basic revenue principles applied to pharma - … revenue principles applied to pharma 201 boot camp...

TRANSCRIPT

Basic Revenue Principles Applied to Pharma

201 Boot Camp – Accounting and Financial Reporting in Life Sciences Companies

Mike Lombardo, Senior Manager March 16, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

Disclaimer

Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Revenue Recognition Refresher

• New Product Launch Considerations

• Collaborations and Alliances

• Multiple Element Arrangements

• Licensing Arrangements

• SEC Comment Letter Trends

Agenda

Revenue Recognition Refresher

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Revenue Recognition

Copyright © 2015 Deloitte Development LLC. All rights reserved.

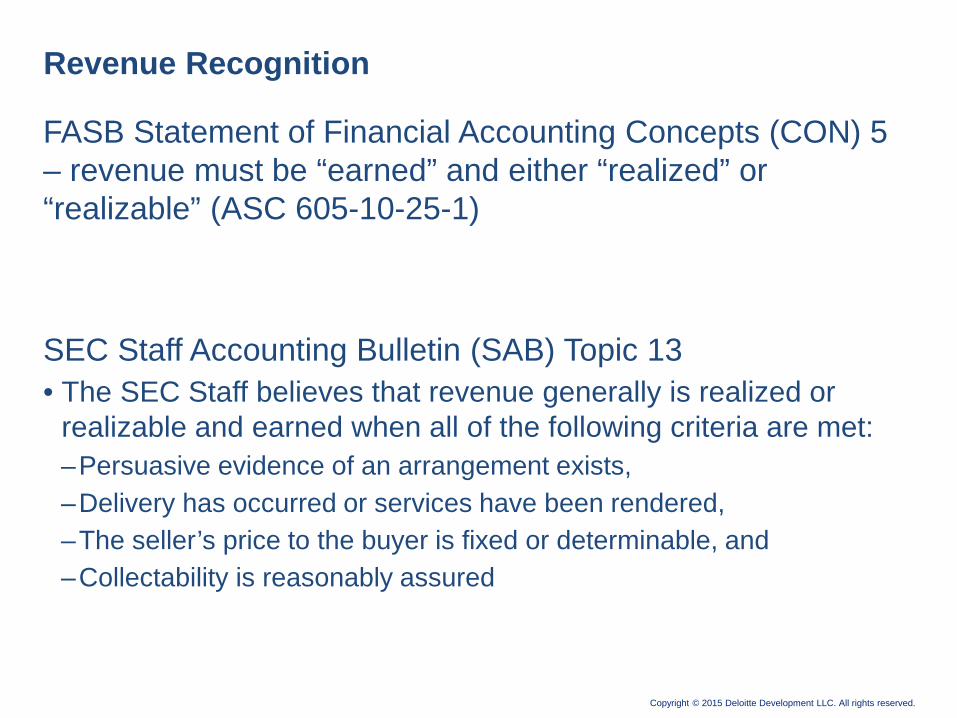

Revenue Recognition

FASB Statement of Financial Accounting Concepts (CON) 5 – revenue must be “earned” and either “realized” or “realizable” (ASC 605-10-25-1)

SEC Staff Accounting Bulletin (SAB) Topic 13 • The SEC Staff believes that revenue generally is realized or

realizable and earned when all of the following criteria are met:–Persuasive evidence of an arrangement exists,–Delivery has occurred or services have been rendered,–The seller’s price to the buyer is fixed or determinable, and–Collectability is reasonably assured

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Revenue Recognition

Sales of Product when Right of Return Exists (ASC 605-15-25-1) –requires that all of the following criteria be met in order to recognize revenue at the time of sale when the right of return exists:

A. Seller’s price is fixed or determinableB. Buyer’s obligation to pay is not contingent on resaleC. Buyer’s obligation is unchanged if products are stolen or damagedD. Buyer has economic substance apart from that provided by the

seller (i.e., their own facilities, employees and capital) E. Seller has no significant future performance obligationsF. Future returns can be reasonably estimated

Significant judgment may be required when evaluating the criteria included in items A and F above

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Revenue Recognition

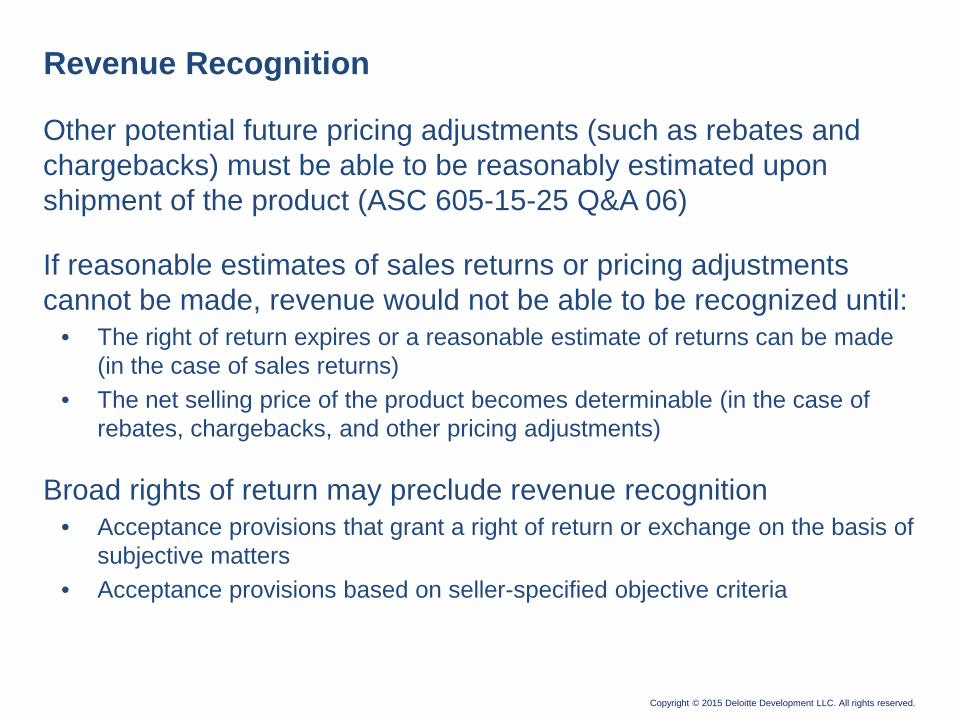

Other potential future pricing adjustments (such as rebates and chargebacks) must be able to be reasonably estimated upon shipment of the product (ASC 605-15-25 Q&A 06)

If reasonable estimates of sales returns or pricing adjustments cannot be made, revenue would not be able to be recognized until:

• The right of return expires or a reasonable estimate of returns can be made (in the case of sales returns)

• The net selling price of the product becomes determinable (in the case of rebates, chargebacks, and other pricing adjustments)

Broad rights of return may preclude revenue recognition• Acceptance provisions that grant a right of return or exchange on the basis of

subjective matters • Acceptance provisions based on seller-specified objective criteria

Copyright © 2015 Deloitte Development LLC. All rights reserved.

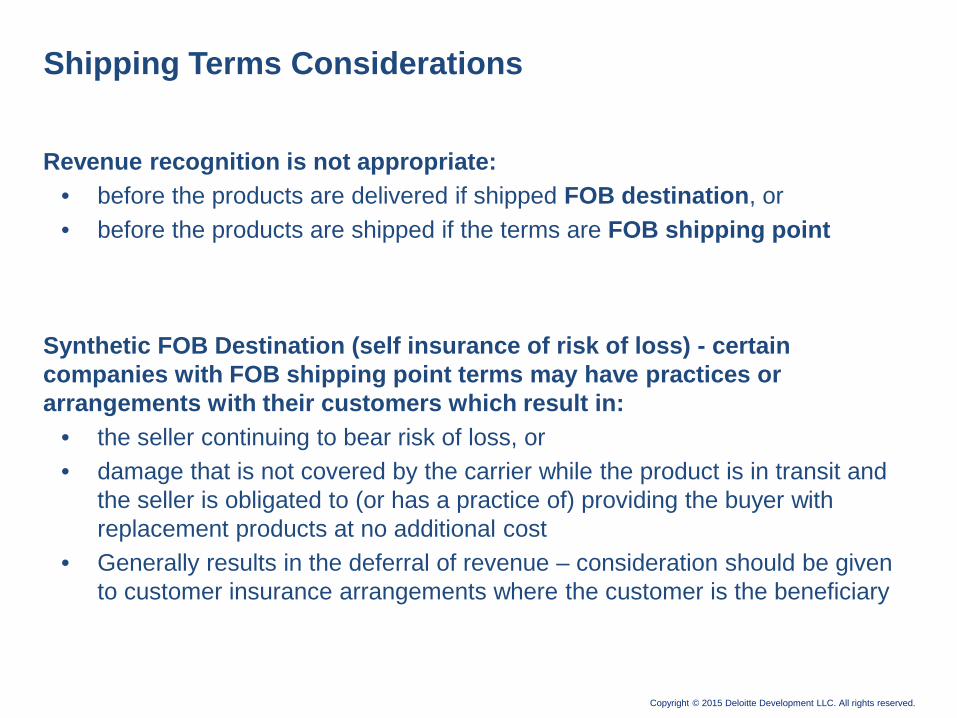

Revenue recognition is not appropriate:• before the products are delivered if shipped FOB destination, or • before the products are shipped if the terms are FOB shipping point

Synthetic FOB Destination (self insurance of risk of loss) - certain companies with FOB shipping point terms may have practices or arrangements with their customers which result in:

• the seller continuing to bear risk of loss, or • damage that is not covered by the carrier while the product is in transit and

the seller is obligated to (or has a practice of) providing the buyer with replacement products at no additional cost

• Generally results in the deferral of revenue – consideration should be given to customer insurance arrangements where the customer is the beneficiary

Shipping Terms Considerations

Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Recording Revenue upon shipment OK with FOB Shipping terms and appropriate customer insurance

• First determine party responsible for damage

• If real Customer Insurance A Company would record revenue and then establish a Goods In Transit reserve

• Controls in place to ensure damaged product is destroyed

Customer Insurance and In-Transit Matters

Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Customer Insurance terms – Not a pass-through

– Requires judgment– Buyer not the Seller is the named insured party– Claims are filed by or on behalf of the Buyer– Under no circumstances would the Seller have any risk for product damage

or loss during shipment– Risk of loss transfers

Customer Insurance and In-Transit Matters, continued

New Product Launch Considerations

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Has your Company launched a new product during the past year, and if so, is revenue being recognized upon shipment or deferred?

A – Yes, revenue recognized upon shipment

B – Yes, revenue deferred

C – No product launches during past year

D – Not sure

Polling Question – New Product Launches

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Delivery / Exchange

• Have the risks and rewards of ownership been transferred?• Has there been a delivery or an exchange? Has legal title passed?

Acceptance • Is there any additional substantive performance required on the part of the seller to gain customer acceptance?

Right of Return

• Under what circumstances can the customer return the product?• Does payment depend on resale?• Can returns be reasonably estimated?• What is industry practice regarding returns?• Is it common practice to accept returns even though there may be no

formal policy?

Terms and Conditions

• Are sales terms uniform and is it clear that all obligations to perform are substantially complete?

General Considerations in Regard to Revenue RecognitionNew Product Launch Considerations

Copyright © 2015 Deloitte Development LLC. All rights reserved.

New Product Launch Considerations

Unique factors must be considered in determining product return estimates prior to initially recognizing revenue

• Require sufficient returns history to reasonably estimate and record returns reserve

• Initial rate of returns should be based on returns for similar products on the market for a similar number of years (analogs)

• May need to consider deferring revenue recognition for new products which are not a line extension of an existing product or for which an appropriate analog does not exist

• For each new product launch, documentation should include the basis for:– Initial position regarding revenue recognition– Selection of an initial accrual rates for sales returns and pricing

adjustments– Appropriateness of analog(s) selected

Copyright © 2015 Deloitte Development LLC. All rights reserved.

New Product Launch Considerations

Other factors to be considered related to market acceptance of a new product include:

• Total estimated gross demand sales relative to total gross factory sales for the same period

• Amount of initial launch quantities sold into the distribution channel• Projected length of time before existing inventory in the distribution channel

will be consumed• Actual sales trend compared to sales trend expectations prior to launch• Distribution channel and visibility to consumption data

If market demand each quarter-end is sufficient, revenue recognition can be appropriate (net of estimated accruals for sales returns and pricing adjustments)

If market demand is not sufficient to consume the volume in the distribution channel, revenue on sales to wholesalers or distributors should be deferred, net of sales to end users

Copyright © 2015 Deloitte Development LLC. All rights reserved.

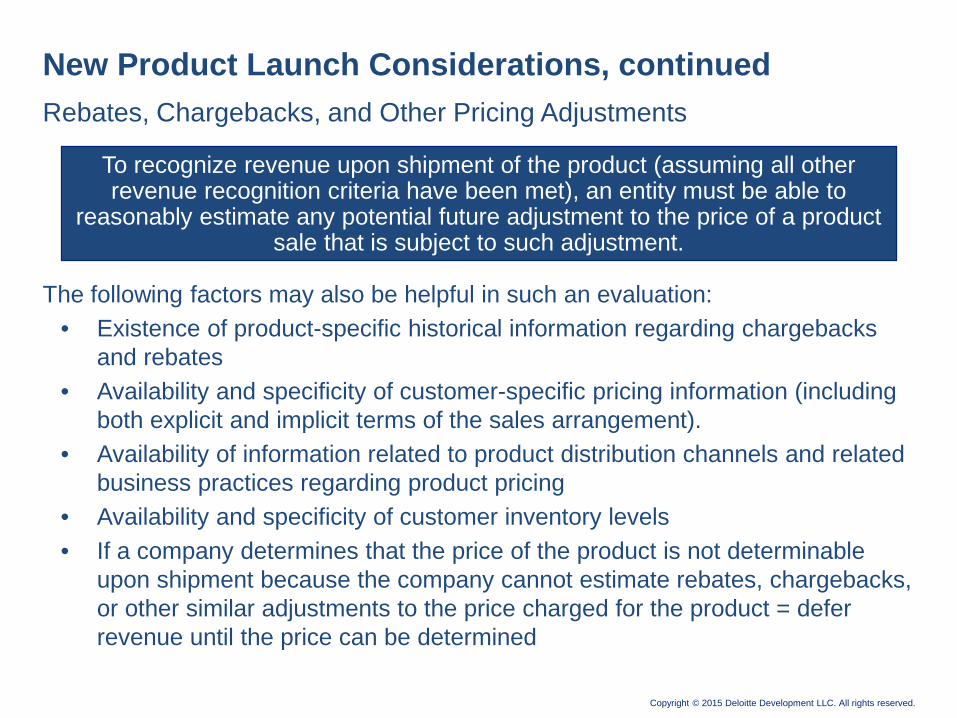

The following factors may also be helpful in such an evaluation:• Existence of product-specific historical information regarding chargebacks

and rebates• Availability and specificity of customer-specific pricing information (including

both explicit and implicit terms of the sales arrangement).• Availability of information related to product distribution channels and related

business practices regarding product pricing• Availability and specificity of customer inventory levels• If a company determines that the price of the product is not determinable

upon shipment because the company cannot estimate rebates, chargebacks, or other similar adjustments to the price charged for the product = defer revenue until the price can be determined

Rebates, Chargebacks, and Other Pricing Adjustments

New Product Launch Considerations, continued

To recognize revenue upon shipment of the product (assuming all other revenue recognition criteria have been met), an entity must be able to

reasonably estimate any potential future adjustment to the price of a product sale that is subject to such adjustment.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Factors that may impair management’s ability to make a reasonable estimate of future pricing adjustments:

• Susceptibility to significant external factors• Lack of historical returns experience• Lag time for returns from customer• Significant increases in or excess levels of inventory in a distribution channel• Lack of visibility into the distribution channel and sales to end users• Significance of a particular distributor / wholesaler• Marketing programs that offer product return provisions outside the standard

return policy• Estimated shelf life, discontinuances, seasonality, and regulatory

considerations such as a more stringent label

New Product Launch Considerations, continued

Collaborations & Alliances

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Overview of Collaborations & Alliances

Why companies in the life sciences industry enter into alliance and collaboration arrangements

• Transfer or share risk of R&D

• Transfer or share manufacturing, sales and marketing efforts once products are approved

• Ability to develop more compounds when resources are limited

• Transform low priority assets into viable and potentially successful assets by partnering

• De-prioritize indications and/or assets

• Accelerate development of certain assets

• Balance financial reporting and liquidity considerations

Copyright © 2015 Deloitte Development LLC. All rights reserved.

ASC 808

ASC 808 defines collaborative arrangements as a contractual arrangement that involves a joint operating activity. These arrangements involve two (or more) parties that meet both of the following requirements:

• They are active participants in the activity • They are exposed to significant risks and rewards dependent on the

commercial success of the activity

Types of collaboration arrangements can include:

• Joint operating activity to jointly develop and commercialize intellectual property or a potential new drug product

• Joint operating activity involving a potential new drug product that includes R&D, marketing (including promotional activities and physician detailing), G&A, manufacturing, and distribution activities

• Generally provide that the participants share, based on contractually defined calculations, the profits or losses from the associated activities

Copyright © 2015 Deloitte Development LLC. All rights reserved.

ASC 808

Participants should evaluate whether an arrangement is a collaborative arrangement at its inception

• Based on the facts and circumstances specific to the arrangement• Can begin at any point in the life schedule of an endeavor• Reevaluate whenever there is a change in either the roles of the participants

or the participants' exposure to significant risks and rewards dependent on the ultimate commercial success of the endeavor

The following are indicators that can be used to identify a collaboration agreement:

• Participants are “active” contributors to the arrangement (actively participate) and are not solely financial investors

• Participants are exposed to significant risks and rewards dependent on the commercial success of the endeavor

• There is a steering committee or other mechanism to provide participating rights to the participants

• The participants conduct their joint activities primarily outside of a legal entity

Copyright © 2015 Deloitte Development LLC. All rights reserved.

ASC 808

What it does – ASC 808 provides guidance on the income statement presentation and disclosures related to collaborative arrangements but does not address recognition or measurement matters, for example, determining the appropriate units of accounting, the appropriate recognition requirements for a given unit of accounting, or when the recognition criteria are met.

What it does not do – Thus, even when a collaboration is within the scope of ASC 808, companies must look to other GAAP (possibly by analogy) to determine the appropriate recognition and measurement for the activities subject to the arrangement.

Looking forward – Collaborative arrangements are specifically scoped out of the new issued revenue recognition guidance.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Income Statement Presentation

Transactions with third parties (parties that do not participate in the arrangement) should be reflected in each entity's respective income statement pursuant to the guidance in ASC 605-45

The principal for a given activity will report revenues and expenses on a gross basis.

Payment between participants are to be classified based upon:• Nature of the arrangement and business operations• Contractual terms• Other income statement classification authoritative accounting literature

(apply relevant provisions)• Analogy to authoritative accounting literature (example – if an arrangement

includes reimbursement for R&D costs by entity A to entity B, that portion of the net payment may be classified in entity A’s income statement as R&D expense)

• If no appropriate analogy, use of a reasonable, rational and consistent policy application is allowed

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Determination of Principal vs. Agent

In order to apply the proper accounting treatment to a collaboration agreement, it is important that companies make the appropriate determination of whether the company is acting as the principal or the agent

Appropriate review of the details of the contract are essential to this process

Copyright © 2015 Deloitte Development LLC. All rights reserved.

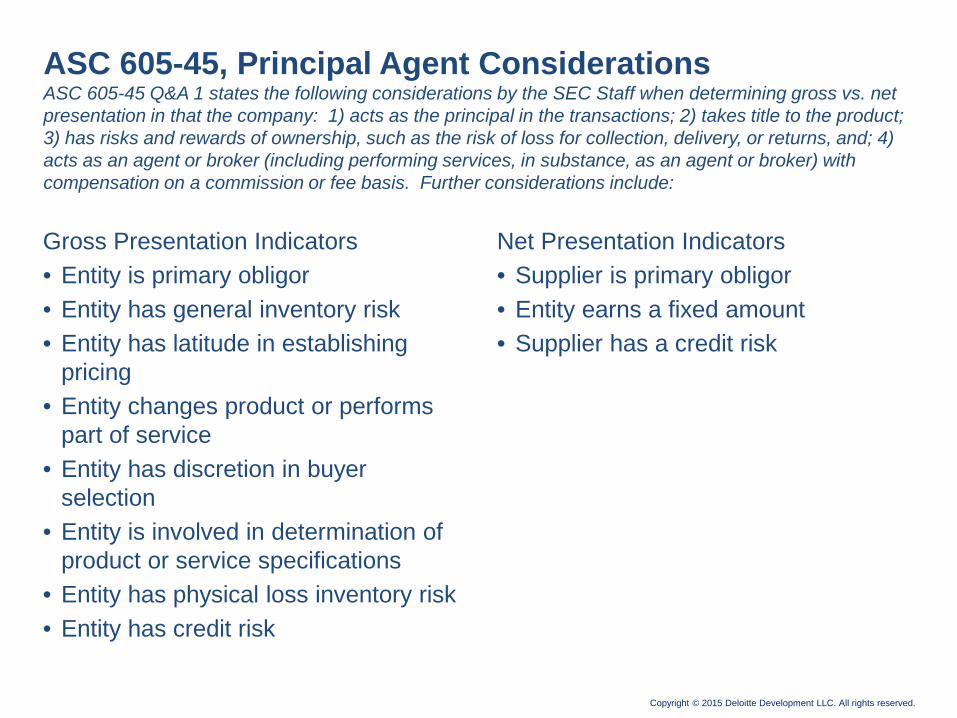

Gross Presentation Indicators• Entity is primary obligor• Entity has general inventory risk• Entity has latitude in establishing

pricing• Entity changes product or performs

part of service• Entity has discretion in buyer

selection• Entity is involved in determination of

product or service specifications• Entity has physical loss inventory risk• Entity has credit risk

Net Presentation Indicators• Supplier is primary obligor• Entity earns a fixed amount• Supplier has a credit risk

ASC 605-45 Q&A 1 states the following considerations by the SEC Staff when determining gross vs. net presentation in that the company: 1) acts as the principal in the transactions; 2) takes title to the product; 3) has risks and rewards of ownership, such as the risk of loss for collection, delivery, or returns, and; 4) acts as an agent or broker (including performing services, in substance, as an agent or broker) with compensation on a commission or fee basis. Further considerations include:

ASC 605-45, Principal Agent Considerations

Multiple Element Arrangements

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Multiple-Element Arrangements

ASU 605-25

• Requires a vendor to evaluate all deliverables in an arrangement to determine whether they represent separate units of accounting.

• Evaluation must be performed at the inception of an arrangement and as each item in the arrangement is delivered.

• No GAAP definition of a “deliverable”• ASU 2009-13 removed previous separation criterion under EITF Issue 00-21

that objective and reliable evidence of the fair value (“VSOE”) of any undelivered items must exist for the delivered items to be considered a separate unit of accounting.

• The selling price of deliverables qualifying for separation must be determined using VSOE, third-party evidence of selling price or by making its best estimate of the selling price.

• The timing and pattern of revenue recognition for a given unit of accounting depends on the nature of the deliverable(s) composing that unit.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

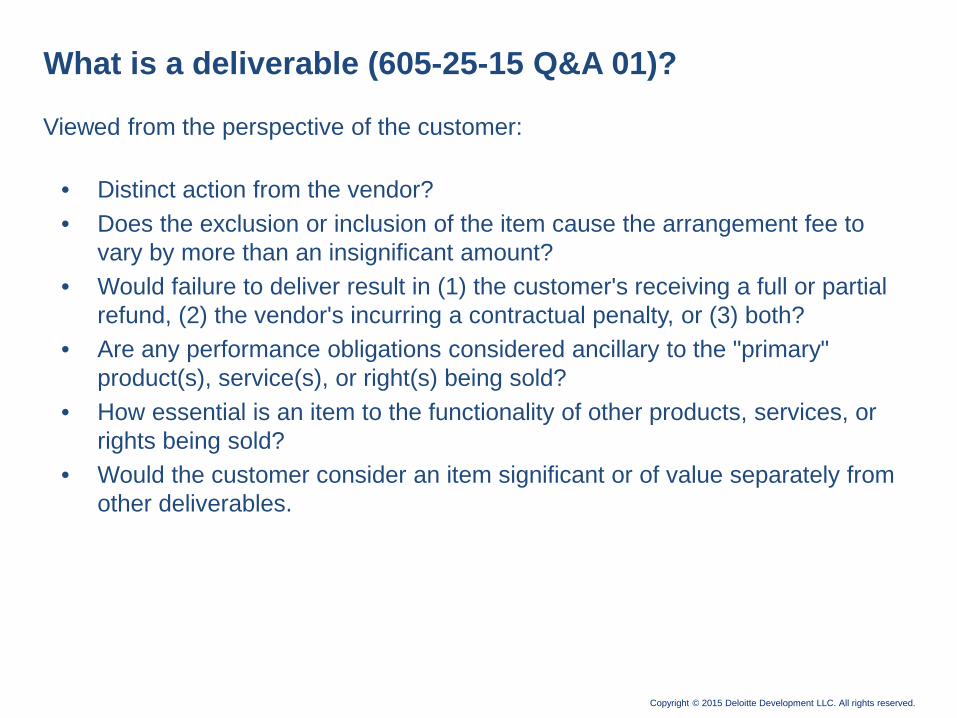

What is a deliverable (605-25-15 Q&A 01)?

Viewed from the perspective of the customer:

• Distinct action from the vendor?• Does the exclusion or inclusion of the item cause the arrangement fee to

vary by more than an insignificant amount?• Would failure to deliver result in (1) the customer's receiving a full or partial

refund, (2) the vendor's incurring a contractual penalty, or (3) both?• Are any performance obligations considered ancillary to the "primary"

product(s), service(s), or right(s) being sold?• How essential is an item to the functionality of other products, services, or

rights being sold?• Would the customer consider an item significant or of value separately from

other deliverables.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

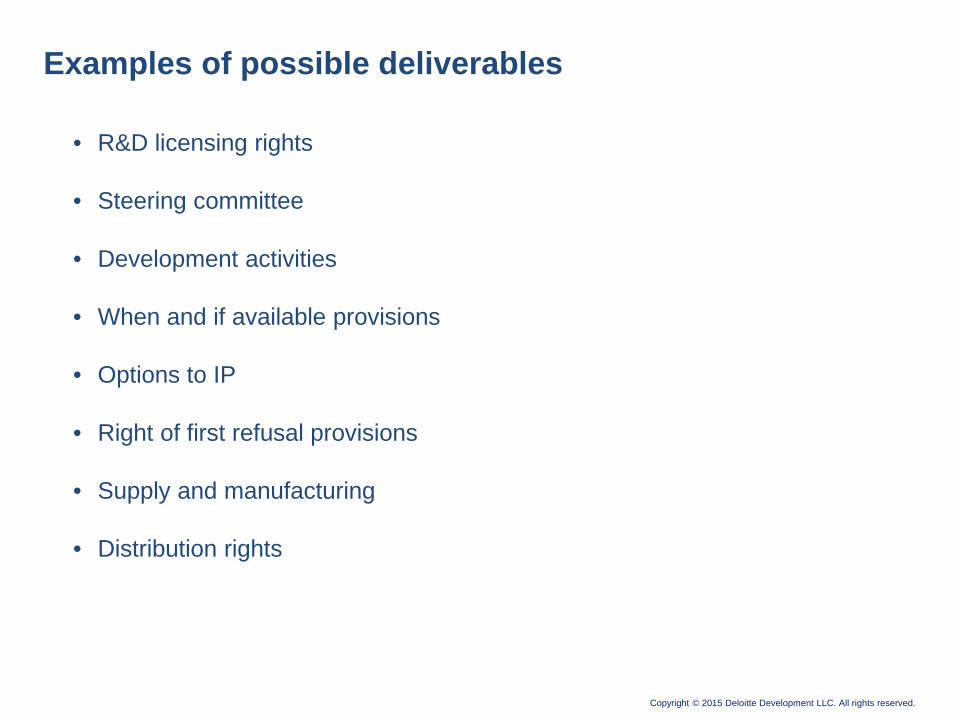

Examples of possible deliverables

• R&D licensing rights

• Steering committee

• Development activities

• When and if available provisions

• Options to IP

• Right of first refusal provisions

• Supply and manufacturing

• Distribution rights

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Stand Alone Value

• Is the undelivered item necessary for the delivered item to have value (i.e., license to IP may not have standalone value without the future R&D)?

• Consider both contractual/legal and practical ability (significant for future manufacturing)

• Does the license provide the customer the ability to have manufacturing performed by others even if intent is for the vendor to manufacturer?

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Allocation of consideration

• Relevant if more than one unit of accounting exist

• Allocation based on relative selling price

• Specified prices in contract are generally irrelevant

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Multiple-Element Arrangements – Example

Revenue Arrangement – Biotech and Pharma

• Facts– Biotech licenses exclusive rights to Pharma for Technology A to develop,

commercialize and manufacture Drug B, using Technology A for 15 years which is the expected patent life of Drug B, if and when approved.

– Biotech provides R&D services on best-efforts basis devoting four full-time equivalents (FTEs) to R&D activities with ultimate objective of receiving FDA or equivalent approval on Drug B.

– Biotech agrees to manufacture Drug B, if successfully developed, for Pharma for a ten year period.

• Arrangement Consideration– Biotech receives $5 million upfront– Biotech receives $2 million upon meeting each of the four substantive milestones– Biotech receives $250,000 per year for each FTE performing R&D activities– Biotech receives cost plus 30 percent for manufacturing Drug B.

All payments are nonrefundable, regardless of whether approval is received. Biotech must perform on a best-efforts basis, and is not obligated to achieve the milestones.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Multiple-Element Arrangements – Example

Revenue Arrangement – Biotech and Pharma (cont’d)

• Discussion of ASC 605-25 Impact

• Determine whether the arrangement has multiple deliverables that should be considered for and meet the criteria for separation

– Three deliverables to consider for separation: 1) license, 2) R&D activities, and 3) contract manufacturing• License for Technology A does not have stand-alone value to Pharma without

the ensuring R&D activities, which is propriety to Biotech• Pharma could not sell the license to another party without Biotech also

agreeing to provide R&D activities• On a combined basis, license and R&D activities may have value as a

separate deliverable, giving consideration to:– Similar arrangements in which Biotech has sold the license and R&D

separately from contract manufacturing– Pharma could sell the combined unit of account to another party– There are no general rights of return in the arrangement

Licensing Arrangements

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Licensing Arrangements

Out-licensing arrangements• Allows a company to license or sell assets to another company which funds

the development

• Licensor receives financial payments, may also receive rights to access program after development

In-licensing arrangements• Allows a company to in-license R&D compounds to quickly expand its

portfolio without the risks and costs involved with substantial R&D, may complement developed in-house compounds

• Additional payments may be made to the licensor when certain milestones are met

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Licensing Arrangements – Straight License

Structure: Straightforward transaction in which licensee receives all rights and licensor receives financial payments in the form of upfronts, milestones and royalties

Rationale: Preferred structure for large biopharma entities, affords licensee immediate and potential future value with no further resource commitment

Frequency: Commonly used structure

Licensee LicensorUpfront, milestones, royalties

Exclusive rights, control

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Licensing ArrangementsRevenue recognition issues to consider when evaluating licensing and royalty arrangements:• Timing of cash collection• Future performance requirements• Required satisfaction of specified criteria

There is no explicit guidance in authoritative accounting literature regarding arrangements for intangible assets such as product rights, patents, etc. which represent the typical licensing arrangements executed within the life sciences industry.

In accounting for these arrangements, entities may consider them to be analogous to licensing and royalty advancements covered in ASC 985-605 (Software); ASC 928-605 (Entertainment — Music); and ASC 926-605 (Entertainment — Films)

For agreements in which the payment represents consideration for the culmination of a separate earnings process, revenue could be recognized immediately (i.e., the specific performance method)

For many other agreements, revenue is more appropriately deferred and recognized over time or production (i.e., the proportional performance method)

The SEC staff indicates in Question 1 of SAB Topic 13.A.3(f) that license fees often represent nonrefundable up-front fees and that "[u]nless the up-front fee is in exchange for products delivered or services performed that represent the culmination of a separate earnings process, the deferral of revenue is appropriate."

SEC Comment Letter Trends

Copyright © 2015 Deloitte Development LLC. All rights reserved.

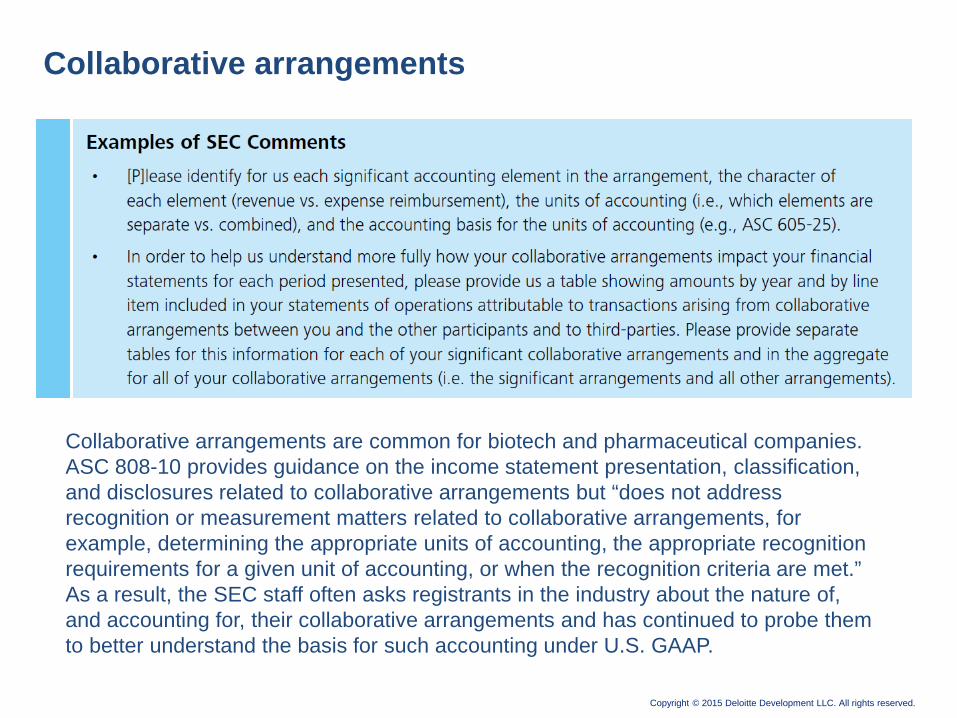

Collaborative arrangements

Collaborative arrangements are common for biotech and pharmaceutical companies. ASC 808-10 provides guidance on the income statement presentation, classification, and disclosures related to collaborative arrangements but “does not address recognition or measurement matters related to collaborative arrangements, for example, determining the appropriate units of accounting, the appropriate recognition requirements for a given unit of accounting, or when the recognition criteria are met.” As a result, the SEC staff often asks registrants in the industry about the nature of, and accounting for, their collaborative arrangements and has continued to probe them to better understand the basis for such accounting under U.S. GAAP.

Copyright © 2015 Deloitte Development LLC. All rights reserved.

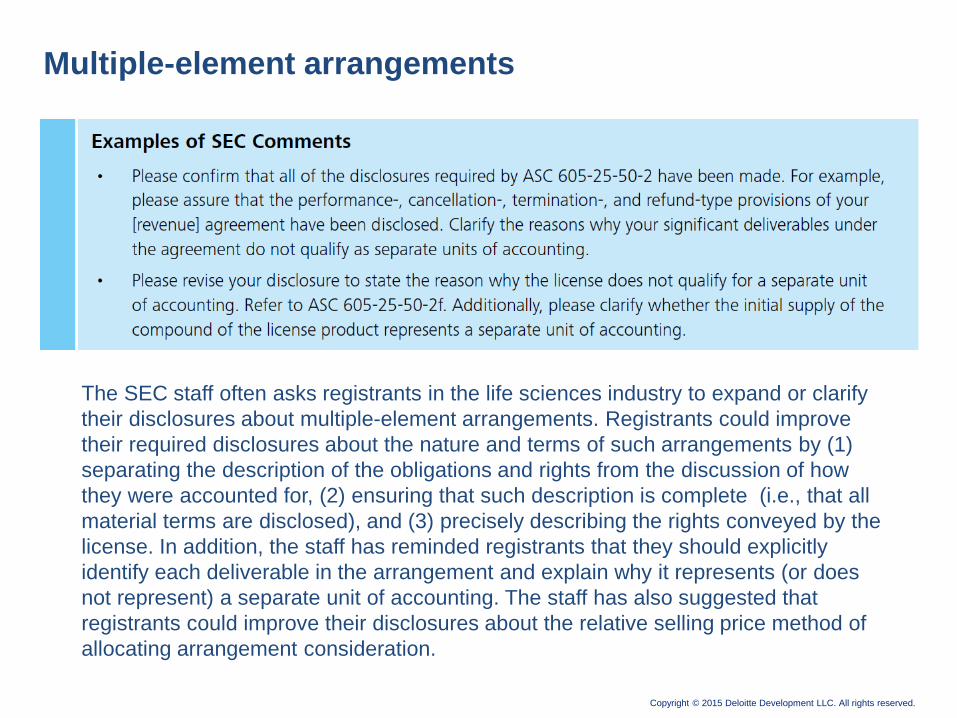

Multiple-element arrangements

The SEC staff often asks registrants in the life sciences industry to expand or clarify their disclosures about multiple-element arrangements. Registrants could improve their required disclosures about the nature and terms of such arrangements by (1) separating the description of the obligations and rights from the discussion of how they were accounted for, (2) ensuring that such description is complete (i.e., that all material terms are disclosed), and (3) precisely describing the rights conveyed by the license. In addition, the staff has reminded registrants that they should explicitly identify each deliverable in the arrangement and explain why it represents (or does not represent) a separate unit of accounting. The staff has also suggested that registrants could improve their disclosures about the relative selling price method of allocating arrangement consideration.