bankers as buyers 2009 - credit and collection news 2009 final.pdf · bankers as buyers 2009 ......

TRANSCRIPT

© 2009 William Mills Agency

1

Bankers As Buyers 2009

A collection of research, observations and articles about what technology, solutions and services bankers will buy in 2009 and the changing financial industry landscape

Prepared by: William Mills Agency www.williammills.com

© 2009 William Mills Agency

2

January 2009 Dear Readers: For the last six years, Bankers As Buyers has focused on what to expect in the coming year from the banking community in terms of spending on technology, information and related services. If you are a news junkie and your mood swings with the market indices, it has been a rough year and 2009 doesn’t look much better. If you look at the details of the banks that folded in 2008, you will see decisions that increased their institutional risk and brought them down. The good news is that the banking industry fuels every other industry. Albeit less, people are still running businesses; buying homes or refinancing loans; investing; making payments; saving; replacing cars; using credit/debit cards; and more. There are financial transactions occurring and customers/members using financial institutions. The run up in the economy and spending of the last few years fueled growth and led to inefficiencies. Today’s current economic environment is causing many of us to renew our focus and make more measured, strategic decisions in order to run better businesses. If you are a vendor to the financial industry, you need to make sure you sell using an ROI model; keep year- one affordable for the institution; tie your product or service to the institution’s strategic objectives; reduce fraud or eliminate waste; and lastly, improve the experience for the customer. This year’s survey has been greatly enhanced by information provided by or originally published by: Aite Group Nancy Atkinson Christine Barry Gwenn Bezard Nick Holland Celent Jacob Jegher Centric Federal Credit Union Chris Craighead Cornerstone Advisors Terrence Roache Credit Union National Association (CUNA) Crone Consulting, LLC Richard Crone Federal Deposit Insurance Corporation (FDIC) Financial Insights Jeanne Capachin

Independent Community Bankers of America (ICBA) Javelin Strategy & Research McAfee Potlach No.1 Federal Credit Union Ron Broddas Securas Consulting Group, LLC Jimmy Sawyers Security Savings Bank Jesse Torres SourceMedia (American Banker) TCS Financial Solutions Dennis Roman TowerGroup, Inc. Virginia Garcia The Washington Trust Company Barbara Perino

It is our pleasure to provide you with this 2009 edition of Bankers As Buyers. While the material is copyright protected, you have our blessing to share this document with your business associates, clients, prospects and friends within the industry. Sincerely,

Scott Mills, APR President William Mills Agency William Mills Agency is the nation’s largest financial public relations firm. William Mills Agency was founded in 1977 and promotes companies that sell virtually every product or service used by commercial banks, mortgage lenders, credit unions, insurers and securities companies. The Atlanta-based agency represents companies throughout North America and Europe. For more information, please visit www.williammills.com or call Mr. Kelly Williams at (678) 781-7202.

© 2009 William Mills Agency

4

Table of Contents PAGE Introduction 5 I. Spending Outlook 6

A. Market Size 6 B. Spending Projections 8

II. Spending Breakdown 11

A. Regulatory Spending 11 B. Security Spending 12 C. Analytics 13 D. Community Bank/Credit Union Perspective 14 E. Mobile Banking 16 F. Software as a Service (SaaS) 17 G. Paper Reduction 18 H. Integration 18 I. Other Technology Spending 18

III. Featured Articles Vendor Strategies in the Financial Services Sector 21 By Jeanne Capachin, Financial Insights, an IDC Company Credit Unions: Time to Optimize Your Delivery Strategy 25 By Richard Crone, Crone Consulting, LLC Top Ten Trends Impacting Bank Technology for 2009 31 By Jimmy Sawyers, Securas Consulting Group, LLC Redefining the Value Experience in Banking 36 By Dennis Roman, TCS Financial Solutions

© 2009 William Mills Agency

5

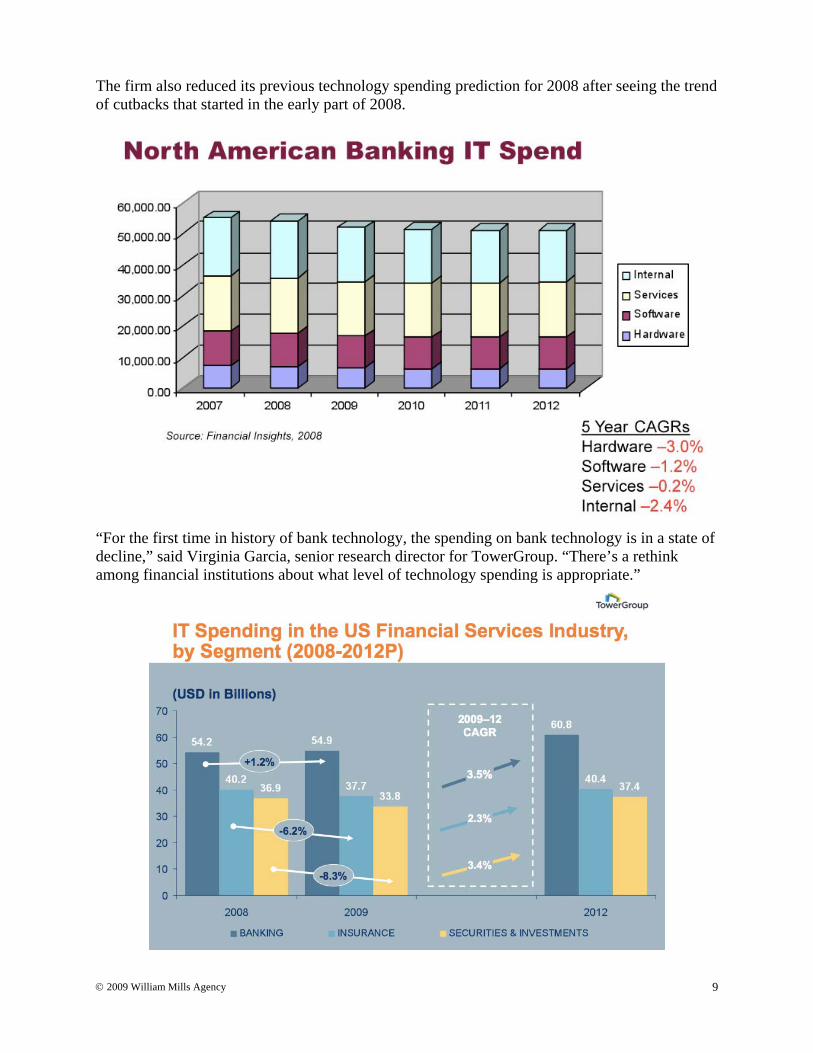

Introduction The slowdown in credit started in 2007, but the market came to a screeching halt in 2008 as declining home prices, mortgage defaults and failures of large financial institutions and brokerage houses led to the government’s Troubled Assets Relief Program (TARP). This year we will see bankers with a renewed focus on growing deposits. For better or for worse, many of them will be managing through consolidations and considering how to use technology to reduce head count. Since the first issue of Bankers As Buyers in 2002, bank technology spending has always been projected to grow in the three to five percent range. 2009 is the first year we should expect a negative growth rate of technology spending, with hardware and internal spending taking the biggest hits. By segment, TowerGroup predicts technology spending in banking to stay flat, with insurance and capital market segments down 6.2 and 8.3 percent respectively. Yet, despite the ongoing concerns in the industry, there are some definite areas where technology spending is expected to grow this year. Analytics Gain in Importance Financial institutions are focusing more on technologies that help them better determine if a borrower can repay a loan, more quickly identify troubled assets and help them collect outstanding payments. Analytics will also help banks better manage what will surely be a more aggressively regulated industry. Collections efforts can be more effective using analytical tools. Mobile Banking Mobile banking was consistently referenced by our sources and in studies as a channel that will see significant growth in 2009 and beyond. Security Concerns Continue Crime tends to increase in times of economic stress, and the current environment is no different. According to the McAfee Virtual Criminology Report for 2008: “Cybercriminals are cashing in on the fact that the economic downturn is causing people worldwide to increasingly turn to the Web to seek the best deals, jobs and to manage their finances. They are preying on fear and uncertainty and taking advantage of the fact that consumers are often more easily duped and distracted during difficult times. In fact, opportunities to attack are on the rise.” Community Financial Institutions Become More Popular As negative news swirled around large financial institutions, consumers concerned about safety have renewed interest in community banks that don’t get involved in credit default swaps and have little or no exposure to risky loans. As a result, community institutions will be focusing on technologies that enable them to better serve their customers, including mobile banking, enhanced telecommunications solutions and online banking improvements.

© 2009 William Mills Agency

6

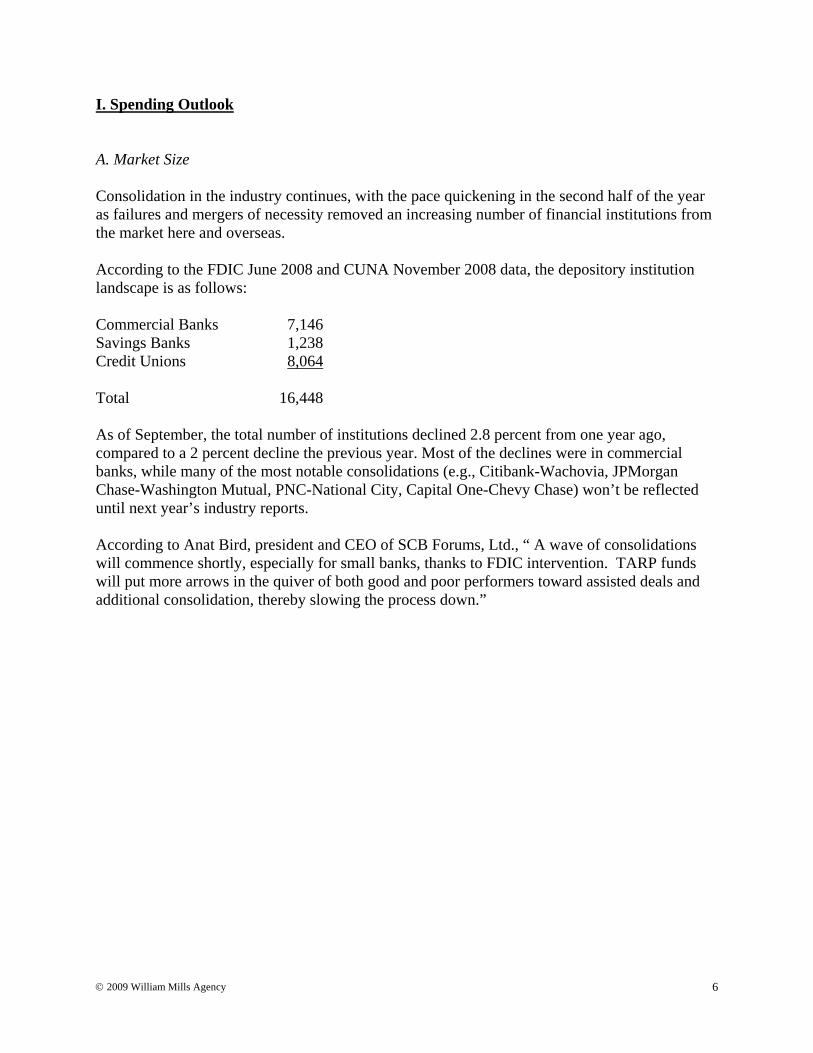

I. Spending Outlook A. Market Size Consolidation in the industry continues, with the pace quickening in the second half of the year as failures and mergers of necessity removed an increasing number of financial institutions from the market here and overseas. According to the FDIC June 2008 and CUNA November 2008 data, the depository institution landscape is as follows: Commercial Banks 7,146 Savings Banks 1,238 Credit Unions 8,064 Total 16,448 As of September, the total number of institutions declined 2.8 percent from one year ago, compared to a 2 percent decline the previous year. Most of the declines were in commercial banks, while many of the most notable consolidations (e.g., Citibank-Wachovia, JPMorgan Chase-Washington Mutual, PNC-National City, Capital One-Chevy Chase) won’t be reflected until next year’s industry reports. According to Anat Bird, president and CEO of SCB Forums, Ltd., “ A wave of consolidations will commence shortly, especially for small banks, thanks to FDIC intervention. TARP funds will put more arrows in the quiver of both good and poor performers toward assisted deals and additional consolidation, thereby slowing the process down.”

© 2009 William Mills Agency

7

The original chart can be found at: http://www2.fdic.gov/qbp/2008sep/all3a2.html

© 2009 William Mills Agency

8

Source: U.S. Credit Union Profile Nov. 25, 2008 by Credit Union National Association (CUNA) B. Spending Projections Bankers and the companies that provide industry products and services will face one of their most challenging years in 2009. Financial Insights is predicting an overall reduction in IT spending for North American banking in 2009. This will mark the first time negative growth has been forecast for the industry since before Financial Insights and its predecessor firm started forecasting IT spending in the mid-1990s, according to Jeanne Capachin, research vice president, global banking.

© 2009 William Mills Agency

9

The firm also reduced its previous technology spending prediction for 2008 after seeing the trend of cutbacks that started in the early part of 2008.

“For the first time in history of bank technology, the spending on bank technology is in a state of decline,” said Virginia Garcia, senior research director for TowerGroup. “There’s a rethink among financial institutions about what level of technology spending is appropriate.”

© 2009 William Mills Agency

10

“I’ve been in the business for 25 years, and I’ve never seen it like this,” said Chris Craighead, president and CEO of $75 million Centric Federal Credit Union, West Monroe, La. “I don’t think anyone knows what the outcome will be. I don’t know if the government intervention will help at all.” Financial institutions are being squeezed tightly by sharply dwindling asset values and increased defaults. Many of the nation’s larger banks failed or were weakened to the point that they had to be absorbed by financial institutions with better cash positions. But even the survivors aren’t as strong as they once were. Therefore, core renewal and any other large projects that might have been on the drawing board, are now on hold for a year or more. Quick returns will be the mantra for any technology purchases beyond those necessary to meet regulatory guidelines or to maintain security. “ROI sells,” said independent financial services consultant Richard Crone, chief executive officer and Founder of Crone Consulting LLC. “I’ve been in the industry more than 30 years, and if you have a technology with positive ROI, there is no better time to be offering it.” Though there is pressure for financial institutions to develop ROI more quickly than ever before, Crone cautions that banks should have an outlook that goes beyond the next year. Barbara Perino, senior vice president of operations and technology for The Washington Trust Company said that her 2009 spending priorities will be “highly-focused,” likely on electronic document management, mobile banking, business intelligence for client retention, wealth management systems and compliance/security. “Banks can’t forget about competing,” agreed Jimmy Sawyers, partner, Securas Consulting Group, LLC. Community banks in particular are focusing on customer-facing technology to attract customers who are seeking new banking relationships after witnessing the hardships of some of the nation’s largest financial institutions. Garcia agreed: “Once the economy recovers, [a bank’s] technology environment needs to support the business challenge. Taking one thing out just to eliminate the cost of the technology can come back to bite financial institutions in a big way further down the line.” As a result, technologies that enable financial institutions to leverage their technology dollars, such as Software as a Service (SaaS) and “virtualization” are expected to continue to gain in popularity. Virtualization is an environment in which a computer or server works multiple devices or processes. For example, rather than using three different servers for different types of operations, one physical server would perform all functions. SaaS is gaining more traction because it gives financial institutions a way to benefit quickly from new technologies without the huge upfront investment required for installed solutions. Virtualization enables financial institutions to do more with less hardware, meaning savings not only on equipment costs, but also on the cost of operation. According to several articles in Data Center Management magazine, some of the largest, data driven banks may become more concerned with energy consumption. Technology budgets include costs associated with operating data systems, both for powering the hardware and for cooling systems to ensure the computers, servers and other equipment don’t overheat.

© 2009 William Mills Agency

11

However, any technology that might have been considered as “nice to have” has been taken off the table, according to Jacob Jegher, senior analyst for Celent, part of Oliver Wyman. II. Spending Breakdown A. Regulatory Spending Nancy Atkinson, senior analyst with Aite Group, said, “I expect that once the government feels they have a safety net in place to create a floor for the economy, they will move their focus to how this happened and will introduce new regulations. As a result, regulatory compliance, which already receives a large portion of banks’ IT budgets, will require even more spending over the next few years. Vendors that support data gathering, analysis and reporting will do well, because those capabilities are needed for regulatory compliance. However, those vendors focused more on new products and services for banks, may be challenged to sell their services.” Within regulatory spending, Terrence Roche, principal with Cornerstone Advisors, expects much of the concentration to be on systems that monitor or aid with compliance, Bank Secrecy Act, fraud detection and fraud management. Regulators will want quick and thorough access to detailed information to ensure that financial institutions are meeting transparency and other regulatory guidelines. Banks are already struggling to meet the compliance burden with their current technology, according to an Aite Group survey.

“Banks will have to use intelligent technology to meet the compliance burden so that they don’t face enforcement actions,” Sawyers said. Jegher doesn’t expect to see much new spending on compliance, “Banks spend a ton on compliance already. Much of the technology is already there.” However, Jegher added that new compliance measures, which some expect, could drive additional spending on compliance technology. Much of any additional compliance concerns will fall on the shoulders of core technology vendors like Jack Henry, Garcia added, saying that 70 percent of compliance concerns information in the core system.

© 2009 William Mills Agency

12

B. Security Spending Closely related to the need for regulatory spending despite tight revenues is the need to keep accounts secure. “Security is like health care, it’s something you need to keep spending money on,” said Capchin, who expects security spending to continue to grow steadily, but slowly. “Most of the spending will be reactive rather than proactive. Banks will be seeking to mitigate risk.” Proof of bankers’ concerns about personal information security is documented by the Independent Community Bankers Association’s 2008 Technology Survey, which revealed that 81 percent of respondents listed this as their top priority for long-term technology.

Source: Independent Community Bankers of America. The full report can be found at: http://www.icba.org/files/ICBASites/PDFs/2008techsurvey.pdf Security breaches can be costly. According to Javelin Strategy & Research, the average ID fraud currently costs $5,574 per victim and takes 26 hours to resolve. Sawyers points out that financial institutions, particularly community banks, suffer loss of reputation as well as financial damages, so they will continue to ensure that any in-house systems are safe and that service providers maintain best security practices. “Most of the focus will be on information management – fraud, Bank Secrecy Act, compliance and those types of systems,” Terrence Roche of Cornerstone Advisors said. “You need to do

© 2009 William Mills Agency

13

them for regulatory reasons to begin with. Any time a regulator wants to look at something, that needs to be at the top of the system.” Phishing attacks continue to target financial institutions, with fraudsters pretending to send messages from financial institutions seeking account information. While the largest institutions tend to be the ones that imposters target, smaller financial institutions are not immune. News events, such as the failure of Washington Mutual, increased attacks by spammers in an attempt to dupe unsuspecting account holders into providing sensitive information. These attempts were increasing as the economy was fading. Insider fraud may be even a wider problem according to Celent. The company estimates that up to half of all insider fraud incidents go unreported. Although a fair percentage of incidents are communicated, those that are not communicated in a timely manner are also problematic.

Source: Internal Fraud: Big Brother Needs New Glasses, by Celent Another complication is the growing popularity of mobile applications. Mobile devices are much less secure than computers, but users aren’t always cognizant of that. C. Analytics Closely tied to regulatory spending in the current environment will be spending on systems to analyze risk. Some blame poor risk evaluation as part of the reason for the current downturn in the financial industry, so good analytics tied to risk management will be needed to meet compliance rules. “The largest banks need have the right analytical tools in place to better evaluate creditworthiness and to have better predictability,” said Christine Barry, research director for Aite Group. “Now it’s more important than ever for banks to lower their risk.” “Financial institutions need to be better able to understand where their positions are with wholesale banks and corporate customers,” Capachin added. Most of the spending will be on systems and applications to better mine internal data. Capachin expects financial institutions to cut some of their spending on purchasing external data. Better analytical tools will also help financial institutions increase their collections, according to Capachin. Good analytics can help a financial institution determine which outstanding accounts

© 2009 William Mills Agency

14

will result in the best returns. It’s not always the accounts that have the largest balances. The analytics for collections takes into account the amount outstanding, the propensity to pay and other factors. Banks are also starting to make collection calls much earlier, sometimes only days after a payment is missed, rather than waiting 60 days or more, as had been the practice. Virginia Garcia of TowerGroup said she expects to see regulators push for more stringent risk management guidelines as a result of the recent financial industry troubles. However, any new compliance requirements are unlikely to be known until the second half of the year.

Managing risks was the top-cited technology concern (81 percent) in the ICBA technology survey. D. Community Bank/Credit Union Perspective Some community financial institutions are picking up customer runoff from larger financial institutions that have shaky financials, according to Sawyers and Capachin. In a December 22, 2008 article in USA TODAY, Pallavi Gogoi writes, “But as the top tier of the financial services industry faltered, small and regional banks, as well as credit unions, started seeing their cash deposits rise dramatically as nervous Americans shied away from big banks. Some of these smaller financial firms saw an increase in small businesses knocking on their doors. And despite rampant headlines about a credit freeze and plunging housing market, they have even been writing more home loans this year than last year.” The article also references an ICBA study which reveals 70 percent of community banks saw an uptick in deposits within the past 12 months and an 11.6 percent rise in new interest checking accounts in the third quarter of 2008. Community financial institutions are focusing their technology spending on customer service and self-service technologies to take advantage of customers’ increased interest in doing business with local financial institutions.

© 2009 William Mills Agency

15

Capachin added that some community financial institutions are looking at replacing core technology systems, even though such changes have been put off by larger institutions. “Community banks are a lot more nimble,” Sawyers added. “And the cost of technology continues to come down.” He expects smaller financial institutions to take advantage of customers’ renewed interest in community banks by installing systems that enable customers to access account information via telephony and online systems. Some institutions will add small contact centers complete with IP telephony solutions that immediately provides the agent with pertinent customer information to help ensure first call resolution. “Installing more customer-facing technologies will help them compete,” Sawyers said. Indeed, Ron Broddas, chief information officer for Potlach No.1 FCU, ($330 million), Lewiston, Idaho, said that while technology spending at his credit union will be up only a very modest 1.7 percent over the previous year, much of the focus will be on technologies that offer members electronic alerts, online account opening, click-to-call features for online banking and similar technologies. “We’re trying to provide the communications paths that our members want to use,” said Broddas, who is also on the Credit Union National Association’s technology committee. According to an American Banker article (Web and Branch Sign-ups Give Small Banks Mortgage Lift, by Kate Berry, December 19, 2008), “Small and midsize banks and credit unions that sat on the sidelines during the mortgage run-up are trying to increase market share during the downturn by taking applications online and training more staff members to do so at local branches.” The article explains that with less competition from larger banks and mortgage brokers that the smaller banks are looking to using technology to increase their capacity without adding staff. The article also mentioned that credit unions now have a 4.5 percent mortgage market share versus a two percent share five years ago.

© 2009 William Mills Agency

16

Source: Independent Community Bankers of America. The full report can be found at: http://www.icba.org/files/ICBASites/PDFs/2008techsurvey.pdf E. Mobile Technology Crone sees continued growth in spending on mobile applications because they can bring financial institutions new customers and new revenue streams, which are in high demand with net interest revenue expected to be tight until the economy starts to turn around. TowerGroup estimates that every month through the first quarter of 2009, between 150 and 300 banks and credit unions in the U.S. will sign contracts for mobile banking solutions. The mobile phone has become more than ubiquitous, with some people dropping their land lines entirely and many people owning more than one hand-held device, Crone said. “It penetrates every demographic. It sets the stage for a low-cost delivery structure.” By providing mobile-friendly applications and by communicating with customers via e-mails, text messaging and phone calls to mobile devices, financial institutions will grow a loyal customer base, Crone said. As proof, he pointed to Bank of America’s mobile banking program, which had 500,000 active mobile customers after only 90 days and 1.6 million after six months. The six-month figure matched the combined totals of the Intuit Quicken, Microsoft Money and Manage Your Money online banking programs enrolled in two years. Beyond growing the customer base, financial institutions can grow revenue streams by selling advertising and additional products and services via the mobile channel, Crone said. To do so, financial institutions need to offer customer defined alerts (e.g., balance below a certain level) and opt-in for different kinds of marketing text messages. For example, a customer could opt in for messages about promotional offers. The technology vendor would pay a fee to place ads, another fee to send them to a targeted customer base and a third fee for any sales, Crone explained. “Financial institutions need to establish a beachhead on “opt-in,” two-way mobile marketing. Other reports support the expectation for growth in mobile banking. According to recent Aite Group research, almost half of current mobile financial service users (45 percent) are likely to subscribe to a mobile data plan by the end of 2009. Large text message bundles are typically included in such data plans, encouraging copious text messaging.

© 2009 William Mills Agency

17

Small-business owners are attracted to financial products and services that save them money or increase convenience. More than 60 percent of small businesses currently bank online and are showing a greater demand for multi-channel banking, including mobile banking services. In fact, approximately one-third of those polled by Aite Group said they were likely to use mobile banking; nearly 10 times the likelihood expressed by credit and debit cardholders in a similar Aite Group survey. Extending mobile banking to small businesses means additional revenue for banks, according to Aite Group. Unlike retail banking customers that have been universally provided with free mobile banking, small businesses can, and do, pay for a number of banking services. “Small businesses clearly show a need for mobile banking, and the segment offers banks a real opportunity to monetize the service – something that has remained largely elusive thus far,” added Nick Holland, senior analyst with Aite Group. “Mobile is an efficient channel, facilitating saved time and expense for people who already have little spare time and money. Banks cannot simply offer the same mobile banking services that are currently offered to retail banking customers, however. Instead, they should carefully assess small-business pain points that can be relieved via a mobile interface.”

F. Software as a Service (SaaS) If outsourcing ever fell out of style, it is now fully back in fashion. Banks are increasingly favoring outsourcing and the SaaS model as opposed to software licensing requiring capital expenditures, said Aite Group analyst Gwenn Bezard, after talking to bankers at the Bank Administration Institute’s annual retail delivery conference in November. Others agree that SaaS will continue to grow as banks seek to contain costs while remaining competitive. “We expect SaaS to grow through 2009 and 10; it’s a prevailing theme in many of our discussions [with financial institutions],” Garcia said. “There’s a marked shift from installed technology to using Software as a Service.” Capachin said that financial institutions are increasingly seeking to remove non-essential staff, including much of the IT department. The need for IT drops greatly when using SaaS. This is true even of larger financial institutions that have traditionally kept much of their technology in-house. By selling off technology and switching to SaaS, these institutions can boost their balance sheets, a critical factor for many financial institutions in these difficult economic times.

© 2009 William Mills Agency

18

Capachin said SaaS investments started growing more quickly in the second half of 2008, a trend she expects to continue in 2009. G. Paper Reduction Last year’s report referenced green spending, which is a marketing element for banks to employ that will also help them to save on paper, mailing and storage costs while becoming more efficient. Spending for green’s sake has slowed considerably; however, promoting green benefits to customers is still in style. Banks are using e-mail and notices on printed mail to encourage customers to turn off the paper. Charter One has gone as far as to launch its Green$ense progran, which pays customers 10 cents every time they pay without paper – using a debit card, paying a bill online, or having an automatic payment charged to your checking account or debit card. A customer can earn up to $120 annually with the program. “Payments are in a state of transformation,” Garcia said. “Electronic payments are growing as banks [and their customers] move away from paper payments.” Roche adds that other institutions, particularly those that have a strong lending focus, are adding enterprise content management (ECM) systems to eliminate paper at the front end of the process. By digitizing documents early in the process, financial institutions can increase efficiency and cut costs, including personnel. “There’s a lot of pressure in the commercial area to cut staff,” Roche said. H. Integration Consolidations of larger financial institutions requires integration of their systems to gain many of the benefits of scale. Acquisitions and consolidation of platforms will take precedence over any other new technology spending, Garcia said. Barry observed that properly integrated technologies will help lower risk for the newly merged financial institutions. Jegher expects that the brisk merger and acquisition environment will lead to a short-term increase in integration technology spending, but then expects a gradual decline. Analysts agree that service oriented architecture (SOA) advances will drive much of the integration projects. I. Other Technology Spending With the items above, and tight revenues, spending on other technologies will likely be limited to necessities. There are a couple of notable exceptions, however.

© 2009 William Mills Agency

19

With mortgage and auto lending at a standstill, some financial institutions will refocus or focus anew on lending, deposits and other services for small business. Remote Deposit Capture grew strongly in 2008, many experts expect another strong year of growth for 2009. Some financial institutions had even expanded Remote Deposit Capture to the consumer market, but Roche expects that to remain a small, niche market. Jegher said that some banks that had relied on technology designed for consumer or middle market customers, will look more closely at small business solutions, not only to attract new business, but also to better evaluate the small business customers that they already have. Jegher cautioned that small businesses, many of which work on thin margins anyway, could be the next wave of challenges for the banks, following on the heels of mortgage and consumer credit woes.

Craighead said his credit union and a neighboring one are redesigning their branches, eliminating traditional teller lines and adding a customer service “pod,” complete with cash dispensers. “This enables [tellers] to work more as member service representatives,” Craighead explained. “This is a lot like the set up that Washington Mutual had. I had to remind our board that it wasn’t the deposits that hurt Washington Mutual.” No, it was ill-advised loans and subsequent declining real estate values that hurt WaMu and many of its peers. Capachin added that JP Morgan Chase is planning to change the WaMu branches that stay open back to traditional branches, which JP Morgan officials feel will provide better cross-sell opportunities. Other technologies that were popular only a few years ago will be on hold, as will any enterprise-wide solutions, according to several experts.

© 2009 William Mills Agency

20

Sawyers said he expects financial institutions to start using more blogging and other Web 2.0 marketing efforts to attract “the Facebook generation.” In a recently published e-book, Community Banker’s Guide to Social Network Marketing, author Jesse Torres, president and CEO of Security Savings Bank, Henderson, Nev., encourages bankers to explore social networking because, “Through social networking community banks can put customers in charge and give them a voice, and in the process, differentiate themselves from the competition. Tips for Selling to Bankers in Today’s Environment Barbara Pernio of The Washington Trust Company shared some tips for selling to bankers that are timely and timeless. Those are:

• Know the bank’s budgeting cycle • Convince them of the value – is there a direct impact on the bottom line? • Does it fill a void for customers or improve the customer experience? • Will it give the bank a competitive edge? • Will it mitigate risk or eliminate a single point of failure?

© 2009 William Mills Agency

21

III. Featured Articles Vendor Strategies in the Financial Services Sector

By Jeanne Capachin Research Vice President, Global Banking Financial Insights, an IDC Company Financial Insights is predicting an overall reduction in IT spending for North American banking in 2009. This will mark that for the first time negative growth has been forecast for the industry since Financial Insights and its predecessor firm started forecasting IT spending. This industry has been very resilient, even weathering the 2002 downturn in IT spending with continuing growth that was not seen in the overall IT industry. This time, it is the U.S. banking industry that is at the eye of the storm. For the first six months of 2008, the magnitude of bank failures, in terms of the size of failed institutions, is greater than at any time since the Great Depression. Financial Insights is forecasting negative growth in IT spending over the next five-year period, with the biggest hit occurring in 2009. Some of the drivers for the lower overall spend in the forecast are contraction of the industry, increased embrace of outsourcing and offshoring, continued datacenter consolidation, and pressure on bank profits. Financial Insights and IDC are predicting economic recovery in late 2009 for banking and the overall North American economies. Despite the infusion of up to $700 billion into the U.S. banking industry, we have not yet turned the corner. Housing prices continue to drop, and loan portfolios and investments keep losing value. Banks interviewed in October and November report halts in 2008 spending and smaller budgets for 2009. Expenses will be lowered by reducing IT staff, continuing virtualization projects, delaying planned hardware purchases, and stalling projects already underway. The largest institutions, controlling more than 70 percent of the IT spend, will focus on acquiring troubled assets and integrating systems of merged institutions. This will actually soften the decline in IT spending by injecting some new spend for 12–24 months post merger but with a lower overall base for the merged institutions. Smaller institutions that are well capitalized will find FinTech vendors more willing than ever to strike deals in 2009. For these banks, the time is better than ever to make this kind of investment. Large banks are focused inwardly and are not able to go forward with innovation projects.

© 2009 William Mills Agency

22

Vendors remain eager to crack the North American market, and with internal support and funding already in place, there is no good reason to halt projects that have already been green lighted if capital is available. In 2009, Financial Insights is projecting a 4 percent decline in IT spending compared with adjusted 2008 levels for the North American banking industry. For the forecast period between 2007 and 2012, spending will fall with a -1.5 percent CAGR as the banking industry constricts and the U.S. economy falls into and then pulls out of recession. Despite the constriction, there will be bright spots, and innovation projects focused on customer experience and acquisition will continue. Fintech vendors that can mine those areas will be well-placed to grow their businesses. But first, which spend areas will be hardest hit? Within payments, spending on check processing will drop precipitously as financial institutions convert to all-image operations and divest themselves of their paper processing equipment. Many institutions will reconsider outsourcing check operations as a means of adjusting their balance sheets and shedding staff. However, will they be able to find willing vendors who can take on that business in a market of declining volumes? That ship may have already sailed. Other hard-hit areas will be human capital management, payroll, and procurement as institutions shrink their staff and as the overall number of institutions shrinks. Looking at technology categories, hardware purchases will be hardest hit. Banks will delay replacement purchases as long as possible and will not undertake big new infrastructure projects. They will also accelerate virtualization and data center consolidation projects. These trends will result in an overall 3 percent decline in hardware spending from 2007 to 2012. Internal IT spending will also suffer disproportionately. Banks will divest of captive offshore operations to free up capital (as Citigroup recently announced), projects will be delayed and resources eliminated, and outsourcing will increase — leading to a 2.4 percent decline in internal IT spending. The flip side of the decrease in internal spend is a much less steep decline in external services spend. Although banks will strive to renegotiate existing contracts, labor arbitrage savings from outsourcing will be hard to ignore and banks’ appetite for outsourcing will increase. This category will only suffer from a 0.2 percent decline. And finally, software spending will decline at a rate of 1.2 percent. Owing to postponement of projects and a decline in the overall number of institutions, spending will fall. Also, impacting software revenue is the upsurge in use of software as a service (SaaS), with Financial Insights predicting that SaaS license sales will spike during the forecast period. One point to keep in mind with forecasts is that there are countervailing forces that will increase spend in some categories. For instance, tier 2 banks will be relatively unscathed by the credit crisis and acquisitions. Spending by these banks will inch toward the positive, ending the five-year forecast period with growth of 0.1 percent. Credit unions will fare well, and except for the smallest institutions — where the ranks are diminishing steadily — they will increase spending as well. In the payments arena, we expect spending on prepaid cards to increase, as financial institutions seek new revenue sources. The largest institutions that are on the right side of acquisition will increase spending dramatically post acquisition in areas such as channels and

© 2009 William Mills Agency

23

system infrastructure but will end the forecast period down because of shrinkage in the absolute number of firms in that category. In Canada, those institutions held a very different approach to risk than the U.S. firms and remained true to their retail banking roots. These banks remain strong, and without the positive impact of the Canadian banks, this forecast would have been even more grave. Financial Insights expects that in the next 12 months the top 5 Canadian banks will look south to make more acquisitions and expand their market presence. The U.S. banking industry is now leading the North American economy into recession. The silver lining is that the banking industry will lead the rest of the economy out of recession. While the banking industry flounders, it will impact the entire economy of North America and much of the world. Among government intervention, real estate prices recovering, and bad investments moving off the books, the banking industry will recover — as it must before the rest of the economy can start its recovery. Financial Insights predicts recovery of the banking sector by late 2009. However, the industry that we see 12 months from now will be more conservative and smaller than what we see now. For those firms serving the financial services industry, 2009 will be the most difficult year ever. The top institutions in the United States are preoccupied either with shoring up their balance sheets or with acquiring merged institutions. New projects will be few and far between, and it will be those vendors that are both financially sound and can strike the most attractive deals will succeed. In particular, vendors with flexible payment terms that can back-load payments will be able to win projects. As mentioned, SaaS will become much more attractive, and Financial Insights expects that large institutions will be much more amenable to outsourcing what were considered core businesses — especially those requiring new infusions of capital such as payments processing. There will be a flight to quality, as banks look for vendors that are fiscally sound, as well as knowledgeable partners. Weaker vendors, like the weaker institutions, will be acquired. Those banks that have cash to spend will find the A-Team of vendors waiting to serve their needs. These institutions can continue with their strategic projects recognizing that many of their competitors will be inwardly focused for the next 12 months. Some of these institutions will move forward with universal banking and core banking investments. They are investing in Web technologies to improve their interactions with clients and attract new deposits. They will continue to lend and gain market share as they take advantage of their financial strength. It is these institutions that stand to benefit the most and will grow during this difficult period. Financial Institutions in 2009 will be focused on four areas – integrating acquired assets, identifying and managing risks, controlling costs – both capital and operational, and retaining and acquiring customers. Selling into the industry in 2009 will require alignment with these four overarching themes. Fintech vendors that are well aligned with these themes have the best chance of success, but we expect that even very good Fintech companies will find a difficult time selling solutions in 2009.

© 2009 William Mills Agency

24

Financial Insights predicts that 10 of the 100 top Fintech firms will be acquired during 2009 in the face of slow growth. For some firms, that’s the desired end game, but most that become acquisition targets in 2009 will do so because of flagging sales and insufficient profits. It will take deft skills and a deep understanding of buyer requirements to weather the storm in 2009. Jeanne Capachin is the Research Vice President for the Global Banking and Insurance practices. Capachin has more than two decades of experience working in and consulting to the banking industry. Capachin works with the global analysts to develop the client driven research agendas, our spending forecast methodologies and guides, and oversees the Financial Insights ranking programs.

© 2009 William Mills Agency

25

Credit Unions: Time to Optimize your Delivery Strategy

By Richard K. Crone Chief Executive Officer and Founder Crone Consulting, LLC First there were branches and telephone contact centers, then ATMs and Voice Response Units, and just as we’re mastering the Internet along comes mobile financial services. How can credit unions be sure they’re providing the best possible service to their members? New service channels have only increased the diversity and complexity of managing member services, rather than replacing an existing channel. For example, the advent of ATMs didn’t decrease the number of branches. Service via an Internet web site didn’t reduce the number of calls to the contact center. This complexity has created a new discipline: channel management and optimization, with the goal of identifying member profiles and needs, and matching them to the most satisfying service option at the least cost. Each service channel has its own strengths and weaknesses. The most successful credit unions know how to squeeze the most value from each channel, and guide their members to the best match at the least cost. You’ll soon see how the mobile phone offers a way to increase the effectiveness of every other channel as well. Channels: the Touchpoints where you reach your members Branches offer a friendly face and personal service, but at a higher cost. Do the teller line, service cubicles, and other physical spaces provide an optimal mix of services and staffing? Here is an opportunity to integrate the full range of service options, if branch personal are properly cross trained to be a “personal guide” and coach in obtaining services electronically. Savvy credit unions use this physical space to extend their presence across the suite of servicing options as well as leverage its unique capabilities such as presenting free seminars on home buying and other financial issues, creating a personal bond with members. ATMs provide easy self service for cash withdrawals, deposits, funds transfer, and balance checking, with the potential for cross promotion of other self services channels and product advertising.

© 2009 William Mills Agency

26

Contact Centers offer the ease of phone access to financial services. But what most credit unions may not realize is that they are already providing mobile financial services. Close to two-thirds of all calls to member contact centers come from mobile phones, and this continues to grow. It’s time to unleash the unique added-value potential for mobile callers by taking advantage of the functionality of cell phones’ built-in voice mail, caller identification, text messaging and access to the mobile Internet. The key first step to leveraging your contact center for mobile financial services is to start identifying mobile numbers and their wireless carriers for your members, using ANI (Automated Number Identification) technology to populate the CIF (Central Information File) of your core application system. Work closely with your credit union’s core application provider. “Mobile functionality is a new strategic asset that creates market strength, and demand for this is growing fast,” says Debbie Wood, General Manager - Marketing & Industry Research for Jack Henry & Associates, Inc. “We’ve already signed up over 65 financial institutions for our mobile offering.” Online Web Sites enable members to educate and serve themselves from anywhere at any time – and this reach now extends to mobile devices. Provident Credit Union has incorporated the appeal of social networking sites in its online offering of “Zopa” inter-member lending, a new type of lending program that is a perfect representation of the credit union philosophy of people helping people. Members can view photographs and descriptions of potential borrowers, along with their reasons for needing a loan, and choose to lend money to the member they would most like to help, even selecting the interest rate they desire.

The Mobile Phone is not just a new service channel; unlike any other channel innovation in history, the mobile phone is present in every other channel experience: the phone is with the member when she walks into the branch, when he calls the contact center, visits a shared branch, or visits an ATM. Mobile transcends all channels, so therefore, mobile capabilities need to be cross functionally integrated.

© 2009 William Mills Agency

27

The service and channels portfolio is like a Rubic’s Cube of strengths and dependencies. On one side you have member profiles and personas. On another you have the service channels, each with its strengths and weaknesses. The third dimension includes the various use cases or services that members wish to access. The credit unions’ challenge: to maintain a high service level delivered consistently across the portfolio of channels, guiding members to the most effective delivery of their needed service; enhancing integration so members can easily find and execute the service they need; empowering members and making electronic self service easy and comfortable. Identify the most frequent use cases How to accomplish this? It starts by first inventorying the use cases, channel touch-points, and the steps involved in consummating a transaction or serving a member. The best place to go to understand and identify the use cases is the teller line and contact center. Take inventory to identify the 80/20 in the service portfolio; that is, what are the 20 percent of transactions that are taking up 80 percent of the teller’s or Member Service Representative’s time or costs (e.g., the top 10 call types to the contact center). Is there a way to re-engineer the delivery of those frequent use cases to a more efficient, member-friendly self-service channel? Case in point: 90 percent of the volume today of a typical voice response unit is for balance checking. It’s no surprise, given the rise of debit card usage and the decline in check writing. Members no longer keep a running balance. Why make the member repeatedly call, stop in, or log in for this essential information? Couldn’t the credit union save costs, and keep the member happier, by using the mobile channel to end this cycle? All mobile phones have caller ID and voice mail. Why not implement member-defined alerts via outbound phone calls at a member-set day, time and frequency or voice mail to voice mail with their balance. They can wake up every morning to a voice mail or text message waiting in their inbox with the balance. Or, for less frequent requests, let the member leave the credit union a voice mail with the request for information or service. No waiting on hold, just a voice or text answer sent to their mobile phone, as does the service Cha Cha (1-800-2CHACHA). Another example is from vlingo, which enables new self service scripts with members through the power of their voice activated services and requests; vlingo provides a quantum leap in usability for mobile data services that are currently restricted by limited user interfaces, all activated via the spoken voice and natural language processing. When ATMs were introduced more than 30 years ago, they emulated what the teller does today, accepting deposits and distributing cash. Members still filled out deposit slips. But simply mechanizing old work flows is like paving a cow path, rather than reengineering the process. Now no deposit slip is necessary. ATMs image the check and cut out steps to the benefit of the credit union and the member. It’s time to revisit the entire inventory of service functions, by service channel, and translate it once again, to yet a new, even more ubiquitous and personal channel, mobile. It’s important to use both deductive and inductive reasoning processes to identify both cost-saving and revenue-generating opportunities. Deductive thinking entails defining a problem, then searching for a solution; inductive thinking, or out of the box thinking, starts with recognizing a powerful solution, then seeking what problems might it solve.

© 2009 William Mills Agency

28

What are your Member Personas? Your credit union may be focused on serving members of a particular company, organization, or geographical area. Your members may be younger, shopping for a new home or a car; or older, shopping for college savings and retirement plans. How can the credit union reach the right member with the right message or self-service functionality at the right time? Channel integration and management is critical. The credit union branches, call centers, ATMs and website need to all tie seamlessly into the member database and central information file, so that, for example, in real time, the most pertinent offer can be presented to a member. This technology, which facilitates cross-channel integration, is being used successfully today by high profile firms in the financial services space such as Schwab and Bank of America. The mobile interface is a key tool to create a personalized message across all channels, optimize self-service, and improve the overall member experience. Nearly every member carries a mobile phone, a touchpoint that can overlap with and enhance every other channel interaction. Mobile has four distinct communication modes: voice, text, WAP2 (the mobile Internet browser) and downloadable applications. When we define the user personas, or market segments of members, voice is the lowest common denominator: every demographic, psychographic and technographic profiles uses voice. Credit unions need to revisit how they work with voice if two-thirds of the calls are coming in from a mobile device. Mobile communications line up with personas: for example voice is used by everybody; text skews mostly younger but also strong for adults with teens; WAP2 (mobile browser) skews both economic extremes: upscale affluent business people, and downscale workers who have abandoned an expensive land line and consume the Internet through the phone; and handset applications have not yet achieved a significant installed base, due to carrier wariness of third-party software on their phones and the difficulty in achieving ubiquitous and consistent access across more than 160 disparate networks, six major handset operating systems and more than 2,400 different mobile phone devices in service today in the U.S. alone. Channel Integration for Self Service Today, most credit unions treat each channel as a separate, isolated entity. If knowledge is gained about a member through the contact center, and what did or didn’t contribute to their experience, it stays with the contact center service person. The organization is not building upon each prior interaction to boost the speed and success of later interactions. There is little or no cross training and cross promotion. Functional silos in the enterprise structure compound this problem. Operations runs the call center; IT oversees the website; marketing handles outbound promotions; each with conflicting goals and agendas. Imagine the benefits of accumulating and sharing member data: instantly recognizing each unique member; their preferences, needs and transaction history, whether they are calling in, stopping by the branch, or logging on to the website. An integrated and complementary customer experience across all channels, through more effective database and channel management, creates a more supportive, welcoming environment where each member feels special and empowered to quickly find the answers they need.

© 2009 William Mills Agency

29

Integrated Electronic Self Service offers speed, ease of repeat usage, higher use of other products, greater loyalty and satisfaction, as well as lower costs. Effectively deployed and maintained, it is not impersonal, but creates mass customization, anytime, anywhere, for anything, for all members. Credit unions can maximize the use and effectiveness of self-service by re-engineering to take advantage of the capabilities of the mobile phone. For example, to protect against fraud, the most effective tool is member account monitoring. When a member makes a withdrawal, if she is signed up for user-defined alerts, she will instantly receive a text or voice mail confirming the transaction, reinforcing the security of all service channels. In the branch or at the ATM, her cell phone receives text or caller ID initiated automated voice or voice mail confirmation. If she receives this alert when she is not making a transaction, she can reply to the alert to stop the fraudsters in their tracks.

Turbo charging the value chain Tighter integration across channels and functions, leveraged by the power of the mobile connection, promise greater member loyalty, more extensive product usage and potential for new revenue streams, as well as a more cost effective service relationship. Through new technologies in voice recognition, interactive text messaging, Internet browsing of images, video and more, the mobile channel enhances all existing channels with a rich, customizable environment Mobile can create value previously unavailable in traditional financial services through self-service and mass customization, where members can manipulate financial information to create new value for themselves. This information is a valuable asset: Google, a search tool, and TV Guide, a programming listing guide, have higher market capitalizations today than the businesses they provide information about. How can credit unions turbocharge the basic data they generate and collect to create new products and services? Not unlike an automobile turbocharger that re-processes exhaust fumes to boost an engine’s power, credit unions can leverage transaction data, resident in their core data processing, to

© 2009 William Mills Agency

30

create new value even more powerful than the source business. Are credit unions ready to use this turbo charging to move into the fast lane? Mr. Crone is the Chief Executive Officer and Founder of Crone Consulting, LLC, a San Carlos, Calif., advisory firm for credit unions, banks, merchants, billers, processors, and investors on channel optimization, electronic payment and mobile customer self-service strategies.

© 2009 William Mills Agency

31

Top Ten Trends Impacting Bank Technology for 2009

By Jimmy Sawyers Partner of the LLC Securas Consulting Group LLC “The Chinese use two brush strokes to write the word ‘crisis.’ One brush stroke stands for danger; the other for opportunity. In a crisis, be aware of the danger — but recognize the opportunity.” John F. Kennedy at a speech in Indianapolis, Indiana — April 12, 1959 One lesson we learned in 2008 is all that is certain is uncertainty. As Wall Street and the U.S. auto industry, both in crisis, approached Washington with hat in hand and palms extended, 401Ks shrank, home foreclosures exploded, jobs were lost, and many Americans saw an economic crisis never before experienced in their lifetimes…quite a wake-up call for younger generations unfamiliar with sacrifice and hard times. Throw in two wars still being fought along with growing fears of global warming, and it is easy to understand why Pepto-Bismol and Rolaids sales are up. Despite the sour note struck at the end of 2008, such crises do present opportunities and no doubt will do so as 2009 progresses. Those who can spot the opportunity amid all the danger will prosper during the recovery that is sure to come. To help prepare for brighter days ahead, we offer ten predictions: 1. The New Three C’s of Banking Bankers will expect their technology investments to fall into categories we call the new Three C’s of Banking: 1. Contain; 2. Comply, and 3. Compete. To contain costs, bankers will look for ways that technology can streamline processes and enhance the efficiency of operations. To comply with new laws and regulations, bankers will invest in a wide range of compliance-related technology, helping to automate much of this burdensome process. Banks balancing the Three C’s by innovating and using technology to compete more aggressively while better serving the customer, will emerge as winners. While tech spending may be down in large banks, expect community banks and regional banks to spend more on technology in 2009 as they take advantage of their larger brethren’s recent stumbles. Well-managed community banks can pick up significant runoff in employees and customers, if technology is utilized effectively to level the playing field with big banks.

© 2009 William Mills Agency

32

As investment banks repair the distrust brought on by their failures, community banks will benefit in their role as trusted, stable, entities. The George Baileys of the world will triumph over Mr. Potter one more time as customers flock to those they trust. This influx of funds to community banks will force bankers to offer more innovative products and services. Another trend that will elevate community banks will be the generational transfer of wealth. As baby boomers retire and eventually expire, a new generation will have cash to invest. Bankers must be ready for a time-stretched, tech-savvy demographic that wants and demands more than their parents did from their banks. 2. Cloud Computing See that cloud on your network diagram? That metaphor for the Internet? A better depiction might be a light bulb or a water faucet. Computing as a utility, cloud computing, Web 2.0, and Software as a Service (SaaS), are all terms referring to IT extending beyond the firewall and into cyberspace. As Gartner noted in August 2008, “Organizations are switching from company-owned hardware and software assets to per-use service-based models.” This shift will result in positives and negatives in the IT industry. A positive for those who offer subscription-based, pay-per-use web-based applications and a negative for some traditional hardware and software providers relying on old methods of distribution. Just as Customer Relationship Management and Human Resources Management have leveraged the cloud, expect Business Intelligence (BI) to be the next big app in the cloud. Cloud computing will help companies cut IT costs as they outsource to firms operating in the cloud. Just as our grandparents and great grandparents were able to stop chopping wood for the pot bellied stove with the advent of rural electrification, cloud computing will fulfill the promise of greater productivity at lower cost. 3. Simplicity and Usability Win Financial services technology works best when the interface is simple and the application is easy to use. Just as consumers are flocking to simpler gadgets like the Nintendo Wii game console and the Flip camcorder, bank customers will gravitate to online services that are uncomplicated, stable, and time-savers. According to Deloitte, Pure Digital Technologies, the manufacturer of the Flip, grew 44,667 percent, making it the fastest growing company in Silicon Valley over the past five years – pretty strong numbers for a very basic camcorder about the size of a deck of cards. More than 1.5 million have been sold since it was introduced in 2007. The two fastest growing companies with more than $1 billion in revenues were Google and Apple, respectively. Over the past five years, Google has experienced 1,032 percent growth and closed 2007 with $16.6 billion in revenue. During that same period, Apple grew 287 percent with 2007 revenues of $24 billion. Both companies exude simplicity and elegant design. Bankers revamping their websites and online services should look to Nintendo, Pure Digital, Google, and Apple for their inspiration in 2009. 4. Handheld Devices Come of Age Smartphones, PDAs, and other handheld devices are now ready for prime time. Expect 2009 to see Apple and Research in Motion (RIM) continue their battle for smartphone dominance. Apple

© 2009 William Mills Agency

33

iPhone sales exceeded sales of Microsoft Windows Mobile Devices for the first time in history and grew 327.5 percent in the third quarter of 2008. Research in Motion enjoyed sales growth of 81.7 percent in the same period and introduced its BlackBerry Storm smartphone as an answer to the iPhone. Google’s Android and Symbian Foundation, open-source initiatives, will chip away at Windows Mobile market share and highlight usability issues. Expect more content to be pushed to handheld devices with more applications being written for such devices. To some, 2009 will be the year their smartphone becomes more important than their PC. For others, this has already occurred. STUDYLOGIC LLC conducted a 2008 study, commissioned by Sheraton, which showed that 85 percent of those surveyed feel their PDA allows them to spend more time out of the office. Seventy-seven percent said the PDA helps them enjoy life. Disturbing news to some, 87 percent bring their PDA into their bedroom and 35 percent would choose their PDA over their spouse. These trends bode well for mobile banking. Banks jumping in front of the handheld device parade will win the love and affection of their customers who are married to their smartphone. 5. Bankers Go Green Report archive. Image item processing. Document imaging. ACH. Internet banking. Bankers were green before green was cool. We just forgot to advertise it. For 2009, bankers will embrace green technologies including Enterprise Content Management, Remote Deposit Capture, Unified Communications, Videoconferencing, Virtualization, and Microsoft Sharepoint. Office Sharepoint Server will help banks better manage content, reduce travel costs, and improve communication. Sharepoint Online, a cloud-based solution, will further Sharepoint’s penetration into smaller organizations. Bankers will assess their networks and find that virtualization can save significant dollars. Recent assessments of community banks have projected hundreds of thousands and sometimes millions of dollars in savings over a five-year period, making virtualization a continued hot technology in 2009. 6. Network Infrastructure Improvements Just as many areas of our nation’s infrastructure need upgrading, bank networks built to handle the light traffic of the 1990s, will be strained to support the flow of images, streaming video, voice, and data. Switches, routers, bandwidth, and other network components will be upgraded to ensure the flow of information and improve the stability of bank networks. In an effort to contain costs, many banks will replace their old phone systems with new IP telephony systems. These new systems will improve network utilization, consolidate circuits, and in turn, save big dollars in telecommunications costs. Additionally, bankers will monitor the health and performance of their networks, just as they do their balance sheets, resulting in more effective network planning and more stable, safe networks. 7. Video Collaboration Tools Along with network infrastructure improvements, bankers will see increased use of video throughout the enterprise. Video collaboration will take on many forms from high-definition displays in lobbies, conference rooms, and offices to videoconferencing via webcams and

© 2009 William Mills Agency

34

laptops, all the way up to sophisticated telepresence systems. High travel costs, a limited number of flights, and the general hassle of travel these days, will help to increase demand for such video tools as bankers tire of hopping planes or taking long drives just to meet briefly, face-to-face with employees at remote locations. Instead, bankers will use unified communications tools to conduct one-on-one or one-to-many videoconferences on the fly and inexpensively, simply by flipping open their laptops, saving time and increasing productivity in the process. 8. Security Gets Serious As security breaches become more prevalent and criminals get more sophisticated, bank customers demand the best possible security measures from their banks. No banker wants to be front-page news due to being the victim of a security breach. Imagine facing customers, the media, and regulators after a security incident and telling them your bank was containing costs and cutting corners regarding security, so the hackers penetrated your systems easily and stole the identities of your customers. Don’t expect much sympathy or a pat on the back for being frugal. Security is not an area in which to pinch pennies, especially in 2009. When asked, “What are your bank’s technology concerns?” bankers cited “managing risk” and “protecting data and infrastructure” as their top two priorities, according to the 2008 ICBA Community Bank Technology Survey. Hiring more people and throwing them at the problem is a costly, losing proposition as it has become humanly impossible for bank personnel to protect their networks 24/7 as is required. Bankers will continue to outsource security to trusted, third-party providers who can bring more resources to bear at a lower cost structure. 9. Customer Information Security Extends Beyond the Bank Threats to customer information will take on a more sinister tone in 2009 as cybercrime gets organized and attacks on banks’ customers become more prevalent. Malware will continue to infect unprotected customer PCs resulting in Trojan horses that steal customer login information and allow the perpetrator to engage in criminal activity, ranging from basic identity theft to initiating fraudulent ACH credits. Spearphishing, a targeted form of phishing, will grow and become a leading cause of malware infection. Bankers will grow weary of customer fraud claims, which could have been prevented with basic PC security measures, and will begin requiring minimum security thresholds for customer systems. Also, more security tokens will be issued to business customers in an effort to mitigate cybercrime. Payment Card Industry Data Security Standards (PCI DSS) will help banks indirectly as merchants and service providers are forced to comply with the new standards to protect cardholder data and beef up their security. One of the requirements of the new version 1.2 of the PCI DSS is the sunsetting of Wired Equivalent Privacy (WEP) wireless security by June 2010. Many merchants are still hacked wirelessly from their parking lots due to no security or weak wireless security such as WEP. 10. Regulators Add Muscle To some, the financial crisis of 2008 was due to subprime lending, derivatives, high oil prices, high unemployment, and tumbling home prices. For others, it was simply a lack of regulatory oversight. Emboldened and empowered, expect regulators to take a “not on my watch again” attitude in 2009 as they descend on banks armed with more resources (read ammunition) than in years past.

© 2009 William Mills Agency

35

In late 2008, the FDIC approved its 2009 operating budget, which adds 1,459 staff positions and represents an increase of more than $1 billion from 2008. Expect insider fraud to increase as economic conditions hit close to home and some people, desperate to make their next mortgage payment or maintain their current lifestyle, resort to embezzlement, fictitious loans, and other illegal activities. Effective internal controls, a strong internal and external audit function, and using technology to detect such fraud will be imperative in 2009. Prudence and practicality aside, regulators will demand such measures. Summary In the words of Rudyard Kipling: “If you can keep your head when all about you / Are losing theirs…/ You’ll be a Man, my son!” 2009 will certainly be a time to keep one’s head and remember that the race is won through seeking wisdom, practicing persistence, and spotting opportunity when others only see danger. Those who manage information best, keep it secure, and make informed decisions regarding technology investments, will surely survive, thrive, and win the race to high performance in 2009 and beyond. Securas Consulting Group LLC provides world-class, client-driven consulting services. Our services are designed and delivered for today’s high-performing financial institutions. We offer technology planning, risk management, business tech solutions, IT support and managed services, and business continuity planning…consulting solutions for today’s 24/7, always-on world. Contact Jimmy Sawyers at [email protected] or call 1.901.888.STAR (7827). Visit www.securas.com for more information. Want to see how Jimmy’s predictions stacked up in past years? View his predictions for 2005, 2006, 2007 and 2008 at: www.securas.com

© 2009 William Mills Agency

36

Redefining the Value Experience in Banking

By Dennis Roman Chief Marketing Officer TCS Financial Solutions Radical shift in thinking – tearing down the walls of the bank to bring in the customer in the truest sense Financial upheavals across the globe have left many ailing institutions bracing for survival. Those that are in good shape are making quick decisions on how to gain competitive advantage while others are assessing the damage. As a leading IT solutions provider for financial services institutions across the globe, we at TCS Financial Solutions, look at what the New Year will bring for banks, our customers, in the form of a new paradigm. We believe that we will soon witness a radical shift in the way banks deliver customer experience. This could result in bankers literally tearing down of the walls of banks to bring in their customers. Reorienting towards this paradigm will herald the advent of new business models and selective investment, by bankers, in technology innovation to gain market and position for growth. Innovation is a bright spot for banks left unscathed by the recent credit debacles, and who see a clear opportunity to distance themselves from their rivals and gain a sustainable first-mover advantage. Banks across the world – those who are consolidating and those setting out with renewed focus (and some caution) – will deploy customer insights gained into service and process innovation to improve customer relationships and provide a sustainable advantage. Growth opportunities in technology innovation would begin from consulting and integration services to next-generation software architectures and services (SOA and BPM and SaaS), to IT outsourcing and governance. The demand for BPO services will also rise for reasons of better cost visibility and variability related to volume fluctuations. Service, value and convenience will be the mantras of success. Process and service innovation will create value for banks by attracting customers through simplicity and efficiency. Organizations will have to embed this idea into their processes, people, systems and business partners to be successful. With the increasing consolidation we are now witnessing in the banking industry, the approach is to reduce spending and free up investment capacity for a few vital technology projects. This will spur a surge in technological innovation in the form of client facing, collaborative, analytical and risk management applications.

© 2009 William Mills Agency

37

Further, for wealth management and transaction services units that have sustained exemplary performance in the past year, demand is picking up in selected emerging market locations, while the unbanked customer segment continues to present untapped potential. Going forward, we will see a growing interest in automation solutions that will help banks reach high-volume, low-value customers and link corporate performance management with finance, accounting and risk management. A proactive approach to gaining visibility into credit exposures and operational performance will attain primary status. Advanced customer and profitability analytics, and the streaming of pervasive information and unstructured data will lead to customer segmentation-specific services and transactions. A fresh generation of applications (from SOA and BPM related to Web 2.0) will emerge in areas such as multifunctional collaboration, targeted marketing, multimedia delivery, and personalized customer experience. In this article, we outline the characteristics that will shape this new persona of banking in 2009 and the related approaches that banks are likely to adopt. A Quantum Leap in Customer Experience and Agility As we said earlier, this new paradigm of banking will drive customer-centricity, which will manifest itself in the form of customer profitability analytics, relationship and dynamic pricing, and a completely new way of looking at customer relationships. Transforming customer comfort levels, for banks, would mean increasing transparency, providing the “right” information to customers instantaneously, and using the right technology applications to make this happen. The focus will shift from products, with banks lowering the costs of serving customers. Relationship-based selling and interactions with customers supported by real-time or at least intra-day analysis of internal and external customer data, will eventually lead to banking becoming more personal. Now, how does this connect with technology? Creating a unique customer experience will begin with banks enforcing simple, consistent customer-aligned processes through the efficient use of next generation architecture and services such as Service-Oriented Architecture, Business Process Management and SaaS. This implies restructuring data warehouses, and a greater adoption of content management and BPM technology to automate decision-making. It will also include the ability to adapt raw products to the individual needs and desires of customers to create individual products or custom products for complex financing, or third-party products to facilitate efficient bundling. Products will need to knit together a mix of solutions – current accounts, loans, derivatives, stocks and funds and insurance – and personalize them for customers (such as high-net-worth-customers or corporate groups). These offerings will be strong on customer longevity and answer diverse demands. In short, we are looking at the emergence of mass personalization in services and products. Agility and transformation 2009 will be a period when banks look to equip themselves on agility – in the form of increased operational efficiency, reduced operating costs, improved overall customer experience, and a holistic approach to risk management. Naturally, this would mean adopting a “do-more-with-less” philosophy; for instance, outsourced services in the ITO and BPO spaces will need to be paired with offshore or “nearshore” deliveries, to drive down costs. Outsourcing core competencies may take on a new meaning as the competency that banks wish to outsource may be redefined. IT and operations will be viewed in a symbiotic manner, where the greater integration of IT and operations to deliver increased value to the business – and the customer –

© 2009 William Mills Agency

38