bharti airtel ltd-result update

TRANSCRIPT

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 1/10Bharti Airtel Limited – Result Update ACMIIL

Bharti Airtel Limited

Analyst

Deepti Chauhan

Tel: (022) 2858 3408

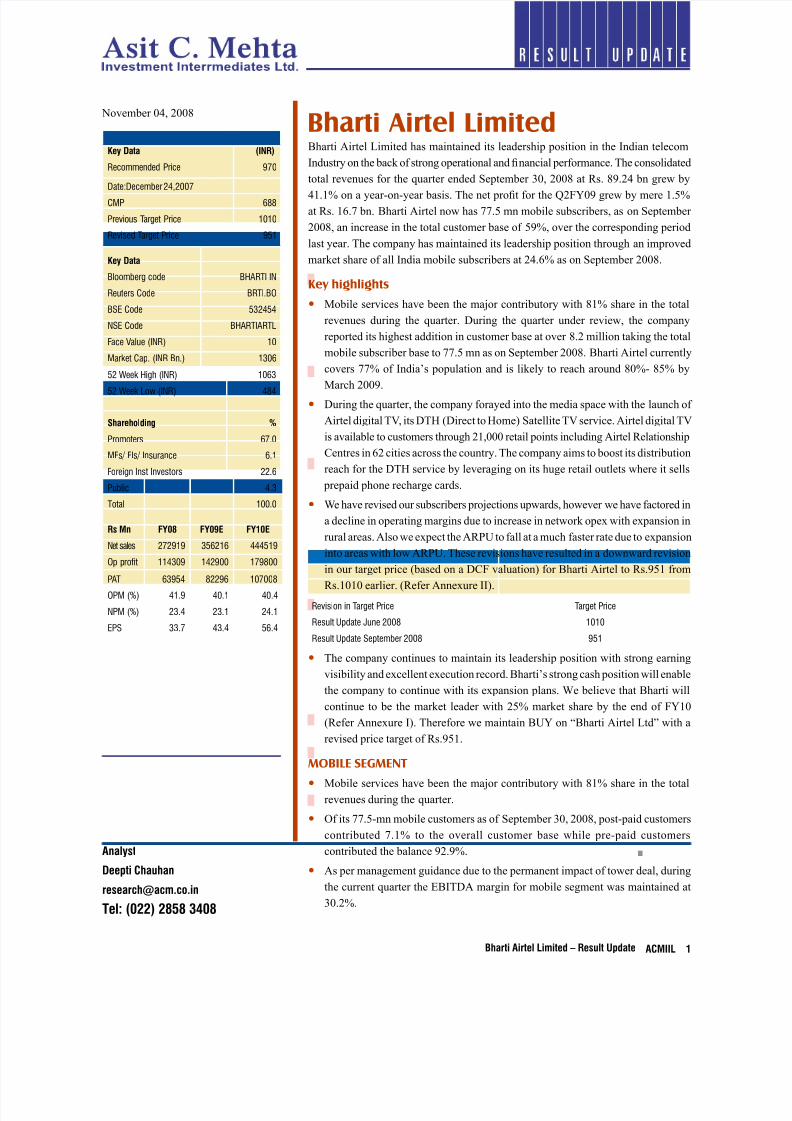

Key Data (INR)

Recommended PriceDate:December 24,2007

970

CMP 688

Previous Target Price 1010

Revised Target Price 951

Key Data

Bloomberg code BHARTI IN

Reuters Code BRTI.BO

BSE Code 532454

NSE Code BHARTIARTL

Face Value (INR) 10Market Cap. (INR Bn.) 1306

52 Week High (INR) 1063

52 Week Low (INR) 484

Shareholding %

Promoters 67.0

MFs/ FIs/ Insurance 6.1

Foreign Inst Investors 22.6

Public 4.3

Total 100.0

Rs Mn FY08 FY09E FY0E

Net sales 272919 356216 444519

Op profit 114309 142900 179800

PAT 63954 82296 107008

OPM (%) 41.9 40.1 40.4

NPM (%) 23.4 23.1 24.1

EPS 33.7 43.4 56.4

November 04, 2008

Bharti Airtel Limited has maintained its leadership position in the Indian telecom

Industry on the back of strong operational and nancial performance. The consolidated

total revenues for the quarter ended September 30, 2008 at Rs. 89.24 bn grew by

41.1% on a year-on-year basis. The net prot for the Q2FY09 grew by mere 1.5%

at Rs. 16.7 bn. Bharti Airtel now has 77.5 mn mobile subscribers, as on September

2008, an increase in the total customer base of 59%, over the corresponding period

last year. The company has maintained its leadership position through an improved

market share of all India mobile subscribers at 24.6% as on September 2008.

Key highlights

Mobile services have been the major contributory with 81% share in the total

revenues during the quarter. During the quarter under review, the company

reported its highest addition in customer base at over 8.2 million taking the total

mobile subscriber base to 77.5 mn as on September 2008. Bharti Airtel currently

covers 77% of India’s population and is likely to reach around 80%- 85% by

March 2009.

During the quarter, the company forayed into the media space with the launch of

Airtel digital TV, its DTH (Direct to Home) Satellite TV service. Airtel digital TV

is available to customers through 21,000 retail points including Airtel Relationship

Centres in 62 cities across the country. The company aims to boost its distribution

reach for the DTH service by leveraging on its huge retail outlets where it sells

prepaid phone recharge cards.

We have revised our subscribers projections upwards, however we have factored in

a decline in operating margins due to increase in network opex with expansion in

rural areas. Also we expect the ARPU to fall at a much faster rate due to expansion

into areas with low ARPU. These revisions have resulted in a downward revision

in our target price (based on a DCF valuation) for Bharti Airtel to Rs.951 from

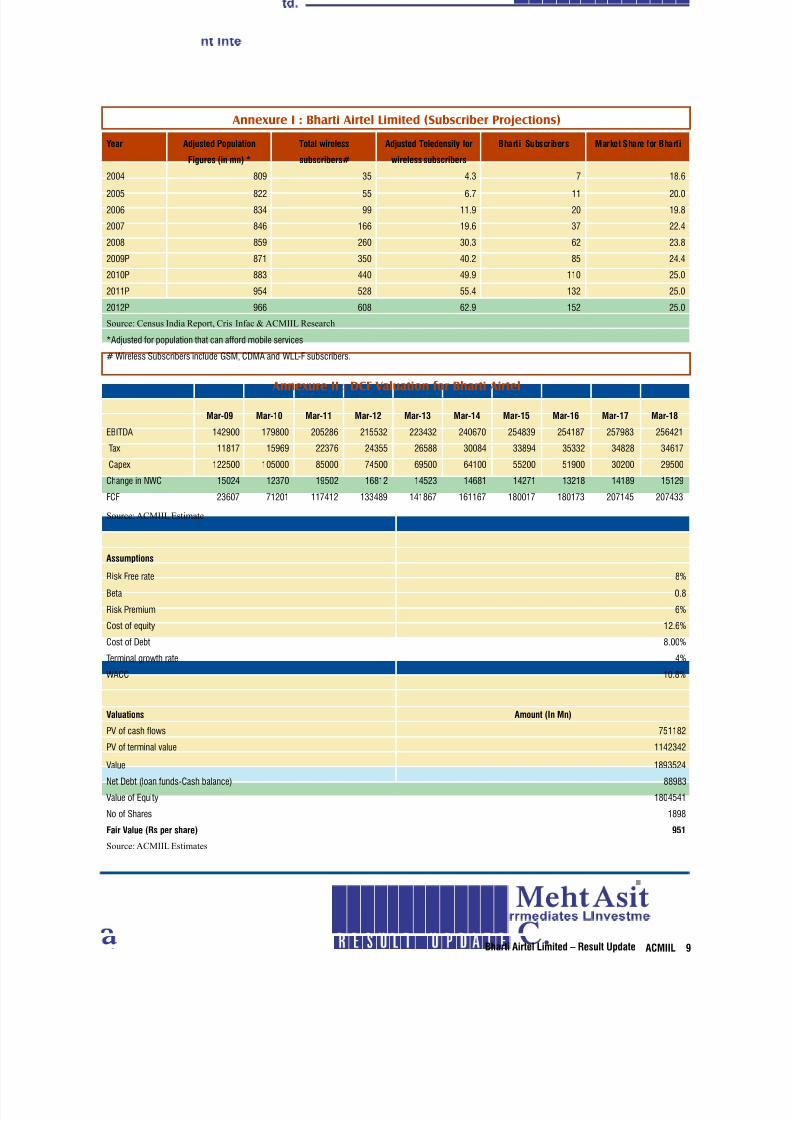

Rs.1010 earlier. (Refer Annexure II).

Revision in Target Price Target Price

Result Update June 2008 1010

Result Update September 2008 951

The company continues to maintain its leadership position with strong earning

visibility and excellent execution record. Bharti’s strong cash position will enable

the company to continue with its expansion plans. We believe that Bharti will

continue to be the market leader with 25% market share by the end of FY10

(Refer Annexure I). Therefore we maintain BUY on “Bharti Airtel Ltd” with a

revised price target of Rs.951.

MOBILE SEGMENT

Mobile services have been the major contributory with 81% share in the total

revenues during the quarter.

Of its 77.5-mn mobile customers as of September 30, 2008, post-paid customers

contributed 7.1% to the overall customer base while pre-paid customers

contributed the balance 92.9%.

As per management guidance due to the permanent impact of tower deal, during

the current quarter the EBITDA margin for mobile segment was maintained at

30.2%.

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 2/10Bharti Airtel Limited – Result Update ACMIIL 2

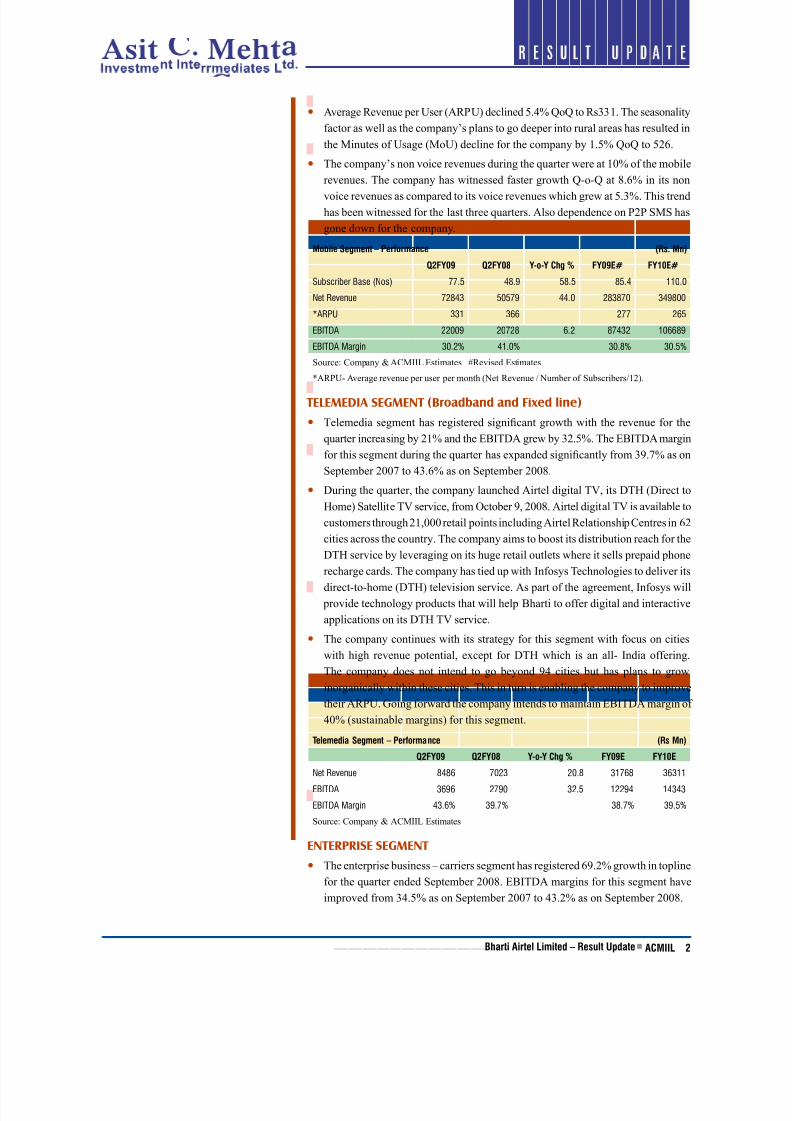

Average Revenue per User (ARPU) declined 5.4% QoQ to Rs331. The seasonality

factor as well as the company’s plans to go deeper into rural areas has resulted in

the Minutes of Usage (MoU) decline for the company by 1.5% QoQ to 526.

The company’s non voice revenues during the quarter were at 10% of the mobile

revenues. The company has witnessed faster growth Q-o-Q at 8.6% in its non

voice revenues as compared to its voice revenues which grew at 5.3%. This trend

has been witnessed for the last three quarters. Also dependence on P2P SMS has

gone down for the company.

Mobile Segment – Performance (Rs. Mn)

Q2FY09 Q2FY08 Y-o-Y Chg % FY09E# FY0E#

Subscriber Base (Nos) 77.5 48.9 58.5 85.4 110.0

Net Revenue 72843 50579 44.0 283870 349800

*ARPU 331 366 277 265

EBITDA 22009 20728 6.2 87432 106689

EBITDA Margin 30.2% 41.0% 30.8% 30.5%

Source: Company & ACMIIL Estimates #Revised Estimates

*ARPU- Average revenue per user per month (Net Revenue / Number of Subscribers/12).

TELEMEDIA SEGMENT (Broadband and Fixed line)

Telemedia segment has registered signicant growth with the revenue for the

quarter increasing by 21% and the EBITDA grew by 32.5%. The EBITDA margin

for this segment during the quarter has expanded signicantly from 39.7% as on

September 2007 to 43.6% as on September 2008.

During the quarter, the company launched Airtel digital TV, its DTH (Direct to

Home) Satellite TV service, from October 9, 2008. Airtel digital TV is available to

customers through 21,000 retail points including Airtel Relationship Centres in 62

cities across the country. The company aims to boost its distribution reach for the

DTH service by leveraging on its huge retail outlets where it sells prepaid phone

recharge cards. The company has tied up with Infosys Technologies to deliver its

direct-to-home (DTH) television service. As part of the agreement, Infosys will

provide technology products that will help Bharti to offer digital and interactive

applications on its DTH TV service.

The company continues with its strategy for this segment with focus on cities

with high revenue potential, except for DTH which is an all- India offering.

The company does not intend to go beyond 94 cities but has plans to grow

inorganically within these cities. This in turn is enabling the company to improvetheir ARPU. Going forward the company intends to maintain EBITDA margin of

40% (sustainable margins) for this segment.

Telemedia Segment – Performance (Rs Mn)

Q2FY09 Q2FY08 Y-o-Y Chg % FY09E FY0E

Net Revenue 8486 7023 20.8 31768 36311

EBITDA 3696 2790 32.5 12294 14343

EBITDA Margin 43.6% 39.7% 38.7% 39.5%

Source: Company & ACMIIL Estimates

ENTERPRISE SEGMENT

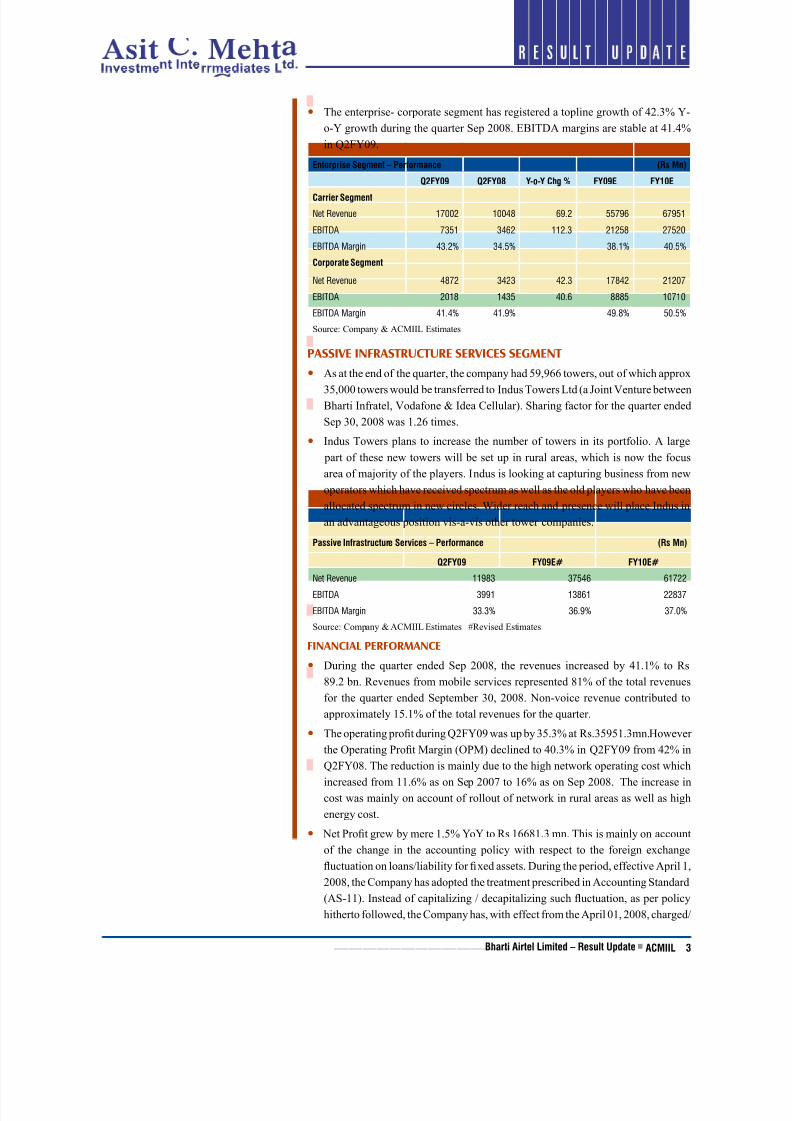

The enterprise business – carriers segment has registered 69.2% growth in topline

for the quarter ended September 2008. EBITDA margins for this segment have

improved from 34.5% as on September 2007 to 43.2% as on September 2008.

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 3/10Bharti Airtel Limited – Result Update ACMIIL 3

The enterprise- corporate segment has registered a topline growth of 42.3% Y-

o-Y growth during the quarter Sep 2008. EBITDA margins are stable at 41.4%

in Q2FY09.

Enterprise Segment – Performance (Rs Mn)

Q2FY09 Q2FY08 Y-o-Y Chg % FY09E FY0E

Carrier Segment

Net Revenue 17002 10048 69.2 55796 67951

EBITDA 7351 3462 112.3 21258 27520

EBITDA Margin 43.2% 34.5% 38.1% 40.5%

Corporate Segment

Net Revenue 4872 3423 42.3 17842 21207

EBITDA 2018 1435 40.6 8885 10710

EBITDA Margin 41.4% 41.9% 49.8% 50.5%

Source: Company & ACMIIL Estimates

PASSIVE INFRASTRUCTURE SERVICES SEGMENT

As at the end of the quarter, the company had 59,966 towers, out of which approx

35,000 towers would be transferred to Indus Towers Ltd (a Joint Venture between

Bharti Infratel, Vodafone & Idea Cellular). Sharing factor for the quarter ended

Sep 30, 2008 was 1.26 times.

Indus Towers plans to increase the number of towers in its portfolio. A large

part of these new towers will be set up in rural areas, which is now the focus

area of majority of the players. Indus is looking at capturing business from new

operators which have received spectrum as well as the old players who have been

allocated spectrum in new circles. Wider reach and presence will place Indus in

an advantageous position vis-a-vis other tower companies.

Passive Infrastructure Services – Performance (Rs Mn)

Q2FY09 FY09E# FY0E#

Net Revenue 11983 37546 61722

EBITDA 3991 13861 22837

EBITDA Margin 33.3% 36.9% 37.0%

Source: Company & ACMIIL Estimates #Revised Estimates

FINANCIAL PERFORMANCE

During the quarter ended Sep 2008, the revenues increased by 41.1% to Rs

89.2 bn. Revenues from mobile services represented 81% of the total revenuesfor the quarter ended September 30, 2008. Non-voice revenue contributed to

approximately 15.1% of the total revenues for the quarter.

The operating prot during Q2FY09 was up by 35.3% at Rs.35951.3mn.However

the Operating Prot Margin (OPM) declined to 40.3% in Q2FY09 from 42% in

Q2FY08. The reduction is mainly due to the high network operating cost which

increased from 11.6% as on Sep 2007 to 16% as on Sep 2008. The increase in

cost was mainly on account of rollout of network in rural areas as well as high

energy cost.

Net Prot grew by mere 1.5% YoY to Rs 16681.3 mn. This is mainly on account

of the change in the accounting policy with respect to the foreign exchange

uctuation on loans/liability for xed assets. During the period, effective April 1,

2008, the Company has adopted the treatment prescribed in Accounting Standard

(AS-11). Instead of capitalizing / decapitalizing such uctuation, as per policy

hitherto followed, the Company has, with effect from the April 01, 2008, charged/

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 4/10Bharti Airtel Limited – Result Update ACMIIL 4

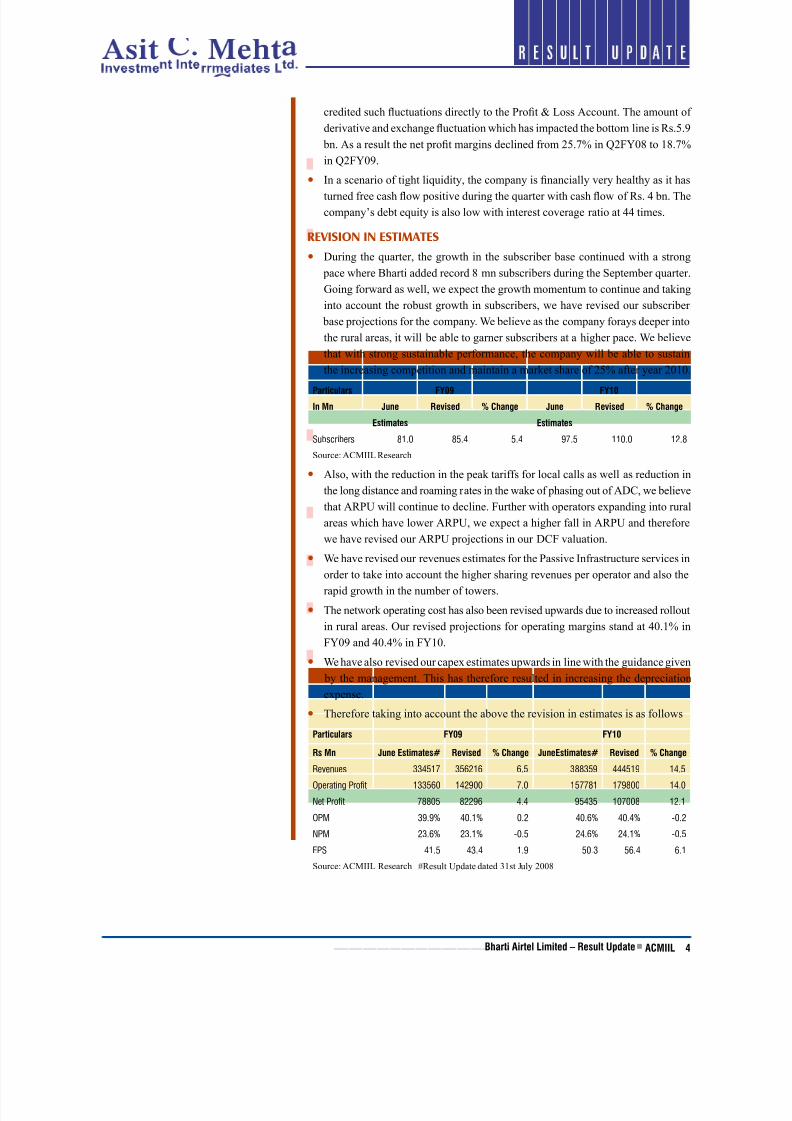

credited such uctuations directly to the Prot & Loss Account. The amount of

derivative and exchange uctuation which has impacted the bottom line is Rs.5.9

bn. As a result the net prot margins declined from 25.7% in Q2FY08 to 18.7%

in Q2FY09.

In a scenario of tight liquidity, the company is nancially very healthy as it has

turned free cash ow positive during the quarter with cash ow of Rs. 4 bn. The

company’s debt equity is also low with interest coverage ratio at 44 times.

REVISION IN ESTIMATES

During the quarter, the growth in the subscriber base continued with a strong

pace where Bharti added record 8 mn subscribers during the September quarter.

Going forward as well, we expect the growth momentum to continue and taking

into account the robust growth in subscribers, we have revised our subscriber

base projections for the company. We believe as the company forays deeper into

the rural areas, it will be able to garner subscribers at a higher pace. We believethat with strong sustainable performance, the company will be able to sustain

the increasing competition and maintain a market share of 25% after year 2010.

Particulars FY09 FY0

In Mn June Revised % Change June Revised % Change

Estimates Estimates

Subscribers 81.0 85.4 5.4 97.5 110.0 12.8

Source: ACMIIL Research

Also, with the reduction in the peak tariffs for local calls as well as reduction in

the long distance and roaming rates in the wake of phasing out of ADC, we believe

that ARPU will continue to decline. Further with operators expanding into rural

areas which have lower ARPU, we expect a higher fall in ARPU and therefore

we have revised our ARPU projections in our DCF valuation.

We have revised our revenues estimates for the Passive Infrastructure services in

order to take into account the higher sharing revenues per operator and also the

rapid growth in the number of towers.

The network operating cost has also been revised upwards due to increased rollout

in rural areas. Our revised projections for operating margins stand at 40.1% in

FY09 and 40.4% in FY10.

We have also revised our capex estimates upwards in line with the guidance given

by the management. This has therefore resulted in increasing the depreciation

expense.

Therefore taking into account the above the revision in estimates is as follows

Particulars FY09 FY0

Rs Mn June Estimates# Revised % Change JuneEstimates# Revised % Change

Revenues 334517 356216 6.5 388359 444519 14.5

Operating Profit 133560 142900 7.0 157781 179800 14.0

Net Profit 78805 82296 4.4 95435 107008 12.1

OPM 39.9% 40.1% 0.2 40.6% 40.4% -0.2

NPM 23.6% 23.1% -0.5 24.6% 24.1% -0.5

EPS 41.5 43.4 1.9 50.3 56.4 6.1

Source: ACMIIL Research #Result Update dated 31st July 2008

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 5/10Bharti Airtel Limited – Result Update ACMIIL 5

VALUATION AND RECOMMENDATION

We have revised our subscribers projections upwards, however we have factored in

a decline in operating margins due to increase in network opex with expansion in

rural areas. Also we expect the ARPU to fall at a much faster rate due to expansioninto areas with low ARPU. These revisions have resulted in a downward revision

in our target prices (based on a DCF valuation) for Bharti Airtel to Rs.951 from

Rs.1010 earlier. (Refer Annexure II).

The company continues to maintain its leadership position with strong earning

visibility and excellent execution record. Bharti’s strong cash position will enable

the company to continue with its expansion plans. We believe that Bharti will

continue to be the market leader with 25% market share by the end of FY10

(Refer Annexure I). Therefore we maintain BUY on “Bharti Airtel Ltd” with a

revised price target of Rs.951.

MAJOR DEVELOPMENTSThe launching of services in SriLanka is on track in terms of network roll out. The

company expects the services to be launched by the end of the year (December).

Bharti Airtel Lanka, a subsidiary of Bharti Airtel, had already announced plans

to launch 2G and 3G services in Sri Lanka under the same brand Airtel. It had

signed a $ 150 million deal with China`s Huawei Technologies to set up a mobile

phone network in Sri Lanka.

The problem of spectrum shortfall is also getting settled with Bharti receiving

additional spectrum in three circles namely Tamil Nadu, Bihar and Karnataka in

the last quarter and is awaiting allocation in six more circles.

The government has slashed licence fees by 2% for players whose services cover over 95% of the residential areas in a state. The new rates will be applicable from

April, 2009. However, the licence fee cuts will not be applicable in the four metros.

At present, telcos pay 10% of their revenues to the government as licence fee in

category A circles, 8% in category B zones and 6% for category C. However, if

their services cover over 95% of the residential areas, the licence fee will be down

to 8%, 6% and 4% for category A, B and C circles, respectively. The company

believes that it would benet from the license fee reduction effective April 2009

as majority of its circles have covered 95% of the areas in the state in which they

have operations.

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 6/10Bharti Airtel Limited – Result Update ACMIIL

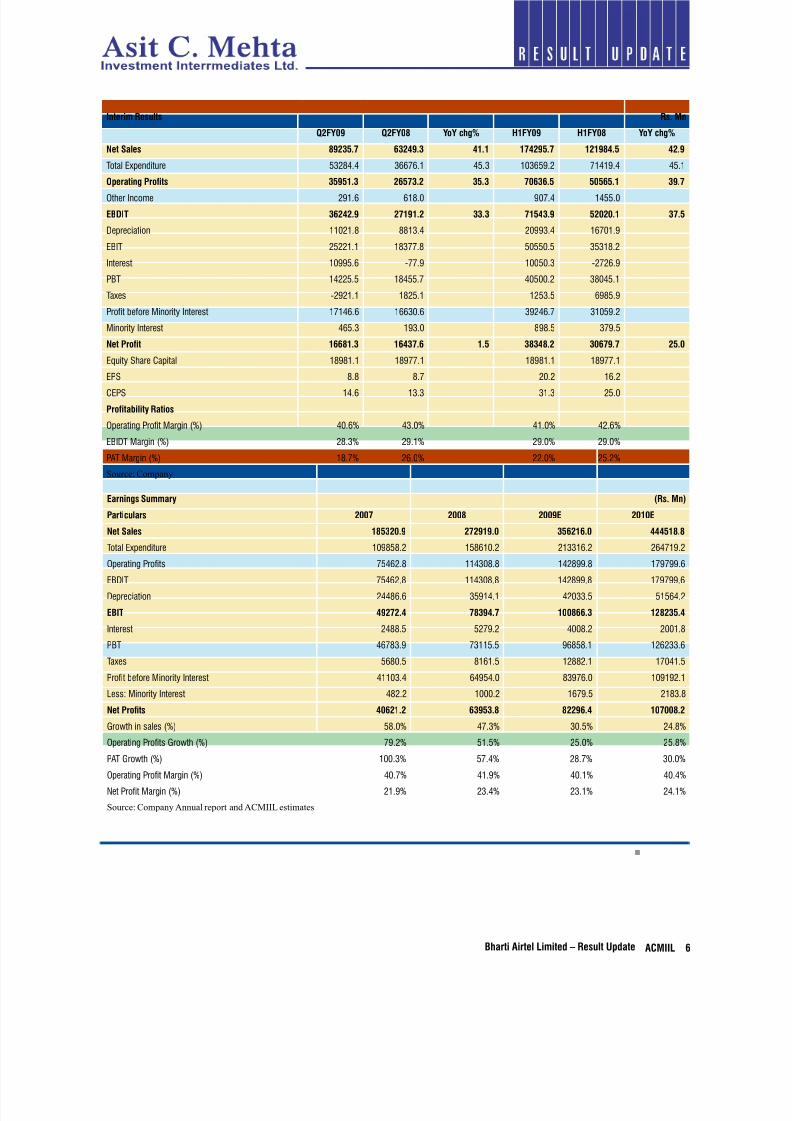

Interim Results Rs. Mn

Q2FY09 Q2FY08 YoY chg% HFY09 HFY08 YoY chg%

Net Sales 89235.7 3249.3 4. 74295.7 2984.5 42.9

Total Expenditure 53284.4 36676.1 45.3 103659.2 71419.4 45.1

Operating Profits 3595.3 2573.2 35.3 703.5 5055. 39.7

Other Income 291.6 618.0 907.4 1455.0

EBDIT 3242.9 279.2 33.3 7543.9 52020. 37.5

Depreciation 11021.8 8813.4 20993.4 16701.9

EBIT 25221.1 18377.8 50550.5 35318.2

Interest 10995.6 -77.9 10050.3 -2726.9

PBT 14225.5 18455.7 40500.2 38045.1

Taxes -2921.1 1825.1 1253.5 6985.9

Profit before Minority Interest 17146.6 16630.6 39246.7 31059.2

Minority Interest 465.3 193.0 898.5 379.5

Net Profit 8.3 437. .5 38348.2 3079.7 25.0

Equity Share Capital 18981.1 18977.1 18981.1 18977.1

EPS 8.8 8.7 20.2 16.2

CEPS 14.6 13.3 31.3 25.0

Profitability Ratios

Operating Profit Margin (%) 40.6% 43.0% 41.0% 42.6%

EBIDT Margin (%) 28.3% 29.1% 29.0% 29.0%

PAT Margin (%) 18.7% 26.0% 22.0% 25.2%

Source: Company

Earnings Summary (Rs. Mn)

Particulars 2007 2008 2009E 200E

Net Sales 85320.9 27299.0 352.0 44458.8

Total Expenditure 109858.2 158610.2 213316.2 264719.2

Operating Profits 75462.8 114308.8 142899.8 179799.6

EBDIT 75462.8 114308.8 142899.8 179799.6

Depreciation 24486.6 35914.1 42033.5 51564.2

EBIT 49272.4 78394.7 008.3 28235.4

Interest 2488.5 5279.2 4008.2 2001.8

PBT 46783.9 73115.5 96858.1 126233.6

Taxes 5680.5 8161.5 12882.1 17041.5

Profit before Minority Interest 41103.4 64954.0 83976.0 109192.1

Less: Minority Interest 482.2 1000.2 1679.5 2183.8

Net Profits 402.2 3953.8 8229.4 07008.2

Growth in sales (%) 58.0% 47.3% 30.5% 24.8%

Operating Profits Growth (%) 79.2% 51.5% 25.0% 25.8%

PAT Growth (%) 100.3% 57.4% 28.7% 30.0%

Operating Profit Margin (%) 40.7% 41.9% 40.1% 40.4%

Net Profit Margin (%) 21.9% 23.4% 23.1% 24.1%

Source: Company Annual report and ACMIIL estimates

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 7/10Bharti Airtel Limited – Result Update ACMIIL 7

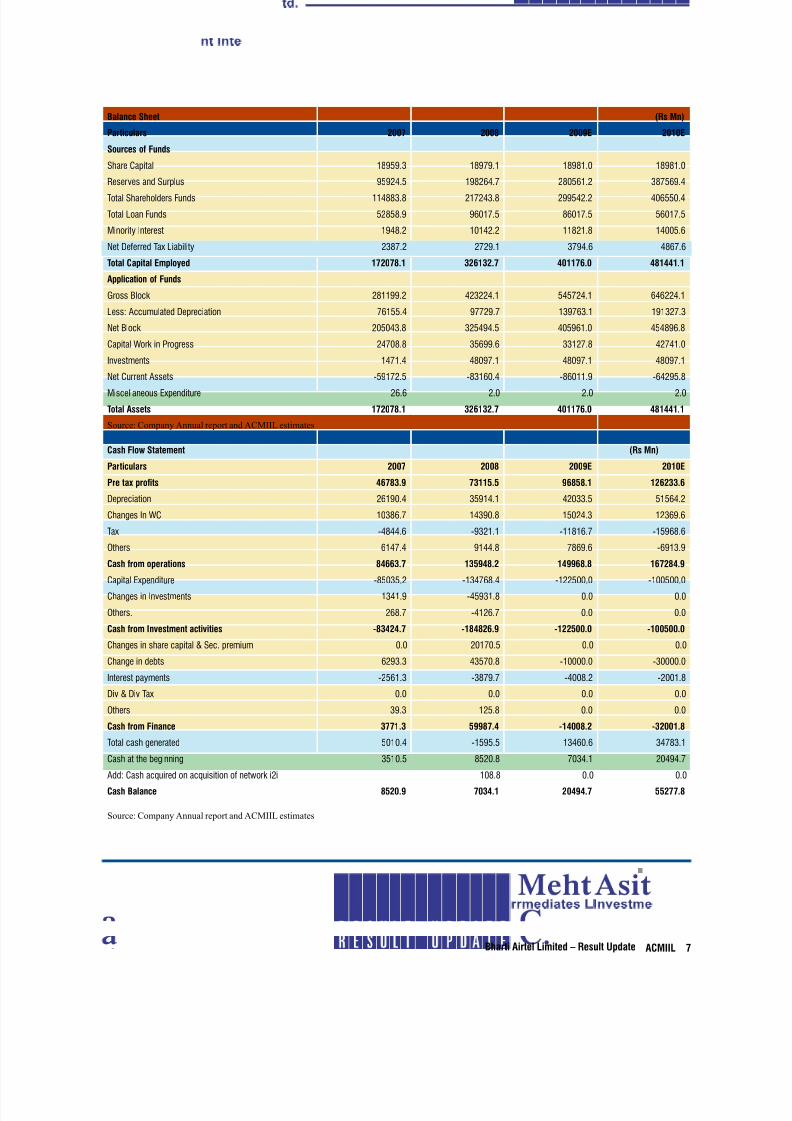

Balance Sheet (Rs Mn)

Particulars 2007 2008 2009E 200E

Sources of Funds

Share Capital 18959.3 18979.1 18981.0 18981.0

Reserves and Surplus 95924.5 198264.7 280561.2 387569.4

Total Shareholders Funds 114883.8 217243.8 299542.2 406550.4

Total Loan Funds 52858.9 96017.5 86017.5 56017.5

Minority Interest 1948.2 10142.2 11821.8 14005.6

Net Deferred Tax Liability 2387.2 2729.1 3794.6 4867.6

Total Capital Employed 72078. 3232.7 407.0 4844.

Application of Funds

Gross Block 281199.2 423224.1 545724.1 646224.1

Less: Accumulated Depreciation 76155.4 97729.7 139763.1 191327.3

Net Block 205043.8 325494.5 405961.0 454896.8

Capital Work in Progress 24708.8 35699.6 33127.8 42741.0

Investments 1471.4 48097.1 48097.1 48097.1

Net Current Assets -59172.5 -83160.4 -86011.9 -64295.8

Miscellaneous Expenditure 26.6 2.0 2.0 2.0

Total Assets 72078. 3232.7 407.0 4844.

Source: Company Annual report and ACMIIL estimates

Cash Flow Statement (Rs Mn)

Particulars 2007 2008 2009E 200E

Pre tax profits 4783.9 735.5 9858. 2233.

Depreciation 26190.4 35914.1 42033.5 51564.2

Changes In WC 10386.7 14390.8 15024.3 12369.6

Tax -4844.6 -9321.1 -11816.7 -15968.6

Others 6147.4 9144.8 7869.6 -6913.9

Cash from operations 843.7 35948.2 4998.8 7284.9

Capital Expenditure -85035.2 -134768.4 -122500.0 -100500.0

Changes in Investments 1341.9 -45931.8 0.0 0.0

Others. 268.7 -4126.7 0.0 0.0

Cash from Investment activities -83424.7 -8482.9 -22500.0 -00500.0

Changes in share capital & Sec. premium 0.0 20170.5 0.0 0.0

Change in debts 6293.3 43570.8 -10000.0 -30000.0

Interest payments -2561.3 -3879.7 -4008.2 -2001.8

Div & Div Tax 0.0 0.0 0.0 0.0

Others 39.3 125.8 0.0 0.0

Cash from Finance 377.3 59987.4 -4008.2 -3200.8

Total cash generated 5010.4 -1595.5 13460.6 34783.1

Cash at the beginning 3510.5 8520.8 7034.1 20494.7

Add: Cash acquired on acquisition of network i2i 108.8 0.0 0.0

Cash Balance 8520.9 7034. 20494.7 55277.8

Source: Company Annual report and ACMIIL estimates

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 8/10Bharti Airtel Limited – Result Update ACMIIL 8

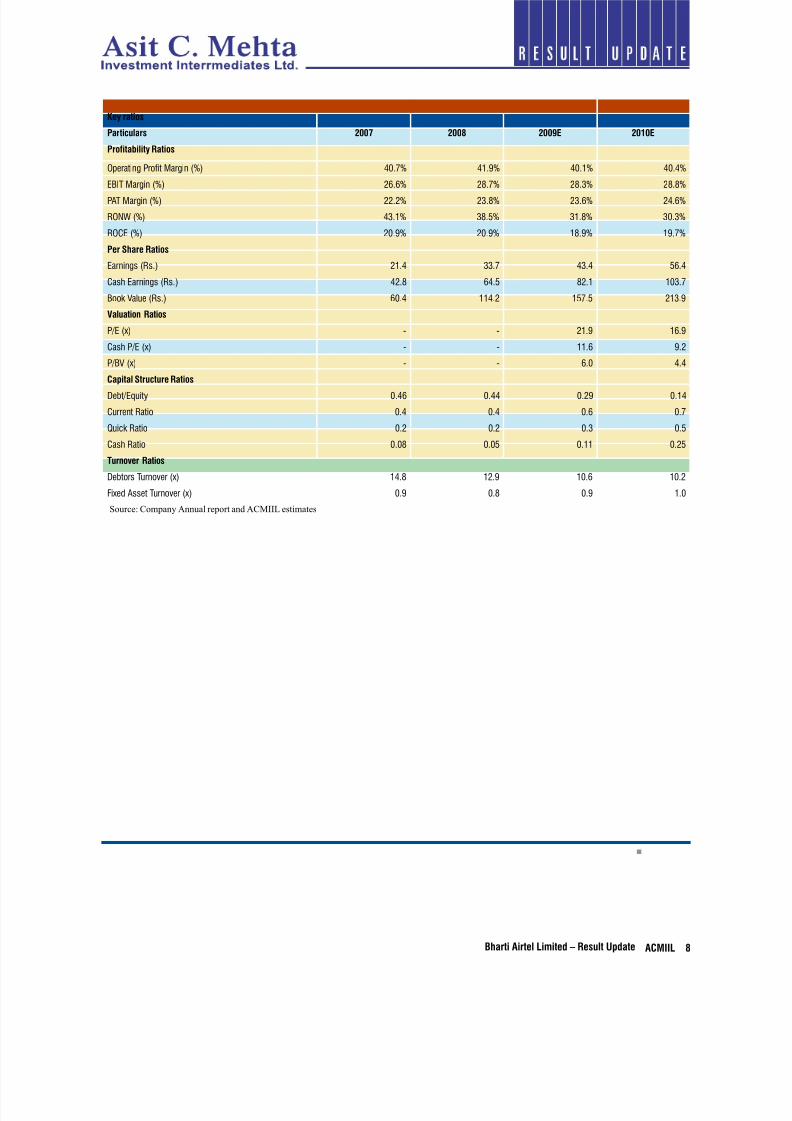

Key ratios

Particulars 2007 2008 2009E 200E

Profitability Ratios

Operating Profit Margin (%) 40.7% 41.9% 40.1% 40.4%EBIT Margin (%) 26.6% 28.7% 28.3% 28.8%

PAT Margin (%) 22.2% 23.8% 23.6% 24.6%

RONW (%) 43.1% 38.5% 31.8% 30.3%

ROCE (%) 20.9% 20.9% 18.9% 19.7%

Per Share Ratios

Earnings (Rs.) 21.4 33.7 43.4 56.4

Cash Earnings (Rs.) 42.8 64.5 82.1 103.7

Book Value (Rs.) 60.4 114.2 157.5 213.9

Valuation Ratios

P/E (x) - - 21.9 16.9

Cash P/E (x) - - 11.6 9.2

P/BV (x) - - 6.0 4.4

Capital Structure Ratios

Debt/Equity 0.46 0.44 0.29 0.14

Current Ratio 0.4 0.4 0.6 0.7

Quick Ratio 0.2 0.2 0.3 0.5

Cash Ratio 0.08 0.05 0.11 0.25

Turnover Ratios

Debtors Turnover (x) 14.8 12.9 10.6 10.2

Fixed Asset Turnover (x) 0.9 0.8 0.9 1.0

Source: Company Annual report and ACMIIL estimates

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 9/10Bharti Airtel Limited – Result Update ACMIIL 9

Year Adjusted Population

Figures (in mn) *

Total wireless

subscribers#

Adjusted Teledensity for

wireless subscribers

Bharti Subscribers Market Share for Bharti

2004 809 35 4.3 7 18.6

2005 822 55 6.7 11 20.0

2006 834 99 11.9 20 19.8

2007 846 166 19.6 37 22.4

2008 859 260 30.3 62 23.8

2009P 871 350 40.2 85 24.4

2010P 883 440 49.9 110 25.0

2011P 954 528 55.4 132 25.0

2012P 966 608 62.9 152 25.0

Source: Census India Report, Cris Infac & ACMIIL Research

*Adjusted for population that can afford mobile services# Wireless Subscribers include GSM, CDMA and WLL-F subscribers.

Mar-09 Mar-0 Mar- Mar-2 Mar-3 Mar-4 Mar-5 Mar- Mar-7 Mar-8

EBITDA 142900 179800 205286 215532 223432 240670 254839 254187 257983 256421

Tax 11817 15969 22376 24355 26588 30084 33894 35332 34828 34617

Capex 122500 105000 85000 74500 69500 64100 55200 51900 30200 29500

Change in NWC 15024 12370 19502 16812 14523 14681 14271 13218 14189 15129

FCF 23607 71201 117412 133489 141867 161167 180017 180173 207145 207433

Source: ACMIIL Estimate

Assumptions

Risk Free rate 8%

Beta 0.8

Risk Premium 6%

Cost of equity 12.6%

Cost of Debt 8.00%

Terminal growth rate 4%

WACC 10.8%

Valuations Amount (In Mn)

PV of cash flows 751182

PV of terminal value 1142342

Value 1893524

Net Debt (loan funds-Cash balance) 88983

Value of Equity 1804541

No of Shares 1898

Fair Value (Rs per share) 95

Source: ACMIIL Estimates

Annexure I : Bharti Airtel Limited (Subscriber Projections)

Annexure II : DCF Valuation for Bharti Airtel

8/6/2019 Bharti Airtel Ltd-Result Update

http://slidepdf.com/reader/full/bharti-airtel-ltd-result-update 10/10Bh ti Ai t l Li it d R lt U d t ACMIIL 0

Disclaimer:

This report is based on information that we consider reliable, but we do not represent that it is accurate or complete and it should not be relied upon such. ACMIIL or

any of its afliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the informationcontained in the report. ACMIIL and/or its afliates and/or employees may have interests/positions, nancial or otherwise in the securities mentioned in this report.

To enhance transparency we have incorporated a Disclosure of Interest Statement in this document. This should however not be treated as endorsement of the views

expressed in the report.

Notes:

HNI Sales:Raju Mewawalla, Tel: +91 22 2858 3220

Institutional Sales:Bharat Patel, Tel: +91 22 2858 3730Kirti Bagri, Tel: +91 22 2858 3731

Himanshu Varia, Tel: +91 22 2858 3732