beyond the fed: incorporating government financial

TRANSCRIPT

BeyondtheFed:IncorporatingGovernmentFinancialInstitutionsandPoliciesintoMacroModels

DeborahLucasMITGolubCenterforFinanceandPolicy

1

Prepared for MFM Summer CampCape Cod

June 12, 2016

1. Needforanewpolicyparadigm

2. Importanceofgovernmentfinancialinstitutions

3. Application:thefiscaleffectsofcreditpolicies

4. Application:governmentasasourceofsystemicrisk

5. Relatedresearchtopics

Overview

2

PolicyanalysisintraditionalmacromodelsFiscalpolicy

• Taxesandaggregategovernment spending• Deficitsprovidestimulus

Monetarypolicy• e.g.,Taylorruletradesoff inflationandoutput

Regulationofprivatefinancialinstitutions(sometimes)

Twopolarviewsofgovernmentpolicy• Benevolent:Actsoptimally tomaximizeawell-specifiedobjectivefunction• Incompetent:Fiscalpolicydestroysvaluethroughdistortionary taxesandwastefulspending (thatdoesnotappearintheutilityfunction)

Theneedforanewpolicyparadigm

3

Whatismissing?Abehavioral approachtopolicy

• Observedgov’tactionsareatoddswitheitherbenevolentor incompetentframeworks

• Theinsightsofbehavioralfinanceapplytopolicymakerstoo:– rulesofthumbandlong-standingpolicies– inconsistent andtime-varyingobjectives– Hencethepotentialforeducationtoimprovepoliciesandoutcomes

Recognitionofthemanywaysthatgovernmentpoliciesaffectmarketsandtheeconomybeyondconventionalmonetaryandfiscalpolicy

• Government-run financialinstitutions• Governmentcontrolofmajorinvestmentdecisions• Regulatorypolicy

Theneedforanewpolicyparadigm

4

Monetary policy Investment and consumption

Regulation

SEC

Federal Reserve

FASB

FDIC

IRS

CFTC

OTC

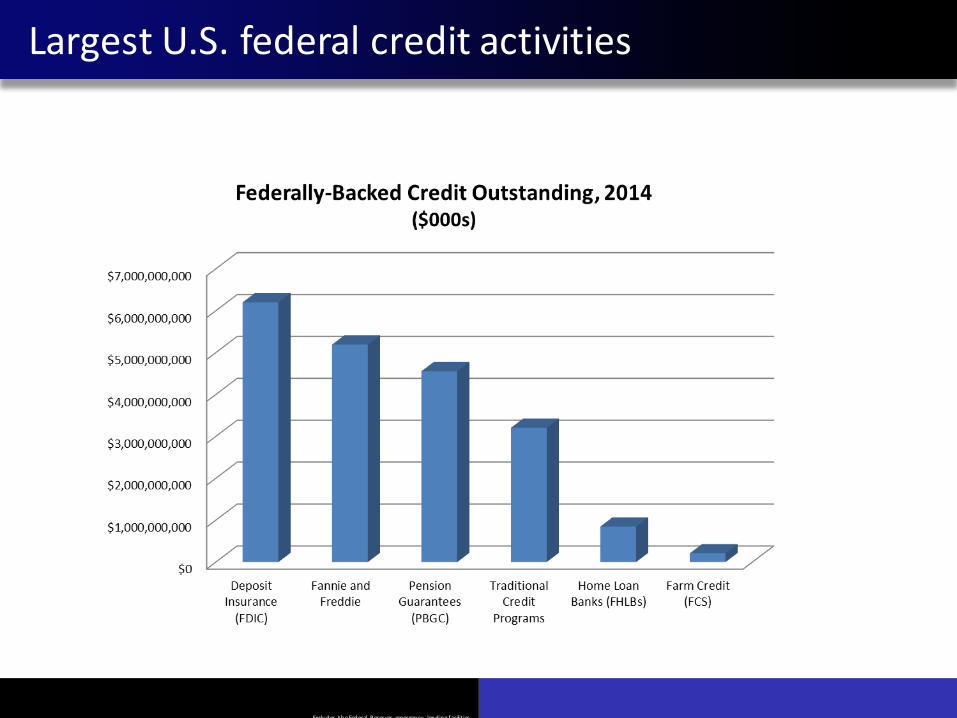

Academics often focus on the government as just a regulator of private financial institutions

But in fact, the U.S. government is the world’s largest financial institution in its own right…

LargestU.S.federalcreditactivities

Excludes theFederal Reserves emergency lendingfacilities

LargestU.S.financialinstitutions

OutstandingGovernment-GuaranteedBondsandDebtofGovernment-RelatedEnterprises,OECDCountries

(percentofGDP)

9Source: IMF 2012 Fiscal Monitor

(Excludes contingent guarantees and national credit programs)

• Astheworld’slargestfinancialinstitutions,governments haveafirst-ordereffectonthedistributionofriskandallocationofcapitalintheworldeconomythroughtheirrealandfinancialinvestments

• Thesamefundamentalissuesariseasforprivatefinancialinstitutions…

Whatarethesystemic/macroeconomiceffectsofgov’tfinancialactivities?

Howshouldagov’tassessitscostofcapital?

Howshould itsfinancialactivitiesbeaccountedfor?

Aretheinstitutionswell-managed?

Governmentsasfinancialinstitutions

• Thesamefundamentalissuesariseasforprivatefinancialinstitutions…

Areitsfinancialproductswell-designed(e.g.,conformingmortgages,studentloans,reversemortgages)?

• Consumerprotectionandbehavioralfinance• Systemicrisk• Pricing

Governmentsasafinancialinstitutions

TheamountofrecentstimulustotheU.S.economyhasbeenseriouslyunderestimatedbecausethefiscaleffectsoffederalcreditpolicieshavebeenoverlooked

ExceptionisWilliamGale(1991)DiscussionherebasedonLucas(2016),“CreditPolicyasFiscalPolicy,”BrookingsPapersonEconomicActivity

In2010,U.S.citizensborrowed$1.6trillion throughfederalcreditprograms

Thespendingresultingfromthatincrementalborrowingprovidedroughly$344billionofstimulus in2010

SimilaramounttotheAmericanRecoveryandReinvestmentActAfractionofthe$1.6trillionReportedbudgetarycostclosetozero

Application:Fiscaleffectsofcreditpolicies

TheoryHowcreditsupportincreasesborrowingvolume

• Creditsubsidies induce incrementalvolumealongintensiveandextensivemargins

Fromincrementalloanvolumetoaggregateoutput

CalibrationSubsidycostsElasticitiesFiscalmultipliersBorrowingincreasesonextensive&intensivemarginsResultsandsensitivityanalysis

Discussion

Application:Fiscaleffectsofcreditpolicies

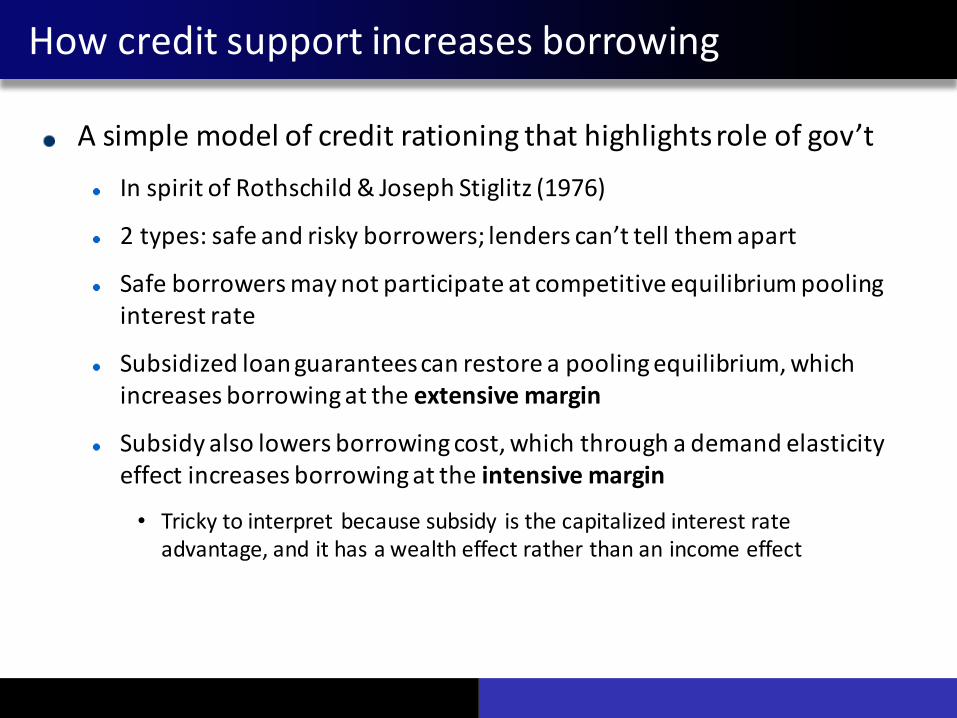

Asimplemodelofcreditrationingthathighlightsroleofgov’tInspiritofRothschild&JosephStiglitz(1976)

2types:safeandriskyborrowers;lenderscan’ttellthemapart

Safeborrowersmaynotparticipateatcompetitiveequilibriumpoolinginterestrate

Subsidizedloanguaranteescanrestoreapoolingequilibrium,whichincreasesborrowingattheextensivemargin

Subsidyalsolowersborrowingcost,whichthroughademandelasticityeffectincreasesborrowingattheintensivemargin

• Trickytointerpretbecausesubsidy isthecapitalizedinterestrateadvantage,andithasawealtheffectratherthananincomeeffect

Howcreditsupportincreasesborrowing

Herewegetamodestintensivemargineffect;largerextensivemargineffectsModelalsosuggestsimportanceofimposingquantitylimitstopreventexcessiveloanstoriskyborrowers

Howcreditsupportincreasesborrowing

ΔB = dA + S(dB/dS) – C • ΔB =incrementalaggregateborrowing• dA =incrementalborrowingonextensivemargin• S(dB/dS) =incrementalborrowingonintensivemargin• C =crowdingoutofotherprivatelending

AfiscalmultiplierapproachisusedtotranslateΔB into ΔY• ΔY isthechangeinaggregateoutput• Δbi istotalincrementalloanvolumeinprogrami• μi isthecorrespondingoutputmultiplier

Fromborrowingtoaggregateoutputeffects

∑ −Δ=Δ i Cii CbY µµ

Separateestimatesforeachmajorcreditprogram+FannieandFreddieasinputintoextensivemargincalculations

Subsidiesestimatedona“fairvalue”basisWhatthegov’twouldhavetopayaprivatelenderupfronttomaketheloanonthesametermsasunderthegov’tprogramEstimatesbasedonlargebodyofCBOstudiesandacademicpapers(&roughlyadjustinggov’testimatesforotherprograms).

• Totalsubsidyusedhereis$71billionin2010• “Subsidy rate”ispresentvaluesubsidyperdollarofloanprincipal

Contrasttoofficialbudgetarycosts• UnderstatessubsidiesbecauseusesTreasuryratesasthecostofcapitalandneglectsofessentialadmincosts

• Totalis-21billion in2010fortraditionalprograms

Subsidycosts

Subsidycosts

Supplyelasticityin2010isassumedtobelarge,hencenocrowdingoutofotherprivatelendingbygov’t

Highlevelofbankreservesandloosemonetarypolicy

CreditdemandelasticitiesAnswerquestionofincrementalamountborrowedasfunctionofdollarsubsidy

TakenfromGale(1991);literatureisinconclusive

• Housing 1.8

• Student loans.65

• Businessandother.8

Elasticities

LiteratureCBO’sdefinition:changeineconomicoutputperdollarofbudgetarycostAuerbachandGorodnichenko (2012)emphasizevariationoverthebusinesscycle

MostbudgetarycostsarecashspentinthatyearForcredit,incrementalborrowingisadditionalcashavailabletohouseholdsorbusinessesHencemultipliersfromliteratureappliedtoincrementalborrowingratherthantosubsidycostHowever,“bang-for-the-buck”isthemultipleofoutputoversubsidycost

Fiscalmultipliers

DifferentprogramsassumedtohavedifferentmultipliersStudentandbusinessloanslike“transferpaymentstoindividuals”MortgageshavemuchsmallermultiplierbecauseofrefinancingsandpurchaseofexistingstructuresIassumehighermultipliersinscenariowithfinancialdistress

CBOsuggestsverywiderangeforARRAmultipliers

Fiscalmultipliers

Table 1. Ranges for U.S. Fiscal Multipliers

Estimated Multipliers

Type of Activity Low Estimate High Estimate

Purchases of Goods and Services by the Federal Government 0.5 2.5 Transfer Payments to State and Local Governments for Infrastructure 0.4 2.2

Transfer Payments to State and Local Governments for Other Purposes 0.4 1.8 Transfer Payments to Individuals 0.4 2.1 One-Time Payments to Retirees 0.2 1.0 Two-Year Tax Cuts for Lower- and Middle-Income People 0.3 1.5 One-Year Tax Cut for Higher-Income People 0.1 0.6 Extension of First-Time Homebuyer Credit 0.2 0.8

Incrementalborrowingonintensivemargin

S(dB/dS)

Bynecessitylargelyjudgmental,butinformedbyobservationsofmarketsandprograms

Astheoryshowed,nosimplerelationtosubsidies

Twoscenariosconsidered:normaltimesandfinancialmarketdistress

2010takentobeinthemiddle

Incrementalborrowingonextensivemargin

Category Agency

2010loanvolume($billions)

Constrainedshare

Incrementalloanvolumeextensivemargin

Incrementalloanvolumeintensivemargin Multiplier

IncrementalOutput

Housing FHA 319 0.10 31.9 14.3 0.3 13.9Housing VAandRHS 80 0.10 8.0 5.0 0.3 3.9StudentLoans ED 105 0.75 78.8 9.6 0.5 44.2Business SBA 17 0.75 12.5 0.8 0.5 6.6OtherTraditional Various 64 0.50 31.9 3.1 0.5 17.5

Subtotal 584 163 33 86Housing Fannie&Freddie 1,011 0.00 0.0 74.6 0.2 15

Total 1,595 163 107 101

Table4PanelA:IncrementalOutputinaNormalPeriod

Puttingitalltogether:aggregatestimulus

∑ −Δ=Δ i Cii CbY µµ

Category Agency

2010loanvolume($billions)

Constrainedshare

Incrementalloanvolumeextensivemargin

Incrementalloanvolumeintensivemargin Multiplier

IncrementalOutput

Housing FHA 319 0.90 286.8 14.3 0.4 120.5Housing VAandRHS 80 0.50 40.0 5.0 0.4 18.0StudentLoans ED 105 0.95 99.8 9.6 2.0 218.6Business SBA 17 0.85 14.1 0.8 2.0 29.9OtherTraditional Various 64 0.75 47.8 3.1 2.0 101.7

Subtotal 584 488 33 488.6Housing Fannie&Freddie 1,011 0.25 252.8 74.6 0.3 98

Total 1,595 741 107 587

Table4PanelB:IncrementalOutputinaDistressedPeriod

Puttingitalltogether:aggregatestimulus

∑ −Δ=Δ i Cii CbY µµ

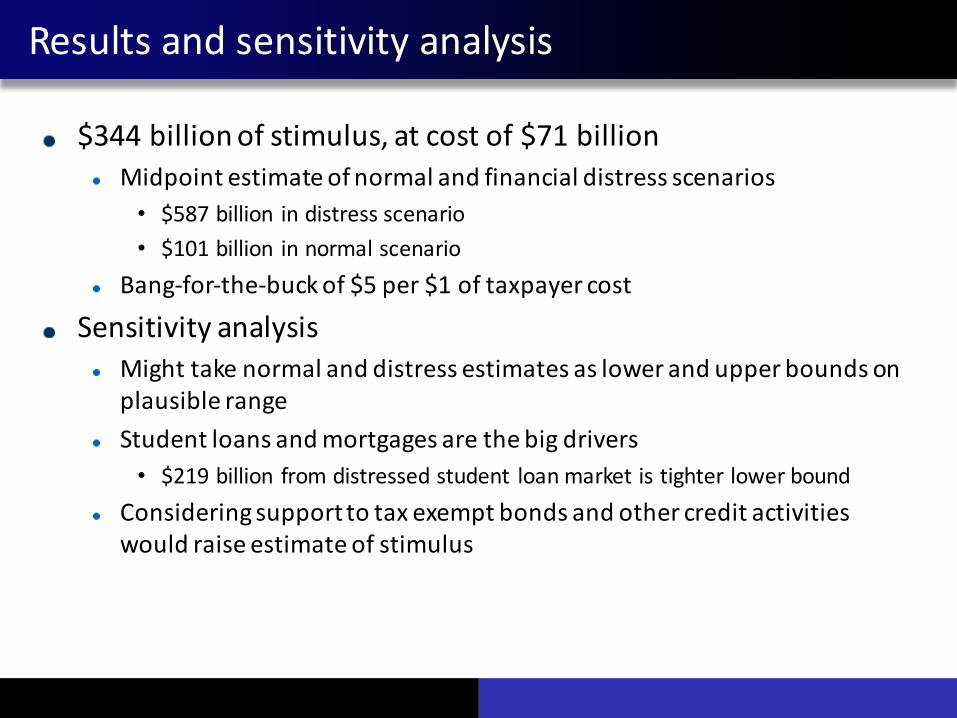

$344billionofstimulus,atcostof$71billionMidpointestimateofnormalandfinancialdistressscenarios

• $587billion indistressscenario• $101billion innormalscenario

Bang-for-the-buckof$5per$1oftaxpayercost

SensitivityanalysisMighttakenormalanddistressestimatesaslowerandupperboundsonplausiblerangeStudentloansandmortgagesarethebigdrivers

• $219billion fromdistressedstudent loanmarketistighterlowerboundConsideringsupporttotaxexemptbondsandothercreditactivitieswouldraiseestimateofstimulus

Resultsandsensitivityanalysis

Howdoresultschangeinterpretationofdepthofrecessionandeffectsofotherpolicies?

Notmuchondepth:AddedstimuluswithinuncertaintyboundsofstimuluseffectsofotherpoliciesCreditpolicymayhavebeenmoreimportantthanmonetarypolicyinrevivingthemortgageandhousingmarkets

Isthisfiscalpolicyormonetarypolicyorsomethingelse?Caseforfiscalpolicyisthatrootcauseofincrementalborrowingisgov’tsubsidiesalthoughchanneldifferentthanmostspendingContrasttospecialmonetarypoliciesthatprovidedliquiditybutminimalsubsidies

Discussion

Howmuchdotheseeffectsplayoutinothercountries?E.g.,Europereliesmuchlessoncreditprograms

Thisisnotawelfareanalysis!Creditpolicieslikelytohaveabigbang-for-the-buckasfiscalstimulusduringrecessionsaccompaniedbyfinancialupheavalsButbenefitshavetobecomparedwiththe(verylarge)costs:

• Target-inefficient• Opaque• Distortcapitalallocationandcrowdoutprivatecapital• Encourageexcessiveindebtedness• Incentivesforexcessiverisk-takingwithsystemicconsequences• Gov’tcreditpoliciesmayhavehelpedcausethe2007financialcrisis

Discussion

Governmentasasourceofsystemicrisk

Asimpleidea:Afterthefinancialcrisis,lawspassedtoaddressconcernthatpolicymakersandinvestorslackedsufficientdatatoanticipateemergingthreatstofinancialstabilityorassesshowshockstoonefinancialfirmcouldimpactthesystemasawhole

• (e.g.,aspartoftheDodd-FrankAct,CongresscreatedFSOC/OFR

Mostdiscussionsoftheneedformoreinformationaboutsystemicriskfocusonprivatesectorinstitutions.

Yetgovernmentsfunctionastheworld’slargestandmostinterconnectedfinancialinstitutions,andrepresentamajorsourceofsystemicrisk.

Hencemoreresearchisneededongovernmentsasasourceofrisk• anditarguablyfallsunder themandateofinstitutions liketheFSOCandOFRtodevoteresourcestomonitoring andstudying it

29

Governmentasasourceofsystemicrisk

OverviewMakethecasethatgovernmentisasourceofsystemicrisk.Identifyanddiscussthemajorreasonswhy:

• Sizeandinfluenceasafinancialinstitution• Incentivescreatedbyitsrulesandregulations• Lackoftransparency• Otherobjectivesmayconflictwithgoalofpromotingfinancialstability

PresentexamplesSuggestspecificareaswhereinstitutionsliketheU.S.OfficeofFinancialResearch(OFR)couldhelptomitigatethoserisks.

Discussiontodaydrawsonongoingworkandtwopapers:• “GovernmentasaSourceofSystemicRisk”JournalofFinancialPolicy• “EvaluatingtheCostofGovernmentCreditSupport:TheOECDContext,”EconomicPolicy

30

Governmentasasourceofsystemicrisk

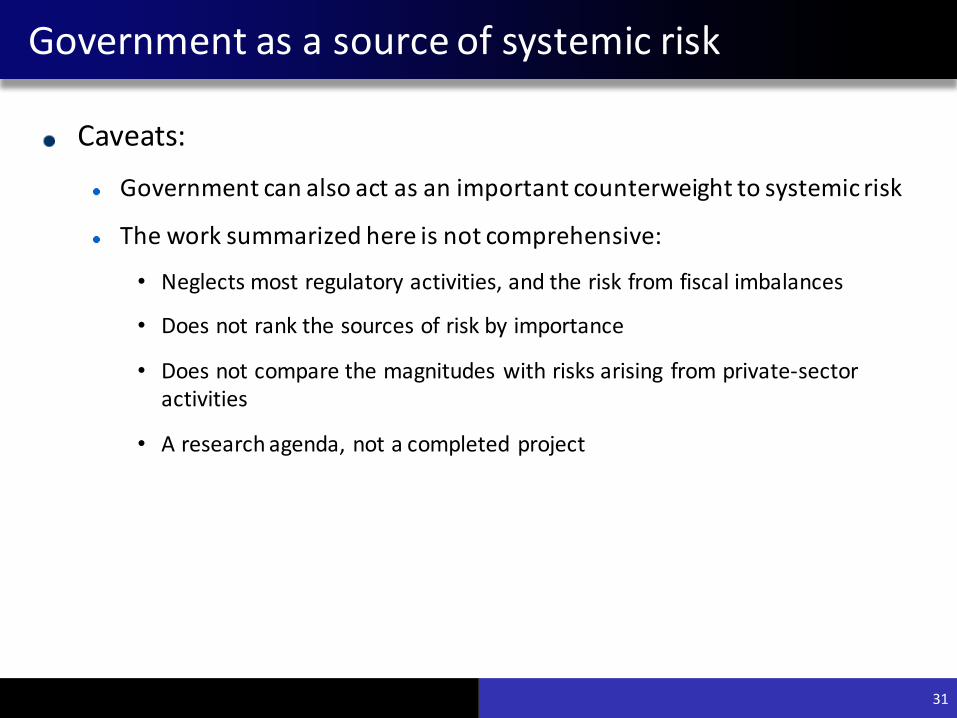

Caveats:Governmentcanalsoactasanimportantcounterweighttosystemicrisk

Theworksummarizedhereisnotcomprehensive:

• Neglectsmostregulatoryactivities,andtheriskfromfiscalimbalances

• Doesnotrankthesourcesofriskbyimportance

• Doesnotcomparethemagnitudeswithrisksarising fromprivate-sectoractivities

• Aresearchagenda,notacompletedproject

31

Governmentasasourceofsystemicrisk

32

Attributesthatgiverisetosystemicriskaresimilarforprivate-sectorandgovernmentfinancialinstitutions

Size(absoluteandrelativetoimportantsectors)

Interconnectednessthroughthefinancialinfrastructure

Lackoftransparency

Inadequatesupervision

Governmentasasourceofsystemicrisk

33

Buttheresultingrisksandtheircausesaredifferentthanforprivate-sectorinstitutionsforanumberofreasons:

Thegovernmentmakestherules(andexemptsitselffrommanyofthem,itcannottieitsownhands)ThegovernmentrespondstopoliticalratherthanfinancialincentivesThegovernmentisslowinitsabilitytoreactandmakechangesThegovernmentdoesn’tengageinhighfrequencytradingThegovernmentisgenerallynotasourceofcounterpartyrisk

Size

34

Alreadyestablishedthatitisenormous.Butthatonlymattersifitaffectsprices,allocations,orincentives.Itdoes(e.g.,previousanalysisoffiscalpolicyeffectsandreferencestherein)

Interconnectionsviathefinancialinfrastructure

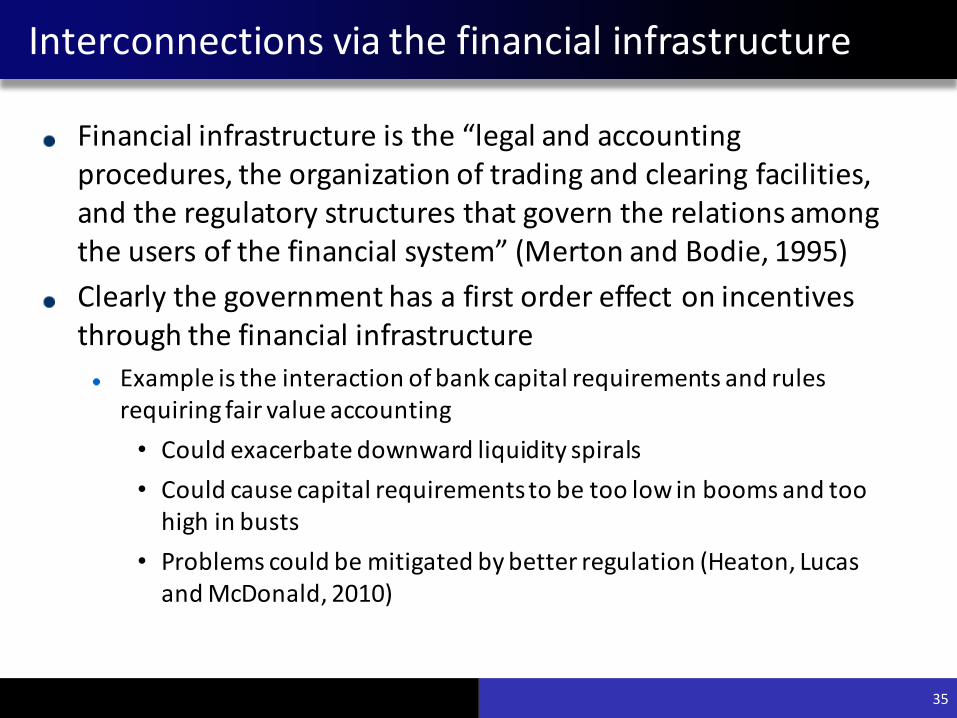

35

Financialinfrastructureisthe“legalandaccountingprocedures,theorganizationoftradingandclearingfacilities,andtheregulatorystructuresthatgoverntherelationsamongtheusersofthefinancialsystem”(MertonandBodie,1995)Clearlythegovernmenthasafirstordereffectonincentivesthroughthefinancialinfrastructure

Exampleistheinteractionofbankcapitalrequirementsandrulesrequiringfairvalueaccounting

• Couldexacerbatedownwardliquidityspirals• Couldcausecapitalrequirementstobetoolowinboomsandtoohighinbusts

• Problemscouldbemitigatedbybetterregulation(Heaton,LucasandMcDonald,2010)

Transparency

36

GovernmentfinancialinstitutionslacktransparencyTherearemanyshortcomingsrelatedtofinancialdisclosure:

Thequalityandscopeoffinancialdisclosuresvarymarkedlyacrossgovernmentagencies.Accountingstandardsdifferacrossgovernmententities,andbetweenthepublicandprivatesectors.ThereisnocentraldatarepositoryliketheSEC’sEdgarforprivatefirmsMarketpriceorfairvalueinformationisgenerallynotavailableGovernmentaccounting

• Cashbasisaccountingusedforbudgeting(exceptforlimitednaïveaccrualinU.S.)

• Governmentwronglytreatsitscostofcapitalasitsownborrowingcost• Createsincentivesforrisk-takingbygovernmentfinancialinstitutions

Robustprinciplesfromfinancetheorypointtoimportanceoffairvaluecostrecognitionforgov’ts

Thecostofcapitalisrelated totheundiversifiablemarketrisk(β)oftheprojectfinancedThecostofcapitalisnotrelated totheproportionofdebtandequityusedtofinancetheproject

Thisisafirstapproximation—taxes,etc.alsoaffectcost

Keyrelations:

𝐸(𝑟$) = 𝑟' + 𝛽$(𝑟' − 𝐸(𝑟+))

= ,-𝐸(𝑟,) +

.-𝐸(𝑟.)

37

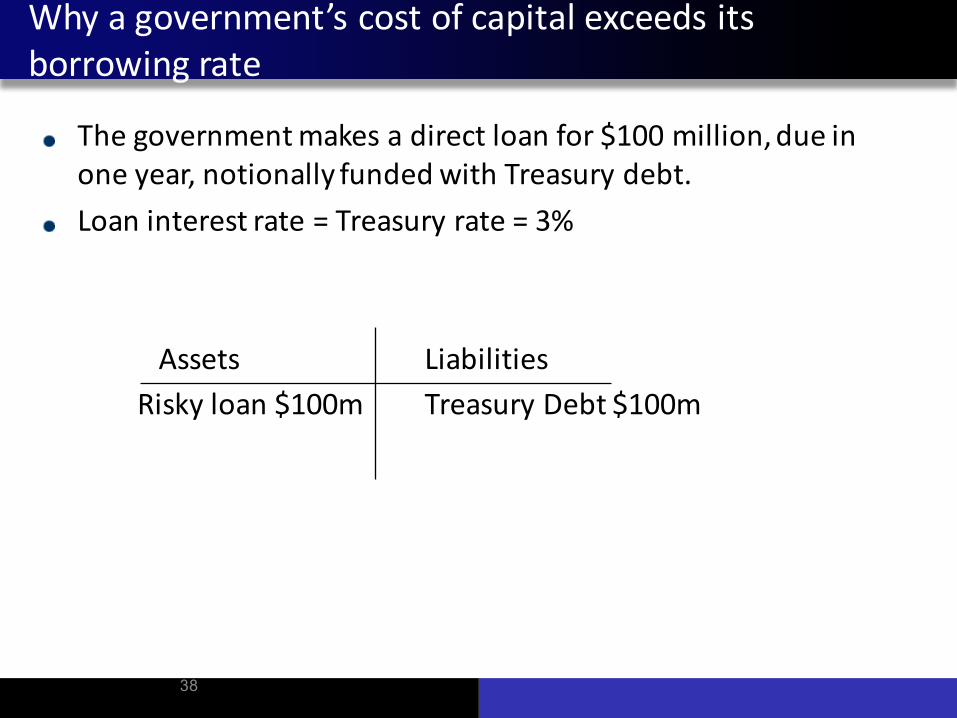

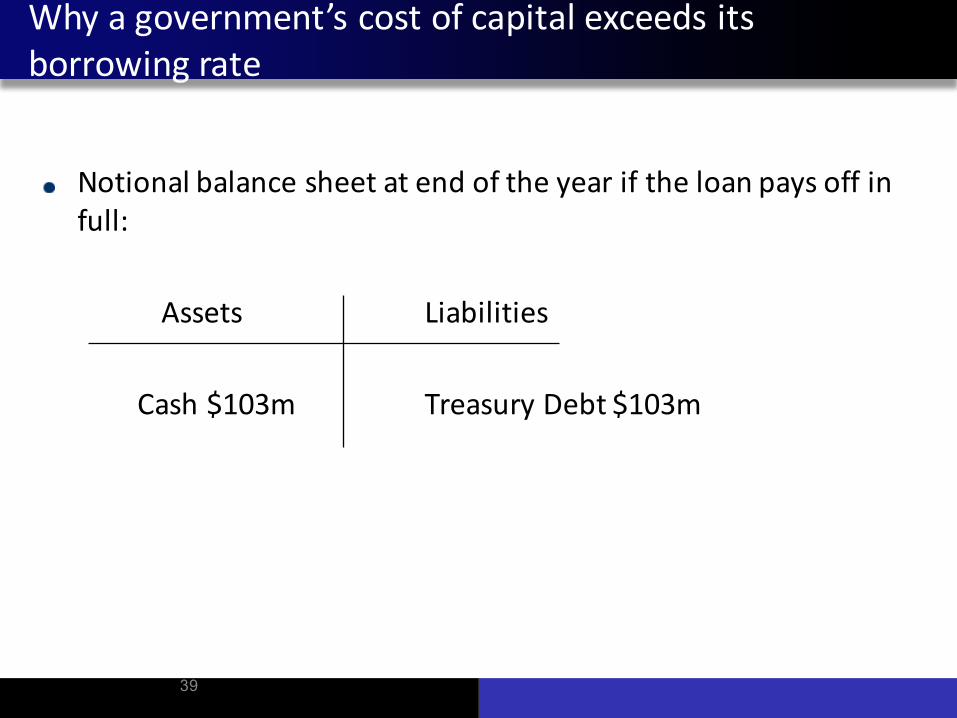

Thegovernmentmakesadirectloanfor$100million,dueinoneyear,notionallyfundedwithTreasurydebt.Loaninterestrate=Treasuryrate=3%

Assets LiabilitiesRiskyloan$100m TreasuryDebt$100m

Whya government’scostofcapitalexceedsitsborrowingrate

38

Notionalbalancesheetatendoftheyeariftheloanpaysoffinfull:

Assets Liabilities

Cash$103m TreasuryDebt$103m

Whya government’scostofcapitalexceedsitsborrowingrate

39

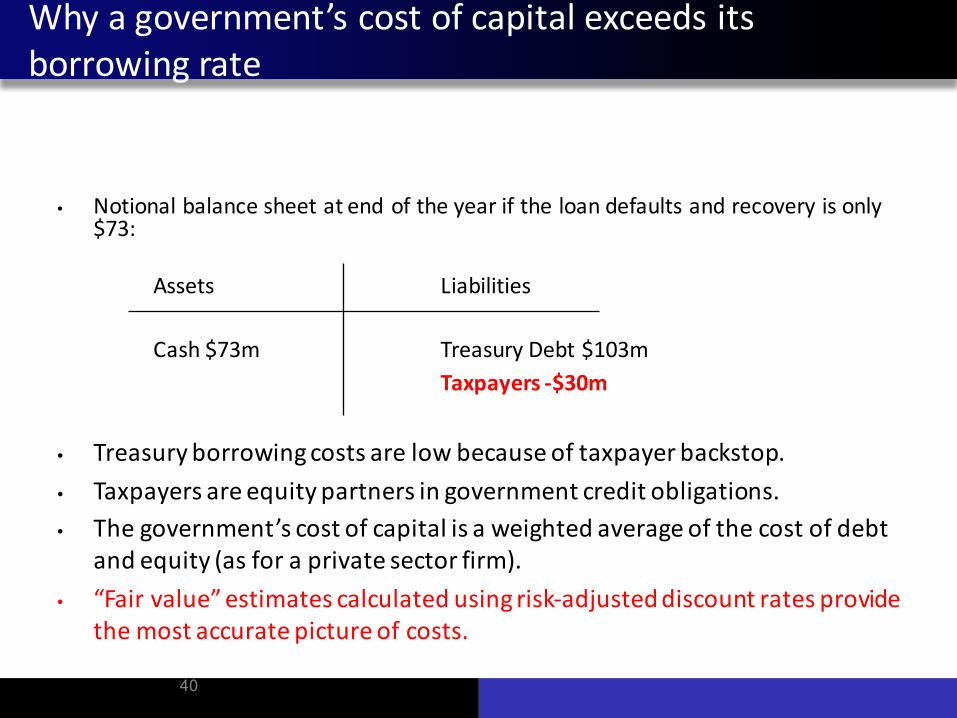

• Notionalbalancesheetatendoftheyeariftheloandefaultsandrecoveryisonly$73:

Assets Liabilities

Cash$73m TreasuryDebt$103mTaxpayers-$30m

• Treasuryborrowingcostsarelowbecauseoftaxpayerbackstop.• Taxpayersareequitypartnersingovernmentcreditobligations.• Thegovernment’scostofcapitalisaweightedaverageofthecostofdebt

andequity(asforaprivatesectorfirm).• “Fairvalue”estimatescalculatedusingrisk-adjusteddiscountratesprovide

themostaccuratepictureofcosts.

Whya government’scostofcapitalexceedsitsborrowingrate

40

Inadequatesupervision

41

Althoughgovernmentinstitutionsaretaskedwithachievingpublicpurposes,theymaystillneedspecialoversighttocontrolsystemicrisk.

Asforprivatefirms,governmentinstitutionshaveobjectivesthatarenarrowlymission-focusedandnotdirectedatfinancialstability.

Thereasonsforcreatinganewsystemicriskregulatortooverseealready-regulatedprivatefinancialinstitutionsalsoapplytogovernmentinstitutions.

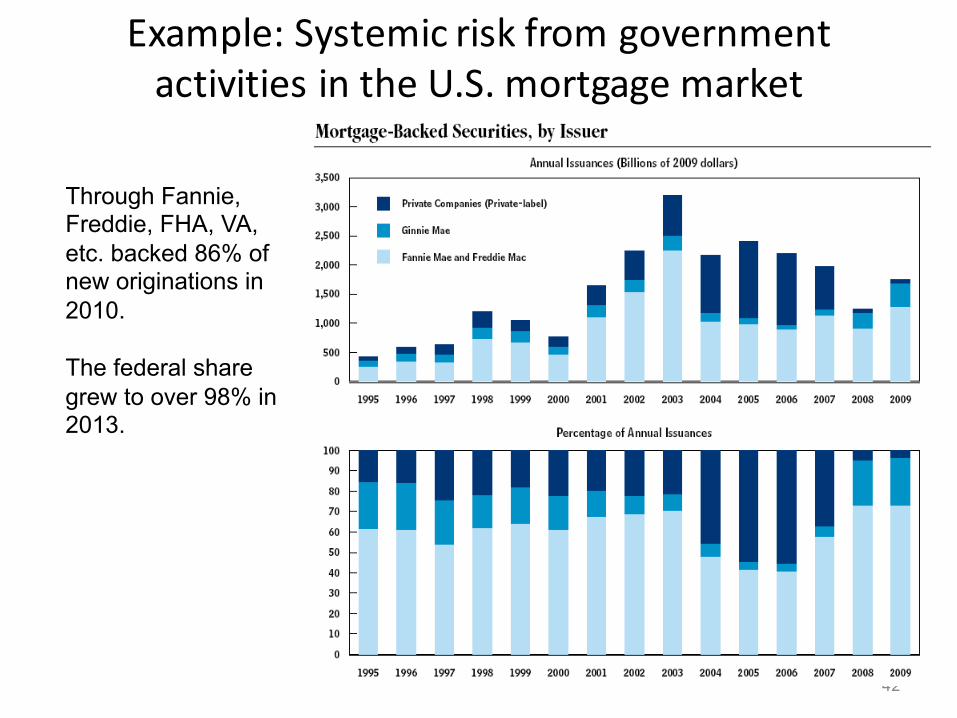

Example:SystemicriskfromgovernmentactivitiesintheU.S.mortgagemarket

42

Through Fannie, Freddie, FHA, VA, etc. backed 86% of new originations in 2010.

The federal share grew to over 98% in 2013.

Systemicriskfromgov’tmortgagepolicies

43

Clearlythegovernmentisinapositiontoinfluenceallocationofmortgagecreditanditsriskiness.

Setsrulesforeligibility, underwriting, guaranteepricing,productsoffered (e.g.,toxic30-yearmortgages)Incentivesforrisk-takingcreatedbyunderpricedguarantees

Butthereisdisagreementabouthowmuchthegovernmentcontributedtothehousingbubbleandsubsequentcrisis.

Alsoaboutwhether itissupplying toomuchortoolittlemortgagecreditnow.

Whatisclearisthatthoseactivitiesturnedouttobecostlytotaxpayers.(Net)paymentsfromTreasurytoFannieandFreddieof$130billion throughMarch2011UpwardreestimatesofbudgetarycostofFHAguaranteesof$40billionbetween1999to2011

Example2:

CallableCapitalfortheEFSF/ESM

TheEFSFwascreatedinMay2010torespondtoEurozonecrisisA rescuemechanismwiththemandateofsafeguardingfinancialstabilitybyprovidingfinancialassistancetoeuroareaMemberStates

ESMisthepermanentversionAuthoritytoissuebondsbackedbymembercapitalandcallablecapital

BondsareratedAA+becauseoftheEUR620billioncallablecapitalGovernments recognizenocostofthecallexposureuntillossesarerealizedCallablecapitalcanbevaluedusingageneralizedoptions-pricingapproachwithjumps(followingLucas&McDonald,2010)

Costofcommittedcallablecapitaltomembersover20yearsforEFSF/ESMestimatedtobe EUR20to80billion

44

CostofCallableCapitalfortheEFSF/ESMMethodology(inbrief)

“Risk-neutral”MonteCarlovaluationmodel• Parallelmodelunderactualmeasuretocomputephysicalprobabilityoflossevents

RiskyassetsofESMevolvestochastically• Ajumpprocessindicatesoccurrenceofinfrequent crisisstate• Assetvolatilityprocesscanbetime- andstatevarying;trickytocalibrate

LiabilitiesincreasebytheamountofnewloansmadeinacrisisCapitaliscalledwhentheratioofliabilities-to-equityexceedsatriggerthreshold

• Theamountcalledissettorestoretargetliability-to-equityratio• Newcapitalisinvestedinsafeliquidassets

Costofcallablecapitalispresentvalueofmodel-predictedcallamounts,averagedover20,000MonteCarlorunsover20years

45

46

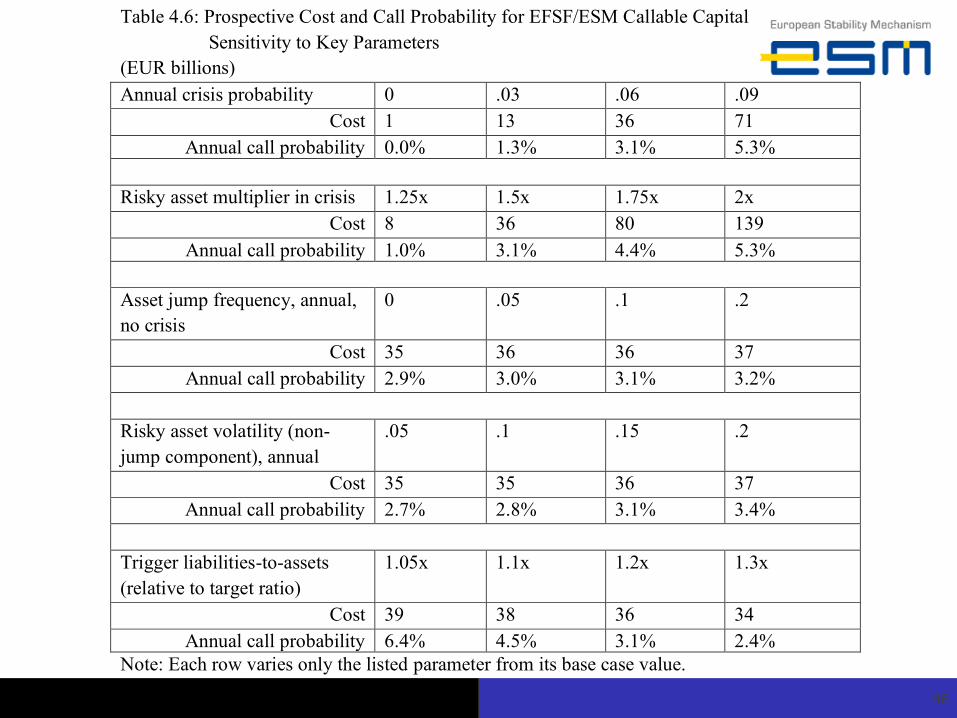

Table 4.6: Prospective Cost and Call Probability for EFSF/ESM Callable Capital Sensitivity to Key Parameters

(EUR billions) Annual crisis probability 0 .03 .06 .09

Cost 1 13 36 71 Annual call probability 0.0% 1.3% 3.1% 5.3%

Risky asset multiplier in crisis 1.25x 1.5x 1.75x 2x

Cost 8 36 80 139 Annual call probability 1.0% 3.1% 4.4% 5.3%

Asset jump frequency, annual, no crisis

0 .05 .1 .2

Cost 35 36 36 37 Annual call probability 2.9% 3.0% 3.1% 3.2%

Risky asset volatility (non-jump component), annual

.05 .1 .15 .2

Cost 35 35 36 37 Annual call probability 2.7% 2.8% 3.1% 3.4%

Trigger liabilities-to-assets (relative to target ratio)

1.05x 1.1x 1.2x 1.3x

Cost 39 38 36 34 Annual call probability 6.4% 4.5% 3.1% 2.4%

Note: Each row varies only the listed parameter from its base case value.

MitigatingtheRisks:DataInitiativesandAnalyses

47

Watchdoginstitutionsforsystemicrisk(liketheOFR)couldundertakeavarietyofinitiativesandanalysesthatcouldhelptomitigatetherisksthathavebeenidentified.Regulatoryaudit.

Undertakeacomprehensiveevaluationoffederalfinancialregulationstoidentifyunintendedsystemicconsequences.

Commenceastudythatcomparesgovernmentandprivatesectoraccountingstandardsandassessesbestpractices.

Studycouldserveasaninputandimpetustomorerapidharmonizationofaccountingstandardsandpractices.

MitigatingtheRisks:DataInitiativesandAnalyses

48

Undertakeinitiativestoimproveandstandardizefinancialdisclosures.

Workwithgovernmentfinancialinstitutions,andwithacademicandprivateaccountingexperts,todevelopmoreuniformandinformativereportingstandards.Houseawebsitethatwouldmakethosedisclosuresreadilyavailabletothepublic.

Encouragetheprovisionoffairvaluedisclosures.Tohelpaddressthelackofmarketpriceinformationthatwouldmakemoretransparentthecostandrisksofgovernmentfinancialactivities

MitigatingtheRisks:DataInitiativesandAnalyses

49

Evaluateunmetdataneeds forassessingsystemicriskfromcreditandinsuranceprograms.

Informationcollectedisprimarilytodetermineeligibility.Itmaybeinsufficienttoassesssystemicrisk.Exampleislackofcreditscoredataforstudentloansthatmakeitmoredifficulttoassesswhetherdebtlevelsaresustainable,andlackoftimelydefaultstatistics.

Createdatasetsthatcombineinformationonfederalandprivatecreditatthehouseholdlevel.

Forexample,gettingcombineddataonfirstandsecondmortgageswouldgreatlyimproveunderstandingofstressesonhouseholds.

MitigatingtheRisks:DataInitiativesandAnalyses

50

Disseminate dataongovernmentcreditprograms.Loanleveldatafromthoseprogramsisgenerallyunavailable.

• Exception isformortgagesinU.S.,butthatdataisveryexpensive• AlsoFOIA

WouldencouragemoreresearchongovernmentfinanceCouldhelpprivatefinancialinstitutionsbetterunderstandtheirownandaggregaterisksFewerconcernsaboutproprietaryvaluethanforprivatefinancialinstitutions;borrowerprivacycouldbeprotectedCostlyforagenciestoundertakesuchinitiativesontheirown.WatchdogentitylikeOFRcouldmakethedatamoreusefulthroughcoordinationandstandardization.

IncorporategovernmentfinancialinstitutionsintosystemicriskmodelsEstimatingthegovernment’scostofcapital

EssentialinputforvaluationofcomplexinvestmentpoliciesEssentialforcost-benefitanalysisoflong-datedpoliciessuchasthoseaimedatabatingclimatechangeManyunexploredapplicationsSee“Lucas,Deborah(2014),“EvaluatingtheCostofGovernmentCreditSupport:TheOECDContext,”EconomicPolicy,Vol.29,Issue79,pp.553-597.“andcitedpapersfordiscussionandexamples

Understandingthedebtcapacityofdevelopedcountries

Additionalandrelatedresearchtopics

51

Governmentfinancialpolicieshaveafirst-ordereffectsthatmacro-financialanalysestraditionallyhaveignoredA fertileareafornewresearch

ParticularlyaneedfornewmodelsexploringtheoreticalchannelsAlsoadearthofempiricalwork

BarrierstoentryHardtochangemindsetNeedtostudyinstitutionaldetailsandtakethemseriouslyRiskthattherearenotrefereesconversantinthisarea

ButhighpotentialreturnsUncrowdedresearchspaceFirstorderimportanceforunderstandingtheworldandofferingsensiblepolicyadvice—peoplewillcareaboutwhatyouhavetosay

Takeaways

52