banking sector report for quarter ended … · banking sector report for quarter ended 30 ......

TRANSCRIPT

RESERVE BANK OF ZIMBABWE

BANKING SECTOR

REPORT FOR QUARTER ENDED 30 JUNE 2014

2

1. EXECUTIVE SUMMARY

1.1. Notwithstanding the challenging operating environment, the banking

sector remained generally stable.

1.2. The banking sector remains well capitalized with 14 out of the 20

operating institutions compliant with the minimum capital requirements

as at 30 June 2014. The remaining non-compliant banks have embarked

on capital raising initiatives to strengthen their capital positions.

1.3. Despite the decline in the overall net income of the banking sector for

the half year ended 30 June 2014, 13 out of 20 operating institutions

recorded profits.

1.4. Credit risk remains a significant challenge facing the banking sector as

reflected by rising non-performing loans.

1.5. A few banking institutions continued to face liquidity challenges.

Capital Banking Corporation’s licence was cancelled with effect from 4

June 2014, following the bank’s voluntary surrender of its licence and

request for cancellation in terms of section 14(4) of the Banking Act on

7 February 2014.

1.6. As at30 June 2014, banking sector deposits amounted to $4.96 billion,

whilst loans and advances were $3.81billion, translating into loans to

deposits ratio of 76.82%. Banks’ lending portfolio continue to be

skewed towards consumptive lending.

3

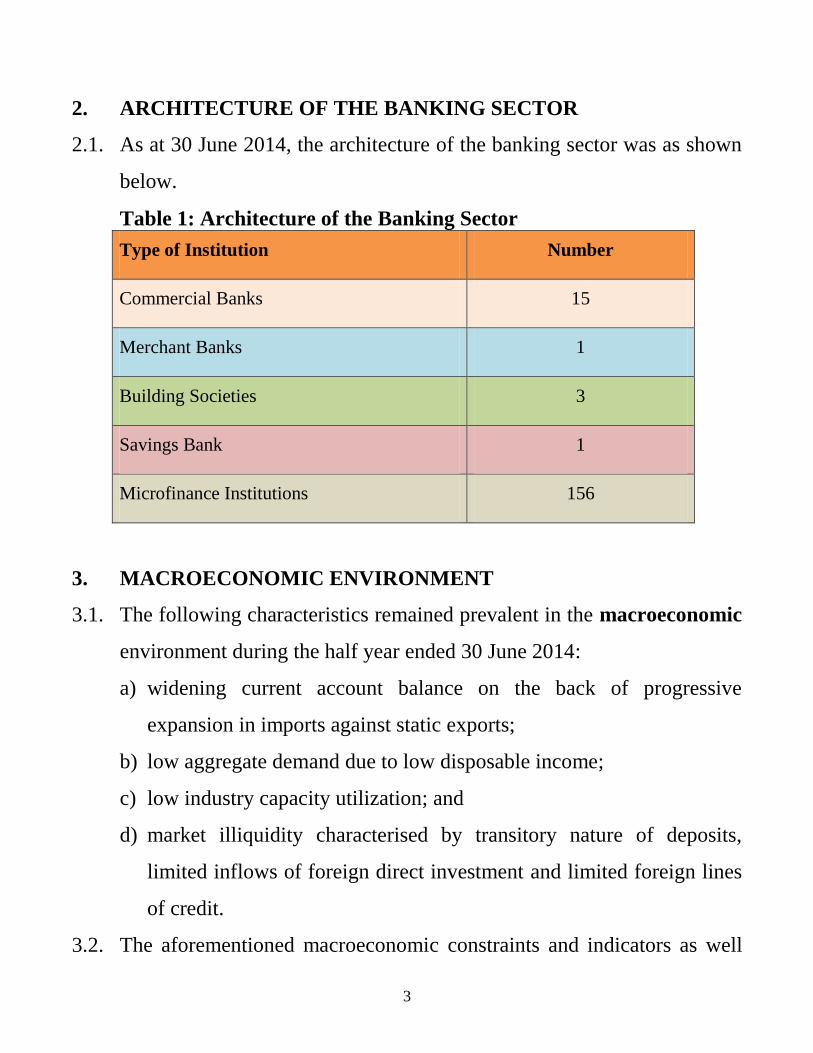

2. ARCHITECTURE OF THE BANKING SECTOR

2.1. As at 30 June 2014, the architecture of the banking sector was as shown

below.

Table 1: Architecture of the Banking Sector

Type of Institution Number

Commercial Banks 15

Merchant Banks 1

Building Societies 3

Savings Bank 1

Microfinance Institutions 156

3. MACROECONOMIC ENVIRONMENT

3.1. The following characteristics remained prevalent in the macroeconomic

environment during the half year ended 30 June 2014:

a) widening current account balance on the back of progressive

expansion in imports against static exports;

b) low aggregate demand due to low disposable income;

c) low industry capacity utilization; and

d) market illiquidity characterised by transitory nature of deposits,

limited inflows of foreign direct investment and limited foreign lines

of credit.

3.2. The aforementioned macroeconomic constraints and indicators as well

4

as institution-specific deficiencies translated into capitalisation, asset

quality, earnings performance and liquidity challenges at a few banks.

4. CONDITION AND PERFORMANCE OF THE SECTOR

4.1. The performance and condition of the banking sector is summarised by

the key banking sector statistics depicted in the table below:

Table 3: Banking Sector Statistics

Key

Indicators Dec -09 Dec-10 Dec -11 Dec - 12 Dec - 13 Mar -14 Jun - 14

Total

Assets

$2.19

billion

$3.69

billion

$4.74

billion

$6.12

billion

$6.74

billion

$6.81

billion

$6.90

billion

Total

Loans

$693

million

$1.56

billion

$2.76

billion

$3.56

billion

$3.08

billion

$3.82

billion

$3.81

billion

Net

Capital

Base

$382

million

$458

million

$512

million

$644

million

$706

million

*$909

million

*$893

million

Total

Deposits

$ 1.36

billion

$ 2.31

billion

$ 3.04

billion

$4.41

billion

$ 4.73

billion

$4.89

billion

$4.96

billion

Net Profit

$9.50

million

$37.95

million

$86

million

$69.23

million

$4.46

million

*$20.47

million

*$26.53

million

ROA 0.60% -2.02% 2.43% 1.64% 0.06% 0.26% 0.49%

ROE 2.47% 0.57% 15.13% 9.17% 0.51% 2.12% 2.72%

CAR 27.26% 27.34% 13.51% 13.07% 14.01% 14.10% 18.56%

Loans to

Deposits 50.99% 86.25% 90.59% 93.27% 102.36% 78.03% 76.82%

ACL/TL 1.80% 10.95% 7.55% 13.46% 15.92% 16.96% 18.49%

Provisions

to ACL 112.81% 887.71% 57.53% 207.45% 70.88% 46.73% 39.29%

NIM 3.29% 5.75% 8.21% 14.81% 15.26% -0.15% 2.03%

Liquidity

Ratio 97.44% 70.88% 56.80% 55.70% 40.57% 38.10% 38.20%

Cost to

Income

Ratio 94.38% 148.95% 185.11% 99.95% 173.43% 87.15% 164.69%

*Excluding one bank which is under curatorship

5

4.2. The Reserve Bank continues to closely monitor a few banking

institutions with a combined market share of 7.36% in terms of assets,

which were facing liquidity and solvency challenges.

4.3. A summary of the condition and performance of the sector based on the

CAMELS framework is provided hereunder.

Capital Adequacy…

4.4. The banking sector remained adequately capitalised during the period

ended 30 June 2014, with the average capital adequacy ratio above the

required minimum regulatory capital adequacy ratio of 12%.

4.5. The trend in the banking industry’s average capital adequacy ratios

(CARs) from June 2013 to June 2014 is indicated in figure 2 below.

0

2

4

6

8

10

12

14

16

18

20

Jun 13 Sep 13 Dec 13 Mar 14 Jun 14

Pe

rce

nta

ge (

%)

Figure 2: Capital Adequacy Ratio

Capital Adequacy Ratio (%)

6

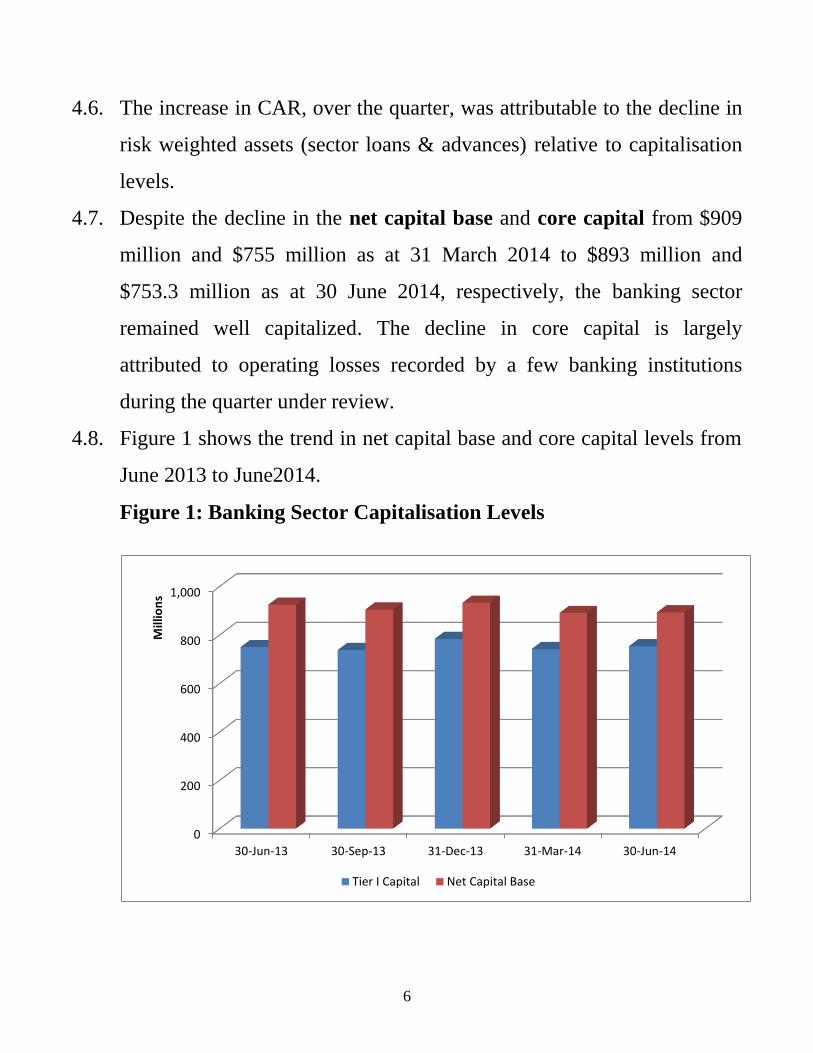

4.6. The increase in CAR, over the quarter, was attributable to the decline in

risk weighted assets (sector loans & advances) relative to capitalisation

levels.

4.7. Despite the decline in the net capital base and core capital from $909

million and $755 million as at 31 March 2014 to $893 million and

$753.3 million as at 30 June 2014, respectively, the banking sector

remained well capitalized. The decline in core capital is largely

attributed to operating losses recorded by a few banking institutions

during the quarter under review.

4.8. Figure 1 shows the trend in net capital base and core capital levels from

June 2013 to June2014.

Figure 1: Banking Sector Capitalisation Levels

0

200

400

600

800

1,000

30-Jun-13 30-Sep-13 31-Dec-13 31-Mar-14 30-Jun-14

Mill

ion

s

Tier I Capital Net Capital Base

7

4.9. As at 30 June 2014, a total of 14 out of 20 operating banking institutions

were in compliance with the prescribed minimum capital requirements.

Non-compliant banks are taking various measures to regularize their

capital positions which are at different stages of implementation.

4.10. Two banking institutions have already surpassed the minimum capital

requirement targets, effective 2020.

Asset Quality...

4.11. Total loans and advances decreased by 0.26% from $3.82 billion as at 31

March 2014 to $3.81 billion as at 30 June 2014. Generally, there has

been a growth in the level of total loans and advances since 2009 as

depicted below:

705.76

2567.61

3584.57

4220.45 4371.174728.07

4894.74 4,962.07

263.49

1669.3

2839.83

3321.13529.88

3701.11 3819.56 3,810.00

0

400

800

1200

1600

2000

2400

2800

3200

3600

4000

4400

4800

5200

5600

30-

Jun

-09

31-

Dec

-09

31-

Dec

-10

31-

Dec

-11

31-

Mar

-12

30-

Jun

-12

30-

Sep

-12

31-

Dec

-12

29-

Mar

-13

31/

09/2

013

31-

Dec

-13

31-

Mar

-14

30-

Jun

-14

Total Deposits ($M) Total Loans and Advances($M)

8

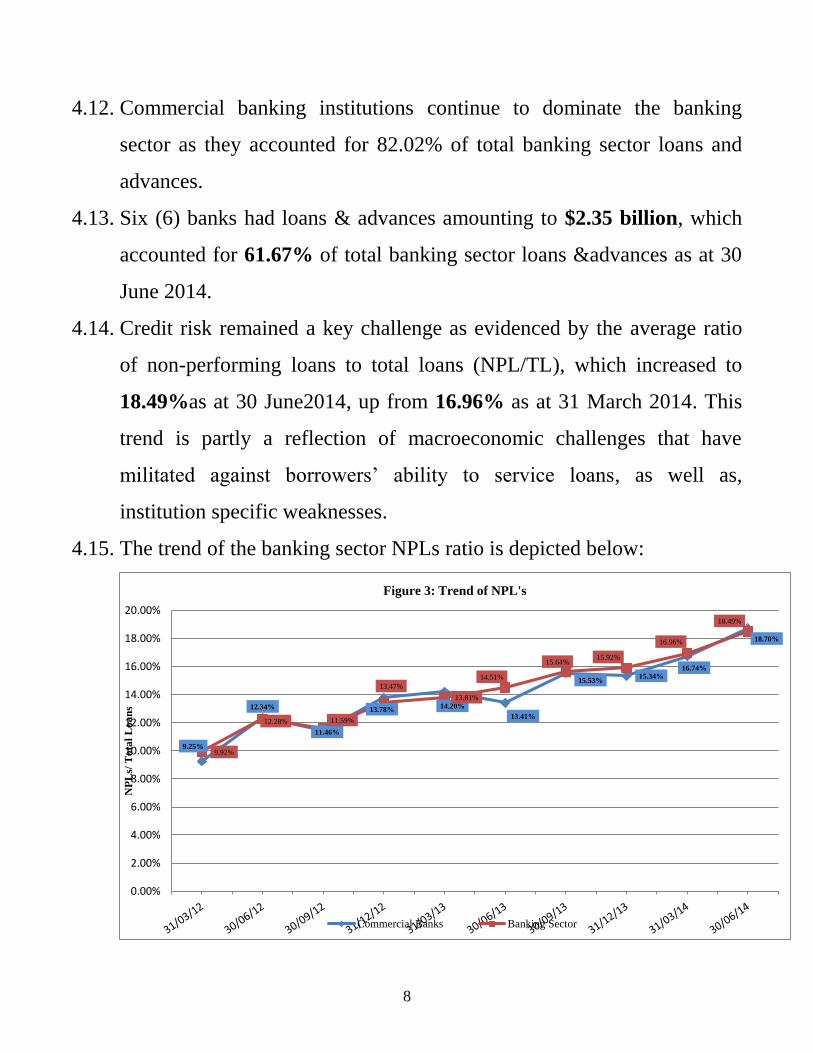

4.12. Commercial banking institutions continue to dominate the banking

sector as they accounted for 82.02% of total banking sector loans and

advances.

4.13. Six (6) banks had loans & advances amounting to $2.35 billion, which

accounted for 61.67% of total banking sector loans &advances as at 30

June 2014.

4.14. Credit risk remained a key challenge as evidenced by the average ratio

of non-performing loans to total loans (NPL/TL), which increased to

18.49%as at 30 June2014, up from 16.96% as at 31 March 2014. This

trend is partly a reflection of macroeconomic challenges that have

militated against borrowers’ ability to service loans, as well as,

institution specific weaknesses.

4.15. The trend of the banking sector NPLs ratio is depicted below:

9.25%

12.34%

11.46%

13.78%14.20%

13.41%

15.53%15.34%

16.74%

18.70%

9.92%

12.28% 11.59%

13.47%

13.81%

14.51%

15.64%15.92%

16.96%

18.49%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

NP

Ls/

To

tal

Lo

an

s

Figure 3: Trend of NPL's

Commercial Banks Banking Sector

9

4.16. The rise in asset impairment has resulted in a dip in profitability. The

surge in delinquencies and loan losses has dampened banks’ risk

appetite. Resultantly, banks have increasingly adopted a risk averse

approach to lending.

4.17. Banking sector lending was largely for consumptive purposes at the

expense of the key productive sectors, with the individuals or household

sector constituting 24.7% of total credit. Construction and mining

sectors constituted 3.80% and 4.2% of total banking sector credit,

respectively.

4.18. The figure below shows the sectoral distribution of credit as at 30 June

2014:

Figure 4: Sectoral Distribution of Credit

31 March 2014 30 June 2014

Mining9% Construction

3.8%

Financial Firms

2%

Transport2%

Individuals24.4%

Services17.7%

Agriculture4.5%

Manufacturing

14.3%

Distribution13%

Communication

7.4%

Mining

4.2%

Construction

3.8% Financial

Firms

2.0%Transport

2.8%

Individuals

24.7%

Services

17.6%

Agriculture

15.6%

Manufacturin

g

13.7%

Distribution

8.5%

Communicati

on

7.1%

10

Earnings...

4.19. The banking sector remained profitable with an aggregate net profit of

$26.53 million (excluding bank under curatorship) for the half year

ended 30 June 2014, up from $4.90 million during the corresponding

period ended June 2013.

4.20. A total of 13 banks out of the 20 operating banking institutions

(including a savings bank) recorded profits for the half year ended 30

June 2014. The losses recorded by the few banking institutions in the

current period are attributed to high levels of non- performing loans,

lack of critical mass in terms of revenue to cover high operating

expenses and deliberate strategy by some banks to clean up bad loan

books through provisioning.

4.21. The income mix for the banking sector is indicated below.

Figure 5: Distribution of Total Income for periods 30 June 2013 &

2014

Interest Income

61%

Non-Interest Income

39%

Income Mix for the Quarter ended 30 June 2013

Interest Income

63%

Non-Interest Income

37%

Income Mix for the Quarter ended 30 June 2014

11

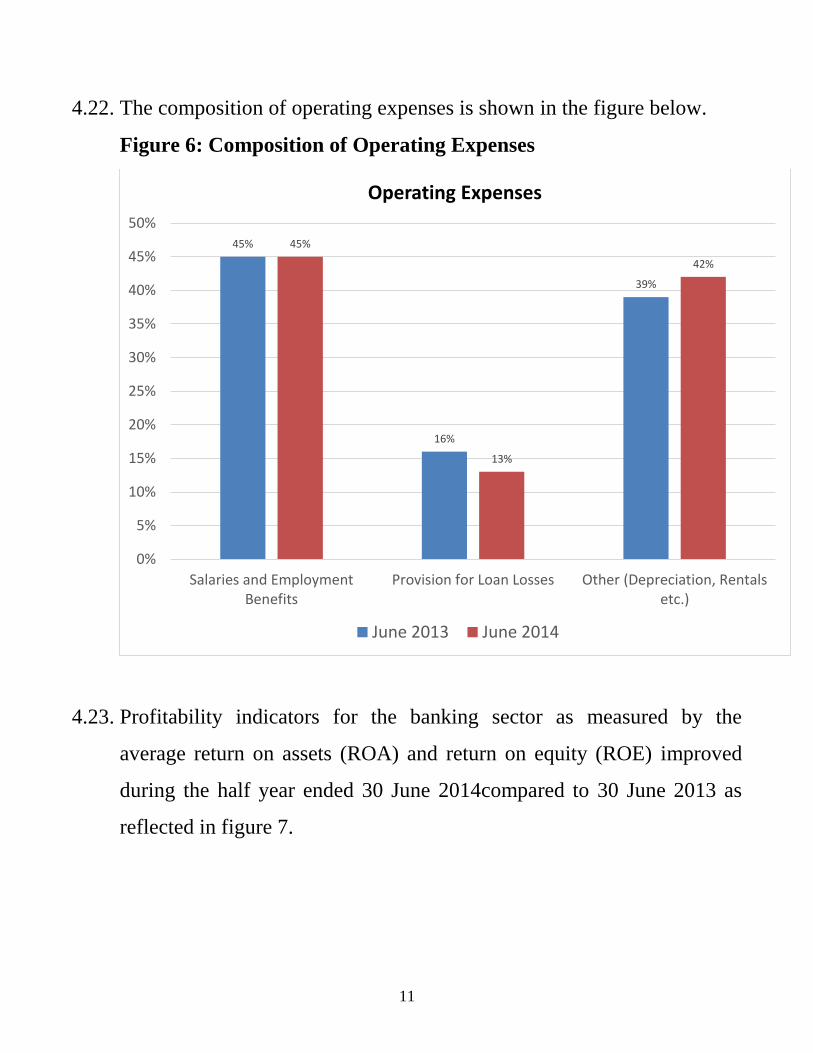

4.22. The composition of operating expenses is shown in the figure below.

Figure 6: Composition of Operating Expenses

4.23. Profitability indicators for the banking sector as measured by the

average return on assets (ROA) and return on equity (ROE) improved

during the half year ended 30 June 2014compared to 30 June 2013 as

reflected in figure 7.

45%

16%

39%

45%

13%

42%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Salaries and EmploymentBenefits

Provision for Loan Losses Other (Depreciation, Rentalsetc.)

Operating Expenses

June 2013 June 2014

12

Figure 7: Profitability Indicators

Liquidity and Funds Management...

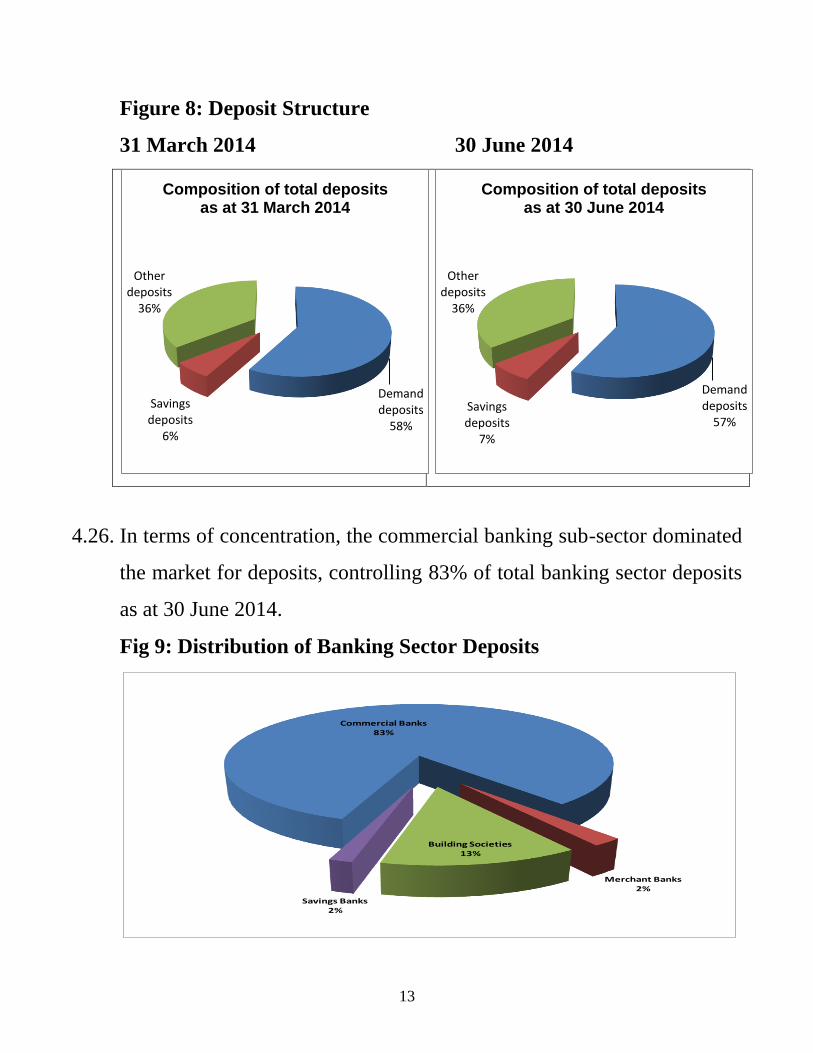

4.24. The trend in the level of deposits is shown below.

4.25. Banking sector deposits continued to be dominated by demand deposits

which accounted for 43.83% of total deposits as at 30 June 2014 as

indicated in figure 8 below:

0.12% 0.13% 0.06%0.26%

0.49%0.59%

-0.24%

0.51%

2.12%

2.72%

-1%

0%

1%

2%

3%

4% Jun 13 Sep 13 Dec 13 Mar 14 Jun 14

ROA ROE

705.76

2567.61

3584.57

4220.45 4371.174728.07 4894.74 4962.08

0400800

120016002000240028003200360040004400480052005600

30-

Jun

-09

31-

Dec

-09

31-

Dec

-10

31-

Dec

-11

31-

Mar

-12

30-

Jun

-12

30-

Sep

-12

31-

Dec

-12

29-

Mar

-13

31/

09/2

013

31-

Dec

-13

31-

Mar

-14

30-

Jun

-14

Total Deposits ($M)

13

Figure 8: Deposit Structure

31 March 2014 30 June 2014

4.26. In terms of concentration, the commercial banking sub-sector dominated

the market for deposits, controlling 83% of total banking sector deposits

as at 30 June 2014.

Fig 9: Distribution of Banking Sector Deposits

Commercial Banks 83%

Merchant Banks 2%

Building Societies 13%

Savings Banks 2%

Demand deposits

58%

Savings deposits

6%

Other deposits

36%

Composition of total deposits as at 31 March 2014

Demand deposits

57%Savings deposits

7%

Other deposits

36%

Composition of total deposits as at 30 June 2014

14

4.27. As at 30 June 2014, six (6) banking institutions had deposits above $300

million each, amounting to $3.35 billion, and representing 67.45% of

total banking sector, indicative of the systemic importance of these

institutions.

4.28. The banking sector average prudential liquidity ratio of 38.20% as at 30

June 2014, was above the regulatory minimum of 30%, and has been

stable since 30 June 2013 as shown below.

Figure 10: Prudential Liquidity Ratio Trend

4.29. While the majority of the banking institutions are compliant with the

38.93% 38.71%

37.64%38.08% 38.20%

25.00%

30.00%

35.00%

40.00%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

PLR Quarterly Trend

Prudential Liquidity Ratio PLR Threshold

15

minimum prudential liquidity ratio, the sector is beset by various

underlying liquidity constraints that mirror the real economy structural

rigidities. Consequently, a few institutions faced liquidity challenges

Sensitivity to Market Risk…

4.30. As at 30 June 2014, the banking sector’s sensitivity to market risk was

moderate. The ratio of Rate Sensitive Assets to Rate Sensitive Liabilities

and Net Open Position to Core Capital were 149.16% and 51.99%,

compared to 159.69% and 43.36%, recorded as at 31 March 2014

respectively.

4.31. The table below shows the average interest rate sensitivity ratios for the

banking sector as at 30 June 2014 and 31 March 2014, respectively.

Table 4: Interest Rate Sensitivity Ratios

Period 3 months 6 months 9 months

Mar-14 127.50% 172.70% 159.69%

June-14 145.18% 147.50% 154.80%

30 June 2014