basic budgeting tips - citizens advice resources... · 08/08/2017 · basic budgeting tips ....

TRANSCRIPT

Basic Budgeting Tips Guidance for conversations on budgeting

Trainers notes for basic budgeting with clients

2 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

This session pack has been produced as part of Citizens Advice Financial Skills for Life.

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Citizens Advice is an operating name of the National Association of Citizens Advice Bureaux, Charity registration number 279057, VAT number 726020276, Company Limited by Guarantee, Registered number 1436945 England. Registered office: Citizens Advice, 3rd Floor North, 200 Aldersgate Street, London, EC1A 4HD.

Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, Citizens Advice assumes no responsibility. The user of the information agrees that the information is subject to change without notice. To the extent permitted by law, Citizens Advice excludes all liability for any claim, loss, demands or damages of any kind whatsoever (whether such claims, loss, demands or damages were foreseeable, known or otherwise) arising out of or in connection with the drafting, accuracy and/or its interpretation, including without limitation, indirect or consequential loss or damage and whether arising in tort (including negligence), contract or otherwise.

3 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Basic Budgeting Tips The aim of this session is to provide guidance to advisers when delivering sessions on budgeting to clients with limited literacy, or with clients where a conversational approach is much more likely to be effective than the usual activity based approach. Objectives for the end of this session are that clients will be able to:

• Identify ways to reduce their outgoings. • Identify ways to increase their income • Understand the uses of a bank account. • Understand what is needed to open a bank account. • Be aware of different payment methods.

General guidance notes on delivering a financial capability session are available elsewhere on the Citizens Advice website. These provide guidance for setting up and administering sessions. These notes are for the trainers use only. A separate handout pack should be used with every client, whether that is one-to-one or group. No signposts are included in the handouts, but an adviser is expected to use this session pack to decide on appropriate avenues for further information and guidance.

Trainers are encouraged to feedback to the Financial Skills for Life team with any feedback about training materials or resources. If you have any comments, please contact: [email protected]

4 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Contents

Session specific guidance 5

Lesson plan 7

1. Budgeting quiz 8

2. Attitudes to cash 9

3. Expenditure cards 10

4. Money personality quiz 17

5. Good reasons for having a budget 18

6. Increasing income and reducing expenditure 19

7. Fifty tips to save money 20

8. Basic spending diary 26

9. Sales jargon 27

Evaluation Guidance 28

Trainers notes 30

5 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Session specific guidance Manage expectations, make it clear to clients that the session is an introduction to budgeting and that if they want more detail, they will have to make that clear to the adviser. Signpost and empower, ensure that clients are aware that after the session they will have a clear idea where to go to answer certain queries and to get further assistance. Timings, all times are only guidelines. Trainers are welcome to be flexible; if that means expanding some activities and dropping others, that’s up to the trainer. Low-pressure commitments, any agreement from the clients to enact any behaviour-change (large or small) should not act as a deterrent to further attendance. It should be stressed that this is NOT a situation to feel pressure about, and that it is a safe learning environment. Any behaviour changes agreed to but not maintained represent a talking-point and learning opportunity.

6 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Top tips

7 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Lesson plan Red activities – Are essential to any session on this topic. Amber activities – Are highly recommended but not essential. Green activities – Are optional activities, if time allows. The size of the bubble indicates roughly how much time, relative to the session, to spend on an activity.

1

2

5

9

3

4

This session can take anything from around 45-120 minutes to deliver: it’s completely up to the adviser and the client. After delivering the first activity, the trainer should be in a position to gauge what other activities to use. Activities 6-8 are recommended together. In other words, if you do one, you should really do all three.

6

7 8

Adu

lt F

inan

cial

Cap

abili

ty F

ram

ewor

k re

fere

nces

: 1

– B

(e) 2

2

– B

(e) 3

3

– B

(e) 3

4

– B

(e) 1

5

– B

(e) 1

6

– B

(e) 2

7

– D

(e) 2

8

– B

(e) 5

9

– B

(e) 2

8 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Budgeting quiz

Use the questions in handout BDA1 as a platform to launch discussion with the clients. Ensure clients discuss which benefits they are on that may be affected by Welfare reform. Stress the importance of having a spending diary, at least initially. Stress that all clients should keep one of these. Introduce the spending diary (several versions are available to be downloaded in this topic, with one attached here). This handout is for clients to take away and fill in, making a note of all their daily expenditure. Clients do not need to fill in bills such as rent or water, as this should be recorded separately via statement or rental book (they may however include these if they wish). Spending diaries are specifically meant to record incidental outgoings and to track gaps in the client income and expenditure. Make clients aware that budgeting involves two sides:

1. The money coming in. 2. The money going out.

Make it very clear that the exercises in this session are focussed on the money going out primarily. Ideal time to signpost them to Money Advice Service budget planner and the Martin Lewis Demotivator. Use a laptop to demonstrate these. Answers

1. C - Plain cuts of meat 2. B - No 3. A - Delay paying off credit card debt 4. Discussion point 5. B - An expense you want but don’t need 6. A - Yes 7. C - 2 – 3 months 8. B - No

AIC 20 – B W

9 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Attitudes to cash

This activity is an easy ice-breaker suitable for groups or one-to-one sessions. It can serve to get a conversation about money rolling, and also allows the advisor to gauge a client’s needs when considering future activities. Advisers should provide handout BDA2, and - if in a one-to-one scenario – may wish to assist the client in completing it. The format of the quiz is designed to be familiar to any users who read tabloid magazines. Answers Mostly A - You’re a debt collectors dream You could be in trouble. If you carry on with this carefree approach you may find that you end up in so much debt that there’s no way out. Learn some simple tricks for looking after your money. Mostly B - You’re a day to day debtor You live for today. You never know quite where you are with your cash - it is the road to debt. A little bit of planning could make your life a lot simpler. Mostly C - You’re a smart spender You are reasonably in control, but would like a little more help. You just need to keep a closer track of your cash. Mostly D - You’re a careful controller You plan for every penny and the unexpected will cause you to worry. Mostly E - You’re a squirrel You love saving - try to learn to spend some today rather than just save for tomorrow.

If that was useful, why not try…

Energy and water - Saving energy in the home

AIC 20 - W

10 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Expenditure cards

Notes for group sessions Put the learners into small groups of 3-4 and give each group a set of expenditure cards with some additional blank cards and ask them to sort them under the heading: important, quite important, not important

In the whole group ask each group in turn to share one of their important spending cards and explain briefly why it was important. Then do the same with an example from each group of a not important spending card. You can note their ideas on flipchart or get them to come and stick their card up on the flipchart, under the headings important or not important. You can repeat this process a number of times so that you have a range of examples of important and not important items with the reasons for the decisions. Finally ask each group in turn to give an example of a card they put in the quite important column or were unable to agree on with the reasons why. Again these can be added to the relevant column on the flipchart. Notes for one-to-one sessions This session was not initially intended for one-to-one work, unless an adviser feels that a client would specifically benefit from it. If a client has very poor literacy, or would significantly prefer a conversational approach, then an adviser can run through the cards with them, sorting them into piles as per the three categories.

If this was useful, why not try…

Budgeting – 50 tips to save money

AIC 20 – B W

11 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

groceries

baby milk

nappies

magazines

mobile

cigarettes

12 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

bread

milk

chocolate

sweets

clothes

gas

13 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

electricity

water

TV licence

rent

council tax

cosmetics

14 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

household

shoes

toys

music

CDs / DVDs

drinks

15 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

insurance

travel

health

telephone

Christmas

takeaway food

16 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Important

Quite important

Not important

17 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Money personality quiz

Quizzes about clients’ attitudes to money can be fun, but are also of limited use. There is a need for an adviser to be careful when choosing a money quiz, as even with the best will in the world, some clients may find the questions invasive or stressful. Quizzes work well as ice-breakers for groups and as platforms for initial discussions with one-to-one clients. The handouts are deliberately split into two equal pages, advisers can start with the first page and gauge the client’s interest before committing to using the second five questions. Answers If you answered mostly A, you have a tendency to be very careful with your money. Nice! If you answered mostly B, you have good intentions with money, but often don’t really follow through on them. If you answered mostly C, you tend to live in the moment, which can easily lead to money worries further down the line.

If that was useful, why not try…

Budgeting – Essential or non-essential

AIC 20 - W

18 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Good reasons for having a budget

This activity requires no handout, and is intended as guidance to offer advisers some structure on a quick and straightforward conversation on budgeting.

As usual, in groups this can take place as a group activity with feedback to the class, and as a one-to-one activity this can be done side-by-side or the client may want to attempt a list and then discuss it with the advisor. Ideas should include:

• Keeping track of where your money is going.

• Reacting to debt.

• Working out how much money you can save.

• Checking if you can afford something.

• Preparing to move into a place of your own.

• Preparing for starting a job.

• Dealing with losing a job.

• Preparing for a new baby.

• Preparing to move in or out with partner.

• Avoiding spending money you don’t have.

If that was useful, why not try…

Budgeting – How to reduce my bills

AIC 20 - B

19 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: increasing income and reducing expenditure

This activity is a simple quick word storm designed to get clients thinking about budgeting tips. It is by nature very brief and will need to be supplemented by handouts available amongst the resources. Possible ideas for increasing income include:

• Check getting right benefits

• Check tax code

• Get a job, part or full time

• Sell something (for example, on ebay)

Possible ideas for reducing spending include:

• Use money off vouchers

• Plan meals in advance and shop with a list, not impulse buying

• Shop at local market

• Use supermarket rather than corner shop for expensive items

• Shop at the end of the day for food reductions

• Cook rather than take away

• Second hand and charity shops

• Set aside money for bills as soon as get pay/benefits, then only spend what’s left

• Put on a jumper, not the heating!

• Check if pre-pay or contract mobile phone better

• Entertain at home rather than go out

If this was useful, why not try…

Budgeting – 50 tips to save money

AIC 20 –W

20 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Fifty tips to save money

This activity is meant for very general ‘placeholder use’. There is no obligation for any adviser to cover all, or even most of these tips. Rather, these are intended to serve as a quick-reference bank of tips to allow advisers to have short – or detailed – conversations with clients about various practical money-saving tips that are easy to take on board. The list is organised into twelve tips per page; this way an adviser can choose to cover only one page (or two, or three) in a session. Many various online lists similar to this exist; advisers are encouraged to use whichever sources of money-saving tips they feel most comfortable discussing with clients. No handouts are provided, but advisers are welcome to show the remainder of the resource with clients for them to pick and choose which topics they would like to discuss. There are only 48 tips; this is deliberate. If the adviser gets through all of them, ask the client to come up with one or two of their own!

If that was useful, why not try…

Energy and Water – Saving energy in the home

AIC 20 – B W

21 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Did you know these 50 tips to save money? 1. Take advantage of cashback and reward credit cards. Barclaycard's Freedom Rewards card is giving £30 worth of vouchers when you spend £300 on the card in the first three months. Santander's 123 credit card offers account holders 3% cashback on fuel, 2% cashback in department stores and 1% cashback at supermarkets. 2. Recycle old mobile phones, DVDs, CDs and clothes. 3. Use comparison sites to find the cheapest supermarket prices. 4. Use balance transfer credit cards to transfer debt from your current credit card that charges a high rate of interest, to one that charges 0% interest. 5. Buy own-brand goods at the supermarket. 6. Cancel your gym membership and opt for pay-as-you-go if there is a strong likelihood that you will stop going. 7. Bulk-buy foods that don't go off, particularly if they are on offer. An open or unopened bottle of tomato ketchup can last up to a year in your cupboard, so if you go through a lot of it, bulk-buying would save you money. 8. Switch energy suppliers. Households could save up to £300 if they switch energy suppliers, but millions don't. In fact, only 14% of homes change their gas and energy tariff each year even though the process is simple. 9. Use discount websites to save on days out. Sites like groupon.co.uk, vouchercodes.co.uk and wowcher.co.uk, to name a few, offer daily deals and discounts on events, activities, travel and restaurants. 10. Cycle/walk to work (if possible) rather than drive or take the tube.

22 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

11. Grow your own herbs. Keeping pots of herbs in your kitchen can save you money on having to repeat purchase packs of herbs. Growing from seed can be even more cost effective. 12. Pay less for your holiday by comparing travel agents online. 13. Find cheap flights for your holidays next year. 14. Rent a new dress rather than buy one. If you have a big event coming up but don't want to fork out for a new outfit you'll only wear once, there are a number of websites you can go to hire a new dress, for a fraction of the cost of a brand new one. GirlMeetsDress.com has hundreds of dresses to search through, and for around £50 you can rent a designer dress (often retailing for hundreds of pounds) for two nights, or pay slightly more for seven nights. 15. Share travel to cut costs. You can join websites like liftshare.com or GoCarShare.com to meet other people who wish to share long-distance travel in order to cut costs. Drivers and passengers can benefit from travelling together, with the driver getting contributions for petrol costs, and the passengers saving on expensive train fares. 16. Open a savings account. 17. Go without a TV licence. A TV licence costs £147, but do you need one? If you watch catch-up TV you do not need a licence, so 4 on Demand and ITV Player are free to use. However, if you use BB iPlayer – even to watch shows that are not live – you will be liable for a TV license. There are concessions in place for those aged over 74 and for partially sighted people. 18. Use a slow-cooker for cooking stews. Using a slow cooker to make a stew is both easier, you can leave it to stew while you're at work all day, and cheaper. It costs around 10p to use a slow cooker for around eight hours, while using an oven will cost far more at 30p for one hour. 19. Do online surveys in your spare time and earn money. MoneySavingExpert.com lists the 20 best survey sites on the web. Number one is Ipsos and number two is Swagbucks. Both are free to join.

23 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

20. Check to see if your children are entitled to any benefits, including free school meals and school uniform. 21. Make sure your child isn't paying tax on their savings account. 22. Don't buy bottled water, fill up a re-usable bottle with tap water. 23. Make your own drinks. Making your own juices and smoothies with a blender or juicer will save you the expense of buying these drinks in the shops. 24. Find the cheapest way to spend abroad. If you go on holiday make sure you are careful with your overseas spending. Pick a credit card that doesn't charge an ATM fee for withdrawing cash abroad. 25. Stock up on Christmas decorations now. Christmas themed wrapping paper and decorations went on sale around Christmas Eve/Boxing Day, so stock up now and save on the cost next year. 26. Have a dry January. If, according to recent figures from the Office for National Statistics, you are an average UK household that spends £15.20 a week on alcohol, by not drinking for the entire month of January, you could save over £60. 27. Use supermarket loyalty cards. People are using their loyalty cards less, according to research conducted in August, but using a supermarket loyalty scheme could save you money on your weekly shop. 28. Patch up worn clothes instead of throwing them out 29. Use a spreadsheet to budget your household finances. Make a spreadsheet on Microsoft Excel adding up every household expense you will have to pay, including mortgage/rent, groceries, transport, utility bills, insurance, phone bills and everything else to ensure you don't overspend. Google "house budget template" for more help. 30. Turn electrical appliances off when not in use. 31. Use energy-saving gadgets to cut costs.

24 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

32. Swap books rather than buy new ones. Once you've read a book, you can swap it with someone else for a book of theirs that you haven't read yet, rather than paying for a new one. 33. Pay your children to do jobs around the house. Get your children to earn their pocket money by doing their bit around the house. Cleaning the house/car, taking the bins out, ironing some clothes or walking the dog will save you money on professional help, and will teach your children the value of money. 34. Make your own meals rather than buy takeaways. Save money on buying takeaways, which you can make yourself or buy from the supermarket much cheaper. 35. Avoid the January sales. Even though you might feel like you're getting a bargain, it is likely you are buying something you never really needed, and would never have bought in the first place had it not been on sale. 36. Check out websites for freebies. Go to websites like Gumtree.co.uk or Freecycle.org for free bits of furniture, old electronics, books, clothes and other unwanted items. 37. Shop at discount supermarkets rather than higher-end ones. 38. Use coupons. A teenager from Essex found fame for "Extreme Couponing" which saw him pay 4p for a £600 shop at Tesco. 39. Rent out a spare room. 40. Cut down on the cost of car insurance. Comparing premiums is easy on online comparison sites. 41. Try and rope your neighbours into a "sharing economy". Families can save hundreds of pounds a year by being part of the “sharing economy” which embraces everything from recycling second-hand goods through to hiring them out to other families on your street or hosting parties where guests bring a range of items to swap.

25 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

42. Sell old comics, postcards and other investment pieces. If you have annuals hidden away in your attic, old toys stashed under your bed or music memorabilia tucked away in your garage, you could be sitting on a lot of money. Old Beano and Dandy annuals have recently sold for up to £20,000 at auction, retro postcards could be worth up to £400 if you're lucky. 43. Buy a 'passive' fund over an 'active' one. If you are an investor, buying a "passive" or "tracker" fund is typically much cheaper than buying traditional funds, as there is no need to pay a professional to manage your money. 44. Collect loose change and pennies in a jar and cash them in at the end of the year. Without even realising you could have saved £40 or £50. 45. Get cashback for shopping online. Cashback sites like Quidco.com or Topcashback.co.uk give you cashback on your purchases once you have created an account with the respective site. You can browse high street and online retailers using the websites and once you buy an item, you will receive a percentage of the value of your shopping as cashback which will be paid into your account. 46. Follow retailers on social networking sites like Twitter. Amazon, ASOS, eBay and Debenhams are some of the retailers who tweet about their latest deals or sales on their website and in store. 47. Pay attention to your smart meter. 48. Don't waste food. The average UK household wastes £470 worth of food each year, or £700 for a family with children. This is equivalent to around £60 each month. 49. 50.

Can you think of your own tip to write here?

Can you think of your own tip to write here?

26 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Basic spending diary

This handout is for the adviser to suggest to clients as a tactic to involve the whole family in budgeting. Advisers should use their discretion as to whether this is relevant for the client or group.

AIC 20 - B

27 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Activity: Sales jargon

This activity allows the adviser to discuss common sales tactics used on the high-street with the client. Advisers should use their own local knowledge and anecdotes to deliver this, but some guidance is also provided. Limited editions – often sold as being worth more to collectors, it’s worth pointing out that collectors would normally buy such items at purchase, not second-hand. Use video games as an example. Unlimited texts/minutes/internet – are they subject to Fair Usage? What does that mean? Buy One Get One Free (BOGOF) – original price may be artificially high. Free Warranty – warranty just means ‘promise’ and so depends on Terms and Conditions. Free Guarantee – guarantee just means ‘promise’ and so depends on Terms and Conditions. Lifetime Guarantee – use example of a watch: ‘lifetime’ may just refer to the watch’s working life, so it is guaranteed to work as long as it works. No hassle refund – there may be small print requiring receipt or original packaging. Interest free credit – may require payment within a certain time or high interest could apply. Loyalty card – a card accruing loyalty points for money spent in-store. Store card – a credit card applicable to a particular store, warn of high APRs. Price match – may exclude online offers or have a geographic limit. Up to 50% off – can mean discounts of nothing, up to discounts of half-price.

AIC 20 - W

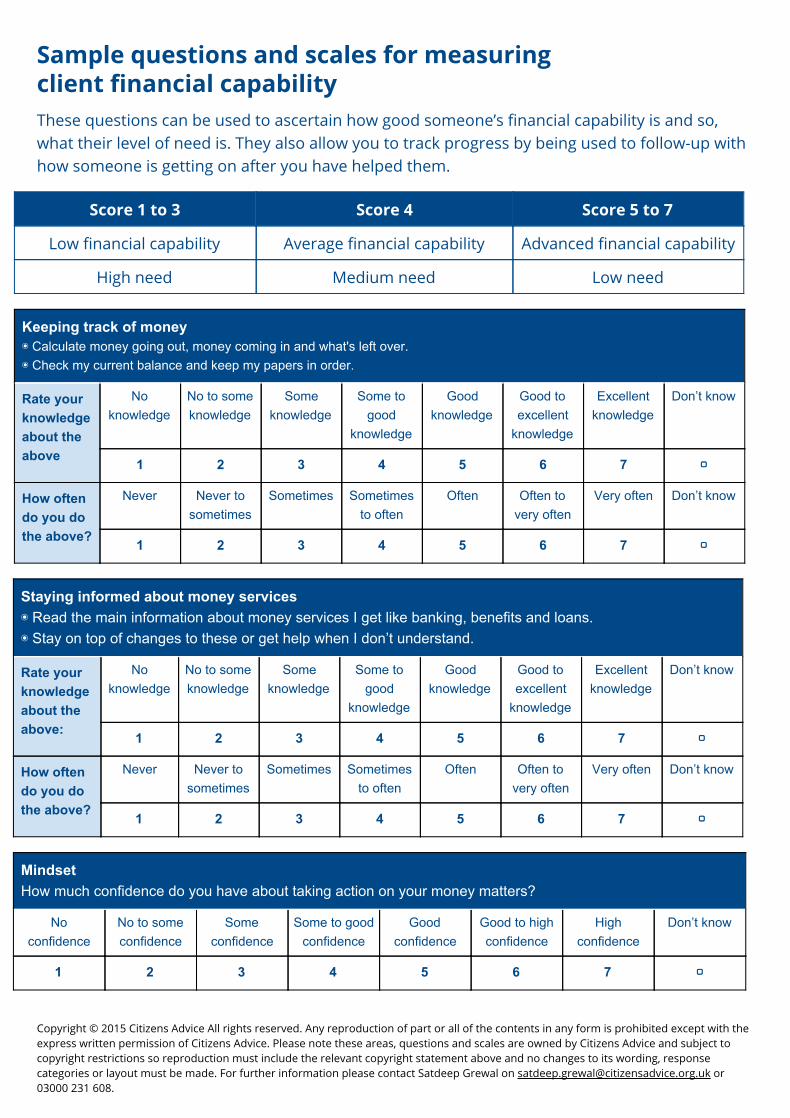

Evaluation Guidance Areas that underpin client financial capability These are the Citizens Advice Financial Capability Areas that were carefully researched and developed by The Impact Team at Citizens Advice to help local offices measure client financial capability robustly and consistently across services. They were developed in line with the MAS UK Financial Capability Strategy Adult Outcomes Framework. Sample questions and scales can be found overleaf. An Impact Tool is available in Petra for recording responses and progress.

Keeping track of money Controlled spending

◉ Keep track of money going out, money coming in and calculate what's left over. ◉ Check my current balance and keep my papers in order.

◉ Spend or save only what I can afford after covering the basics I need to live, like food, housing and electricity.

Having enough money to live Planning ahead with money

◉ Have enough money to cover the basics I need to live like food, housing and electricity.

◉ Know when my bills and payments are due and keep on top of priority bills, like for electricity, loans and council tax. ◉ Put some money aside for big or unexpected costs.

Looking for the best deals Staying informed about money services

◉ Look at different options and buying the best deal for things like food, clothes, large items or services like phone, electricity or insurance. ◉ Get different opinions on what I am buying, like from reviews and comparison websites.

◉ Read the main information about money services I get like banking, benefits and loans. ◉ Stay on top of changes to these or get help when I don’t understand.

Mindset

◉ Confidence about taking action on my money matters.

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Please note these areas, questions and scales are owned by Citizens Advice and subject to copyright restrictions so reproduction must include the relevant copyright statement above and no changes to its wording, response categories or layout must be made. For further information please contact Satdeep Grewal on [email protected] or 03000 231 608.

Sample questions and scales for measuring client financial capability These questions can be used to ascertain how good someone’s financial capability is and so, what their level of need is. They also allow you to track progress by being used to follow-up with how someone is getting on after you have helped them.

Score 1 to 3 Score 4 Score 5 to 7

Low financial capability Average financial capability Advanced financial capability

High need Medium need Low need

Keeping track of money ◉ Calculate money going out, money coming in and what's left over. ◉ Check my current balance and keep my papers in order. Rate your knowledge about the above

No knowledge

No to some knowledge

Some knowledge

Some to good

knowledge

Good knowledge

Good to excellent knowledge

Excellent knowledge

Don’t know

1 2 3 4 5 6 7 ▢

How often do you do the above?

Never Never to sometimes

Sometimes

Sometimes to often

Often

Often to very often

Very often

Don’t know

1 2 3 4 5 6 7 ▢

Staying informed about money services ◉ Read the main information about money services I get like banking, benefits and loans. ◉ Stay on top of changes to these or get help when I don’t understand. Rate your knowledge about the above:

No knowledge

No to some knowledge

Some knowledge

Some to good

knowledge

Good knowledge

Good to excellent knowledge

Excellent knowledge

Don’t know

1 2 3 4 5 6 7 ▢

How often do you do the above?

Never Never to sometimes

Sometimes

Sometimes to often

Often

Often to very often

Very often

Don’t know

1 2 3 4 5 6 7 ▢

Mindset How much confidence do you have about taking action on your money matters?

No confidence

No to some confidence

Some confidence

Some to good confidence

Good confidence

Good to high confidence

High confidence

Don’t know

1 2 3 4 5 6 7 ▢

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Please note these areas, questions and scales are owned by Citizens Advice and subject to copyright restrictions so reproduction must include the relevant copyright statement above and no changes to its wording, response categories or layout must be made. For further information please contact Satdeep Grewal on [email protected] or 03000 231 608.

30 ©2015 Citizens Advice Basic budgeting trainers notes/Aug17/v2

Citizens Advice financial capability

Trainers notes