benefits enrollment guide 2018 - bank of america · evaluate your benefit options. review your...

TRANSCRIPT

It’s time to choose the benefit options that fit your life

2018Benefits Enrollment Guide

At Bank of America, we believe that employees are the foundation of our success

To support you during the moments that matter most, we offer a wide range of

benefits, programs and resources that are competitive, diverse and flexible to meet

your needs. It’s one of the most important things we do as a company, and part of

our commitment to making Bank of America a great place to work.

We offer a variety of health and insurance benefits to meet your needs

This enrollment guide is designed to help you understand the comprehensive

medical, prescription, dental and vision coverage available for you and your

family. You’ll also learn about the available life and disability insurance options,

including what’s provided automatically by the bank.

You’ll see that wellness is a key component of our medical plans, as we’re committed

to helping you learn more about your health and save money in the long run. You can

keep a credit toward your annual medical premium by completing two voluntary

wellness activities, and you’ll have access to personal health coaches and nurses to

help you improve your health, manage chronic conditions and more.

2018 Benefits | About this guide 1

Benefits that work for your life

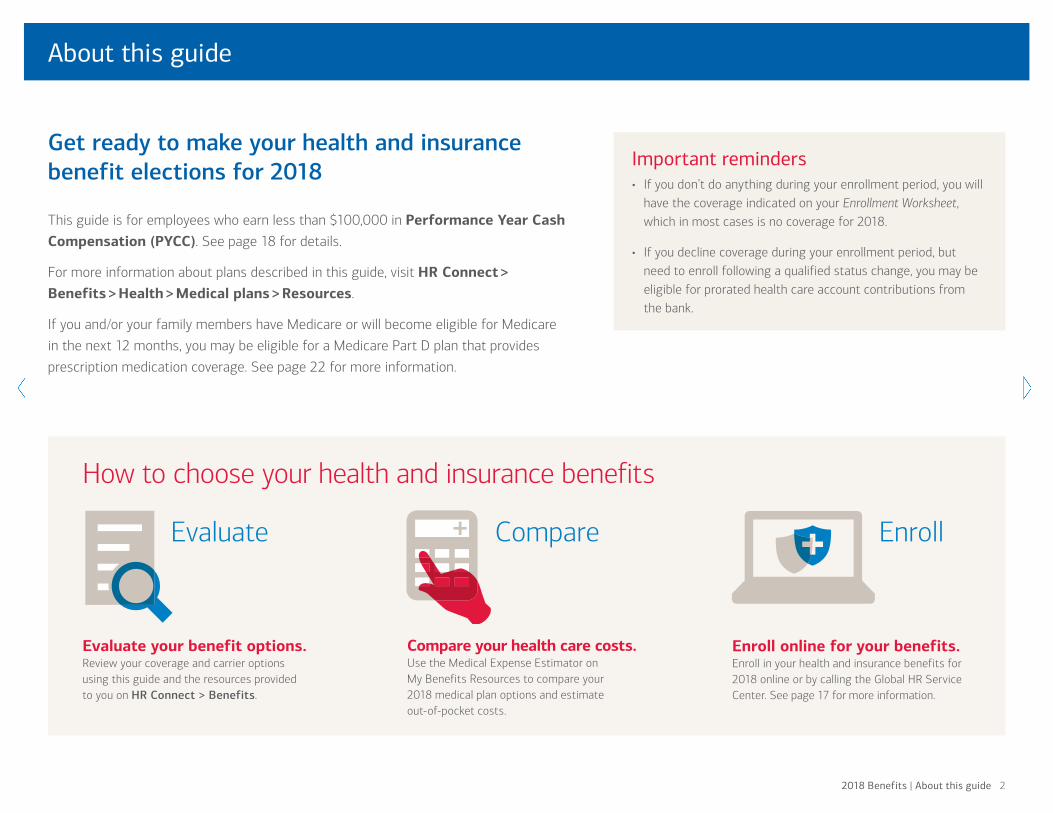

Get ready to make your health and insurance benefit elections for 2018

This guide is for employees who earn less than $100,000 in Performance Year Cash Compensation (PYCC). See page 18 for details.

For more information about plans described in this guide, visit HR Connect > Benefits > Health > Medical plans > Resources.

If you and/or your family members have Medicare or will become eligible for Medicare

in the next 12 months, you may be eligible for a Medicare Part D plan that provides

prescription medication coverage. See page 22 for more information.

How to choose your health and insurance benefits

Evaluate EnrollCompare

Evaluate your benefit options. Review your coverage and carrier options using this guide and the resources provided to you on HR Connect > Benefits.

Compare your health care costs. Use the Medical Expense Estimator on My Benefits Resources to compare your 2018 medical plan options and estimate out-of-pocket costs.

Enroll online for your benefits. Enroll in your health and insurance benefits for 2018 online or by calling the Global HR Service Center. See page 17 for more information.

Important reminders• If you don’t do anything during your enrollment period, you will

have the coverage indicated on your Enrollment Worksheet, which in most cases is no coverage for 2018.

• If you decline coverage during your enrollment period, but need to enroll following a qualified status change, you may be eligible for prorated health care account contributions from the bank.

2018 Benefits | About this guide 2

About this guide

Review

2018 Benefits | Review 3

What to consider during your enrollment period

When choosing your health and insurance coverage for 2018, review the benefit options available to you and make the elections that are right for you and your family.

Medical, dental and vision questions

■Which medical plan will work best for you and

your family?

■Which medical carrier fits your needs?

■Do you want to enroll in dental or vision plans?

Insurance and disability question

■If something were to happen to you and your

income was lost, do you have enough life and

disability insurance to take care of your family?

Family care question

■Do you have a total household adjusted gross

income of $100,000 or less and expect to

have child care expenses that could be

reimbursed by Child Care Plus®?

Important reminder questions

■Do you need to add beneficiary designations

for your life insurance and Health Savings

Account (HSA), if applicable?

■Do you need to cover eligible family members

under your health or insurance benefits?

Remember, if you cover a child who is turning

26 in 2018, coverage under your plan will end

at the close of his or her birthday month.

■If the health care account that works with

your chosen medical plan allows employee

contributions, how much do you want

to contribute?Save up to $1,000!Complete the bank’s voluntary wellness activities and you can keep a $500 credit toward your annual medical plan premium. You’ll keep an additional $500 if your covered spouse or partner also completes theirs. If your benefits coverage begins after Jan. 1, we’ll prorate the credit based on when your medical plan coverage takes effect. See page 16 for details.

Have questions?

Financial counselors at the Benefits Education & Planning Center (BEPC) can help answer

questions you may have on the topics covered in

this guide.

Call 866.777.8187 Monday through Friday, 9 a.m.

to 8 p.m. Eastern (excluding certain holidays).

To help you compare your medical, dental and

vision plan choices, access the compare tool

available on My Benefits Resources (mybenefitsresources.bankofamerica.com).

What’s inside this guide

Medical 5

Health care accounts 9

Dental 11

Vision 12

Life and disability insurance 13

Family care and other benefits 15

Wellness 16

When and how to enroll 17

Important notes about your benefits 18

Helpful contact information 25

5

Table of contents

2018 Benefits | Table of contents 4

You have two medical choices to make during your enrollment period: your medical carrier and your medical plan

All our national medical carriers offer the same medical plans and are

high-quality options with similar services and networks. (We also offer

Kaiser Permanente as a carrier in select markets. Please refer to the

Compare Medical Plan Details feature on My Benefits Resources

for specific Kaiser plan information.)

Your medical premiums will be based on your pay tier, the plan

you choose, the number of people you cover, the carrier you

select, the ZIP code you live in and whether or not you complete

wellness activities or use tobacco.

We’ve designed our medical plans to meet the diverse needs of our employees

We offer medical plans that provide quality health care and

100% coverage for in-network preventive care. Each plan has

the predictability of an annual deductible and the security of an

out-of-pocket maximum. The medical plan you choose determines:

• The amount of coverage you receive

• When you pay for care. (For example, with the Comprehensive

PPO, you’ll pay more every pay period than you would in either

of the consumer-directed plans. With the consumer-directed

plans, you have lower per-pay-period costs and pay more when

you receive care.)

• The type of health care account(s) available to you

• Your prescription drug coverage

medical plan

medical carrier

Aetna

Comprehensive PPO plan

Consumer directed high

deductible plan

Consumer directed plan

Anthem

Kaiser Permanente (in select markets)

UnitedHealthcare

2018 Benefits | Medical 5

What comes out of my pay?

Annual premium

The annual cost to pay for medical coverage is

spread across the year, so you pay a portion of it

in each pay period on a pretax basis. Medical

premiums are based on your pay tier, the plan you

choose, the number of people you cover, the

carrier you select, the ZIP code you live in and

whether or not you’ve completed wellness

activities or use tobacco.

What will I pay when I begin receiving medical care?

Annual deductible

You won’t pay for in-network preventive care

defined by the U.S. Preventive Services Task

Force, such as your annual checkup. Confirm with

your carrier which services are considered

preventive. Generally, for all other covered care,

you’ll pay out-of-pocket until you reach your

annual deductible, at which point your medical

plan will start to pay for the majority of your

in-network services.

What will I pay after I meet my annual deductible?

Coinsurance

After you meet the annual deductible, generally,

you’ll continue to pay 20% of the cost for

in-network covered medical services until you

meet the out-of-pocket maximum. The plan

pays the rest.

What does it mean to stay in network?

In network vs. out of network

In-network providers have agreed to your carrier’s

negotiated rates. An out-of-network provider may

charge more than the carrier is willing to pay.

Because of this, you have an out-of-network

deductible that is higher than your in-network

deductible. Check with your carrier to be sure

doctors, labs, hospitals and specialists are in

network before receiving treatment.

What’s the most I’d have to pay out of my own pocket?

Out-of-pocket maximum

Each plan has a pre-determined out-of-pocket

maximum that’s the most you’d pay for covered

medical services in a calendar year. Once you

meet it, the plan pays the full cost of additional

covered expenses. Think of it as your safety net.

How is my annual premium determined?

PYCC

Your premiums for medical coverage are

determined by tiers based on your Performance

Year Cash Compensation (PYCC). See page 18

for more information.

Those pay tiers are:

• Less than $50,000 PYCC

• $50,000 to less than $100,000 PYCC

• $100,000 to less than $150,000 PYCC

• $150,000 to less than $250,000 PYCC

• $250,000 to less than $500,000 PYCC

• $500,000 PYCC or more

2018 Benefits | Medical 6

2018 Benefits | Medical 7

Comprehensive PPO or Consumer Directed Plan

Consumer Directed High Deductible Plan*

Here’s how deductibles and out-of-pocket maximums for employees with family coverage compare across plans

Annual deductible/coinsurance

• For any family member whose eligible out-of-pocket expenses meet his or her individual annual deductible, coinsurance begins for that person.

• Coinsurance begins for everyone covered by the plan once the eligible out-of-pocket expenses of two people combine to meet the family deductible.

Out-of-pocket maximum

100% of eligible costs are covered:

• For any family member who reaches his or her individual out-of-pocket maximum

• For everyone on the plan once two people combine to reach the out-of-pocket maximum

Annual deductible/coinsurance

• If anyone covered on the plan meets the family annual deductible, or the eligible out-of-pocket expenses of two or more family members combine to reach it, coinsurance begins for everyone on the plan.

Out-of-pocket maximum

• The in-network, out-of-pocket maximum for this plan is $8,000 per family.

• If one person covered under the plan reaches the individual out-of-pocket maximum of $7,350, 100% of additional costs for eligible services are covered for that person.

• If another family member adds $650 (for a total of $8,000) in eligible out-of-pocket expenses, 100% of additional costs for covered services for everyone on the plan are covered.

* Kaiser California plans have a different deductible and out-of-pocket maximum for employees choosing family coverage. Please contact Kaiser for further information.

During your benefits enrollment period, you can add a spouse, partner, adult dependent or eligible child to your coverage

If you add an adult to your coverage, you’ll be required to verify his or her eligibility. You’ll receive a Dependent Verification letter at your address on file with more information about deadlines and the documents required to verify the eligibility of your adult family member.

Some of your benefits, including when bank contributions to your health care account are available, may be affected if there’s a delay verifying the eligibility of your adult family member. If you don’t provide all the required documentation by the deadline provided to you, the individual will be dropped from your health and insurance coverage. This means the individual will no longer be covered under the plans you elected during enrollment.

TIPDon’t forget to take a look at the Medical Expense Estimator on My Benefits Resources to compare your medical plan options, premiums and estimated out-of-pocket costs across the plans and carriers.

Important remindersIf you get married, have a baby, get a divorce or experience another event that is considered a qualified status change, you must notify the Global HR Service Center within 31 calendar days of the date of the change. For more information about who’s eligible for coverage under the plans, see page 19.

Your children are eligible to be covered under your medical, dental and vision plans until age 26. Note: If your child will turn 26 in 2018 and is covered under your plan, his or her coverage will end on the last day of his or her birthday month.

Comprehensive PPO Plan Consumer Directed Plan Consumer Directed High Deductible Plan

Annual deductible

In network, you pay up to $500 per individual or $1,000 per family.

Out of network, you pay up to $1,000 per individual or $2,000 per family.

In network, you pay up to $1,200 per individual or $2,400 per family.

Out of network, you pay up to $2,400 per individual or $4,800 per family.

In network, you pay up to $2,250 per individual or $4,500 per family.

Out of network, you pay up to $4,500 per individual or $9,000 per family.

Coinsurance

In network, you pay 20%.

Out of network, you pay 40%.

In network, you pay 20%.

Out of network, you pay 40%.

In network, you pay 20%.

Out of network, you pay 40%.

Out-of-pocket maximum

In network, you will pay no more than $2,000 per individual or $4,000 per family.

Out of network, you will pay no more than $4,000 per individual or $8,000 per family.

In network, you will pay no more than $3,500 per individual or $7,000 per family.

Out of network, you will pay no more than $7,000 per individual or $14,000 per family.

In network, you will pay no more than $4,000 per employee only, $7,350 per individual or up to $8,000 per family.

Out of network, you will pay no more than $8,000 per employee only or $16,000 per family.

Preventive services

In network, you pay $0, according to government guidelines.

Out of network, you pay the full negotiated rate until you meet the deductible, then you pay coinsurance.

In network, you pay $0, according to government guidelines.

Out of network, you pay the full negotiated rate until you meet the deductible, then you pay coinsurance.

In network, you pay $0, according to government guidelines.

Out of network, you pay the full negotiated rate until you meet the deductible, then you pay coinsurance.

Office visits

In network, you pay a $15 copayment for primary care and a $25 copayment for a specialist visit.

Out of network, you pay the full negotiated rate until you meet the annual deductible, then you pay coinsurance.

You pay the full negotiated rate until you meet the annual deductible, then you pay coinsurance.

You pay the full negotiated rate until you meet the annual deductible, then you pay coinsurance.

Prescription medication at retail

(30-day supply)

In network, you pay Generic: $5 copayment Preferred brand: $25 copayment Non-preferred brand: $50 copayment

Out of network, you pay 40% coinsurance.

In network, you pay Generic: $5 copayment Preferred brand: 30% coinsurance ($100 max) Non-preferred brand: 45% coinsurance ($150 max)

Out of network, you pay 40% coinsurance.

In-network preventive medication: You pay 20% coinsurance prior to reaching your deductible.In-network non-preventive medication: You pay the full negotiated price until you meet the annual deductible, then you pay 20% coinsurance.Out-of-network medication: You pay 40% coinsurance.

Health care account(s)(More details on page 10)

Health Flexible Spending Account (Health FSA) Health Reimbursement Arrangement (HRA) Health Flexible Spending Account (Health FSA)

Health Savings Account (HSA)Limited Purpose Flexible Spending Account (Limited Purpose FSA)

2018 Benefits | Medical 8

It pays to stay in network!During your benefits enrollment period, carefully consider your medical plan elections and ensure your preferred providers are in network to avoid additional costs later. Find out if your doctors are in network across the carriers by going to My Benefits Resources and using the Find Doctors and Facilities link available on the medical and dental election pages.

Health care accounts can help offset your out-of-pocket medical expenses, such as copayments, prescription medications, eyeglasses and lab work

The amount the bank will contribute to your health care account is based on your

PYCC (see page 18) and the family members you cover. Depending on the type

of health care account that is paired with your medical plan, you and the

bank may be able to contribute to the account.

If you remain eligible, any health care account contributions you

receive from the bank will not change in 2018, even if you have a

qualified status change that changes the number of people you

cover under a medical plan.

NoteBe aware that the IRS prohibits you from making or receiving contributions to an HSA while enrolled in Medicare or a Medicare Advantage plan. While contributions to an HSA aren’t allowed once enrolled in Medicare, you can still use any existing HSA balance to pay for eligible health care expenses now or in future years.

2018 Benefits | Health care accounts 9

TIPIf you have selected a Consumer Directed medical plan with the Health Reimbursement Arrangement (HRA), remember that only your eligible expenses and those of your dependents who are also covered under the same Bank of America medical plan are eligible for reimbursement from the HRA.

Health Flexible Spending Account (Health FSA) Health Reimbursement Arrangement (HRA)

Health Savings Account (HSA) Limited Purpose Flexible Spending Account (Limited Purpose FSA)

Which plan(s) is this account available for?

Comprehensive PPOConsumer Directed Plan

You don’t need to be enrolled in a medical plan in order to contribute to a Health FSA.

Consumer Directed Plan Consumer Directed High Deductible Plan Consumer Directed High Deductible Plan

What would I use this account for?

Eligible health care expenses, including dental, vision and prescription medication expenses

Eligible health care expenses, including dental, vision and prescription medication expenses

To save for future health care expenses, but also to pay for eligible health care expenses, including dental, vision and prescription medication expenses

This health care account is only available if you have an HSA, and you can only use it for eligible vision and dental expenses.

What is the maximum amount that the bank and I combined can contribute to this account?

$2,650, the IRS pretax contribution limit Employee contributions may not be made to an HRA.

$3,450 Employee-only coverage$6,900 Family coverageIf you’ll be at least 55 years old in 2018, you can make an additional $1,000 catch-up contribution.

$2,650, the IRS pretax contribution limit

What does the company contribute?

The bank does not contribute to this account. PYCC is less than $50K$500 Employee-only coverage$750 Employee plus spouse/partner OR

Employee plus child(ren) coverage$1,000 Family coverage

PYCC is $50K to less than $100K$400 Employee-only coverage$600 Employee plus spouse/partner OR

Employee plus child(ren) coverage$800 Family coverage

PYCC is less than $50K$500 Employee-only coverage$750 Employee plus spouse/partner OR

Employee plus child(ren) coverage$1,000 Family coverage

PYCC is $50K to less than $100K$400 Employee-only coverage$600 Employee plus spouse/partner OR

Employee plus child(ren) coverage$800 Family coverage

The bank does not contribute to this account.

When are the funds available?

Your entire contribution amount is available at the beginning of the year.

The entire bank contribution amount is available at the beginning of the year.

Your contribution amount is available as it comes out of your paycheck each pay period — so your entire contribution amount is not available at the beginning of the year.

The entire bank contribution is available at the beginning of the year.

Your entire contribution amount is available at the beginning of the year.

What happens if I don’t use the money during the year?

Up to $500 in unused funds will roll over automatically to your 2019 Health FSA.

All unused funds will automatically roll over to your 2019 HRA, and you will generally have access to the funds as long as you stay enrolled in a medical plan that works with the HRA. Please note that if you leave the bank with a balance and have not met the Rule of 60, it will be forfeited. See page 19 for more information.

All unused funds will remain in your HSA (which is available to you after 2018). Also, if you have more than $1,000 in your HSA, you can invest it, and any earnings are generally tax free. You can take HSA funds with you when you leave the company or retire.

Up to $500 in unused funds will roll over automatically to pay for eligible expenses in the following year.

2018 Benefits | Health care accounts 10

MetLife is the carrier for our Dental PPO Plan

Visit metlife.com/mybenefits to see if your dentist is in network for the MetLife Dental PPO Plan.

In select markets, the Aetna Dental DMO Plan is available. Visit aetna.com/bankofamerica to check if your dentist is in the Aetna DMO network. If you choose this plan, your primary care dentist must be in the Aetna DMO network and accepting new DMO patients in order for you to receive any coverage. Be sure to confirm this before you elect this plan.

Out-of-network coverage

A dentist who is “out of network” hasn’t agreed to negotiated rates. The MetLife Dental PPO Plan pays benefits based on the usual and customary charge for a particular service. If the out-of-network provider charges more, you’ll be responsible for paying the amount that exceeds the usual and customary limit plus the applicable coinsurance and deductible. Aetna DMO does not have out-of-network coverage; therefore, services received from a provider who is not in the Aetna DMO network will not be covered.

* The coverage and lifetime maximum for implants and adult orthodontics apply only to those services or the placement of braces that will occur on or after Jan. 1, 2018. Treatment that began before this time will be subject to the original terms and conditions.

MetLife Dental PPO (in network) Aetna DMO (select markets, in network)

General dental expenses

Annual deductible $50 individual, $150 family The deductible is waived for preventive/diagnostic care and applies to basic and major expenses.Annual maximum coverage per person (excludes orthodontia and preventive care services) $2,000Lifetime maximum for orthodontia* (covered adults and children starting treatment before age 20) $2,000Office visit copayment None

Annual deductible None

Annual maximum coverage per person (excludes orthodontia) There is no annual maximum.

Lifetime maximum for orthodontia* (covered adults and children starting treatment before age 20) 24 months active treatment plus 24 months retention per lifetimeOffice visit copayment $5 per visit

Preventive care

Exams Plan pays 100% of covered services; services do not count toward annual maximum. Limited to two routine visits and two problem-focused visits per calendar year.Cleaning Plan pays 100% of covered services; services do not count toward annual maximum. Limited to two visits per calendar year.Dental X-rays Plan pays 100% of covered X-rays; services do not count toward annual maximum. Limited to one set of full mouth series every five years, and two sets of bitewing X-rays per calendar year for children and one set per calendar year for adults.

Exams Plan pays 100% of covered services, limited to four visits per calendar year.Cleaning Plan pays 100% of covered services, limited to two visits per calendar year.Dental X-rays Plan pays 100% of covered X-rays; services do not count toward the annual maximum. Limited to one set of full mouth series every five years, and two sets of bitewing X-rays per calendar year for children and one set per calendar year for adults.

Services Amalgam (silver) fillings You pay 20% of covered services.Composite fillings You pay 20% of covered services; limitations may apply.Extractions You pay 20% of covered services.Crowns, Dentures & Bridges You pay 50% of covered services; each individual service is limited to one time, per person, every seven years.Implants* You pay 50% of covered services.Oral surgery You pay 20% of covered services.Orthodontia* (adults and children) You pay 50% of covered services.

Amalgam (silver) fillings You pay 20% of covered services.Composite fillings You pay 20% of covered services; limitations may apply.Extractions You pay 20% of covered services; uncomplicated, non-bony impactions.Crowns, Dentures & Bridges You pay 50% of covered services; crowns & dentures limited to initial placement and replacements for appliances that are seven years old or more; bridges limited to initial placement only. Replacements for bridge appliances that are seven years old or more are considered.Implants* You pay 50% of covered services.Oral surgery You pay 20% of covered services for basic surgery; 50% of covered major surgery.Orthodontia* (adults and children) You pay 50% of covered services.

2018 Benefits | Dental 11

TIPThose who have Aetna as their medical carrier automatically have access at no cost to the Aetna Vision Discount Program as an alternative to the vision plan under Aetna or VSP. This program offers discounts for routine eye exams, eyeglasses, LASIK surgery, contact lenses and other eye care accessories. For more information, call Aetna at 877.444.1012 or refer to the 2016 Summary Plan Description (SPD) and subsequent Summaries of Material Modifications (SMMs) on HR Connect > Benefits > Health > Medical plans > Resources.

We offer two options for vision coverage: Aetna and VSP

Visit aetna.com/bankofamerica or vsp.com/bankofamerica to see if your eye care provider is in network.

Aetna VSP

In network Out of network In network Out of network

Routine vision exams (once per calendar year)

$10 copayment Plan pays a reimbursement, up to $40.

$10 copayment Plan pays a reimbursement, up to $45.

Eyeglasses Single vision lenses

(once per calendar year)Plan pays 100% of covered services, limited to standard uncoated plastic lenses.

Plan pays a reimbursement, up to $40.

Plan pays 100% of covered services. Plan pays a reimbursement, up to $40.

Bifocal lenses (once per calendar year)

Plan pays 100% of covered services for standard uncoated plastic lenses.

Plan pays a reimbursement, up to $60.

Plan pays 100% of covered services for lined bifocals.

Plan pays a reimbursement, up to $60.

Frame allowance (once every other calendar year)

Plan provides a $130 frame allowance, 20% discount thereafter.

Plan pays a reimbursement, up to $50.

Plan provides a $130 frame allowance ($150 for select brands), 20% discount thereafter; $70 allowance at Costco and Walmart.

Plan pays a reimbursement, up to $54.

Contact lenses Standard lens fit and follow-up (once per calendar year)

$0 copayment Plan pays a reimbursement, up to $40.

$30 copayment Cost is included in $125 contact lens allowance.

Premium contact fit and follow-up (once per calendar year)

Plan provides up to a $55 allowance, 10% discount thereafter.

Not covered $30 copayment Cost is included in $125 contact lens allowance.

Medically necessary prescription lenses for specific eye conditions that would prohibit the use of glasses (once per calendar year; prior approval is needed)

Plan pays 100% of covered services. Plan pays a reimbursement, up to $210.

Plan pays 100% of covered services. Plan pays a reimbursement, up to $210.

Elective prescription lenses (once per calendar year)

Plan provides a $125 allowance in lieu of eyeglasses; a 15% discount is applied to conventional contacts over the $125 allowance.

Plan provides a $125 allowance in lieu of eyeglasses.

Plan provides a $125 allowance in lieu of eyeglasses.

Plan provides a $125 allowance in lieu of eyeglasses.

2018 Benefits | Vision 12

Associate life insurance

Short- and long-term disability insurance

Business travel accident insurance

Our company-paid associate life insurance is provided by MetLife.

Annual base pay (or ABBR) x 1Rounded up to the next $1,000, up to a maximum of $2 millionSee information about ABBR on page 18.

The company provides you with: • Short-term disability benefits for up to 26 weeks

from the date of your disability after you’ve worked one continuous year

• Long-term disability benefits if you are unable to work for an extended period of time due to a qualifying disability due to a sickness or as a result of an accidental injury

Short-term disability (STD)

100% / 70% weekly base pay1 (or ABBR)

One week notification period 100% for eight weeks (weeks 2–9) 70% for up to 17 additional weeks (weeks 10–26)

Long-term disability (LTD)

50% weekly base pay2 (or ABBR)

For full-time employees only. Part-time employees can purchase LTD coverage during their enrollment period on My Benefits Resources.

Business travel accident insurance protects you in the event of death or serious covered injury caused by an accident that occurs while traveling on business for the bank. Everyday commuting is excluded.

Annual base pay x 5Rounded up to the next $1,000, up to a maximum of $3 million

For family members who travel with you on an authorized trip or relocation, we provide:

$150,000 coverage for your spouse or partner

$50,000 coverage for each child

Life and disability insurance can provide income protection for you and your familyCore coverage: Bank of America provides these insurance benefits automatically at no cost to you.

Important considerationAsk yourself how much your family would need if you became unable to work due to an injury or disability. You may want to consider purchasing additional supplemental life and/or disability insurance. You can always call the BEPC to help you understand what you may need based on your situation. See page 4 for contact information.

TIPDuring your benefits enrollment period, ensure you’ve designated a beneficiary for all your insurance benefits.

1 Or current compensation2 Or current compensation prior to the date your LTD benefits

payments begin. See page 20 for more information. 2018 Benefits | Insurance options 13

Supplemental coverage: You can elect to purchase these additional insurance benefits for you and your family during your benefits enrollment period.

Long-term disability (LTD) insurance

You may elect to purchase additional LTD coverage on top of the LTD coverage provided by the bank on a post-tax basis, up to a maximum combined coverage amount of $360,000 per year ($30,000 a month). The premiums will be calculated based on:

60% annual base pay* (or ABBR)

60% eligible compensation(annual base pay* + eligible bonus) Note: ABBR employees are not eligible for the 60% eligible compensation option.

50% annual base pay* (part-time employees)

The amount of benefits you would receive while on LTD is based on your election and current compensation prior to the date your LTD benefit payments begin.

Accidental death and dismemberment (AD&D) insurance

You may elect additional financial protection in the event of a serious accidental injury or death on a pretax basis.

Eligible compensation x 1 – 8 (annual base pay + eligible bonus) or ABBR

up to a maximum of $3 million

Family accidental death and dismemberment (AD&D) insurance

You may also elect to purchase family AD&D coverage for your spouse or partner and children, so long as they are under age 65, not full-time military and more than seven days old. You pay for this coverage on a pretax basis.

You must have employee AD&D coverage to elect coverage for your dependents.

Spouse or partner

60% of your coverage amount, up to $600,000

Each child

20% of your coverage amount, up to $50,000

Associate supplemental life insurance

You may elect to purchase associate supplemental life insurance on a post-tax basis.

Eligible compensation x 1 – 8 (annual base pay + eligible bonus) or ABBR

Rounded up to the next $1,000, up to a maximum of $3 million

A Statement of Health may be required. See page 20 for more information.

Dependent life insurance

Dependent life insurance is paid for on a post-tax basis and assists you with the additional expenses you might have if your spouse or partner or child dies. You need to decide which coverage level, if any, is right for you.

A Statement of Health may be required. See page 20 for more information.

Spouse or partner life insurance Coverage options available:

$10,000$25,000$50,000

$75,000$100,000

$125,000 $150,000

Child life insurance Coverage options available:

$5,000/child$10,000/child

$15,000/child$20,000/child

$25,000/child

NoteEligible bonus does not include cash incentives, bonuses, relocation payments or similar compensation paid to employees from a non-U.S. payroll.

*Or current compensation prior to the date your LTD benefit payments begin. See page 20 for more information. 2018 Benefits | Insurance options 14

Benefits What we offer Who’s eligible Actions you can take

Dependent Care Flexible Spending Account (Dependent Care FSA)

• You can use pretax dollars to pay for eligible dependent care expenses, including:

– Adult day care centers

– Babysitters and nannies

– Summer day camps

• You can use this account for dependent care expenses incurred so you and your spouse or partner can work, or so your spouse or partner can attend school full time. If your spouse or partner stays home full time, you are not eligible for the tax benefit.

• Dependent Care FSA participants have the option of paying for eligible dependent care expenses that have already been incurred with a debit card, instead of paying out of pocket and filing for reimbursement.

• Employees with children under age 13 and anyone who is a dependent under IRS rules, or who is mentally or physically incapable of taking care of himself or herself are eligible.

• Employees in New Jersey and Pennsylvania can’t make pretax contributions, per state regulations.

• Employees in Puerto Rico, Guam and the U.S. Virgin Islands are not eligible.

• Employees scheduled to work less than 20 hours per week are not eligible.

• Contribute up to $5,000 per year to the account (or $2,500 if you are married and filing separate tax returns).

• Use your health account debit card to pay for eligible dependent care expenses at time of service. Or, opt to pay out-of-pocket and submit receipts online, via the Bank of America Online Portal, for reimbursement. Remember to keep your receipts regardless of how you choose to pay, in case you need to verify expense eligibility later.

• Keep track of your expenses through the year. Back-up care, child care reimbursements and Dependent Care FSA contributions in excess of $5,000 are considered taxable income.

Purchased time off (PTO)

• You may purchase time off from work above your annual vacation allotment.

• You can pay for a minimum of four whole hours and a maximum of your weekly scheduled hours (up to 40).

• All U.S.-based employees who are scheduled to work at least 20 hours per week, except those in bands 0–3, commissioned employees or employees working in Puerto Rico are eligible.

• Receive permission from your manager before you purchase time off.

• If your benefits coverage starts Jan. 1, 2018, you can purchase time off from work. If your coverage starts later, you can purchase time off during the next Annual Benefits Enrollment.

Prepaid Legal • For $14.50 per month, you have access to experienced attorneys for many personal legal services and unlimited advice through Hyatt Legal plans. Advice is available through the plan for:

– Wills

– Real estate matters

• Most network attorney fees are covered by the plan.

• Active, U.S.-based full- and part-time employees are eligible.

• Employees scheduled to work less than 20 hours per week are not eligible.

• You are only able to enroll in Prepaid Legal during your enrollment period and must remain in the plan for the calendar year.

We offer several family care and other benefit options for you and your family

Familiarize yourself with what’s available and the elections you can make during your benefits enrollment period.

Do you have child care expenses?If your total household adjusted gross income, as measured on your most recent federal tax return, is $100,000 or less, you may be eligible for child care reimbursements (up to $240 per month, per child) through Child Care Plus®. If you are eligible, you may enroll in Child Care Plus for 2018 during your benefits enrollment period or at any time throughout the year. You will be required to provide documentation validating your household income as well as your child’s eligibility. Information on the child care provider will be required when a request for reimbursement is made.

– Before- and after-school programs

– Child day care

– Small claims

– Family matters

2018 Benefits | Family care 15

Learn about the two wellness activities and how the $500 credit works.

When you’re ready to complete your wellness activities, log on to

My Benefits Resources and select the Wellness tab.

The results of the health screening and health questionnaire

won’t affect your per-pay-period costs, coverage or eligibility.

Bank of America will not have access to your individual results.

Focusing on wellness is an investment in your health, which can save you money in the long run

When you’re in good health and feel well, you can be your best at home and at work.

To help you better understand your health, take advantage of the voluntary wellness

activities — a health screening and health questionnaire. You’ll get to know your

numbers, and keep a $500 credit toward your annual medical plan premium (or a

$1,000 credit if your covered spouse or partner completes theirs as well).1

Once you know about your health, you can take advantage of the benefits and

programs available to support your wellness. You have access to:

• Free one-on-one health coach sessions

• Wellness challenges with your teammates

• Programs that can help you quit using tobacco

• A hypertension management program to help you manage your blood pressure2

2. Complete your health questionnaireThe online questionnaire takes just a few minutes and

measures your overall health and lifestyle risks.

1. Complete your health screening It includes height, weight, waist, blood pressure and

total cholesterol measurements.

$500 + $500 = $1,000You complete and submit both wellness activities

Your spouse or partner completes and submits both wellness activities

Total credit to your annual medical plan premium

1 If your benefits coverage begins after Jan. 1, we’ll prorate the credit based on when your medical plan coverage takes effect. If you and your spouse or partner choose not to complete the wellness activities, your per-pay-period costs for medical plan coverage will go up by about $28 per adult.

2 Only individuals whose blood pressure reads above the normal range when tested during the health screening will be sent information about joining the program.

Important reminderYou have approximately 60 days from when your medical plan coverage becomes effective to complete your wellness activities. You can find your exact wellness activities deadline when you enroll in your benefits on My Benefits Resources. Your health and screening results and your health questionnaire must be submitted by the deadline to be considered complete.

2018 Benefits | Wellness 16

2018 Benefits | Enrollment 17

Or call the Global HR Service Center at 800.556.6044 to enrollWhen you’re logged on to the bank’s network:

1. Log on to My Benefits Resources using your standard ID and password.

2. From the Home tab, click Enroll in your benefits.

3. When you’re finished, confirm your choices by clicking Complete Enrollment. Your elections

will not be saved unless you complete this step. You will see a Confirmation Statement,

which you should print for your records.

If you’re not logged on to the bank’s network:

1. Log on to mybenefitsresources.bankofamerica.com using your Person Number and

password. If you don’t know your Person Number, you can use the Person Number Lookup

tool on Flagscape.

2. From the Home tab, click Enroll in your benefits.

3. When you’re finished, confirm your choices by clicking Complete Enrollment. Your elections

will not be saved unless you complete this step. You will see a Confirmation Statement, which

you should print for your records.

Representatives are available:

Monday through Friday (excluding certain holidays),

8 a.m. to 8 p.m. Eastern. Have your enrollment elections

ready when you call and enter your Person Number.

Once authenticated, say “Health and Insurance”

to speak to a Global HR Service Center representative,

who will take your benefit elections and validate your

dependent information.

Special service phone numbers:

• Hearing-impaired access: Dial 711, then call

800.556.6044.

• Overseas access: Dial your country’s toll-free

AT&T USADirect® access number, then enter

800.556.6044. In the U.S., call 800.331.1140 to obtain AT&T USADirect access numbers. From

anywhere in the world, access numbers are

available online at att.com/traveler or from

your local operator.

The fastest and easiest way to enroll is online, through My Benefits Resources

TIPIf you want to enroll anywhere, anytime from your smartphone or tablet, follow the log in instructions for those not logged on to the bank network.

For more information about plans described in this guide, visit the Medical plan details section on HR Connect > Benefits > Health > Medical plans > Resources.

Compensation Performance Year Cash Compensation (PYCC)If you were newly hired by the bank or became benefits-eligible for the first time after June 30, 2017, your performance year cash compensation (PYCC) for 2018 is your base salary as of your date of hire, or the date you became benefits-eligible.

If you rejoined the bank after June 30, 2017:

• If you were rehired within 180 days of leaving the bank, your previous PYCC amount will be used again.

• If you were rehired more than 180 days after leaving the bank, your PYCC is your base salary as of your date of rehire.

Your PYCC is used to determine available medical plans and your medical premium costs. This amount is also used to determine how much the bank will contribute to your health care account.

Any changes to your base pay in 2017 or 2018 will not affect the PYCC amount used to determine your pay tier.

Annual Benefits Base Rate (ABBR)For employees in all lines of business including Consumer Operations: ABBR is based on your annual base salary as of Dec. 31, 2016, draw paid in 2016 and any benefits-eligible cash incentives, which include most commission pay and annual bonus earned for 2016 and paid before July 2017.

For employees in the GWIM line of business: ABBR is based on your benefits-eligible compensation earned in 2016, plus any benefits-eligible cash incentives, which include most commission pay and annual incentives earned for 2016 and paid before July 2017.

Benefits-eligible cash incentives do not include cash incentives, bonuses, relocation payments or similar compensation paid to employees from a non-U.S. payroll.

Find your 2018 PYCC or ABBR1. Log on to My Benefits Resources using your Person Number

and the password you created for the site.

2. Click Your Profile on the top right-hand corner of the screen and select Personal Information from the drop-down list and then select the Personal Details tab.

Any changes to your annual base pay after Dec. 31, 2016 will not change the PYCC amount.

For some commission-based employees, we calculate an ABBR, which is used as your PYCC to determine available medical plans, your medical premium costs and how much the bank will contribute

to your health care account.

Eligible bonus amountFor associate supplemental life, AD&D and LTD insurance coverage amounts for 2018, your eligible bonus amount consists of any performance-based, benefits-eligible cash incentives and special equity awards earned for 2016 and paid by June 30, 2017. Your eligible bonus amount remains fixed for the plan year. Eligible bonus does not include cash incentives, bonuses, relocation payments or

similar compensation paid to employees from a non-U.S. payroll.

WellnessHealth screening and health questionnaireIf you are pregnant, or it is medically inadvisable or unreasonably difficult for you to participate in the health screening and/or health questionnaire based on a medical condition, you may submit a Health Care Provider Medical Waiver Form (2018 Wellness Program) signed by your health care provider in place of completing one or both steps of the wellness activities. Your physician will indicate which activities the waiver covers. If your waiver doesn’t cover both steps of the wellness activities, you will still need to complete the step that is not covered by the deadline in order to maintain the wellness credit. The form is available on My Benefits Resources > Wellness tab > Quick Links.

Tobacco users pay moreFor 2018, adults who have used tobacco in the last 12 months and are covered under Bank of America medical plans will pay a tobacco-user rate for their coverage. This rate is $900 more annually than the rate for adults who don’t use tobacco.

To qualify for the lower rate, the covered adult must certify during his or her enrollment period that he or she has not used tobacco products during the prior 12 months, including, but not limited to: cigarettes, cigars, pipes, chewing tobacco, snuff, dip and loose tobacco smoked by pipe.

During your enrollment period, you’ll be asked to provide your tobacco-user status separately from the tobacco-user status of your spouse or partner.

Note for medical coverage only: If you or your covered spouse or partner currently use tobacco products but intend to quit in 2018, you must indicate this when you enroll and you will not pay the higher tobacco-user rate. You will be contacted by your medical carrier about the tobacco cessation programs and resources available. The tobacco-user rate will still apply to associate supplemental life insurance or life insurance premiums for your spouse or partner.

If you or your covered spouse or partner or other adult dependent uses tobacco and is unable to meet the non-tobacco-user standard, you may still qualify for the lower non-tobacco-user medical rates. Contact the Global HR Service Center to discuss an alternative standard that will provide the same non-tobacco-user medical rates in light of your health status.

You must contact the Global HR Service Center and complete

certain steps prior to the end of your benefits enrollment period.

Health care accountsDepending on your enrollment choices, you may receive a Visa® debit card for your health care account.

Bank contributions Your PYCC, the plan and the coverage level you elect are used to determine how much the bank will contribute to your health care account.

Eligible dependents Eligible dependents for purposes of the HRA, Health FSA and Limited Purpose FSA include the participant’s spouse; birth, adopted or placed-for-adoption, step and foster children under the age of 26; and dependents that you claim (or you could have claimed) on your tax return.

However, per IRS requirements, the definition of an eligible dependent under an HSA only includes your spouse and family members whom you can claim as dependents on your federal income tax return. If you are uncertain if a child or other individual qualifies as your eligible dependent, call the Global HR Service Center.

If you have selected the Consumer Directed medical plan with the HRA, you may only submit claims for reimbursement from your HRA for yourself and those eligible dependents currently covered under your Bank of America medical plan, per IRS rules.

Important notes about your benefits

2018 Benefits | Important notes 18

Maintaining access to your HRA balance

If you have an existing HRA, you can maintain access to any balance

in that account by enrolling in an HRA-eligible medical plan and

remaining employed by the bank. If you’re still employed by the bank

and choose a plan that’s not HRA-eligible or choose not to enroll in a

medical plan, your HRA balance will continue to roll over. However,

the balance won’t be accessible until you re-enroll in an HRA-eligible

medical plan or leave the bank after meeting the Rule of 60.

HRA-eligible plans generally include the Comprehensive PPO plan

and the Consumer Directed plan. For more information, refer to the

2016 Summary Plan Description (SPD) and subsequent Summaries

of Material Modifications (SMMs) on HR Connect > Benefits > Health > Medical plans > Resources.

Tax considerations

Some circumstances could result in you being taxed on all or part of

the contribution to your health care account, including debit card

transactions, so be sure to keep receipts and documentation for

health care account purchases.

• You may need to verify that your debit card transactions were for

eligible health care expenses. If you don’t verify them, your Visa

debit card may be deactivated and/or you may be taxed on the

value of the transaction. For the HSA, there can also be a 20%

penalty from the IRS for ineligible expenses.

• If you receive bank contributions in an HRA for a family member

who is not your tax dependent, you must pay taxes on the amount

of the contribution. This is included in your imputed income

calculation, if applicable.

• If your contribution to an HSA, combined with any bank

contribution to your HSA, exceeds the IRS limit, you will pay taxes

on the amount of the contribution that exceeds the limit.

• California and New Jersey tax employer contributions to HSAs.

New Jersey also taxes employee contributions for HSAs, Health

FSAs and Limited Purpose FSAs.

Health Flexible Spending Account (Health FSA) and Limited Purpose Flexible Spending Account (Limited Purpose FSA) Your account is credited in full on Jan. 1 or the date you become

benefits-eligible. Eligible expenses must be incurred during the

period in which you actively contribute to your Health FSA or Limited

Purpose FSA. An expense is incurred when you actually receive a

service or make a purchase, not when you receive or pay a bill.

Health Savings Account (HSA) Verifying your information

If you enroll in an HSA, the federal government may require you to verify

certain information, such as your name or address, before your HSA can

be opened. If you don’t provide this information, your account won’t be

opened, which may result in forfeiture of any bank contributions.

The contributions you make would be returned during the year.

Who is eligible for coverage under our medical, dental and vision plans? For detailed information about dependent eligibility, refer to the 2016

SPD on HR Connect > Benefits > Health > Medical plans > Resources. If you add a dependent to your coverage for 2018, take

time to verify their eligibility and confirm their personal information.

Benefits eligibilityEmployees who were previously not eligible for benefits and work

30 hours or more per week over a 12-month “look back” period will

be eligible for medical benefits and health care accounts.

ChildrenGenerally, your children are eligible to be covered under our plans

until age 26, regardless of whether they attend school full- or

part-time.

Spouse or partnerGenerally, your spouse or partner is eligible to be covered under

our plans.

The U.S. Treasury and IRS guidance state that all same-sex couples

who are legally married are treated as married for federal tax

purposes, where marriage is a factor, including personal and

dependent exemptions and deductions, IRA contributions, tax credits

and eligibility for coverage under employee benefit plans.

Other adult dependentFor an individual to qualify as your other adult dependent,

he or she must:

• Be under age 65

• Be your dependent for federal income tax purposes. (To qualify

for coverage in a given year, the individual must have been your

tax dependent for the previous tax year and must continue to

be your tax dependent for the current tax year.)

• Live with you and be considered a member of your family

• Not be eligible for, and not have declined or deferred

coverage through the Bank of America employee or retiree

health care program

For information regarding health and insurance coverage for adult

family members, visit My Benefits Resources or call the Global HR

Service Center. If you’re uncertain if an adult family member qualifies

as your eligible dependent, call the Global HR Service Center.

When a dependent loses eligibilityYou have up to 31 calendar days to call the Global HR Service Center

and let us know that one of your dependents should be dropped

from the plan, for example, upon divorce. If your dependent receives

benefits from a plan after the date coverage ends, you’re responsible

for reimbursing the plan for benefits provided during that period.

Changes to your contribution amounts will take effect on the first

day of the month after you notify the Global HR Service Center that

your dependent is no longer eligible.

If your child will turn 26 in 2018 and does not qualify as an adult

dependent (see eligibility criteria above), he or she will automatically

be dropped from your coverage at the end of the last day of his or

her 26th birthday month. (As our plans cover your eligible children

through age 25.)

Important notes about your benefits

2018 Benefits | Important notes 19

Qualified status changeFor details on what’s considered a qualified status change, visit

HR Connect > Benefits > Health > Medical plans > Resources then click on Summary Plan Description (SPD) and Summary of Material Modifications (SMM) and select

the document that applies to you.

Life and disability insuranceAssociate supplemental life insurance Tobacco users pay a higher rate for associate supplemental life

insurance. When enrolling, you can indicate that you are not a

smoker if you have not used any tobacco products in the past

12 months.

When you first become eligible to enroll in supplemental life

insurance (for example, when you’re hired or if you switch from

part-time working less than 20 hours to full- or part-time status

working more than 20 hours), you may elect supplemental coverage

of one, two or three times your eligible compensation, to a

maximum that is less than $500,000, without providing a statement

of health. You must enroll within 31 days of becoming eligible.

If you initially elect supplemental coverage that’s greater than three

times your eligible compensation, or if you elect coverage that is

greater than or equal to $500,000, you must provide a Statement of

Health that’s satisfactory to the insurance company. If a Statement

of Health is required, your increased coverage begins the first of the

month following the date your Statement of Health is approved by

the insurance company. Until a Statement of Health is approved, or

if you fail to provide a Statement of Health when required, coverage

defaults to the highest level that does not require a Statement

of Health.

During future Annual Benefits Enrollment periods or when you have

a qualified status change, you’ll need to provide a Statement of

Health if you:

• Elect supplemental coverage for the first time

• Increase supplemental coverage by more than one level

• Elect supplemental coverage that’s greater than or equal to

$500,000. (This doesn’t apply if your coverage goes above

$500,000 because of a change in salary.)

Dependent life insurance Your per-pay-period costs for spouse or partner dependent life

insurance coverage will be higher if your spouse or partner is a

tobacco user. When enrolling, you can indicate that your spouse or

partner is not a smoker if he or she has not used any tobacco

products in the past 12 months.

When you elect coverage for the first time, and later, if you increase

coverage by more than one level or elect coverage over $50,000,

your spouse or partner must provide a Statement of Health. If a

Statement of Health is required, the increased coverage begins the

first of the month following the date your spouse’s or partner’s

Statement of Health is approved by the insurance company. Until a

Statement of Health is approved, or if your spouse or partner fails to

provide a Statement of Health when required, coverage defaults to

the highest level that does not require a Statement of Health.

Long-term disability insurance (LTD)The amount that you pay for LTD coverage depends on your age, the

level of coverage you elect when you are first eligible, during Annual

Benefits Enrollment or through a qualified status change, and

whether you are a full- or part-time employee.

While satisfying the elimination period for LTD, the amount of STD

benefits you receive will be based on your current compensation.

Benefits paid while on LTD will continue to be based on what your

compensation was during the elimination period and will not take into

account any changes in compensation after LTD benefit payments

begin. If your current compensation pay rate changes while you are

receiving LTD benefit payments or during the LTD elimination period,

your monthly LTD premium will increase accordingly during that time

and your new monthly pay rate will take effect on the date you are

again actively at work.

No benefit is payable for any disability that is caused by or

contributed to by a pre-existing condition and that starts before the

end of the first 12 months following your effective date of coverage.

A disease or injury is a pre-existing condition if during the three

months before your effective date of coverage:

• It was diagnosed or treated

• Services were received for the diagnosis or treatment of

the disease or injury

• You took drugs or medicines prescribed or recommended

by a physician for that condition

If you happen to be ill or injured and away from work on the date

your coverage would take effect, the coverage will not take effect

until the date you return to work to your regular part- or full-time

schedule. You will be considered to be active at work on any of your

scheduled work days if on that day you are performing the regular

duties of your job for the number of hours you are normally

scheduled to work. In addition, you will be considered to be active at

work on the following days:

• Any day which is not one of your employer’s scheduled work days

if you were active at work on the preceding scheduled work day

• A normal vacation day

These pre-existing conditions and actively-at-work provisions also

apply to an increase in your coverage. No benefit is payable for any

disability that is caused by or contributed to by a pre-existing

condition and that starts before the end of the first 12 months

following an increase in coverage. A disease or injury is a pre-

existing condition if during the six months before your effective date

of an increase in coverage:

• It was diagnosed or treated

• Services were received for the diagnosis or treatment of the

disease or injury

• You took drugs or medicines prescribed or recommended by a

physician for that condition

And, if you are not actively at work on the date your coverage

increases, your increased coverage will take effect on the date you

are again actively at work. The maximum monthly benefit, together

with all other income benefits, is $30,000.

Important notes about your benefits

2018 Benefits | Important notes 20

Important notes about your benefits

Imputed incomeThe value of certain benefits is considered imputed income,

which means that you pay taxes on the value of that coverage.

If imputed income affects you, you will see it on the first payroll

statement you receive after electing your benefits or, if later, your

coverage start date. For more information about imputed income,

refer to the 2016 Summary Plan Description (SPD) and subsequent

Summaries of Material Modifications (SMMs) on HR Connect > Benefits > Health > Medical plans > Resources.

• Associate basic life insurance: You will have imputed income if

your company-paid life insurance coverage exceeds $50,000.

• Dependent life insurance: Some participants may have imputed

income on their dependent life insurance coverage (for coverage

of more than $2,000).

• Coverage for a partner: The value of coverage for your partner

and/or your partner’s children who are not your tax dependents

is considered imputed income for purposes of medical, dental,

vision and AD&D insurance, as well as the value of any bank

contributions to your HRA, to the extent you are not paying the

full value of such coverage on a post-tax basis. (If you are

enrolling your partner and/or your partner’s children whom you

can claim as your dependents on your federal income tax return,

you must do so through the Global HR Service Center. If you are

enrolling your partner and/or your partner’s children whom you

cannot claim as your dependents on your federal income tax

return, you may do so through either My Benefits Resources

or the Global HR Service Center.)

Lifetime maximumA lifetime maximum, or the most the plan will pay for benefits,

applies to some medical and dental services. Please check with your

plan’s insurer or claims administrator regarding any benefit limits.

Falsification of information

If you or an enrolled dependent knowingly submit(s) false

information when enrolling in, changing or claiming health and

insurance benefits, or if you fail to notify the Global HR Service

Center that an enrolled dependent is no longer eligible for coverage,

participation for you and your dependents may be immediately,

retroactively and permanently canceled. In addition, the insurance

company may deny coverage. Pending claims may not be paid, and

you must reimburse the plan for any previous claims incurred that

should not have been paid. In addition, you may be asked to provide

proof of dependent eligibility at a future date. The bank reserves the

right to audit your dependent enrollment information at any time.

See page 19 for more information about dependent eligibility.

2018 Benefits | Important notes 21

Important notes about your benefits

Summary of Benefits and Coverage — Availability NoticeAs a result of the Patient Protection and Affordable Care Act, Bank of America is required to provide standardized Summaries of Benefits and Coverage (SBCs). The SBCs summarize, in a standard format, important information about the bank’s health plans. This is another resource to help you compare your plan choices. To take a look at the SBCs, log on to My Benefits Resources and go to Enroll in your benefits > Medical View/Change > Compare Medical Options for the applicable medical option SBC. If you have specific questions about what’s covered, call your medical carrier to ask about coverage for specific health conditions.

For a paper copy, call the Global HR Service Center at 800.556.6044.

When you enroll or continue participation in the Bank of America

plans, you are acknowledging that the benefits you have elected are

subject to the provisions of the Bank of America Group Benefits

Program and the terms and conditions of the benefit plans, and you

are authorizing the bank to withhold from your pay any employee

contributions required for such benefits. You acknowledge that if

you enroll in a plan that provides for binding arbitration of any

controversy between a plan member or beneficiary and a plan,

including, as applicable, its agents, associates, providers and staff

physicians, then any such controversy is subject to binding arbitration.

Important notice from Bank of America about your prescription drug coverage and MedicarePlease read this notice carefully and keep it where you can find it. This

notice has information about your current prescription drug coverage

with Bank of America and about your options under Medicare’s

prescription drug coverage. This information can help you decide

whether or not you want to join a Medicare drug plan. If you are

considering joining, you should compare your current coverage,

including which drugs are covered at what cost, with the coverage

and costs of the plans offering Medicare prescription drug coverage in

your area. Information about where you can get help to make decisions

about your prescription drug coverage is at the end of this notice.

There are two important things you need to know about your

current coverage and Medicare’s prescription drug coverage:

1. Medicare prescription drug coverage became available in 2006

to everyone with Medicare. You can get this coverage if you join

a Medicare Prescription Drug Plan or join a Medicare Advantage

Plan (like an HMO or PPO) that offers prescription drug coverage.

All Medicare drug plans provide at least a standard level of

coverage set by Medicare. Some plans may also offer more

coverage for a higher monthly premium.

2. For 2018, Bank of America has determined that the prescription

drug coverage offered by your Bank of America-sponsored

medical plan is, on average for all plan participants, expected to

pay out as much as standard Medicare prescription drug coverage

pays and is therefore considered Creditable Coverage. Because

your existing coverage is Creditable Coverage, you can keep this

coverage and not pay a higher premium (a penalty) if you later

decide to join a Medicare drug plan.

When can you join a Medicare drug plan?You can join a Medicare drug plan when you first become eligible for

Medicare and each year from Oct. 15 to Dec. 7. However, if you lose

your current creditable prescription drug coverage, through no fault

of your own, you will also be eligible for a two-month Special

Enrollment Period (SEP) to join a Medicare drug plan.

What happens to your current coverage if you decide to join a Medicare drug plan?Medicare-eligible employees and retirees are eligible for coverage

under medical plans that provide prescription drug coverage. Before

you decide whether to enroll in Medicare Part D, (1) carefully compare

the prescription drug benefits offered under the Bank of America plan,

the cost and the drugs covered with the benefits, and the cost and

drugs covered under the Medicare Part D plan; and (2) read below to

understand how your Bank of America medical and prescription drug

coverage will be affected.

• Medicare Advantage Plan: If you enroll in a Medicare Part D

plan, you will be automatically disenrolled from your

Bank of America Medicare Advantage plan and enrolled in another

Bank of America retiree medical plan. Before enrolling in a

Medicare Part D plan, please call the Bank of America Global HR

Service Center at 800.556.6044 for more information.

• Medical Plan other than a Medicare Advantage Plan: If you enroll in a Medicare Part D plan, you will have prescription

drug coverage under two plans. Note that your monthly

contributions for coverage under the Bank of America plan will

not be reduced if you enroll in a Medicare Part D prescription drug

2018 Benefits | Important notes 22

Important notes about your benefits

plan. However, your Bank of America medical coverage will be

coordinated with coverage under the Medicare Part D plan as follows:

– If you are an active employee, your Bank of America plan will

pay primary for prescription drugs covered by Medicare. This

means that if the Bank of America plan’s prescription drug

coverage is less generous than your Medicare Part D plan’s

coverage, your Medicare Part D plan will pay an additional

amount. However, if the Bank of America prescription drug

coverage is just as generous or more generous than the

Medicare Part D plan’s coverage, the Medicare Part D plan will

not provide any additional prescription drug coverage.

– If you are a retiree or a participant in the Bank of America Long-term Disability Plan, your Bank of America prescription

drug coverage will pay secondary for prescription drugs

covered by Medicare. This means that if the Medicare part D

plan’s coverage is less generous than the Bank of America

prescription drug coverage, your Bank of America plan will pay

an additional amount. However, if the Medicare Part D plan is

just as generous or more generous than the Bank of America

plan’s prescription drug coverage, the Bank of America plan will

not provide any additional prescription drug coverage.

If you do decide to join a Medicare Part D plan and drop your Bank of America medical plan coverage, you and your dependents may not be able to re-enroll in Bank of America medical plan coverage at a later time. Before dropping or

declining coverage under a Bank of America medical plan, please call

the Bank of America Global HR Service Center at 800.556.6044 to

learn whether you can re-enroll in Bank of America coverage at a later

date and the conditions for re-enrollment. Note that retirees from

certain predecessor companies or those enrolled in certain retiree

medical plans of predecessor companies may not drop retiree medical

coverage and re-enroll at a later time, and retirees who drop coverage

and are permitted to re-enroll in a Bank of America retiree medical

plan must provide proof of coverage under another medical plan (other

than Medicare) for 12 consecutive months prior to the date they wish

to re-enroll.

When will you pay a higher premium (penalty) to join a Medicare drug plan?You should also know that if you drop or lose your current coverage

with Bank of America and don’t join a Medicare drug plan within

63 continuous days after your current coverage ends, you may pay

a higher premium (a penalty) to join a Medicare drug plan later.

If you go 63 continuous days or longer without creditable

prescription drug coverage, your monthly premium may go up by

at least 1% of the Medicare base beneficiary premium per month

for every month that you did not have that coverage. For example,

if you go 19 months without Creditable Coverage, your premium

may consistently be at least 19% higher than the Medicare base

beneficiary premium. You may have to pay this higher premium (a

penalty) as long as you have Medicare prescription drug coverage. In

addition, you may have to wait until the following October to join.

For more information about this notice or your current prescription

drug coverage, contact the Global HR Service Center at

800.556.6044. Note: You’ll get this notice each year. You will also

get it before the next period you can join a Medicare drug plan, and

if this coverage through Bank of America changes. You may also

request a copy of this notice at any time.

More detailed information about Medicare plans that offer

prescription drug coverage is in the Medicare & You handbook. You’ll

get a copy of the handbook in the mail every year from Medicare.

You may also be contacted directly by Medicare drug plans.

For more information about Medicare prescription drug coverage:

• Visit medicare.gov.

• Call your State Health Insurance Assistance Program

(see the inside back cover of your copy of the Medicare & You

handbook for their telephone number) for personalized help.

• Call 800.MEDICARE (800.633.4227) (TTY: 877.486.2048).

If you have limited income and resources, extra help paying for

Medicare prescription drug coverage is available. For more

information about this extra help, visit socialsecurity.gov or call

800.772.1213 (TTY: 800.325.0778).

Remember: Keep this Creditable Coverage notice. If you decide to

join one of the Medicare drug plans, you may be required to provide

a copy of this notice when you join to show whether or not you have

maintained Creditable Coverage and, therefore, whether or not you

are required to pay a higher premium (a penalty).

Women’s Health and Cancer Rights ActAs required by the Women’s Health and Cancer Rights Act of 1998,

each medical plan provides the following medical and surgical

benefits with respect to a mastectomy:

• Reconstruction of the breast on which the mastectomy has

been performed

• Surgery and reconstruction of the other breast to produce

a symmetrical appearance

• Prostheses and treatment of physical complications of all stages

of the mastectomy, including lymphedema

These services must be provided in a manner determined in

consultation with the attending physician and the patient. This

coverage may be subject to annual deductibles, coinsurance and

copayment provisions applicable to other such medical and surgical

benefits provided under the plans.

Please refer to your Health Plan Comparison Charts available in the

Summary Plan Description for deductibles and copayment information

applicable to the medical plan in which you choose to enroll. The

Summary Plan Description is available on My Benefits Resources or

upon request by calling the Global HR Service Center at

800.556.6044.

2018 Benefits | Important notes 23

Availability of Notice of Privacy PracticesThe Bank of America Group Benefits Program (the “Plan”) maintains

a Notice of Privacy Practices that provides information to individuals

whose protected health information will be used or maintained by

the Plan. The notice was recently updated to direct readers to

contact the Global HR Service Center at the following address:

BANK OF AMERICA GLOBAL HR SERVICE CENTER

P.O. BOX 64046

THE WOODLANDS, TX 77387-4046

If you would like a copy of the Plan’s Notice of Privacy Practices, visit

My Benefits Resources and click Knowledge Center > Plan Information Page > Legal Notices or call the Global HR Service

Center at 800.556.6044.

Marketplace special enrollment windows related to COBRAUnder the Affordable Care Act, you can enroll in a medical plan

through your state’s health care exchange during an open enrollment

period or designated special enrollment periods. A special enrollment

period will be available when you become eligible for COBRA, or

after you are no longer eligible for COBRA. There is no special

enrollment period if you voluntarily end your COBRA coverage.

For more information about specific enrollment rules or plans

offered through health care exchanges, please visit healthcare.gov

or call 800.318.2596 (TTY: 855.889.4325).

Fully insured medical plansAetna International, Kaiser Permanente, HMSA Hawaii and Triple-S

Salud medical plans may have other changes in coverage for 2018.

Please contact these carriers with any questions.

DisclaimerThis document provides information about certain Bank of America benefits. Receipt of this document does not automatically entitle

you to benefits offered by Bank of America.

Every effort has been made to ensure the accuracy of the contents of this document. However, if there are discrepancies between