banking policy direction in 2011

TRANSCRIPT

2 0 11

Bank IndonesiaDepartment of Banking Research and Regulation (DPNP)Jl. MH. Thamrin No. 2, Jakarta, Indonesia - 10350Telephon : (+62-21) 2310108, ext.4798, 4794, 8623 and 7725Fax : (+62-21) 3518946 dan 3518629Email : [email protected]

Banking Supervision Report2011

Banking Supervision Report 2011iv

Foreword

Table of Contents Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performancein 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

BI MissionTo achieve and maintain rupiah stability by maintaining monetary stability and by

promoting financial system stability for Indonesia’s long term sustainable development.

BI VisionTo be recognized, domestically and internationally, as a credible central bank

through the strength of our values and achievement of low, stable rates of inflation.

Strategic Values of Bank IndonesiaCompetency - Integrity - Transparency - Accountability - Cohesiveness.

Visi:“Menjadi lembaga bank sentral yang dapat dipercaya secara nasional

maupun internasional melalui penguatan nilai-nilai strategis yang dimiliki serta

pencapaian inflasi yang rendah dan stabil”

Misi:“Mencapai dan memelihara kestabilan nilai rupiah melalui pemeliharaan

kestabilan moneter dan pengembangan stabilitas sistem keuangan untuk

pembangunan jangka panjang yang berkesinambungan”

Nilai-nilai Strategis Organisasi Bank Indonesia:“Nilai-nilai yang menjadi dasar Bank Indonesia, manajemen dan pegawai untuk

bertindak dan atau berperilaku, yang terdiri atas Kompetensi, Integritas, Transparansi,

Akuntabilitas dan Kebersamaan”

This page intentionally blank

v

Foreword

Table of Contents Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performancein 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

We would like to express our sincere gratitude to God Almighty, for it is with His mercy and grace that

the 2011 edition of the Banking Supervision Report was compiled and published. Publication of the Banking

Supervision Report represents a form of transparency and accountability to the general public regarding the

supervision and regulation of banks pursuant to Act No. 23, 1999 on Bank Indonesia, subsequently amended

by Act No. 6, 2009. The scope of the Banking Supervision Report covers all types of bank in Indonesia, namely

conventional commercial banks, Islamic banks and rural banks.

This edition contains, among others, a profusion of information on the development and performance of the

banking sector, including a number of key performance indicators for 2011 in comparison to years previous. The

Banking Supervision Report also explains banking policy direction in 2011 as well as the regulations and policies

instituted during the reporting year. In addition, the banking supervision process conducted by Bank Indonesia

during 2011 is also reported alongside the results and follow-up actions required looking ahead. Furthermore,

the development of banking supervision is also detailed, including information system development, as well as

bank investigations and mediation. Analyses are presented in the final chapter regarding future prospects and

the direction of banking policy in 2012, namely to boost competitiveness, bolster resilience and nurture bank

intermediation.

One salient upshot of banking supervision in 2011 was sustainable bank performance. In general, growth in

deposits remained solid, of which the majority was used to finance credit extension. Meanwhile, the quality of

credit was maintained with non-performing loans remaining low. Accordingly, profitability was sufficient to buoy

bank capital. Notwithstanding, a number of incidents occurred in 2011 that attracted public scrutiny, including

fraudulent wealth management services, erroneous credit card billing and fraudulent SMS schemes exploiting

bank accounts. Consequently, Bank Indonesia in conjunction with the banking community implemented a number

of actions to resolve problems at the banks, restore public confidence and prevent any future reoccurrence of

similar issues.

In closing, we expect the 2011 Banking Supervision Report to function as a form of media to communicate

to our stakeholders what has been undertaken by Bank Indonesia during 2011 in terms of banking regulation and

supervision, as well as future banking policy direction. All comments are welcome and will be discussed further

in order to ensure the accuracy and functionality of the Banking Supervision Report.

Jakarta, 2nd May 2012

DEPUTY GOVERNOR OF BANK INDONESIAI

IA

Muliaman D. Hadad

Foreword

This page intentionally blank

vii

Table of Contents

Foreword Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performance in 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

Foreword ........... ................................................................................................. v

Table of Contents ........... ..................................................................................... vii List of Tables .......... ............................................................................................................................. ix List of Figures .......... ........................................................................................................................... x

Executive Summary ............................................................................................. 1

Chapter I Bank Structure and Performance in 2011 ............................................. 7 Bank Structure .................................................................................................................................... 9 Commercial Banks ....................................................................................................................... 9 Islamic Banking ............................................................................................................................ 11 Rural Banks (BPR) ......................................................................................................................... 12 Bank Performance .............................................................................................................................. 14 Commercial Banks ........................................................................................................................ 15 Islamic Banking ............................................................................................................................ 19 Rural Banks (BPR) ......................................................................................................................... 25 Box 1.1 MSME Credit and Small Loans (KUR) ......................................................................... 28

Chapter II Banking Policy and Regulation in 2011 ................................................ 33 Banking Policy Direction in 2011 ......................................................................................................... 35

Conventional Commercial Banks .................................................................................................. 35 Islamic Banks ................................................................................................................................ 35 Rural Banks (BPR) .......................................................................................................................... 37 Banking Regulation in 2011 ................................................................................................................. 38 Conventional Commercial Banks .................................................................................................. 38 Islamic Banks ................................................................................................................................ 41 Rural Banks (BPR) ......................................................................................................................... 43 Bank Indonesia Coordination and Participation with its Stakeholders ......................................... 46 Box 2.1 Public Education Program ......................................................................................... 51 Box 2.2 Transparent Publication of Prime Lending Rates ....................................................... 53 Box 2.3 LDR based Statutory Reserves ................................................................................... 57 Box 2.4 Rural Bank Business Model ....................................................................................... 59

Chapter III Bank Supervision Implementation and Follow-Up in 2011 .................. 61 Conventional Commercial Banks ........................................................................................................ 63 Islamic Banks ...................................................................................................................................... 65 Rural Banks (BPR) ............................................................................................................................... 67 Fit and Proper Tests ............................................................................................................................ 68 Conventional Commercial Banks ................................................................................................. 68 Islamic Banks ................................................................................................................................ 69 Rural Banks (BPR) .......................................................................................................................... 69 Banking Information System (BIS) ...................................................................................................... 70 Banking Investigations ........................................................................................................................ 70 Bank Mediation .................................................................................................................................. 73

Table of Contents

Banking Supervision Report 2011viii

Table of Contents

Foreword Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performance in 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

Box 3.1 Strengthening Banking Supervision based on Risk (Risk Based Bank Ratings) ................ 75 Box 3.2 Handling Cases of Fraud concerning Prime Customers and Credit Card Billing .............. 77

Chapter IV Prospects and Banking Policy Direction in 2012 .................................. 79 Challenges and Prospects .................................................................................................................... 81 Banking Policy Direction in 2012 ........................................................................................................ 82 Conventional Commercial Banks ................................................................................................. 82 Islamic Banks ................................................................................................................................ 82 Rural Banks (BPR) ......................................................................................................................... 85

ix

Table of Contents

Foreword Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performance in 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

Table 1.1 Number of Banks and Branch Offices ......................................................................................... 9Table 1.2 Number of Banks based on Core Capital ................................................................................... 10Table 1.3 New Islamic Rural Banks in 2011 ............................................................................................... 12Table 1.4 Development of the Islamic Bank Office Network ..................................................................... 12Table 1.5 The Office Network of Conventional Rural Banks ...................................................................... 12Table 1.6 The Development of Rural Banks ............................................................................................... 13Table 1.7 Mergers and Consolidations in the Rural Banking Industry ........................................................ 13Table 1.8 Licensing Data for 2011 ............................................................................................................. 14Table 1.9 Number of Rural Banks based on Typeof Legal Entity ............................................................... 14Table 1.10 Key Indicators for Commercial Banks ......................................................................................... 15Table 1.11 Key Indicators of Islamic Banks and Sharia Business Units ......................................................... 20Table 1.12 Key Indicators for Islamic Rural Banks ........................................................................................ 23Table 1.13 Credit based on Business Type and Usage ................................................................................. 26Table 1.14 Key Indicators of Rural Banks ..................................................................................................... 26

Table 2.1 Average Prime Lending Rates in the Banking Industry (%) ......................................................... 55Table 2.2 LDR of Conventional Commercial Banks ..................................................................................... 58

Table 3.1 Breakdown of Fit and Proper Tests for Conventional Commercial Banks ................................... 69Table 3.2 Investigation Statistics of Criminal Activity in the Banking Sector during 2011 .......................... 71Tabel 3.3 Pemenuhan Pemberian Keterangan Saksi dan Ahli BI ................................................................ 75Tabel 3.4 Jumlah Sengketa yang Diterima Bank Indonesia ........................................................................ 76

List of Tables

Banking Supervision Report 2011x

Table of Contents

Foreword Executive Summary Prospects and BankingPolicy Direction

Bank Structure and Performance in 2011

Banking Policy and Regulationin 2011

Bank Supervision Implementation

Figure 1.1 Bank Composition by Bank Group in 2011 ............................................................................... 11Figure 1.2 Number of Banks ...................................................................................................................... 11Figure 1.3 Total Assets by Bank Group ...................................................................................................... 11Figure 1.4 Asset Composition by Bank Group in 2011 .............................................................................. 11Figure 1.5 Performance of Credit, Deposits and LDR ................................................................................ 15Figure 1.6 Credit Growth by Loan Type ..................................................................................................... 16Figure 1.7 Credit Growth by Economic Sector .......................................................................................... 16Figure 1.8 Non-Performing Loans ............................................................................................................. 17Figure 1.9 Deposit Growth by Component ............................................................................................... 18Figure 1.10 Composition of Deposits by Component in 2011 .................................................................... 18Figure 1.11 Average Lending Rates and Savings Rates of Commercial Banks ............................................. 19Figure 1.12 Credit by Sector (BUS and UUS) in 2011 .................................................................................. 21Figure 1.13 Income, Costs and Efficiency of BUS and UUS ......................................................................... 22Figure 1.14 Profitability of Islamic banks .................................................................................................... 22Figure 1.15 Composition of Islamic Rural Bank Financing in 2011 .............................................................. 23Figure 1.16 Financing based on Type in 2011 ............................................................................................. 24Figure 1.17 Financing based on Economic Sector in 2011 ........................................................................... 24Figure 1.18 Total Assets, Credit and Deposits ............................................................................................. 25Figure 1.19 Growth in Credit and Deposits ................................................................................................. 25Figure 1.20 Interest Rates ............................................................................................................................ 27Figure 1.21 Realisation of Small Loans ........................................................................................................ 29Figure 1.22 Small Loan Allocation by Economic Sector ............................................................................... 30Figure 1.23 Non-Performing Loans (NPL) and Non-Performing Guarantee (NPG) ...................................... 31

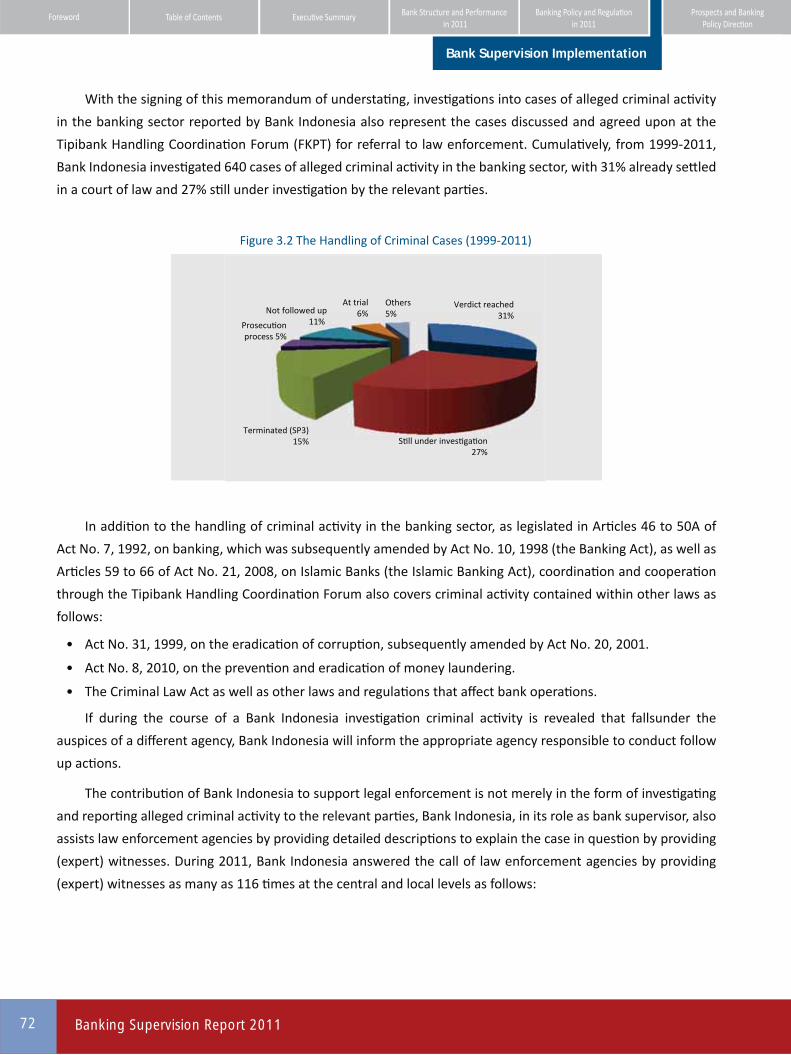

Figure 3.1 Cases of Tipibank by Type in 2011 ........................................................................................... 71Figure 3.2 The Handling of Criminal Cases (1999-2011) ........................................................................... 72

List of Figures

Executive Summary

Banking Supervision Report 20112

Executive Summary

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Structure and Performancein 2011

Bank Supervision Implementation

This page intentionally blank

3

Executive Summary

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Structure and Performancein 2011

Bank Supervision Implementation

Banking structure and performance in 2011 was positive. In line with the 6.5% economic growth posted in

2011 in Indonesia, the banking sector continued to expand through new branch offices opened in various regions

across the archipelago. The total number of conventional commercial banks operating at yearend 2011 was 109.

Meanwhile, the number of Islamic banks in 2011 also increased in line with the establishment of new banks in

the form of Sharia Business Units (BUS) at conventional commercial banks as well as Islamic rural banks (BPRS).

The number of Sharia business units increased to 24, while Islamic commercial banks totalled 11 and Islamic

rural banks amounted to 155. In addition, the number of branch offices and service coverage of rural banks

continued to expand with rural bank branch offices totalling 1,223 and cash handling offices reaching 1,280.

In 2011, bank performance continued to improve. Ongoing global financial turmoil as a result of the

debt crisis in Europe and the languid US economy did not appear to generate any significant fallout in the

domestic banking sector. Accordingly, bank deposits grew robustly, of which the majority was used to finance

credit extension. Credit was expanded with due regard to the prevailing prudential corridor, thereby maintaining

a low non-performing loans ratio. Furthermore, bank capital was buttressed on the back of sound profitability.

Banking policy and regulation in 2011 represented the foundation by which to increase and strengthen

the banking supervision function implemented by Bank Indonesia. Conventional commercial bank regulation

aimed to foster bank intermediation, enhance bank resilience as well as strengthen supervision and the

macroprudential function. Concomitant Islamic banking regulations were designed to harmonise the regulatory

framework with that of conventional banks, while relaxing certain regulations and enforcing others like Act No.

21, 2008, on Islamic Banking, in order to mandate Bank Indonesia as the regulator of the banking industry

with preparations for banking based on sharia principles. Furthermore, rural banking regulations were directed

towards strengthening capital and supporting infrastructure as well as improving the quality of supervision and

the competence of supervisors.

During the past year of 2011, Bank Indonesia promulgated an array of regulations for conventional commercial

banks, Islamic banks and rural banks. The regulations issued include new regulations as well as amendments to

existing regulations and/or previously rescinded regulations. In broad terms, the regulations aimed to support

economic growth and catalyse the real sector, expand customer protection, improve banking supervision,

comply with international supervisory standards, as well as foster micro, small and medium enterprise (MSME)

development, along with other institutional and prudential regulations. In the case of MSME policy, Bank

Indonesia conducted a range of research as policy guidelines to nurture MSME development and accelerate

credit allocation to the MSME sector (research-based policy). Bank Indonesia also provided training and technical

assistance in order to raise the eligibility and capability of MSME, broaden bank expertise concerning MSME, as

well as provide up-to-date information on MSME through the INFOUMKM section on the official Bank Indonesia

website. In addition, Bank Indonesia established and strengthened supporting institutions (among others by

creating regional credit guarantee companies) as well as introduced MSME credit ratings.

Banking supervision focused on three pillars during 2011, namely to encourage bank intermediation,

to enhance bank resilience and to strengthen the supervision function for conventional commercial banks,

Islamic banks and rural banks. Bank Indonesia favours risk-based bank supervision, which incorporates a strategy

Banking Supervision Report 20114

Executive Summary

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Structure and Performancein 2011

Bank Supervision Implementation

and methodology based on risk that permits bank supervisors to detect significant risks in a bank’s business

activity early, thereby allowing for appropriate and timely supervisory actions to be taken. Quality assurance is in

place to ensure the inputs, processes and outputs of risk-based bank supervision meet international standards,

thereby honing the quality of supervision (quality assurance) in order to continuously improve the efficacy of

bank supervision. Of the numerous aspects assessed, the level of soundness, risk profile, level of good corporate

governance, implementation of anti-money laundering and prevention of terrorism funding, as well as bank

supervision status all appeared to improve when compared to the previous year of 2010.

As part of the bank supervision process, to create a sound banking system, protect the interests of the

stakeholders and ensure compliance to prevailing regulations, good corporate governance is a prerequisite for

the banking industry. The realisation of good corporate governance is only possible if the banking industry

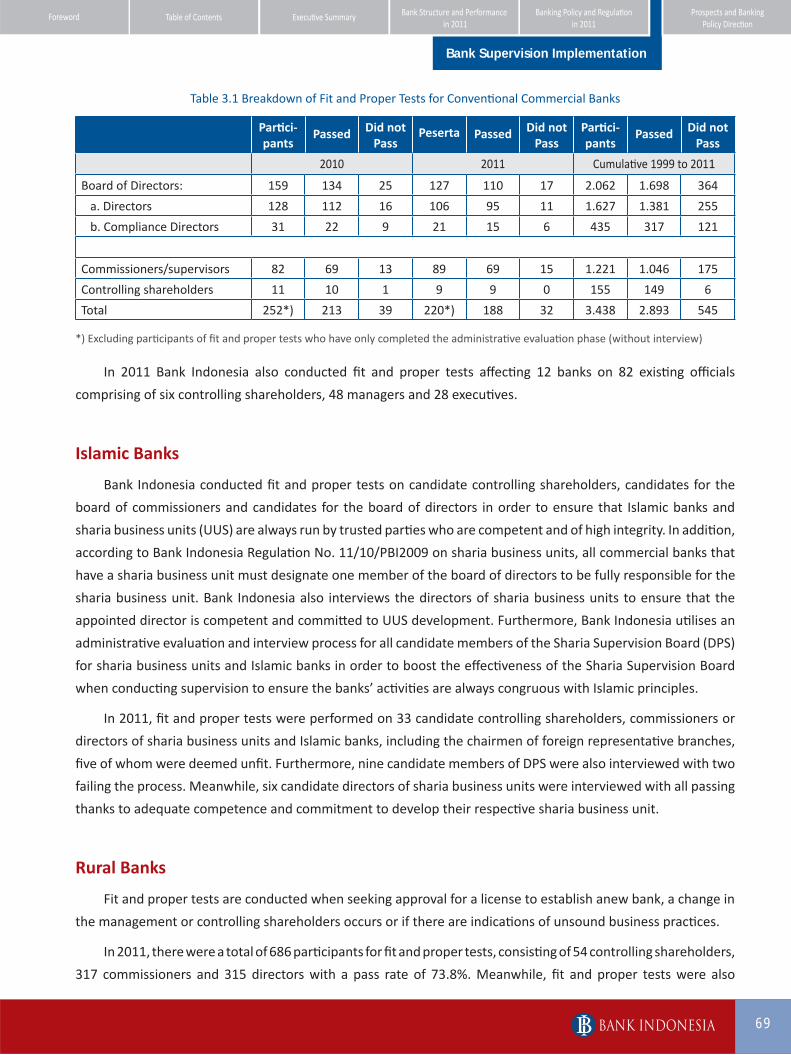

is owned and managed by those fulfilling fit and proper requirements. Therefore, in its first line of defence,

Bank Indonesia utilises fit and proper tests in its selection process of candidate commissioners, directors and

controlling shareholders. Fit and proper tests are compulsory for new entry as well as existing candidates.

In addition to policy, regulation and supervision, the information system that represents the backbone of

the supervision process was also addressed by Bank Indonesia. Bank Indonesia developed a Banking Information

System (SIP) to replace the more antiquated Bank Indonesia Banking Sector Management Information System

(SIM-SPBI) in order to meet the changing needs of the banking sector in terms of enhancing the quality of

information, particularly regarding the implementation of new regulations. Another important aspect that is

inextricably linked to the supervision process conducted at Bank Indonesia is investigation and mediation. Bank

Indonesia is fully aware that as the banking industry develops, so potentially do the opportunities, quality and

complexity. Under such circumstances, efforts to raise bank compliance to prevailing laws and regulations are

vital to protect the public’s funds as well as prevent the emergence of structural problems in the banking system

that could undermine the national economy. Meanwhile, Bank Indonesia began facilitating a mediation function

in 2006 in order to protect bank customers. Dispute resolution through bank mediation is only applicable

subsequent to a failed customer complaint settlement process by the related bank. Bank mediation also aims to

give smaller customers access to dispute resolution with a bank through a simple, cheap and prompt method.

A number of arduous challenges continue to mar the banking sector at the beginning of 2012. Externally,

the main threat stems form a potential further slowdown in the already protracted global economic recovery

process. Meanwhile, internally, the contribution made by the banking sector to national economic development

remains sub-optimal. A corresponding increase in the contribution to the national economy has not occurred

in harmony with asset growth in the banking industry, among others, due to unproductive bank assets from a

macro perspective in the form of excess liquidity placed in monetary instruments as well as tradable government

securities (SBN). Furthermore, the level of efficiency in the banking industry also remains relatively low. These

issues contribute to the relatively high lending rates offered by banks in Indonesia. Therefore, future banking

policy will continue to prioritise bank competitiveness, while strengthening bank resilience and encouraging

bank intermediation.

Chapter IBank Structure andPerformance in 2011

Banking Supervision Report 20118

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

This page is intentionally left blank

9

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Bank StructureCongruent to 6.5% domestic economic growth in 2011, the banking sector reinforced its position as a pivotal

element of the financial system in Indonesia by expanding its business interests through additional branch offices

in various regions of the archipelago. Nearly 1,000 new office units were reported in 2011 consisting of branch

offices, sub-branch offices and cash handling offices, dominated by foreign exchange banks, which aggressively

moved to expand their network coverage.

Table 1.1 Number of Banks and Branch Offices

State-owned Banks Total Banks 4 4 4 Total Branch Offices 3854 4189 4362

Foreign Exchange Banks Total Banks 34 36 36 Total Branch Offices 6181 6608 7209

Non-Foreign Exchange Banks Total Banks 31 31 30 Total Branch Offices 976 1131 1288

Regional Banks Total Banks 26 26 26 Total Branch Offices 1358 1413 1472

Joint-Venture Banks Total Banks 16 15 14 Total Branch Offices 238 263 260

Foreign Banks Total Banks 10 10 10 Total Branch Offices 230 233 206

Total Total Banks 121 122 120 Total Branch Offices 12837 13837 14797

Number of Conventional Commercial Banks 115 111 109Number of Islamic Banks 6 11 11

Bank Group 2009 2010 2011

Commercial Banks1

The number of conventional commercial banks operating at yearend 2011 totalled 109 compared to 111 in

the preceding year. The slight decline was attributable to a merger and business license revocation as follows:

1. The merger between PT. Bank OCBCNISP and PT. Bank OCBC Indonesia to become PT. Bank OCBCNISPTbk pursuant to Governor Decree No.12/86/KEP.GBI/2010, dated 22nd December 2010. However, the merger was executed in 2011.

1) Commercial banks here refer to conventional commercial banks and Islamic banks.

Banking Supervision Report 201110

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

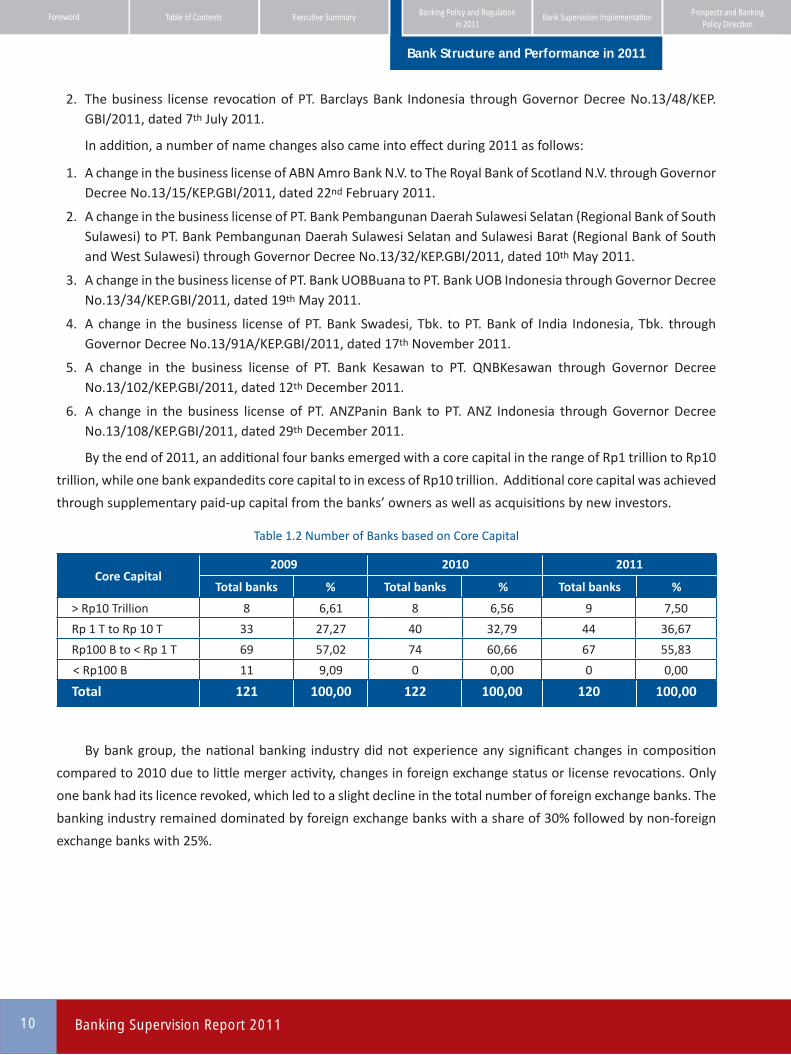

2. The business license revocation of PT. Barclays Bank Indonesia through Governor Decree No.13/48/KEP.GBI/2011, dated 7th July 2011.

In addition, a number of name changes also came into effect during 2011 as follows:

1. A change in the business license of ABN Amro Bank N.V. to The Royal Bank of Scotland N.V. through Governor Decree No.13/15/KEP.GBI/2011, dated 22nd February 2011.

2. A change in the business license of PT. Bank Pembangunan Daerah Sulawesi Selatan (Regional Bank of South Sulawesi) to PT. Bank Pembangunan Daerah Sulawesi Selatan and Sulawesi Barat (Regional Bank of South and West Sulawesi) through Governor Decree No.13/32/KEP.GBI/2011, dated 10th May 2011.

3. A change in the business license of PT. Bank UOBBuana to PT. Bank UOB Indonesia through Governor Decree No.13/34/KEP.GBI/2011, dated 19th May 2011.

4. A change in the business license of PT. Bank Swadesi, Tbk. to PT. Bank of India Indonesia, Tbk. through Governor Decree No.13/91A/KEP.GBI/2011, dated 17th November 2011.

5. A change in the business license of PT. Bank Kesawan to PT. QNBKesawan through Governor Decree No.13/102/KEP.GBI/2011, dated 12th December 2011.

6. A change in the business license of PT. ANZPanin Bank to PT. ANZ Indonesia through Governor Decree No.13/108/KEP.GBI/2011, dated 29th December 2011.

By the end of 2011, an additional four banks emerged with a core capital in the range of Rp1 trillion to Rp10

trillion, while one bank expandedits core capital to in excess of Rp10 trillion. Additional core capital was achieved

through supplementary paid-up capital from the banks’ owners as well as acquisitions by new investors.

Table 1.2 Number of Banks based on Core Capital

> Rp10 Trillion 8 6,61 8 6,56 9 7,50

Rp 1 T to Rp 10 T 33 27,27 40 32,79 44 36,67

Rp100 B to < Rp 1 T 69 57,02 74 60,66 67 55,83

< Rp100 B 11 9,09 0 0,00 0 0,00

Total 121 100,00 122 100,00 120 100,00

Core CapitalTotal banks Total banks Total banks% % %

2009 2010 2011

By bank group, the national banking industry did not experience any significant changes in composition

compared to 2010 due to little merger activity, changes in foreign exchange status or license revocations. Only

one bank had its licence revoked, which led to a slight decline in the total number of foreign exchange banks. The

banking industry remained dominated by foreign exchange banks with a share of 30% followed by non-foreign

exchange banks with 25%.

11

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

When observed in terms of asset composition, foreign exchange banks continued to dominate, followed by

state-owned banks, which despite numbering just four in total accounted for an impressive 36.67% of total bank

assets. In general, all bank groups experienced asset growth during the period from 2009 to 2011.

State-owned

Foreign exchange

Non-foreign exchange

Regional

Joint-venture

Foreign

22%

25%

12%8%

3%

30%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

(Million Rp)

2009 2010 2011

State-owned Foreignexchange

Non-foreignexchange

Regional Joint-venture Foreign

5

10

15

20

25

30

35

40

Stateowned

Foreignexchange

Non-foreignexchange

Regional Jointventure

Foreign

Dec 2009 Dec 2010 Dec 2011

5%7%

31%

40%

3%

8% State-owned

Foreign exchange

Non-foreign exchange

Regional

Joint-venture

Foreign

Figure 1.1 Bank Composition by Bank Group in 2011

Figure 1.3 Total Assets by Bank Group

Figure 1.2 Number of Banks

Figure 1.4 Asset Composition by Bank Group in 2011

Islamic Banking

The number of banks undertaking business activity based on Islamic principles increased during the reporting

period in line with the establishment of new banks, sharia business units (UUS) at conventional commercial banks

as well as new Islamic rural banks. The number of sharia business units increased by one from 23 to 24, namely

UUS BPD Jambi, while no change was reported in the number of Islamic banks, which total 11. The number

of Islamic rural banks (BPRS) increased by five from 150 to 155, consisting of six new business licenses, one

conversion from a conventional rural bank, one merger and one BPRS license revocation. BPRS SyarifHidayatullah

in the operational area of Cirebon had its business license revoked, while the one merger was BPRS BerkahAmal

Salman absorbed into BPRS Al Salaam Amal Salman.

Banking Supervision Report 201112

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

The establishment of new Islamic banks followed by an additional 338 Islamic bank branch offices in 2011

helped broaden service coverage. Of that total, 260 offices represented a new office network of BUS-UUS, while

78 made up a new network of Islamic rural banks. The majority of new branch offices were established in the

form of sub-branches (KCP). In addition to the Islamic bank office network, Islamic Service Units operating at

1,277 branches of conventional commercial banks also offer Islamic banking services.

Name of Bank Operational Area

PT. BPRS Way Kanan LampungPT. BPRS Oloan Ummah Sidempuan SibolgaPT. BPRS Dharma Kuwera Solo

PT. BPRS Kota Mojokerto Surabaya

PT. BPRS Mitra Harmoni Kota Bandung Bandung

PT. BPRS Gajahtongga Kotopiliang Padang

PT. BPRS Cahaya Hidup Yogyakarta

Table 1.3 New Islamic Rural Banks in 2011

Bank Group 2009 2010 2011

Islamic Commercial Bank 6 11 11 Islamic Business Unit 25 23 24 - Number of BUS and UUS branches 998 1477 1737 - Number of Islamic Service Units 1929 1277 1277 Islamic Rural Banks 138 150 155 - Number of Islamic Rural Banks branches 260 286 364

Table 1.4 Development of the Islamic Bank Office Network

Office Network 2009 2010 2011

Head Office 1.733 1.706 1.669 Branch Office 946 1.088 1.223 Cash Office 965 1.116 1.280 Total 3.644 3.910 4.172

Table 1.5 The Office Network of Conventional Rural Banks

Rural Banks (BPR)

The number of branches and service coverage area continued to expand, which further extended rural

banking services to micro and small enterprises (MSE). The number of branch offices reached 1,223 in 2011,

while cash handling offices totalled 1,280.

13

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

The establishment of new rural banks outside the islands of Java and Bali increased. Bank Indonesia

continuously strives to nurture BPR growth evenly in all regions of Indonesia but primarily away from the

islands of Java and Bali due to the higher concentrations found there. Lower paid-up capital requirements are

applicable to areas outside of Java and Bali, which aims to spread the benefits of rural banking services to all

regions in the archipelago, particularly to micro, small and medium enterprises.

Of the 25 new rural banks, 23 are located outside the islands of Java and Bali. Furthermore, the mergers

of 23 rural banks operating on Java and Bali explain why the number of rural banks on these two islands

experienced a decline. In addition, Bank Indonesia was forced to revoke the business licenses of 14 rural

banks in 2011, 10 of which were located on Java and Bali.

Location of Rural Bank2009 2010 2011

Total % Total % Total %

Java-Bali 1.294 74,7 1.264 74,1 1.208 72,4 Outside Java-Bali 439 25,3 442 25,9 461 27,6 Total 1.733 100 1.706 100 1.669 100

Table 1.6 The Development of Rural Banks

Legal Entity2009 2010 2011

from to from to from to

Limited Company 52 6 26 4 2 1 Regional Company 23 4 5 1 53 6 Cooperative - - - - - - Total 75 10 31 5 55 7

Table 1.7 Mergers and Consolidations in the Rural Banking Industry

Policy to reinforce the structure of the rural banking industry was implemented by, among others,

encouraging mergers (combining two or more rural banks to maintain the business continuity of one of the

rural banks) and consolidation (combining two or more rural banks to form a new rural bank). In 2011, a

total of 55 rural banks were merged and consolidated into just seven rural banks. Of the total 55 rural banks,

local government owned 53 as regional companies (PD), of which 21 merged into three rural banks and

32 consolidated into another three rural banks. In addition, two rural banks were privately owned limited

companies that merged into one rural bank.

Banking Supervision Report 201114

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Currently, the number of limited company rural banks is on the increase in line with Bank Indonesia

policy to encourage the formation of limited company rural banks. Limited company rural banks are ideal

for the banking industry rather than regional companies (PD) and cooperatives. In the context of the rural

banking industry the form of legal entity reflects the ownership composition of the rural bank in question. For

instance, a PD rural bank is owned by the local government, while a limited company denotes that some or

all of the shares are privately owned.

License

Area Principle License

Business License

Merger

from to

Jabodetabek * - 1 - - Jawa Barat - 1 51 5 Jawa Tengah & DIY 1 - - - Jawa Timur - - 2 1 Bali & Nusa Tenggara 1 1 2 1 Sumatera 5 12 - - Kalimantan 5 2 - - Sulampua ** 1 8 - - Total 13 25 55 7

Table 1.8 Licensing Data for 2011

*) Jakarta, Bogor, Depok, Tangerang/Banten, Bekasi dan Karawang **) Sulawesi, Maluku dan Papua

Legal Entity2009 2010 2011

Total % Total % Total %

Limited Company 1.375 79,3 1.384 81,1 1.388 83,2 Regional Company 324 18,7 288 16,9 247 14,8 Cooperative 34 2,0 3,4 2,0 34 2,0 Total 1.733 100 1.706 100 1.669 100

Table 1.9 Number of Rural Banks based on Typeof Legal Entity

Bank PerformanceThe performance of the banking sector was positive during 2011. Anaemic global financial conditions

stemming from a protracted debt crisis in Europe and a sluggish US economy had no discernable impact on the

banking sector in Indonesia. Financial system stability was maintained, as reflected by the variety of positive

achievements attained by the banking industry throughout 2011. Bank deposits grew robustly, of which the

majority was used to finance credit growth. Credit expansion was undertaken paying due regard to the prevailing

prudential corridor, thereby maintaining non-performing loans at an acceptably low level. Furthermore, bank

capital was preserved at an adequate level buoyed by solid profitability.

15

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

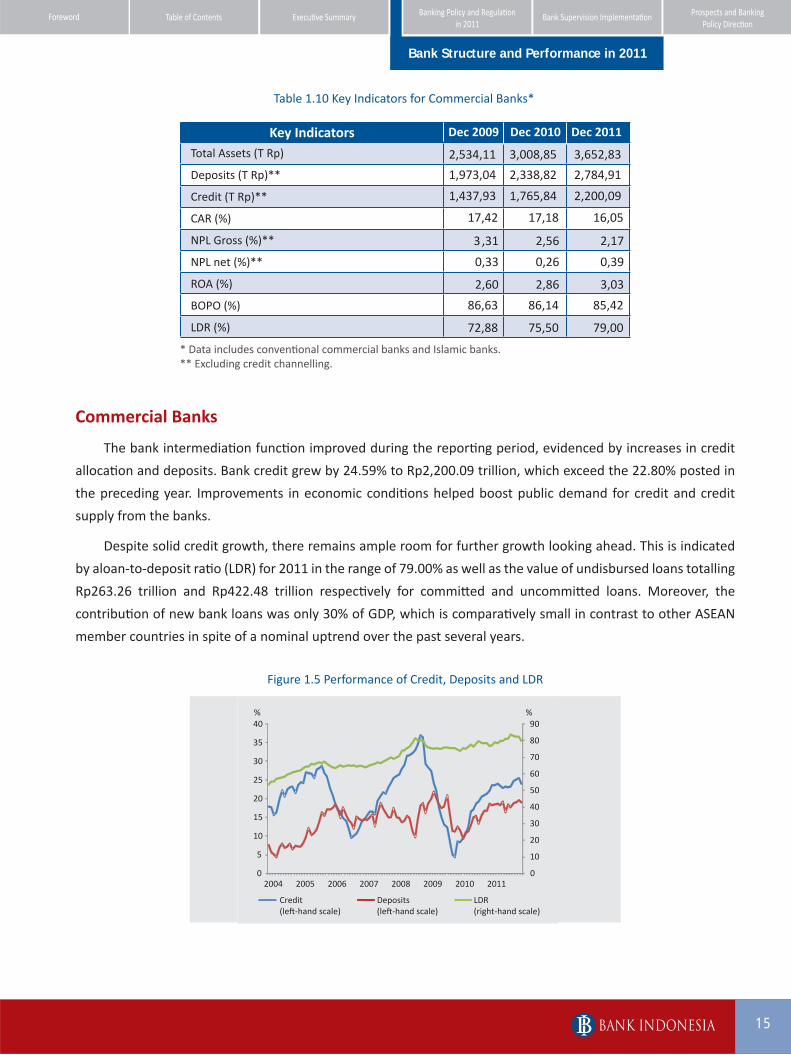

Table 1.10 Key Indicators for Commercial Banks*

* Data includes conventional commercial banks and Islamic banks.** Excluding credit channelling.

Commercial Banks

The bank intermediation function improved during the reporting period, evidenced by increases in credit

allocation and deposits. Bank credit grew by 24.59% to Rp2,200.09 trillion, which exceed the 22.80% posted in

the preceding year. Improvements in economic conditions helped boost public demand for credit and credit

supply from the banks.

Despite solid credit growth, there remains ample room for further growth looking ahead. This is indicated

by aloan-to-deposit ratio (LDR) for 2011 in the range of 79.00% as well as the value of undisbursed loans totalling

Rp263.26 trillion and Rp422.48 trillion respectively for committed and uncommitted loans. Moreover, the

contribution of new bank loans was only 30% of GDP, which is comparatively small in contrast to other ASEAN

member countries in spite of a nominal uptrend over the past several years.

0

10

20

30

40

50

60

70

80

90

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011

% %

Credit(left-hand scale)

Deposits(left-hand scale)

LDR(right-hand scale)

Figure 1.5 Performance of Credit, Deposits and LDR

2,534,11 3,008,85 3,652,83

1,973,04 2,338,82 2,784,91

1,437,93 1,765,84 2,200,09

17,42 17,18 16,05

* 3 ,31

2,56

2,17

* 0,33 0,26 0,39

2,60 2,86 3,03

86,63 86,14 85,42

72,88 75,50 79,00

Total Assets (T Rp)

Deposits (T Rp)**

Credit (T Rp)**

CAR (%)

NPL Gross (%)**

NPL net (%)**

ROA (%)

BOPO (%)

LDR (%)

Key Indicators Dec 2009 Dec 2010 Dec 2011

Banking Supervision Report 201116

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Growth in productive credit, namely working capital credit and investment credit, continued to dominate

overall credit growth. Investment credit posted significant growth at 33.21% compared to that recorded in

2009 and 2010 at 16.43% and 16.98% correspondingly. Impressive growth in investment credit was primarily

attributable to improvements in the national economy coupled with positive investor expectations as a result

of Indonesia’s upgraded status to investment grade affirmed by Fitch Ratings in December 2011. Propitious

domestic economic conditions further catalysed activity in the business community, thereby expanding the

share of micro and small enterprises in the national credit portfolio by 24.21%. Meanwhile, the 24.21% growth

reported in consumption credit originated from mortgages, motor vehicle loans, credit cards and multipurpose

loans.

2.7%

16.4% 19.0%

10.0%

25.2%

17.0%

22.9% 22.8% 21.4%

33.2%

24.2% 24.6%

0%

5%

10%

15%

20%

25%

30%

35%

WorkingCapital Credit

InvestmentCredit

ConsumptionCredit

Total Credit

2009 2010 2011

Figure 1.6 Credit Growth by Loan Type

26.07%

43.04%

25.12%

34.37%

18.73%

19.37%

26.70%

24.94%

31.08%

24.41%

24.59%

-50% 0% 50% 100% 150% 200%

2009

2010

2011

Total

Others

Social Services

Corporate Services

Transportation

Trade

Construction

Electricity

Industry

Mining

Agriculture

Figure 1.7 Credit Growth by Economic Sector

All economic sectors experienced positive credit growth in 2011. The strongest credit growth was reported in

the mining sector (43.04%), followed by electricity (34.37%) and social services (31.08%). Nominally, the largest

increases in credit stemmed from the others sector, industrial sector and trade sector. In addition, the following

sectors experienced larger increases in credit compared to the previous year, namely the manufacturing sector,

mining, agriculture, utilities (electricity, gas and water), construction and corporate services.

17

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Encouragingly, non-performing loans trended downwards, despite increasing from the first until third

quarter of 2011, thanks to a dramatic decline in the final quarter in line with bank restructuring and write-offs.

At yearend 2011, the gross ratio of non-performing bank loans had dropped to 2.17% (the lowest in a decade) as

a result of improved credit quality followed by rapid credit growth.

0

10

20

30

40

50

60

0

1

2

3

4

5

6

2007 2008 2009 2010 2011

Rp T% PPAP

(right scale)

Nominal NPL (right scale)

NPL Gross(left scale)NPL Net

(left scale)

Figure 1.8 Non-Performing Loans

The composition of credit in earning assets reached a share of 64.47% in 2011, topping that recorded

in the preceding year at 63.84%. Meanwhile, another earning asset that also experienced an increase was

placements at Bank Indonesia (predominantly using the deposit facility). In contrast, placements in securities

(including SUN) underwent a decline.

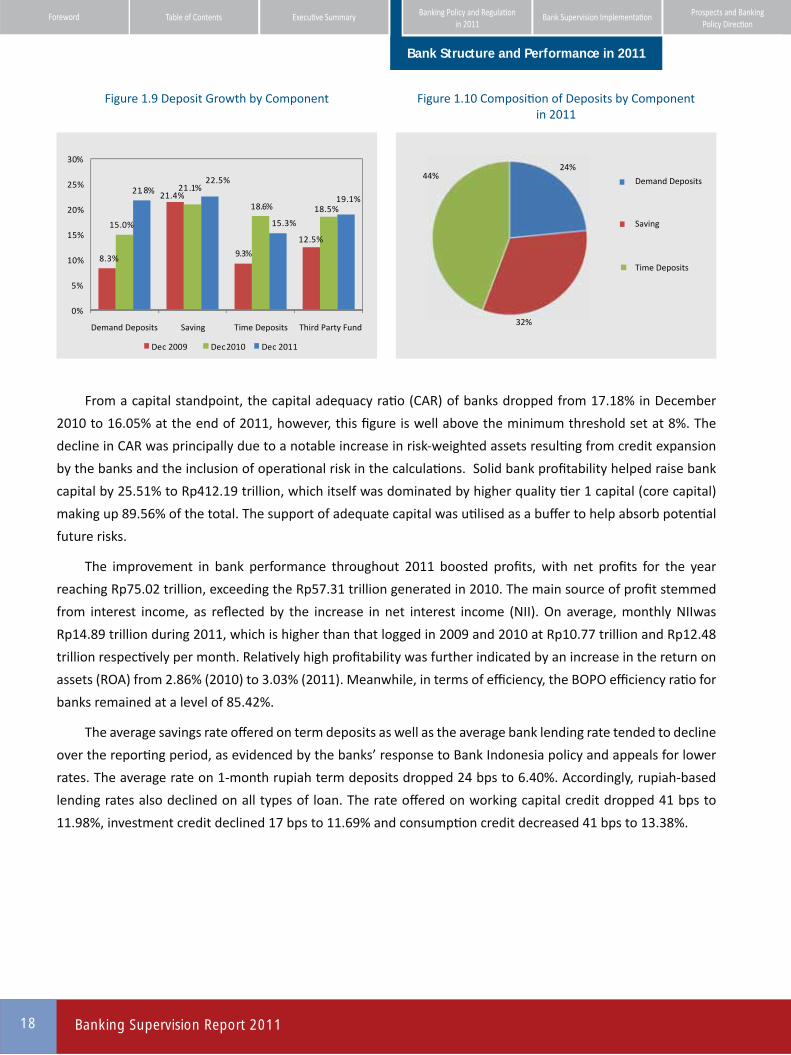

Positive performance was further reported on all components of deposits, namely checking accounts,

savings accounts and term deposits. Deposits grew by 19.07% to Rp2,784.91 trillion. By component, checking

accounts grew 21.80%to Rp652.65 trillion, exceeding growth posted in 2009 and 2010 when just 8.35% and

15.02% growth was documented respectively. Term deposits grew 15.34% to Rp1,233.97 trillion, which was

less impressive than the growth registered in 2010 at 18.64% but higher than that in 2009 (9.34%). The growth

in savings accounts during the reporting period was 22.52%, surpassing that in 2009 and 2010 at 21.00%.

Holistically, term deposits continued to dominate bank deposits with a 44.31% share, shrinking slightly when

compared to the previous year at 45.74%. The growth in deposits was harmonious with the escalation in activity

in the business community as well as growing interest from the general public to deposit their funds at a bank.

Banking Supervision Report 201118

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

From a capital standpoint, the capital adequacy ratio (CAR) of banks dropped from 17.18% in December

2010 to 16.05% at the end of 2011, however, this figure is well above the minimum threshold set at 8%. The

decline in CAR was principally due to a notable increase in risk-weighted assets resulting from credit expansion

by the banks and the inclusion of operational risk in the calculations. Solid bank profitability helped raise bank

capital by 25.51% to Rp412.19 trillion, which itself was dominated by higher quality tier 1 capital (core capital)

making up 89.56% of the total. The support of adequate capital was utilised as a buffer to help absorb potential

future risks.

The improvement in bank performance throughout 2011 boosted profits, with net profits for the year

reaching Rp75.02 trillion, exceeding the Rp57.31 trillion generated in 2010. The main source of profit stemmed

from interest income, as reflected by the increase in net interest income (NII). On average, monthly NIIwas

Rp14.89 trillion during 2011, which is higher than that logged in 2009 and 2010 at Rp10.77 trillion and Rp12.48

trillion respectively per month. Relatively high profitability was further indicated by an increase in the return on

assets (ROA) from 2.86% (2010) to 3.03% (2011). Meanwhile, in terms of efficiency, the BOPO efficiency ratio for

banks remained at a level of 85.42%.

The average savings rate offered on term deposits as well as the average bank lending rate tended to decline

over the reporting period, as evidenced by the banks’ response to Bank Indonesia policy and appeals for lower

rates. The average rate on 1-month rupiah term deposits dropped 24 bps to 6.40%. Accordingly, rupiah-based

lending rates also declined on all types of loan. The rate offered on working capital credit dropped 41 bps to

11.98%, investment credit declined 17 bps to 11.69% and consumption credit decreased 41 bps to 13.38%.

8.3%

21.4%

9.3%

12.5%

15.0%

21.1%

18.6% 18.5%

21.8%22.5%

15.3%

19.1%

0%

5%

10%

15%

20%

25%

30%

Demand Deposits Time DepositsSaving Third Party Fund

Dec 2009 Dec 2010 Dec 2011

44%24%

32%

Demand Deposits

Time Deposits

Saving

Figure 1.9 Deposit Growth by Component Figure 1.10 Composition of Deposits by Componentin 2011

19

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Islamic Banks

In a similar vein as conventional banks, the performance of Islamic banks in 2011 was positive. Despite

the ongoing wave of global financial turmoil, Islamic banks have remained unexposed and unaffected by global

conditions due to their lack of exposure to domestic and global financial markets. Pursuant to Act No.21, 2008,

Islamic banks operate to store and allocate the public’s funds in order to support national development. In

addition, Islamic banks also have a social function as treasury receiving funds from zakat, infak, sedakah, grants

and other social funds and subsequently allocating the funds to zakat management organisations. Another social

function is storing wakaf funds and disbursing them to a wakaf manager.

Sound performance by Islamic banks was further demonstrated through strong gains in terms of

accumulating funds, the majority of which was used to extend financing. Financing was expanded with due

consideration paid to prudential banking as the policy direction of Bank Indonesia as well as sharia compliance

outlined by the National Sharia Board. Therefore, the ratio of non-performing financing remained under control

while holding steadfast in the corridor of business activity based on Islamic principles. Capital at Islamic banks

was also maintained, among others, supported by solid business profitability.

Islamic Banks (BUS) and Sharia Business Units (UUS)

The intermediation function of Islamic banks and sharia business units improved during 2011, as indicated

by increases in deposits held and financing allocated. Deposits grew expansively by Rp39.38 trillion (51.80%) and,

similarly, financing grew by Rp34.47 trillion (50.56%) compared to 45.43% in the previous year. Meanwhile, the

intermediation function in 2011, according to the financing-to-deposit ratio (FDR), surpassed that of conventional

banks amounting to 88.94%.

2006

(%)

WCC

19181716151413121110

987654

IC CC 1-Month Term Deposits

2007 2008 2009 2010 2011

Figure 1.11 Average Lending Rates and Savings Rates ofCommercial Banks

Banking Supervision Report 201120

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Financing dominated funds placed at Islamic banks compared to other types of placement, like placements

held at Bank Indonesia, other banks or securities. This is clearly evidenced by the 70.57% share of financing in

the total assets of Islamic banks and sharia business units, while for Islamic rural banks the share is more like

76.10%. Consequently, Islamic bank intermediation functioned well. Nominally, the increase in share was in

line with the rate of Islamic bank financing growth that achieved 49.96% (yoy), surpassing growth posted in the

previous year at 44.91%.

In addition to financing, Islamic banks also held placements at Bank Indonesia, amounting to 18.65% of their

total assets. Excluding checking accounts to meet the minimum statutory reserve requirement, in 2011 Islamic

banks placed Rp20.89 trillion in FASBIS and SBIS instruments as part of their liquidity management strategy. In

accord with the burgeoning placements in FASBIS and SBIS as secondary reserves, the liquid assets of Islamic

banks and sharia business units increased by 49.04% (yoy) to Rp30.99 trillion. This growth in liquid assets helped

strengthen the capacity of Islamic banks to cover potential withdrawals of deposits. This is also indicated by the

ratio of liquid assets to non-core deposits, which skyrocketed 155.28% to 159.12% in the same period. Such

conditions reflect the growing ability of Islamic banks to anticipate liquidity risk.

Nominally, consumption financing and working capital dominated Islamic bank financing (BUS and UUS)

with respective shares amounting to 41.94% and 40.62%. In terms of growth, however, consumption financing

grew most rapidly by 87.92% over the previous year. This increase was dominated by qardhgold-backed

transactions, better known among the general public as ‘Gadai Emas’ (Pawning Gold). Considering that Islamic

banks help stimulate real sector growth, Bank Indonesia re-evaluated the regulations concerning pawning gold

by prioritising the use of this product to meet the urgent needs of the community and to avoid providing any

space for speculative activity stemming from gold price hikes.

Key Indicators 2009 2010 2011

Total Assets (T Rp) 66,09 97,52 145,47Deposits (T Rp) 52,27 76,03 115,41iB Financing (T Rp) 46,88 68,18 102,65CAR (%) 10,77 16,25 16,63NPFs Gross (%) 4,01 3,02 2,52NPFs Net (%) 1,84 1,6 1,34ROA (%) 1,48 1,67 1,79BOPO (%) 86,63 86,14 85,42FDR (%) 89,70 89,67 88,94

Table 1.11 Key Indicators of Islamic Banks and Sharia Business Units

21

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Agriculture

42,05%

2,14% 1,69%3,97% 2,32%

5,71%

9,53%

3,28%

24,97%4,35%

Construction

Social

Mining

Trade

Industry

Transportation

Electricity

World

Others

Figure 1.12 Credit by Sector (BUS and UUS) in 2011

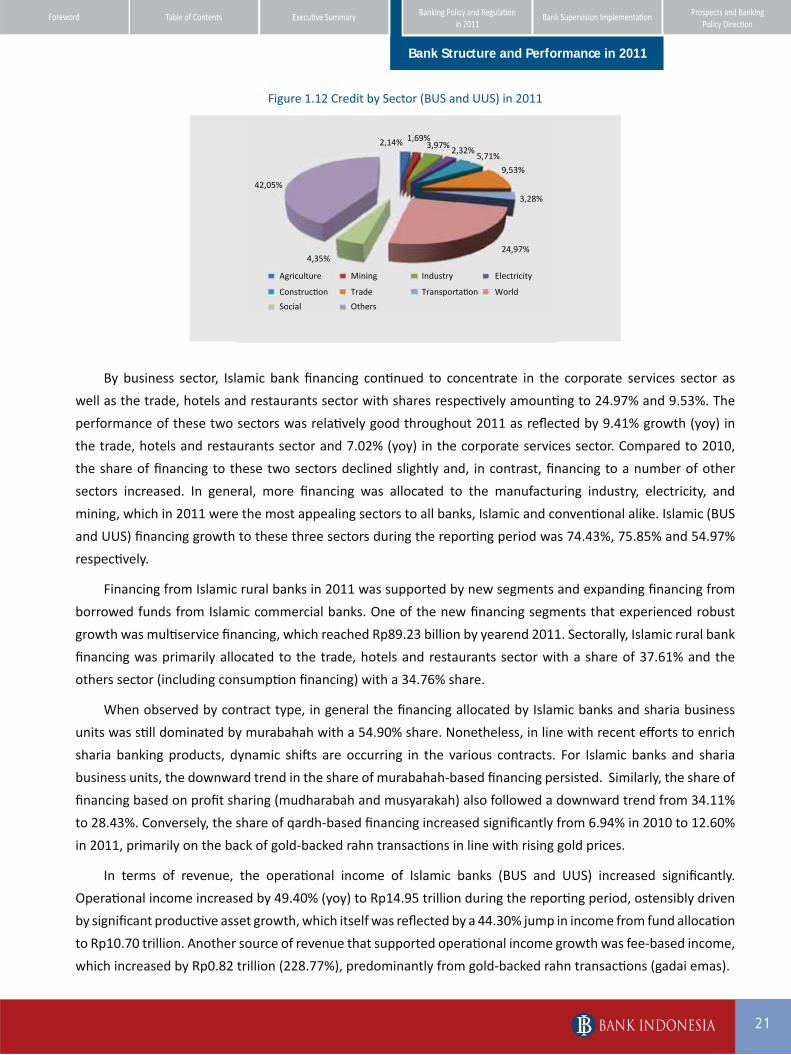

By business sector, Islamic bank financing continued to concentrate in the corporate services sector as

well as the trade, hotels and restaurants sector with shares respectively amounting to 24.97% and 9.53%. The

performance of these two sectors was relatively good throughout 2011 as reflected by 9.41% growth (yoy) in

the trade, hotels and restaurants sector and 7.02% (yoy) in the corporate services sector. Compared to 2010,

the share of financing to these two sectors declined slightly and, in contrast, financing to a number of other

sectors increased. In general, more financing was allocated to the manufacturing industry, electricity, and

mining, which in 2011 were the most appealing sectors to all banks, Islamic and conventional alike. Islamic (BUS

and UUS) financing growth to these three sectors during the reporting period was 74.43%, 75.85% and 54.97%

respectively.

Financing from Islamic rural banks in 2011 was supported by new segments and expanding financing from

borrowed funds from Islamic commercial banks. One of the new financing segments that experienced robust

growth was multiservice financing, which reached Rp89.23 billion by yearend 2011. Sectorally, Islamic rural bank

financing was primarily allocated to the trade, hotels and restaurants sector with a share of 37.61% and the

others sector (including consumption financing) with a 34.76% share.

When observed by contract type, in general the financing allocated by Islamic banks and sharia business

units was still dominated by murabahah with a 54.90% share. Nonetheless, in line with recent efforts to enrich

sharia banking products, dynamic shifts are occurring in the various contracts. For Islamic banks and sharia

business units, the downward trend in the share of murabahah-based financing persisted. Similarly, the share of

financing based on profit sharing (mudharabah and musyarakah) also followed a downward trend from 34.11%

to 28.43%. Conversely, the share of qardh-based financing increased significantly from 6.94% in 2010 to 12.60%

in 2011, primarily on the back of gold-backed rahn transactions in line with rising gold prices.

In terms of revenue, the operational income of Islamic banks (BUS and UUS) increased significantly.

Operational income increased by 49.40% (yoy) to Rp14.95 trillion during the reporting period, ostensibly driven

by significant productive asset growth, which itself was reflected by a 44.30% jump in income from fund allocation

to Rp10.70 trillion. Another source of revenue that supported operational income growth was fee-based income,

which increased by Rp0.82 trillion (228.77%), predominantly from gold-backed rahn transactions (gadai emas).

Banking Supervision Report 201122

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Figure 1.14 Profitability of Islamic banks

Figure 1.13 Income, Costs and Efficiency of BUS and UUS

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2

4

6

8

10

12

14

16(T Rp)

2009 2010 2011

Operational income(left scale)

profit sharing(left scale)

overheads(left scale)

profit sharing/operational income(right scale)

overheads/operational income(right scale)

0%

3%

6%

9%

12%

15%

18%

21%

24%

27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2009 2010 2011

Profit of BUS and UUS(%, yoy) (left scale)

Profit of Islamic rural banks(%, yoy) (left scale)

ROE of BUS(right scale)

ROE of Islamic rural banks(right scale)

ROA of BUS and UUS(right scale)

ROA of Islamic rural banks(right scale)

The accomplishment of (increased) asset productivity and efficiency raised the net operational margin of

Islamic banks (BUS and UUS) from 1.73% (2010) to 1.94% (2011). The 2011 profits of BUS and UUS grew by

40.33% to Rp1.48 trillion. This increase in profit precipitated a corresponding increase in the return on assets

from 1.67% in 2010 to 1.79% in 2011. Meanwhile, in terms of the return on investment, the increase in profit

was not accompanied by an increase in ROE, which actually declined from 17.63% to 15.72%. This was caused by

additional paid-up capital at a number of Islamic commercial banks.

Islamic Rural Banks

The condition of Islamic rural banks during the past year of 2011 was sound with financial indicators

demonstrating positive growth, even exceeding that posted in the preceding year. Total assets of Islamic rural

banks increased 28.21% from Rp2.73 trillion (2010) to Rp3.50 trillion (2011). Meanwhile, the financing allocated

and deposits accumulated grew respectively by 29.61% and 30.63% on the strength of aggressive business

expansion in terms accruing funds (funding) and extending financing. In 2011, Islamic rural banks maintained a

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

23ix

Daftar Isi

Kata Pengantar Ringkasan EksekutifStruktur dan Kinerja

PerbankanKebijakan dan Regulasi

PerbankanPengawasan Perbankan

Prospek dan Arah Kebijakan Perbankan

Lampiran Glosari

Daftar Tabel1.1 Perkembangan Jumlah Bank dan Kantor Bank 11

1.2 Jumlah Bank Berdasarkan Modal Inti 13

1.3 Perkembangan Jumlah Bank Umum Syariah dan Jaringan Kantor 15

1.4 Pendirian BPRS Baru Tahun 2010 16

1.5 Perkembangan Jaringan Kantor BPR Konvensional 16

1.6 Penyebaran BPR 17

1.7 Perkembangan Merger dan Konsolidasi Industri BPR 18

1.8 Data Perizinan dan Pencabutan izin Usaha BPR Tahun 2010 18

1.9 Indikator Utama Bank Umum 23

1.10 Perkembangan Indikator Perbankan Syariah (BUS dan UUS) 28

1.11 Perkembangan Indikator BPRS 30

1.12 Perkembangan Kredit dan Kualitas kredit BPR 32

1.13 Indikator Utama BPR 33

2.1 Pokok-pokok Pengaturan dan Jadwal Implementasi Basel III 61

3.1 Realisasi Pemeriksaan Bank Umum Konvensional 2010 88

3.2 Uji Kemampuan dan Kepatutan Bank Umum Konvensional 93

3.3 Rekapitulasi Fit dan Proper test BPR Konvensional Tahun 2010 94

3.4 Statistik Investigasi Periode Januari - Desember 2010 95

3.5 Jumlah Sengketa yang Diterima Bank Indonesia 97

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

competitive level of profit sharing, which nurtured long-term customer loyalty and attracted new customers. In

addition, a relatively competitive murabahah financing margin helped BPRS financing flourish.

Key Indicators 2009 2010 2011

Total Assets (T Rp) 2,12 2,73 3,50Deposits (T Rp) 1,25 1,60 2,09iB Financing (T Rp) 1,58 2,06 2,67CAR (%) 30,00 27,50 23,50NPFs Gross (%) 8,12 6,50 6,11NPFs Net (%) 6,65 5,36 5,14ROA (%) 3,50 3,50 2,70BOPO (%) 77,00 78,10 76,30FDR (%) 126,47 128,47 127,71

Table 1.12 Key Indicators for Islamic Rural Banks

One reason for the increase in Islamic rural bank financing was expansion, as denoted by the financing-to-

deposit ratio (FDR) in 2011 totalling 127.71%, which was made possible by dynamic business expansion to new

financing segments as well as new financing funded by resources borrowed from Islamic commercial banks (BUS)

(executing). Financing based on sales as well as profit sharing remained the preferred transaction at Islamic rural

banks (BPRS). Murabahahcontinued to dominate the composition of financing with an 80.51% share. Meanwhile,

musyarakahdominatedfinancing based on profit sharing with a share of 9.22%, followed by mudharabah with a

2.83% share. In addition, multiservice financing also performed well amounting to some Rp89.23 billion, which

indicates that Islamic rural banks have successfully earned the trust of the general public to fund their health,

educational and religious needs.

Figure 1.15 Composition of Islamic Rural Bank Financing in 2011

Murabahah

Mudharabah

Musyarakah

Qardh

Multiservice

Others

80%

2,8%

9,2%

2,7%3,3% 1,4%

Banking Supervision Report 201124

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary Foreword

Working capital

Investment

Consumption

35%

55%

10%

Figure 1.16 Financing based on Type in 2011

Figure 1.17 Financing based on Economic Sector in 2011

0,09%

0,10%

1,26%

1,36%

3,44%

3,46%

8,37%

9,54%

34,76%

37,61%

0,00% 5,00% 10,00% 15,00% 20,00% 25,00% 30,00% 35,00% 40,00%

Trade, Restaurants and Hotels

Others

Corporate Services

Agriculture

Construction

Social Services

Transportation, Warehousing and Communications

Industry

Electricity, Gas and Water

Mining

Relatively high financing growth was accompanied by a decline in non-performing financing at Islamic rural

banks from 5.36% in 2010 to 5.14% in 2011. The NPF ratio of Islamic rural banks was lower than that of rural

banks nationally for the same period (5.22%). Increasing competition among customer businesses was partially

responsible for the small nominal increase in non-performing financing. Solid financing growth coupled with

a low NPF ratio allowed Islamic rural banks to post greater profits than in the previous year. The operational

income of Islamic rural banks increased 20.97% to Rp0.59 trillion in 2011. Meanwhile, the operational costs of

Islamic rural banks increased 22.12% to Rp299.247 billion in the same period. Consequently, 21.17% growth in

profits was recorded from Rp83.9 billion in 2010 to Rp101.66 billion in 2011.

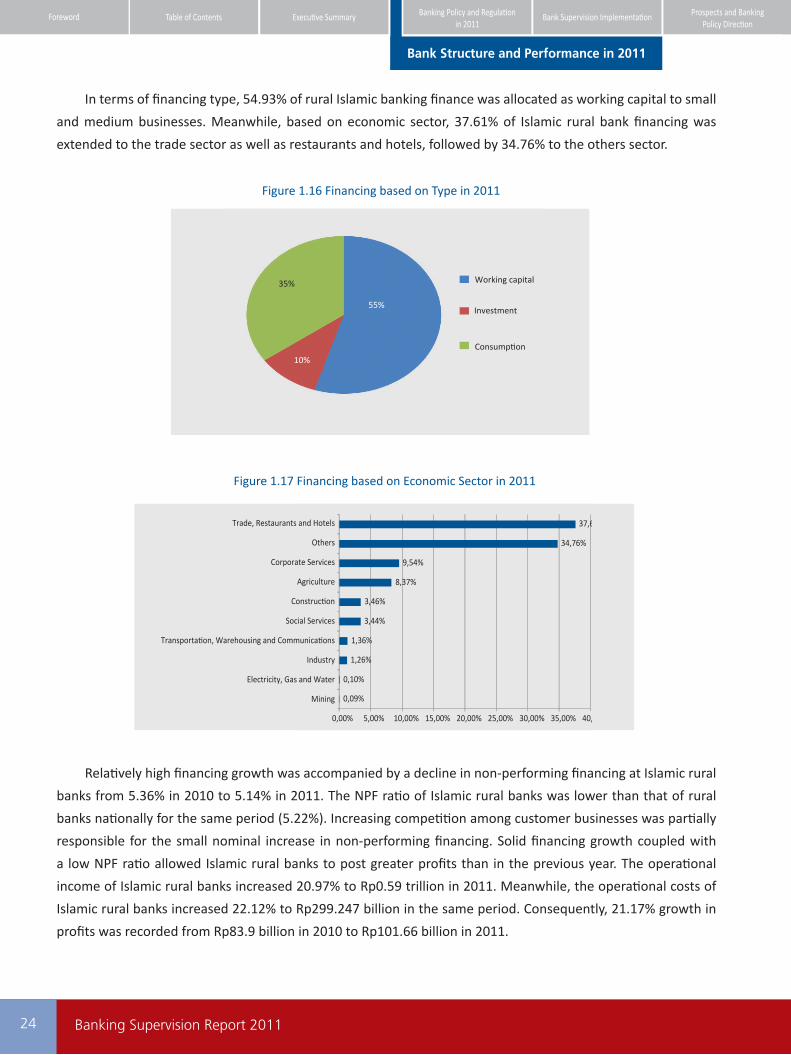

In terms of financing type, 54.93% of rural Islamic banking finance was allocated as working capital to small

and medium businesses. Meanwhile, based on economic sector, 37.61% of Islamic rural bank financing was

extended to the trade sector as well as restaurants and hotels, followed by 34.76% to the others sector.

25

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Rural Banks (BPR)

The rural banking industry managed to grow amid increasingly tight competition. The ever-expanding

number of micro-finance institutions had no discernable effect on BPR performance. In 2011, the rural banking

industry developed naturally, with total assets increasing by 21.99% from Rp45.74 trillion to Rp55.78 trillion,

while credit grew 21.44% from Rp38.84 trillion to Rp41.10 trillion. Furthermore, growth in deposits achieved

22.03% from Rp31.31 trillion to Rp38.21 trillion. In a similar vein, rural banks maintained a loan-to-deposit ratio

(LDR) at a level of 78.54%. Meanwhile, ongoing efforts to gradually raise rural bank capital since 2006 have

forced rural banks to augment their paid-up capital according to their location. Paid-up capital increased 16.00%

from Rp4.75 trillion to Rp5.51 trillion in 2011, which raised core capital by 17.10% from Rp6.45 trillion to Rp7.55

trillion. The additional capital helped boost the competitiveness of rural banks, particularly in terms of allocating

financing to micro and small enterprises.

The majority of credit extended by rural banks is to micro, small and medium enterprises (MSME) as their

primary market. Currently, credit from rural banks is grouped according to business type using the criteria for

MSME as stipulated in Act No. 20, 2008, on Micro, Small and Medium Enterprises.

Figure 1.18 Total Assets, Credit and Deposits Figure 1.19 Growth in Credit and Deposits

Dec-2009

Total Assets Credit Deposits

Dec-2010 Dec-2011

60.000

(B Rp)

50.000

40.000

30.000

20.000

10.000

-

- 5,00 10,00 15,00 20,00 25,00 %

2009

2010

2011

Deposits Credit

In line with efforts to expand the role of rural banks in micro financing, the majority of BPR loans are used to

fund productive sectors in the form of working capital credit. The share of working capital credit reached 47.60%

(Rp19.55 trillion), followed by consumption credit accounting for 46.70% (Rp19.17 trillion) and investment credit

with 5.80% (Rp2.36 trillion). Based on business scale, rural bank loans to micro, small and medium enterprises

reached Rp20.51 trillion (49.90%) of total credit equalling Rp41.09 trillion.

Banking Supervision Report 201126

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Key Indicators 2009 2010 2011

Total Assets (T Rp) 37,56 45,74 55,78Deposits (T Rp) 25,55 31,31 38,21Credit (T Rp) 28,00 33,84 41,10CAR (%) 24,17 30,01 28,68NPLs Gross (%) 6,90 6,12 5,22NPLs Net (%) 3,97 4,25 3,67ROA (%) 3,09 3,16 3,32BOPO (%) 81,82 80,97 79,47LDR (%) 109,58 108,09 107,57

Table 1.14 Key Indicators of Rural Banks

Congruous with the improvement in economic conditions subsequent to the economic debacle in 2008,

the rural banking industry has successfully raised the quality of credit it allocates. This was demonstrated by

a decline in the gross NPL ratio of rural banks from 6.12% in 2010 to 5.22% in 2011. In fact, this is the lowest

gross NPL ratio recorded in the past decade. The low level of NPL reduced the burden of reserves that must be

maintained by rural banks, thereby allowing the banks to focus more on credit expansion.

Table 1.13 Credit based on Business Type and Usage

6,12

6,12

5,22

5,22

Credit CategoryPosition (B Rp) Growth (%) Share (%)

By Business type* a. micro b. small c. medium d. large (non-MSME)By Usage a. Working capital b. Investment c. Consumption

*) For 2010 and 2011 data, the criteria for credit based on business type were adjusted according to the MSME criteria stipulated in Act No. 20, 2008, on MSME.

The interest rates offered by rural banks have steadily declined over the past three years. Average rates in

2011 were 30.56% (credit), 5.21% (savings) and 10.25% (term deposits), which were above the average rates

offered by conventional commercial banks. This was due to high transaction costs, like marketing costs and credit

monitoring, as a result of the high volume of borrowers but with relatively small loans. Other factors that have

led to higher lending rates are the relatively high cost of funds and overheads.

27

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Figure 1.20 Interest Rates

0

5

10

15

20

25

30

35

40

%

Jun

-200

8

Aug

-200

8

Oct

-200

8

Dec

-200

8

Feb

-200

9

Apr

-200

9

Jun

-200

9

Aug

-200

9

Oct

-200

9

Dec

-200

9

Feb

-201

0

Apr

-201

0

Jun

-201

0

Aug

-201

0

Oct

-201

0

Dec

-201

0

Feb

-201

1

Apr

-201

1

Jun

-201

1

Aug

-201

1

Oct

-201

1

Dec

-201

1

Savings Term Deposits Allocated Credit

Banking Supervision Report 201128

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

MSME Credit

In January 2011, statistics for MSME credit acknowledged the definition of MSME pursuant to Act

No. 20/2008, which defines micro, small and medium enterprises as productive businesses based on their

assets and turnover (previously defined by the credit ceiling and included consumption loans). MSME credit

statistics present productive credit data for conventional commercial banks, conventional rural banks and

Islamic rural banks. However, during the transition phase MSME credit statistics are presented alongside

MSE credit data (based on credit ceiling) for comparison.

MSME credit growth in 2011 was supported by conducive economic conditions, reflected by the

realisation of Rp85.59 trillion in MSME loans and credit growth amounting to 21.71% (yoy) from Rp394.30

trillion in 2010 to Rp479.89 trillion in 2011. In comparison, when using data based on the credit ceiling, MSE

credit growth at the end of December 2011 equalled 23.93%, up from Rp961.71 to Rp1,191.86 trillion.

The contribution of MSME credit to total bank credit was 21.24%, while the portion of MSE credit to

total bank credit was 52.74%. The difference in the two values stems from the exclusion of consumption

credit in the MSME credit data pursuant to Act No. 20/2008. Based on segment, MSME credit is dominated

by medium enterprises (47.11%), while MSE credit is led by small loans (43.23%). By loan type, nearly all

MSME credit is allocated in the form of working capital credit, while MSE credit favours consumption loans.

By sector, most MSME credit is extended to the trade sector as well as the manufacturing industry, whereas

MSE credit (consumption and productive) seems to favour the trade sector and industry.

Based on bank groups, foreign exchange banks, state-owned banks and regional development banks all

extend MSME and MSE loans. Nevertheless, in December 2011 the respective market share of these three

types of bank underwent a change, where the share of foreign exchange banks and regional development

banks declined respectively from 38.09% and 13.01% to 36.87% and 6.53% and the share of state-owned

banks swelled from 34.87% to 46.40%. This serves as an indication that state-owned banks are favouring

productive MSME loans. Another type of bank that also experienced a slight increase in share of MSME

credit was rural banks, expanding from 3.40% to 4.53%.

Referring to the quality of credit, non-performing MSME loans in December 2011 were noted at 3.63%,

while the NPL ratio for MSE credit was even lower at 2.39%. This disparity was attributable to the exclusion

of consumption credit from MSME data. The highest non-performing MSME loan ratio was ascribed to small

businesses (4.89%). When compared to the position in December 2010 at 4.18% and 2.73% respectively, the

NPL ratios for MSME and MSE credit have improved.

Box 1.1 MSME Credit and Small Loans (KUR)

Bank Structure and Performance in 2011

29

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

Small Loans (KUR)

The realisation of small loans allocated by 19 banks in 2011 exceeded the predetermined target of

Rp20 trillion by 145.02%, reaching Rp29 trillion in December 2011. Therefore, overall the total realisation

of small loans since the program was launched in 2007 is Rp63.42 trillion.

Figure 1.21 Realisation of Small Loans

2007

30,00

Trillion Rp

Realisation

Target

18,00 18,00 18,00 18,00

29,00

20,0017,23

20,00

10,00

25,00

15,00

5,00

0,00

20082009

20102011

11,48

4,730,98

The number of borrowers at the end of December 2011 totalled 5,722,470; up 1,909,912 on the

previous year. The average size of micro loans was Rp5.63 million per borrower, while the average retail

loan was Rp83.09 million. The trade sector dominated the allocation of small loans up to 2011 with 60.51%

of the total, while credit to priority sectors like agriculture, fisheries and the manufacturing industry only

accounted for 19.51%. Consequently, the Small Loans Policy Committee set a target of 25% loan allocation

to priority sectors.

Bank Structure and Performance in 2011

Banking Supervision Report 201130

Bank Structure and Performance in 2011

Foreword Table of Contents Banking Policy and Regulationin 2011

Prospects and BankingPolicy Direction

Bank Supervision ImplementationExecutive Summary

The majority of small loans are concentrated on the island of Java, accounting for 51.81% of the total,

followed by Sumatera (22.04%), Sulawesi (9.88%), Kalimantan (9.18%), Bali NTT and NTB (4.44%) and Papua

Maluku (2.65%).

In terms of credit quality, the ratio of non-performing small loans in 2011 was 2.10%, which is lower

than that reported in 2010 at 2.31%. NPL data is sourced from small loan realisation reports submitted by