before doing comparative research with sem … prof. jarosław górniak institute of sociology...

Post on 21-Dec-2015

213 views

TRANSCRIPT

Before doing comparative research with SEM …

Prof. Jarosław Górniak

Institute of Sociology

Jagiellonian University

Krakow

What is worth to consider

Think about your theory Check your data Explore your data Build your model carefully Think about survey error:

Systematic => Are the country samples representative? Is the non-response properly addressed?

Sampling variance => Is it computed properly? Consequently: are our model tests properly computed?

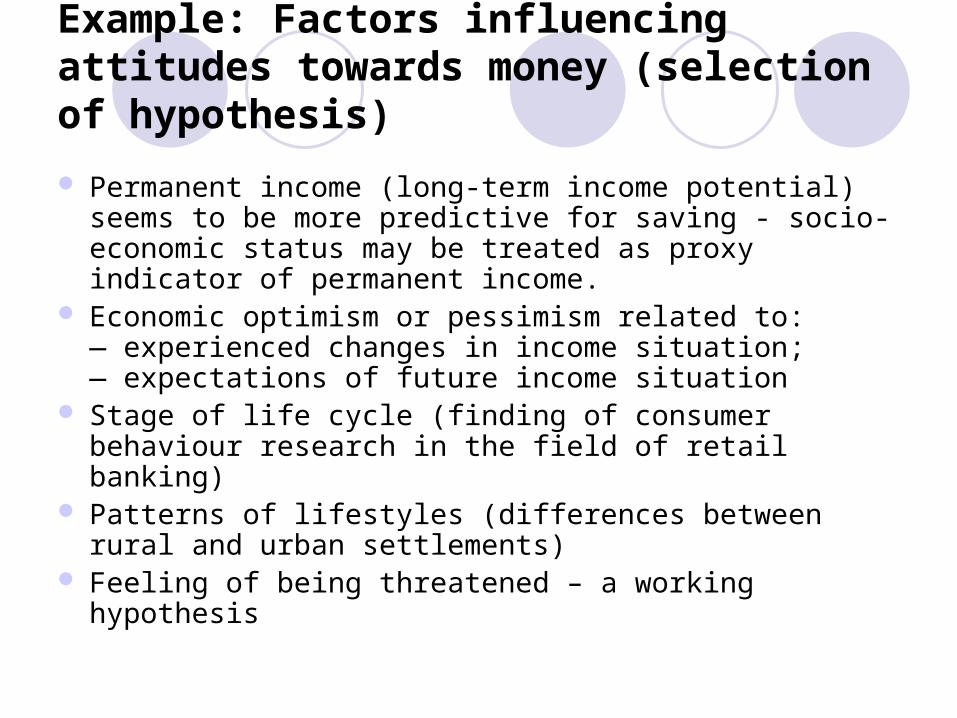

Example: Factors influencing attitudes towards money (selection of hypothesis)

Permanent income (long-term income potential) seems to be more predictive for saving - socio-economic status may be treated as proxy indicator of permanent income.

Economic optimism or pessimism related to: — experienced changes in income situation;— expectations of future income situation

Stage of life cycle (finding of consumer behaviour research in the field of retail banking)

Patterns of lifestyles (differences between rural and urban settlements)

Feeling of being threatened – a working hypothesis

Exploratory data analysis – theory driven insight into data

-0.6 -0.4 -0.2 0.2 0.4 0.6 0.8

-0.6

-0.4

-0.2

0.2

0.4

0.6

0.8

A good custom: don't borrowCredit is rather necessary evil

Credit - unresonable

G. custom: Don't borrow!Buy for money you have

Credit is dangerous

Credit = bad economy

Credit - yes if business

Would like to buy for instalment

Better to take loan than save

Rather spends than saves

Saving is resonable

Spending more attractingSavers don't enjoy life

Better to invest with risk

Respect for savers

Better cash at home

Try to put money aside

Prone to risk if profits

Children should learn saving

18-25

26-35 36-45 46-55

56-65

66+

Element.

Voational

Full second.Prof. college

Higher

Business/Professional

White collar

Blue collar/farmer

Pensioner

Student

Other not work.

Bank 1/week

Bank 1/monthBank less often

Bank not in last year

Savings book

Current account

Fixed deposits PLN

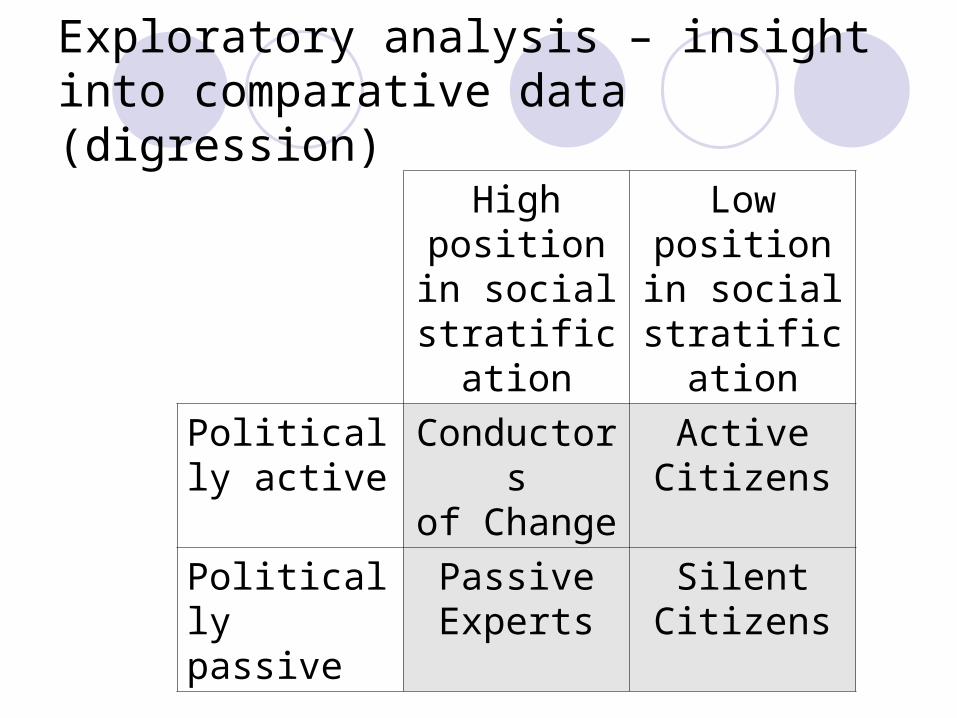

Exploratory analysis – insight into comparative data (digression)

Factor Loadings (PCA) of Attitude Scales for Pooled Sample 1994-1995of ten Central and Eastern European Countries

Factor 1

Fa

cto

r 2

Leftism

AuthoritarianismNationalism

Business Aptitute

Political Mobil.

Economic Optimism

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

1,0

-0,8 -0,6 -0,4 -0,2 0,0 0,2 0,4 0,6 0,8 1,0

Exploratory analysis – insight into comparative data (digression)

Mean Factor Scores (PCA) for CountriesPooled Sample 1994-1995

Factor 1: National Socialism?

Fa

cto

r 2

: Act

ivis

m Poland 94

Poland 95 Hungary 94

Czech 94Czech Re 95

Slovakia 94

Slovakia 95

Estonia 94

Estonia 95

Latvia 94

Latvia 95Lithuani 94

Lithuani 95

Russia 94

Russia 95

Ukraine 94 Ukraine 95

Belarus 94Belarus 95

Bulgaria 95

Romania 95

-0,4

-0,2

0,0

0,2

0,4

-0,8 -0,6 -0,4 -0,2 0,0 0,2 0,4 0,6

Exploratory analysis – insight into comparative data (digression)

Highposition in

social stratification

Lowposition in

social stratification

Politically active

Conductorsof Change

ActiveCitizens

Politically passive

PassiveExperts

SilentCitizens

Political Actors in ten Countries (1994)Positioning in PSE Model factor space

Factor 1: National Socialism

Fa

cto

r 2

: E

con

om

ic &

Po

litic

al A

ctiv

ism

Conductors of ChangeACTORS:

Pol

Hun

CzechSlov

LatLit

Rus

UkrBel

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

-1,4 -0,8 -0,2 0,4 1,0

Passive ExpertsACTORS:

PolHun

Czech

SlovEst

LatLit Rus

Ukr Bel

-1,4 -0,8 -0,2 0,4 1,0

Active CitizensACTORS:

PolHun

CzechSlov

Est

Lat

Lit Rus

Ukr

Bel

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

-1,4 -0,8 -0,2 0,4 1,0

Silent CitizensACTORS:

Pol

Hun

Czech

SlovEstLatLit Rus

Ukr

Bel

-1,4 -0,8 -0,2 0,4 1,0

Est

Exploratory analysis – insight into comparative data (digression)

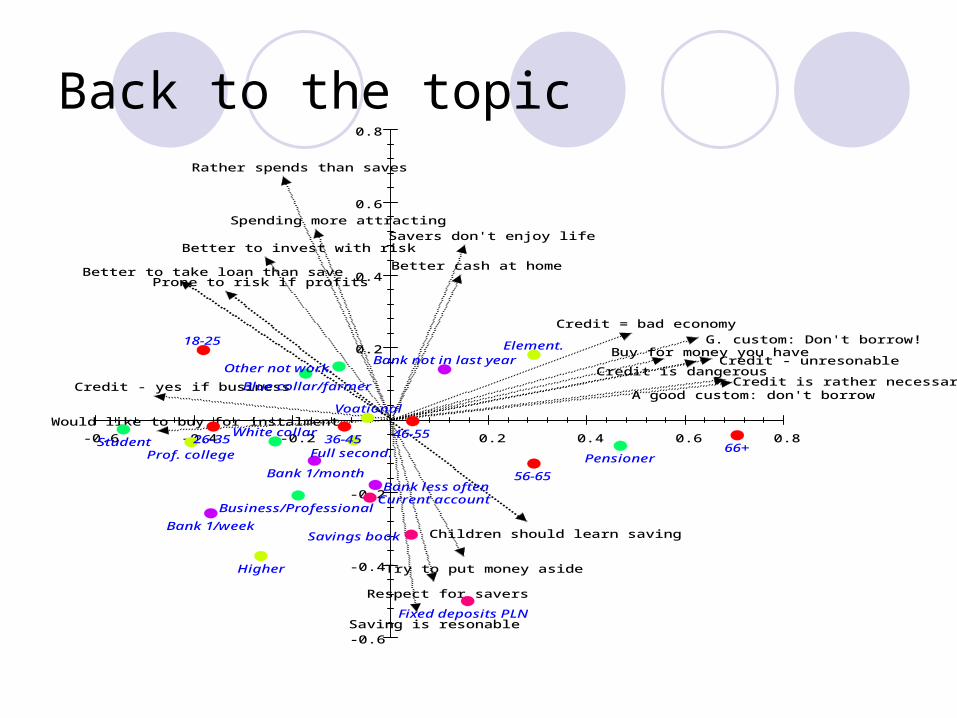

Back to the topic

-0.6 -0.4 -0.2 0.2 0.4 0.6 0.8

-0.6

-0.4

-0.2

0.2

0.4

0.6

0.8

A good custom: don't borrowCredit is rather necessary evil

Credit - unresonable

G. custom: Don't borrow!Buy for money you have

Credit is dangerous

Credit = bad economy

Credit - yes if business

Would like to buy for instalment

Better to take loan than save

Rather spends than saves

Saving is resonable

Spending more attractingSavers don't enjoy life

Better to invest with risk

Respect for savers

Better cash at home

Try to put money aside

Prone to risk if profits

Children should learn saving

18-25

26-35 36-45 46-55

56-65

66+

Element.

Voational

Full second.Prof. college

Higher

Business/Professional

White collar

Blue collar/farmer

Pensioner

Student

Other not work.

Bank 1/week

Bank 1/monthBank less often

Bank not in last year

Savings book

Current account

Fixed deposits PLN

General idea of the path model

Attitude toward saving

Attitude toward debt

Sense of being threatened

Socio-economic status- optimal scale

Age

z4

1

z1

z2

1

Size of settlement

Economic pessimism

z31

1

Attitude towards debt – one factor solution

,36In current situation it is

not reasonable to contracta credit

,43

Taking credits is onlya bad necessity

,24It is dangerous

to contract creditat a bank

,47Good custom - do not

borrow moneyfrom anybody

,31One should buy only formoney one owns, and

not for credit or instalment

,20Buying for credit or instalment

indicates bad moneymanagement

,13

I would like to buy forcredit or instalment

Chi sq. = 413,05p = ,00; Chi sq./df = 20,65

RMSEA = ,14; RMSEA D90 = ,13; RMSEA G90 = ,15Pr(RMSEA <= .05) = ,00GFI = ,89; AGFI = ,80

Hoelter's N (.05) = 76,00

,42

One shouldn't borrowmoney from anybody

d19

d18

d6

d24

d25

d22

d13

d17

No debt

,60

,65

,49

,55

,45

-,37

,68

,64

Attitude towards debt – three factors solution

,51In current situation it is

not reasonable to contracta credit

,57

Taking credits is onlya bad necessity

,33It is dangerous

to contract creditat a bank

,56Good custom - do not

borrow moneyfrom anybody

,61One should buy only formoney one owns, and

not for credit or instalment

,32Buying for credit or instalment

indicates bad moneymanagement

,28

I would like to buy forcredit or instalment

No credits

No instalments

,72

,76

,58

,78

,57

-,53

Chi sq. = 54,93p = ,00; Chi sq./df = 3,23

RMSEA = ,05; RMSEA D90 = ,03; RMSEA G90 = ,06Pr(RMSEA <= .05) = ,60GFI = ,99; AGFI = ,97

Hoelter's N (.05) = 502,00

,50

One shouldn't borrowmoney from anybody

d19

d18

d6

d24

d25

d22

d13

d17

Don't borrow

,75

,71

,70

,66

,45

,57In current situation it is

not reasonable to contracta credit

,55

Taking credits is onlya bad necessity

,34It is dangerous

to contract creditat a bank

,46Good custom - do not

borrow moneyfrom anybody

,64One should buy only formoney one owns, and

not for credit or instalment

,32Buying for credit or instalment

indicates bad moneymanagement

,28

I would like to buy forcredit or instalment

,62

No credits

,50

No instalments

,76

,74

,59

,80

,56

-,53

Chi sq. = 91,52p = ,00; Chi sq./df = 4,82

RMSEA = ,06; RMSEA D90 = ,05; RMSEA G90 = ,07Pr(RMSEA <= .05) = ,06GFI = ,98; AGFI = ,96

Hoelter's N (.05) = 329,00

,54

One shouldn't borrowmoney from anybody

d19

d18

d6

d24

d25

d22

d13

d17

,73

Don't borrow

Z1

Z2

,68

,74

No debt,85

Z3,79

,71

Attitude towards debt – hierarchical CFA

Psychographics – problem with correlated error terms

„How, in your opinion, has the economic situation changed in Poland in the last 12 months?"

„Do you think that in the next 12 months the economic situation in Poland will be:"

„Comparing your current financialsituation with a year ago,

would you say that the situatiom today is:"

„What changes do you expect in yourliving standard in the next 12 months"

„I often fear when I think about my future”

„I'm really concerned about myliving standard in the future”

„I'm afraid that I can have an accident”

„I fear that my flat may be broken into”

Economic pessimism

,58

,58

,67

,70

Sense of beingthreatened

,56

,81

,38

,22

,40

d_v1,81

d_v2,82

d_v6,74

d_v7,72

d17.5,83

d18.2,59

d18.3,92

d18.6,98

Chi sq. = 75,68df= 17 p = ,00; Chi kw./ss = 4,45

RMSEA = ,06;Pr(RMSEA <= .05) = ,13

GFI = ,98; AGFI = ,96,31

,30

Structural model – non-correlated error terms

,48

Prodigality

,18

Affirmation of saving as a norm

,38

Aversion towardscredits

,31Aversion towards

buyingon instalment,62

Aversion towardsborrowing money

in general

,10

Pronenessto save money

,23

General aversiontowards debt

-,69

,43

,61,56

,79

d1

d2

d3

d4

d5

,11

Sense of being threatened

Socio-economicstatus -

optimal scale

Age

,03z5

,11

,26

z1

,27,22

-,10

z2

Size of settlement-,11

-,32

,18

Economicpessimism

z3

,13

-,14

-,12

,33

Chi sq. = 456,24df= 91 p = ,00; Chi kw./ss = 5,01

RMSEA = ,06;Pr(RMSEA <= .05) = ,00GFI = ,94; AGFI = ,92

Hoelter's N (.05) = 250,00

,23

-,24

-,13

,47How... economicsituation changed

in ... last 12 m.

d6,47

in the next 12 m.economic situation

in PL will be:

d7

,69

,38Comparing yourcurrent fin. sit.with a year ago

d8

,62

,42What changes

...expect in yourliving standard...

d9

,08I fear that

my flat maybe broken into

d13

,28,19

I'm afraidthat I can have

an accident

d12

,44,57I'm really concernedabout my living std

in the future”

d11

,75,34I often fearwhen I think

about my future

d10

,58

,69 ,65

-,03

Hybrid model – using parcels in SEM

Hybrid model: includes a combination of latent and observed variables

Parcels are indexes computed by summing or averaging 2 or more items More reliable than items More normally distributed than items Usually higher loadings and better fit Less problems with identification, especially compared with

hierarchical factor models The use of parcels is controversial Is less controversial if scaling diagnostics is done:

Using parcels you better check for unidimensionality Using parcels check in FA if the loadings of the items are similar Determine reliability

Structural model – correlated error terms

,48

Prodigality

,18

Affirmation of saving as a norm

,38

Aversion towardscredits

,31Aversion towards

buyingon instalment,62

Aversion towardsborrowing money

in general

,10

Pronenessto save money

,22

General aversiontowards debt

-,69

,42

,61,56

,79

d1

d2

d3

d4

d5

,11

Sense of being threatened

Socio-economicstatus -

optimal scale

Age

-,01z5

,10

,27

z1

,28,21

-,10

z2

Size of settlement-,10

-,33

,20

Economicpessimism

z3

,19

-,14

-,13

,32

Chi sq. = 302,85df = 88 p = ,00; Chi kw./ss = 3,44

RMSEA = ,05;Pr(RMSEA <= .05) = ,55GFI = ,96; AGFI = ,94

Hoelter's N (.05) = 366,00

,23

-,24

-,13

,28How... economicsituation changed

in ... last 12 m.

d6,29

in the next 12 m.economic situation

in PL will be:

d7

,54

,50Comparing yourcurrent fin. sit.with a year ago

d8

,71

,59What changes

...expect in yourliving standard...

d9

,04I fear that

my flat maybe broken into

d13

,20,14

I'm afraidthat I can have

an accident

d12

,38,66I'm really concernedabout my living std

in the future”

d11

,81,32I often fearwhen I think

about my future

d10

,56

,53 ,77

,36

,31

-,03

-,17

SEM are not causal models

,50

Prodigality

,18Affirmationof saving

as a norm

,37

Aversion towardscredits

,31Aversion towards

buyingon instalment,62

Aversion towardsborrowing money

in general

,15

Pronenessto save money

,17

General aversiontowards debt

-,70

,42

,61,56

,79

d1

d2

d3

d4

d5

,14

Sense of being threatened

,75Socio-economic

status -optimal scale

Agez5

z1

,19

z2

,21

Economicpessimism

z3-,12

,31

Chi sq. = 307,13df= 88 p = ,00; Chi kw./ss = 3,49

RMSEA = ,05;Pr(RMSEA <= .05) = ,49GFI = ,96; AGFI = ,94

Hoelter's N (.05) = 361,00,28

How... economicsituation changed

in ... last 12 m.

d6,30

in the next 12 m.economic situation

in PL will be:

d7

,54

,50Comparing yourcurrent fin. sit.with a year ago

d8

,71

,59What changes

...expect in yourliving standard...

d9

,04I fear that

my flat maybe broken into

d13

,21,14

I'm afraidthat I can have

an accident

d12

,38,66I'm really concernedabout my living std

in the future”

d11

,81,32I often fearwhen I think

about my future

d10

,56

,53 ,77

SES

,17

-,07

-,38

-,17

d15

,87

Size of settlement,18

,20

,33

-,03

-,07

-,28

-,15

-,03

,36 -,16

,31

,23

Single indicator constructs – using reliability information

Using single indicator (like SES scale): fix the variance of indicator error term at the

level =(1-alpha)*variance of the indicator If the scale is standardised (automatically done

in optimal scaling like MCA) – the formula simplifies

Fix the loading of this indicator at 1

The reliability information can be used in terms of any indicator with known reliability

Structural model – using known reliability of the scale

Prodigality

Affirmationof saving

as a norm

Aversion towardscredits

Aversion towardsbuying

on instalment

Aversion towardsborrowing money

in general

Pronenessto save money

General aversiontowards debt

1

1

d11

d21

d31

d41

d51 Sense of being

threatened

Socio-economicstatus -

optimal scale

Agez5

z11

z2

1

Economicpessimism

z3

1

How... economicsituation changed

in ... last 12 m.

d6

in the next 12 m.economic situation

in PL will be:

d7

1

Comparing yourcurrent fin. sit.with a year ago

d8

1

What changes...expect in yourliving standard...

d91

I fear thatmy flat may

be broken into

d13

1

1I'm afraid

that I can havean accident

d12

1

I'm really concernedabout my living std

in the future”

d11

1

I often fearwhen I think

about my future

d101

1

1

1

SES

0,25d15

1

Size of settlement

1

Structural model – using known reliability of the scale

,48

Prodigality

,18Affirmationof saving

as a norm

,37

Aversion towardscredits

,31Aversion towards

buyingon instalment,62

Aversion towardsborrowing money

in general

,11

Pronenessto save money

,23

General aversiontowards debt

-,69

,42

,61,56

,79

d1

d2

d3

d4

d5

,14

Sense of being threatened

,75Socio-economic

status -optimal scale

Agez5

z1

,20

z2

,20

Economicpessimism

z3-,12

,31

Chi sq. = 302,86df= 88 p = ,00; Chi kw./ss = 3,44

RMSEA = ,05;Pr(RMSEA <= .05) = ,55GFI = ,96; AGFI = ,94

Hoelter's N (.05) = 366,00

,24

,28How... economicsituation changed

in ... last 12 m.

d6,29

in the next 12 m.economic situation

in PL will be:

d7

,54

,50Comparing yourcurrent fin. sit.with a year ago

d8

,71

,59What changes

...expect in yourliving standard...

d9

,04I fear that

my flat maybe broken into

d13

,20,14

I'm afraidthat I can have

an accident

d12

,38,66I'm really concernedabout my living std

in the future”

d11

,81,32I often fearwhen I think

about my future

d10

,56

,53 ,77

SES

,13

-,11

-,38

-,17d15

,87

Size of settlement

,18

,27

,27

-,03

-,10

-,28

-,15

-,03

,36 -,18

,31

Prodigality

Affirmationof saving

as a norm

Aversion towardscredits

Aversion towardsbuying

on instalment

Aversion towardsborrowing money

in general

Pronenessto save money

General aversiontowards debt

1

1

0,24d1

1

0,216d2

1

0,21d3

1

0,29d4

1

0,345d5

1 Sense of being threatened

Socio-economicstatus -

optimal scale

Agez5

z11

z2

1

Economicpessimism

z3

1

How... economicsituation changed

in ... last 12 m.

d6

in the next 12 m.economic situation

in PL will be:

d7

1

Comparing yourcurrent fin. sit.with a year ago

d8

1

What changes...expect in yourliving standard...

d91

I fear thatmy flat may

be broken into

d13

1

1

I'm afraidthat I can have

an accident

d12

1

I'm really concernedabout my living std

in the future”

d11

1

I often fearwhen I think

about my future

d10

11

1

1

SES

0,25d15

1

Size of settlement

1

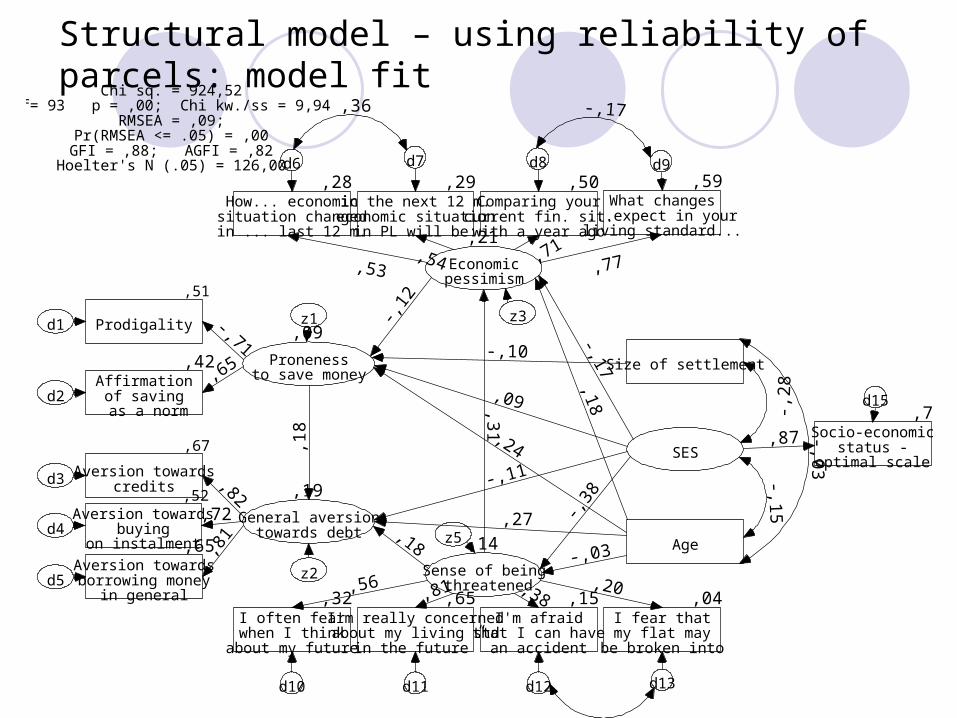

Structural model – using known reliability of parcels

Structural model – using reliability of parcels: model fit

,51

Prodigality

,42Affirmationof saving

as a norm

,67

Aversion towardscredits

,52Aversion towards

buyingon instalment,65

Aversion towardsborrowing money

in general

,09

Pronenessto save money

,19

General aversiontowards debt

-,71

,65

,82,72

,81

d1

d2

d3

d4

d5

,14

Sense of being threatened

,75Socio-economic

status -optimal scale

Agez5

z1

,18

z2

,21

Economicpessimism

z3-,12

,31

Chi sq. = 924,52df= 93 p = ,00; Chi kw./ss = 9,94

RMSEA = ,09;Pr(RMSEA <= .05) = ,00GFI = ,88; AGFI = ,82

Hoelter's N (.05) = 126,00

,18

,28How... economicsituation changed

in ... last 12 m.

d6,29

in the next 12 m.economic situation

in PL will be:

d7

,54

,50Comparing yourcurrent fin. sit.with a year ago

d8

,71

,59What changes

...expect in yourliving standard...

d9

,04I fear that

my flat maybe broken into

d13

,20,15

I'm afraidthat I can have

an accident

d12

,38,65I'm really concernedabout my living std

in the future”

d11

,81,32I often fearwhen I think

about my future

d10

,56

,53 ,77

SES

,09

-,11

-,38

-,17

d15

,87

Size of settlement,18

,24

,27

-,03

-,10

-,28

-,15

-,03

,36 -,17

,31

Topics which are usually less considered in SEM context but are very important Complex samples and SEM

Sampling variance changed by clustering, stratification and weighting for non equal inclusion probabilities

Weighting not always available (like in AMOS) Non-response and SEM:

Item non-response – solutions exists Special estimation algorithms (like in AMOS) Imputation before analysis

Survey non-response Falling response rates – what populations we model? The non-response mechanism is not MAR (Missing

Completely at Random) Usual post-hoc solution is weighting for non-response but

not always possible in SEM (AMOS) Addressing systematic error increases sampling

variance, but this is not considered in popular SEM applications

Before doing comparative research with SEM…

Check if your theory is plausible Think about your model, construct definitions

and indicators before fieldwork Examine your data, also secondary data Explore your data with theoretical background Build your SEM model carefully Check alternative models Think about survey error and … do something

about it!