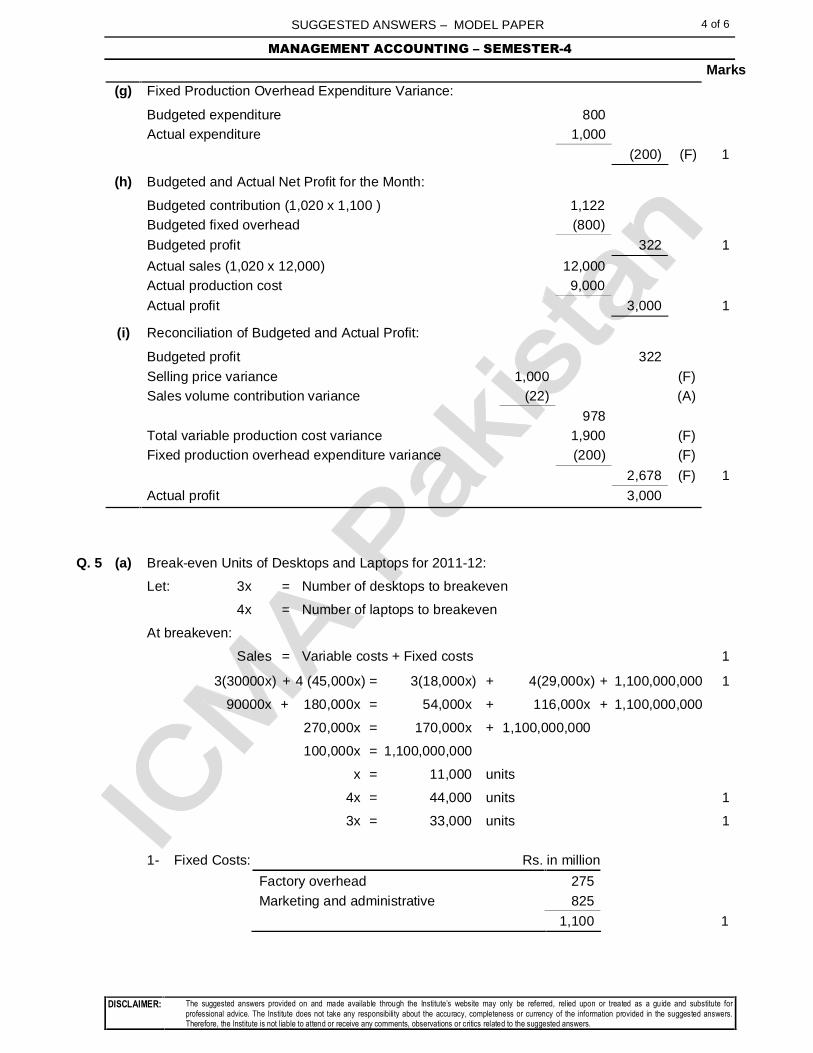

binder 1

DESCRIPTION

VTRANSCRIPT

RMA-MP 1 of 2 PTO (Note: The number of questions and their marks may vary in the examination paper)

ICMA.

Pakistan

MODEL PAPER

RISK MANAGEMENT AND AUDIT (BAF-502)

SEMESTER-5

Time Allowed: 3 hours Maximum Marks: 100 Roll No.:

(i) Attempt all questions.

(ii) Answers must be neat, relevant and brief.

(iii) In marking the question paper, the examiners take into account clarity of exposition, logic of arguments, effective presentation, language and use of clear diagram/ chart, where appropriate.

(iv) Read the instructions printed inside the top cover of answer script CAREFULLY before attempting the paper.

(v) Use of non-programmable scientific calculators of any model is allowed.

(vi) DO NOT write your Name, Reg. No. or Roll No., or any irrelevant information inside the answer script.

(vii) Question Paper must be returned to invigilator before leaving the examination hall.

Marks

Q. 1 (a) Milestone-dot-com is an online retailer, offers various electronic products including mobiles phones, televisions, refrigerators and microwave ovens on its website. Customers select their desired products and pay via credit cards. The system of revenue recording is complex as it involves information technology and company�s interface/ interlink for comprehensive operations.

Required:

On the basis of the information mentioned above, identify any six (06) risks which may be associated with the revenue and general operations of Milestone-dot-com and also describe the measures which can be taken to mitigate such risks. 12

(b) Risk identification is a continuous process so that new risks and changes affecting

existing risks may be identified before they can cause unacceptable losses. Discuss various means of identifying conditions leading to risks (potential sources of loss). 07

Q. 2 (a) Recent worldwide events of fraud have raised several questions over the role of external

auditors in relation to identification of fraud. Required: (i) Define the term �fraud� and describe any two major categories of fraud. 10

(ii) There are certain conditions that are generally present when fraud exists. Identify such conditions. 03

(b) As per the International Standards on Auditing, the assertions used by the auditor to

consider different types of potential misstatements that may occur, are divided into three categories. Briefly discuss the assertions about �classes of transactions and events for the period� under audit. 05

Q. 3 (a) Auditors are regulated by professional bodies and should follow recognized auditing standards such as International Standards on Auditing (ISAs). Explain why it is important that audit is to be conducted in accordance with auditing standards that are common to all audits? 05

RMA-MP 2 of 2 (Note: The number of questions and their marks may vary in the examination paper)

Marks (b) M/s. Farooq Enterprises, a trading company, has recently engaged M/s. APNG & Co.,

Chartered Accountants to audit its accounts for the year ended December 31, 2013. You are working as an Auditor of the firm and your Engagement Manager has given you a task to prepare the audit procedures for M/s. Farooq Enterprise for the test of control.

Required:

Discuss any six (06) audit procedures for M/s. Farooq Enterprise for the test of control of the following:

(i) Cash payment 06

(ii) Payroll 06 Q. 4 (a) Under ISA 501, when and how does the auditor design and perform audit procedures in

order to identify litigation and financial claims against the company? 04 (b) State the circumstances that necessitate direct communication of an external auditor

with the entity�s external legal counsel in respect of litigation and financial claims. Further, describe the matters which should be discussed in such a communication. 09

(c) State the situations where the auditor shall modify the opinion in the auditor�s report

during the course of performing audit procedures regarding litigation and claims of the entity. 05

Q. 5 ABC and Co., manufactures and sells consumer goods in local markets and it has in-house internal audit function led by a professional accountant. The company has appointed a CMA Firm as its external auditors. The management advised the Firm of external auditors to cooperate with the internal auditors to complete their audit in efficient manner and rely on certain work already performed by the internal audit function.

It was informed that the internal auditors provide the following services to the company:

(i) A periodic audit of the operation of internal controls in the company�s major functions (operations, finance, customer support and information services);

(ii) Annual review of the structure of internal controls in each major function of the company;

(iii) An annual review of the effectiveness of measures put in place by the management to minimize the major risks facing the company.

During the current year, the company has gone through a major internal restructuring in its information services function and the internal auditors have been closely involved in the preparation of plans for restructuring, and in the related post-implementation review.

Required: (a) Describe the information that external auditors will seek from the internal auditors of

ABC and Co., in order to determine the extent of their reliance. 06

(b) Under what circumstances and in which major areas would it be necessary for the

external auditor to perform his own work in addition to relying on the work performed by internal auditor of the company? 07

Q.6 (a) Describe the key aspects that a cost auditor should consider at the planning stage while employing the personnel for cost audit. 08

(b) Briefly narrate the criteria laid down for ineligibility in relation to appointment of the cost

auditor under Rule 3(4) of the Companies (Audit of Cost Accounts) Rules, 1998. 07

THE END

SUGGESTED ANSWERS � MODEL PAPER 1 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q.1 (a) Risk Associated with Revenue and General Operations: (Any six @ 1 mark each) 06

(i) The system may get hang and the payment made might not reflect in Milestonedotcom Account.

(ii) The bank�s system may not be able to reconcile the total transactions against the revenue generated by Milestonedotcom.

(iii) The collection staff may not claim on timely basis the funds from the relevant Bank.

(iv) The revenue earned by Milestonedotcom could be from the credit card hacked by the User.

(v) Available inventory for sale may not be updated on timely basis.

(vi) The web-link may remain down without timely intimation/knowledge of the management.

(vii) Item bought on the net, may not be delivered timely on customers given address.

(viii) I.T protocols for the operation may not be adhered, hence resulting in any sort of virus/hacking of the System.

Measures to Manage the Risk of Revenue and General Operations: (Any six @ 1 mark each):

06

Revenue:

(i) An automated alert system should be installed in the system which confirms the receipt of funds from credit card.

(ii) Daily reconciliation with the Bank should be obtained & monitored.

(iii) All funds receipt should be checked against on-line sales on daily basis.

(iv) CNIC &/or PIN based verification of customer system should be installed in the System.

(v) Inventory should be updated on line against the placed orders on real time basis.

(vi) A real time system needs to be installed which should automatically triggers any alert relating to system downtime.

(vii) On daily basis the customer�s receipt note should be cross matched/checked against the deliveries made.

(viii) A recommended anti virus should be installed that could have features to safe guard the system.

(b) Risk Conditions: (1 mark each) 07

Means of identifying conditions leading to risks (potential sources of loss) include:

(a) Physical inspection, which will show up risks such as poor housekeeping (for example rubbish left on floors, for people to slip on and to sustain fires)

(b) Enquiries, from which the frequency and extent of product quality controls and checks on new employees� reference, for example, can be ascertained.

(c) Checking a copy of every letter and memo issued in the organization for early indications of major changes and new projects.

(d) Brainstorming with representatives of different departments.

(e) Checklists ensuring risk areas are not missed.

(f) Benchmarking against other sections within the organization or external experiences.

(g) Human reliability analysis, reviewing decision points within operational processes.

SUGGESTED ANSWERS � MODEL PAPER 2 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q.2 (a) (i) Fraud:

An intentional act by one or more individuals among management, those charged with governance, employees, or third parties, involving the use of deception to obtain an unjust or illegal advantage.

There are two types of fraud relevant to auditor�s consideration: i) Misappropriation of assets and ii) fraudulent financial reporting.

Misappropriation of assets:

Misappropriation of assets involves the theft of an entity's assets and is often perpetrated by employees in relatively small and immaterial amounts. However, it can also involve management who are usually more able to disguise or conceal misappropriations in ways that are difficult to detect. Misappropriation of assets can be accomplished in a variety of ways including:

a) Embezzling receipts (for example, misappropriating collections on accounts receivable or diverting receipts in respect of written-off accounts to personal bank accounts).

b) Stealing physical assets or intellectual property (for example, stealing inventory for personal use or for sale, stealing scrap for resale, colluding with a competitor by disclosing technological data in return for payment).

c) Causing an entity to pay for goods and services not received (for example, payments to fictitious vendors, kickbacks paid by vendors to the entity's purchasing agents in return for inflating prices, payments to fictitious employees).

d) Using an entity's assets for personal use (for example, using the entity's assets as collateral for a personal loan or a loan to a related party).

Misappropriation of assets is often accompanied by false or misleading records or documents in order to conceal the fact that the assets are missing or have been pledged without proper authorization.

Fraudulent financial reporting:

Fraudulent financial reporting involves intentional misstatements including omissions of amounts or disclosures in financial statements to deceive financial statement users. It can be caused by the efforts of management to manage earnings in order to deceive financial statement users by influencing their perceptions as to the entity's performance and profitability. Such earnings management may start out with small actions or inappropriate adjustment of assumptions and changes in judgments by management. Pressures and incentives may lead these actions to increase to the extent that they result in fraudulent financial reporting. Such a situation could occur when, due to pressures to meet market expectations or a desire to maximize compensation based on performance, management intentionally takes positions that lead to fraudulent financial reporting by materially misstating the financial statements. In some entities, management may be motivated to reduce earnings by a material amount to minimize tax or to inflate earnings to secure bank financing.

Fraudulent financial reporting may be accomplished by the following:

a) Manipulation, falsification (including forgery), or alteration of accounting records or supporting documentation from which the financial statements are prepared.

b) Misrepresentation in, or intentional omission from, the financial statements of events, transactions or other significant information.

c) Intentional misapplication of accounting principles relating to amounts, classification, manner of presentation, or disclosure.

02

04

04

SUGGESTED ANSWERS � MODEL PAPER 3 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Fraudulent financial reporting often involves management override of controls that otherwise may appear to be operating effectively.

(ii) The risk factor related to fraudulent financial reporting and misappropriation of assets are classified based on the three conditions that are generally present when fraud exists:

An incentive or pressure to commit fraud

A perceived opportunity to commit fraud and

An ability to rationalize the fraudulent action.

01

01

01

(b) Assertions used by the auditor to consider the different types of potential misstatements that may occur fall into the following three categories and may take the following forms: (a) Assertions about classes of transactions and events for the period under audit:

a. Occurrence: transactions and events that have been recorded have occurred and pertain to the entity.

b. Completeness: all transactions and events that should have been recorded have been recorded.

c. Accuracy: amounts and other data relating to recorded transactions and events have been recorded appropriately.

d. Cutoff: transactions and events have been recorded in the correct accounting period.

e. Classification: transactions and events have been recorded in the proper accounts.

01

01

01

01

01

Q.3 (a) Importance of Auditing Standards:

A variety of stakeholders might read a company�s financial statements. Some of these readers will not just be reading a single company�s financial statements, but will also be looking at those of a large number of companies and making comparisons, and making comparisons between them.

05

It is important that the audit profession is regulated and that auditors follow the same standards because many of these readers want assurance that when making comparisons, the reliability of the financial statements does not vary from company to company.

The assurance will be obtained not just from knowing that each set of financial statements has been audited, but from knowing that this has been done in accordance with common standards.

(b) (i) Tests of Controls � Cash Payments: (Any six @ 1 mark each)

1. Compare payments with paid cheques.

2. Verify that cheques signatories are authorized.

3. Check payments with suppliers� invoices and other supporting.

4. Test sequence of cheque numbers.

5. On a test basis, reper form reconciliation.

6. Verify that reconciliations are prepared and reviewed independently, throughout the period.

7. Inspect reconciliations for long outstanding items.

8. Check petty cash payment with supporting documents.

06

SUGGESTED ANSWERS � MODEL PAPER 4 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

9. Check that supporting documents have been marked �paid� to avoid misuse.

10. Observe security arrangements for cheque books.

(ii)Tests of Controls-Payroll: (Any six @ 1 mark each)

1. Check that payroll summary is approved.

2. Check that controls over payments to joiners and leavers are independently applied.

3. Test accuracy of computation of wages and salaries.

4. Check authorization of rates of pay.

5. Check hours with production records, time sheets and other evidence for hours worked.

6. Observe pay out of wages to ensure that control procedures are being followed.

7. Examine receipt given by the employee.

8. Check reconciliation of payroll with previous month�s records, clock cards, time sheets and job cards.

9. Check additions of the payroll summary.

10. Check that payments to tax authorities are accurate.

06

Q.4 (a) Designing and Performing Audit Procedures to Identify Litigation and Claims:

The auditor shall design and perform audit procedures in order to identify litigation and claims involving the entity when such matters give rise to a risk of material misstatement. This exercise is carried out by:

(i) Inquiry of management and, where applicable, others within the entity, including in-house legal counsel;

(ii) Reviewing minutes of meetings of those charged with governance and correspondence between the entity and its external legal counsel; and

(iii) Reviewing legal expense accounts.

04

(b) Direct Communication with the Entity�s External Legal Counsel:

If the auditor assesses a risk of material misstatement regarding litigation or claims that have been identified, or when audit procedures performed indicate that other material litigation or claims may exist, the auditor shall, in addition to the procedures required by other International Standards on Auditing, seek direct communication with the entity�s external legal counsel.

The auditor shall do so through a letter of enquiry, prepared by management and sent by the auditor, requesting the entity�s external legal counsel to communicate directly with the auditor. If law, regulation or the respective legal professional body prohibits the entity�s external legal counsel from communicating directly with the auditor, the auditor shall perform alternative audit procedures.

09

The matters which should be discussed in a letter to the legal counsel should include.

1- Legal cases in progress.

2- Current status of each significant legal case.

3- The legal counsel assessment of the possible outcome of each legal case.

4- Incase of a possibility of a company loosing a case, the potential financial impact.

5- Any penalty / fines/ damages imposed on the company which the legal counsel is aware of.

SUGGESTED ANSWERS � MODEL PAPER 5 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

(c) Modification of the Opinion in the Auditor�s Report Regarding Litigation and Claims:

The auditor shall modify the opinion in the auditor�s report in accordance with ISA 705 when:

(i) The management of the entity refuses to give the auditor permission to communicate or meet with the entity�s external legal counsel, or the entity�s external legal counsel refuses to respond appropriately to the letter of enquiry, or is prohibited from responding; and

(ii) The auditor is unable to obtain sufficient appropriate audit evidence by performing alternative audit procedures.

05

Q.5 (a) Information that External Auditors Seek from the Internal Auditors in order to Determine the Extent of their Reliance: (any six points)

Records detailing the qualifications and experience of internal audit staff:

Procedure manuals setting out the organization�s quality control standards for internal audit and evidence that this is monitored and reviewed.

For the periodic audit of the operation of internal controls working papers showing:

That the work is adequately planned, executed and reviewed

The results of tests of controls particularly in respect of financial and information systems.

06

For the restructuring of the information services function:

Documentation showing the way in which the restructure was planned and the basis on which decisions were made.

The results of the post-implementation review.

Any documents relating to this function prior to the changes (as part of the year would have been based on the old system).

For the review of the structure of internal controls the most recent report produced to determine how up-to-date the information is.

For the annual review of risk management measures working papers showing:

Planning of this work

Results of key tests performed (controls, substantive)

Key conclusions

Management responses.

(b) Circumstances and major areas where it is necessary for the external auditor to perform his own work in addition to relying on the work performed by internal auditor:

It will be necessary for the external auditor to perform his own work in the following circumstances:

Where balances are material to the financial statements: This is because the external auditor cannot delegate responsibility for the audit opinion. The external auditor needs sufficient appropriate evidence on which to form his opinion and auditor generated evidence is the most reliable.

07

SUGGESTED ANSWERS � MODEL PAPER 6 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

In areas of increased risks: this will include areas where complex accounting treatments are involved or where judgment is required. In this instance inventory valuation is likely to be a risk area, as well as being material. Leasing transactions may also be complex and will therefore require independent appraisal by the external auditor.

Where the objectives of the internal audit work differ from those of the external auditor: The roles of the internal and external auditor are very different. In some instances while the internal auditor may have done some work on a particular area the approach taken may not be adequate for the purposes of expressing an opinion on truth and fairness. This particularly the case where the internal audit department concentrates on operational aspects rather than matters which affect the financial statement.

As regards particular areas where the External Auditor may perform his own work rather than solely rely on the Internal Auditor, this would vary from entity to entity. Below are some examples that highlight when an External Auditor may perform his own work in addition to considering the tasks performed by the Internal Auditor.:

In a manufacturing concern, inventory is likely to always be an area of high risk of material misstatement. In such an instance, whilst the external auditor may rely to some extent on the stock count exercise attended by the internal auditor as regards Existence Assertion, they may still want to review the Valuation Assertion of the inventory themselves by obtaining and critically analyzing the aged stock movement.

Further, in case of an audit of financial institutions, the external auditor may rely on the internal auditor�s work regarding Existence Assertion of loans and advances, they would nevertheless want to evaluate the recoverability of each significant/ material loan advanced to major customers to assess whether it has been valued appropriately in the statement of financial position.

In service sector organizations, the �percentage completion method� is sometimes used to determine Revenue. The external auditor is almost always going to consider risk of improper revenue recognition on the higher side and therefore it is likely that he would perform cut-off procedures on revenue himself rather than rely on the work performed by the Internal Auditor.

Q.6 (a) Key Aspects for a Cost Auditor for Employing Personnel: (2 marks each)

(i) Qualification:

Cost audit work is to be assigned to personnel who have the degree of technical training and proficiency required in the circumstances. The personnel needs should be planned, keeping in view the staffing and timing requirements of specific cost audit.

Qualifications of personnel as to experience, position, background and special expertise should be evaluated. Care should be exercised not to assign any staff who may have any disqualifying relationship. The following aspects of personnel are also to be considered:

(ii) Experience:

Experience and training of cost audit personnel should be considered, particularly keeping the relevant industry in view, as the cost and management accounting procedures and techniques considerably differ on the basis of the nature and type of industry. Earlier cost audit or other practical experience of the industry helps in carrying out cost audit of a unit of that industry.

08

SUGGESTED ANSWERS � MODEL PAPER 7 of 7 RISK MANAGEMENT AND AUDIT � SEMESTER-5

MARKS

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

(iii) Directions:

Assistants to whom work is to be delegated need appropriate direction and supervision. Direction involves informing assistants of their responsibilities and the objective of the procedures they are to perform.

It includes informing them about the nature of the industry, possible cost accounting and auditing problems that may affect the cost audit routine and the procedures that they are to perform. The cost audit program, in providing the time budget and the overall audit plan, should also prove helpful in providing necessary audit directions.

(iv) Supervision:

Supervision involves both direction and review of audit work. Personnel carrying out supervisory responsibilities generally perform functions like monitoring the progress during the cost audit, assessing the level of competence and skill of the audit personnel, execution of cost audit in accordance with the overall cost audit plan.

(b) Criteria for Ineligibility of Cost Auditor:

The persons ineligible for appointment as Cost Auditor have been specified in sub-rule 4 of Rule 3 of the Companies (Audit of Cost Accounts) Rules, 1998. Following persons are ineligible for appointment as cost auditor:

(i) The same accountant or accounting firm, who has been appointed as an auditor of the Company, under Section 252 of the Companies Ordinance 1984 shall not be appointed as a cost auditor. A financial or corporate auditor of a company, therefore, shall not be appointed as a cost auditor of the same company at the same time. Accountants who are already acting as auditors of financial statements of a company shall not be appointed as cost auditors of the same company.

(ii) A person who is, or has been at any time during the preceding three years, a director, officer or employee of the company shall not be appointed as cost auditor.

(iii) A person who is a partner of a director, officer or employee of the company; or an employee of a director, officer or employee of the company shall not be appointed as a cost auditor. The cost auditor cannot be a partner or an employee of any director, officer or employee of the company.

(iv) A spouse of a director of the company shall not be appointed as a cost auditor of that company.

(v) A person who is indebted to the company for any amount at the relevant time.

(vi) A corporate body shall not be appointed as a cost auditor. A cost auditor, therefore, has to be an individual or a firm, and not a corporate body.

07

THE END

CLSP-MP 1 of 3 PTO (Note: The number of questions and their marks may vary in the examination paper)

ICMA.

Pakistan

MODEL PAPER

CORPORATE LAWS AND SECRETARIAL PRACTICES (BLE-403)

SEMESTER-4

Time Allowed: 02 Hours 30 Minutes Maximum Marks: 70 Roll No.:

(i) Attempt all questions.

(ii) Answers must be neat, relevant and brief.

(iii) In marking the question paper, the examiners take into account clarity of exposition, logic of arguments, effective presentation, language and use of clear diagram/ chart, where appropriate.

(iv) Read the instructions printed inside the top cover of answer script CAREFULLY before attempting the paper.

(v) DO NOT write your Name, Reg. No. or Roll No., or any irrelevant information inside the answer script.

(vi) Question Paper must be returned to invigilator before leaving the examination hall.

Marks

Q.1 The first question printed separately comprises 30 MCQs of one (1) mark each having allowed time of 30 minutes is an integral part of this question paper.

Q.2 You have been working as a Corporate Consultant for M/s. Carlton Limited which is a public

limited company, established in 1983. The Board of Directors is seeking your advice in respect of the following matter:

The financial year of the company ended on June 30, 2013 and its annual general meeting was scheduled to be held on 25th October, 2013 at 12:30 p.m. There were 8 ordinary shareholders present including 3 joint shareholders, Mr. Waqar, Mr. Saleem and Mr. Shafique (all ordinary shareholders representing 25% voting power including joint shareholders) and two preference shareholders holding 10% preference shares capital. The number of shareholders turned up in the next 10 minutes and the meeting started at 12:45 p.m., after meeting quorum requirements.

The matter relating to increase in authorized capital was debated threadbare and it was decided to carry out a voting by show of hands. Shareholders raised a number of objections during the meeting and the Board of Directors of the company request you to explain the legal provisions to the shareholders for the following objections:

Required:

(a) Some of the shareholders said that since the meeting was not started on scheduled time therefore this is invalid. The shareholders who were present in time objected that they were present in time and should have been considered as quorum. Explain the legal position with respect to shareholder�s objection and also mention the Law relating to adjournment of AGM and quorum requirements with particular reference to presence of preference shareholders and joint holders. 07

(b) Mr. Waqar, Mr. Saleem and Mr. Shafique, three brothers and joint shareholders of the

company were also present in the meeting. Mr. Saleem objected that why the notice of the meeting was sent to only one of them i.e., Mr. Waqar only and not to all three brothers including himself, Mr. Waqar and Mr. Shafique? 02

(c) There was a conflict between Mr. Waqar, Mr. Saleem and Mr. Shafique as to whose

vote would be considered for show of hand. Would your answer be different, if a poll was demanded instead of voting by show of hands? 03

CLSP-MP 2 of 3 (Note: The number of questions and their marks may vary in the examination paper)

Marks Q.3 (a) M/s. Hilton Petroleum Limited is a public limited company, listed on all three stock

exchanges Karachi, Lahore and Islamabad. The annual general meeting of the company was scheduled to be held on 30th September, 2013 at its Head Office situated in Karachi. After conclusion of the meeting some of the shareholders appear to be dissatisfied. Four of them, each holding 1% of the ordinary share capital gathered at a corner and started a discussion. One of the employees working in the company�s legal department over heard them saying that they were planning to go to the court challenging AGM�s proceedings on the following grounds:

The lunch arrangements made by the company were not proper.

There was some defect in the appointment of one of the directors and therefore his decision at the BOD meeting was not valid.

The Chairman called Mr. Ahmed, a Company Secretary to explain the following:

Required:

(i) Legal provisions relating to, challenge of AGM�s proceeding in the court. 05

(ii) Validity of the act of the Director, if the defect in the appointment is discovered. 03 (b) As per the Single Member Companies Rules, 2008 briefly state the rule for transfer of

shares of a single member. Under what circumstances these shares can be transferred to two or more persons? 03

Q. 4 As per provisions contained in the Companies (Issue of Capital) Rules, 1996 answer the

following:

Required:

(a) List down any five items which are not included in computation of �free reserves�. 06 (b) Specify any five conditions to be complied with by a listed company for issuing right

shares. 10 Q.5 A listed company intends to purchase its own shares and therefore considering the relevant

provisions of the Companies Ordinance, 1984 and the Companies (Buy-Back of Shares) Rules, 1999. Briefly describe the legal provisions for the following in respect of the above:

Required:

(a) Enumerate the contents of statement accompanied with notice of the shareholders meeting for passing special resolution for purchase of its own shares by the company. 05

(b) List down any seven contents to be included in the offer by a shareholder interested to

sell his shares to the company in response to the tender. 07 Q. 6 (a) Define the term �Housing Finance Services� as per the Non-Banking Finance

Companies (Establishment and Regulation) Rules, 2003. 03

(b) Explain the legal provisions under the Non-banking Finance Companies

(Establishment and Regulations) Rules, 2003 for opening or closure of bank accounts and account with a broker or branches of NBFC. 04

CLSP-MP 3 of 3 PTO (Note: The number of questions and their marks may vary in the examination paper)

Marks Q. 7 (a) Ms. Ambreen is the Secretary of Moon-Light Company Limited which is a listed

company. The Chief Executive has asked you to draft Statement of Compliance with the Code of Corporate Governance for inclusion in the annual report, 2012.

Required:

(i) Draft the opening paragraph for inclusion in the above statement. 02

(ii) Draft any four statements relating to directors/board of directors for inclusion in the above statement. 08

(b) When a listed company is required to determine a �closed period� as per the Code of

Corporate Governance? Discuss the restrictions imposed on the director and chief executive officer regarding dealing in the shares of the listed company during closed period. 02

THE END

1

.

SUGGESTED ANSWERS � MODEL PAPER 1 of 5

CORPORATE LAWS AND SECRETARIAL PRACTICES � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q.2 (a) Quorum of the AGM:

The AGM held at 12:45 p.m. is valid, as per the Ordinance, if within half an hour

from the time appointed for the meeting, a quorum is not present, the meeting

may either be dissolved or adjourned. Since the quorum was present within 30

minutes, the meeting is valid.

Regarding quorum of public listed company, 10 members present personally

representing not less than twenty-five per cent of the total voting power either of their

own account or as proxies or higher number provided in Articles of Association, form

quorum.

In the given situations there were ten shareholders present eight ordinary shareholders

including three joint shareholders and two preference shareholders.

Preference shareholders cannot be counted for determining the quorum except in

respect of items of business where they have a right to vote under the Ordinance.

Further three joint shareholders would be treated as one for the purpose of the quorum.

Therefore the quorum requirement of ten members was not met at appointed time

despite the fact that the requirement relating to 25% of the voting power was met.

07

(b) Notice to Joint Holder:

The contention of Mr. Saleem is not valid as in case of Joint holder of shares the notice

may be given to one of the joint holder who named first in the register in

respect of the shares.

02

(c) Vote for Show of Hands or Poll:

The joint holders are individually entitled to be present and take part in the

debate at such meetings and vote on resolutions decided on a show of hands

but on a poll the voting right can be exercised only by all of them acting together. Joint

shareholders must concur in voting unless the articles provide to the contrary.

03

Q.3 (a) (i) Legal Provisions relating to Challenge Of AGM�s Proceeding in the Court:

The Court may, on a petition by members having not less than ten per cent

of the voting power in the company that the proceedings of a general

meeting be declared invalid by reason of any material defect or omission in

the notice or irregularity in the proceedings of the meeting which

prevented members from using effectively their rights, declare such

proceedings or part thereof invalid Provided that the petition shall be

made within thirty days of the impugned meeting.

In the given situation the members planning to challenge the proceeding did not

have the required voting power of 10%. Further unsatisfactory lunch

arrangement cannot be a reason for making AGM invalid.

05

SUGGESTED ANSWERS � MODEL PAPER 2 of 5

CORPORATE LAWS AND SECRETARIAL PRACTICES � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

(ii) Validity of the Act of the Director if the Defect in the Appointment is

Discovered:

The defect in the appointment of any director does not make his act or act of

board of director invalid.

The director is restrained to exercise his right if defect in his appointment comes

into his notice.

Defect is required to be rectified as soon as the defect comes to the notice of the

directors.

03

(b) Rule for Transfer of Shares of a Single Member and Circumstances Where

Shares can be Transferred to Two or More Persons:

The Single member may transfer all of his shares to a single person under

the authority of an ordinary resolution whereby the company shall remain a

single member company as it was before such transfer.

The company can transfer all of the shares of a single member to two or more

persons under the authority of a special resolution for change of status from

single member company to private company and to alter its articles accordingly.

03

Q.4 (a) Items not Included in Free Reserves: (Any six)

�Free Reserves� do not include -

1. reserves created as a result of re-valuation of fixed assets;

2. goodwill reserve;

3. depreciation reserve to the extent of ordinary depreciation including

allowance for extra shifts admissible under the Income Tax Ordinance,

1979;

4. development allowance reserve created under the provisions of the

Income Tax Ordinance, 1979;

5. workers welfare fund;

6. provisions for taxation to the extent of the deferred or current liability of the

company and;

7. capital redemption reserve.

06

(b) Issue of Right Shares By a Listed Company: (Any five conditions)

A listed company may issue right shares subject to following conditions, namely:-

1. The company shall not make a right issue within one year of the first issue

of capital to the public or further issue of capital through right issue;

2. The company, while announcing right issue, shall clearly state the purpose

of the right issue, benefits to the company, use of funds and financial

projections for three years. The financial plan and projections shall be

signed by all the directors who were present in the meeting in which the

right issue was approved;

10

SUGGESTED ANSWERS � MODEL PAPER 3 of 5

CORPORATE LAWS AND SECRETARIAL PRACTICES � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

3. The decision of the company to issue right shares shall be communicated

to the Commission and the respective stock exchange on the day of the

decision;

4. The company may charge premium on right shares up to the free reserves

per share as certified by the company�s auditors and the certificate of the

auditors shall be furnished to the Commission and the respective stock

exchange along with intimation of the proposed right issue:

Provided that where a company proposes to charge premium on right issue above

the free reserves per share it shall be required to fulfill the following requirements,

namely:-

At least forty per cent of all the shareholders undertake to subscribe

their portion of right issue; and

The remaining right issue shall be fully underwritten and the

underwriters, not being associated companies, shall include at least two

financial institutions including commercial banks and investment banks

and the underwriters shall give full justification of the amount of

premium in their independent due diligence reports;

5. right issue of a loss making company or a company whose market share

price during the preceding six months has remained below par value shall

be fully and firmly underwritten;

6. book closure shall be made within forty-five days of the announcement of

the right issue and the payment and renunciation date once announced for

the letter of right shall not be extended except with the permission of the

respective stock exchange under special circumstances; and

7. if the announcement of bonus and right issue is made simultaneously,

resolution of the board of directors shall specify whether the bonus shares

covered by the announcement quality for right entitlement.

SUGGESTED ANSWERS � MODEL PAPER 4 of 5

CORPORATE LAWS AND SECRETARIAL PRACTICES � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q.5 (a) Contents Of Statement Accompanied with Notice of the Shareholders Meeting for

Passing Special Resolution for Purchase of its Own Shares by the Company:

The notice of the meeting in which the special resolution authorizing the purchase

of shares is proposed to be moved, shall be accompanied by an explanatory

statement containing all material facts including the following:-

1. justification for the purchase;

2. source of funding;

3. effect on the financial position of the company; and

4. nature and extent of the interest, if any, of every director, whether directly or

indirectly.

05

(b) Information required to be provided by Shareholder, Interested to Sell His Shares

to the Company in Response to the Tender Notice: (Any seven contents)

A Shareholder, interested to sell his shares to the company in response to the

tender notice, shall make the offer in writing through the designated branches of

an authorized bank, providing the following information in the offer, namely:-

1. Name of the shareholder;

2. His father�s name and in the case of a married woman or a widow, her

husband�s name;

3. National Identity Card No;

4. Address of the shareholder registered with the company;

5. number of shares offered for repurchase by the company;

6. Distinctive numbers of share certificates (if not in the Central Depository);

7. Folio No. (if not in the Central Depository); and

8. Sub-account number with the Central Depository, if any.

07

Q.6 (a) Housing Finance Services:

Housing finance services means the loan provided to individuals for the

purchase of residential house or apartment or land including the facilities

availed for the purpose of making improvements in house or apartment or land.

03

(b) Opening or Closure of Bank Accounts and Account with a Broker or Branches of

NBFC.

Opening or closure of any bank accounts, account with a broker or branches of an

NBFC shall be approved in a board meeting by the board of directors of the NBFC after

carefully analyzing its merits and financial impact and the reasons must be recorded in

the minutes of board meeting. Such decisions and minutes of the board meeting

shall be communicated to the Commission within fourteen days of the said meeting.

04

SUGGESTED ANSWERS � MODEL PAPER 5 of 5

CORPORATE LAWS AND SECRETARIAL PRACTICES � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q.7 (a) (i) Opening Paragraph for Inclusion in the Statement of Compliance:

This statement is being presented to comply with the Code of Corporate

Governance (CCG) contained in Regulation No. 35 of Listing Regulations of

Islamabad, Karachi and Lahore Stock Exchanges for the purpose of establishing a

framework of good governance, whereby a listed company is managed in

compliance with the best practices of corporate governance.

02

(ii) Statements Relating To Directors/Board Of Directors For Inclusion In The

Statement of Compliance: (Any four)

The directors have confirmed that none of them is serving as director on more

than seven listed companies, including this company (excluding the listed

subsidiaries of listed holding companies where applicable).

All the resident directors of the Company are registered as taxpayers and none of

them has defaulted in payment of any loan to a banking company, a Development

Finance Institution (DFI) or an NBFI or, being a member of stock exchange, has

been declared as a defaulter by that stock exchange.

The Board had developed a vision/mission statement, overall corporate strategy

and significant policies of the Company. A complete record of particulars of

significant policies along with the dates on which they were approved or amended

has been maintained.

All the powers of the Board have been duly exercised and decisions on material

transactions, including appointment and determination of remuneration and terms

and conditions of employment of the CEO, other executive and non-executive

directors, have been taken by the Board / shareholders.

All the directors on the Board are fully conversant with their duties and

responsibilities as directors of corporate bodies. The directors were apprised of

their duties and responsibilities through orientation courses.

The directors, CEO and executives do not hold any interest in the shares of the

Company other than that disclosed in the pattern of shareholding.

08

(b) Closed Period:

Each listed company shall determine a closed period prior to the announcement

of interim/ final results and any business decision, which may materially affect

the market price of its shares. No director, CEO or executive shall, directly or

indirectly, deal in the shares of the listed company in any manner during the

closed period.

02

THE END

MA-MP 1 of 4 PTO (Note: The number of questions and their marks may vary in the examination paper)

ICMA.

Pakistan

MODEL PAPER

MANAGEMENT ACCOUNTING (BAF-401)

SEMESTER-4

Extra Reading Time: 15 Minutes Writing Time: 02 Hours 30 Minutes

Maximum Marks: 80 Roll No.:

(i) Attempt all questions. (ii) Answers must be neat, relevant and brief.

(iii) In marking the question paper, the examiners take into account clarity of exposition, logic of arguments, effective presentation, language and use of clear diagram/ chart, where appropriate.

(iv) Read the instructions printed inside the top cover of answer script CAREFULLY before attempting the paper. (v) Use of non-programmable scientific calculators of any model is allowed.

(vi) DO NOT write your Name, Reg. No. or Roll No., or any irrelevant information inside the answer script. (vii) Question Paper must be returned to invigilator before leaving the examination hall.

Answer Script will be provided after lapse of 15 minutes Extra Reading Time (9:45 a.m. or 2:45 p.m. [PST] as the case may be).

Marks Q. 1 The first question printed separately comprises 20 MCQs of one (1) mark

each having allowed time of 30 minutes is an integral part of this question paper.

Q. 2 (a) Following data have been taken from Naseem & Sons' records:

Production

(Units) Total Cost (Rupees)

Price Level Index (Average)

Year-0 65,600 145,000 100 Year-1 79,800 179,200 112 Year-2 90,000 213,000 125 Year-3 60,000 196,560 140 Year-4 75,400 244,900 157 Expected in Year-5 91,200 ? 175

Required: Workout the following:

(i) Variable cost per unit at 100 average price level index. 04

(ii) Fixed cost per annum at 100 average price level index. 02

(iii) Total cost for Year-5. 03 (b) Javed Associates have following data for May 2013:

Budget Actual Unit Rupees Unit Rupees Production / Sales Quantity 250 225 Sales 75,000 70,000 Variable costs

Labour 35,000 30,000 Material 13,000 15,000

48,000 45,000 Contribution 27,000 25,000 Fixed cost 19,000 15,000 Profit 8,000 10,000

Required: Report showing actual, flexible budget and variances. 06

MA-MP 2 of 4 (Note: The number of questions and their marks may vary in the examination paper)

Marks

Q. 3 (a) Delight Textile has received an offer from local Power Generation firm to provide breakdown free power supply for longer term. The equipment and installations of transmission line would cost Rs. 5,000,000. Management believes that the power supply would provide substantial annual reductions in costs, as shown below:

Rupees Electricity cost 695,000 Power breakdown cost 555,000

The new power system would require considerable maintenance work to keep it in

proper adjustment. The company engineers estimate that maintenance cost would increase by Rs. 16,000 per annum if new system operates. The transmission system needs an overhaul at the end of every 2 years amounting to Rs. 200,000 per overhaul.

The contract period would be 10 years with salvage value (of installations) of Rs. 70,000. After 10 years company will be able to purchase a new power generation system from an international supplier amounting to Rs. 30 million.

Delight Textile requires a rate of return before tax of at least 18% on investment and uses straight-line deprecation method.

Required: (i) Should Delight Textile accept the offer or not? Ignore taxation. 08

(ii) Should Delight Textile accept the offer or not, if taxation rate is 35%? 08

(Support your answers with proper working) (b) Alaska Ltd., wants to buy a new item of equipment. Two models of equipment are

available, one with a slightly higher capacity and greater reliability than the other. The expected costs and profits of each item are as follows:

Rupees

Equipment item �A� �B� Capital cost 80,000 150,000 Life (years) 5 5 Profit before depreciation:

Year-1 50,000 50,000 Year-2 50,000 50,000 Year-3 30,000 60,000 Year-4 20,000 60,000 Year-5 10,000 60,000

Disposal value � �

Required: Which equipment should be selected using accounting rate of return (ARR) method? 04 Q. 4 ChemHouse, operates a standard marginal costing system. It makes a single product using a

single raw material. Standard data has been worked-out per bag of product as under:

Rupees/ Bag Selling price 11,000 Direct material 50 kgs@ Rs. 150 per kg 7,500 Direct labour 40 hrs @ Rs. 40 per hr 1,600 Variable production overhead 40 hrs @ Rs. 20 per hr 800

9,900 Contribution margin 1,100

MA-MP 3 of 4 PTO (Note: The number of questions and their marks may vary in the examination paper)

Marks Budgeted production is 1,020 bags per month and budgeted fixed overhead are Rs. 800,000

per month.

During March 1,000 bags were produced and sold @ Rs. 12,000 per bag. Relevant details of this production are as under:

Rs. '000' Direct material, (MS), bought and used 45,000 kgs costing 6,100 Direct labour, worked 30,000 hours, total wages for the month were 1,350 Actual variable production overhead for the month was 550 8,000 Actual fixed overheads for the month were 1,000 Total production cost 9,000

Required: (a) Selling price variance. 01 (b) Sales volume contribution variance. 01 (c) Direct material cost variance, analysed into price and usage variances. 03 (d) Direct labour cost variance, analysed into rate and efficiency variances. 03 (e) Variable production overhead variance, analysed into expenditure and efficiency

variances. 02 (f) Total variable production cost variance. 01 (g) Fixed production overhead expenditure variance. 01 (h) Budgeted and actual net profit for the month. 02 (i) Reconciliation of budgeted and actual profit. 01 Q. 5 Brilliant Tech produces and sells desktop and laptop computers having sales units mix of

3 : 4. Its Income Statement for the year is:

Brilliant Tech Income Statement

For the year Ended June 30, 2012

Desktops Laptops Total Per Unit Total Per Unit

Total

(Rs. in million) (Rs. '000') (Rs. in million) (Rs. '000') (Rs. in million)

Sales 2,250 30 4,500 45 6,750

Production costs: Materials 675 9 1,500 15 2,175 Direct labour 450 6 700 7 1,150 Variable factory overhead 225 3 700 7 925

Fixed factory overhead 75 1 200 2 275

Total production cost 1,425 19 3,100 31 4,525

Gross profit 825 11 1,400 14 2,225

Fixed marketing and administrative expenses (825)

Income before tax 1,400

Income tax @ 50.0% (700)

Net Income 700

Due to saturation of desktop market, management has decided to reduce laptop price to rupees 40,000, effective July 01, 2012, and to spend an additional amount of Rs. 25 million in 2012-13 for advertising. As a result Brilliant Tech estimates that 80% of its 2012-13 revenue will be from laptop sales. The sales unit mix for desktops and laptops are expected to be 1 : 3 in 2012-13 at all volume levels. Material costs are expected to drop 20% and 14% for desktops and laptops, respectively: however, all direct labour costs are to increase 30%.

MA-MP 4 of 4 (Note: The number of questions and their marks may vary in the examination paper)

Marks

Required:

(a) Break-even units of desktops and laptops for 2011-12. 05

(b) Sales (Rupee) required to earn profit of 7.5% on sales in 2012-13. 07

(c) Break-even units of desktops and laptops for 2012-13. 03 Q. 6 (a) Differentiate between conventional cost accounting and throughput accounting. 04 (b) Following data of M/s. Perfect Confectioners is available for latest period:

Machine Hours per Unit Machine hours required: Alpha Beta Gama Blending machine 1 2 3 Baking oven 2 4 2 Packing machine 3 3 3 Sales demand (units) 2,000 1,500 2,400

Maximum capacity is as follows:

Hours Available Blending machine 14,000 Baking oven 15,400 Packing machine 14,000

Required:

(i) Calculate the machine utilisation rate for each machine. 04

(ii) Identify which machine is the bottleneck resource. 01 (c) Data extracted from records of M/s. Burhan & Co., is tabulated below:

(Rs./ Hour)

Product Simplex Delux Sales price 150 200 Material cost 70 110

Conversion cost for both product is Rs. 60 per hour.

Required:

(i) Calculate TA ratio for both products. 03

(ii) Rank products. 01 (d) Define backflush accounting. 02

THE END

SUGGESTED ANSWERS � MODEL PAPER 1 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q. 2 (a) (i) Variable Cost per Unit:

(i) (ii) (iii) (iv)

Production

(Units) Total Cost (Rupees)

Price Level Index (Average)

Total Cost (rupees) at Price Index 100

(ii) x 100 ÷ (iii)

High level 90,000 213,000 125 170,400 1 Low level 60,000 196,560 140 140,400 1

Variable cost 30,000 30,000 1

The variable cost per unit is (30,000 ÷ 30,000) = Rs.1 per unit 1

(ii) Fixed Cost per Annum:

Rupees

Total cost of 90,000 (index 100) 170,400 Variable cost of 90,000 at Rs.1 per unit 90,000 1

Fixed costs (index 100) 80,400 1

(iii) Total Cost for Year-5:

Rupees

Variable costs (index 100) 91,200 1 Fixed costs (index 100) 80,400 Total costs (index 100) 171,600 1

Total costs (index 175) (171,600 x 175 ÷ 100) 300,300 1

(b) Actual, Flexible Budget and Variances: Rupees

Budget

250 Units Budget/

Unit Flexed budget

225 units Actual

225 Units Variance

Sales 75,000 300 67,500 70,000 2,500 (F) 1 Variable costs -

Labour 35,000 140 31,500 30,000 1,500 (F) 1 Material 13,000 52 11,700 15,000 (3,300) (A) 1

48,000 192 43,200 45,000

Contribution 27,000 108 24,300 25,000 700 (F) 1 Determine which of alternative is preferred. 19,000 19,000 15,000 4,000 (F) 1

Profit 8,000 5,300 10,000 4,700 (F) 1

OR 2 + 2 + ` 2 = 6

SUGGESTED ANSWERS � MODEL PAPER 2 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q. 3 (a) (i) Decision to Accept the Offer or not, Ignoring Taxation:

Year Cash outflow Cash Saving Net CF PV Factory at 18% PV 0 (5,000,000) (5,000,000) 1.0000 (5,000,000) 1 (16,000) 1,250,000 1,234,000 0.8475 1,045,763 1 2 (216,000) 1,250,000 1,034,000 0.7182 742,603 ½ 3 (16,000) 1,250,000 1,234,000 0.6086 751,050 ½ 4 (216,000) 1,250,000 1,034,000 0.5158 533,326 ½ 5 (16,000) 1,250,000 1,234,000 0.4371 539,393 ½ 6 (216,000) 1,250,000 1,034,000 0.3704 383,026 ½ 7 (16,000) 1,250,000 1,234,000 0.3139 387,383 ½ 8 (216,000) 1,250,000 1,034,000 0.2660 275,083 ½ 9 (16,000) 1,250,000 1,234,000 0.2255 278,213 ½

10 (16,000) 1,320,000 1,304,000 0.1911 249,148 1 NPV 184,988 1

2 + 2 + 1 + 2 = 7

Decision: Accept the offer. 1

(ii) Decision to Accept the Offer or not, With 35% Taxation:

Year Cash Outflow

Cash Saving

Deprecation Add-Profit

PAT Net CF PV Factory at 11.70%

PV

A B C D E (C-B-D)

F (E x 65%)

G (F + D)

H I (G x H)

0 (5,000,000) (5,000,000) 1.0000 (5,000,000) 1 (16,000) 1,250,000 (493,000) 741,000 481,650 974,650 0.8953 872,560 1 2 (216,000) 1,250,000 (493,000) 541,000 351,650 844,650 0.8015 676,972 ½ 3 (16,000) 1,250,000 (493,000) 741,000 481,650 974,650 0.7175 699,341 ½ 4 (216,000) 1,250,000 (493,000) 541,000 351,650 844,650 0.6424 542,580 ½ 5 (16,000) 1,250,000 (493,000) 741,000 481,650 974,650 0.5751 560,509 ½ 6 (216,000) 1,250,000 (493,000) 541,000 351,650 844,650 0.5149 434,868 ½ 7 (16,000) 1,250,000 (493,000) 741,000 481,650 974,650 0.4609 449,238 ½ 8 (216,000) 1,250,000 (493,000) 541,000 351,650 844,650 0.4126 348,539 ½ 9 (16,000) 1,250,000 (493,000) 741,000 481,650 974,650 0.3694 360,056 ½

10 (16,000) 1,320,000 (493,000) 811,000 527,150 1,020,150 0.3307 337,390 1

NPV 282,054 1 2 + 2 + 2 + 1 = 7

Decision: Accept the offer. 1 (b) Calculation of Accounting Rate of Return (ARR): Rupees

Item �A� Item �B� Total profit over life of equipment

Before depreciation 160,000 280,000 After depreciation 80,000 130,000

Average annual profit after depreciation 16,000 26,000 Average investment {(capital cost + disposal value) ÷ 2} 40,000 75,000 ARR 40.0% 34.7%

2 + 2 = 4

Both projects would earn a return of 30%, but since item �A� would earn a bigger ARR, it would be preferred to item �B�, even though the profits from �B� would be higher by an average of Rs.10,000 a year.

SUGGESTED ANSWERS � MODEL PAPER 3 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

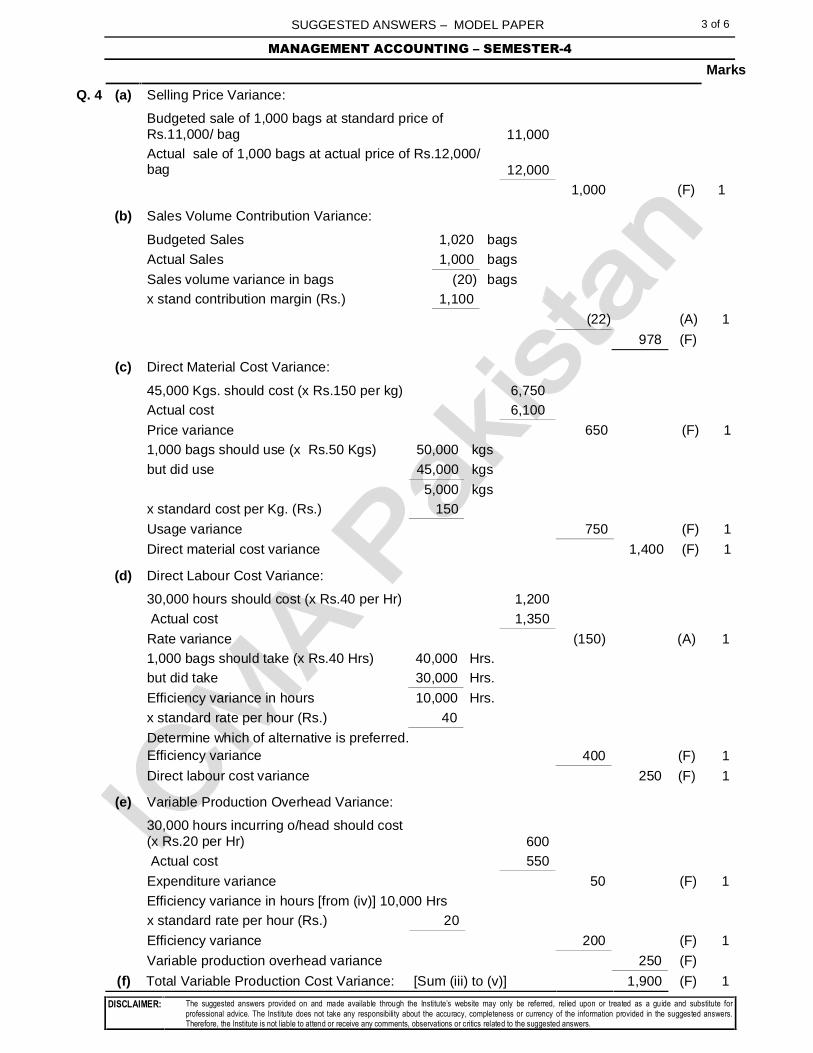

Q. 4 (a) Selling Price Variance:

Budgeted sale of 1,000 bags at standard price of Rs.11,000/ bag 11,000

Actual sale of 1,000 bags at actual price of Rs.12,000/ bag 12,000

1,000 (F) 1

(b) Sales Volume Contribution Variance:

Budgeted Sales 1,020 bags Actual Sales 1,000 bags

Sales volume variance in bags (20) bags x stand contribution margin (Rs.) 1,100

(22) (A) 1

978 (F)

(c) Direct Material Cost Variance:

45,000 Kgs. should cost (x Rs.150 per kg) 6,750 Actual cost 6,100

Price variance 650 (F) 1 1,000 bags should use (x Rs.50 Kgs) 50,000 kgs but did use 45,000 kgs

5,000 kgs x standard cost per Kg. (Rs.) 150

Usage variance 750 (F) 1

Direct material cost variance 1,400 (F) 1

(d) Direct Labour Cost Variance:

30,000 hours should cost (x Rs.40 per Hr) 1,200 Actual cost 1,350

Rate variance (150) (A) 1 1,000 bags should take (x Rs.40 Hrs) 40,000 Hrs. but did take 30,000 Hrs.

Efficiency variance in hours 10,000 Hrs. x standard rate per hour (Rs.) 40

Determine which of alternative is preferred. Efficiency variance 400 (F) 1

Direct labour cost variance 250 (F) 1

(e) Variable Production Overhead Variance:

30,000 hours incurring o/head should cost (x Rs.20 per Hr) 600

Actual cost 550

Expenditure variance 50 (F) 1 Efficiency variance in hours [from (iv)] 10,000 Hrs x standard rate per hour (Rs.) 20

Efficiency variance 200 (F) 1

Variable production overhead variance 250 (F)

(f) Total Variable Production Cost Variance: [Sum (iii) to (v)] 1,900 (F) 1

SUGGESTED ANSWERS � MODEL PAPER 4 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

(g) Fixed Production Overhead Expenditure Variance:

Budgeted expenditure 800 Actual expenditure 1,000

(200) (F) 1

(h) Budgeted and Actual Net Profit for the Month:

Budgeted contribution (1,020 x 1,100 ) 1,122 Budgeted fixed overhead (800)

Budgeted profit 322 1

Actual sales (1,020 x 12,000) 12,000 Actual production cost 9,000

Actual profit 3,000 1

(i) Reconciliation of Budgeted and Actual Profit:

Budgeted profit 322 Selling price variance 1,000 (F) Sales volume contribution variance (22) (A)

978 Total variable production cost variance 1,900 (F) Fixed production overhead expenditure variance (200) (F)

2,678 (F) 1

Actual profit 3,000

Q. 5 (a) Break-even Units of Desktops and Laptops for 2011-12:

Let: 3x = Number of desktops to breakeven

4x = Number of laptops to breakeven

At breakeven:

Sales = Variable costs + Fixed costs 1

3(30000x) + 4 (45,000x) = 3(18,000x) + 4(29,000x) + 1,100,000,000 1

90000x + 180,000x = 54,000x + 116,000x + 1,100,000,000

270,000x = 170,000x + 1,100,000,000

100,000x = 1,100,000,000

x = 11,000 units

4x = 44,000 units 1

3x = 33,000 units 1

1- Fixed Costs: Rs. in million

Factory overhead 275 Marketing and administrative 825

1,100 1

SUGGESTED ANSWERS � MODEL PAPER 5 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

(b) Sales (Rupee) Required to Earn Profit of 7.5% on Sales in 2012-13: Let: S = Sales Volume (rupees) required

VC(S) = Variable costs as a %age of S FC = Fixed costs P(S) = Targeted profit as %age of S T = Income Tax Rate

Then: P(S)

S = VC(S) + FC + 1 - T

1

0.075(S) Determine which of

alternative is preferred. S = 0.70S1 + 1,125,000,000 2 +

(1 - .50) S = 0.70S + 1,125,000,000 + 0.15S

0.15 S = 1,125,000,000

S = Rs. 7,500,000,000 1

1- Variable costs as a %age of S:

Desktops Laptops Per Unit Per Unit

Total

Rupees %age

Rupees %age

%age Sales 30,000 100.0% 40,000 100.0% Production costs: Materials 7,200 12,900 Direct labour 7,800 9,100

1

Variable factory overhead 3,000 7,000 Total variable cost 18,000 60.0% 29,000 72.5% 1 Revenue ratio X 20.0% X 80.0%

VC(S) = (0.12 + 0.58) = 0.70 1

OR 1 1 1 3

2- Fixed Costs: Rs. in million

Factory overhead 275 Marketing and administrative 825 Additional advertising 25 1,125 2

(c) Break-even Units of Desktops and Laptops for 2012-13: Let: x = Number of desktops to breakeven

3 x = Number of laptops to breakeven At breakeven: Sales = Variable costs + Fixed costs

30,000x + 3 (40,000x) = 18,000x + 3(29,000x) + 1,125,000,000 1 30,000x + 120,000x = 18,000x + 87,000x + 1,125,000,000

150,000x = 105,000x + 1,125,000,000 45,000x = 1,125,000,000 x = 25,000 units 1 3x = 75,000 units 1

SUGGESTED ANSWERS � MODEL PAPER 6 of 6

MANAGEMENT ACCOUNTING � SEMESTER-4

Marks

DISCLAIMER: The suggested answers provided on and made available through the Institute�s website may only be referred, relied upon or treated as a guide and substitute for professional advice. The Institute does not take any responsibility about the accuracy, completeness or currency of the information provided in the suggested answers. Therefore, the Institute is not liable to attend or receive any comments, observations or critics related to the suggested answers.

Q. 6 (a) Difference between Conventional Cost Accounting and Throughput Accounting:

Conventional Cost Accounting Throughput Accounting

Inventory is not an asset. Inventory is not an asset. It is a result of unsynchronised manufacturing and is a barrier to making profit. 1

Cost can be classified as either direct or indirect.

Such classifications are no longer useful. 1

Product profitability can be determined by deducting a product from selling price.

Profitability is determined by the rate at which money is earned. 1

Profit is a function of costs. Profit is a function of throughput as well as cost. 1

(b) (i) Machine Utilisation Rate:

Number of machine hours required to fulfill sales demand:

Machine Hours Required to Meet Sales Demand

Alpha Beta Gama Total

Machine Hours

Available

Machine* Utilization

Blending machine 2,000 3,000 7,200 12,200 14,000 87.1% 1

Baking machine 4,000 6,000 4,800 14,800 15,400 96.1% 1 Packing machine 6,000 4,500 7,200 17,700 14,000 126.4% 1

*Machine utilization rate = Machine hours required to meet sales demand Machine hours available

1

(ii) Packing machine is bottleneck resource: 1

(c) (i) & (ii) TA Ratio for both Products and their Ranks:

Product (Rupees/ Hour)

Simplex Delux

Sales price 150 200 Martial cost 70 110

Throughput 80 90 1 Conversion cost 60 60

Profit 20 30

Determine which of alternative is preferred. 80 90

TA ratio = 60 60

1

TA ratio = 20 30 1

Rank = 2 1 1

(d) Backflush Accounting:

Backflush accounting is a method of accounting that can be used with just-in time (JIT) production system. It saves a considerable amount of time as it avoids having to make a number of accounting entries that are required by a traditional system 2

THE END