behaviorscan - faculty.fuqua.duke.edu

TRANSCRIPT

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

BehaviorScanThe Next Generation

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Test New Products & What Options are Available?Why Test TV Advertising & What Options are AvailableBehaviorScan: How it Works & What You GetNew Multi-Outlet Panel DataImproved Panel ANCOVA ModelAppendices

Agenda

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

3Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Should you Test New Products?

Many new products launches are failing, costing $millionsIncrease the odds of success by testing

The biggest opportunities have the biggest risksAccurately evaluate innovative ideas – without betting the company on them

Bscan is more accurate than STMs and less costly than Roll N’Reads

Test the NEW: New brand, major line extension/restage, new usage and benefits, 3rd entry or later

Why Test New Products?

4Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

% of Total New Brands Introduced in CPG Food & Beverage Categories by Year One Dollar Sales (F/D/M)

Most New Products Are Bunts, Not HomerunsWhy Test New Products?

Source: New food & beverage Pacesetter brand sales based on 52 weeks of dollar sales after achieving 30% ACV distribution between February 2003 and January 2004

InfoScan® Reviews Advantage, Food/Supermarkets, Drugstores & Mass Merchandisers, excluding Wal-Mart data for 2002-04 Pacesetters; 1997 – 2001 based on FDM including Wal-Mart store data.

2004 = 851 total new brands; 2003 = 749 total new brands; 1997 – 2002 = 3,567 total new brands

79%

3%7% 8%

2% 1%

76%

4% 8% 9%2% 1%

78%

4% 8% 7%2% 1%

<$7.5MM $7.5- $10MM $10- $20MM $20- $50MM $50- $100MM $100MM+

1997-2002 2003 2004

5Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

And New Products Are ExpensiveAverage launch-only costs: $25 million (range: $5 million - $100 million)Trade

Retail slotting fees: $1-2 million per SKU

Off-invoice allowances, feature ad & display fees: 5-20% of sales

Sales force time & sell-in materials/sales kits

ConsumerAdvertising: $5 - 75 million

Couponing: $5 - 10 million

Other: R&D, Market Research, etc

Cost of a Typical Failure: $14,200,000

Why Test New Products?

6Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Testing Significantly Reduces the Risk of Failure

SOURCE: IRI New Product Trends 2000

Why Test New Products?

Success48%

Failure52%

Of all new products introduced nationally,

less than half succeed.

Of new products tested in BehaviorScan and introduced nationally, over 84% succeed.

SOURCE: IRI New Product Trends 2000

Not Rolled

Out60%

Success38%

Failure 2%

40%rolled

out

7Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

What Options do You Have for New Product Testing?

Simulated Test Market (STM)

Roll & Read Test

BehaviorScan

Testing Options: New Product Tests

8Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Good diagnosticsBased on what people say, not what they do

Insights

Only a concept board stimulusJust norms for marketing mix elements

Completeness

Good where norms existCan be very wrong for unusual products

Accuracy

Almost guaranteedConfidentiality

Supplier handles everythingVery limited product requirements

Effort Required

Typically under $100k Cost

2-4 week setupResults in 6-12 weeks

Speed

CommentsScoreCriteria

Simulated Test Markets: Less Accuracy & Insights

ExcellentGoodAverage Low Poor

Testing Options: New Product Tests

9Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

STM’s promise +/- 20% accuracy 80% of the time, BUT…

+43%$40mm$70mmFrozen Snack

+58%$25mm$60mmShelf Stable Pasta

-60%$150mm$90mmCleaning Product

+60%$40mm$100mmFrozen Ethnic Food

+62%$15mm$40mmAnalgesic

+79%$15mm$70mmSkin Care

ErrorActualSTM Brand/Category

The more unique the product,the higher potential for error.

Testing Options: New Product Tests

10Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

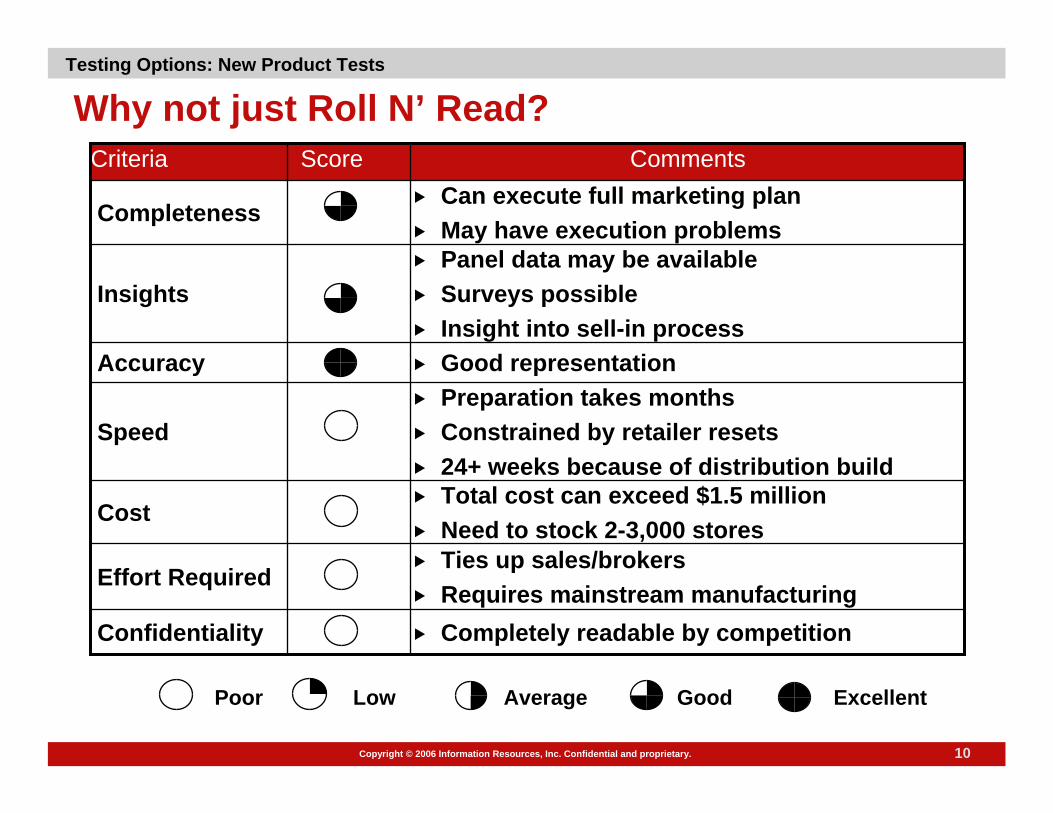

Why not just Roll N’ Read?

Panel data may be availableSurveys possibleInsight into sell-in process

Insights

Can execute full marketing planMay have execution problems

Completeness

Good representationAccuracy

Completely readable by competitionConfidentiality

Ties up sales/brokersRequires mainstream manufacturing

Effort Required

Total cost can exceed $1.5 millionNeed to stock 2-3,000 stores

Cost

Preparation takes monthsConstrained by retailer resets24+ weeks because of distribution build

Speed

CommentsScoreCriteria

ExcellentGoodAverage Low Poor

Testing Options: New Product Tests

11Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Complete panel data availableCan test/model alternative marketing plansCan identify and survey triers

Insights

Can execute full marketing plan. Full controlCompleteness

IntroCast validates at +/- 9%, 90% of timeAccuracy

Some of store data is maskedAll of panel data is masked

Confidentiality

IRI negotiates with retailer IRI stocks and merchandises product

Effort Required

Research costs $350k+Need to stock 20-40 stores

Cost

6 week setup12-24 weeks to run

Speed

CommentsScoreCriteria

ExcellentGoodAverage Low Poor

BehaviorScanTesting Options: New Product Tests

12Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

When to use STM vs. BScan?

Need results in 12-24 weeksNeed results in 6-8 weeks

Some exposure acceptableConfidentiality critical

High riskLow risk

High investmentLow investment

“Unique” marketing plan“Typical” marketing plan

Cannibalization importantCannibalization not important

New or multiple categoriesEstablished category

BscanSTM

Testing Options: New Product Tests

13Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

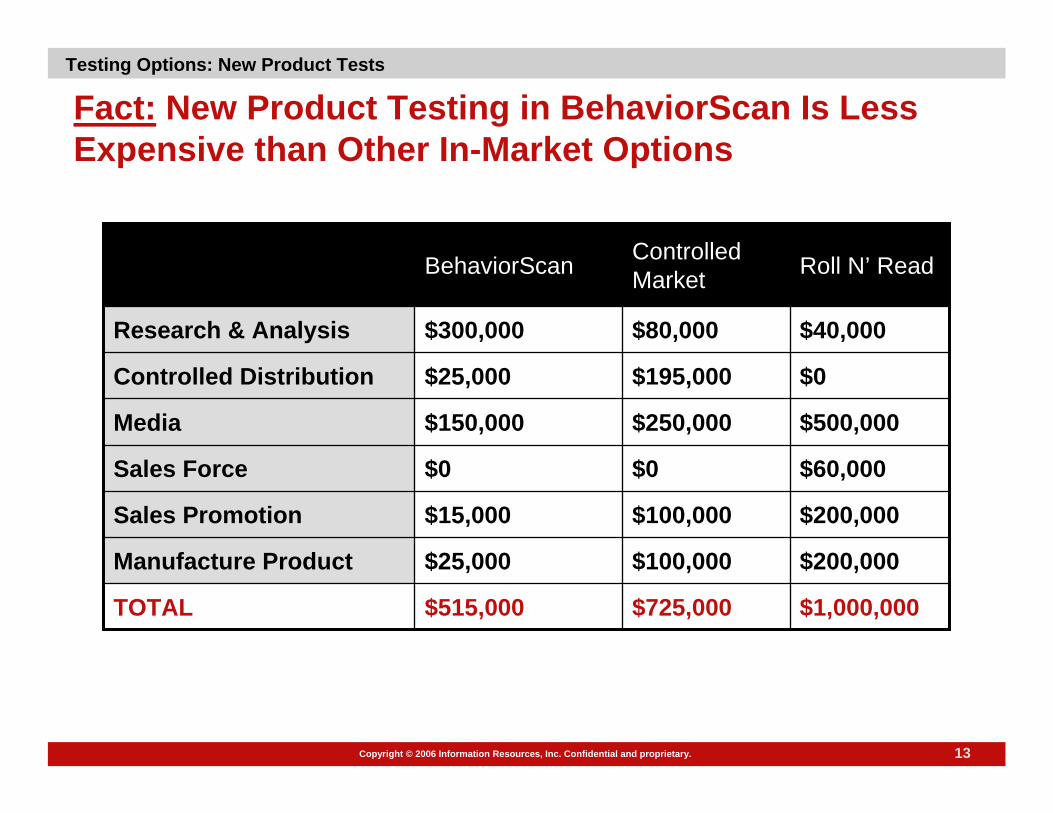

Fact: New Product Testing in BehaviorScan Is Less Expensive than Other In-Market Options

$1,000,000$725,000$515,000TOTAL

$200,000$100,000$25,000Manufacture Product

$200,000$100,000$15,000Sales Promotion

$60,000$0$0Sales Force

$500,000$250,000$150,000Media

$0$195,000$25,000Controlled Distribution

$40,000$80,000$300,000Research & Analysis

Roll N’ ReadControlled MarketBehaviorScan

Testing Options: New Product Tests

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Test New Products & What Options are Available?Why Test TV Advertising & What Options are AvailableBehaviorScan: How it Works & What You GetNew Multi-Outlet Panel DataImproved Panel ANCOVA ModelAppendices

Agenda

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

15Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Should you Test TV Advertising?

Many advertising programs have negative ROI’sAdvertising doesn’t always work – you need to test itGet more for your marketing dollar; reduce uncertainty

The media has changed; you must adapt

Bscan is more accurate than Matched Market tests and often costsless

Test TV: Heavy or reduced spend, broadcast vs. cable, in/out season, 15s vs. 30s, multi vs. single brand

Why Test TV Advertising?

16Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

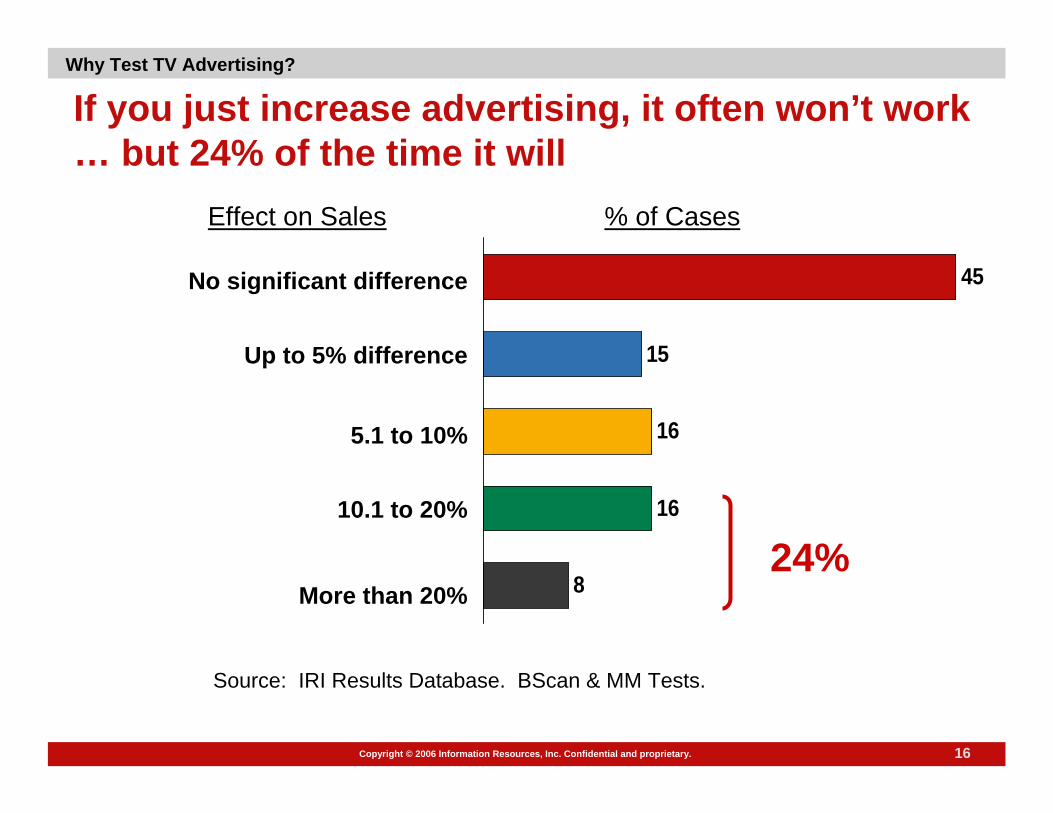

If you just increase advertising, it often won’t work … but 24% of the time it will

Why Test TV Advertising?

No significant difference

Up to 5% difference

5.1 to 10%

10.1 to 20%

More than 20%

Effect on Sales % of Cases

Source: IRI Results Database. BScan & MM Tests.

24%8

16

16

15

45

17Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Most Marketing Programs Have Negative ROI’s

57%

51%

72%

Advertising

Coupons

Trade

Incremental Profit Per Marketing Dollar Spent

Source: 21 Recent Mix Drivers Studies

Why Test TV Advertising?

18Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

The Media has Changed

More channels, more choices means more opportunity for media targeting

# of Channels in the Avg Home

10.0

100

1980

2004

TV is more expensive:A 414% increase in CPM vs. a

212% increase in Cost of Living.

Cost per Thousand Viewers (CPM $)

4.8

19.9

1980

2004

Source: Media Dynamics

Why Test TV Advertising?

19Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

What Options do you Have for TV Ad Testing?

Look to the Past: Model

Advertising Tests: Informal Matched Market Statistical Matched MarketBehaviorScan

Copy Testing

Testing Options: TV Ad Tests

20Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

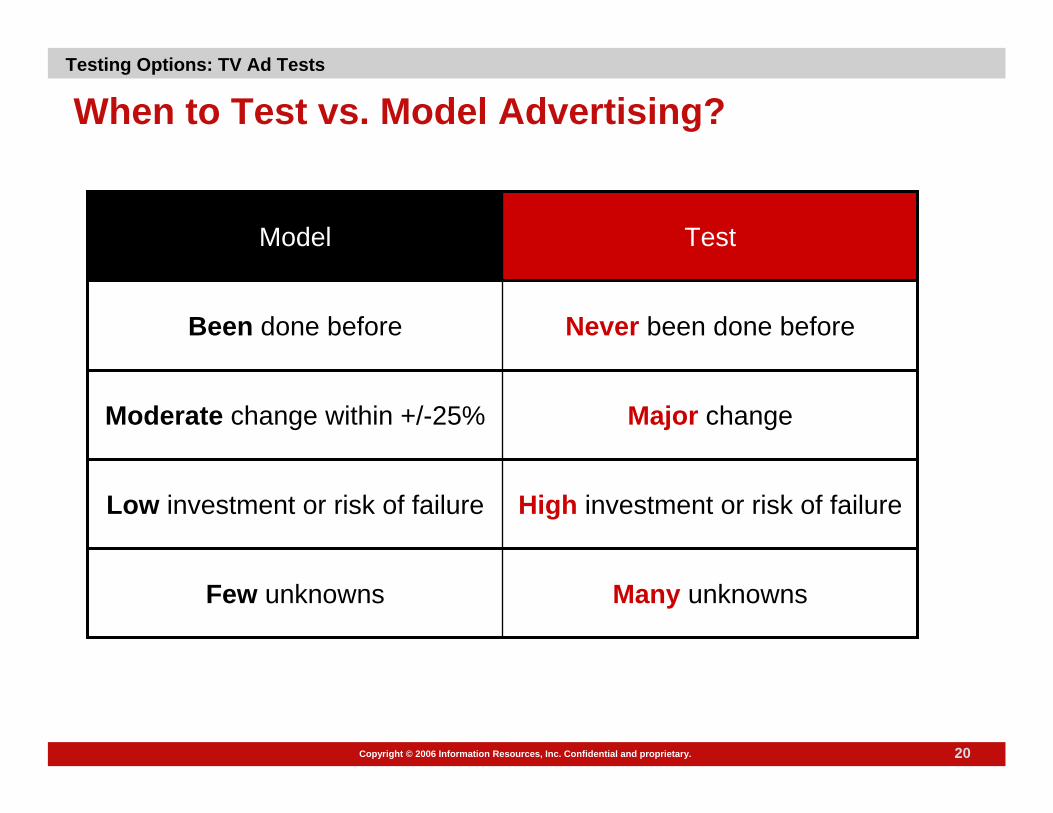

When to Test vs. Model Advertising?

Many unknownsFew unknowns

High investment or risk of failureLow investment or risk of failure

Major changeModerate change within +/-25%

Never been done beforeBeen done before

TestModel

Testing Options: TV Ad Tests

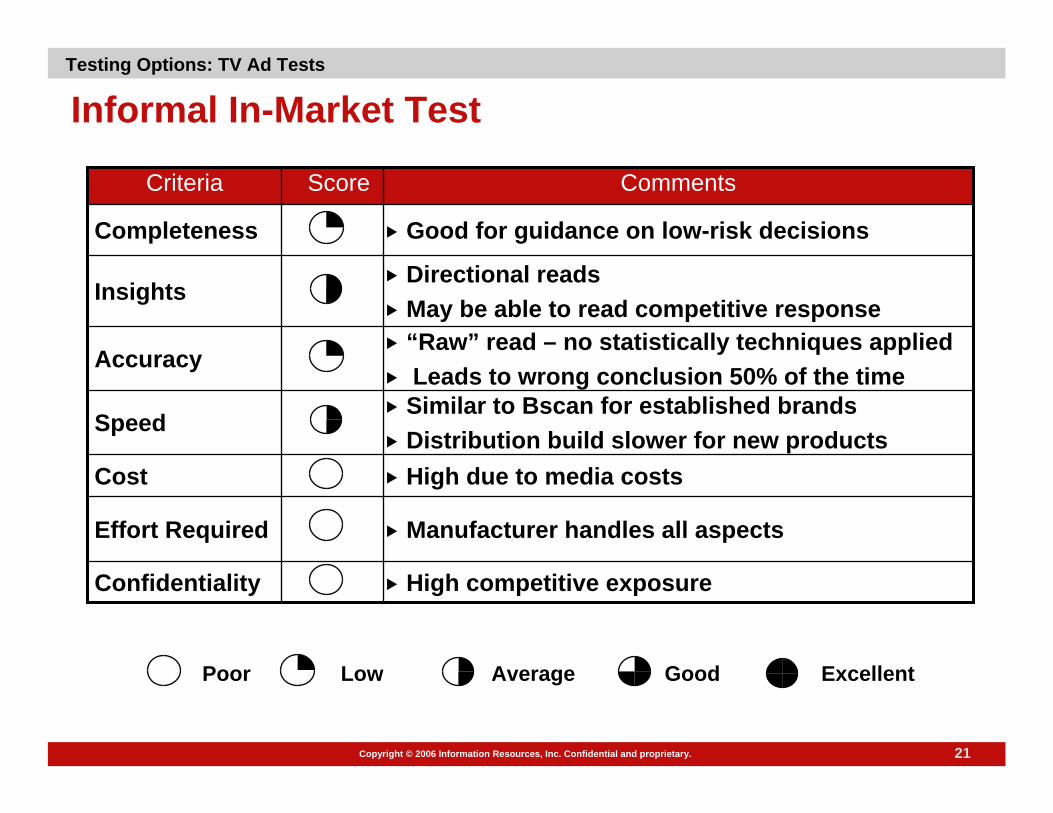

21Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Directional readsMay be able to read competitive response

Insights

Good for guidance on low-risk decisionsCompleteness

“Raw” read – no statistically techniques appliedLeads to wrong conclusion 50% of the time

Accuracy

High competitive exposureConfidentiality

Manufacturer handles all aspectsEffort Required

High due to media costsCost

Similar to Bscan for established brandsDistribution build slower for new products

Speed

CommentsScoreCriteria

ExcellentGoodAverage Low Poor

Informal In-Market Test Testing Options: TV Ad Tests

22Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

ExcellentGoodAverage Low Poor

Panel overlay possibleMay be able to read competitive responseInsights

Good for analyses that can’t be tested at the HH-level like consumer promotions and radio advertising.Completeness

Statistical match and ANCOVA greatly improve accuracyLess control/more unknowns than Bscan

Accuracy

High competitive exposureConfidentiality

Client sales force executes treatmentIRI matches markets and analyzes results Effort Required

Usually higher than Bscan due to media costsCost

Similar to Bscan for established brandsDistribution build slower for new productsSpeed

CommentsScoreCriteria

Statistical Matched Market Test Testing Options: TV Ad Tests

23Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

ExcellentGoodAverage Low Poor

Reads actual panel sales; surveys also available.Multi-outlet panel captures Wal-Mart purchases

Insights

Controlled, real-world environment.Often the only way to test new copy in the real world

Completeness

Most accurate design: test and control cells exposed to the same conditions with targetable TV

Representative marketsStatistical procedures like ANCOVA improvesensitivity

Accuracy

Most store and all panel data is masked.Possibility of competitive exposure

Confidentiality

IRI handles all execution (e.g., cut-ins), except media buyLow panelist burden

Effort Required

Typical Media + Research = $325Frequently lower than MMT’s due to media costs

Cost

Typical test is 52 weeks; 12-24 reads are possibleSpeed

CommentsScoreCriteria BehaviorScan TV Ad Testing

Testing Options: TV Ad Tests

24Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

ExcellentGoodAverage Low Poor

Measures recall, awareness, ad effectiveness Extensive databases available

Insights

Good for ranking of alternative copy ideasNot helpful for new copy or significant changes

Completeness

Based on recall, not actual behaviorLow sample size

Accuracy

Low competitive exposureConfidentiality

Ads do not have to be complete to be tested Respondents watch tape more than once and are interviewed extensively

Effort Required

Low end $15K; average test $50-60KCostTypical test takes at least 5 wks (start to finish)Speed

CommentsScoreCriteria

Copy Testing Testing Options: TV Ad Tests

25Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

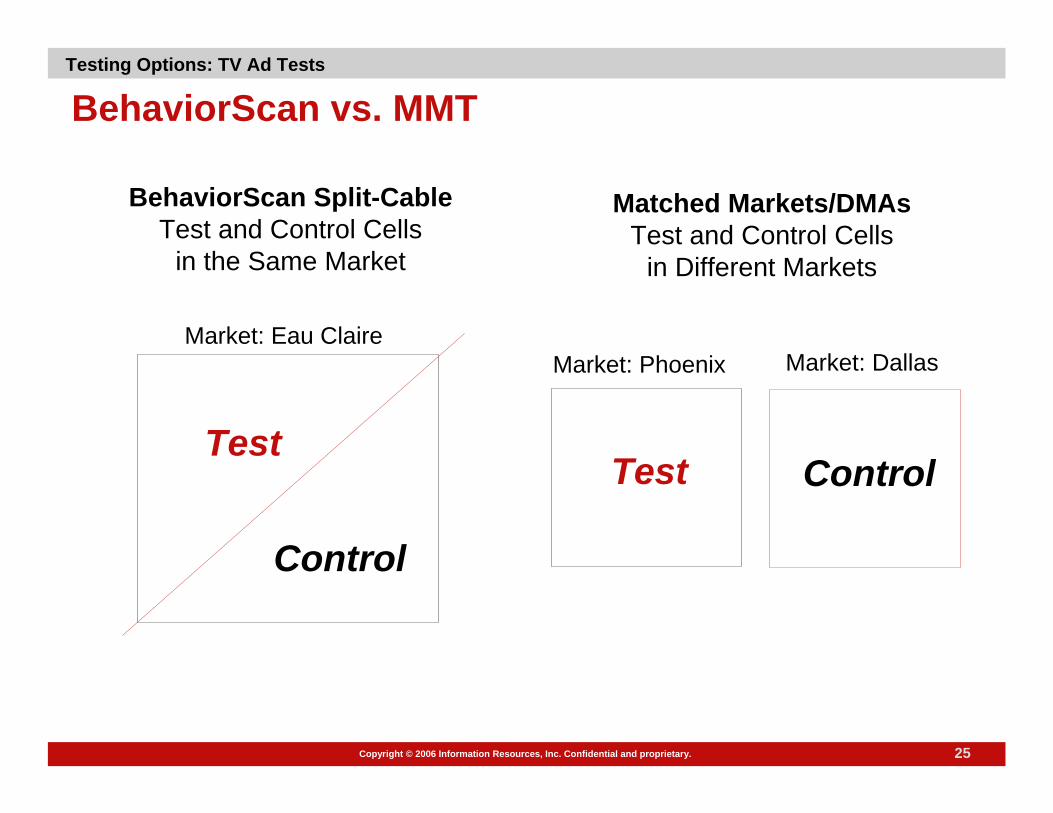

BehaviorScan vs. MMT

BehaviorScan Split-CableTest and Control Cells

in the Same Market

Matched Markets/DMAsTest and Control Cells

in Different Markets

Test

Control

Test Control

Market: Eau ClaireMarket: Phoenix Market: Dallas

Testing Options: TV Ad Tests

26Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Fact: For TV Ad Testing, BehaviorScan is Often Cheaper than Matched Market

Lower media costs in small markets offset higher research costs

Research Cost for B-Scan: 24-week contract (1 outlet, 2 markets) with 20%under-utilized category discount, analytics, and TV ad cut-ins.Research Cost for MMT: IRI analytics only, 1 outlet. (NOTE: Albany is the worst case; other markets are less expensive.)

AND you get much more with BehaviorScan!

$5,000SAVINGS

$330,000$325,000Total Cost

$50,000$165,000Research Cost *$280,000$160,000Media Cost

Nashville + Indianapolis

Pittsfield (Albany) + MidlandMarkets

Matched MarketBscan

Testing Options: TV Ad Tests

27Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

This Client Saved Nearly $400K with Bscan

$392,000SAVINGS$762,000$370,000Total Cost

$50,000$250,000Research Cost$712,000$120,000Media Cost

2 DMAs2 Bscan MarketsMarkets

Matched MarketBscan

Testing Options: TV Ad Tests

28Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Flipping a coin would be just as accurate

54%

8%17%

Informal MarketComparison

Matched Mkt w/Statistical Methods

BehaviorScan WithinMarket

% False Positive*

* Reporting a “test effect” when none exists

Bscan is the Most Accurate MethodTesting Options: TV Ad Tests

29Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

A Major Client said…

“In 2003, our ad spending rose to 8.9 percent of sales, while trade and consumer spending fell to 10.2 percent. Most importantly, rigorous testing tells us that we’re spending our money on marketing and advertising programs that are among the very best in persuasion and impact.”

Jim Kilts, the CEO of Gillette

Testing Options: TV Ad Tests

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Test New Products & What Options are Available?Why Test TV Advertising & What Options are AvailableBehaviorScan: How it Works & What You GetNew Multi-Outlet Panel DataImproved Panel ANCOVA ModelAppendices

Agenda

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

31Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

BehaviorScan is . . .

Full retail execution for testing new products

The nation’s only within-market Targetable TV system for testing new creative and alternative media plansIn-depth analytics

Retail sales Household purchasingAttitudinal surveys available

Benefits

32Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

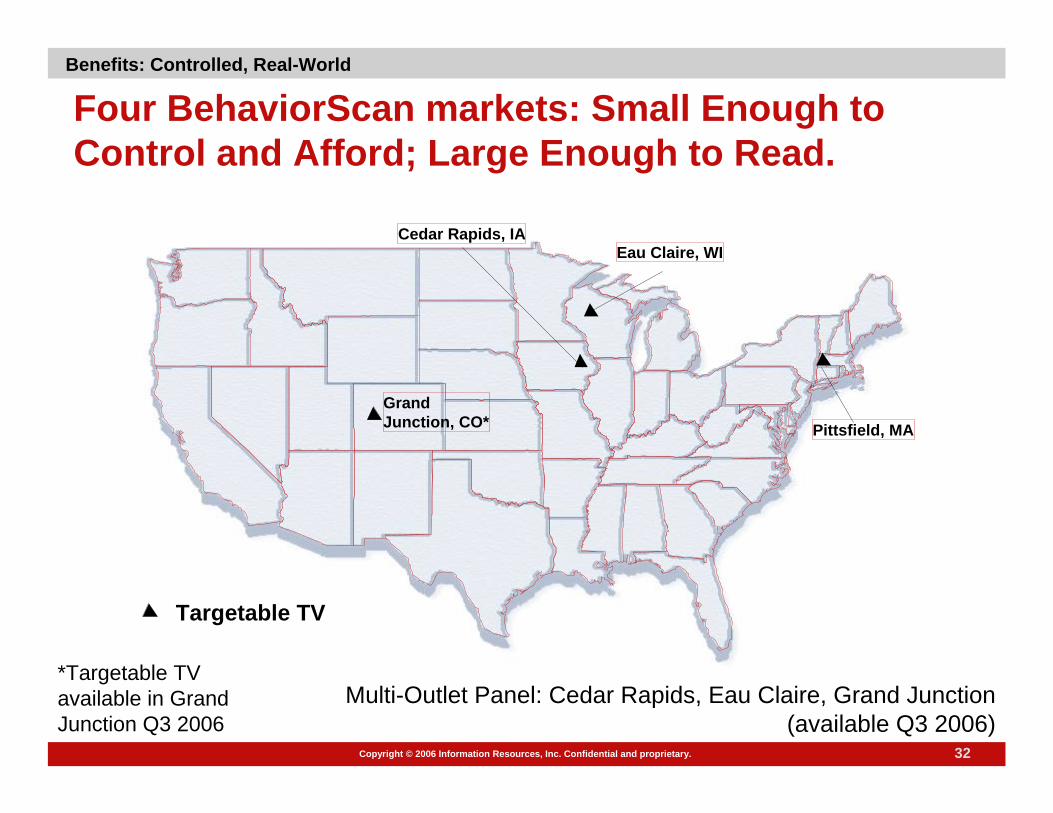

Four BehaviorScan markets: Small Enough to Control and Afford; Large Enough to Read.

GrandJunction, CO* Pittsfield, MA

Cedar Rapids, IAEau Claire, WI

Targetable TV

Multi-Outlet Panel: Cedar Rapids, Eau Claire, Grand Junction (available Q3 2006)

Benefits: Controlled, Real-World

*Targetable TV available in Grand Junction Q3 2006

33Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

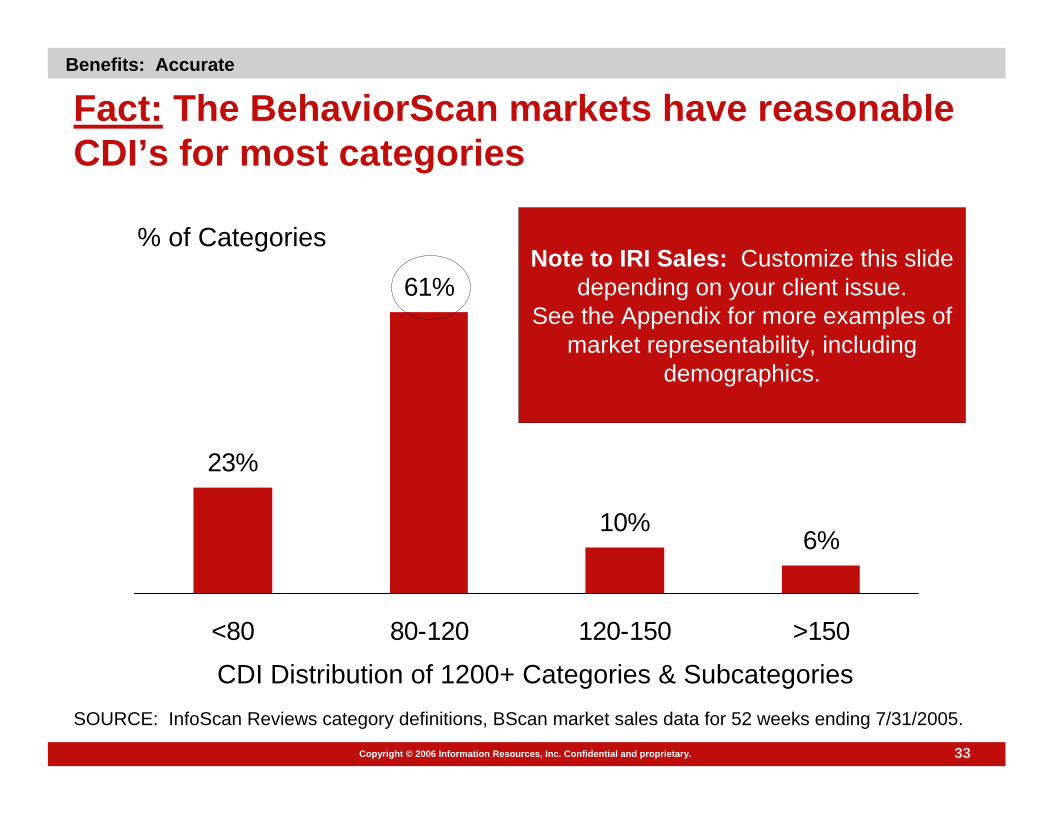

Fact: The BehaviorScan markets have reasonable CDI’s for most categories

23%

61%

10%6%

<80 80-120 120-150 >150

CDI Distribution of 1200+ Categories & Subcategories

% of Categories

SOURCE: InfoScan Reviews category definitions, BScan market sales data for 52 weeks ending 7/31/2005.

Note to IRI Sales: Customize this slide depending on your client issue.

See the Appendix for more examples of market representability, including

demographics.

Benefits: Accurate

34Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Complete Coverage of Retail Sales & Merchandising Retail scanner sales data collected weekly from nearly all grocery, drug, and mass merchandise stores*Weekly collection of feature ads and displaysData from other sources can also be incorporated

Participating in each BScan market are:

7 to 12 FOOD stores

1 to 14 DRUG stores

3 to 5 MASS stores*

*Mass stores are not under contract but can be approached on a test-by-test basis

Benefits: Accurate

35Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Turnkey Product Handling & Retail ExecutionWarehouses for storing and delivering test products (shelf stable, refrigerated, and frozen)

Delivery vehicles

Permanent, experienced staff obtain retailer authorization, deliver and shelve test products, execute promotions, perform shelf audits, etc.

Benefits: Controlled, Real-World

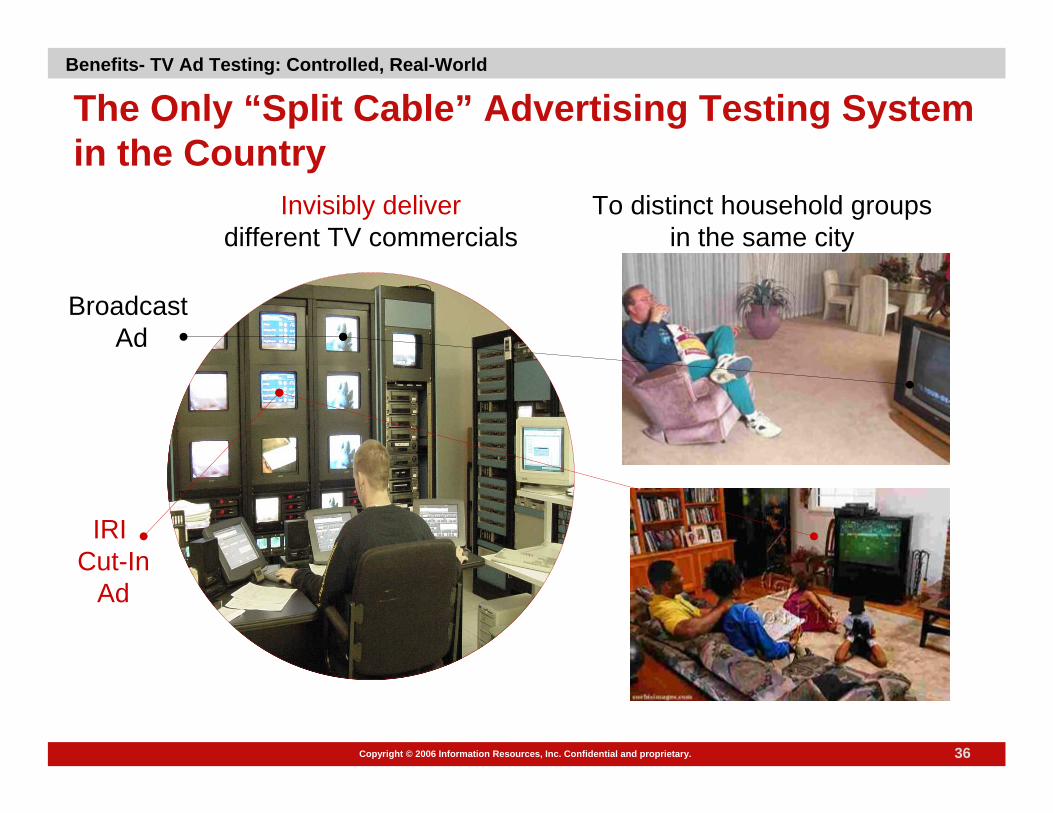

36Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

The Only “Split Cable” Advertising Testing System in the Country

Invisibly deliverdifferent TV commercials

Broadcast Ad

IRI Cut-In

Ad

To distinct household groupsin the same city

Benefits- TV Ad Testing: Controlled, Real-World

37Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

AA

A

BB

C

A

A

B

CA

A

B

B

C

A C

Markets have 30+ fiber optic “nodes”, grouped into three demographically balanced cells.Covers all TV channels in that market and all TV sets in the householdLarge sample for survey researchNo panelist workload

Checkerboard TV Ad Testing Using Underlying Cable System

Benefits- TV Ad Testing: Controlled, Real-World

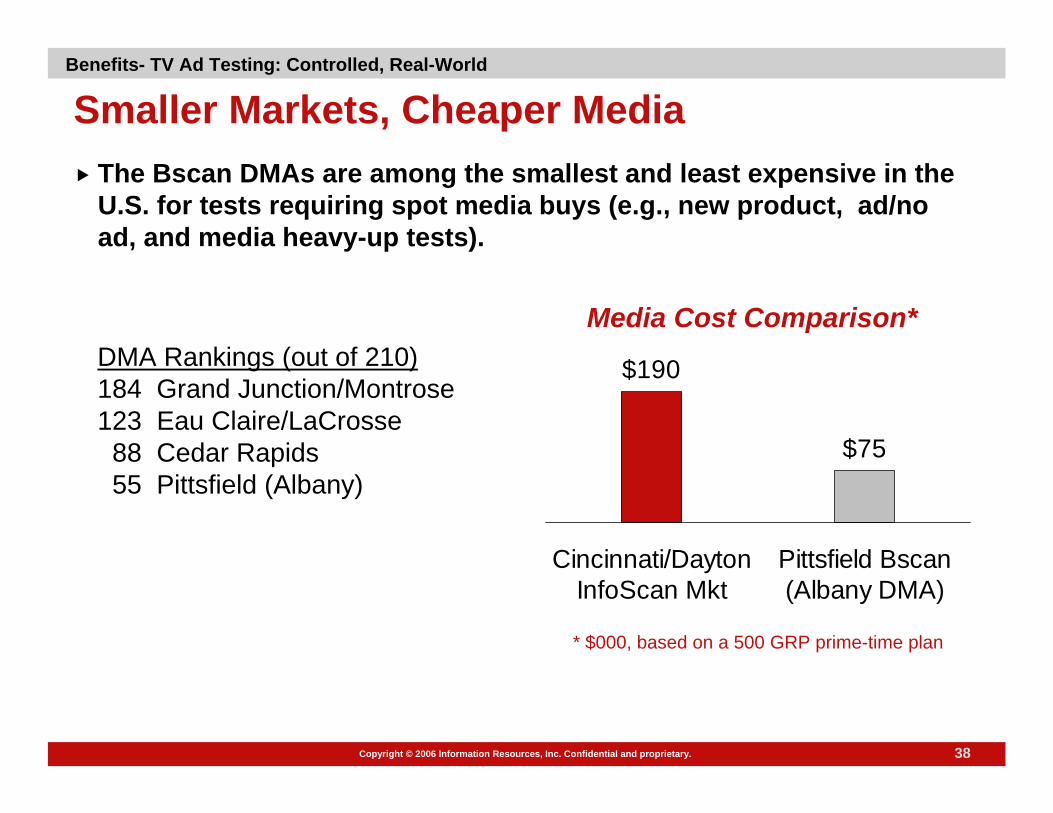

38Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Smaller Markets, Cheaper MediaThe Bscan DMAs are among the smallest and least expensive in the U.S. for tests requiring spot media buys (e.g., new product, ad/no ad, and media heavy-up tests).

DMA Rankings (out of 210)184 Grand Junction/Montrose123 Eau Claire/LaCrosse88 Cedar Rapids55 Pittsfield (Albany)

* $000, based on a 500 GRP prime-time plan

Media Cost Comparison*

$190

$75

Cincinnati/DaytonInfoScan Mkt

Pittsfield Bscan(Albany DMA)

Benefits- TV Ad Testing: Controlled, Real-World

39Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Quicker Ad Test Reads are Available

A 52-week read is preferred, however 12- and 24-week reads are generally feasible.

If there is going to be a long term effect, you will begin to see it within 8 weeks.

Benefits- TV Ad Testing: Speed

40Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

IntroCast Forecasting Model

TRIAL REPEAT ADDITONAL REPEAT

Potential Additional Repeaters

Potential Repeaters

Potential Triers

Advertising, Consumer and Trade Promotion

• Accurate forecasts in 12-16 weeks

• Ability to simulate alternative marketing plans

Benefits- New Product Testing: Speed

41Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

An Accurate Forecast After 12-24 Weeks

Accuracy when predicting year-one after 12-24 weeks in-market: IntroCast validation: ± 9% in 90% of the casesMajor manufacturer validated at ±7% at 12 weeksYear-one forecast in 12-16 weeks for many products

Length of test depends on purchase cycle and product incidence

Need at least 150 triers and 50 repeaters

Benefits- New Product Testing: Speed

42Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Volume Decomposition by Marketing Mix Element

Base PlanYear One Sales = 20MM units

Advertising 15%

Coupons 10%

Trade 15%

Synergy 10%

Base 50%

Benefits- New Product Testing: Actionable

43Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Ability to Evaluate Alternative Marketing Plans

Base Plan with Coupons

20MM Units

Revised Plan, No Coupons

18MM Units

Trade

Coupons

Advertising

Base

Benefits- New Product Testing: Actionable

44Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Attitudinal Research OptionsAttitudeLinkTM: Survey IRI panelists to evaluate Trial & Repeat and other new product measures by consumer segment

comScore Behavior Activated Research (BAR): Survey invitation via coupon issued through Catalina check-out machines triggered by purchase and/or purchase history (e.g. brand buyer, trier that switched to competitor)

Available through 3rd parties:Phone surveys of non-panelists: Awareness, Usage, & Attitudes (must use Survey Sampling)Focus groups / one-on-one interviewsShopper intercept interviews and retailer feedback surveys

Benefits: Actionable

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Attitudinal Option: BAR® Consumer Insights Benefits: Actionable

Direct integration of attitudinal insights and sales performanceSupplement quantitative test results with qualitative consumer insightsRecruit quality sample for focus groups

Advantages:Accurately, efficiently locate ACTUAL buyers and consumers of interestLeverage current and historical purchase behavior for identificationQuick survey execution

46Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

BAR® Survey Process

ShoppingShopping Research InvitationResearch InvitationCheckoutCheckout

Call InitiatedCall Initiated Telephone InterviewTelephone Interview Web InterviewWeb Interview

Picture of a check?

Incentive RewardIncentive Reward

POSPOS

Qualifies potential survey respondents using in-store purchase data from the Catalina Marketing Network®Triggers survey invitations at checkout registersConsumers respond via telephone or Web to receive cash incentive

Benefits: Actionable

47Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Attitudinal Insights:

Buyer Profile, Buyer Influencers; Non-Buyer ProfileUser ProfileAwareness Levels, Source of Awareness Attitudes on Media EffortsReasons for TrialStore Location, In-Store ExperienceProduct Usage OccasionRepurchase IntentLikes & Dislikes - Total, By FlavorCompetitive Preferences & OpinionsOverall SatisfactionSuggested Improvements

BAR® Survey Insights

Adds the Attitudinal Piece of the Pie!

Benefits: Actionable

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Test New Products & What Options are Available?Why Test TV Advertising & What Options are AvailableBehaviorScan: How it Works & What You GetNew Multi-Outlet Panel DataImproved Panel ANCOVA ModelAppendices

Agenda

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

49Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

What’s Exciting About the New BehaviorScan?

Accuracy & CoverageImproved coverage: captures Wal-Mart and other outlets Better sensitivity: more transactions from more householdsNew panel ANCOVA methodology = better sensitivity, tighter results

ActionabilityMore relevant for Non-Food categories and anyone that has Wal-Mart as a top clientNew ways to collect attitudinal data

Still the most controlled, real-world testing environment

Benefits

50Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

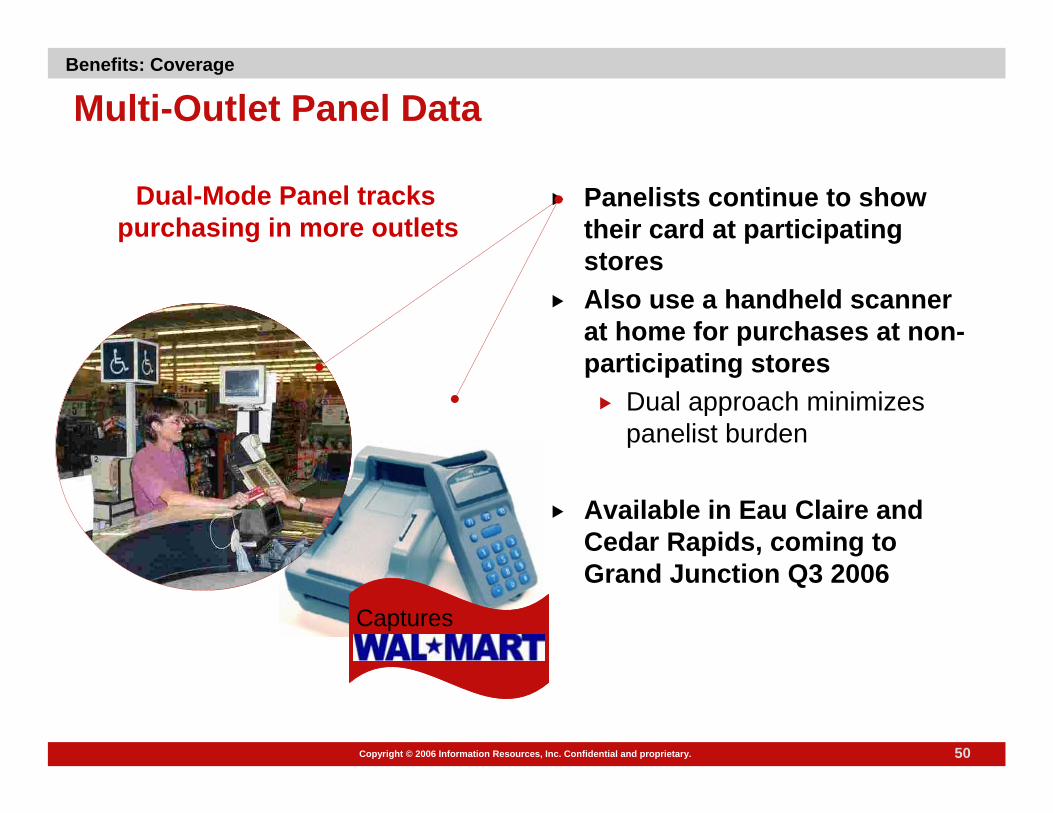

Multi-Outlet Panel Data

Dual-Mode Panel tracks purchasing in more outlets

Panelists continue to show their card at participating stores Also use a handheld scanner at home for purchases at non-participating stores

Dual approach minimizes panelist burden

Available in Eau Claire and Cedar Rapids, coming to Grand Junction Q3 2006

Captures

Benefits: Coverage

51Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

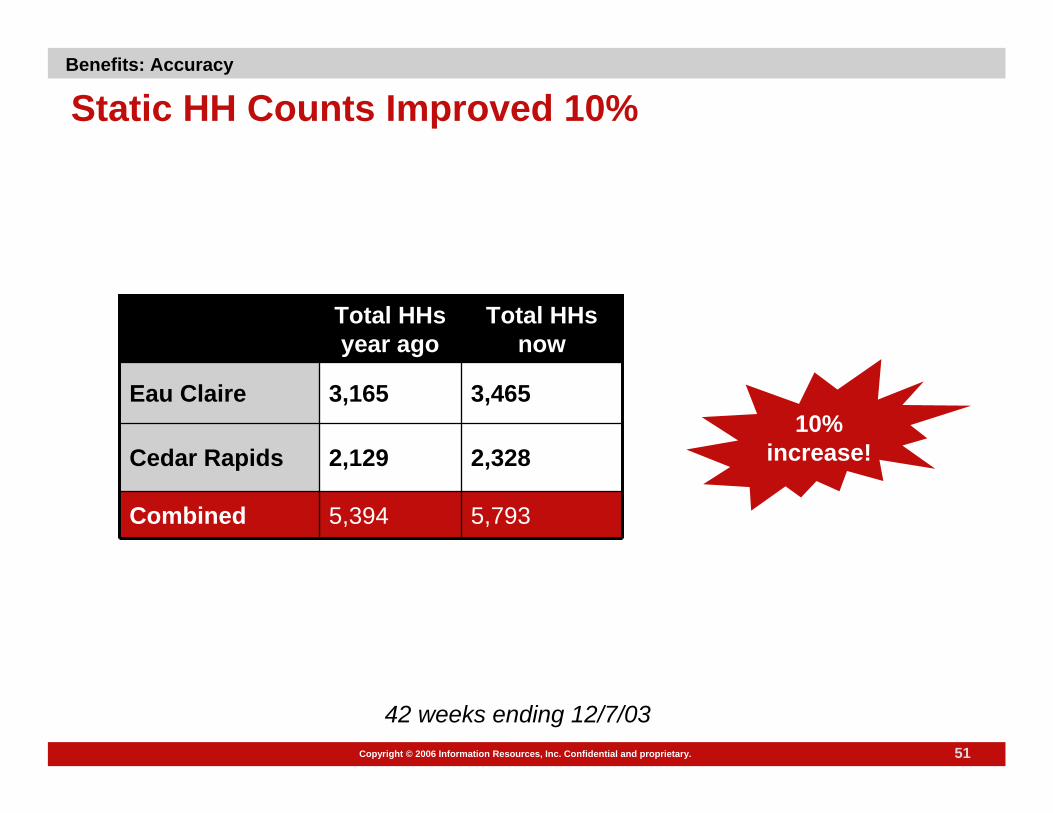

Static HH Counts Improved 10%

5,7935,394Combined

2,328

3,465

Total HHs now

2,129Cedar Rapids

3,165Eau Claire

Total HHs year ago

42 weeks ending 12/7/03

10% increase!

Benefits: Accuracy

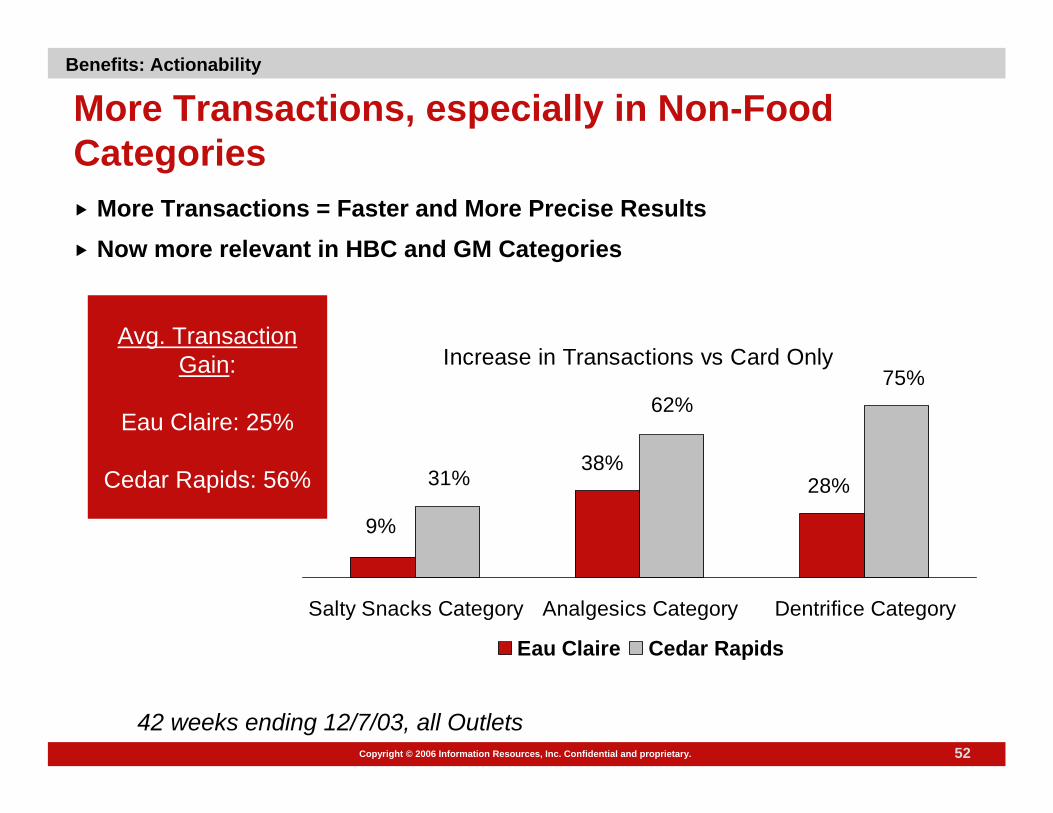

52Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

More Transactions, especially in Non-Food Categories

Increase in Transactions vs Card Only

9%

38%28%31%

62%75%

Salty Snacks Category Analgesics Category Dentrifice Category

Eau Claire Cedar Rapids

More Transactions = Faster and More Precise ResultsNow more relevant in HBC and GM Categories

42 weeks ending 12/7/03, all Outlets

Avg. Transaction Gain:

Eau Claire: 25%

Cedar Rapids: 56%

Benefits: Actionability

53Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Multi-Outlet Improves Test Sensitivity by 15%

Source: EC & CR combined – 52 pre vs 52 post - Sensitivities at 80% CL

11.5

10

Grocery Only Panel Multi-Outlet Panel

Average Sensitivity Across 6 Non-Food Brands with Long Purchase Cycles

15% improvement!

Benefits: Accuracy

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Test New Products & What Options are Available?Why Test TV Advertising & What Options are AvailableBehaviorScan: How it Works & What You GetNew Multi-Outlet Panel DataImproved Panel ANCOVA ModelAppendices

Agenda

Copyright © 2004 Information Resources, Inc. Confidential and proprietary.

55Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Panel ANCOVA Model

Analyzes data at household levelUpdated methodology due to use of ScanKey dataCompares HH purchases in test period to pre period, and to control market

Controls for differences in price and promotionCausal data comes from Panel data only, which incorporates storecausal info where available

Handles both multi-outlet markets (Eau Claire, Cedar Rapids, and Grand Junction as of Q3 2006) and grocery markets (Pittsfield)New corresponding Panel Sensitivity program

Benefits: Accuracy

56Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Estimate

-15.3% +15.3%

The New ANCOVA Model Provides Tighter Results

Estimate

+7.8%-7.8%

Old Covariate New Covariate

Results from Validation of 8 Tests

Benefits: Accuracy

57Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Yields the Most Accurate Results

Controlled, representative marketsReal-world = reads consumer sales, not claimed intentOften cheaper than other methods, more insightsMulti-Outlet Panel data

Improved relevancy: captures Wal-Mart and other outlets Better sensitivity: more transactions from more households

New ANCOVA methodology = better accuracyAttitudinal surveys available

Summary

58Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Appendices

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

More on Building the Business CaseMore Examples of BScan Market RepresentabilityMore on Methodology

Appendices

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

60Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Assumptions: Brand w/$75MM sales/yr, 4 SKUs, $40MM ad budget, $10MM capital investment

Bscan Gives you Better OddsTake the Net Present Value of Operating Income streams over 6 years for the average “homerun” new product …

Bscan reduces risk by $12.1 MM!

NPV of -$10.9 MMBrand 0perating income over 6 yrs

NPV of $1.2 MMBrand operating income over 6 yrs

38% Success ($8 MM)

2% Failure (-$32.2 MM)

60% Not Rolled (-$2 MM)

48% Success (+$11 MM)

52% Failure (-$31.2 MM)

Without Bscan

With Bscan

Why Test New Products?

Note to IRI Sales: A spreadsheet is available

for you to customize these calculations for your client. Contact

Claire Boyle.

61Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why New Products Fail

30% -- Poorly articulated positioning

30% -- Product fails to meet consumer expectations

20% -- Insufficient awareness / advertisingMedia weight, compelling copy

10% -- Insufficient promotion (incentive to try)10% -- Inadequate distribution

SOURCE: Clancy & Shulman, Marketing Myths that are Killing Business

Test marketing

solves!

Why Test New Products?

62Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Criteria for a New Product Test

Able to test the total marketing planCompleteness

Restrict competitors ability to read testConfidentialityMinimum effort required by brokers, sales forceEffort Required

Research Product requirementsSlotting allowancesMarketing programs

Cost

Fast to get into the fieldFast results

Speed

A reliable national forecastEstimates of category expansion and cannibalization

Accuracy

Trial, repeat and other consumer dynamicsAttitudinal measuresImpact of marketing programs

Insights

Why Test New Products?

63Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

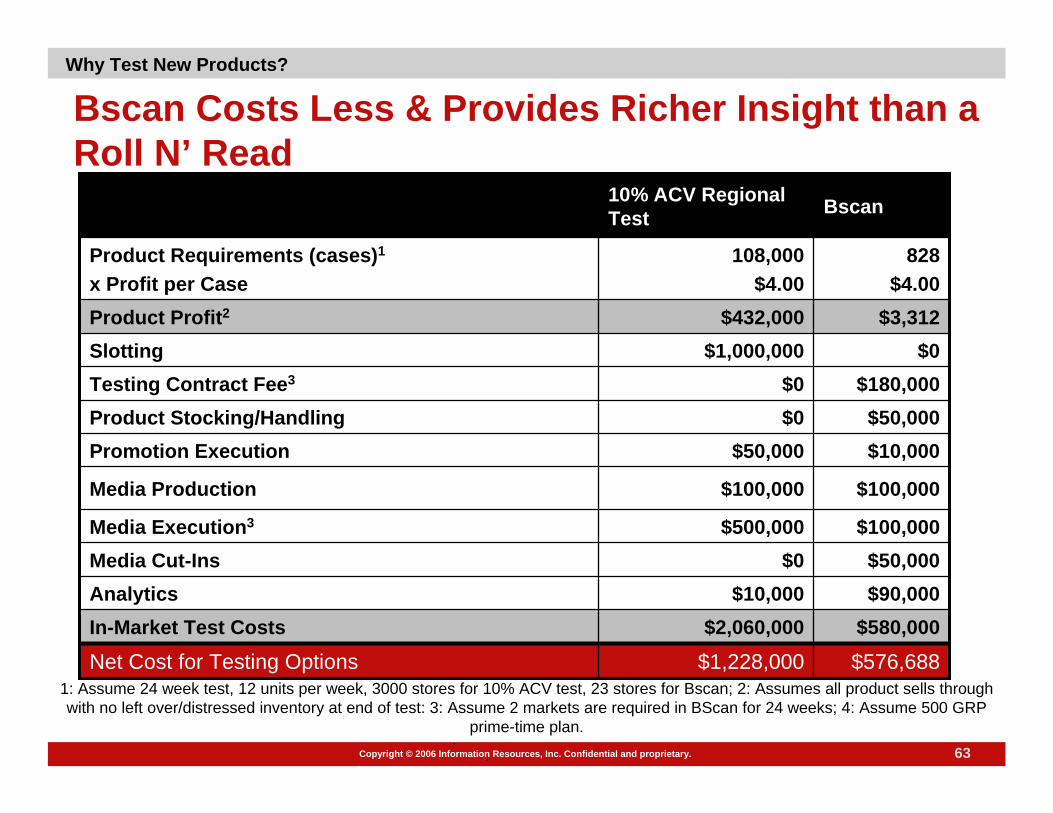

Bscan Costs Less & Provides Richer Insight than a Roll N’ Read

1: Assume 24 week test, 12 units per week, 3000 stores for 10% ACV test, 23 stores for Bscan; 2: Assumes all product sells through with no left over/distressed inventory at end of test: 3: Assume 2 markets are required in BScan for 24 weeks; 4: Assume 500 GRP

prime-time plan..

.

$576,688$1,228,000Net Cost for Testing Options$580,000$2,060,000In-Market Test Costs

$90,000$10,000Analytics$50,000$0Media Cut-Ins

$100,000$500,000Media Execution3

$100,000$100,000Media Production

$10,000$50,000Promotion Execution$50,000$0Product Stocking/Handling

$180,000$0Testing Contract Fee3

$0$1,000,000Slotting$3,312$432,000Product Profit2

828$4.00

108,000$4.00

Product Requirements (cases)1

x Profit per Case

Bscan10% ACV Regional Test

Why Test New Products?

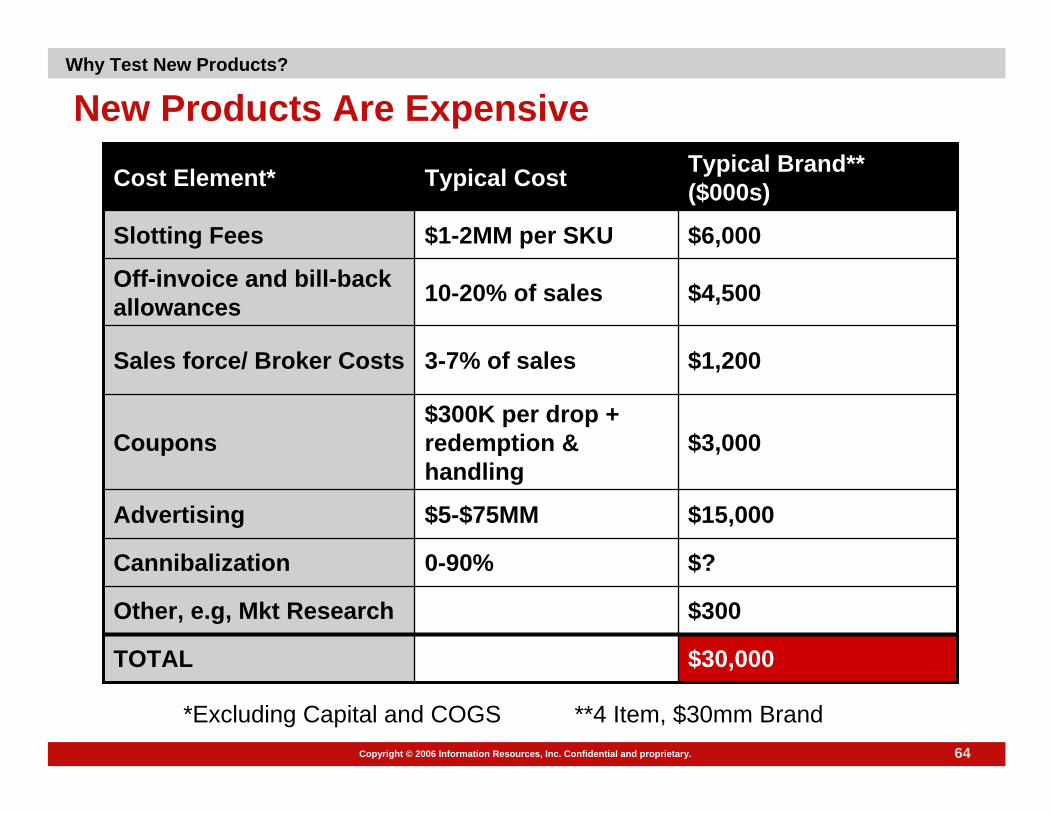

64Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

New Products Are Expensive

**4 Item, $30mm Brand

$30,000TOTAL

$300Other, e.g, Mkt Research

$?0-90%Cannibalization

$15,000$5-$75MMAdvertising

$3,000$300K per drop + redemption & handling

Coupons

$1,2003-7% of salesSales force/ Broker Costs

$4,50010-20% of salesOff-invoice and bill-back allowances

$6,000$1-2MM per SKUSlotting Fees

Typical Brand** ($000s)Typical CostCost Element*

*Excluding Capital and COGS

Why Test New Products?

65Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

The Cost of a Typical New Product Failure (000s)

($14,200)LOSS

$20,000Total Costs

$200Other

$10,000Advertising

$2,000Coupons

$2,000Off-invoice and bill-back allowances

$6,000Slotting allowances

Costs

$6,000Contribution

40%Profit Margin$15,000Revenue from product sold

Income

Why Test New Products?

66Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Why Make Costly Decisions on the Basis of a Shaky set of Assumptions?

Consumer statementsActual ObservedSource of Volume

Claimed frequency of purchase, adjusted based on benchmarksSame as aboveAdditional Repeats

Claimed after 1 week use, adjusted based on benchmarksSame as aboveFirst Repeat

Claimed after viewing concept board, adjusted based on benchmarks

Actual to date, with forecast based on intro-to-date response to marketing as actually executed

Trial

Forecast based on planned marketing eventsActualAwareness

Planned (Quality of created estimated)

Actual, including actual creativeMarketing Events

EstimatedActualDistribution

Simulation (BASES)In-Market Launch (e.g., w/ IRI IntroCast used in Bscan)

Most crucial to long-term volume

and most often wrong in STM

Why Test New Products?

67Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

A Leading Client Says:

“BehaviorScan is a critical component of Frito-Lay’s go-to-market strategy for a couple of reasons.

First, it gives us absolutely the most accurate read on the sales potential of a new product, and a well-rounded view of consumer response to all elements of the marketing mix.

Second, BehaviorScan TV ad testing has enabled us to significantly increase our return on our advertising investment.

We definitely plan to continue using BehaviorScan, especially with the new multi-outlet panel enhancement.”

Dwight RiskeySenior Vice President, Frito-Lay

October 29, 2001

Why Test New Products?

68Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

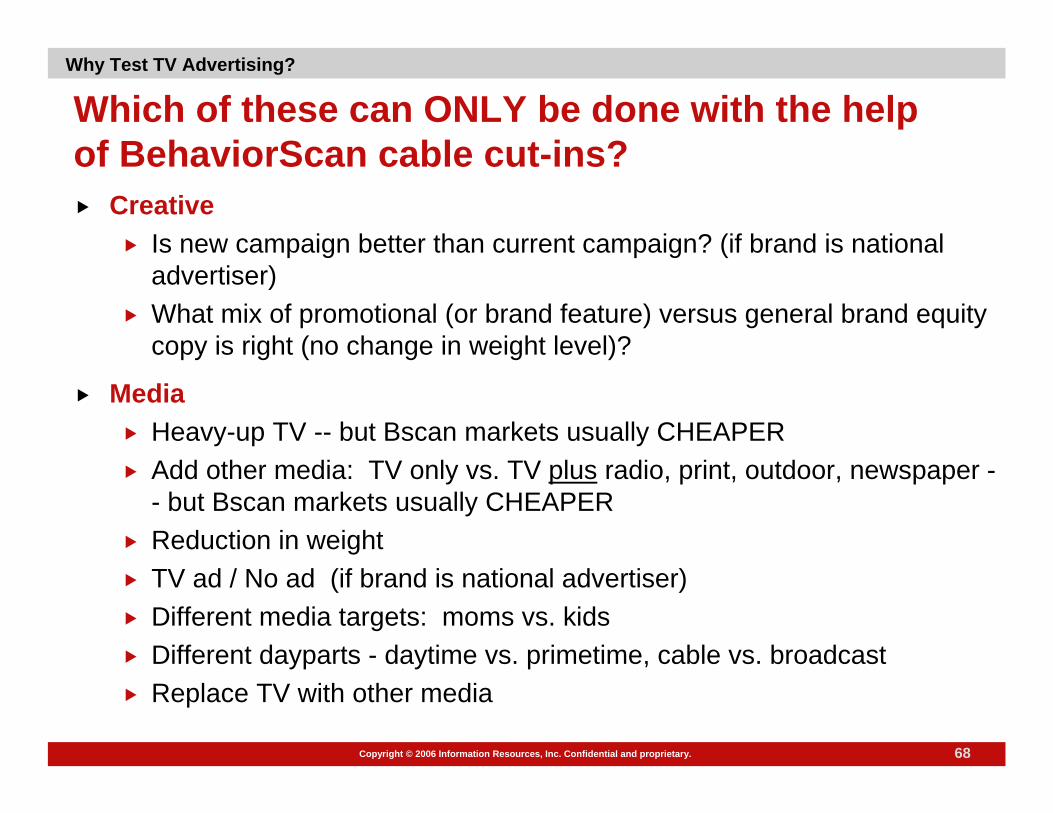

Which of these can ONLY be done with the help of BehaviorScan cable cut-ins?

CreativeIs new campaign better than current campaign? (if brand is national advertiser)What mix of promotional (or brand feature) versus general brand equity copy is right (no change in weight level)?

MediaHeavy-up TV -- but Bscan markets usually CHEAPERAdd other media: TV only vs. TV plus radio, print, outdoor, newspaper -- but Bscan markets usually CHEAPERReduction in weightTV ad / No ad (if brand is national advertiser)Different media targets: moms vs. kidsDifferent dayparts - daytime vs. primetime, cable vs. broadcastReplace TV with other media

Why Test TV Advertising?

69Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Many of the Leading Companies Use BScan*

WrigleyImpressFerreroVlasicOcean SprayDreyersVisaNovartisDialSuiza FoodsMottsDean FoodsStorckMicroSoftConAgraSoldanMichelinChurch & DwightSara LeeKraftCap OneS.C. JohnsonKelloggCampbell SoupReckitt BenckiserJohnson & JohnsonBush BrothersProcter & GambleHersheyBristol MyersPinnacle FoodsHeinzBrachsPillsburyGilletteBinney & SmithPfizerGeneral MillsBayerPepsiCoFoster FarmsBarilla

*Conducted BehaviorScan Tests in 2000-2003

Benefits

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

More on Building the Business CaseMore Examples of BScan Market Representability

Comparison of Bscan vs. US regarding demographics, market dynamics, stores, and media climate

More on Methodology

Appendices

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

71Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Isolated but Representative MarketsDemographics: Accuracy

35.133.845.640.843.2*$45K+ Income

68.9

20.5

Grand Junction

72.9

16.8

Cedar Rapids

63.658.858.61-2 Persons

25.426.829.3**With Kids

Eau ClairePittsfieldTotal U.S.%HHs

Bscan Markets vs. Total U.S.(Survey of Buying Power 2004)

Source: Survey of Buying Power 2004*Source: Est. figures based on Survey of Buying Power 2004

**Source: U.S. Census, Total US Distribution of Demographics - March 2002 update

72Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Occupations

Avg TotalU.S.

Avg BscanMarkets

Management, professional, and related occupations

Source: U.S. Census Bureau; Profile of Selected Social Characteristics, 2000 Census

33.6% 33.3%

Sales and office occupations

33.6%26.7%

Production, transportation, material moving occupations

Avg TotalU.S.

Avg BscanMarkets

14.6% 12.4%

Service occupations

33.6%

Avg TotalU.S.

Avg BscanMarkets

14.9% 16.9%

Demographics

Avg TotalU.S.

Avg BscanMarkets

26.7% 28.7%

73Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

HH IncomeDemographics

28.7%

18.6%

28.1%24.5%

28.5%

19.5%20.3%

29.7%

Less than $25,000 $25,000 - 44,999 $45,000 - 64,999 $65,000 or more

Avg Total U.S.Avg Bscan Markets

Source: Survey of Buying Power, 2004. *Estimated Figures based on Survey of Buying Power 2004

Household Income

*

*

*

74Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

EducationDemographics

Source: U.S. Census Bureau; Profile of Selected Social Characteristics, 2000 Census

80.4%

93.2%90.1%

83.7%

89.8%

Total U.S. Cedar Rapids Eau Claire GrandJunction

Pittsfield

% High School Graduate or Higher

75Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

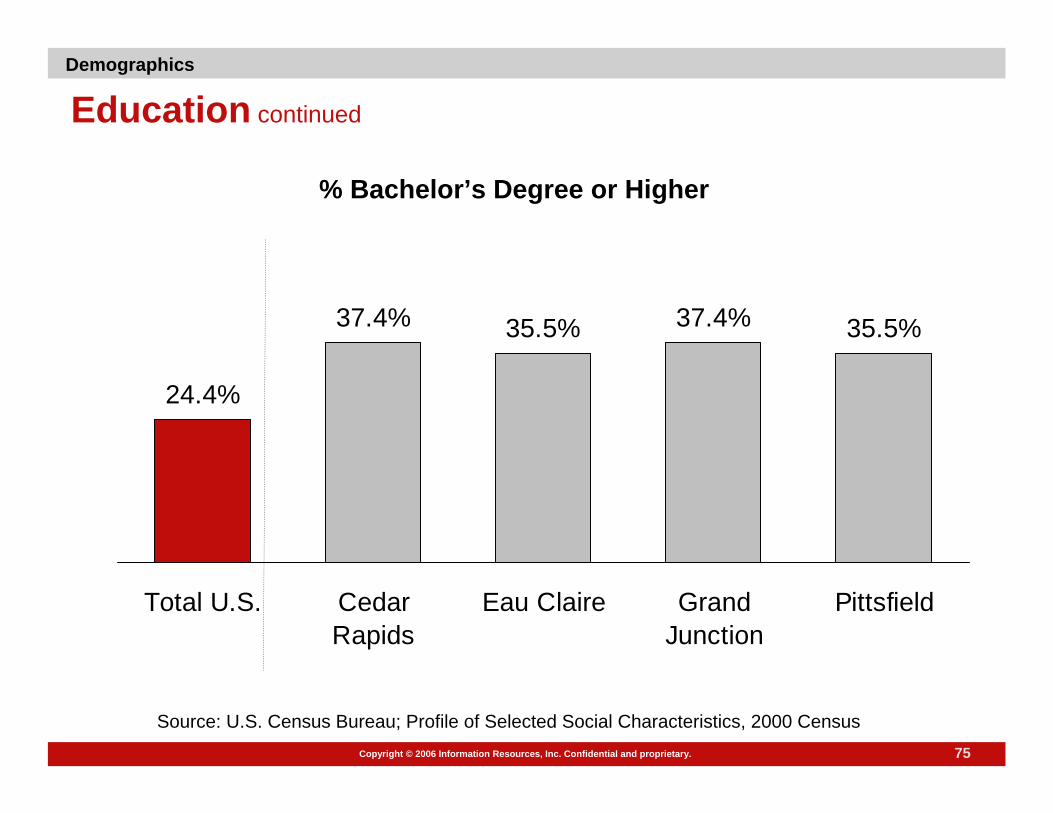

Education continued

Demographics

Source: U.S. Census Bureau; Profile of Selected Social Characteristics, 2000 Census

24.4%

37.4% 35.5% 37.4% 35.5%

Total U.S. CedarRapids

Eau Claire GrandJunction

Pittsfield

% Bachelor’s Degree or Higher

76Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Household SizeDemographics

Source: Survey of Buying Power, 2004.

26.1%

6.5% 4.2%

43.5%

14.0%16.7%

32.4%

22.0%

14.1% 13.2%

5.2%2.0%

1 Member 2 Member 3 Member 4 Member 5 Member 6+Member

Avg Total U.S.Avg Bscan Markets

% of Households

77Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

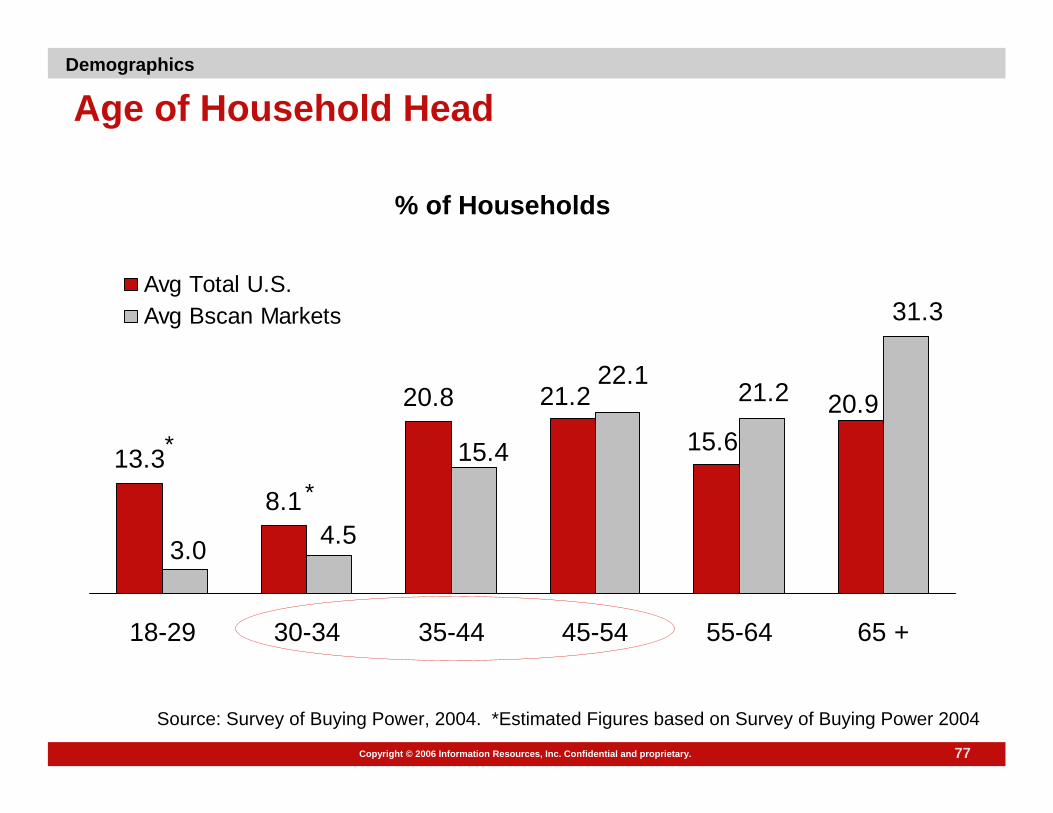

Age of Household HeadDemographics

13.38.1

20.8 21.2 20.915.6

4.5

31.3

21.222.1

15.4

3.0

18-29 30-34 35-44 45-54 55-64 65 +

Avg Total U.S.Avg Bscan Markets

% of Households

Source: Survey of Buying Power, 2004. *Estimated Figures based on Survey of Buying Power 2004

*

*

78Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Market Dynamics: Bscan Consumers buy like the Rest of the Country

Source: IRI Panel Dollars per Buyer; All IRI Categories; 52 Week Ending 6/29/03

$48

$193

$106$147

$53

$484

$52$107

$152

$49

$489

$192

Frito-Lay Kraft GeneralMills

P&G Quaker PrivateLabel

U.S. MarketsBscan Markets

Dollars per Buyer Over 1 Year

Market Dynamics

79Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

The Top 50 Products Sold in Bscan Markets Reflect U.S. Buying Habits

Source: Bscan Market Video, IRI InfoScan Reviews, 52 week period ending 7/13/03, ranking based on top edible categories.

2925General Mils Cheerios 15 oz

2216Nabisco Ritz Crackers 16 oz

2314Oscar Mayer Sliced Bacon 16 oz

2113Philadelphia Cream Cheese 8 oz

1112Lays Potato Chips 12 oz

12Pepsi Cola 144 oz

21Coke Classic 144 oz

Bscan Market Rank

U.S. Market Rank

Market Dynamics

80Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Bscan Markets are Comprised Largely of Chain Grocery Stores

78% 71% 75%

100% 100%

Total U.S. Pittsfield Eau Claire GrandJunction

CedarRapids

% of Chain Stores

Source: Bscan market video, 6/03

Market Dynamics

81Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Bscan Grocery Stores are Somewhat Larger than the U.S. Average

27.2

38.047.0 43.9

39.6

Total U.S. Pittsfield Eau Claire GrandJunction

CedarRapids

Average Store Square Footage (000s)

Source: Bscan market video, 6/03

Market Dynamics

82Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

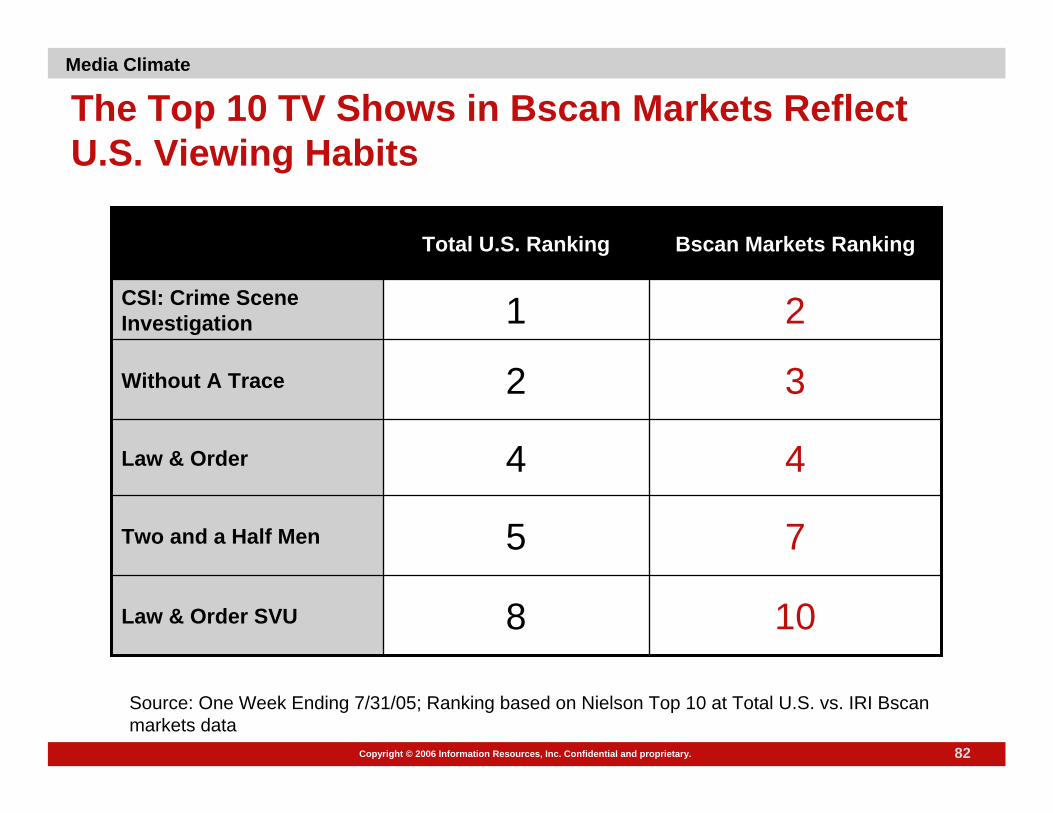

The Top 10 TV Shows in Bscan Markets Reflect U.S. Viewing Habits

Source: One Week Ending 7/31/05; Ranking based on Nielson Top 10 at Total U.S. vs. IRI Bscan markets data

108Law & Order SVU

75Two and a Half Men

44Law & Order

3

2

Bscan Markets Ranking

2Without A Trace

1CSI: Crime Scene Investigation

Total U.S. Ranking

Media Climate

83Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

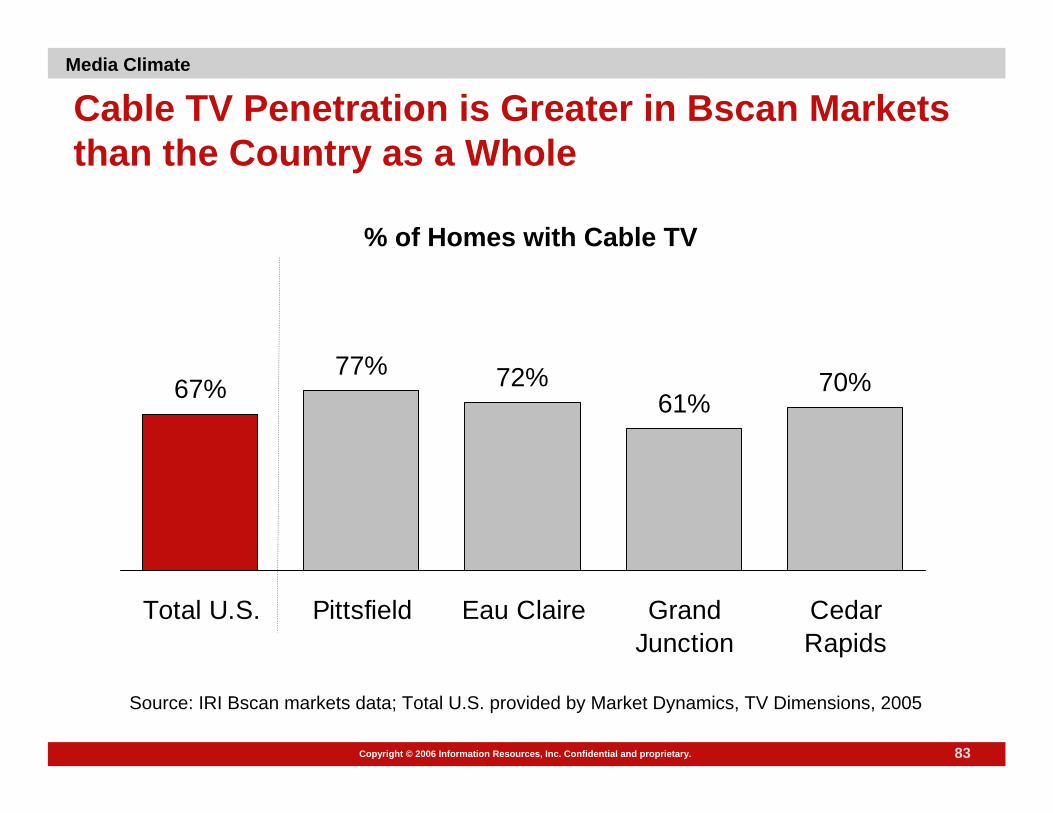

Cable TV Penetration is Greater in Bscan Markets than the Country as a Whole

% of Homes with Cable TV

67%77% 72%

61%70%

Total U.S. Pittsfield Eau Claire GrandJunction

CedarRapids

Source: IRI Bscan markets data; Total U.S. provided by Market Dynamics, TV Dimensions, 2005

Media Climate

84Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

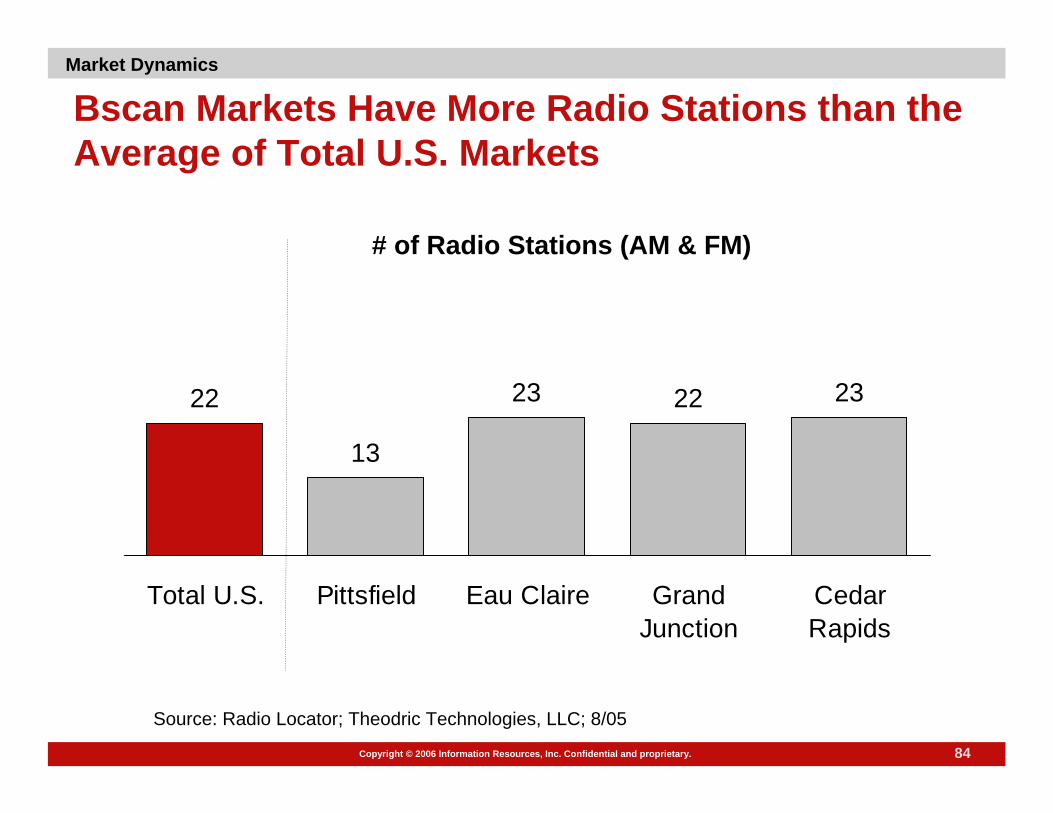

Bscan Markets Have More Radio Stations than the Average of Total U.S. Markets

22

13

23 22 23

Total U.S. Pittsfield Eau Claire GrandJunction

CedarRapids

# of Radio Stations (AM & FM)

Source: Radio Locator; Theodric Technologies, LLC; 8/05

Market Dynamics

85Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Internet Penetration is Similar in Bscan Markets to the Total U.S.

Internet Penetration*

Source: Total U.S. Computerwire 3/22/04; IRI Bscan Household Panel Survey 6/2005.

75% 77% 74% 73% 73%

Total U.S. Pittsfield Eau Claire GrandJunction

CedarRapids

Market Dynamics

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

More on Building the Business CaseMore Examples of BScan Market RepresentabilityMore on Methodology

Appendices

Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

87Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

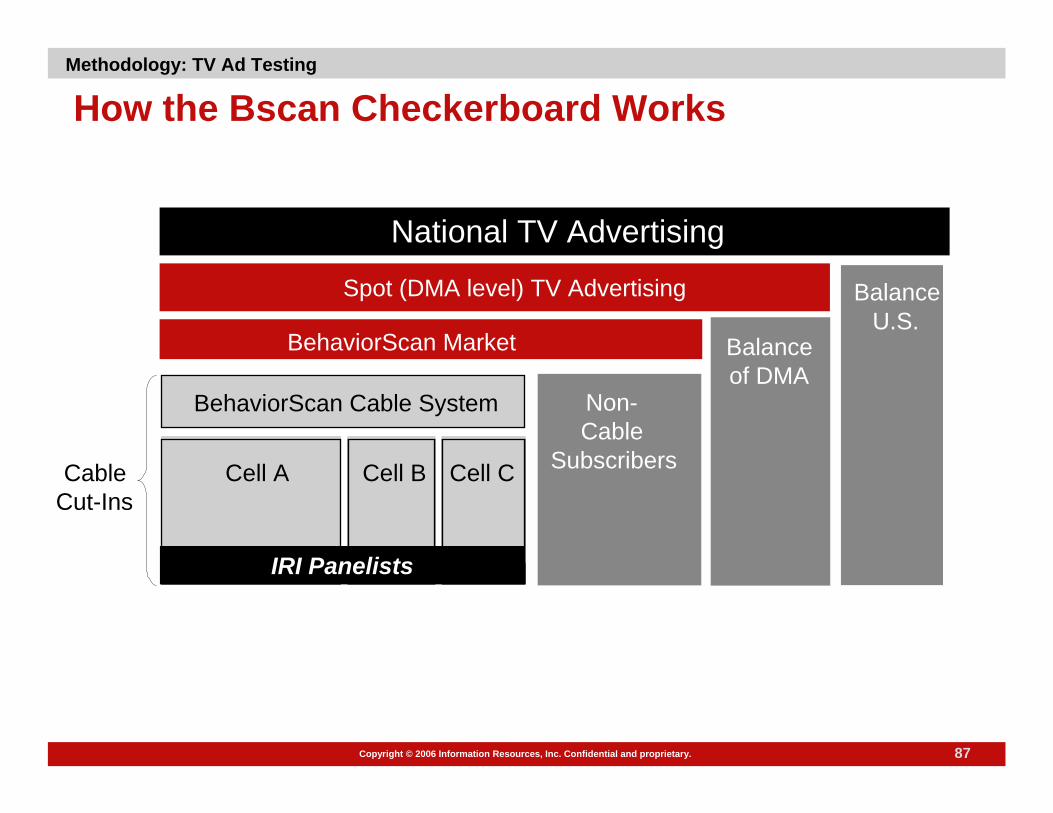

How the Bscan Checkerboard Works

BalanceU.S.

Balanceof DMA

BehaviorScan Cable System Non-Cable

SubscribersCell A Cell B Cell CCableCut-Ins

National TV Advertising

Spot (DMA level) TV Advertising

BehaviorScan Market

IRI Panelists

Methodology: TV Ad Testing

88Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Within-Market Design Ensures an “Apples to Apples” Comparison

Test and control cells experience the same ...Environmental conditions - temperature, humidity, weather disastersLocal festivals and special eventsCompetitive advertising and promotionsRetailer presence and outlet mixAlternative media presencePublicity / press coverage, other business conditions

Market 1Test

Control Test

Control

Market 2

Methodology: TV Ad Testing

89Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

BehaviorScan Split-Cable TV Ad Testing Who Sees What

Cell A Cell B Cell C-Test- -Control-

Non-CableSubscribers

DMA ConditionDMA Condition

Local Cable System / BehaviorScan Studio

¤¤¤¤¤¤¤¤¤ ¤¤¤¤ ¤¤¤¤

¤ = IRI Panel HHs

National Condition

30% of market

30% of market

30% of market

Methodology: TV Ad Testing

90Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

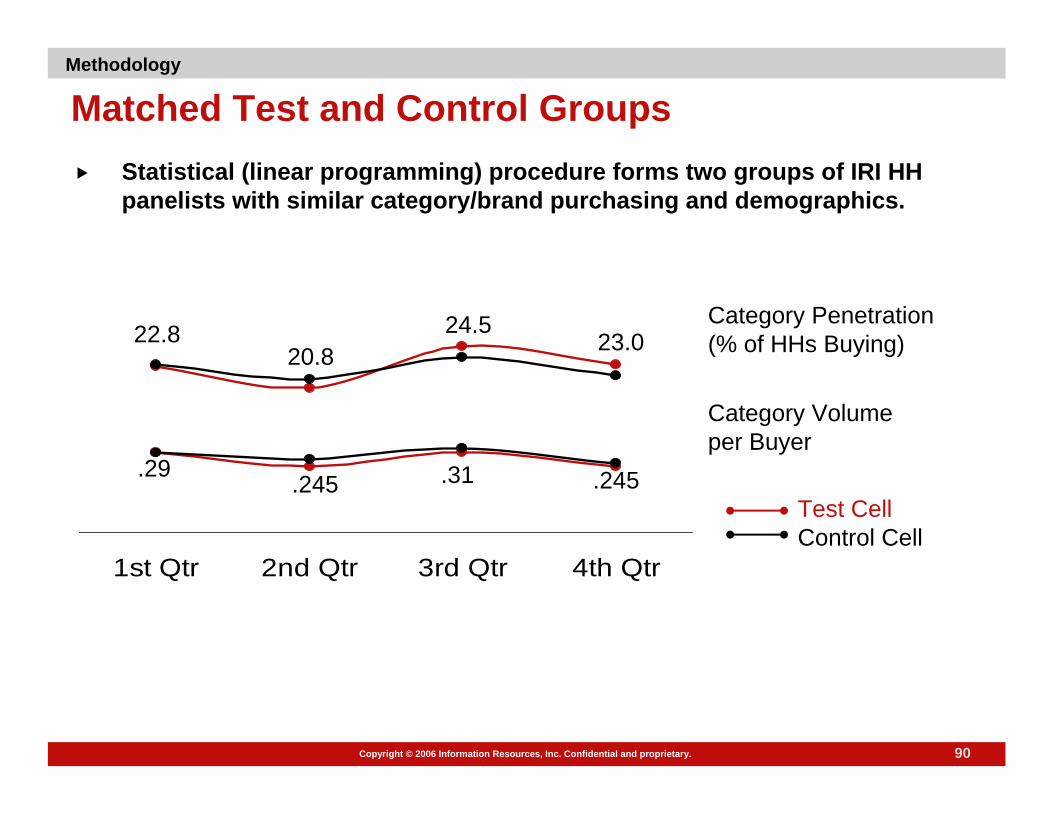

Matched Test and Control GroupsStatistical (linear programming) procedure forms two groups of IRI HH panelists with similar category/brand purchasing and demographics.

Methodology

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

Category Penetration (% of HHs Buying)

Category Volume per Buyer

20.822.8 24.5

.245.31.245.29

23.0

Test CellControl Cell

91Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

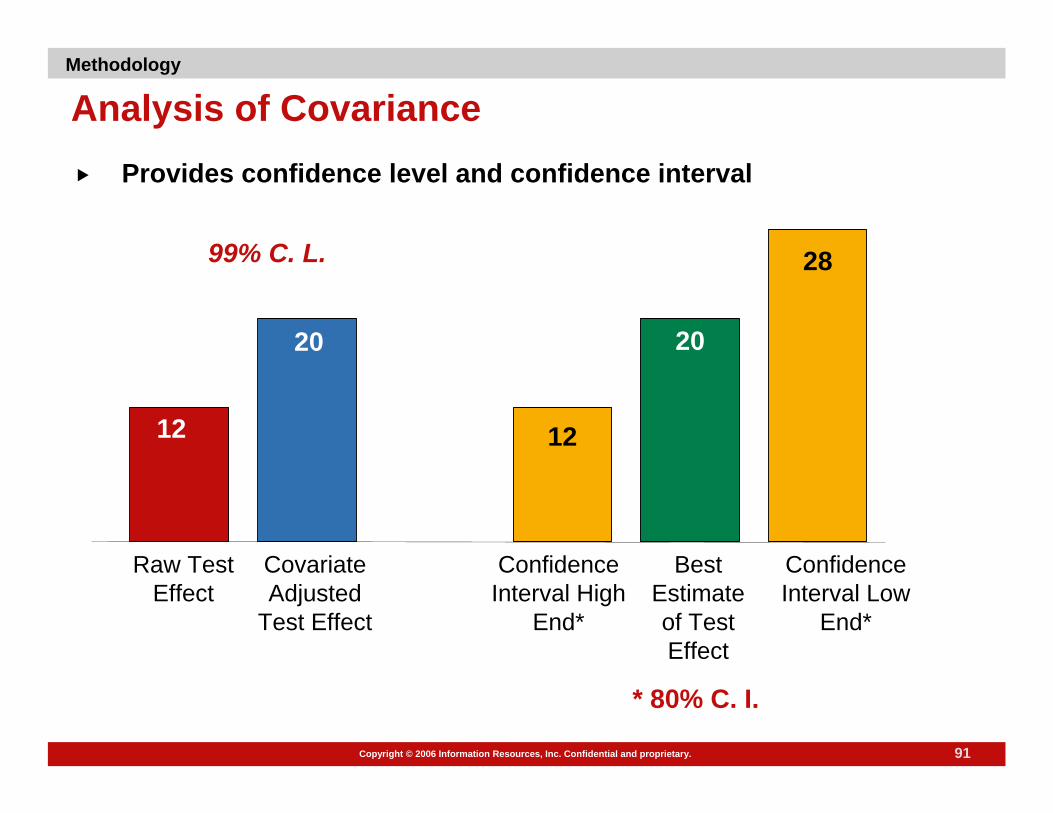

Analysis of CovarianceProvides confidence level and confidence interval

Raw Test Effect

Confidence Interval Low

End*

Best Estimate of Test Effect

Covariate Adjusted

Test Effect

Confidence Interval High

End*

99% C. L.

* 80% C. I.

12

20

28

12

20

Methodology

92Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

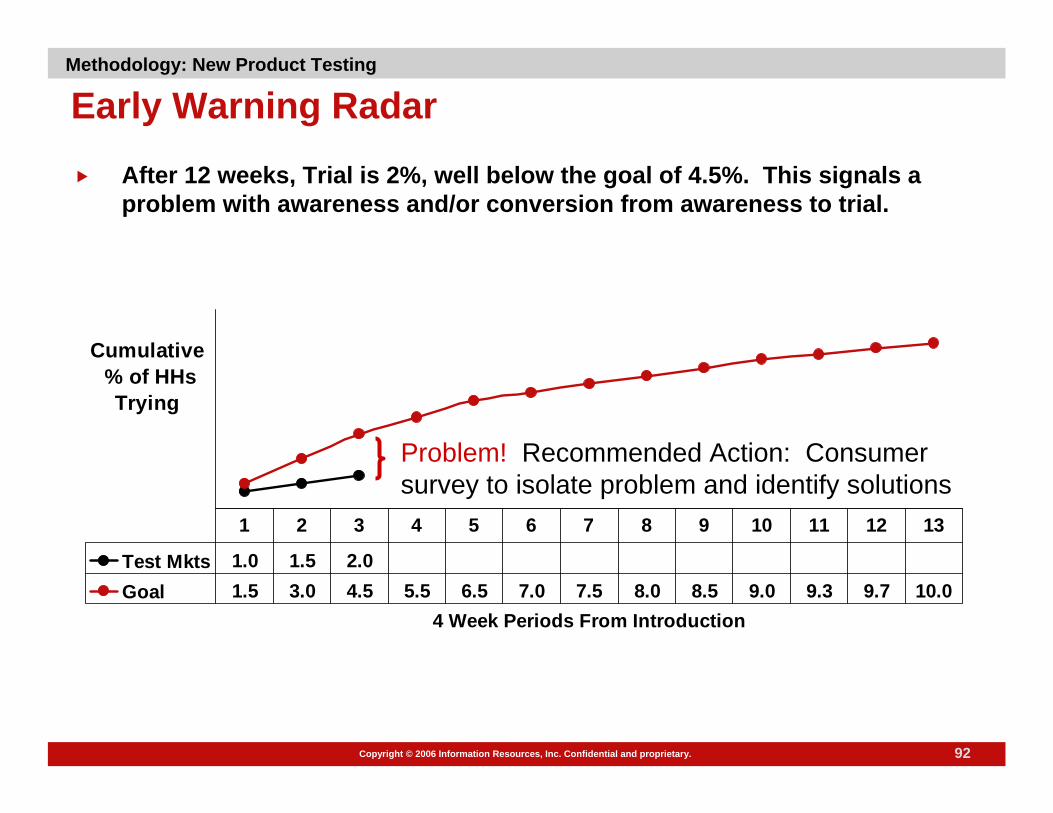

Early Warning Radar

After 12 weeks, Trial is 2%, well below the goal of 4.5%. This signals a problem with awareness and/or conversion from awareness to trial.

Methodology: New Product Testing

Cumulative % of HHs

Trying

4 Week Periods From Introduction

Test Mkts 1.0 1.5 2.0Goal 1.5 3.0 4.5 5.5 6.5 7.0 7.5 8.0 8.5 9.0 9.3 9.7 10.0

1 2 3 4 5 6 7 8 9 10 11 12 13

Problem! Recommended Action: Consumer survey to isolate problem and identify solutions

93Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Estimate “National Year-One” Sales Potential

IntroCast Post-Launch

0 1 2 3 4 5 6 7 8 9 10 11 12 134 week periods from introduction

Year OneVolume Sales (MM)

ForecastActualActual

Varianceto Goal

Methodology: New Product Testing

94Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

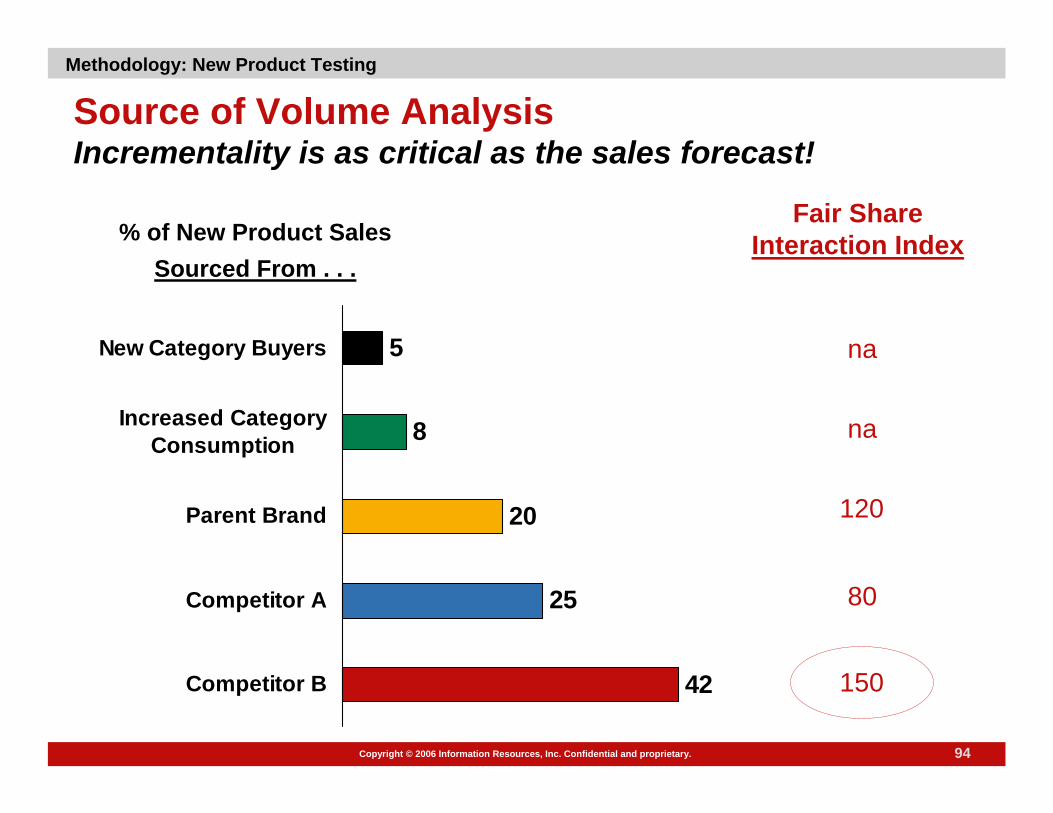

Source of Volume Analysis Incrementality is as critical as the sales forecast!

Methodology: New Product Testing

Fair Share Interaction Index

na

na

120

80

150

% of New Product Sales Sourced From . . .

42

25

20

8

5

Competitor B

Competitor A

Parent Brand

Increased CategoryConsumption

New Category Buyers

95Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

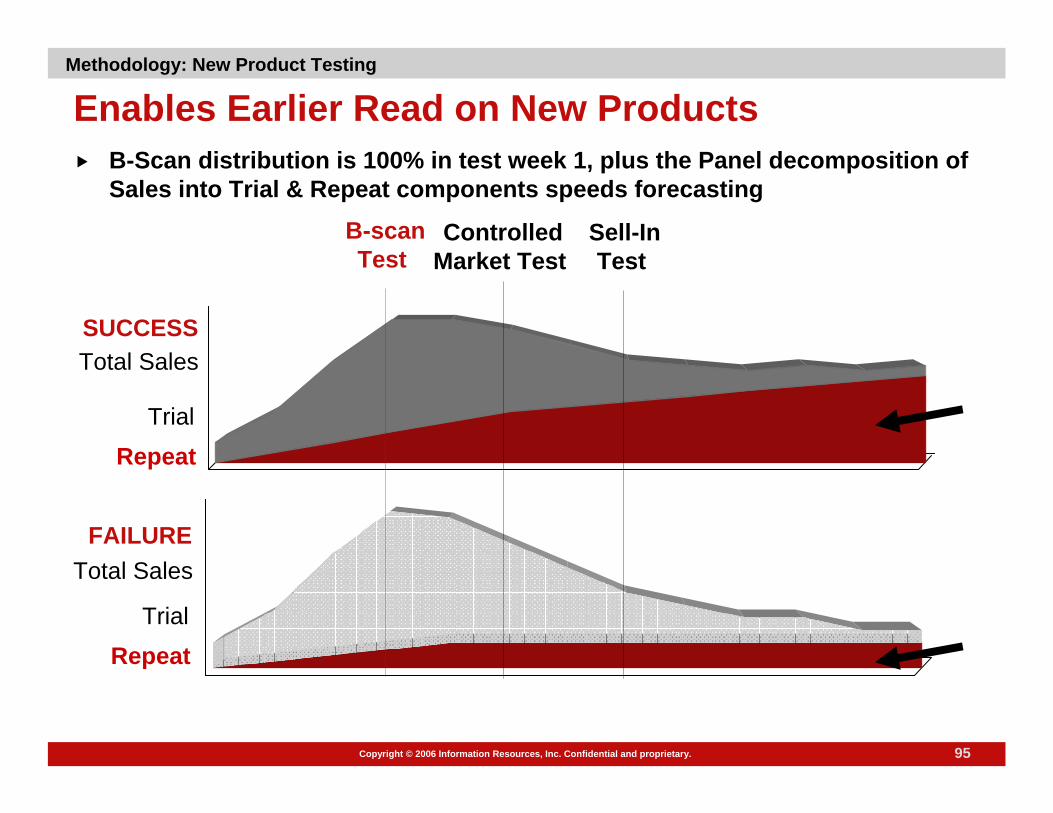

Enables Earlier Read on New ProductsB-Scan distribution is 100% in test week 1, plus the Panel decomposition of Sales into Trial & Repeat components speeds forecasting

B-scanTest

ControlledMarket Test

Sell-InTest

SUCCESSTotal Sales

Trial

Repeat

FAILURETotal Sales

Trial

Repeat

Methodology: New Product Testing

96Copyright © 2006 Information Resources, Inc. Confidential and proprietary.

Assess Performance vs. GoalsMethodology: New Product Testing

Total DollarSales ($MM)

% of HHs Trial % of TriersRepeating

AdditionalRepeaters

AvgVol/Occasion

GoalForcast

Critical Success Factors

40

8

35

1.1

12

50

8

35

2.1

12

+20% +20% Over Over Goal!Goal!