beyond transactions: creating value through customer partnerships in high-tech

TRANSCRIPT

Beyond transactionsCreating value through customer partnerships in high-techAn Economist Intelligence Unit white paperSponsored by SAP

Beyond transactionsCreating value through customer partnerships in high-tech

© Economist Intelligence Unit Limited 20091

Preface

Beyond transactions: Creating value through customer partnerships in high-tech is an Economist Intelligence Unit report sponsored by SAP. The Economist Intelligence Unit bears sole responsibility for this report. The Economist Intelligence Unit’s editorial team conducted the interviews and wrote the report. The fi ndings and views expressed in this report do not necessarily refl ect the views of the sponsor. Dan Armstrong was the editor of the report and Dorian Benkoil as the author. Mike Kenny was responsible for layout and design. Our thanks are due to all of the executives who responded to the survey.

September 2009

© Economist Intelligence Unit Limited 2009

Beyond transactionsCreating value through customer partnerships in high-tech

2

Contents

Introduction 3

Key fi ndings 4

Conclusion 8

Appendix 1: Overall survey results 9

Appendix 2: Americas survey results 14

Appendix 3: Asia-Pacifi c survey results 19

Appendix 4: EMEA survey results 24

Beyond transactionsCreating value through customer partnerships in high-tech

© Economist Intelligence Unit Limited 20093

Introduction

Nearly half of all capital investment in modern economies is in technology. Such spending can help to enhance productivity and maintain a competitive edge. But investments require profi ts or new fi nancing, both of which are in short supply. And much of the spending in the sector comes in the form of upgrades and enhancements that can be postponed. Furthermore, when the economy slows, there is more scrutiny of spending—customers dither and sales come in more slowly.

In this challenging environment, technology companies are focusing more intensely on their customers. From lead generation to post-sales service, they are trying to collect information from every interaction, and share it with sales and product development teams. Ultimately, they want to close sales faster. But they also want to identify the fraction of customers that account for an outsize proportion of revenue and profi t, and provide the added value needed to retain customers and increase business.

About the survey

In July 2009, the Economist Intelligence Unit surveyed 89 high-tech company executives on the challenges of getting customer-facing departments to work together more consistently and effectively. One-half of respondents came from software fi rms, 10% from

original equipment manufacturers (OEMs), 8% from semiconductors and components, and the rest from other tech sectors. Fifty-six percent focused exclusively on business-to-business sales, and almost all of the rest sold to both business and consumers. Respondents spanned the globe, with 30% based in Asia-Pacifi c, 36% in the Americas and the rest in EMEA. Respondents came from strategy and business development, general management, IT, sales, marketing and fi nance.

© Economist Intelligence Unit Limited 2009

Beyond transactionsCreating value through customer partnerships in high-tech

4

Gaining better insight into customer needsIn an industry in which personal selling and relationships are key, survey respondents understand that customer interaction provides the best opportunities for gathering intelligence. Whereas 81% have established at least some procedures for incorporating customer feedback into the product development process, nearly half say they need to better integrate customer tracking throughout customer-facing departments: customer service, marketing and sales. In particular, they say that the single greatest improvement they could make would be to build on their ability to turn information about customers (or potential customers) into qualifi ed leads.

The lack of strong processesMost survey respondents from high-tech companies agree that their core strengths lie in their ability to provide customer service and innovative products. They are confi dent that they can compete on features and, when necessary, price. They say that their fi rms are good at responding quickly to customer complaints. However, most feel that their departments do poorly in working together to gather, analyse, share and use knowledge about customers. Processes that tend to occur within a single department—answering a customer service call or following up on a sales lead, for example—are well developed. But when judgments must be made and departments must work together, executives are far less confi dent in their processes.

Do products incorporate customer feedback in every respect, for example? Executives are split. Although marketers can segment customers, this information is often not acted upon, and information from sales or customer service is seldom used. Similarly, few executives express confi dence in their ability to evaluate the effectiveness of customer-related processes.

Bringing customer information into marketingHigh-tech companies are often dominated by engineers. Although smart sales, marketing and customer service teams are essential in packaging and presenting the company’s products, these departments are often marginalised. Developers, engineers and designers work with customer feedback every day, but the views of customers are less likely to be incorporated into the activities of sales, marketing and customer service.

Key fi ndings

Beyond transactionsCreating value through customer partnerships in high-tech

© Economist Intelligence Unit Limited 20095

How well do customer-facing departments—sales, marketing, customer service—work together?

Source: Economist Intelligence Unit survey, July 2009.

Responding to customer demands or complaints

Generating, tracking and measuring leads

Gauging customer satisfaction

Developing and launching new products

Planning and executing campaigns

Incorporating customer feedback into products/services

Analysing and segmenting customers

Measuring effectiveness of processes

Ad hoc integration Broad and systematic integration

-20% -10% 0% 10% 20% 30%

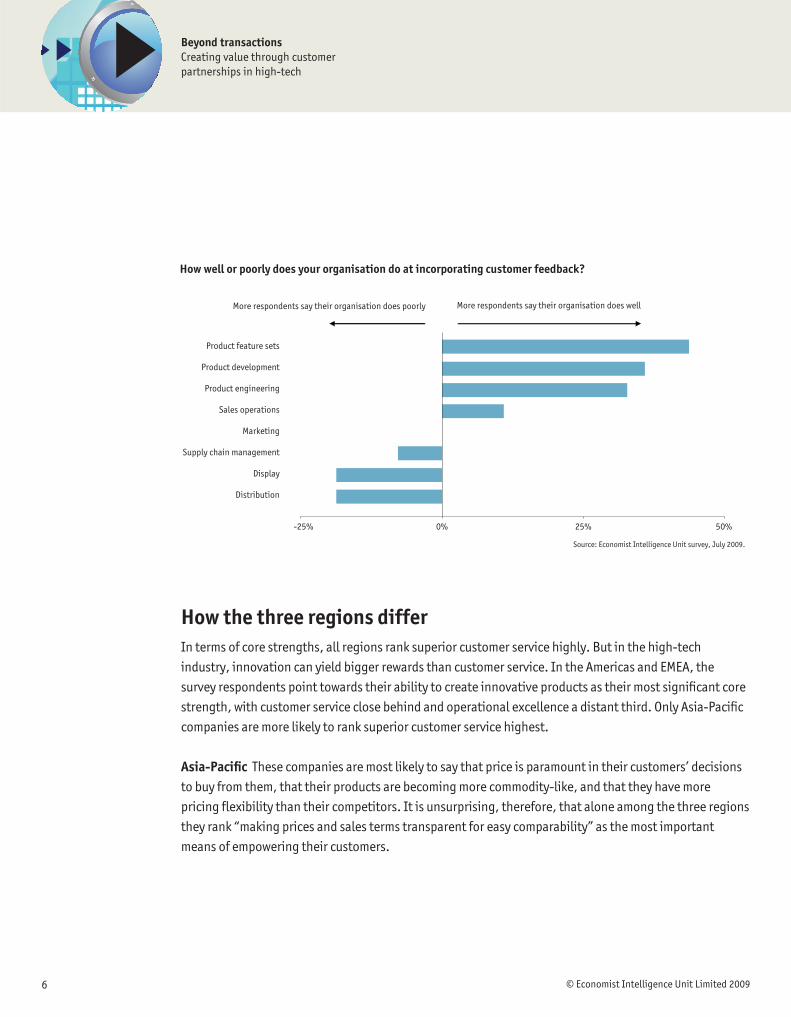

The executives who responded to the survey recognise this shortcoming. Most respondents say that their organisations do a good job incorporating customer feedback into tangible product features and other aspects of the product. But they are evenly split on the role of customer feedback in improving marketing, and report that distribution—the ability to get the right product to the right customer at the right time—does not benefi t from good customer intelligence. Nor does display, although this is relevant mainly to retail companies.

Online, they fall even shorter during interactions with their customers. Although half of respondents say their companies empower customers by improving functionality of customer-facing websites—more than any other mechanism—and by improving online or self-service product support tools (40%), only 14% say that useful feedback is gleaned from these efforts. Just 30% are developing social media strategies to pull intelligence from the highly participatory high-tech community. In short, while tech companies may talk a good game about web-based interaction with customers, many of these fi rms have a long way to go.

© Economist Intelligence Unit Limited 2009

Beyond transactionsCreating value through customer partnerships in high-tech

6

How the three regions differIn terms of core strengths, all regions rank superior customer service highly. But in the high-tech industry, innovation can yield bigger rewards than customer service. In the Americas and EMEA, the survey respondents point towards their ability to create innovative products as their most signifi cant core strength, with customer service close behind and operational excellence a distant third. Only Asia-Pacifi c companies are more likely to rank superior customer service highest.

Asia-Pacifi c These companies are most likely to say that price is paramount in their customers’ decisions to buy from them, that their products are becoming more commodity-like, and that they have more pricing fl exibility than their competitors. It is unsurprising, therefore, that alone among the three regions they rank “making prices and sales terms transparent for easy comparability” as the most important means of empowering their customers.

How well or poorly does your organisation do at incorporating customer feedback?

More respondents say their organisation does poorly

Product feature sets

Product development

Product engineering

Sales operations

Marketing

Supply chain management

Display

Distribution

More respondents say their organisation does well

Source: Economist Intelligence Unit survey, July 2009.

-25% 0% 25% 50%

Beyond transactionsCreating value through customer partnerships in high-tech

© Economist Intelligence Unit Limited 20097

EMEA These companies stand out in their desire to build long-term relationships in an industry marked by rapid change and fl eeting loyalty. Consistent with the equal focus on innovation and customer service (43% and 40%, respectively), they seek to improve their ability to collaborate with customers in developing new products and services (co-creation). Signifi cantly, they say that they are already good at co-developing products with customers—but they want to become even better.

Americas As in EMEA, high-tech companies in the Americas are almost equally likely to cite as core strengths innovation and customer services (41% and 38%, respectively). One difference is that fi rms in the Americas are most likely to focus on reducing the cost of sales by effi ciently targeting, acquiring and upselling customers, while EMEA fi rms tend to cite the importance of retaining customers (long-term relationships).

Asia-Pacific companies are more likely to see customer service as a core strenght;EMEA and Americas firms are more likely to comete on innovation

Product innovation: First to market with groundbreaking new products or services

Customer services: Providing superior service to cients

Operational excellence: Creating highly efficient processes

EMEA

Americas

Asia-Pacific

0% 10% 20% 30% 40% 50% 60%

Source: Economist Intelligence Unit survey, July 2009.

© Economist Intelligence Unit Limited 2009

Beyond transactionsCreating value through customer partnerships in high-tech

8

In a global economic downturn, high-tech executives need to glean the intelligence from customer interactions that will enable them to retain their most profi table customers. To make this happen, companies need to:

l Help customer-facing departments improve the fl ow of information from customers to the company.l Use the information not just to improve products, but also to aid in sales, marketing and customer

service efforts.l Offer current and potential customers the opportunity to interact through the web and social media,

while improving their ability to gather data through these channels.l Improve demand forecasting, especially for existing products, in order to decrease development and

distribution costs, and bolster profi t margins.l Focus on competing through value rather than price. Sixty-four percent of executives say price is not

the most important concern for their customers.l Use customer feedback to guide operational improvements, especially in weak areas such as

distribution. Most high-tech executives feel that their companies do not excel in operations—getting the right product to the right customer at the right time.

Most executives know of Pareto’s Law, which suggests that a small number of customers account for the bulk of the revenue and profi t. But high-tech companies also need to pay attention to one of Pareto’s lesser-known concepts: the limit of the effi cient frontier, where both seller and buyer extract the greatest benefi t from a given product or service, and any change would make one or the other worse off. By incorporating customer intelligence into every part of their operations, organisations can get close to this effi cient frontier, providing the maximum value to their customers—and gaining long-term, profi table relationships for themselves.

Conclusion

Appendix 1Overall survey results

Beyond transactionsCreating value through customer partnerships in high-tech

9 Economist Intelligence Unit 2009

Appendix: Overall survey results

44

37

19

0

Customer service: Providing superior service to clients

Product innovation: First to market with groundbreaking new products or services

Operational excellence: Creating highly efficient processes

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

0 20 40 60 80 100

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Generating, tracking and measuring leads

Developing and launching new products

Planning and executing campaigns

Analysing and segmenting customers

Gauging customer satisfaction

Measuring effectiveness of processes

Responding to customer demands or complaints

Incorporating customer feedback into products/services

Other

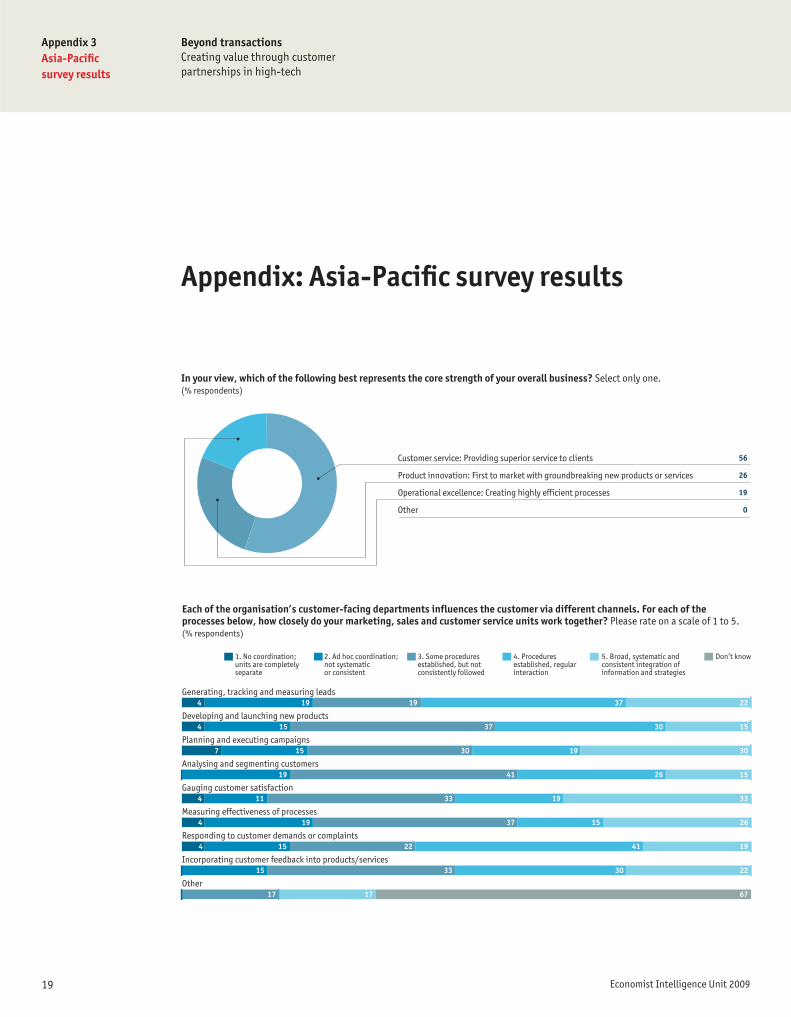

Each of the organisation’s customer-facing departments influences the customer via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

5 10 25 33 24 2

4 11 21 36 24 3

5 13 25 31 26 1

2 16 30 32 16 3

5 15 27 27 23 3

8 16 35 17 20 3

5 11 19 40 23 2

5 13 27 32 20 3

5 5 10 10 14 57

10 Economist Intelligence Unit 2009

Appendix 1Overall survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Generating qualified leads

Gathering customer intelligence in the course of providing service

Targeting the right customers in order to close a high percentage of prospects

Building long-term relationships

Efficiently acquiring customers (eg, reducing the cost of sales)

Cross-selling or upselling customers

Segmenting and profiling customers

Maximising the number of repeat sales

Providing a consistent customer experience

Measuring/optimising effectiveness of marketing and promotional campaigns

Involving customers product/service development (eg, co-creation)

Measuring customer satisfaction and loyalty

Creating effective collateral

Ensuring that customer complaints are resolved quickly

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

39

36

34

29

29

28

22

21

20

18

18

17

16

15

2

0

Integrating customer tracking from lead through post-sales service

Developing and sharing a detailed picture of customers, behaviour and preferences

Making each unit aware of how the others have interacted with a given customer

Prioritising resources directed towards customers by total value over life of customer

Presenting customers with a consistent picture of the organisation

Measuring the probability that leads will turn into sales, and using these scores to guide sales

Establishing common definitions, assumptions and data

Helping each function find and act on ways to support the others

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

45

37

34

33

28

26

25

19

4

1

0

0 20 40 60 80 100

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most customers consider

Compared to our competitors, my organisation’s customers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Customers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

Agree Disagree Don’t know

33 64 3

61 16 23

32 44 24

43 44 13

32 45 23

53 31 16

60 27 13

47 42 11

48 43 9

45 42 13

Appendix 1Overall survey results

Beyond transactionsCreating value through customer partnerships in high-tech

11 Economist Intelligence Unit 2009

Global economic downturn

Significant demand shifts for our products/services

Changing customer requirements

Emergence of new competitors

Disruptive technology developments

Emergence of new markets for our products and services

Finding access to credit/capital

Accessing key components or resources through our supply chain

Focusing on sustainability efforts

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

71

31

31

25

25

20

19

18

12

3

0

Improving usability, search and navigation of customer-facing websites

Making prices and sales terms more transparent for easy comparability

Improving online or self-service product support tools

Building or supporting online customer communities

Investing in self-service tools across multiple channels (eg, web, mobile devices, e-mail, point of sale)

Other

Don’t know

In which of the following ways does your organisation empower its customers? Select all that apply.(% respondents)

49

46

40

35

35

4

8

In-person customer service

Market research/customer surveys

Online customer service

Company-sponsored user forums

Feedback from value-added resellers (VARs)

Company website

Third-party forums and other social media

In-store feedback

Wholesale buyer feedback

Third-party online publications

Other

Don’t know

Through which channels does your organisation get the most useful customer feedback about its products? Select up to three. (% respondents)

62

36

27

24

24

13

10

10

10

6

1

3

Anticipate customer demand for new features and products

Anticipate customer demand for existing products

Achieve the right balance between price and features

Promote positive feelings about the brand

Quickly incorporate customer feedback into design updates

Sell add-ons, peripheral products or extra components

Anticipate customer demand for smoother supply chain operations

Other

Don’t know

Given current economic conditions, my organisation is specifically looking for feedback that helps it to: Select up to two. (% respondents)

52

37

28

24

21

16

8

0

3

12 Economist Intelligence Unit 2009

Appendix 1Overall survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Product engineering

Product development

Product feature sets

Supply chain management

Distribution

Display

Sales operations

Marketing

Other

Don’t know

How well does your organisation incorporate customer feedback into its products? We do best at incorporating customer feedback into:Choose up to three from each column. (% respondents)

We do best at incorporating customer feedback into:We have the most difficulty incorporating customer feedback into:

44 19

58 25

54 10

19 20

13 26

7 24

28 19

24 22

1 2

6 10

North America

Asia-Pacific

Western Europe

Latin America

Eastern Europe

Middle East and Africa

In which region are you personally based? (% respondents)

31

30

27

4

4

2

49

10

8

33

Software

OEM

Semiconductors and components

Other

Which of the following best describes your company’s business? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

5

23

5

9

3

9

3

11

26

6

Appendix 1Overall survey results

Beyond transactionsCreating value through customer partnerships in high-tech

13 Economist Intelligence Unit 2009

48

8

12

7

25

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

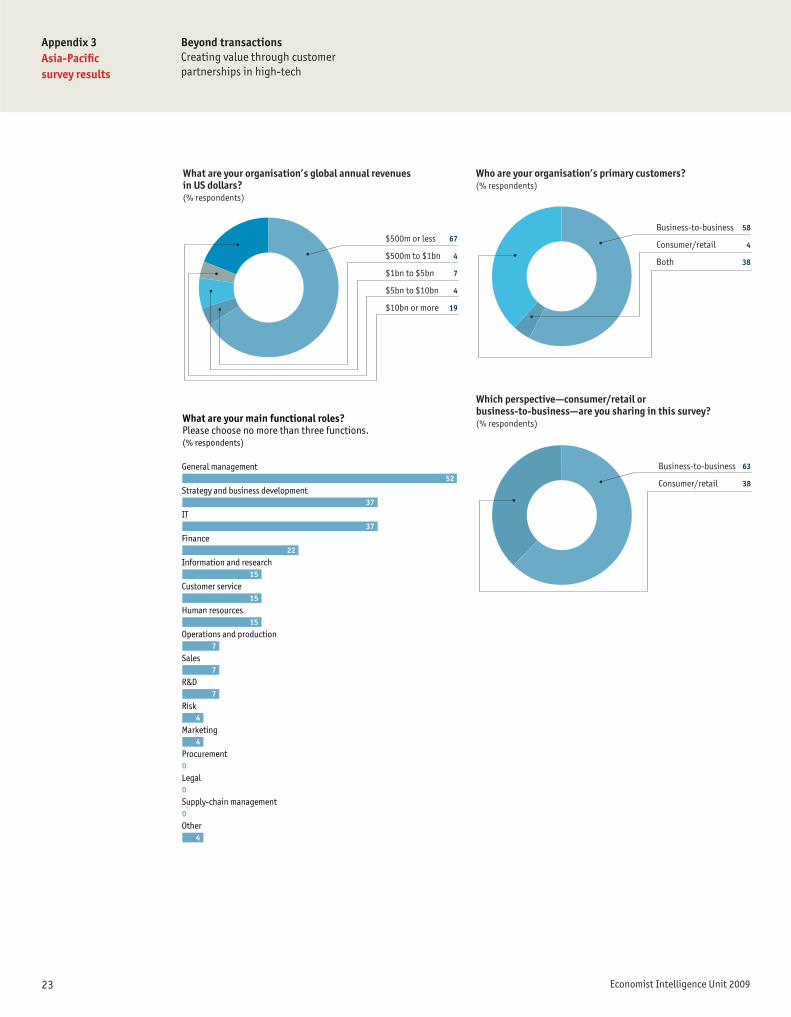

What are your organisation’s global annual revenues in US dollars? (% respondents)

Strategy and business development

IT

General management

Sales

Finance

Information and research

R&D

Marketing

Customer service

Operations and production

Human resources

Risk

Supply-chain management

Procurement

Legal

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

46

36

34

20

17

13

11

10

10

9

7

6

1

0

0

2

56

11

32

Business-to-business

Consumer/retail

Both

Who are your organisation’s primary customers?(% respondents)

61

39

Consumer/retail

Business-to-business

Which perspective—consumer/retail or business-to-business—are you sharing in this survey?(% respondents)

14 Economist Intelligence Unit 2009

Appendix 2Americas survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Appendix: Americas survey results

41

38

22

0

Product innovation: First to market with groundbreaking new products or services

Customer service: Providing superior service to clients

Operational excellence: Creating highly efficient processes

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

0 20 40 60 80 100

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Generating, tracking and measuring leads

Developing and launching new products

Planning and executing campaigns

Analysing and segmenting customers

Gauging customer satisfaction

Measuring effectiveness of processes

Responding to customer demands or complaints

Incorporating customer feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the customer via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

3 10 30 30 20 7

3 19 9 44 19 6

13 29 35 19 3

3 10 27 33 17 10

3 19 23 29 16 10

6 16 42 13 16 6

3 13 23 32 26 3

6 16 19 23 29 6

9 9 18 64

Appendix 2Americas survey results

Beyond transactionsCreating value through customer partnerships in high-tech

15 Economist Intelligence Unit 2009

Targeting the right customers in order to close a high percentage of prospects

Cross-selling or upselling customers

Efficiently acquiring customers (eg, reducing the cost of sales)

Gathering customer intelligence in the course of providing service

Generating qualified leads

Measuring/optimising effectiveness of marketing and promotional campaigns

Segmenting and profiling customers

Creating effective collateral

Maximising the number of repeat sales

Building long-term relationships

Providing a consistent customer experience

Ensuring that customer complaints are resolved quickly

Measuring customer satisfaction and loyalty

Involving customers product/service development (eg, co-creation)

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

44

34

34

34

31

28

25

22

19

19

19

16

13

3

0

0

Integrating customer tracking from lead through post-sales service

Presenting customers with a consistent picture of the organisation

Making each unit aware of how the others have interacted with a given customer

Developing and sharing a detailed picture of customers, behaviour and preferences

Prioritising resources directed towards customers by total value over life of customer

Establishing common definitions, assumptions and data

Helping each function find and act on ways to support the others

Measuring the probability that leads will turn into sales, and using these scores to guide sales

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

44

34

34

31

28

25

22

22

9

0

0

0 20 40 60 80 100

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most customers consider

Compared to our competitors, my organisation’s customers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Customers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

Agree Disagree Don’t know

39 58 3

56 22 22

32 52 16

52 45 3

39 42 19

52 32 16

53 34 13

47 38 16

48 35 16

48 45 6

16 Economist Intelligence Unit 2009

Appendix 2Americas survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Global economic downturn

Significant demand shifts for our products/services

Emergence of new competitors

Disruptive technology developments

Accessing key components or resources through our supply chain

Changing customer requirements

Finding access to credit/capital

Emergence of new markets for our products and services

Focusing on sustainability efforts

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

66

44

34

25

25

25

22

9

6

6

0

Improving usability, search and navigation of customer-facing websites

Making prices and sales terms more transparent for easy comparability

Building or supporting online customer communities

Improving online or self-service product support tools

Investing in self-service tools across multiple channels (eg, web, mobile devices, e-mail, point of sale)

Other

Don’t know

In which of the following ways does your organisation empower its customers? Select all that apply.(% respondents)

53

47

44

44

28

0

3

In-person customer service

Market research/customer surveys

Company-sponsored user forums

Online customer service

Feedback from value-added resellers (VARs)

Third-party forums and other social media

Wholesale buyer feedback

In-store feedback

Company website

Third-party online publications

Other

Don’t know

Through which channels does your organisation get the most useful customer feedback about its products? Select up to three. (% respondents)

50

31

31

31

25

19

19

16

9

6

0

3

Anticipate customer demand for new features and products

Achieve the right balance between price and features

Anticipate customer demand for existing products

Quickly incorporate customer feedback into design updates

Promote positive feelings about the brand

Anticipate customer demand for smoother supply chain operations

Sell add-ons, peripheral products or extra components

Other

Don’t know

Given current economic conditions, my organisation is specifically looking for feedback that helps it to: Select up to two. (% respondents)

44

38

31

28

22

16

6

0

3

Appendix 2Americas survey results

Beyond transactionsCreating value through customer partnerships in high-tech

17 Economist Intelligence Unit 2009

Product engineering

Product development

Product feature sets

Supply chain management

Distribution

Display

Sales operations

Marketing

Other

Don’t know

How well does your organisation incorporate customer feedback into its products? We do best at incorporating customer feedback into:Choose up to three from each column. (% respondents)

We do best at incorporating customer feedback into:We have the most difficulty incorporating customer feedback into:

38 22

59 25

47 9

22 13

19 16

16 16

13 16

19 34

00

6 16

North America

Latin America

Asia-Pacific

Eastern Europe

Western Europe

Middle East and Africa

In which region are you personally based? (% respondents)

88

13

0

0

0

0

47

16

9

28

Software

OEM

Semiconductors and components

Other

Which of the following best describes your company’s business? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

3

23

0

10

6

6

3

10

32

6

18 Economist Intelligence Unit 2009

Appendix 2Americas survey results

Beyond transactionsCreating value through customer partnerships in high-tech

44

16

9

6

25

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

Strategy and business development

IT

General management

Information and research

Marketing

R&D

Finance

Sales

Risk

Operations and production

Customer service

Supply-chain management

Procurement

Legal

Human resources

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

56

44

25

22

19

19

16

13

9

9

6

3

0

0

0

0

48

23

29

Business-to-business

Consumer/retail

Both

Who are your organisation’s primary customers?(% respondents)

50

50

Consumer/retail

Business-to-business

Which perspective—consumer/retail or business-to-business—are you sharing in this survey?(% respondents)

Appendix 3Asia-Pacifi c survey results

Beyond transactionsCreating value through customer partnerships in high-tech

19 Economist Intelligence Unit 2009

Appendix: Asia-Pacifi c survey results

56

26

19

0

Customer service: Providing superior service to clients

Product innovation: First to market with groundbreaking new products or services

Operational excellence: Creating highly efficient processes

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

0 20 40 60 80 100

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Generating, tracking and measuring leads

Developing and launching new products

Planning and executing campaigns

Analysing and segmenting customers

Gauging customer satisfaction

Measuring effectiveness of processes

Responding to customer demands or complaints

Incorporating customer feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the customer via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

4 19 19 37 22 0

4 15 37 30 15 0

7 15 30 19 30 0

19 41 26 15 0

4 11 33 19 33 0

4 19 37 15 26 0

4 15 22 41 19 0

15 33 30 22 0

17 17 67

20 Economist Intelligence Unit 2009

Appendix 3Asia-Pacifi c survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Generating qualified leads

Gathering customer intelligence in the course of providing service

Efficiently acquiring customers (eg, reducing the cost of sales)

Targeting the right customers in order to close a high percentage of prospects

Building long-term relationships

Maximising the number of repeat sales

Measuring customer satisfaction and loyalty

Segmenting and profiling customers

Cross-selling or upselling customers

Providing a consistent customer experience

Measuring/optimising effectiveness of marketing and promotional campaigns

Involving customers product/service development (eg, co-creation)

Creating effective collateral

Ensuring that customer complaints are resolved quickly

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

41

37

33

30

30

26

26

22

22

22

19

19

11

11

4

0

Integrating customer tracking from lead through post-sales service

Prioritising resources directed towards customers by total value over life of customer

Developing and sharing a detailed picture of customers, behaviour and preferences

Making each unit aware of how the others have interacted with a given customer

Helping each function find and act on ways to support the others

Measuring the probability that leads will turn into sales, and using these scores to guide sales

Establishing common definitions, assumptions and data

Presenting customers with a consistent picture of the organisation

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

56

48

44

37

26

26

19

19

0

0

0

0 20 40 60 80 100

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most customers consider

Compared to our competitors, my organisation’s customers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Customers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

Agree Disagree Don’t know

41 56 4

67 19 15

30 41 30

33 44 22

30 33 37

56 30 15

67 22 11

41 52 7

52 48 0

48 44 7

Appendix 3Asia-Pacifi c survey results

Beyond transactionsCreating value through customer partnerships in high-tech

21 Economist Intelligence Unit 2009

Global economic downturn

Changing customer requirements

Disruptive technology developments

Significant demand shifts for our products/services

Emergence of new markets for our products and services

Focusing on sustainability efforts

Finding access to credit/capital

Emergence of new competitors

Accessing key components or resources through our supply chain

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

63

41

37

37

22

22

19

19

15

0

0

Making prices and sales terms more transparent for easy comparability

Improving usability, search and navigation of customer-facing websites

Investing in self-service tools across multiple channels (eg, web, mobile devices, e-mail, point of sale)

Building or supporting online customer communities

Improving online or self-service product support tools

Other

Don’t know

In which of the following ways does your organisation empower its customers? Select all that apply.(% respondents)

59

41

41

37

30

0

4

In-person customer service

Market research/customer surveys

Company-sponsored user forums

Online customer service

Company website

Feedback from value-added resellers (VARs)

Third-party forums and other social media

Third-party online publications

In-store feedback

Wholesale buyer feedback

Other

Don’t know

Through which channels does your organisation get the most useful customer feedback about its products? Select up to three. (% respondents)

74

44

26

26

19

11

7

4

4

4

0

0

Anticipate customer demand for new features and products

Anticipate customer demand for existing products

Promote positive feelings about the brand

Achieve the right balance between price and features

Quickly incorporate customer feedback into design updates

Sell add-ons, peripheral products or extra components

Anticipate customer demand for smoother supply chain operations

Other

Don’t know

Given current economic conditions, my organisation is specifically looking for feedback that helps it to: Select up to two. (% respondents)

56

41

33

22

19

15

4

0

4

22 Economist Intelligence Unit 2009

Appendix 3Asia-Pacifi c survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Product engineering

Product development

Product feature sets

Supply chain management

Distribution

Display

Sales operations

Marketing

Other

Don’t know

How well does your organisation incorporate customer feedback into its products? We do best at incorporating customer feedback into:Choose up to three from each column. (% respondents)

We do best at incorporating customer feedback into:We have the most difficulty incorporating customer feedback into:

41 19

44 26

52 11

22 37

19 34

4 24

33 18

30 5

00

7 4

Asia-Pacific

Latin America

North America

Eastern Europe

Western Europe

Middle East and Africa

In which region are you personally based? (% respondents)

100

0

0

0

0

0

48

11

0

41

Software

OEM

Semiconductors and components

Other

Which of the following best describes your company’s business? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

4

22

11

11

4

11

0

11

15

11

Appendix 3Asia-Pacifi c survey results

Beyond transactionsCreating value through customer partnerships in high-tech

23 Economist Intelligence Unit 2009

67

4

7

4

19

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

General management

Strategy and business development

IT

Finance

Information and research

Customer service

Human resources

Operations and production

Sales

R&D

Risk

Marketing

Procurement

Legal

Supply-chain management

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

52

37

37

22

15

15

15

7

7

7

4

4

0

0

0

4

58

4

38

Business-to-business

Consumer/retail

Both

Who are your organisation’s primary customers?(% respondents)

63

38

Business-to-business

Consumer/retail

Which perspective—consumer/retail or business-to-business—are you sharing in this survey?(% respondents)

24 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Appendix: Europe Middle East and Africasurvey results

43

40

17

0

Product innovation: First to market with groundbreaking new products or services

Customer service: Providing superior service to clients

Operational excellence: Creating highly efficient processes

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

0 20 40 60 80 100

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Generating, tracking and measuring leads

Developing and launching new products

Planning and executing campaigns

Analysing and segmenting customers

Gauging customer satisfaction

Measuring effectiveness of processes

Responding to customer demands or complaints

Incorporating customer feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the customer via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

7 3 27 33 30 0

7 20 33 37 3

7 10 17 37 30 0

3 20 23 37 17 0

7 13 27 33 20 0

13 13 27 23 20 3

7 7 13 47 23 3

7 7 30 43 10 3

25 25 25 25

Appendix 4EMEA survey results

Beyond transactionsCreating value through customer partnerships in high-tech

25 Economist Intelligence Unit 2009

Generating qualified leads

Building long-term relationships

Gathering customer intelligence in the course of providing service

Involving customers product/service development (eg, co-creation)

Targeting the right customers in order to close a high percentage of prospects

Cross-selling or upselling customers

Segmenting and profiling customers

Maximising the number of repeat sales

Efficiently acquiring customers (eg, reducing the cost of sales)

Providing a consistent customer experience

Ensuring that customer complaints are resolved quickly

Creating effective collateral

Measuring customer satisfaction and loyalty

Measuring/optimising effectiveness of marketing and promotional campaigns

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

47

40

37

33

27

27

20

20

20

20

17

13

13

7

3

0

Integrating customer tracking from lead through post-sales service

Developing and sharing a detailed picture of customers, behaviour and preferences

Establishing common definitions, assumptions and data

Presenting customers with a consistent picture of the organisation

Making each unit aware of how the others have interacted with a given customer

Measuring the probability that leads will turn into sales, and using these scores to guide sales

Prioritising resources directed towards customers by total value over life of customer

Helping each function find and act on ways to support the others

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

37

37

30

30

30

30

23

10

3

3

0

0 20 40 60 80 100

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most customers consider

Compared to our competitors, my organisation’s customers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Customers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

Agree Disagree Don’t know

20 77 3

62 7 31

34 38 28

43 43 13

27 60 13

53 30 17

60 23 17

53 37 10

43 47 10

40 37 23

26 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsCreating value through customer partnerships in high-tech

Global economic downturn

Emergence of new markets for our products and services

Changing customer requirements

Emergence of new competitors

Finding access to credit/capital

Disruptive technology developments

Accessing key components or resources through our supply chain

Significant demand shifts for our products/services

Focusing on sustainability efforts

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

83

30

30

20

17

13

13

13

10

3

0

Improving usability, search and navigation of customer-facing websites

Improving online or self-service product support tools

Investing in self-service tools across multiple channels (eg, web, mobile devices, e-mail, point of sale)

Making prices and sales terms more transparent for easy comparability

Building or supporting online customer communities

Other

Don’t know

In which of the following ways does your organisation empower its customers? Select all that apply.(% respondents)

53

47

37

33

23

13

17

In-person customer service

Market research/customer surveys

Feedback from value-added resellers (VARs)

Online customer service

Company website

Company-sponsored user forums

In-store feedback

Third-party online publications

Wholesale buyer feedback

Third-party forums and other social media

Other

Don’t know

Through which channels does your organisation get the most useful customer feedback about its products? Select up to three. (% respondents)

63

33

33

23

13

13

10

7

7

3

3

7

Anticipate customer demand for new features and products

Anticipate customer demand for existing products

Sell add-ons, peripheral products or extra components

Achieve the right balance between price and features

Quickly incorporate customer feedback into design updates

Promote positive feelings about the brand

Anticipate customer demand for smoother supply chain operations

Other

Don’t know

Given current economic conditions, my organisation is specifically looking for feedback that helps it to: Select up to two. (% respondents)

57

40

27

23

17

17

3

0

3

Appendix 4EMEA survey results

Beyond transactionsCreating value through customer partnerships in high-tech

27 Economist Intelligence Unit 2009

Product engineering

Product development

Product feature sets

Supply chain management

Distribution

Display

Sales operations

Marketing

Other

Don’t know

How well does your organisation incorporate customer feedback into its products? We do best at incorporating customer feedback into:Choose up to three from each column. (% respondents)

We do best at incorporating customer feedback into:We have the most difficulty incorporating customer feedback into:

53 17

70 23

63 10

13 13

3 30

0 33

40 23

23 17

3 7

3 10

Western Europe

Eastern Europe

Middle East and Africa

Asia-Pacific

Latin America

North America

In which region are you personally based? (% respondents)

80

13

7

0

0

0

53

13

3

30

Software

Semiconductors and components

OEM

Other

Which of the following best describes your company’s business? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

7

23

3

7

0

10

7

13

30

0

28 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsCreating value through customer partnerships in high-tech

37

3

20

10

30

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

Strategy and business development

Sales

General management

IT

Finance

Operations and production

Customer service

Marketing

R&D

Human resources

Risk

Information and research

Procurement

Legal

Supply-chain management

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

43

40

27

27

13

10

10

7

7

7

3

3

0

0

0

3

58

7

30

Business-to-business

Consumer/retail

Both

Who are your organisation’s primary customers?(% respondents)

71

29

Business-to-business

Consumer/retail

Which perspective—consumer/retail or business-to-business—are you sharing in this survey?(% respondents)

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsors of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in the white paper. Co

ver i

mag

e: S

hutt

erst

ock

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8476E-mail: [email protected]

NEW YORK111 West 57th StreetNew York NY 10019United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]