bc natural gas industry competitiveness study natural gas industry competitiveness study september...

TRANSCRIPT

BC Natural Gas Industry Competitiveness Study

Natural Gas Industry Competitiveness Study

September 1999

BC Natural Gas Industry Competitiveness Study

BC Gas Demand Forecast

• Domestic and Export markets are expected to grow at a rate of 1 to 2% annually. – This excludes demand created by the addition

of the following major projects.

• Additional demand will be created by Vancouver Island cogenerators, Burrard Thermal Plant, and the Alliance Pipeline by the year 2001.

BC Natural Gas Industry Competitiveness Study

BC Gas Demand Forecast

0

200

400

600

800

1000

1200

1400

1600

1980 1985 1990 1995 2000 2005 2010 2015 2020

Year

Pro

du

ctio

n in

Bcf

of

Mar

keta

ble

Gas

Low Total Demand

Base Total Demand

High Total Demand

NEB ProductionForecast

Historical Forecast

Alliance Pipeline, Burrard Thermal andVancouver Island Cogenerators

BC Natural Gas Industry Competitiveness Study

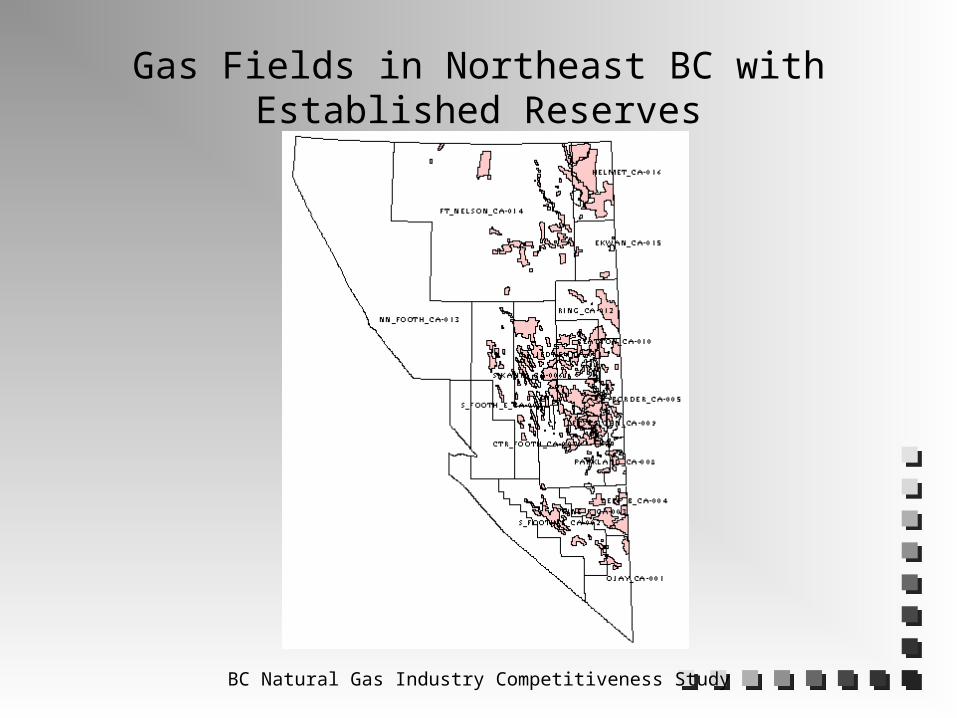

Gas Fields in Northeast BC with Established Reserves

BC Natural Gas Industry Competitiveness Study

Northeast BC Remaining Gas Potential

BC Natural Gas Industry Competitiveness Study

Northeast BC Established Gas Reserves as of December 31, 1998 in Trillion Cubic

Feet of Marketable Gas

Initial Established Reserves 20.4Cumulative Production 12.2Remaining Established Reserves 8.2Remaining Undiscovered Reserves 34.6Ultimate Potential 55

BC Natural Gas Industry Competitiveness Study

Northeast BC Gas Reserves by Cost Areas

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.001 2 3 4 5 6 7 8 9 10

11 12

13

14

15

16

Cost Areas

Ga

s R

es

erv

es

in T

cf

of

Ma

rke

tab

le G

as

Total Cumulative Production Total Remaining Established Reserve Remaining Undiscovered Potential

BC Natural Gas Industry Competitiveness Study

Production Forecast to Meet Demand

Base Demand Forecast BC Marketable Gas Well Producibility Forecast

0

5000

10000

15000

20000

25000

30000

35000

1995 2000 2005 2010 2015 2020

Year

Ma

rke

tab

le G

as

We

ll P

rod

uc

ibil

ity

an

d A

ver

ag

e G

as

P

rod

uct

ion

in 1

0^

6 m

3

Connected Well Producibility

Unconnected Well Producibility

Producibility from Well Addition to meet PeakDay Demand

Average Demand

Peak Day Deliverability Restricted toInfrastructure

Required Infrastructure

BC Natural Gas Industry Competitiveness Study

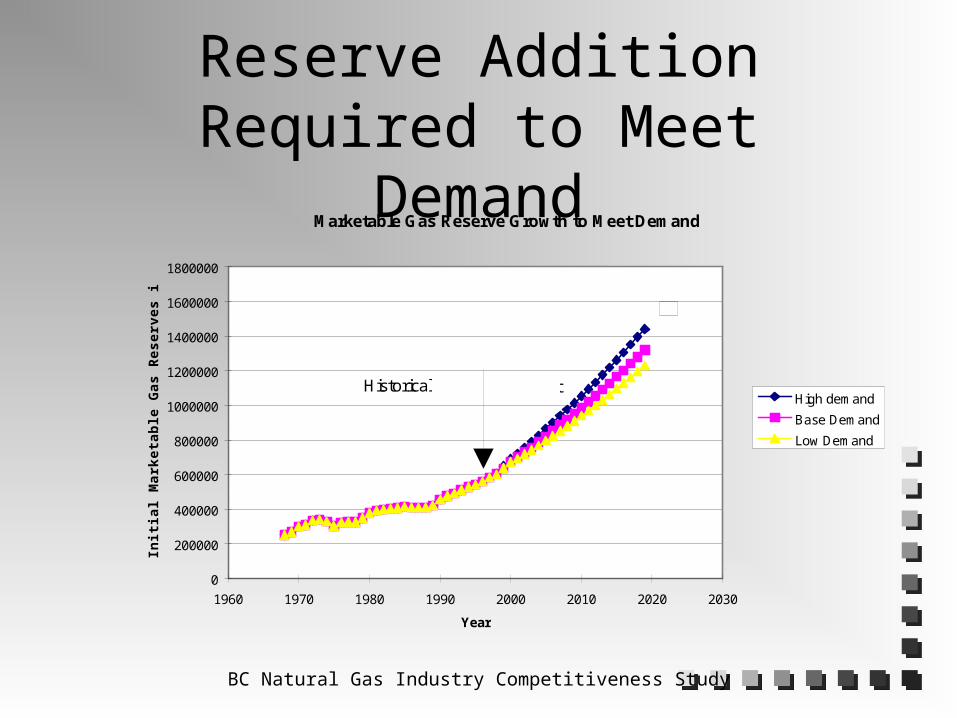

Reserve Addition Required to Meet DemandMarketable Gas Reserve Growth to Meet Demand

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

1960 1970 1980 1990 2000 2010 2020 2030

Year

Init

ial

Ma

rke

tab

le G

as

Re

se

rve

s i

n 1

0^

6 m

3

High demand

Base Demand

Low Demand

Historical Forecast

Estimate Ultimate Potential of 1560 10^9 m3

BC Natural Gas Industry Competitiveness Study

Reserve Additions per Well

• Reserve Additions per well have been declining

• Considerable amount of drilling activity is required to counteract declines in existing pools and meet future increases in demand

BC Natural Gas Industry Competitiveness Study

Reserve Addition Per Meter Drilled

Reserve Addition per Meter Gas Intent Drilling

1

10

100

1000

1000 10000

Cummulative Meter of Gas Intent Drilling in Km

(Re

se

rve

Ad

dit

ion

in 1

0^

6 m

3 o

f M

ark

eta

ble

Ga

s/C

um

m.

Me

ter

Ga

s In

ten

t D

rilli

ng

in K

m)

Actual values Calculated based on Regression

BC Natural Gas Industry Competitiveness Study

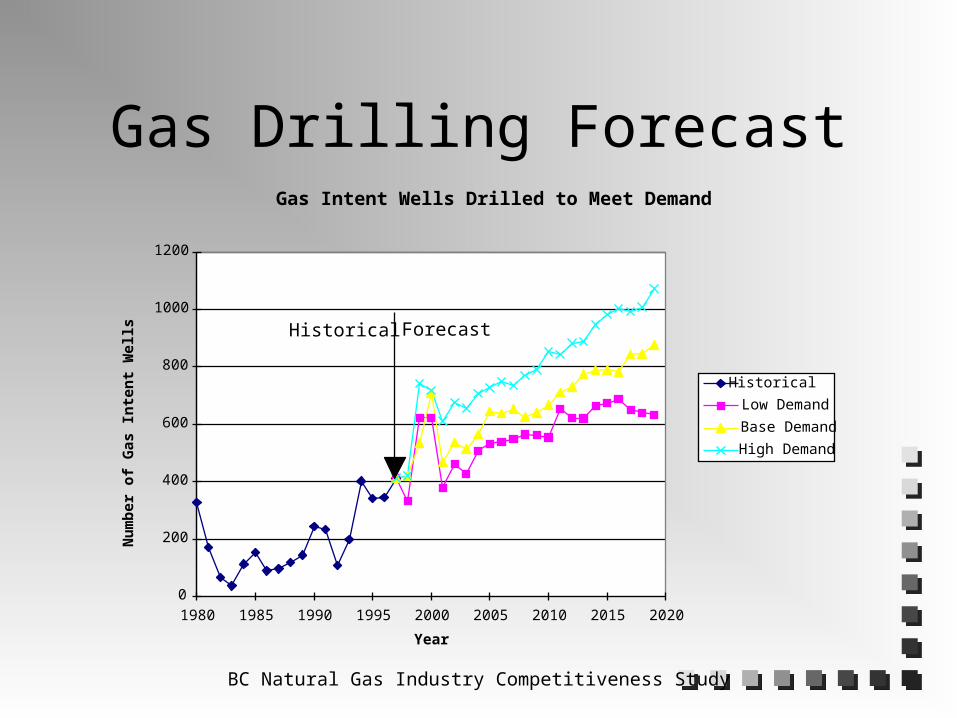

Gas Drilling Forecast Gas Intent Wells Drilled to Meet Demand

0

200

400

600

800

1000

1200

1980 1985 1990 1995 2000 2005 2010 2015 2020

Year

Nu

mb

er o

f G

as I

nte

nt

Wel

ls

Historical

Low Demand

Base Demand

High Demand

Historical Forecast

BC Natural Gas Industry Competitiveness Study

Forecast of Cumulative Gas Wells

Forecast of Gas Intent Wells Required to Meet Demand

0

5000

10000

15000

20000

25000

30000

35000

1960 1970 1980 1990 2000 2010 2020 2030 2040

Year

No

of

Ga

s I

nte

nt

We

lls

High Demand

Base Demand

Low Demand

NEB (1994 to 2010)Historical Forecast

Possible Drilling Location (Excludes PAS) 33,000

BC Natural Gas Industry Competitiveness Study

HISTORY Done with co-operation and encouragement of Industry and CAPP. Terms of Reference distributed in Fall 1996. Industry was invited

to contribute comments and data.

We actively sought data, we kept industry and CAPP informed. Data, methodology and progress presented to industry at BC

Petroleum Executive Forums June 11, 1997 and December 11, 1997.

Industry and CAPP input and consultation from 1996 to 1997. We used every piece of data provided by industry and CAPP.

Preliminary results presented to CAPP, Westcoast, BC Gas, BCUC, MoFCR Treasury Board Staff and other stakeholders in September/October 1997.

Work stopped in 1998 for about 10 months while new royalties

were finalized under OGI 1.

BC Natural Gas Industry Competitiveness Study

We are here to:

Explain the data and methodology. Show the results. Receive comments and any further data. Identify problems with BC cost

competitiveness and suggest and receive suggestions on solutions to continue the Oil and Gas Initiative process.

BC Natural Gas Industry Competitiveness Study

Study Objective:

compare the cost competitiveness of natural gas exploration, production, gathering and processing in British Columbia to the costs of the same processes in Alberta.

Costs and revenues are to the plant exit.

BC Natural Gas Industry Competitiveness Study

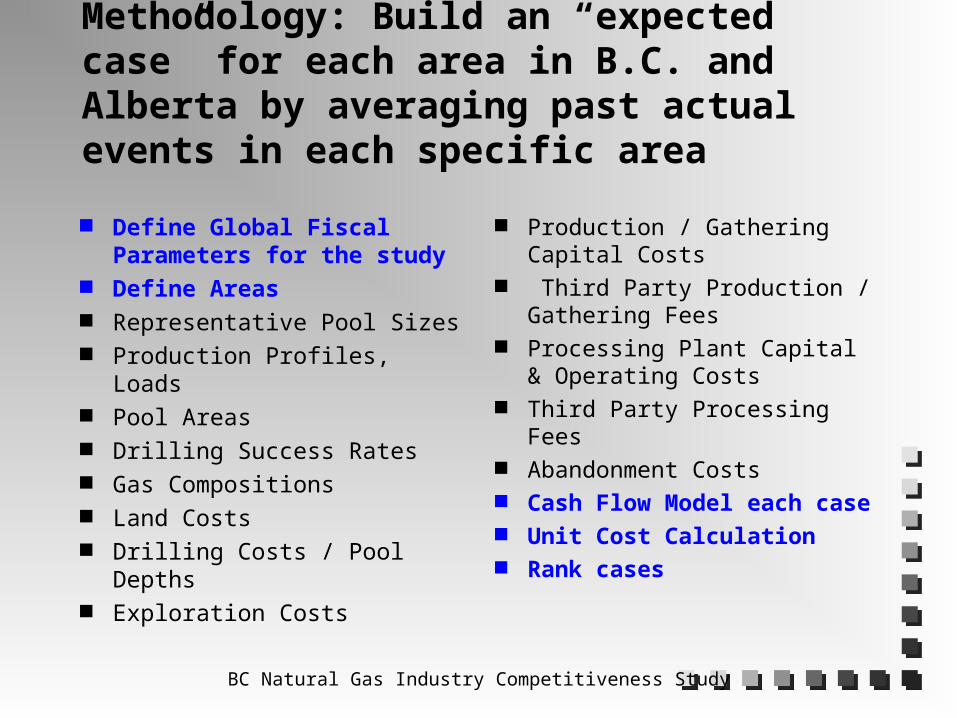

Methodology: Build an “expected case” for each area in B.C. and Alberta by averaging past actual events in each specific area

Define Global Fiscal Parameters for the study

Define Areas Representative Pool Sizes Production Profiles, Loads Pool Areas Drilling Success Rates Gas Compositions Land Costs Drilling Costs / Pool Depths Exploration Costs

Production / Gathering Capital Costs

Third Party Production / Gathering Fees

Processing Plant Capital & Operating Costs

Third Party Processing Fees Abandonment Costs Cash Flow Model each

case Unit Cost Calculation Rank cases

BC Natural Gas Industry Competitiveness Study

FISCAL PARAMETERSCERI 1996 Plant Gate Price Forecast similar to MEM forecast distinct differential between Alberta and BC plant prices consistent but conservative compared to other

forecasts developed by a respected outside agency necessary to make our cash flow model run

Discount Rate: Final Results discounted at 7% reflects long term cost of money - study is primarily

concerned with costs rather than profit.

BC Natural Gas Industry Competitiveness Study

CERI 1996 and NEB 1999 Plantgate Forecasts

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

C$

/ m

cf

NEB Alberta - Case 1NEB Alberta - Case 2BC 1996 CERIAB 1996 CERI

Sources: CERI North American Natural Gas Outlook: Basin on Basin CompetitionNEB Canadian Energy Supply and Demand to 2025

BC Natural Gas Industry Competitiveness Study

BC Natural Gas Industry Competitiveness Study

BC Natural Gas Industry Competitiveness Study

Jedney BC Area 11 Actual Pool Sizes Discovered from 1988 to 1995

0

5

10

15

20

25

30

35

40

BC

F

Lognormal Mean Pool = 23 BCF

BC Natural Gas Industry Competitiveness Study

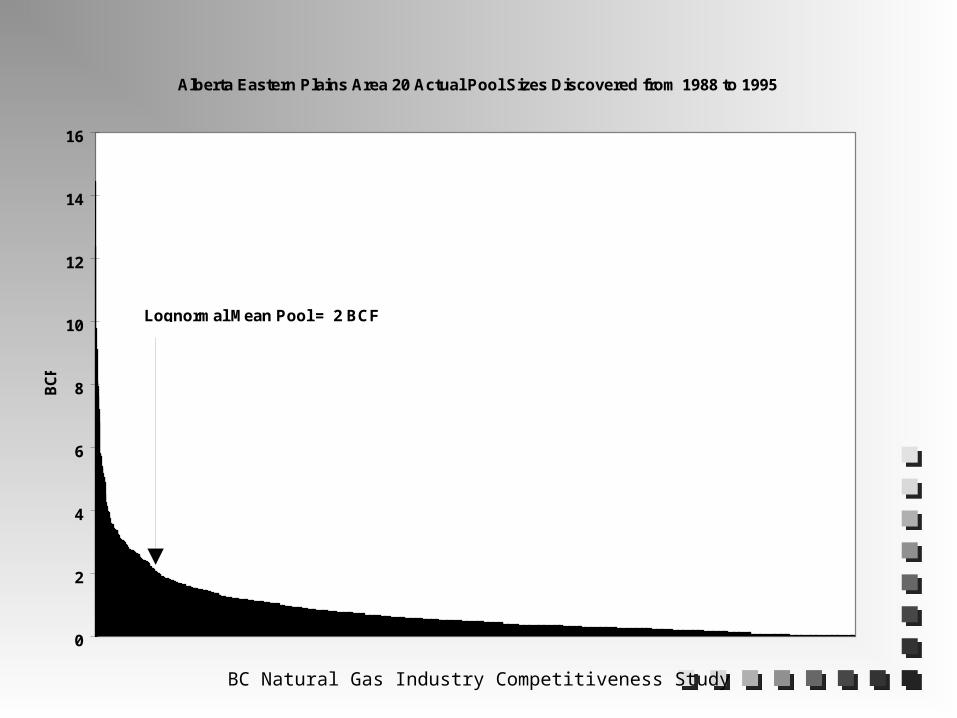

Alberta Eastern Plains Area 20 Actual Pool Sizes Discovered from 1988 to 1995

0

2

4

6

8

10

12

14

16

BC

F

Lognormal Mean Pool = 2 BCF

BC Natural Gas Industry Competitiveness Study

B.C and Alberta Pool Sizes and Pool Initial Production Rates

71

42

34

2926

23

18 17

12 11

31

26

21

10 10 9 95 4 4 3 3 2 2 0.75

48

20

3

1013

7

12

75 5

86

32

4 4 42 1 2

4

1 1 1

19

0

10

20

30

40

50

60

70

80

BC

3 P

ine

Riv

er

BC

14 F

t N

elso

n

BC

16 H

elm

et

AB

90

BC

6 S

ikan

ni

BC

5 B

orde

r

AB

63

BC

11 J

edne

y

AB

72

BC

8 P

arkl

and

BC

9 F

SJ

BC

10 B

eatt

on

BC

4 D

eep

Bas

in

AB

40

AB

80

AB

62

AB

71

AB

33

AB

10

AB

61

AB

32

AB

34

AB

20

AB

31

AB

50

BC

F

0

5

10

15

20

25

30

35

40

45

50

Po

ol

Init

ial

Rat

e m

mcf

/d

BC Pool Size BCF

Alberta Pool Size BCF

Pool Initial Rate mmcf/d

BC Natural Gas Industry Competitiveness Study

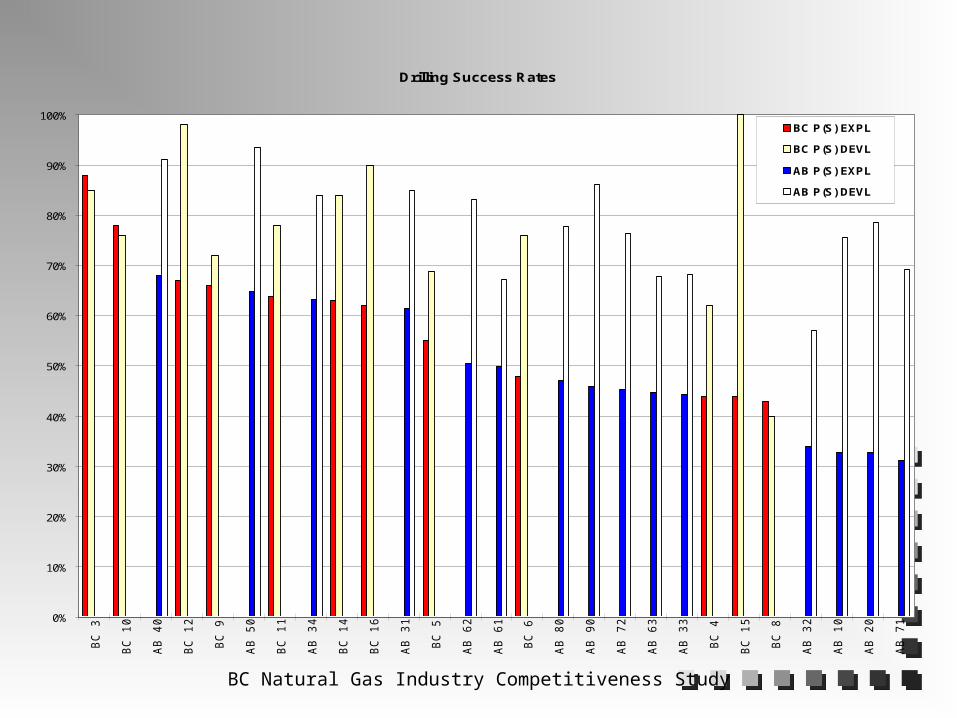

Drilling Success Rates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

BC

3

BC

10

AB

40

BC

12

BC

9

AB

50

BC

11

AB

34

BC

14

BC

16

AB

31

BC

5

AB

62

AB

61

BC

6

AB

80

AB

90

AB

72

AB

63

AB

33

BC

4

BC

15

BC

8

AB

32

AB

10

AB

20

AB

71

BC P(S) EXPL

BC P(S) DEVL

AB P(S) EXPL

AB P(S) DEVL

BC Natural Gas Industry Competitiveness Study

British Columbia and Alberta 1996 Licence Cost

$242

$275

$328

$258

$313

$335

$235

$140

$215

$107

$169

$203

$99

$196

$85

$166$167

$106

$162

$116$118$110

$64

$86$76

$97

$58

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000B

C 3

AB

90

BC

11

BC

5

BC

10

BC

9

BC

8

BC

16

AB

72

BC

14

AB

34

BC

4

BC

6

AB

80

AB

50

BC

12

AB

62

AB

61

AB

20

AB

40

AB

71

AB

33

BC

15

AB

63

AB

10

AB

32

AB

31

Tota

l B

on

us

per

Lic

ense

$0

$50

$100

$150

$200

$250

$300

$350

Do

llar

s p

er H

ecta

re

BC Bonus

AB Bonus

Avg/Ha

BC Natural Gas Industry Competitiveness Study

POOL AREA CALCULATION

Calculated using: database correlations of wells linked to

discovered pools database correlations of historic values

of reserves produced per well PEEP production profiles which resulted

in reasonable pool declines

BC Natural Gas Industry Competitiveness Study

PRODUCTION PROFILES AND WELL LOADS Aggregated a production profile from all

wells coming onstream in 1994 in each area using Merak Forecast.

Maximum rate used as initial rate. Initial rate combined with pool reserves

used to calculate decline.

Well load factors calculated from well onstream time. (Actual production hours divided by possible production hours)

BC Natural Gas Industry Competitiveness Study

Average Acid Gas Composition

0

0.05

0.1

0.15

0.2

0.25

0.3

BC

3 T

r

BC

14

BC

16

SP

AB

90

AB

50

BC

11

BC

3 O

ther

BC

6

AB

72

BC

15

BC

5

BC

9

AB

80

BC

7

BC

8

BC

10

BC

4

AB

62

BC

16

JM

AB

61

AB

63

AB

10

BC

12

Deb

olt

AB

20

AB

71

AB

33

AB

40

AB

32

BC

12

AB

34

AB

31

Mole

Fra

cti

on

CO2

H2S

BC Natural Gas Industry Competitiveness Study

Comparison of C3+ Liquids in the Raw Gas Stream and Liquids Recovered Allocated to Producers up to 1995

0.00

10.00

20.00

30.00

40.00

50.00

60.00

AB

63

AB

80

AB

50

AB

72

BC

11

BC

9

BC

10

AB

62

AB

90

BC

12

AB

10

AB

71

BC

4

BC

5

BC

6

AB

20

BC

7

BC

8

AB

61

BC

15

AB

32

BC

16

JM

BC

14

AB

33

AB

31

BC

16

SP

AB

34

AB

40

BC

3

Area

C3

+ B

bl./

Mm

sc

f

C3+ Recoverd Allocated to ProducersBbl./Mmscf

C3+ Unrecovered or Not Allocated toProducers Bbl./Mmscf

BC Natural Gas Industry Competitiveness Study

DRILLING COST ESTIMATE METHODOLOGY

Alberta Drilling Costs: Drilling days and depth determined for each area. Adjusted to PSAC study estimates for wells in same

region. Results compared to drilling cost data in Natural

Gas Royalty Review outline, Sproule Associates Oil and Gas Property Evaluation text, and ERCB 92-A Ultimate Potential and Supply of Natural Gas in Alberta.

BC Drilling Costs: Drilling and completion data obtained from Ministry

wellfiles - over 600 wells searched. Adjusted using Alberta methodology.

BC Natural Gas Industry Competitiveness Study

Alberta Area 90 (Foothills) Wells - 1988 to 1995

0

1000

2000

3000

4000

5000

6000

0 50 100 150 200 250 300

Days (RR-Spud Date)

Dep

th (M

eter

s)

Actual Depth

Calculated Depth

Average Well

BC Natural Gas Industry Competitiveness Study

Depth, Days Drilling Time and Drilling Rate

0

20

40

60

80

100

120

BC13

BC3

BC 1

AB 9

0BC

6BC

7BC

14BC

15 H

ZBC

15BC

4BC

5BC

16 H

ZBC

8AB

50

BC9

HZ

BC11

HZ

BC11

BC16

AB 6

3BC

10AB

72

BC9

AB 6

1BC

12AB

40

AB 8

0AB

62

AB 7

1AB

33

AB 3

2AB

34

AB 1

0AB

20

AB 3

1

Area

Depth*100 m/

Days

0

50

100

150

200

250

(M

/ D

ay)

Depth (100 m) Days Metres/Day

BC Natural Gas Industry Competitiveness Study

GATHERING AND PRODUCTION FACILITIES COSTSBC Gathering and Production Facilities Capital and operating costs of pipeline, dehydrators, and field

treatment plants based on 1996 Gas Production Facilities Study done for MEM for Producer Cost of Service (PCOS)

determination.Alberta Gathering and Production Facilities

Capital costs from several sources: Recent survey of vendors installed equipment costs. Studies such as Natural Gas Royalty Review Outline, Sproule

Associates Oil and Gas Property Evaluation course, ERCB 92-A Ultimate Potential and Supply of Natural Gas in Alberta and CAPP Well Operating Cost Study.

Discussions with producers, contractors and government agencies.

Operating costs estimated at 10% to 15% of capital costs.

BC Natural Gas Industry Competitiveness Study

Installed Dehydration Cost

0

50

100

150

200

250

0 10 20 30 40 50 60 70 80 90 100

Size (MMscf/d)

Un

it In

stal

led

Co

st (

$K/M

Msc

f/d

)

Alberta Sw eet Alberta Sour BC Sw eet BC Sour

BC Natural Gas Industry Competitiveness Study

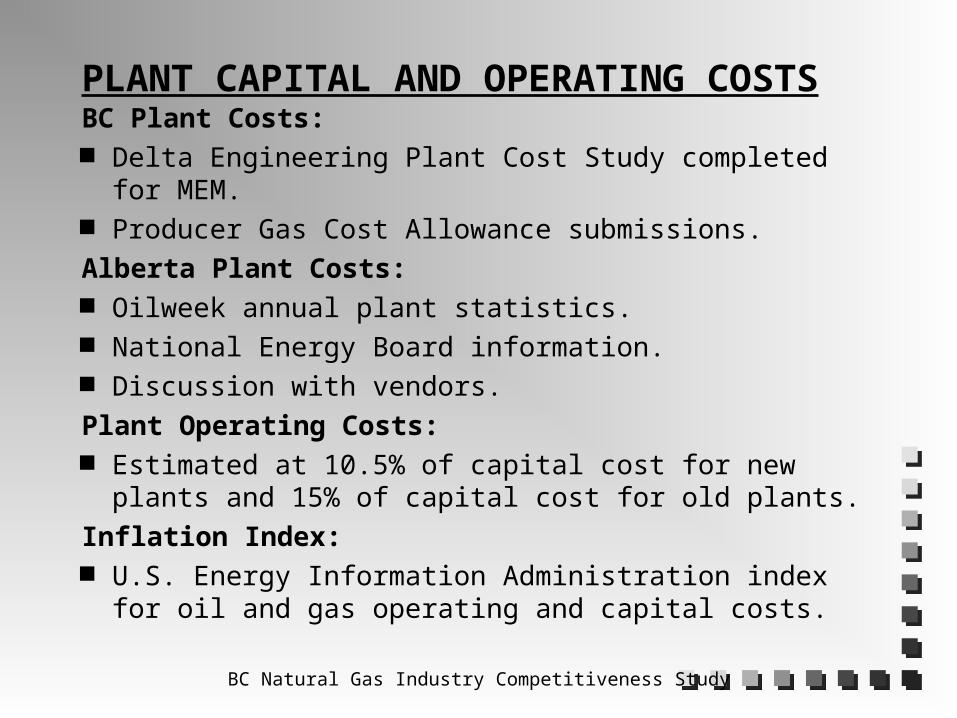

PLANT CAPITAL AND OPERATING COSTSBC Plant Costs: Delta Engineering Plant Cost Study completed for MEM. Producer Gas Cost Allowance submissions.

Alberta Plant Costs: Oilweek annual plant statistics. National Energy Board information. Discussion with vendors.

Plant Operating Costs: Estimated at 10.5% of capital cost for new plants and

15% of capital cost for old plants.

Inflation Index: U.S. Energy Information Administration index for oil and

gas operating and capital costs.

BC Natural Gas Industry Competitiveness Study

Dewpoint Plant Cost Trend Comparison(based on Regression)

0

10

20

30

40

50

60

70

80

90

0 50 100 150 200 250 300 350

Plant Capacity (Mmscf/d)

$MM

(19

95)

BC Dewpoint Plant Cost Alberta Dewpoint Plant Cost

BC Natural Gas Industry Competitiveness Study

Sour Gas Plant Cost Comparison

0

50

100

150

200

250

300

350

0 500 1000 1500 2000 2500 3000

Tonnes of Sulphur per Day

$ M

illio

ns

Inst

alle

d

($19

95)

Actual BC Cost BC Cost Based on Regression

Alberta Cost Based on Regression

BC Natural Gas Industry Competitiveness Study

THIRD PARTY PROCESSING COSTSBC Third Party Processing Fees Negotiated Westcoast tolls for treatment and RGT

service based on average gas composition. Non-Westcoast plant fees based on replacement costs

using JP 95 guidelines.

Alberta Third Party Processing Fees NEB information. Data from Natural Gas Royalty Review Outline and

ERCB 92-A Ultimate Potential and Supply of Natural Gas in Alberta.

Plant fees based on replacement costs using JP 95 guidelines.

Discussions with major plant operators.

BC Natural Gas Industry Competitiveness Study

THIRD PARTY GATHERING AND PRODUCTION FEES

BC Third Party Gathering and Production Fees:

Estimated from Producer Cost of Service (PCOS) data with returns based on the JP 95 formula.

Alberta Third Party Gathering and Production Fees:

National Energy Board information. Estimated based on replacement costs using

the JP 95 guidelines.

BC Natural Gas Industry Competitiveness Study

Unit Cost Methodology

Streams of Costs, Revenue and Production were discounted at 7%.

Unit costs are calculated by dividing the discounted cost by the discounted production to get $ per mcf.

Assigns a value for cost and revenue to each unit of production in a project.

BC Natural Gas Industry Competitiveness Study

AREA COMPARISONS

Cash Flow Model each case Unit Cost Calculation Rank cases

BC Natural Gas Industry Competitiveness Study

BC 9 FORT ST. JOHNUNIT COSTS, BURDENS AND REVENUE

$ / MCF7% DISCOUNT

$0.06 $0.01

$1.86

$0.27

$0.12

$0.04

$0.07

$0.65

$0.14

$0.32

$0.07

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

COSTS BURDENS REVENUE

Processing

Operating Gathering

Drilling

Exploration

$1.30

$0.40

$1.90

Land

Gas Royalty

Provincial Tax

Federal Tax

Fee + Levy

Gas Revenue

Liquids Revenue

BC Natural Gas Industry Competitiveness Study

AB90

BC8

BC6

BC16

AB72

BC4 ELM

AB62

BC3

AB50

BC5 AA

BC5 McM

AB34

BC14

AB10

BC10

AB32

AB61

BC9

AB20

BC11

AB33

AB80

AB71

AB40

AB63

AB31

$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00

AB90

BC8

BC6

BC16

AB72

BC4 ELM

AB62

BC3

AB50

BC5 AA

BC5 McM

AB34

BC14

AB10

BC10

AB32

AB61

BC9

AB20

BC11

AB33

AB80

AB71

AB40

AB63

AB31

DRILLING COST - $ / MCF7% DISCOUNT

BC Exploration Cost

BC Drilling Cost

Alberta Exploration Cost

Alberta Drilling Cost

Mean = $0.45

Median = $0.38

BC Natural Gas Industry Competitiveness Study

BC3

AB90

BC14

BC11

AB72

BC9

BC10

AB61

AB40

BC4 ELM

AB10

AB50

BC8

AB34

AB71

AB62

AB80

BC6

AB33

AB32

AB20

BC5 AA

BC5 McM

AB31

AB63

BC16

$0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40

BC3

AB90

BC14

BC11

AB72

BC9

BC10

AB61

AB40

BC4 ELM

AB10

AB50

BC8

AB34

AB71

AB62

AB80

BC6

AB33

AB32

AB20

BC5 AA

BC5 McM

AB31

AB63

BC16

OPERATING, GATHERING AND PROCESSING COSTS$ / MCF

7% DISCOUNT

BC Processing

BC Gathering

Alberta Processing

Alberta Gathering

Alberta Well OC

Median = $0.79

Mean = $0.81

BC Natural Gas Industry Competitiveness Study

AB63

AB80

AB20

AB32

AB10

BC5 AA

AB61

AB62

AB40

AB33

BC5 McM

AB72

AB34

BC4 ELM

BC10

AB50

AB31

BC9

AB71

BC11

BC16

BC8

AB90

BC14

BC6

BC3

$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00

AB63

AB80

AB20

AB32

AB10

BC5 AA

AB61

AB62

AB40

AB33

BC5 McM

AB72

AB34

BC4 ELM

BC10

AB50

AB31

BC9

AB71

BC11

BC16

BC8

AB90

BC14

BC6

BC3

TOTAL BURDENS - $ / MCF7% DISCOUNT

BC Bonus

BC Fees

BC Crown Royalty

BC Provincial Tax

Alberta Bonus

Alberta Fees

Alberta Crown Royalty

Alberta Provincial Tax

Federal Tax

Median = $0.50

Mean = $0.48

BC Natural Gas Industry Competitiveness Study

AB63

AB80

BC5 AA

AB32

AB62

AB20

AB10

AB72

AB40

AB33

AB61

BC4 ELM

BC5 McM

AB34

BC9

BC10

AB31

AB50

AB71

BC8

AB90

BC11

BC6

BC16

BC14

BC3

$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60

AB63

AB80

BC5 AA

AB32

AB62

AB20

AB10

AB72

AB40

AB33

AB61

BC4 ELM

BC5 McM

AB34

BC9

BC10

AB31

AB50

AB71

BC8

AB90

BC11

BC6

BC16

BC14

BC3

PROVINCIAL BURDENS - $ / MCF7% DISCOUNT

BC Administration Fees

BC Crown Royalty

BC Provincial Tax

Alberta Administration Fees

Alberta Crown Royalty

Alberta Provincial Tax

Mean = $0.24

Median = $0.24

BC Natural Gas Industry Competitiveness Study

AB63

AB80

BC5 AA

AB62

AB32

BC4 ELM

AB72

AB20

AB10

AB33

AB61

AB40

AB34

BC8

AB90

AB50

BC9

BC5 McM

AB31

BC6

AB71

BC10

BC16

BC11

BC14

BC3

$0.25

$0.23

$0.21

$0.20

$0.20

$0.20

$0.20

$0.20

$0.18

$0.18

$0.17

$0.16

$0.16

$0.16

$0.15

$0.15

$0.14

$0.12

$0.12

$0.12

$0.11

$0.11

$0.10

$0.10

$0.10

$0.06

$- $0.05 $0.10 $0.15 $0.20 $0.25 $0.30

AB63

AB80

BC5 AA

AB62

AB32

BC4 ELM

AB72

AB20

AB10

AB33

AB61

AB40

AB34

BC8

AB90

AB50

BC9

BC5 McM

AB31

BC6

AB71

BC10

BC16

BC11

BC14

BC3

CROWN ROYALTY - $ / MCF7% DISCOUNT

BC Crown Royalty

Alberta Crown Royalty

Mean = $0.16

Median = $0.16

BC Natural Gas Industry Competitiveness Study

BC8

BC4 ELM

BC5 AA

BC5 McM

BC9

BC16

BC10

AB50

AB10

BC6

AB40

BC11

BC14

AB34

BC3

AB20

AB31

AB61

AB33

AB32

AB71

AB62

AB72

AB80

AB63

AB90

$0.012

$0.010

$0.010

$0.010

$0.010

$0.010

$0.010

$0.008

$0.0082

$0.008

$0.008

$0.008

$0.007

$0.007

$0.007

$0.006

$0.006

$0.006

$0.005

$0.005

$0.004

$0.004

$0.004

$0.003

$0.002

$0.002

$0

.00

0

$0

.00

2

$0

.00

4

$0

.00

6

$0

.00

8

$0

.01

0

$0

.01

2BC8

BC4 ELM

BC5 AA

BC5 McM

BC9

BC16

BC10

AB50

AB10

BC6

AB40

BC11

BC14

AB34

BC3

AB20

AB31

AB61

AB33

AB32

AB71

AB62

AB72

AB80

AB63

AB90

ADMINISTRATIVE FEES AND LEVIES - $ / MCF7% DISCOUNT

BC Fee+Levy

Alberta Fee

Mean and Median = $0.007

BC Natural Gas Industry Competitiveness Study

AB20

BC4 ELM

AB61

AB50

AB34

AB32

AB10

BC16

AB80

AB71

BC11

AB33

BC8

BC9

AB62

AB31

AB90

BC10

AB40

AB72

BC5 AA

BC5 McM

BC6

AB63

BC14

BC3

$0.32

$0.16

$0.16

$0.15

$0.15

$0.13

$0.12

$0.10

$0.10

$0.09

$0.08

$0.08

$0.07

$0.07

$0.07

$0.06

$0.06

$0.06

$0.05

$0.05

$0.04

$0.04

$0.03

$0.02

$0.02

$0.02

$0.00 $0.05 $0.10 $0.15 $0.20 $0.25 $0.30 $0.35

AB20

BC4 ELM

AB61

AB50

AB34

AB32

AB10

BC16

AB80

AB71

BC11

AB33

BC8

BC9

AB62

AB31

AB90

BC10

AB40

AB72

BC5 AA

BC5 McM

BC6

AB63

BC14

BC3

LAND COSTS- $ / MCF7% DISCOUNT

BC Bonus

Alberta Bonus

Median = $ 0.07

Mean = $0.09

BC Natural Gas Industry Competitiveness Study

BC16

BC3

AB34

BC14

BC11

AB50

AB31

AB33

BC9

BC8

BC6

BC4 ELM

BC5 AA

BC5 McM

AB40

AB20

AB61

BC10

AB32

AB10

AB71

AB62

AB90

AB72

AB80

AB63

$0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00

BC16

BC3

AB34

BC14

BC11

AB50

AB31

AB33

BC9

BC8

BC6

BC4 ELM

BC5 AA

BC5 McM

AB40

AB20

AB61

BC10

AB32

AB10

AB71

AB62

AB90

AB72

AB80

AB63

GAS AND LIQUIDS GROSS REVENUE - $ / MCF7% DISCOUNT

Liquids Revenue

BC Gas Revenue

Liquids Revenue

Alberta Gas Revenue

Mean = $2.10

Median = $2.08

BC Natural Gas Industry Competitiveness Study

BC3

BC8

AB90

BC16

BC4 ELM

BC6

AB34

BC14

AB50

BC9

BC11

AB61

AB20

AB72

AB33

BC10

AB10

BC5 AA

AB40

AB62

BC5 McM

AB32

AB31

AB80

AB71

AB63

-$0.20 $0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20

BC3

BC8

AB90

BC16

BC4 ELM

BC6

AB34

BC14

AB50

BC9

BC11

AB61

AB20

AB72

AB33

BC10

AB10

BC5 AA

AB40

AB62

BC5 McM

AB32

AB31

AB80

AB71

AB63

NET REVENUE AT PLANT EXITCosts and Burdens Subtracted From Gas Revenue

$ / MCF7% DISCOUNT

BC Liquid Revenue

BC Gas Revenue -(Costs + Burdens)

Alberta Liquid Revenue

Alberta Gas Revenue -(Costs + Burdens)

Costs do not include downstream costs such as pipeline transportation, storage, marketing and rate of return.

BC Natural Gas Industry Competitiveness Study

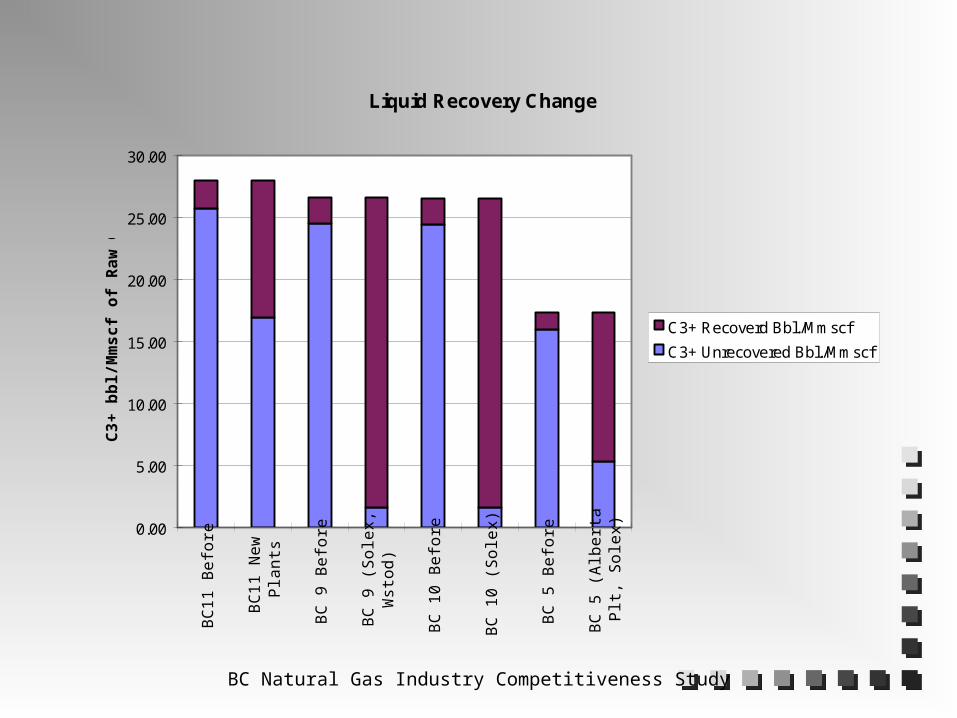

Liquid Recovery Change

0.00

5.00

10.00

15.00

20.00

25.00

30.00

BC

11 B

efo

re

BC

11 N

ew

Pla

nts

BC

9 B

efo

re

BC

9 (

So

lex,

Wst

od

)

BC

10

Be

fore

BC

10

(S

ole

x)

BC

5 B

efo

re

BC

5 (

Alb

ert

aP

lt, S

ole

x)

C3

+ b

bl/

Mm

sc

f o

f R

aw

Ga

s

C3+ Recoverd Bbl./Mmscf

C3+ Unrecovered Bbl./Mmscf

BC Natural Gas Industry Competitiveness Study

ECONOMIC INDICATORS

$10,585

$2,210$1,965

$1,739$1,656

$1,192$866 $787 $699

$379 $326 $310 $295$62

-$1,819

$7,799

$7,080

$3,167$2,893$2,771

$1,879

$1,382$1,237

$603 $458

-$114

-$2,000

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000A

B6

3

BC

5 M

cM

BC

5 A

A

BC

14

BC

10

BC

11

AB

80

AB

72

BC

9

AB

40

AB

62

BC

6

BC

4 E

LM

AB

33

AB

71

AB

32

AB

10

BC

16

BC

3

AB

61

AB

31

AB

20

AB

34

AB

50

BC

8

AB

90

NP

V @

10%

(M

$)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

RO

R

Alberta NPV @ 10%

BC NPV @ 10%

ROR

BC Mean NPV @ 10% = $2,650

BC Median NPV @ 10% = $1,879

Alberta Mean NPV @ 10% = $1,417

Alberta Median NPV @ 10% = $787

Mean = $1,939 Median = $1,215

Distribution Mean NPV @ 10% = $1,939

Distribution Median NPV @ 10% = $1,215

BC Natural Gas Industry Competitiveness Study

BC Gas Wells Drilled from 1996 to Sept. 1999

0

50

100

150

200

250

300

350A

rea

14

Are

a 9

Are

a 1

0

Are

a 1

1

Are

a 5

Are

a 1

2

Are

a 1

6

Are

a 4

Are

a 1

5

Are

a 6

Are

a 7

Are

a 8

Are

a 3

Are

a 1

Are

a 1

3

Are

a 2

Ga

s W

ells

Dri

lled

Development

Exploration

BC Natural Gas Industry Competitiveness Study

POSITIVES

Larger pool sizes, higher initial production rates, better drilling success rates.

Project Net Present Value and Rate of Return are competitive in many areas.

Direct burdens are very competitive. Treaty 8 MOUs ==> Costs predictable. EA Review thresholds have been raised. WCB issues are not significant problems.

BC Natural Gas Industry Competitiveness Study

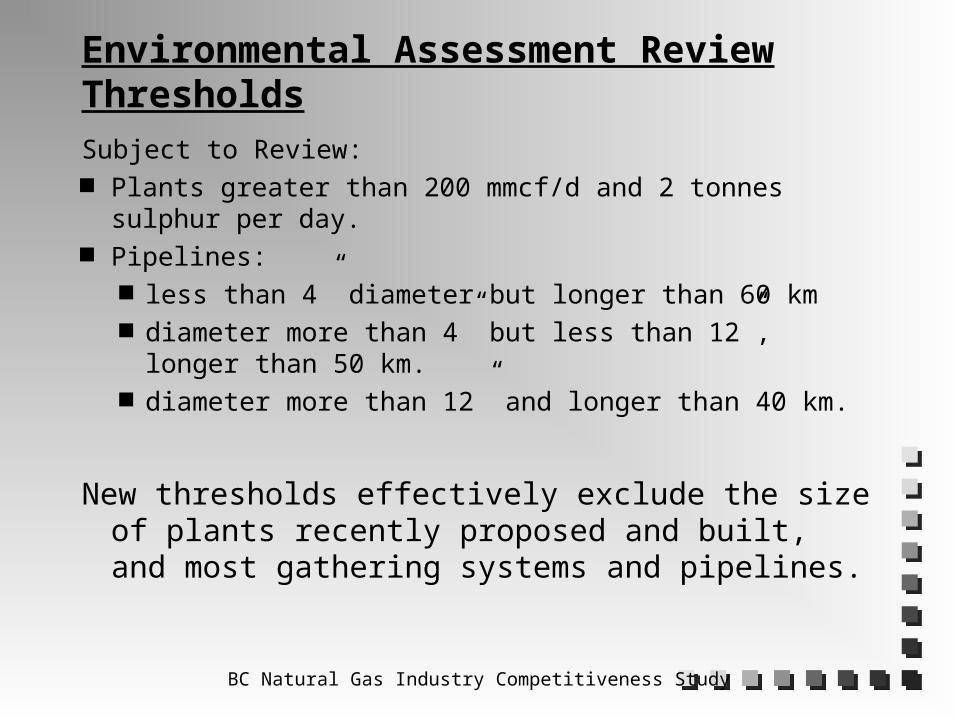

Environmental Assessment Review Thresholds

Subject to Review: Plants greater than 200 mmcf/d and 2 tonnes sulphur per

day. Pipelines:

less than 4” diameter but longer than 60 km diameter more than 4” but less than 12”, longer than

50 km. diameter more than 12” and longer than 40 km.

New thresholds effectively exclude the size of plants recently proposed and built, and most gathering systems and pipelines.

BC Natural Gas Industry Competitiveness Study

WCB Issues Large gap between WCB and Industry perceptions of

operating environment (with Energy and Mines caught in between).

WCB: Problems resolved years ago after consultation.

Style difference - “Involved” vs. “Hands-off”. Regulations are similar in Alberta and BC.

Anecdotes or documented incidents? 1998 Drilling Industry Assessment Rates:

Alberta: $1.99 per $100 payroll BC: $1.69 per $100 payroll

BC Natural Gas Industry Competitiveness Study

Labour Cost Wages are about 3% higher in BC due

to the negotiated exclusion from the Employment Standards Act. (Drilling example)

Used CAODC data for a typical rig. Same hours worked but more hours

paid as overtime.

BC Natural Gas Industry Competitiveness Study

Costs Due to Resource Characteristics Completed well costs are higher in BC

because pools are deeper, and often in remote areas. Road improvements would help reduce these costs.

Facility and processing costs are higher due to higher CO2 and H2S contents.

Revenue is less due to lower liquids content.

BC Natural Gas Industry Competitiveness Study

Well Load Factors are lower in BC.

Ratio of hours a well operates to possible operating hours (“on-time”).

Significantly affects economics and profitability.

Comparison suggests plant capacity or suitability is less optimal than in Alberta.

BC Natural Gas Industry Competitiveness Study

BC

11

BC

10

BC

4

BC

6

BC

9

BC

15

BC

5

AB

72

AB

61

AB

20

AB

71

AB

80

BC

12

BC

14

BC

3

BC

8

AB

32

AB

34

AB

50

AB

62

AB

33

BC

16

AB

31

AB

40

AB

63

AB

90

AB

10

73%74%75%

80%80%

84%85% 85%86%87%

88%88%

89%89%90%90% 90%90%90%91%92%93% 93%94%94%94%95%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%B

C1

1

BC

10

BC

4

BC

6

BC

9

BC

15

BC

5

AB

72

AB

61

AB

20

AB

71

AB

80

BC

12

BC

14

BC

3

BC

8

AB

32

AB

34

AB

50

AB

62

AB

33

BC

16

AB

31

AB

40

AB

63

AB

90

AB

10

Area Well Load Factors

BC Natural Gas Industry Competitiveness Study

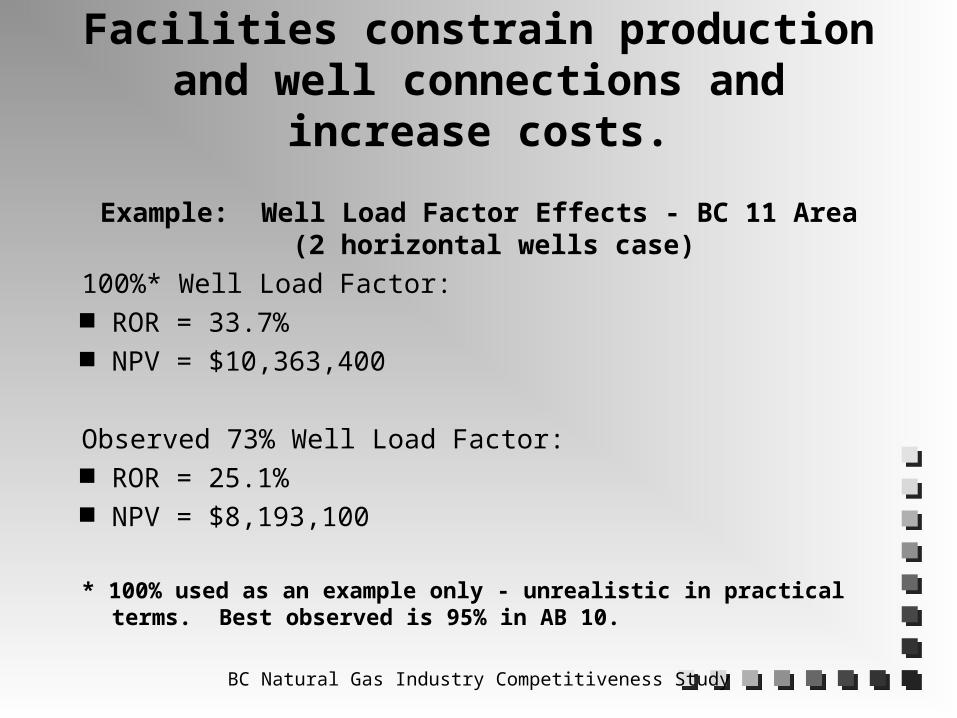

Facilities constrain production and well connections and increase costs.

Example: Well Load Factor Effects - BC 11 Area(2 horizontal wells case)

100%* Well Load Factor: ROR = 33.7% NPV = $10,363,400

Observed 73% Well Load Factor: ROR = 25.1% NPV = $8,193,100

* 100% used as an example only - unrealistic in practical terms. Best observed is 95% in AB 10.

BC Natural Gas Industry Competitiveness Study

Trends:

1. Increasing proportion of connections to smaller plants due to:

higher well loads more efficient liquids extraction flexible tolling

2. Increasing exploration target land sales in border areas and near smaller plants.

BC Natural Gas Industry Competitiveness Study

Zone to Plant Connections

73%77% 76%

81%

66%

57% 56%

27%23% 24%

19%

34%

43% 44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1990 1991 1992 1993 1994 1995 1996to

Sept1997

NEB

Non-NEB

BC Natural Gas Industry Competitiveness Study

Taxes

The Compressor Fuel Tax adds two cents per mcf to costs to the plant exit.

Social Services Tax increases costs 2.4%. Property taxes appear to be slightly higher

in BC. Estimated at 2.4 cents per mcf in Alberta versus

2.8 cents per mcf in BC. Need better data - too much uncertainty.

BC Natural Gas Industry Competitiveness Study

Social Services Tax increases costs by 2.4%, not 7%.

Activity Spending Subject to Tax Effective TaxDrilling and Completions 34% 2.4%Facilities and Equipment 48% 3.4%Total Capital 40% 2.8%Operating Expenditures 20% 1.4%Total Expenditures 34% 2.4%

BC Natural Gas Industry Competitiveness Study

Roads

Poor public road infrastructure increases all costs, constrains production and revenue and discourages investment.

BC Natural Gas Industry Competitiveness Study

OPPORTUNITIES FOR IMPROVEMENT

Improve road infrastructure and maintenance.

Improve plant infrastructure and promote even more competition in the processing sector.

Improve liquids infrastructure. Fort St. John as centre of competitive service

industry.