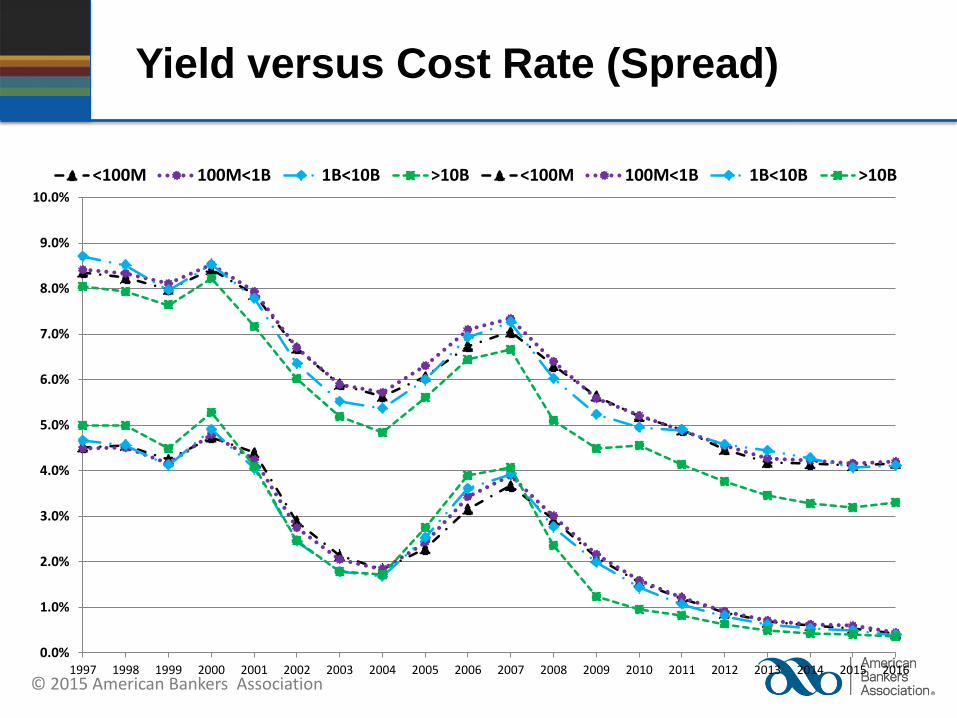

Yield versus Cost Rate (Spread)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B <100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Driver Ratios

Net Interest Margin

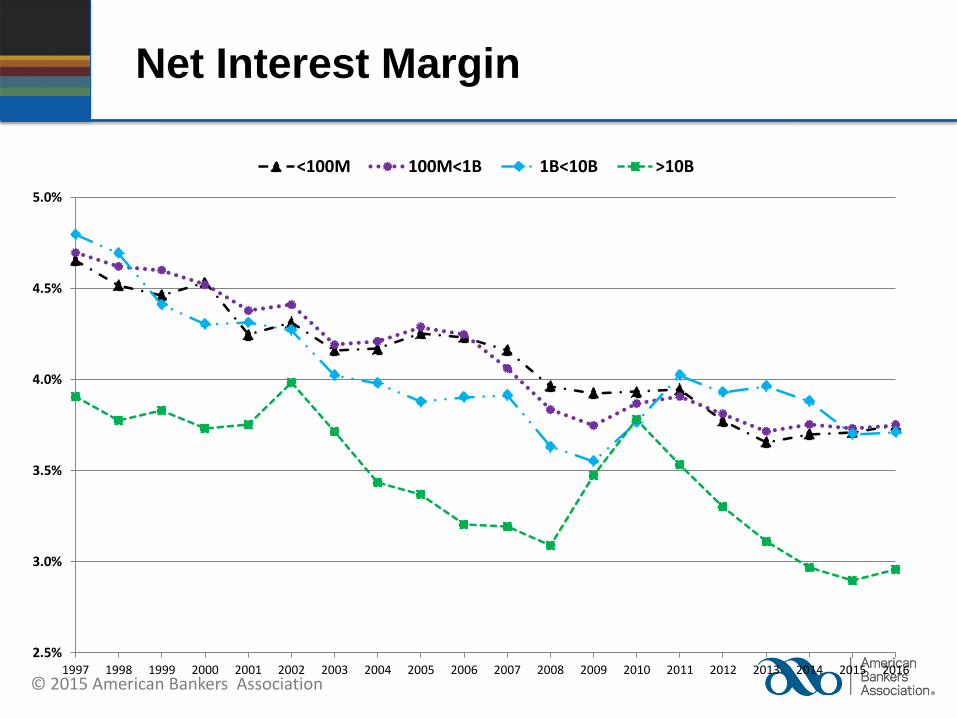

Large banks have lower Net Int. Margin

Lower yield on EA, higher cost rate on IBL

Very hard to grow and maintain high NIMs

Overall trend is downward

But no cataclysmic decrease in 2008

Net Interest Margin = Net Interest Income

Earning Assets

© 2015 American Bankers Association

Net Interest Margin

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Driver Ratios

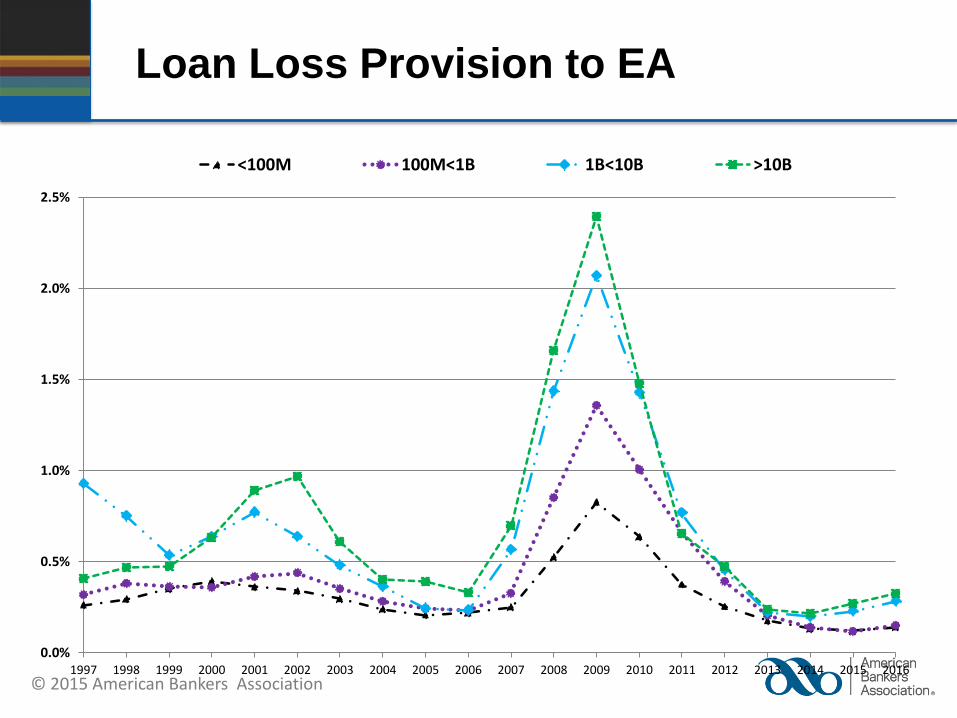

Loan Loss Provision to Earning Assets

Industry was very clean

Quality of loans, economic expansion

Until late 2006/early 2007

Early 2000’s Recession was short-lived

Many banks with negative provisioning in ‘04, ‘05, and ’06

Recession problems in 2007/2008

Loan Loss Provision to EA = Loan Loss Provision

Earning Assets

© 2015 American Bankers Association

Loan Loss Provision to EA

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Driver Ratios

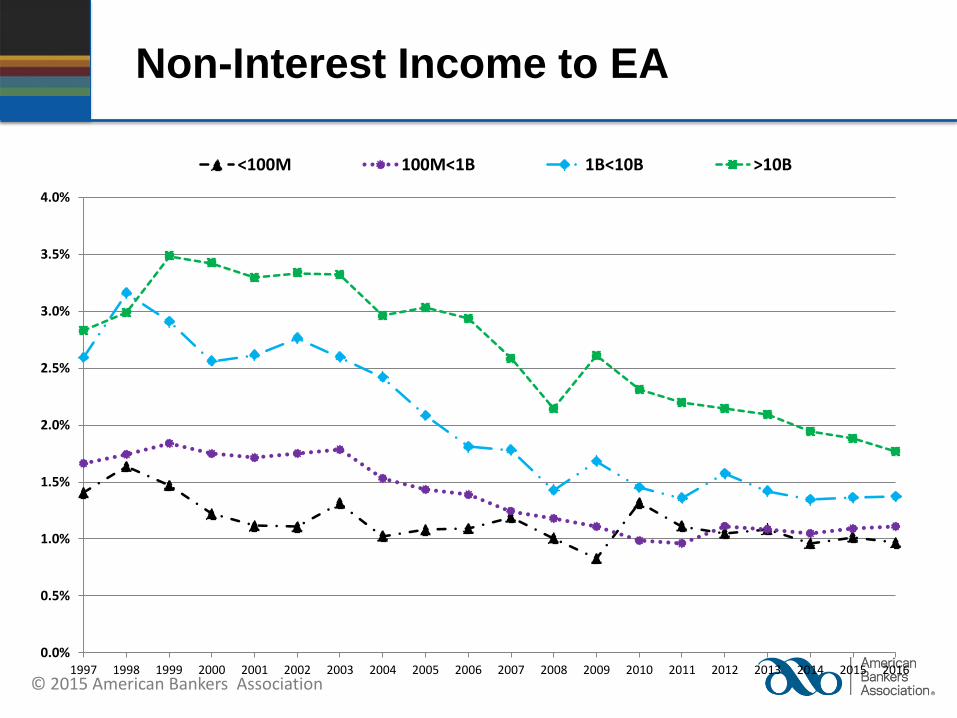

Non-Interest Income to EA

Steady increase in industry in 1990’s

Nondeposit fee income

Gains in trading income

But gains have not continued in 2000s

Non-Interest Income to EA = Non-Interest Income

Earning Assets

© 2015 American Bankers Association

Non-Interest Income to EA

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

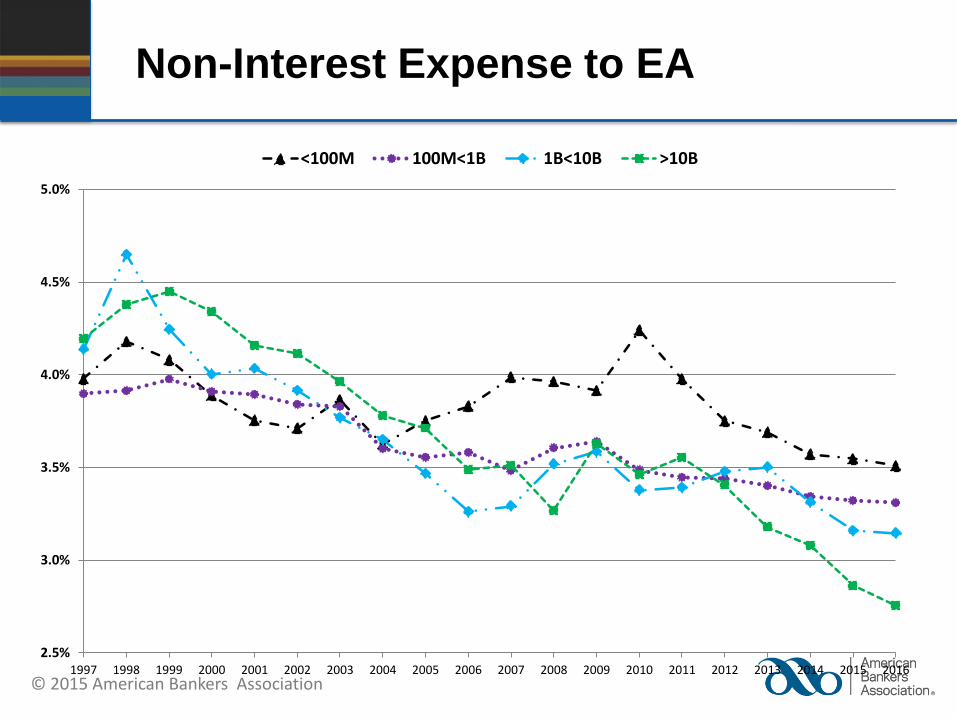

Performance Driver Ratios

Non-Interest Expense to EA

Industry has been stable, downward trend

Larger banks are lowest

Non-interest burden is decreasing

But gains are on expense side rather than income side—need to focus on revenue

Meltdown did not see dramatic effect

Non-Interest Expense to EA = Non-Interest Expense

Earning Assets

© 2015 American Bankers Association

Non-Interest Expense to EA

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

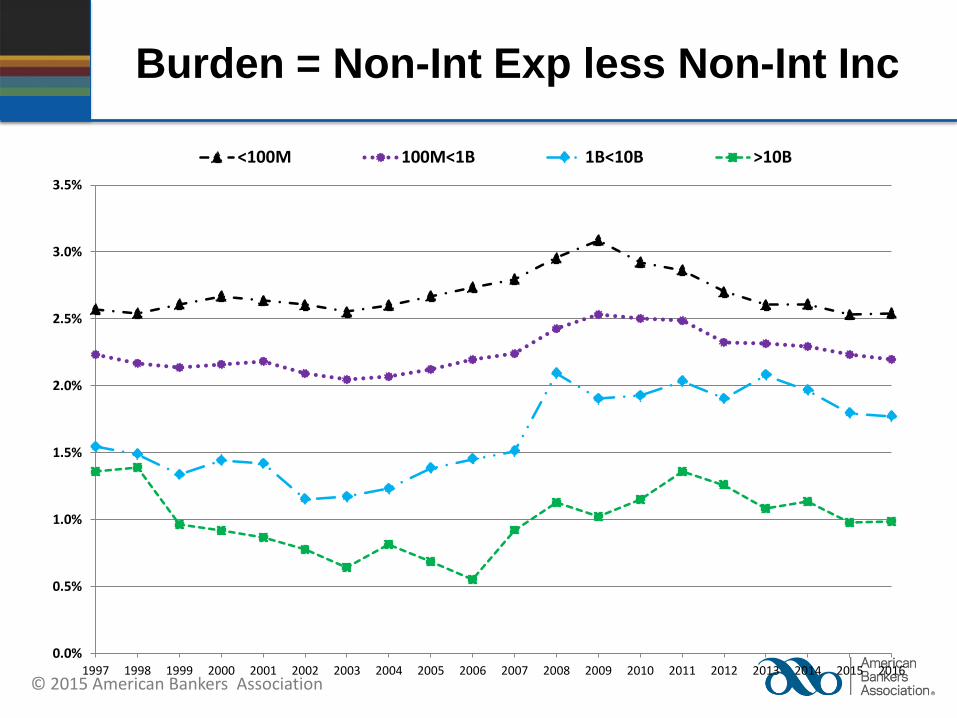

Burden = Non-Int Exp less Non-Int Inc

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Driver Ratios

Efficiency Ratio

Not a decomposition driver, but an important metric in managing bank efficiency.

Measures the cost of producing a dollar of revenue net of financing cost.

Meltdown sees big increase due to decreased revenue streams, but largest cut costs

Efficiency Ratio = Non-Interest Expense

Net Int Income + Non-Int Income

© 2015 American Bankers Association

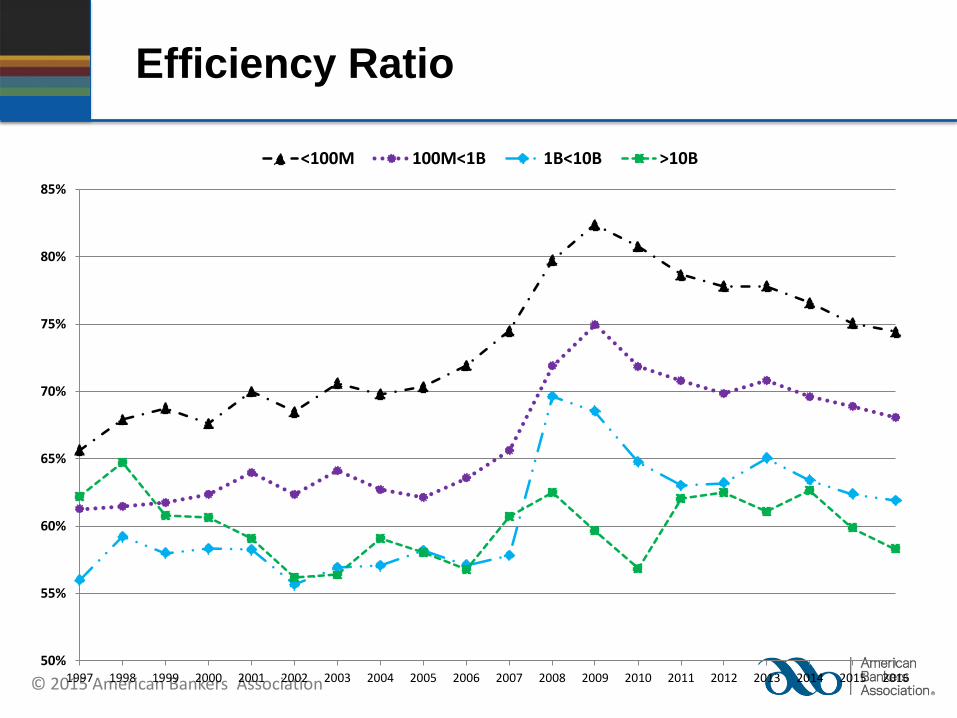

Efficiency Ratio

50%

55%

60%

65%

70%

75%

80%

85%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Gain/Loss on Asset Sales to EA

Gain/Loss on Asset Sales to EA

Can have a significant impact on

individual banks

Industry numbers are too small to view in

a graph

Gain/Loss on Asset Sales

Earning Assets

© 2015 American Bankers Association

Performance Relationships

Yield on EA

- Cost Rate on IBL

≈ Net Interest Margin (actually spread)

- Loan Loss Provision to EA

+ Non-Interest Income to EA

- Non-Interest Expense to EA

+ Gain/Loss on Transactions to EA

© 2015 American Bankers Association

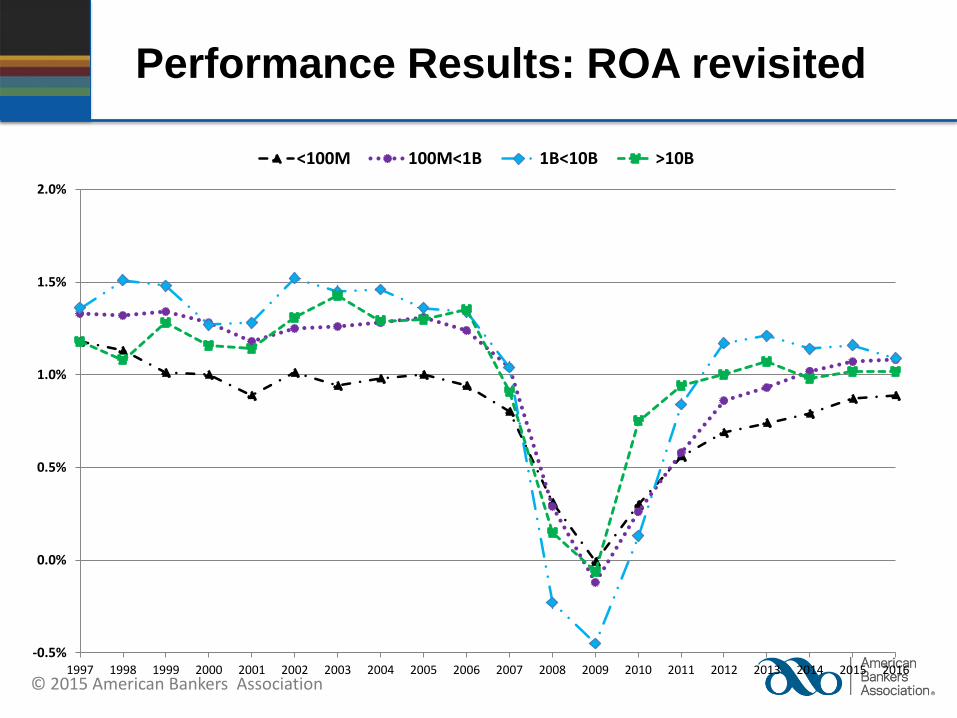

Performance Results: ROA revisited

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

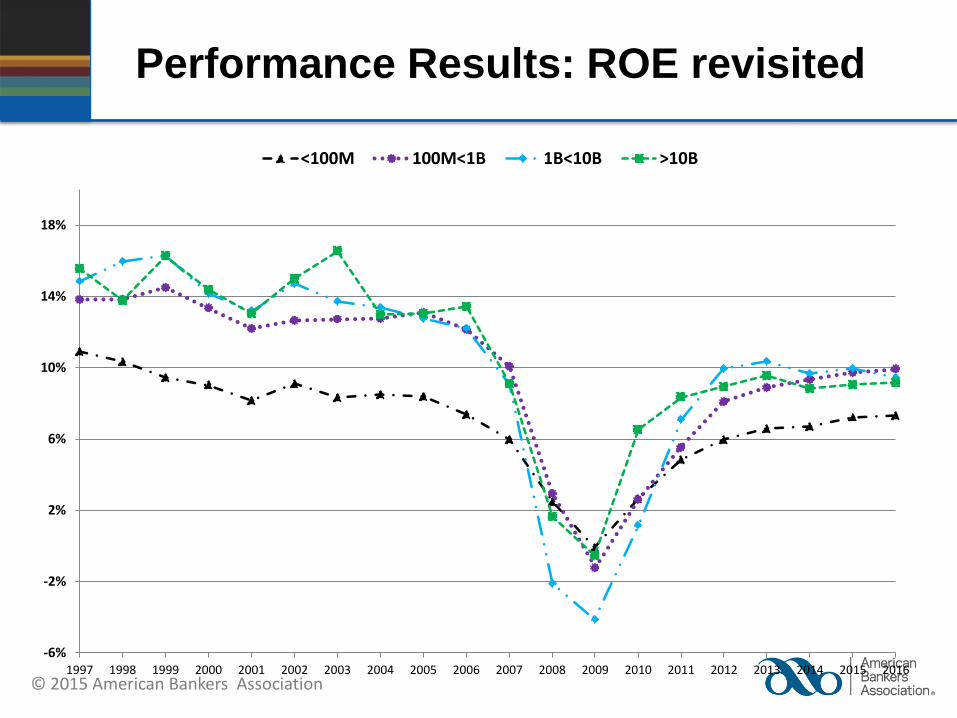

Performance Results: ROE revisited

-6%

-2%

2%

6%

10%

14%

18%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

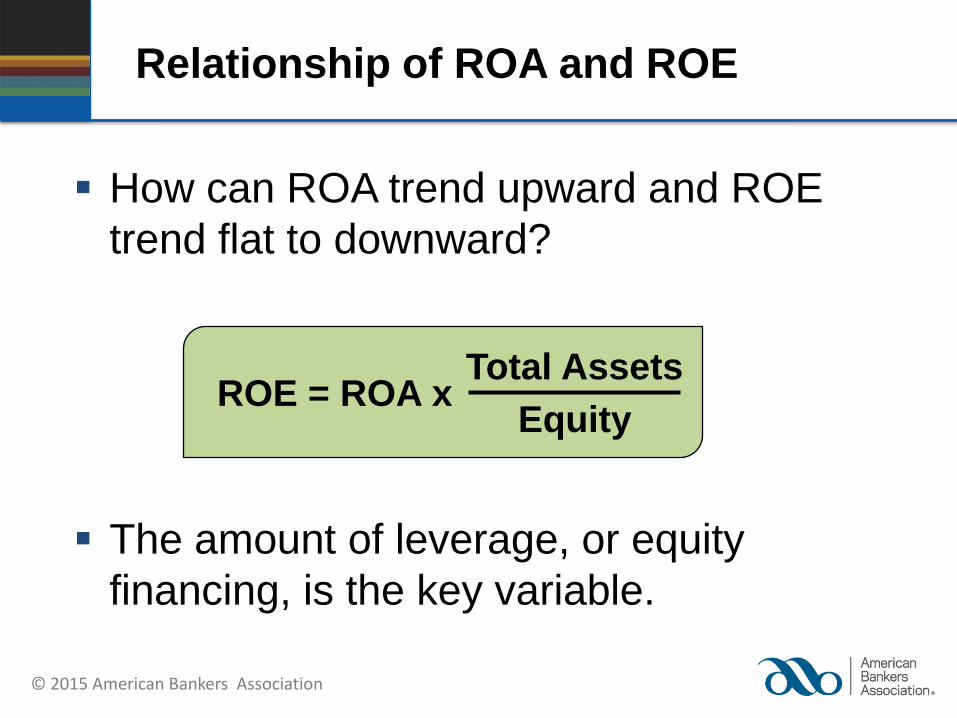

Relationship of ROA and ROE

How can ROA trend upward and ROE

trend flat to downward?

The amount of leverage, or equity

financing, is the key variable.

Total Assets

Equity ROE = ROA x

© 2015 American Bankers Association

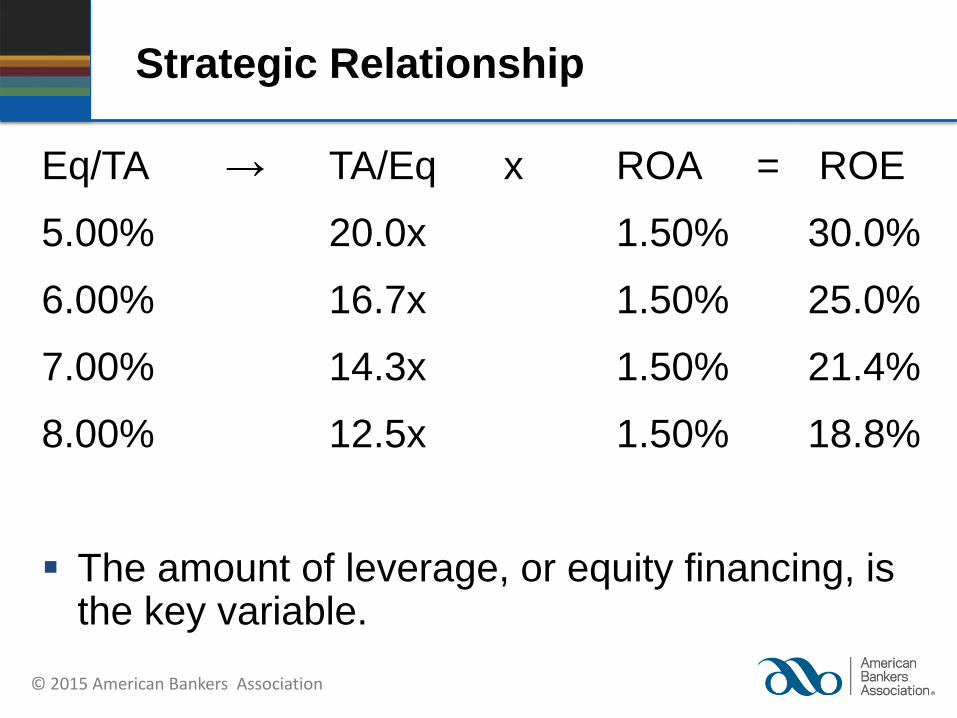

Strategic Relationship

Eq/TA → TA/Eq x ROA = ROE

5.00% 20.0x 1.50% 30.0%

6.00% 16.7x 1.50% 25.0%

7.00% 14.3x 1.50% 21.4%

8.00% 12.5x 1.50% 18.8%

The amount of leverage, or equity financing, is the key variable.

© 2015 American Bankers Association

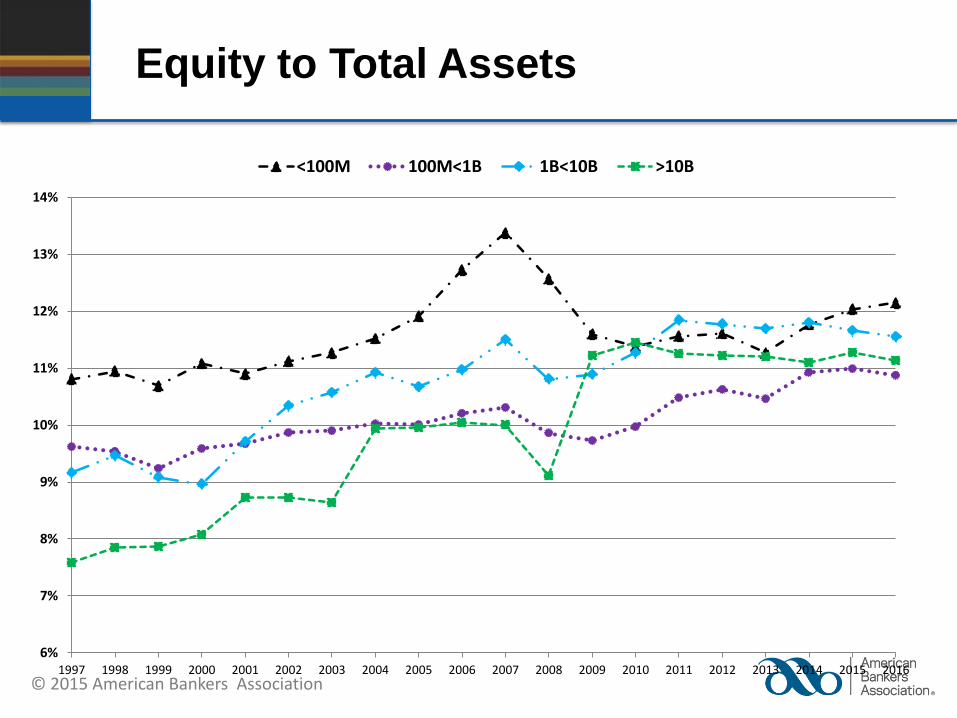

Equity to Total Assets

6%

7%

8%

9%

10%

11%

12%

13%

14%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

<100M 100M<1B 1B<10B >10B

© 2015 American Bankers Association

Performance Analysis

The analysis that we have just completed

can be arrayed in a strategic relationship

Any change in the drivers will cause a

change in results variables (ROA and ROE)

Strategic initiatives should be designed to

cause specific changes in the drivers

Actual calculations can be done on the basis

of total assets rather than earning assets

© 2015 American Bankers Association

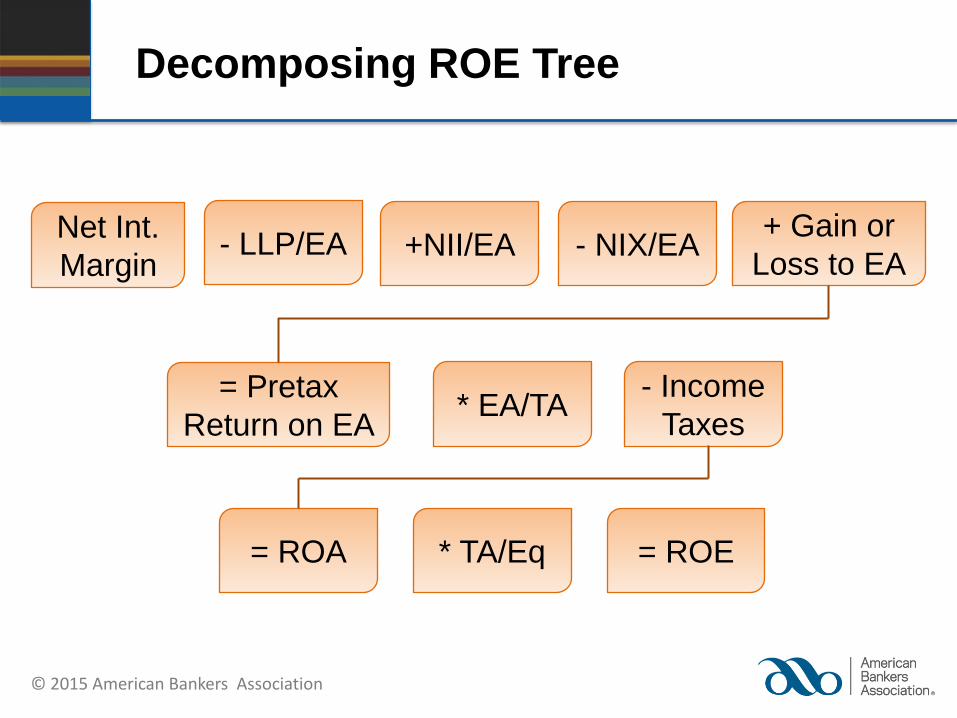

Decomposing ROE Tree

Net Int.

Margin - LLP/EA +NII/EA - NIX/EA

+ Gain or

Loss to EA

= Pretax

Return on EA * EA/TA

- Income

Taxes

* TA/Eq = ROA = ROE

© 2015 American Bankers Association

Performance Summary Industry

ROA and ROE recovering last couple of

years

– Net interest margin has been declining

– Lower loan loss provisions

– Pressure on non-interest income

– Non-interest expense leveling out to up

© 2015 American Bankers Association

Decisions Affecting ROE

Pricing and mix of assets

Pricing and mix of liabilities

Quality and growth of loans

Service charges and fee income

Expense control

Choice to sell assets

Amount of earning assets

Ability to manage taxes

Payment of dividends

Use of deposits and debt

© 2015 American Bankers Association

Data Sources

Comparative Data Sources

FDIC Statistics on Depository Institutions (SDI)

Similar data can also be obtained from the FDIC via www5.fdic.gov/qbp and www5.fdic.gov/SDI/SOB

Industry definitions

– SDI offers several predefined peer groups: <100M, 100M to 300M, 300M to 500M, 500M to 1B, 100M to 1B, 1B to 10B, and >10B

– Custom peer groups may also be defined by the user