banyule city council 13 april 2015 ordinary meeting - agenda attachments 4

DESCRIPTION

Banyule City Council Ordinary Meeting 13 April 2015 Agenda Attachments Part 4 of 4TRANSCRIPT

Att

ach

men

t 1

5.1

Item: 5.1 Attachment 1: Manningham MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 384

MAV State Council Meeting – 15 May 2015

To submit a motion for consideration by State Council on 15 May 2015, please complete this form and email to State Council, no later than Friday,17 April 2015 . Please note, deadlines are strictly observed.

MOTION RATE CAPPING FRAMEWORK FOR LOCAL GOVERNMENT

Submitted by: Manningham City Council

MOTION: That the MAV take into account the following when advocating to the State Government on the development of the rate capping framework by the Essential Services Commission.

That the Sector Panel overseeing development of the Framework:

1. seek and consider submissions from independant experts on the economic and social impact of any proposed rate capping framework, prior to adoption;

2. fully assess the impact of long term cost shifting from both State and Federal governments and provide options to offset the financial impact of future changes to coincide with the introduction of the framework.

3. seek additional time to enable local government to fully participate in the development of the framework and to prepare for implementation.

4. consider embedding sufficient flexibility in the framework to enable it to be implemented in each council in a manner which responds to particular local needs and demands.

RATIONALE: The mandate of Local Government is underpinned by principles of efficiency and transparency. The Labor Government has instructed the Essential Services Commission to develop a framework to inform their election commitment to cap annual council rate increases and to advise the Ministers for Finance and Local Government on options and a recommended approach for a rates capping framework for implementation from the 2016-17 financial year. The State Government’s objective is to “contain the cost of living in Victoria while supporting council autonomy and ensuring greater accountability and transparency in local government budgeting and service delivery”. To ensure the optimim model, it is essential that the correct balance between sustainability, service provision and efficiency is reached. The informative process must be robust and comprehensive to achieve recommendations, framework and legislation that supports an approach that allows Councils to responds to the needs of their unique local community.

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 385

MUNICIPAL ASSOCIATION OF VICTORIA STATE COUNCIL MEETING

15 MAY 2015

DRAFT MOTIONS (Updated 26 March 2015)

MOTION 1

COUNCIL LIABILITY- VCAT PLANNING DECISIONS

Submitted by: Maroondah City Council

MOTION: THAT THE MUNICIPAL ASSOCIATION OF VICTORIA STATE COUNCIL CALLS ON THE STATE GOVERNMENT TO ENSURE:-

1. THAT VCAT TAKE RESPONSIBILITY FOR THE DEFENCE OF LITIGATION AGAINST PLANNING DETERMINATIONS MADE BY VCAT; AND

2. THE IMPOST OF THE CURRENT COST TO VICTORIAN LOCAL GOVERNMENT IN DEFENDING SUCH LITIGATION IS LIFTED FROM THE SECTOR.

RATIONALE: The cost of defending litigation against VCAT decisions in issuing planning permits is presently carried by the Local Government sector. This is viewed as an unreasonable impost especially as the determinations frequently overturn the originally planning decisions made by Councils. A more equitable approach would be for VCAT to conduct this defence and so relieving Councils of the burden, or for the sector to be reimbursed for costs. The incongruous situation of Council bearing the cost of such legal defence is exacerbated by the fees/levy that the State Government will collect from the newly introduced Victorian Planning Authority that will take effect from 1 July this year. The levy will be on planning permit application fees for a project in excess of $1 million and it is projected the levy will raise an estimated $17.1 million. The Authority has very little if anything to do with the planning process except collect a mandatory fee with no amount being channelled into the Local Government sector. It is this source of monies – raised by the Victorian Planning Authority – that could be used to offset the costs to Council of defending litigation against VCAT decisions.

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 386

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 387

MOTION 2

MUNICIPAL DEVELOPMENT CONTRIBUTION PLAN

Submitted by: Maroondah City Council

MOTION: THAT THE MUNICIPAL ASSOCIATION OF VICTORIA STATE COUNCIL CALLS ON THE STATE GOVERNMENT TO PROVIDE A CLEAR PROCESS TO ENABLE MUNICIPALITIES TO INTRODUCE A DEVELOPMENT CONTRIBUTION PLAN ON A MUNICIPAL WIDE BASIS.

Rationale:

Currently, Development Contribution Plans (DCP) – a development infrastructure levy and/or a community infrastructure levy – do not apply across a whole municipality but is broken down into a series of charge areas. Maroondah for instance has an existing DCP applicable to the Ringwood Metropolitan Activity Centre but not a municipal wide equivalent. The growing cost of infrastructure is an ever increasing impost upon Council’s budget and an overall DCP would provide additional funding to make up for shortfalls between current income and the cost of infrastructure. It would potentially include capital infrastructure projects such as roads, drainage, footpath, streetscape works as well as community infrastructure projects, such as child care centres, Maternal and Child Health Centres and neighbourhood houses. The infrastructure is required to cope with the growing population of the municipality and the consequential increased demand. The development contributions go directly towards projects which would be used by the development, because they are located in the same area. A municipality would typically been broken down into ‘Charge Areas’ (generally by suburb). Each Charge Area would have a different list of projects, and so the required payment for each area would be different. In addition, there are a range of development categories (eg residential, industrial and commercial). To calculate the cost a party would be required to pay, there would be a need to identify the Charge Area in which a site is located, what type of development is proposed, and either the number of dwellings or the size of the commercial/ industrial floor area being proposed. A Planning Panel recently (November 2014) provided support to Moreland City Council to pursue a municipal wide DCP. This suggests that the concept is a feasible and one that should be pursued.

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 388

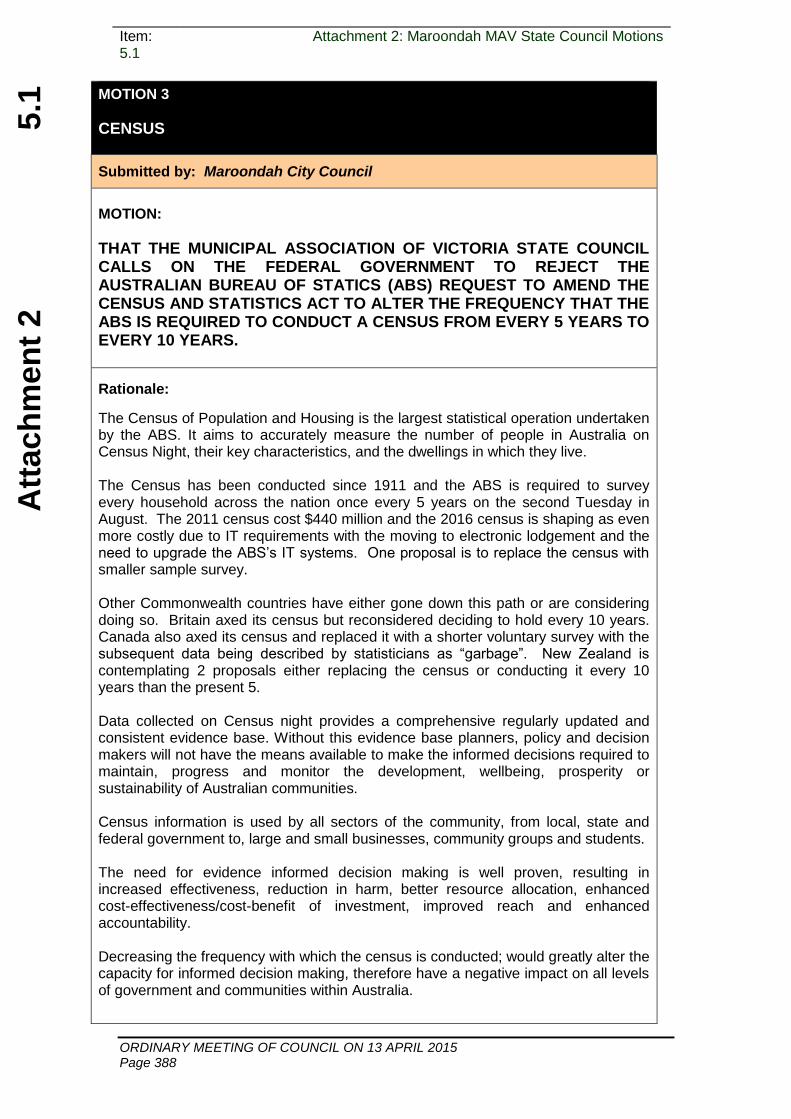

MOTION 3

CENSUS

Submitted by: Maroondah City Council

MOTION:

THAT THE MUNICIPAL ASSOCIATION OF VICTORIA STATE COUNCIL CALLS ON THE FEDERAL GOVERNMENT TO REJECT THE AUSTRALIAN BUREAU OF STATICS (ABS) REQUEST TO AMEND THE CENSUS AND STATISTICS ACT TO ALTER THE FREQUENCY THAT THE ABS IS REQUIRED TO CONDUCT A CENSUS FROM EVERY 5 YEARS TO EVERY 10 YEARS.

Rationale:

The Census of Population and Housing is the largest statistical operation undertaken by the ABS. It aims to accurately measure the number of people in Australia on Census Night, their key characteristics, and the dwellings in which they live. The Census has been conducted since 1911 and the ABS is required to survey every household across the nation once every 5 years on the second Tuesday in August. The 2011 census cost $440 million and the 2016 census is shaping as even more costly due to IT requirements with the moving to electronic lodgement and the need to upgrade the ABS’s IT systems. One proposal is to replace the census with smaller sample survey. Other Commonwealth countries have either gone down this path or are considering doing so. Britain axed its census but reconsidered deciding to hold every 10 years. Canada also axed its census and replaced it with a shorter voluntary survey with the subsequent data being described by statisticians as “garbage”. New Zealand is contemplating 2 proposals either replacing the census or conducting it every 10 years than the present 5. Data collected on Census night provides a comprehensive regularly updated and consistent evidence base. Without this evidence base planners, policy and decision makers will not have the means available to make the informed decisions required to maintain, progress and monitor the development, wellbeing, prosperity or sustainability of Australian communities. Census information is used by all sectors of the community, from local, state and federal government to, large and small businesses, community groups and students. The need for evidence informed decision making is well proven, resulting in increased effectiveness, reduction in harm, better resource allocation, enhanced cost-effectiveness/cost-benefit of investment, improved reach and enhanced accountability. Decreasing the frequency with which the census is conducted; would greatly alter the capacity for informed decision making, therefore have a negative impact on all levels of government and communities within Australia.

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 389

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 390

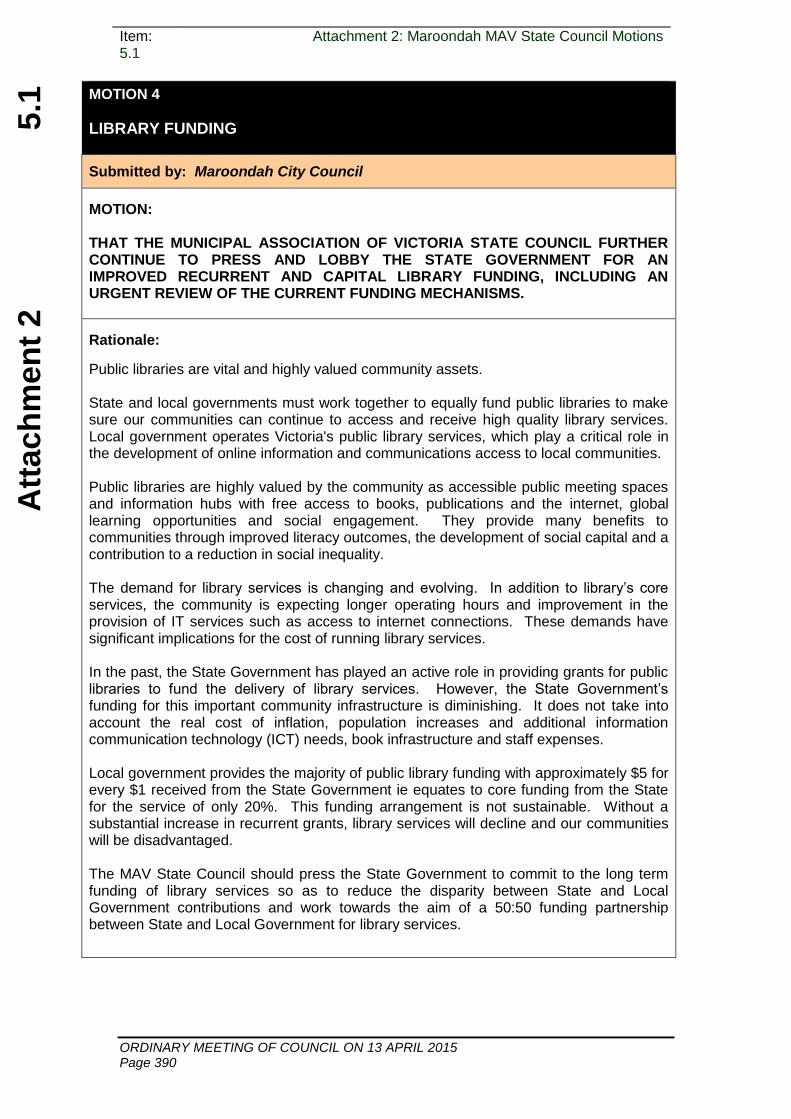

MOTION 4

LIBRARY FUNDING

Submitted by: Maroondah City Council

MOTION: THAT THE MUNICIPAL ASSOCIATION OF VICTORIA STATE COUNCIL FURTHER CONTINUE TO PRESS AND LOBBY THE STATE GOVERNMENT FOR AN IMPROVED RECURRENT AND CAPITAL LIBRARY FUNDING, INCLUDING AN URGENT REVIEW OF THE CURRENT FUNDING MECHANISMS.

Rationale:

Public libraries are vital and highly valued community assets. State and local governments must work together to equally fund public libraries to make sure our communities can continue to access and receive high quality library services. Local government operates Victoria's public library services, which play a critical role in the development of online information and communications access to local communities. Public libraries are highly valued by the community as accessible public meeting spaces and information hubs with free access to books, publications and the internet, global learning opportunities and social engagement. They provide many benefits to communities through improved literacy outcomes, the development of social capital and a contribution to a reduction in social inequality. The demand for library services is changing and evolving. In addition to library’s core services, the community is expecting longer operating hours and improvement in the provision of IT services such as access to internet connections. These demands have significant implications for the cost of running library services. In the past, the State Government has played an active role in providing grants for public libraries to fund the delivery of library services. However, the State Government’s funding for this important community infrastructure is diminishing. It does not take into account the real cost of inflation, population increases and additional information communication technology (ICT) needs, book infrastructure and staff expenses. Local government provides the majority of public library funding with approximately $5 for every $1 received from the State Government ie equates to core funding from the State for the service of only 20%. This funding arrangement is not sustainable. Without a substantial increase in recurrent grants, library services will decline and our communities will be disadvantaged. The MAV State Council should press the State Government to commit to the long term funding of library services so as to reduce the disparity between State and Local Government contributions and work towards the aim of a 50:50 funding partnership between State and Local Government for library services.

Att

ach

men

t 2

5.1

Item: 5.1

Attachment 2: Maroondah MAV State Council Motions

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 391

Att

ach

men

t 3

5.1

Item: 5.1 Attachment 3: Banyule City Council MAV State Council Motions 2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 392

MAV State Council Meeting – 15 May 2015

To submit a motion for consideration by State Council on 15 May 2015, please complete this form and email to State Council, no later than Friday,17 April 2015 . Please note, deadlines are strictly observed.

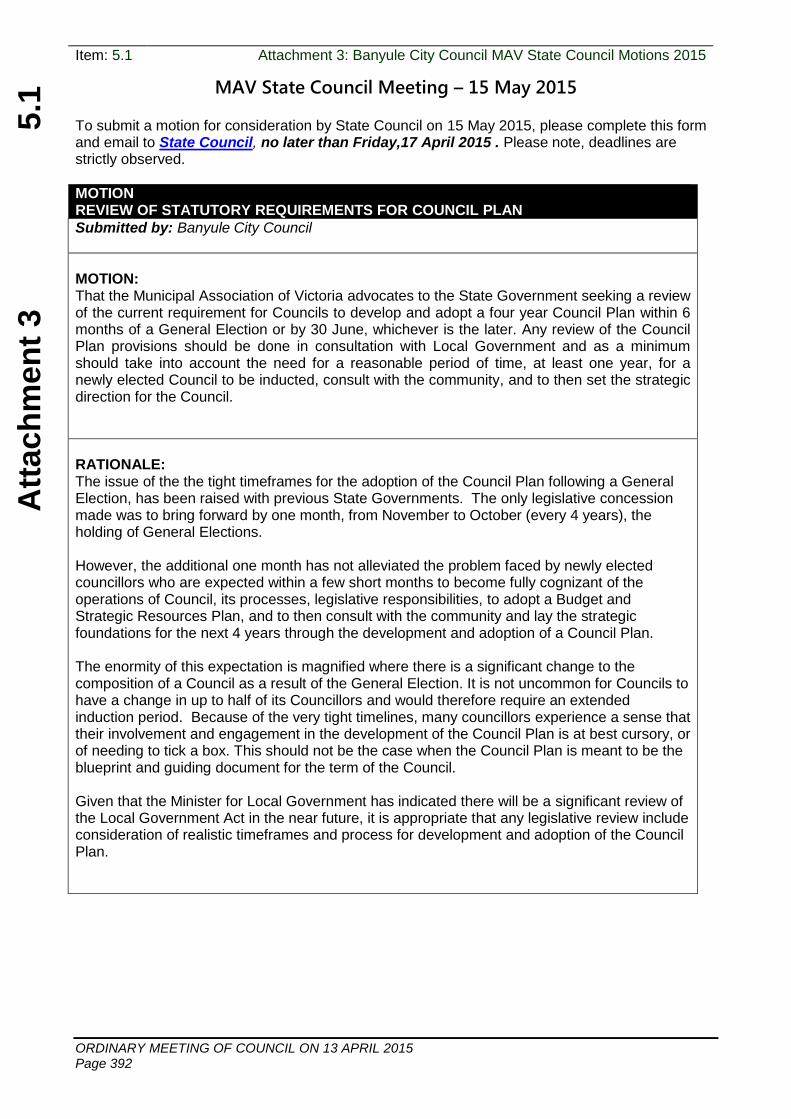

MOTION REVIEW OF STATUTORY REQUIREMENTS FOR COUNCIL PLAN

Submitted by: Banyule City Council

MOTION: That the Municipal Association of Victoria advocates to the State Government seeking a review of the current requirement for Councils to develop and adopt a four year Council Plan within 6 months of a General Election or by 30 June, whichever is the later. Any review of the Council Plan provisions should be done in consultation with Local Government and as a minimum should take into account the need for a reasonable period of time, at least one year, for a newly elected Council to be inducted, consult with the community, and to then set the strategic direction for the Council.

RATIONALE: The issue of the the tight timeframes for the adoption of the Council Plan following a General Election, has been raised with previous State Governments. The only legislative concession made was to bring forward by one month, from November to October (every 4 years), the holding of General Elections. However, the additional one month has not alleviated the problem faced by newly elected councillors who are expected within a few short months to become fully cognizant of the operations of Council, its processes, legislative responsibilities, to adopt a Budget and Strategic Resources Plan, and to then consult with the community and lay the strategic foundations for the next 4 years through the development and adoption of a Council Plan. The enormity of this expectation is magnified where there is a significant change to the composition of a Council as a result of the General Election. It is not uncommon for Councils to have a change in up to half of its Councillors and would therefore require an extended induction period. Because of the very tight timelines, many councillors experience a sense that their involvement and engagement in the development of the Council Plan is at best cursory, or of needing to tick a box. This should not be the case when the Council Plan is meant to be the blueprint and guiding document for the term of the Council. Given that the Minister for Local Government has indicated there will be a significant review of the Local Government Act in the near future, it is appropriate that any legislative review include consideration of realistic timeframes and process for development and adoption of the Council Plan.

Att

ach

men

t 3

5.1

Item: 5.1 Attachment 3: Banyule City Council MAV State Council Motions 2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 393

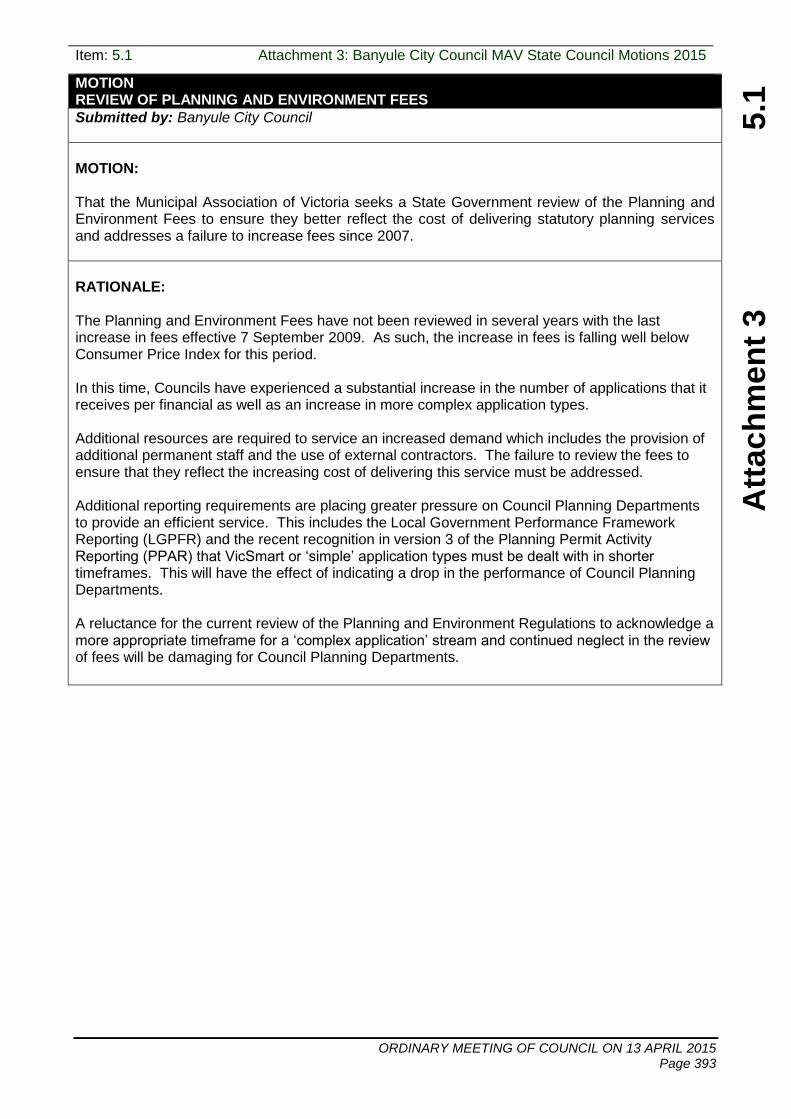

MOTION REVIEW OF PLANNING AND ENVIRONMENT FEES

Submitted by: Banyule City Council

MOTION: That the Municipal Association of Victoria seeks a State Government review of the Planning and Environment Fees to ensure they better reflect the cost of delivering statutory planning services and addresses a failure to increase fees since 2007.

RATIONALE: The Planning and Environment Fees have not been reviewed in several years with the last increase in fees effective 7 September 2009. As such, the increase in fees is falling well below Consumer Price Index for this period. In this time, Councils have experienced a substantial increase in the number of applications that it receives per financial as well as an increase in more complex application types. Additional resources are required to service an increased demand which includes the provision of additional permanent staff and the use of external contractors. The failure to review the fees to ensure that they reflect the increasing cost of delivering this service must be addressed. Additional reporting requirements are placing greater pressure on Council Planning Departments to provide an efficient service. This includes the Local Government Performance Framework Reporting (LGPFR) and the recent recognition in version 3 of the Planning Permit Activity Reporting (PPAR) that VicSmart or ‘simple’ application types must be dealt with in shorter timeframes. This will have the effect of indicating a drop in the performance of Council Planning Departments. A reluctance for the current review of the Planning and Environment Regulations to acknowledge a more appropriate timeframe for a ‘complex application’ stream and continued neglect in the review of fees will be damaging for Council Planning Departments.

Att

ach

men

t 3

5.1

Item: 5.1 Attachment 3: Banyule City Council MAV State Council Motions 2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 394

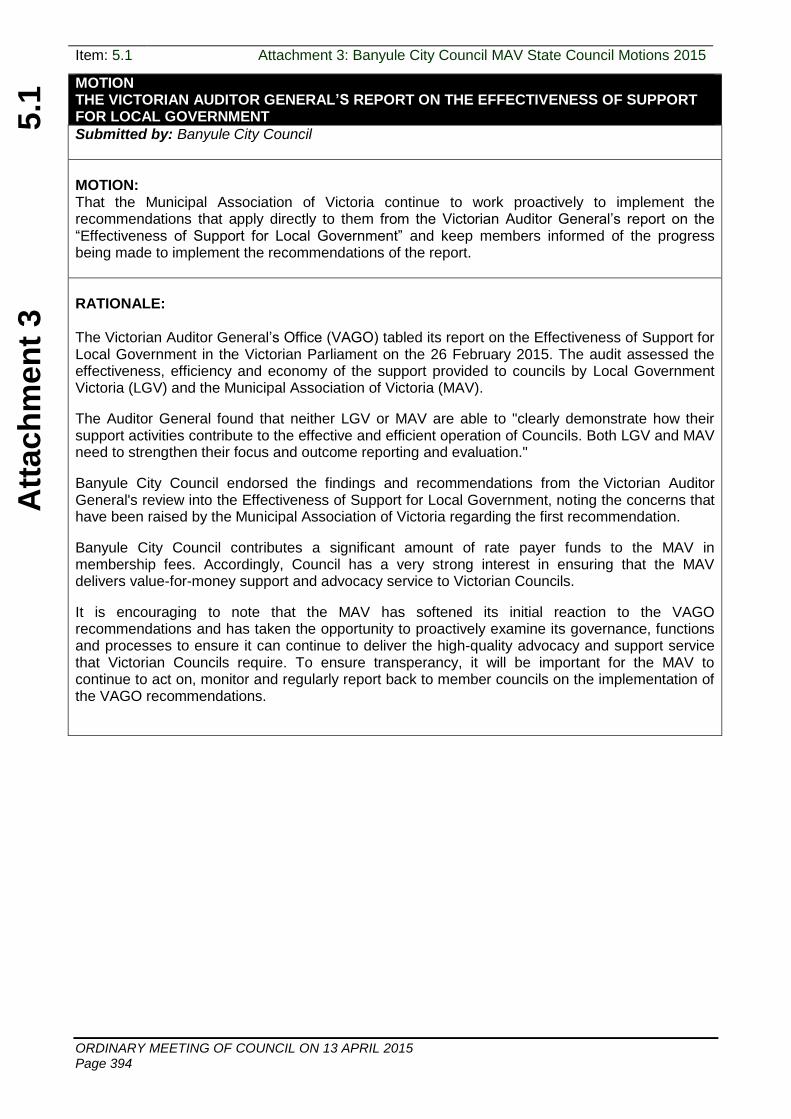

MOTION THE VICTORIAN AUDITOR GENERAL’S REPORT ON THE EFFECTIVENESS OF SUPPORT FOR LOCAL GOVERNMENT

Submitted by: Banyule City Council

MOTION: That the Municipal Association of Victoria continue to work proactively to implement the recommendations that apply directly to them from the Victorian Auditor General’s report on the “Effectiveness of Support for Local Government” and keep members informed of the progress being made to implement the recommendations of the report.

RATIONALE: The Victorian Auditor General’s Office (VAGO) tabled its report on the Effectiveness of Support for Local Government in the Victorian Parliament on the 26 February 2015. The audit assessed the effectiveness, efficiency and economy of the support provided to councils by Local Government Victoria (LGV) and the Municipal Association of Victoria (MAV).

The Auditor General found that neither LGV or MAV are able to "clearly demonstrate how their support activities contribute to the effective and efficient operation of Councils. Both LGV and MAV need to strengthen their focus and outcome reporting and evaluation."

Banyule City Council endorsed the findings and recommendations from the Victorian Auditor General's review into the Effectiveness of Support for Local Government, noting the concerns that have been raised by the Municipal Association of Victoria regarding the first recommendation.

Banyule City Council contributes a significant amount of rate payer funds to the MAV in membership fees. Accordingly, Council has a very strong interest in ensuring that the MAV delivers value-for-money support and advocacy service to Victorian Councils.

It is encouraging to note that the MAV has softened its initial reaction to the VAGO recommendations and has taken the opportunity to proactively examine its governance, functions and processes to ensure it can continue to deliver the high-quality advocacy and support service that Victorian Councils require. To ensure transperancy, it will be important for the MAV to continue to act on, monitor and regularly report back to member councils on the implementation of the VAGO recommendations.

Att

ach

men

t 4

5.1

Item: 5.1 Attachment 4: Whitehorse City Council MAV State Council Motions 2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 395

MAV State Council Meeting – 15 May 2015

To submit a motion for consideration by State Council on 15 May 2015, please complete this form and email to State Council, no later than Friday,17 April 2015 . Please note, deadlines are strictly observed.

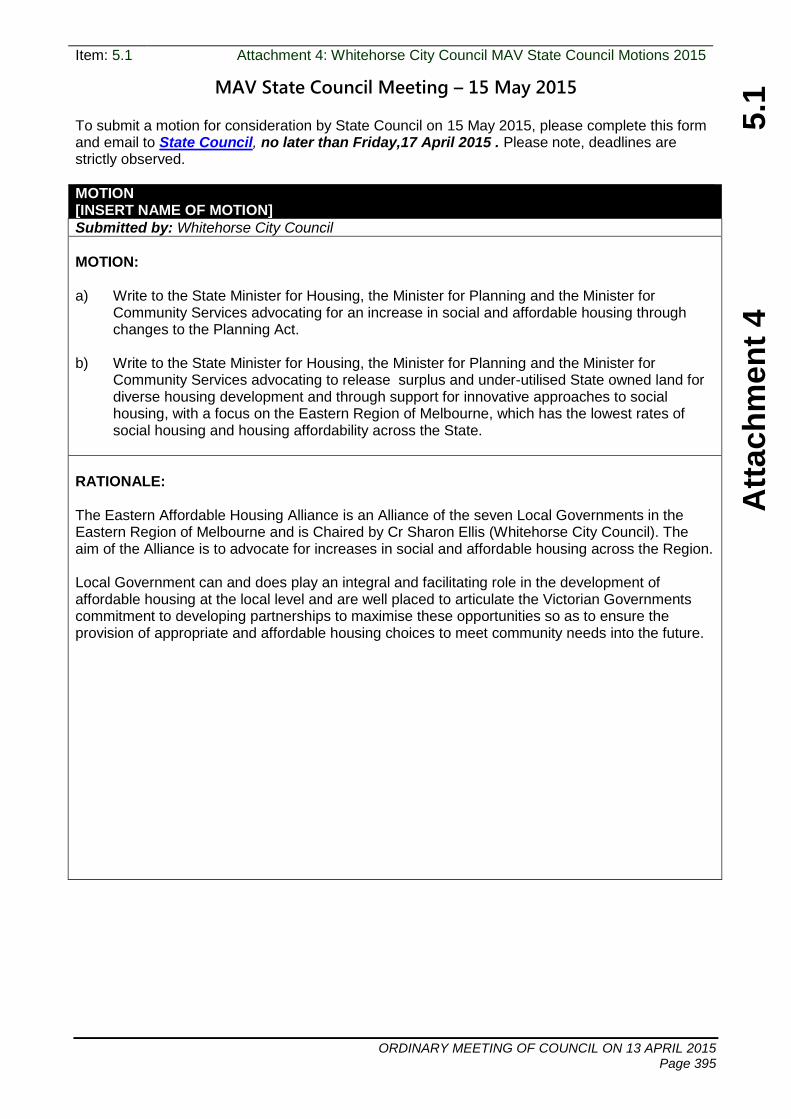

MOTION [INSERT NAME OF MOTION]

Submitted by: Whitehorse City Council

MOTION: a) Write to the State Minister for Housing, the Minister for Planning and the Minister for

Community Services advocating for an increase in social and affordable housing through changes to the Planning Act.

b) Write to the State Minister for Housing, the Minister for Planning and the Minister for

Community Services advocating to release surplus and under-utilised State owned land for diverse housing development and through support for innovative approaches to social housing, with a focus on the Eastern Region of Melbourne, which has the lowest rates of social housing and housing affordability across the State.

RATIONALE: The Eastern Affordable Housing Alliance is an Alliance of the seven Local Governments in the Eastern Region of Melbourne and is Chaired by Cr Sharon Ellis (Whitehorse City Council). The aim of the Alliance is to advocate for increases in social and affordable housing across the Region. Local Government can and does play an integral and facilitating role in the development of affordable housing at the local level and are well placed to articulate the Victorian Governments commitment to developing partnerships to maximise these opportunities so as to ensure the provision of appropriate and affordable housing choices to meet community needs into the future.

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 396

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 397

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 398

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 399

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 400

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 401

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 402

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 403

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 404

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 405

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 406

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 407

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 408

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 409

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 410

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 411

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 412

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 413

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 414

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 415

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 416

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 417

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 418

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 419

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 420

Att

ach

men

t 1

5.2

Item: 5.2 Attachment 1: Advocacy Report 1 July 2014 - 31 December 2014

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 421

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 422

Rating Strategy

2014/2015

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 423

1. Introduction

To ensure the Local Government Act rating objectives of equity and efficiency are

achieved, it is important that Banyule City Council has a rating strategy in place that is

transparent to the community and reviewed annually as part of the budget process.

The existing valuation methods available for taxation of property is limited by the Local

Government Act 1989t; however the application of an alternate rating method (e.g. income

tax rate) is not available within the current constraints of existing legislation.

The important matters to be considered in relation to the Rating Strategy include:

The legislative framework (Section 2)

What rates and charges can be declared (Section 3)

The rate base (Section 4)

Uniform or Differential rates (Section 5)

Differential Rates (Section 6)

Impact of Council revaluations and supplementary valuations (Section 7)

The municipal charge (Section 8)

Service rates and charges (Section 9)

Special rates and charges (Section 10)

Rebates and concessions (Section 11)

Exempt Properties (Section 12)

Collections (Section 13)

1.1 What is a Rating Strategy?

A rating strategy is the method by which council systematically considers factors of importance that informs its decisions about the rating system. The rating system determines how Council will raise money from properties within the municipality. It does not influence the total amount to be raised, only the share of revenue contributed by each property. The rating system comprises the valuation base and actual rating instruments allowed under the Local Government Act (1989) to calculate property owners’ liability for rates.

The Local Government Act 1989 (The Act) requires Councils to exercise sound

financial management. In particular, The Act states that the principles of sound

financial management are to:

a) manage financial risks faced by Council prudently having regard to economic

circumstances;

b) pursue spending and rating policies that are consistent with a reasonable degree of

stability of the rates effort;

c) ensure that decisions are made and actions are taken having regard to their

financial effects on future generations;

d) ensure full, accurate and timely disclosure of financial information relating to the

Council

The Council articulates its objectives, strategies and activities through community

consultation and the development of key documents such as:

the City Plan 2013/17, and

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 424

the Strategic Resource Plan, and

the Council Budget

Generally Councils can fund their activities through revenue (including rates), capital

grants and borrowing. As rates are a significant part of Councils revenue, a rating

strategy is a key element in the Council exercising sound financial management.

1.2 Objectives of the Strategic Resource Plan

When reviewing the rating strategy, Council needs to meet the objectives set out in the Strategic Resource Plan (Council’s 4 year financial plan).

Council's commitment to managing resources wisely will be achieved by the following

key directions as outlined in the Strategic Resource Plan 2013/17:

Develop and deliver best value services and facilities

Provide reasonable financial management and business planning processes

Enable good governance and accountability with minimal risk

Create a productive and engaged workforce

Maintain and strengthen corporate information and innovation, and

Plan and manage the systems and assets that support Council’s service delivery

The Strategic Resource Plan is updated annually.

Council’s focus areas and initiatives are wide ranging and include:

Improving preschools infrastructure

Maintaining and upgrading of roads, drains and footpaths

Ensuring our natural environment and tree assets are appropriately maintained

Responding to land use planning issues in consistent, fair and timely manner

Delivering social and economic benefits for our community

Producing quality community festivals and events across the municipality

2. Rating – the Legislative Framework

The purpose of this section is to outline the legislative framework in which Council has to

operate in constructing its rating system and the various issues that Council must consider

in making its decision on the rating objectives.

2.1 Objectives

The legislation specifies a number of major objectives for the rating system:

the equitable imposition of rates and charges

a reasonable degree of stability in the level of the rates effort

contribute to the equitable and efficient carrying out of its functions and

consistent with principles of financial management, councils also generally apply

principles of simplicity or transparency.

It must be acknowledged from the start that these objectives can conflict.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 425

The two objectives which the rating system must have the greatest regard to are the

achievement of equity and efficiency.

2.1.1 Equity

Having determined that Council must review its rating strategy in terms of the

equitable imposition of rates and charges, it is a much more vexed question in

terms of how to define and determine what is in fact equitable in the view of the

Council.

Horizontal equity refers to justice or fairness in the treatment of like properties - in

other words, that similar rates are paid by similar properties. Obviously there is a

fundamental importance on which characteristics define similarity. On the

assumption that Council valuations fairly reflect the true valuation of like

properties, horizontal equity will be achieved.

Vertical equity refers to justice or fairness in the treatment of properties in

different circumstances (e.g. different property types – residential/commercial/

vacant land/ electronic gaming machine land). It implies a "relativity" dimension to

the fairness of the tax burden.

In the case of property taxation it may be considered equitable for one type of

property to have to bear more or less of the rates effort than another type of

property. Clearly, however, affordability criteria may be a significant concern that

influences views about vertical equity.

Rates are essentially a wealth tax, determined on the value of property. A pure

“wealth tax” approach implies that the rates paid relate directly to the value of a

ratepayer’s real property. The tests of horizontal and vertical equity are solely

based on property value.

There is some debate surrounding the characteristics of property owners that

may impinge on the application of an equity principle.

The three main ways in which positions can vary are:

the benefit or user pays principle – some groups have more access to, make

more use of, and benefit from more, specific council services;

the capacity to pay principle – some ratepayers have more ability to pay rates

than do others with similarly valued properties;

the incentive or encouragement principle – some ratepayers may be doing

more towards achieving council goals than others in areas such as

environmental or heritage protection.

The Benefit Principle

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 426

A popular complaint levelled at councils is that “the rates I pay have no

correlation with the services I consume or the benefits I receive”. This argument

is based on the benefit principle (the opposite of the wealth tax principle) that

argues there should be a nexus between consumption/benefit and the rate effort.

Application of the benefit principle is difficult in practice because of the complexity

and, in some cases, impossibility, of measuring the relative levels of access and

consumption across the full range of council services. In some ways the arguing

of the benefit principle with respect to council rates is like trying to do the same

for the income tax that is used to fund a wide range of universally accessed

services.

It is likely to be quite costly to regularly undertake in-depth analyses on service

access, consumption patterns and costs in order to attempt to review the level of

benefit. In any event many subjective assumptions will have to be introduced.

Other pricing instruments such as user charges, special rates and charges and

service rates and charges better lend themselves to dealing with the issue of

benefit.

Capacity to Pay

Notwithstanding the practical limitations, council can make choices about the tax

treatment of classes of real property in so much as they believe that a class of

property will reflect the financial position of a household or business and its

capacity to pay. However, the most vexed issue related to capacity to pay is

assessing it across different classes of property.

While personal income tax is more reflective of the capacity to pay, it is not

possible to expect a property tax system to deal practically with all aspects of

capacity to pay based on individual households and businesses. It is also not

practical or acceptable to shift, modify or manipulate the existing system to the

benefit of one group of ratepayers at the expense of another unless such shift is

widely accepted and for a proper purpose.

In fact, Local Government has no mandate or ability to universally apply a

“capacity to pay” test.

Council has the option of introducing a Council rebate to certain groups to reduce

that property’s rate effort. Presently pensioners within the municipality are able to

access the State Government Rebate.

2.1.2 Efficiency

Efficiency can be defined as the ratio of ends produced (output) to means used

(inputs). In other words it can be considered directly related to the cost of

administering the rates system. Administration costs include the issuing of

assessments, collection of rates, including maintaining and improving collection

systems, monitoring outcomes, educating and informing ratepayers, and

enforcement and debt recovery. It also includes the maximization of additional

rate income through supplementary valuations by ensuring the timeliness and

accuracy of amended rate notices.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 427

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 428

A simple rating system is more transparent, meaning that the underlying purpose

and principles behind the design of a rate are clearer - who is liable for a

particular rate and how rate liability is calculated. However, it is also possible for

a simple rate system to be costly if it is unpopular and results in increased

appeals and higher collection costs.

2.2 Anomalies with Property Taxation

Property taxes do not recognise the situation where ratepayers are “asset rich” and

“income poor”. In these cases ratepayers may have considerable wealth reflected in the

property they own but have a low level of income. Examples include pensioners,

businesses subject to cyclical downturn, and households with large families and property

owners with little equity. In a commercial sense the argument has also been expressed in

terms of the ability of property to generate a reasonable return.

2.3 Recent legislative changes

2.3.1 Local Government Legislation Amendment (Miscellaneous) Bill

2012

The Local Government Legislation Amendment (Miscellaneous) Bill 2012 was

enacted in October 2012. This legislation requires the Minister to issue guidelines

which Councils must have regard to before declaring a differential rate for any

land. The guidelines may address the objectives of differential rating; suitable

uses of differential rating powers; and types of land that are appropriate for

differential rating.

The Minister is given the power to seek an Order prohibiting any Council from

making a declaration of a differential rate if the Minister considers the declaration

would be inconsistent with any guideline. It is important to note that any

prohibition Order does not have retrospective effect.

The ministerial guidelines were released in April 2013. These guidelines are

available from: http://www.dpcd.vic.gov.au/localgovernment/projects-and-

programs/differential-rates-guidelines

2.3.1.1 Key messages from the Ministerial Guidelines

The Ministerial Guidelines state that Council should establish the suitable

use of a differential rate by considering:

Other rating instruments available under the Local Government Act and the merits or shortcomings of each in achieving specified objectives; and

The anticipated relative effectiveness of the proposed differential rate to achieve the specified objectives determined by council.

The guidelines also require the specified objectives of differential rates to

align to the strategic objectives set out in the Council Plan.

Types and classes of land categories stated by the guidelines that are considered ‘appropriate’ for differential rates include the following:

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 429

General land

Residential land

Farm land

Commercial land

Industrial land

Retirement village land

Vacant land

Derelict; and

Cultural and recreational.

The types and classes of land categories stated by guidelines that are considered ‘not appropriate’ for differential rates include:

Electronic gaming machine venues or casinos

Liquor licensed venues or liquor outlet premises

Business premises defined whole or in part by hours of trade

Fast food franchises or premises

Tree plantations in the farming and rural activity zones; and

Land within the Urban Growth Zone without an approved Precinct Structure Plan in place.

2.3.2 Fire Services Levy

From 1 July 2013, the Victorian Government have introduced a property based

levy to fund the Metropolitan Fire Brigade (MFB) and the Country Fire Authority

(CFA).

The Fire Services Property Levy will replace the existing insurance-based funding

model as recommended by the Victorian Bushfires Royal Commission.

Until now, the fire services have been largely funded by contributions made by

the insurance industry and the State Government. The insurance industry passed

the cost of its contribution on to Victorian policy holders through a fire services

levy on insurance premiums.

Under the property-based levy:

councils collect the levy through rates notices;

the levy will be calculated based on the capital improved value of a property;

the levy will consist of a fixed component plus a variable component calculated as a percentage of capital improved property values;

the fixed component will vary for residential properties and non-residential properties; and

the levy rate will vary for different property types such as residential, industrial, commercial and primary production.

The fire services property levy is shown separately on rate notices.

It is important to note that Council is not raising any additional revenue from the

levy; it is merely acting as a collection agency on behalf of the State Government.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 430

Useful websites for more information on the Fire Services levy:

Department of Treasury and Finance - www.dtf.vic.gov.au/firelevy

Fire Services Levy Monitor - www.firelevymonitor.vic.gov.au

3. What rates and Charges may a Council declare?

Section 155 of the Local Government Act provides that Council may declare the following

rates and charges on rateable land:

Rating option

Description Current Banyule structure

General rate A general rate is applied to all properties and can be set as either a uniform rate or a number of differential rates.

Banyule applies the differential

rates listed below.

Uniform rate A uniform rate is a single rate in the

dollar that is applied to the value of all

properties in the municipality.

Banyule does not apply a

uniform rate.

Differential

Rates

Differential rates are different rates in

the dollar that are applied to different

classes of properties and are permitted

if the Council uses Capital Improved

Value as the rating valuation base.

The Act allows the use of differential

rates if the Council considers that this

will contribute to the equitable and

efficient carrying out of its functions.

The following differential rates

are levied:

Residential Improved

Residential Vacant (set at 1.35 times the residential improved rate)

Commercial Improved (set at 1.25 times the residential improved rate)

Commercial Vacant (set at 1.75 times the residential improved rate)

Industrial Improved (set at 1.25 times the residential improved rate)

Industrial Vacant (set at 1.75 times the residential improved rate)

Cultural & Recreational (set at 84% of the residential improved rate) on only four properties within the city.

Municipal

Charge

A municipal charge to cover some of

the administrative costs of the Council.

This is a flat-rate charge applied to all

properties excluding cultural and

recreational properties.

Banyule levies a municipal

charge

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 431

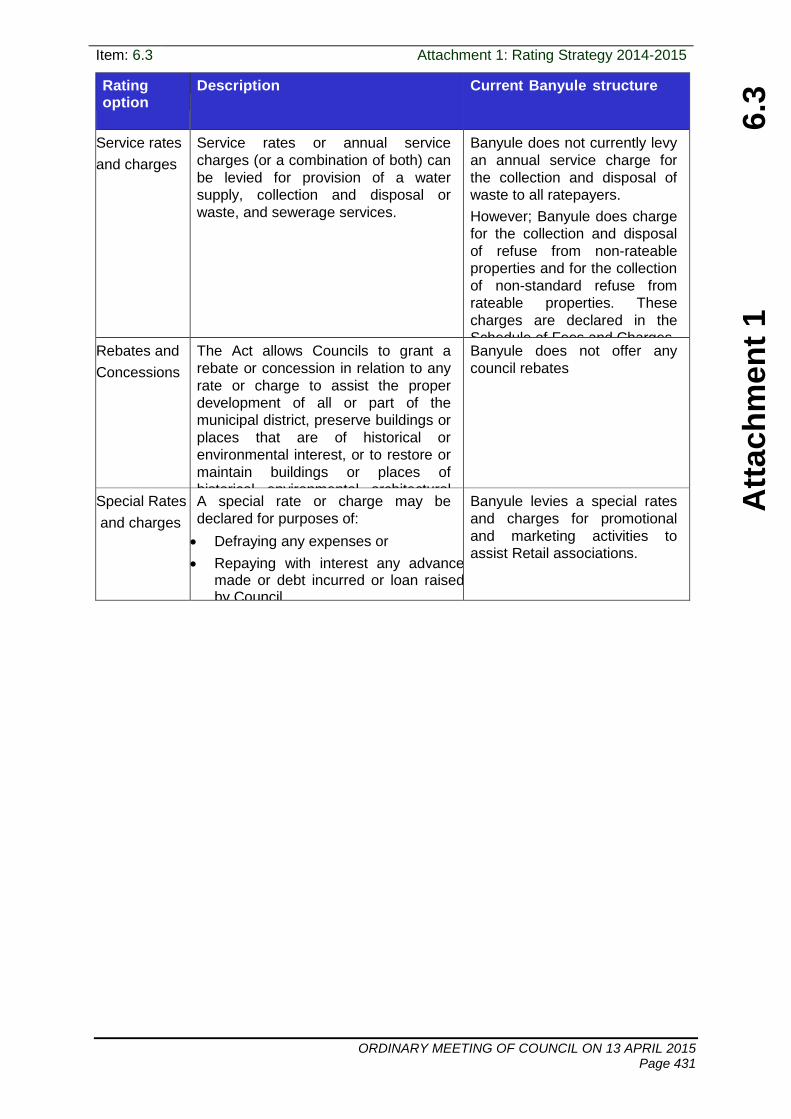

Rating option

Description Current Banyule structure

Service rates

and charges

Service rates or annual service

charges (or a combination of both) can

be levied for provision of a water

supply, collection and disposal or

waste, and sewerage services.

Banyule does not currently levy

an annual service charge for

the collection and disposal of

waste to all ratepayers.

However; Banyule does charge

for the collection and disposal

of refuse from non-rateable

properties and for the collection

of non-standard refuse from

rateable properties. These

charges are declared in the

Schedule of Fees and Charges. Rebates and

Concessions

The Act allows Councils to grant a

rebate or concession in relation to any

rate or charge to assist the proper

development of all or part of the

municipal district, preserve buildings or

places that are of historical or

environmental interest, or to restore or

maintain buildings or places of

historical, environmental, architectural

or scientific importance.

Banyule does not offer any

council rebates

Special Rates

and charges

A special rate or charge may be

declared for purposes of:

Defraying any expenses or

Repaying with interest any advance made or debt incurred or loan raised by Council.

Banyule levies a special rates

and charges for promotional

and marketing activities to

assist Retail associations.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 432

4. Determining which valuation base to use

The purpose of this section is to outline the different methods that Council can utilise to

value land and the issues that Council must consider in making its decision on the

valuation method.

4.1 Introduction

Three methods of valuing land are allowed under the Act:

Site Value (SV) – Value of land only

Net Annual Value (NAV) – rental valuation based on Capital improvement Value (CIV). For residential and farm properties, NAV is calculated at 5 per cent of the CIV. For commercial properties NAV is calculated as the greater of the estimated annual rental value or 5 per cent of the CIV.

Capital Improved value (CIV) – value of land and improvements upon the land

Banyule uses capital improved value for rating valuation purposes, along with the

majority of other Victorian Councils.

4.2 Site Value

This method places a value on the land only and does not consider any value of

any buildings constructed on the land. It is not considered to result in the most

equitable distribution of the rate effort.

With valuations based simply on the valuation of the land and with only very

limited ability to apply differential rates, the implementation of site value in

Banyule would cause a significant shift in rate effort from the business sector into

the residential sector. In addition, there would be further rating movements away

from modern townhouse style developments on relatively small land parcels to

older established homes on the more typical quarter acre residential block.

There is no Victorian Council that currently uses this valuation base.

4.3 Net Annual Value

Net Annual value, in concept, represents the annual rental value of a property.

However, in practice, NAV is closely linked to capital improved value. For

residential properties Valuers derive the NAV directly as 5 per cent of the CIV.

In contrast to the treatment of residential, NAV for business properties are

assessed with regard to the actual market rental. This differing treatment of

business versus residential has led to some suggestions that all properties

should be valued on a rental basis. There is currently no legislation that supports

this suggestion.

Where a Council utilises NAV, it may only apply three differential rates. For

example, City of Melbourne utilise NAV, applying a differential rate for residential

and non-residential land only.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 433

4.4 Capital Improved Value

Capital improved valuation is the most commonly used valuation method by

Victorian Local Government with 73 Councils applying this methodology. Based

on the value of both land and all improvements on the land, it is relatively easy to

understand by ratepayers as it equates to the market value of the property.

For CIV, business properties are valued primarily by the capitalisation method of

valuation. This method of valuation is the industry standard for assessing the

value of business properties and has as its base sale price and market rent of the

property. For this reason, rental details are sought by rating valuers every 2

years. When analysed on a per square meter basis, rents provide a means of

establishing the rental market in a location.

The advantages of using CIV include:

CIV includes all improvements and hence is often supported on the basis that it more closely reflects ‘capacity to pay’. The CIV rating method takes into account the full development value of the property, and hence better meets the equity criteria than site value or NAV.

The concept of the market value of property is far more easily understood with CIV rather than NAV or Site Value.

The use of CIV allows Council to apply differential rates which greatly adds to Council’s ability to equitably distribute the rating effort based on ability to afford Council rates.

The major disadvantage with CIV, and indeed all the other rating methods, is that

rates are based on the property value which may not necessarily reflect the

income level of the property owner as with pensioners and low income earners.

5. Determining the Rating System – Uniform or differential

The purpose of this section is to outline the two rating systems (uniform or differential) that

Council can utilise to apply rates and the issues that Council must consider in making its

decision on the rating system.

5.1 Uniform rate

If a Council declares that general rates will be raised by application of a uniform

rate, the Council must specify a percentage as a uniform rate. A uniform rate will

apply to the value of every rateable property within the municipality.

Rates will be determined by multiplying the percentage (the rate in the dollar) by

the value of the land.

Banyule believes that a uniform rate should not be applied to all properties

because it is not equitable. In particular, such a rate does not reflect the use of

Council services and infrastructure nor does it create incentive for best use of

property in the municipality.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 434

Banyule has adopted differential rating as it considers that differential rating

contributes to the equitable distribution of the rating effort. Differential rating

allows particular classes of properties to be assessed at different levels from the

general rate set for the municipality. Differential rating allows Council to shift part

of the rate effort from some groups of ratepayers to others, through different

‘rates in the dollar’ for each class of property.

Council is entitled to apply many differential rates provided it used Capital

Improved Valuations as its base for rating.

Section 161 of The Act outlines the regulations relating to differential rates. This

section is outlined below:

1) A Council must raise any general rates by application of a differential rate, if it uses the capital improved value system of valuing rates,

a) Council considers that the differential rate will contribute to the equitable and efficient carrying out of its functions.

2) If a Council declares a differential rate for any land, the Council must:

a) Specify the objectives of the differential rate, which must be consistent with the equitable and efficient carrying out of the Councils functions and must include the following:

i. A definition of the types of classes of land which are subject to the rate and a statement of the reasons for the use and level of that rate.

ii. An identification of the type or classes of land which are subject to the rate in respect of the uses, geographical location (other than location on the basis of whether or not the land is within a specific ward in Councils district) and planning scheme zoning of the land, and

iii. If there has been a change in the valuation system, any provision for relief from a rate to ease the transition for that land, and

b) Specify the characteristics of the land which are the

criteria for declaring the differential rate.

The maximum differential allowed is no more than 4 times the lowest differential

rate. For Banyule, the lowest rate is the residential rate.

Council has the option of increasing each respective differential rate in order to

influence the behaviour of landowners.

There is no theoretical limit on the number or type of differentials which can be

levied.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 435

6. Differential Rates

6.1 Advantages of a differential rating system

The perceived advantages of utilising a differential rating system are:

There is a greater flexibility to distribute the rate effort between all classes of property and therefore link rates with the ability to pay and reflecting the tax deductibility of rates for businesses;

Differential rates allows Council to better reflect the investment required by Council to establish infrastructure to meet the needs to the commercial and industrial sector; and

Enables Council to encourage particular developments through it rating approach e.g. encourage building on vacant land.

6.2 Disadvantages of a differential rating system

The perceived disadvantages of utilising a differential rating system are:

The justification of the differential rate can at times be difficult for the various rating groups to understand, giving rise to queries, objections and complaints.

Differential rating involves a degree of administrative complexity, as properties can change from one classification to another (e.g. vacant land to residential) requiring Council to process supplementary valuations.

6.3 Objectives of the rate and characteristics

Council considers that each differential rate will contribute to the equitable and efficient carrying out of Council functions.

Details of the objectives of each differential rate are set out below.

6.3.1 Residential Vacant Land

Objective:

To encourage the development of land for residential purposes; and to ensure that such rateable land makes an equitable financial contribution to the cost of carrying out the functions of Council, including the:

1) Implementation of good governance and sound financial stewardship; and

2) Construction, renewal, upgrade, expansion and maintenance of infrastructure assets; and

3) Development and provision of health, environmental, conservation, leisure, recreation, youth and family community services; and

4) Provision of strategic and economic management, town planning and general support services; and

5) Promotion of cultural, heritage and tourism aspects of Council’s municipal district.

Types and Classes

Any rateable land on which no dwelling is erected but which, by reason of its locality and zoning under the Banyule Planning Scheme, would, if developed, be or be likely to be used primarily for residential purposes.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 436

Use and Level of Differential Rate:

The differential rate will be used to fund some of those items of expenditure and Capital Works described in the Budget adopted by Council.

The level of the differential rate is the level which Council considers is necessary to achieve the objectives specified above.

Geographic Location:

Wherever located within the municipal district.

Use of Land:

Any use permitted under the Banyule Planning Scheme.

Planning Scheme Zoning:

The zoning applicable to each rateable land within this category, as determined by consulting maps referred to in the relevant Banyule Planning Scheme.

6.3.2 Commercial/Industrial Vacant Land

Objective:

To encourage the development of land for commercial or industrial purposes; and to ensure that

such rateable land makes an equitable financial contribution to the cost of carrying out the functions of Council, including the:

1) Implementation of good governance and sound financial stewardship; and

2) Construction, renewal, upgrade, expansion and maintenance of infrastructure assets; and

3) Development and provision of health, environmental, conservation, leisure, recreation, youth and family community services; and

4) Provision of strategic and economic management, town planning and general support services; and

5) Promotion of cultural, heritage and tourism aspects of Council’s municipal district.

Types and Classes:

Any rateable land on which no dwelling is erected but which, by reason of its locality and zoning under the Banyule Planning Scheme, would, if developed, be or be likely to be used primarily for commercial or industrial purposes.

Use and Level of Differential Rate:

The differential rate will be used to fund some of those items of expenditure and Capital Works described in the Budget adopted by Council.

The level of the differential rate is the level which Council considers is necessary to achieve the objectives specified above.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 437

Geographic Location:

Wherever located within the municipal district.

Use of Land:

Any use permitted under the Banyule Planning Scheme.

Planning Scheme Zoning:

The zoning applicable to each rateable land within this category, as determined by consulting maps referred to in the Banyule Planning Scheme.

6.3.3 Commercial/Industrial Improved Land

Objective:

To ensure that such rateable land makes an equitable financial contribution to the cost of carrying out the functions of Council having regard to the capacity of such land to be used to yield income and the demands such land makes on Council's infrastructure.

Those functions include the:

1) Implementation of good governance and sound financial stewardship; and

2) Construction, renewal, upgrade, expansion and maintenance of infrastructure assets; and

3) Development and provision of health, environmental, conservation, leisure, recreation, youth and family community services; and

4) Provision of strategic and economic management, town planning and general support services; and

5) Promotion of cultural, heritage and tourism aspects of Council’s municipal district.

Types and Classes:

Any rateable land which is used, or designed or adapted to be used, primarily for commercial or industrial purposes.

Use and Level of Differential Rate:

The differential rate will be used to fund some of those items of expenditure and

Capital Works described in the Budget adopted by Council.

The level of the differential rate is the level which Council considers is necessary

to achieve the objectives specified above.

Geographic Location:

Wherever located within the municipal district.

Use of Land:

Any use permitted under the Banyule Planning Scheme.

Planning Scheme Zoning:

The zoning applicable to each rateable land within this category, as determined

by consulting maps referred to in the Banyule Planning Scheme.

Types of Buildings:

All buildings which are now constructed on the land or which are constructed

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 438

prior to the expiry of the 2013/2014 Financial Year.

6.3.4 Other Land (Including Residential Improved Land)

Objective:

To ensure that such rateable land makes an equitable financial contribution to the

cost of carrying out the functions of Council, having regard to the relative benefits

derived from the carrying out of such functions.

Those functions include the:

1) Implementation of good governance and sound financial stewardship; and

2) Construction, renewal, upgrade, expansion and maintenance of infrastructure assets; and

3) Development and provision of health, environmental, conservation, leisure, recreation, youth and family community services; and

4) Provision of strategic and economic management, town planning and general support services; and

5) Promotion of cultural, heritage and tourism aspects of Council’s municipal district.

Types and Classes:

Any rateable land which is not Residential Vacant Land, Commercial / Industrial

Vacant Land or Commercial / Industrial Improved Land.

Use and Level of Differential Rate:

The differential rate will be used to fund some of those items of expenditure and

Capital Works described in the Budget adopted by Council.

The level of the differential rate is the level which Council considers is necessary

to achieve the objectives specified above.

Geographic Location:

Wherever located within the municipal district.

Use of Land:

Any use permitted under the Banyule Planning Scheme.

Planning Scheme Zoning:

The zoning applicable to each rateable land within this category, as determined

by consulting maps referred to in the Banyule Planning Scheme.

Types of Buildings:

All buildings which are now constructed on the land or which are constructed

prior to the expiry of the 2013/2014 Financial Year.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 439

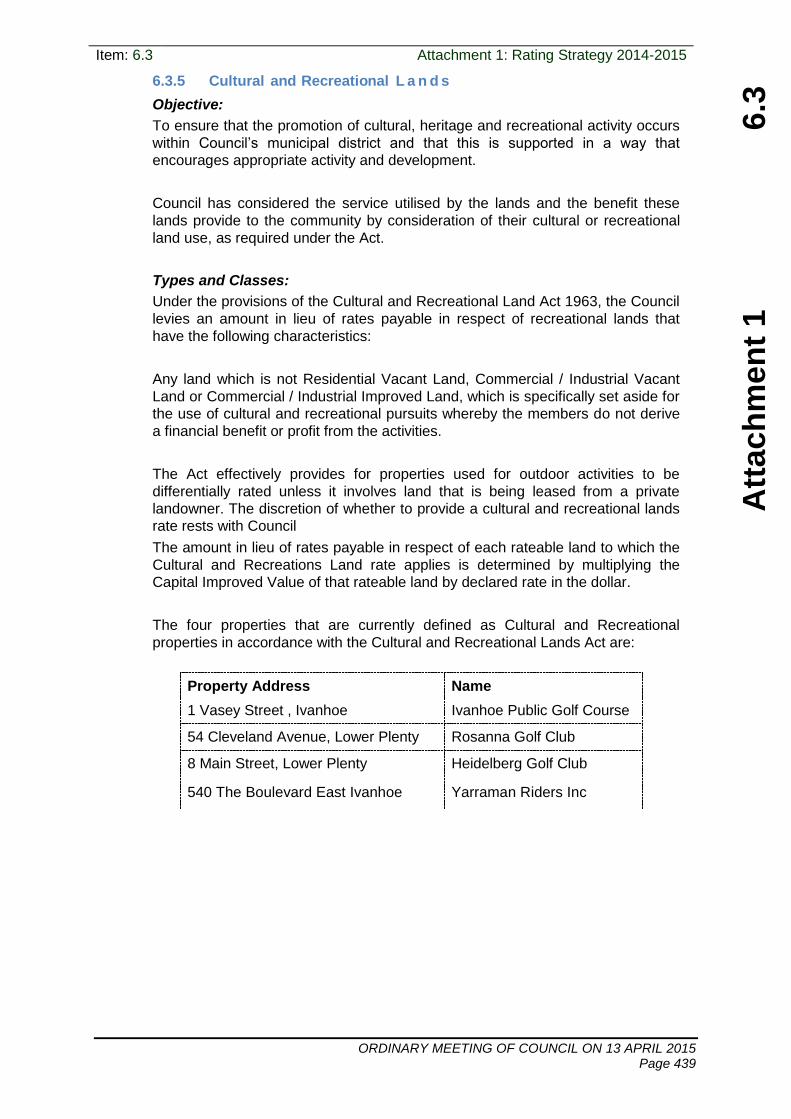

6.3.5 Cultural and Recreational L a n d s

Objective:

To ensure that the promotion of cultural, heritage and recreational activity occurs

within Council’s municipal district and that this is supported in a way that

encourages appropriate activity and development.

Council has considered the service utilised by the lands and the benefit these

lands provide to the community by consideration of their cultural or recreational

land use, as required under the Act.

Types and Classes:

Under the provisions of the Cultural and Recreational Land Act 1963, the Council

levies an amount in lieu of rates payable in respect of recreational lands that

have the following characteristics:

Any land which is not Residential Vacant Land, Commercial / Industrial Vacant

Land or Commercial / Industrial Improved Land, which is specifically set aside for

the use of cultural and recreational pursuits whereby the members do not derive

a financial benefit or profit from the activities.

The Act effectively provides for properties used for outdoor activities to be

differentially rated unless it involves land that is being leased from a private

landowner. The discretion of whether to provide a cultural and recreational lands

rate rests with Council

The amount in lieu of rates payable in respect of each rateable land to which the

Cultural and Recreations Land rate applies is determined by multiplying the

Capital Improved Value of that rateable land by declared rate in the dollar.

The four properties that are currently defined as Cultural and Recreational

properties in accordance with the Cultural and Recreational Lands Act are:

Property Address Name

1 Vasey Street , Ivanhoe Ivanhoe Public Golf Course

54 Cleveland Avenue, Lower Plenty

Rosanna Golf Club

8 Main Street, Lower Plenty Heidelberg Golf Club

540 The Boulevard East Ivanhoe Yarraman Riders Inc

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 440

7. Understanding the impacts of Council Revaluations and Supplementary Valuations

The purpose of this section is to provide an overview of the rate revaluation and

supplementary valuation processes.

7.1 Introduction

All Victorian Councils are required under the Valuations of Land Act 1960 to revalue

properties every two years.

Property values are determined by qualified valuers comparing each property to the

recent sales figures of similar properties in the neighbourhood. The key factors are

location, land size, type of house and condition.

The Valuer General of Victoria is responsible for reviewing the total valuation of each

municipality for accuracy before certifying that the valuations are true and correct.

Valuations are conducted using Best Practice Guidelines formulated and published by

the Valuer General Victoria.

7.2 No Windfall Gain

There is a common misconception that if a property’s valuation rises then Council

receives a “windfall gain” with additional income. This is not so as the revaluation

process results in a redistribution of the rate effort across all properties in the

municipality. Any increase to total valuations of the municipality is offset by a reduction

to the rate in dollar (ad valorem rate) used to calculate the rate for each property. Total

income is fixed each year as part of the budget process

7.3 How does this affect my rates?

The general revaluation process enables Council to re-apportion the rate income

across the municipality in accordance with movements in property values. Properties

which have increased in value by more than the average will receive a rate increase of

more than the headline rate. Properties with an increase in value less than the

average will receive a rate increase less than the headline rate.

7.4 Supplementary Valuations

In accordance with the Valuation of Land Act further Valuations are required to be carried out between General revaluations, these are known as Supplementary Valuations.

Supplementary Valuations are completed when properties are physically changed by buildings being erected, demolished or altered, when properties are amalgamated, subdivided, portions sold off, rezoned or roads constructed.

Supplementary Valuations are adopted to bring the value of properties into line with values assigned to other properties in the municipality. This is to ensure that as near as practicable the rating valuation reflects the current property condition at the date prescribed for the General revaluation.

8. Municipal Charge

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 441

The purpose of this section is to outline the municipal charge that Council utilises to apply

rates and the issues that Council consider when applying a municipal charge.

8.1 Introduction

In addition to differential rates, Council may declare a municipal charge to cover some

of the administrative costs of Council. The total revenue from a municipal charge must

not exceed 20% of the sum total of the general rates and municipal charge combined

in a financial year.

The application of a municipal charge represents a choice to raise a portion of the rates

by a flat fee for all properties, rather than sole use of the CIV valuation method.

Banyule currently levies a Municipal Charge on all rateable properties this charge is

used by Council to ensure that all properties contribute equally toward defraying a

portion of Council’s administrative costs.

8.2 Advantages of a municipal charge

The arguments in favour of a municipal charge are they apply equally to all properties

and are based upon the recovery of fixed costs of providing administrative services

irrespective of valuation. The same contribution amount per assessment to cover a

portion of Councils administrative costs can be seen as an equitable method of

recovering these costs.

8.3 Disadvantages of a municipal charge

The argument against a municipal charge is that this charge is regressive in nature and

would result in lower valued properties paying higher overall rates and charges than

they do at present. The equity objective in levying rates against property values is lost

in a municipal charge as it is levied uniformly across all assessments.

9. Service Charges

The purpose of this section is to outline the service rates and charges that Council

currently applies and new charges that could be utilised and the issues that Council must

consider in making its decision when reviewing these service rates and charges.

Section 162 of the Act allows Council to declare a service rate for specified services.

9.1 Advantages of a Service Charge

If a service charge is levied for collection and disposal of refuse it is easily understood by

the residents as a user pays system.

9.2 Disadvantages of a Service Charge

The argument against a service charge is that this charge is regressive in nature and

would result in lower valued properties paying higher overall rates and charges than

they do at present. The equity objective in levying rates against property values is lost

in a service charge as it is levied uniformly across all assessments.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 442

9.3 Current use of Service Charges

Banyule does not currently levy an annual service charge for the collection and

disposal of waste to all ratepayers. A standard service is provided to residential

rateable properties and is funded from general rates.

9.4 Annual Charges for Non-Rateable land

Banyule charges for the collection and disposal of refuse from non-rateable properties.

These charges are declared in the Schedule of Fees and Charges.

The revenue received covers the costs of providing this service.

9.5 Annual Charges for Rateable land

Banyule charges for non-standard and additional collection and disposal of refuse

from rateable properties.

These charges are declared in the Schedule of Fees and Charges.

10. Special Rates

The purpose of this section is to outline the special rates and charges that Council

currently applies and new charges that could be utilised.

10.1 Introduction

Section 163 of the Act permits councils to declare a special rate in relation to the

performance of a function where Council considers that the function is or will be of

special benefit to the persons required to pay the special rate.

10.2 Special Rates Schemes

Council currently has 12 Special Rate and or Charge schemes in operation, 11 are

Promotional Schemes and one is a Constructional Scheme.

10.2.1 Promotional Schemes

These schemes are declared for strip shopping centres within the City. They are

primarily for the encouragement of commerce, retail activity and employment

opportunities in and around the scheme area.

Council considers that there would be a special benefit to the area as the

viability of the Precinct as a business, commercial, retail and professional area

the value and the use, occupation and enjoyment of the properties and the

businesses included in the scheme area will be maintained or enhanced

through increased economic activity.

The amount collected from the scheme is matched by council (to 2011 capped

amounts) and payments are made to the traders on a quarterly basis.

A decision to review special rates and or Charge Schemes occurs at the expiry

of the current special rates, not during the budget discussions and is subject to

extensive consultation with stakeholders and separate Council discussion and

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 443

approval.

10.2.2 Constructional Schemes

These schemes are declared when there is something constructed that would

be of special benefit to the persons required to pay it. For example road, drain

and car parking construction.

The scheme that exists within Banyule is for road construction and it runs for a

period of 10 years. Contributors have the option of paying the account in full at

the commencement of the scheme and therefore avoiding the financing

surcharge or paying it off over a 10 year period.

These schemes are declared as required following extensive consultation with

stakeholders and do not form part of the budget process.

11. Rebates and Concessions

The purpose of this section is to outline the rebates and concessions that could be utilised

and the issues that Council must consider in making its decision when reviewing these

rebates and concessions.

11.1 Introduction

Under The Act, Council has the power to grant a rebate or concession in relation to

any rate or charge to assist ‘proper’ development and the preservation of buildings or

places of historical, environmental, architectural or scientific importance within the

municipality.

While the original intent of the term ‘proper’ development has a land use perspective,

Councils have been known to use the provision to assist economic development.

Rebates and concessions should be used with respect to individual properties within

a property class. The legislation intended that differential rates be used to achieve an

outcome for a class of properties.

The granting of rebates and concessions results in a higher rating effort being applied

to other properties to raise the same level of rate revenue.

Att

ach

men

t 1

6.3

Item: 6.3 Attachment 1: Rating Strategy 2014-2015

ORDINARY MEETING OF COUNCIL ON 13 APRIL 2015 Page 444

11.2 Pensioner Rebate

11.2.1 State Government Pensioner Rebate

Pensioners may qualify for a maximum 50% State Government rate rebate (to

a gazetted maximum) for the home in which they are living. A $50 rebate may

also apply for the Fires Services Property Levy. To be eligible, a ratepayer

must hold one of the following concession cards:

Pensioner Concession Card from Centrelink or Veterans' Affairs

Gold Card from Department of Veterans Affairs specifying War Widow (WW) or Totally and Permanently Incapacitated (TPI).

Other than administrative costs this State Government Rebate scheme is cost

neutral to Council as this is fully funded by the State Government.

11.2.2 Council Pensioner Rebate

Council has the option of introducing a pensioner rebate to complement the

existing State Government rebate. A Council Pensioner rate rebate

redistributes the rate effort with other ratepayers bearing the cost by way of

higher rates and charges. The rate effort for non-pensioners is likely to be

greater as the number of pensioners increases.

Once a rebate has been introduced, it may be difficult to remove. Ratepayers

receiving the benefit would not support the removal of this benefit.

Council does not grant any further rebates or concessions than those afforded

by the State Government Pensioner Rebate scheme.