battery industry

TRANSCRIPT

Please refer to important disclosures at the end of this report 1

Strong performance by the battery industry

The ~Rs9,700cr Indian storage batteries sector (as estimated in FY2010) has anorganised market pegged at around ~Rs7,300cr. Over FY2005-10, the batterysector received a boost with industry revenues recording strong ~30% CAGR andnet income registering ~50% CAGR on the back of changing demographics,which in turn supported the secular growth in consumption in the Indian markets.

Growth momentum to sustain

Overall, we estimate the battery sector to register ~19.7% CAGR in revenues overFY2010-13. For the battery manufacturing companies in India, auto andindustrial growth remains the key revenue driver. Industrial segment revenues areestimated to increase at ~19.4% CAGR during FY2010-13, while we expect theauto battery segment revenues to post a CAGR of ~20% during the mentionedperiod. Moreover, we believe that next few years will continue to be aninvestment phase for these companies, as they are operating at almost ~95%utilisation levels in the automotive battery segment and around ~75% in theindustrial segment.

Robust volumes, stable margins to drive earnings growth

Going ahead, we model margins to contract with the LME lead prices estimatedto increase by around 10% annually, which would gradually be passed on with alag effect. We expect Exide Industries (Exide) to outperform Amara Raja Batteries(ARBL) on the earnings front following the increase in the contribution from thecaptive lead smelter to total consumption of lead (almost ~50%). While Exide isset to emerge a clear winner with earnings CAGR of ~17% due to cost savings onraw material front, ARBL is expected to report ~11% earnings CAGR duringFY2010-13.

High returns profile drives higher valuation, caps downside risks

Over the last few years, the battery manufacturers have clocked significantincrease in return ratios on the back of sustained volume growth and highmargins. On an average, these stocks delivered CAGR returns of ~50-60% overthe last five years. We attribute the steady earnings CAGR of ~50-60% as the keyfactor behind this outperformance. Over the next couple of years, profitability ofthe battery manufacturers would continue to be determined by growing demand.With the industry operating at higher capacity utilisation levels and apparentpricing flexibility would result in RoCE and RoE improving going forward and capdownside risks. We believe that investing in these stocks at current valuationswould fetch good returns for investors as the consumption theme plays out infavour of the Indian market. Thus, we maintain an Accumulate on Exide and Buyon ARBL.

Exide Industries CMP Rs158

Target Price Rs171

Recommendation Accumulate

Market Cap (Rs cr) 13,464

52 Week High/Low 169/87

Avg. Daily Volume 367,791

Reuters Code EXID.BO

Bloomberg Code EXID@IN

Amara Raja Batteries CMP Rs213

Target Price Rs261

Recommendation Buy

Market Cap (Rs cr) 1,818

52 Week High/Low 225/131

Avg. Daily Volume 79,508

Reuters Code AMAR.BO

Bloomberg Code AMRJ@IN

Vaishali Jajoo

022-4040 3800 Ext: 344 [email protected]

Yaresh Kothari

022-4040 3800 Ext: 313 [email protected]

Volume ‘Lead’ growth

Auto Ancillary

September 2010

Valuation Summary

Rating CMP Target Price P/E (x) P/BV (x) EV/EBITDA (x) EV/Sales (x) RoE (%)

(Rs) (Rs) FY11E FY12E FY11E FY12E FY11E FY12E FY11E FY12E FY11E FY12E

Exide Accumulate 158 171 20.4 17.8 4.9 4.0 11.2 9.5 2.5 2.0 26.4 24.5

ARBL Buy 213 261 11.9 9.2 2.7 2.1 6.8 5.6 1.0 0.8 24.8 25.5

HBL Power* Not Rated 28 - 7.8 6.4 1.2 1.0 5.8 4.8 0.9 0.7 16.0 17.0

Source: C-line, Bloomberg, Angel Research; Note: *Consensus, Market price as of September 20, 2010

Battery

Auto Ancillary

September 2010 2

Table of Contents

Industry 3

Strong performance by battery industry 4

Growth momentum to sustain 4

Stable lead price, backward integration helped margin expansion 6

Robust volumes to drive earnings growth 7

Expansion to capture volume growth 7

High returns profile drives higher valuation, caps downside risks 8

Stocks outperform on fundamental grounds – Exide excels 9

Exide re-rates on superior performance 10

Exide - ARBL valuation gap contracts 11

Companies 13

Exide Industries - Defensive appeal 14

Amara Raja Batteries - Catching up 30

Annexure 47

Battery Industry - Overview 48

Automotive batteries – Riding secular growth in auto sector 48

Industrial batteries – Growing with economy 53

Key risks 55

Auto Ancillary

September 2010 3

Industry

Auto Ancillary

September 2010 4

Strong performance by the battery industry

The ~Rs9,700cr Indian storage batteries sector (as estimated in FY2010) has an organised market pegged at around ~Rs7,300cr. Over FY2005-10, the battery sector received a boost with industry revenues recording strong ~30% CAGR and net income registering ~50% CAGR on the back of changing demographics, which in turn supported the secular growth in consumption in the Indian markets.

Exhibit 1: Indian battery market – Growth trend

Source: Industry, Company, Angel Research; Note : * CAGR

Exhibit 2: Battery industry’s revenue break-up

Source: Industry, Company, Angel Research

Growth momentum to sustain

The organised battery sector recorded a CAGR of ~14.1% during FY2008-10 aided by the ~10.2% and ~18.8% CAGR registered by the automotive and industrial batteries segments respectively, during the mentioned period. For the battery manufacturing companies in India, auto and industrial growth remains the key revenue driver. Going ahead, the industrial segment revenues are estimated to increase at ~19.4% CAGR over FY2010-13, while the auto battery segment revenue is estimated to post a CAGR of ~20% during the period. Overall, we estimate the battery sector to register ~19.7% CAGR in revenues over the mentioned period.

Exhibit 3: New vehicle sales, increasing vehicle population and healthy industrial growth drives battery demand

Particular FY08 FY09 FY10P FY11E FY12E FY13E CAGR FY2008-10

CAGR FY2010-13E

New OEM vehicle volume ('000 units) 10,370 10,732 13,155 15,008 16,603 18,258 12.6 11.5

yoy growth (%) 3.5 22.6 14.1 10.6 10.0

Vehicle population* ('000 units) 99,626 106,888 115,759 125,704 136,860 149,549 7.8 8.9

yoy growth (%) 7.3 8.3 8.6 8.9 9.3

Batteries Volume

Automotive volume (mn units) 30.7 35.0 40.6 47.9 54.7 60.4 15.0 14.1

yoy growth (%) 14.0 16.1 18.0 14.0 10.5

OEM volume (mn units) 10.1 11.1 13.4 15.8 17.5 19.0 15.1 12.5

yoy growth (%) 9.9 20.4 18.4 10.5 8.8

Replacement volume (mn units) 20.6 23.9 27.3 32.1 37.2 41.4 15.0 14.9

yoy growth (%) 16.0 14.1 17.8 15.7 11.3

Industrial volume (mnAH) 2,220 3,071 3,625 4,119 4,782 5,517 27.8 15.0

yoy growth (%) 38.3 18.0 13.6 16.1 15.4

Source: Industry, SIAM, Company, Angel Research; Note: *Projected

65

21

7

2418 18

2230

20

76

29

57

14 16 19

29

50

16

0

5

10

15

20

25

01020304050607080

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

FY

01-1

0*

FY

05-1

0*

FY

10-1

3E*

(%)(%) Revenue growth (%) Net income growthOperating margin (RHS)

59 60

41 40

0%

20%

40%

60%

80%

100%

FY09 FY10

Automobile Industrial

Auto Ancillary

September 2010 5

We expect the auto original equipment (OE) battery volume to register 13-14% CAGR over FY2010-13 aided by healthy ~12% CAGR in automobile volumes. Auto replacement demand is expected to post 14-15% CAGR in volumes during FY2010-13. We believe that sustained auto volume growth has resulted in a large base for the replacement market. Thus, with a sharp increase in vehicle population, we see a corresponding pick up in replacement demand. Further, positive industry (IIP) cycle, increasing demand from railways and UPS segment would support healthy growth of industrial battery segment.

Exhibit 4: Strong auto, industrial growth to boost battery industry’s revenue

Source: Industry, Company, Angel Research; Note : * CAGR

We believe that the Indian battery sector offers an excellent opportunity for investors to cash in on the strong economic growth and emerging consumerism theme in India. We expect Exide and ARBL to register robust ~21% and ~23% CAGR in net sales and ~17% and ~11% CAGR in net profit respectively, during FY2010-13.

Exhibit 5: Angel’s Battery Universe – Financial Projections

(Rs cr) Exide ARBL CAGR FY2010-13E (%)

FY2010 FY2011E FY2012E FY2013E FY2010 FY2011E FY2012E FY2013E Exide Amara Raja

Revenue 3,794 4,788 5,682 6,691 1,465 1,871 2,267 2,727 20.8 23.0

EBITDA 892 1,065 1,218 1,388 281 273 327 385 15.9 11.0

PAT 537 659 757 859 167 152 197 227 16.9 10.7

Source: Company, Angel Research

Exhibit 6: Revenue growth trend

Source: Company, Angel Research; Note * CAGR

40

1

2218 18 19 19

6

14

25

18 17

10

20

0

5

10

15

20

25

30

35

40

45

FY2009 FY2010 FY2011E FY2012E FY2013E FY08-10* FY10-13E*

(%) yoy growth ind. battery revenue yoy growth auto battery revenue

22 17

36

52

19 12

26 19 18

9

26 21

34

54 64

82

21 12

28 21 20

16

44

23

0

20

40

60

80

100

FY05

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

FY13

E

FY00

-05*

FY05

-10*

FY10

-13E

*

(%) Exide ARBL

Auto Ancillary

September 2010 6

Stable lead price, backward integration helped margin expansion

Stable lead prices and smelter acquisition by industry leader, Exide, helped the industry clock higher margins in the last couple of years. As a result, the impact of the fluctuations in the lead prices on margins has reduced in recent quarters particularly for majors like Exide. The lead smelter acquisition has reduced Exide’s dependence on imports and purchase of pure lead from the market owing to which we model it EBITDA margins in the range of 20-22% going ahead. ARBL is expected to operate at margins of around 14-15% going forward.

Exhibit 7: Sensitivity to Exide’s FY12E EBITDA margin

LME Lead prices ($/kg)

1.9 2.2 2.4 2.6 2.9

Rupe

e-D

olla

r ra

te 41.5 34.7 31.6 28.7 26.6 24.7

43.7 32.3 29.3 26.6 25.0 23.0

46.0 26.7 23.9 21.4 20.0 18.8

48.3 28.4 25.7 23.4 22.2 21.6

50.7 24.2 21.7 19.7 18.9 18.6

Source: Bloomberg, Company, Angel Research

Exhibit 8: Sensitivity to ARBL’s FY12E EBITDA margin

LME Lead prices ($/kg)

1.9 2.2 2.4 2.6 2.9

Rupe

e-D

olla

r ra

te 41.5 23.3 19.9 16.8 14.6 12.9

43.7 21.6 18.3 15.5 13.6 12.4

46.0 20.0 16.9 14.4 12.9 12.1

48.3 18.5 15.7 13.5 12.3 12.0

50.7 17.1 14.6 12.8 12.1 12.2

Source: Bloomberg, Company, Angel Research

Exide procures ~50% of its lead requirement from captive smelters and produces recycled lead, which gives it 10-15% of cost advantage. Imports constitute ~30% of its lead consumption. In comparison, ARBL imports around ~60% of its lead requirements on account of which it operates at lower margins to Exide and is more sensitive to the changes in the LME lead prices.

Exhibit 9: High inventory levels to stabilise lead prices

Source: Bloomberg, Company, Angel Research

Exhibit 10: EBITDA margin trend

Source: Company, Angel Research

Going ahead, we model margins to contract with the LME lead prices estimated to increase by around 10% annually, which would gradually be passed on with lag effect.

0

50,000

100,000

150,000

200,000

250,000

0

1,000

2,000

3,000

4,000

5,000

Aug

-01

Aug

-02

Aug

-03

Aug

-04

Aug

-05

Aug

-06

Aug

-07

Aug

-08

Aug

-09

Aug

-10

Lead inventory (RHS) Lead prices (LHS)(USD/tonne) (tonne)

15 16 16 17 16

24 22 21 21

9

13 14 15

11

19

15 14 14

0

5

10

15

20

25

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%) Exide ARBL

Auto Ancillary

September 2010 7

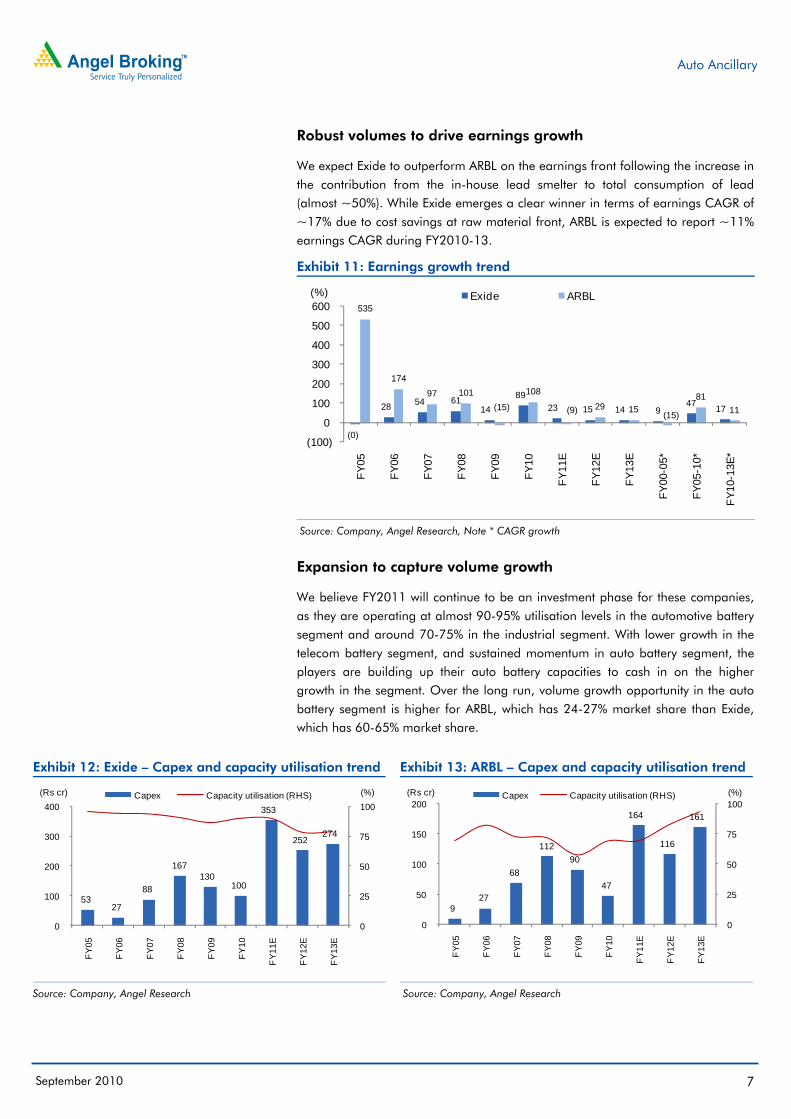

Robust volumes to drive earnings growth

We expect Exide to outperform ARBL on the earnings front following the increase in the contribution from the in-house lead smelter to total consumption of lead (almost ~50%). While Exide emerges a clear winner in terms of earnings CAGR of ~17% due to cost savings at raw material front, ARBL is expected to report ~11% earnings CAGR during FY2010-13.

Exhibit 11: Earnings growth trend

Source: Company, Angel Research, Note * CAGR growth

Expansion to capture volume growth

We believe FY2011 will continue to be an investment phase for these companies, as they are operating at almost 90-95% utilisation levels in the automotive battery segment and around 70-75% in the industrial segment. With lower growth in the telecom battery segment, and sustained momentum in auto battery segment, the players are building up their auto battery capacities to cash in on the higher growth in the segment. Over the long run, volume growth opportunity in the auto battery segment is higher for ARBL, which has 24-27% market share than Exide, which has 60-65% market share.

Exhibit 12: Exide – Capex and capacity utilisation trend

Source: Company, Angel Research

Exhibit 13: ARBL – Capex and capacity utilisation trend

Source: Company, Angel Research

(0)

28 54 61 14

89 23 15 14 9

47 17

535

174 97 101

(15)

108

(9) 29 15 (15)

81 11

(100)

0

100

200

300

400

500

600

FY05

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

FY13

E

FY00

-05*

FY05

-10*

FY10

-13E

*

(%) Exide ARBL

53 27

88

167 130

100

353

252 274

0

25

50

75

100

0

100

200

300

400

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%)(Rs cr) Capex Capacity utilisation (RHS)

9 27

68

112 90

47

164

116

161

0

25

50

75

100

0

50

100

150

200

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%)(Rs cr) Capex Capacity utilisation (RHS)

Auto Ancillary

September 2010 8

Exhibit 14: Exide – Capex v/s FCF

Source: Company, Angel Research

Exhibit 15: ARBL – Capex v/s FCF

Source: Company, Angel Research

We believe that both the companies are well placed in terms of funding their expansion plans owing to strong operating cash flow and low debt/equity ratio. The capacity expansions would broadly be funded through internal accruals.

Exhibit 16: Debt/Equity trend

Source: Company, Angel Research

Exhibit 17: Asset turnover trend

Source: Company, Angel Research

High returns profile drives higher valuation, caps downside risks

Over the last few years, the battery manufacturers have clocked significant increase in return ratios on the back of sustained volume growth and high margins. Going ahead, over the next couple of years, profitability of the battery manufacturers would continue to be determined largely by growing demand. Further, on the back of higher capacity utilisation levels and apparent pricing flexibility the high levels of RoCE and RoE would be maintained going forward in turn capping downside risks.

53 2788

167130 100

353

252 274

42

194

10733

313

459

370

490

617

0

200

400

600

800

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(Rs cr) Capex FCF

927

68

11290

47

164

116

161

(5) (2)

(112)(149)

94

169

(93)

27 22

(200)

(150)

(100)

(50)

0

50

100

150

200

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(Rs cr) Capex FCF

0.6 0.5 0.5

0.3 0.3

0.0 0.0 0.0 0.0 0.1

0.2

0.6

0.9

0.7

0.20.2

0.10.1

0.0

0.2

0.4

0.6

0.8

1.0

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%) Exide ARBL

1.5 1.7

2.0

2.8 2.9 2.9 3.1 3.1 3.2

1.4

1.9 2.1 2.3 2.2

2.5 2.8 2.8 2.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%) Exide ARBL

Auto Ancillary

September 2010 9

Exhibit 18: RoE

Source: Company, Angel Research

Exhibit 19: RoCE

Source: Company, Angel Research

Strong auto and industrial volumes and higher contribution from backward integration coupled with a significant correction in input costs led to consistent earnings upgrades driving the outperformance of the stocks. Going ahead too, with the long-term consumption story of India intact, we expect the companies (Exide and ARBL) to continue to outperform the benchmark indices.

Stocks outperform on fundamental grounds – Exide excels

On the bourses, over the past ten years, most battery stocks broadly outperformed the benchmark indices reflecting sustained volume growth, significant margin expansion and steady earnings growth. Exide in particular registered superior performance during the period.

Exhibit 20: Exide, ARBL outperform benchmark

Source: Bloomberg, Angel Research

Exhibit 21: ARBL outperforms on higher earnings growth

Source: Bloomberg, Angel Research

In the recent past, most battery players witnessed a sharp rally and touched their life-time highs. Leader Exide is perceived as a defensive play (low beta) due to consistent growth performance, strong cash-flow and prudent execution track record. Thus, during the economic downturn it not only exhibited significant strength, but also outperformed the benchmark indices over the last five years. ARBL followed suit with strong growth in the industrial battery segment (telecom). Nonetheless, the ARBL stock fluctuated and reflected the growth contraction during the period due to contraction in demand of telecom batteries.

Over FY2005-10, ARBL has shown relative outperformance to Exide largely owing to higher contribution from the telecom battery segment. However, the recent structural shift in the telecom industry has impacted the industrial telecom battery

18 20

25 30

25

31 26 24 23

5

12

21

33

22

35

25 25 23

0

10

20

30

40

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%) Exide ARBL

16 20

26

33 32

41 37 34 32

3

13

20 26

17

35

28 29 29

0

10

20

30

40

50

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%) Exide ARBL

0

1,000

2,000

3,000

4,000

5,000

6,000

Apr

-01

Dec

-01

Aug

-02

Apr

-03

Dec

-03

Aug

-04

Apr

-05

Dec

-05

Aug

-06

Apr

-07

Dec

-07

Aug

-08

Apr

-09

Dec

-09

Aug

-10

Sensex ARBL Exide

0

500

1,000

1,500

2,000

Apr

-05

Sep-

05

Feb-

06

Jul-0

6

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug

-08

Jan-

09

Jun-

09

Nov

-09

Apr

-10

Sep-

10

Sensex ARBL Exide

Auto Ancillary

September 2010 10

business of these companies, wherein the demand for telecom batteries has seen a sharp correction in the growth rate. This in turn resulted in loss of bargaining power and lower realisation from the telecom battery segment. As a result, companies generating higher revenues from the telecom battery segment (ARBL and HBL) relatively underperformed the market leader, Exide, in the recent past.

Exhibit 22: Absolute and relative performance CMP (Rs) 1 Month 3 Month 6 Month 1 Year 3 Year 5 Year

Absolute Returns (%)

Exide 158 7.5 23.7 37.0 73.6 163.7 681.1 Amara Raja 213 12.9 21.5 27.5 54.1 121.2 896.0 HBL 28 14.1 (12.2) (19.9) (17.3) (17.2) 7.8 BSE Auto 9,397 5.9 15.5 23.2 42.3 82.9 162.5 BSE Sensex 19,906 8.2 13.3 13.2 18.9 21.8 134.2 Relative Returns v/s Sensex (%)

Exide 158 (0.7) 10.4 23.8 54.7 142.0 546.9 Amara Raja 213 4.7 8.2 14.3 35.2 99.4 761.8 HBL 28 5.9 (25.5) (33.1) (36.2) (38.9) (126.4) BSE Auto 9,397 (2.3) 2.2 9.9 23.4 61.2 28.3

Source: Bloomberg, Angel Research; Note: Market price as of September 20, 2010

On an average, these stocks delivered CAGR returns of ~50-60% over the last five years. We attribute the steady earnings CAGR of ~50-60% as the key factor behind this outperformance.

Exide re-rates on superior performance

In terms of their one-year forward P/Es, most companies are trading in line with their three-year averages, but at a ~20-30% discount to their peak valuations of FY2007-08. The P/E of Exide has sharply expanded in the past five years on the back of growth in domestic volumes. We note that, Exide’s multiple expansion and investment strategies along with backward integration accelerated in FY2008. Moreover, the company is immune to the fiscal pressures in the developed markets owing to which there has been high appetite for such defensives during the global downturn. On the other hand, companies generating higher revenues from industrial battery segment like ARBL have relatively underperformed due to reduced demand in telecom segment batteries in the last couple of years.

Exhibit 23: Exide – P/E multiple expands

Source: Bloomberg, Company, Angel Research

Exhibit 24: ARBL – P/E tracked industry cycle

Source: Bloomberg, Company, Angel Research

0

5

10

15

20

25

30

Apr

-01

Dec

-01

Aug

-02

Apr

-03

Dec

-03

Aug

-04

Apr

-05

Dec

-05

Aug

-06

Apr

-07

Dec

-07

Aug

-08

Apr

-09

Dec

-09

Aug

-10

One-yr forward P/E Three-yr average P/E

Long term average P/E(x)

0

5

10

15

20

25

30

Apr

-01

Dec

-01

Aug

-02

Apr

-03

Dec

-03

Aug

-04

Apr

-05

Dec

-05

Aug

-06

Apr

-07

Dec

-07

Aug

-08

Apr

-09

Dec

-09

Aug

-10

One-yr forward P/E Three-yr average P/ELong term average P/E

(x)

Auto Ancillary

September 2010 11

Exide - ARBL valuation gap contracts

ARBL entered the auto battery segment in 2000 and gained significant market share, which was captured in the stock performance over FY2001-03 and it traded at a significant premium to leader Exide. However, simultaneously ARBL also increased its investments in the industrial (specifically telecom) battery segment, and the stock tracked the industry cycles. Thus, ARBL’s latest underperformance to Exide reflected the lower demand for telecom battery segment.

Exhibit 25: Exide, ARBL – Relative P/E performance

Source: Bloomberg, Company, Angel Research

Exhibit 26: ARBL – Premium/Discount to Exide

Source: Bloomberg, Company, Angel Research; Note: Exide P/E adjusted for

Insurance business

ARBL is currently trading at ~35% discount to industry leader, Exide (adjusted for insurance business). The gap is due to Exide's leadership position, higher margins (backward integration through acquisition of lead smelters) and its less dependence on the telecom battery segment. However, ARBL products have exhibited strong performance and continuously increased market share through innovative marketing strategies over the last ten years. ARBL is also in the process of channelising its efforts to increase market share in the auto battery segment through capacity, technology, customer and market expansion. Improved fundamentals are expected to perk up the company’s return ratios compared to its historical levels. Thus, ARBL’s valuation has increased on sustained volume growth and earnings visibility, and the valuation gap with Exide has reduced to reasonable levels of ~35% (as against five year average discount of ~50%).

We believe that investing in these stocks at current valuations would fetch good returns for investors as the consumption theme plays out in favour of the Indian market.

Exhibit 27: Global valuation – Relative

(US $mn) P/E (x) P/B (x) EV/EBITDA (x) EV/Sales (x)

Market Cap Sales* PAT* FY11E FY12E FY11E FY12E FY11E FY12E FY11E FY12E

Exide Technologies, USA 371 2,685 (12) 9.0 6.7 - - 4.4 4.0 0.1 0.1

Johnson Controls# 19,923 28,497 (338) 15.1 12.3 2.0 1.8 9.2 7.5 0.6 0.5

GS Yuasa Corp 2,911 2,666 70 28.8 22.6 2.3 2.2 10.5 8.7 0.9 0.8

Enersys 1,240 1,579 62 11.8 9.9 - - 6.7 5.7 0.7 0.6

Exide Industries 2,946 830 118 20.4 17.8 4.9 4.0 11.2 9.5 2.5 2.0

Amara Raja Batteries 398 321 37 11.9 9.2 2.7 2.1 6.8 5.6 1.0 0.8

HBL Power System 155 243 22 7.8 6.4 1.2 1.0 5.8 4.8 0.9 0.7

Source: Bloomberg, Company, Angel Research; Note: # Year end September, * Latest financial year-end, Market price as on September 20, 2010

0

5

10

15

20

25

30

Apr-

01

Dec

-01

Aug

-02

Apr-

03

Dec

-03

Aug

-04

Apr-

05

Dec

-05

Aug

-06

Apr-

07

Dec

-07

Aug

-08

Apr-

09

Dec

-09

Aug

-10

(x) AMRL Exide Adj. for Insurance

(90)(80)(70)(60)(50)(40)(30)(20)(10)

0

Apr

-04

Nov

-04

Jun-

05

Jan-

06

Aug-

06

Mar

-07

Oct

-07

May

-08

Dec

-08

Jul-0

9

Feb

-10

Sep-

10

(%) prem./ disc. to Exide Three-yr average Prem/DiscFive-yr average Prem/Disc

Auto Ancillary

September 2010 12

Exhibit 28: EV/Sales

Source: Bloomberg, Company, Angel Research

Exhibit 29: EV/EBITDA

Source: Bloomberg, Company, Angel Research

Exhibit 30: P/E

Source: Bloomberg, Company, Angel Research

Exhibit 31: P/CEPS

Source: Bloomberg, Company, Angel Research

Exhibit 32: P/BV

Source: Bloomberg, Company, Angel Research

Exhibit 33: PEG

Source: Bloomberg, Company, Angel Research

3.2

2.5

2.01.7

1.21.0

0.8 0.7

0

1

1

2

2

3

3

4

FY10 FY11E FY12E FY13E

Exide ARBL(x)14

11

9 8

7 7 6

5

0

5

10

15

FY10 FY11E FY12E FY13E

(x) Exide ARBL

25

20 18

16

11 12 9 8

0

10

20

30

FY10 FY11E FY12E FY13E

(x) Exide ARBL

22

1816

14

9 97 6

0

5

10

15

20

25

FY10 FY11E FY12E FY13E

(x) Exide ARBL

6

5

4 3 3

3 2

2

0

2

4

6

8

FY10 FY11E FY12E FY13E

(x) Exide ARBL

0.3

0.9

1.2 1.2

0.1

0.3

0.5

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

FY10 FY11E FY12E FY13E

Exide ARBL(x)

Auto Ancillary

September 2010 13

Companies

Please refer to important disclosures at the end of this report 14

Exide Industries is a leader in the domestic battery industry. Strong brand image and capacity addition will enable Exide to cater to the burgeoning demand for auto and industrial batteries, offering a clear growth visibility going ahead. Moreover, with increased lead sourcing from captive smelters and focus on higher-margin replacement segment will improve profitability and return ratios. At Rs158, the stock is trading at 20.4x FY2011E and 17.8x FY2012E earnings. We estimate Exide to post a 21.1% revenue CAGR over FY2010–13E, leading to a 16.9% earnings CAGR. We maintain Accumulate on the stock with an SOTP Target Price of Rs171. Owing to Exide’s defensive appeal and healthy and consistent fundamentals, we value its core operations at 17.3x (20% premium to historical average of 14.4x) its FY2012E earnings at Rs154. We have valued Exide’s stake in ING Vysya Life Insurance at Rs11/share on FY2012E NBAP and have assigned a value of Rs6/share to lead smelters (8x FY2012E PAT).

Robust demand scenario for automotive and industrial batteries: We expect auto and industrial battery market to post revenue CAGRs of 20% and 19.4%, respectively, over FY2010–13E, driven by strong demand for batteries. As such, we expect Exide to register revenue CAGRs of 20.9% and 21.7% in auto and industrial batteries, respectively, leading to overall gross revenue growth of 21.1%.

Market leader with wider reach and strong pricing power: Exide enjoys a firm pricing power, owing to its strong brand equity and well-entrenched pan India distribution network. We believe Exide is in a position to leverage its market leadership and pricing power to pass on cost increases, thereby improving its realisation, which is estimated to register a ~6% CAGR over FY2010–13E.

Captive sourcing reduces impact of lead price volatility: Exide expects to increase lead sourcing from captive smelters to ~70% in FY2012E (~50% in FY2010). We believe captive sourcing of lead reduces the raw material costs by 10-15%. Thus, our sensitivity analysis suggests that every 10% increase in sourcing from the captive smelters results in EBITDA margins expanding by ~50bp (assuming stable lead prices).

Capacity expansion to increase volumes: To cater to growing demand, Exide plans to increase its two-wheeler and four-wheeler battery capacity by 28% and 60%, respectively, with an investment of Rs400cr in FY2011E. With utilisation set to remain at high levels, we expect Exide to post volume CAGRs of 13.9% and 15.6% in the auto and industrial battery segments, respectively.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 3,393 3,794 4,788 5,682

% chg 19.3 11.8 26.2 18.7

Net Profit 283 537 659 757

% chg 14.2 89.7 22.6 14.9

EBITDA (%) 16.1 23.5 22.2 21.4

EPS (Rs) 3.6 6.3 7.7 8.9

P/E (x) 44.6 25.1 20.4 17.8

P/BV (x) 10.4 6.1 4.9 4.0

RoE (%) 25.0 31.0 26.4 24.5

RoCE (%) 31.7 40.8 36.6 34.3

EV/Sales (x) 3.9 3.2 2.5 2.0

EV/EBITDA (x) 23.9 13.7 11.2 9.5 Source: Company, Angel Research; Note: Market price as on September 20, 2010

ACCUMULATE CMP Rs158 Target Price Rs171

Investment Period 12 Months Stock Info

Sector

Bloomberg Code

Shareholding Pattern (%)

Promoters 46.0

MF / Banks / Indian Fls 28.0

FII / NRIs / OCBs 14.5

Indian Public / Others 11.5

Abs. (%) 3m 1yr 3yr

Sensex 13.3 18.9 21.8

Exide Industries 23.7 73.6 163.7

Face Value (Rs)

BSE Sensex

Nifty

Reuters Code

13,464

0.65

169/87

367,791

Auto Ancillary

Avg. Daily Volume

Market Cap (Rs cr)

Beta

52 Week High / Low

1

19,906

5,980

EXID.BO

EXID@IN

Vaishali Jajoo

022-4040 3800 Ext: 344 [email protected]

Yaresh Kothari

022-4040 3800 Ext: 313 [email protected]

Exide Industries Defensive appeal

Auto Ancillary

September 2010

Exide Industries | Auto Ancillary

September 2010 15

Investment rationale

Auto and industrial batteries: Robust demand scenario

The automotive and industrial battery segments have been witnessing strong growth post the economic downturn, driven by robust demand-pull on account of higher auto and industrial production and increased consumer spending. We expect the auto and industrial battery segments to continue to grow, generating robust revenue CAGRs of ~20% and ~19.4%, respectively, over FY2010–13E. Hence, we forecast Exide to register strong revenue CAGRs of 20.9% and 21.7% in the auto and industrial battery segments, respectively.

Automotive OEM segment

The automotive OEM segment has registered strong sales volume post the economic downturn, and domestic demand continues to witness a strong traction across all segments. The prospect for automotive batteries looks encouraging, supported by the fact that major global automotive players have set up their base in India due to low production cost and lower penetration levels. We expect volume growth to be robust and forecast passenger vehicles, commercial vehicles and two-wheelers to post CAGRs of ~13%, ~12% and ~11%, respectively, in sales between FY2010–13E, leading to sustainable demand for batteries. Consequently, Exide, which caters to 65–67% of OEM demand, is set to benefit from the expected surge in vehicle production over FY2010–13E.

Exhibit 1: Volumes to maintain growth momentum

Source: Company, Angel Research

Exhibit 2: Auto battery revenue to register 20.9% CAGR

Source: Company, Angel Research

Automotive replacement segment

The average life of an automotive battery is 3–4 years, after which it needs to be replaced; there could be as much as three battery replacements in a vehicle’s life. Going ahead, demand for replacement batteries is expected to continue to be buoyant, led by a strong base of vehicles and burgeoning automotive OEM sales.

Exide derives 48–50% of its overall revenue from the automotive replacement segment. The company has a 60-62% market share in the branded replacement market. Exide is looking to expand its market share at the cost of unorganised players, using its excellent sales and distribution network. We believe Exide is well placed to capitalise on the opportunity going ahead, given a promising outlook for the replacement market.

11.9 13.2

14.5 15.8

18.8 21.2

23.3

(5)

0

5

10

15

20

25

0

5

10

15

20

25

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(mn units) Auto battery volume yoy growth (RHS)

1,668

2,561 2,905 3,108

3,975

4,683

5,495

0

10

20

30

40

50

60

0

1,000

2,000

3,000

4,000

5,000

6,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(Rs cr) Auto battery revenue yoy growth (RHS)

Exide derives ~69% and 31% of its revenuefrom the automotive and industrial batterysegments, respectively

Exide derives 48–50% of its overallrevenue from the automotive replacementsegment

Exide Industries | Auto Ancillary

September 2010 16

Industrial battery segment

Demand for industrial batteries surged in last ten years largely owing to favourable economic scenario and growth in industrial activity. Further, during FY2007-09, largely due to significant boom in the telecom sector the segment recorded substantial jump in volumes. (Telecom sector uses batteries as a backup power source for telecom towers.) However, due to the slowdown in the telecom space, we expect demand for telecom batteries to remain subdued. Demand will mainly be driven by replacement demand for telecom batteries, which have a useful life of 5–6 years.

Exhibit 3: Ind. battery volumes to post a 15.6% CAGR

Source: Company, Angel Research

Exhibit 4: ...driving growth in industrial revenue

Source: Company, Angel Research

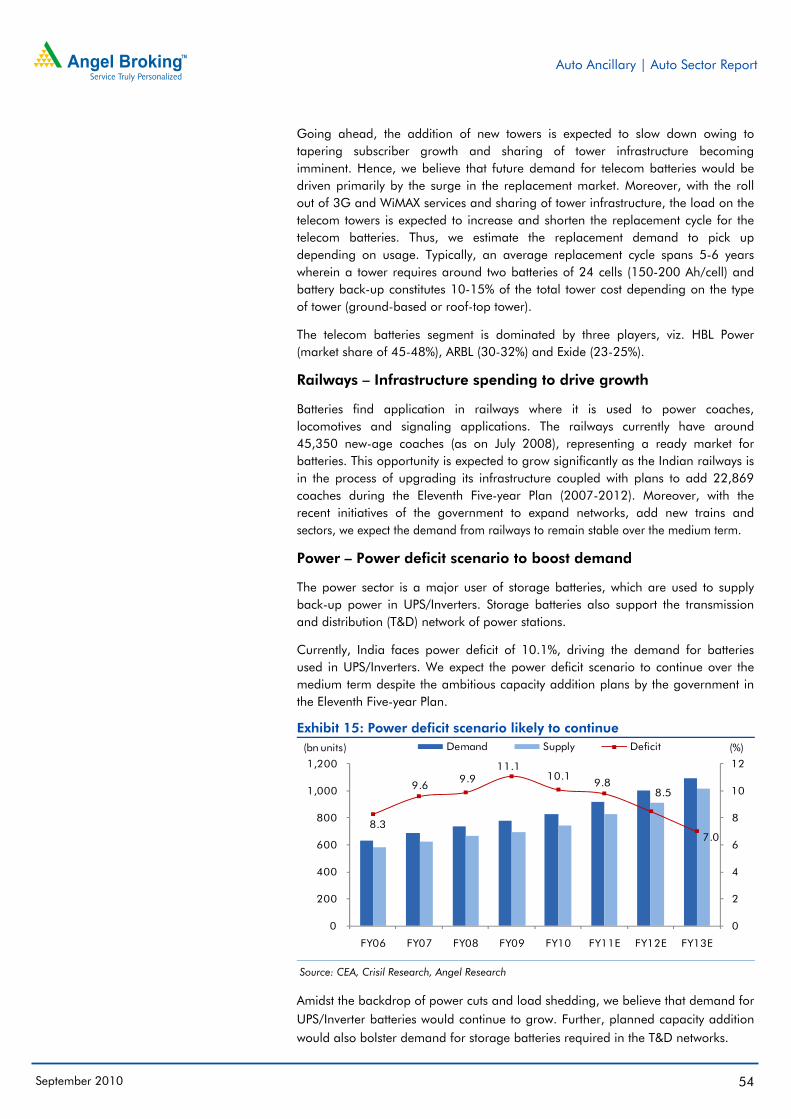

We expect industrial battery demand to be mainly driven by demand from the power back-up segment (UPS) and railways. Over the last five years, battery demand in the UPS/inverter segment has witnessed a 15% CAGR, driven by large-scale computerisation of banking networks and government departments and power deficit over the last few years (10.1% in FY2010). We believe demand for UPS/inverter batteries will continue to grow, as the power demand-supply gap will continue over the medium term, with deficit to be ~7.0% in FY2013E.

959 1,170

1,324 1,450

1,717

1,992

2,238

0

5

10

15

20

25

0

500

1,000

1,500

2,000

2,500

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(mnAH) Ind battery volume (mnAH) yoy growth (RHS)

715

1,019 1,269

1,397

1,753

2,117

2,516

0

5

10

15

20

25

30

35

40

45

0

500

1,000

1,500

2,000

2,500

3,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(Rs cr) Ind battery revenue yoy growth (RHS)

UPS/inverter batteries to drive industrialbattery demand

Industrial battery segment’s revenue topost a 21.7% CAGR over FY2010–13E

Exide Industries | Auto Ancillary

September 2010 17

Market leader with wider reach and strong pricing power

Exide is a dominant player in the automotive battery (OEM and replacement) and industrial battery segments with market share of 60-65% and 40–45% respectively.

Exide has leveraged upon its brand equity, better quality proposition and wider reach to consolidate its position in the market, which gives it a superior pricing power compared to peers. Over the years, Exide has been able to improve its realisation across the automobile and industrial battery businesses, which has more than offset the movements in input prices. We expect Exide to continue to leverage upon its market leadership position and pricing power, which would enhance the company’s ability to pass on cost increases in the future as well. Hence, we expect average realisation to grow at a ~6% CAGR over FY2010–13E.

Exhibit 5: Market share across segments

Source: Company, Angel Research

Exhibit 6: Average realisation to remain strong

Source: Company, Angel Research

Along with strong brand equity, Exide has a well-entrenched distribution network across India. The company has close to 38,500 retail outlets for aftermarket sales, over 9,000 main dealers and 210 hub offices, which the company plans to increase to 250 by the end of FY2011E and further to 510 by FY2013E. Exide operates through authorised distributors and dealers who, in addition to selling to consumers, sell to a tertiary distribution network, which constitutes garages and is called the ‘Humsafar Partner’ network (~21,970 partners). The company also has a separate distribution network called the ’C Dealer’ network (~500 dealers) for heavy commercial vehicles and ‘Kisaan Dealer’ network (~3,197 dealers) for tractors. On the back of its excellent service and distribution network, which is the largest among battery manufacturers, Exide continues to penetrate the replacement market.

6575

3762

5535

4080

9030

35

0 25 50 75 100

Auto (OE)Auto (OE) - PV

Auto (Replacement) incl. unorganisedBranded (Replacement)

Two WheelersPower ProjectsUPS/Inverters

TractionCap Lamps

TelecomRailways

(%)(10)

0

10

20

30

40

50

0

500

1,000

1,500

2,000

2,500

3,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(Rs) Average realisation/unit yoy growth (RHS)

Exide Industries | Auto Ancillary

September 2010 18

Captive lead sourcing reduces impact of lead price volatility

Lead is the key raw material for Exide, accounting for 75–80% of its raw-material cost. The company acquired two smelters to recycle used lead. This helped in reducing the vulnerability of rising lead prices and augmented domestic availability of lead for Exide. These acquisitions helped Exide to increase its use of recycled lead and lead alloys for making storage batteries. This, in turn, reduced the company's dependence on imported lead in FY2010 to ~32% (~36% in FY2009).

Total lead supplied by the captive smelter increased to ~50% in FY2010 from ~35% in FY2009. Exide has benefitted from its captive sourcing strategy, as lead sourcing from captive smelters is 10–15% cheaper compared to market rates. Margins during FY2010 were substantially higher compared to average margins of 18.1% in FY2007–10.

Exhibit 7: Lead prices v/s EBITDA margin

Source: Bloomberg, Company, Angel Research

Exhibit 8: Captive lead sourcing benefits Exide

Source: Company, Angel Research

Going forward, the company plans to further increase sourcing from its smelters to ~55% in FY2011E and ~70% by FY2012E. Hence, the company is expanding its lead smelter capacity to 100,000tpa by March 2011. Going ahead, we model margins to contract with the LME lead prices estimated to increase by around ~10% annually, which would gradually be passed on with lag effect. We expect Exide to leverage upon its low-cost structure relative to its competitors.

We have assumed a ~10% increase in lead prices in FY2011E, from ~US $1,990/tonne to ~US $2,180/tonne, followed by another ~10% rise in FY2012E to ~US $2,400/tonne.

0

5

10

15

20

25

30

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1QF

Y08

2QF

Y08

3QF

Y08

4QF

Y08

1QF

Y09

2QF

Y09

3QF

Y09

4QF

Y09

1QF

Y10

2QF

Y10

3QF

Y10

4QF

Y10

1QF

Y11

FY

11E

FY

12E

FY

13E

(%)(US $/tonne) Avg. Lead Price (LHS) EBITDA Margin (RHS)

0

5

10

15

20

25

0

10

20

30

40

50

60

70

80

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(%) Captive consumption EBITDA Margin (RHS)

Exide acquired 100% in Tandon Metalsin October 2007 and 51% in LeadageAlloys in June 2008. In August 2010,the stake in Leadage Alloys wasincreased to 100%

Exide Industries | Auto Ancillary

September 2010 19

Exhibit 9: Impact of captive sourcing on FY2012E EBITDA margins

Cap

tive

sour

cing

(%) Lead price (Rs/kg)

114.7 120.7 127.1 133.5 140.1

70 26.1 23.8 21.4 19.1 16.6

60 25.6 23.3 20.9 18.5 16.0

50 25.1 22.8 20.4 18.0 15.5

40 24.7 22.4 19.9 17.5 14.9

30 24.2 21.9 19.4 16.9 14.4

Source: Bloomberg, Company, Angel Research

Our sensitivity analysis suggests that every 10% increase in sourcing from the captive smelters, EBITDA margins expands by ~50bp (assuming stable lead prices).

Capacity expansion to increase volume growth

Exide has been operating at ~90% utilisation levels over the past five years. The company plans to increase its battery capacity with an investment of Rs400cr in FY2011E to cater to growing demand. Exide plans to increase its two-wheeler battery capacity to 15.4mn units from 9.6mn units by setting up a new plant at Ahmednagar, Maharashtra, at a cost of Rs80cr. The company also plans to increase its four-wheeler capacity to 10.2mn units from 8mn units by FY2011.

Though the electric vehicle (EV) segment in India is still at a nascent stage, the company wants to be prepared for the opportunity as and when it arises. Hence, it plans to spend Rs40cr on EV battery capacity over the next 2–3 years.

Exhibit 10: Utilisation to remain at high levels

Source: Company, Angel Research

Exhibit 11: Adding capacities to meet demand

Source: Company, Angel Research

As a result of increased capacity, we believe Exide is well placed to meet the rising automotive battery demand. We estimate the overall utilisation level to remain at 78–80% in FY2013E. We expect Exide to post volume CAGRs of 13.9% and 15.6% in the automotive and industrial battery segments, respectively.

18.3 19.8 22.7 24.2

29.1

37.8 41.6

0 10 20 30 40 50 60 70 80 90 100

0

5

10

15

20

25

30

35

40

45

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(mn units) Installed Capacity Utilisation (RHS)

0

2

4

6

8

10

12

14

16

18

2-wheeler 4-wheeler

(mn units) FY10 FY11E

60%

28%

Exide Industries | Auto Ancillary

September 2010 20

Financial performance

Net revenue to post a 20.8% CAGR over FY2010–13E

We expect Exide to post a 20.8% CAGR in its net revenue over FY2010–13E, driven by volume growth and improved realisation. Overall, battery volume (mnAH terms) is expected to grow at a 14.1% CAGR over FY2010–13E. We forecast realisation to improve at a ~6% CAGR during the same period.

Exhibit 12: 14.1% CAGR in volume over FY2010–13E

Source: Company, Angel Research

Exhibit 13: ...will lead to an 20.8% revenue CAGR

Source: Company, Angel Research

Exhibit 14: Key assumptions Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E FY2013E

Storage Batteries ('000 units) 17,686 17,996 19,109 21,899 25,977 29,405 32,534

% yoy chg 22.1 1.8 6.2 14.6 18.6 13.2 10.6

Realisation per Battery (Rs) 1,347 1,978 2,206 2,069 2,216 2,324 2,474

% yoy chg 10.8 46.8 11.5 (6.2) 7.1 4.9 6.5

Million Ampere Hours (mnAH) 2,721 3,124 3,475 3,949 4,675 5,296 5,861

% yoy chg - 14.8 11.2 13.6 18.4 13.3 10.7

Total Revenue 2,383 3,606 4,233 4,542 5,769 6,846 8,062

Automotive (Rs cr) 1,668 2,561 2,905 3,108 3,975 4,683 5,495

% yoy chg - 53.6 13.4 7.0 27.9 17.8 17.3

Industrial (Rs cr) 715 1,019 1,269 1,397 1,753 2,117 2,516

% yoy chg - 42.6 24.5 10.1 25.5 20.8 18.8

Other (Rs cr) 0.1 25.5 59.8 36.7 40.8 45.4 50.8

Source: Company, Angel Research

EBITDA to grow at a CAGR of 15.9% over FY2010-13E

Exide’s captive lead sourcing is expected to increase from ~50% in FY2010 to ~70% by FY2013E. We believe this will mitigate the impact of increase in lead prices to a certain extent. We expect margins to be in the range of 21-22% going forward. Thus, EBITDA is expected to register a 15.9% CAGR over FY2010–13E.

2,721 3,124

3,475 3,949

4,675 5,296

5,861

0

5

10

15

20

25

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(mnAH ) Overall volumes yoy growth (RHS)

1,870

2,845 3,393

3,794

4,788

5,682

6,691

0

10

20

30

40

50

60

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(Rs cr) Net sales yoy growth (RHS)

Exide Industries | Auto Ancillary

September 2010 21

Exhibit 15: Lead prices expected to remain stable

Source: Bloomberg, Company, Angel Research

Exhibit 16: EBITDA margins to stabilise around 21-22%

Source: Bloomberg, Company, Angel Research

Return ratios expected to remain healthy

We forecast net profit to increase to Rs859cr in FY2013E (Rs537cr in FY2010), witnessing a 16.9% CAGR over FY2010–13E. We expect return ratios to remain strong, mainly driven by the increase in asset turnover along with high operating margins. Exide’s RoE and RoCE are expected to remain high at 24-27% and 34-37%, respectively, in line with its historical levels on account of higher profitability.

Exhibit 17: Net profit to grow at a 16.9% CAGR

Source: Company, Angel Research

Exhibit 18: Return ratios to remain strong

Source: Company, Angel Research

0

50,000

100,000

150,000

200,000

250,000

0

1,000

2,000

3,000

4,000

5,000

Aug-

01

Aug-

02

Aug-

03

Aug-

04

Aug-

05

Aug-

06

Aug-

07

Aug-

08

Aug-

09

Aug-

10

(tonne)(USD/tonne) Lead inventory (RHS) Lead prices (LHS)

0

5

10

15

20

25

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY

07

FY

08

FY

09

FY

10

FY

11E

FY

12E

FY

13E

(%)(US $/tonne) Avg. Lead Price (LHS) EBITDA Margin (RHS)

0 10 20 30 40 50 60 70 80 90 100

0 100 200 300 400 500 600 700 800 900

1,000

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%)(Rs cr) Net profit yoy growth (RHS)

25.4 29.5

25.0

31.0 26.4 24.5 22.8

26.0

33.1 31.7

40.8 36.6

34.3 32.3

0 5

10 15 20 25 30 35 40 45

FY07 FY08 FY09 FY10 FY11E FY12E FY13E

(%) RoE RoCE

Exide Industries | Auto Ancillary

September 2010 22

Stake in ING Vysya Life valued at Rs11/share

Exide has a 50% stake in ING Vysya Life Insurance Company Limited, a JV with ING Group, Netherlands. ING Vysya Life Insurance has a ~2% market share among private players in India. Exide plans to continue investing in this business and has no plans of selling out in the medium term.

We value Exide’s stake in ING Vysya Life Insurance Company at Rs11/share based on 15x FY2012E NBAP, with an NBAP margin of ~17% on an estimated annual premium equivalent (APE) amount of Rs657cr in FY2012E. Exhibit 19: Valuation of Exide’s stake in ING Vysya Life Insurance

FY2010 FY2011E FY2012E

APE (New business) 628.4 596.9 656.6

NBAP margin (%) 17.0 17.0 17.0

NBAP (Rs cr) 106.8 101.5 111.6

NBAP multiple (x) 15.0 15.0 15.0

Value of Insurance Business (Rs cr) 1,602 1,522 1,674

Exide's Holding (%) 50 50 50

Per Share Value of Insurance Business (Rs) 10 9.5 11

Source: IRDA, Company, Angel Research

Key concerns

Slowdown in demand for automobile and industrial batteries

Exide generates 15–17% of its revenue from OEM sales, which are highly dependent on off-take in cars, commercial vehicles and two-wheelers. Any decline in demand due to a slowdown in economic activity or rise in interest rates will have an adverse impact on automobile demand, which poses a downside risk to our volume and earnings estimates.

Further, the slowdown in economic activity will have a negative impact on industrial battery demand as well. Industrial battery demand is expected to remain subdued in FY2011, mainly due to the slowdown in the telecom segment. The telecom segment, which contributes 30–35% of industrial battery sales, declined in FY2010. Going ahead, if the decline in demand is severe, it would negatively impact our estimates.

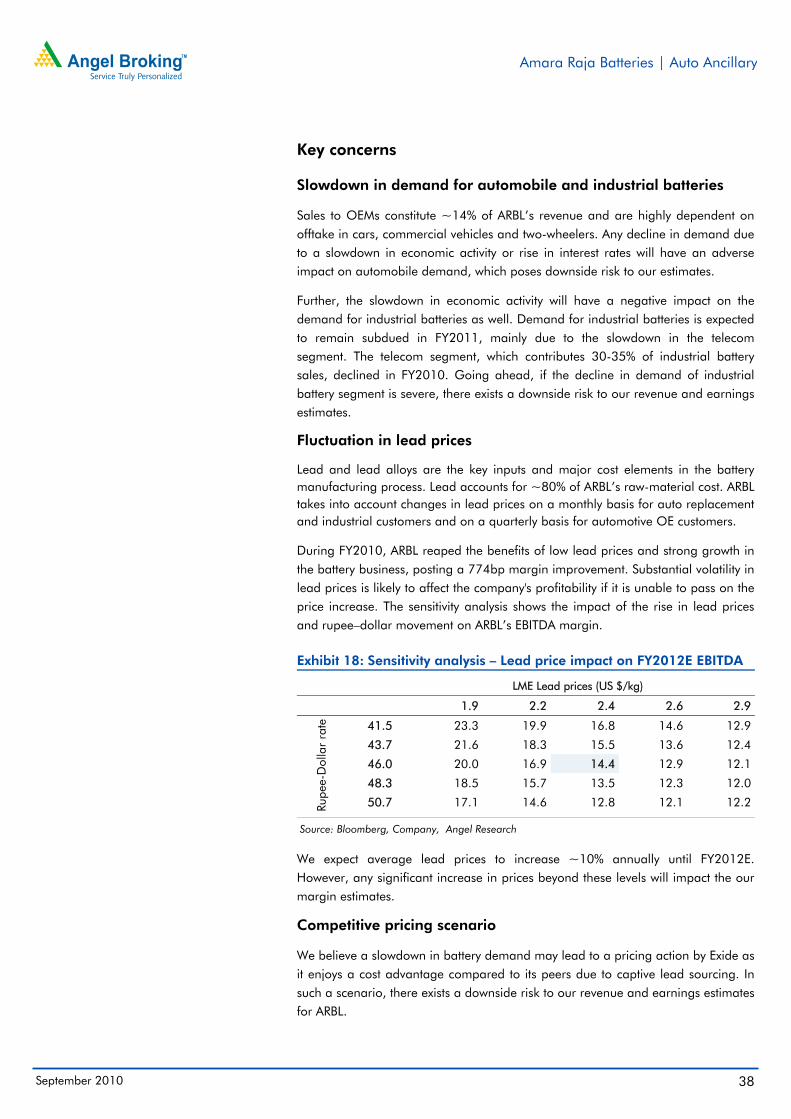

Fluctuation in lead prices

Lead and lead alloys are the key inputs and major cost elements in the battery manufacturing process. Lead accounts for 75–80% of Exide’s raw-material cost. Although Exide plans to secure the supply from its own smelters, a significant increase in lead prices will have a negative impact on our earnings estimates.

Exide Industries | Auto Ancillary

September 2010 23

Outlook and valuation

We estimate Exide to post a 21.1% CAGR in gross revenue over FY2010–13E, backed by 20.9% and 21.7% revenue CAGRs in auto and industrial battery segments. Thus, we expect the bottom line to post a substantial 16.9% CAGR over the same period. Moreover, Exide's strong brand image has been creating value, while continuously improving its RoCE, due to better asset turnover on incremental capacities. We believe Exide will continue to achieve higher return ratios and margins on the back of its superior pricing power and assuming a stable input cost scenario. Going ahead, a strong balance sheet and lower debt-equity ratio will aid the company in sustaining strong cash flows.

At Rs158, the stock is quoting at 20.4x FY2011E and 17.8x FY2012E earnings. We maintain an Accumulate rating on the stock with an SOTP Target Price of Rs171. Owing to its defensive appeal and healthy and consistent business fundamentals; we are valuing the company at 17.3x (20% premium to its historical average of 14.4x) FY2012E earnings at Rs154. We have valued the company’s stake in ING Vysya Life Insurance at Rs11/share on FY2012E NBAP and have assigned a value of Rs6/share to lead smelters (8x FY2012E PAT).

Exhibit 20: One-year forward P/E band

Source: Bloomberg, Company, Angel Research

Exhibit 21: One-year forward P/E chart

Source: Bloomberg, Company, Angel Research

Exhibit 22: One-year forward EV/EBITDA band

Source: Bloomberg, Company, Angel Research

Exhibit 23: One-year forward EV/EBITDA chart

Source Bloomberg, Company, Angel Research

0

50

100

150

200

Apr-

01

Dec

-01

Aug

-02

Apr-

03

Dec

-03

Aug

-04

Apr-

05

Dec

-05

Aug

-06

Apr-

07

Dec

-07

Aug

-08

Apr-

09

Dec

-09

Aug

-10

(Rs) Share price (Rs) 6x 10x 14x 18x

0

5

10

15

20

25

30

Apr

-01

Dec

-01

Aug-

02

Apr

-03

Dec

-03

Aug-

04

Apr

-05

Dec

-05

Aug-

06

Apr

-07

Dec

-07

Aug-

08

Apr

-09

Dec

-09

Aug-

10

(x) One-yr forward P/E Three-yr average P/ELong term average P/E

0

4,000

8,000

12,000

16,000

Apr-

01

Dec

-01

Aug-

02

Apr-

03

Dec

-03

Aug-

04

Apr-

05

Dec

-05

Aug-

06

Apr-

07

Dec

-07

Aug-

08

Apr-

09

Dec

-09

Aug-

10

(Rs cr) EV (Rs cr) 2x 5x 8x 11x

0

4

8

12

16

Apr-

01

Dec

-01

Aug

-02

Apr-

03

Dec

-03

Aug

-04

Apr-

05

Dec

-05

Aug

-06

Apr-

07

Dec

-07

Aug

-08

Apr-

09

Dec

-09

Aug

-10

(x) One-yr forward EV/EBITDA Three-yr average EV/EBITDALong term average EV/EBITDA

Exide Industries | Auto Ancillary

September 2010 24

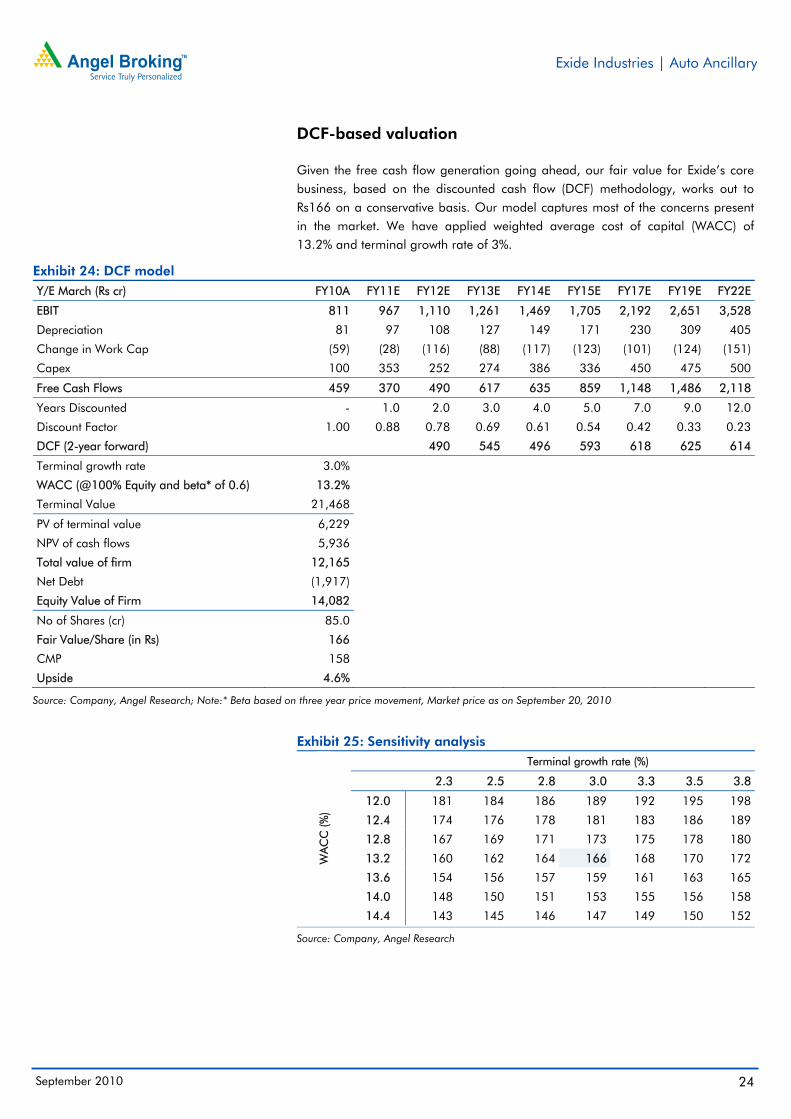

DCF-based valuation

Given the free cash flow generation going ahead, our fair value for Exide’s core business, based on the discounted cash flow (DCF) methodology, works out to Rs166 on a conservative basis. Our model captures most of the concerns present in the market. We have applied weighted average cost of capital (WACC) of 13.2% and terminal growth rate of 3%.

Exhibit 24: DCF model Y/E March (Rs cr) FY10A FY11E FY12E FY13E FY14E FY15E FY17E FY19E FY22E

EBIT 811 967 1,110 1,261 1,469 1,705 2,192 2,651 3,528

Depreciation 81 97 108 127 149 171 230 309 405

Change in Work Cap (59) (28) (116) (88) (117) (123) (101) (124) (151)

Capex 100 353 252 274 386 336 450 475 500

Free Cash Flows 459 370 490 617 635 859 1,148 1,486 2,118

Years Discounted - 1.0 2.0 3.0 4.0 5.0 7.0 9.0 12.0

Discount Factor 1.00 0.88 0.78 0.69 0.61 0.54 0.42 0.33 0.23

DCF (2-year forward) 490 545 496 593 618 625 614

Terminal growth rate 3.0%

WACC (@100% Equity and beta* of 0.6) 13.2%

Terminal Value 21,468

PV of terminal value 6,229

NPV of cash flows 5,936

Total value of firm 12,165

Net Debt (1,917)

Equity Value of Firm 14,082

No of Shares (cr) 85.0

Fair Value/Share (in Rs) 166

CMP 158

Upside 4.6%

Source: Company, Angel Research; Note:* Beta based on three year price movement, Market price as on September 20, 2010

Exhibit 25: Sensitivity analysis

WA

CC

(%)

Terminal growth rate (%)

2.3 2.5 2.8 3.0 3.3 3.5 3.8

12.0 181 184 186 189 192 195 198

12.4 174 176 178 181 183 186 189

12.8 167 169 171 173 175 178 180

13.2 160 162 164 166 168 170 172

13.6 154 156 157 159 161 163 165

14.0 148 150 151 153 155 156 158

14.4 143 145 146 147 149 150 152

Source: Company, Angel Research

Exide Industries | Auto Ancillary

September 2010 25

Company background

Exide is the largest manufacturer of lead acid storage batteries with manufacturing presence in India, Sri Lanka, UK, Singapore and Australia. The company manufactures batteries, ranging from 2.5Ah to 20,400Ah, having applications in the automotive and industrial segments. Exide has a technological tie-up with Shin Kobe, Furukawa Battery, Changxing Noble and Thunder Sky Battery. The business segment of the company comprises automotive batteries (~69% of revenue), industrial batteries (~30% of revenue) and submarine batteries (1% of revenue).

Exhibit 26: Auto battery segment’s revenue break-up

Source: Company, Angel Research

Exhibit 27: Ind. battery segment’s revenue break-up

Source: Company, Angel Research

Exhibit 28: Sectors and customers for automotive and industrial batteries Automobile

Cars Maruti Suzuki, Tata Motors, Fiat, General Motors, Honda, Hyundai, Mitsubishi, Toyota

Commercial Vehicles Tata Motors, Iveco, Ashok Leyland, Piaggio, Mazda

Motorcycle Bajaj Auto, Honda, Yamaha

Tractors Eicher Tractors, John Deere, Mahindra Tractors, New Holland Tractors

Special Purpose Vehicles Caterpillar India, JC Bamford

Industrial

Motive Power (Electric vehicles, mining locomotives, miners' cap lamps)

India Railways, Macneill & Magor, Godrej, Voltas, Josts, BHEL, Escorts, Indian Navy

Standby (Power, Telecom, UPS, Inverter) Fujitsu, Alctel, Siemens, Tata Lucent, BSNL, MTNL, AT&T, Compton Greaves, Tata Telecom, Reliance Telecom

Railways(Train lightning, AC, Electric Multiple Units, Diesel Loco Starters, Signaling and Telecom Railways

Source: Company, Angel Research

Exhibit 29: Major brands Automotive batteries Exide, SF Sonic, Standard Furukawa

Industrial batteries Exide, Index, SF, Ceil, Power Safe, Chloride

Source: Company, Angel Research

Exide has a strong sales and distribution network and offers quality customer service with a pan India presence.

After-market73%

OEM26%

Others1%

Power back-up67%

Infrastructure20%

Exports6%

Traction2%

Others5%

Exide Industries | Auto Ancillary

September 2010 26

Exhibit 30: Exide’s dealer and service network

Source: Company, Angel Research

Exhibit 31: Distribution network’s strength

Authorised dealers 13,400

Outlets 38,500

Humsafar partners 21,970

Depot cum service stations 202

Power centre shops 29

Source: Company, Angel Research

Exhibit 32: Key management team T V Ramanathan MD & CEO

G Chatterjee Director - Industrial division

P K Kataky Director - Automotive division

A K Mukherjee Director - Finance & CFO

S K Mittal Director - R&D

Supriya Coomer Company Secretary, VP - Legal and Administration

Nadeem Kazim Executive VP Human Resource

Source: Company, Angel Research

Exhibit 33: Plant location and capacity Plant Location Capacity (mn units)

Bawal, Haryana Motor-cycle 6.1

Chinchwad, Maharashtra Auto/ Motor-cycle 1.8/3.3

Haldia, West Bengal Auto/Industrial 1.0/0.3

Hosur, Tamil Nadu Auto/Industrial 1.6/0.8

Shamnagar, West Bengal Auto/Industrial 1.0/0.3

Taloja, Maharashtra Auto 1.7

Source: Company, Angel Research

Exhibit 34: Subsidiary information Subsidiary companies Objective % stake Sales (Rs. cr) PBT (Rs. cr)

Espex Batteries, UK Selling and marketing of lead acid batteries 51 30.2 0.36

Caldyne Automatics, Kolkata Design and manufacturing of battery chargers and DC/AC distribution boards 100 37 37

Chloride Batteries SE Asia Pte, Singapore Production and sales of lead acid batteries 100 122.67 4.73

Chloride International Operations in non-conventional energy systems 100 12 0.37

Chloride Metals, Pune Lead smelting and refining activities 100 264 15

Leadage Alloys, Karnataka Lead smelting and refining activities 100 546 54

Associated Battery Manufacturers, Sri Lanka Manufacturing and marketing of lead acid batteries 61.5 63.96 6.2

Source: Company, Angel Research; Note: Financial information for FY2010

OEM

Branches

Main Dealer

Customers

Subdealers/ Retailers

Factories

After-Sales Staff

Government

Institutions

Exide Industries | Auto Ancillary

September 2010 27

Profit & Loss Statement Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E FY13E

Gross sales 2,383 3,606 4,233 4,542 5,769 6,846 8,062

Less: Excise Duty 300 449 464 328 461 548 645

Less: Sales Tax, VAT, Octroi 213 312 376 419 519 616 726

Net Sales 1,870 2,845 3,393 3,794 4,788 5,682 6,691

Total operating income 1,870 2,845 3,393 3,794 4,788 5,682 6,691

% chg 35.6 52.1 19.3 11.8 26.2 18.7 17.8

Total Expenditure 1,565 2,373 2,845 2,902 3,723 4,464 5,303

Net Raw Materials 1,141 1,874 2,248 2,181 2,882 3,396 4,061

Other Mfg costs 143 163 188 219 262 303 352

Personnel 120 146 165 219 252 340 401

Other 161 191 243 284 327 426 489

EBITDA 305 472 548 892 1,065 1,218 1,388

% chg 38.8 54.5 16.1 62.8 19.4 14.4 14.0

(% of Net Sales) 16.3 16.6 16.1 23.5 22.2 21.4 20.7

Depreciation & Amortisation 54 64 68 81 97 108 127

EBIT 251 408 480 811 967 1,110 1,261

% chg 52.0 62.2 17.8 69.0 19.2 14.8 13.6

(% of Net Sales) 13.4 14.3 14.1 21.4 20.2 19.5 18.8

Interest & other Charges 31 41 52 14 7 7 7

Other Income 15 7 7 12 14 16 19

(% of PBT) 6.3 2.0 1.6 1.5 1.5 1.5 1.5

Recurring PBT 235 374 435 810 974 1,120 1,273

% chg 55.1 59.2 16.3 86.2 20.2 14.9 13.7

Extraordinary Expense/(Inc.) 3 2 1 - - - -

PBT (reported) 232 372 434 811 974 1,120 1,273

Tax 80 124 151 273 316 363 413

(% of PBT) 34.4 33.3 34.7 33.7 32.4 32.4 32.5

PAT (reported) 152 248 283 537 659 757 860

ADJ. PAT 155 250 284 537 659 757 859

% chg 54.1 61.3 13.6 88.9 22.6 14.9 13.4

(% of Net Sales) 8.3 8.8 8.4 14.2 13.8 13.3 12.8

Basic EPS (Rs) 2.1 3.1 3.6 6.3 7.7 8.9 10.1

Fully Diluted EPS (Rs) 2.1 3.1 3.6 6.3 7.7 8.9 10.1

% chg 54.1 51.2 13.6 77.7 22.6 14.9 13.4

Exide Industries | Auto Ancillary

September 2010 28

Balance Sheet

Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E FY13E

SOURCES OF FUNDS

Equity Share Capital 75 80 80 85 85 85 85

Reserves& Surplus 595 946 1,170 2,135 2,694 3,327 4,037

Shareholder’s Funds 670 1,026 1,250 2,220 2,779 3,412 4,122

Total Loans 325 350 317 90 90 90 90

Deferred Tax Liability 45 48 41 59 54 49 43

Total Liabilities 1,040 1,424 1,609 2,369 2,923 3,550 4,255

APPLICATION OF FUNDS

Gross Block 946 1,097 1,257 1,336 1,710 1,959 2,230

Less: Acc. Depreciation 480 542 589 660 757 865 992

Net Block 466 555 668 677 953 1,094 1,238

Capital Work-in-Progress 31 47 17 38 17 20 22

Investments 378 518 668 1,335 1,637 1,952 2,383

Current Assets 575 876 742 912 1,060 1,366 1,647

Cash 1 2 34 3 1 54 97

Loans & Advances 29 45 38 48 48 63 74

Other 545 830 669 861 1,011 1,249 1,477

Current liabilities 410 572 487 593 744 882 1,035

Net Current Assets 165 304 255 319 316 484 611

Total Assets 1,040 1,424 1,609 2,369 2,923 3,550 4,255

Cash Flow Statement Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E FY13E

Profit before tax 232 372 434 811 974 1,120 1,273

Depreciation 54 64 68 81 97 108 127

Change in Working Capital 25 124 (55) 62 15 102 77

Less: Other income 42 243 (202) 159 11 234 185

Direct taxes paid 80 124 151 273 316 363 413

Cash Flow from Operations 189 194 498 521 760 732 879

(Inc.)/Dec. in Fixed Assets (88) (167) (130) (100) (353) (252) (274)

(Inc.)/Dec. in Investments (99) (140) (150) (667) (301) (316) (430)

(Inc.)/Dec. in loans and advances (0) (13) 6 3 (14) (15) (11)

Other income (7) 14 (41) (11) - - -

Cash Flow from Investing (194) (307) (315) (775) (668) (582) (715)

Issue of Equity - 149 - 530 - - -

Inc./(Dec.) in loans 35 25 (33) (227) (0) - -

Dividend Paid (Incl. Tax) 26 31 37 56 95 99 124

Others (71) (91) (156) (135) (189) (196) (246)

Cash Flow from Financing (10) 113 (151) 224 (94) (97) (122)

Inc./(Dec.) in Cash (16) 0 32 (31) (2) 53 42

Opening Cash balances 17 1 2 34 3 1 54

Closing Cash balances 1 2 34 3 1 54 97

Exide Industries | Auto Ancillary

September 2010 29

Key Ratios

Y/E March FY07 FY08 FY09 FY10 FY11E FY12E FY13E

Valuation Ratio (x)

P/E (on FDEPS) 76.5 50.6 44.6 25.1 20.4 17.8 15.7

P/CEPS 56.7 40.3 36.0 21.8 17.8 15.6 13.6

P/BV 18.9 12.8 10.4 6.1 4.9 4.0 3.3

Dividend yield (%) 0.2 0.3 0.4 0.6 0.6 0.8 0.9

EV/Sales 7.2 4.7 3.9 3.2 2.5 2.0 1.7

EV/EBITDA 43.9 28.2 23.9 13.7 11.2 9.5 8.0

EV / Total Assets 12.9 9.3 8.1 5.2 4.1 3.3 2.6

Per Share Data (Rs)

EPS (Basic) 2.1 3.1 3.6 6.3 7.7 8.9 10.1

EPS (fully diluted) 2.1 3.1 3.6 6.3 7.7 8.9 10.1

Cash EPS 2.8 3.9 4.4 7.3 8.9 10.2 11.6

DPS 0.4 0.4 0.6 1.0 1.0 1.3 1.5

Book Value 8.4 12.4 15.2 25.8 32.3 39.8 48.1

DuPont Analysis

EBIT margin 13.4 14.3 14.1 21.4 20.2 19.5 18.8

Tax retention ratio 0.7 0.7 0.7 0.7 0.7 0.7 0.7

Asset turnover (x) 3.2 3.8 3.9 4.0 4.2 4.1 4.1

ROIC (Post-tax) 28.3 36.6 36.0 57.4 58.0 54.2 52.3

Cost of Debt (Post Tax) 6.6 8.1 10.1 4.4 5.4 5.4 5.4

Leverage (x) - - - - - - -

Operating ROE 28.3 36.6 36.0 57.4 58.0 54.2 52.3

Returns (%)

ROCE (Pre-tax) 26.0 33.1 31.7 40.8 36.6 34.3 32.3

Angel ROIC (Pre-tax) 40.7 47.0 54.9 81.1 77.1 73.4 72.3

ROE 25.4 29.5 25.0 31.0 26.4 24.5 22.8

Turnover ratios (x)

Asset Turnover (Gross Block) 2.0 2.8 2.9 2.9 3.1 3.1 3.2

Inventory / Sales (days) 62 62 54 50 49 49 50

Receivables (days) 29 26 26 23 26 26 26

Payables (days) 53 51 46 42 40 39 40

Working capital cycle (ex-cash) (days) 30 30 28 26 24 24 26

Solvency ratios (x)

Net debt to equity (0.1) (0.2) (0.3) (0.6) (0.6) (0.6) (0.6)

Net debt to EBITDA (0.2) (0.4) (0.7) (1.4) (1.5) (1.6) (1.7)

Interest Coverage (EBIT / Interest) 8.1 10.0 9.3 60.1 134.6 154.5 175.5

Note: Market price as on September 20, 2010

Please refer to important disclosures at the end of this report 30

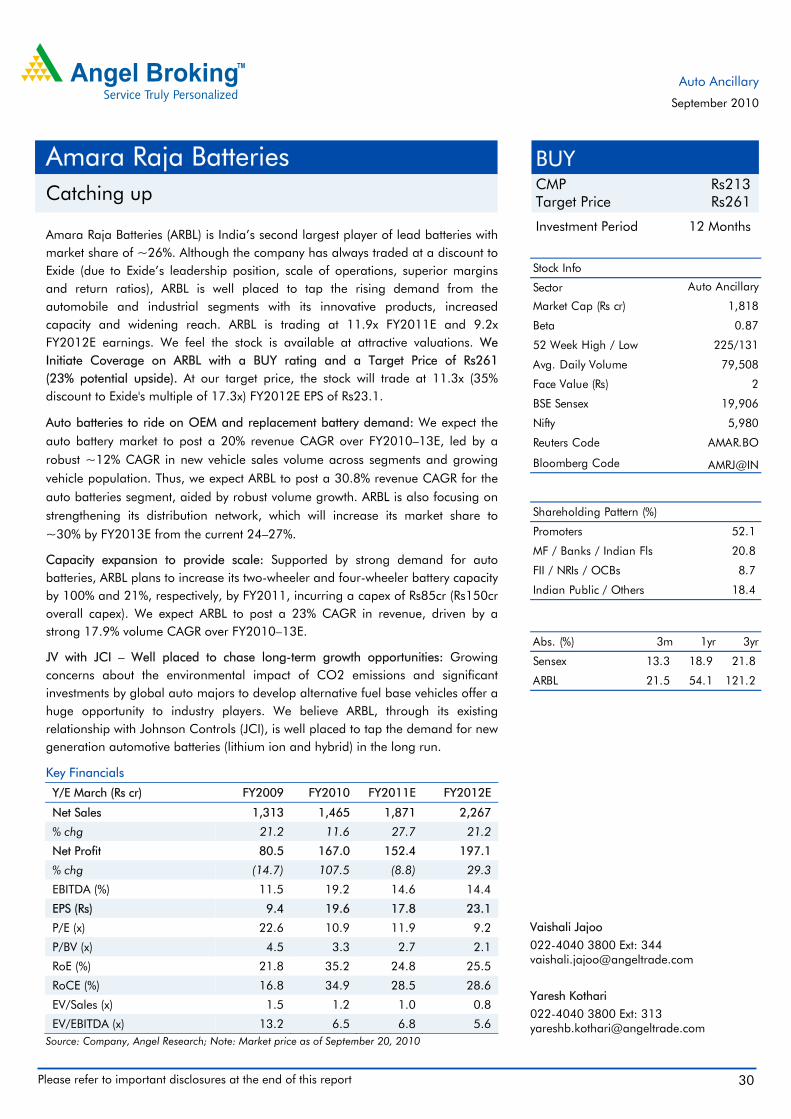

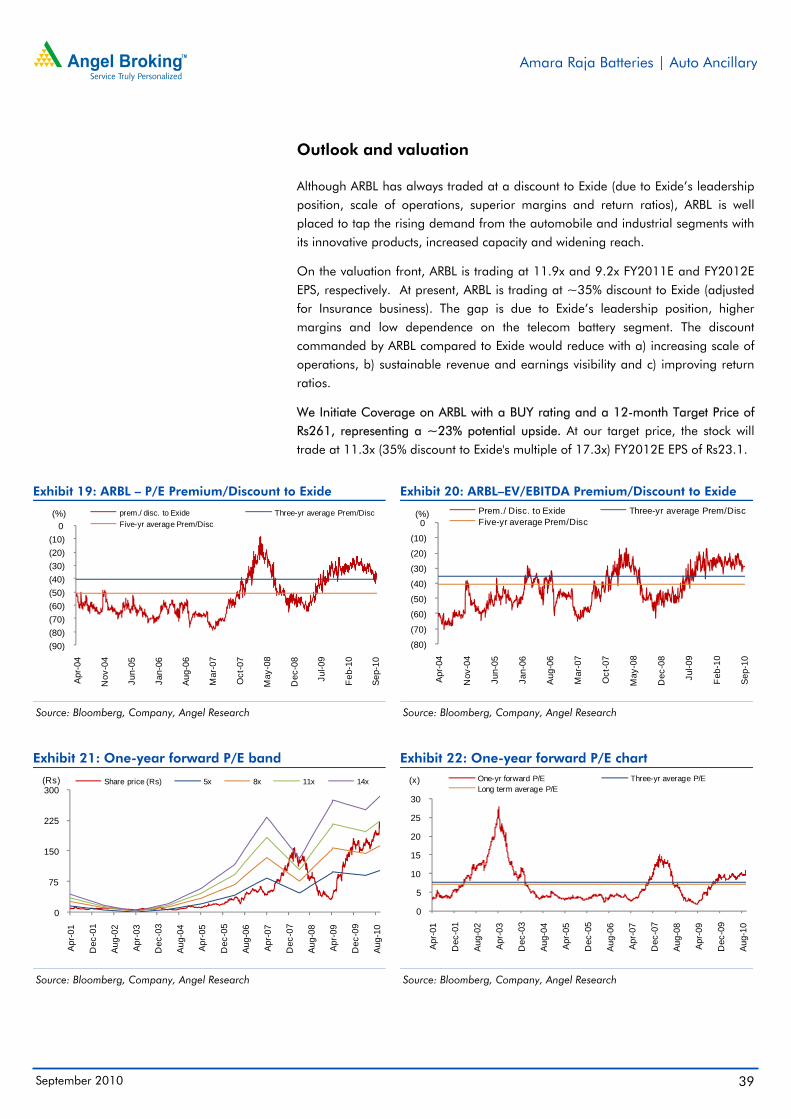

Amara Raja Batteries (ARBL) is India’s second largest player of lead batteries with market share of ~26%. Although the company has always traded at a discount to Exide (due to Exide’s leadership position, scale of operations, superior margins and return ratios), ARBL is well placed to tap the rising demand from the automobile and industrial segments with its innovative products, increased capacity and widening reach. ARBL is trading at 11.9x FY2011E and 9.2x FY2012E earnings. We feel the stock is available at attractive valuations. We Initiate Coverage on ARBL with a BUY rating and a Target Price of Rs261 (23% potential upside). At our target price, the stock will trade at 11.3x (35% discount to Exide's multiple of 17.3x) FY2012E EPS of Rs23.1.

Auto batteries to ride on OEM and replacement battery demand: We expect the auto battery market to post a 20% revenue CAGR over FY2010–13E, led by a robust ~12% CAGR in new vehicle sales volume across segments and growing vehicle population. Thus, we expect ARBL to post a 30.8% revenue CAGR for the auto batteries segment, aided by robust volume growth. ARBL is also focusing on strengthening its distribution network, which will increase its market share to ~30% by FY2013E from the current 24–27%.

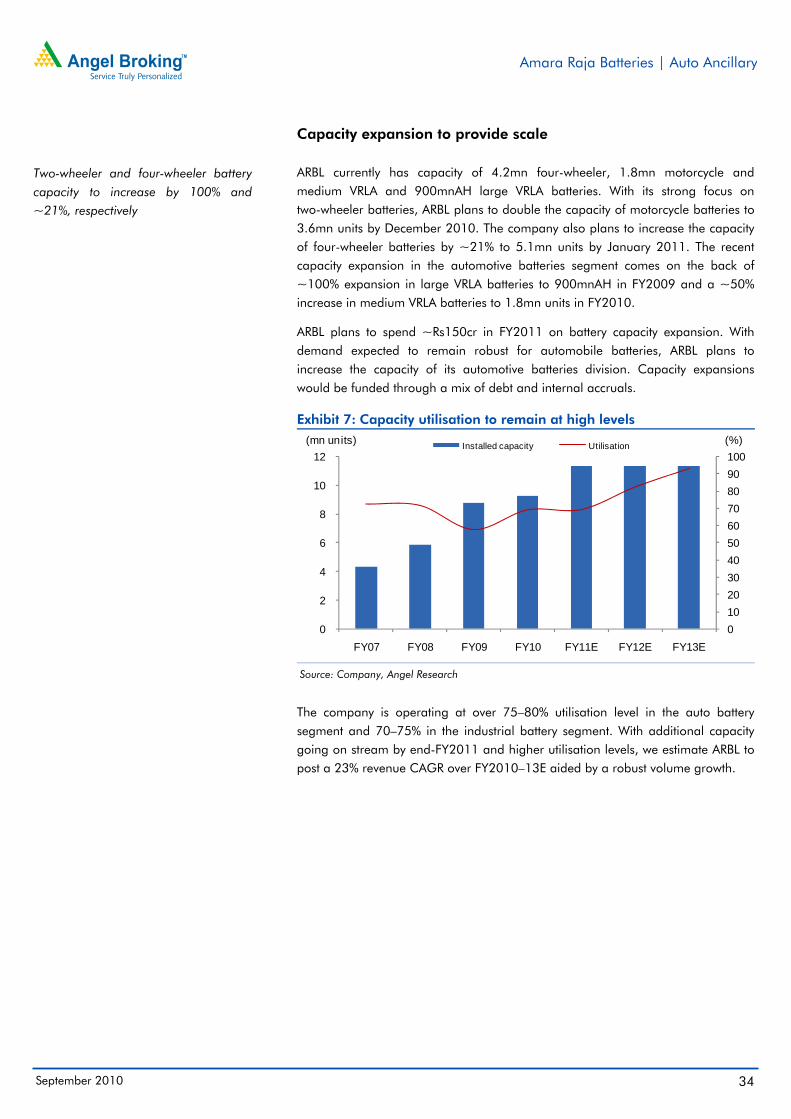

Capacity expansion to provide scale: Supported by strong demand for auto batteries, ARBL plans to increase its two-wheeler and four-wheeler battery capacity by 100% and 21%, respectively, by FY2011, incurring a capex of Rs85cr (Rs150cr overall capex). We expect ARBL to post a 23% CAGR in revenue, driven by a strong 17.9% volume CAGR over FY2010–13E.

JV with JCI – Well placed to chase long-term growth opportunities: Growing concerns about the environmental impact of CO2 emissions and significant investments by global auto majors to develop alternative fuel base vehicles offer a huge opportunity to industry players. We believe ARBL, through its existing relationship with Johnson Controls (JCI), is well placed to tap the demand for new generation automotive batteries (lithium ion and hybrid) in the long run.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 1,313 1,465 1,871 2,267

% chg 21.2 11.6 27.7 21.2

Net Profit 80.5 167.0 152.4 197.1

% chg (14.7) 107.5 (8.8) 29.3

EBITDA (%) 11.5 19.2 14.6 14.4

EPS (Rs) 9.4 19.6 17.8 23.1

P/E (x) 22.6 10.9 11.9 9.2

P/BV (x) 4.5 3.3 2.7 2.1

RoE (%) 21.8 35.2 24.8 25.5

RoCE (%) 16.8 34.9 28.5 28.6

EV/Sales (x) 1.5 1.2 1.0 0.8

EV/EBITDA (x) 13.2 6.5 6.8 5.6 Source: Company, Angel Research; Note: Market price as of September 20, 2010

BUY CMP Rs213 Target Price Rs261

Investment Period 12 Months

Stock Info

Sector

Bloomberg Code

Shareholding Pattern (%)

Promoters 52.1

MF / Banks / Indian Fls 20.8

FII / NRIs / OCBs 8.7

Indian Public / Others 18.4

Abs. (%) 3m 1yr 3yr

Sensex 13.3 18.9 21.8

ARBL 21.5 54.1 121.2

2

19,906

5,980

AMAR.BO

AMRJ@IN

1,818

0.87

225/131

79,508

Auto Ancillary

Avg. Daily Volume

Market Cap (Rs cr)

Beta

52 Week High / Low

Face Value (Rs)

BSE Sensex

Nifty

Reuters Code

Vaishali Jajoo

022-4040 3800 Ext: 344 [email protected]

Yaresh Kothari

022-4040 3800 Ext: 313 [email protected]

Amara Raja Batteries Catching up

Auto Ancillary

September 2010

Amara Raja Batteries | Auto Ancillary

September 2010 31

Investment rationale

Auto batteries to ride on OEM and replacement battery demand

ARBL derives ~50% of its revenue from the automotive battery segment. ARBL and Exide cater to almost the entire organised automotive battery market, with Exide being the market leader having a market share of 60-65%, followed by ARBL with a share of 24–27%. We expect the automotive battery market to post a 20% CAGR in sales over FY2010–13E. Consequently, we expect ARBL to post a 17.9% volume CAGR. ARBL’s low base of volume offers more leeway to increase its market share in the OEM and replacement segments compared to Exide.

Exhibit 1: Volume to grow at a 17.9% CAGR

Source: Company, Angel Research

Exhibit 2: Auto battery revenue to drive total revenue

Source: Company, Angel Research

OE segment to aid demand for automobile batteries

The automobile industry, which is a barometer for the country’s economic strength, posted a 9.1% volume CAGR over FY2006–10, led by buoyant economic activity. The industry has also benefitted from the introduction of new models, easy availability of finance and aggressive pricing by players. Favourable demographics, low penetration level and higher per capita income would support the long-term increase in auto volumes in India. We expect the four-wheeler and two-wheeler segments to report volume CAGRs of ~13% and ~11%, respectively, over FY2010–13E, resulting in the auto industry witnessing a ~12% volume CAGR. The expected surge in auto volumes would create a sustainable demand for automotive batteries going ahead, thus benefitting ARBL.

ARBL derives ~14% of its revenue from OEMs and enjoys a 24–27% market share in the automotive OEM market. The company supplies automotive batteries to major OEMs in the country, including Ashok Leyland, Hyundai, M&M, Maruti, Tata Motors, General Motors, TAFE and FIAT. ARBL is also an exclusive supplier to Daimler Chrysler, Ford and the Maruti-Swift platform.

4,230 5,094

6,417

7,482 8,326

0

5

10

15

20

25

30

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY09 FY10 FY11E FY12E FY13E

(%)('000 units) Auto battery volume yoy growth (RHS)

790 846

1,237

1,531

1,893

0 5 10 15 20 25 30 35 40 45 50

0 200 400 600 800

1,000 1,200 1,400 1,600 1,800 2,000

FY09 FY10 FY11E FY12E FY13E

(%)(Rs cr) Auto battery revenue yoy growth (RHS)

ARBL has 24–27% market share in theOEM segment

Amara Raja Batteries | Auto Ancillary

September 2010 32

Replacement demand to drive growth

The short lifespan of automotive batteries, which is 3–4 years for four-wheelers and two-wheelers, creates an attractive replacement market. The replacement market largely tracks the number of vehicles on the road. We estimate vehicle penetration in India to grow at a CAGR of ~9% over FY2010–13E. On the back of healthy growth in OE sales in the last few years, we expect replacement battery demand to witness a 13–15% CAGR over FY2010–13E. This will benefit ARBL, as the company derives ~65% of its automotive battery segment’s revenue from the replacement market.

Over the past three years, ARBL has been focusing on branding. The company has steadily expanded its retail distribution network, as a strong distribution network is essential to serve the replacement market effectively. ARBL has successfully established itself in a market that is dominated by Exide. The company has a network of over 18,000 retailers, 200 franchisees and 700 PowerZone outlets, catering to the semi-urban and rural markets. ARBL’s market share in the replacement market now stands at ~26%. The company plans to widen its retail network to further increase its penetration in the replacement market.

Exhibit 3: Distribution network

FY07 FY08 FY09 FY10

AQUA - 50 70 75

Franchises 152 175 189 200

Amaron PitStops 115 120 145 145

Retailers 14,000 18,000 18,000+ 18,000+

PowerZone - 400 600 700

Source: Company, Angel Research

Exhibit 4: OEM and replacement market share

Source: Company, Angel Research

25 26 28 27

20

26 25 26

0

5

10

15

20

25

30

FY07 FY08 FY09 FY10

(%) OEM Organised replacement

ARBL derives ~33% of its revenue fromthe replacement segment

Amara Raja Batteries | Auto Ancillary

September 2010 33

Industrial batteries

UPS/inverter segment to drive demand

Demand for industrial batteries has been fairly strong over the past couple of years, largely due to the significant boom in the telecom sector. As a result, ARBL’s industrial battery business grew at a ~34% CAGR over FY2006–10. ARBL enjoys strong ties with its customers and has emerged as a preferred supplier to leading telecom operators. ARBL commanded a market share of 30–32% in the telecom battery segment in FY2010. However, the telecom sector, which constitutes 28–30% of ARBL’s sales, is expected to post modest growth going forward due to the slowdown in the telecom space. We estimate the company’s telecom battery segment to register a single-digit CAGR (~5%) in volumes over FY2010–13E.

Exhibit 5: Ind. battery segment – Stable market share

Source: Company, Angel Research

Exhibit 6: UPS/inverter batteries to contribute more

Source: Company, Angel Research