billabong international limited

TRANSCRIPT

BILLABONG INTERNATIONAL LIMITED30 August 2010

Investor presentation highlights

2010$m

2009$m

2010Change %

Results in Constant Currency (AUD)

• Sales Revenue 1,482.3 1,482.6 (0.0)

• EBITDA 253.3 255.6 (0.9)

• NPAT (pre-impairment charge) 146.0 141.6 3.1

• NPAT (pre-acquisition transaction costs and pre-impairment charge)

148.7 141.6 5.0

• NPAT (post-impairment charge) 146.0 135.0 8.1

Results As Reported (AUD)

• Sales Revenue 1,482.3 1,669.1 (11.2)

• EBITDA 253.3 284.8 (11.1)

• EBITDA Margin 17.1% 17.1%

Earnings Per Share 58.3c 69.2c (15.8)

Return on Capital Employed 12.9% 15.7%

RESULTSFY10

RESULTSConstant Currency

Americas48%

Europe23%

Australasia29%

Sales FY10

Americas49%

Europe22%

Australasia29%

Sales FY09

Americas36%

Europe28%

Australasia35%

Global1%

EBITDA FY10

Americas34%

Europe26%

Australasia39%

Global1%

EBITDA FY09

2010$m

2009$m

2010Change %

Working Capital in Constant Currency (AUD)

• Net Working Capital 422.4 413.1 2.3

• % of 12 Months Sales stated at FY10 Year End Exchange Rates

28.3% 27.9%

Gearing Levels As Reported (AUD)

• Borrowings (net) 216.7 225.0 (3.7)

• Gearing Ratio (Net Debt / Net Debt + Equity) 15.1% 16.0%

• Interest Cover 12.6 times 7.1 times

• Borrowing Headroom 79% 69%

Cash Flow As Reported (AUD)

• Net cash receipts from customers and payments to third parties

252.1 258.6

• EBITDA 253.3 284.8

• Net cash receipts as a % of EBITDA 100% 91%

RESULTSFY10

EVOLUTIONof Billabong Group

Designer

Manufacturer

Wholesaler International

Domestic

Supply chain

Brand expansion

Licensee territories

Restructure and float

Present day

Retail

BUSINESS MODEL

Production and supply chain

Branding, marketing and merchandising

Third party wholesale*

Company owned retail*

Str

ateg

ic o

bjec

tive

s

Quality and stability

Unique design and product innovations

Control brand integrity

Consumer insights

Strong focused brands

Strengthen the distribution

channel

*% varies by market

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Summer

‐ Orders

‐ Deliveries

Hi‐summer

‐ Orders

‐ Deliveries

AUSTRALIAForward Orders

FINANCIAL METRICSGuiding principles for the business

Aspiration to achieve and maintain strong wholesale and retail EBITDA margins

Mid to high teen EBITDA margins in the medium term, following transition year

Ongoing improvements to pre-tax return on capital employed (ROCE) relative to the Group’s pre-tax cost of capital of approx. 12%

Return to industry leading ROCE in the medium term

Conservative gearing Gearing Ratio (Net Debt / Net Debt + Equity) < 30-35% over plan period

Maintenance of appropriate financing headroom

Available headroom 40-50% over plan period

BRANDSGrowth drivers

Existing Market Penetration

Brand Design & Marketing Innovation

New/ Emerging Market Development

New Category Growth

Brand market share varies significantly by Region

Significant potential to increase penetration of existing brands into the established channels

Emerging markets (Asia, S. America and E. Europe) are seeing strong growth in their middle class who will increasingly have the disposable income and leisure time to consider action sports

Most brands in the portfolio have potential to extend into new categories

Broader action sport and lifestyle segments hold further potential for Billabong

Fundamental to Billabong’s future growth is continued design and marketing innovation

BILLABONGWholesale Sales

0%10%20%30%40%50%60%70%80%90%

100%

Americas Europe Australasia Consol

Including Sales to Related Retail Excluding Pac Sun (Constant Currency)

FY08 FY09 FY10

ELEMENTWholesale Sales

0%

20%

40%

60%

80%

100%

120%

140%

Americas Europe Australasia Consol

Including Sales to Related Retail Excluding Pac Sun (Constant Currency)

FY08 FY09 FY10

NIXONWholesale Sales

0%

20%

40%

60%

80%

100%

120%

140%

160%

Americas Europe Australasia Consol

Including Sales to Related Retail (Constant Currency)

FY08 FY09 FY10

RETAILGrowth driver support

Controllable floor space supports all 4 key growth drivers for Billabong as well as enhancing the value of wholesale acquisitions

Controllable Floor Space (Partner Programs, Retail, Online)

Industry development

Space for exposure of wider range (particularly younger brands)

Direct consumer feedback Space for experimentation Volumes to support fast

fashion

Existing Market Penetration

Brand Design & Marketing Innovation

New/ Emerging Market Development

New Category Growth

Controlled brand exposure Replacement of lost surf

channel distribution as independents exit

Partner programs symbiotic with owned retail

Selective Acquisitions/ Alliances

Increase Vertical % and retail profitability

RETAILSpeed to market

RangeDevelop-

mentSell-in Production & Delivery

Trim, Samples, Fabric Sourcing

30 60 60 120

270

Range Develop

Production & Delivery

Trim, Samples,

Fabric

20 40 50

Range Develop

Production & Delivery

Trim, Samples,

Fabric

20 40

50

90

BBG Leadtime:

Required Time:

Typical Vertical Retailer:

Comparison of BBG vs. Typical Apparel Retailer Leadtimes

Retail provides the scale to short-circuit the current sell-in process to wholesalers for part of the range and deliver newranges in a comparable timeframe to vertical apparel retailers

Retail does not require the sell in process as long as retail planners are linked into wholesale design team

Range release schedule required for wholesale indent model is not relevant for retail

COMPANY RETAILJune/July 2010

44

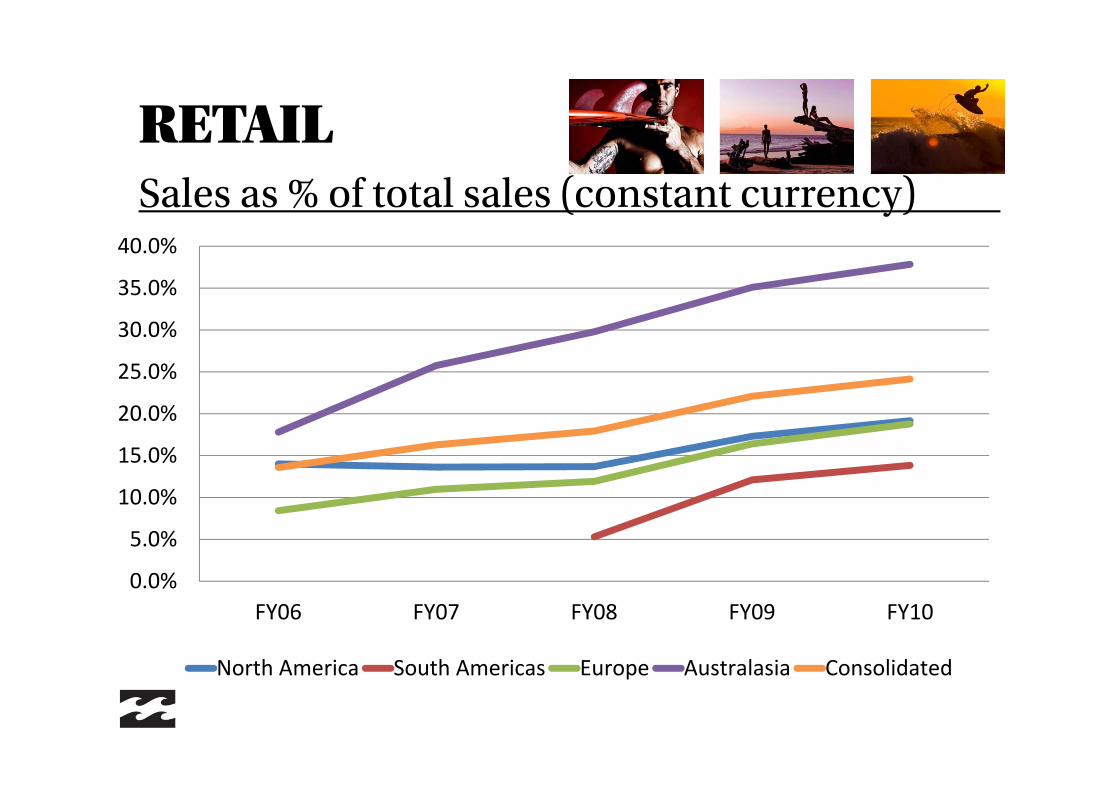

RETAILSales as % of total sales (constant currency)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY06 FY07 FY08 FY09 FY10

North America South Americas Europe Australasia Consolidated

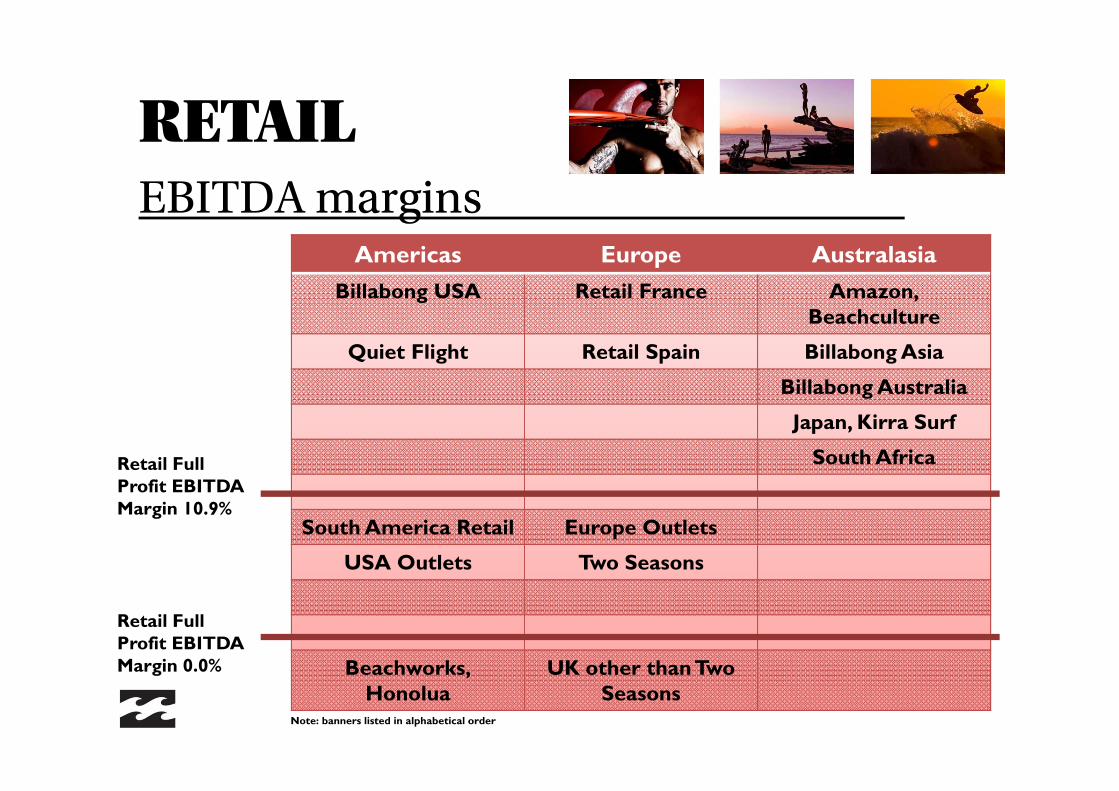

Americas Europe Australasia

Billabong USA Retail France Amazon,Beachculture

Quiet Flight Retail Spain Billabong Asia

Billabong Australia

Japan, Kirra Surf

South Africa

South America Retail Europe Outlets

USA Outlets Two Seasons

Beachworks,Honolua

UK other than Two Seasons

Retail Full Profit EBITDA Margin 10.9%

Retail Full Profit EBITDA Margin 0.0%

RETAILEBITDA margins

Note: banners listed in alphabetical order

RETAILFY10

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

NorthAmerica

SouthAmericas

Europe Australasia Consolidated

Retail Full Profit EBITDA Margin (Constant Currency)

RETAILFY10

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

NorthAmerica

SouthAmericas

Europe Australasia Consolidated

Retail Full Profit EBITDA Margin (Constant Currency)

Excluding Beachworks &

Honolua

Excluding Beachworks &

Honolua

RETAILFY10

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

NorthAmerica

SouthAmericas

Europe Australasia Consolidated

Retail Full Profit EBITDA Margin (Constant Currency)

Excluding Beachworks &

Honolua

Excluding Beachworks &

Honolua

Stores open more than 2yrs,

excluding Beachworks &

Honolua

NORTH AMERICA

North AmericaFY06

US$000sFY10

US$000s CAGRTotal Sales 362,650 554,435 11.20%

Sales ExclTop 5 231,274 441,399 17.54%

Top 5 Sales 131,376 113,037 -3.69%

PacSun incl. in Top 5 - down from $95 million to $36 million

RETAIL METRICSStore evaluation (2nd full-year after opening)

Full Profit EBIT Margin Target > 15%

Return on Capital Employed Target > 20%

IRR Target > 20%

NPV Must be positive assuming 20% discount rate

RETAILFull profit actual

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

35,000 35,500 36,000 36,500 37,000 37,500 38,000 38,500 39,000

FY09 FY10

Quiet Flight (US$000s)

Sales EBITDA

% BBG Family 61.0% 70.0%

ROCE 5.1% 10.9%

EBITDA Margin 8.6% 15.4%

RETAILFull profit actual

-

2,000

4,000

6,000

8,000

10,000

-

10,000

20,000

30,000

40,000

50,000

60,000

FY07 FY08 FY09 FY10

Amazon (NZ$000s)

Sales EBITDA

% BBG Family 25.0% 40.0% 50.0% 55.0%

ROCE 38.4% 42.6% 36.1% 34.9%

EBITDA Margin 21.4% 20.3% 18.6% 16.8%

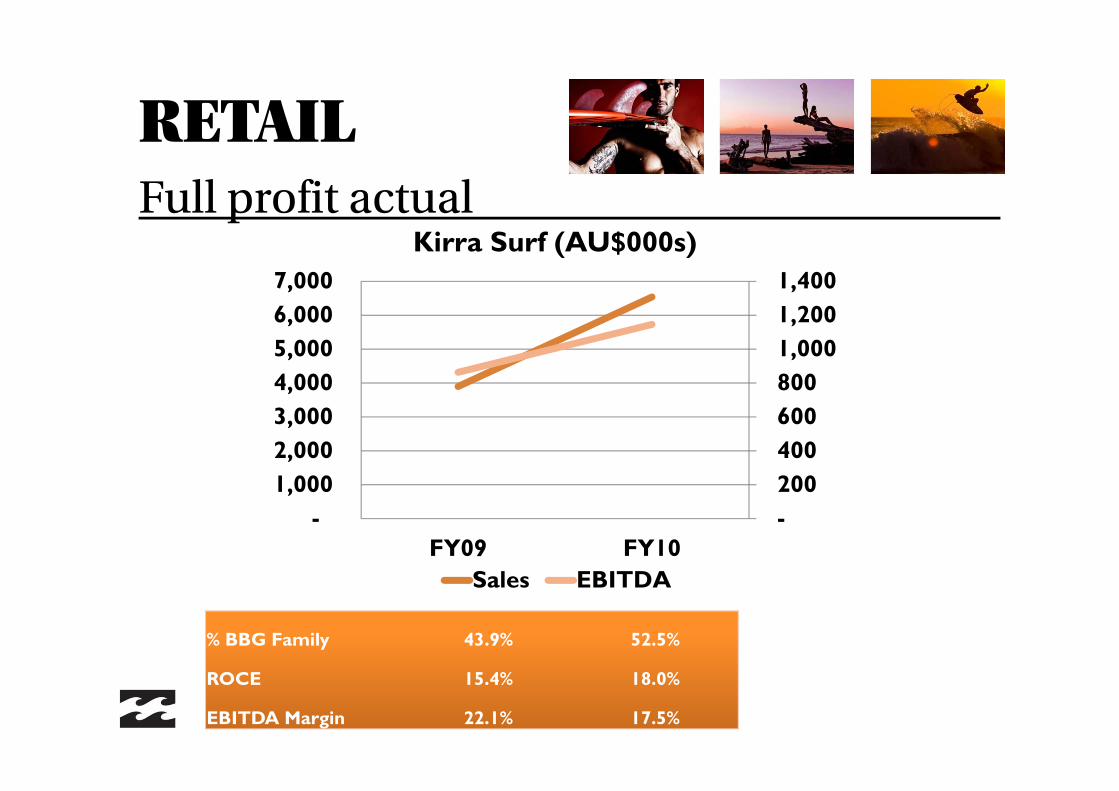

RETAILFull profit actual

- 200 400 600 800 1,000 1,200 1,400

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

FY09 FY10

Kirra Surf (AU$000s)

Sales EBITDA

% BBG Family 43.9% 52.5%

ROCE 15.4% 18.0%

EBITDA Margin 22.1% 17.5%

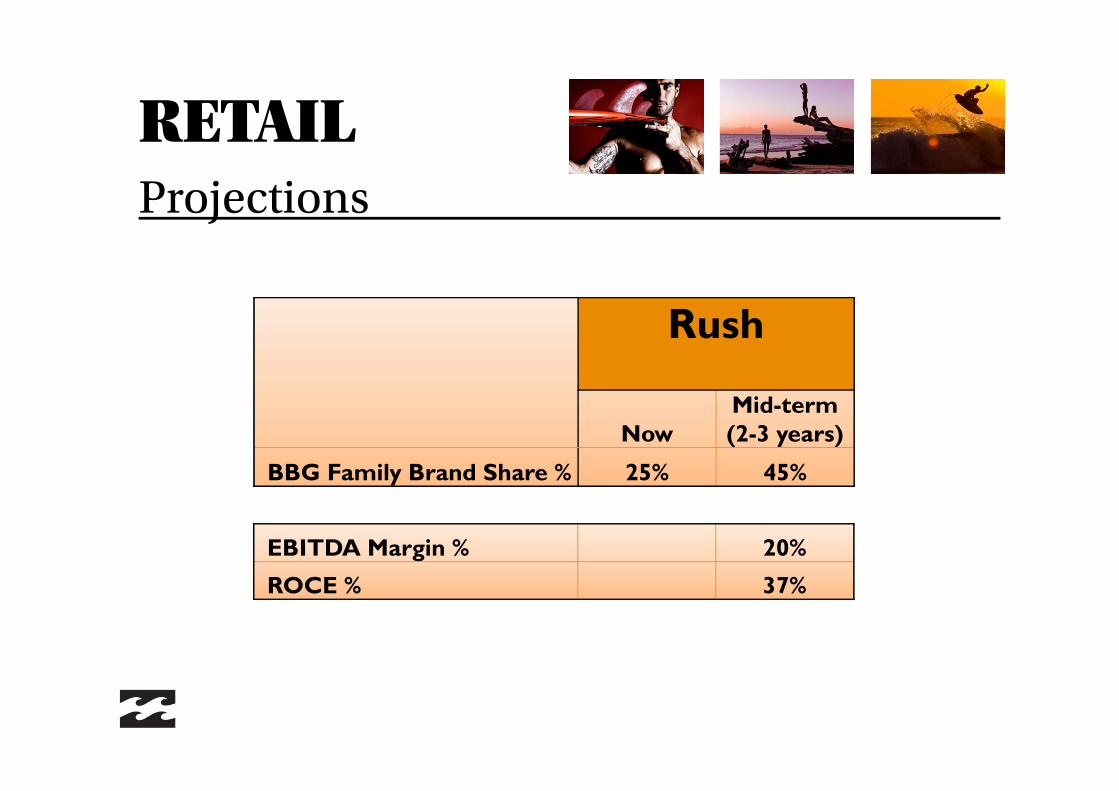

RETAILProjections

Rush

NowMid-term(2-3 years)

BBG Family Brand Share % 25% 45%

EBITDA Margin % 20%

ROCE % 37%

RETAILProjections

West 49

NowMid-term(2-3 years)

BBG Family Brand Share % 15% 45%

EBITDA Margin % 15%

ROCE % 25%

EVOLUTIONROCE impact

Retail Network

49 stores 64 stores110 stores

159 stores

242 stores

335 stores

510 stores*

* Pro forma store numbers

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

25.4% 22.6% 22.0% 15.7% 12.9%ROCE =

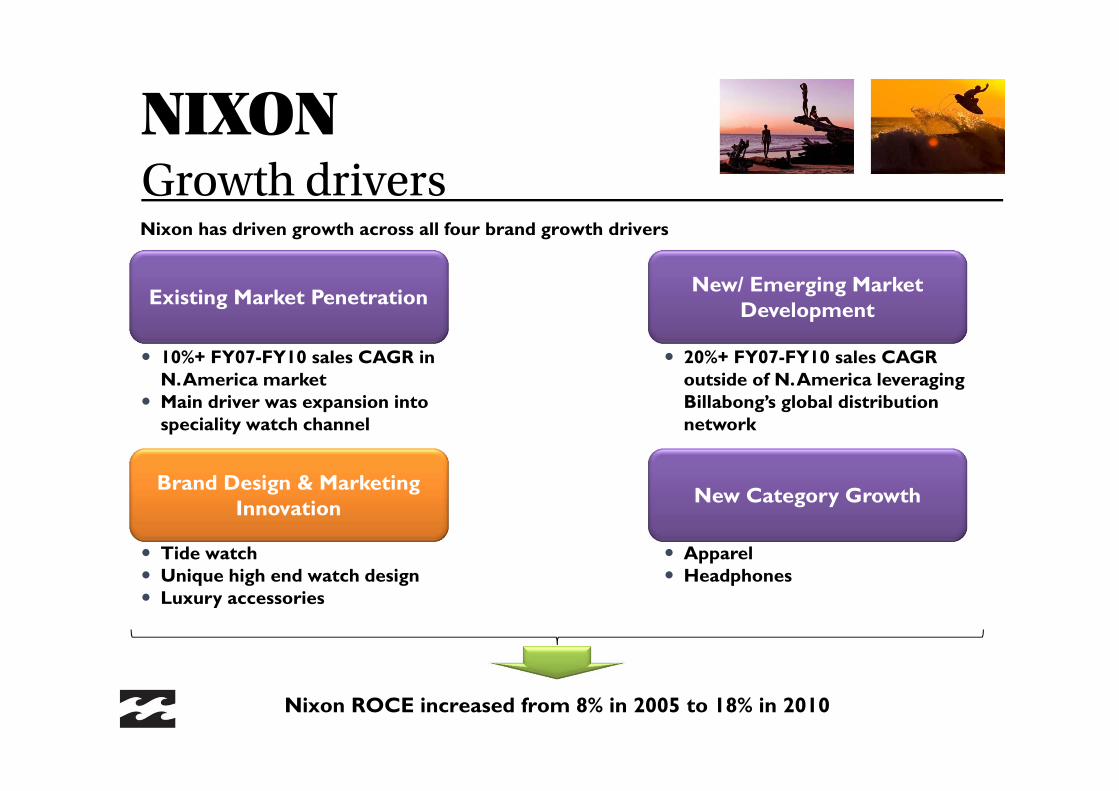

NIXONGrowth drivers

Existing Market Penetration

Brand Design & Marketing Innovation

New/ Emerging Market Development

New Category Growth

Nixon has driven growth across all four brand growth drivers

10%+ FY07-FY10 sales CAGR in N. America market

Main driver was expansion into speciality watch channel

20%+ FY07-FY10 sales CAGR outside of N. America leveraging Billabong’s global distribution network

Apparel Headphones

Tide watch Unique high end watch design Luxury accessories

Nixon ROCE increased from 8% in 2005 to 18% in 2010

ROCEHistorical view

• To ‘Inspire Youth’ through innovative and profitable retail concepts• Provide a controllable retail operational platform and distribution channel to

showcase our brands

Purpose:

RETAIL (AUS/NZ)Strategy

Guiding Principles:

• Create innovative, incomparable and profitable retail concepts that inspire youth• Attract and retain great retailers who are equally passionate about our organisation• Build strong Retail Brands by creating innovative and aspirational marketing with

authenticity and integrity • Superior customer clarity, insight and service through connecting/living the same

lifestyle• Operational excellence in all areas of our Retail business

Strategic objectives:

1. Build a “best in class” operational platform

3. Grow retail presence in bricks & mortar stores and online

4. Drive value from integrated wholesale/ retail model

2. Develop partner store program to protect independent channel

RETAIL (AUS/NZ)Improve operational capability