best practices symposium - reaganconsulting.com

TRANSCRIPT

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

WELCOME

Bobby Reagan and Tom DoranReagan Consulting

WiFi Information:

Network:

IIABA

Password (case sensitive):

bigimeet

3

Download the

BigIEvents

APP

Best Practices Symposium Password: BPS2020

Important Things to Know

Three Breakouts:

9 Separate Sessions

Cocktails and Dine-Arounds Tonight

Optional Devotional

Tuesday Morning

4

Breakouts

• Breakout One: 10:10 a.m. – The Impact of Consolidation

• Breakout Two: 2:10 p.m. – Producer Recruiting and Development

• Breakout Three: 3:55 p.m. – Developing a Sales Culture

5

Important Things to Know

Three Breakouts:

9 Separate Sessions

Cocktails and Dine-Arounds Tonight

Optional Devotional

Tuesday Morning

6

Your Dine Around Hosts

7

Antoine’s Brennan’s Cochon Emeril’s Delmonico

Galatoire’s GW Fins Mr. B’s Restaurant R’evolution

Brian McNeely Bobby Reagan Tom Doran Kevin Stipe

Brian Deitz Jim Campbell Harrison Brooks Mark Crites

Dinner Tonight – Dine Arounds

8

Keep your name badge on during dinner, please

Important Things to Know

Three Breakouts:

9 Separate Sessions

Cocktails and Dine-Arounds Tonight

Optional Devotional

Tuesday Morning

9

10

Friday Morning Devotional

We Want Your Input and Feedback!

Text to:

(747) 444-3548Message:

reagan

11

14

Bob RusbuldtPresident & CEO

The Big “I”

Bobby ReaganChief Executive Officer

Reagan Consulting

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

We have come a long way……are we there yet?

Bobby ReaganReagan Consulting

16

Strong competition (especially from direct writers)

Loss of market share

Number of independent agents declining

Carriers pulling back on business writing / agents represented

Value of independent agents declining

• The IIAA formed The Presidential Commission to Enhance Agency Values with three key objectives:

1) Improve efficiency of agency/company relations

2) Improve legislative and regulatory environment

3) Help agents operate more efficiently

In the early 1990s…

17

• I met Shirley Lukens with the Big I and began developing a concept that became the Best Practices Study

• Our two organizations came together to jointly create, produce and distribute the Best Practices Study for the benefit of the Big I members, for the insurance carriers that depend on independent agents and for the insureds we collectively serve.

In the early 1990s…

18

1993 – 201927 Best Practices Studies Performed

19

1993 – 2019: Are we there yet?

20

Pro Forma Profit

Revenue per Employee

Typical INTERNAL Agency Valuation(multiple of revenue)

Typical EXTERNAL Agency Valuation(multiple of revenue)

12% 27%

$80,793 $179,303

1.0x 1.6x

1.4x 2.5x

✓ Performance has improved tremendously

1993 – 2019: Are we there yet?

✓ Performance has improved tremendously

✓ Market share has stabilized

✓ Direct writers are coming over to our side (Liberty, Nationwide)

✓ Still consolidation but are selling out of strength

21

1993 – 2019: Are we there yet?

There is still room for improvement, even for those in this room (i.e., the Best)

Insureds’ needs and expectations are growing

Existing peers will begin to elevate their performance

New competitors will come onto the scene

Change will come even more rapidly than in the past

22

Is the Best Practices Study still needed?

23

We need to continue to adapt, improve, anticipate

We need to provide more “real time” data

We need to provide more opportunities for Best Practices agents and brokers to learn from each other

The Big I and Reagan Consulting are committed to your future and to making Best Practices a driving force to help you get

“there”

24

on being a Best Practices Agency

Our challenge to you is to get everything out of Best Practices and this Symposium that you can

25

New ideas or strategies for your agency

New personal relationships

New ways to help you personally

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

The Impact of Consolidation

Kevin StipeReagan Consulting

303

200244

311

364

245

360

492457

558597

643

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

2019 sets another new M&A record

Source: SNL Financial as of December 31, 2019 (based on Announcement Date). Includes whole company, franchise and asset sales.

29

Source: SNL Financial as of December 31, 2019 (based on Announcement Date). Includes whole company, franchise and asset sales.

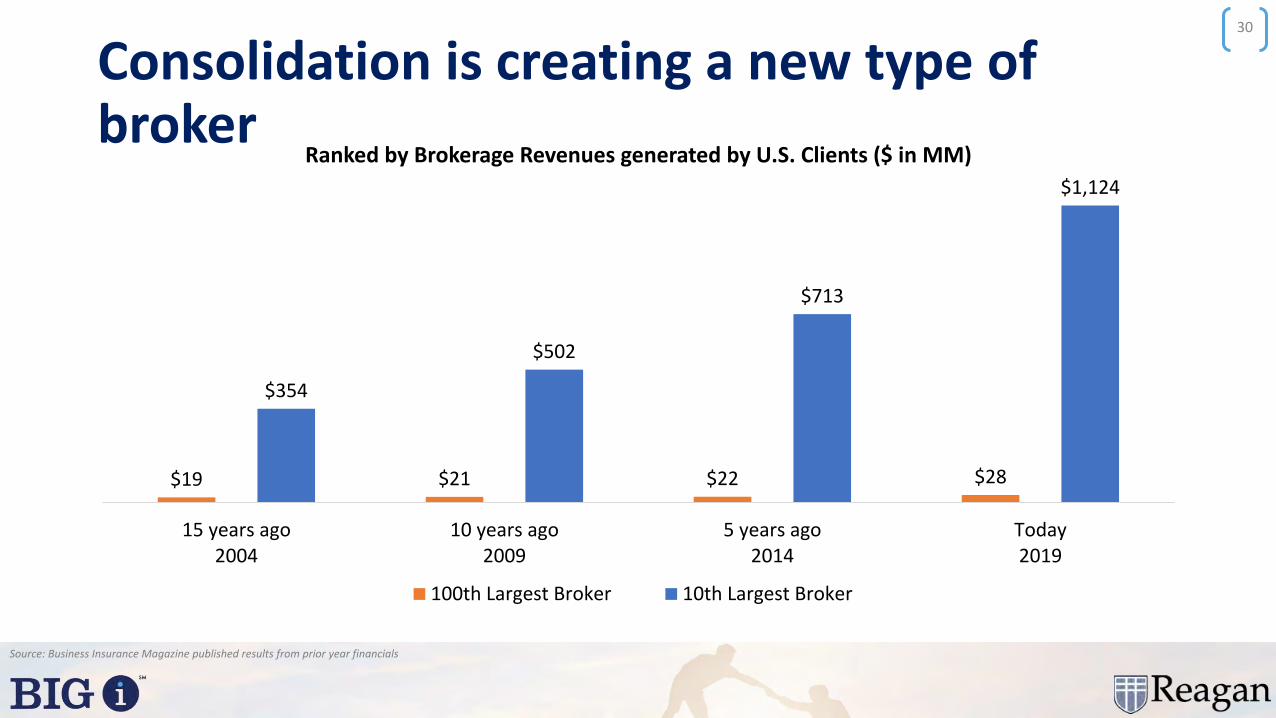

Consolidation is creating a new type of broker

30

$19 $21 $22 $28

$354

$502

$713

$1,124

15 years ago2004

10 years ago2009

5 years ago2014

Today2019

Ranked by Brokerage Revenues generated by U.S. Clients ($ in MM)

100th Largest Broker 10th Largest Broker

Source: Business Insurance Magazine published results from prior year financials

Billionaires Club – 1984Billionaires Club – 2013Billionaires Club – 2020

31

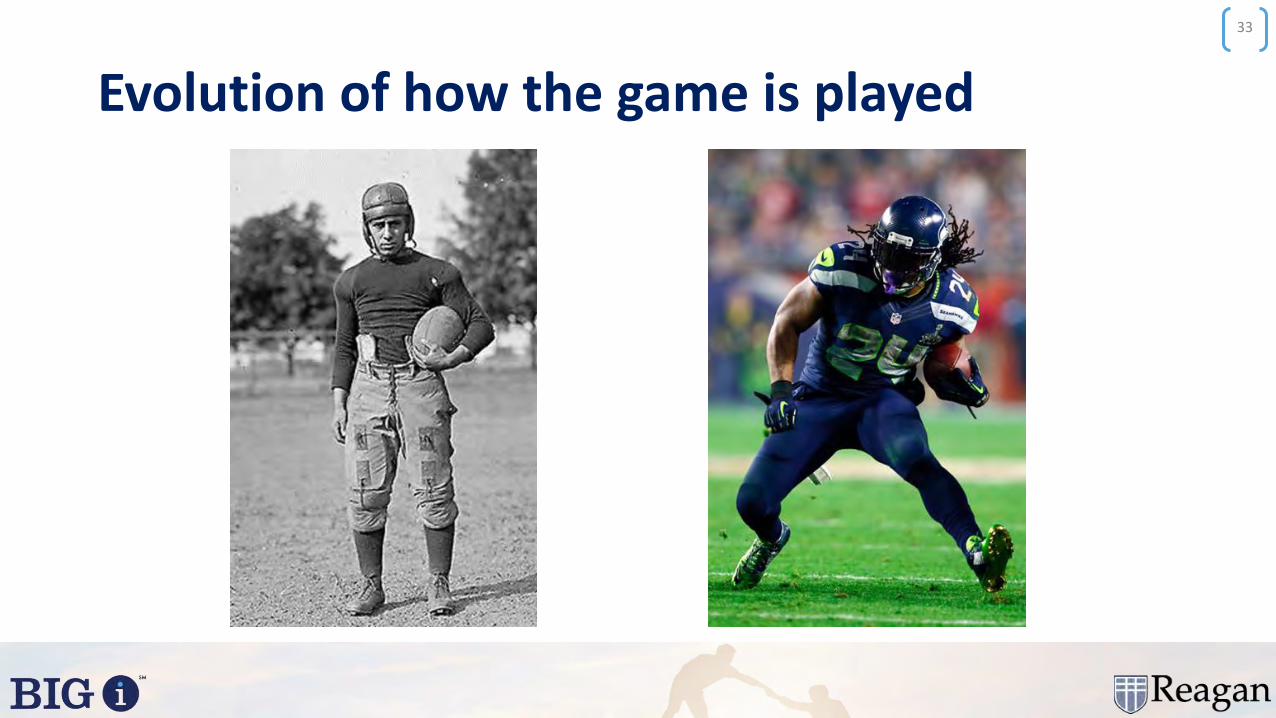

Evolution of how the game is played

33

Consolidation’s competing theories

34

Passing FadCatalyst for

Radical Change

Panelists35

Grace PeabodyPartner

Trevor BaldwinChief Executive Officer

Brad BolingerVice President of Sales

Brian HetheringtonChairman

Peabody Insurance Baldwin Risk Partners Higgins Insurance and Benefits ABD

HQ: Fenton, MI HQ: Tampa, FL HQ: Hopkinsville, KY HQ: San Mateo CA

Rev Category: $2.5M-$5.0M Rev Category: Over $25.0M Rev Category: $5.0M-$10.0M Rev Category: Over $25.0M

Year Founded: 2013 Year Founded: 2006 Year Founded: 1897 Year Founded: 2011

Roundtable Discussion Questions40

1) Which of the two theories do you believe about consolidation and why?

• Passing Fad

• Catalyst for Radical Change

2) What are your firm’s greatest disadvantages relative to larger firms?

3) What are your firm’s greatest advantages relative to larger firms?

4) What steps can your firm take to level the playing field and compete in a world where size matters more than in the past?

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Best Practices Awards Luncheon Banquet

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Top Performing Best Practices Agenciesby Revenue Category

Source:

20

2019 Highest Performing BPA:Under $1.25 Million in Revenue

Source:

Nelson Hatchett

2019 Highest Performing BPA:$1.25 - $2.5 Million in Revenue

Source:

Bob Klinger

2019 Highest Performing BPA:$2.5 - $5.0 Million in Revenue

Source:

Adam Yeager

2019 Highest Performing BPA:$5.0 - $10.0 Million in Revenue

Source:

J. R. Reilly

The Reilly Company

2019 Highest Performing BPA:$10.0 - $25.0 Million in Revenue

Source:

John Marek

2019 Highest Performing BPA:Over $25.0 Million in Revenue

Source:

Kurt de GroszBrian Heatherington

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Producer Recruiting & Development –Redefining the Issue

Brian Deitz & Mark CritesReagan Consulting

Our Industry Doesn’t Hire Enough

Source: Reagan Consulting Producer Recruiting & Development Study

5

55%-60%of agents not hiring enough producers to

grow and perpetuate

Source: Reagan Consulting Best Practices Study

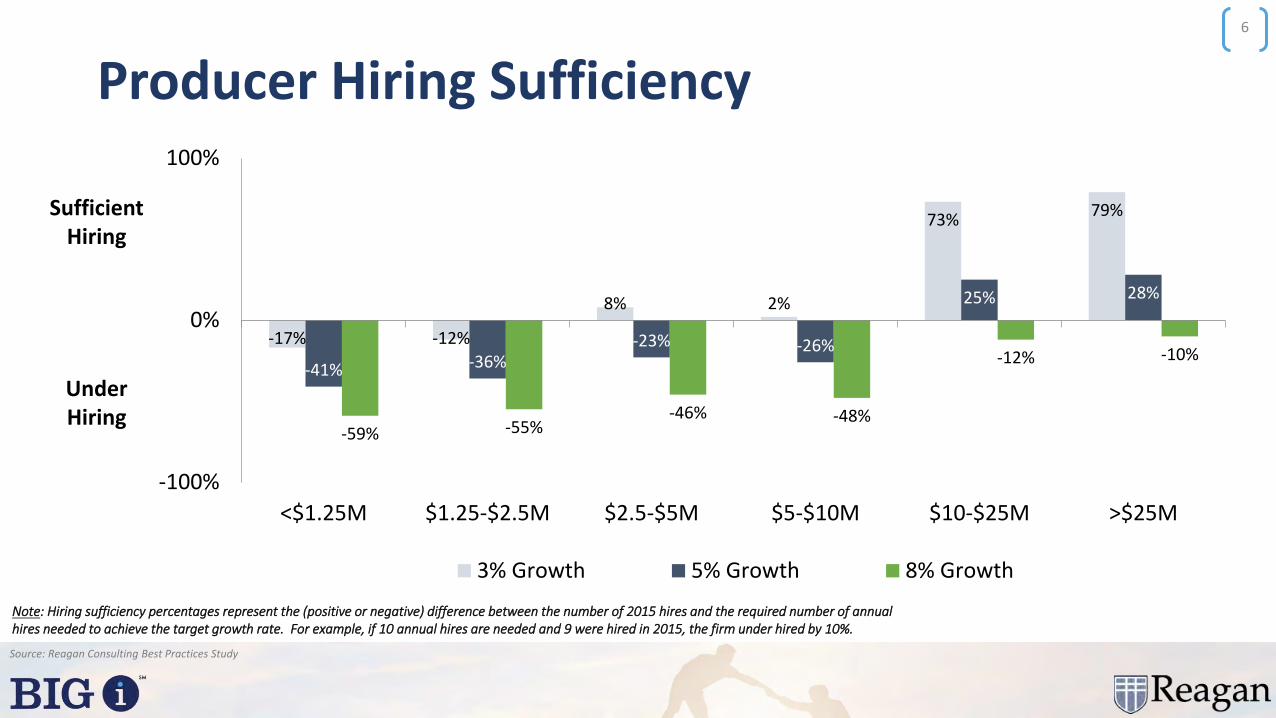

6

Note: Hiring sufficiency percentages represent the (positive or negative) difference between the number of 2015 hires and the required number of annual hires needed to achieve the target growth rate. For example, if 10 annual hires are needed and 9 were hired in 2015, the firm under hired by 10%.

-17% -12%

8% 2%

73%79%

-41% -36%-23% -26%

25% 28%

-59% -55%-46% -48%

-12% -10%

-100%

0%

100%

<$1.25M $1.25-$2.5M $2.5-$5M $5-$10M $10-$25M >$25M

3% Growth 5% Growth 8% Growth

SufficientHiring

UnderHiring

Producer Hiring Sufficiency

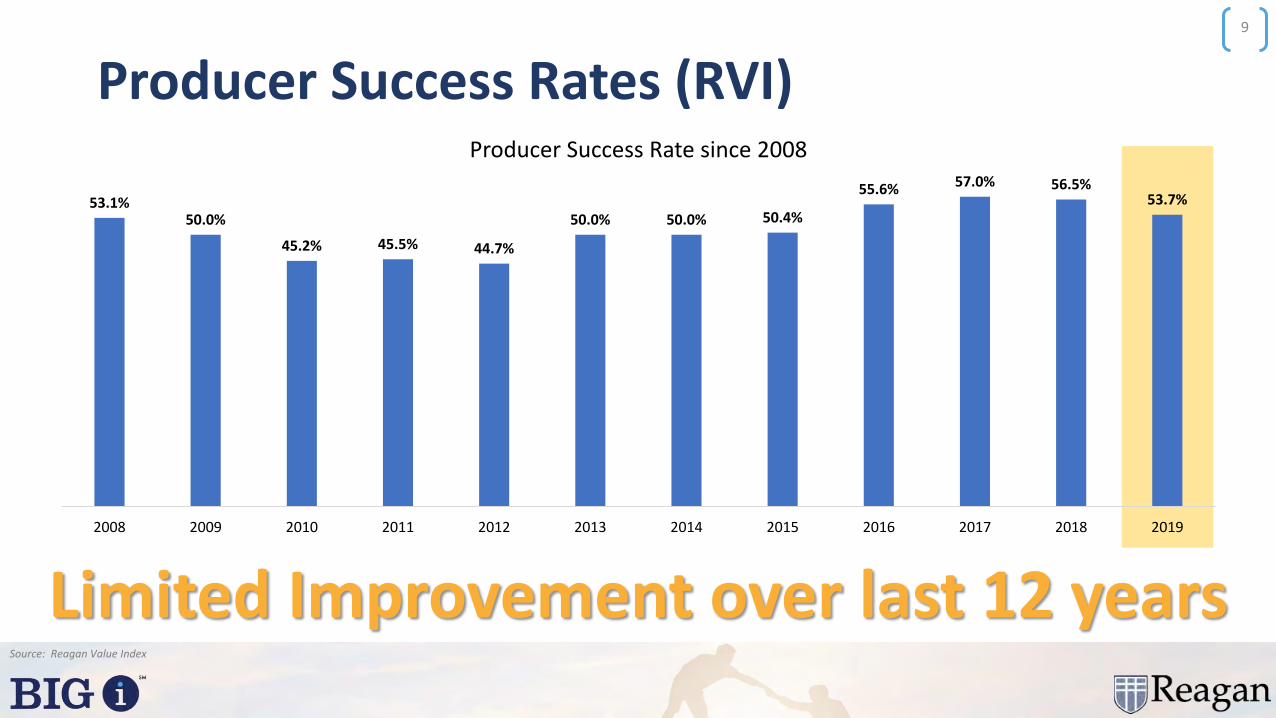

Producer Success Rates

Source: Reagan Value Index

7

53.1%2008 Producer Hiring

Success Rate

The Industry to The Rescue8

Studies / Articles Dedicated Professionals

Producer Success Rates (RVI)

Source: Reagan Value Index

9

53.1%50.0%

45.2% 45.5% 44.7%

50.0% 50.0% 50.4%

55.6% 57.0% 56.5%53.7%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Producer Success Rate since 2008

Limited Improvement over last 12 years

Redefining Success

Source: Over the Cap; The Balance Careers; Monster Finance

10

20%-30%graduation rate

30%-50%make it to Partner

Navy Seal BUDs

63%of players from 2015 draft still on NFL team in 2018

Is Being Successful Worth it?

Source: Reagan Consulting Producer Recruiting & Development Study; Reagan Consulting Analysis

12

Successful Producer Unsuccessful Producer

Starting Salary $60,000 $60,000

Year 2 Compensation $65,000 $32,500

Year 3 Compensation $70,000 $0

Year 4 Compensation Validated (40% / 30%) $0

Year 5 Compensation Validated (40% / 30%) $0

Year 1 Business Written $25,000 $0

Year 2 Business Written $50,000 $0

Year 3 Business Written $75,000 $0

Year 4 Business Written $90,000 $0

Year 5 Business Written $90,000 $0

Year 5 Book $306,000 $0

• The chart at right looks at basic assumptions for a typical producer hire

• We assumed a roughly 20% - 23% margin on the book of business in years 3 – 5

• The book of business is worth 1.5 x revenue - a standard internal valuation multiple

What is the Investment Return for...

Source: Reagan Consulting

13

...one successful producer hire?

5-Year Internal Investment Return of

88.6%

5-Year Cumulative Cash Flow of

$24K

What is the Investment Return for...

Source: Reagan Consulting

14

...one successful producer hire and one unsuccessful producer hire?

5-Year Internal Investment Return of

50.5%

5-Year Cumulative Cash Flow of

($45K)

What is the Investment Return for...

Source: Reagan Consulting

15

...one successful producer hire and two unsuccessful producer hires?

5-Year Internal Investment Return of

33.1%

5-Year Cumulative Cash Flow of

($114K)

What is the Investment Return for...

Source: Reagan Consulting

16

...one successful producer hire and three unsuccessful producer hires?

5-Year Internal Investment Return of

22.2%

5-Year Cumulative Cash Flow of

($183K)

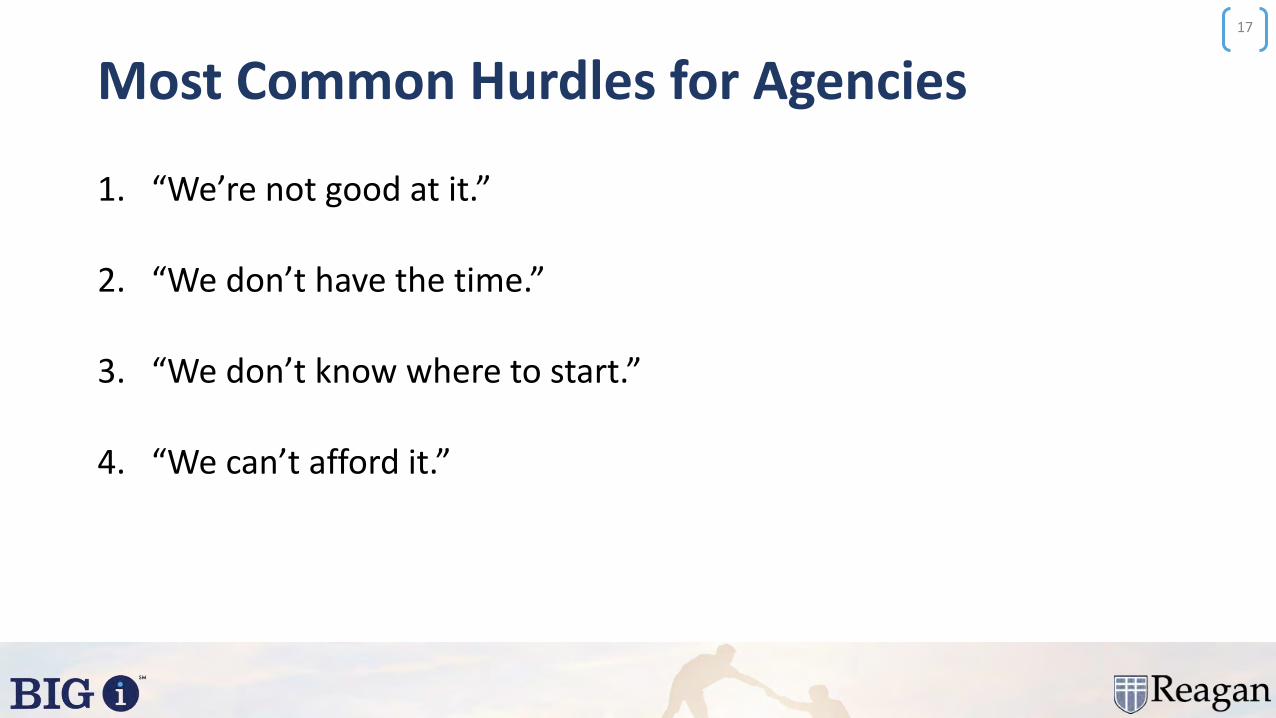

Most Common Hurdles for Agencies

1. “We’re not good at it.”

2. “We don’t have the time.”

3. “We don’t know where to start.”

4. “We can’t afford it.”

17

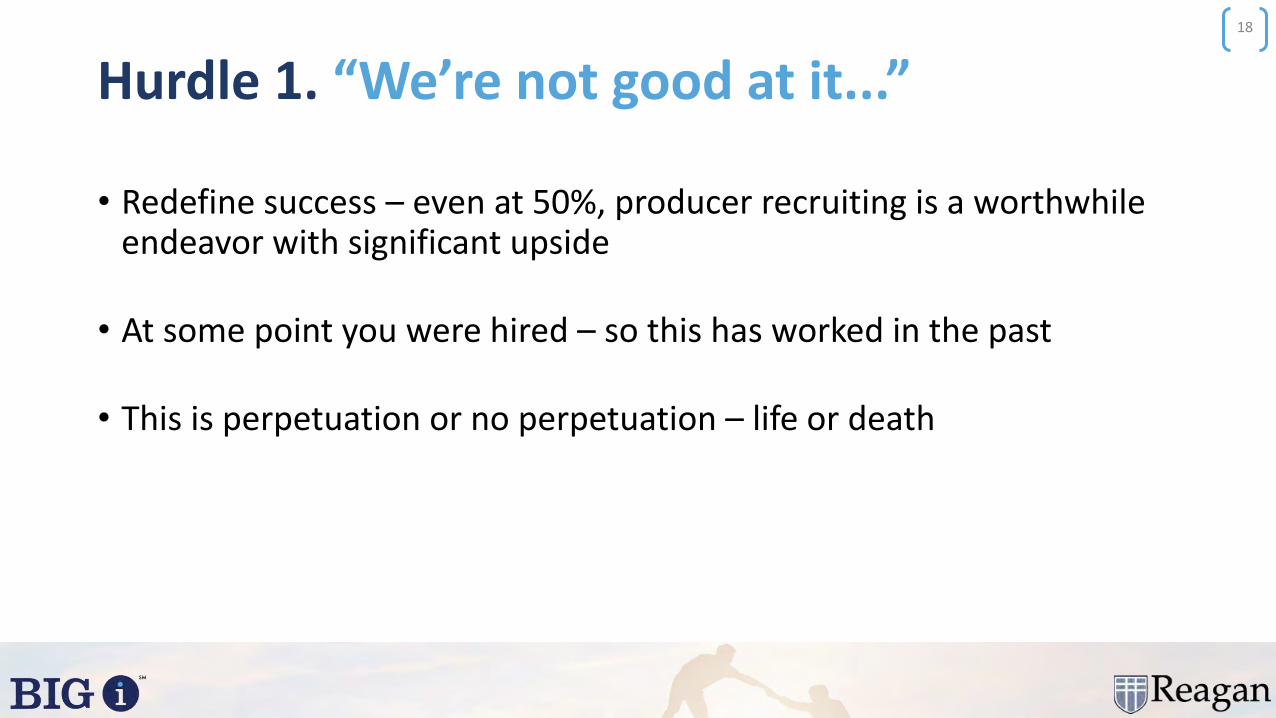

Hurdle 1. “We’re not good at it...”18

• Redefine success – even at 50%, producer recruiting is a worthwhile endeavor with significant upside

• At some point you were hired – so this has worked in the past

• This is perpetuation or no perpetuation – life or death

Hurdle 2. “We don’t have the time...”19

• Someone has to own this

• If you don’t have the time…you don’t understand the importance of it

• Producing producers is way more important than producing new business

20

Hurdle 3. “We don’t know where to start...”

Source: Reagan Consulting Producer Recruiting & Development Study

21

• Start building a plan – how many people should we hire?

• It depends on the following:

• Generational health

• Targeted growth rate (4%, 6%, 8%, 10%, etc.)

• Investment opportunity (what is budget?)

• Hiring success rate

• Internal capacity to hire and train producers

• Rely on the PRAD study →

Hurdle 4. “We can’t afford it…”22

• Can you afford to remain independent?

• Who can’t afford it – the agency itself or agency owners?

The Importance of Recruiting: Three Lessons23

1. Industry standard success produces exceptional returns

2. It is rare that a run of value creation is not precipitated by producer hiring and development

3. You can’t afford to miss the big picture

Do We Have the Right Perspective?

“I don't know if I'm different from everybody else, but there's really only two things to me that are really, really important – recruiting good players in the program and developing those players once they get here.”

- Nick Saban

“That damn game cost me a week of recruiting.”

– Nick Saban, referring to the National Championship Game

24

Discussion Questions for Breakout1) Does your firm place the appropriate emphasis on producer recruiting? If

not, how would you change that?

2) What is stopping your firm from being more successful at producer hiring and development?

3) How does you firm create more time for producer recruiting?

4) Has your agency developed the profile of a successful producer recruit for your firm?

5) What are two things you can do in 2020 to focus on producer recruiting and development – the biggest challenge in our industry and the key to internal perpetuation?

25

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Developing a Sales Culture

Tom Doran and Jim CampbellReagan Consulting

“I know it when I see it.”

32

United States Supreme Court Justice Potter Stewart in 1964 when asked to define “obscenity” in Jacobellis v. Ohio

What is it?

What is it?

33

Outstanding New Business Results

#1 Strategic Focus - New Business

Organization Structured to Support Sales

Aggressive Growth Investments

Ideal home for high-performance

producers

Creative & Entrepreneurial

Strategies to Support Sales

Why does it matter?34

A sales culture is a growth culture. A growth culture…

Supports a Premium Valuation

2:1AND

Leads to long-term viability and prosperity

• Generates a growing profit stream to fund growth and perpetuation investments

• Attracts highest caliber talent in the industry

• Provides market muscle with carriers

• Is simply more fun!The value of a point of growth versus a point of profitability

“Success leaves clues, and if you sow the same seeds, you’ll reap the same rewards.”

35

Author Brad Thor

How to measure it?

How to measure it?

Organic Growth

Sales Velocity

New Business per Producer

36

How to measure it?37

Organic Growth

2018Commission & Fee Income

$6,000,000

2019Commission & Fee Income

$7,100,00018.3%

($600,000) Book purchase

$6,500,000 Adjusted C&F Income

2018Commission & Fee Income

$6,000,000

2019Commission & Fee Income

$7,100,000

8.3%

Source: 2019 Best Practices Study

38

BPS Revenue Category Median Top Quartile

<$1.25M 9.6% 26.2%

$1.25M - $2.5M 7.9% 30.1%

$2.5M - $5.0M 7.9% 19.2%

$5.0M - $10.0M 7.5% 16.2%

$10.0M - $25.0M 7.1% 15.1%

>$25.0M 6.4% 11.9%

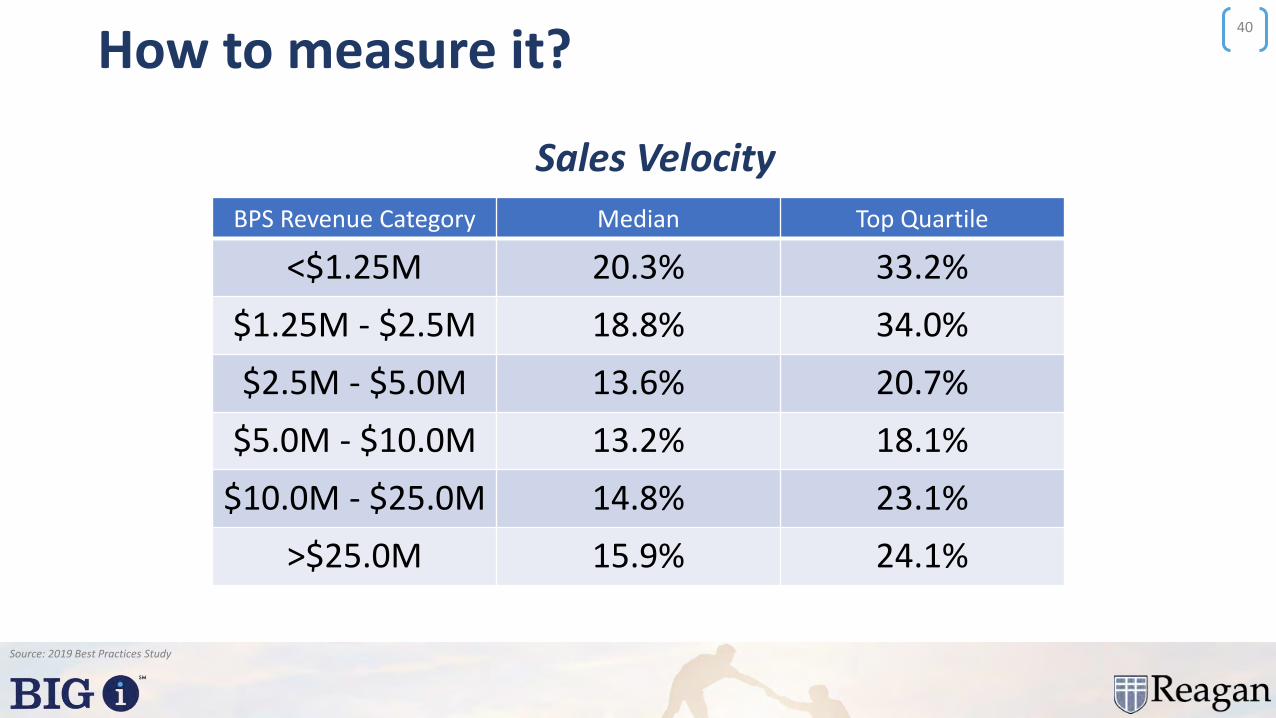

How to measure it?

Organic Growth

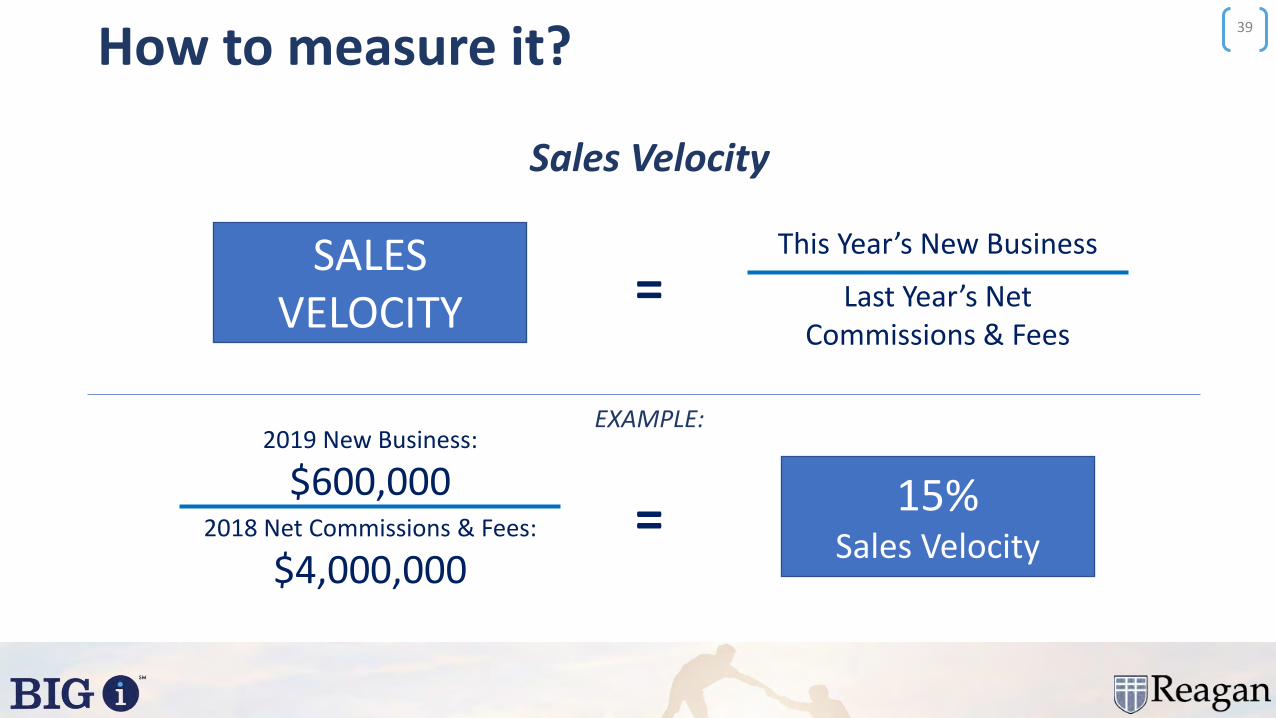

How to measure it?39

SALESVELOCITY

This Year’s New Business

Last Year’s Net Commissions & Fees

=

Sales Velocity

=

EXAMPLE:

15% Sales Velocity

2019 New Business:

$600,0002018 Net Commissions & Fees:

$4,000,000

How to measure it?

Source: 2019 Best Practices Study

40

BPS Revenue Category Median Top Quartile

<$1.25M 20.3% 33.2%

$1.25M - $2.5M 18.8% 34.0%

$2.5M - $5.0M 13.6% 20.7%

$5.0M - $10.0M 13.2% 18.1%

$10.0M - $25.0M 14.8% 23.1%

>$25.0M 15.9% 24.1%

Sales Velocity

How to measure it?

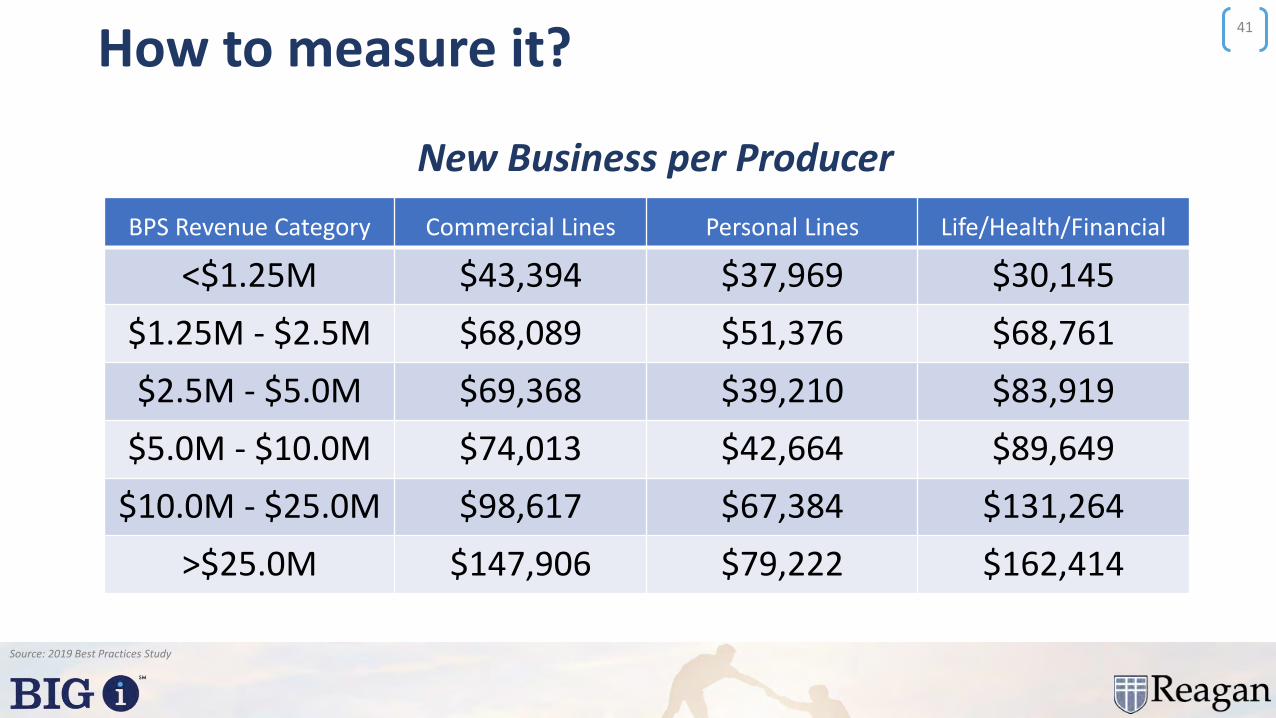

Source: 2019 Best Practices Study

41

BPS Revenue Category Commercial Lines Personal Lines Life/Health/Financial

<$1.25M $43,394 $37,969 $30,145

$1.25M - $2.5M $68,089 $51,376 $68,761

$2.5M - $5.0M $69,368 $39,210 $83,919

$5.0M - $10.0M $74,013 $42,664 $89,649

$10.0M - $25.0M $98,617 $67,384 $131,264

>$25.0M $147,906 $79,222 $162,414

New Business per Producer

How?

42

Essential Elements of a Great Sales Culture43

Model Leaders

Investment in Talent

Accountability

“At least if he had been walking with us, he would have had some moral authority.”

44

Lt. Gen. John R. Vines

Essential Elements of a Great Sales Culture45

Model LeadersInvestment in

TalentAccountability

NUPP and Organic Growth

9.6%

7.9% 7.9% 7.5% 7.1%6.4%

15.5%

11.7%

9.0%8.3%

7.4%8.3%

<$1.25 $1.25-$2.5M

$2.5-$5.0M

$5.0-$10.0M

$10.0-$25.0M

>$25.0M

Do the Top Quartile NUPP firms have above average organic growth?

All BPS Firms' Median Organic Growth Top Quartile NUPP Firms' Median Organic Growth

Source: 2019 Best Practices Study

46

Essential Elements of a Great Sales Culture47

Model LeadersInvestment in

TalentAccountability

Effective Accountability

• Are performance expectations clearly defined and communicated?

• Are we coaching / mentoring?

• Do we have a plan to address those who fall behind?

• Do we celebrate wins and recognize achievements?

48

Roundtable Discussion Questions1) How does your leadership team model leadership for your producers?

2) What do you do to recognize achievements and celebrate victories with your team?

3) What one change has been most impactful in enhancing your sales culture?

4) How do you motivate and help mature producers with big books of business to continue to generate new business?

5) What specific practices have helped you to make your sales meetings more effective?

6) What commission percentages do you pay your producers for new / renewal business? Are there compensation Best Practices that you have found helpful in motivating new business?

49

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Staying Private

Brian McNeely and John MerrillReagan Consulting

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

6

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

7

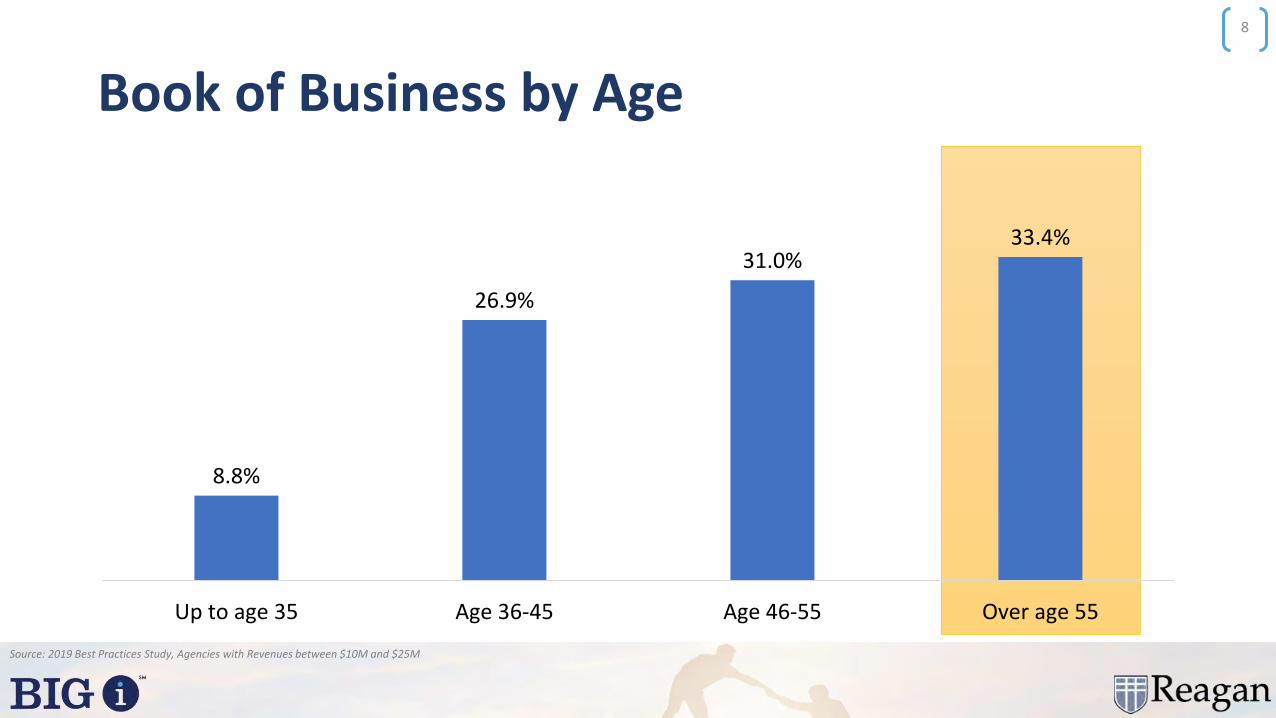

Book of Business by Age

8.8%

26.9%

31.0%33.4%

Up to age 35 Age 36-45 Age 46-55 Over age 55

8

Source: 2019 Best Practices Study, Agencies with Revenues between $10M and $25M

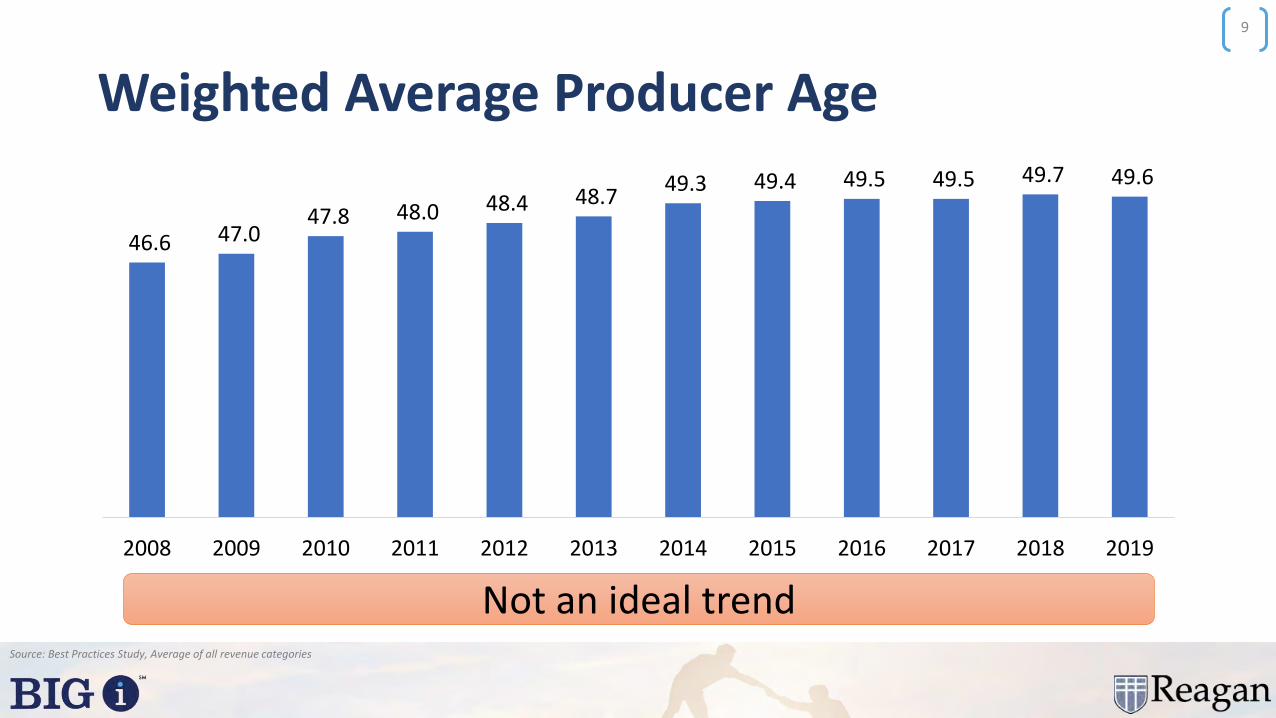

Weighted Average Producer Age

46.6 47.0 47.8 48.0 48.4 48.7

49.3 49.4 49.5 49.5 49.7 49.6

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: Best Practices Study, Average of all revenue categories

9

Not an ideal trend

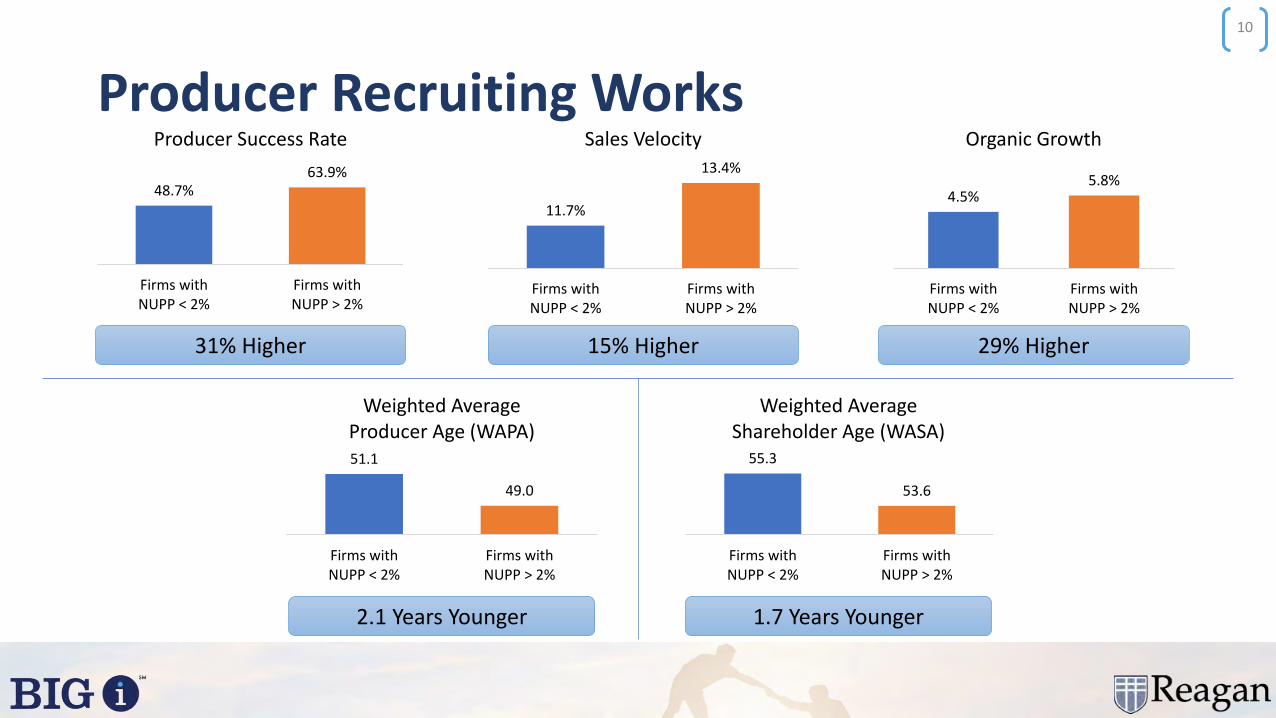

Producer Recruiting Works

10

48.7%63.9%

Firms withNUPP < 2%

Firms withNUPP > 2%

Producer Success Rate

51.1

49.0

Firms withNUPP < 2%

Firms withNUPP > 2%

Weighted Average Producer Age (WAPA)

4.5%5.8%

Firms withNUPP < 2%

Firms withNUPP > 2%

Organic Growth

11.7%

13.4%

Firms withNUPP < 2%

Firms withNUPP > 2%

Sales Velocity

55.3

53.6

Firms withNUPP < 2%

Firms withNUPP > 2%

Weighted Average Shareholder Age (WASA)

15% Higher 29% Higher

2.1 Years Younger 1.7 Years Younger

31% Higher

Non-Producer Average Age

Top Quartile Bottom Quartile

36 38 40 42 44 46 48 50

RVI

Average Age of Service/Sales Support Staff

MEDIAN:

Source: Reagan Value Index

11

It’s not just about production

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

12

FASTERGROWING &

MOREPROFITABLE

Why it Works

NOGEOGRAPHICBOUNDARIES

SIZE DOESN’T ALWAYS MATTER

13

What is Specialization?

14

In-depth industry / product knowledge

Concentrations of Business

Specialization is not . . .

Just Marketing

Restrictive

Specialization is . . .

Empowering

Difference-making for clients

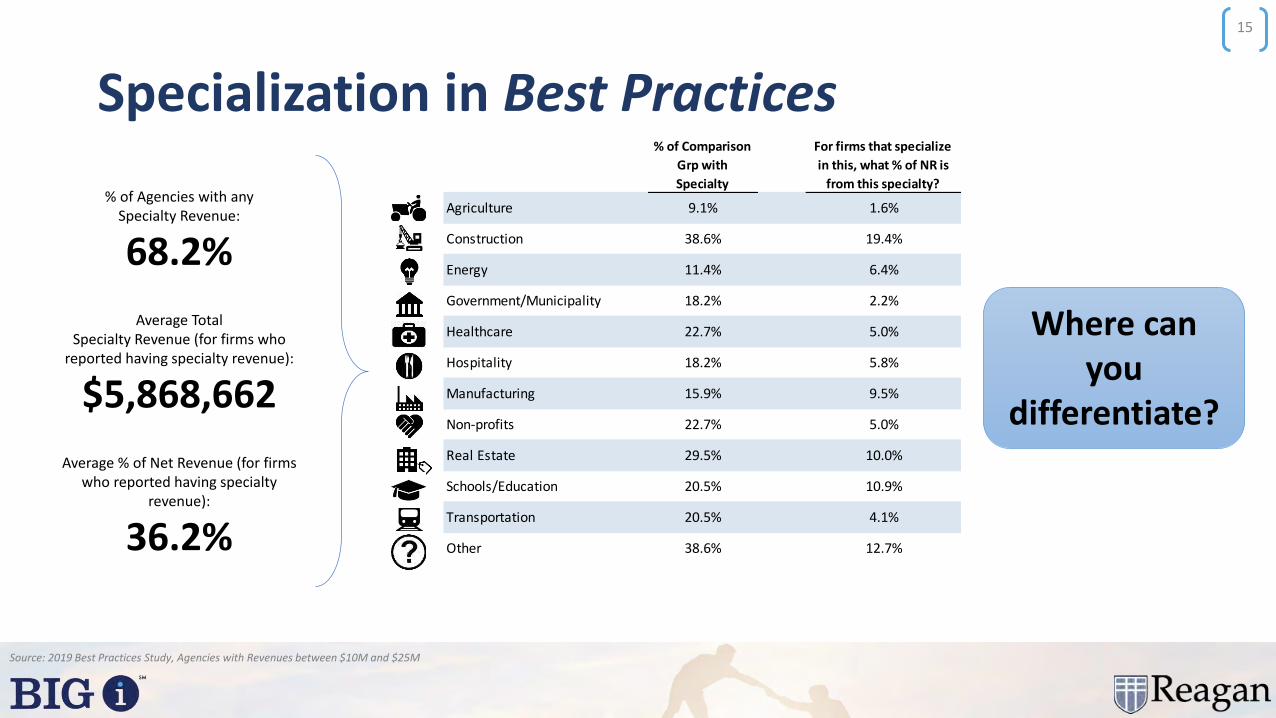

Specialization in Best Practices

Source: 2019 Best Practices Study, Agencies with Revenues between $10M and $25M

1.6%

Transportation

Other

19.4%

6.4%

2.2%

22.7%

18.2%

5.0%

18.2%

Healthcare

Hospitality

Manufacturing

5.0%

5.8%

9.5%

Energy

12.7%

Schools/Education

22.7%

29.5%

20.5%

20.5%

Real Estate

Construction

Non-profits

% of Comparison

Grp with

Specialty

Agriculture

38.6%

15.9%

10.9%

10.0%

For firms that specialize

in this, what % of NR is

from this specialty?

11.4%

9.1%

38.6%

Government/Municipality

4.1%

% of Agencies with any Specialty Revenue:

68.2%

Average Total Specialty Revenue (for firms who

reported having specialty revenue):

$5,868,662

Average % of Net Revenue (for firms who reported having specialty

revenue):

36.2%

15

Where can you

differentiate?

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

16

Tools & Resources

17

What the customer wants…

Risk Modeling

Loss Control

Risk Mitigation

Risk Transfer

Training

Claims Advocacy

Call Center Support

Compliance Support & Oversight

Billing Consolidation

HR Administration

Administrative Assistance

World Class Local Touch

Health Promotion

Employee Communication

Strategic Forecast Model

Data Analytics & Informatics

Pharmacy Management

ACA Impact Analysis

Digital Solutions

Online Learning

Actuarial and Underwriting

Appraisal Services

Client-Focused Attention

Personal Asset Protection Services

Multi-Generational PlanningClaims Advocates

Industry SpecializationProprietary Products

Market Insight

Benchmarking & Business Analytics

Online Tools with 24/7 Access

Executive & Professional Specialty Practice

Safety & Health Management Environmental ConsultingInternational ResourcesPrivate Equity

Industry Specialization

Educational Seminars

Auto & Exotic Vehicle Insurance

High Net Worth

Collectibles

Farms & Ranches

Homeowners Life & Disability Insurance

Contract Surety

Access to Tools and Resources

18

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

19

M&A Activity

14% 15%23% 27% 30%

42% 41%46%

55% 54%59%

20%28%

32%29%

28%

26% 28%24%

21% 22%19%

22%

28%

15% 16% 13%

10% 10%14%

10% 11% 9%

24%

17% 17% 15% 20%13% 15% 9% 9% 8% 10%20%

14% 13% 14% 10% 9% 6% 8% 5% 6% 3%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Private Equity Private Brokers Other Public Brokers Banks

Source: SNL Financial as of June 30, 2019 (based on Announcement Date). Includes whole company, franchise and asset sales.

53%59%

24%22%

10%9%

8%7%

5% 3%

H1 2018 H1 2019

20

Producer lift outsThe Free Agent Opportunity in Our Industry

INSURANCE

I need resources and a

platform for growing

my business.

I need to find a new

home for me and my

book of business.

21

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

22

The Four Pillars of Perpetuation

23

ReasonableSellers

Current Market Pricing

Source: Good quality agents and brokers, $3-$10 million in revenue

24

6.0x 5.8x 6.0x 6.3x 6.5x 6.8x 7.0x 7.5x 8.0x 8.0x 9.0x

3.0x 3.0x 2.5x 2.5x 2.5x 3.0x 3.0x

3.0x 3.0x 3.0x

3.0x

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Typical Guaranteed Price Earn-Out Opportunity

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

25

Debt

% of Firms that have Identified Debt 62.7%

Average Total Debt

Total Leverage (Total Debt / Pro Forma EBITDA)

Average Effective Interest Rate

Average Term (Years to Maturity) 5.5

$4,131,024

1.2x

4.3%

Source: 2019 Best Practices Study, Agencies with Revenues between $10M and $25M

26

A debt averse industry

>6.0x

2.5x

1.2x

PrivateEquity

Public Brokers

BPS Firms($10-$25M in Rev)

Debt to EBITDA Ratio

Source: 2019 Best Practices Study, Agencies with Revenues between $10M and $25M

27

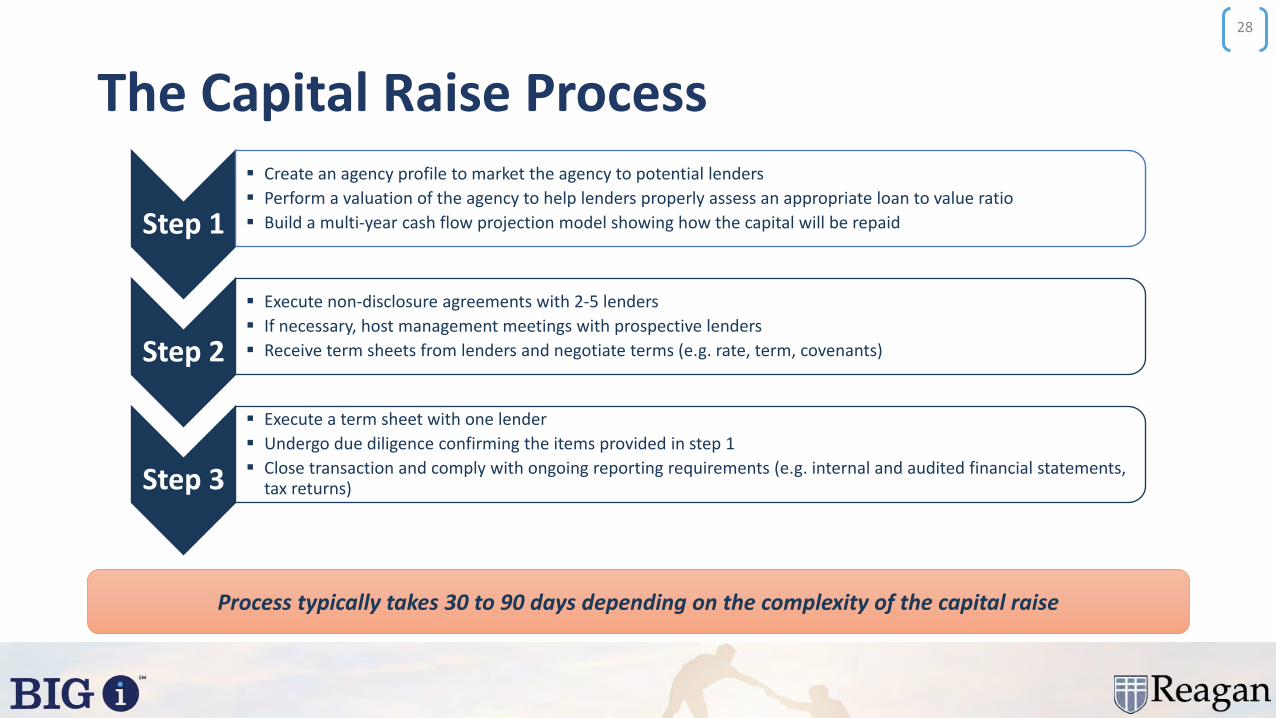

The Capital Raise Process

28

Step 1

▪ Create an agency profile to market the agency to potential lenders

▪ Perform a valuation of the agency to help lenders properly assess an appropriate loan to value ratio

▪ Build a multi-year cash flow projection model showing how the capital will be repaid

Step 2

▪ Execute non-disclosure agreements with 2-5 lenders

▪ If necessary, host management meetings with prospective lenders

▪ Receive term sheets from lenders and negotiate terms (e.g. rate, term, covenants)

Step 3

▪ Execute a term sheet with one lender

▪ Undergo due diligence confirming the items provided in step 1

▪ Close transaction and comply with ongoing reporting requirements (e.g. internal and audited financial statements, tax returns)

Process typically takes 30 to 90 days depending on the complexity of the capital raise

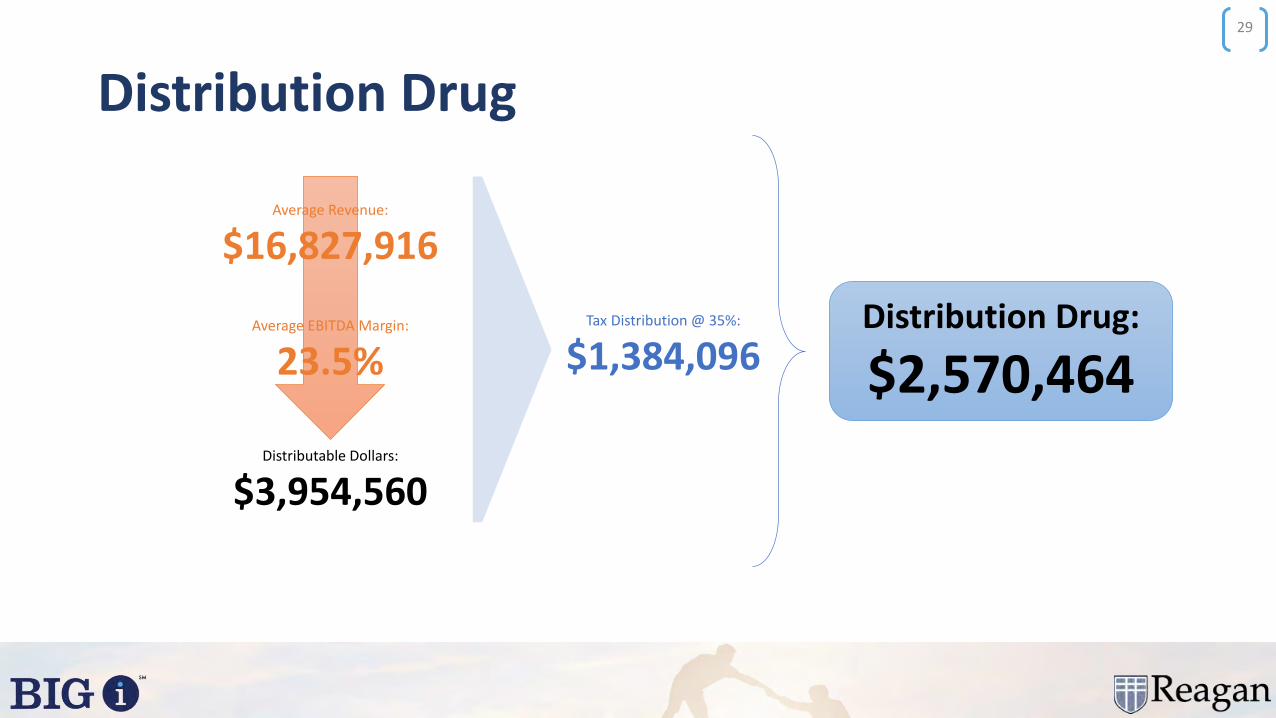

Distribution Drug

29

Average Revenue:

$16,827,916

Average EBITDA Margin:

23.5%Distribution Drug:

$2,570,464Distributable Dollars:

$3,954,560

Tax Distribution @ 35%:

$1,384,096

Distribution Drug

30

Obviously reinvesting might mean taking a pay cut if you’re the owner, but that’s how a company progresses.

Forbes

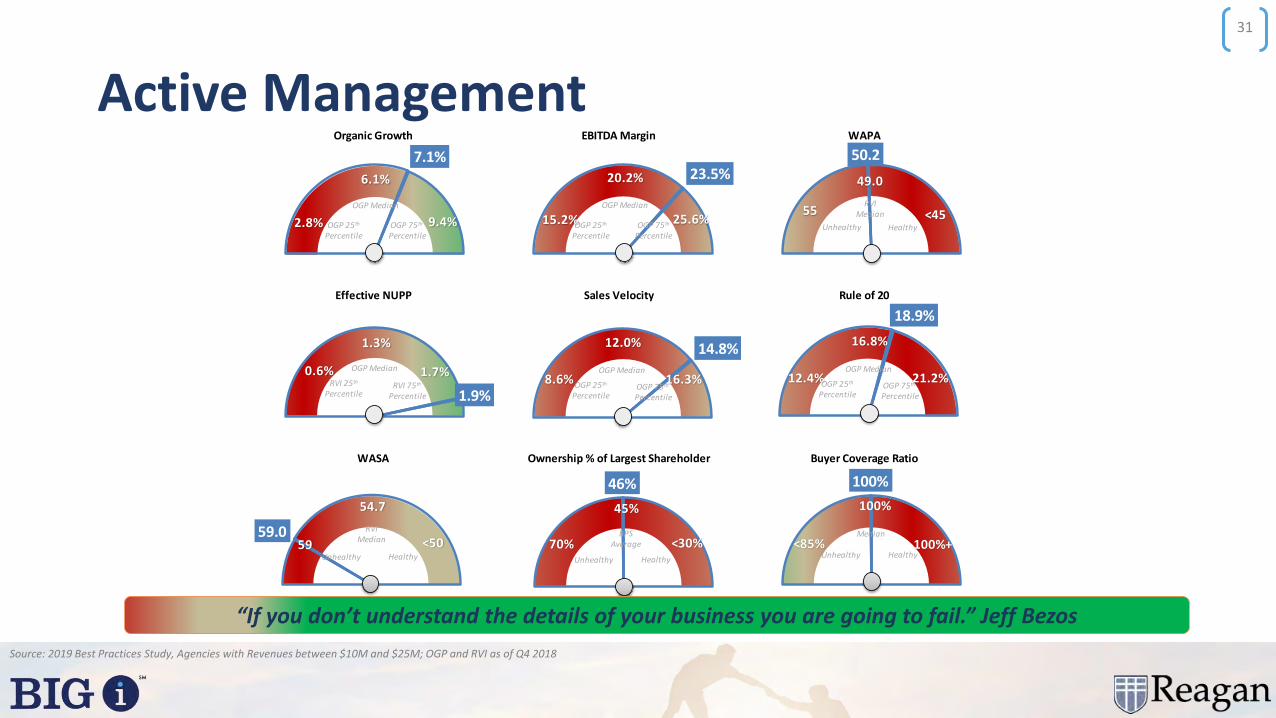

Active Management

31

Organic Growth EBITDA Margin WAPA

Effective NUPP Sales Velocity Rule of 20

WASA Ownership % of Largest Shareholder Buyer Coverage Ratio

46%

18.9%

14.8%

23.5%50.2

1.9%

7.1%20.2% 49.0

2.8%

6.1%

9.4%OGP 75th

PercentileOGP 25th

Percentile

15.2% 25.6%OGP 75th

Percentile

OGP Median

OGP 25th

Percentile

<45Healthy

RVI Median

Unhealthy

0.6%

1.3%

1.7%RVI 75th

Percentile

RVI 25th

Percentile

8.6%

12.0%

16.3%OGP 75th

Percentile

OGP 25th

Percentile

55

Healthy

BPSAverage

Unhealthy

100%

<85%

100%

100%+Median

HealthyUnhealthy

OGP Median

OGP MedianOGP Median

70%

45%

<30%

12.4%

16.8%

21.2%OGP 75th

Percentile

OGP 25th

Percentile

OGP Median

59.0

54.7

59 <50Healthy

RVI Median

Unhealthy

Source: 2019 Best Practices Study, Agencies with Revenues between $10M and $25M; OGP and RVI as of Q4 2018

“If you don’t understand the details of your business you are going to fail.” Jeff Bezos

Active Management

32

Aggregation Groups

33

5 Areas of

1

Talent

2

Specialization

3

Tools & Resources

4

Be Nimble & Opportunistic

5

Perpetuation Plan

34

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

Value Creation: Who Does it Best and How They Do It

Bobby Reagan and Mitchell GentryReagan Consulting

How do you measure value?

8

Organic Growth

Profitability

Total Revenues

Employees:CapabilityStability

Age

Customers:Size

StabilityProfitability

Fair Market Value

INTERNAL(Appraisal)

Fair Market Value

EXTERNAL(Offer or

Purchase)

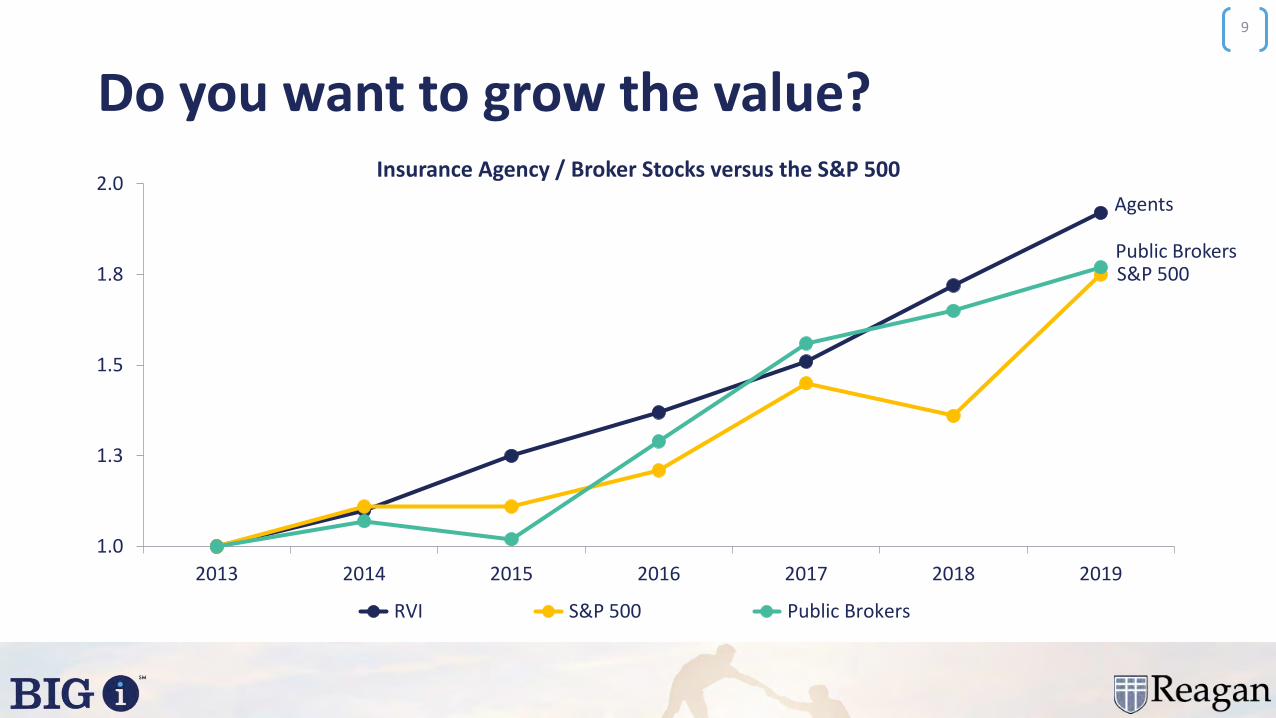

Do you want to grow the value?

9

Insurance Agency / Broker Stocks versus the S&P 500

1.0

1.3

1.5

1.8

2.0

2013 2014 2015 2016 2017 2018 2019

RVI S&P 500 Public Brokers

Agents

Public BrokersS&P 500

Q4 2018 BPS Scatterplot

Source: 2019 Best Practices Study

10

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

-10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

Pro

fita

bili

ty (

EBIT

DA

Mar

gin

)

Organic Growth

Agencies with revenues less than $1.25M Agencies with revenues between $1.25 and $2.5M

Value Creation over the next decade

• How are you going to do it?

• Should you maximize profits? Organic Growth? Both?

• Which is more important: profit or growth?

• If you make investments, how and where should they be made?

11

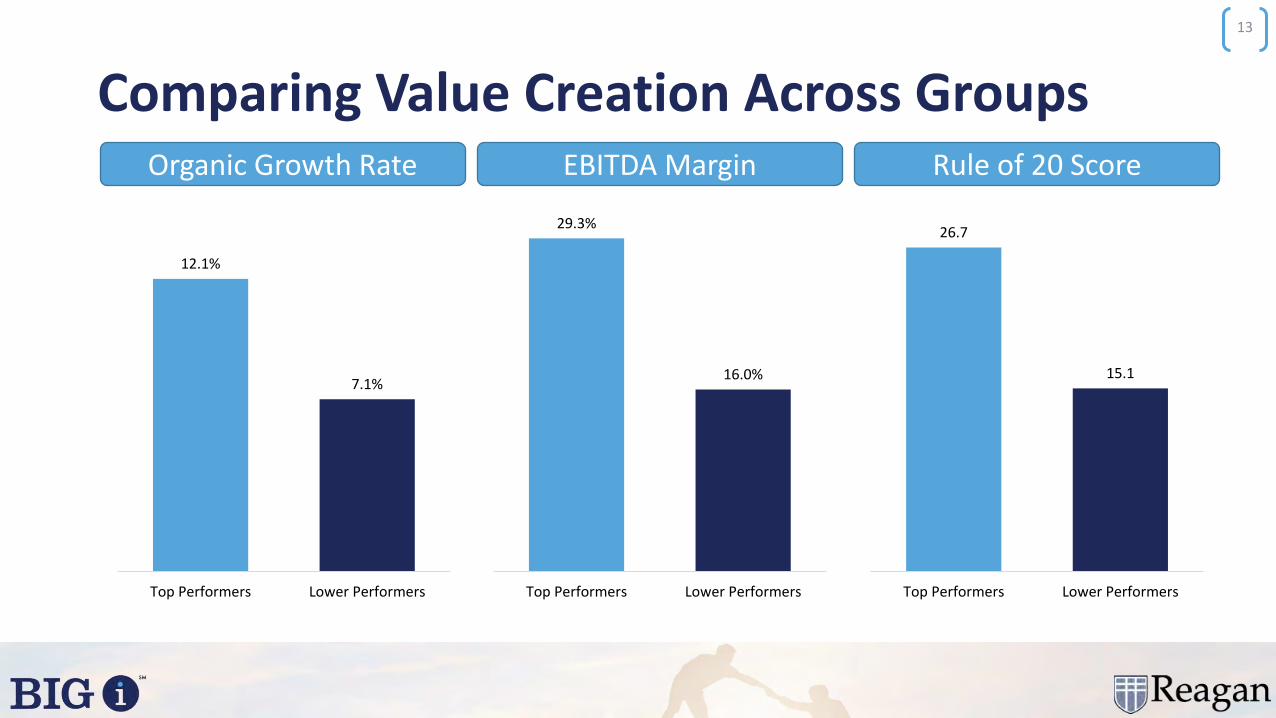

Who is most successfully growing value?• We scored Best Practices firms with $5 to $25 million in revenues

based on their performance across 10 metrics, including organic growth, EBITDA margin and Rule of 20 score, among others.

• We then compared the performance of 15 “top-performing” firms to that of the 15 firms with the lowest composite score across 19 variables that could potentially drive value creation.

• We would emphasize that, while this data is limited to 2018 performance, most of the selected firms are continually excelling relative to their peers.

12

Comparing Value Creation Across Groups

13

Organic Growth Rate

12.1%

7.1%

Top Performers Lower Performers

EBITDA Margin Rule of 20 Score

29.3%

16.0%

Top Performers Lower Performers

26.7

15.1

Top Performers Lower Performers

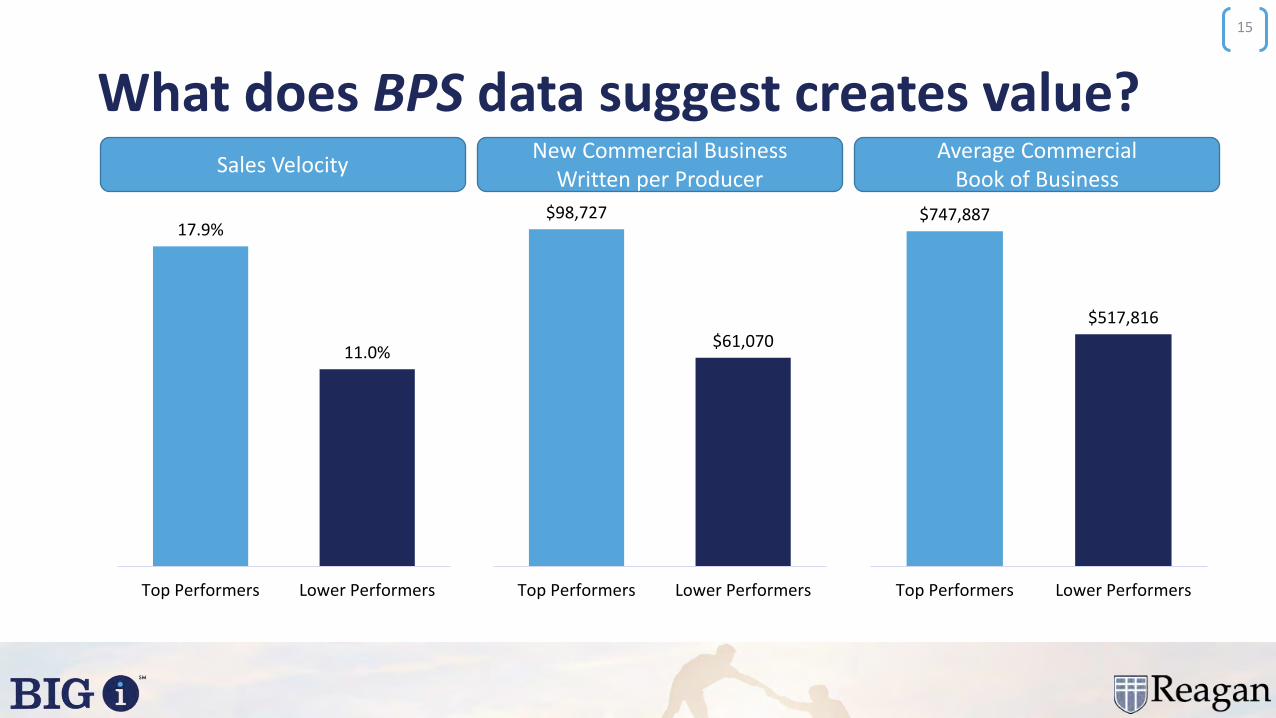

What does BPS data suggest creates value?

• According to the Best Practices data, outsized performance in the following metrics plays a meaningful role in value creation:

14

Sales Velocity

Producer book size

Weighted average shareholder age (WASA)

Revenue per employee

Spread per employee

Specialization (% of revenue)

What does BPS data suggest creates value?

15

Sales Velocity

17.9%

11.0%

Top Performers Lower Performers

New Commercial Business Written per Producer

Average Commercial Book of Business

$98,727

$61,070

Top Performers Lower Performers

$747,887

$517,816

Top Performers Lower Performers

What does BPS data suggest creates value?

16

Revenue per Employee

41.8%

33.5%

Top Performers Lower Performers

Spread per Employee Spread as a % of Revenue

$220,460

$170,635

Top Performers Lower Performers

$92,243

$55,426

Top Performers Lower Performers

What does BPS data suggest creates value?

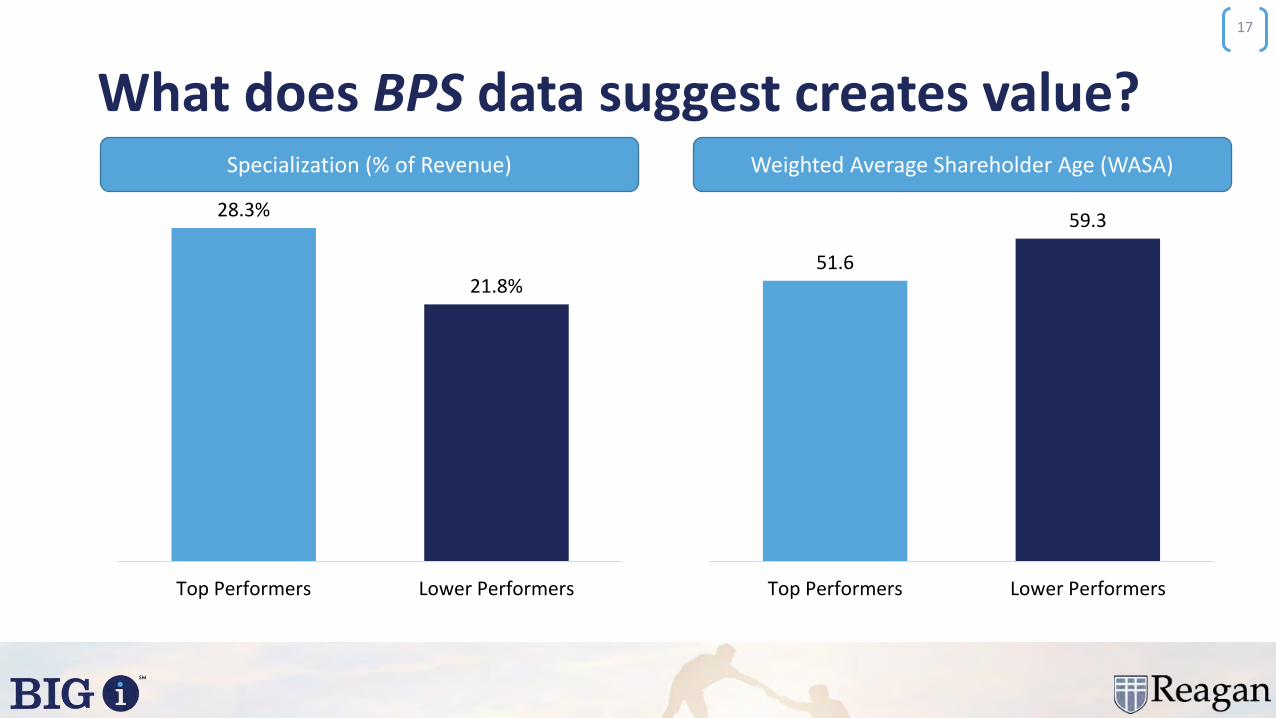

17

Specialization (% of Revenue)

28.3%

21.8%

Top Performers Lower Performers

Weighted Average Shareholder Age (WASA)

51.6

59.3

Top Performers Lower Performers

This BPS data is helpful and is clear evidence of higher value creation, but…

18

It does not answer the question of the steps that need to be taken or the strategic path to superior value creation.

1995 – 2020

19

Uniquely positioned to know how value has been and can be created

Annually appraised their operating performance

Facilitated strategic planning sessions for many

Consulted with the highest performing firms in the U.S.

What we know about superior value creation…• Not everyone does it the same way

• Strategies generally driven by market, history, opportunity

• All have strengths and weaknesses but several key things will set them apart

• All have a vision, are driven and are able to execute

• All succeed based on their ability to attract, retain and motivate talented people

20

How the most successful are growing value:

1) Superior leadership and management

2) Superior producers, sales process and sales leadership

3) Gaining competitive advantage

4) Superior operations, efficiency and customer service

5) Superior ownership, perpetuation and sustainability model

6) Successful acquisition strategy

21

How the most successful are growing value

1) Superior Leadership and Management

• Vision / Mission, Plan and Execution

• Culture and Corporate Values

• Recruiting (People, Carriers, Programs, and Acquisitions)

22

How the most successful are growing value

2) Superior Producers, Sales Process, and Sales Leadership

• Better people, recruiting, training

• Better sales culture

• Better sales tools and resources

• Better sales process

• More accountability and sales leadership

• Level of producer hiring aligned with objectives and needs

23

How the most successful are growing value

3) Gaining Competitive advantage

24

• Better Employees

• Better Culture

• Specialization

• Value Added Capabilities

• Carrier access, relations, and leverage

• Better reputation and brand

• Better market(s), niches, centers of influence

• Disciplined business development focus

• Leveraging big data / information

• Innovation

How the most successful are growing value

4) Superior Operations, Efficiency, Customer Service

• Operating metrics closely tracked and managed

• Technology effectively utilized

• Better structure, work flows, and procedures

• Better people, training, motivation, and management

• Service offerings properly aligned by client segments

• Quality control

• Purging and avoiding non-strategic and unprofitable clients or blocks of business

25

How the most successful are growing value

5) Superior Ownership, Perpetuation and Sustainability Model

• Healthy investment in hiring and people development

• Agency equity property valued and owned

• Plan in place for the perpetuation of ownership and operations

• Ownership used to attract, retain and motivate key employees

• Proper shareholder and employment agreements in place

26

How the most successful are growing value

6) Successful Acquisition Strategy

• Team Lift Outs

• Producers with Books

• Mergers

• Acquisitions

• Use of Leverage (Debt)

27

If we had to summarize how superior value is achieved…

28

Committed to Grow

Creating Organizations with Capacity

to Grow

Investing in Growth

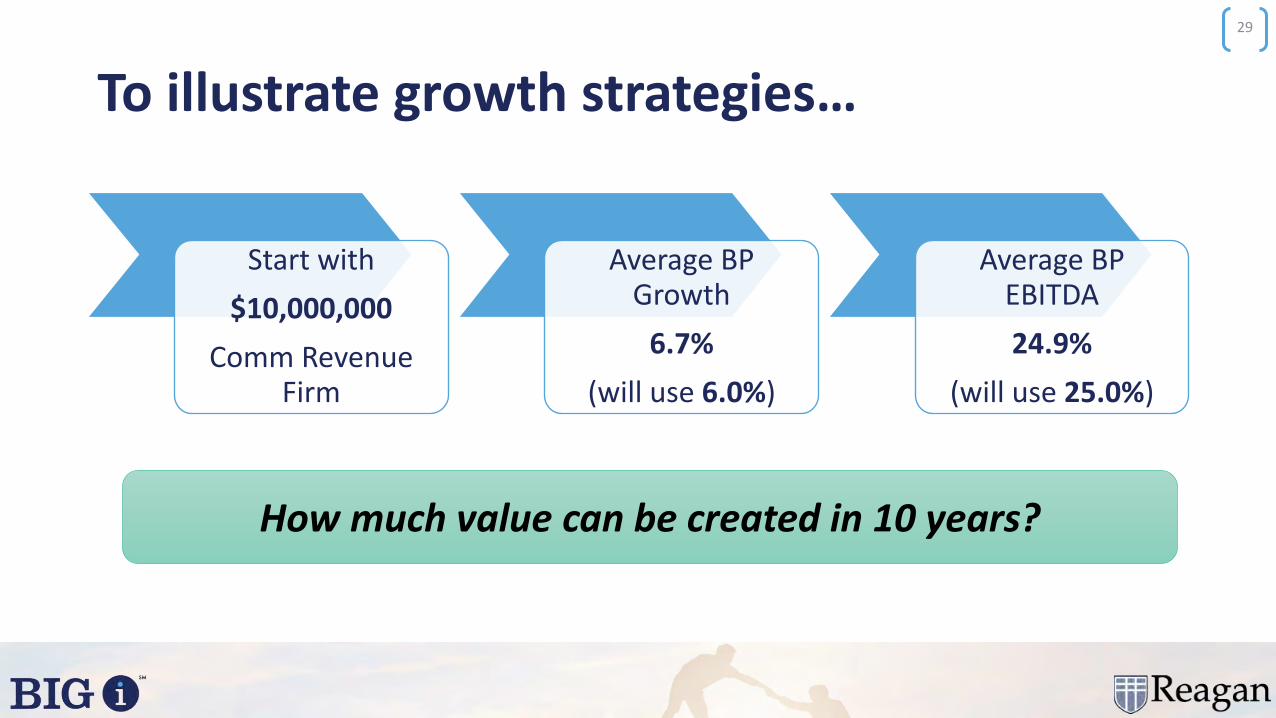

To illustrate growth strategies…

29

Start with

$10,000,000

Comm Revenue Firm

Average BP Growth

6.7%

(will use 6.0%)

Average BP EBITDA

24.9%

(will use 25.0%)

How much value can be created in 10 years?

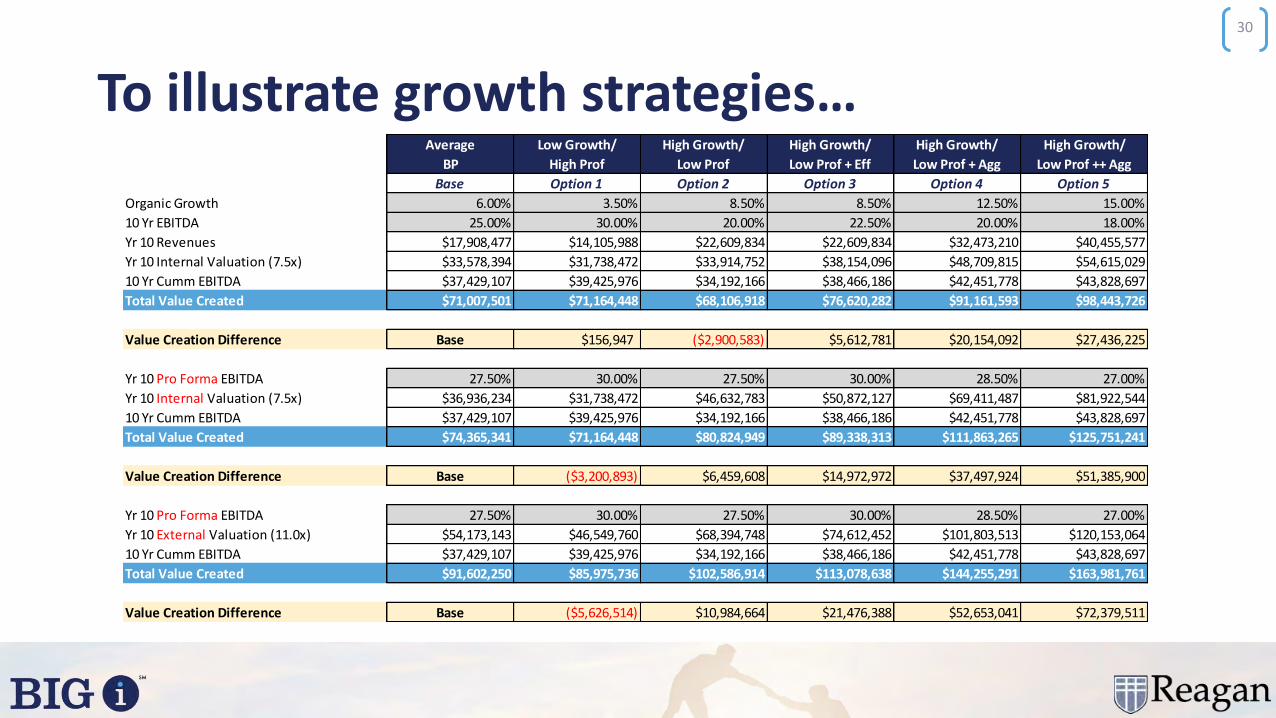

To illustrate growth strategies…

30

Average

BP

Base

Organic Growth 6.00%

10 Yr EBITDA 25.00%

Yr 10 Revenues $17,908,477

Yr 10 Internal Valuation (7.5x) $33,578,394

10 Yr Cumm EBITDA $37,429,107

Total Value Created $71,007,501

Value Creation Difference Base

Yr 10 Pro Forma EBITDA 27.50%

Yr 10 Internal Valuation (7.5x) $36,936,234

10 Yr Cumm EBITDA $37,429,107

Total Value Created $74,365,341

Value Creation Difference Base

Yr 10 Pro Forma EBITDA 27.50%

Yr 10 External Valuation (11.0x) $54,173,143

10 Yr Cumm EBITDA $37,429,107

Total Value Created $91,602,250

Value Creation Difference Base

Average

BP

Low Growth/

High Prof

High Growth/

Low Prof

High Growth/

Low Prof + Eff

High Growth/

Low Prof + Agg

High Growth/

Low Prof ++ Agg

Base Option 1 Option 2 Option 3 Option 4 Option 5

Organic Growth 6.00% 3.50% 8.50% 8.50% 12.50% 15.00%

10 Yr EBITDA 25.00% 30.00% 20.00% 22.50% 20.00% 18.00%

Yr 10 Revenues $17,908,477

Yr 10 Internal Valuation (7.5x) $33,578,394

10 Yr Cumm EBITDA $37,429,107

Total Value Created $71,007,501

Value Creation Difference Base

Yr 10 Pro Forma EBITDA 27.50%

Yr 10 Internal Valuation (7.5x) $36,936,234

10 Yr Cumm EBITDA $37,429,107

Total Value Created $74,365,341

Value Creation Difference Base

Yr 10 Pro Forma EBITDA 27.50%

Yr 10 External Valuation (11.0x) $54,173,143

10 Yr Cumm EBITDA $37,429,107

Total Value Created $91,602,250

Value Creation Difference Base

Average

BP

Low Growth/

High Prof

High Growth/

Low Prof

High Growth/

Low Prof + Eff

High Growth/

Low Prof + Agg

High Growth/

Low Prof ++ Agg

Base Option 1 Option 2 Option 3 Option 4 Option 5

Organic Growth 6.00% 3.50% 8.50% 8.50% 12.50% 15.00%

10 Yr EBITDA 25.00% 30.00% 20.00% 22.50% 20.00% 18.00%

Yr 10 Revenues $17,908,477 $14,105,988 $22,609,834 $22,609,834 $32,473,210 $40,455,577

Yr 10 Internal Valuation (7.5x) $33,578,394 $31,738,472 $33,914,752 $38,154,096 $48,709,815 $54,615,029

10 Yr Cumm EBITDA $37,429,107 $39,425,976 $34,192,166 $38,466,186 $42,451,778 $43,828,697

Total Value Created $71,007,501 $71,164,448 $68,106,918 $76,620,282 $91,161,593 $98,443,726

Value Creation Difference Base $156,947 ($2,900,583) $5,612,781 $20,154,092 $27,436,225

Yr 10 Pro Forma EBITDA 27.50% 30.00% 27.50% 30.00% 28.50% 27.00%

Yr 10 Internal Valuation (7.5x) $36,936,234 $31,738,472 $46,632,783 $50,872,127 $69,411,487 $81,922,544

10 Yr Cumm EBITDA $37,429,107 $39,425,976 $34,192,166 $38,466,186 $42,451,778 $43,828,697

Total Value Created $74,365,341 $71,164,448 $80,824,949 $89,338,313 $111,863,265 $125,751,241

Value Creation Difference Base ($3,200,893) $6,459,608 $14,972,972 $37,497,924 $51,385,900

Yr 10 Pro Forma EBITDA 27.50% 30.00% 27.50% 30.00% 28.50% 27.00%

Yr 10 External Valuation (11.0x) $54,173,143 $46,549,760 $68,394,748 $74,612,452 $101,803,513 $120,153,064

10 Yr Cumm EBITDA $37,429,107 $39,425,976 $34,192,166 $38,466,186 $42,451,778 $43,828,697

Total Value Created $91,602,250 $85,975,736 $102,586,914 $113,078,638 $144,255,291 $163,981,761

Value Creation Difference Base ($5,626,514) $10,984,664 $21,476,388 $52,653,041 $72,379,511

10 Year Value Creation

$7

1,0

07

,50

1

$7

1,1

64

,44

8

$6

8,1

06

,91

8

$7

6,6

20

,28

2

$9

1,1

61

,59

3

$9

8,4

43

,72

6

$7

4,3

65

,34

1

$7

1,1

64

,44

8

$8

0,8

24

,94

9

$8

9,3

38

,31

3

$1

11

,86

3,2

65

$1

25

,75

1,2

41

$9

1,6

02

,25

0

$8

5,9

75

,73

6

$1

02

,58

6,9

14

$1

13

,07

8,6

38

$1

44

,25

5,2

91

$1

63

,98

1,7

61

$0

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

$140,000,000

$160,000,000

$180,000,000

Base Option 1 Option2 Option3 Option4 Option5

10 Year Internal Value Created 10 Yr Pro Forma Internal Value Created 10 Yr Pro Forma External Value Created

31

Organic Growth 6.0% 3.5% 8.5% 8.5% 12.5% 15.0%

EBITDA 25.0% 30.0% 20.0% 22.5% 20.0% 18.0%

Pro Forma EBITDA 27.5% 30.0% 27.5% 30.0% 28.5% 27.0%

Base Option 1 Option 2 Option 3 Option 4 Option 5

An Actual Client’s Value Creation Strategy

1) Changed the firm’s governance and with that their culture

2) Addressed some problem employees

3) Addressed their ownership perpetuation model – got it working for them

4) Got younger – brought in the next generation (especially producers)

5) Merged with another firm to achieve scale

6) Started planning – got aggressive – effectively executed deals

32

Value Creation

There is a huge opportunity in front of you

Build on your strengths / Address your weaknesses

Decide where some wise investments can be made

Sell your team on a value creation vision that they will benefit from and be rewarded by

Source:

33

J a n u a r y 1 5 - 1 7 , 2 0 2 0 | N e w O r l e a n s , L A

BEST PRACTICES

SYMPOSIUM

PTI – Buy / Sell the Industry

Brian Deitz and Harrison BrooksReagan Consulting

Consulting

Seven industries that will be disrupted in the next 10 years

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Financial Services Healthcare Fashion Clothing

Legal Services Moving Industry Home Furnishings

Insurance

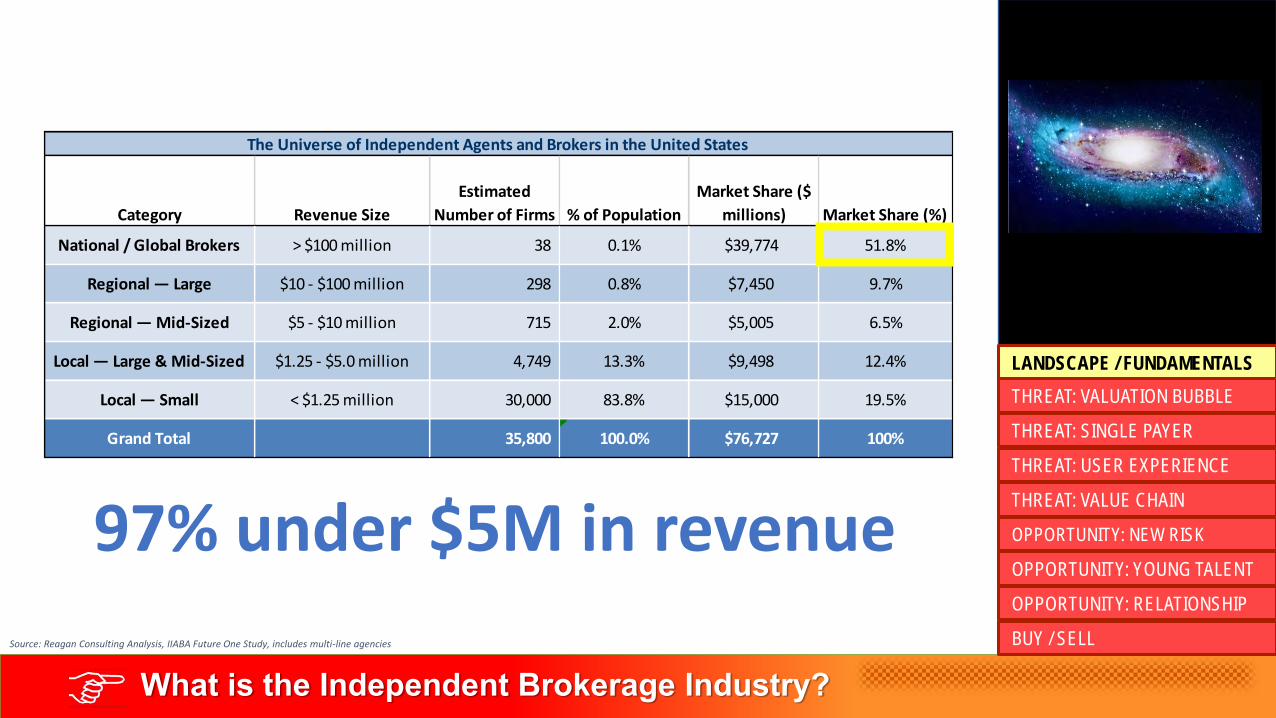

What is the Independent Brokerage Industry?Source: Reagan Consulting Analysis, IIABA Future One Study, includes multi-line agencies

Category Revenue Size

Estimated

Number of Firms % of Population

Market Share ($

millions) Market Share (%)

National / Global Brokers > $100 million 38 0.1% $39,774 51.8%

Regional — Large $10 - $100 million 298 0.8% $7,450 9.7%

Regional — Mid-Sized $5 - $10 million 715 2.0% $5,005 6.5%

Local — Large & Mid-Sized $1.25 - $5.0 million 4,749 13.3% $9,498 12.4%

Local — Small < $1.25 million 30,000 83.8% $15,000 19.5%

Grand Total 35,800 100.0% $76,727 100%

The Universe of Independent Agents and Brokers in the United States

97% under $5M in revenue

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What is the Independent Brokerage Industry?

35,000+ AGENCIES

Average Revenue by Source (across all revenue categories)

60%25%

15%Commercial P&C

Personal P&C

Life/Health/Financial

Median OGP Organic Growth Rate:

6.1%

Median OGP EBITDA Margin:

23.5%

Source: Reagan Consulting Organic Growth and Profitability Survey, Q3 2019

70%

30% Direct Writers

Independent Channel

30%

70%

PERSONAL P&C Market Share

COMMERCIAL P&CMarket Share

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

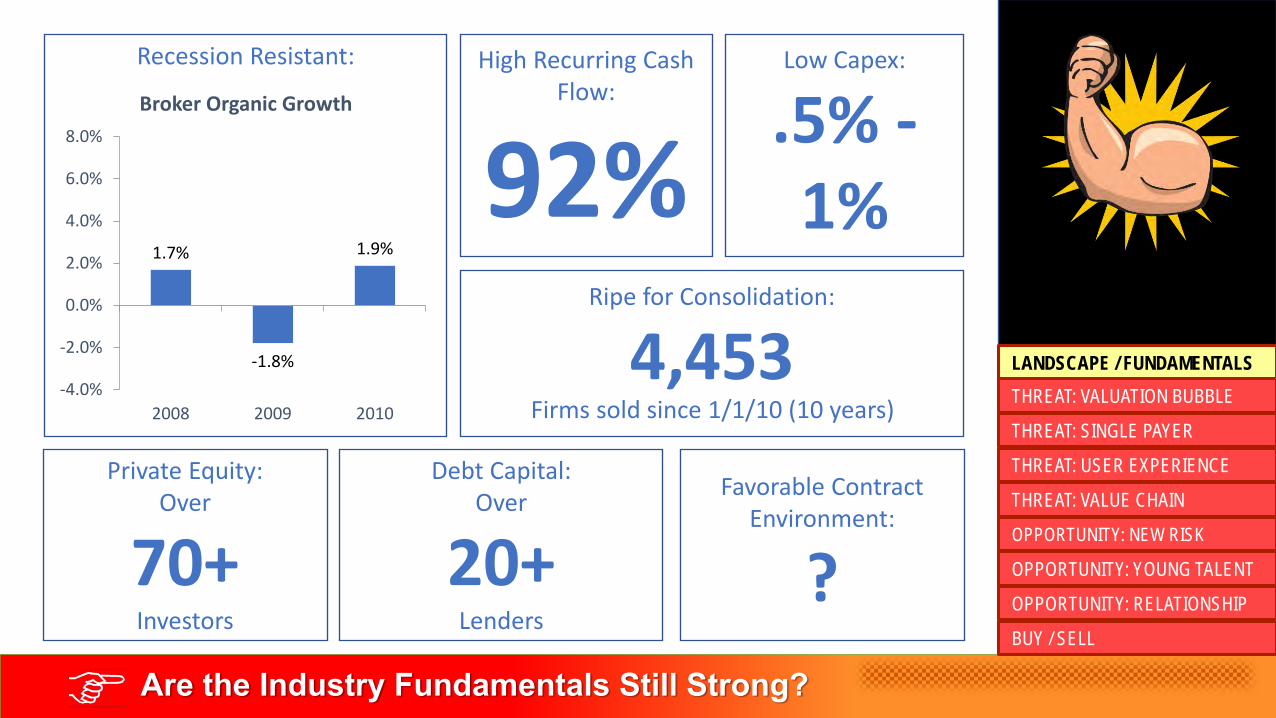

Are the Industry Fundamentals Still Strong?

1.7%

-1.8%

1.9%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2008 2009 2010

Broker Organic Growth

Recession Resistant: High Recurring Cash Flow:

92%

Low Capex:

.5% -1%

Ripe for Consolidation:

4,453Firms sold since 1/1/10 (10 years)

Private Equity:Over

70+Investors

Debt Capital:Over

20+Lenders

Favorable Contract Environment:

?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Are the Industry Fundamentals Still Strong?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Are the Industry Fundamentals Still Strong?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

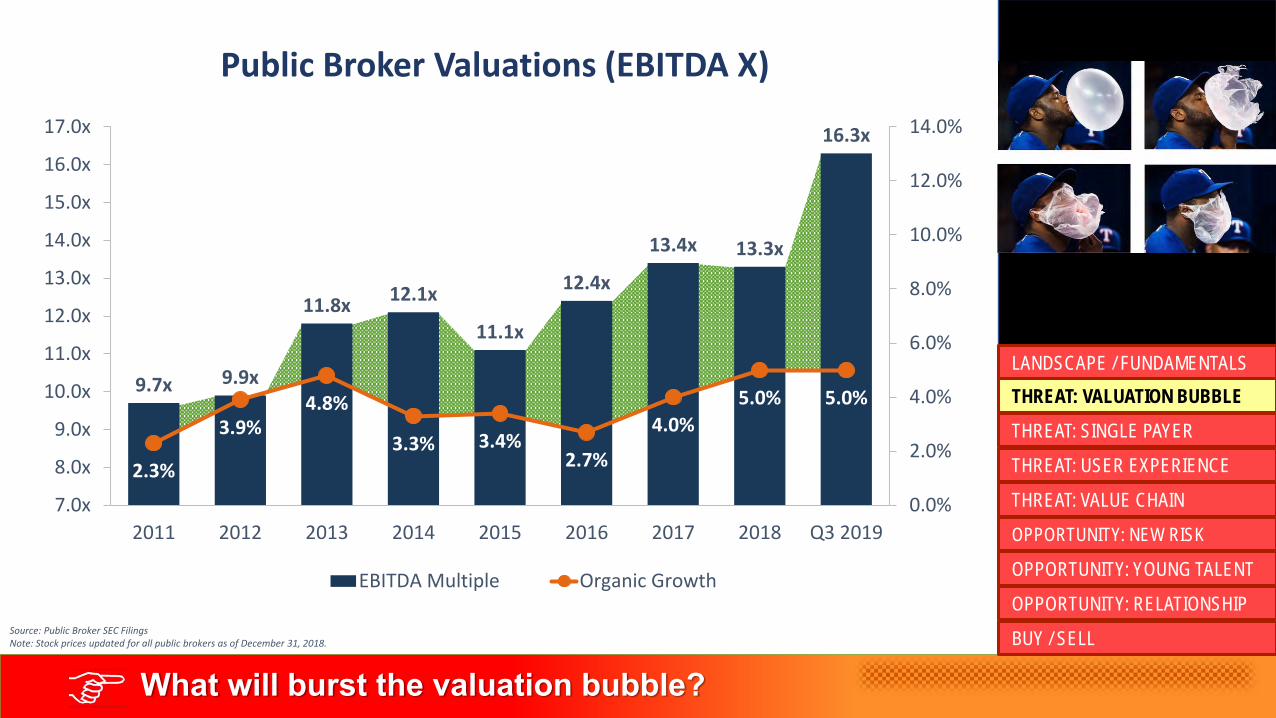

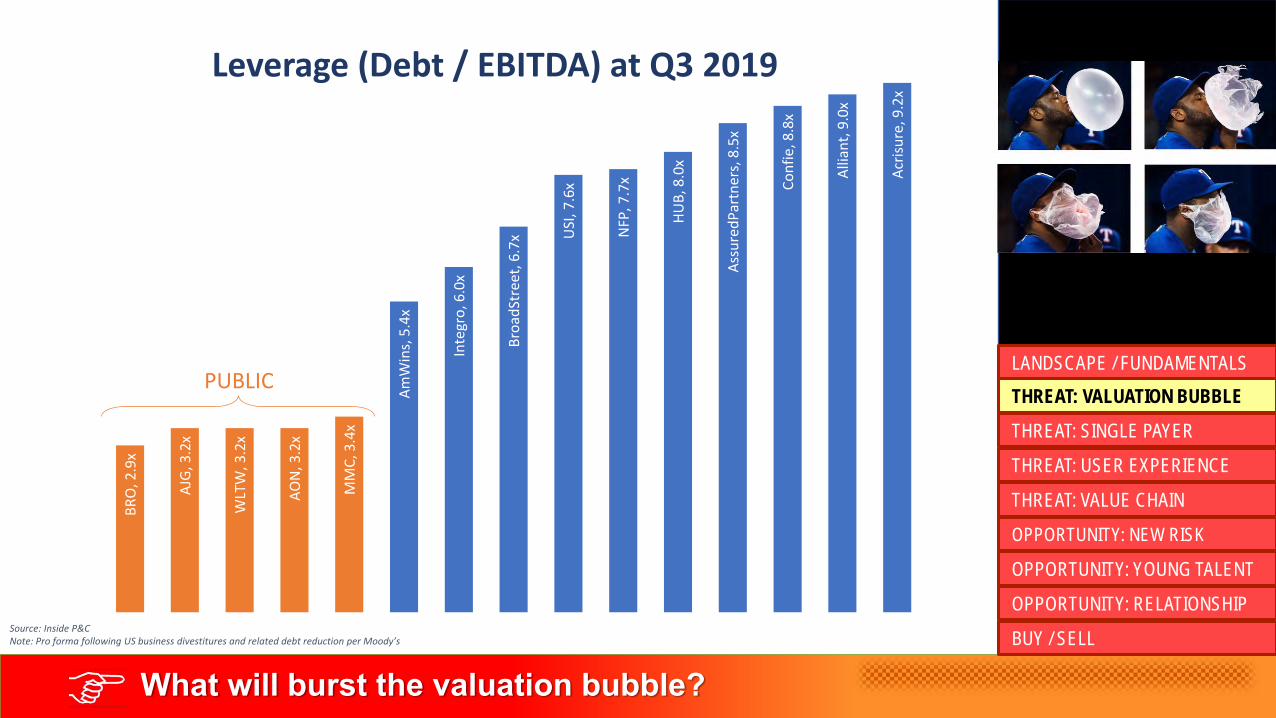

What will burst the valuation bubble?

6.5x 6.0x 5.8x 6.0x 6.3x 6.5x 6.8x 7.0x 7.5x 8.0x 8.0x 9.0x 9.5x

3.5x

3.0x 3.0x 2.5x 2.5x 2.5x 3.0x 3.0x

3.0x 3.0x 3.0x

3.0x 3.0x

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Typical Guaranteed Price Earn-Out Opportunity

M&A Valuations in the Brokerage Industry

Source: Reagan Consulting Analysis. Includes high-quality $3-$10 million firms.

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

9.7x 9.9x

11.8x12.1x

11.1x

12.4x

13.4x 13.3x

16.3x

2.3%

3.9%4.8%

3.3% 3.4%2.7%

4.0%

5.0% 5.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

15.0x

16.0x

17.0x

2011 2012 2013 2014 2015 2016 2017 2018 Q3 2019

EBITDA Multiple Organic Growth

What will burst the valuation bubble?

Source: Public Broker SEC FilingsNote: Stock prices updated for all public brokers as of December 31, 2018.

Public Broker Valuations (EBITDA X)

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What will burst the valuation bubble?

BR

O, 2

.9x

AJG

, 3.2

x

WLT

W, 3

.2x

AO

N, 3

.2x

MM

C, 3

.4x

Am

Win

s, 5

.4x

Inte

gro

, 6.0

x

Bro

adSt

reet

, 6.7

x USI

, 7.6

x

NFP

, 7.7

x

HU

B, 8

.0x

Ass

ure

dP

artn

ers,

8.5

x

Co

nfi

e, 8

.8x

Alli

ant,

9.0

x

Acr

isu

re, 9

.2x

PUBLIC

Source: Inside P&CNote: Pro forma following US business divestitures and related debt reduction per Moody’s

Leverage (Debt / EBITDA) at Q3 2019

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What will burst the valuation bubble?

What is the Outlook for Corporate Taxes?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

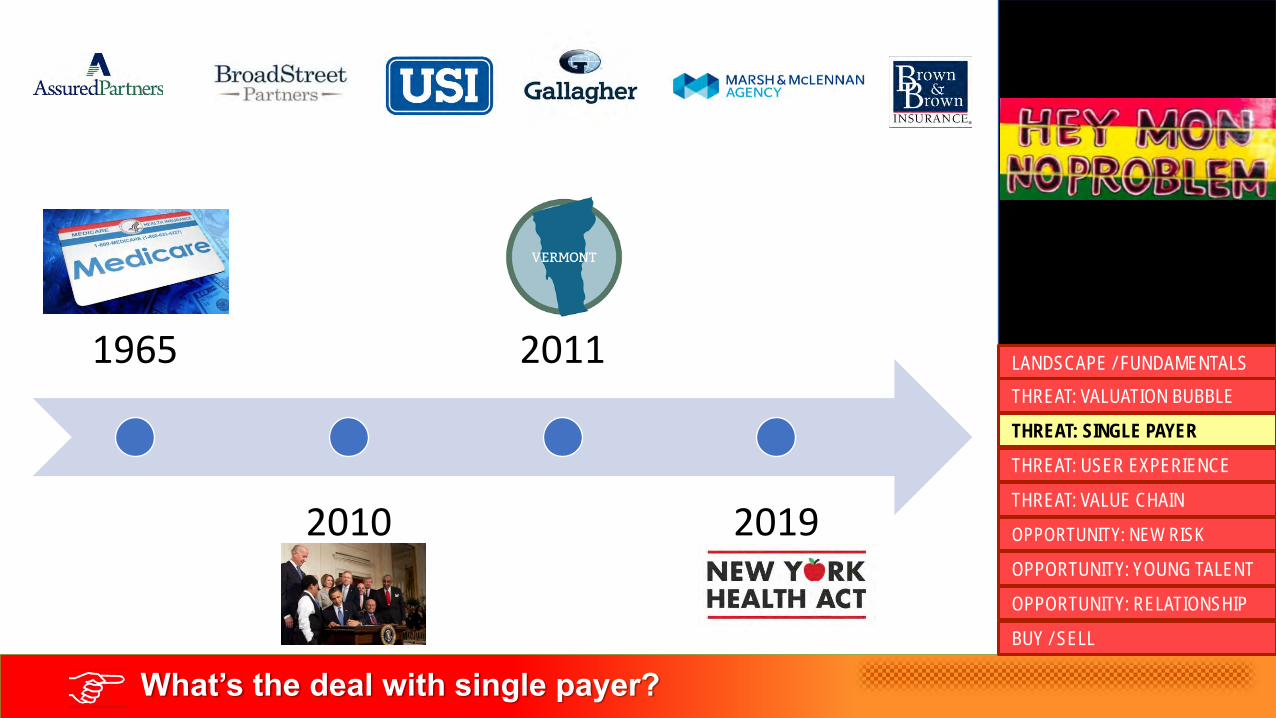

1965

2010

2011

2019

What’s the deal with single payer?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What’s the deal with single payer?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What’s the deal with single payer?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What’s the deal with single payer?

▪ Revenue opportunity for a Canadian group is less than half of the revenue for a US group

▪ Margins in Canadian benefits business are well above margins in the US

▪ The sale is a highly consultative sale focused on the supplemental

▪ Is there an opportunity for more sophisticated players to gain market share?

▪ Would carrier consolidation lead to consolidation in distribution?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What is the User Experience Threat?

Demographic Shift

Improving Technology+ =

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

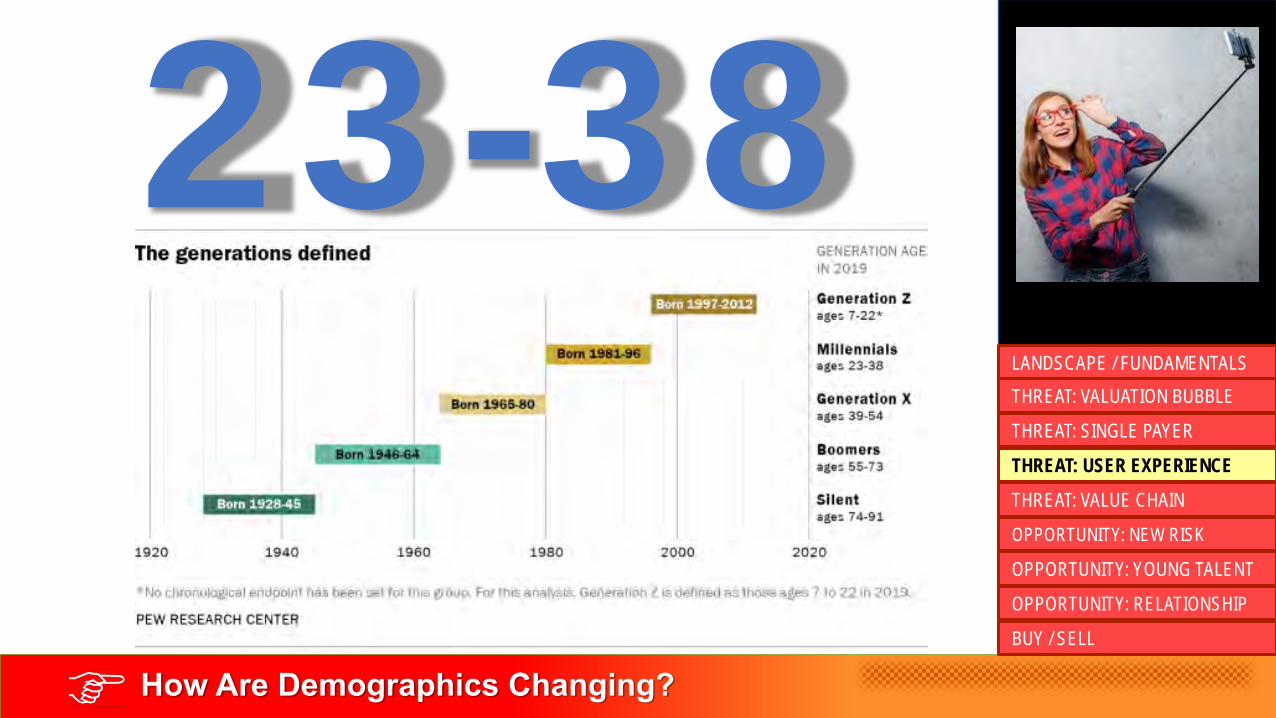

How Are Demographics Changing?

23-38THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Is Technology Evolving Fast Enough?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Is Technology Evolving Fast Enough?

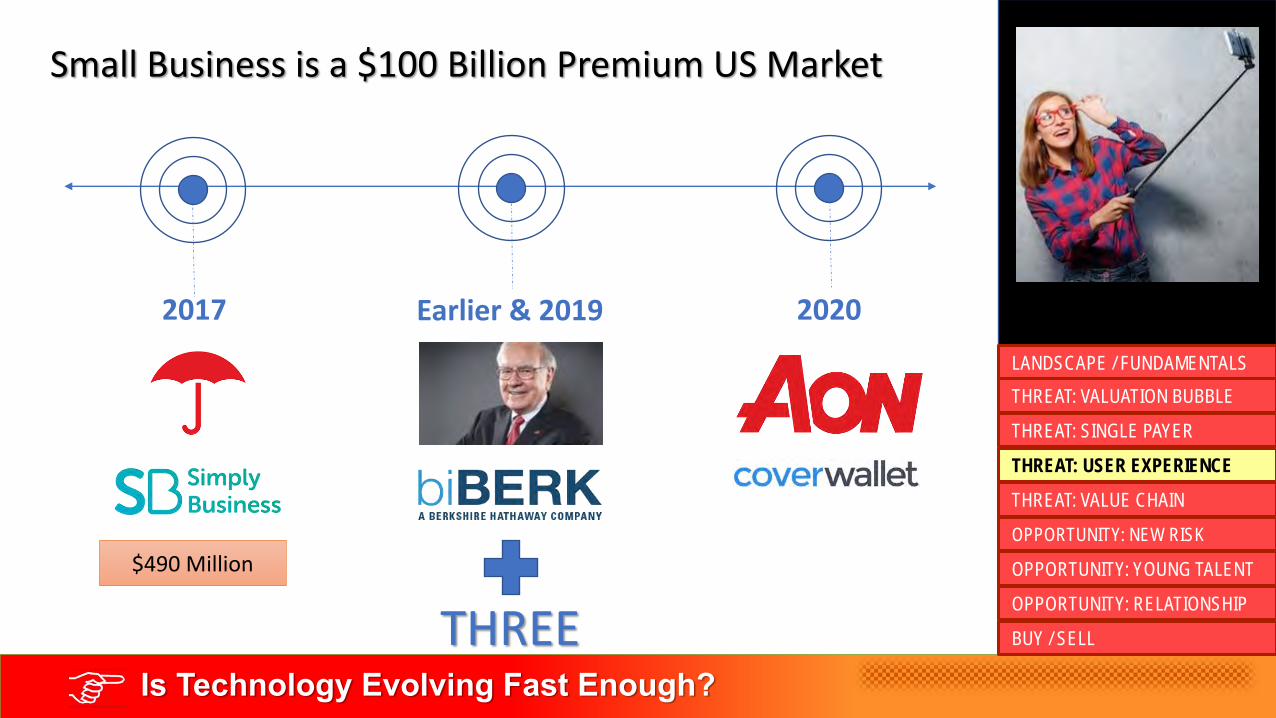

Small Business is a $100 Billion Premium US Market

2017 Earlier & 2019

$490 Million

2020

THREE

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

How do Brokers Respond?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

What is the impact of the consolidating carrier landscape?

Capital Markets

Carrier Broker Insured

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Capital Markets

Carrier Broker Insured

Capital Markets

Carrier Broker Insured

Capital Markets

Carrier Broker Insured

Will new risks drive significant opportunity for brokers?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

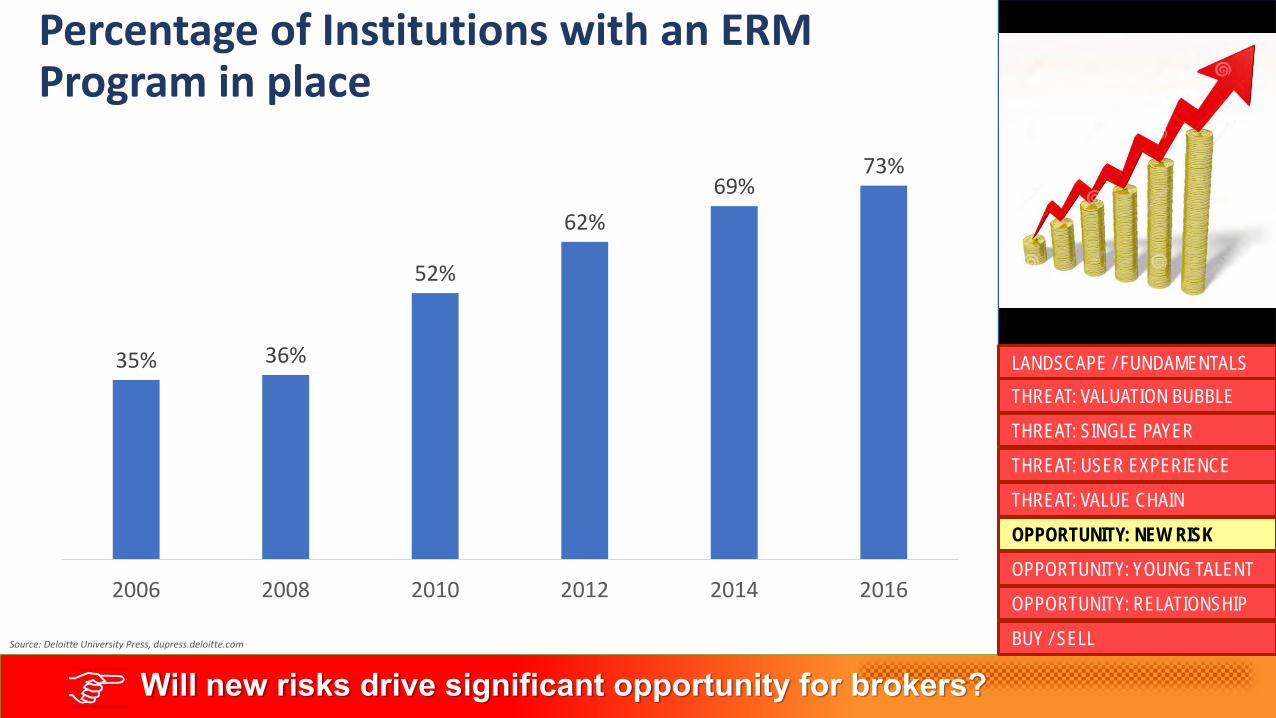

BUY / SELLSource: Deloitte University Press, dupress.deloitte.com

Percentage of Institutions with an ERM Program in place

35% 36%

52%

62%

69%73%

2006 2008 2010 2012 2014 2016

Will new risks drive significant opportunity for brokers?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELLSource: A.M. Best (2007-2013), ISO (2014-2018)

-2.0%

-4.2%

0.9%

3.3%

4.3% 4.6%4.1%

3.4%2.7%

4.6%

10.8%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Net Written Premium Growth (All P/C Lines):Annual Change, 2008-2018

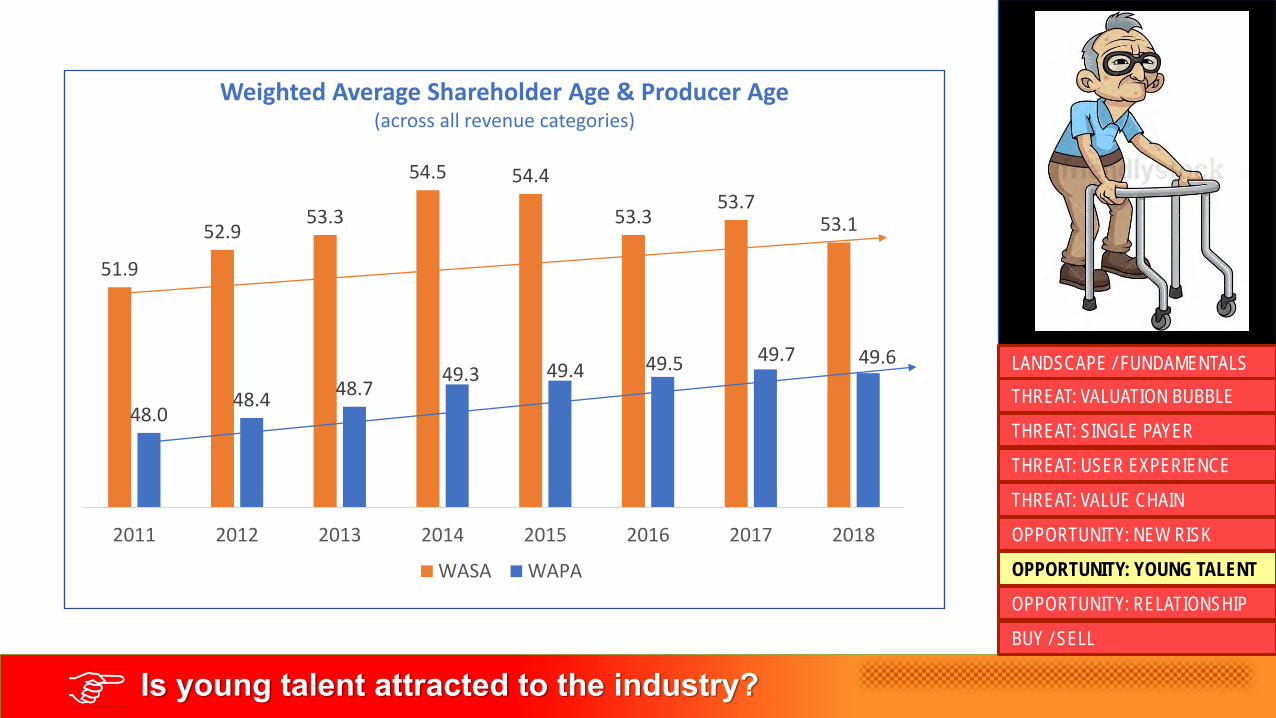

51.9

52.953.3

54.5 54.4

53.353.7

53.1

48.048.4

48.749.3 49.4 49.5 49.7 49.6

2011 2012 2013 2014 2015 2016 2017 2018

WASA WAPA

Is young talent attracted to the industry?

Weighted Average Shareholder Age & Producer Age(across all revenue categories)

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Is young talent attracted to the industry?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Is young talent attracted to the industry?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

@Appalachian State University

We have a Risk Management Program

Tweet

@Baylor University

Us TooTweet

@ButlerUniversity

Us Too

Tweet@California State University Fullerton

Us Too

Tweet@East Carolina University

Us Too

Tweet

@Eastern Kentucky University

Us Too

Tweet

@Florida State University

Us Too

Tweet

@Gannon University

Us TooTweet

@Georgia State University

Us TooTweet

@Howard University

Us Too

Tweet

@Illinois State University

Us TooTweet

@Baylor University

Us TooTweet

@Indiana State University

Us TooTweet

@Middle Tennessee State University

Us TooTweet

@Mississippi State University

Us TooTweet

@LaSalle University

Us TooTweet

@Missouri State University

Us TooTweet

@New Mexico State University

Us Too

Tweet

@Northern Michigan University

Us TooTweet

@Old Dominion University

Us TooTweet

@Olivet College

Us TooTweet

@St. John’s University

Us TooTweet

@St. Joseph’s University

Us TooTweet

@St. Mary’s University

Us TooTweet

@Temple University

Us TooTweet

@University of Akron

Us TooTweet

@University of Alabama

Us TooTweet

@University of Central Arkansas

Us TooTweet

@University of Cincinnati

Us TooTweet

@University of Colorado Denver

Us TooTweet

@University of Georgia

Us TooTweet

@University of Hartford

Us TooTweet

@University of Hawaii

Us TooTweet

@University of Houston Downtown

Us TooTweet

@University of Iowa

Us TooTweet

@California State University Northridge

Us TooTweet

@California State University Sacramento

Us TooTweet

@Ferris State University

Us TooTweet

@University of Louisiana Lafayette

Us TooTweet

@University of Louisiana Monroe

Us TooTweet

@University of Minnesota

Us TooTweet

@University of Mississippi

Us TooTweet

@University of Missouri

Us TooTweet

@University of North Carolina Charlotte

Us TooTweet

@University of North Texas

Us TooTweet

@University of South Carolina

Us TooTweet

@University of Southern Maine

Us TooTweet

@University of Texas Dallas

Us TooTweet

@University of Wisconsin Madison

Us TooTweet

@Virginia Commonwealth University

Us TooTweet

Does the broker control the customer relationship?

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Are you buying or selling the industry?

➢Fewer agencies

➢More competition

➢More technology

➢Smarter underwriting

➢Enhanced client expectations of services offered and speed of information

➢Increased reliance on knowledge as risks grow more complex

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Predictions

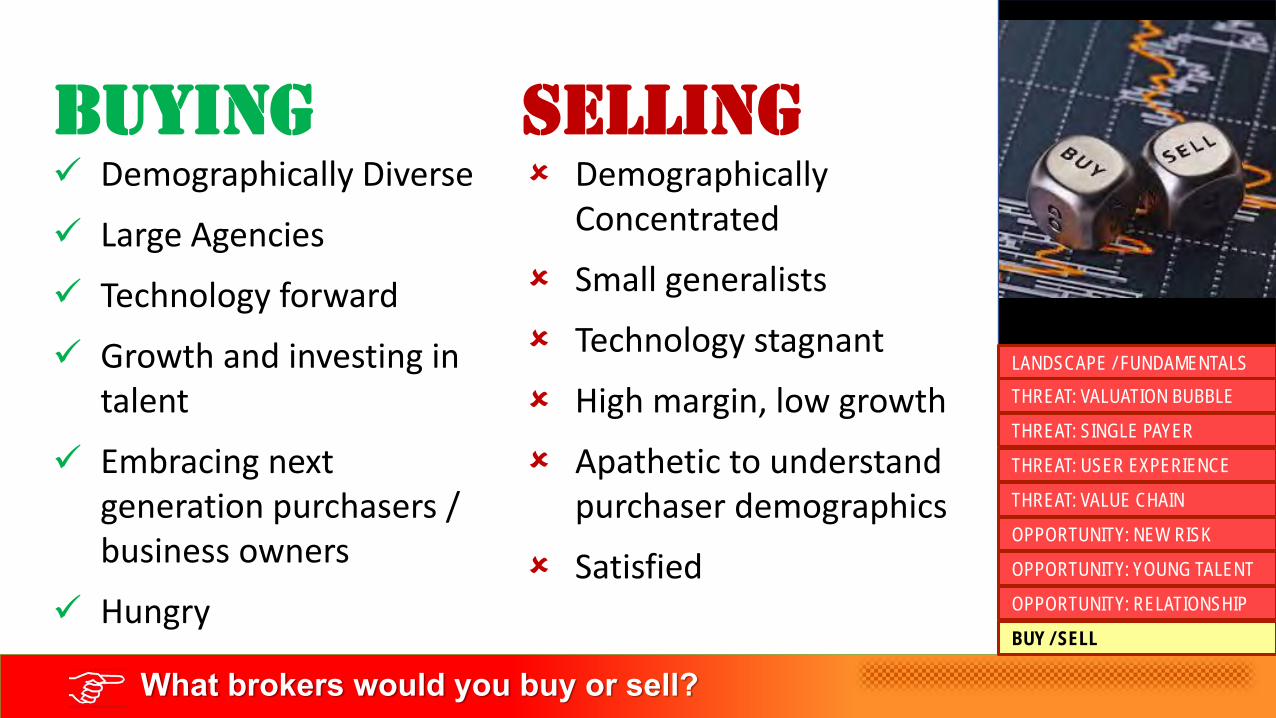

What brokers would you buy or sell?

✓ Demographically Diverse

✓ Large Agencies

✓ Technology forward

✓ Growth and investing in talent

✓ Embracing next generation purchasers / business owners

✓ Hungry

Demographically Concentrated

Small generalists

Technology stagnant

High margin, low growth

Apathetic to understand purchaser demographics

Satisfied

Buying selling

THREAT: SINGLE PAYER

THREAT: USER EXPERIENCE

LANDSCAPE / FUNDAMENTALS

THREAT: VALUATION BUBBLE

OPPORTUNITY: YOUNG TALENT

OPPORTUNITY: RELATIONSHIP

THREAT: VALUE CHAIN

OPPORTUNITY: NEW RISK

BUY / SELL

Consulting