basel iii disclosures - citizens...

TRANSCRIPT

Basel III Disclosures

For the quarterly period ended March 31, 2015

Table of Contents

Introduction 4

Report overview 4

Scope of application 5

Risk Governance 6

Capital Structure and Adequacy 9

Capital Structure 9

Capital Adequacy 11

Capital Conservation Buffer 15

Credit Risk 16

General Disclosures 16

Counterparty Credit Risk-Related Disclosures 22

Credit Risk Mitigation 25

Securitization 25

Equities (Non-Trading) 27

Interest Rate Risk (Non-Trading) 28

Market Risk 29

Appendix 1 – Citizens Financial Group Basel III Disclosures Matrix 30

Appendix 2 – Forward-Looking Statements 44

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

1

GLOSSARY OF ACRONYMS AND TERMS

The following listing provides a comprehensive reference of common acronyms and terms we regularly use in ourfinancial reporting:

1Q15 Form 10-Q March 31, 2015 Quarterly Report on Form 10-Q2014 Form 10-K 2014 Annual Report on Form 10-KALLL Allowance for Loan and Lease LossesAOCI Accumulated Other Comprehensive IncomeBHC Bank Holding CompanyBoard Citizens Financial Group, Inc. Board of DirectorsCBNA Citizens Bank, N.A.CBPA Citizens Bank of PennsylvaniaCCAR Comprehensive Capital Analysis and ReviewCCB Capital Conservation BufferCCO Chief Credit OfficerCET1 Common Equity Tier 1CEO Chief Executive OfficerCFO Chief Financial OfficerCitizens or CFG or theCompany

Citizens Financial Group, Inc. and its Subsidiaries

CRA Community Reinvestment ActCRO Chief Risk OfficerCSA Credit Support AnnexCVA Credit Valuation AdjustmentDodd-Frank Act The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010FDIC Federal Deposit Insurance CorporationFFCB Federal Farm Credit BanksFHLB Federal Home Loan BankFHLMC Federal Home Loan Mortgage CorporationFNMA Federal National Mortgage AssociationFRB Federal Reserve BankFR Y-9C Regulatory Financial Statements for Bank Holding CompaniesGAAP Accounting Principles Generally Accepted in the United States of AmericaGNMA Government National Mortgage AssociationMBS Mortgage-Backed SecuritiesMD&A Management’s Discussion and Analysis of Financial Condition and Results of

OperationsNRSRO Nationally Recognized Statistical Ratings OrganizationsOCC Office of the Comptroller of the CurrencyOTC Over the CounterPFE Potential Future ExposureRBS The Royal Bank of Scotland Group plc or any of its subsidiariesRWA Risk-Weighted Assets

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

2

SBLI Savings Bank Life InsuranceSBO Serviced by Others Loan PortfolioSSFA Simplified Supervisory Formula ApproachVaR Value-at-Risk

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

3

Introduction

Citizens Financial Group, Inc. was the 13th largest retail BHC in the United States as of March 31,2015, according to SNL Financial, with $136.5 billion of total assets. Headquartered in Providence,Rhode Island, we deliver a broad range of retail and commercial banking products and services toindividuals, institutions and companies. Our approximately 17,800 employees strive to meet thefinancial needs of customers and prospects through approximately 1,200 branches andapproximately 3,200 ATMs operated in an 11-state footprint across the New England, Mid-Atlanticand Midwest regions and through our online, telephone and mobile banking platforms.

Our primary subsidiaries are CBNA, a national banking association whose primary Federal regulatoris the OCC, and CBPA, a Pennsylvania-chartered savings bank regulated by the Department ofBanking of the Commonwealth of Pennsylvania and supervised by the FDIC as its primary Federalregulator.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

4

Report overview

As required under U.S. regulation that interprets global regulatory standards known as “Basel III,”which have been established by the Basel Committee on Banking Supervision1, CFG will producethis report quarterly to update market participants regarding risk-based capital and risk exposures.The Basel Committee refers to this ongoing requirement as “Pillar 3 Disclosure." This reportprovides information on the Company’s capital structure, capital adequacy, risk exposures, andRWA. This report also includes information on the methodologies used to calculate RWA. Thisreport is unaudited and should be read in conjunction with CFG’s 2014 Form 10-K and 1Q15 Form10-Q, which include important information on risk management policies and practices. This reportalso references certain regulatory disclosures provided in the Company’s FR Y-9C. A disclosurematrix is contained in the Appendix 1 of this report and specific references have been made herein.

The disclosures presented in this report are intended to comply with the public disclosurerequirements of the U.S. Basel III final rule, which was issued by the FRB, OCC and FDIC in July2013. The final rule implements the Basel III capital framework and certain provisions of the Dodd-Frank Act, including the Collins Amendment, which establishes minimum risk-based capital andleverage requirements on a consolidated basis for insured depository institutions and their bankholding companies. Certain aspects of the final rule, such as new minimum capital ratios, changesto the prompt corrective action ratios to reflect higher minimum capital ratios for the various capitaltiers, and a revised methodology for calculating RWA became effective on January 1, 2015. Otheraspects of the final rule, such as the capital conservation buffer and new regulatory deductions fromand adjustments to capital, will be phased in over several years beginning on January 1, 2015.

__________________1 The Basel Committee on Banking Supervision is a cooperative international forum that seeks to strengthen risk-based controlsand supervision of the world-wide financial system.

This report contains forward-looking statements within the Private Securities Litigation ReformAct of 1995. Any statement that does not describe historical or current facts is a forward-lookingstatement, as outlined in Appendix 2 of this document.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

5

Scope of application

The Basel III framework applies to CFG and its subsidiary banks. CFG is a “standardized approach”reporting institution under Basel III.

The Company’s basis for consolidation used for regulatory financial statement reporting purposesis the same as the basis used for our financial statements prepared under GAAP. Please refer toFinancial Statements and Supplementary Data - Note 1 - Significant Accounting Policies: Basis ofPresentation on page 156 in the Company’s 2014 Form 10-K for more information on the basis forconsolidation for financial reporting purposes. For regulatory capital reporting purposes, the capitaland assets associated with our two financial subsidiaries (Citizens Securities, Inc. and RBS InsuranceAgency, Inc.) are excluded from regulatory capital and all associated capital ratios of consolidatedCBNA (per instruction from the OCC).

Restrictions on transfers between CFG and its subsidiary banks

A number of regulations and statutes restrict transfers of funds and capital within CFG. As a financialholding company and a BHC, CFG is regulated and supervised by the FRB. The OCC is the primaryregulator and supervisor for CBNA, while the State of Pennsylvania and the FDIC regulate andsupervise CBPA. Transfers of funds and capital between these entities may be restricted by applicablestatutes and regulations that may pertain either to the BHC, one or both of its subsidiary banks, orall entities as affiliates.

Sections 23A and 23B of the Federal Reserve Act and FRB Regulation W are primary restrictorsof lending, borrowing and otherwise transacting business between affiliates. Please refer to Business- Regulation and Supervision - Transactions with Affiliates and Insiders on pages 23-24 of theCompany’s 2014 Form 10-K for a full discussion of these regulations.

Restrictions on the payment of dividends and other capital distributions within the group weighmost heavily on the banks. The FRB expects bank holding companies to act as a “source of strength”to each individual subsidiary bank, providing capital to the banks as needed. Consistent with thisview, bank regulators establish strong controls to ensure that capital will not be returned to the BHCin a manner that would undermine a bank’s overall “safety and soundness.” Therefore, both CBNAand CBPA are subject to specific qualitative and quantitative tests and examinations that may restrictthem from paying dividends or otherwise returning capital to the BHC. Please refer to Business -Regulation and Supervision on pages 15-25 of the Company’s 2014 Form 10-K for an overview ofthe general controls and restrictions imposed on distributions of capital by the banks and for detailsof the current status of each bank versus its applicable regulatory restrictions.

In addition, the BHC, CBNA, and CBPA are subject to capital adequacy and liquidity standards. Ifeither bank or the BHC fail to meet these standards, our financial condition and operations would

be adversely affected. Please refer to Risk Factors - Risks Related to Regulations Governing OurIndustry on pages 46-47 of the Company’s 2014 Form 10-K for additional information regardingthis risk.

Financial subsidiaries

Although empowered as a financial holding company, CFG does not currently hold directsubsidiaries that conduct activities beyond those permitted under banking powers. The Company’sprimary subsidiaries are CBNA and CBPA. Other direct subsidiaries are immaterial and not subjectto additional risk-based requirements as might be imposed on a subsidiary that engaged in securitiestrading or insurance underwriting. As CFG’s primary bank, CBNA holds two financial subsidiariesthat are appropriately deconsolidated from CBNA for purposes of determining its risk-based capitaladequacy.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

6

Risk Governance

We are committed to maintaining a strong, integrated and proactive approach to the managementof all risks to which we are exposed in pursuit of our business objectives. A key aspect of our Board'sresponsibility as the main decision making body is setting our risk appetite to ensure that the levelsof risk we are willing to accept in the attainment of our strategic business and financial objectivesare clearly understood.

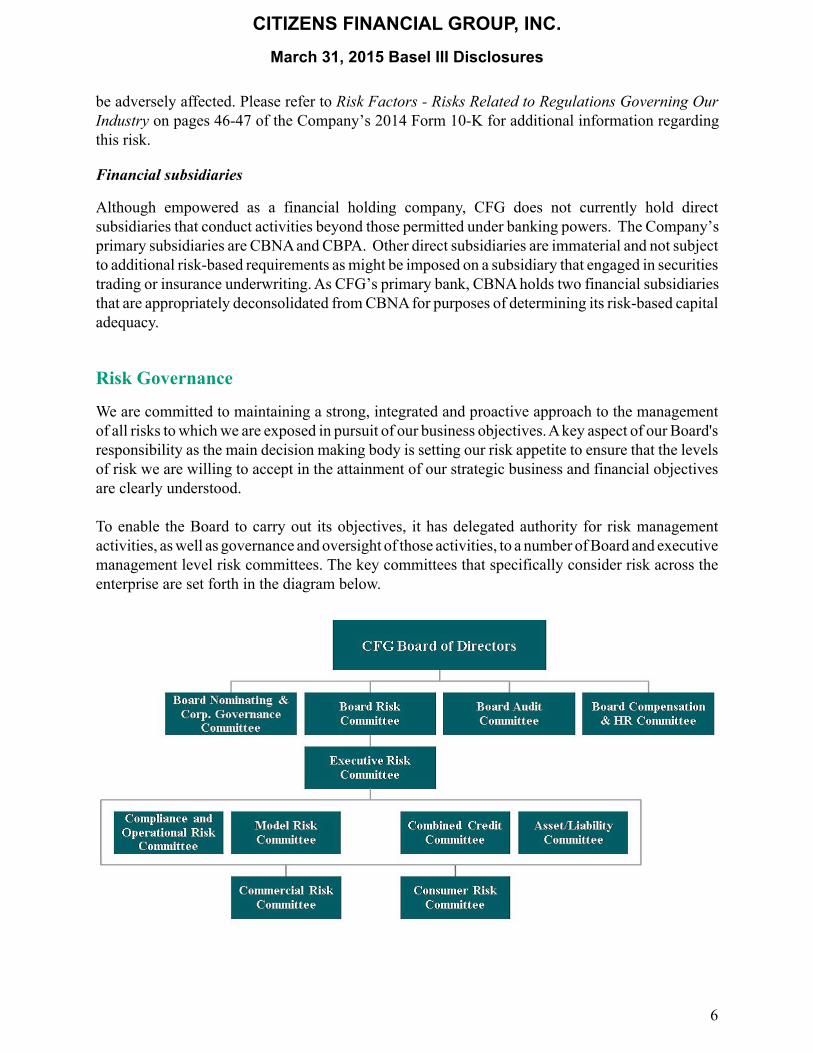

To enable the Board to carry out its objectives, it has delegated authority for risk managementactivities, as well as governance and oversight of those activities, to a number of Board and executivemanagement level risk committees. The key committees that specifically consider risk across theenterprise are set forth in the diagram below.

Chief Risk Officer

The CRO directs our overall risk management function overseeing the compliance, regulatory,operational and credit risk management. In addition, the CRO has oversight of the management ofmarket, liquidity and strategic risks. The CRO reports to our CEO and our Board Risk Committee.

Risk Framework

Our risk management framework is embedded in our business through a “Three Lines of Defense”model which defines responsibilities and accountabilities.

First Line of Defense

The business lines (including their associated support functions) are the First Line of Defense andare accountable for owning and managing, within our defined risk appetite, the risks which existin their respective business areas. The business lines are responsible for performing regular riskassessments to identify and assess the material risks that arise in their area of responsibility,complying with relevant risk policies, testing and certifying the adequacy and effectiveness of theircontrols on a regular basis, establishing and documenting operating procedures and establishingand owning a governance structure for identifying and managing risk.

Second Line of Defense

The Second Line of Defense includes independent monitoring and control functions accountablefor developing and ensuring implementation of risk and control frameworks, oversight of risk,financial management and valuation, and regulatory compliance. This centralized risk function isappropriately independent from the business and is accountable for overseeing and challenging ourbusiness lines on the effective management of their risks. This risk function utilizes training,communications and awareness to provide expert support and advice to the business lines. Thisincludes interpreting the risk policy standards and risk management framework, overseeingcompliance by the businesses with policies and responsibilities, including providing relevantmanagement information and escalating concerns where appropriate.

The Executive Risk Committee, chaired by the CRO, actively considers our inherent material risks,analyzes our overall risk profile and seeks confirmation that the risks are being appropriatelyidentified, assessed and mitigated.

Third Line of Defense

Our internal audit function is the Third Line of Defense acting as an independent appraisal andassurance function. As an independent assurance function, internal audit ensures the key businessrisks are being managed to an acceptable level and that the risk management and internal controlframework is operating effectively. Independent assessments are provided to our Audit Committeeon a monthly basis and to the Board and executive management in the form of quarterly opinions.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

7

Risk Appetite

Risk Appetite is a strategic business and risk management tool. We define our risk appetite as themaximum limit of acceptable risk beyond which we would either be unable to achieve our strategicobjectives and capital adequacy obligations or would assume an unacceptable amount of risk to doso. The Board Risk Committee advises our Board in relation to current and potential future riskstrategy, including determination of risk appetite and tolerance.

The principal non-market risks to which we are subject are: credit risk, operational risk, liquidityrisk, strategic risk and reputational risk. We are also subject to market risk. Market risk refers topotential losses arising from changes in interest rates, foreign exchange rates, equity prices,commodity prices and/or other relevant market rates or prices. Market risk does not result fromproprietary trading, which we prohibit. Rather, modest market risk arises from trading activitiesthat serve customer needs, including hedging of interest rate and foreign exchange risk. As describedbelow, more material market risk arises from our non-trading banking activities, such as loanorigination and deposit gathering. We have established enterprise-wide policies and methodologiesto identify, measure, monitor and report market risk. We actively manage both trading and non-trading market risks.

Our risk appetite framework and risk limit structure establishes guidelines to determine the balancebetween existing and desired levels of risk and supports the implementation, measurement andmanagement of our risk appetite policy.

Please refer to Management’s Discussion and Analysis of Financial Condition and Results ofOperations — Risk Governance on pages 120-129 of the Company’s 2014 Form 10-K for moreinformation on risk governance.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

8

Capital Structure and Adequacy

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

9

Capital Structure

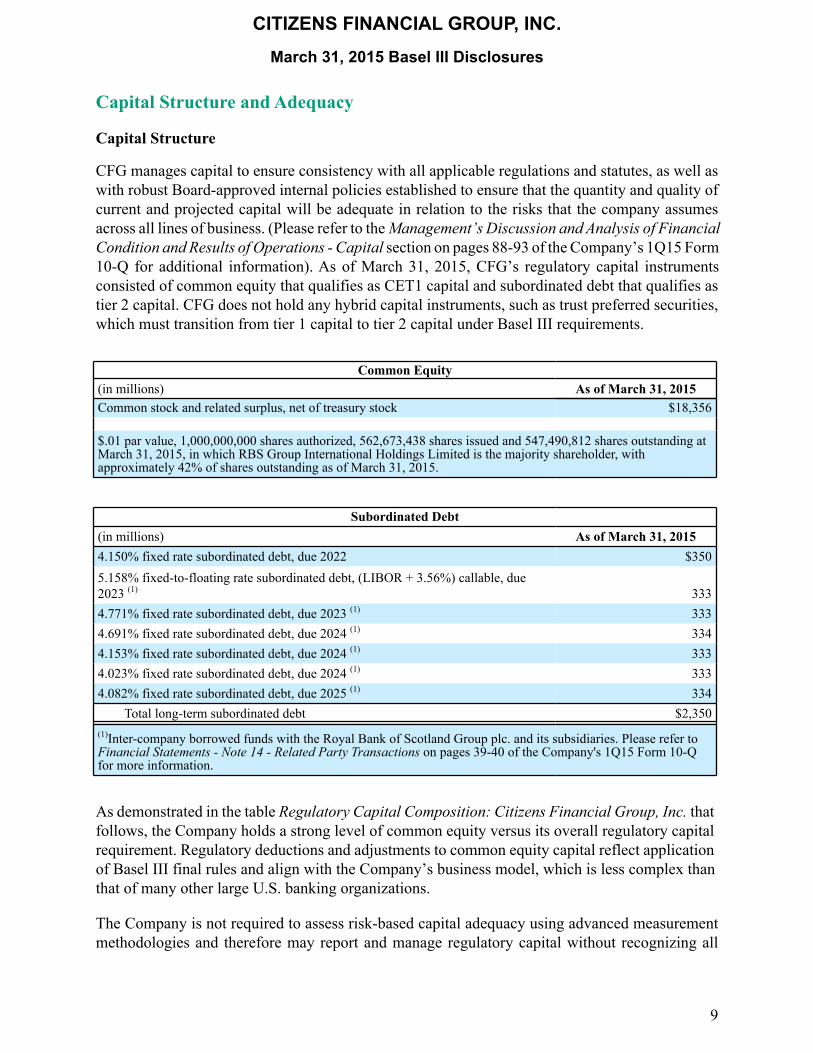

CFG manages capital to ensure consistency with all applicable regulations and statutes, as well aswith robust Board-approved internal policies established to ensure that the quantity and quality ofcurrent and projected capital will be adequate in relation to the risks that the company assumesacross all lines of business. (Please refer to the Management’s Discussion and Analysis of FinancialCondition and Results of Operations - Capital section on pages 88-93 of the Company’s 1Q15 Form10-Q for additional information). As of March 31, 2015, CFG’s regulatory capital instrumentsconsisted of common equity that qualifies as CET1 capital and subordinated debt that qualifies astier 2 capital. CFG does not hold any hybrid capital instruments, such as trust preferred securities,which must transition from tier 1 capital to tier 2 capital under Basel III requirements.

As demonstrated in the table Regulatory Capital Composition: Citizens Financial Group, Inc. thatfollows, the Company holds a strong level of common equity versus its overall regulatory capitalrequirement. Regulatory deductions and adjustments to common equity capital reflect applicationof Basel III final rules and align with the Company’s business model, which is less complex thanthat of many other large U.S. banking organizations.

The Company is not required to assess risk-based capital adequacy using advanced measurementmethodologies and therefore may report and manage regulatory capital without recognizing all

Common Equity(in millions) As of March 31, 2015Common stock and related surplus, net of treasury stock $18,356

$.01 par value, 1,000,000,000 shares authorized, 562,673,438 shares issued and 547,490,812 shares outstanding atMarch 31, 2015, in which RBS Group International Holdings Limited is the majority shareholder, withapproximately 42% of shares outstanding as of March 31, 2015.

Subordinated Debt(in millions) As of March 31, 20154.150% fixed rate subordinated debt, due 2022 $3505.158% fixed-to-floating rate subordinated debt, (LIBOR + 3.56%) callable, due2023 (1) 3334.771% fixed rate subordinated debt, due 2023 (1) 3334.691% fixed rate subordinated debt, due 2024 (1) 3344.153% fixed rate subordinated debt, due 2024 (1) 3334.023% fixed rate subordinated debt, due 2024 (1) 3334.082% fixed rate subordinated debt, due 2025 (1) 334

Total long-term subordinated debt $2,350(1)Inter-company borrowed funds with the Royal Bank of Scotland Group plc. and its subsidiaries. Please refer toFinancial Statements - Note 14 - Related Party Transactions on pages 39-40 of the Company's 1Q15 Form 10-Qfor more information.

elements of AOCI that are included in equity, as reported under U.S. GAAP. As an AOCI Opt-outinstitution, the Company is not required to include unrealized gains and losses on available-for-salesecurities, derivatives held as fair-value cash flow hedges or defined pension benefits in commonequity. The Company opted for this approach because risks inherent in the Company’s available-for-sale securities portfolio are significantly less systemic than risks generally inherent in portfoliosheld by advanced approach institutions. In addition, the Company’s ability to continue to pledgethese assets to support bank funding in stress conditions mitigates the risk of capital deteriorationdue to a forced sale at depressed market values. Lastly, opting out of the inclusion of AOCI inregulatory capital avoids unnecessary and potentially misleading volatility in the Company’s capitalratios.

The Company’s exposure to other potential deductions and adjustments to capital is minimal. TheCompany does not invest in its own regulatory capital instruments, directly or indirectly, except inrelation to treasury stock, which is deducted from regulatory capital in accordance with regulatoryrules. The Company does not measure liabilities at fair value on its balance sheet and does not holdmaterial interests in unconsolidated financial institutions. The Company’s subsidiary banks do notissue capital instruments to third parties, which would expose the Company to a “minority interest”deduction for third-party capital. Lastly, the Company had $163 million of mortgage servicingrights as of March 31, 2015, and was below the threshold that determines when these assets mustbe deducted from capital.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

10

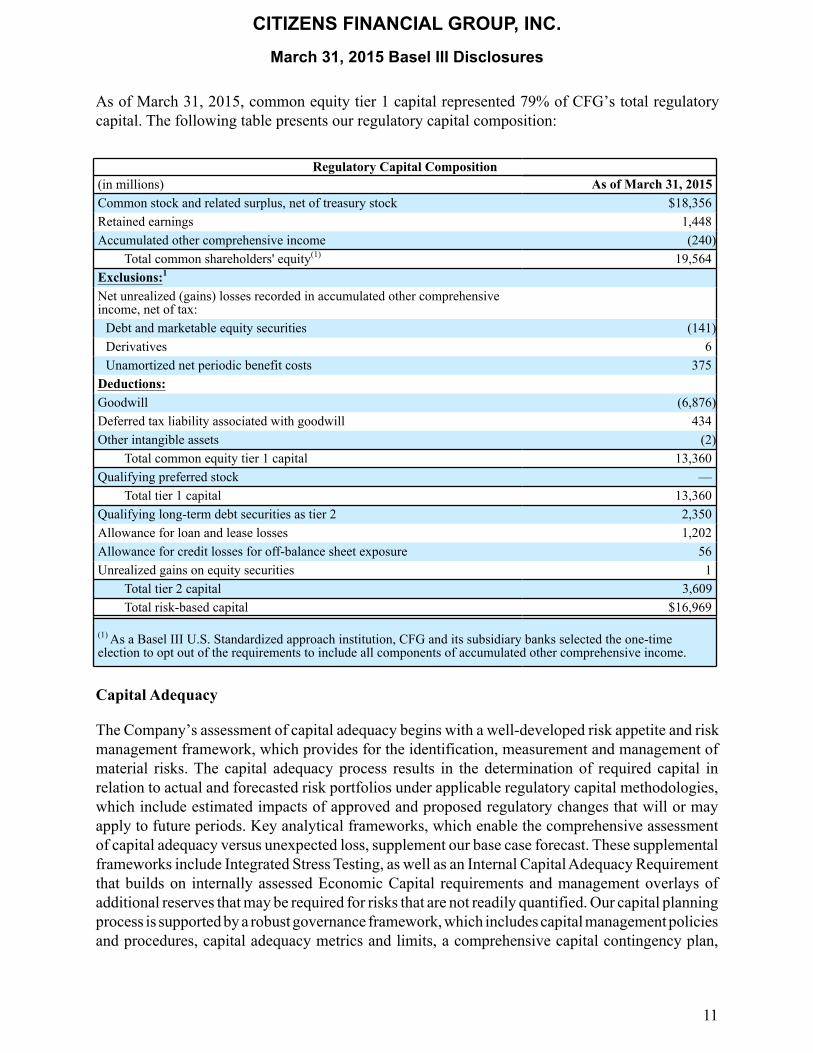

As of March 31, 2015, common equity tier 1 capital represented 79% of CFG’s total regulatorycapital. The following table presents our regulatory capital composition:

Regulatory Capital Composition(in millions) As of March 31, 2015Common stock and related surplus, net of treasury stock $18,356Retained earnings 1,448Accumulated other comprehensive income (240)

Total common shareholders' equity(1) 19,564Exclusions:1

Net unrealized (gains) losses recorded in accumulated other comprehensiveincome, net of tax:

Debt and marketable equity securities (141)Derivatives 6Unamortized net periodic benefit costs 375

Deductions:Goodwill (6,876)Deferred tax liability associated with goodwill 434Other intangible assets (2)

Total common equity tier 1 capital 13,360Qualifying preferred stock —

Total tier 1 capital 13,360Qualifying long-term debt securities as tier 2 2,350Allowance for loan and lease losses 1,202Allowance for credit losses for off-balance sheet exposure 56Unrealized gains on equity securities 1

Total tier 2 capital 3,609Total risk-based capital $16,969

(1) As a Basel III U.S. Standardized approach institution, CFG and its subsidiary banks selected the one-timeelection to opt out of the requirements to include all components of accumulated other comprehensive income.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

11

Capital Adequacy

The Company’s assessment of capital adequacy begins with a well-developed risk appetite and riskmanagement framework, which provides for the identification, measurement and management ofmaterial risks. The capital adequacy process results in the determination of required capital inrelation to actual and forecasted risk portfolios under applicable regulatory capital methodologies,which include estimated impacts of approved and proposed regulatory changes that will or mayapply to future periods. Key analytical frameworks, which enable the comprehensive assessmentof capital adequacy versus unexpected loss, supplement our base case forecast. These supplementalframeworks include Integrated Stress Testing, as well as an Internal Capital Adequacy Requirementthat builds on internally assessed Economic Capital requirements and management overlays ofadditional reserves that may be required for risks that are not readily quantified. Our capital planningprocess is supported by a robust governance framework, which includes capital management policiesand procedures, capital adequacy metrics and limits, a comprehensive capital contingency plan,

and the active engagement of both legal-entity Boards and senior management in oversight anddecision-making.

Forward-looking assessments of capital adequacy for the Company and for CBNA and CBPA feeddevelopment of capital plans that are submitted to the FRB and to our bank supervisors. We preparethe consolidated CFG capital plan in full compliance with the FRB’s Regulation Y Capital PlanRule, and we participate in the annual CCAR process. The Company also participates in stress testsrequired annually by the CCAR process and semiannually by the Dodd-Frank Act. The FRB mayeither object to our capital plan, in whole or in part, or provide a notice of non-objection. If the FRBobjects to a capital plan, we may not make any capital distribution other than those with respect towhich the FRB has indicated its non-objection.

The Company develops capital plans and conducts routine capital management activities incompliance with internal target operating levels that are established for each regulatory capital ratio.These targets are intended to meet both regulatory and market expectations, while also ensuring anefficient return to shareholders. The Company sets these operating targets to comply with the fullyphased-in Basel III minimum, which includes the capital conservation buffer of 250 basis pointsfor each risk-based capital ratio. (Please refer to the related discussion in the Capital ConservationBuffer section of this document.) To each fully phased-in minimum, CFG adds an internally-definedstress and uncertainty buffer that is calibrated annually. As a result of this conservative approach,the Company and the banks maintain strong capital ratios and are prepared to meet fully phased-in Basel III requirements.

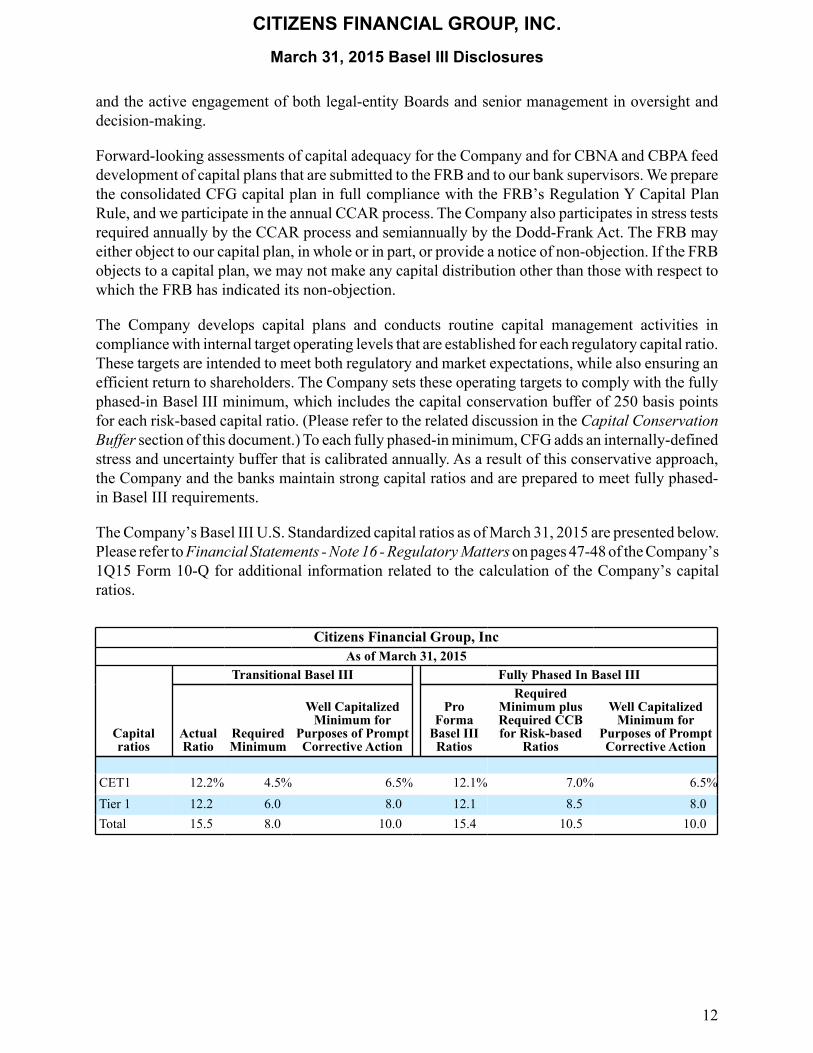

The Company’s Basel III U.S. Standardized capital ratios as of March 31, 2015 are presented below.Please refer to Financial Statements - Note 16 - Regulatory Matters on pages 47-48 of the Company’s1Q15 Form 10-Q for additional information related to the calculation of the Company’s capitalratios.

Citizens Financial Group, IncAs of March 31, 2015

Transitional Basel III Fully Phased In Basel III

Capitalratios

ActualRatio

RequiredMinimum

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

ProForma

Basel IIIRatios

RequiredMinimum plusRequired CCBfor Risk-based

Ratios

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

CET1 12.2% 4.5% 6.5% 12.1% 7.0% 6.5%Tier 1 12.2 6.0 8.0 12.1 8.5 8.0Total 15.5 8.0 10.0 15.4 10.5 10.0

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

12

As of January 1, 2015, CFG and its subsidiary banks transitioned to the Basel III U.S. Standardizedrisk-weighting approach for determining capital requirements related to on- and off-balance sheetexposures, and began the transition to new Basel III regulatory capital definitions. Credit riskexposures are measured by applying fixed risk weights to each exposure, as determined based onthe characteristics of the exposure, such as type of obligor, Organization for Economic Cooperationand Development country risk code, and maturity, among others. Only CFG’s market risk RWAposition is reported using an advanced risk-quantification process. The total RWA calculation isused in determining the Company's capital requirements.

Please refer to the Management’s Discussion and Analysis of Financial Condition and Results ofOperations - Standardized Approach section on pages 89-90 of the Company’s 1Q15 Form 10-Qfor more information regarding the Company’s transition to the fully phased in Basel III U.S.Standardized rules.

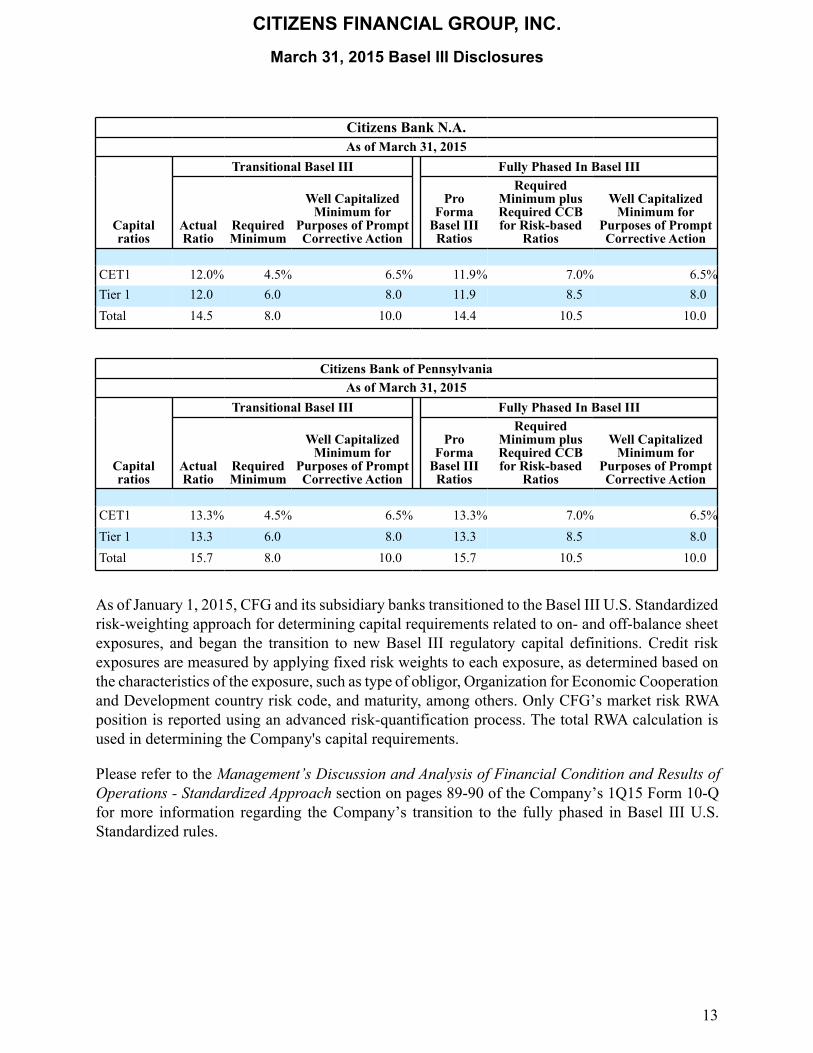

Citizens Bank N.A.As of March 31, 2015

Transitional Basel III Fully Phased In Basel III

Capitalratios

ActualRatio

RequiredMinimum

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

ProForma

Basel IIIRatios

RequiredMinimum plusRequired CCBfor Risk-based

Ratios

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

CET1 12.0% 4.5% 6.5% 11.9% 7.0% 6.5%Tier 1 12.0 6.0 8.0 11.9 8.5 8.0Total 14.5 8.0 10.0 14.4 10.5 10.0

Citizens Bank of PennsylvaniaAs of March 31, 2015

Transitional Basel III Fully Phased In Basel III

Capitalratios

ActualRatio

RequiredMinimum

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

ProForma

Basel IIIRatios

RequiredMinimum plusRequired CCBfor Risk-based

Ratios

Well CapitalizedMinimum for

Purposes of PromptCorrective Action

CET1 13.3% 4.5% 6.5% 13.3% 7.0% 6.5%Tier 1 13.3 6.0 8.0 13.3 8.5 8.0Total 15.7 8.0 10.0 15.7 10.5 10.0

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

13

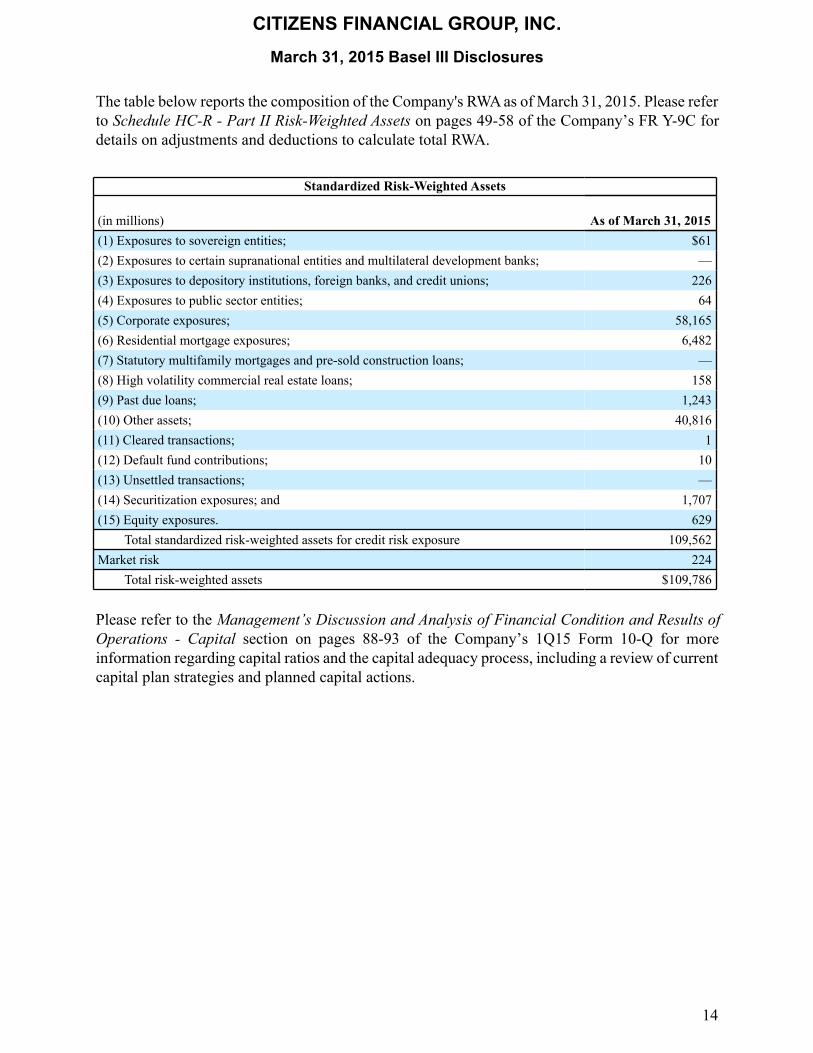

The table below reports the composition of the Company's RWA as of March 31, 2015. Please referto Schedule HC-R - Part II Risk-Weighted Assets on pages 49-58 of the Company’s FR Y-9C fordetails on adjustments and deductions to calculate total RWA.

Please refer to the Management’s Discussion and Analysis of Financial Condition and Results ofOperations - Capital section on pages 88-93 of the Company’s 1Q15 Form 10-Q for moreinformation regarding capital ratios and the capital adequacy process, including a review of currentcapital plan strategies and planned capital actions.

Standardized Risk-Weighted Assets

(in millions) As of March 31, 2015(1) Exposures to sovereign entities; $61(2) Exposures to certain supranational entities and multilateral development banks; —(3) Exposures to depository institutions, foreign banks, and credit unions; 226(4) Exposures to public sector entities; 64(5) Corporate exposures; 58,165(6) Residential mortgage exposures; 6,482(7) Statutory multifamily mortgages and pre-sold construction loans; —(8) High volatility commercial real estate loans; 158(9) Past due loans; 1,243(10) Other assets; 40,816(11) Cleared transactions; 1(12) Default fund contributions; 10(13) Unsettled transactions; —(14) Securitization exposures; and 1,707(15) Equity exposures. 629

Total standardized risk-weighted assets for credit risk exposure 109,562Market risk 224

Total risk-weighted assets $109,786

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

14

Capital Conservation Buffer

The Basel III U.S. Standardized Rule introduces a required CCB of 250 basis points that eachinstitution is expected to maintain over and above the regulatory minimum set for each risk-basedcapital ratio (hence, 4.5% plus 2.5% for CET1, 6.0% plus 2.5% for Tier 1 Risk-Based and 8.0%plus 2.5% for Total Risk-Based). When this CCB has been fully implemented and subject to othersupervisory actions, laws and regulations, any institution failing to maintain 100% of the requiredcapital conservation buffer in any quarter will be restricted as to the maximum amount of eligibleretained income2 that may be distributed as discretionary dividends and executive bonuses.Restrictions on pay-out of eligible net income will continue until the CCB has been fully restored.

The Basel III CCB requirement phases in for CFG between January 1, 2016 and January 1, 2019,consistent with a delayed start for this requirement for non-advanced banks. Beginning in 2019, ifCFG were unable to meet the full CCB requirement for all ratios, its ability to pay planned commondividends could be restricted. However, as noted in Basel III U.S. Standardized Capital Ratiosabove, the Company currently meets the full requirement, reflecting CFG’s conservative approachto setting operating targets, which is discussed in that same section.

__________________2 Eligible retained income is net income for the four calendar quarters preceding the current calendar quarter, net of anydistributions and associated tax effects not already reflected in net income.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

15

Credit Risk

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

16

General Disclosures

Overview

Credit risk represents the potential for loss arising from a customer, counterparty, or issuer failingto perform in accordance with the contractual terms of the obligation. While the majority of ourcredit risk is associated with lending activities, we do engage with other financial counterpartiesfor a variety of purposes including investing, asset and liability management, and trading activities.Given the financial impact of credit risk on our earnings and balance sheet, the assessment, approval,and management of credit risk represents a major part of our overall risk-management responsibility.

Objective

The credit risk management organization is responsible for approving credit transactions, monitoringportfolio performance, identifying problem loans, and ensuring remedial management.

Organizational Structure

Management and oversight of credit risk is the responsibility of both the line of business and thesecond line of defense. The Second Line of Defense, the independent Credit Risk Function, is ledby the CCO who oversees all of our credit risk. The CCO reports to the CRO. The CCO, acting ina manner consistent with Board policies, has responsibility for, among other things, the governanceprocess around policies, procedures, risk acceptance criteria, credit risk appetite, limits, andauthority delegation. The CCO and his team also have responsibility for credit approvals for largeror more risky transactions and oversight of line of business credit risk activities. Reporting to theCCO are the heads of the second line of defense credit functions specializing in Consumer Banking,Business Banking and Commercial Banking, as well as the head of Citizens RestructuringManagement. Each team under these leaders consists of highly experienced credit professionals.The credit risk teams operate independently from the business lines to ensure decisions are notinfluenced by unbalanced objectives. Each team consists of senior credit officers who possessextensive experience structuring and approving loans.

The primary mechanisms used to govern our credit risk function are our consumer and commercialcredit policies. These policies outline the minimum acceptable lending standards that align withour desired risk appetite. Material issues or changes are identified by the individual committees andpresented to the Combined Credit Risk Committee, Executive Risk Committee and the Board forapproval, as required.

Please refer to Management’s Discussion and Analysis of Financial Condition and Results ofOperations - Risk Governance - Credit Risk on pages 122-124 of the Company’s 2014 Form 10-Kfor more information on credit risk governance.

The Company’s investment securities portfolio includes U.S. Treasury and agency securities, agencymortgage-backed securities, and non-agency mortgage-backed securities. The most importantelement management relies on when assessing credit risk for U.S. Treasury and agency securities

and agency mortgage-backed securities is the guarantee of the Federal Government or one of itsagencies. When applicable, the Company considers geography as a factor when managing itsinvestments in securities issued by state and political subdivisions; the Company did not holdmaterial positions in such securities as of March 31, 2015. The credit risk for non-agency mortgagebacked securities is assessed based on senior to subordinated credit support levels and an analysisof the bond’s underlying collateral characteristics. As a secondary measure, ratings by NRSRO areconsidered, but not solely relied upon, to determine the creditworthiness of the issue.

The Company’s credit-related accounting policies are presented in Financial Statements andSupplementary Data - Note 1 - Significant Accounting Policies on pages 156 - 163 of the Company’s2014 Form 10-K.

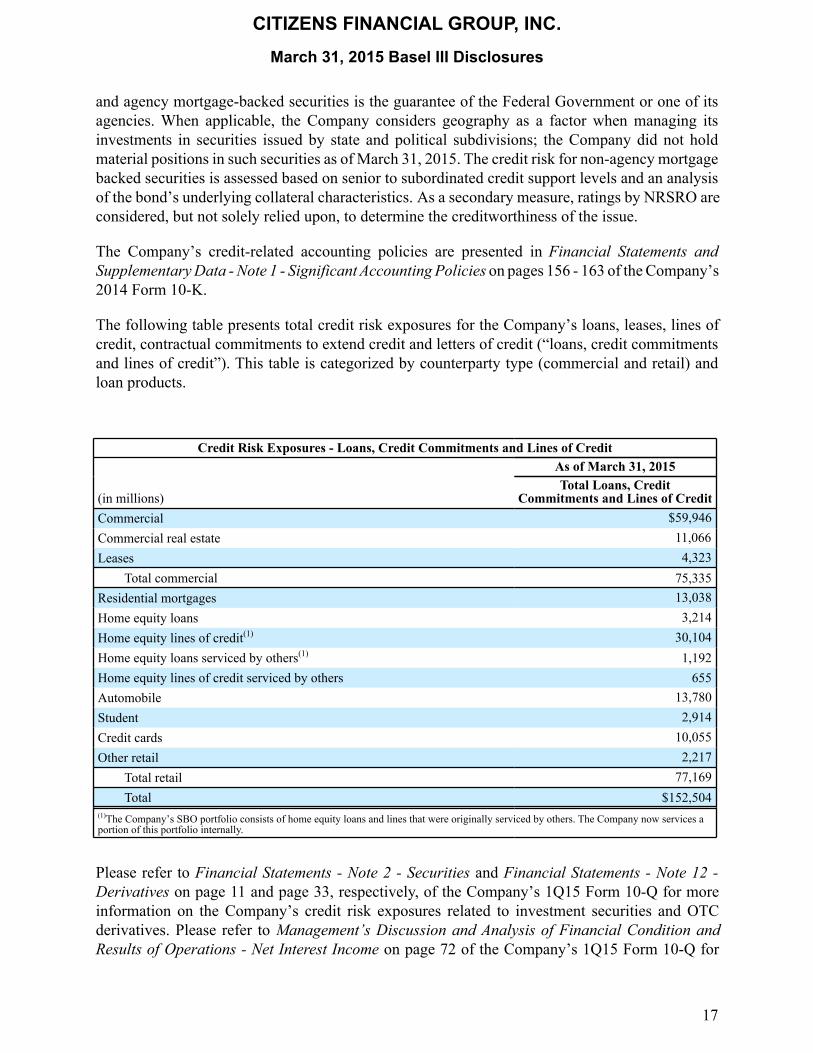

The following table presents total credit risk exposures for the Company’s loans, leases, lines ofcredit, contractual commitments to extend credit and letters of credit (“loans, credit commitmentsand lines of credit”). This table is categorized by counterparty type (commercial and retail) andloan products.

Please refer to Financial Statements - Note 2 - Securities and Financial Statements - Note 12 -Derivatives on page 11 and page 33, respectively, of the Company’s 1Q15 Form 10-Q for moreinformation on the Company’s credit risk exposures related to investment securities and OTCderivatives. Please refer to Management’s Discussion and Analysis of Financial Condition andResults of Operations - Net Interest Income on page 72 of the Company’s 1Q15 Form 10-Q for

Credit Risk Exposures - Loans, Credit Commitments and Lines of CreditAs of March 31, 2015

(in millions)Total Loans, Credit

Commitments and Lines of CreditCommercial $59,946Commercial real estate 11,066Leases 4,323

Total commercial 75,335Residential mortgages 13,038Home equity loans 3,214Home equity lines of credit(1) 30,104Home equity loans serviced by others(1) 1,192Home equity lines of credit serviced by others 655Automobile 13,780Student 2,914Credit cards 10,055Other retail 2,217

Total retail 77,169Total $152,504

(1)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

17

average balances of the Company’s loans and investment securities. The average credit risk exposurerelated to the Company’s OTC derivatives as of March 31, 2015 was $724 million.

Please refer to Financial Statements- Note 13 - Commitments and Contingencies on pages 36-39of the Company’s 1Q15 Form 10-Q for more information on the credit risk exposure related to ouroff-balance sheet commitments (including contractual commitments to extend credit, lines of creditand letters of credit). The average credit risk exposure associated with the Company’s off-balancesheet credit commitments and lines of credit as of March 31, 2015 was $58.0 billion.

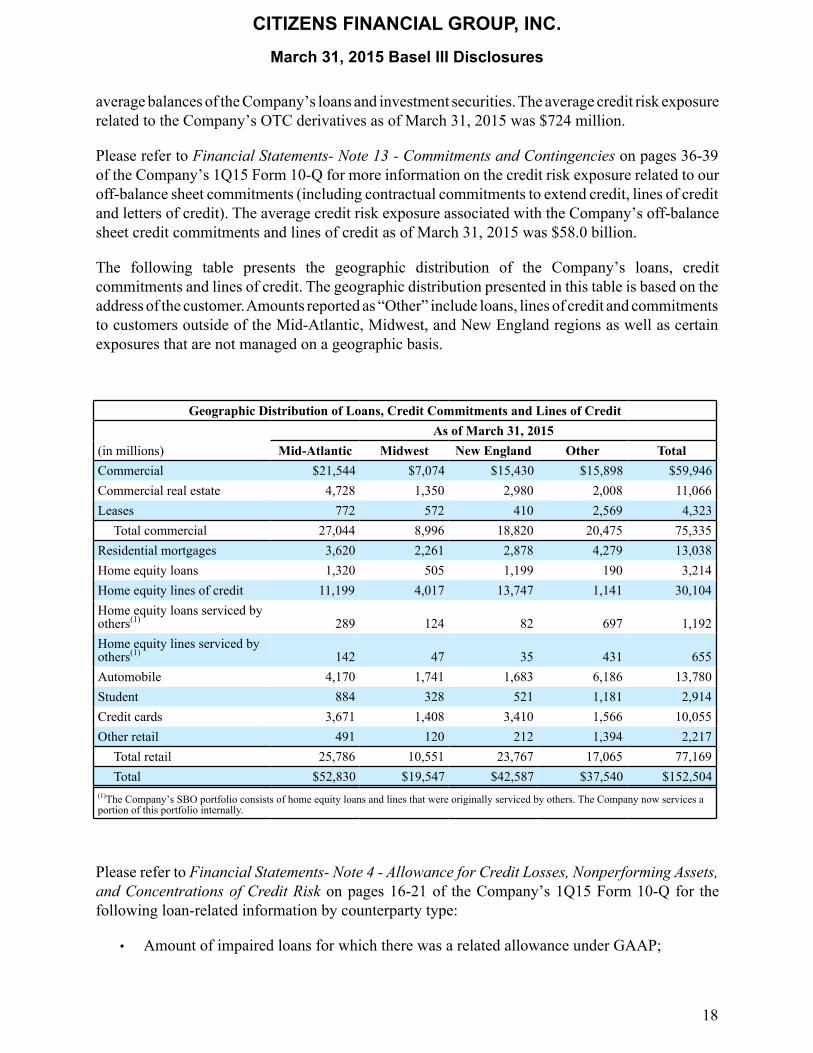

The following table presents the geographic distribution of the Company’s loans, creditcommitments and lines of credit. The geographic distribution presented in this table is based on theaddress of the customer. Amounts reported as “Other” include loans, lines of credit and commitmentsto customers outside of the Mid-Atlantic, Midwest, and New England regions as well as certainexposures that are not managed on a geographic basis.

Please refer to Financial Statements- Note 4 - Allowance for Credit Losses, Nonperforming Assets,and Concentrations of Credit Risk on pages 16-21 of the Company’s 1Q15 Form 10-Q for thefollowing loan-related information by counterparty type:

• Amount of impaired loans for which there was a related allowance under GAAP;

Geographic Distribution of Loans, Credit Commitments and Lines of CreditAs of March 31, 2015

(in millions) Mid-Atlantic Midwest New England Other TotalCommercial $21,544 $7,074 $15,430 $15,898 $59,946Commercial real estate 4,728 1,350 2,980 2,008 11,066Leases 772 572 410 2,569 4,323

Total commercial 27,044 8,996 18,820 20,475 75,335Residential mortgages 3,620 2,261 2,878 4,279 13,038Home equity loans 1,320 505 1,199 190 3,214Home equity lines of credit 11,199 4,017 13,747 1,141 30,104Home equity loans serviced byothers(1) 289 124 82 697 1,192Home equity lines serviced byothers(1) 142 47 35 431 655Automobile 4,170 1,741 1,683 6,186 13,780Student 884 328 521 1,181 2,914Credit cards 3,671 1,408 3,410 1,566 10,055Other retail 491 120 212 1,394 2,217

Total retail 25,786 10,551 23,767 17,065 77,169Total $52,830 $19,547 $42,587 $37,540 $152,504

(1)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

18

• Amount of impaired loans for which there was no related allowance under GAAP; and• ALLL balances and related charge-off information

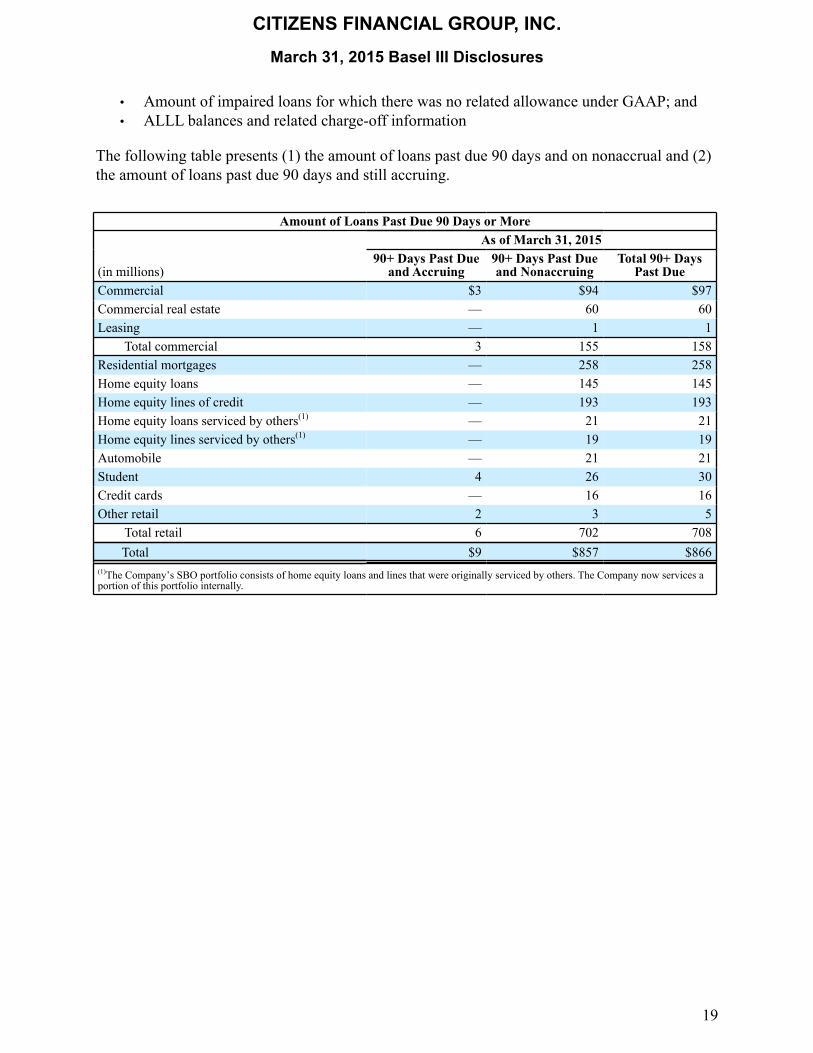

The following table presents (1) the amount of loans past due 90 days and on nonaccrual and (2)the amount of loans past due 90 days and still accruing.

Amount of Loans Past Due 90 Days or MoreAs of March 31, 2015

(in millions)90+ Days Past Due

and Accruing90+ Days Past Dueand Nonaccruing

Total 90+ DaysPast Due

Commercial $3 $94 $97Commercial real estate — 60 60Leasing — 1 1

Total commercial 3 155 158Residential mortgages — 258 258Home equity loans — 145 145Home equity lines of credit — 193 193Home equity loans serviced by others(1) — 21 21Home equity lines serviced by others(1) — 19 19Automobile — 21 21Student 4 26 30Credit cards — 16 16Other retail 2 3 5

Total retail 6 702 708Total $9 $857 $866

(1)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

19

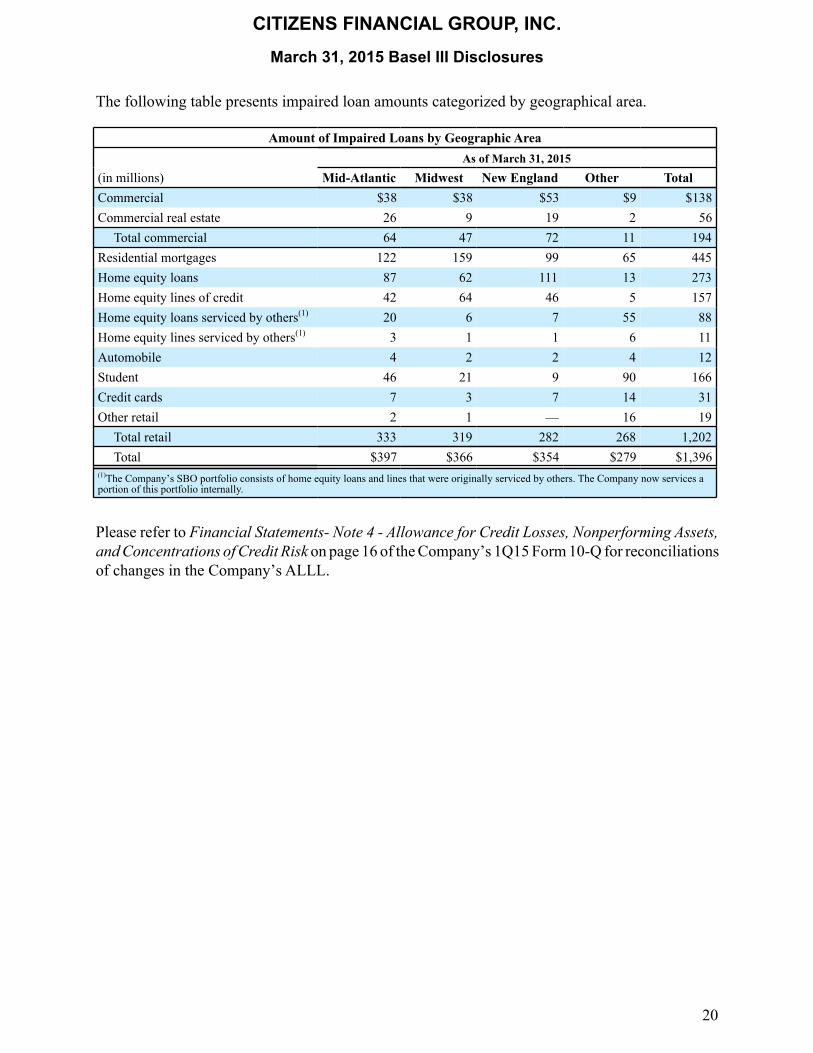

The following table presents impaired loan amounts categorized by geographical area.

Please refer to Financial Statements- Note 4 - Allowance for Credit Losses, Nonperforming Assets,and Concentrations of Credit Risk on page 16 of the Company’s 1Q15 Form 10-Q for reconciliationsof changes in the Company’s ALLL.

Amount of Impaired Loans by Geographic AreaAs of March 31, 2015

(in millions) Mid-Atlantic Midwest New England Other TotalCommercial $38 $38 $53 $9 $138Commercial real estate 26 9 19 2 56

Total commercial 64 47 72 11 194Residential mortgages 122 159 99 65 445Home equity loans 87 62 111 13 273Home equity lines of credit 42 64 46 5 157Home equity loans serviced by others(1) 20 6 7 55 88Home equity lines serviced by others(1) 3 1 1 6 11Automobile 4 2 2 4 12Student 46 21 9 90 166Credit cards 7 3 7 14 31Other retail 2 1 — 16 19

Total retail 333 319 282 268 1,202Total $397 $366 $354 $279 $1,396

(1)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

20

The following table presents a summary of loans and leases by remaining maturity or repricingdate.

Loans by Remaining Maturity or Repricing DateAs of March 31, 2015

(in millions)One Year or

Less (1)

Over One YearThrough Five

Years Over Five Years TotalCommercial $27,718 $2,810 $1,791 $32,319Commercial real estate 7,450 237 176 7,863Leasing 604 2,032 1,234 3,870

Total commercial 35,772 5,079 3,201 44,052

Residential mortgages 1,639 1,102 9,332 12,073Home equity loans 688 529 1,995 3,212Home equity lines of credit 10,756 2,900 1,471 15,127Home equity loans serviced by others(2) — 27 1,165 1,192Home equity lines serviced by others(2) 544 — — 544Automobile 108 6,499 6,572 13,179Student 9 94 2,749 2,852Credit cards 1,445 184 — 1,629Other retail 487 130 393 1,010

Total retail 15,676 11,465 23,677 50,818Total $51,448 $16,544 $26,878 $94,870

(1) Loans held for sale are included in One Year or Less category(2)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

21

The following table presents a summary of credit commitments and lines of credit by remainingmaturity or repricing date.

Please refer to Financial Statements- Note 2 - Securities on page 13 of the Company’s 1Q15 Form10-Q for a summary of securities by contractual maturity.

Please refer to Schedule HC-R - Part II Risk-Weighted Assets on page 59 of the Company’s FRY-9C for a summary of OTC derivative notional amounts by remaining maturity.

Credit Commitments and Lines of Credit by Remaining Maturity or Repricing DateAs of March 31, 2015

(in millions) One Year or LessGreater than

One Year TotalUnfunded commitments and lines of credit (1)

Commercial and commercial real estate $7,592 $20,828 $28,420Leases 310 143 453

Total commercial 7,902 20,971 28,873Residential mortgages 965 — 965Home equity loans 1 — 1Home equity lines of credit 946 14,033 14,979Home equity lines serviced by others(2) 111 — 111Automobile 600 — 600Student 62 — 62Credit cards 8,426 — 8,426Other retail 749 458 1,207

Total retail 11,860 14,491 26,351Total unfunded commitments and lines of credit $19,762 $35,462 $55,224

Letters of credit (1)

Financial standby $996 $1,296 $2,292Performance 55 5 60Commercial 26 32 58

Total letters of credit 1,077 1,333 2,410

Total credit commitments and lines of credit 20,839 36,795 57,634(1) Net of participations sold(2)The Company’s SBO portfolio consists of home equity loans and lines that were originally serviced by others. The Company now services aportion of this portfolio internally.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

22

Counterparty Credit Risk-Related Disclosures

Counterparty exposure arises primarily from the OTC derivative transactions in the Company’scustomer and institutional derivative portfolios. The amount of this exposure depends on the valueof underlying market factors (e.g., interest rates), which can be volatile and uncertain in nature.

Counterparty exposure also arises (to a lesser extent) from the Company’s securities lending andborrowing activities, which includes entering into repurchase agreements.

The customer derivatives portfolio consists of interest rate swap agreements and option contractsthat are transacted to meet the financing needs of the Company’s customers. Offsetting swap andcap agreements are simultaneously transacted on a bi-lateral basis with dealers and cleared withcentral counterparties, on terms consistent with institutional trades described below, to effectivelyeliminate the Company’s market risk associated with customer derivative products. The customerderivative portfolio also includes foreign exchange contracts that are entered into on behalf ofcustomers for the purpose of hedging exposure related to cash orders and loans and depositsdenominated in foreign currencies. Customer trades are primarily unsecured and are not subject todaily margin or posting of financial collateral. These trades are commonly executed concurrentlywith new loan transactions, with any business collateral received from a counterparty being appliedto both the derivative and loan. Accordingly, the underwriting process for establishing customerderivative credit limits is equivalent to the process used for corporate loan exposure. These limitsare established based on PFE using an Add-On approach, which involves multiplying the tradenotional amount by a risk factor. The Company manages the credit risk of its customer derivativepositions by diversifying its positions among various counterparties, and, in certain cases,transferring the counterparty credit risk related to interest rate swaps to third parties through theuse of risk participation agreements. When measuring the fair value of its customer derivativeportfolio for U.S. GAAP financial reporting purposes, the Company includes a CVA that reflectsthe credit quality of the swap counterparty. Please refer to Financial Statements- Note 15 - FairValue Measurements on pages 40-47 of the Company’s 1Q15 Form 10-Q for more information onthe Company’s valuation methodologies.

The institutional derivative portfolio primarily consists of interest rate swap agreements that areused to hedge the interest rate risk associated with the Company’s loans and financing liabilities(i.e., borrowed funds, deposits, etc.). Institutional swaps and swaps executed to eliminate the marketrisk associated with our customer derivative products include bi-lateral trades with dealers andcleared trades with central counterparties. These trades are subject to daily margin requirementsand posting of financial collateral based on pre-defined “posting thresholds”. Posting thresholdsrepresent the amount of exposure that counterparties are willing to accept on an unsecured basis.Collateral is posted only when the market value of any outstanding swaps exceeds that threshold.Changes in the Company’s own creditworthiness do not generally impact the amount of collateralposted given zero thresholds have become the market convention. The majority of the Company’sbi-lateral derivative trades have been transacted with our parent company, RBS; such trades aresubject to guidance limits monitored by RBS Group Treasury. Bi-lateral trades with dealers andcleared trades with central counterparties are subject to counterparty credit limits for initial marginrequirements where collateral is posted, but not segregated.

The Company’s repurchase agreements are typically short-term transactions (e.g., overnight), butthey may be extended to longer terms-to-maturity. Such transactions are fully collateralized and areaccounted for as secured borrowings on the Company’s financial statements. Counterparty creditlimits are established to monitor the Company’s over-collateralized position. When permitted by

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

23

GAAP, the Company offsets the short-term receivables associated with its reverse repurchaseagreements with the short-term payables associated with its repurchase agreements.

Counterparty credit exposures are monitored daily for counterparties with an established CSA toassure collateral levels are appropriately sized to cover risk. Any collateral received from thirdparties is managed by the Company and held pursuant to the terms of the governing CSA agreementfor the counterparty, in either a tri-party custodial, segregated or an omnibus account. Collateraltypes that are “acceptable” (as defined in the CSA) generally include the following:

Please refer to Financial Statements - Note 12 - Derivatives on page 33 of the Company’s 1Q15Form 10-Q for fair value of the Company’s derivative transactions. This disclosure presents thesefair values both on a gross and a net basis. As of March 31, 2015, the Company held an immaterialamount of collateral from third parties. Therefore, the net basis presented represents the impact oflegally enforceable master netting agreements.

Please refer to Financial Statements- Note 2 - Securities on page 14 of the Company’s 1Q15 Form 10-Q for the gross and net carrying values of the Company’s repurchase agreements. Please refer to Financial Statements- Note 15 - Fair Value Measurements on page 47 of the Company’s 1Q15 Form 10-Q for the fair value of the Company’s repurchase agreements.

Acceptable collateral types Valuation %Cash 100%

Treasury Bills Negotiable debt obligations issued by the U.S. Treasury Department havinga remaining maturity of not more than one year.

98%

Treasury Notes Negotiable debt obligations issued by the U.S. Treasury Department havinga remaining maturity of more than one year but not more than 10 years.

98%

Treasury Bonds Negotiable debt obligations issued by the U.S. Treasury Department havinga remaining maturity of more than 10 years but not more than 30 years.

98%

Agency Securities Negotiable debt obligations of the FNMA, FHLMC, FHLB, or FFCBhaving a remaining maturity of not more than 30 years.

92%

FHLMC Certificates Mortgage participation certificates issued by FHLMC evidencingundivided interests or participations in pools of first lien conventional orFHA/VA residential mortgages or deeds of trust, guaranteed by FHLMC,and having a remaining maturity of not more than 30 years.

92%

FNMA Certificates Mortgage-backed pass-through certificates issued by FNMA evidencingundivided interests in pools of first lien mortgages or deeds of trust onresidential properties, guaranteed by FNMA, and having a remainingmaturity of not more than 30 years.

92%

GNMA Certificates Mortgage-backed pass-through certificates issued by private entities,evidencing undivided interests in pools of first lien mortgages or deeds oftrust on single family residences, guaranteed by the GNMA with the fullfaith and credit of the United States, and having a remaining maturity ofnot more than 30 years.

92%

Other EligibleCollateral

With respect to a party, as may be agreed in writing between the parties forpurposes of this Annex, together with the applicable Valuation Percentage.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

24

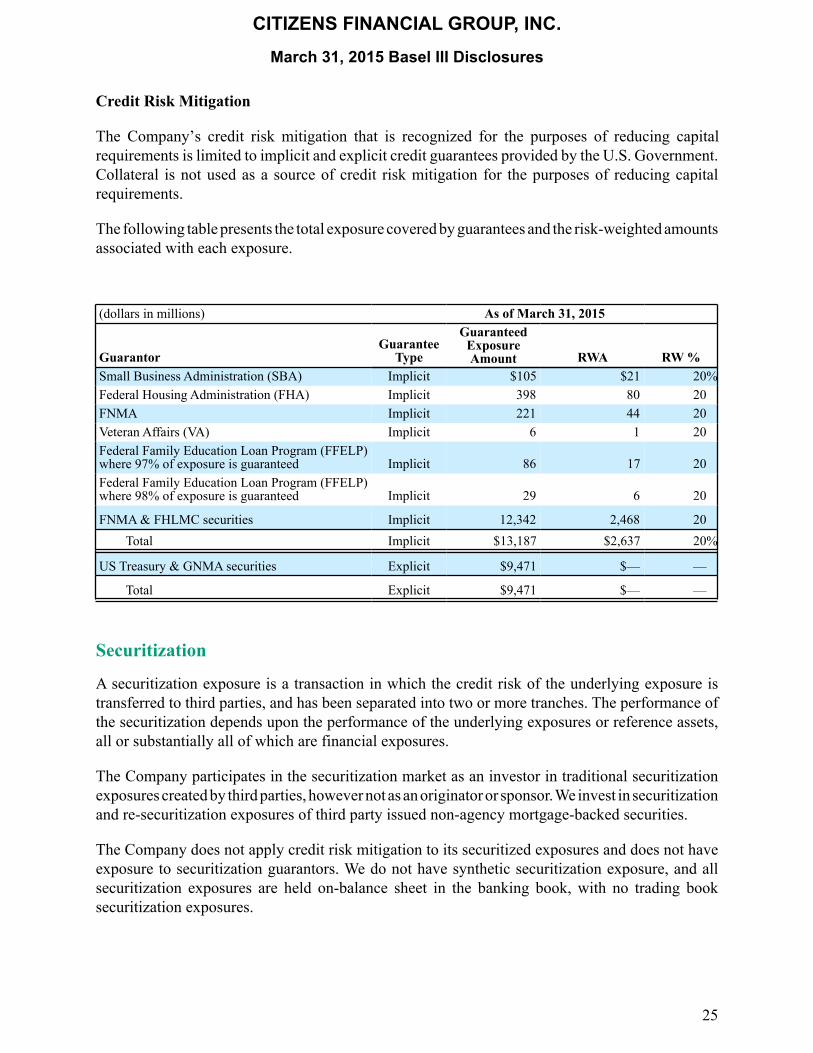

Credit Risk Mitigation

The Company’s credit risk mitigation that is recognized for the purposes of reducing capitalrequirements is limited to implicit and explicit credit guarantees provided by the U.S. Government.Collateral is not used as a source of credit risk mitigation for the purposes of reducing capitalrequirements.

The following table presents the total exposure covered by guarantees and the risk-weighted amountsassociated with each exposure.

(dollars in millions) As of March 31, 2015

GuarantorGuarantee

Type

GuaranteedExposureAmount RWA RW %

Small Business Administration (SBA) Implicit $105 $21 20%Federal Housing Administration (FHA) Implicit 398 80 20FNMA Implicit 221 44 20Veteran Affairs (VA) Implicit 6 1 20Federal Family Education Loan Program (FFELP)where 97% of exposure is guaranteed Implicit 86 17 20Federal Family Education Loan Program (FFELP)where 98% of exposure is guaranteed Implicit 29 6 20

FNMA & FHLMC securities Implicit 12,342 2,468 20Total Implicit $13,187 $2,637 20%

US Treasury & GNMA securities Explicit $9,471 $— —

Total Explicit $9,471 $— —

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

25

Securitization

A securitization exposure is a transaction in which the credit risk of the underlying exposure istransferred to third parties, and has been separated into two or more tranches. The performance ofthe securitization depends upon the performance of the underlying exposures or reference assets,all or substantially all of which are financial exposures.

The Company participates in the securitization market as an investor in traditional securitizationexposures created by third parties, however not as an originator or sponsor. We invest in securitizationand re-securitization exposures of third party issued non-agency mortgage-backed securities.

The Company does not apply credit risk mitigation to its securitized exposures and does not haveexposure to securitization guarantors. We do not have synthetic securitization exposure, and allsecuritization exposures are held on-balance sheet in the banking book, with no trading booksecuritization exposures.

The Company calculates the regulatory capital requirement for securitization exposure inaccordance with the Basel III U.S. Standardized Approach Hierarchy of approaches framework.The SSFA is used to determine RWA for its securitization exposures. The SSFA framework considersthe Company's seniority in the securitization structure and risk factors inherent in the underlyingassets.

Risk Management

The risks related to securitization and re-securitization positions are managed in accordance withthe Company’s investment, credit, and interest rate risk management policies. Please refer toManagement’s Discussion and Analysis of Financial Condition and Results of Operations - RiskGovernance on pages 120-126 of the Company’s 2014 Form 10-K for more information on theCompany’s credit risk and interest rate risk (i.e., non-trading risk) governance.

For each securitization and re-securitization position, we perform due diligence on the creditworthiness of each position prior to entering into that position. The Company’s due diligenceprocedures are designed to provide a comprehensive understanding of the features that wouldmaterially affect the performance of a securitization, and are commensurate with the complexityof each securitization or re-securitization position held.

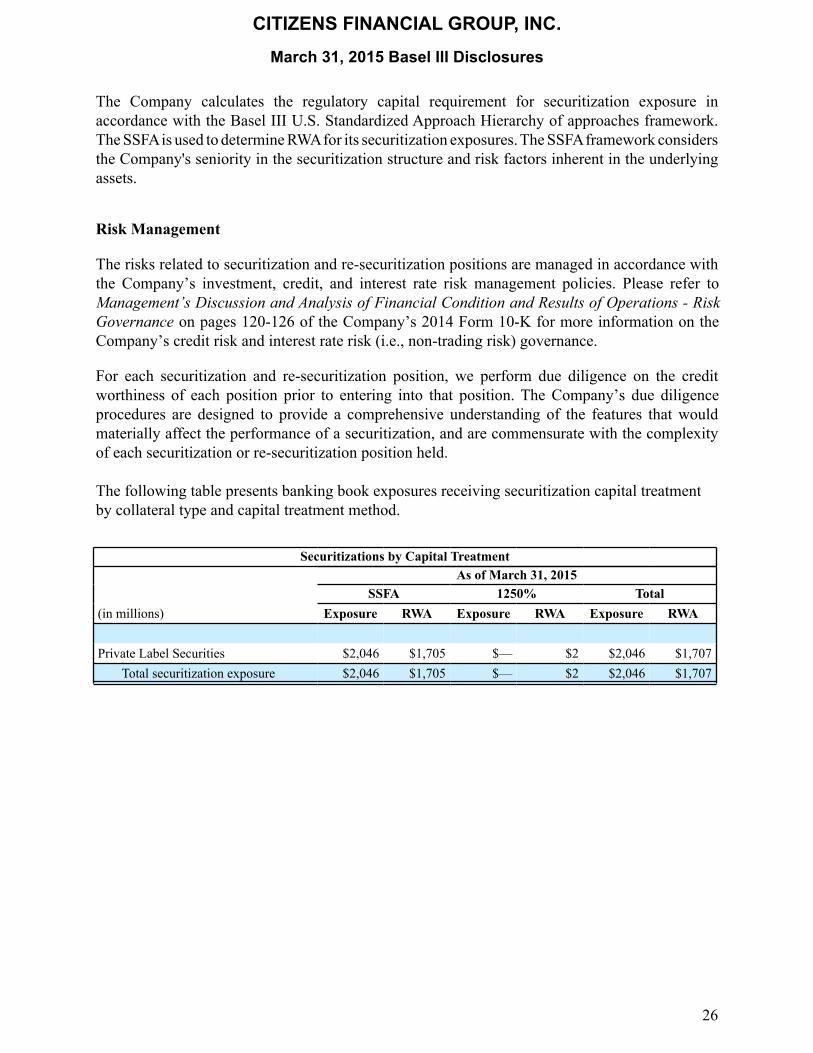

The following table presents banking book exposures receiving securitization capital treatmentby collateral type and capital treatment method.

Securitizations by Capital TreatmentAs of March 31, 2015

SSFA 1250% Total(in millions) Exposure RWA Exposure RWA Exposure RWA

Private Label Securities $2,046 $1,705 $— $2 $2,046 $1,707Total securitization exposure $2,046 $1,705 $— $2 $2,046 $1,707

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

26

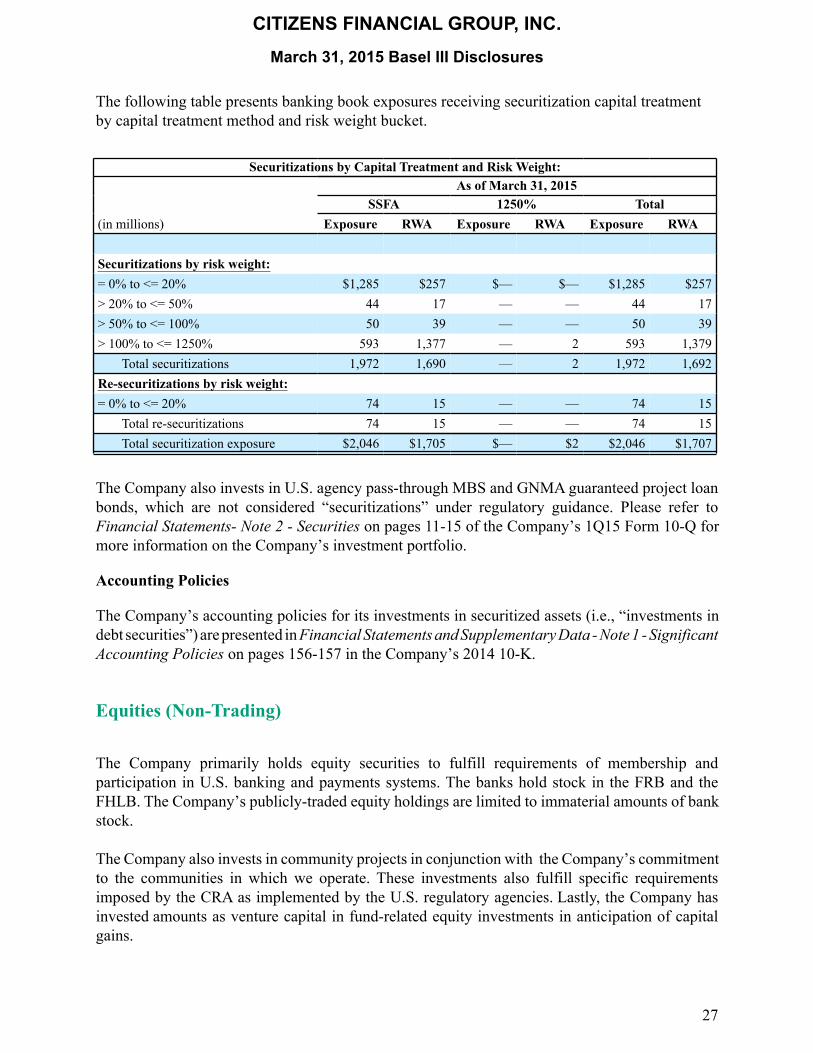

The following table presents banking book exposures receiving securitization capital treatmentby capital treatment method and risk weight bucket.

The Company also invests in U.S. agency pass-through MBS and GNMA guaranteed project loanbonds, which are not considered “securitizations” under regulatory guidance. Please refer toFinancial Statements- Note 2 - Securities on pages 11-15 of the Company’s 1Q15 Form 10-Q formore information on the Company’s investment portfolio.

Accounting Policies

The Company’s accounting policies for its investments in securitized assets (i.e., “investments indebt securities”) are presented in Financial Statements and Supplementary Data - Note 1 - SignificantAccounting Policies on pages 156-157 in the Company’s 2014 10-K.

Securitizations by Capital Treatment and Risk Weight:As of March 31, 2015

SSFA 1250% Total(in millions) Exposure RWA Exposure RWA Exposure RWA

Securitizations by risk weight:= 0% to <= 20% $1,285 $257 $— $— $1,285 $257> 20% to <= 50% 44 17 — — 44 17> 50% to <= 100% 50 39 — — 50 39> 100% to <= 1250% 593 1,377 — 2 593 1,379

Total securitizations 1,972 1,690 — 2 1,972 1,692Re-securitizations by risk weight:= 0% to <= 20% 74 15 — — 74 15

Total re-securitizations 74 15 — — 74 15Total securitization exposure $2,046 $1,705 $— $2 $2,046 $1,707

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

27

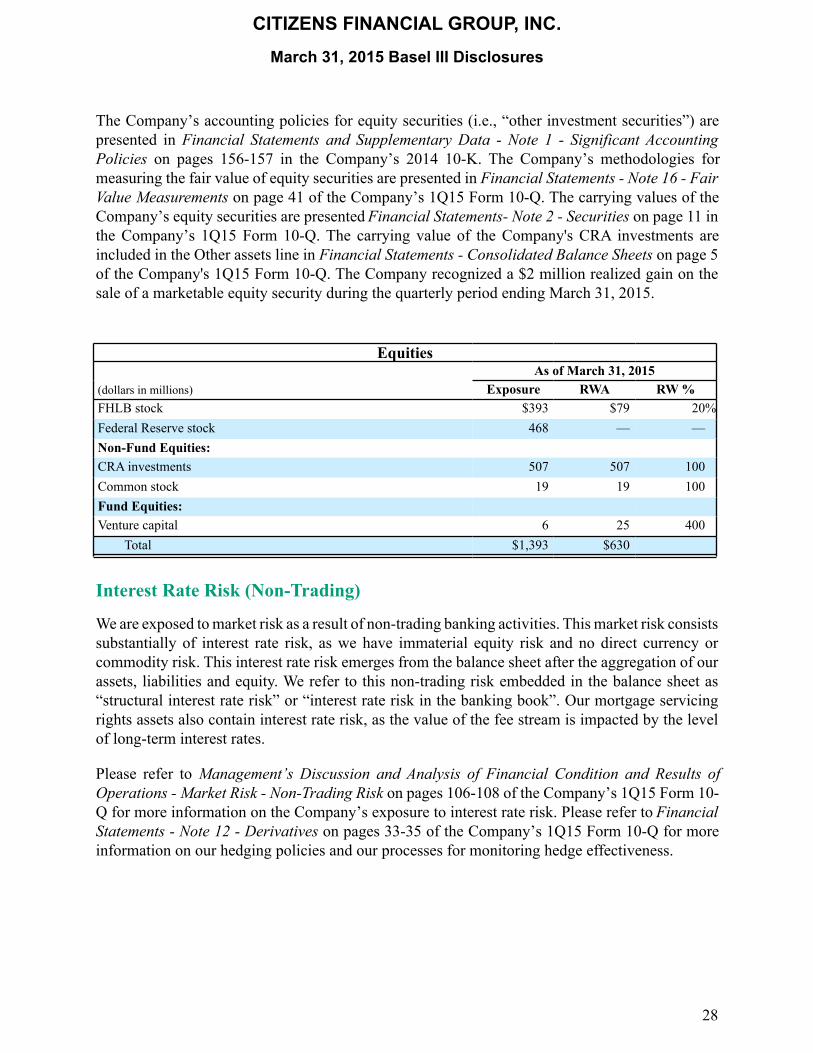

Equities (Non-Trading)

The Company primarily holds equity securities to fulfill requirements of membership andparticipation in U.S. banking and payments systems. The banks hold stock in the FRB and theFHLB. The Company’s publicly-traded equity holdings are limited to immaterial amounts of bankstock.

The Company also invests in community projects in conjunction with the Company’s commitmentto the communities in which we operate. These investments also fulfill specific requirementsimposed by the CRA as implemented by the U.S. regulatory agencies. Lastly, the Company hasinvested amounts as venture capital in fund-related equity investments in anticipation of capitalgains.

The Company’s accounting policies for equity securities (i.e., “other investment securities”) arepresented in Financial Statements and Supplementary Data - Note 1 - Significant AccountingPolicies on pages 156-157 in the Company’s 2014 10-K. The Company’s methodologies formeasuring the fair value of equity securities are presented in Financial Statements - Note 16 - FairValue Measurements on page 41 of the Company’s 1Q15 Form 10-Q. The carrying values of theCompany’s equity securities are presented Financial Statements- Note 2 - Securities on page 11 inthe Company’s 1Q15 Form 10-Q. The carrying value of the Company's CRA investments areincluded in the Other assets line in Financial Statements - Consolidated Balance Sheets on page 5of the Company's 1Q15 Form 10-Q. The Company recognized a $2 million realized gain on thesale of a marketable equity security during the quarterly period ending March 31, 2015.

EquitiesAs of March 31, 2015

(dollars in millions) Exposure RWA RW %FHLB stock $393 $79 20%Federal Reserve stock 468 — —Non-Fund Equities:CRA investments 507 507 100Common stock 19 19 100Fund Equities:Venture capital 6 25 400

Total $1,393 $630

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

28

Interest Rate Risk (Non-Trading)

We are exposed to market risk as a result of non-trading banking activities. This market risk consistssubstantially of interest rate risk, as we have immaterial equity risk and no direct currency orcommodity risk. This interest rate risk emerges from the balance sheet after the aggregation of ourassets, liabilities and equity. We refer to this non-trading risk embedded in the balance sheet as“structural interest rate risk” or “interest rate risk in the banking book”. Our mortgage servicingrights assets also contain interest rate risk, as the value of the fee stream is impacted by the levelof long-term interest rates.

Please refer to Management’s Discussion and Analysis of Financial Condition and Results ofOperations - Market Risk - Non-Trading Risk on pages 106-108 of the Company’s 1Q15 Form 10-Q for more information on the Company’s exposure to interest rate risk. Please refer to FinancialStatements - Note 12 - Derivatives on pages 33-35 of the Company’s 1Q15 Form 10-Q for moreinformation on our hedging policies and our processes for monitoring hedge effectiveness.

Market Risk

We are exposed to market risk price volatility across a select range of interest rates, foreign exchangerates and credit spreads through our client facilitation activities covering interest rate derivatives,foreign exchange products and secondary loans. These trading activities are covered under theMarket Risk Rule and are conducted through our two banking subsidiaries, CBNA and CBPA.

As of March 31, 2015, our market risk RWA stood at $224 million, reflecting general interest raterisk and specific risk. Our specific risk is not modeled through the VaR based process and thus aspecific risk add-on is calculated under a standardized measurement method. We do not calculateincremental risk or comprehensive risk, as we take a standardized specific risk add-on and we donot participate in correlation trading related activities.

For further discussion related to market risk governance, risk measurements, VaR methodology andvalidation, and regulatory capital, please refer to the Management’s Discussion and Analysis ofFinancial Condition and Results of Operations - Risk Governance section on pages 120-124 of theCompany’s 2014 Form 10-K and Management’s Discussion and Analysis of Financial Conditionand Results of Operations - Market Risk section on pages 108-111 of the Company’s 1Q15 Form10-Q.

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

29

Appendix 1 – Citizens Financial Group Basel III Disclosures Matrix

The disclosures required by the U.S. Basel III final rule3 are listed below. Most of these disclosures have been included inother financial reporting documents, and some in this report. This matrix provides a reference to the location of eachrequired disclosure.

__________________3 Code of Federal Regulations, Part 217 - Capital Adequacy of Bank Holding Companies, Savings and Loan Holding Companies, and State Member Banks (RegulationQ).

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

30

General Disclosure Requirements and Scope of Application

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

§217.63DISCLOSURES BYBOARD-REGULATEDINSTITUTIONS(INTRODUCTION)

(a) A Board-regulated institution must publicly disclose eachquarter the following:

(1) Common equity tier 1 capital, additional tier 1 capital,tier 2 capital, tier 1 and total capital ratios, includingthe regulatory capital elements and all the regulatoryadjustments and deductions needed to calculate thenumerator of such ratios;

Pg. 9-11

(2) Total risk-weighted assets, including the differentregulatory adjustments and deductions needed tocalculate total RWA;

Pg. 14Sch. HC-R Part IIPg. 49-58

(3) Regulatory capital ratios during any transition periods,including a description of all the regulatory capitalelements and all regulatory adjustments anddeductions needed to calculate the numerator anddenominator of each capital ratio during any transitionperiod; and

Pg. 12-13

(4) A reconciliation of regulatory capital elements as theyrelate to its balance sheet in any audited consolidatedfinancial statements.

Pg. 11

§217.63 TABLE 1 —SCOPE OFAPPLICATION

(a) The name of the top corporate entity in the group to whichsubpart D (Risk Weighted Assets - Standardized Approach) ofthis part applies.

Pg. 5

(b) A brief description of the differences in the basis forconsolidating entities for accounting and regulatory purposes,with a description of those entities:

(1) That are fully consolidated;

(2) That are deconsolidated and deducted from total capital;

(3) For which the total capital requirement is deducted; and

(4) That are neither consolidated nor deducted (forexample, where the investment in the entity is assigneda risk weight in accordance with this subpart).

Pg. 5 Pg. 156

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

(c) Any restrictions, or other major impediments, on transfer offunds or total capital within the group.

Pg. 5-6

(d) The aggregate amount of surplus capital of insurancesubsidiaries included in the total capital of the consolidatedgroup.

Pg. 6

(e) The aggregate amount by which actual total capital is lessthan the minimum total capital requirement in all subsidiaries,with total capital requirements and the name(s) of thesubsidiaries with such deficiencies.

N/A

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

31

Capital Structure and Adequacy

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

§217.63 TABLE 2 —CAPITALSTRUCTURE

(a) Summary information on the terms and conditions of the mainfeatures of all regulatory capital instruments.

Pg. 9-11

(b) The amount of common equity tier 1 capital, with separatedisclosure of:

Pg. 9-11

(c) The amount of tier 1 capital, with separate disclosure of:

(1) Additional tier 1 capital elements, including additionaltier 1 capital instruments and tier 1 minority interest notincluded in common equity tier 1 capital; and

(2) Regulatory deductions and adjustments made to tier 1capital

Pg. 9-11

(d) The amount of total capital, with separate disclosure of:

(1) Tier 2 capital elements, including tier 2 capitalinstruments and total capital minority interest notincluded in tier 1 capital; and

(2) Regulatory deductions and adjustments made to totalcapital.

Pg. 9-11

§217.63 TABLE 3 —CAPITALADEQUACY

(a) A summary discussion of the Bank’s approach to assessingthe adequacy of its capital to support current and futureactivities.

Pg. 11-12

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

(b) Risk-weighted assets for:

(1) Exposures to sovereign entities;

(2) Exposures to certain supranational entities and MDBs;

(3) Exposures to depository institutions, foreign banks, andcredit unions;

(4) Exposures to PSEs;

(5) Corporate exposures;

(6) Residential mortgage exposures;

(7) Statutory multifamily mortgages and pre-soldconstruction loans;

(8) HVCRE loans;

(9) Past due loans;

(10) Other assets;

(11) Cleared transactions;

(12) Default fund contributions;

(13) Unsettled transactions;

(14) Securitization exposures; and

(15) Equity exposures.

Pg. 14

(c) Standardized market risk-weighted assets as calculated undersubpart F of this part.

Pg. 14

(d) Common equity tier 1, tier 1 and total risk-based capitalratios:

(1) For the top consolidated group; and

(2) For each depository institution subsidiary

Pg. 12-13

(e) Total standardized risk-weighted assets Pg. 14

§217.63 TABLE 4 —CAPITALCONSERVATIONBUFFER

(a) At least quarterly, the Bank must calculate and publiclydisclose the capital conservation buffer as described under §217.11.

Pg. 15

(b) At least quarterly, Bank must calculate and publicly disclosethe eligible retained income of the Bank, as described under §217.11.

Pg. 15

(c) At least quarterly, the Bank must calculate and publiclydisclose any limitations it has on capital distributions anddiscretionary bonus payments resulting from the capitalconservation buffer framework described under § 217.11,including the maximum payout amount for the quarter.

Pg. 15

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

32

Credit Risk

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

§217.63 TABLE 5 —CREDIT RISK:GENERALDISCLOSURES

• General qualitative disclosure requirement. For each separaterisk area described in Tables 5 through 10, the Board-regulated institution must describe its risk managementobjectives and policies, including: Strategies and processes;the structure and organization of the relevant risk managementfunction; the scope and nature of risk reporting and/ormeasurement systems; policies for hedging and/or mitigatingrisk and strategies and processes for monitoring the continuingeffectiveness of hedges/mitigants.

Pg. 16-17 Pg.122-124

(a) The general qualitative disclosure requirement with respect tocredit risk (excluding counterparty credit risk disclosed inaccordance with Table 6), including the:

(1) Policy for determining past due or delinquency status;

(2) Policy for placing loans on nonaccrual;

(3) Policy for returning loans to accrual status;

(4) Definition of and policy for identifying impaired loans(for financial accounting purposes);

(5) Description of the methodology that the Board-regulated institution uses to estimate its allowance forloan and lease losses, including statistical methods usedwhere applicable;

(6) Policy for charging-off uncollectible amounts; and

(7) Discussion of the Board-regulated institution's creditrisk management policy.

Pg. 17 Items (1) –(4): Pg.158-159

Item (5):Pg.

157-158

Item (6):Pg.

158-159

Item (7):Pg.

122-124

(b) Total credit risk exposures and average credit risk exposures,after accounting offsets in accordance with GAAP, withouttaking into account the effects of credit risk mitigationtechniques (for example, collateral and netting not permittedunder GAAP), over the period categorized by major types ofcredit exposure. For example, Board-regulated institutionscould use categories similar to that used for financialstatement purposes. Such categories might include, forinstance:

(1) Loans, off-balance sheet commitments, and other non-derivative off-balance sheet exposures;

(2) Debt securities; and

(3) OTC derivatives.

Pg. 17-18 Pg. 11, 33,36 and 72

(c) Geographic distribution of exposures, categorized insignificant areas by major types of credit exposure.

Pg. 18

(d) Industry or counterparty type distribution of exposures,categorized by major types of credit exposure.

Pg. 17-18

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

33

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

(e) By major industry or counterparty type:

(1) Amount of impaired loans for which there was a relatedallowance under GAAP;

(2) Amount of impaired loans for which there was norelated allowance under GAAP;

(3) Amount of loans past due 90 days and on nonaccrual;

(4) Amount of loans past due 90 days and still accruing;

(5) The balance in the allowance for loan and lease losses atthe end of each period, disaggregated on the basis of theBoard-regulated institution's impairment method. Todisaggregate the information required on the basis ofimpairment methodology, an entity shall separatelydisclose the amounts based on the requirements inGAAP; and

(6) Charge-offs during the period.

Pg. 18-19 Items (1) &(2):

Pg. 21

Item (5):Pg. 16

Item (6):Pg. 16

(f) Amount of impaired loans and, if available, the amount of pastdue loans categorized by significant geographic areasincluding, if practical, the amounts of allowances related toeach geographical area, further categorized as required byGAAP.

Pg. 20

(g) Reconciliation of changes in ALLL. The reconciliation shouldinclude the following: A description of the allowance; theopening balance of the allowance; charge-offs taken againstthe allowance during the period; amounts provided (orreversed) for estimated probable loan losses during the period;any other adjustments (for example, exchange rate differences,business combinations, acquisitions and disposals ofsubsidiaries), including transfers between allowances; and theclosing balance of the allowance. Charge-offs and recoveriesthat have been recorded directly to the income statementshould be disclosed separately.

Pg. 20 Pg. 16

(h) Remaining contractual maturity delineation (for example, oneyear or less) of the whole portfolio, categorized by creditexposure.

Pg. 21-22 Pg. 13Sch. HC-R Part IIPg. 59

§217.63 TABLE 6 —GENERALDISCLOSURE FORCOUNTERPARTYCREDIT RISK-RELATEDEXPOSURES

(a) The general qualitative disclosure requirement with respect toOTC derivatives, eligible margin loans, and repo-styletransactions, including a discussion of:

(1) The methodology used to assign credit limits forcounterparty credit exposures;

(2) Policies for securing collateral, valuing and managingcollateral, and establishing credit reserves;

(3) The primary types of collateral taken; and

(4) The impact of the amount of collateral the Board-regulated institution would have to provide given adeterioration in the Board-regulated institution’s owncreditworthiness.

Pg. 22-24

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

34

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

(b) Gross positive fair value of contracts, collateral held(including type, for example, cash, government securities),and net unsecured credit exposure. Net unsecured creditexposure is the credit exposure after considering both thebenefits from legally enforceable netting agreements andcollateral arrangements without taking into account haircutsfor price volatility, liquidity, etc.

A Board-regulated institution also must disclose the notionalvalue of credit derivative hedges purchased for counterpartycredit risk protection and the distribution of current creditexposure by exposure type. This may include interest ratederivative contracts, foreign exchange derivative contracts,equity derivative contracts, credit derivatives, commodity orother derivative contracts, repo-style transactions, andeligible margin loans.

Pg. 24 Pg. 14, 33and 47

(c) Notional amount of purchased and sold credit derivatives,segregated between use for the Board-regulated institution'sown credit portfolio and in its intermediation activities,including the distribution of the credit derivative productsused, categorized further by protection bought and sold withineach product group.

N/A

§217.63 TABLE 7 —CREDIT RISKMITIGATION

(a) The general qualitative disclosure requirement with respect tocredit risk mitigation, including:

(1) Policies and processes for collateral valuation andmanagement;

(2) A description of the main types of collateral taken bythe Board-regulated institution

(3) The main types of guarantors/credit derivativecounterparties and their creditworthiness; and

(4) Information about (market or credit) risk concentrationswith respect to credit risk mitigation.

Pg. 25

(b) For each separately disclosed credit risk portfolio, the totalexposure that is covered by eligible financial collateral, andafter the application of haircuts.

N/A

(c) For each separately disclosed portfolio, the total exposure thatis covered by guarantees/credit derivatives and the risk-weighted asset amount associated with that exposure. Creditderivatives that are treated, for the purposes of this subpart, assynthetic securitization exposures should be excluded fromthe credit risk mitigation disclosures and included within thoserelating to securitization (Table 8).

Pg. 25

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

35

Securitization

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

§217.63 TABLE 8 —SECURITIZATION

• General qualitative disclosure requirement. For each separaterisk area described in Tables 5 through 10, the Board-regulated institution must describe its risk managementobjectives and policies, including: Strategies and processes;the structure and organization of the relevant risk managementfunction; the scope and nature of risk reporting and/ormeasurement systems; policies for hedging and/or mitigatingrisk and strategies and processes for monitoring the continuingeffectiveness of hedges/mitigants.

Pg. 25-26 Pg.120-126

(a) The general qualitative disclosure requirement with respect toa securitization (including synthetic securitizations), includinga discussion of:

(1) The Board-regulated institution's objectives forsecuritizing assets, including the extent to which theseactivities transfer credit risk of the underlying exposuresaway from the Board-regulated institution to otherentities and including the type of risks assumed andretained with resecuritization activity. The Board-regulated institution should describe the structure ofresecuritizations in which it participates; this descriptionshould be provided for the main categories ofresecuritization products in which the Board-regulatedinstitution is active;

(2) The nature of the risks (e.g. liquidity risk) inherent in thesecuritized assets;

(3) The roles played by the Board-regulated institution in thesecuritization process (for example, these roles mayinclude originator, investor, servicer, provider of creditenhancement, sponsor, liquidity provider, or swapprovider) and an indication of the extent of the Board-regulated institution's involvement in each of them;

(4) The processes in place to monitor changes in the creditand market risk of securitization exposures includinghow those processes differ for resecuritization exposures;

(5) The Board-regulated institution's policy for mitigatingthe credit risk retained through securitization andresecuritization exposures; and

(6) The risk-based capital approaches that the Board-regulated institution follows for its securitizationexposures including the type of securitization exposure towhich each approach applies.

Pg. 25-26

CITIZENS FINANCIAL GROUP, INC.

March 31, 2015 Basel III Disclosures

36

Pillar III Requirement Required Disclosures Basel IIIPage #

2014 10-KPage #

Q1 10-QPage #

FRY9CPage #

(b) A list of:

(1) The type of securitization SPEs that the Board-regulatedinstitution, as sponsor, uses to securitize third-partyexposures. The Board-regulated institution must indicatewhether it has exposure to these SPEs, either on- or off-balance sheet.; and

(2) Affiliated entities:

i. That the Board-regulated institution manages oradvises; and