big data - an actuarial perspective

TRANSCRIPT

Mateusz Maj Chairman of IABE

Big Data WG [email protected]

Big Data an actuarial perspective

1st IABE Big Data Forum

What is Big Data?

What is Big Data?

What is Big Data?

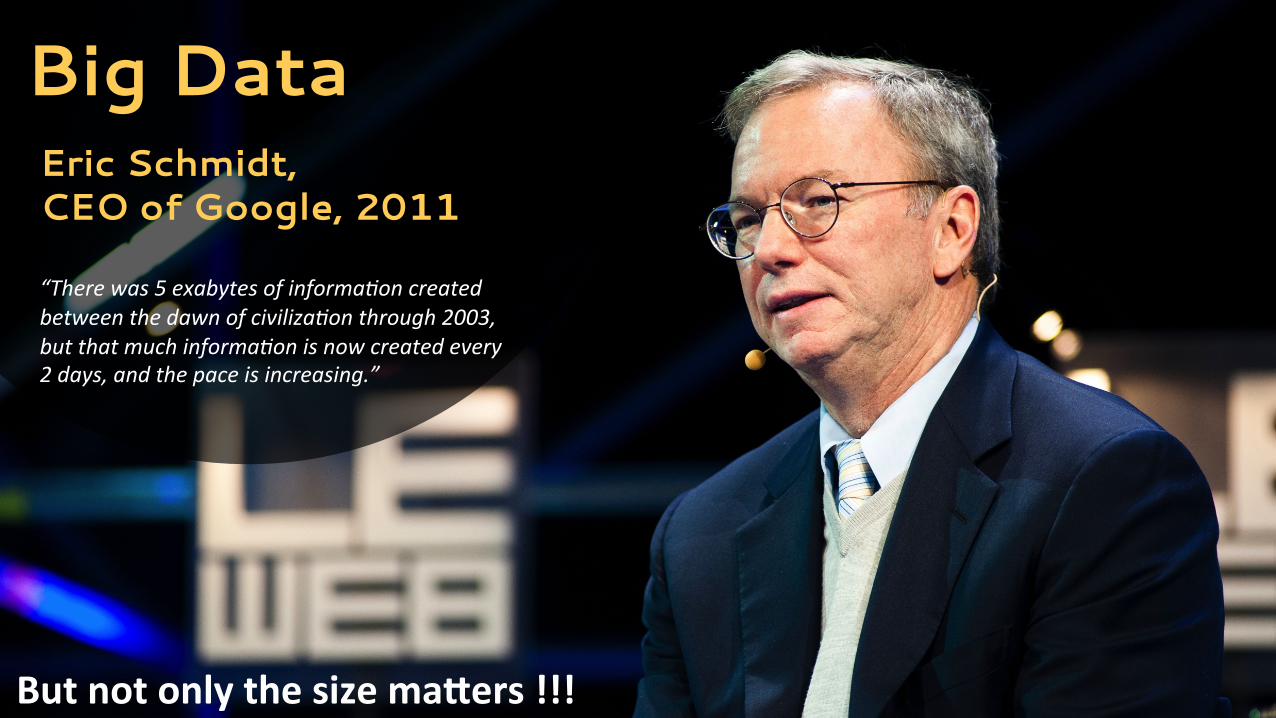

What is Big Data? Big Data Eric Schmidt, CEO of Google, 2011 “There was 5 exabytes of informa4on created between the dawn of civiliza4on through 2003, but that much informa4on is now created every 2 days, and the pace is increasing.”

But not only the size ma0ers !!!

Big Data WG Why?

Discuss:

• Impact of Big Data on insurance sector and the actuarial profession;

• Present challenges and good practices when working with Big Data;

• Educate actuarial profession about Big Data.

Big Data WG How?

• Big Data information paper ;

• Regular meetings with guest lecturers presenting different

aspects of Big Data, at least bi-monthly;

• Seminars;

• CPD courses – Big Data/Data science program – from 2016;

• Further technical notes on the topic.

Insurance value chain: undewriting Covers different

Underwriting

360 degree customer view

Combine different sources and apply analytics to

create comprehensive customer view and: • Maximize profitability of the current portfolio • Detect cross-sell and up-sell opportunities;

• Increase customer satisfaction and loyalty;

• Acquire new profitable customers and reduce marketing costs.

Underwriting

Underwriting Tesco group – UK

Motor – 1M Pet – 0.45M Travel - 0.175M Life – 0.175M Home – 0.4M

• Insurance prevention program with discounts and rewards for good

driving

• ‘Phased’ approach: • Phase 1: combine data from different sources i.e. traditional channels, online channels,

external service providers, Tesco group warehouses;

• Phase 2: Identify the right customers within Tesco network;

• Phase 3: Provide initial offer and reward drivers with initial rewards from Tesco group;

• Phase 4: Iterate and provide personalized insurance offers.

Underwriting making insurance sexy

Pricing

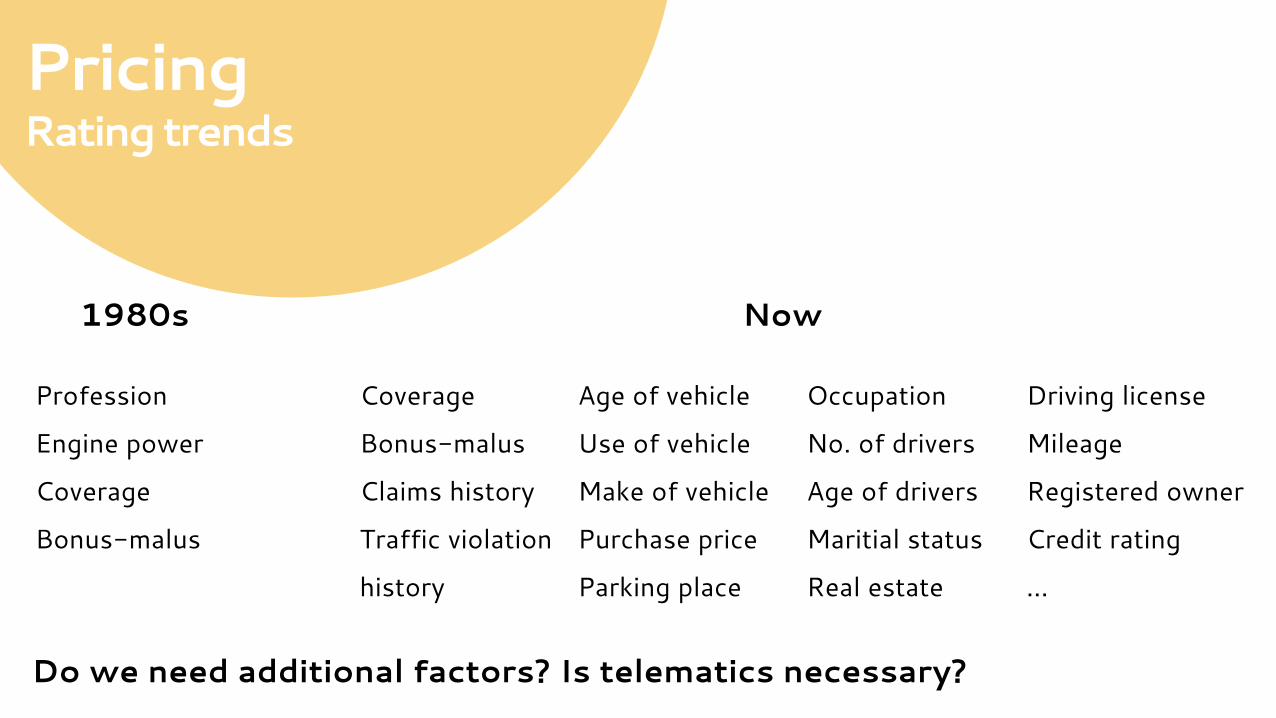

Pricing Rating trends

1980s Now

Profession

Engine power

Coverage

Bonus-malus

Coverage

Bonus-malus

Claims history

Traffic violation

history

Age of vehicle

Use of vehicle

Make of vehicle

Purchase price

Parking place

Occupation

No. of drivers

Age of drivers

Maritial status

Real estate

Driving license

Mileage

Registered owner

Credit rating

…

Do we need additional factors? Is telematics necessary?

Univariate

basis

Risk

modelling

Technical

premium

modelling

Scenario

testing

Price

optimisation

Extra data

sources

Telematics

data?

Pricing Rating trends

• New rating factors;

• Flexible, dynamic risk pricing;

• New modelling techniques like machine learning;

• New, disruptive insurance offerings like Usage-

Based Insurance.

Pricing

Pricing Usage-Based Insurance (UBI)

UBI is the scheme where insurance premiums are

calculated based on dynamic causal data, including

actual usage and riskier driving behavior.

Insurance value chain: undewriting Covers different

Claims management & Fraud detection

Insurers loose 5% of the annual revenue due to fraud

Coalition Against Insurance Fraud (US) in the 2014 report has

stresses that technology & Big Data plays a growing role in

fighting fraud

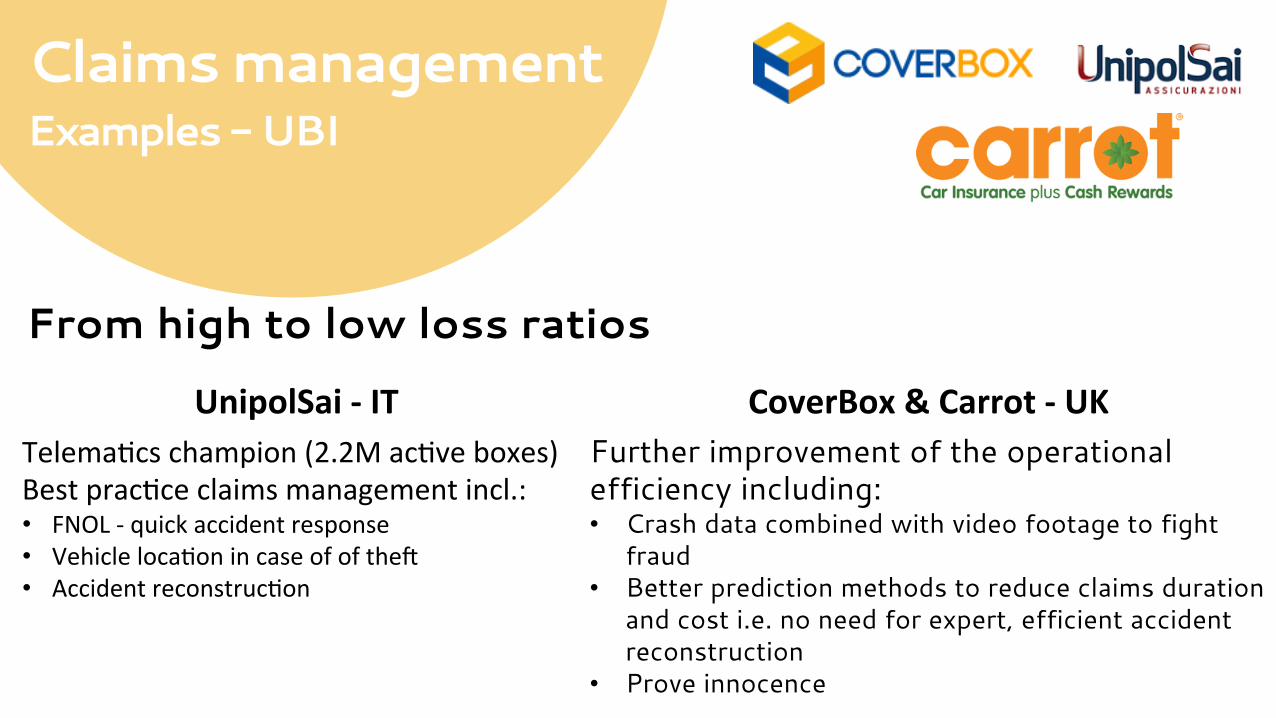

Claims management Examples - UBI

From high to low loss ratios

UnipolSai -‐ IT CoverBox & Carrot -‐ UK Telema'cs champion (2.2M ac've boxes) Best prac'ce claims management incl.: • FNOL -‐ quick accident response • Vehicle loca'on in case of of theG • Accident reconstruc'on

Further improvement of the operational efficiency including: • Crash data combined with video footage to fight

fraud • Better prediction methods to reduce claims duration

and cost i.e. no need for expert, efficient accident reconstruction

• Prove innocence

Covers different

Legislation

EU-wide law under construction

Innovation

Big Data can boost innovation

Why Change?

- Expensive customer acquisition

- Little contact with customer

- Low brand loyalty and retention

- Regulatory pressure …

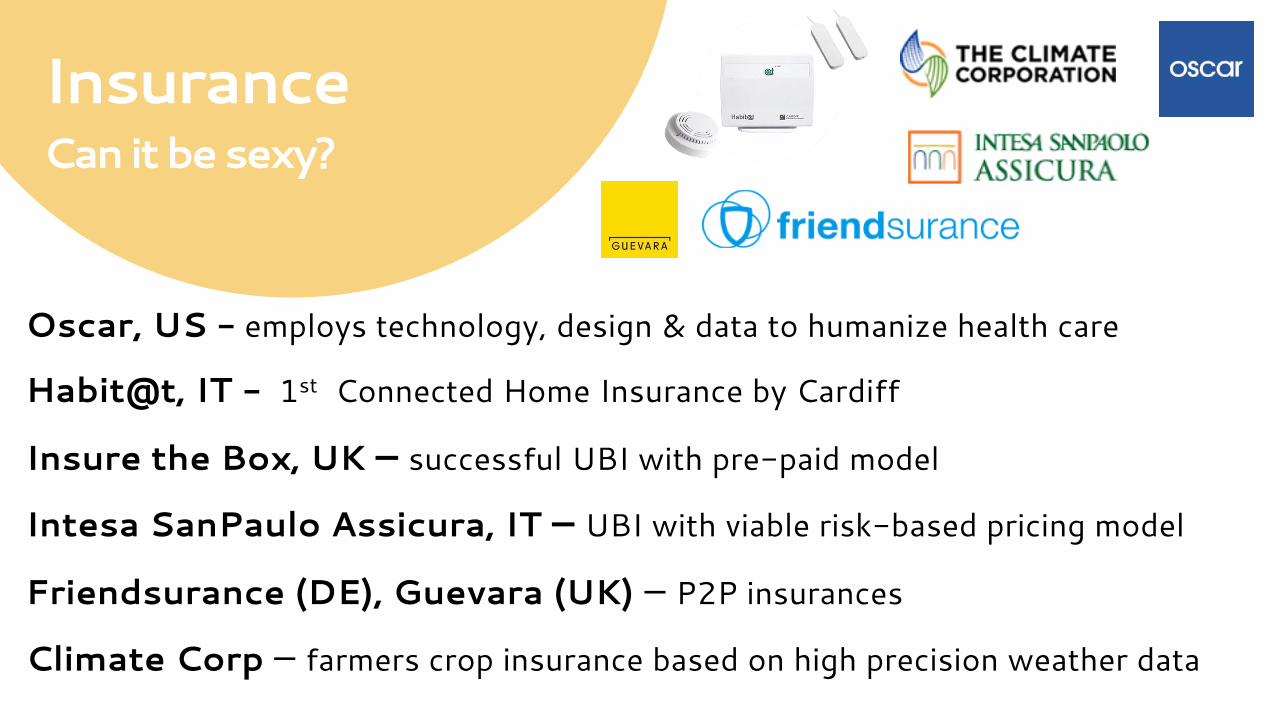

Insurance Can it be sexy?

Oscar, US - employs technology, design & data to humanize health care

Habit@t, IT - 1st Connected Home Insurance by Cardiff

Insure the Box, UK – successful UBI with pre-paid model

Intesa SanPaulo Assicura, IT – UBI with viable risk-based pricing model

Friendsurance (DE), Guevara (UK) – P2P insurances

Climate Corp – farmers crop insurance based on high precision weather data

EU-wide law under construction

Role of actuaries

Data scientists for insurers and beyond