baw2.practice assessment 1 - osbornebooks.co.uk · practice assessment 2 7 task 4 ... 02 jun scotts...

TRANSCRIPT

Osborne Books Tutor Zone

BookkeepingControlsPractice assessment 2

© Osborne Books Limited, 2016

Complete all 10 tasks.

Each task is independent. You will not need to refer to your answers in previous tasks.

The tasks are set in a business where the following apply:• You are employed by the business, Clean Style, as a bookkeeper.• Clean Style uses a manual bookkeeping system.• Double-entry takes place in the general ledger. Individual accounts of trade receivables and trade

payables are kept in the sales and purchases ledgers as subsidiary accounts.• The cash book and petty cash book should be treated as part of the double-entry system

unless the task instructions state otherwise. • The VAT rate is 20%.

2 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 1(a) Show which of the following payment methods best suits each situation below. Choose one

payment method for each situation.

Direct debit Faster paymentBusiness credit card CashCHAPS payment Standing orderBank draft Cheque

Variable monthly bill for broadband and telephone services

Payment of a credit supplier’s account due in one day

Purchase of computer equipment online in a one-day special offer.No credit account exists

Guaranteed payment for a new vehicle costing £26,000. Paymentmust be made in person when the vehicle is collected from thedealer.

(b) Indicate whether each of the statements below is true or false.

True False

(a) When Clean Style makes payments to suppliers by credit card, theamount leaves the bank current account immediately

(b) When Clean Style makes payments to suppliers by debit card, theamount paid does not affect the bank current account

p r a c t i c e a s s e s s m e n t 2 3

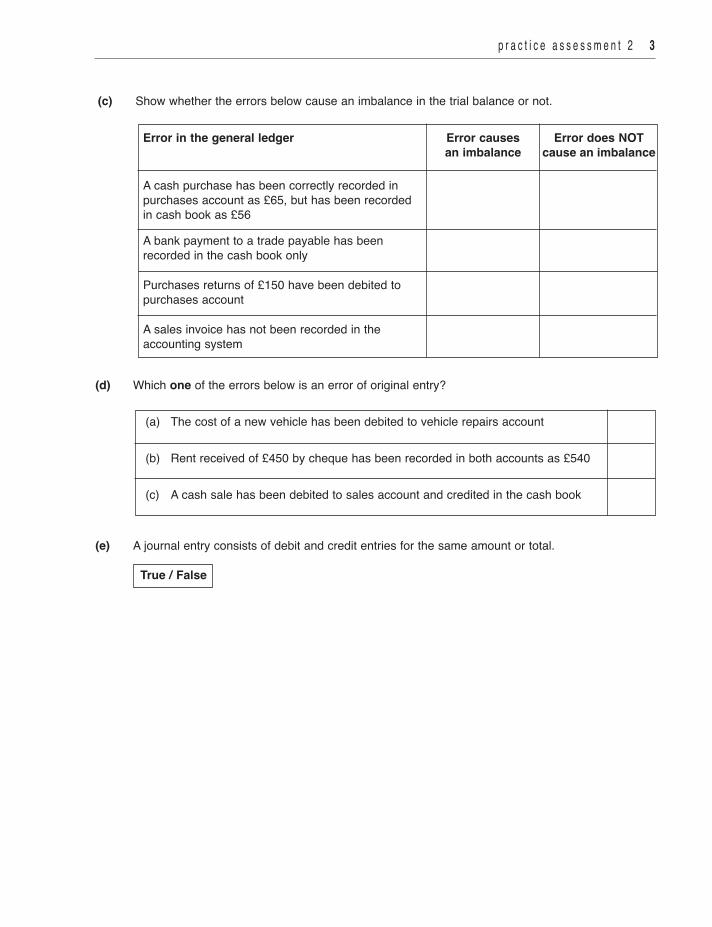

(c) Show whether the errors below cause an imbalance in the trial balance or not.

Error in the general ledger Error causes Error does NOT an imbalance cause an imbalance

A cash purchase has been correctly recorded inpurchases account as £65, but has been recordedin cash book as £56

A bank payment to a trade payable has been recorded in the cash book only

Purchases returns of £150 have been debited to purchases account

A sales invoice has not been recorded in the accounting system

(d) Which one of the errors below is an error of original entry?

(a) The cost of a new vehicle has been debited to vehicle repairs account

(b) Rent received of £450 by cheque has been recorded in both accounts as £540

(c) A cash sale has been debited to sales account and credited in the cash book

(e) A journal entry consists of debit and credit entries for the same amount or total.

True / False

4 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 2

Clean Style pays its employees every month and maintains a wages control account. A summary of lastmonth’s payroll transactions is shown below:

Item £Gross wages 24,105Employer’s NI 1,981Employees’ NI 1,624Income tax 3,544Employer’s pension contributions 655Employees’ pension contributions 655

Record the journal entries needed in the general ledger to:

(a) Record the wages expense.

(b) Record the HM Revenue & Customs liability.

(c) Record the net wages paid to the employees.

(d) Record the pension fund liability.

Select your account names from the following list: Bank, Employees’ NI, Employer’s NI, HMRevenue & Customs, Income tax, Net wages, Pension fund, Wages control, Wages expense.Enter the names and amounts and tick the appropriate debit or credit column.

(a)Account name Amount Debit Credit

£

(b) Account name Amount Debit Credit

£

p r a c t i c e a s s e s s m e n t 2 5

(c) Account name Amount Debit Credit

£

(d) Account name Amount Debit Credit £

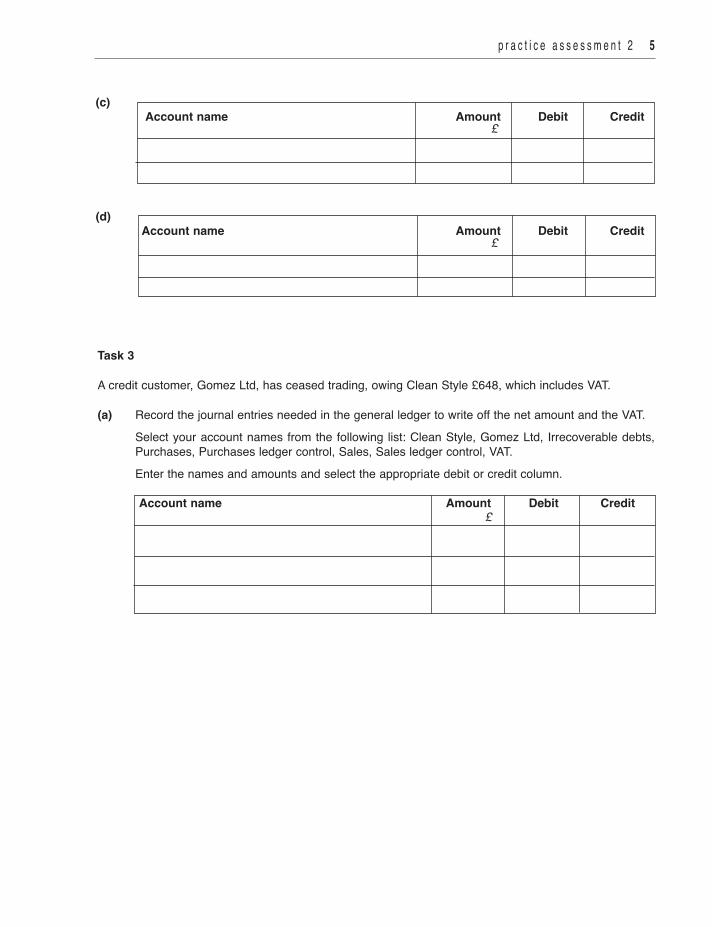

Task 3

A credit customer, Gomez Ltd, has ceased trading, owing Clean Style £648, which includes VAT.

(a) Record the journal entries needed in the general ledger to write off the net amount and the VAT.Select your account names from the following list: Clean Style, Gomez Ltd, Irrecoverable debts,Purchases, Purchases ledger control, Sales, Sales ledger control, VAT.Enter the names and amounts and select the appropriate debit or credit column.

Account name Amount Debit Credit £

6 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

(b) Clean Style has started a new business, Clean Home, and a new set of accounts are to be opened.A partially completed journal to record the opening entries is shown below.Record the journal entries needed in the accounts in the general ledger of Clean Home to deal withthe opening entries.

Account name Amount Debit Credit £

Inventory 4,108Bank overdraft 1,095Capital 21,757Sales ledger control 12,395Purchases ledger control 7,962Wages 3,855Miscellaneous expenses 976Machinery 4,550Office equipment 2,680Rent 2,250

Journal to record the opening entries of new business

p r a c t i c e a s s e s s m e n t 2 7

Task 4The following is a list of the VAT totals from Clean Style’s books of prime entry:

Books of prime entry VAT totals for quarter £Sales day book 13,104Purchases day book 6,373Sales returns day book 469Purchases returns day book 346Discounts allowed day book 340Discounts received day book 166Cash book: cash sales 924Cash book: cash purchases 224 Other VAT items for the quarter are as follows:

VAT on irrecoverable debt written off 90VAT on purchase of computer equipment 460VAT paid to HMRC 5,273

(a) What will be the entries in the VAT control account to record the VAT transactions in the quarter?Select your entries for the Details columns from the following list: Bank, Cash book, Cashpurchases, Cash sales, Discounts allowed, Discounts received, Irrecoverable debt, Officeequipment, Petty cash, Purchases, Purchases returns, Sales, Sales returns, VAT.

(b) What will be the balance brought down on the VAT control account after the transactions have beenrecorded?

Amount £ Dr Cr

VAT control account

Details Amount £

Details Amount £

Balance b/f 5,273

8 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 5

(a) This is a summary of transactions with credit suppliers during the month of June.Show whether each entry will be a debit or credit in the purchases ledger control account in thegeneral ledger.

Details Amount Debit Credit £

Balance of credit suppliers at 1 June 13,241Goods bought on credit 6,935Payments made to credit suppliers 6,752Discount received 112Goods returned to credit suppliers 1,046

(b) What will be the balance brought down on 1 July on the account from (a)?

(a) Dr £12,266(b) Cr £12,266(c) Dr £11,900 (d) Cr £11,900(e) Dr £12,490(f) Cr £12,490

(c) The following credit balances were in the purchases ledger on 1 July. £Southern Suppliers Ltd 3,097Martley Manufacturing 2,636Nelson & Co 1,792Linsell & Stuart 2,081Felsberg & Co 1,238Hudson Ltd 1,201

p r a c t i c e a s s e s s m e n t 2 9

What is the difference between the total of the balances shown on the previous page and thepurchases ledger control account balance calculated in part (b)?

£Purchases ledger control account balance as at 1 July

Total of purchases ledger accounts as at 1 July

Difference

(d) What may have caused the difference you calculated in part (c)?

(a) An invoice was entered twice in the purchases ledger

(b) A credit note was not entered in the purchases ledger

(c) A payment to a credit supplier was entered twice in the purchases ledger

(d) Settlement (cash) discount was entered twice in the purchases ledger control account

1 0 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 6 On 28 June Clean Style received the following bank statement as at 24 June.

BANK STATEMENTDate Details Paid out Paid in Balance20-4 £ £ £01 Jun Balance brought forward 1,860 D02 Jun Cheque 240764 485 2,345 D04 Jun BACS credit: Scotts 3,640 1,295 C06 Jun Cheque 240765 839 456 C12 Jun Cheque 240766 248 208 C15 Jun Cheque 240768 1,107 899 D19 Jun Direct debit: Western Gas 763 1,662 D20 Jun Direct debit: Aiken Insurance 1,241 2,903 D20 Jun Paid into bank 2,469 434 D22 Jun Bank charges 255 689 D24 Jun Cheque 240770 2,322 3,011 D24 Jun BACS credit: Amery Ltd 2,384 627 D

D = Debit C = Credit

p r a c t i c e a s s e s s m e n t 2 1 1

The cash book as at 24 June is shown below.

CASH BOOKDate Details Bank Date Cheque Details Bank20-4 £ 20-4 number £

02 Jun Scotts 3,640 01 Jun Balance b/f 2,345

19 Jun D Dunlevy 1,638 01 Jun 240765 Walls plc 839

20 Jun Melia & Co 831 03 Jun 240766 Linsell & Stuart 248

24 Jun Dixon & Co 1,747 06 Jun 240767 Silk & Co 493

24 Jun Trew Ltd 3,745 10 Jun 240768 Siddique Brothers 1,107

14 Jun 240769 Hudson Ltd 554

19 Jun 240770 Yanez Ltd 2,322

19 Jun Western Gas 763

Check the items on the bank statement against the items in the cash book.• Enter any items in the cash book as needed.• Total the cash book and clearly show the balance carried down at 24 June (closing balance) and

brought down at 25 June (opening balance).

Select your entries for the ‘Details’ columns from the following list: Aiken Insurance, Amery Ltd, Balanceb/d, Balance c/d, Bank charges, Closing balance, Dixon & Co, D Dunlevy, Hudson Ltd, Linsell & Stuart,Melia & Co, Opening balance, Scotts, Siddique Brothers, Silk & Co, Trew Ltd, Walls plc, Western Gas,Yanez Ltd.

1 2 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

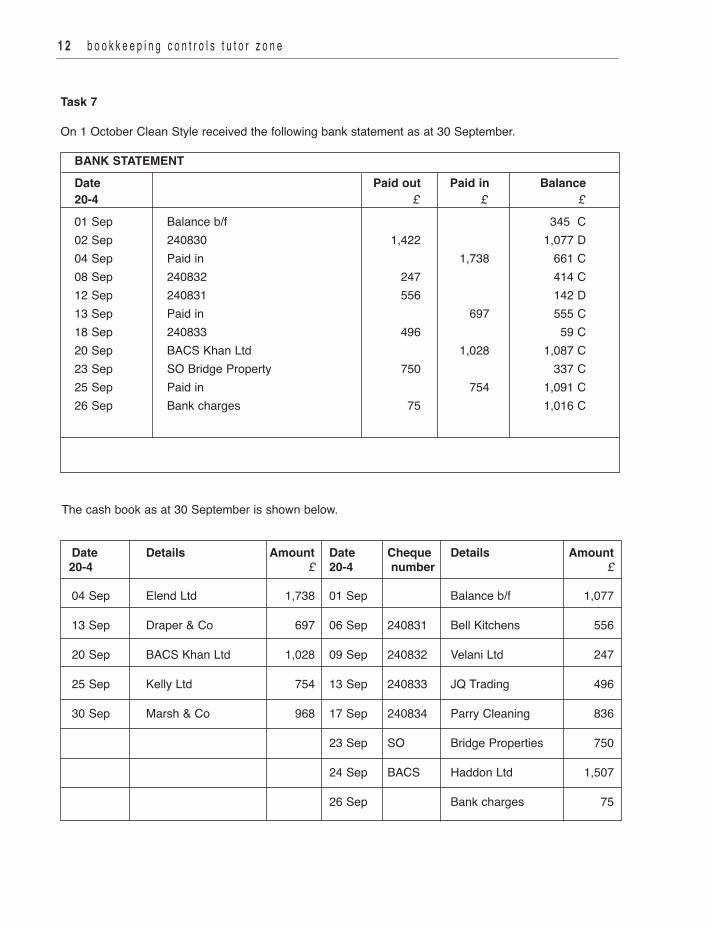

Task 7

On 1 October Clean Style received the following bank statement as at 30 September. BANK STATEMENTDate Paid out Paid in Balance20-4 £ £ £ 01 Sep Balance b/f 345 C02 Sep 240830 1,422 1,077 D04 Sep Paid in 1,738 661 C08 Sep 240832 247 414 C12 Sep 240831 556 142 D13 Sep Paid in 697 555 C18 Sep 240833 496 59 C20 Sep BACS Khan Ltd 1,028 1,087 C23 Sep SO Bridge Property 750 337 C25 Sep Paid in 754 1,091 C26 Sep Bank charges 75 1,016 C

The cash book as at 30 September is shown below.

Date Details Amount Date Cheque Details Amount20-4 £ 20-4 number £

04 Sep Elend Ltd 1,738 01 Sep Balance b/f 1,077

13 Sep Draper & Co 697 06 Sep 240831 Bell Kitchens 556

20 Sep BACS Khan Ltd 1,028 09 Sep 240832 Velani Ltd 247

25 Sep Kelly Ltd 754 13 Sep 240833 JQ Trading 496

30 Sep Marsh & Co 968 17 Sep 240834 Parry Cleaning 836

23 Sep SO Bridge Properties 750

24 Sep BACS Haddon Ltd 1,507

26 Sep Bank charges 75

p r a c t i c e a s s e s s m e n t 2 1 3

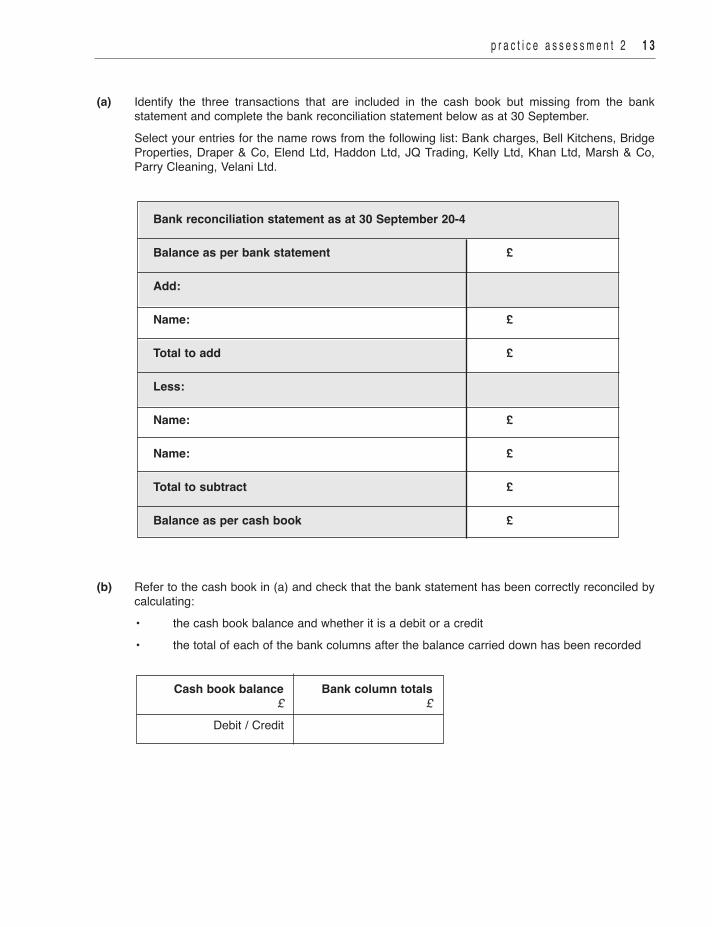

(a) Identify the three transactions that are included in the cash book but missing from the bankstatement and complete the bank reconciliation statement below as at 30 September.Select your entries for the name rows from the following list: Bank charges, Bell Kitchens, BridgeProperties, Draper & Co, Elend Ltd, Haddon Ltd, JQ Trading, Kelly Ltd, Khan Ltd, Marsh & Co,Parry Cleaning, Velani Ltd.

Bank reconciliation statement as at 30 September 20-4

Balance as per bank statement £

Add:

Name: £

Total to add £

Less:

Name: £

Name: £

Total to subtract £

Balance as per cash book £

(b) Refer to the cash book in (a) and check that the bank statement has been correctly reconciled bycalculating:• the cash book balance and whether it is a debit or a credit• the total of each of the bank columns after the balance carried down has been recorded

Cash book balance Bank column totals £ £ Debit / Credit

1 4 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 8

A suspense account has been opened with a balance of £100.The error has been traced to the sales returns day book shown below.

Sales returns day book

Date 20-4 Details Credit note number Total £ VAT £ Net £30 Jun Western Trains CN45 1,440 240 1,20030 Jun Blenheim Care CN46 684 114 57030 Jun Nelson Hotel Ltd CN47 384 64 320 Totals 2,508 418 2,190

(a) Identify the error and record the journal entries needed in the general ledger to:(1) Remove the incorrect entry.(2) Record the correct entry.(3) Remove the suspense account balance.

Select your account names from the following list: Blenheim Care, Nelson Hotel Ltd, Purchases,Purchases ledger control, Purchases returns, Sales, Sales ledger control, Sales returns,Suspense, VAT, Western Trains.Enter the names and amounts and tick the appropriate debit or credit column.

(1)Account name Amount Debit Credit

£

(2)Account name Amount Debit Credit

£

(3)Account name Amount Debit Credit

£

p r a c t i c e a s s e s s m e n t 2 1 5

(b) A direct debit for insurance of £870 has been entered in the accounts as £780. Record the journal entries needed in the general ledger to remove the incorrect entry. Select your account names from the following list: Bank, Cash, Direct debit, Insurance, Purchases,

Suspense. Enter the names and amounts and select the appropriate debit or credit column.

Account name Amount Debit Credit £

Record the journal entries needed in the general ledger to record the correct entry. Select your account names from the following list: Bank, Cash, Direct debit, Insurance, Purchases,

Suspense. Enter the names and amounts and tick the appropriate debit or credit column.

Account name Amount Debit Credit £

1 6 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Task 9

Journal entries shown below have been prepared to correct an error.

Journal entriesAccount name Debit £ Credit £Rent received 1,245Suspense 1,245Suspense 1,425Rent received 1,425

Record the journal entries in the general ledger accounts and show the balance carried down on the rentreceived account.

Select your entries from the following list: Balance b/d, Balance c/d, Bank, Rent received, Suspense

Suspense

Details Amount £ Details Amount £

Balance b/d 180

Rent received

Details Amount £ Details Amount £

Balance b/d 1,245

p r a c t i c e a s s e s s m e n t 2 1 7

Task 10(a) On 31 July a trial balance was extracted and did not balance. The debit column totalled £116,953

and the credit column totalled £116,023. What entry is needed in the suspense account to balance the trial balance?

Account name Debit CreditSuspense

(b) The journals to correct the bookkeeping errors, and a list of balances as they appear in the trialbalance, are shown below.

Journal entries

Account name Debit Credit £ £Suspense 330

Commission received 330

Suspense 330

Commission received 330

Account name Debit Credit £ £Sales 1,360

Suspense 1,360

Suspense 1,630

Sales 1,630

Complete the table on the next page to show:• the balance of each account after the journal entries have been recorded• whether each balance will be a debit or credit entry in the trial balance

1 8 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Account name Original balance £ New balance £ Debit CreditCommission received 1,392 Sales 73,391

(c) On 30 September a partially prepared trial balance had debit balances totalling £117,493 and creditbalances totalling £120,613. The accounts below have not yet been entered into the trial balance.Complete the table below to show whether each balance is a debit or a credit entry in the trialbalance.

Account name Balance £ Debit in the Credit in the trial balance trial balanceCapital 16,271 Sales ledger control 15,624 Advertising 3,767

(d) What will be the totals of each column of the trial balance after the balances in (c) have beenentered?

Account name Debit CreditTotals