better ways to manage foreign exchange from the investor’s ...€¦ · better ways to manage...

TRANSCRIPT

New South Wales Treasury Corporation

Insert NSW flag

Better ways to manage foreign exchange from the investor’s perspective

Jonathan Green Head of Investment Management

April 2013

New South Wales Treasury Corporation 2

Disclaimer This presentation is provided for information purposes only and is intended for your use only. The presentation should not be relied on for trading or other business purposes. The presentation does not constitute investment advice and TCorp does not make any recommendation as to the suitability of any of the products or transactions mentioned. This presentation is not intended to forecast or predict future events. Past performance is not a guarantee or indication of future results. Any opinions contained in this presentation constitute the presenters personal views and are not necessarily the views of TCorp. TCorp does not guarantee the accuracy, timeliness, reliability or completeness of the information or data and will not be liable for any errors or actions taken in reliance on the information or data.

New South Wales Treasury Corporation 3

Outline

n Global Currency Markets

n Foreign Exchange Execution Efficiency

n Emerging Market Currency Challenges

n Key Learnings

New South Wales Treasury Corporation 4

Global Currency Markets

New South Wales Treasury Corporation 5

Global currency markets

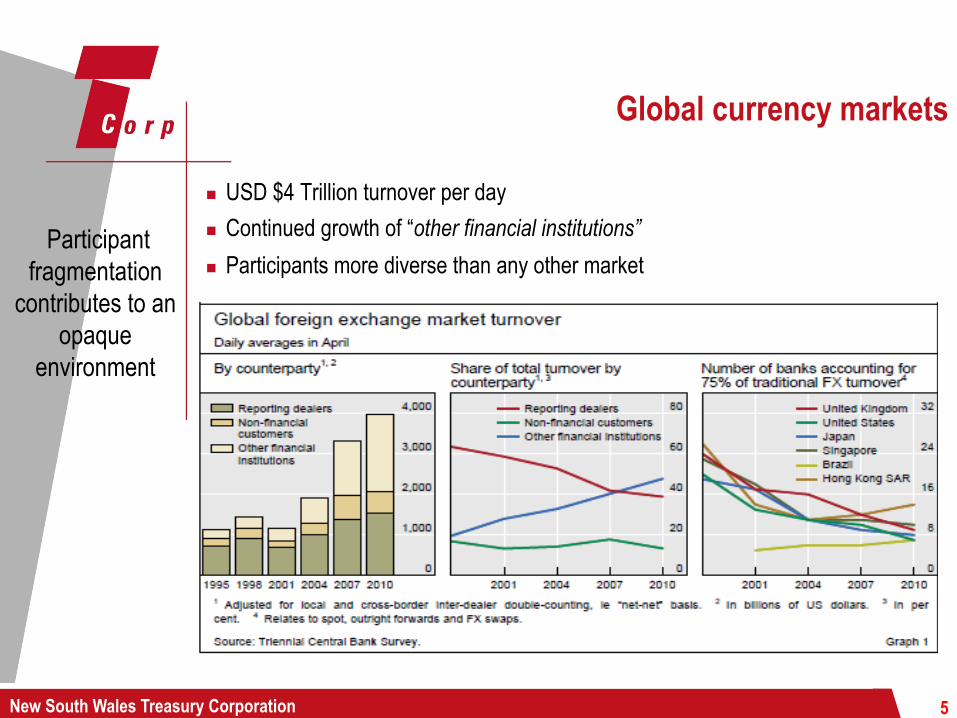

n USD $4 Trillion turnover per day n Continued growth of “other financial institutions” n Participants more diverse than any other market

Participant fragmentation

contributes to an opaque

environment

New South Wales Treasury Corporation 6

Significant liquidity dispersion

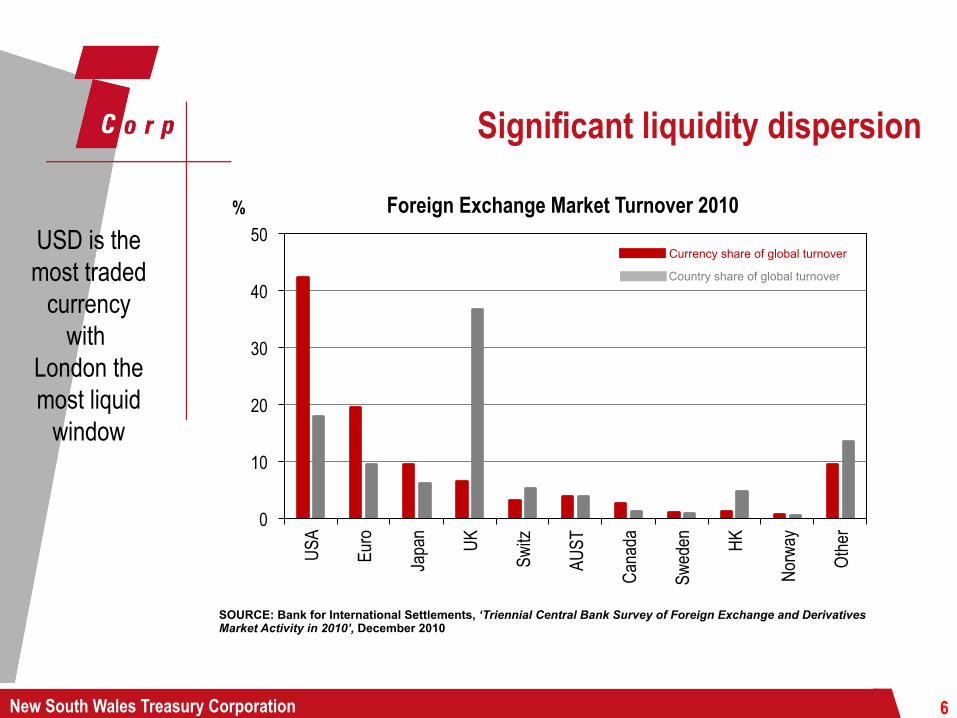

USD is the most traded

currency with

London the most liquid

window

0

10

20

30

40

50

USA

Euro

Japa

n UK

Switz

AUST

Cana

da

Swed

en

HK

Norw

ay

Othe

r

% Foreign Exchange Market Turnover 2010

Currency share of global turnover

Country share of global turnover

SOURCE: Bank for International Settlements, ‘Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in 2010’, December 2010

New South Wales Treasury Corporation 7

Importance to asset owners

Global pension assets

December 2012 $ USD 29.7 trn

Circa USD $6 trn in offshore assets

SOURCE :Towers Watson, ‘Global Pension Asset Study ‘ , January 2013

New South Wales Treasury Corporation

Broaden the focus

8

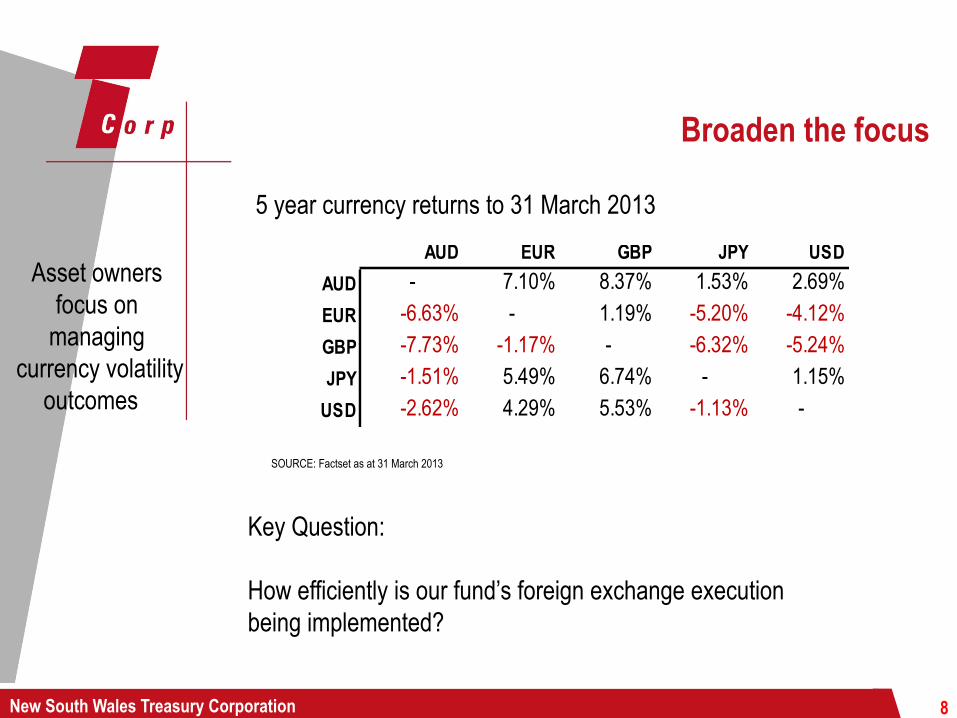

5 year currency returns to 31 March 2013

Asset owners focus on

managing currency volatility

outcomes

Key Question: How efficiently is our fund’s foreign exchange execution being implemented?

SOURCE: Factset as at 31 March 2013

AUD EUR GBP JPY USDAUD - 7.10% 8.37% 1.53% 2.69%

EUR -6.63% - 1.19% -5.20% -4.12%

GBP -7.73% -1.17% - -6.32% -5.24%

JPY -1.51% 5.49% 6.74% - 1.15%

USD -2.62% 4.29% 5.53% -1.13% -

New South Wales Treasury Corporation 9

Regulation and guidelines

n MiFID, the SEC, and ASIC impose regulatory requirements or issue guidance notes around “best execution”

n “Best execution” is often a standard clause in many IMA’s

n Fund managers promote their execution capabilities

n False sense of security….

Securities focus

New South Wales Treasury Corporation

Headline news in recent years

10

n The Boeing Worker Retirement Plan filed a lawsuit against its FX service provider of overcharging on forex trades Reuters, 19 October 2012

n A large US custodian bank was sued by state attorneys-general from New York, Florida and Virginia, alleging the bank overcharged its clients. C Panteli, Professional

Pensions, 5 October 2011

n The Louisiana Municipal Police Employees’ Retirement System filed a complaint in Manhattan federal court alleging that the bank took advantage of investors by causing them to pay what were often the worst currency rates available on a given trading day C Smythe , Bloomberg, 1 September 2012

n The Financial Conduct Authority (FCA) in UK has targeted the transparency of fees via various practitioners within the financial services industry Financial Times, ‘

Regulator to Probe Transition Management, Custody, Fund Fees’, March,25 2013

New South Wales Treasury Corporation 11

Investor expectations

Asset owners

anticipate a normal

distribution

SOURCE: 1. Raynor, L, ‘Still overpaying for FX’, Russell Research, May 2012, pp.1-14

New South Wales Treasury Corporation 12

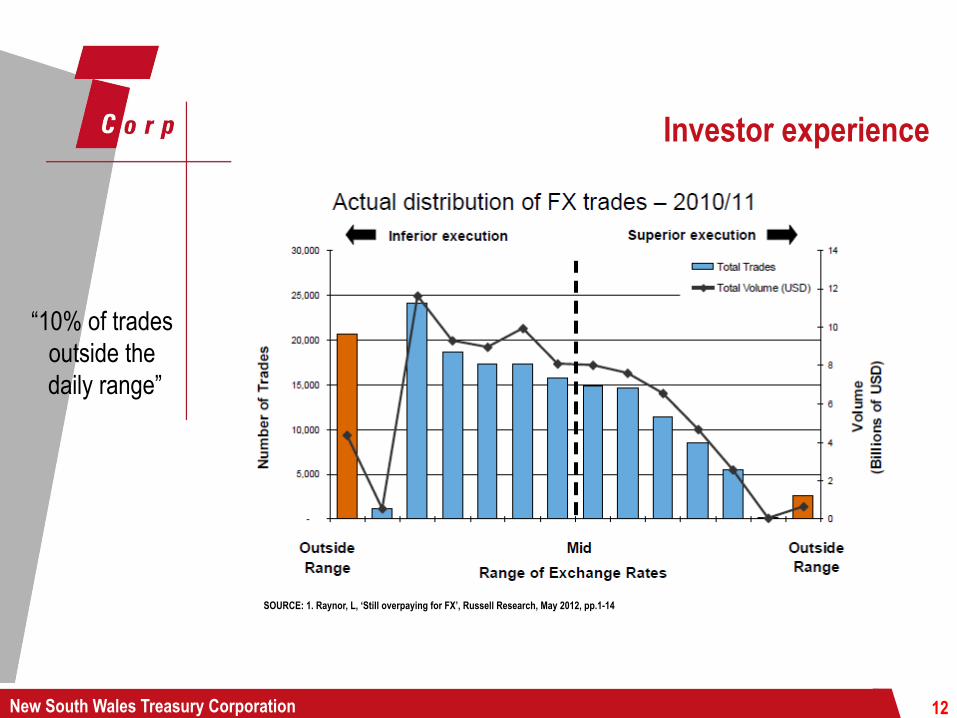

Investor experience

“10% of trades

outside the daily range”

SOURCE: 1. Raynor, L, ‘Still overpaying for FX’, Russell Research, May 2012, pp.1-14

1

New South Wales Treasury Corporation 13

Foreign Exchange Execution Efficiency

New South Wales Treasury Corporation

Where to start?

14

Cartoonist: Paul Taylor

Foreign exchange leakage

Efficient

Implementation

New South Wales Treasury Corporation

Shared responsibility

Not only a custodian challenge

Asset Owner

Custodian Fund

Manager

OPTIMAL Narrow the responsibility

gap

15

New South Wales Treasury Corporation

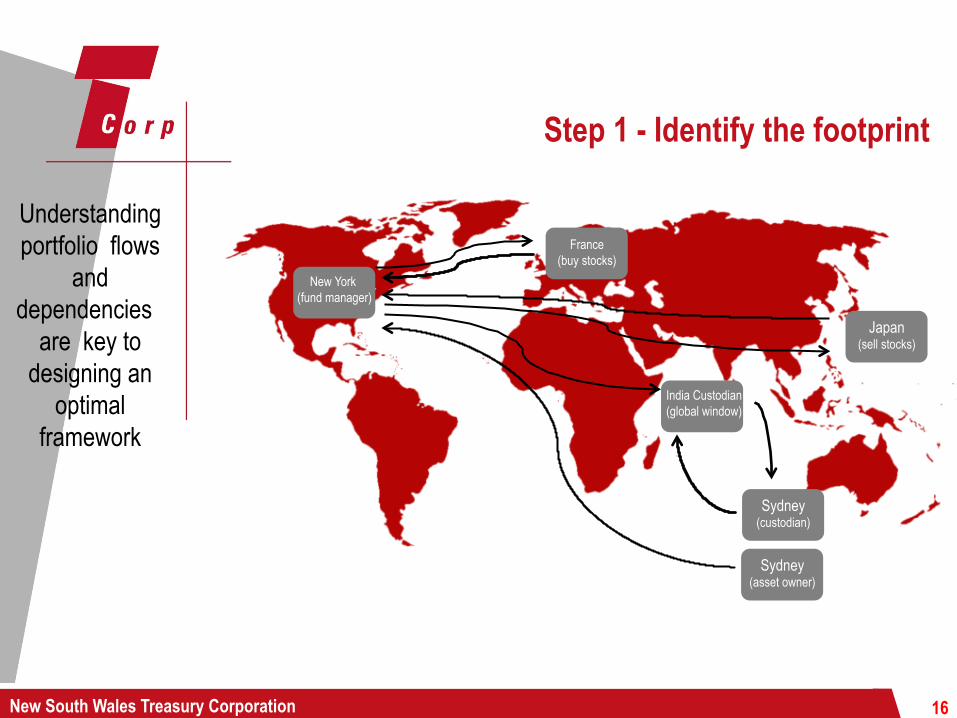

Step 1 - Identify the footprint

Understanding portfolio flows

and dependencies

are key to designing an

optimal framework

New York (fund manager)

France (buy stocks)

Japan (sell stocks)

Sydney (custodian)

India Custodian (global window)

Sydney (asset owner)

16

New South Wales Treasury Corporation 17

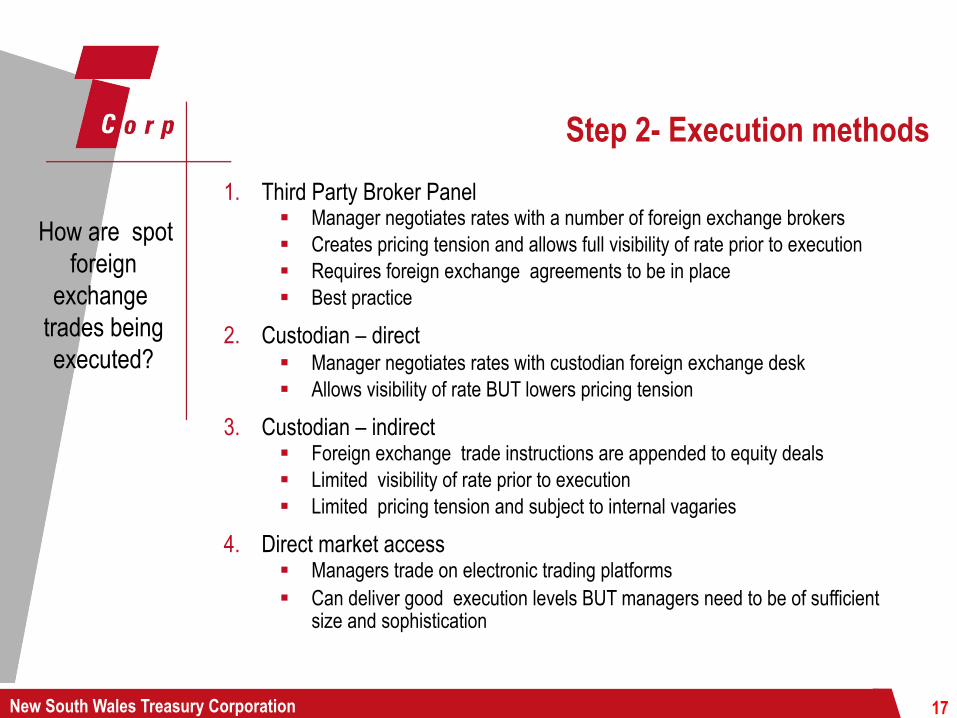

Step 2- Execution methods 1. Third Party Broker Panel

§ Manager negotiates rates with a number of foreign exchange brokers § Creates pricing tension and allows full visibility of rate prior to execution § Requires foreign exchange agreements to be in place § Best practice

2. Custodian – direct § Manager negotiates rates with custodian foreign exchange desk § Allows visibility of rate BUT lowers pricing tension

3. Custodian – indirect § Foreign exchange trade instructions are appended to equity deals § Limited visibility of rate prior to execution § Limited pricing tension and subject to internal vagaries

4. Direct market access § Managers trade on electronic trading platforms § Can deliver good execution levels BUT managers need to be of sufficient

size and sophistication

How are spot foreign

exchange trades being executed?

New South Wales Treasury Corporation 18

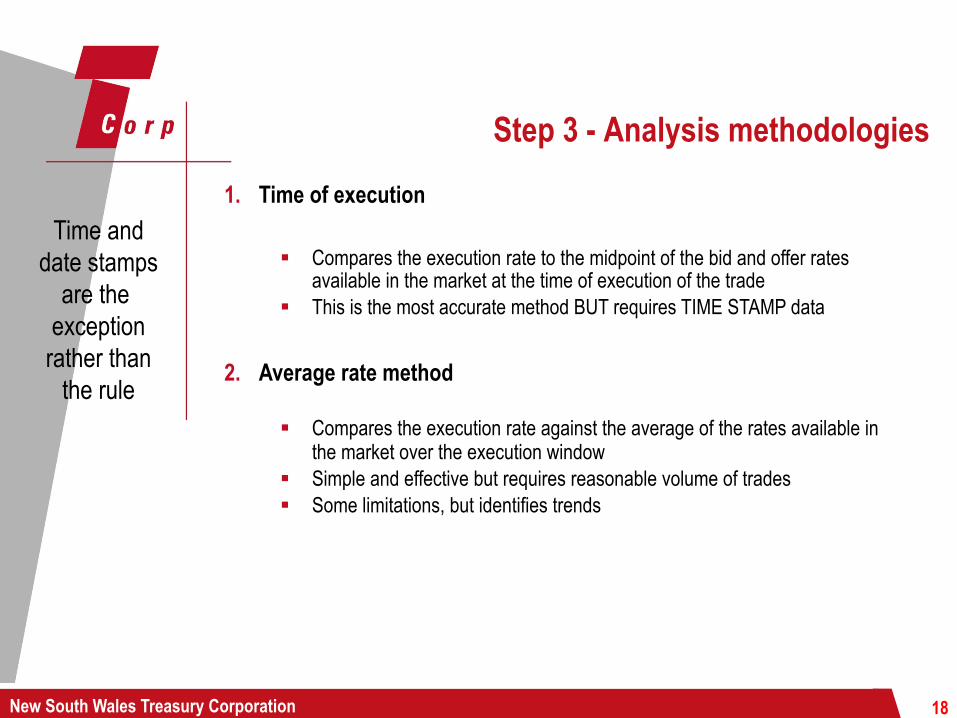

Step 3 - Analysis methodologies 1. Time of execution

§ Compares the execution rate to the midpoint of the bid and offer rates available in the market at the time of execution of the trade

§ This is the most accurate method BUT requires TIME STAMP data

2. Average rate method § Compares the execution rate against the average of the rates available in

the market over the execution window § Simple and effective but requires reasonable volume of trades § Some limitations, but identifies trends

Time and date stamps

are the exception rather than

the rule

New South Wales Treasury Corporation 19

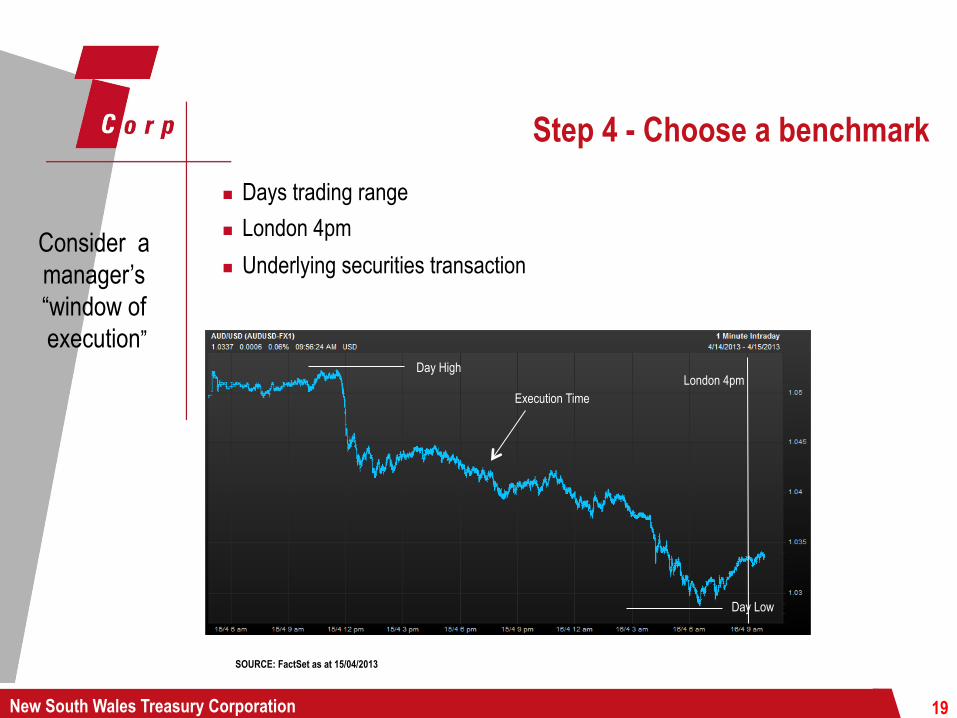

Step 4 - Choose a benchmark n Days trading range n London 4pm n Underlying securities transaction

Consider a manager’s “window of execution”

Day High

Day Low SOURCE: FactSet as at 15/04/2013

London 4pm Execution Time

Day Low

New South Wales Treasury Corporation

TCorp case study n In 2009

Service provider Russell Investments Period October 2006 to October 2009 FUM $1.6 billion Number of Transactions 7,351 Volume (A$) $2 billion Benchmark Daily Range

n In 2012 Service provider TCorp Period October 2009 to October 2012 FUM $2.6 billion Number of Transactions 12,680 Volume (A$) $4.6 billion Benchmark Daily Range

20

Put this into

practice

New South Wales Treasury Corporation 21

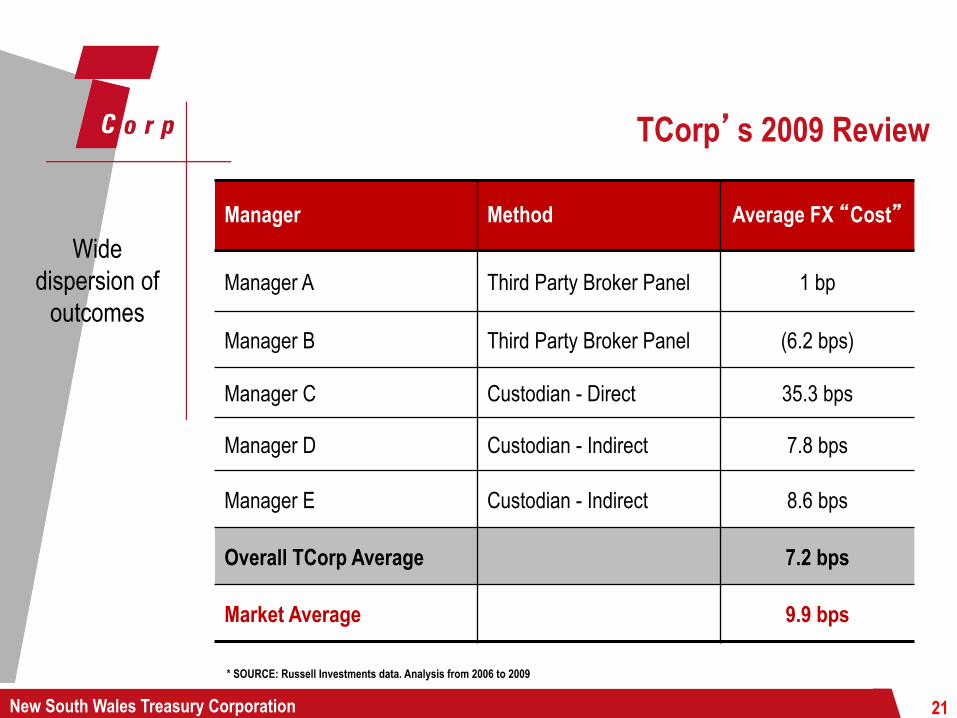

TCorp’s 2009 Review

Manager Method Average FX “Cost”

Manager A Third Party Broker Panel 1 bp

Manager B Third Party Broker Panel (6.2 bps)

Manager C Custodian - Direct 35.3 bps

Manager D Custodian - Indirect 7.8 bps

Manager E Custodian - Indirect 8.6 bps

Overall TCorp Average 7.2 bps

Market Average 9.9 bps

Wide dispersion of

outcomes

* SOURCE: Russell Investments data. Analysis from 2006 to 2009

New South Wales Treasury Corporation 22

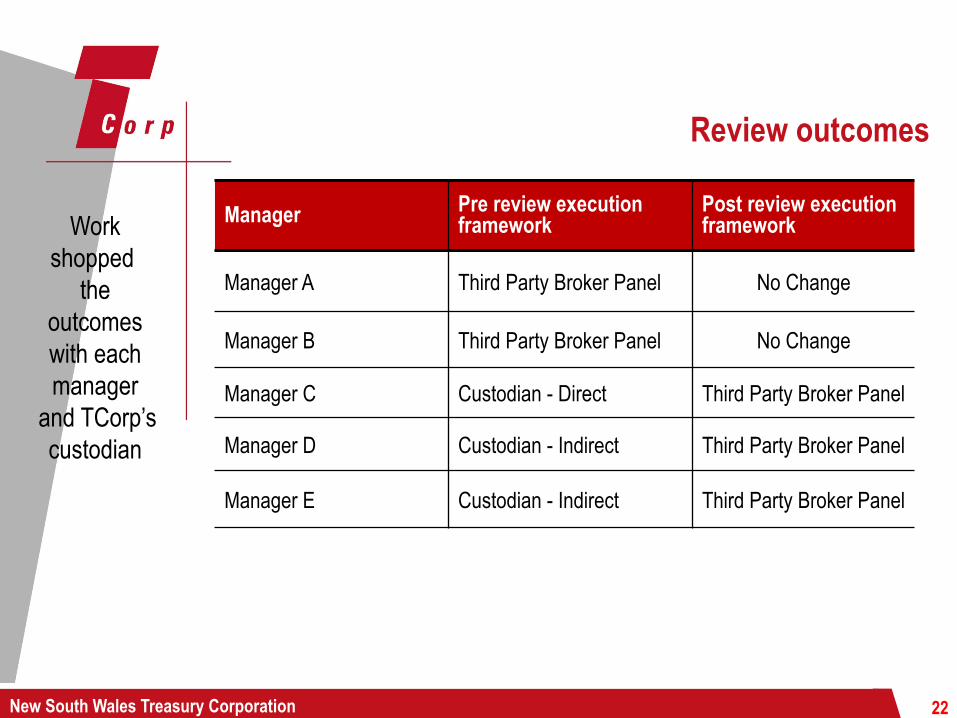

Review outcomes

Manager Pre review execution framework

Post review execution framework

Manager A Third Party Broker Panel No Change

Manager B Third Party Broker Panel No Change

Manager C Custodian - Direct Third Party Broker Panel

Manager D Custodian - Indirect Third Party Broker Panel

Manager E Custodian - Indirect Third Party Broker Panel

Work shopped

the outcomes with each manager

and TCorp’s custodian

New South Wales Treasury Corporation 23

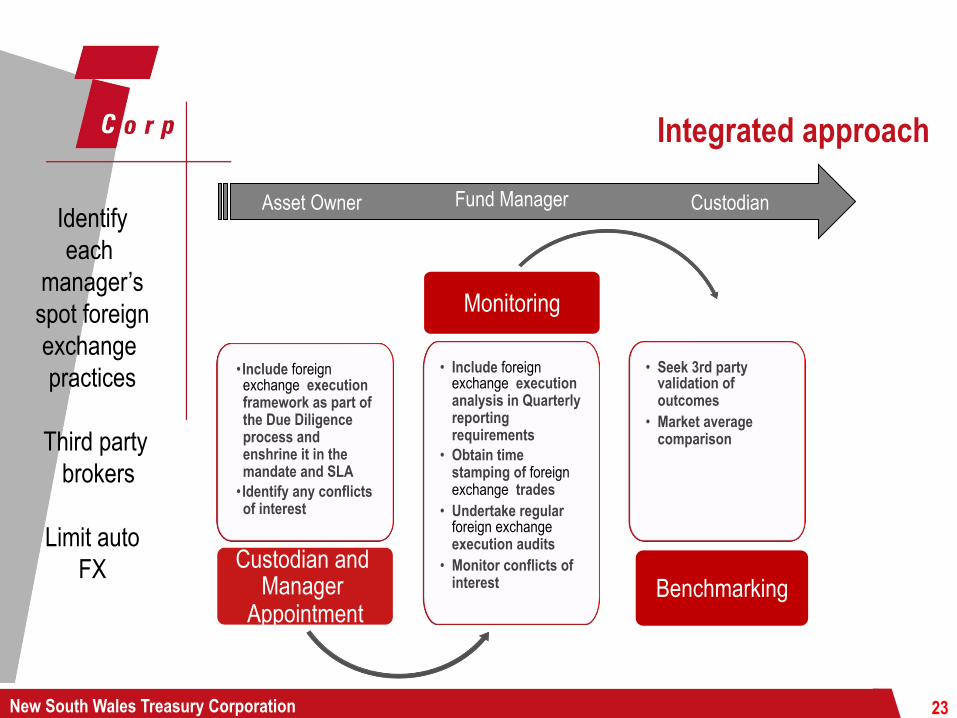

• Include foreign exchange execution framework as part of the Due Diligence process and enshrine it in the mandate and SLA

• Identify any conflicts of interest

Custodian and Manager

Appointment

Monitoring

Benchmarking

Integrated approach

Identify each

manager’s spot foreign exchange practices

Third party

brokers

Limit auto FX

Asset Owner Fund Manager Custodian

• Include foreign exchange execution analysis in Quarterly reporting requirements

• Obtain time stamping of foreign exchange trades

• Undertake regular foreign exchange execution audits

• Monitor conflicts of interest

• Seek 3rd party validation of outcomes

• Market average comparison

New South Wales Treasury Corporation 24

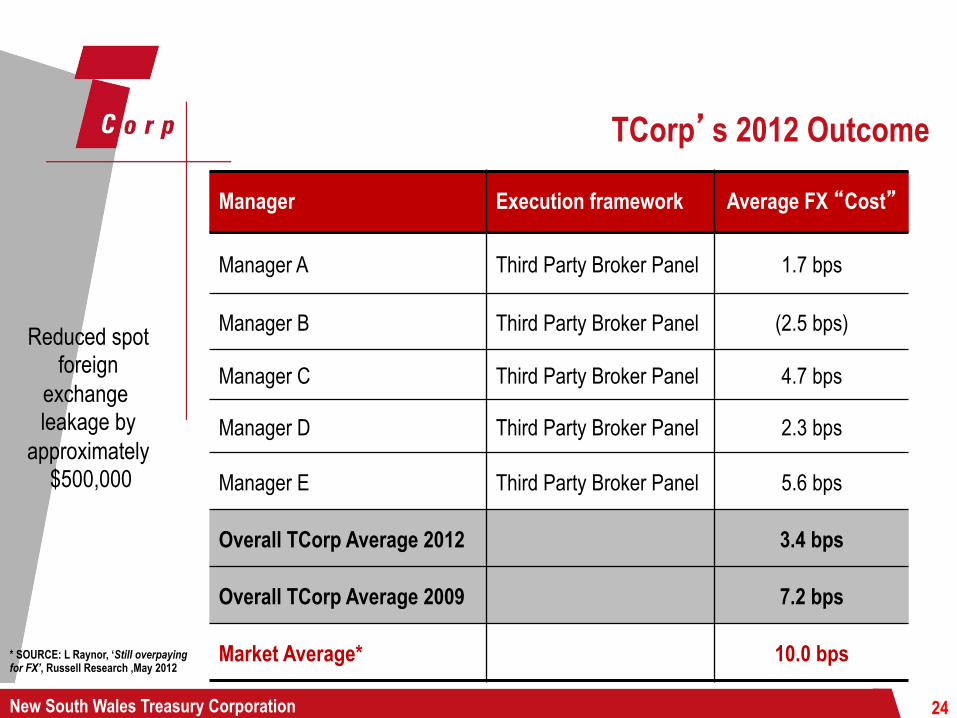

TCorp’s 2012 Outcome

Manager Execution framework Average FX “Cost”

Manager A Third Party Broker Panel 1.7 bps

Manager B Third Party Broker Panel (2.5 bps)

Manager C Third Party Broker Panel 4.7 bps

Manager D Third Party Broker Panel 2.3 bps

Manager E Third Party Broker Panel 5.6 bps

Overall TCorp Average 2012 3.4 bps

Overall TCorp Average 2009 7.2 bps

Market Average* 10.0 bps

Reduced spot foreign

exchange leakage by

approximately $500,000

* SOURCE: L Raynor, ‘Still overpaying for FX’, Russell Research ,May 2012

New South Wales Treasury Corporation

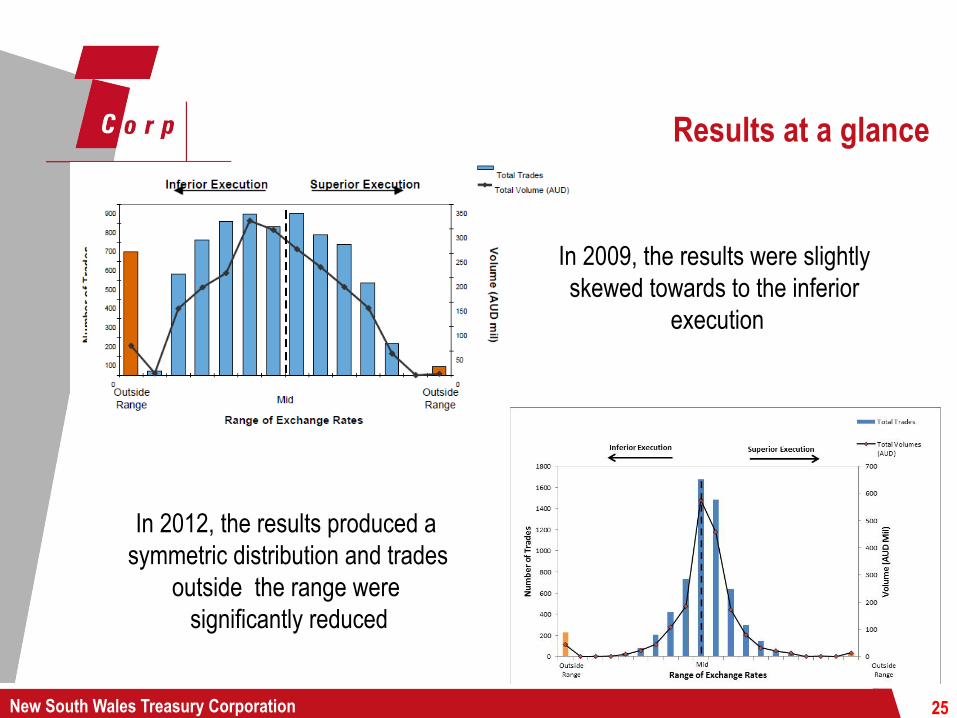

Results at a glance

25

In 2009, the results were slightly skewed towards to the inferior

execution

In 2012, the results produced a symmetric distribution and trades

outside the range were significantly reduced

New South Wales Treasury Corporation 26

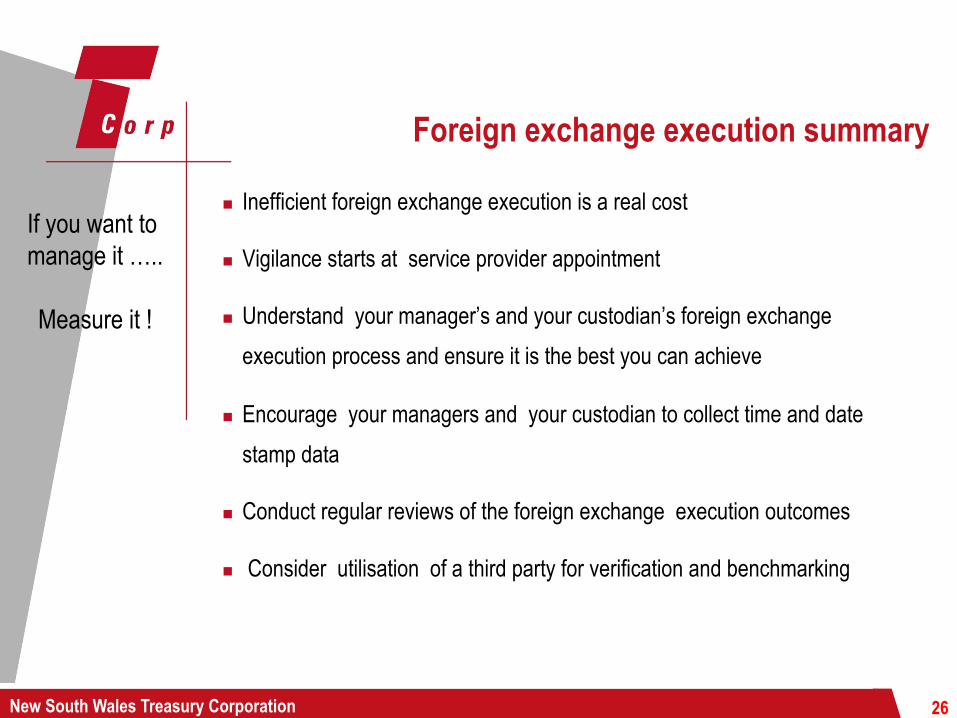

Foreign exchange execution summary

n Inefficient foreign exchange execution is a real cost

n Vigilance starts at service provider appointment

n Understand your manager’s and your custodian’s foreign exchange execution process and ensure it is the best you can achieve

n Encourage your managers and your custodian to collect time and date stamp data

n Conduct regular reviews of the foreign exchange execution outcomes

n Consider utilisation of a third party for verification and benchmarking

If you want to manage it …..

Measure it !

New South Wales Treasury Corporation 27

Emerging Market Currency Challenges

New South Wales Treasury Corporation 28

New South Wales Treasury Corporation

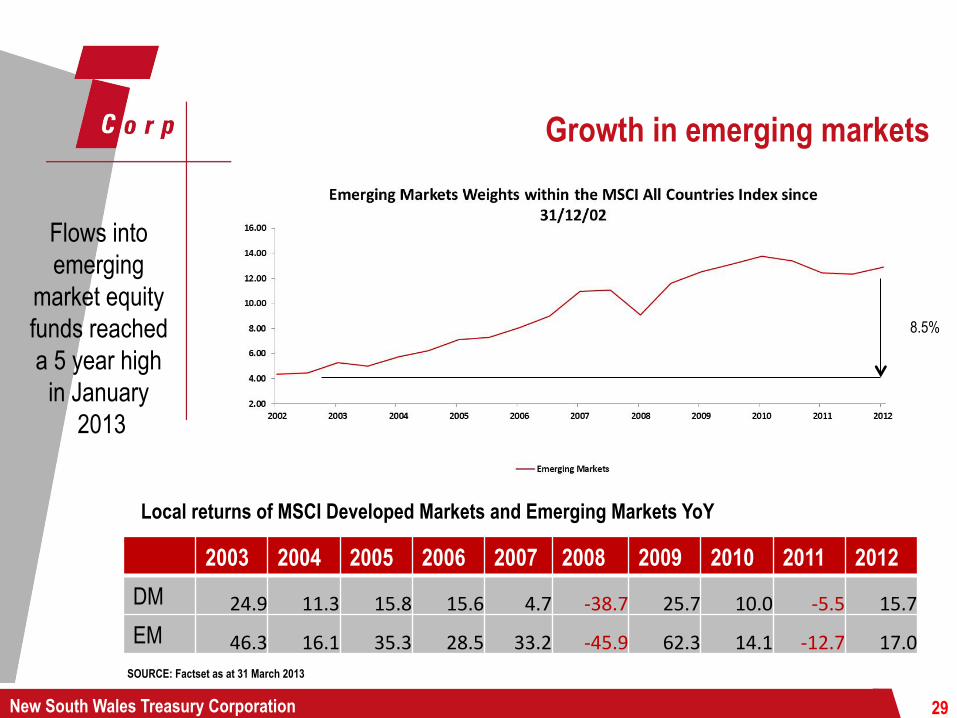

Growth in emerging markets

29

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 DM 24.9 11.3 15.8 15.6 4.7 -‐38.7 25.7 10.0 -‐5.5 15.7 EM 46.3 16.1 35.3 28.5 33.2 -‐45.9 62.3 14.1 -‐12.7 17.0

Local returns of MSCI Developed Markets and Emerging Markets YoY

8.5%

Flows into emerging

market equity funds reached a 5 year high

in January 2013

SOURCE: Factset as at 31 March 2013

New South Wales Treasury Corporation 30

Emerging markets currencies

n There are 11 “restricted currency” markets

n Emerging market currencies are subject to a variety of trading rules

n Typically, the execution of transactions in emerging market currencies are undertaken by the custodian

n Due diligence of the custodian’s and manager’s process around restricted currencies is recommended

New South Wales Treasury Corporation

Sample of foreign exchange challenges

§ Onshore trading allowed only during local market hours

§ Local agent required to facilitate foreign exchange transaction

§ Foreign exchange must be matched to underlying securities trading

§ Different restrictions applying to purchasing and selling local currency

§ Overdrafts are not allowed

§ Pre funding requirement

31

New South Wales Treasury Corporation

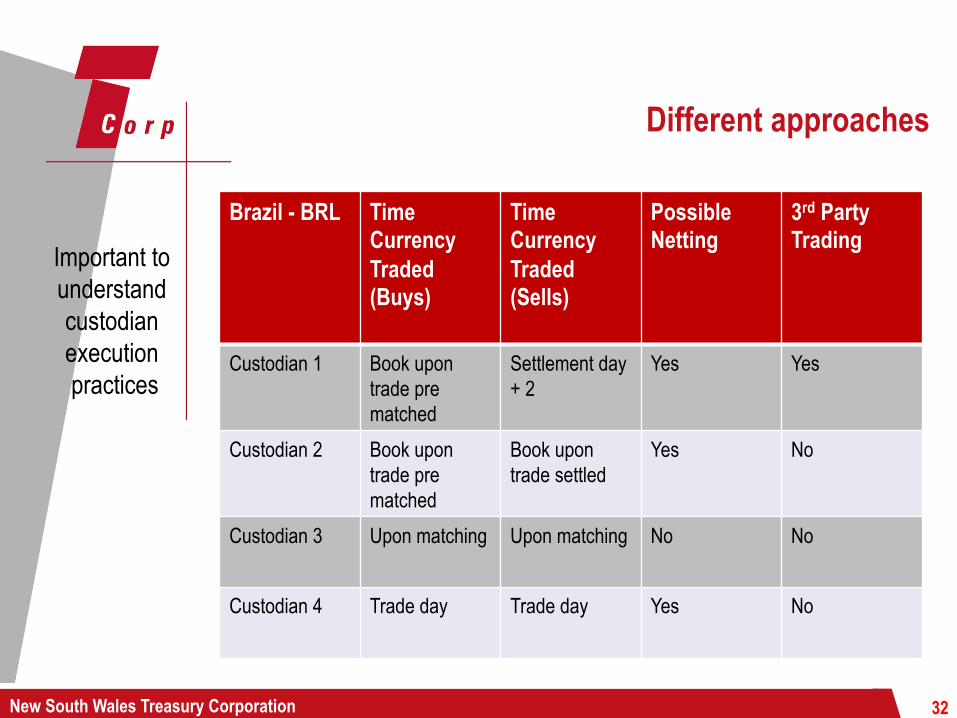

Different approaches

Brazil - BRL Time Currency Traded (Buys)

Time Currency Traded (Sells)

Possible Netting

3rd Party Trading

Custodian 1 Book upon trade pre matched

Settlement day + 2

Yes Yes

Custodian 2 Book upon trade pre matched

Book upon trade settled

Yes No

Custodian 3 Upon matching Upon matching No No

Custodian 4 Trade day Trade day Yes No

Important to understand custodian execution practices

32

New South Wales Treasury Corporation

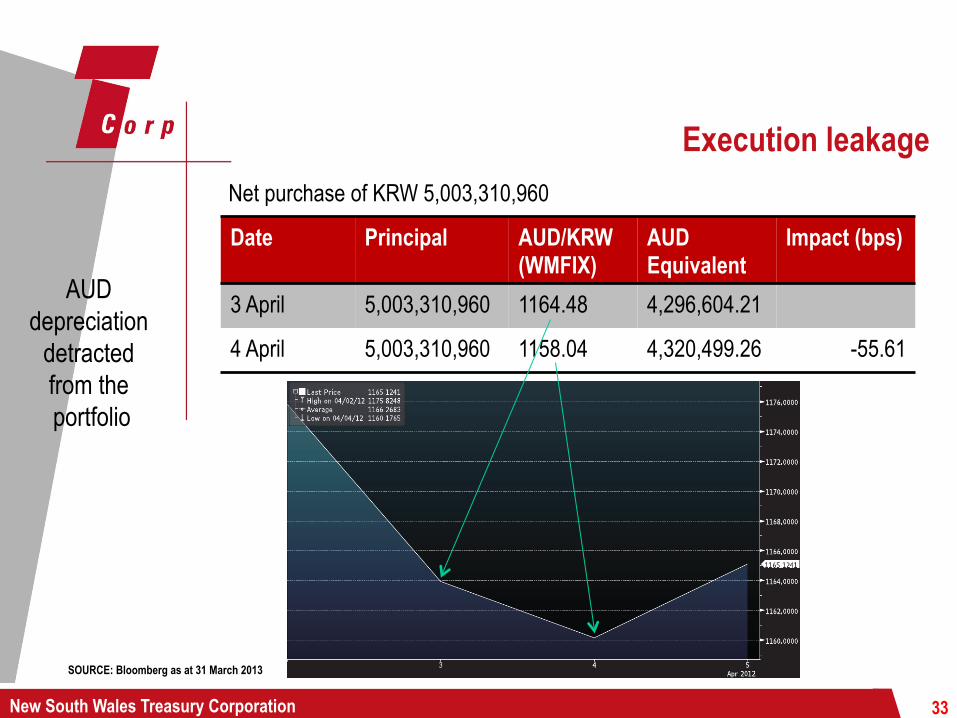

Execution leakage

AUD depreciation

detracted from the portfolio

Date Principal AUD/KRW (WMFIX)

AUD Equivalent

Impact (bps)

3 April 5,003,310,960 1164.48 4,296,604.21

4 April 5,003,310,960 1158.04 4,320,499.26 -55.61

Net purchase of KRW 5,003,310,960

SOURCE: Bloomberg as at 31 March 2013

33

New South Wales Treasury Corporation

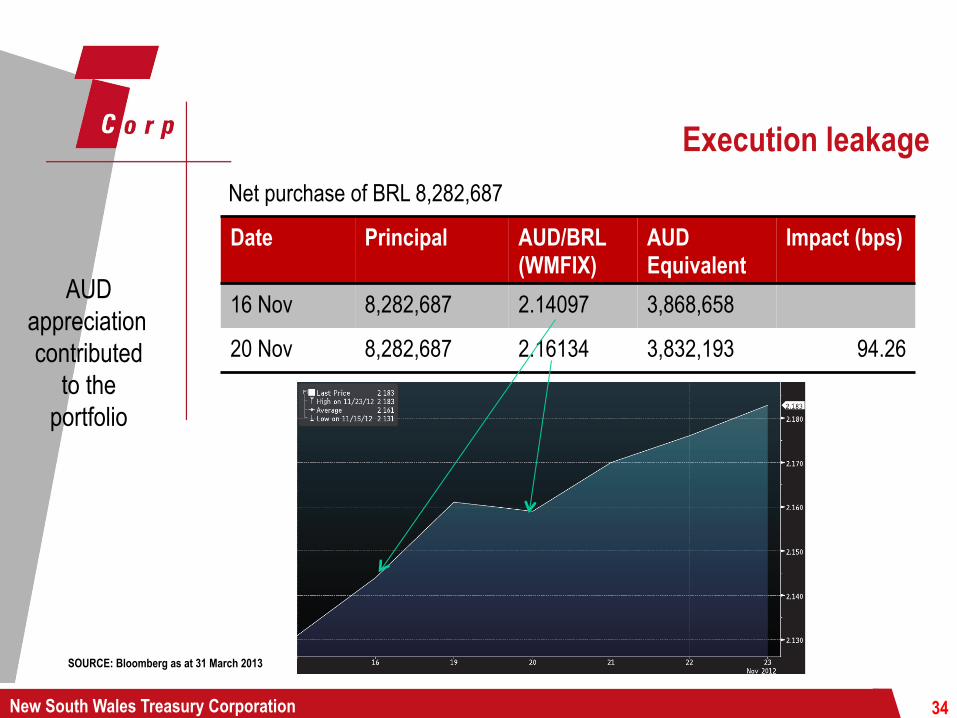

Execution leakage

AUD appreciation contributed

to the portfolio

Date Principal AUD/BRL (WMFIX)

AUD Equivalent

Impact (bps)

16 Nov 8,282,687 2.14097 3,868,658

20 Nov 8,282,687 2.16134 3,832,193 94.26

Net purchase of BRL 8,282,687

SOURCE: Bloomberg as at 31 March 2013

34

New South Wales Treasury Corporation 35

Key Learnings

New South Wales Treasury Corporation 36

Key Learnings

n Tangible reward for targeting inefficient foreign exchange execution

n Shared responsibility of all stakeholders

n Requires a structured and integrated framework

n Straight forward implementation

n Specific focus required on emerging market countries

n Embrace continuous improvement

An increased focus by asset

owners on foreign

exchange execution will

deliver tangible benefits to all

New South Wales Treasury Corporation

NSW Treasury Corporation

Level 22, Governor Phillip Tower 1 Farrer Place

SYDNEY NSW 2000 AUSTRALIA

Tel: +61 2 9325 9325 Fax: +61 2 9325 9333

www.tcorp.nsw.gov.au

37