beps reporting and compliance considerations

TRANSCRIPT

BEPS reporting and compliance considerations

32nd Annual TEI-SJSU High Tech Tax InstituteNovember 7-8, 2016

2© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

Presenters

BEPS reporting and compliance considerations Kara Boatman, Principal – KPMG Jay Das, Principa l – Deloitte Tax LLP David Nickson, Principal – PwC Bernadette Pinamont, Director, Chief

Tax Office – Vertex Inc.

3© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

Implemented Draft bills/Public discussion draft Intention to Implement

CbCR Final Legislation

United States

CbCR/MF/LF Final Legislation

Mexico

CbCRDraft legislation

Canada

CbCR/MF/LF Final Legislation

Australia

China

CbCR/MF/LFFinal Legislation

Norway

CbCRFinal Legislation

France

CbCRFinal Legislation

IrelandCbCR/MF/LF

Final Legislation

Japan

CbCRDraft

South Korea

MF/LF Final

South Africa

CbCRIntentions

Nigeria

CbCR/MF/LFIntentions

New Zealand

CbCR/MF/LFIntentions

TaiwanCbCRFinal

Portugal

MF/LF Intention

CbCR/MF/LF Draft Legislation

SwedenCbCR/MF/LF

Draft Legislation

Finland

CbCRDraft legislation

SingaporeIsrael

United Kingdom

CbCRDraft

MF/LF Intention

CbCR/MF/LFIntentions

Chile

Russia

CbCR/MF/LFDraft Legislation

Romania

CbCRIntention

MF/LF Final

CbCRIntentions

Bermuda

Belgium

CbCR/MF/LFFinal Legislation

CbCRDraft legislation

Luxembourg

CbCR/MF/LFIntentions

Malaysia

IndiaCbCRFinal

MF/LF Draft

CbCRDraft

MF/LF Intention

CbCR/MF/LFIntentions

Peru CbCR/LFDraft

MFIntention

CbCR/MFDraft legislation

Uruguay

CbCRFinal

MF/LF Intention

Country implementation summaryBEPS action 13

CbCR/MF/LF Final Legislation

Spain

CbCRIntentions

Jersey

Germany

CbCR/MFDraft

LF Intention

Switzerland

CbCRDraft

MF/LF Intention

CbCRFinal Legislation

Italy

Austria

CbCR/MF/LFFinal Legislation

CbCR/MF/LF Final Legislation

Denmark

CbCR/MF/LF Final Legislation

Netherlands

CbCR/MF/LF Final Legislation

Poland

CbCR/MF/LFIntentions

Indonesia

Source: KPMG International member firms

4© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

BEPS reporting and compliance considerations— Country by Country Reporting

- Do we have to comply? What if we don’t?— Penalties— Audit risk

- Where/when do we need to file?- What about public disclosure?

— Master File- When?- How much information should we include?

— “A” versus “C” report— Value chain analysis: yes or no?

- What about countries that don’t have the same $$ threshold?

5© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

BEPS reporting and compliance considerations (continued)— Local Files

- Centralized versus decentralized approach- When?

— Should we prepare for countries that haven’t yet implemented LF requirements?

- How much information?- What about China?

6© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

Consider a more strategic approach

Recommendations & Stakeholder Communications

BEPS Strategy

Fact Gathering & Documentation

Value Chain Analysis

Transparency Considerations

BEPS Risk Assessment

7© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

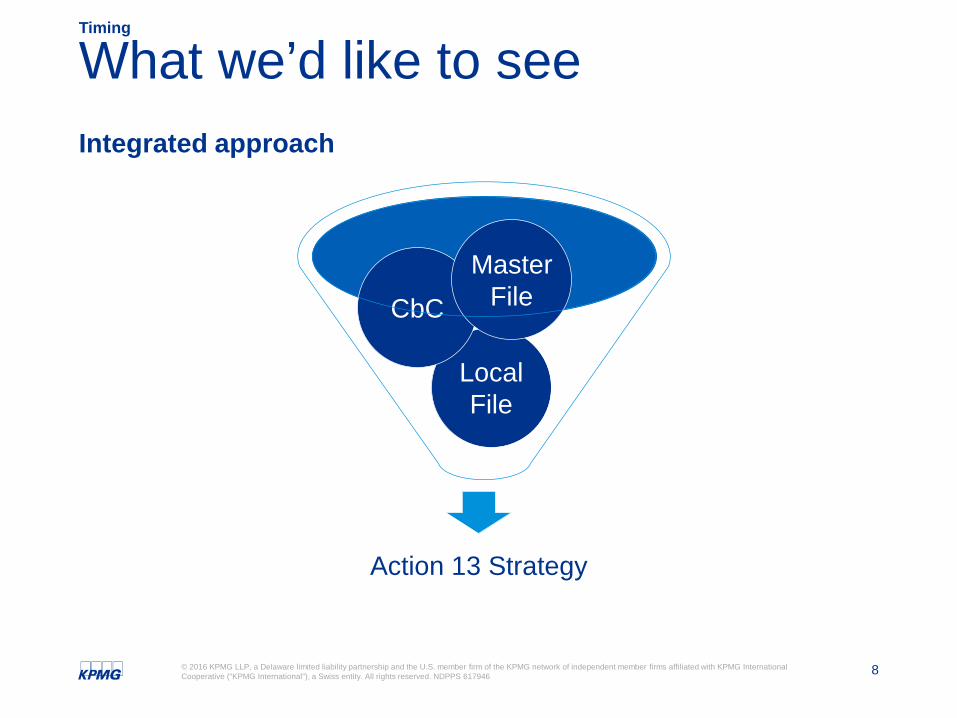

What we seeLinear approach

Timing

CbC Master File Local File

8© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

What we’d like to seeIntegrated approach

Timing

Action 13 Strategy

Local File

CbCMaster

File

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 617946

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Accounting and Data Challenges and Solutions

PwC/VertexPwC/Vertex

Typical challenges ‘at the coal face’Companies initially viewed CbCR as a purely compliance burden, but this has quickly evolved into a broader evaluation of system capability for tax and legal entity reporting

Challenges Themes to investigate

Entity level data

Local variation for intercompany transactions

Complex data and technology landscape

Significant effort required to map management reporting to legal entity activity● Ledger configuration● Alignment legal to tax.● Offline calculations and reallocations.

Statutory accounting processes and other challenges● Timing mismatch of local statutory financial statements as compared to required CbCR

deadlines● Current statutory processes not systemized/centralized● Ledger to entity/branch uniqueness

● Where I/C transactions recorded e.g. retained earnings (or similar) ● Elimination of activity is subject to significant variability

● Multiple disparate local and aggregated ledgers ● Decentralized location for collection, manipulation and management of general ledger and

transactional data● Process related to periodic review and control of legal entity structure● Workflow needed to integrate multiple data sources.

11

PwC/VertexPwC/Vertex

Fundamental challenges – 1. tensions between global and local reporting

Local statutory accounts/

tax returns

Global financial

statements

CbCR?Alignment to

local file

Time intensive, and greater system

challenges

Fastercompilation

Reconciliationchallenges on

audit

Local file

Masterfile

12

PwC/VertexPwC/Vertex

Fundamental challenges – 2. additional accounting tasks

Aggregated approach to country results build up:

• Addition of P&Ls/balance sheets without elimination

• Deconsolidation/gross-up of financial/operational/taxation results?

• Stripping out ‘negative cost’ in cross allocation processes to identify related party revenues

Anticipated reconciliations and audit trail

• Ability to reconcile the CbCR to:

− local statutory statements − worldwide audited statements − legal entity books − local tax returns − transfer pricing documentation − local international reporting (5471)

• Ability to provide audit trails:

− Auditable trail back to source data− Record retention of the data over multiple years for consistency − Versioning control

13

PwC/Vertex

Fundamental challenges – 3. Culture and IT landscape

14

Data Management to prepare for the end to end process of CbC reporting may be a challenge for numerous MNCs. Many companies we talk to are initially thinking they can get the data from their ERP and that may or may not be true.

Supporting processes in the controllership function are critical

Business culture, resource availability, and timing of data

Core ERP and Business Intelligence systems capability/configuration to handle data granularity

PwC/Vertex

High Level Data Flow for CbC Reporting

HR systems

Exchange rates

LE/BUmappings

Fixed Asset Systems

Revenue sub ledgers

ERPs

A/P & A/R

Cash taxes

CbCR Table #1

CbCR Table #2

Tax applications

Self service reporting

Provision & compliance tools

Tax data mart(s)

SAP Connector

Oracle Connector

Flat File

ExcelAdd-In

Other ERP Connectors

Active processing

Collected & Loaded Validated & Transformed Reported, Reconciled & Retained

PwC/Vertex

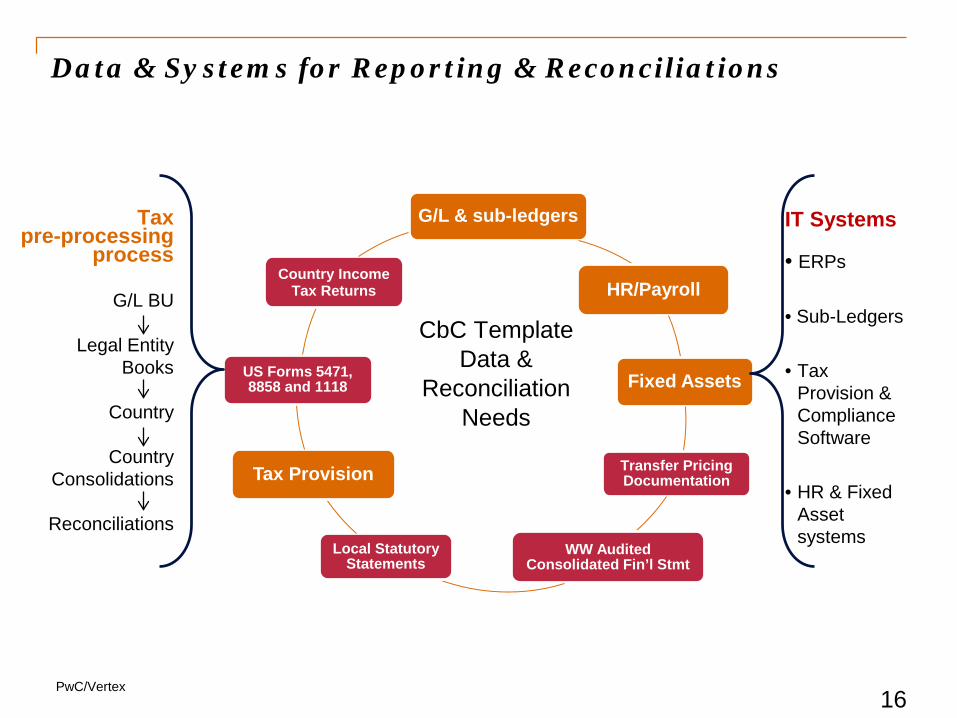

Data & Systems for Reporting & Reconciliations

16

G/L & sub-ledgers

HR/Payroll

Fixed Assets

Transfer Pricing Documentation

WW Audited Consolidated Fin’l Stmt

Local Statutory Statements

Tax Provision

US Forms 5471, 8858 and 1118

Country Income Tax Returns

CbC Template Data &

ReconciliationNeeds

IT Systems

• ERPs

• Sub-Ledgers

• Tax Provision & Compliance Software

• HR & Fixed Asset systems

Tax pre-processing

process

G/L BU

Legal EntityBooks

Country

Country Consolidations

Reconciliations

PwC/Vertex

Further considerations

Data in multiple source systems with different formats and different meanings.

Data errors, identified too late in the process, increase

risk.

Data translation (from Finance view to Tax view) is complex

and error prone if done manually

Accurate data translations• Business Unit and Cost Center financial data

aggregated and consolidated • Financial details translated as necessary to

Parent MNE reporting currency, by legal entity and by country

• HR and Fixed Asset data aggregated by Country

• Business Activity data by legal entity• In a repeatable, reliable, and accurate process

Data Errors• Early Detection: find errors early before final reports

and filings are completed• Account Balances: Rules can highlight accounts that

don’t balance• Easily Determine Root Cause: Drill down to lowest

level of detail to determine source of problem ccuratedata translations

Data and Systems• Degree of centralization of ERP and Business Intelligence systems • Degree of standardization in the charts of accounts • Stable platform of centralized and standardized system and processes • GAAP rules of the local companies can be easily converted to parent company

GAAP rules

17

PwC/Vertex

Key Questions

18

• Single instance globally or fragmented?

• Stable platform, or ‘in transition’ (ERP rollout or acquisitive behavior)

• System optimized for legal entity reporting; reconciliation capability local GAAP to U.S?

• Standardized chart of accounts or ERP templates?

• Degree of BI centralization, maturity of reporting, and business support available

• Difference between management and legal entity accounting…and reconciliation capability

ERP and Business intelligence landscape

• Degree of centralization and cultural values• Maturity and stability level of systems?• Existing processes to leverage (5471s, provision,

management allocations, FTC, tax cashflowforecasting)

• Plan for data mapping & reconciliations• Plan for workflow approach (build v buy, insource

v outsource)• Does the complexity of your corporate structure

require that you run several trials?• Record Retention

Current tax processes

PwC/Vertex

Learnings & Best Practice Recommendations

It is critical to create cross-organization momentum

- Identify drivers in other functions that align with the CbC agenda (e.g. FP&A and insights into fully loaded profitability/customer analysis)

- Leverage organizational investments in IT wherever possible

- Focus on time/resource impacts for the finance organization to support analysis, as a driver to support the investment in technology

- Engage with shared services/GBS/GFS type functions and start the ‘service level agreement’ discussion early

- Present the issues as related to transparency and intercompany accounting/reporting as opposed to ‘tax compliance’

- Elevate the reputation and confidentiality risk issues associated with the granular reporting of profitability data

- Establish a task force/sponsorship group across tax, finance, and IT

- Maximize the use of technology for data collection, validation, transformation, and reconciliation to ensure overall transfer pricing story is properly told and to provide an audit trail.

- Start preparing now

19

Common Issues Around CbC Reporting, Master File & Local File

October 2016

Introduction

• In this presentation, we will discuss the common issues companies experience when navigating Country by Country (“CbC”) Reporting, Master File (“MF”) and Local File (“LF”) filing requirements.

• The common issues can be classified in the following categories:• CbC Reporting Interpretation • Technical Issues• Gray areas in the CbC reporting that are

addressed in MF/LF• Gray areas in MF/LF

• The following slides showcase a list of sample issues Clients has encountered while preparing for the CbC, MF and LF filing.

21

CbC Reporting Interpretation Issues

• Interpretation of “Total accrued tax expense” in CbC Reporting• Should total accrued tax expense be net of foreign tax credits for US tax purposes? • Should deferred taxes and provisions of uncertain tax liabilities be excluded from total accrued

tax expense?

• Treatment of stateless income in CBC reporting• How should income from the various types of entities such as the following be treated for

purposes of CbC reporting? • Reverse Hybrid• Cayman Company• Partnership • Branch registered in Ireland with no income tax

• Treatment of related party revenues for CbC and MF purposes• Should revenue from entities, where Clients holds less than 50% of its ownership, be included in

the US CbC reporting.

• Should dividend income be excluded from profit/loss before tax?• There were no clear guidance on whether dividend income should be included in profit/loss

before tax in the CbC reporting.

22

Technical Issues

• Which jurisdictions allow for surrogate parent filing• To date, the U.S. income tax treaty and tax information exchange agreement (“TIEA”) network cover

approximately 95+ countries. However prior to automatic exchanging information, the IRS must enter into a competent authority (“CA”) arrangement specifying the rules under which such exchange will take place. For jurisdictions within the US treaty and TIEA network that the US does not enter into CA arrangement with for the exchange of CbC info, they may require secondary filing of the CbC report under local rules similar to the OECD model legislation.

• Currently there are concerns around exchange of information with/from Chile, China, Singapore, Switzerland and Taiwan, where Clients have significant businesses.

• China for example, is an “in network” country but since it does not have a BDI automatic exchange relationship with the US under FATCA, Clients China may be required to meet local filing requirements in China.

• To avoid additional local filing requirements, Clients could utilize a parent that have passed legislation or otherwise indicated that they are willing to serve as a surrogate.

• May need to conduct analysis to compare between US treaty network and the networks of the following potential surrogate countries:

• Mexico• Japan• Australia• Canada• UK • Netherlands

23

Gray areas in the CbC reporting which has to be outlined in the master file/local file.

• Should LF be provided on an entity by entity basis or aggregated for the entire Clients business operation in that jurisdiction?

• These are done through on a country by country basis to understand local filing requirements for respective jurisdictions.

• Reporting contract labor in CbC and MF/LF• US CBC regulation §1.6038-4(d)(3)(iii) writes that “independent contractors that participate in the

ordinary operating activities of a constituent entity may be considered employees of such constituent entity.” Therefore do companies have the flexibility or exclude contract labors in the reporting of total employees?

• Main Business Activity: Should companies check one or multiple boxes in CbC Reporting form if the entity is involved in multiple business lines?

• Do business lines reported in the CbC Reporting form need to agree with the descriptions in the MF.

24

Gray areas in MF/LF

• Clarification on MF requirements and presentation of the legal ownership chart in the MF

• Should the organizational chart include holding and dormant entities? Should the entities included in the organizational chart reconcile with entities listed in the CbC reporting?

• Local file reporting requirements for holding companies and dormant entities• What are the minimum LF reporting requirements for holding and dormant

companies that perform little to no functions..

• Clarification on MF requirements for top 5 products/service offerings• What is the definition of product line? Can it be interpreted that Client’s top 5

business segments are the top 5 products/ service offerings?

• Should intangibles be reported for business segments that account for less than 5% of Client’s overall business?

• Should constituent entities such as business unit’s intangibles be reported in the MF even though these entities account for less than 5% of Client’s overall business?

25