beverage container management board (bcmb) · beverage container management system that is ... to...

TRANSCRIPT

BEVERAGE CONTAINER

(BCMB)

Benchmarking Evaluation of Alberta’s StewardshipProgram for Recycling Empty Beverage Containers

Final Report

Prepared For: Beverage Container Management Board

Prepared By: Meyers Norris Penny400, 10104

Edmonton AB T5J 0H8

MNP Contact: Rod Simpson

Date: Monday

ONTAINER MANAGEMENT BOARD

enchmarking Evaluation of Alberta’s StewardshipProgram for Recycling Empty Beverage Containers

Beverage Container Management Board

Meyers Norris Penny LLP

400, 10104 - 103 Avenue

Edmonton AB T5J 0H8

Rod Simpson

Monday, June 28, 2010

OARD

2

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

AUTHORS

QUALITY ASSURANCE PARTNER

Rod Simpson

PROJECT MANAGER

Nicole Asselin

SUBJECT MATTER ADVISOR

Charlie Meredith

2

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

TABLE OF CONTENTS

Executive Summary ..............................................................................................................................4

1. Introduction................................................................................................................................16

1.1. Project Objectives and Scope of Work ..........................................................................................................................161.2. Key Questions to be Addressed....................................................................................................................................161.3. Project Deliverables and Timelines ...............................................................................................................................17

2. Approach & Methodology.........................................................................................................18

2.1. Preliminary Research....................................................................................................................................................182.2. In Depth Benchmarking ................................................................................................................................................182.3. Assessment and Evaluation..........................................................................................................................................20

3. Program Attributes & Performance.........................................................................................21

3.1. Legislation ....................................................................................................................................................................213.2. Governing Structure......................................................................................................................................................233.3. Program Structure ........................................................................................................................................................253.4. Depot Infrastructure and Operations .............................................................................................................................263.5. Technology...................................................................................................................................................................293.6. Transportation ..............................................................................................................................................................323.7. Funding Mechanism......................................................................................................................................................333.8. Program Scope.............................................................................................................................................................363.9. Deposit Values..............................................................................................................................................................373.10. Beverage Container Sales ............................................................................................................................................393.11. Recoveries....................................................................................................................................................................423.12. Costs ............................................................................................................................................................................453.13. Marketing Initiatives ......................................................................................................................................................473.14. Research and Development..........................................................................................................................................493.15. Incineration for End Use ...............................................................................................................................................493.16. Comparisons ................................................................................................................................................................503.17. Learnings from Europe .................................................................................................................................................50

4. Opportunities for Consideration..............................................................................................52

4.1. Fundamentally Change the Funding Modelto Create Incentives for Brandowners to Enhance Container Design ..........524.2. Further Broaden Program Scope ..................................................................................................................................534.3. Develop and Support Regional Downstream Markets ...................................................................................................544.4. Support Research Projects to Enhance RE-Use and Recycling ....................................................................................544.5. Enhance Depot Role, Technology, Location and Operations ........................................................................................554.6. There are few Strategic and Operational Synergies with Other Recycling Programs.....................................................584.7. Local Marketing Initiatives Appear to Most Effectively Increase Recoveries ..................................................................59

5. Program Summaries .................................................................................................................61

5.1. Alberta ..........................................................................................................................................................................615.2. British Columbia............................................................................................................................................................655.3. Saskatchewan ..............................................................................................................................................................695.4. New Brunswick .............................................................................................................................................................715.5. California ......................................................................................................................................................................745.6. Connecticut...................................................................................................................................................................775.7. Michigan .......................................................................................................................................................................795.8. New York......................................................................................................................................................................805.9. Denmark.......................................................................................................................................................................815.10. Germany.......................................................................................................................................................................835.11. Norway .........................................................................................................................................................................855.12. Sweden ........................................................................................................................................................................885.13. South Australia .............................................................................................................................................................89

6. Appendices ................................................................................................................................91

6.1. Phase 1 – Interim Report ..............................................................................................................................................916.2. Data Questionnaire.....................................................................................................................................................1016.3. Interview Protocol .......................................................................................................................................................1056.4. Bibliography and References ......................................................................................................................................108

4

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

EXECUTIVE SUMMARY

The Beverage Container Management Board’s (BCMB) mission is to establish and administer a leadingbeverage container management system that is innovative, accessible, and cost effective. The BCMB’sbroad mandate is to collect and recycle beverage containers throughout Alberta, and continually ensurestheir current approach to container recycling fulfils the requirements placed upon the organization.

Toward that end, BCMB has engaged Meyers Norris Penny (MNP) to conduct a benchmarking study ofAlberta’s beverage container stewardship program with a particular focus on program evaluation andassessing leading practices and innovations in comparable jurisdictions. This benchmarking study buildsupon a similar study completed in 2004. The 2004 benchmarking study prepared by BearingPointidentified five opportunities for the BCMB to consider that may enhance the program and improverecoveries. Significant initiatives have been implemented, addressing each of the five opportunities asfollows:

1. The program scope continues to be significantly broadened with other food and dairy products tocontinue to divert an increasing number of containers from the waste stream. Alberta is the firstjurisdiction to include a broad range of dairy containers.

2. Deposit levels were doubled in most cases based on other jurisdiction’s success increasing theirdeposit rates and experiencing a significant improvement in recoveries. Alberta’s recoveries havecontinued to increase since deposit rates were increased. The harmonization of the deposit ratefor aluminum containers to 10 cents also created significant operational efficiencies.

3. Portions of beer and non-beer processing streams are currently being consolidated reducingduplication and costs. This is a major cost reduction initiative. Unlike most North Americanjurisdictions, collection of beer and non beer containers was largely consolidated to a depotsystem years ago enhancing consumer convenience, standardizing the deposit redemption forbeer and reducing overall program costs (with the exception of 62 retail liquor stores collectingapproximately 1.5% of the recovered containers).

4. Handling commissions were reduced after a thorough cost analysis that reduced overall programcosts, given handling commission represent over 60% of net program costs. New high speedsorting and compaction technology is presently being evaluated that may further reduce overallcosts throughout the system.

5. Marketing initiatives were implemented to improve public awareness and increase recoveries,with many specific initiatives focused on specific communities and products. Increasingrecoveries can be partially attributed to these marketing initiatives.

A major challenge in the beverage container recycling industry is that there is not a clearinghouse forprogram information. Each jurisdiction, and in many cases the brandowners within each jurisdiction,collects and reports their own results with varying commonality, disclosure and audit requirements;making comparisons challenging. This study is based upon the best data available.

Research and benchmarking efforts were conducted to answer the six key questions presented in theRFP for this project.

1. How does the overall effectiveness of Alberta’s program compare, in terms of achievingmandated outcomes (e.g. material collection rates with programs targeting those samematerials in other jurisdictions and, scope of materials covered)?

Alberta deploys a very effective container recycling program. Alberta has the highest sales percapita creating a potentially larger environmental liability regarding containers than comparablejurisdictions.

Alberta has the broadest program scope, incorporating by far the highest number of uniquecontainers. Alberta also was the first jurisdiction to include a broad range of dairy containers (milkand cream) in its deposit program.

5

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Alberta’s program is mature and recoveries had plateaued over the past several years. Depositrates were recently increased and significant funds are being expended in a broad marketingcampaign, resulting in increased recoveries for comparable aluminum, plastic, glass and papercategories trending towards the recoveries of the jurisdictions with the highest recoveries in NorthAmerica and Europe. Overall recoveries increased from 77% to 83% in one year as ofDecember, 2009, compared to the world leaders with recoveries in the 87% range (and all withmuch narrower and easier to recover program scopes).

2. How does Alberta’s program compare with those in other jurisdictions in terms to thetypes of environmental performance indicators that are tracked and measured by theprogram’s managing organization (from the collection through final disposition of thecontainers)?

Virtually all jurisdictions track environmental performance indicators in a comparable way. TheBCMB effectively tracks environmental performance indicators throughout their process.

3. What are the financial costs attributable to achieving mandated outcomes of Alberta’sprogram and how does this compare with the program costs in other jurisdictions?

Alberta’s net cost per container is as low as any comparable jurisdiction in North America, despitea large geographic area with a relatively sparse population.

Most of the jurisdictions examined have legislated an extended producer responsibility or productstewardship model designed to encourage brandowners to fundamentally change designs,packaging, etc to reduce waste while increase the re-use and recycling of waste materials.Despite this, most program costs are borne by consumers and governments, with minimal directcost to industry.

Alberta’s program (with the exception of refillable beer where a brandowner fee is levied,representing 9% of the container volume), like all comparable programs except California’s andthose in Europe, is funded by unredeemed deposits, consumer fees and revenues fromprocessed collected containers. There is no direct funding by government or by brandowners forall other products.

Major program costs are handling fees (primarily collection depots), processing, transportation,communications and administration expenditures.

4. How does Alberta’s program compare with programs in other jurisdictions in terms of thedisposition of collected materials (i.e. the amount of material that is re-used, recycled,recovered and the amount of material that ends up as residual disposed of in landfill)?

All collected materials are recycled, at times at a loss, in a closed loop system as Alberta and allother North American jurisdictions generally do not incinerate or landfill collected containers.There is minimal incineration including incineration for energy capture and gasification in mostjurisdictions.

Collected containers are commodities with varying values. The only material that has maintaineda substantial value is aluminum, it tends to stay “cash positive”, although this market is now injeopardy given mergers in the aluminum manufacturing industry. Glass and the various types ofplastic and paper tend to have low to nil values. Recycling of these products is heavily subsidizedthrough consumer or brandowner fees.

California is the only North American jurisdiction identified that has embarked on developinglegislation that may prescribe a minimum recycled content in containers. California is alsopartnering with academic institutions to research alternative container product compositions toimprove environmental breakdown and create more sustainable packaging and recyclingcapability. It can be debated whether this is the role for government, industry or whether whodoes it matters.

6

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

5. Are the most appropriate and efficient mechanisms being employed to achieve programobjectives in Alberta?

Alberta’s improving recoveries combined with low cost per container indicate that the Albertabeverage container recycling program is effective, thus mechanisms appear appropriate andefficient. This effectiveness is even greater when Alberta’s broad program scope, largegeographic area and relatively sparse population are considered.

Alberta’s program appears financially sound as escheatment practices, where excess depositfunds are re-allocated to provincial or state government general revenues as happens in manyUS jurisdictions as well as Saskatchewan, New Brunswick and Nova Scotia, does not occur in theprovince. California is an example of a jurisdiction where financial stress has been placed on theprogram because unredeemed deposits have been directed to general revenues.

Alberta’s program continues to add products to the program scope, and has the largest programscope in terms of number of unique items. The large majority of containers sold and collectedtraditionally have been aluminum, plastic and glass; but the recent introduction of dairy productcontainers to the program increases the volume of HDPE plastic and paper type products.

Two significant process changes have or are occurring. The first is the harmonization of depositrates for aluminum at 10 cents. As a result beer and non-beer aluminum streams need not besorted, creating tremendous process efficiency particularly given that aluminum is a large portionof the total volume of collected containers. The second change is been the ongoing consolidationof two collection agents. The official consolidation is targeted for January 2011. BrewersDistributor Limited (BDL) currently contracts Alberta Beverage Container Recycling Corporation(ABCRC) to collect all non-refillable beer. The goal is for beer and non-beer containers to becollected by one collection agent, receiving containers from 216 licensed collection depots inaddition to licensed liquor establishments that collect primarily refillable beer containers.

The number of container depots has not changed in many years and may require revision tomatch the change in Alberta’s population and demographics. While the number of depots has notchanged, the capacity of the depots in the system has increased drastically over that time.Depots have changed location, built bigger buildings or increased the number of service points.Several rural depots have closed and urban depots opened, thus the number has remainedstatic, the capacity has not.

On a broader basis, the North American container recycling industry has also been largely staticfor many years with most jurisdictions deploying similar physical operating models. The majorcost elements for all jurisdictions are labour, occupancy and transportation to sort, count andmove recovered containers to downstream processors, many outside of the jurisdiction.

To date sorting technology has yielded disappointing results, as reverse vending machines(RVMs) have generally proven to be slow, unreliable, and in the Alberta context, incapable ofhandling Alberta’s large program scope and climate. RVMs were intended to both increaseefficiency in depots as well as provide “mini-depots” throughout the community increasingrecoveries of difficult to recover containers consumed outside of consumer’s homes, schools andoffices – the first generation RVM technology has proven incapable of this second objective.

Newer technology that can automate sorting and counting in depots is being evaluated andappears promising. A new generation of RVMs designed as stand-alone kiosks to be located atgas stations, convenience stores et al as a joint venture between Pepsi and Waste Managementwill be tested in US jurisdictions in 2010 with the goal to recover the hereto unreachablecontainers.

Compaction has also been problematic, as audit and integrity requirements preventedcompaction at a depot level, resulting in double handling and counting driving significantly higherlabour, occupancy and transportation costs throughout the system. New sorting technologies maymake compaction at the depot level viable potentially driving process change and reducing costs.

7

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Some jurisdictions deploy a more rigorous franchise like contractual model for their collectiondepots, specifying signage, corporate dress, hours of operation, equipment, operating standardsand procedures, etc. Alberta’s collection depots operate with some independence within astructured set of standards. These jurisdictions view the commonality in their collection depotsincreases their ability to improve customer experience and potentially increase recoveries.

Alberta spends significantly more per capita on marketing than any other jurisdiction. Thiscommunications expenditure has increased in advance in preparation for the introduction of dairycontainers into the program and the increase in deposit levels.

6. What are the examples of best practices or innovative approaches to waste stewardship ofempty beverage containers that can be identified from this analysis that would beappropriate for consideration in Alberta?

The deposit program in Alberta is effective and cost efficient compared to others. The program isthe broadest, has the lowest cost per collected container, and recovery rates are rising andappear to be heading towards the 85% plus range matching the global leaders. To furtherincrease recoveries and reduce costs to match and potentially exceed where the leaders arenow, strategic initiatives regarding the financial model, container life cycle (design, materials,packaging and material end markets), recycling processes, and consumer engagement must bedeveloped and implemented. Seven strategic opportunities have been identified for Alberta toconsider based upon the review of other jurisdictions in North America, Australia and Europe thatmay provide incremental program benefit.

1. Consider Fundamental Changes to the Funding Model

Investigate moving from the current consumer/brandowner fee structure to cover financialshortfalls as recoveries increase to a California style brandowner fee based on brandownerproduct specific recovery facilitated by the implementation of next generation automatedcounting and sorting equipment.

Virtually all deposit programs are structured through legislation describing extended producerresponsibility or product stewardship; all programs are presently funded through unredeemeddeposits and revenue from processed containers, with consumer/brandowner fees applied tofund program. This is the Alberta model, whereby consumer fees (with brandowner fees forrefillable beer) increase as recoveries increase given the correlated unredeemed depositsdecrease. This is a closed loop system that will always remain viable, but total costs toconsumers (and refillable beer brandowners fees that may be partially or fully passed on toconsumers) also increase as recoveries increase, assuming static commodity prices forrecycled material.

California is unique where the State has legislated strictly brandowner fees on a materialstream basis. The major objective for brandowner fees in California is to create financialincentives that can fundamentally change the container life cycle (design, materials,packaging and end markets) to better facilitate recycling and improve environmentaloutcomes, and ultimately reduce brandowner net costs. Their view is that consumer fees maynot realize this same objective with consumers potentially viewing these fees as a tax,although it may be argued that consumers view products on a total cost basis, thus theincentive remains for brandowners to enhance the entire container life cycle to ultimatelyreduce overall costs.

To this end, California implemented a “processing fee offset” policy whereby the State pays ahigher portion of the processing cost shortfall as recoveries increased to preset benchmarks.This has resulted in brandowners paying as little as 15% up to a maximum of 65% of the netrecycling costs as recoveries have increased in conjunction with several simultaneousinitiatives. Given the state has escheated a significant portion of the unredeemed deposits,the processing fee offset has been cancelled and brandowners will pay a larger portion of thefinancial shortfall in 2010.

8

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

The current funding structure in Alberta creates several considerations:

The current structure creates a natural tension between increasing recoveries (thatautomatically reduces unredeemed deposits), and the financial integrity of the programthat currently survives on these unredeemed deposits, revenue from recoveredcontainers and consumer/brandowner fees. Higher recoveries may mean higher productcosts to consumers and potentially lower sales for brandowners.

Most US jurisdictions and several provinces escheat unredeemed deposits. Escheatsinvariably result in higher consumer/brandowner fees again resulting in higher prices forconsumers and potentially lower sales for brandowners.

Collected containers are commodities with fluctuating values. Aluminum has traditionallybeen cash positive whereas other materials such as PET, HDPE, glass and others havehad low to minimal values. Decreases in the value of these commodities will invariablyresult in higher consumer/brandowner fees.

Increasing deposit rates generate short term cash surpluses due to the value ofunredeemed deposits increasing and appear to result in increased recoveries. In theshort term increases in unredeemed deposits due to the higher deposit rates may declineas recoveries increase, resulting in higher consumer/brandowner fees.

Regardless whether a fee is charged to consumers or brandowners, it appears indifferentto consumers as both result in higher prices and potentially lower sales for brandowners.Current processes and technology deployed does not allow jurisdictions to trackrecoveries by brandowner or by brandowner product, thus brandowner fees are appliedby material stream regardless of the greater or lesser efforts made by particularbrandowners to improve the recovery and ability to recycle their containers. However, asthere is currently no subsidization between material streams, manufacturers may benefitby choosing a container material stream that has low fees.

Brandowners maintain and closely guard two proprietary items - their product formulaand their sales. Moving to a brandowner fee based on actual recovery by product andbrandowner would require sales and return data by product and brandowner. Albertadoes not currently have access to return data by product and brandowner, althoughCollection System Agents (CSAs) perform the critical role of information clearinghouseensuring the protection and security of this sales information.

California implemented a brandowner fee across the board largely because theirjurisdiction is approximately the size of Canada thus a market large enough to effectivelynegotiate with brandowners. Alberta, one tenth the size of California, may be in a poorernegotiation position, and may have to partner with other jurisdictions to effectivelyimplement widespread brandowner fees.

A California style brandowner fee based on brandowner product specific recovery embodiesthe principal of extended producer responsibility. This may create the financial incentive forbrandowners to compete with each other to fundamentally change design, materials,packaging et al with the goal to optimize recoveries and improve overall environmentaloutcomes. This type of fundamental move would require the implementation of nextgeneration automated counting and sorting equipment allowing Alberta and many otherjurisdictions to provide the actual recovery by brandowner and product.

2. Further Broadening the Program Scope Involves Broadening the Program Mandate

Alberta presently has the largest beverage container recycling deposit program scope in theworld as well as the highest per capita consumption of in scope beverages - 25% greaterthan BC and 66% more than Saskatchewan. The vast majority of beverages sold in theprovince (including aluminum, plastic, glass and paper containers) are already in theprogram. Further expansion of the program would logically go in two directions -incorporating food and cleaning containers that are constructed of the same material types asbeverage containers already in the program; and/or incorporating non sealing beveragecontainers such as paper/plastic/styrofoam cups and containers.

9

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Both options would be a significant extension from the current program mandate, and wouldventure into an area no other jurisdiction has attempted to pursue. There are significantvolumes of containers in both areas thus diversion from landfills may be significant. Potentialissues include resistance from brandowners and retailers, contamination concerns and thedevelopment of end markets where few exist now.

3. Develop and Support Regional Downstream Markets

Downstream markets are critical to the financial viability of a recycling program. Aluminum isthe only material that consistently generates enough revenue to cover the associatedrecycling costs. Plastic, glass (except refillables) and especially paper have consistently hadweak downstream markets and commodity values. That said, the one advantage recyclingprograms have is that they can deliver a constant supply of product which at times is valuablein the commodity marketplace.

California has developed a local market for plastics through a subsidization program.Approximately $5 million in subsidies are paid to downstream processors annually. Californiahas the critical mass to invest in market development given its size ($1.2 billion in programgross revenue and 16.2 billion recovered containers).

Given geographic proximity, Alberta and brandowners may consider partnering withneighbouring jurisdictions to investigate opportunities to leverage their cumulative volume todevelop regional markets for materials where few viable markets currently exist.

4. Support Research Projects to Enhance Re-use and Recycling

Only one jurisdiction appears to be funding third party research regarding container designand materials. California has partnered with academic institutions to develop alternativecontainer designs and materials that are easier to recycle and breakdown faster in theoceans, rivers and landfills.

One major project is the development of “bio plastic”. The State of California is alsoresearching methane based plastics (PHA) and industry has developed corn basedcontainers (PLA) and seeks to improve processing and enhance awareness with the public.The challenge with introducing both PHA and PLA containers is that they look very much likePET containers which may cause contamination problems in the PET recycling stream.

A second major project is gasification. Gasification has become a viable option for recycling(including containers) in Europe. Gasification is a flexible, reliable, and clean energytechnology that can turn a variety of low-value feed stocks into high-value products, replacingtraditional oil and natural gas as an energy source, and can provide a clean alternativesource of base load electricity, fertilizers, fuels, and chemicals. It is a manufacturing processthat converts any material containing carbon—such as coal, petroleum coke (petcoke),biomass, or many types of beverage containers—into synthesis gas (syngas). The syngascan be burned to produce electricity or further processed to manufacture chemicals,fertilizers, liquid fuels, substitute natural gas (SNG), or hydrogen. Gasification has beenreliably used on a commercial scale worldwide for more than 50 years.

Alberta and all North American jurisdictions have long standing objections regardingtraditional incineration (whether for waste or low efficiency energy recovery) which isgenerally viewed as comparable to land filling. Gasification appears to be an incremental toexponential improvement upon traditional burning technologies, and a case can be made thatgasification may be a far better end use of some container streams for the environment thantraditional recycling processes. This is an area that may be worth further scrutiny; especiallygiven the City of Edmonton is building a gasification plant.

As a separate North American wide solely brandowner funded initiative, Coca-Colaintroduced the “PlantBottle” in the fall of 2009 that is made from a blend of petroleum-basedmaterials and up to 30 percent plant-based materials. The "PlantBottle" is currently made

10

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

through a process that turns sugar cane and molasses, a by-product of sugar production, intoa key component for PET plastic. Manufacturing the new plastic bottle is reportedly moreenvironmentally efficient as well. Coca-Cola claims a life-cycle analysis indicates the"PlantBottle" with 30 percent plant-base material reduces carbon emissions by up to 25percent, compared with petroleum-based PET. A significant advantage to the "PlantBottle" isthat, unlike other plant-based plastics, it can be processed through existing manufacturingand recycling facilities without contaminating traditional PET. Another brandowner driveninitiative has been the significant reduction of plastic (PET) in containers over the past coupleof years, especially water bottles.

These initiatives are a conundrum, as the philosophy driving existing container recyclinglegislation is extended producer responsibility based on brandowners driving this effort tofundamentally redesign containers and packaging to facilitate re-use and recycling, andprotection of the environment, and not government organizations and their delegatedauthorities. Conversely, it may be indifferent to consumers how dollars are collected that fundresearch like this, whether it be through increased product costs, consumer fees,unredeemed deposits, or provincial/federal taxes; as the net total cost to the consumer maybe unchanged. In addition, initiatives such as gasification may require legislative support.

5. Enhance Depot Role, Technology, Location and Operations

a. Increase Depot Responsibility for Local Recovery RateThe Alberta depots presently are licensed to accept empty registered beveragecontainers, refunding customer deposits as per legislation, and receive compensationfrom the brandowner’s operational entities, ABCRC and ABCC. Depots are licensedindependently from the ABCRC and are under the jurisdiction of the BCMB. BCMB andthe brandowners are presently responsible for recoveries, not the depots, yet the depotsare the only organization that interacts with the public and in the local communities.Depots are currently a service provider with no direct responsibility for recoveriesalthough they are directly impacted by recoveries, as their revenue increases as theirvolume of redeemed containers increases which should relate to recoveries.

Most jurisdictions interviewed indicated that in their experience, the most effectivemarketing initiatives appear to be community based rather than broad jurisdiction wideinitiatives. If this philosophy is accepted and embraced, the depot appears bestpositioned to drive community based marketing programs to drive recoveries versusBCMB or the brandowners.

California deploys a program whereby depots are eligible for a bonus for increasing theirvolume to certain pre-established benchmarks. The intent is to entice depots to market“recycling” in their local area to increase their volumes thus increasing recoveries – thisprogram was implemented simultaneously with increased deposit rates resulting inincreased overall state recoveries. This initiative’s risk is that volumes are transferredfrom one depot to another with net recoveries unchanged.

There may be merit investigating the sharing of strategic responsibility for recoveries withthe depots. One option to consider is the California model, whereby financial incentivesare provided for increases in depot volume. A second option is revising the depotcompensation model whereby recoveries are managed by sales in the depot area, anddepots are compensated partially based on recoveries in their “area” – a much morecomplex approach. This may create significant additional financial incentives to optimizerecoveries on a local basis.

b. Add Capital Intensive Technology to Reduce Variable Labour CostsThe current manual sorting at the depot and the ABCRC levels is extremely expensive,susceptible to human error, and slow. Reverse vending machines (RVMs) have beentested in Alberta and are deployed in other jurisdictions with minimal success. They are

11

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

slow, unreliable, and unable to process many of the containers that are within theAlberta’s program scope. RVMs have proven not to mitigate much of the labourcomponent and cost, and also don’t solve the current audit and compaction issues.

A new generation of automated counting and sorting technologies as well as compactiontechnologies at the depot level are currently being investigated by Alberta and otherjurisdictions. Several sorting, counting and compaction technologies employed by otherjurisdictions were documented during the benchmarking initiative. The leading technologyis from Denmark and marketed by Anker Anderson. This technology is capable of 32material type sorts and uses a bar code scanner with reported accuracy ratings of 98-99%. Given Alberta’s wide range of material types in its program and manually sortsreturned containers, the implementation of this type of technology presents potentiallysignificant process improvement opportunities.

The benefit would be reducing overall provincial processing costs (primarily labour) ascontainers can be counted, sorted, compacted and audited at the depot level- thus amove to single handling of containers. Depot capacities would also be greatly increasedwith minimal requirements for additional floor space. Consumers will have theircontainers counted and sorted extremely quickly and accurately. Given this equipmentsorts by bar code, contamination can mitigated if and when PLA containers areintroduced to the container stream.

The issue is the high capital cost, as the cost of each sorting unit ranges between$200,000 and $400,000. Compaction units are also capital intensive.

Consistent with the implementation of new and expensive technologies at the depot levelis the concept of ABCRC moving to a cross dock and brokerage operation rather asecondary sorting, compacting and audit operation, reducing overall system costs.

c. Locate More Depots in Retail Areas to Improve Customer AccessAlberta’s program, like most North American jurisdiction’s programs, began in the 1970sand 1980s based on a return to retail concept that beer retailers have successfullyoperated long before the advent of deposit systems for non beer containers in the 1970s.

The initial deposit systems for non beer containers were based primarily on a return toretail model similar to the beer. Beer retailers have continued to maintain return to retailoperations in Alberta and most other jurisdictions; while non beer container recyclingmigrated to stand alone depots that are now located primarily in industrial or commercialareas due to local zoning restrictions. Municipal ordinances restricting depot locations toindustrial and commercial areas is a common complaint by most North Americanjurisdictions as a barrier to improving recovery as customer access is potentially poor.

Alberta has largely merged the beer return to retail system with the non beer depots, asthere are now only 62 beer retailers collecting beer containers representingapproximately 1.5% of the total container stream. These 62 beer retailers remain out ofthe 145 beer retailers that were grandfathered into the system in 2001 when beer wasregulated in the Beverage Container Recycling Regulation. The BCMB has not acceptedany application from beer retailers for permits since these original retailers weregrandfathered. Other jurisdictions such as BC and Saskatchewan are merged to a lesserdegree.

One reason for this being beer retailers remit consumers their entire deposit whereassome depots remit only a portion of the consumer’s deposit. The result is that mostjurisdictions have beer retailers collecting beer containers in retail areas and depotscollecting all containers (including beer containers, but in many cases remitting onlypartial deposits) located in commercial or light industrial areas. Regardless of thereasons, consumers outside of Alberta with beer and non beer containers must sort and

12

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

return their containers to different collection systems to redeem a discounted rate on theirpaid deposits.

California’s structure has merged the depot system with return to retail. Large grocerystores are legislated by the State as a “convenience zone” and in very simplistic termsmust provide a recycling depot within a half mile of their store (the legislation is muchmore complex than this, and allows for one depot to service several retailers in closeproximity). As a result, many large grocery stores have a depot located in their parking lotbeside or behind the store (the customers and containers don’t enter the store, and trafficand trucks are already present). The depot provides the customer a ticket voucher that isredeemed in the grocery store for cash or merchandise.

Pepsi and Waste Management have announced a program to place a new generation ofRVMs in public areas such as gas stations, convenience stores, stadiums, parks, etcoffering a personal reward system, allowing consumers to collect and redeem points foreach bottle or can they recycle in the RVM beginning in 2010. This may also be anopportunity to investigate to improve customer access if the technical issues that plaguedthe first generation of RVMs can be resolved (acceptance of complete program scope,mechanical reliability, climate compatibility, etc).

Alberta may want to investigate the California “convenience zone” structure as it may beviable in many communities as a way to improve visibility and consumer access. Thisprocess can facilitate better cash management, and is a marketing venture for thegrocery store without the issues historically related to return to retail as originallydesigned. This also provides a cross marketing opportunity for the retailer to market toconsumers redeeming their deposit through coupons, offers, etc.

d. Review and Update Depot Network and Geographic CoverageA thorough review of the existing depot network and the communities they serve shouldbe considered. The network of 216 Alberta depots has been in place for many yearswhile the communities they serve have grown, and in many cases the growth has beenimmense. While the numbers of depots has not substantially changed, the capacities andthroughput of the existing depots have increased substantially. Despite this capacityincrease, there may be incongruence’s between the network and the communities thatthey serve regarding access, service and capability.

Determining the optimal number of depots is difficult. Geography, populationdemographics, transportation networks, depot location dynamics (retail vs. commercialvs. Industrial) and depot size all impact the assessment, and make a “depots per capita”comparison of lesser value.

The potential deployment of new equipment estimated to cost hundreds of thousands ofdollars per depot may present the appropriate opportunity to review the depot networkincluding the number, size, geographic location, zoning location (retail vs. commercial vs.industrial locations), capability, service standards et al; and adjust the network based onthe current and forecast market requirements in conjunction to determining where andhow to deploy this expensive technology. There are obviously barriers in place in Albertaregarding adjusting the network, not the least of which are zoning challenges and overallresistance within communities to the location of depots in retail areas.

The significant cost of this technology may drive the depot network to move to a “hub andspoke” system used by numerous distribution, warehousing and transportationorganizations. The result of this type of network would result in small depots that don’thave the volume to justify expensive technologies transporting containers to largerregional depots for counting, sorting, audit and compaction rather than the present modelwhere all 216 depots collect containers and then transport the same containers to

13

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

ABCRC processing centres in Calgary, Edmonton, Lethbridge and Red Deer forcounting, sorting, audit and compaction (once the ABCC consolidation is complete).

e. Enhance Commonality of Alberta’s DepotsAlberta’s depots, as with depots in most jurisdictions, operate with a degree ofindependence. Alberta depots adhere to a series of service standards, but generally donot have common signage, corporate dress, hours of service, or specific servicestandards in place—each depot is very different from the next. Saskatchewan depotsoperate on more of a “franchise” model basis with many more common elements such assignage, corporate dress, etc. Most jurisdictions interviewed would prefer that theirdepots operate with the premise that a standardized approach to depot operationsensures a standard for customer service and is a contributing factor to optimizingrecoveries. The reality is that most jurisdictions operate a legacy network of independentdepots making standardization a difficult process.

There may be opportunities to enhance the service at Alberta depots that may contributeto increased recoveries through the implementation of more provincial standards fordepot signage, appearance, location and service. This is in line with the vast majority ofsuccessful retail and service organizations that strive to standardize their operations froma customer perspective to optimize revenue and profit (and in the case of depots,recoveries and their profits).

6. Minimal Strategic and Operational Synergies with other Recycling Programs

Alberta, and most other North American jurisdictions, has separate recycling programs fortires, lubricating oil, oil containers, glycol containers oil filters, electronics, batteries, paint,hazardous household waste and dairy containers (outside of Alberta). Municipal blue boxprograms are also proliferating. Some depots in Alberta (approximately 50) andSaskatchewan collect used oil and electronics, with depots in other jurisdictions alsocollecting those and other recyclable products.

There appear to be few synergies with other programs at both the strategic and operationslevel due to different customer requirements for collection, risk and cost of crosscontamination (many of the other products contain toxins), the differing requirements ofprocessing and end markets, and the need to optimize labour and transportation efficiencies.A direct comparison between deposit programs and blue box programs was not explored, asthe focus of this report was to compare deposit programs.

7. Local Marketing Initiatives Appear to Most Effectively Increase Recoveries

The relationship between marketing (and specifically funds spent) and recovery rates isdebatable. Alberta spent $4.3 million on marketing in 2008 in anticipation of the increase indeposit rates and the addition of dairy containers to the program. Recoveries for non-beeraluminum, plastic and glass increased almost immediately as a result of the combinedincrease in deposit levels, a massive marketing effort and a downturn in the provincialeconomy. Separating the impact of each is difficult – most other jurisdictions view depositrates as the driver of recoveries versus marketing, but few have ever spent this magnitude offunds on marketing.

Virtually all other jurisdictions continue to spend relatively few dollars on marketing initiativesexcept BC. Marketing initiatives consist of traditional media advertising (TV, radio, print andinternet), joint ventures with partners that generally takes the form of fundraising for non-profitorganizations, community initiatives lead by local champions (community clean upcampaigns, etc) and small scale local initiatives.

14

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

a. Traditional Advertising Quickly has Diminishing ReturnsMost jurisdictions do little advertising through media such as print, TV, radio and internet.Beverage container recycling programs tend to be mature and have been well brandedsince their introduction. The consensus of reviewed jurisdictions is that the messagerequires reinforcement, but there are quickly diminishing returns.

15

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

b. Recycling Initiatives with Community Partners Appear PromisingAlberta and most jurisdictions have had success partnering with primarily non-profitorganizations to drive local recoveries while assisting the partner organization to raisefunds. The non-profit organization essentially collects containers in the local communityideally including containers that otherwise may not have been recycled.

c. Focus Marketing Locally in Each CommunitiesAlberta and most jurisdictions have found that the most effective marketing is in localcommunity and not jurisdiction wide advertising campaigns. Local marketing take theform of community clean ups, recycling drives in schools, etc, and usually are mosteffective when there is a local “champion”. There may be opportunities to leverage thedepot’s presence in their communities regarding local marketing.

d. Investigate Customer Rewards InitiativesCustomer loyalty programs have been extremely successful in numerous industries,ranging from earning “points” or “coupons” redeemable for merchandise, services, airtravel, etc.

In the recycling field, California has seen the beginning of industry developed loyaltyprograms. Los Angeles has recruited marketing partners whereby frequent users (basedon the volume of materials in the curb side boxes) receive coupons from participatingsponsors. The “Toll Roads”, a DAO like organization that manages the toll freeways insouthern California, has partnered with several retailers who in one case will pay $5 in acustomer’s Toll Road account for every $100 spent in the retailer’s store. A large highprofile grocery store will pay $0.10 per gallon of gas at a specific service station chain toa maximum amount for every $100 spent in their store (gas stations in Alberta havesimilar programs with air travel organizations).

There is also the Pepsi – Waste Management Dream Machine initiative referenced earlierthat is also based on a loyalty program.

There may be opportunities worth investigating in this area to drive additional recoveriesof containers through a “frequent beverage container recycler program” whereby aperson earns points, coupons or other types of perceptive value based on volumesrecycled.

16

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

1. INTRODUCTION

1.1. PROJECT OBJECTIVES AND SCOPE OF WORK

The BCMB has been given ambitious targets for beverage container recycling in Alberta. Over the nextfew years, the BCMB is expected to achieve a minimum recovery rate of 85% and become a leader in thebeverage container recycling industry with a system that meets the Province’s expectations and that isinnovative, accessible and cost effective. The BCMB’s 2009 – 2011 Three Year Business plan identifiesfive priorities for beverage container recycling system:

Improved (and thus sustained) return rates. Reduced environmental impact for container use. Cost effective recycling system operations. Effective governance and management. Accountability and transparency.

Given the ambitious timeframes and the need to move quickly, Meyers Norris Penny (MNP) was engagedto identify opportunities that may contribute to increased return rates and to system cost effectiveness.Effectiveness was evaluated with respect to achieving mandated beverage container recycling outcomes,environmental performance, cost efficiencies, and the disposition and use of processed containers.Industry innovation and leading practice information was collected to provide a broad evaluation ofsystems in other jurisdictions and to consider opportunities for Alberta’s container recycling system.

1.2. KEY QUESTIONS TO BE ADDRESSED

As presented in the Request for Proposal for this engagement, the research and analysis needed toaddress the following six key questions

1:

1. How does the overall effectiveness of Alberta’s program compare, in terms of achievingmandated outcomes (e.g. material collection rates with programs targeting those same materialsin other jurisdictions and, scope of materials covered)?

2. How does Alberta’s program compare with those in other jurisdictions in terms to the types ofenvironmental performance indicators that are tracked and measured by the program’s managingorganization (from the collection through final disposition of the containers)?

3. What are the financial costs attributable to achieving mandated outcomes of Alberta’s programand how does this compare with the programs costs in other jurisdictions?

4. How does Alberta’s program compare with programs in other jurisdictions in terms of thedisposition of collected materials (i.e. the amount of material that is re-used, recycled, recoveredand the amount of material that ends up as residual disposed of in landfill)?

5. Are the most appropriate and efficient mechanisms being employed to achieve programobjectives in Alberta?

6. What are the examples of best practices or innovative approaches to waste stewardship of emptybeverage containers that can be identified form this analysis that would be appropriate forconsideration in Alberta?

1 Key Questions to be Addressed. Request for Proposal Benchmarking Evaluation of Alberta’s Stewardship Program for Recyclingof Empty Beverage Containers. Beverage Container Management Board. Issue date: September 28, 2009. Page 1.

17

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Building a response to these key questions required research effort in four main areas, these were theprimary focus of MNP’s work:

The achievements of the BCMB’s program compared with other jurisdictions. Focus is placed onkey mandated outcomes such as material collection rates on a container stream specific basis.

The environmental performance indicators that are tracked and measured by the BCMBcompared to other jurisdictions. These indicators relate to all aspects of the program fromcollection through to final disposition of containers.

The financial costs attributed to achieving the mandated outcomes. The disposition of collected materials in Alberta and other jurisdictions. This includes

comparisons of the amounts of material re-used, recycled and recovered versus land filled.

Additionally, leading practices and innovative approaches identified through the research and analysis ofother jurisdictions are to be highlighted for consideration by Alberta’s beverage container stewardshipprogram.

A major challenge in the beverage container recycling industry is that there is not a clearinghouse forprogram information. Each jurisdiction, and in many cases the brandowners within each jurisdiction,collects and reports their own results with varying commonality, disclosure and audit requirements;making comparisons challenging. This study is based upon the best data available.

1.3. PROJECT DELIVERABLES AND TIMELINES

Project deliverables and timelines were discussed during the project planning and initiation activities inPhase 1. The projected project end was initially March 12, 2010. Due to delays in engaging comparablejurisdictions, timelines for the project shifted. The final report, this document, was provided to BCMB onFriday, June 25.

18

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

2. APPROACH & METHODOLOGY

2.1. PRELIMINARY RESEARCH

MNP conducted desktop research reviewing current beverage container deposit systems in jurisdictionsacross Canada, the United States (US) and Europe. A preliminary evaluation revealed a number ofpotential comparable jurisdictions that may be effectively benchmarked against Alberta’s approach andsystem for container recycling. The selection was based on the jurisdictions: 1) comparability to theAlberta model in the areas of governance structure, the types of containers collected and the source ofprogram funds, and 2) the overall strength of the collection program including the demonstration ofleading practices and innovative approaches.

The beverage container recycling programs chosen for comparison were organized into two tiers. Thefirst encompassed eight programs or jurisdictions that were considered relevant for effectivebenchmarking. Research to date revealed that these programs, spanning Canada, the US, Europe andAustralia, lead the field in terms of their organizational structure, overall effectiveness, or their innovativepractices.

BC Saskatchewan Oregon California Norway Denmark Germany South Australia

There is a second tier of programs that were considered to add value to the benchmarking despiteduplicating some of the systems examined in Tier 1 or possessing key characteristics that may limit directcomparisons to Alberta’s approach. These jurisdictions are particularly well-suited to an investigation ofleading practices, and further research can enhance the benchmarking analysis. The following fourprograms were chosen to be studied in greater depth and compared to Alberta:

New Brunswick Michigan New York Sweden

2.2. IN DEPTH BENCHMARKING

MNP conducted a review of leading practices within the industry during the in depth benchmarking studyof selected jurisdictions. The differing approaches to beverage container recycling deployed by certainNorth American and international jurisdictions provide a basis for a review of alternative approaches andleading practices that may be applied towards improvements in Alberta’s system. In addition to evaluatingprogram scope, deposit levels, sales, recoveries and costs, a review of leading practices was conductedin the following categories:

Legislation and regulation; Program structure including depot incentives and deposit rates; Depot infrastructure and operations including depot organization, depot locations and corporate

standards; Technology; Transportation; Marketing initiatives; Incineration for end use; and European initiatives.

19

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Data questionnaires were designed to collect information about a jurisdiction’s program, containersincluded in the program, recycling volumes, return rates, deposit rates, financial data (revenues andcosts), materials handling and disposition practices, environmental performance measures and leadingpractices. The complete data questionnaire is provided in Appendix B.

Data questionnaires were sent to representatives in jurisdictions that agreed to participate in the study. Insome cases, the data questionnaire was sent as part of the request for participation to facilitate identifyingthe appropriate contact in a jurisdiction. Interview protocols were developed to guide a telephoneinterview discussing additional program details, evaluating leading practices about technology, marketingbudget spending, environmental activities, and performance measures. The interview protocol sent tointerviewees is provided in Appendix C.

Given the amount and diversity of information being requested, in some cases answers and knowledgeabout a jurisdiction’s recycling program was spread across numerous people, departments and/orcompanies. In those cases, every reasonable effort was made to engage the right stakeholders whileensuring each key player was given the opportunity to participate. For example, in New Brunswick asystem regulated by the New Brunswick Environment (government) and implemented by two agents.MNP was successful in engaging the government and one agent, Alcool. Rayan Investments, the otheragent, declined to participate in our study. In this case, two data questionnaires were collected and twointerviews conducted to ensure MNP gathered as much information as possible to develop a strongunderstanding about all aspects of the jurisdiction’s practices.

The following table, Exhibit 2-1 depicts by jurisdiction the departments/companies contacted and whatinformation MNP was able to collect.

Exhibit 2-1Jurisdiction Participation Summary

Jurisdiction Agent/ Company/ Government Department Data Questionnaire Interview Notes

Encorp Pacific ● ●

Brewers Distributor Ltd ● ●

Saskatchewan SARCAN ● ●

New Brunswick Environment ● ●

Alcool ● ●

Rayan Investments - -

California

Department of Resources Recycling and

Recovery● ●

Oregon - - Declined to participate

Department of Environmental Protection ● ● Subsitution for Oregon

Department of Environmental Protection,

Recycling Division- -

Department of Environmental Protection,

Pollution Division- -

Department of Treasury ● -

Used Beverage Container Recovery (UBCR) - ●

New York Department of Environmental Conservation - -

Norway Norsk Resirk - -

Sweden Environmental Protection Agency - -

Denmark Retursystem - - Received notes from John Bachinski

Germany Pfandsystem GmbH - - Received marketing materials

Statewide Recycling Pty. Ltd ● ●

Marine Store Pty. Ltd - -

Environmental Protection Agency - -

● Information collected - Information not collected

British Columbia

New Brunswick

Connecticut

Michigan

South Australia

20

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

In some cases, identifying an appropriate contact in particular jurisdictions willing to participate in thebenchmarking presented significant challenges. Mid-way through the project Oregon was substituted forConnecticut as they declined to participate. While other jurisdictions initially agreed to participate, theyeventually declined. Online information has been used to populate tables where possible.

Jurisdictions track and monitor program performance differently. Sales, recoveries and cost informationare inconsistently reported and often not directly comparable to other jurisdictions. Our approach was tonormalize all data where feasible to facilitate accurate comparisons. Additionally, private sectororganizations in many jurisdictions are responsible for beverage container recycling and view some of allof the information requested to be proprietary, thus little to no information in some jurisdictions could beaccessed, particularly in Europe. Despite the challenges, a critical mass of information was collected toeffectively benchmark the BCMB program and answer the six questions posed as the basis of theengagement.

2.3. ASSESSMENT AND EVALUATION

Information and data collected throughout the research and benchmarking activities was compiled andorganized to facilitate review. Using the evaluation framework developed in advance of the researchactivities, evaluation and analysis was undertaken to answer the questions posed as the basis of theengagement.

Quantitative and qualitative analysis was conducted to determine findings and draw conclusions about:

The BCMB’s achievement of its program mandate including its collection rates and the scope ofmaterials covered.

Environmental performance including the tracking and monitoring that occurs to monitorachievements from container collection through disposition.

Program costs based on calculations that normalize comparisons between jurisdictions wherepractical.

The disposition of collected materials and opportunities to improve the reuse, recovery andrecycling of containers through the identification of practices that reduce recyclables in landfills.

The effectiveness of different approaches used to meet recycling program objectives and theopportunities for improvement.

The relevant marketing, technology and partnership arrangements that other jurisdictions haveentered into.

Appropriate leading practice opportunities for Alberta to improve waste stewardship of emptybeverage containers and develop innovative approaches for future consideration.

21

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

3. PROGRAM ATTRIBUTES & PERFORMANCE

Benchmarked programs operate similarly in that they each refund a deposit (or portion thereof) thatconsumers paid when they purchased a beverage container. Empty containers are collected, processedand recycled for the material to be used again thereby reducing waste and protecting the environment.Different funding strategies exist but most jurisdictions finance operations by using unredeemed deposits,an additional consumer fee (termed a Consumer Recycling Fee, or CRF, in Alberta), a brandowner feeand the sale of processed containers.

This chapter contains program information and performance data for reviewed jurisdictions whereinformation was available. Several jurisdictions selected for in-depth study declined to providebenchmarking data required to undertake analysis and draw conclusions. All Canadian jurisdictions not inthe scope of the in-depth benchmarking but whose data was readily accessible are included in theprogram performance evaluation to better compare Alberta to others in the beverage container recyclingindustry.

3.1. LEGISLATION

Beverage container stewardship exists in varying forms where regulation may define programparameters, governance model, materials scope, funding model, licensing and permitting depotoperations, and set deposit-refund amounts and recovery rate targets. Across jurisdictions, the objectiveof implementing stewardship programs is consistent; to maximize recovery of containers to reduce theenvironmental impact of beverage containers on the environment, to divert materials from landfills and tore-use or recycle beverage containers. In many cases, beverage container stewardship legislationoriginates in a government’s efforts to solve a common problem: litter.

As early as 1970, Canadian provinces began legislating beverage container recycling many to reduce theimpact of litter in communities. BC led legislating beverage container stewardship by introducing theirRecycling Regulation in 1970, followed closely by Alberta in 1972 with the Alberta Beverage ContainerRecycling Program. Several other Canadian provinces and US jurisdictions soon followed in the late1970s and 1980s. European countries began legislating beverage container recycling programs in the1980s and 1990s. South Australia introduced legislation in 1975 and while planning is underway, theycontinue to this day as the only Australian state with a beverage container stewardship program in place.

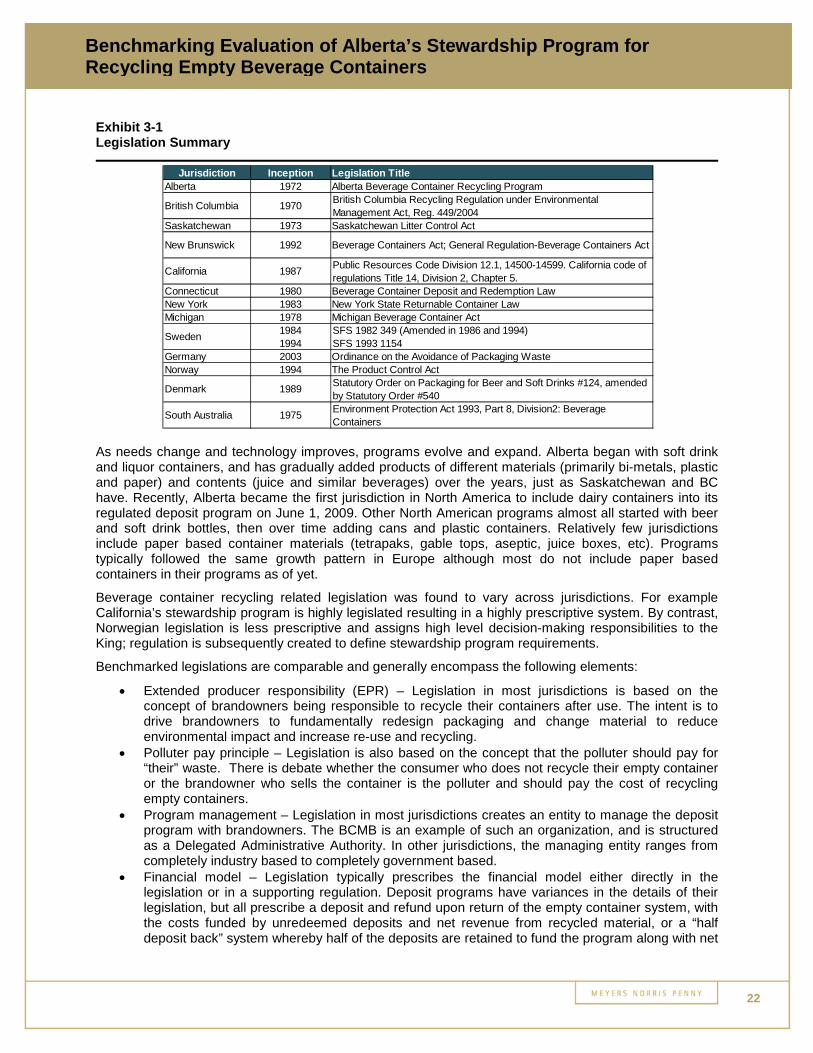

Exhibit 3-1 illustrates an overview of the dates stewardship programs were implemented in eachjurisdiction. It also states the legislation that led to the program's existence.

22

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Exhibit 3-1Legislation Summary

As needs change and technology improves, programs evolve and expand. Alberta began with soft drinkand liquor containers, and has gradually added products of different materials (primarily bi-metals, plasticand paper) and contents (juice and similar beverages) over the years, just as Saskatchewan and BChave. Recently, Alberta became the first jurisdiction in North America to include dairy containers into itsregulated deposit program on June 1, 2009. Other North American programs almost all started with beerand soft drink bottles, then over time adding cans and plastic containers. Relatively few jurisdictionsinclude paper based container materials (tetrapaks, gable tops, aseptic, juice boxes, etc). Programstypically followed the same growth pattern in Europe although most do not include paper basedcontainers in their programs as of yet.

Beverage container recycling related legislation was found to vary across jurisdictions. For exampleCalifornia’s stewardship program is highly legislated resulting in a highly prescriptive system. By contrast,Norwegian legislation is less prescriptive and assigns high level decision-making responsibilities to theKing; regulation is subsequently created to define stewardship program requirements.

Benchmarked legislations are comparable and generally encompass the following elements:

Extended producer responsibility (EPR) – Legislation in most jurisdictions is based on theconcept of brandowners being responsible to recycle their containers after use. The intent is todrive brandowners to fundamentally redesign packaging and change material to reduceenvironmental impact and increase re-use and recycling.

Polluter pay principle – Legislation is also based on the concept that the polluter should pay for“their” waste. There is debate whether the consumer who does not recycle their empty containeror the brandowner who sells the container is the polluter and should pay the cost of recyclingempty containers.

Program management – Legislation in most jurisdictions creates an entity to manage the depositprogram with brandowners. The BCMB is an example of such an organization, and is structuredas a Delegated Administrative Authority. In other jurisdictions, the managing entity ranges fromcompletely industry based to completely government based.

Financial model – Legislation typically prescribes the financial model either directly in thelegislation or in a supporting regulation. Deposit programs have variances in the details of theirlegislation, but all prescribe a deposit and refund upon return of the empty container system, withthe costs funded by unredeemed deposits and net revenue from recycled material, or a “halfdeposit back” system whereby half of the deposits are retained to fund the program along with net

Jurisdiction Inception Legislation Title

Alberta 1972 Alberta Beverage Container Recycling Program

British Columbia 1970British Columbia Recycling Regulation under Environmental

Management Act, Reg. 449/2004

Saskatchewan 1973 Saskatchewan Litter Control Act

New Brunswick 1992 Beverage Containers Act; General Regulation-Beverage Containers Act

California 1987Public Resources Code Division 12.1, 14500-14599. California code of

regulations Title 14, Division 2, Chapter 5.

Connecticut 1980 Beverage Container Deposit and Redemption Law

New York 1983 New York State Returnable Container Law

Michigan 1978 Michigan Beverage Container Act

Sweden1984

1994

SFS 1982 349 (Amended in 1986 and 1994)

SFS 1993 1154

Germany 2003 Ordinance on the Avoidance of Packaging Waste

Norway 1994 The Product Control Act

Denmark 1989Statutory Order on Packaging for Beer and Soft Drinks #124, amended

by Statutory Order #540

South Australia 1975Environment Protection Act 1993, Part 8, Division2: Beverage

Containers

23

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

revenue from recycled material. Additional consumer fees are typically allowed within thelegislation or within policy where unredeemed deposits and recycled material revenues to not fullyfund the program.

Escheats – Legislation, typically in US jurisdictions, allow state governments to use unredeemeddeposits for other purposes. Escheating in California has recently contributed to funding instabilityof the State beverage container recycling program. Some Canadian programs that employ a half-back refund return rate are considered to escheat as does Saskatchewan where the provincialgovernment retains all deposits and grants their program operating funds.

End use – With the exception of California, all North American jurisdictions prohibit the burning ofrecycled beverage containers by legislation or by practice (with minimal exceptions in mostjurisdictions, primarily some paper products). Most European jurisdictions do allow burning forenergy recovery, as they consider this a re-use of the material.

3.1.1. Legislated Program Scope, Deposit-Refund Rates & Recovery Rates

Program scope and recovery are defined in all jurisdictions either by legislation or by regulation.Legislation in jurisdictions such as BC, New Brunswick and California specifically describe whichcontainers are included and excluded in program scope whereas other jurisdictions such as Alberta andSaskatchewan describe program scope in regulations and/or policies.

Deposit-refund rates are legislated in some jurisdictions such as Alberta, BC, New Brunswick, Californiaand Denmark. Jurisdictions such as Norway and Saskatchewan do not legislatively mandate deposit-refund rates but assign them in regulations and policy.

Four jurisdictions reviewed mandate recovery rate targets in legislation. BC requires 75% recovery,California mandated an 80% recovery and Denmark a 98%. Distributors in South Australia are required tosubmit stewardship plans to achieve a 75% return rate within two years of the commencement of theplan, and a recovery rate of 80% within five years. Each jurisdiction has relatively unique agreementsbetween the governing entity and brandowners that were not provided for purposes of this study by therespective jurisdictions.

3.2. GOVERNING STRUCTURE

Stewardship programs across North America and Europe are structured differently in order to efficientlyoperate within its jurisdiction’s unique economic and demographic environment. However, all jurisdictionsshare high level similarities in its governance structure; each program is overseen by the government, anarm’s length organization, or the beverage industry itself.

Extended Producer Responsibility Organization: Legislation is in place to impose recycling obligationson the beverage industry (brandowners). Under this model, government has no direct involvement in howindustry undertakes and performs recycling responsibilities. In these cases, industry may collaborate andstructure itself or outsource its responsibilities to a third party to ensure recycling requirements arecollectively fulfilled. Decision making is taken in the best of interest of the participant companies, who allhave strong motivation to meet their legislated duties.

Governmental Administrative Agency: Programs that are publicly administered and managed underthe Government’s Environmental Ministry or equivalent department follow this governance structure.Participation of industry stakeholders is limited to input and collaboration between relevant agents, butneither they nor the public, have direct influence or decision-making power within the program.

Delegated Administrative Organization (DAO): Stewardship programs may operate by an arm’s lengthorganization that is delegated government authority to impose requirements on recycling programstakeholders. DAO’s are unique as a range of stakeholders are encouraged to participate, such asindustry, government, and the public. These parties are primarily involved in program stewardshipthrough appointments to the Board of Directors.

24

Benchmarking Evaluation of Alberta’s Stewardship Program forRecycling Empty Beverage Containers

Exhibit 3-2 summarizes the governance structure for each jurisdiction reviewed.

Exhibit 3-2Governance Structure by Jurisdiction