banking sector reforms lesson from pakistan

TRANSCRIPT

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 1/15

B A N K I N G S E C T O R R E F O R M S L E S SO N S F R O M P A K I S T A N

I S H R A T H U S A I N

This paper is a imed at drawing lessons from the recent experience of Pakis tan i

implementation of Financial Sector Reforms. Indonesia has also made many impressive

during the past several years in strengthening its financial sector. I believe learning is a tw

process and learning from each other's experiences is a very useful way of assimilating and ad

good practices and knowledge. Pakistan can learn a lot from Indonesia 's experiences and

forward to listening to your interventions this morning.

Befo re I get into the contents of the reforms I would like to begin b y add ressing

the following three questions:

What are the benefits of a robust financial sector for the real economy?

W hy did w e need reforms in the banking sector in the first place?

W hat is the exact role of the Central Bank in the reform p rocess?

a) Financial sector and real economy

Financial Sector Development and Economic Development are inter-related. No eco

can grow and improve the living standards of its population in the absence of a well functioni

efficient financial sector. Banks in Pakistan account for 95 percent of the financial sector and

a sound and healthy banking system is directly related to economic growth and developm

Pakistan.

The modern grow th theory identifies two m ain channels through w hich the financial

might affect long-run growth in a country: first , through catalyzing the capital accum

(including both human and physical capital) and second by increasing the rate of technol

progress.

Financial intermediaries perform five basic functions that affect the real economy.

(i) mobilizing savings from domestic households and corporates

(ii) pooling and managing risk (iii) acquiring and dissemina ting information about investmen t opportunities

(iv) monitoring borrow ers and exerting corporate control and

(v) fac ili ta ting the exchange o f goods and serv ices .

Invited Lecture delivered at the Bank Indonesia Exe cutive Leadership program at Jakanta on July 4,2006.

1

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 2/15

These functions of an efficiently working financial sector allow the above two chan

work for promoting growth by:

a) mobil iz ing savings for investment

b) facilitating and encouraging capital inflows and

c) allocating the capital efficiently among competing uses

Empirical studies have demonstrated preponderance of evidence suggesting a p

relationship between financial development and econom ic growth.

b) W hy were reforms needed?

What was wrong with the Pakistani banking system that such massive reforms had

undertaken?

Banks in P akistan have been catering basically to the needs of the G overnment, public

organizations, serving a few large corporations and engaging in trade financing. There was no

to small and medium enterprises, to the housing sector or to the agricultural sector, which crea

of the growth and employment in Pakistan. Most important, the financial system suffer

polit ical interference in lending decisions and also in the appointment of the B oards an

Executives. The middle class which is the backbone of any economy was not given due atte

the banking sector. There were several legitimate reasons for such an errant behavior.

First, the government's fiscal deficit was so high that most of the deposits the banks u

get were loaned to the government and government corporations. This was safe lendin

fetched goo d returns and the ba nks mad e good pro fit out of it. Naturally, there was little incen

them to do anything else except lend to the Government which was both r isk free and

remunerative.

Secondly, the government ow ned m ost of the banks. In the government banks the

worked like typical government employees, coming to office at 9:00 a.m., checking files; h

nothing important to do and leaving at 5.00 p.m. w ithout doing m uch work. These banks su

from a high bureaucratic approach, overstaffing, unprofitable branches and poor customer se

Adm inistrative costs were high reducing p rofits of depositors.

2

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 3/15

Thirdly, recovery rate w as so low that almost 25% of the loans w ere stuck up. A

number of loans to the private sector borrowers were not given on the merit of the proposal b

political considerations. These influential borrowers hardly repaid their loans.

Fourth, banking ind ustry faced a high tax rate of 58 percent while the rest of the corp

sector paid only 35 percent. This high punitive rate along with the burden of stuck loan

inefficiency of the staff w as passed on to the customers in form of high lending rates an

deposit rates . The banking industry was not a tt rac tive for new entrants who could

competition and improve efficiency.

Because of these factors, i .e . high administrative costs, burden of stuCk-up loans

excessive tax rates, the average interest rate for lending was about 21% per annum. The m

class borrowers could not afford to get credit on such high interest rates and pay it back.

Banking sector reforms were thus needed badly to address these and other constrain

that the banks could play their due role in the economic development of the country. Alth

there is no room for complacency and a lot still needs to be done, even the w orst critics co

that if there is one sector which has undergo ne basic transformation that is the banking s ecto

IMF and the W orld Bank w ho are not always very generous or effusive in their praise had t

say about the Banking sector in Pakistan after completing a comprehensive and thorough rev

early2004.

Quote: "far reaching reforms have resulted in a more efficient and competitivefinancial system. In particular, the pre-dominantlystate-owned banking system has

been transformed into one that is predominantly under the control of the privatesector. The legislative framework and the State Bank of Pakistan 's supervisorycapacity have been improved substantially. As a result, the financial sector issounder and exhibits an increased resilience to shocks". Unquote.

c) Role of the State B ank of Pakistan.

What was the role of the State Bank of Pakistan (SBP) in these reforms and how did

about performing th is ro le? The SBP is both the Central Bank as wel l as the f inancial

supervisory authority. As a matter of fact, it has four major functions to perform under the law

• Ensuring Soundness o f the Financial Sector.

• M aintaining Price Stability w ith Growth.

• Prudent Managem ent of the Exchange Ra te.

• Strengthening of the Paym ent System.

3

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 4/15

It was felt and agreed between the Government and the State Bank of Pakistan that m

deep rooted reforms had to be undertaken as cosm etic changes have not achieved anything ta

As a regulator and supervisor as well as adviser to the G overnment, the SB P carried out diag

studies, prioritized the constraints facing the banking sector, designed the reform strategy an d

plan, sought the assistance of the G overnment of Pakistan in m aking legal and policy chang

international financial institutions for technical and financial resources, monitored the progre

ensured implementation of policy, regulatory and institutional changes required to move the p

forward.

The task of the SBP was h ighly faci l i ta ted by a cr i t ical pol icy decis ion taken b

Musharraf Government i.e. they will not keep the banks under Government ownership and c

but privatize them. Politically tough problems such as reducing the labour force and closing

redundant and unprofitable branches were dealt with boldly. The Government injected Rs

billion($ 600 million) to offset the losses incurred by these nationalized commercial bank

recapitalize them. Professional bankers w ere appointed as Chief Executives and person

private sector enjoying reputation of competence and integrity were taken on the B oard of D i

of the state-owned banks. These new comer/ outsiders were committed to the restructuring

banks prior to their privatization and indeed carried o ut serious preparatory w ork that proved

extremely useful subsequently in the successful sale of the banks.

R E F O R M S IM P L E M E N T E D

What were the major reforms that had been implemented during the last seven yea

would not go into the details of each one of them , but summ arize some of the salient features:

(i ) Privatization of NC Bs:

All the Nationalized Commercial Banks (NCBs) under the public sector, except

have been p rivatized. As a consequence the private sector owns, manages a nd con

about 80 percent of the banking assets in the country - a reversal of the situation

early 1990s when NCBs held 80 percent of total assets. Even in the case of Nat

Bank of Pakistan 23.5 percent shares have been floated through Stock M arket m

aimed a t small retail investors.

(ii) Corporate Governance:

4

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 5/15

Strong corporate governance promotes transparency, accountability and protect

depositors' interests. The SB P has taken several measures in the last four years to p

place and enforce good governance practices to improve internal controls, ensure st

oversight and bring about a change in the organizational culture.

(iii) Capital Strengthening:

Capital requirements of the banking sector have to be adequate to ensure a strong

and w ithstand unanticipated shocks. The minimum paid-up capital requirements o

banks have been gradually raised from$ 1 0 million to reach$ 100 million by 2009.

This has already resulted in mergers and consolidation of many financial institu

and w eeding out of several weaker banks from the financial system.

(iv) Improving Asset Q uality:

The stock of gross non-performing loans (NPLs) that amounted to 2S percent of

advances of the banking system and D Fls has been reduced to 9 percent by M

2006. M ore than two-thirds of these loans are fully p rovided for and net NPLs t

advances ratio has come down to as low as 2 percent for the commercial banks

positive development is that the quality of new loans disbursed since 199

improved and recovery rate is 97 percent.

(v) Liberalization of Foreign Exchange Regime:

Pakistan has further liberalized its foreign exch ange regime and allowed setting

foreign exchange companies in the private sector to meet the demands of Paki

citizens for foreign exch ange transactions. Pakistani Corpo rate sector companies

also been allowed to acquire equity abroad. Foreign registered investors can bri

and take back their capital, profits, dividends, remittances, royalties, ete. f

without any restrictions. There are no restrictions on the entry to any sector o

econom y. Banking, insurance, real estate, retailing and all other sectors can be o

upto 100 p ercent by foreigners.

(vi) Consumer Financing:

5

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 6/15

By removing restrictions imposed on nationalized commercial banks for cons

financing, the State Bank of Pakistan has given a big boost to consumer finan

Middle income groups can now afford to purchase cars, TVs, air conditioners, V

ete. on installment basis. This, in turn, has given a large stimulus to the dom

manu facturing of these products.

(vii)Mortgage Financing:

A number of incentives have been provided to encourage m ortgage financing b

banks. The upper ceiling has been raised, tax deduction on interest paymen

mortgage has been allowed, and a new recoverylaw aimed at expediting repossession

of property by the banks has been promulgated. The banks have been allowed to

long term funds through rated and listed debt instruments to match their long

mo rtgage assets w ith their liabilities.

(viii) Legal Reforms:

Legal difficulties and time delays in recovery of defaulted loans have been rem

through a new ordinance Le. The Financial Ins ti tu tions (Recovery of Fina

Ordinance, 200 1. The new recovery laws ensure the right of foreclosure and sa

mortgaged p roperty w ith or w ithout intervention of court and autom atic transfer of

to execution proceeding. A Banking Laws Reforms Commission has reviewed

revised several pieces of legislations and is drafting new laws such as bankruptcy la

(ix) Prudential Regulations:

The prudent ia l regulations in force were mainly aimed at corporate and bus

financing. The SBP in consultation with the Pakistan Banking Association and

stakeholders has developed a new set of regulations w hich cater to the specific sep

needs of corporate, consumer and SM E financing. The new prudential regulations

enabled the banks to expand their scope of lending and customer outreach.

(x) Micro Financing:

SBP has brought m icrofinance urider the purview of i ts regulatory and superv

ambit. How ever, the licensing and regulatory requirements for Micro Credit and R

financial ins ti tu t ions have been relaxed and have been made s imple to faci

6

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 7/15

widespread access to small borrowers part icularly in the rural areas. Unl ike

commercial banks, the Microfinance Ins ti tu tions (MFls) can be set up at d is

provincial and national levels with varying capi ta l requirements . There is

stringency and more facilitative thrust em bedded in the prudential regulationsdesigned

for this type of institutions. Six microfinance institutions are already operating an

outreach has crossed half a million customers. But in this field we have to learn

from the Indonesian experience particularly the BRI and the regulatory set up in the

of Indonesia.

(xi) SME Financing:

The access of small and medium entrepreneurs to credit has been a major constra

expansion of their business and up gradation of their technology. A Small and M

Enterprise (SME) Bank has been established to provide leadership in developin

products such as program loans, new credit appraisal and documentation technique

nurturing new skills in SM E lending w hich can then be replicated and transferred to

banks in the country. Program lending is the most appropriate method to assist the

financing needs. The new prudential regulations for SMEs do not require collater

asset conversion cycle and cash flow generation as the basis for loan approval. The

Bank is also helping the banks in developing their credit appraisal capacity for

lending. Indonesian exp erience in this field will also be particularly helpfulto us.

(xii)Taxation:

The G overnment has already reduced the corporate tax rate on b anks from 58 perc

35 percent during the last six years and brought at par with the general corporate ta

This has m ade banking a highly profitable business and the banks have earned abo$ 1

billion of profits in 2005 - a big jump from the hu ge losses incurred until a few year

(xiii)Agriculture Credit:

A complete revamping of A griculture C redit Scheme has been done recently w i

help of commercial banks. The scope of the Scheme which was limited to prod

loans for inputs has been broadened tothe who le value chain of agriculture sector. The

broadening of the scope as well the removal of other restrictions have enable

7

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 8/15

commercial banks to substantially increase their lending for agriculture by a multip

five times compared to FY 1999-00 thus mainstreaming agriculture lending as pa

their corporate business. Unlike the previous years when they were prepared to

penalt ies for under performance under mandatory credit scheme the banks

achieved consistently rising higher targets every year. S mall private com mercial b

have also accelerated their agriculture lending as they face large unmet dema

remunerative margins.

(xiv) Islamic Banking:

Indonesia and Pakistan have begun their journey in Islamic banking only rece

Pakistan has a llowed Islamic banking sys tem to opera te in para ll el wi th

conven tional banking p rov id ing a cho ice to the consumers . A la rge numbe

Pakistanis have remained withdrawn from commercial banking because of their st

belief against riba-based banking. These individuals and firms - m ainly middle and

class - w ill have the opportunity to invest in trade and businesses by availing of

from Islamic banks and thus expand economic activity and employment. Several

f ledged Islamic banks have a lready opened the doors for business and m

conventional banks have branches exclusively dedicated to Islamic banking pro

and services.

(xv) E-Banking:

There is a big surge among the banks to upgrade their technology platform, on

banking services and move towards E-banking. During the last four years has b

large expansion in the A TMs and at present more than 1000 A TMs are wor

throughout the country. Progress in creating automated or on-line branches of bank

been quite significant so far and it is expected that by 2007 alm ost all the bank b ran

will be on-line or automated.

(xvi)Human Resources:

The banks have recently embarked on merit-based recruitment to build up their h

resource base - an area w hich has been neglected so far. The p rivate banks have t

lead in this respect by holding competitive examinations, interviews and selecti

8

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 9/15

most qualified candidates. The era of appointment on the basis of connection

recommendations from the politicians has almost come to an end as the private o

want to attract and retain the best available talent which can m aximize their profits

new generation of bankers will usher in a culture of professionalism and rigour

banking industry and produce bankers of stature who will provide leadership

future.

(xvii) Credit Rating:

To facilitate the depositors to make informed judgments about placing their saving

the banks, it has been made mandatory for all banks to get themselves evaluated by

rating agencies. These ratings are then disclosed to the general public by the SB

also d is seminated to the Chambers o f Commerce and Trade bod ies. Such

disclosure will allow the depositors to choose between various banks.

(xviii) Supervision and Regulatory Cap acity:

The bank ing supervi sion and regulato ry capac ity o f the Central Bank has

strengthened. Merit - based recruitment, com petency - enhancing training, perform

linked promotion, technology - driven process, induction of skilled huma n resourc

greater emphasis on values such as integrity, trust , team work have brought ab

structural transformation in the character of the institution. The responsibili

supervision of non-bank f inance companies has been separated and t ransfer

Securities Exchange Commission. The SSP itself has beendivided into two parts - o ne

looking after central banking and the other after retail banking for the go vernmen t.

(xix) Payment Systems:

Finally, the country's paym ent system infrastructure is being strengthened to proconvenience in transfer of payments to the customers. The Real-Time Gross Settlem

(RTGS) system will process large value and critical transactions on real time w

electronic clearing sy stems w ill be established in all cities.

These reforms w ill go a long w ay in further strengthening the Banking sector but a vig

supervisory regime by the State Bank w ill help steer the future direction.

9

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 10/15

O U T C O M E S :

W hat have been the results of the above reforms?

Pakistan's economy w as stuck in a low equ ilibrium trap in the decade of t 990s.

Per-capita growth rates were anemic and stagnant. Incidence of poverty was on the rise, s

unemployment rate. Fiscal imbalances, high debt ratios, large external imbalances, dep

foreign reserves and a depreciating currency had made macroeconomic management extr

difficult.

The structural reforms introduced since 2000 in a wide variety of sectors impr

economic governance and prudent economic m anagement have brought about a turnaround

economy. Last year the economy grew at 8.4 percent - the second to C hina and all macroeco

indicators are showing positive movement and stable levels. Incidence of poverty has dec

from 34 percent in FYO 1 to 24 percent in FYOS. Unemployment rate has recorded a

Financial soundn ess indicators are all healthy and robust.

The banking business is no longer confined to meeting government's budgetary deficit

the losses of public enterprises or catering to the requirements of bigcorporate houses and big

names in business. The customer b ase for loans has expanded from 1 million to 4 million dur

last s ix years. Agricult .ure , the largest sector of economy, which the commercial ban

neglected, has now begun to receive large allocations. The commercial banks are giving

agriculture loans than even in the history of Pakistan If this trend persists, the rural househol

be able to intensify the use of mo dern inputs and raise their productivity and incom e.

Credit cards, debit cards, personal loans and consumer durable loans are catching up

Refrigerators, air conditioners, VCRs, Televisions are now available on credit. The consum

forced to save w hen a specific am ount is cut from their salary every m onth to pay the insta

M ortgage financing is helping the middle class families to own apartments and residential h

For the first t ime in the history of Pakistan, the middle class is beginning to benefit fro banking system.

Microfinance institutions are expanding their branches and providing credit withou

collateral or security to poor households. Many people have availed this opportunity, some bo

cow, some bought a milk buffalo or opened a small shop and female borrowers bought s

machines. T hey have started income-generating activit ies and recovery is no problem fro

10

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 11/15

micro-finance banks. Approximately, 500,000 poor household have benefited from these lo

the last few years.

The banking system which had recorded negative returns on assets (RoA) and neg

returns on equity (RoE) six years ago is now showing impressive R oAs and RoEs com par

best international banks. Capital base is strong, quality of assets has improved, m ana

practices are sound, corporate governance standards are being followed and risk managem

much better. Rapid credit growth in consumer segment and repricing of loans at higher interes

are the new challenges that the banking industry is currently facing. But I am sanguine that th

be also to meet these challenges prudently and wisely.

L E S S O N S L E A R N T

W hat are the lessons we have learnt in implementing the financial sector reforms in the last

years?

1 . Ban king r efo rms c an no t b e su cc es sfu lly imp leme nte d an d sus ta in ed in

absence of a favourable and stable macroeconomic environment. Pakistan's t

record in macroeconomic management and governance during the 1990s was dis

The M usharraf government, which came to power in October 1999, embarked up

serious program of macroeconomic stabilization, structural reforms, good governa

and the establishment of credibility with International Financial Institutions. D es

several major exogenous shocks, including September 11, the mobilization of tro

on the Indian bo rder, severe drought incidents of terror attacks and oil price shock

country has been able to m ake a dramatic turnaround in its economic indicators.

include fiscal retrenchm ent and a primary su rplus on budget, inflation contained to

level for the first four years the current accoun t turning surplus, debt indicators mo

in the direction of sustainability and foreign reserves rising about twelve times

addition, this period witnessed the lowering of the interest rate s tructure ,

appreciation of the exchange rate and a record grow th in workers' remittances. All

amply demonstrates the seriousness of efforts made during the last six years. G

grow th has averaged more than 6 percent since 2002.

2 . F in an ci al s ec to r re fo rms ca n o nly b e impleme nted if t he re i s po litic al w

ownership and commitment of government. Once this becomes obvious a b

11

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 12/15

consensus has to be built up on the direction, contents, phasing and sequencing

intensive consultation of all the stakeholders. The banking industry, the regula

authorities and the Ministry with Finance have to work together in building su

consensus, otherwise the reforms can prove to be short lived without sustainabilit

the long run. But to achieve such a co nsensus there has to be a cham pion that can p

the reforms throug h the legal, parliamentary and institutional measures, fine tune t

and correct the course during the implementation process, monitor and evaluate

impact of the reforms and ensure that the unintended consequences are prop

tackled. There must be proactive communication with the public at large and m

and the champion has to respond to their concerns. In absence of sllch a champ

inertia and passivity would overw helm the reform p rocess and derail it.

3. A p riv ate s ec to r o wn ed a nd m ana ged fin ancial s ystem can p ro vid e la

benefits to the economy only if some pre-requisites are in place. These pre-requi

are healthy competitive, environment, efficiently functioning markets, sound finan

infrastructure but m ost imp ortant a strong and effective regulator. In cases where

Central Bank or the Regulatory Authority is weak and not upto the mark in sk

competencies and systems the collusive and anti-competitive behavior of the pri

sector can create serious systemic problems for the financial sector and for

econom y. We have w itnessed in Pakistan that the weak capacity of regulator has g

rise to cartelization in good s market for sugar, cem ent ete.

4 . T he serv ic e s ta nd ard s, p ro du ct o ffe rin gs , sys tem impro vemen t, te ch no lo

transfer and skill upgradation in the domestic banking systems can be facilitate

exposing the domestic banks to competition from foreign banks. As the state ow

commercial banks had become highly politicized and lost their professional rigo

was by drawing upon the human resources and Pakistani managers workin

international banks that we were able to restructure and strengthen our ban

systems. These managers introduced culture, systems and procedures, and techno

platform that has m ade it po ssible for the domestic private banks to expand, bec

efficient and highly profitable and revive professionalism. The apprehension tha

foreign banks will displace the domestic banks in the market place and capture ma

share is in fact highly exaggerated. As a m atter of fact ten out of twenty foreign ow

12

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 13/15

banks have packed up and wound up their operations in Pakistan because they c

no longer compete with the domestic banks that have a large network and have n

become more efficient. The share of foreign banks in the banking assets and depo

has, as a matter of fact, shrunk compared to the 1990s. Foreign banks were earn

huge rents because of the inefficiencies of the domestic banks. But as the dome

banks have become strong and a com petitive environment exists that favours scal

operations, network and a variety of product and service offerings, the foreign b

have lost their market share.

5. Sta te -owned banks can be successfu lly privat ized only i f compet

professionals and men and women of highest integrity from outside the banks

brought in as Chief Executives and members of the Boards of Directors. Most insi

have vested14

13

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 14/15

6. in terests to perpetuate the s ta tus-quo and therefore offer a lo t of

resistance during the process vitiating, negating or retarding the progress.

These insiders may sincerely believe in the efficacy of public sector banks

and may therefore have serious conflict of interest with the government

decision of privatization. The outsiders should be given a performance-

based contract for limited time period to complete the task assigned to

them.

14

8/2/2019 Banking Sector Reforms Lesson From Pakistan

http://slidepdf.com/reader/full/banking-sector-reforms-lesson-from-pakistan 15/15

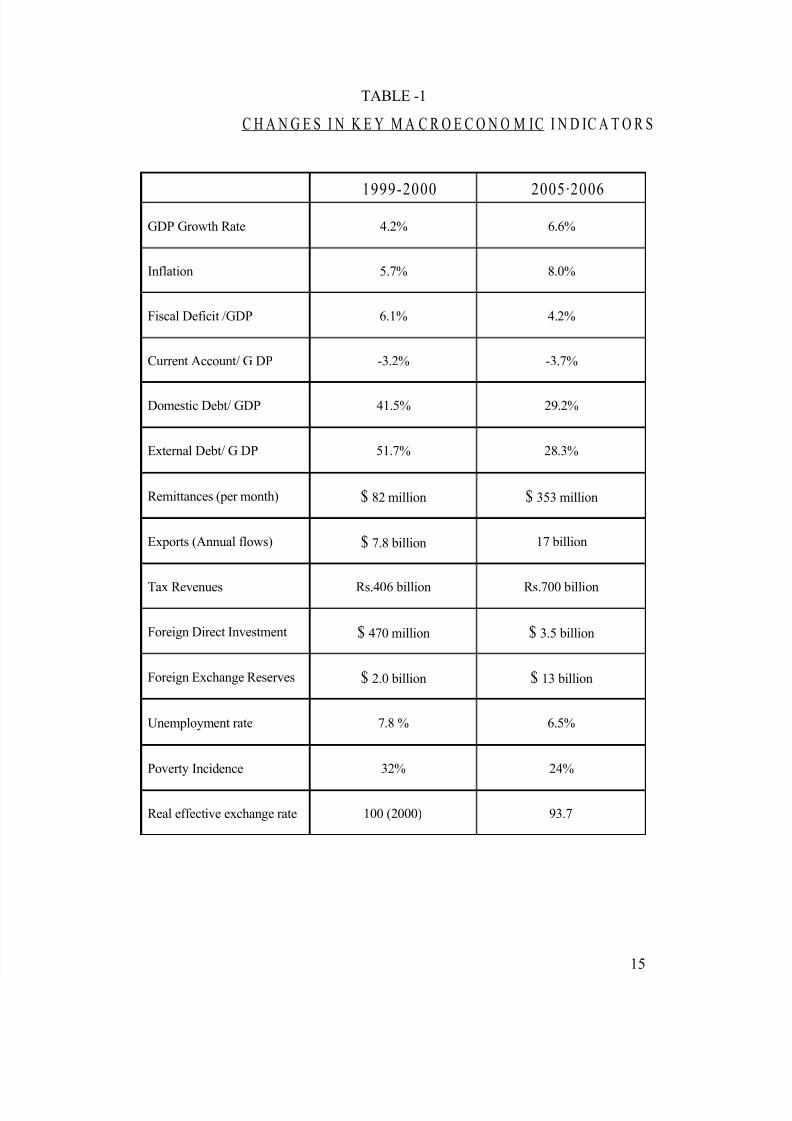

TABLE -1

C H A N G E S I N K E Y M A C R O E C O N O M IC I N D IC A T O R S

1999-2000 2005·2006

GDP Growth Rate 4.2% 6.6%

Inflation 5.7% 8.0%

Fiscal Deficit /GDP 6.1% 4.2%

Current Account/ G DP -3.2% -3.7%

Domestic Debt/ GDP 41.5% 29.2%

External Debt/ G DP 51.7% 28.3%

Remittances (per month) $ 82 million $ 353 million

Exports (Annual flows) $ 7.8 billion 17 billion

Tax Revenues Rs.406 billion Rs.700 billion

Foreign Direct Investment $ 470 million $ 3.5 billion

Foreign Exchange Reserves $ 2.0 billion $ 13 billion

Unemployment rate 7.8 % 6.5%

Poverty Incidence 32% 24%

Real effective exchange rate 100 (2000) 93.7

15