bell ringer see “money creation” video. money creation chapter 33

TRANSCRIPT

Bell Ringer

• See “Money Creation” Video

Money Creation

Chapter 33

Goldsmiths and Fractional Reserve Banking

• Traders used gold to make transactions until they realized it was too difficult to use

• They began depositing their gold with the Goldsmiths who would give them a receipt for the deposit and charge them a fee for the service

• Eventually, the goldsmiths' receipts were used to pay for goods, and became the first type of currency

• At this time, goldsmiths backed their circulating paper money receipts fully with the gold they held in their vaults (it was a 100% reserve system)

• Goldsmiths realized that the public had completely accepted the receipts as paper money– The amount of gold being deposited in their "reserves" exceeded

the amount that was being withdrawn.

Goldsmiths and Fractional Reserve Banking

• The goldsmiths began to issue paper receipts in excess of the amount of gold being held in their vaults

• They put these receipts into circulation by making interest-earning loans to merchants, producers and consumers

• Lenders willingly accepted loans in the form of gold receipts (receipts were accepted as a medium of exchange in the market).

• The goldsmiths began the fractional reserve system of banking– the reserves in bank vaults are a fraction of the total

money supply just as the gold reserves were a fraction of the circulating paper money back then

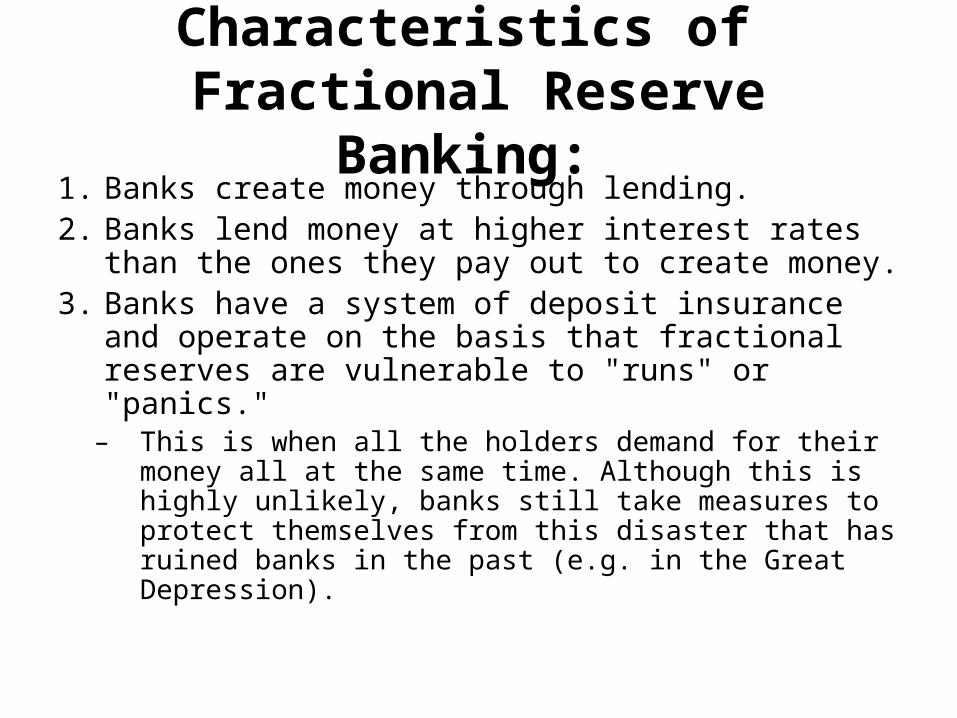

Characteristics of Fractional Reserve Banking:

1. Banks create money through lending. 2. Banks lend money at higher interest rates than

the ones they pay out to create money. 3. Banks have a system of deposit insurance and

operate on the basis that fractional reserves are vulnerable to "runs" or "panics."

– This is when all the holders demand for their money all at the same time. Although this is highly unlikely, banks still take measures to protect themselves from this disaster that has ruined banks in the past (e.g. in the Great Depression).

A Single Commercial Bank• Balance sheet is a statement of assets, liabilities, and net

worth (capital stock) of the bank at a certain time– value of assets must equal the amount of claims against the

assets• When federal reserve ratios change, the balance sheet for

banks is skewed– they must recall loans (make your repay right then) and/or take

out loans to balance their accounts• Assets = liabilities + net worth

– Every $1 change in assets must equal a $1 change in liabilities and net worth (and vise versa)

• Vault cash = cash held by a bank (money you can withdraw)

Bank’s Balance Sheet• Typical items on Bank of America’s balance

sheet– Checking Deposits (D) $100 million– Bonds (US gov’t securities) $19 million– Loans (L) $70 million– Reserves (R) $11 million

• What are reserves?– deposits that banks are required to hold on to plus any

additional cash they do not loan out (excess reserves)

Bank’s Balance SheetBank of America’s Balance sheet

Assets Liabilities and Net Worth

Checkable Deposits $100 millionBonds $19 million

Loans $70 million

Reserves $11 million

Total: $100 million in Assets Total: $100 million in Liabilities and Net Worth

Reserves and excess reserves• Excess reserves

= Total Reserves minus Required Reserves

• Loans are made out of excess reserves–Banks give loans because loans earn a profit (interest) while excess reserves earn nothing

• Think of your own money—if you put it in your checking account or in your sock drawer it doesn’t make money but if you put it in savings it does

• Loaned up–When excess reserves = 0, the bank is “loaned up” or “fully loaned” and can’t make any new loans

Profits, Liquidity, and the Federal Funds Market

• Bank has two conflicting goals: – Earn profit by making loans and buying securities – Balance liquid assets and excess reserves; therefore, must

restrict lending • When banks lend temporary excess reserves held at the

Federal Reserve Banks to other commercial banks, it achieves the two conflicting goals because first it is earning a profit from the interest and second it is a transaction of excess reserves, which preserves the reserve requirement

• If banks don't have enough excess reserves at the end of the day to fulfill the 10% requirement (in the US) set by the Fed, they must borrow from other banks in order to keep at least 10% of their total checkable deposits. They can also borrow from the Fed, but that's usually a last resort.

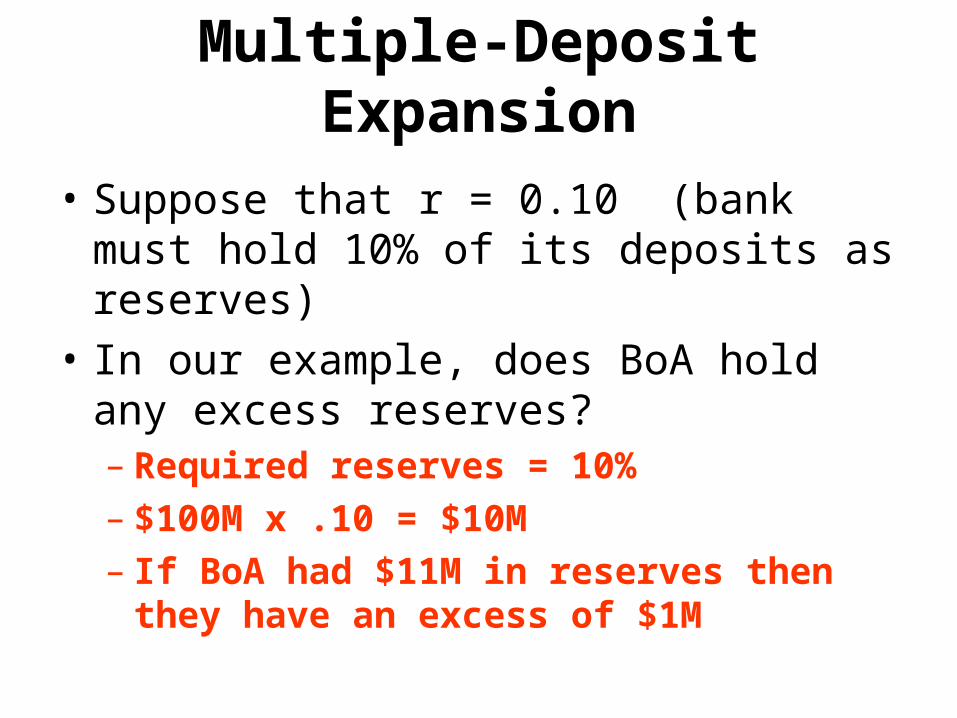

Multiple-Deposit Expansion

• Suppose that r = 0.10 (bank must hold 10% of its deposits as reserves)

• In our example, does BoA hold any excess reserves?– Required reserves = 10% – $100M x .10 = $10M– If BoA had $11M in reserves then they

have an excess of $1M

Multiple-Deposit Expansion

• What to do with excess reserves?– BoA loans Proctor and Gamble $1M

to buy computers

– Proctor and Gamble gives loan check to Dell

– Dell deposits the check into Wells Fargo

Multiple-Deposit Expansion

Changes in balance sheets

BoA Bank

Assets Liabilities

Wells Fargo Bank

Assets Liabilities

R - $1ML + $1M

R + $1M D - $ 1M

Notice that their assets total stays the same

Notice that they now have $1M in reserves they did not have before

Multiple-Deposit Expansion

• Did deposits rise? Did deposits fall?

• Deposits rose by $1M at Wells Fargo but stayed the same at BoA– meaning M1 rose $1M

Multiple-Deposit Expansion

• Not the end of the story...........

• Does Wells Fargo now have any excess reserves?– Required reserves = .10 (1M) = $100K– Excess reserves = 1M – 100K = $900K

Multiple-Deposit Expansion

• What to do with excess reserves?• Wells Fargo loans South Lake

Hospital $900K for an addition– South Lake Hospital gives loan check to

Marbek Construction– Marbek Construction deposits the check in

SunTrust

Multiple-Deposit Expansion

Changes in balance sheets

Wells Fargo Bank

Assets Liabilities

SunTrust Bank Assets Liabilities

D + $900KR + $900K

R - $900KL + $900K

Multiple-Deposit Expansion

Did deposits rise? Did deposits fall?

• Deposits rose by another $900K but did not fall in any other bank

• M1 rose $900K on this transaction• M1 has risen $1.9M ($1M + $900K) when

combining the two transactions together

Multiple-Deposit Expansion

• Not the end of the story...........

• Does SunTrust now have any excess reserves?

• Required reserves = .1 (900K) = $90K

• Excess reserves = $900K-90K = 810K– YES, SunTrust has excess reserves of

$810K

Multiple-Deposit Expansion

• Process continues over, and over, and over, and over (we could do this all day…but it’s boring)

• So—let’s use a shortcut to figure out the maximum change in the money supply

• The maximum change in money supply = the Money Multiplier (1/r) x initial excess reserves

Money Multiplier• In our example, what is the maximum

change in the money supply?• Money multiplier = 1/r = 1/.10 = 10• Initial excess reserves = $1M (BoA)• Maximum change in money supply = 10 x (+ $1M) = + $10M• Off of BoA’s $1M excess reserve loan the

economy has grown by $10M

Money Multiplier

• When the reserve ratio changes because of the monetary policy, the money multiplier also changes. – As Reserve Ratio increases, Money Multiplier

decreases – As Reserve Ratio decreases, Money

Multiplier increases

Your Turn!

• Complete the “Where did that money come from?” worksheet provided