banking in emerging markets - seizing oppurtunities ... · needed antidote to the challenges of...

TRANSCRIPT

Banking in emerging markets

Seizing opportunities, overcoming challenges

ContentsIntroduction 3

Section one

Section two

Section three

2 www.ey.com/banking

Introduction

Yet these markets are far from homogenous. Success for both global and local banks operating (or seeking to operate) in them is contingent on understanding the specific opportunities that exist in each and overcoming the inevitable, and sometimes unique, challenges.

With expanding economies and a fast-growing customer base for financial services, the emerging markets are an attractive prospect for any bank looking to grow its revenues. They also provide a much-needed antidote to the challenges of some developed markets.

However, the financial prospects and needs of emerging market customers tend to be much more fluid than those in developed markets. Many of the economies remain volatile, and an economic shock can dampen the appetite for banking products. Technological advancement can open up previously inaccessible and unprofitable customer pools. As things can change so rapidly, it is important for financial institutions in these markets to monitor the evolving appetite for products and services, to understand what is driving demand and to identify how they can operate most profitably.

Ernst & Young has launched a survey to help track changes in sentiment in the emerging markets and to provide insight into opportunities and challenges for both domestic and international banks operating in these markets. This report initiates our emerging market coverage and incorporates the results from the first edition of the survey.

We focus on 10 rapid-growth markets (RGMs) that our clients have identified as part of the next wave of developing markets beyond the BRICs:

Nigeria, Vietnam

Colombia, Egypt, Indonesia

Chile, Malaysia, Mexico, Turkey, South Africa

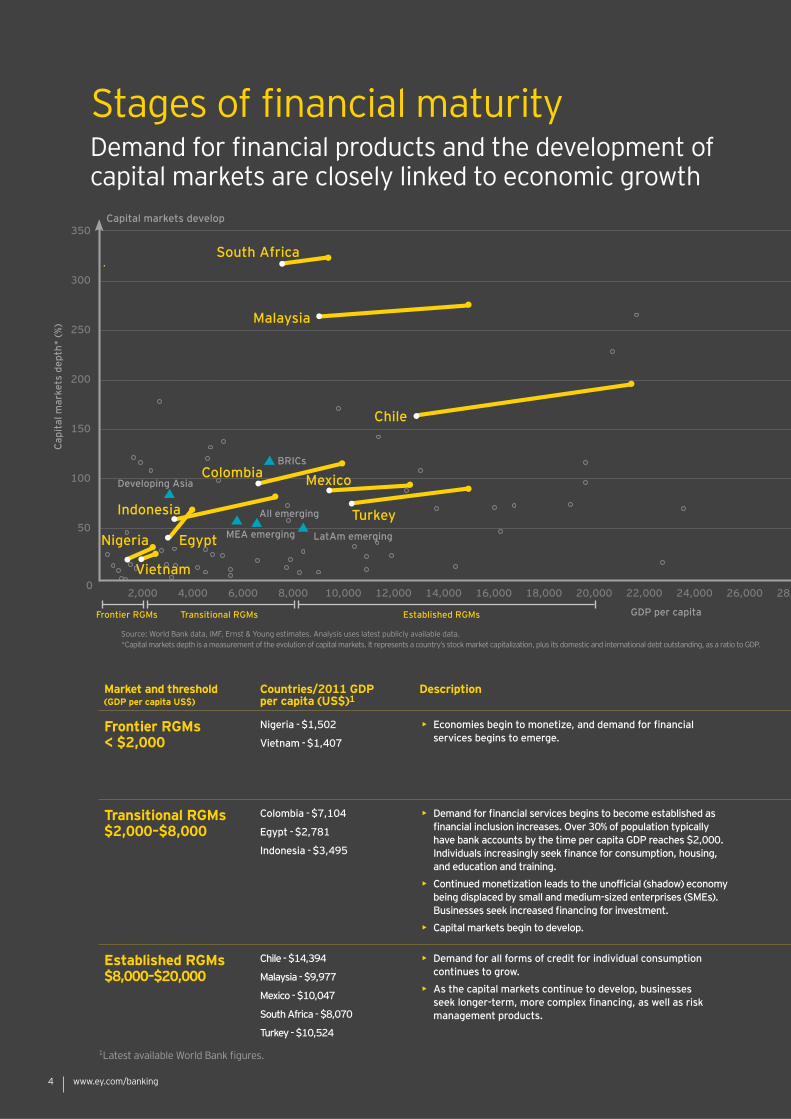

We have also selected these markets because they are at different stages of financial maturity. Our frontier RGMs have per capita GDP below US$2,000, the point at which deposit and savings products typically emerge. Our established RGMs have all exceeded US$8,000 per capita GDP, the point at which credit products become established. Our transitional RGMs lie between the two. These 10 markets can therefore stand as proxies for other countries at similar stages of evolution.

Despite their differences, there is a common thread running through all of these markets. These countries are experiencing rapid growth and, as their economies grow, they are seeing dramatically increased demand for banking products and services. Banks operating in these markets face some similar challenges:

How can they serve the unbanked without developed market infrastructure?

How can they meet growing demand for retail and corporate lending when their balance sheets are constrained or the capital markets are underdeveloped?

competition?

Identifying and learning lessons from institutions in markets that have already faced similar challenges, and successfully adapting them to their local context, will be key to the success of banks looking to exploit growth opportunities in these economies. We hope this report will provide some food for thought on addressing both the opportunities and the challenges. This report deals with the 10 RGMs at a global level and the companion report contains specific analysis on each of the 10 markets. Both have been developed through a survey and interviews with senior executives from more than 50 major institutions operating across these markets, conducted in Spring 2013. The banks represented account for over 40% of the combined banking assets across these markets and include most of their largest domestic banks and a sample of global banks.

Where is growth expected? What products do customers want? What investments should be made to compete successfully? How are other banks responding to opportunities and challenges? These are some of the key questions our clients are asking themselves about the emerging markets.

3Banking in emerging markets

Stages of financial maturityDemand for financial products and the development of capital markets are closely linked to economic growth

1

Source: World Bank data, IMF, Ernst & Young estimates. Analysis uses latest publicly available data. *Capital markets depth is a measurement of the evolution of capital markets. It represents a country’s stock market capitalization, plus its domestic and international debt outstanding, as a ratio to GDP.

BRICs

South Africa

Nigeria

Indonesia

Mexico

Frontier RGMs

Market and threshold (GDP per capita US$)

Countries/2011 GDP per capita (US$)1

Description

Frontier RGMs < $2,000

Transitional RGMs $2,000–$8,000

Established RGMs $8,000–$20,000

www.ey.com/banking4

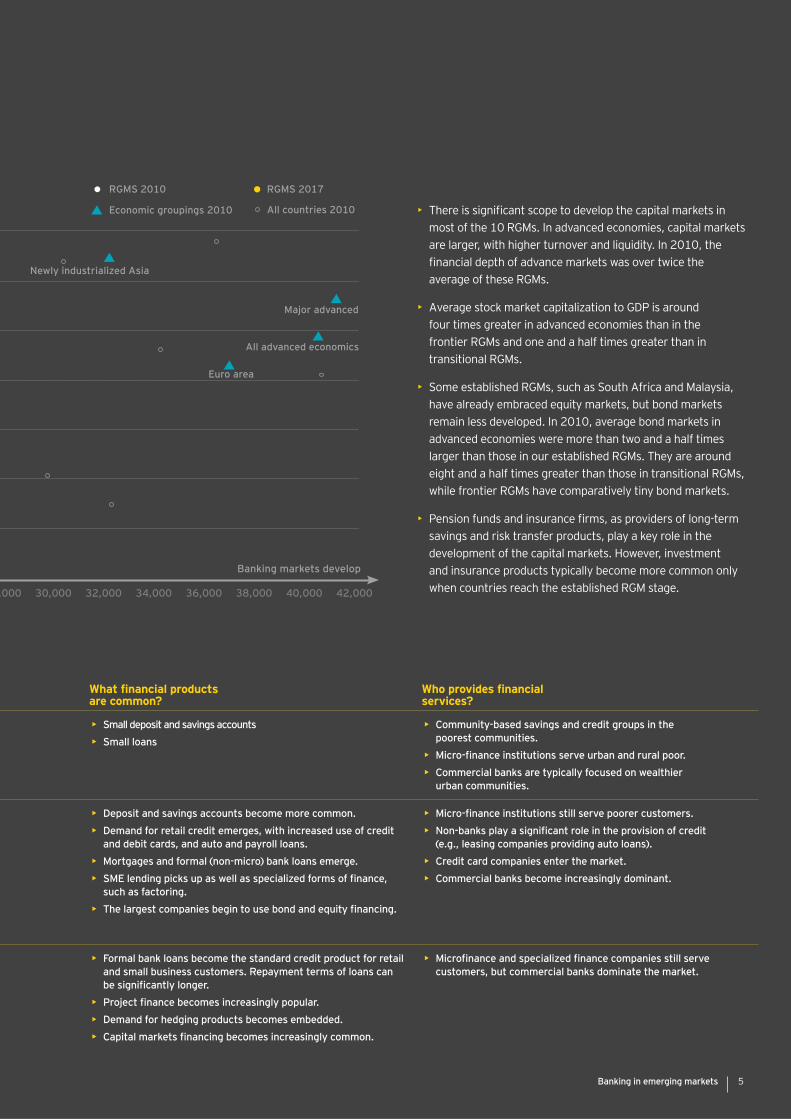

most of the 10 RGMs. In advanced economies, capital markets are larger, with higher turnover and liquidity. In 2010, the

average of these RGMs.

Average stock market capitalization to GDP is around four times greater in advanced economies than in the frontier RGMs and one and a half times greater than in transitional RGMs.

Some established RGMs, such as South Africa and Malaysia, have already embraced equity markets, but bond markets remain less developed. In 2010, average bond markets in advanced economies were more than two and a half times larger than those in our established RGMs. They are around eight and a half times greater than those in transitional RGMs, while frontier RGMs have comparatively tiny bond markets.

savings and risk transfer products, play a key role in the development of the capital markets. However, investment and insurance products typically become more common only when countries reach the established RGM stage.

What financial products are common?

Who provides financial services?

Euro area

Major advanced

5

Executive summary

But amid the bullishness throughout these RGMs lie creeping concerns about the ability of local banks to maintain profitability and capture market share as balance sheets come under pressure and resources become constrained in an increasingly competitive environment. The need to find new sources of funding and the need to grow and nurture talent are both key issues at an industry level.

The potentially volatile nature of these markets can also make global banks hesitant to commit the resources necessary to establish a major presence there, for fear that political or social upheaval might erode profitability or damage their reputation. However, there are significant long-term opportunities for international banks willing to make the commitments necessary to capitalize on them.

To achieve profitable growth, banks in these markets must balance their desire to expand rapidly with the need to do so efficiently. As a result of the pressures of funding, competition and declining margins, efficiency is already rapidly becoming the watchword of RGM bankers. Domestic banks are looking to maximize returns on existing assets and cut costs. However, they must also invest in growth, and some of these cost savings will need to be reinvested in growth areas.

We have four core initiatives that banks need to focus on as they look to overcome the challenges and capture the growth in these markets. Key to each of these will be identifying where the lessons of other markets, emerging or developed, can be applied locally, and how they should be adapted to take into account local variances. The specific investments that banks must make will depend not only on the markets in which they are operating, but also on the segments they are targeting, as well as their own existing capabilities.

There

cost retail products from poorer customers. Banks must not only meet that demand, but also move ahead of it.

Strong capabilities in debt and equity financing will be increasingly important for banks looking to fund transformative infrastructure programs and for businesses looking to expand domestically and overseas, especially in transitional and established RGMs. Demand for credit in these

markets is expected to be high, but domestic banks, with restricted balance sheets, may struggle to meet this demand. Without significant investment in corporate and investment banking capabilities, international and regional banks with large balance sheets and access to cheaper funding will gain market share in these areas.

Advisory services and hedging products will be critical for banks that want to retain and grow with their business customers. As companies, particularly those in more established RGMs, expand their presence beyond domestic borders, they will need support to manage the risks and complexities of international trade. Many domestic banks already play a leading role in the provision of hedging products, but they will need to invest to develop more advanced products as their clients’ needs evolve. As clients look for support with cross-border expansion, banks that have already expanded into neighboring markets will have local knowledge and be better placed to offer their clients the advice they need. If this support cannot be provided locally, businesses are likely to look to regional banks with a pan-continental presence across South America, Africa or Asia for guidance.

New wealth management products are needed to persuade the affluent to invest onshore. While the wealthiest investors are likely to favor established global wealth management brands, we believe local banks that offer a broad range of products and services will be better positioned to capture and nurture mass-affluent customers. As opportunities for domestic investment become more established, high-net-worth individuals may also be tempted to invest some of their wealth onshore, using local institutions for some of these services.

Low-cost retail banking products will be critical for banks expanding lending into lower-income segments. Many institutions have been reluctant to serve this customer base, as it is costly to manage a high volume of low-value transactions. But with the limits of easy growth being reached in more established RGMs, banks now see the unbanked segment as an opportunity. However, many traditional products are inappropriate to the needs of these individuals, and we believe banks targeting this segment must develop innovative products that can better match customer needs at a lower cost to both customers and the bank.

There is a wealth of optimism in our 10 rapid-growth markets (RGMs). Retail banks are growing as increasing affluence in under-penetrated banking markets drives demand for more financial products and services. Corporate and investment banks are expanding as government programs, aimed at improving infrastructure and public services and attracting foreign investment, create the conditions for business growth.

6 www.ey.com/banking

This will give an edge to banks without the funding, capacity or expertise to serve new segments independently.

Collaborating with a global institution can give domestic banks, and their customers, access to stronger balance sheets and greater technical know-how. This offers a convenient way for banks in frontier and transitional RGMs to build employees’ skills as resources become increasingly constrained. By collaborating with local banks, global institutions can gain local knowledge and access to new markets without large investments in distribution networks.

Partnerships with telecommunications companies can give banks across our 10 RGMs access to new mobile banking technology without significant investment costs. We believe telecommunications providers are unlikely to develop their own suite of banking products, as they would be subject to increased regulation and capital requirements and would require a larger balance sheet to support lending. Alliances such as these will help banks reach rural and unbanked segments more efficiently than by establishing a branch network. Although the needs of unbanked customers will initially be limited, those banks that have established relationships at this early stage will be better placed to capture market share as customers’ needs expand.

Partnerships with micro-finance institutions can give local banks with strong balance sheets the opportunity to diversify into higher-margin segments without recruiting a wide network of skilled agents to assess customers, while giving micro-finance institutions access to greater funds. This will be crucial for banks in transitional and established RGMs that are beginning to target higher-yielding customer segments to offset margin compression. It will also help banks in some countries meet government policy requirements to target lending to these areas.

This will be critical

the credit curve to boost margins. Innovative approaches to risk management will help banks that are targeting higher-risk customer segments, such as those with no credit history.

Developing new ways to assess credit risk, such as mobile phone usage or utilities payment data, is vital as more individuals and businesses with limited credit histories require financial services. This is recognized as a key concern by bankers in frontier markets, where the economies are less stable and where many customers are new to banking and therefore have no credit histories. Banks in these markets should also consider adapting credit products to more closely match the needs and lives of less affluent customers.

Advanced risk management capabilities are critical for banks moving down the credit curve to boost margins. Competition for deposits and lending is putting interest margins under pressure, and banks in transitional and established emerging markets are beginning to diversify from simpler lending products into higher-risk segments such as micro- and unsecured lending. The need for strong credit risk assessment is recognized as a key priority by some but will need to be a focus across all banks if they are to avoid repeating the mistakes of the past.

This is a crucial enabler of low-cost, high-touch banking in all markets. Technology will be a critical factor in reaching new retail customers without the cost of establishing extensive branch networks, and improving relationships and cross-selling prospects with existing customers. However, adapting technology to deliver the right service to

Mobile technology and other innovative distribution models will reduce the cost to serve, giving banks access to untapped customer pools. This is particularly important in frontier and transitional RGMs, where the cost of operating an account is a significant barrier to financial inclusion.

Developing the mobile channel and using technology to improve customer service can give customers more flexibility in the way they engage with their bank and provide a source of fee income to offset declining interest margins. This is critical in established RGMs, where banks are increasingly seeking opportunities to deepen relationships with and cross-sell to existing customers. It is also important to minimize additional costs.

Core banking technology and automation will improve efficiency and streamline processes, enabling banks to alleviate staffing pressures by rebalancing employees from manual back office roles to the front office, to support growth areas. This will become increasingly important as frontier and transitional economies become more established.

The paths to profitable growth will be different in each country and for each institution, but bankers in these markets can learn from the lessons of others that are in, or have come through, similar situations. As demonstrated by those that have tried and failed, banks will struggle to make the investment required to be successful in all areas of the business. With many of these markets moving into the next phase of growth, banks have the opportunity to assess their current capabilities and leverage them to focus on areas of strength and target investment in key growth segments.

7Banking in emerging markets

8 www.ey.com/banking

Bankers in our 10 RGMs are bullish. The vast majority believe their bank’s performance will improve over the next year, building on strong customer demand in expanding economies (Figure 1). The contrast with developed economies is marked. When questioned on their expectations for their bank’s performance, almost 80% of respondents in our RGMs forecast improvement. When their European counterparts were asked about future performance, just 37% expected improvement. A quarter feared their bank’s performance would deteriorate.1

The optimism of our interviewees is founded on long-term expectations for economic growth. While not unscathed by the financial crisis (of the 10 RGM economies, five contracted in 2009), these countries recovered swiftly and all have exceeded 2008 GDP levels. Projections of future growth are also well in excess of developed markets — Eurozone GDP is unlikely to recover to 2008 levels until 2014-15.

Nonetheless, these markets are far from homogenous. The strongest growth is predicted in our frontier markets and those transitional markets with the lowest per capita GDP: Vietnam, Nigeria, Indonesia and Egypt are all expected to see GDP growth of 6%-7% a year by 2015. These markets have the lowest base to grow from, but even our other RGMs should achieve between 3% and 5% growth. In developed markets, the strongest growth is forecast for the US, but this will only be around 3% by 2015 — the lowest level of growth anticipated across our RGMs.2

Despite these forecasts, the volatile nature of these economies means growth can be derailed by political and social upheaval. This is especially a problem for frontier and transitional economies, where growth is not as embedded as in more established RGMs. While 56% of all respondents are positive about their country’s economic prospects, there is pessimism from some who expect their economies to deteriorate (Figure 2).

Section one A tale of tempered optimism in banking

1European Banking Barometer (Autumn/Winter), Ernst & Young, 2012. 2World Economic Outlook, IMF, April 2013

Figure 1: Financial performance

Frontier RGMs

Note: Percentage of respondents answering “don’t know” is not displayed

Figure 2: Economic outlook

Frontier RGMs

Note: Percentage of respondents answering “don’t know” is not displayed

9Banking in emerging markets

Perhaps not surprisingly, political stability and security is seen as a key issue facing the Egyptian economy where, in the wake of the Arab Spring, our respondents are equally split on whether the economy will improve or deteriorate. Nigerian respondents, who have witnessed a resurgence in kidnappings and pipeline vandalism, cited similar concerns. The greatest pessimism is in Colombia, where industrial action and protests have disrupted the coal and coffee industries (Colombia’s second- and third-biggest exports) in recent months. Two-thirds of Colombian respondents feel the economy will deteriorate over the next 12 months. Social and industrial unrest is also of concern in South Africa, where study respondents were muted in their optimism for growth and some expect a slight deterioration.

More broadly, interviewees are worried about whether the potential in these markets will actually be realized. This was underscored by comments from a number of interviewees that a lack of investment in infrastructure has kept the cost of doing business high; they called for both more investment and improved delivery on existing projects. These discordant notes serve as a warning to anyone thinking the emerging markets offer unfettered growth.

Despite occasional misgivings about the economic outlook, interviewees were overwhelmingly confident about their bank’s prospects. Only 2% of respondents fear their bank’s performance will decline over the next year. There is variance in the outlook for business lines, however (Figure 3). Respondents are most positive about retail financial services and corporate banking. It is more straightforward to capture natural growth in these areas, where products remain vanilla, rather than in the more complex capital markets products. As a result, interviewees expect an increase in both retail deposits and lending, as well as growth in the small and medium-sized enterprise (SME) segment.

Bankers across these markets also expect wealth management to be a growth area as an increasing number of affluent individuals look for more sophisticated savings and investment products. There is also the hope that, over time and as these economies become more stable, a greater proportion of wealthy customers will keep their assets onshore instead of banking in offshore centers such as Miami, Singapore and Switzerland.

There is less optimism about investment banking. Historical analysis suggests that debt and equity markets only become more developed when countries reach about US$6,000 per capita GDP. It is therefore unsurprising that respondents in Vietnam, Egypt and Nigeria are ambivalent about the outlook for investment banking. Perhaps more surprising is that fewer than half the interviewees in South Africa and Malaysia — countries that have begun to embrace the capital markets — expect the outlook for issuance and advisory to improve beyond current levels. However, banks in both these

countries do face intense competition in investment banking from international firms with a more global reach.

Later in this report, we will explore in more detail the outlook for banks serving individuals (section two) and businesses (section three), but it is readily apparent that there will be significant opportunities in each. And not just for domestic banks. Regional and global banks are also looking for opportunities to acquire new customers and increase market share in these countries. However, capitalizing on the potential in these markets will not be straightforward, and the general bullishness of respondents should not disguise the challenges that institutions in these markets face.

Banks in emerging markets are increasingly concerned about their ability to maintain returns on equity as multiple pressures challenge profitability (Figure 4). One interviewee spoke of a “fundamentally lower ROE and ROA environment from a combination of margin compression, changing capital and liquidity requirements, further sector liberalization, greater operational flexibility of foreign banks and cost pressure from investments.”

If local banks are to achieve their expected growth targets, and if foreign banks are to expand successfully, they must address a triple threat to profitability that is becoming a growing concern across our RGMs:

A. Margin compression

B. Increased competition and cost of doing business

C. Impact of domestic and international regulatory changes

Figure 3: Business line outlook

Securities services

Securities trading

Trade finance

issuance

Project finance

Note: Percentage of respondents answering “don’t know” is not displayed

10 www.ey.com/banking

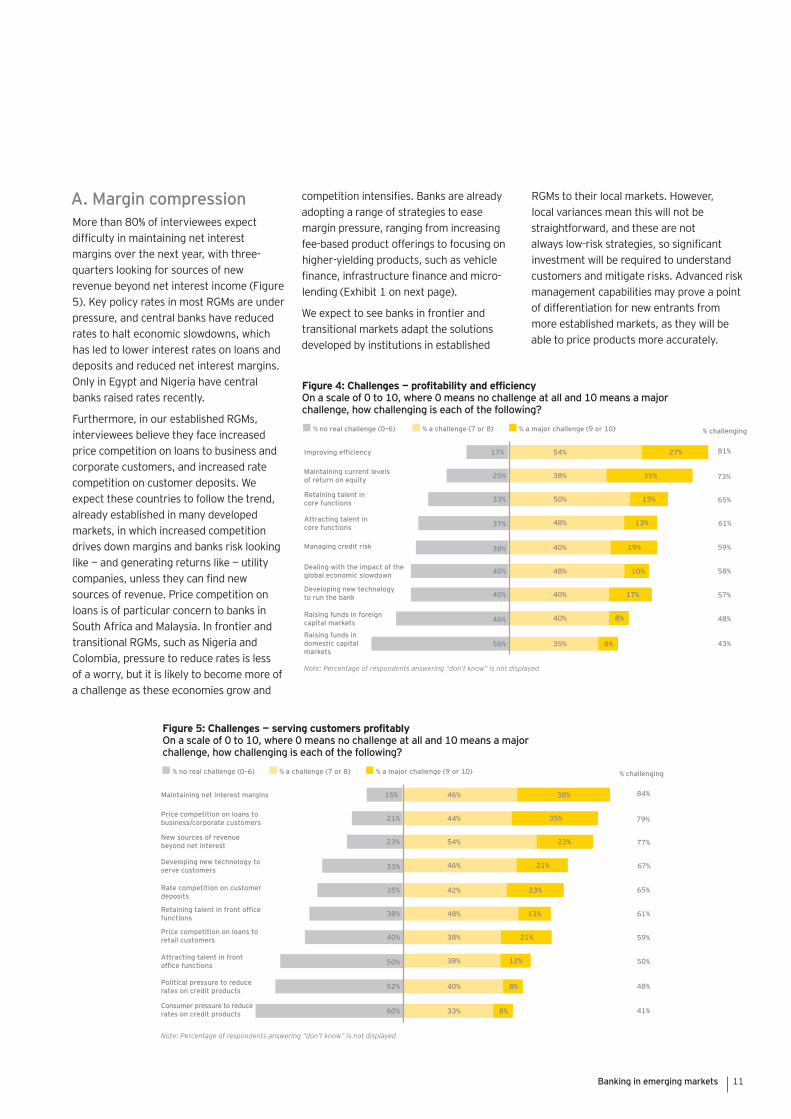

More than 80% of interviewees expect difficulty in maintaining net interest margins over the next year, with three-quarters looking for sources of new revenue beyond net interest income (Figure 5). Key policy rates in most RGMs are under pressure, and central banks have reduced rates to halt economic slowdowns, which has led to lower interest rates on loans and deposits and reduced net interest margins. Only in Egypt and Nigeria have central banks raised rates recently.

Furthermore, in our established RGMs, interviewees believe they face increased price competition on loans to business and corporate customers, and increased rate competition on customer deposits. We expect these countries to follow the trend, already established in many developed markets, in which increased competition drives down margins and banks risk looking like — and generating returns like — utility companies, unless they can find new sources of revenue. Price competition on loans is of particular concern to banks in South Africa and Malaysia. In frontier and transitional RGMs, such as Nigeria and Colombia, pressure to reduce rates is less of a worry, but it is likely to become more of a challenge as these economies grow and

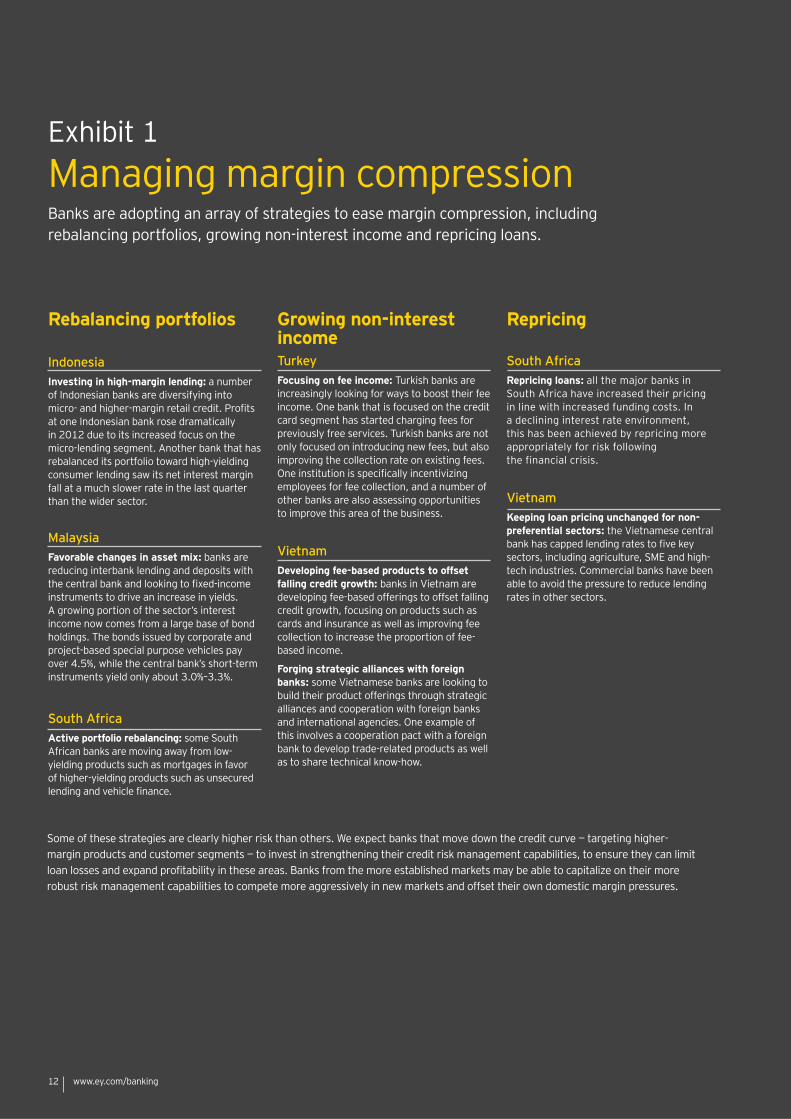

competition intensifies. Banks are already adopting a range of strategies to ease margin pressure, ranging from increasing fee-based product offerings to focusing on higher-yielding products, such as vehicle finance, infrastructure finance and micro-lending (Exhibit 1 on next page).

We expect to see banks in frontier and transitional markets adapt the solutions developed by institutions in established

RGMs to their local markets. However, local variances mean this will not be straightforward, and these are not always low-risk strategies, so significant investment will be required to understand customers and mitigate risks. Advanced risk management capabilities may prove a point of differentiation for new entrants from more established markets, as they will be able to price products more accurately.

Figure 4: Challenges — profitability and efficiency

core functions

Raising funds in foreign

core functions

Raising funds in

Note: Percentage of respondents answering “don’t know” is not displayed

Figure 5: Challenges — serving customers profitably

office functions

New sources of revenue

functions

Note: Percentage of respondents answering “don’t know” is not displayed

11Banking in emerging markets

Rebalancing portfolios

IndonesiaInvesting in high-margin lending: a number of Indonesian banks are diversifying into micro- and higher-margin retail credit. Profits at one Indonesian bank rose dramatically in 2012 due to its increased focus on the micro-lending segment. Another bank that has rebalanced its portfolio toward high-yielding consumer lending saw its net interest margin fall at a much slower rate in the last quarter than the wider sector.

Favorable changes in asset mix: banks are reducing interbank lending and deposits with the central bank and looking to fixed-income instruments to drive an increase in yields. A growing portion of the sector’s interest income now comes from a large base of bond holdings. The bonds issued by corporate and project-based special purpose vehicles pay over 4.5%, while the central bank’s short-term instruments yield only about 3.0%–3.3%.

South AfricaActive portfolio rebalancing: some South African banks are moving away from low-yielding products such as mortgages in favor of higher-yielding products such as unsecured lending and vehicle finance.

Growing non-interest income

Focusing on fee income: Turkish banks are increasingly looking for ways to boost their fee income. One bank that is focused on the credit card segment has started charging fees for previously free services. Turkish banks are not only focused on introducing new fees, but also improving the collection rate on existing fees. One institution is specifically incentivizing employees for fee collection, and a number of other banks are also assessing opportunities to improve this area of the business.

Developing fee-based products to offset falling credit growth: banks in Vietnam are developing fee-based offerings to offset falling credit growth, focusing on products such as cards and insurance as well as improving fee collection to increase the proportion of fee-based income.

Forging strategic alliances with foreign banks: some Vietnamese banks are looking to build their product offerings through strategic alliances and cooperation with foreign banks and international agencies. One example of this involves a cooperation pact with a foreign bank to develop trade-related products as well as to share technical know-how.

Repricing South AfricaRepricing loans: all the major banks in South Africa have increased their pricing in line with increased funding costs. In a declining interest rate environment, this has been achieved by repricing more appropriately for risk following the financial crisis.

Keeping loan pricing unchanged for non-preferential sectors: the Vietnamese central bank has capped lending rates to five key sectors, including agriculture, SME and high-tech industries. Commercial banks have been able to avoid the pressure to reduce lending rates in other sectors.

Exhibit 1Managing margin compression Banks are adopting an array of strategies to ease margin compression, including rebalancing portfolios, growing non-interest income and repricing loans.

Some of these strategies are clearly higher risk than others. We expect banks that move down the credit curve — targeting higher-margin products and customer segments — to invest in strengthening their credit risk management capabilities, to ensure they can limit loan losses and expand profitability in these areas. Banks from the more established markets may be able to capitalize on their more robust risk management capabilities to compete more aggressively in new markets and offset their own domestic margin pressures.

12 www.ey.com/banking

New, foreign entrants are reshaping the banking landscape in many of these RGMs (Figures 6 and 7). These new entrants are not all from developed markets. Banks from neighboring countries are identified as the greatest competitive threat in Egypt, Nigeria, Malaysia, Indonesia and Colombia. In Colombia, for example, where all respondents see regional banks as their main threat, institutions from Brazil, Mexico and Ecuador have stated intentions to be operating in Colombia by the end of 2013.

We are beginning to see the emergence of pan-Latin American, pan-African and pan-Asian retail banking networks. Regional competitors are beginning to reach the limits of easy growth in domestic markets, and there is real potential for those with strong balance sheets to apply the lessons they have learned in their home markets to serve similar customer segments in neighboring countries. Such institutions will become increasingly important in meeting the expected demand for retail banking products over the longer term.

In the wake of the global financial crisis, a number of developed market banks exited some of their emerging market operations. In some cases, these institutions had expanded too quickly into new markets, which did not deliver on their potential. Facing capital, political and profitability pressures in their home markets, these banks decided to retrench. However, the financial crisis has not drawn a line through international expansion, and nearly two-thirds of respondents see European or US banks as a main source of competition. Global banks are once again looking at opportunities in emerging markets, but they are now more selective in their investment decisions. Institutions are increasingly restricting their growth ambitions to neighboring markets or to countries where they have an historic or cultural affinity, as illustrated by European banks being identified as the main competitive threat in Turkey and Mexico. With the retail banking offerings becoming increasingly evolved in our RGMs, and in the face of strong regional competitors, developed market banks also need to ensure they have sufficiently differentiated products and

offerings to compete against local institutions with established customer relationships, and think about how they can operate in these markets most efficiently (see Exhibit 2 on next page). As a result, the focus of many international banks will be on capital markets and wealth management, where local institutions do not yet have the same global reach and technical know-how.

Increased competition, from a combination of global, regional and domestic banks, means banks must strive harder to attract and retain customers — particularly those in the most profitable segments — as well as counteract the impact of greater price competition. Bankers in established RGMs already recognize the important role of technology in doing this; over 80% of interviewees in Malaysia, South Africa and Mexico see

Figure 6: The banking landscape

*Of those who agree there will be a significant change to the banking landscape in their countries

nor disagree

Figure 7: Main sources of competition

countries or the

*Percentage of those who considered that foreign banks would become a source of competition

No answer

13Banking in emerging markets

Expansion into any new market can be fraught with complexity. Getting it wrong can erode profitability and damage an institution’s reputation. More than one-third of CFOs underestimate the costs involved in entering emerging markets, and 40% underestimate the time.3 As many of these markets are already quite sophisticated in their retail and commercial offerings, new entrants need to determine which sub-sectors offer the greatest potential and how they can differentiate themselves from local competition, — for example, through technology and innovation to bring down the cost of serving customers in these markets, or through enhanced product or service capabilities.

Developing the right underlying operating model is also essential for new entrants. There are, in essence, three models new banks tend to pursue:

1. The local operating model, where all the systems and infrastructure supporting a country’s operations are located in that country. This model is likely to be used in markets where local regulations require back office functions to be located in-country. This model can make it difficult to serve smaller or lower-margin markets effectively.

2. The regional hub, whereby countries in a region may share systems and operations hosted in a single country. This model can be more cost-effective, but the markets it supports require a degree of harmonization and therefore may only work across a smaller number of relatively homogenous markets rather than an entire continent.

3. A centralized operating model, where the infrastructure and systems for all countries, either globally or in a particular region, are located (as much as possible) in a single country. This model is more efficient than the regional operating model but may not be able to cope with the inconsistent demands of the local markets it serves.

Regulators do not necessarily allow all these models — for example, companies may be required to locate their back office in the country of operation. New entrants must therefore consider the impact of such regulations on their ability to function profitably in these markets.

The quality and reliability of local infrastructure will also influence a variety of issues, from the requirement for a branch structure to the cost of cash management. And the availability of a sufficiently skilled and experienced workforce will be a factor if banks are to avoid big recruitment and retention challenges.

Finally, banks must consider their mode of entry. Here again options may be limited by local regulations. Joint ventures can offer foreign banks access to local market knowledge and offer local banks access to greater technical know-how and a broader range of products. However, if institutions have different objectives, in addition to the challenge of different cultures, joint ventures may prove unsuccessful.

Entry by acquisition can give investors greater control than a joint venture and provide quick access to market share, skills and existing distribution channels. However, valuations of targets in emerging markets can be difficult; disclosure requirements may not be as rigorous as in the acquirer’s home market; and corporate governance not as robust. Again, ensuring cultural alignment will also be crucial, particularly if resource challenges force banks to bring in staff from offices in other markets.

Acquisition is not always possible, as local regulations in many markets limit foreign ownership of companies. As an alternative, banks might consider establishing a branch or a subsidiary. Of these, a branch can be less costly and more efficient than establishing an independent, separately capitalized subsidiary — a situation that will be exacerbated by moves to Basel III. However, as a branch can be more difficult to resolve in the event of the failure of a banking group, regulators are increasingly requiring new entrants to establish subsidiaries. In deciding the right mode of entry to a new market, banks must consider not only what is most efficient now, but what will be most efficient in the future, in light of an evolving regulatory landscape.

Exhibit 2Successful expansion into new markets

3The Master CFO Series, Volume 2: What lies beneath? The hidden cost of entering rapid-growth markets, Ernst & Young, 2011.

14 www.ey.com/banking

investing in technology to serve customers as a critical activity for the next year. This investment will help banks compete more efficiently for affluent urban customers who are increasingly demanding higher-touch service and improved products.

Banks in frontier and transitional RGMs will be more focused on developing low-cost, basic services for rural and poorer customers, such as point-of-sale and simple mobile technology. These can be effective substitutes for branches, but as their economies grow, these countries too will have to deliver higher-quality and more tailored services.

The ever-increasing competition for customers, the need to improve service levels and the need to invest in technology all risk sparking a war for talent. Interviewees expect their banks to increase headcount in high-growth areas, especially retail, SME and commercial banking (Figure 8). Competition for front office talent will be fierce, and two-thirds of interviewees expect retaining staff to be a challenge over the next 12 months. Malaysian banks are also worried about staff shortages in Islamic banking.

Although interviewees generally expect reductions in staff in head office functions, it is clear that there will be recruitment in key back office roles such as IT. Respondents from Egypt, Malaysia and South Africa all highlighted plans to invest in technology. Resource challenges are only likely to intensify, and in some cases, banks may be underestimating the need for key staff in these areas. More banks will need to review and, in some cases, develop employee retention plans to ensure they do not lose key talent to rivals.

The cost of managing regulatory change is a major challenge for banks in all markets, and the 10 in this report are no exception. A clear majority of interviewees expect the regulatory burden to increase over the next year, with clear implications for bank profitability (Figure 9).

Figure 8: Headcount

Percentage of respondents answering “don’t know” is not displayed; 21% expected headcount to stay the same* Percentage of all who say they expect headcount to increase

Head office functions

Figure 9: Levels of regulation affecting banking

Frontier RGMs

Note: Percentage of respondents answering “don’t know” is not displayed

retaining key staff will be increasingly challenging over the next 12 months.”

15Banking in emerging markets

In addition to new global standards, banks are grappling with a raft of domestic regulatory changes. In Nigeria, banks are managing the move to IFRS accounting standards. They will also face an increased focus on consumer protection initiatives following the establishment of a Customer and Financial Protection Department. In South Africa, banks will need to reshape their approach to compliance as the regulator moves to a twin-peaks model over the next two years.4 The introduction of the Financial Services Bill in Malaysia will reform the ownership structure of financial institutions. At the same time that banks are having to comply with Basel III global standards, or at least stricter local capital requirements, there are also extraterritorial regulations such as FATCA to consider. The impact of the introduction of a financial transaction tax in Europe will also have to be determined. Some of our RGMs, such as Indonesia, Chile and Turkey, already have their own taxes on securities transactions, but they may be adapted if a new global standard emerges. The cost of compliance is already a major burden in Europe and the US and will become an increasing one in RGMs too.

The introduction of new capital standards is also increasing the cost of funding. Some markets, such as Vietnam, are still transitioning to Basel II, but many are already plotting the shift to Basel III. Colombia has introduced new capital rules that come into effect in August 2013 and will lay the foundations for banks to achieve Basel III. The Nigerian central bank has revised risk weights on certain exposures across the industry. Raising additional capital will be expensive for banks. As their sovereign ratings are generally lower than those of developed markets, and these banks’ own debt is typically priced off their sovereign rate, it is more expensive for them to achieve funding through the capital markets than it is for their European or US peers. Furthermore, higher risk weightings are attached to holding their sovereign bonds for liquidity purposes. While capital adequacy will improve

the resilience of the financial sector, it is unlikely to enable banks to compensate for margin compression by expanding lending, as it reduces banks’ risk appetite and the availability of credit (Figure 10).

Regulation can pose different challenges for foreign banks operating in these markets. In some cases, the regulatory systems are still in an early stage of development and therefore rules are unclear. In other cases, the challenge is excessive complexity and bureaucracy. As with many developed markets, more local regulators in these markets are demanding foreign banks establish subsidiaries instead of operating under a branch structure, and while many of our markets, such as Turkey, are increasingly open to foreign entrants, this can swiftly change. In Indonesia, regulators are becoming much more selective about foreign ownership.

The impact of margin compression, regulatory costs and competitive pressures are forcing banks to focus on efficiency much more than may have been necessary in the past. The top four change activities interviewees are focused on are related to efficiency, risk and cost reduction (Figure 11).

A number of banks in these markets have already initiated cost reduction strategies. In some cases, this has involved partnering with a technology provider to create a customer-centric banking model that also delivers a lower efficiency ratio. Others are planning multibillion-dollar investments in their commercial networks and technology infrastructures to achieve improved operational efficiency. Nigerian banks are focusing on reducing costs through branch rationalization and headcount reduction. As profitability continues to come under pressure, more banks will need to pursue aggressive efficiency strategies.

Figure 10: Basel III

for trade finance

Credit costs for

Ranked by percentage of net increase; percentage of respondents answering “don’t know” is not displayed

4Refers to separating the oversight of market conduct regulation from prudential regulation

16 www.ey.com/banking

However, banks in these markets face a dilemma. They must balance the drive to reduce costs with the need for targeted investment in growth. With only 12% of interviewees seeing reducing their product range as important, it is clear that they understand the need to develop a variety of offerings to win customers in an increasingly competitive environment. But these banks must not seek to differentiate themselves at any cost. They must avoid product proliferation, and it will be the ability of banks to differentiate effectively that will determine success.

As profitability is challenged, and as talent becomes increasingly scarce and more expensive, banks that are developing robust operating models will have a clear advantage over those that maintain old, less efficient systems and processes. There may also be opportunities for collaboration between global banks with more expansive, easily exportable product sets and domestic banks that have wide distribution networks or a dominant position serving particular customer segments. Those that have invested in strengthening credit risks assessment will be better placed to expand into higher-risk segments. Investments must be targeted but, as ever, it will be those banks whose operations are underpinned by efficient processes and technology that will be best placed to succeed in ever more competitive markets.

Ranked by percentage of net importance; percentage who did not answer not shown

Figure 11: Managing change

Cutting costs

Retaining staff

“The top four change activities are

cost reduction.”

17Banking in emerging markets

18 www.ey.com/banking

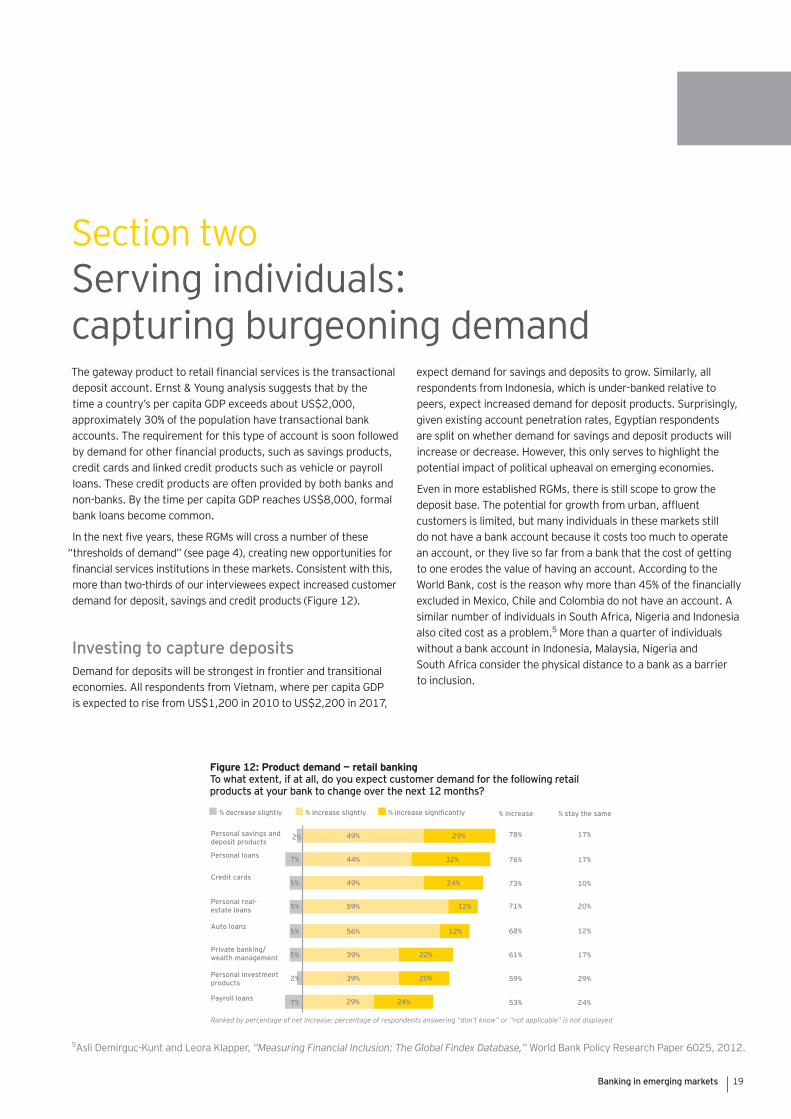

The gateway product to retail financial services is the transactional deposit account. Ernst & Young analysis suggests that by the time a country’s per capita GDP exceeds about US$2,000, approximately 30% of the population have transactional bank accounts. The requirement for this type of account is soon followed by demand for other financial products, such as savings products, credit cards and linked credit products such as vehicle or payroll loans. These credit products are often provided by both banks and non-banks. By the time per capita GDP reaches US$8,000, formal bank loans become common.

In the next five years, these RGMs will cross a number of these “thresholds of demand” (see page 4), creating new opportunities for financial services institutions in these markets. Consistent with this, more than two-thirds of our interviewees expect increased customer demand for deposit, savings and credit products (Figure 12).

Demand for deposits will be strongest in frontier and transitional economies. All respondents from Vietnam, where per capita GDP is expected to rise from US$1,200 in 2010 to US$2,200 in 2017,

expect demand for savings and deposits to grow. Similarly, all respondents from Indonesia, which is under-banked relative to peers, expect increased demand for deposit products. Surprisingly, given existing account penetration rates, Egyptian respondents are split on whether demand for savings and deposit products will increase or decrease. However, this only serves to highlight the potential impact of political upheaval on emerging economies.

Even in more established RGMs, there is still scope to grow the deposit base. The potential for growth from urban, affluent customers is limited, but many individuals in these markets still do not have a bank account because it costs too much to operate an account, or they live so far from a bank that the cost of getting to one erodes the value of having an account. According to the World Bank, cost is the reason why more than 45% of the financially excluded in Mexico, Chile and Colombia do not have an account. A similar number of individuals in South Africa, Nigeria and Indonesia also cited cost as a problem.5 More than a quarter of individuals without a bank account in Indonesia, Malaysia, Nigeria and South Africa consider the physical distance to a bank as a barrier to inclusion.

Section two Serving individuals: capturing burgeoning demand

Figure 12: Product demand — retail banking

Credit cards

Ranked by percentage of net increase; percentage of respondents answering “don’t know” or “not applicable” is not displayed

5Asli Demirguc-Kunt and Leora Klapper, “Measuring Financial Inclusion: The Global Findex Database,” World Bank Policy Research Paper 6025, 2012.

19Banking in emerging markets

Islamic banking also offers a relatively untapped pool of deposits. Although few individuals cite religious reasons for their lack of participation in financial services, the introduction of Sharia-compliant products is a major opportunity for institutions operating in a number of RGMs. Currently, several core Islamic finance markets lack regulatory clarity, but recent initiatives by the Islamic Development Bank could see more jurisdictions introducing Islamic banking legislation and regulatory frameworks. Recent political change in Egypt is likely to lead that country to become a core market for Islamic banking. In Malaysia, the market is dominated by conventional banks, but if there were consolidation among the numerous small Islamic banks, they could improve their efficiency and build their capacity locally.

As banks face increasing capital pressures, they will struggle to fulfill the expected demand for credit, and deposits from rural and other previously unbanked groups can provide a new source of funding. We believe banks will be increasingly focused on finding innovative ways to reach these customers, but they will have to invest now if they want to capture the customer relationship at an early stage. We expect that banks will rethink their existing channels, with mobile banking being the most obvious way for banks to leapfrog traditional branch structures.

The increasing ubiquity of mobile phones in emerging markets offers banks the opportunity to deliver lower-cost financial services without the traditional branch infrastructure. To date, around 167 mobile money services have been deployed across Asia, Latin America and Africa, with a further 107 planned.6 Traditionally these were focused on basic domestic peer-to-peer payments and airtime top-ups, as a way to reach rural communities, but since 2010 there has been rapid growth in other offerings, including bill payments and point-of-sale payments. This is likely to remain the dominant form of mobile banking in frontier markets, but a small and growing number of providers are also starting to offer traditional banking products, such as savings and loans, through mobile devices. Governments can play a role in driving mobile money adoption by using it for government-to-person (G2P) payments, but we believe that the development of low-cost smartphones will be the most transformative factor in mobile money usage.

The rapid growth in smartphone shipments to Asia, Latin America and Africa bears witness to the rise in popularity of these devices, but they still remain beyond the reach of most consumers in these markets. As prices come down and smartphones become more ubiquitous, they have the potential to radically change mobile money offerings in transitional and established RGMs. However, to fulfill this potential investment, there must be sufficient investment in mobile broadband infrastructure. In many countries, mobile data services are patchy and expensive. In South Africa, which has

a mobile penetration rate of over 120%, only 24% of people have accessed the internet through their phone.7

We believe collaborations between mobile providers and banks will be key to driving mobile banking adoption and developing new mobile offerings. Banks, as licensed deposit-taking institutions with advanced risk assessment capabilities, are also able to move mobile money beyond payments to more complex savings and lending products. Examples of collaboration are already evident. In addition to the well-known example from Kenya, M-Pesa, where a mobile money provider has entered into a partnership with a domestic bank to offer micro-savings, micro-credit and micro-insurance products, other examples are also emerging. Although a greater share of the revenues from serving poorer, more rural customers may initially go to the telecommunications partner, if banks can build relationships with these individuals, they will be better placed to serve them as their banking needs evolve.

Mobile money is not the only area in which banks should invest. We believe there are opportunities for banks to attract and retain customers through better use of existing market infrastructure and redesign of products and services (Exhibit 3).8

We expect that technology will be a key area for investment in all our RGMs as banks develop new distribution models and redesign their products to attract more deposits and serve their customers more efficiently. However, they must do this in a way that adapts to the nuances of the local market and the needs of different segments within those markets. Those banks that do so successfully will not only capture deposits to ease funding concerns but also develop new customer relationships and increase customer satisfaction, which will provide greater opportunity to cross-sell new products and services.

Interviewees expect demand for personal loans to increase in all RGMs, but the nature of personal lending differs widely across markets. The use of basic asset finance in the form of automotive loans is particularly common in Asian markets, where 80% of respondents expect demand for this form of finance to increase over the next 12 months. Only 60% of respondents from Latin America and 50% from Europe and Africa expect demand for this form of finance to increase over the next year. Higher demand for auto loans also reflects low vehicle penetration. For Vietnam, which has an average of 1.3 vehicles per 100 people, all respondents expect demand for loans to rise next year. For Mexico, which has 27.4 cars per 100 people, only 50% of respondents expect demand for car loans to rise.

6Mobile Money for the Unbanked Deployment Tracker, http://tinyurl.com/cbyxw43, accessed April 2013 7World Development Indicators, The World Bank; “The New Wave” report, Indra de Lanerolle, http://tinyurl.com/bn76x4c 8Opportunities in mobile money are touched on in this study but are covered in greater detail in Ernst & Young’s electronic wallet, 2013

20 www.ey.com/banking

Exhibit 3Leading banks are innovating to reach new customersEnhancing distribution to reach new customers efficiently

Utilizing existing infrastructure and capabilities

Expanding services and offerings

To expand their reach, a number of Brazilian banks have pioneered a new form of mobile banking, installing bank branches on vessels traveling the Amazon.

One Sri Lankan bank uses mobile banking units that travel to strategic locations with high consumer traffic, such as schools, marketplaces and fairs, outside normal banking hours. Its employees are able to collect small savings through a small handheld device with online connection to the bank through GPRS. In Malaysia, low-cost no-frills branches have been launched in densely populated urban centers.

Offering financial services through agent or correspondent arrangements with non-financial firms, such as retailers, lottery outlets or post offices, allows banks to extend their reach without expanding their branch networks. Agents are equipped by banks to enable them to conduct transactions for customers, taking the place of branch tellers.

Brazil has led the way with this banking model, with a large network of correspondents offering financial services through cards and point-of-sale terminals. Other countries in Latin America have followed suit, including Chile, Colombia and Mexico. Banks either have a direct relationship with their agents or the relationship is through a management company. While a direct relationship with agents may enable more effective data capture, an institution may not have the capacity to manage a wide network of agents. Using a management company is likely to prove more expensive and yield less control of the agent network.

Local regulations about who can act as an agent can restrict the growth of this model. Banks also need to consider whether they will have an exclusive relationship with an agent. In Brazil and Mexico, agents often represent more than one institution, but this is rare in Colombia.

Companies have been developing behavioral scoring tools based on analysis of mobile (including pre-pay) usage data, including call and text message patterns. One such company has been running a trial of its platform in Brazil and expects live deployment in 2013.

While the expansion of mobile money gives banks greater access to an emerging customer pool, the development of such new and innovative tools to understand customer behaviors will enable banks to better assess risk and offer those customers much more diverse, and appropriate, products. The technology, however, is still relatively new and untested, and success unproven.

The entry of one of Colombia’s utilities providers into financial services illustrates how a wide range of customer data can be used to assess credit risk.

The utility provider was able to supplement credit reference agency data with its own customer data, as well as use its existing billing and payments infrastructure, to advertise, disburse and collect loans.

Eight years after launching, it sold a stake in the financial services business to a bank, which took over responsibility for credit assessment and loan monitoring and began offering existing customers a range of new products. The utility company still runs its own customer service, invoicing and loan recovery operations.

Such partnership models enable banks to offer services to a wider low-income segment, and also allow many customers to establish a credit history for the first time.

With limited credit data, lending to groups or individuals must be based on analysis of character and the cash flow of the borrower(s). This often requires a loan officer who has better knowledge of an individual or community than is common in most banks.

To make lending more cost-effective (small loans to individuals are often insufficiently profitable), institutions may lend to groups of individuals who are jointly liable for the loan. In some instances, borrowers will have to deposit compulsory savings before receiving a loan to demonstrate a willingness and ability to make repayments.

Products focused on specific needs are often more valued than untargeted credit products. Rickshaw loans — in effect a hire purchase agreement — to rickshaw pullers in India are a good example of this sort of targeted lending. Seasonal loan repayments are another innovation that can help expand access to credit. For example, a loan by a fishermen’s cooperative in southern India permits a specified number of repayment holidays that correspond to the off season for fishing.

Restrictions on many micro-finance institutions taking deposits make this a prime opportunity for banks to expand into, or to partner with, micro-finance institutions, using their network of loan officers.

There is significant demand for savings products in our RGMs, but existing products are often not suited to the needs of poorer customers. For example, flat maintenance fees deducted directly from savings accounts can lead to a total loss of the original amount deposited. Alternative models, such as transaction pricing, should be considered. Some South African banks offer basic accounts with no minimum balance and a low fee structure.

Institutions may also struggle to offer savings products cost effectively to this customer segment, where they must collect high volumes of low-value transactions. We believe banks should take a longer-term view of these customers’ value. By offering savings products, institutions are able to build a better understanding of their customers to enhance their risk management capabilities, and build a customer base of borrowers to cross-sell products to as they become wealthier. Savings accounts also help facilitate and encourage repayment of credit. In Thailand, a government-promoted initiative takes savings efforts of individuals into account as part of eligibility for micro-loans.

21

Demand for payroll loans is higher in frontier and transitional economies, such as Vietnam and Indonesia. These types of loans are an efficient product for managing credit risk in these markets where credit histories are limited and, perhaps as a result of this, some banks in our transitional markets are not as concerned with strengthening credit risk management as their frontier RGM counterparts. But as affluence increases, we expect customers to look for alternative credit products — formal bank loans and mortgages are much more popular in established RGMs — and managing credit risk will become a key area of future investment.

Interviewees clearly see cross-selling products to existing customers as key to their bank’s expansion (Figure 13). Established customers should be easier to sell products and services to than new customers, but improving penetration rates with existing customers will not be easy. Ernst & Young’s 2012 Global Consumer Banking Survey revealed that more customers are becoming multi-banked. In South Africa, although 78% of consumers held savings accounts with their main bank, just 49% had loans and 39% mortgages with the same provider. In Colombia, while 70% had their savings account at their main bank, just 49% held their personal loan and 52% a credit card with the same provider. Other markets told a similar story: in Indonesia, 87% of customers bank with two or more providers; in Malaysia it is 91%.

Banks should take steps to improve customer loyalty to ensure that if they hold a customer’s transactional account, they will also provide their savings, lending or mortgage products. Satisfaction with branch experience and service quality in RGMs often ranks below that of customers in developed markets. With high fees being the main driver of attrition in these markets, banks are already looking for ways to serve customers more efficiently. Over 80% of our interviewees see developing new customer channels such as online and mobile as important. However, improving customer service will also be crucial and may differentiate providers in those markets where consumers remain dissatisfied with the quality of service from their banks.

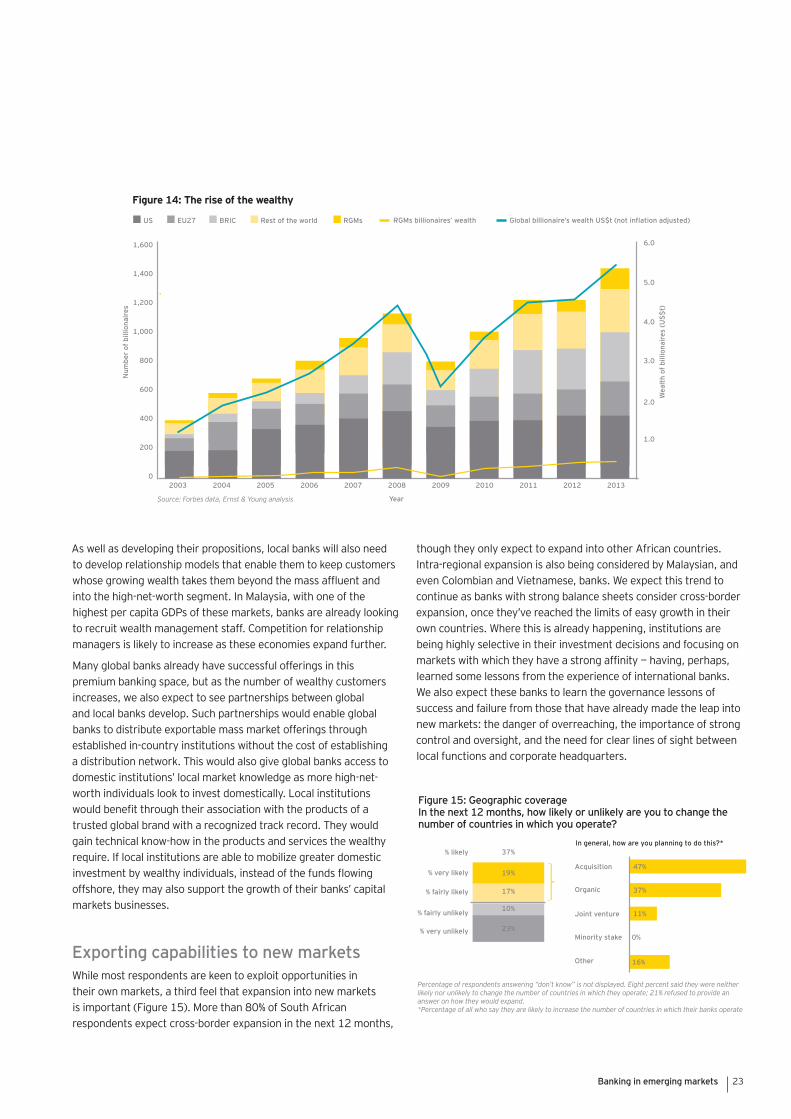

There are now more emerging market billionaires than European ones. In the decade to 2012, the number of billionaires in our 10 RGMs grew from just 29 to 108, and their net worth grew from US$66 billion to US$386 billion (Figure 14). Beyond this new class of super-rich, there are growing numbers of high-net-worth and mass affluent individuals that are driving demand for wealth management services in these economies. The outlook for wealth management is a derivative of broader views on the economic prospects, so it’s not surprising that respondents from Egypt and Colombia predict deterioration in the outlook for wealth management. Fifty percent of interviewees are optimistic about the outlook for private banking and wealth management in their markets over the next 12 months, and 49% expect demand for wealth products at their bank to increase.

However, meeting this demand may prove challenging for local banks. The wealthiest investors are likely to favor trusted and proven products that are managed by world-class investment managers with long-term track records. They are also likely to favor institutions that have a global reach and international banking network — in short, established global wealth management brands. However, due to the cost of establishing a branch network, these institutions are likely to focus on providing flagship products to only the wealthiest individuals. They are unlikely to target customers further down the wealth spectrum.

It is the mass affluent segment that presents the greatest opportunity to local banks, but customer service will become increasingly important if they are to capture, nurture and retain increasingly wealthy customers. More banks will need to follow the example of those that have invested in dedicated branches, better-trained staff and a broader range of products and services. We’re already seeing some examples of this in our established RGMs — for example, in Mexico and Malaysia.

Ranked by percentage of net importance; percentage who did not answer not shown

Figure 13: Expansion

22 www.ey.com/banking

As well as developing their propositions, local banks will also need to develop relationship models that enable them to keep customers whose growing wealth takes them beyond the mass affluent and into the high-net-worth segment. In Malaysia, with one of the highest per capita GDPs of these markets, banks are already looking to recruit wealth management staff. Competition for relationship managers is likely to increase as these economies expand further.

Many global banks already have successful offerings in this premium banking space, but as the number of wealthy customers increases, we also expect to see partnerships between global and local banks develop. Such partnerships would enable global banks to distribute exportable mass market offerings through established in-country institutions without the cost of establishing a distribution network. This would also give global banks access to domestic institutions’ local market knowledge as more high-net-worth individuals look to invest domestically. Local institutions would benefit through their association with the products of a trusted global brand with a recognized track record. They would gain technical know-how in the products and services the wealthy require. If local institutions are able to mobilize greater domestic investment by wealthy individuals, instead of the funds flowing offshore, they may also support the growth of their banks’ capital markets businesses.

While most respondents are keen to exploit opportunities in their own markets, a third feel that expansion into new markets is important (Figure 15). More than 80% of South African respondents expect cross-border expansion in the next 12 months,

though they only expect to expand into other African countries. Intra-regional expansion is also being considered by Malaysian, and even Colombian and Vietnamese, banks. We expect this trend to continue as banks with strong balance sheets consider cross-border expansion, once they’ve reached the limits of easy growth in their own countries. Where this is already happening, institutions are being highly selective in their investment decisions and focusing on markets with which they have a strong affinity — having, perhaps, learned some lessons from the experience of international banks. We also expect these banks to learn the governance lessons of success and failure from those that have already made the leap into new markets: the danger of overreaching, the importance of strong control and oversight, and the need for clear lines of sight between local functions and corporate headquarters.

Figure 14: The rise of the wealthy

Source: Forbes data, Ernst & Young analysis Year

BRICUS RGMs

Percentage of respondents answering “don’t know” is not displayed. Eight percent said they were neither likely nor unlikely to change the number of countries in which they operate; 21% refused to provide an answer on how they would expand.*Percentage of all who say they are likely to increase the number of countries in which their banks operate

Joint venture

23Banking in emerging markets

www.ey.com/banking24

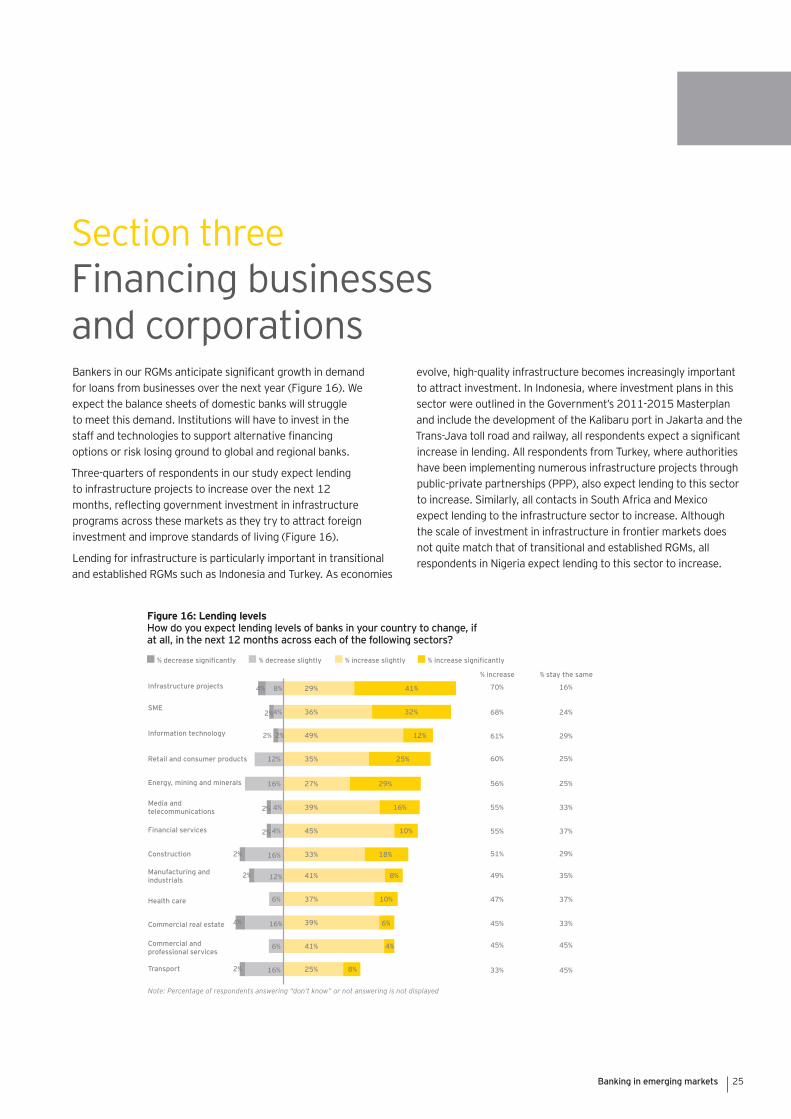

Bankers in our RGMs anticipate significant growth in demand for loans from businesses over the next year (Figure 16). We expect the balance sheets of domestic banks will struggle to meet this demand. Institutions will have to invest in the staff and technologies to support alternative financing options or risk losing ground to global and regional banks.

Three-quarters of respondents in our study expect lending to infrastructure projects to increase over the next 12 months, reflecting government investment in infrastructure programs across these markets as they try to attract foreign investment and improve standards of living (Figure 16).

Lending for infrastructure is particularly important in transitional and established RGMs such as Indonesia and Turkey. As economies

evolve, high-quality infrastructure becomes increasingly important to attract investment. In Indonesia, where investment plans in this sector were outlined in the Government’s 2011-2015 Masterplan and include the development of the Kalibaru port in Jakarta and the Trans-Java toll road and railway, all respondents expect a significant increase in lending. All respondents from Turkey, where authorities have been implementing numerous infrastructure projects through public-private partnerships (PPP), also expect lending to this sector to increase. Similarly, all contacts in South Africa and Mexico expect lending to the infrastructure sector to increase. Although the scale of investment in infrastructure in frontier markets does not quite match that of transitional and established RGMs, all respondents in Nigeria expect lending to this sector to increase.

Section three Financing businesses and corporations

Figure 16: Lending levels

Construction

SME

Media and

Manufacturing and

Note: Percentage of respondents answering “don’t know” or not answering is not displayed

25Banking in emerging markets

Demand for credit will also be high in the IT sector, but reasons for this vary across different economies, with all respondents in Turkey, Vietnam, Indonesia and Mexico anticipating growth. In Turkey, this is driven by the government, but in Vietnam, Indonesia and Mexico it is driven by technology companies seeking lower-cost locations to outsource manufacturing or services. A series of technology manufacturers have opened factories in Vietnam, while Indonesia has attracted investment in the e-commerce sector and is increasingly being seen as a new IT outsourcing location. Mexico is also growing as an IT outsourcing hub for those US companies preferring solutions closer to home than Asia.

Demand for corporate loans and project and trade finance reflects the growth and the increasingly globalized nature of these economies. It also highlights an opportunity for domestic institutions to fill a gap left by some developed market banks that have been cutting back on project and trade finance as they shrink their balance sheets. However, other global banks from markets such as Japan are stepping in, and it is also an opportunity for strong regional banks. Domestic institutions, more familiar with vanilla lending, will have to act swiftly to address any capability gaps if they are to capitalize on their home advantage.

We also expect to see a significant increase in demand from the SME sector. As emerging economies monetize, and incomes rise, the unofficial (shadow) economy is displaced by a more formal SME sector. According to interviewees, the greatest demand will be in frontier markets, where this displacement is occurring most swiftly.

Assessing the viability of loans to the credit-hungry SME sector is challenging, as there is often little credit data associated with these companies. Many of them may not have held bank accounts for very long, or their company accounts may in practice have been personal accounts. Furthermore, their financial accounts may be limited and opaque. Banks focusing on this sector need both local knowledge of businesses and communities and advanced risk management capabilities to be able to assess lending to emerging companies.

Only 39% of interviewees expect to increase loan loss provisions over the next year, suggesting a majority feel that continued economic growth will outweigh the risk of bad loans (Figure 17). However, with lending levels expected to grow, it is inevitable that some loans will fall into arrears and default, if only because asset quality cannot be sustained. Banks must monitor lending closely to avoid being caught out if the economy swiftly deteriorates. Fortunately, a focus on credit risk is evident in most countries, with 69% of interviewees stressing its importance. There is an even greater emphasis on credit risk in frontier economies, where demand for SME lending will be greatest; 90% of interviewees in these markets think strengthening credit risk is critical.

Given the anticipated demand for SME finance, we expect some banks — particularly in frontier and transitional markets — to specialize in this sector, focusing on those smaller businesses making the transition into the formal economy. The investment needed to target this segment can be high, but it also offers higher margins than corporate lending. We believe institutions serving SMEs in these markets will have to hire highly trained staff with local knowledge, and to strengthen their credit risk technology to support lending to the sector.

We also expect more banks to look beyond vanilla lending and to invest in the technology and skilled staff required to provide support and advice to both rapidly expanding SMEs and larger businesses. As these businesses evolve, they will need banks to offer increasingly sophisticated additional products and services, such as hedging products and treasury services.

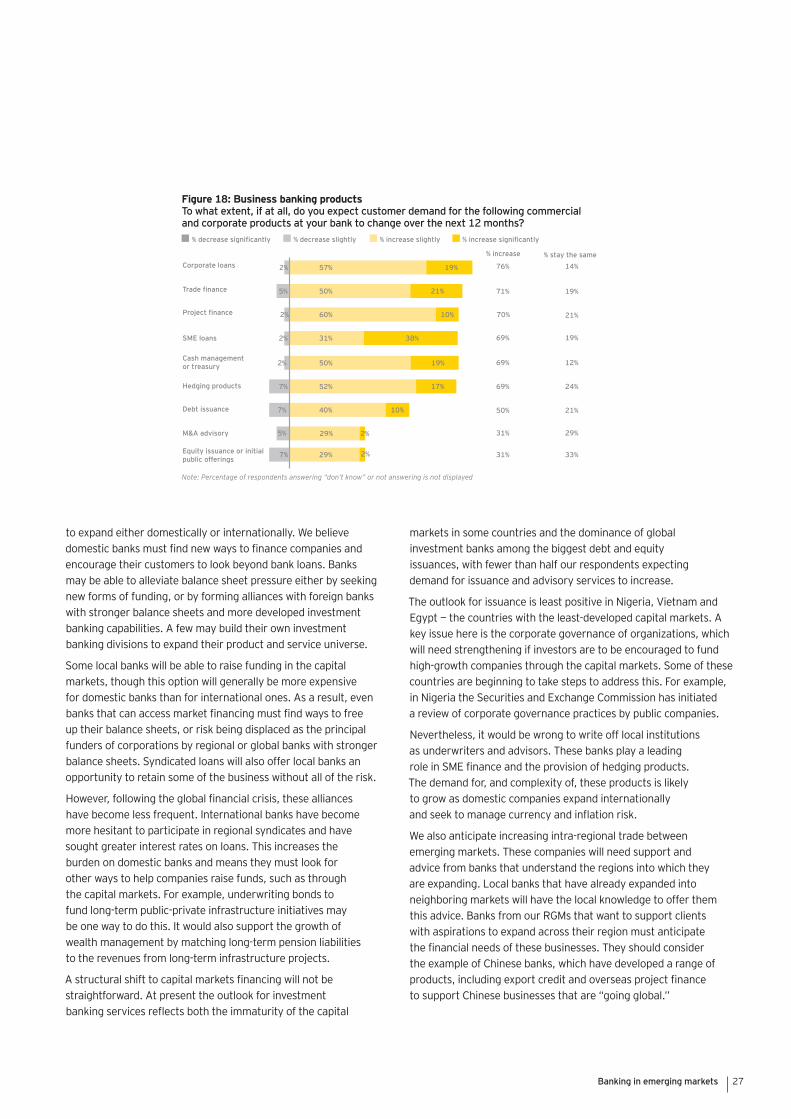

Companies in our RGMs are currently heavily reliant on bank lending to meet their financing needs. With demand for lending expected to increase dramatically (and with ever higher capital requirements for lending), we expect banks will struggle to meet this demand (Figure 18). There is a high risk that growth could be constrained in markets where banks do not have the balance sheets required to finance the needs of larger companies looking

Figure 17: Provisions against loan losses

deteriorate

Note: Percentage of respondents answering “don’t know” or not answering is not displayed. Responses have been analyzed against interviewees’ expectations for the overall economy.

26 www.ey.com/banking

to expand either domestically or internationally. We believe domestic banks must find new ways to finance companies and encourage their customers to look beyond bank loans. Banks may be able to alleviate balance sheet pressure either by seeking new forms of funding, or by forming alliances with foreign banks with stronger balance sheets and more developed investment banking capabilities. A few may build their own investment banking divisions to expand their product and service universe.

Some local banks will be able to raise funding in the capital markets, though this option will generally be more expensive for domestic banks than for international ones. As a result, even banks that can access market financing must find ways to free up their balance sheets, or risk being displaced as the principal funders of corporations by regional or global banks with stronger balance sheets. Syndicated loans will also offer local banks an opportunity to retain some of the business without all of the risk.

However, following the global financial crisis, these alliances have become less frequent. International banks have become more hesitant to participate in regional syndicates and have sought greater interest rates on loans. This increases the burden on domestic banks and means they must look for other ways to help companies raise funds, such as through the capital markets. For example, underwriting bonds to fund long-term public-private infrastructure initiatives may be one way to do this. It would also support the growth of wealth management by matching long-term pension liabilities to the revenues from long-term infrastructure projects.

A structural shift to capital markets financing will not be straightforward. At present the outlook for investment banking services reflects both the immaturity of the capital

markets in some countries and the dominance of global investment banks among the biggest debt and equity issuances, with fewer than half our respondents expecting demand for issuance and advisory services to increase.

The outlook for issuance is least positive in Nigeria, Vietnam and Egypt — the countries with the least-developed capital markets. A key issue here is the corporate governance of organizations, which will need strengthening if investors are to be encouraged to fund high-growth companies through the capital markets. Some of these countries are beginning to take steps to address this. For example, in Nigeria the Securities and Exchange Commission has initiated a review of corporate governance practices by public companies.

Nevertheless, it would be wrong to write off local institutions as underwriters and advisors. These banks play a leading role in SME finance and the provision of hedging products. The demand for, and complexity of, these products is likely to grow as domestic companies expand internationally and seek to manage currency and inflation risk.

We also anticipate increasing intra-regional trade between emerging markets. These companies will need support and advice from banks that understand the regions into which they are expanding. Local banks that have already expanded into neighboring markets will have the local knowledge to offer them this advice. Banks from our RGMs that want to support clients with aspirations to expand across their region must anticipate the financial needs of these businesses. They should consider the example of Chinese banks, which have developed a range of products, including export credit and overseas project finance to support Chinese businesses that are “going global.”

Note: Percentage of respondents answering “don’t know” or not answering is not displayed

Figure 18: Business banking products

Project finance

Trade finance

27Banking in emerging markets

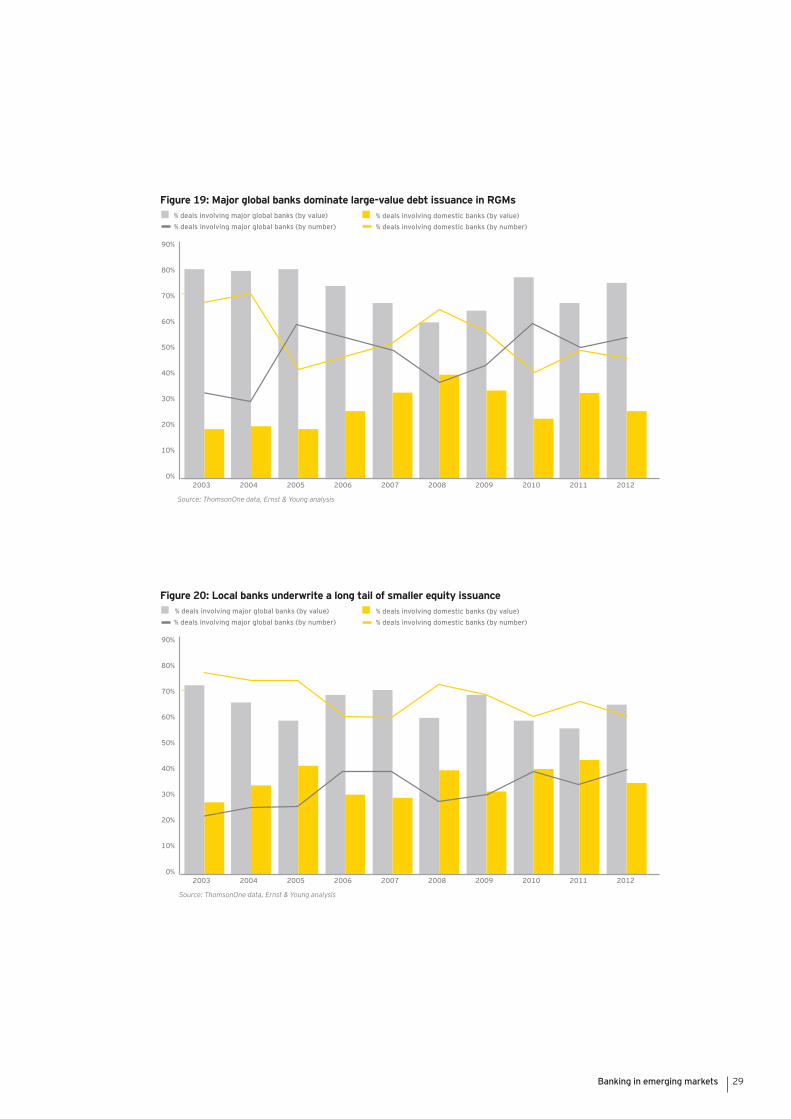

Many local banks already have strong existing relationships with fast-growing domestic companies that should enable these financial institutions to expand with them. Although major global banks dominate the largest deals in these markets, domestic banks are involved in a significant number of smaller deals. Over the last decade, they have been involved in underwriting 68% of all equity issues and 53% of bond issues (Figure 19, Figure 20). That these constituted, respectively, just 35% and 27% of deals by value indicates a long tail of companies seeking capital market funding that are too small to be of interest to the bulge bracket investment banks. We expect that as debt and equity issuance become more common, local banks will play a greater role in larger deals, collaborating with global investment banks. This will offer them opportunities to build the capabilities of their staff and plug any skills gaps.