be sure to utilize legal and accounting counsel before ... to assist leadership and staff in...

TRANSCRIPT

Information to assist leadership and staff in reviewing and adopting policiesidentified in the new IRS Form 990 (Dec. 2007.)

The new form will be used in 2009 for the 2008 tax year. According to theIRS website, “Form 990 has not been significantly revised since 1979, and itis universally regarded as needing major revision. It has failed to keep pacewith changes in the law and with the increasing size, diversity, andcomplexity of the exempt sector. As a result, the current form fails to meetthe Service’s tax compliance interests or the transparency and accountabilityneeds of the states, the general public, and local communities served by theorganization.”

For a copy of Form 990, visit www.irs.gov/pub/irs-tege/f-990rcore.pdf

Be sure to utilize legal and accounting counsel before adopting policies.

This information supplements the article titled, “Year of the Policy Manual –2008.”

Contents

• Document Destruction – Record Retention• Conflict of Interest• Audit – Audit Committee

For educational purposes only. Rely on legal and accounting counselwhen reviewing governance, laws, etc.

Resources at Grant Thornton can be found at www.grantthornton.com.

Policy Samples Packet4-08

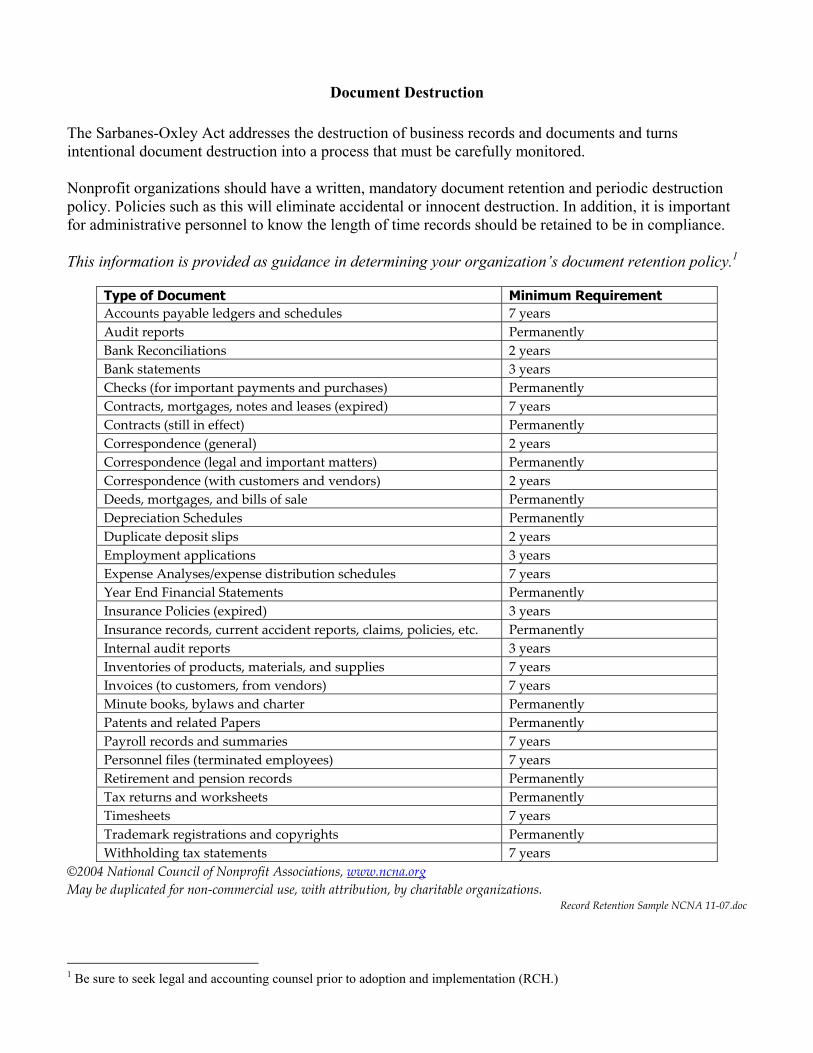

Document Destruction

The Sarbanes-Oxley Act addresses the destruction of business records and documents and turnsintentional document destruction into a process that must be carefully monitored.

Nonprofit organizations should have a written, mandatory document retention and periodic destructionpolicy. Policies such as this will eliminate accidental or innocent destruction. In addition, it is importantfor administrative personnel to know the length of time records should be retained to be in compliance.

This information is provided as guidance in determining your organization’s document retention policy.1

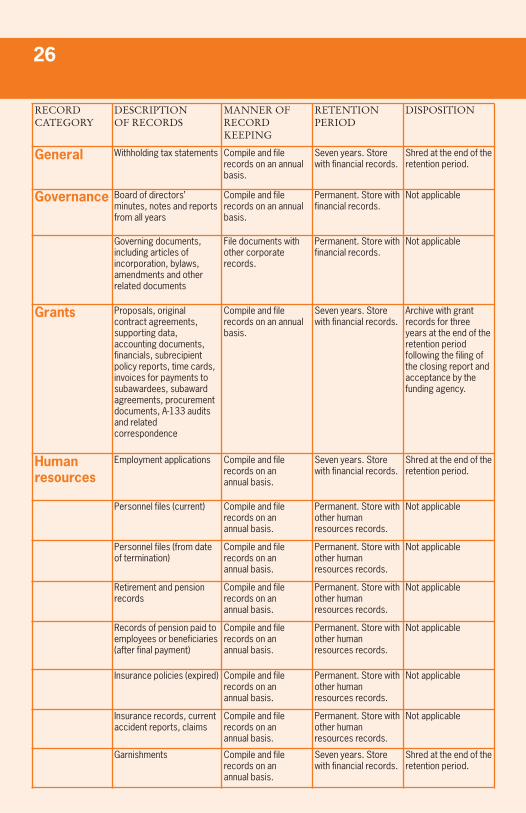

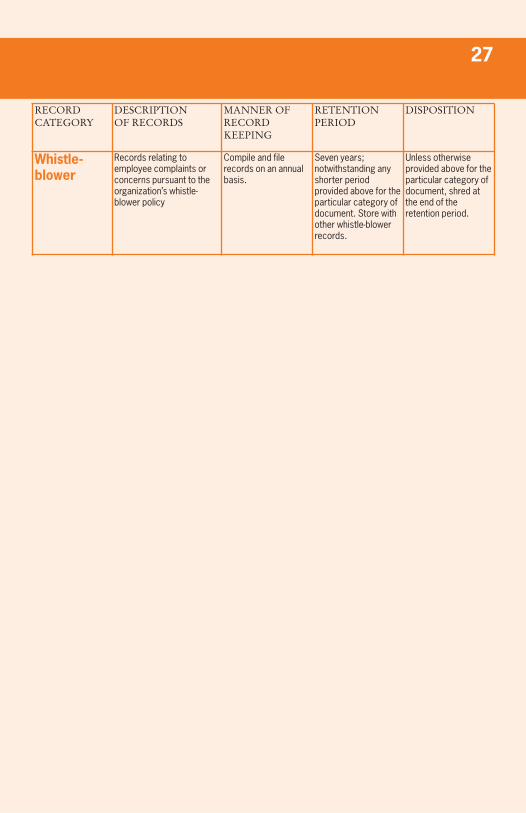

Type of Document Minimum RequirementAccounts payable ledgers and schedules 7 yearsAudit reports PermanentlyBank Reconciliations 2 yearsBank statements 3 yearsChecks (for important payments and purchases) PermanentlyContracts, mortgages, notes and leases (expired) 7 yearsContracts (still in effect) PermanentlyCorrespondence (general) 2 yearsCorrespondence (legal and important matters) PermanentlyCorrespondence (with customers and vendors) 2 yearsDeeds, mortgages, and bills of sale PermanentlyDepreciation Schedules PermanentlyDuplicate deposit slips 2 yearsEmployment applications 3 yearsExpense Analyses/expense distribution schedules 7 yearsYear End Financial Statements PermanentlyInsurance Policies (expired) 3 yearsInsurance records, current accident reports, claims, policies, etc. PermanentlyInternal audit reports 3 yearsInventories of products, materials, and supplies 7 yearsInvoices (to customers, from vendors) 7 yearsMinute books, bylaws and charter PermanentlyPatents and related Papers PermanentlyPayroll records and summaries 7 yearsPersonnel files (terminated employees) 7 yearsRetirement and pension records PermanentlyTax returns and worksheets PermanentlyTimesheets 7 yearsTrademark registrations and copyrights PermanentlyWithholding tax statements 7 years

©2004 National Council of Nonprofit Associations, www.ncna.orgMay be duplicated for non-commercial use, with attribution, by charitable organizations.

Record Retention Sample NCNA 11-07.doc

1 Be sure to seek legal and accounting counsel prior to adoption and implementation (RCH.)

MPLS-Word 126260.1 1

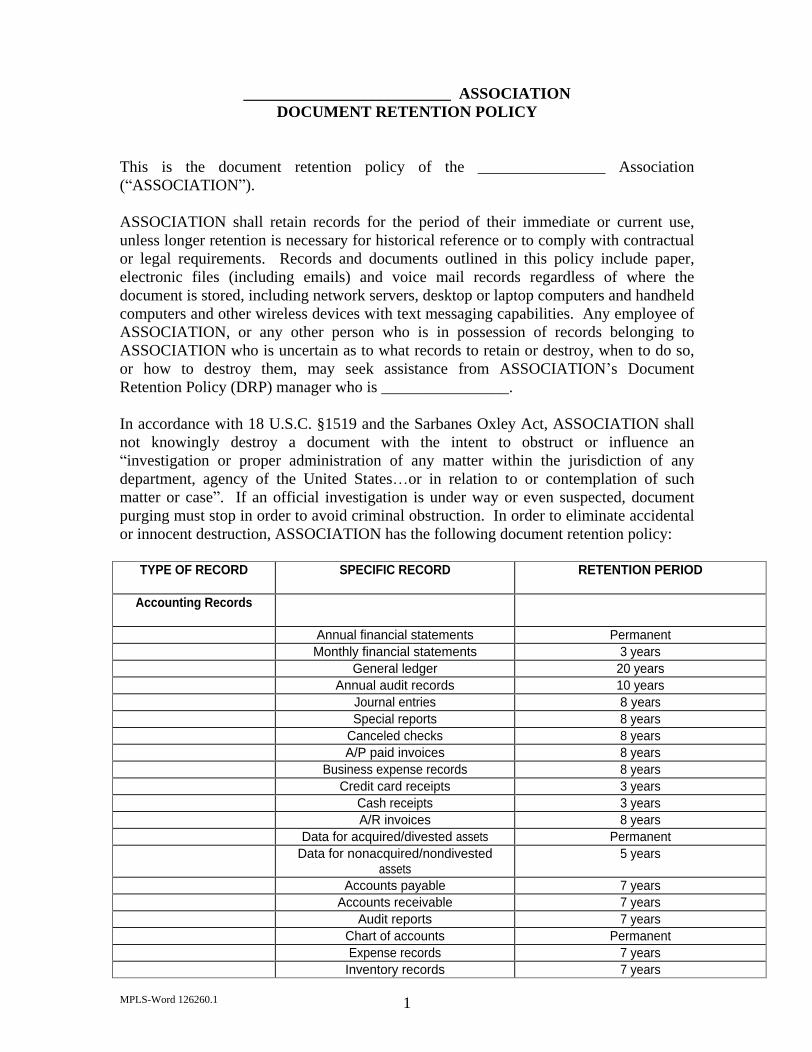

__________________________ ASSOCIATION

DOCUMENT RETENTION POLICY

This is the document retention policy of the ________________ Association ( ASSOCIATION ).

ASSOCIATION shall retain records for the period of their immediate or current use, unless longer retention is necessary for historical reference or to comply with contractual or legal requirements. Records and documents outlined in this policy include paper, electronic files (including emails) and voice mail records regardless of where the document is stored, including network servers, desktop or laptop computers and handheld computers and other wireless devices with text messaging capabilities. Any employee of ASSOCIATION, or any other person who is in possession of records belonging to ASSOCIATION who is uncertain as to what records to retain or destroy, when to do so, or how to destroy them, may seek assistance from ASSOCIATION s Document Retention Policy (DRP) manager who is ________________.

In accordance with 18 U.S.C. §1519 and the Sarbanes Oxley Act, ASSOCIATION shall not knowingly destroy a document with the intent to obstruct or influence an investigation or proper administration of any matter within the jurisdiction of any

department, agency of the United States or in relation to or contemplation of such matter or case . If an official investigation is under way or even suspected, document purging must stop in order to avoid criminal obstruction. In order to eliminate accidental or innocent destruction, ASSOCIATION has the following document retention policy:

TYPE OF RECORD SPECIFIC RECORD RETENTION PERIOD

Accounting Records

Annual financial statements Permanent

Monthly financial statements 3 years

General ledger 20 years

Annual audit records 10 years

Journal entries 8 years

Special reports 8 years

Canceled checks 8 years

A/P paid invoices 8 years

Business expense records 8 years

Credit card receipts 3 years

Cash receipts 3 years

A/R invoices 8 years

Data for acquired/divested assets Permanent

Data for nonacquired/nondivested assets

5 years

Accounts payable 7 years

Accounts receivable 7 years

Audit reports 7 years

Chart of accounts Permanent

Expense records 7 years

Inventory records 7 years

MPLS-Word 126260.1 2

TYPE OF RECORD SPECIFIC RECORD RETENTION PERIOD

Loan documents 7 years after final payment

Purchase orders 7 years

Sales records 7 years

Stop payment orders 3 years

Bank reconciliations 3 years

Tax Records

Federal tax returns (not payroll)

Permanent

State & local tax returns Permanent

Form 990 & supporting documentation

Permanent

Form 990-T & supporting documentation

Permanent

Supporting documentation for taxes

4 years

City & State excise tax reports & supporting

documentation

5 years (or longer if designated by state law)

Unclaimed property filings & supporting documentation

6 years (or longer if designated by state law)

1099 forms 8 years

Magnetic tape & similar records

1 year

Payroll taxes (W2, W3) Permanent

Payroll taxes (Form 941, state withholding forms,

state unemployment returns)

8 years (or longer if designated by state law)

Payroll Records

Wage rate tables 3 years

Cost of living tables 3 years

Wage 6 years

Salary 6 years

Payroll deductions 6 years

Time cards or forms 5 years

W-2 forms 8 years

W-4 forms 8 years

Garnishments 4 years after termination

Payroll registers Permanent

State employment forms 4 years

State unemployment tax records

Permanent

Cancelled payroll checks 8 years

Deductions register 8 years

Earnings records 8 years

Changes or adjustments to salary

8 years

MPLS-Word 126260.1 3

TYPE OF RECORD SPECIFIC RECORD RETENTION PERIOD

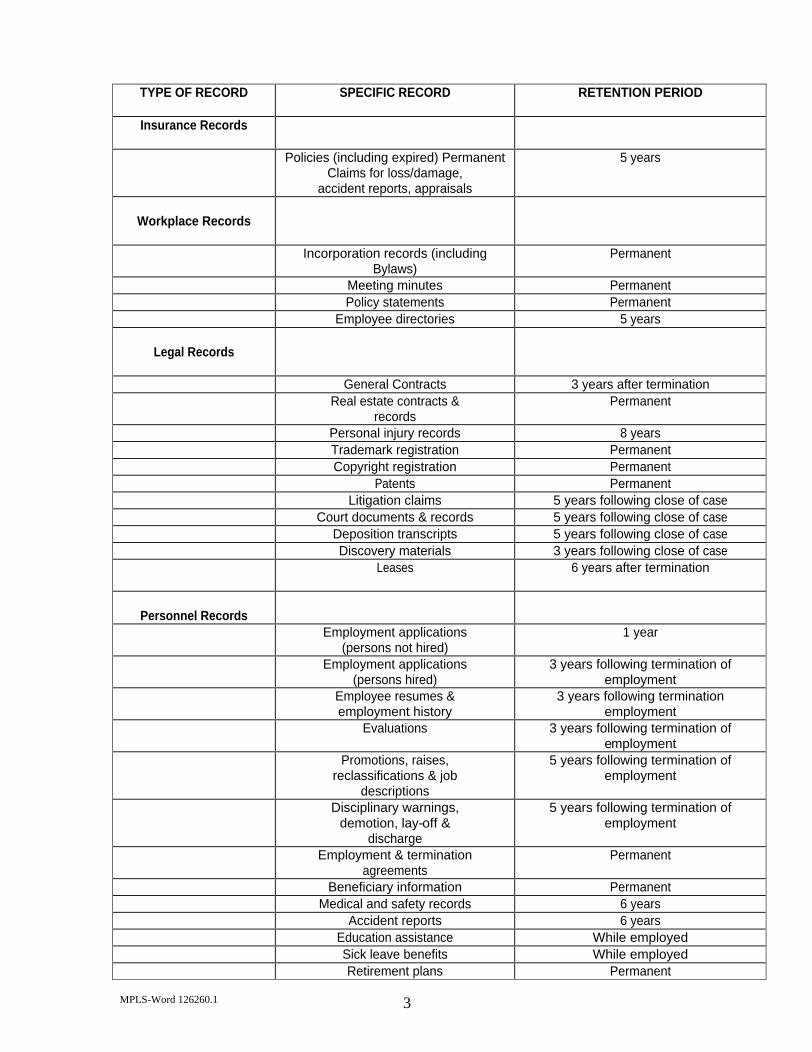

Insurance Records

Policies (including expired) Permanent

Claims for loss/damage, accident reports, appraisals

5 years

Workplace Records

Incorporation records (including Bylaws)

Permanent

Meeting minutes Permanent

Policy statements Permanent

Employee directories 5 years

Legal Records

General Contracts 3 years after termination

Real estate contracts & records

Permanent

Personal injury records 8 years

Trademark registration Permanent

Copyright registration Permanent

Patents Permanent

Litigation claims 5 years following close of case

Court documents & records 5 years following close of case

Deposition transcripts 5 years following close of case

Discovery materials 3 years following close of case

Leases 6 years after termination

Personnel Records

Employment applications (persons not hired)

1 year

Employment applications (persons hired)

3 years following termination of employment

Employee resumes & employment history

3 years following termination employment

Evaluations 3 years following termination of employment

Promotions, raises, reclassifications & job

descriptions

5 years following termination of employment

Disciplinary warnings, demotion, lay-off &

discharge

5 years following termination of employment

Employment & termination agreements

Permanent

Beneficiary information Permanent

Medical and safety records 6 years

Accident reports 6 years

Education assistance While employed

Sick leave benefits While employed

Retirement plans Permanent

MPLS-Word 126260.1 4

TYPE OF RECORD SPECIFIC RECORD RETENTION PERIOD

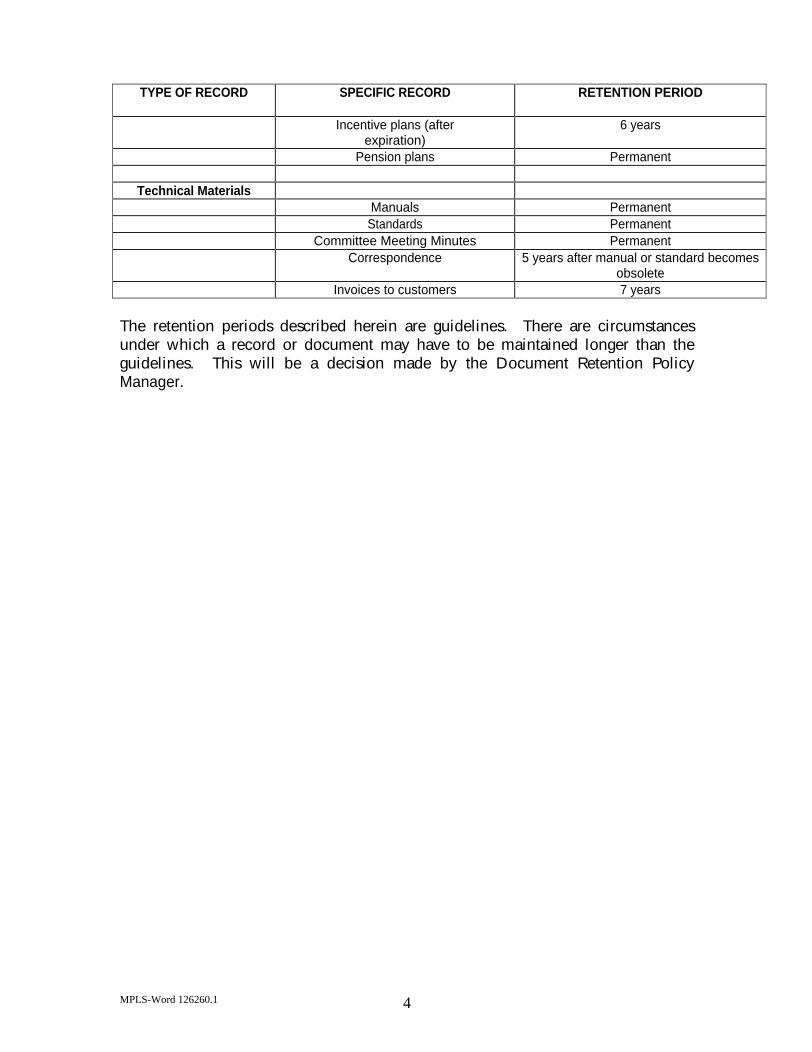

Incentive plans (after

expiration) 6 years

Pension plans Permanent

Technical Materials

Manuals Permanent

Standards Permanent

Committee Meeting Minutes Permanent

Correspondence 5 years after manual or standard becomes obsolete

Invoices to customers 7 years

The retention periods described herein are guidelines. There are circumstances under which a record or document may have to be maintained longer than the guidelines. This will be a decision made by the Document Retention Policy Manager.

Code of EthicsBoard of Directors and Officers

Of the_____________________

Service on the Board of Directors of a national organization is an importanthonor and responsibility. Much is expected of officers and the governing Board of the________. The membership of the association relies on its officers and Board to act inits best interests, to be knowledgeable about and proactive on the issues facing theearly childhood care and education industry, to study the questions before it and tobase decisions on reliable information, to be a good steward of the resources of theassociation, and to be honest and trustworthy in all actions. To assure the trust andethical expectations of the members of the ______ Association, I affirm the following:

Duty of Care

In all matters affecting the ______ Association, I will act in good faith and exercise mybest efforts in the performance of my duties.

I will faithfully prepare for discussions and decisions that affect the association byreading information sent to me by the association officers and staff and by striving tobe knowledgeable on issues of importance to the association and its members.

I will be responsible for disseminating information I receive as a Director to allmembers, with my primary responsibility to inform my constituency, i.e., stateassociation, national, or regional company, or at-large members. (See attachedexamples)

I will make decisions based on factual data rather than unsubstantiated opinions.

I will make decisions based on what is in the best interest of all members of theassociation, rather than any one group, individual, or special interest.

I will be honest in doing the work of the association and in speaking on behalf of theassociation and its leadership in order to foster trust among association members andthe public.

I will respect my fellow Directors and the members of the association, acknowledgingdifferences of opinion, providing for open and respectful discussion, and makingdecisions only after listening to all points of view and all available data.

I will publicly support the majority decisions made by the Board of Directors.

I will refrain from any discussion of tuition, fees, wages, etc. that might be construedas an infraction of anti-trust law or price fixing.

I will support and encourage participation in all association programs includingendorsed programs.

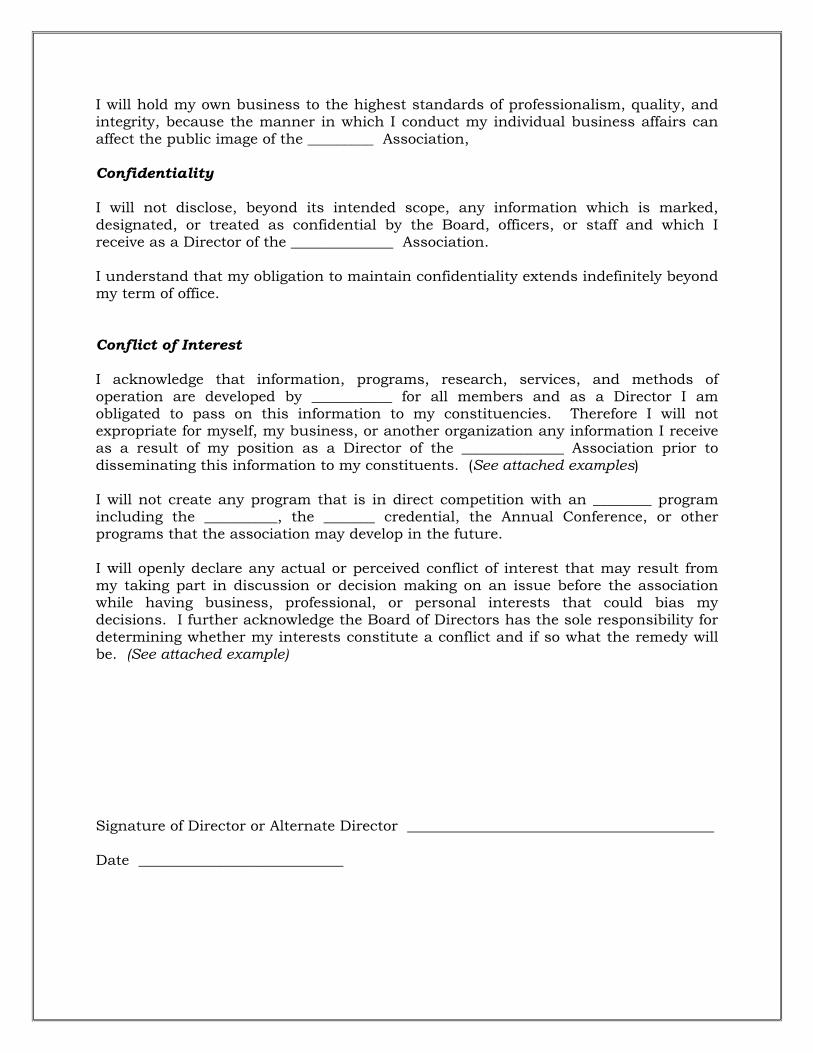

I will hold my own business to the highest standards of professionalism, quality, andintegrity, because the manner in which I conduct my individual business affairs canaffect the public image of the _________ Association,

Confidentiality

I will not disclose, beyond its intended scope, any information which is marked,designated, or treated as confidential by the Board, officers, or staff and which Ireceive as a Director of the ______________ Association. I understand that my obligation to maintain confidentiality extends indefinitely beyondmy term of office.

Conflict of Interest

I acknowledge that information, programs, research, services, and methods ofoperation are developed by ___________ for all members and as a Director I amobligated to pass on this information to my constituencies. Therefore I will notexpropriate for myself, my business, or another organization any information I receiveas a result of my position as a Director of the ______________ Association prior todisseminating this information to my constituents. (See attached examples)

I will not create any program that is in direct competition with an ________ programincluding the __________, the _______ credential, the Annual Conference, or otherprograms that the association may develop in the future.

I will openly declare any actual or perceived conflict of interest that may result frommy taking part in discussion or decision making on an issue before the associationwhile having business, professional, or personal interests that could bias mydecisions. I further acknowledge the Board of Directors has the sole responsibility fordetermining whether my interests constitute a conflict and if so what the remedy willbe. (See attached example)

Signature of Director or Alternate Director __________________________________________

Date ____________________________

Example of Duty of Care:

“I will be responsible for disseminating information I receive as a Director to all members withmy primary responsibility to inform my constituency, i.e., state association, national, orregional company, or at-large members.”

______ Director, John Doe, receives a notice on the _______ Board of Directors list serveabout a grant available to child care centers in all states. John fails to pass thisinformation on to his state association members.

• As the representative of the membership as a whole, John is obligated to pass onthis information to his constituency, and in the spirit of leadership, should makea reasonable effort to do so immediately in order to equalize the opportunityamong members, including himself.

Examples of Conflict of Interest:

“I acknowledge that information, programs, research, services, and methods of operation aredeveloped by ______ for all members and as a Director I am obligated to pass on thisinformation to my constituencies. Therefore I will not expropriate for myself, my business, oranother organization any information I receive as a result of my position as a Director of the_________ Association prior to disseminating this information to my constituents.”

1. In the example above, John not only does not pass on the information he receivesthrough the Board-only list serve, he applies for the grant for his own center.

• John is taking advantage of information available to him in his capacity asa member of the Board of Directors of ______ and using this information forhis personal gain.

2. _______ Board member John Doe conducts a training class for Field Counselorswhich is not the _________ prescribed training and/or charges a fee for thetraining.

• John Doe is taking advantage of his position as a Director to profit when hecharges a fee which is contrary to _____’s policy and interest. ____ providesthis training free of charge.

• John Doe is not using the prescribed training approved by _____ and thereforeis negatively impacting the integrity of the ____ program.

3. _______ Director Mary Doe uses association-developed programs, data, papers, orother intellectual property (correspondence, procedure manuals, methods ofoperation, curriculum, presentations) without permission of the associationand/or without citing the association as the creator or fails to reportunauthorized use by his/her state association or company.

• Even though the association material Mary uses may not be copyrighted, it isunethical to use the association’s property for one’s own benefit or tomisrepresent the origin of the material. If the material is copyrighted, Mary’sactions are also illegal.

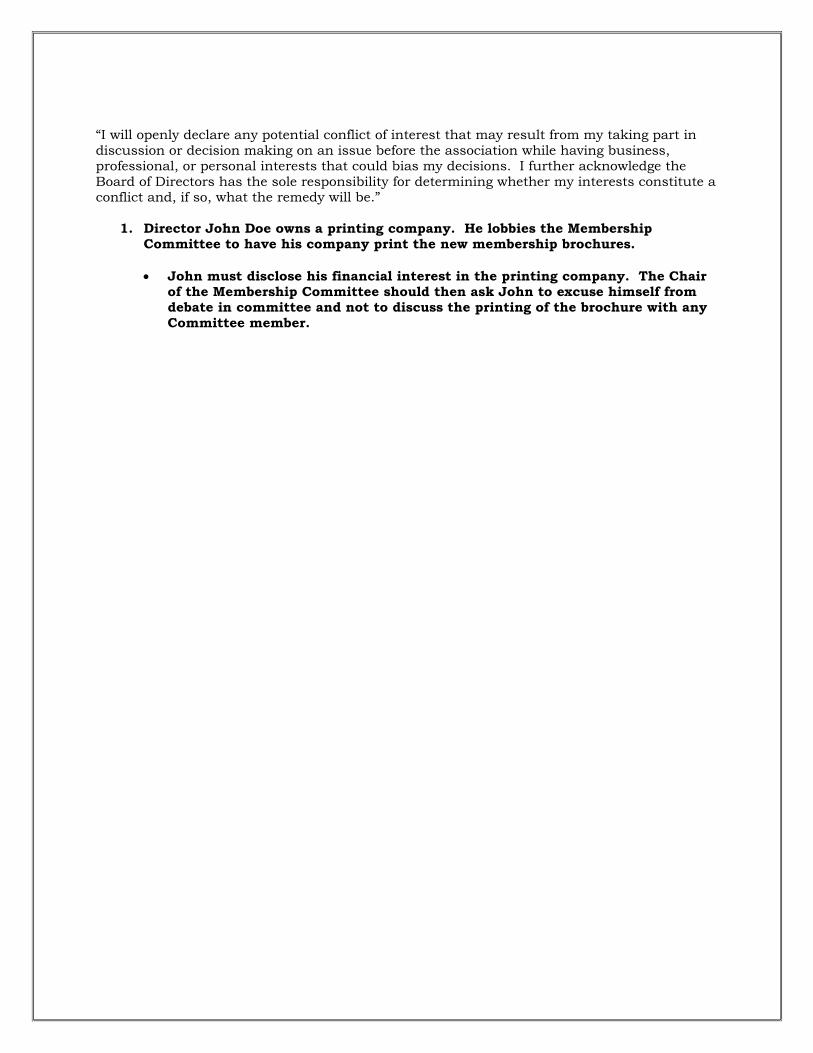

“I will openly declare any potential conflict of interest that may result from my taking part indiscussion or decision making on an issue before the association while having business,professional, or personal interests that could bias my decisions. I further acknowledge theBoard of Directors has the sole responsibility for determining whether my interests constitute aconflict and, if so, what the remedy will be.”

1. Director John Doe owns a printing company. He lobbies the MembershipCommittee to have his company print the new membership brochures.

• John must disclose his financial interest in the printing company. The Chairof the Membership Committee should then ask John to excuse himself fromdebate in committee and not to discuss the printing of the brochure with anyCommittee member.

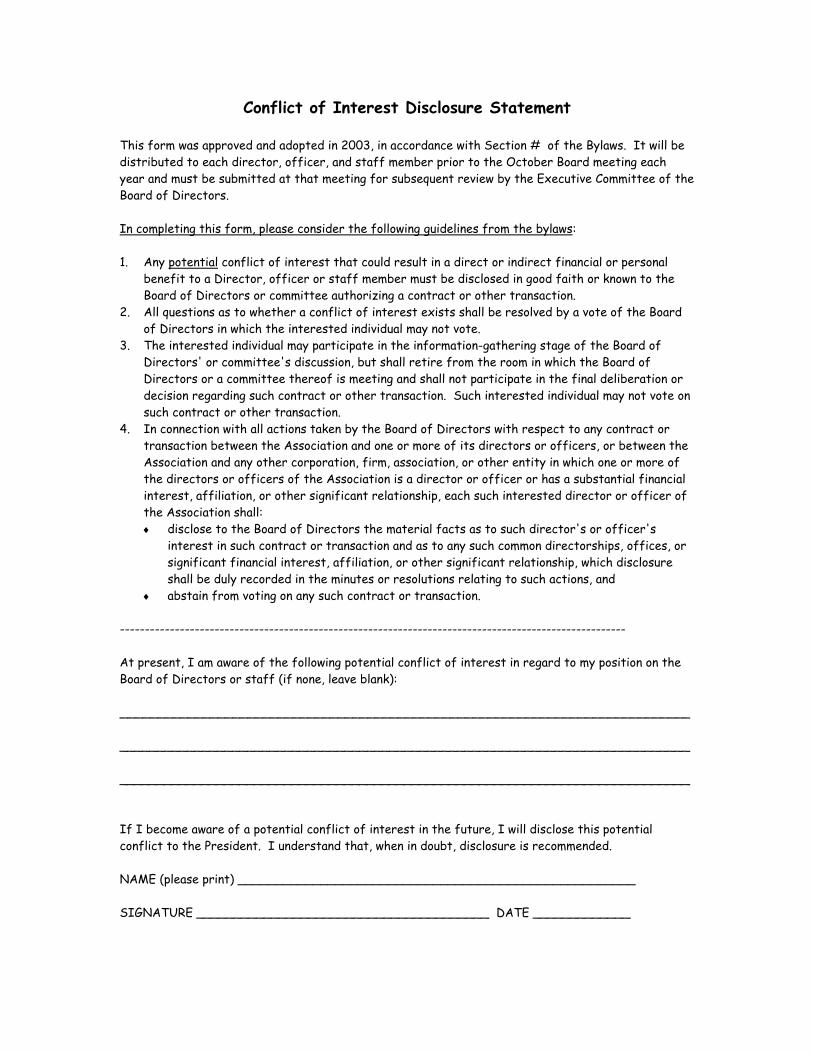

Conflict of Interest Disclosure Statement

This form was approved and adopted in 2003, in accordance with Section # of the Bylaws. It will bedistributed to each director, officer, and staff member prior to the October Board meeting eachyear and must be submitted at that meeting for subsequent review by the Executive Committee of theBoard of Directors.

In completing this form, please consider the following guidelines from the bylaws:

1. Any potential conflict of interest that could result in a direct or indirect financial or personalbenefit to a Director, officer or staff member must be disclosed in good faith or known to theBoard of Directors or committee authorizing a contract or other transaction.

2. All questions as to whether a conflict of interest exists shall be resolved by a vote of the Boardof Directors in which the interested individual may not vote.

3. The interested individual may participate in the information-gathering stage of the Board ofDirectors' or committee's discussion, but shall retire from the room in which the Board ofDirectors or a committee thereof is meeting and shall not participate in the final deliberation ordecision regarding such contract or other transaction. Such interested individual may not vote onsuch contract or other transaction.

4. In connection with all actions taken by the Board of Directors with respect to any contract ortransaction between the Association and one or more of its directors or officers, or between theAssociation and any other corporation, firm, association, or other entity in which one or more ofthe directors or officers of the Association is a director or officer or has a substantial financialinterest, affiliation, or other significant relationship, each such interested director or officer ofthe Association shall:♦ disclose to the Board of Directors the material facts as to such director's or officer's

interest in such contract or transaction and as to any such common directorships, offices, orsignificant financial interest, affiliation, or other significant relationship, which disclosureshall be duly recorded in the minutes or resolutions relating to such actions, and

♦ abstain from voting on any such contract or transaction.

------------------------------------------------------------------------------------------------------

At present, I am aware of the following potential conflict of interest in regard to my position on theBoard of Directors or staff (if none, leave blank):

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

If I become aware of a potential conflict of interest in the future, I will disclose this potentialconflict to the President. I understand that, when in doubt, disclosure is recommended.

NAME (please print) _____________________________________________________

SIGNATURE _______________________________________ DATE _____________

1

In response to an ASAE Listserv query in February 2008, associations contributedthe following examples. Be sure to rely on legal and accounting professionals fordevelopment of policies.

IRS References

General Definitions

One who reveals wrongdoing within an organization to the public or to those in positionsof authority: “The Pentagon's most famous whistleblower is . . . hoping to get anotherchance to search for government waste” (Washington Post).

The disclosure by a person, usually an employee, in a government agency or privateenterprise; to the public or to those in authority, of mismanagement, corruption, illegality,or some other wrongdoing.

2

#1 Whistleblower Protection Policy

Association prides itself on its adherence to federal, state, and local laws and/orregulations, including business ethics policies. As such, even though it is notobligated to do so, the Association has decided to voluntarily adopt awhistleblower protection policy. Pursuant to this policy, any employee whobecomes aware of any violation of federal, state, or local law or regulation,including any financial wrongdoing, should immediately report the violation to theExecutive Vice President to allow the organization to investigate and, if applicable,correct the situation or condition.

If the Executive Vice President is involved or is believed to be involved in thematter being reported, employees may, in the alternative, make a report to theAssociation’s legal counsel. The Association will conduct an investigation andtake appropriate action within a reasonable period of time. Such complaints willbe held in confidence to the extent the needs of the investigation permit.

“Financial wrongdoing” may include, but is not limited to:

• Questionable accounting practices;

• Fraud or deliberate error in financial statements or recordkeeping;

• Deficiencies of internal accounting controls;

• Misrepresentations to company officers or the accounting department

(including deviation from full reporting of financial conditions).

If any employee reports in good faith what the employee believes to be a violationof the law and/or financial wrongdoing to the Association, its legal counsel, or to afederal, state, or local agency or assists in an investigation concerning financialwrongdoing, it is the Association’s policy that there will be no retaliation takenagainst the employee.

Employees are reminded of the importance of keeping financial mattersconfidential. Employees with questions concerning the confidentiality orappropriateness of disclosure of particular information should contact theExecutive Vice President.

# # #

3

#2 Whistleblower Policy

Purpose

The Association is committed to high standards of ethical, moral and legal businessconduct. In line with this commitment and association’s commitment to opencommunication, this policy provides an avenue for employees to raise concerns. Italso provides reassurance that employees will be protected from reprisals orvictimization for whistleblowing. (For purposes of this policy, an employee isdefined as any individual who is paid for providing services to associationheadquarters and includes both full-time and part-time employees.)

This whistleblowing policy is intended to offer protections if an employees raisesconcerns regarding association, including concerns regarding:

• incorrect financial reporting;• unlawful activity;• activities that are not in line with association policy; or• any other activities that constitute serious improper conduct.

Safeguards

Harassment or Victimization - Harassment or victimization for reporting concernsunder this policy will not be tolerated.

Confidentiality - Every effort will be made to treat the complainant’s identity withappropriate regard for confidentiality.

Anonymous Allegations - This policy encourages employees to put their names toallegations because appropriate follow-up questions and investigation may not bepossible unless the source of the information is identified. Concerns expressedanonymously will be explored appropriately, but consideration will be given to:The seriousness of the issue raised;The credibility of the concern; andthe likelihood of confirming the allegation from attributable sources.

Bad Faith Allegations - Although the employee is not expected to prove the truthof an allegation, the employee should be able to demonstrate to the personcontacted that the report is being made in good faith. Allegations made in bad faithmay result in disciplinary action.

4

Procedure: 1. Process for Raising a Concern

Reporting- The whistleblowing procedure is intended to be used for serious andsensitive issues. Such concerns, including those relating to financial reporting,unethical or illegal conduct, may be reported directly to the association GeneralCounsel:

[Insert Contact Information Here]

Employment-related concerns should continue to be reported through your normalchannels such as to a supervisor or the CEO.

Timing - The earlier a concern is expressed, the easier it is to take action.

Procedure: 2. How the Report of Concern Will be Handled

The action taken by association in response to a report of concern under this policywill depend on the nature of the concern. The Audit Committee of the association’sExecutive Committee shall receive information on each report of concern andfollow-up information on actions taken.

Initial Inquiries - Initial inquiries will be made to determine whether aninvestigation is appropriate, and the form that it should take. Some concerns maybe resolved without the need for investigation.

Further Information -The amount of contact between the complainant and theperson or persons investigating the concern will depend on the nature of the issueand the clarity of information provided. Further information may be sought from orprovided to the person reporting the concern.

# # #

5

# 3 Reporting and Investigating Wrongdoing Policy

The Association has a responsibility for the stewardship of member and employeecontributions and resources. In fulfilling that responsibility, the Association iscommitted to compliance to all laws and regulations to which it is subject.

In addition to complying with the law, it is the policy of the association to promoteethical practices and ethical treatment of its members and employees. Whetherknown or suspected, instances of misuse of Association resources or otherimproper activities should be reported and appropriately investigated. Membersand employees have a responsibility to each other and to the organization tomaintain an environment in which problems are addressed immediately, and theyare therefore protected from retaliation for making such reports.

The association endorses and utilizes internal controls and operating proceduresintended to detect and prevent improper activities. If, however, those controls orprocedures fail to safeguard against irregularity, or if intentional or unintentionalviolation of laws or regulations occur, it is the policy of the association thatmembers and employees are encouraged to report those irregularities andviolations.

It is also the policy of association not to hide, destroy, alter or falsify documents toprevent their use in litigation or other official proceedings. Toward that end, theAssociation will have and regularly review a document retention policy. Officers,members, and employees of the association are expected to adhere to this policy.

Last, the association (through its Conflict of Interest Policy) has asked the Board ofDirectors to disclose any real, perceived, or potential conflicts of interest that relateto board duties or deliberations, and to recuse him/herself when the board makesdecisions affected by the conflict. Refusal to abide by the organization’s conflictof interest policy may result in removal from office and a referral to theAssociation’s Ethics Committee for review. Employees may not engage in anyactivity, paid or unpaid, that conflicts, or gives the appearance of conflicting withtheir obligations to association.

The provisions of this policy statement do not negate or minimize the effect orimport of the association’s Code of Ethics, Membership Standards and Sanctions,or the Employee Handbook. Individual complaints about the professional conductof members or of employees will be handled according to those governingdocuments.

# # #

Whistleblower Policy

PURPOSE OF THIS POLICY: A key defense against fraud occurring in an organization is the availability of a means for employees and other constituents to anonymously report suspected wrongdoing (whistleblowing). Respondents to a 2004 survey by the Association of Certified Fraud Examiners (ACFE) revealed that various forms of fraud are detected 40 percent of the time by tips, the leading method for detecting fraud.

While whistleblower programs are not required of not-for-profit organizations, CRS believes that it is a prudent practice to follow. In addition, some states have adopted whistleblower provisions, and federal law prohibits retaliation against anyone “blowing the whistle” with respect to a violation of a federal law or regulation. These would include:

� Forgery or alteration of documents

� Unauthorized alteration or manipulation of computer files

� Fraudulent financial reporting

� Pursuit of a benefit or advantage in violation with the CRS conflict of interest policy

� Misappropriation or misuse of CRS resources, such as funds, supplies, or other assets

� Authorizing or receiving compensation for goods not received or services not performed

� Authorizing or receiving compensation for hours not worked

CRS Whistleblower Policy General The CRS Code of Conduct (hereinafter referred to as the Code) requires directors, other volunteers, and employees to observe high standards of business and personal ethics in the conduct of their duties and responsibilities. Employees and representatives of the organization must practice honesty and integrity in fulfilling their responsibilities and comply with all applicable laws and regulations.

The objectives of the CRS Whistleblower Policy are to establish policies and procedures for:

• The submission of concerns regarding questionable accounting or auditing matters by employees, directors, officers, and other stakeholders of the organization, on a confidential and anonymous basis.

• The receipt, retention, and treatment of complaints received by the organization regarding accounting, internal controls, or auditing matters.

• The protection of directors, volunteers and employees reporting concerns from retaliatory actions.

Reporting Responsibility Each director, volunteer, and employee of CRS has an obligation to report in accordance with this Whistleblower Policy (a) questionable or improper accounting or auditing matters, and (b) violations and suspected violations of CRS’s Code (hereinafter collectively referred to as Concerns).

Authority of Executive Committee All reported Concerns will be forwarded to the Executive Committee in accordance with the procedures set forth herein. The Executive Committee shall be responsible for investigating, and making appropriate recommendations to the Board of Directors, with respect to all reported Concerns.

No Retaliation This Whistleblower Policy is intended to encourage and enable directors, volunteers, and employees to raise Concerns within the Organization for investigation and appropriate action. With this goal in mind, no director, volunteer, or employee who, in good faith, reports a Concern shall be subject to retaliation or, in the case of an employee, adverse employment consequences. Moreover, a volunteer or employee who retaliates against someone who has reported a Concern in good faith is subject to discipline up to and including dismissal from the volunteer position or termination of employment.

Reporting Concerns

Employees Employees should first discuss their Concern with their immediate supervisor. If, after speaking with his or her supervisor, the individual continues to have reasonable grounds to believe the Concern is valid, the individual should report the Concern to the Chief Executive Officer (CEO) or the Vice President of Operations (VPO). In addition, if the individual is uncomfortable speaking with his or her supervisor, or the supervisor is a subject of the Concern, the individual should report his or her Concern directly to the CEO or Vice President of Operations.

If the Concern was reported verbally to the CEO or VPO, the reporting individual, with assistance from the CEO or VPO, shall reduce the Concern to writing. The CEO or VPO is required to promptly report the Concern to the Chair of the Executive Committee, who has specific and exclusive responsibility to investigate all Concerns. If the CEO or VPO, for any reason, does not promptly forward the Concern to the Executive Committee, the reporting individual should directly report the Concern to the Chair of the Executive Committee. Contact information for the Chair of the Executive Committee may be obtained either through the Leadership Manual or by calling the CRS office. Concerns may be also be submitted

anonymously. Such anonymous Concerns should be in writing and sent directly to the Chair of the Executive Committee.

Directors and Other Volunteers Directors and other volunteers should submit Concerns in writing directly to the Chair of the Executive Committee. Contact information for the Chair of the Executive Committee may be obtained from the CEO.

Handling of Reported Violations The Executive Committee shall address all reported Concerns. The Chair of the Executive Committee shall immediately notify the Executive Committee, the CEO and the VPO of any such report. The Chair of the Executive Committee will notify the sender and acknowledge receipt of the Concern within five business days, if possible. It will not be possible to acknowledge receipt of anonymously submitted Concerns.

All reports will be promptly investigated by the Executive Committee, and appropriate corrective action will be recommended to the Board of Directors, if warranted by the investigation. In addition, action taken must include a conclusion and/or follow-up with the complainant for complete closure of the Concern.

The Executive Committee has the authority to retain outside legal counsel, accountants, private investigators, or any other resource deemed necessary to conduct a full and complete investigation of the allegations.

Acting in Good Faith Anyone reporting a Concern must act in good faith and have reasonable grounds for believing the information disclosed indicates an improper accounting or auditing practice, or a violation of the Codes. The act of making allegations that prove to be unsubstantiated, and that prove to have been made maliciously, recklessly, or with the foreknowledge that the allegations are false, will be viewed as a serious disciplinary offense and may result in discipline, up to and including dismissal from the volunteer position or termination of employment. Such conduct may also give rise to other actions, including civil lawsuits.

Confidentiality Reports of Concerns, and investigations pertaining thereto, shall be kept confidential to the extent possible, consistent with the need to conduct an adequate investigation.

Disclosure of reports of Concerns to individuals not involved in the investigation will be viewed as a serious disciplinary offense and may result indiscipline, up to and including termination of employment. Such conduct may also give rise to other actions, including civil lawsuits.

1

Definition: Onewho revealswrongdoing withinan organization tothe public or tothose in positionsof authority.

A key element ofSarbanes Oxley.

Whistleblower Policy - Sample

Introduction

[ORGANIZATION NAME] Code of Ethics and Conduct requires directors, officers andemployees to observe high standards of business and personal ethics in the conduct of theirduties and responsibilities. As employees and representatives of theOrganization, we must practice honesty and integrity in fulfilling ourresponsibilities and comply with all applicable laws and regulations.

Reporting Responsibility

It is the responsibility of all directors, officers and employees to complywith the Code and to report violations or suspected violations in accordancewith this Whistleblower Policy.

Retaliation

No director, officer or employee who in good faith reports a violation of the Code shall sufferharassment, retaliation or adverse employment consequence. An employee who retaliatesagainst someone who has reported a violation in good faith is subject to discipline up to andincluding termination of employment. This Whistleblower Policy is intended to encourage andenable employees and others to raise serious concerns within the Organization prior to seekingresolution outside the Organization.

Reporting Violations

The Code addresses the Organization’s open door policy and suggests that employees share theirquestions, concerns, suggestions or complaints with someone who can address them properly. Inmost cases, an employee’s supervisor is in the best position to address an area of concern.However, if you are not comfortable speaking with your supervisor or you are not satisfied withyour supervisor’s response, you are encouraged to speak with someone in the Human ResourcesDepartment or anyone in management whom you are comfortable in approaching. Supervisorsand managers are required to report suspected violations of the Code of Conduct to theOrganization’s Compliance Officer, who has specific and exclusive responsibility to investigateall reported violations. For suspected fraud, or when you are not satisfied or uncomfortable withfollowing the Organization’s open door policy, individuals should contact the Organization’sCompliance Officer directly.

2

Compliance Officer1

The Organization’s Compliance Officer is responsible for investigating and resolving allreported complaints and allegations concerning violations of the Code and, at his discretion, shalladvise the Executive Director and/or the audit committee. The Compliance Officer has directaccess to the audit committee of the board of directors and is required to report to the auditcommittee at least annually on compliance activity. The Organization’s Compliance Officer isthe chair of the audit committee.

Accounting and Auditing Matters

The audit committee of the board of directors shall address all reported concerns or complaintsregarding corporate accounting practices, internal controls or auditing. The Compliance Officershall immediately notify the audit committee of any such complaint and work with thecommittee until the matter is resolved.

Acting in Good Faith

Anyone filing a complaint concerning a violation or suspected violation of the Code must beacting in good faith and have reasonable grounds for believing the information disclosedindicates a violation of the Code. Any allegations that prove not to be substantiated and whichprove to have been made maliciously or knowingly to be false will be viewed as a seriousdisciplinary offense.

Confidentiality

Violations or suspected violations may be submitted on a confidential basis by the complainantor may be submitted anonymously. Reports of violations or suspected violations will be keptconfidential to the extent possible, consistent with the need to conduct an adequate investigation.

Handling of Reported Violations

The Compliance Officer will notify the sender and acknowledge receipt of the reported violationor suspected violation within five business days. All reports will be promptly investigated andappropriate corrective action will be taken if warranted by the investigation.

This sample may used for non-commercial use by nonprofit organizations with the followingattribution: Copyright 2004, National Council of Nonprofit Associations, www.ncna.org.

Whistleblower Sample NCNA 11-07.doc

1 Note: Compliance officer could be a committee of the board, a designated director, or a third party such as an HRSpecialist or the board attorney (rch.)

Audit Committee

Audit CommitteeMembers of a board of directors who are responsible for dealing with the external and internalauditors.

AuditThe result of an independent accountant’s review of the statements and footnotes to ensurecompliance with generally accepted accounting principles (GAAP) and to render an opinion onthe fairness of the financial statements.

Audit ReportA report issued by an independent CPA that expresses an opinion about whether the financialstatements present fairly a company’s financial position, operating results, and cash flows inaccordance with generally accepted accounting principles (GAAP).

ReviewPerforming inquiry and analytical procedures that provide the accountant with a reasonable basisfor expressing limited assurance that there are no material modifications that should be made tothe financial statements in order for them to be in conformity with generally accepted accountingprinciples (GAAP)

CompilationInformation resented in the form of financial statement information that is the representation ofmanagement without undertaking to express any assurance on the statements. It is a cursoryreview of an organization’s financial operations.

Audit Committee.doc

Serving on the audit committee of a not-for-profit organization is an important undertaking. Recent scrutiny offinancial responsibility in both the not-for-profit and for-profit...

Audit committeehandbook for not-for-profitorganizations

...sectors has brought the role of the audit committeeinto the public eye. Grant Thornton LLP has created thisaudit committee handbook to provide an overview ofwhat you can expect in your role and what will, in turn,be expected of you by the various stakeholders of theorganization.

Your organization’s most valuable asset is its reputationand good name. As an audit committee member, yourfundamental task is to help the board of directorsassure the integrity and credibility of the organization’sfinancial statements and financial management. Thattask can be rewarding, yet challenging.

This handbook outlines the organization, functions andduties of an audit committee. It also covers some ofthe tax concerns affecting not-for-profit organizations,including intermediate sanctions, private inurement andunrelated business income tax.

If you have further questions or require more detailedinformation than this booklet provides, please contactGrant Thornton LLP’s not-for-profit professionals for theanswers you’re looking for.

2 Accountability and independence

3 The audit committee’s missionComposition of the audit committeeMember liability

6 The inside perspective: Working within a not-for-profit organizationThe audit committee and the boardThe audit committee and managementWorking with internal auditors

8 A vigilant team: Working with your external auditorsThe pre-audit meetingThe post-audit meetingEvaluating your external auditorsAudit and compliance committee

13 Special financial, tax and regulatory concerns for not-for-profit organizationsTax-exempt statusPrivate inurementIntermediate sanctionsUnrelated business income taxIssues related to donationsThe importance of staff

19 A healthy skepticism

20 Appendices

28 About Grant Thornton

The contents of this guide are intended for information purposes only and should not be construed as legal oraccounting advice or opinion on any specific facts or circumstances. You should not rely on the contents of thisguide as a substitute for obtaining legal or other professional counsel. This content is not intended to create, andreceipt of it by you does not constitute, an attorney-client, accountant-client, or any other relationship. You areurged to consult with an attorney or an accountant regarding your own situation and any specific questions youmay have.

Table of contents 1

The guiding principles of the auditcommittee can be summed up in twowords: accountability and independence.

A not-for-profit organization isaccountable to its various stakeholdersfor the use of funds received either asfees, donations, grants, or exchangecontracts. These include the donors ofthe funds and the people who use theresources of the organization.

In addition, the organization’s tax-exempt status carries with it a muchbroader responsibility to society at large.Tax-exempt status is, in part, recognitionof the societal value of the services anot-for-profit organization performs. Itis also a method by which all taxpayersunderwrite these services. In effect,every taxpayer is a stakeholder in yourorganization.

The primary role of the auditcommittee is to instill confidence thatthe funds of the organization are used ina manner consistent with good financialpractice. This includes making certainthat funds are used only for thepurposes for which they were intendedand in ways that do not violate theprinciples that resulted in tax-exemptstatus.

IndependenceThe audit committee is charged withprotecting not only financial assets, butalso the organization’s most importantasset: its good name and reputation.

To maintain this independence, theaudit committee is charged withensuring that:

• The audit committee itself isindependent of the organization’smanagement and its external auditor,focusing solely on representing theboard’s responsibility to protect themission and best interests of theorganization.

• The organization’s internal auditor isindependent from management andthat the auditor’s opinion is basedonly on its independent professionaljudgment.

• The organization’s board membersand management are independentfrom vendors to the board or, if notindependent, that the relationships arefully disclosed.

2 Accountability and independence

3

A not-for-profit organization’s auditcommittee has three main missions.

First, it represents the board ofdirectors in overseeing the establishmentand implementation of appropriateaccounting policies and internal controlsso that financial reporting is accurateand reliable and fraud is avoided.Therefore, the audit committee needs towork diligently to ensure properstewardship over the organization’sassets and to protect the organization’sreputation through fiscal transparency.

Second, the audit committee assessesthe business risks for the organizationand determines whether it is planningadequately for those risks. To do this,the committee should review theorganization’s overall risk managementprofile, including investment practices,adherence to tax regulations, disasterrecovery plans, compliance withdonor/grantor requirements, statecharitable registration and unclaimedproperty reporting, and adequateinsurance coverage.

Third, the audit committee monitorsthe roles of the board, management andinternal and external auditors to ensurethat the organization follows goodfinancial governance practices.

The exact responsibilities assigned tothe audit committee to fulfill thesemissions will vary from organization toorganization, depending on the not-for-profit’s size and the nature of itsactivities.

The tasks most commonly assigned toan audit committee include:

• Recommending to the board, orappointing directly, an independentaudit firm.

• Ensuring the appropriateness offinancial statement presentation andthe adequacy of footnote disclosures.

• Ensuring clear communication offinancial information usingappropriate communicationmethodology.

• Reviewing the scope and plan for theindependent audit.

• Receiving and acting upon the resultsof the audit with the external auditors,including reporting the results to thefull board.

• Providing oversight of the internalcontrol structure.

• Approving the annual internal auditplan and review the resulting reportsprepared by the internal auditor.

• Reviewing or approving thecontracting for any non-audit servicesprovided by the external auditors.

• Resolving disagreements betweenauditors and management.

• Reviewing the Form 990 that is filedwith the Internal Revenue Service(IRS).Audit committee members should

meet with the organization’s auditors atleast twice a year — once to discuss theauditor’s workplan and once to reviewtheir findings before they are presentedto the board. In most cases, however,audit committee members’ duties aremore involved.

In larger not-for-profit organizationsthat have an internal audit department,

The audit committee’s mission

the audit committee approves thedepartment’s workplan, receives itsreports and oversees the department’sstaffing and performance. In some cases,the internal audit department reportsadministratively to the chief financialofficer, but its workplan and reportsshould be approved and received by theaudit committee. The internal auditdirector should have confidential accessto the audit committee chair.Additionally, the committee shouldevaluate the performance of the internalaudit director.

The committee should make sure theinternal audit and external audit plans aare thorough and complement eachother.

As part of its duties, the auditcommittee should be charged withmonitoring specific policies thatrepresent best practices, such as:• A code of ethics for the organization,

including the board;• A conflict-of-interest policy for the

organization, including the board (thecode-of-ethics and the conflict-of-interest policy can also beincorporated into one policy);

• A whistle-blower policy throughwhich stakeholders, includingemployees, can raise concerns withoutfear of retaliation; and

• A records-retention policy so thatcritical documents are preserved for acertain period of time.

Some organizations incorporate auditcommittee functions into their financecommittees. The trend, however, is

toward the establishment of separateaudit committees with standingcommittee status. The role of an auditcommittee is quite different than theroles usually assigned to a financecommittee.

A finance committee’s principal task isthe approval and monitoring of thebudget, which requires individuals whounderstand the programmatic structureand mission of the organization. Anaudit committee, however, puts thefocus on understanding the fundamentalprinciples of accountability, financialreporting and internal controls and itsmembers are likely to view theorganization more critically.

If your audit committee is new,consider working with the board todraft an audit committee charter thatspells out, in writing, the committee’sexact responsibilities. (For an example ofan audit committee charter, seeAppendix I.)

Composition of the audit committeeThe audit committee generally should becomposed of three to five membersdrawn from the board of directors. Allaudit committee members should beindependent of organizationmanagement: i.e., they should not haveaccepted, directly or indirectly, anysalary or compensatory fees from theorganization.

Most or all of the audit committeemembers should have a solid groundingin business and finance and a goodunderstanding of internal control issues.

4

5

They should be financially literate: i.e.,be able to read and interpret a financialstatement and be conversant in basicfinancial terminology.

One or more of the members shouldbe a financial expert with a professionalknowledge of financial reporting(including generally accepted accountingprinciples or GAAP), business riskassessment and internal controlpractices. Ideally, there should also beindividuals on the committee withspecific knowledge of not-for-profitaccounting and business issues.

Of course, the supply of individualswith such backgrounds will varyconsiderably from one organization tothe next. If your organization does nothave board members with a financialbackground, you should actively recruitsuch individuals, including bankers,accountants and other financialprofessionals to fill this need.

The number of finance committeemembers serving on the audit committeeshould be limited. The audit committeemonitors the business operations of theorganization creating a conflict-of-interest for finance committee membersserving on the audit committee.

It is very important for auditcommittee members to have a healthyskepticism about what they are told andabout how the organization operates.The audit committee should askmanagement difficult questions about itspractices and policies and pursue issuesuntil it is satisfied with the answers.

Individuals who are uncomfortable

asking difficult questions or coming tocritical conclusions can’t serveeffectively on an audit committee.

The final characteristic an auditcommittee member must possess is awillingness to commit the time andeffort necessary to do the job.

Depending on your organization’ssize and structure, this time commitmentmay be substantial.

Member liabilityBoard members of not-for-profitorganizations face potential personallegal liabilities, so the question ofwhether serving on an audit committeeentails any further legal risk is alegitimate one.

Since many of the events that couldresult in liability for the board as awhole stem from failures in internalcontrols, the audit committee is partlyresponsible for protecting itself — andthe rest of the board — from suchliability.

Before considering any boardposition, you may wish to investigatewhether your organization carriesadequate directors and officers’ (D&O)insurance coverage. D&O insurancecoverage protects boards againstallegations of wrongdoing.

When reviewing the D&O policy, besure it covers legal costs, which will beincurred regardless of the outcome of alawsuit. You may also wish to consultwith legal counsel regarding the specificlaws in your state concerning yourexposure.

An effective audit committee must workwith a variety of groups within anorganization.

Specifically, the audit committeeworks with the board as a whole, withthe organization’s management team,and, if one exists, with the internal auditdepartment. Understanding the audit committee’s role in each of these relationships is essential.

The audit committee and the board The audit committee represents theboard of directors in fulfilling some ofthe board’s responsibilities for financialoversight of the organization.

Although a share of the auditcommittee may be made up of boardmembers, not all audit committeemembers need be board members.Including board members provides theexpertise needed, while non-boardmembers provide an independentperspective.

The committee should report at leasttwice a year to the board on 1) results ofexternal and internal audits and anyissues that arose in those audits thatmerit the board’s attention, 2) issues offinancial accountability and business riskthat the organization faces, 3) anyinternal control or procedural issues, 4) new systems and controls evaluatedand put in place, and 5) regulatoryissues.

The audit committee and managementManagement is responsible for creatingand maintaining internal controls andthe audit committee is responsible forseeing that those controls are adequateand implemented. While the committeewill work collaboratively with theexternal auditors, internal auditors — ifany — and management, the committeeis independent of each of these groupsand must come to its own conclusions.

As part of the audit process, theexternal auditors will consider theorganization’s internal controls. Theiraudit findings should include a list ofcontrol issues they believe needaddressing and suggestions forimproving them. If you have internalauditors, they, too, will test and reporton internal control issues.

The audit committee should discussthese control issues with managementand review management’s plans forfixing them. In some cases, managementmay recommend against implementingan auditor’s suggestions on a cost-benefit basis, or they may recommendan alternative solution.

The audit committee should considerthese suggestions, discuss them with theauditors, if necessary, and bring anyunresolved material disputes to theboard’s attention.

The audit committee can also providemanagement with a valuable, objective

6 The inside perspective: Working within a not-for-profit organization

sounding board for any issues dealing with internal controls or the publictrust. By giving management anopportunity to discuss sensitivematters up front, the audit committeecan help head off potential problemsbefore they arise.

Working with internal auditorsToday, audit committees are expectingmore from their internal auditfunctions. If your not-for-profitorganization has an internal auditfunction, the audit committee shouldwork with it in much the same waythat it works with your externalauditors.

The committee should review andapprove the internal audit work plan,including the areas within theorganization targeted for detailedexamination. The audit committeeshould receive and review the group’sfindings and discuss any control issuesthat have arisen.

Audit committees are also lookingto internal auditors to monitor thestatus of various findings andrecommendations to ensureappropriate corrective action plans areimplemented.

Some internal auditors aredeveloping more elaborate systems toidentify findings as materialweaknesses, significant deficiencies orreportable conditions.

Internal auditors may requireperiodic reports to be issued by theauditee on the status of the correctiveaction plan, require the auditee topresent their responses to the auditcommittee or require a re-audit after acertain period of time.

7

The audit committee will spend much ofits time dealing with your organization’sexternal auditors, who have beenappointed by the committee (or theboard itself) to assist in assessing theorganization’s financial condition andfinancial oversight.

The pre-audit meetingOne of the audit committee’s mostimportant jobs is working with yourauditors to ensure an effective auditeffort.

Prior to the audit, the audit committeeshould meet with the external auditorsto review their work plans. An auditor’swork plan spells out its strategy forconducting the audit. It will identifythose areas that the auditor has targetedfor the greatest scrutiny, indicate staffinglevels and set a schedule for the audit.

The audit committee should reviewthe work plan with the auditors in lightof the committee’s own concernsregarding business risks, internalcontrols and other issues. If the auditcommittee has concerns about a specificfinancial area, the auditor’s work planshould include that area.

If the plan does not include the area,the committee must decide whether toadd it, or substitute it, for another area.It must then determine the cost of anyadditional work it requests, and whetherthere are steps the organization can taketo help control the cost of the audit.

The pre-audit meeting is also thevenue for the auditors to solicit input

from the committee on areas of financialstatement and internal control risk,including the risk of fraud.

The audit committee should alsodiscuss with the auditors any internalcontrol or other issues raised by theprior year’s audit. The committee shouldinform the auditor of the steps, if any,management has taken to resolve thoseissues, and should seek the auditor’sopinion of those solutions.

The post-audit meetingAs its name would imply, the post-auditmeeting is held after the auditorscomplete their fieldwork. At thismeeting, the audit committee willdiscuss many items with the auditors.

The auditors will present audit results,including draft reports, supplementalfinancial information and related auditorreports for review and discussion by thecommittee. In addition, the auditors’professional standards require that theycommunicate certain matters to thecommittee.

Statement of Auditing Standards(SAS) No. 60, “Communications ofInternal Control Structure MattersNoted in an Audit,” requires auditors toreport to the audit committee mattersthat “… in the auditors’ judgment…represent reportable conditions in thedesign or operations of the internalcontrol structure, which wouldadversely affect the organization’s abilityto record, process, summarize, andreport financial data consistent with the

8 A vigilant team: Working with your externalauditors

9

assertions of management in thefinancial statements.”

These are referred to as a “reportableconditions” and are normally includedin the management advisory commentletter with the auditors’ otherrecommendations to management.

SAS No. 61, “Communications withAudit Committees,” mandates that theauditor discuss the following issues:

• The auditors’ responsibility underGAAPThe auditors must communicate theirlevel of responsibility for matters suchas review of, and reports related to,the internal control structure andwhether the financial statements arefree of material misstatement.Auditors also must make sure that thecommittee understands thefundamental concepts of an audit.Specifically, they should make it clearto the committee that an audit isdesigned to deliver reasonable, notabsolute, assurance that the financialstatements are presented fairly and inaccordance with GAAP.

• Significant accounting policiesThe auditors should inform the auditcommittee about selection of, changesin or application of significantaccounting principles and financialreporting practices and policies.Discussions should include the effectof these practices and policies incontroversial or emerging areas andany likely future changes.

• Judgments of management andaccounting estimatesAccounting estimates are an integralpart of financial statements. They canbe particularly sensitive because of thepossibility that future amounts maydiffer significantly from thoseestimates. The auditors should educatethe audit committee on the processthat management employed toformulate sensitive accountingestimates and on the basis for theauditors’ conclusions regarding thereasonableness of those estimates. Theallowance for uncollectible accountsreceivable is an example of asignificant estimate.

• Significant audit adjustmentsThe audit committee should beinformed of all significant adjustmentsmade as a result of the audit that maynot have been otherwise detected bymanagement. Management should alsoprovide the audit committee with alisting of proposed audit adjustmentsthat were not recorded because theamounts involved were not consideredmaterial to the financial statements,either on an individual basis or in theaggregate.

• Responsibility for other information indocuments containing auditedfinancial statementsThe auditors should discuss theirresponsibility and involvement withinformation in other documentscontaining audited financial

statements, such as published annualreports.

• Disagreements with managementThe auditors should discuss anydisagreements with managementabout matters related to accountingprinciples, financial reportingpractices and policies, and auditingmatters that could be significant tothe financial statements or theauditors’ report. Thesedisagreements might includeapplication of accounting principles,judgments about accountingestimates, the scope of the audit, orthe wording of the auditors’ report.

• Consultation with other accountantsIf the auditors are aware thatmanagement has consulted withother auditors about auditing,accounting or financial reportingmatters, the views of those auditorsshould be discussed with the auditcommittee.

• Major issues discussed withmanagement prior to retentionThe auditors and the auditcommittee should review any majormanagement issues raised when theauditors were retained, includingdiscussions about accountingprinciples, financial reportingpractices and policies, and auditingstandards and procedures.

• Difficulties encountered inperforming the auditThe auditors should inform the auditcommittee of serious difficulties indealing with management whileperforming the audit, such as failureto provide necessary information,unreasonable delays, unavailabilityof client personnel, or failure ofclient personnel to completerequested schedules on a timelybasis.

In addition to these topics, the auditcommittee may also want to discussthe following areas with the auditors:

• Assessment of the audit comparedwith anticipated results.

• Any need to expand auditprocedures and the reasons for doing so.

• Changes in report format or notedisclosures from the previous yearand the reasons for these changes.

• Evaluation of personnel involved inpreparing and controlling thefinancial information.

• Non-audit services provided to theorganization by the external auditorsfor the prior year and related fees.

• The report of the audit committee

10

11

that the audit committee chairpersonwill present to the governing boardof directors.

Generally, during the post-auditmeeting, the audit committee will meetin separate executive sessions with theexternal auditors, the internal auditorsand with financial management.

If an executive session deals withissues including compliance or whistle-blower situations, the audit committeemay consider having its own legalcounsel present.

Evaluating your external auditorsPart of the audit committee’sresponsibility is to evaluate thequalities of your external auditors. Theaudit committee should consider manyfactors when evaluating the auditors,including:

• Industry expertise — The not-for-profit sector has a variety of specificaccounting requirements that anauditor should know intimately.Strong experience in the not-for-profit sector is a desirablecharacteristic in your auditor.

• Tax capabilities — You should lookfor a firm with a strong tax specialtyin the not-for-profit area. Not-for-profit organizations have many taxissues and, because an organization’stax-exempt status is critical, it is vital

that the firm understand relevant taxissues.

• Manpower and location—Does youraudit firm have sufficient staff to dothe job? Insufficient staff can lead todelays or poor performance. Whereis its staff located? If your audit willbe staffed from out of town, travelexpenses may add to your bill.

• Depth of expert resources—The firmshould have the depth of expertise toprovide its own staff and yourorganization with information andexperience that provides criticalbusiness advice to improve yourorganization’s operations.

• Price—While price should not bethe sole determining factor in yourauditor choice, it is certainly aconsideration. Be sure to evaluateboth what the auditors propose todo for their fee and their ability toserve the special needs of yourorganization.

• Use of technology—Informationtechnology plays an important rolein the accounting profession. Yourauditors will have to work withelectronic data from your systems.An ability to use technology allowsthe auditor to work more effectivelyand efficiently with less disruptionof your staff.

• Chemistry — The audit committee,management and people throughoutyour organization will all have towork closely with your auditors.The personal chemistry between keypersonnel in your organization andthe partners, managers and staff ofyour auditors is very important.

A not-for-profit organization mayput its audit work out for proposal fora variety of reasons, some having to dowith the auditor, some having to dowith the organization itself, and somehaving to do with a policy ofperiodically re-bidding all procurementarrangements.

If it becomes necessary to solicitproposals, the audit committee, usuallywith management’s assistance, shouldprepare or approve a list of potentialaccounting firms and a request forproposal (RFP). The RFP spells outthe scope of services your organizationrequires, as well as specific questionsthat management would like proposingfirms to answer.

The management team, or the auditcommittee itself, usually reviews theproposals and identifies a short list ofcandidates for oral presentations. Theaudit committee, often in conjunctionwith management, conducts the oralinterviews and then presents itsselection to the board for approval.

Audit and compliance committeeMany not-for-profit organizations arestudying the possibility of enhancingthe responsibility of the auditcommittee by adding complianceoversight responsibilities. To cover thescope of its duties, some organizationshave changed the name of the auditcommittee to audit and compliancecommittee.

Compliance would entail a reviewand monitoring of legal and regulatoryissues, which are are presently beyondthe responsibility of most auditcommittees.

12

13

While audit committee members shouldhave a solid grounding in finance beforebeing appointed, they also need a basicunderstanding of the specific financialmanagement issues that face not-for-profit organizations.

Six issues audit committee membersshould consider as they address theirorganization’s controls and financialreports are tax-exempt status, privateinurement, intermediate sanctions,unrelated business income tax, issuesrelated to donations, and the importanceof staff.

Tax-exempt statusThe Internal Revenue Code (IRC)provides more than 20 categories of tax-exempt status; however, most not-for-profit organizations derive their tax-exempt status from one of the followingfive sections of the IRC:• Section 501(c)(3)—Religious,charitable, educational, and scientificorganizations; • Section 501(c)(4)—Social welfareorganizations and civic clubs; • Section 501(c)(5)—Labor unions andagricultural organizations; • Section 501(c)(6)—Trade andprofessional associations; and • Section 501(c)(7)—Social clubs.

One of the greatest responsibilities foraudit committee members — and,indeed, for all board members — is toensure that the organization is incompliance with tax laws and does notendanger its tax-exempt status.

Losing tax-exempt status coulddevastate your organization throughresulting large income tax liabilities,excise taxes (some of which may beimposed on officers and directorspersonally), denied tax deductions foryour contributors, loss of governmentgrants, ineligibility for reduced postagerates, and loss of various state taxexemptions.

The category of your tax-exemptstatus generally determines the primarythrust of your activities. For example,organizations exempt under 501(c)(3)and 501(c)(4) usually have an outwardfocus and provide some type of publicgood.

Organizations exempt under 501(c)(5)or 501(c)(7) are generally inwardlyfocused and act for the benefit of theirmembers, while 501(c)(6) organizationsmust maintain or improve businessconditions for an industry as a whole, asopposed to providing specific servicesfor members.

The category of your tax-exemptstatus also determines, in part, whatactivities would threaten its tax-exemptstatus.

Intervention in political campaignactivities can cause problems for mostnot-for-profit organizations. Specifically,Section 501(c)(3) organizations arestrictly prohibited from intervening inpartisan political campaigns to elect,defeat or appoint persons to publicoffice.

Special financial, tax and regulatory concernsfor not-for-profit organizations

Violation of the rules may result inloss of tax-exempt status, and theimposition of income taxes and excisetaxes on the organization and thosepersons (in their personal capacity) whoviolated the rules. Other not-for-profitorganizations may incur a substantial taxon any money spent for politicalpurposes.

The category of your tax-exemptstatus also determines the extent towhich your organization is allowed tolobby. While lobbying may be a keyactivity for a trade association or socialwelfare organization, no substantial partof a charitable organization’s activitiesmay constitute lobbying.

Not-for-profit organizations thatlobby may be subject to lobbying taxes.You should ensure that management hasadequately addressed the applicablelobbying rules.

Tax-exempt status normally requiresthe filing of IRS Form 990, which is apublic document. That means you mustprovide a copy in a timely manner toanyone who requests it. Consequently,the audit committee should realize thatany interested party (e.g., yourcompetitors, the news media, youremployees, your members, or yourdonors) may review the organization’sfinancial activities.

Public disclosure demands that youfocus on the information contained inForm 990 and anticipate questions fromthe public. You should carefullyconsider how you will address the

questions that may result when thepublic at large views your organization’sForm 990.

Private inurementSome transactions may result in the lossof tax-exempt status for any not-for-profit organization. One of the greatestdangers, both to your organization’s tax-exempt status and to its public image, isprivate inurement.

Private inurement may result whenthe organization’s assets or earnings areused for the benefit of an insider ratherthan for the good of the organizationitself or its stakeholders.

Insiders are generally directors,officers and certain key employees, aswell as their families or businesses.Embezzlement or theft are obviouscases, but there are other more commonexamples.

For instance, compensation paid toemployees that is disproportionatelyhigh compared with their duties couldbe considered private inurement.Excessive travel or entertainmentexpenses could also constitute privateinurement. Procuring merchandise orservices from vendors who are relativesor friends of insiders at higher thanmarket rates or for other inappropriatereasons can also constitute privateinurement.

You should closely scrutinize alltransactions with insiders because of theinherent conflict of interest that exists.Not-for-profit organizations are alsoprohibited from distributing theirearnings to their members.

14

15

Another major consequence of privateinurement is severe damage to theorganization’s reputation. Therefore, theaudit committee and your organizationas a whole should set and follow verystrict standards concerningcompensation and benefits; travel,entertainment and other expenses; andany financial dealings between theorganization and any parties related tostaff, management or the board.

In addition, under the excess benefitrules, called “intermediate sanctions,”improper dealing with insiders can alsoresult in severe financial penalties in theform of excise taxes imposed directly onthose insiders in their personal capacitywho took unfair advantage of a 501(c)(3)or 501(c)(4) organization and on thosemanagers who knowingly approved thetransactions. These provisions arediscussed in more detail in the nextsection.

Intermediate sanctionsThe intermediate sanctions apply toorganizations exempt from tax under501(c)(3) and 501(c)(4) and provideanother strong reason to guard againstprivate inurement.

Where the IRS previously only hadthe option of revoking a not-for-profitorganization’s tax-exempt status as apenalty for private inurement, it cannow force “disqualified persons”(generally directors, officers, keyemployees, or others with substantialinfluence over the organization’s affairs)

benefiting from inappropriatetransactions to pay an excise tax of 25 percent of the excess benefit received.

Those persons must also undo theinappropriate transaction by returningthe excess benefit, including interest, tothe organization or face an additionalexcise tax of 200 percent of the improperbenefit.

In short, they have to at least pay a 25 percent excise tax on the improperbenefit and then return the money theyare taxed on — a stiff penalty, indeed.

Any officer, director, trustee, orsimilarly empowered person within theorganization who knowingly andwillfully approves the transaction alsofaces an excise tax of 10 percent of theexcess benefit — up to a limit of $10,000per transaction.

A transaction is covered if the benefitprovided to the insider exceeds the valueof the consideration the organizationreceives. This consideration can consistof services provided in exchange forcompensation.

Typical transactions covered includeunreasonable salaries and benefits;selling goods, property, or services tothe organization for more than they areworth, or paying less than fair marketvalue for the organization’s assets.

Persons who have a substantialinfluence over the organization’s affairsare covered by the law. Thisdetermination is based on facts andcircumstances and generally will includemembers of the governing body (the

board), the chief executive officer, chiefoperating officer, and chief financialofficer.

Audit committee members aredisqualified persons if they are membersof the board.

Once someone is covered by thisdefinition, that person, his or her familymembers and any business in whichthey own a 35 percent interest is alsoincluded. Even when persons resignfrom the organization, they retainclassification as a disqualified person forfive years.

As an audit committee member, youshould ensure the organization hasprocedures in place to prevent conflictsof interest and excessive payments todisqualified persons.

All transactions involving insidersshould be approved by the board ofdirectors or a committee that has noconflicts of interest with the personwhose transaction is underconsideration. You should also makesure that all compensation and benefits,including those provided to you as aboard member or officer, are properlydisclosed on Form 990 and, if taxable,reported on Form 1099 or Form W-2 asappropriate.

Failure to properly document andreport compensation and benefits islikely to result in violations of theserules.

The intermediate sanctions violationsalso carry a heavy public relations cost.