bio-based polymers in the · pdf filebio-based polymers in the world capacities,production and...

TRANSCRIPT

Market study on

Edited by: Adriana Sanz Mirabal, Lena Scholz, Michael Carus

Bio-based Polymers in the WorldCapacities,Production and Applications:

Status Quo and Trends towards 2020

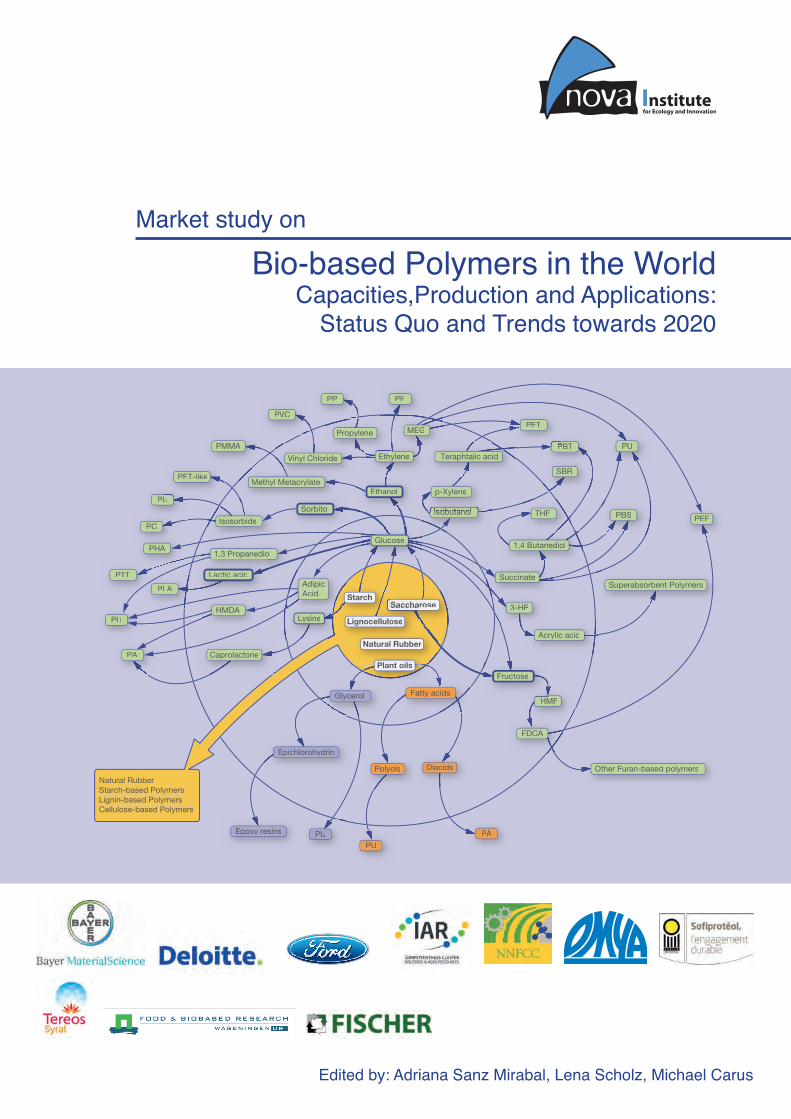

Saccharose

Fatty acids

Diacids

Glycerol

Epichlorohydrin

Epoxy resins

Starch

1,3 Propanediol

Isobutanol

Succinate

Acrylic acid

Superabsorbent Polymers

Other Furan-based polymers

PEF

1,4 Butanediol

Isobutanol

p-Xylene

Ethylene

Propylene

Vinyl Chloride

Methyl Metacrylate

Isosorbide

MEG

SBR

THF

Teraphtalic acidPBT

PBS

PBT

PET

PE

PU

PU

PA

Polyols

PU

PP

PU

PC

PVC

PTT

PLA

HMF

FDCA

PHA

PA

PMMA

HMDA

Caprolactone

AdipicAcid

3-HP

PET-like

Lactic acid

Sorbitol

Ethanol

Saccharose

Lignocellulose

Natural Rubber

Plant oilsFructose

Natural RubberStarch-based PolymersLignin-based PolymersCellulose-based Polymers

Glucose

Lysine

PU

Market study on

Bio-based Polymers in the WorldCapacities,Production and Applications: Status Quo and Trends towards 2020

nova-Institut GmbH

Edited by: Adriana Sanz Mirabal, Lena Scholz, Michael Carus

February 2013

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

4

The expert team of the Market Study (authors) has made every attempt to ensure the accuracy and reliability of the information provided on this study. The included market and trend analyses and forecasts are

performed to the best of the authors‘ knowledge and beliefs on the basis of the current state of knowledge and the latest research and inquiries. Nevertheless, authors, editors, and publisher do not warrant the information contained in this study, to be free of errors or will prove to be accurate. The information,

conclusions and findings provided in this study are not intended as legal or financial advice. The authors cannot accept liability for actions taken based on the content of this Market Study.

© 2013 nova-Institut GmbH, Germany

Publisher:

Michael Carus (v.i.S.d.P), nova-Institute GmbH, Chemiepark Knapsack, Industriestr. 300, 50354 Huerth Germany, Phone: +49 (0) 2233 48 14 40, Fax: +49 (0) 2233 48 14 50, [email protected],

www.nova-institut.eu

Layout:

ftdesign - kreativ Büro www.ftd-kreativbuero.de

All rights reserved (including those of the translation into other languages).

No part of this publication shall be reproduced, transmitted, displayed, published, broadcast or resold in whole or in part in any form, without the prior written consent of the authors.

Registered names, trademarks, etc. used in this study, even when not specifically marked as such, are not to be considered unprotected by law. The rights remain with the holders of the respective trademarks. The

nomination of product- or service-designations serves exclusively the purposes of identification.

Authors (in alphabetical order)

Wolfgang Baltus, National Innovation Agency (NIA), Thailand

Janpeter Beckmann, nova-Institut GmbH, Germany

Dirk Carrez, Clever Consult, Belgium

Michael Carus, nova-Institut GmbH, Germany

Lara Dammer, nova-Institut GmbH, Germany

Roland Essel, nova-Institut GmbH, Germany

Harald Kaeb, narocon, Germany

Jan Ravenstijn, Jan Ravenstijn Consulting, Netherlands

Adriana Sanz Mirabal, nova-Institut GmbH, Germany

Lena Scholz, nova-Institut GmbH, Germany

Fabrizio Sibilla, nova-Institut GmbH, Germany

Stephan Zepnik, Fraunhofer UMSICHT, Germany

5

Table of Content

Table of Content

1 Executive Summary 6

2 Introduction 12

Market Data

3 Market Data 17

4 Qualitative analyses of selected bio-based Polymers 55

Trend reports

5 Policies impacting bioplastics market development 65

6 Bio-based polymers, a revolutionary change 100

7 Asian markets for bio-based resins 137

8 Environmental evaluation of bio-based polymers and plastics 168

9 Green Premium within the value chain from chemicals to bioplastics 186

10 Brands: Sustainability Strategies and Bioplastics Information from the fast moving consumer goods industries (focus packaging) 206

Company

11 Company Profiles 221

12 Company product index 349

13 List of Acronyms 358

17

Market Data

3 Market Data

Table of Content

3.1. Polyamide (PA) 20

3.2. Polybutylene Adipate Terephthalat (PBAT) 24

3.3. Polybutylene succinate (PBS) 28

3.4. Polyethylene (PE) 31

3.5. Polyethylene Terephthalat (PET) 34

3.6. Polyhydroxy Alkanoate (PHA) 37

3.7. Polylactic acid (PLA) 42

3.8. Polypropylene (PP) 46

3.9. Polyvinyl Chloride (PVC) 48

3.10. Starch Blends 50

55

Market Data

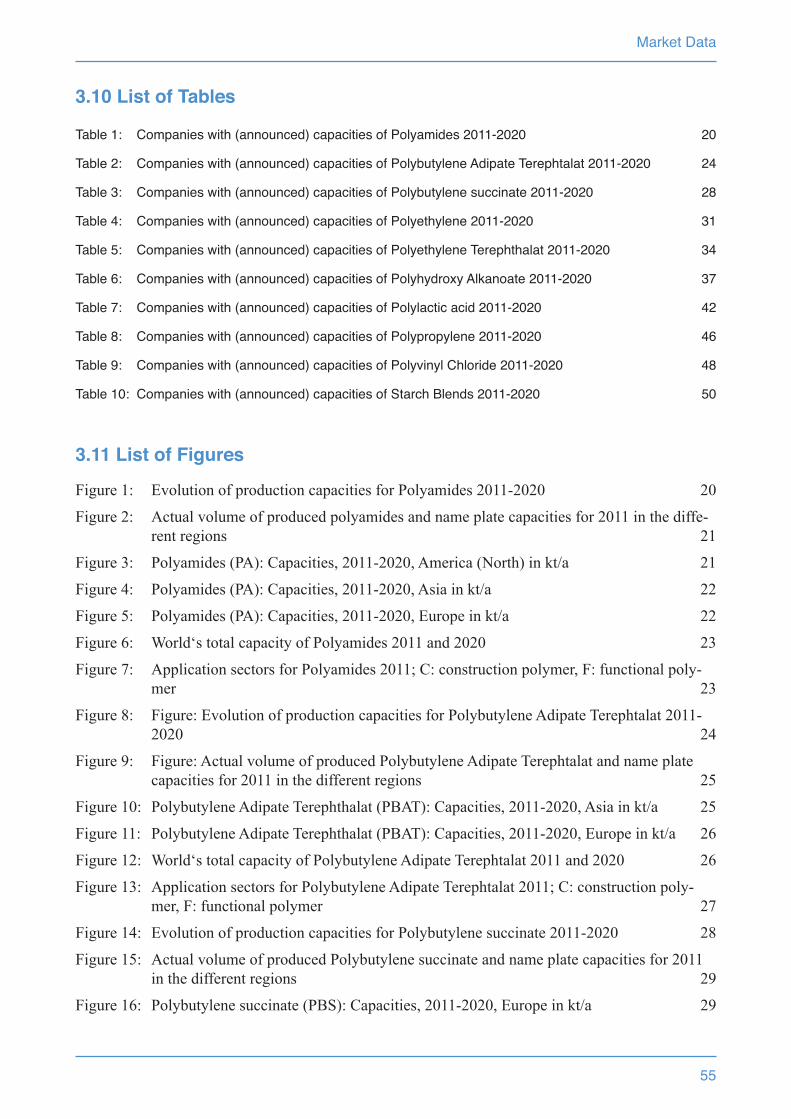

3.11 List of Figures

Figure 1: Evolution of production capacities for Polyamides 2011-2020 20

Figure 2: Actual volume of produced polyamides and name plate capacities for 2011 in the diffe-rent regions 21

Figure 3: Polyamides (PA): Capacities, 2011-2020, America (North) in kt/a 21

Figure 4: Polyamides (PA): Capacities, 2011-2020, Asia in kt/a 22

Figure 5: Polyamides (PA): Capacities, 2011-2020, Europe in kt/a 22

Figure 6: World‘s total capacity of Polyamides 2011 and 2020 23

Figure 7: Application sectors for Polyamides 2011; C: construction polymer, F: functional poly-mer 23

Figure 8: Figure: Evolution of production capacities for Polybutylene Adipate Terephtalat 2011-2020 24

Figure 9: Figure: Actual volume of produced Polybutylene Adipate Terephtalat and name plate capacities for 2011 in the different regions 25

Figure 10: Polybutylene Adipate Terephthalat (PBAT): Capacities, 2011-2020, Asia in kt/a 25

Figure 11: Polybutylene Adipate Terephthalat (PBAT): Capacities, 2011-2020, Europe in kt/a 26

Figure 12: World‘s total capacity of Polybutylene Adipate Terephtalat 2011 and 2020 26

Figure 13: Application sectors for Polybutylene Adipate Terephtalat 2011; C: construction poly-mer, F: functional polymer 27

Figure 14: Evolution of production capacities for Polybutylene succinate 2011-2020 28

Figure 15: Actual volume of produced Polybutylene succinate and name plate capacities for 2011 in the different regions 29

Figure 16: Polybutylene succinate (PBS): Capacities, 2011-2020, Europe in kt/a 29

3.10 List of Tables

Table 1: Companies with (announced) capacities of Polyamides 2011-2020 20

Table 2: Companies with (announced) capacities of Polybutylene Adipate Terephtalat 2011-2020 24

Table 3: Companies with (announced) capacities of Polybutylene succinate 2011-2020 28

Table 4: Companies with (announced) capacities of Polyethylene 2011-2020 31

Table 5: Companies with (announced) capacities of Polyethylene Terephthalat 2011-2020 34

Table 6: Companies with (announced) capacities of Polyhydroxy Alkanoate 2011-2020 37

Table 7: Companies with (announced) capacities of Polylactic acid 2011-2020 42

Table 8: Companies with (announced) capacities of Polypropylene 2011-2020 46

Table 9: Companies with (announced) capacities of Polyvinyl Chloride 2011-2020 48

Table 10: Companies with (announced) capacities of Starch Blends 2011-2020 50

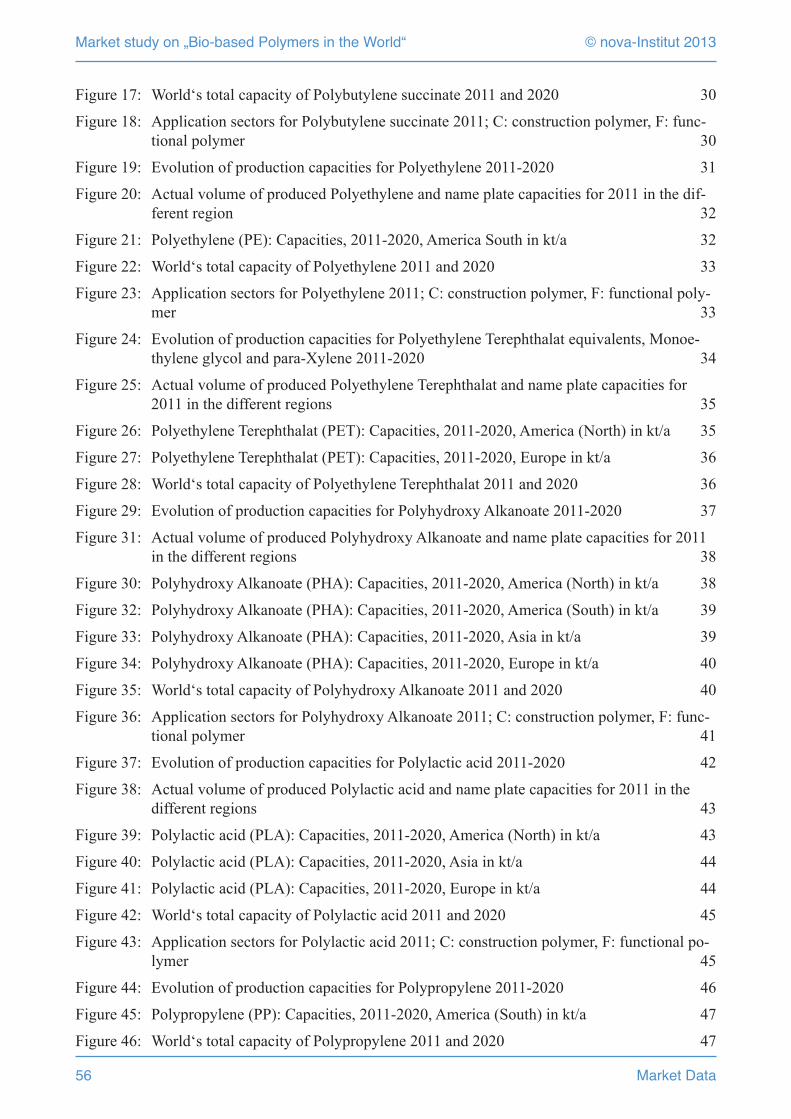

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

56 Market Data

Figure 17: World‘s total capacity of Polybutylene succinate 2011 and 2020 30

Figure 18: Application sectors for Polybutylene succinate 2011; C: construction polymer, F: func-tional polymer 30

Figure 19: Evolution of production capacities for Polyethylene 2011-2020 31

Figure 20: Actual volume of produced Polyethylene and name plate capacities for 2011 in the dif-ferent region 32

Figure 21: Polyethylene (PE): Capacities, 2011-2020, America South in kt/a 32

Figure 22: World‘s total capacity of Polyethylene 2011 and 2020 33

Figure 23: Application sectors for Polyethylene 2011; C: construction polymer, F: functional poly-mer 33

Figure 24: Evolution of production capacities for Polyethylene Terephthalat equivalents, Monoe-thylene glycol and para-Xylene 2011-2020 34

Figure 25: Actual volume of produced Polyethylene Terephthalat and name plate capacities for 2011 in the different regions 35

Figure 26: Polyethylene Terephthalat (PET): Capacities, 2011-2020, America (North) in kt/a 35

Figure 27: Polyethylene Terephthalat (PET): Capacities, 2011-2020, Europe in kt/a 36

Figure 28: World‘s total capacity of Polyethylene Terephthalat 2011 and 2020 36

Figure 29: Evolution of production capacities for Polyhydroxy Alkanoate 2011-2020 37

Figure 31: Actual volume of produced Polyhydroxy Alkanoate and name plate capacities for 2011 in the different regions 38

Figure 30: Polyhydroxy Alkanoate (PHA): Capacities, 2011-2020, America (North) in kt/a 38

Figure 32: Polyhydroxy Alkanoate (PHA): Capacities, 2011-2020, America (South) in kt/a 39

Figure 33: Polyhydroxy Alkanoate (PHA): Capacities, 2011-2020, Asia in kt/a 39

Figure 34: Polyhydroxy Alkanoate (PHA): Capacities, 2011-2020, Europe in kt/a 40

Figure 35: World‘s total capacity of Polyhydroxy Alkanoate 2011 and 2020 40

Figure 36: Application sectors for Polyhydroxy Alkanoate 2011; C: construction polymer, F: func-tional polymer 41

Figure 37: Evolution of production capacities for Polylactic acid 2011-2020 42

Figure 38: Actual volume of produced Polylactic acid and name plate capacities for 2011 in the different regions 43

Figure 39: Polylactic acid (PLA): Capacities, 2011-2020, America (North) in kt/a 43

Figure 40: Polylactic acid (PLA): Capacities, 2011-2020, Asia in kt/a 44

Figure 41: Polylactic acid (PLA): Capacities, 2011-2020, Europe in kt/a 44

Figure 42: World‘s total capacity of Polylactic acid 2011 and 2020 45

Figure 43: Application sectors for Polylactic acid 2011; C: construction polymer, F: functional po-lymer 45

Figure 44: Evolution of production capacities for Polypropylene 2011-2020 46

Figure 45: Polypropylene (PP): Capacities, 2011-2020, America (South) in kt/a 47

Figure 46: World‘s total capacity of Polypropylene 2011 and 2020 47

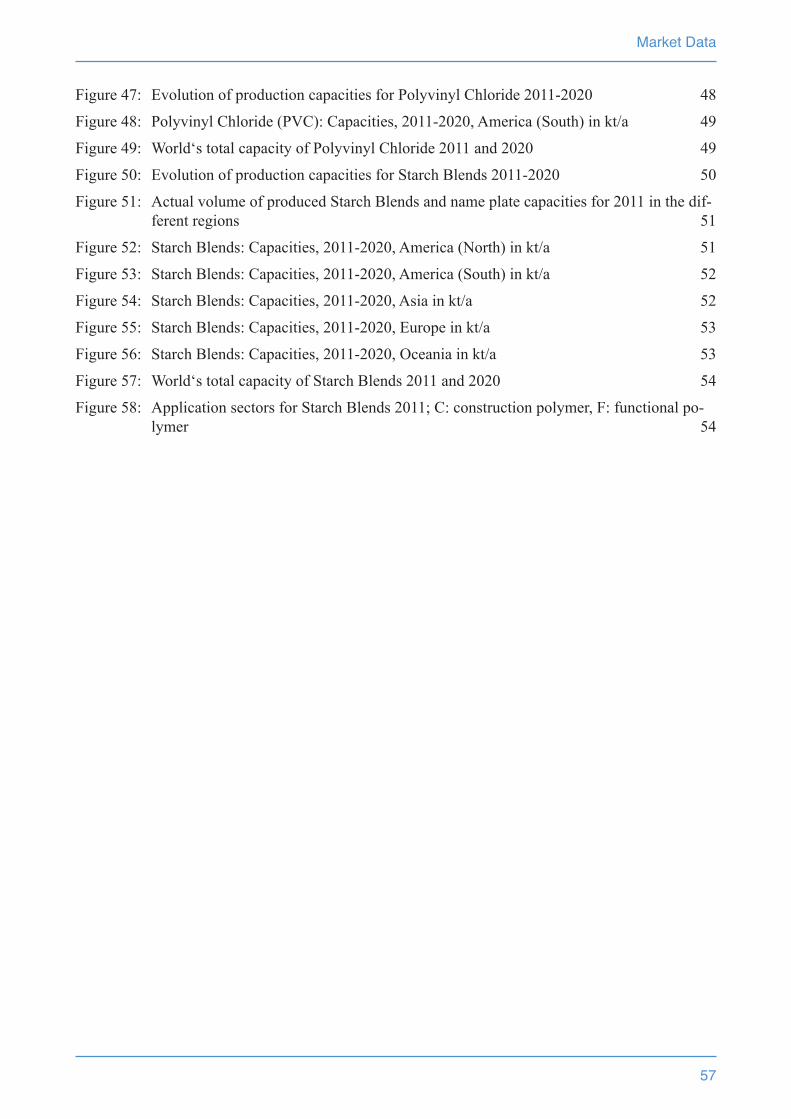

57

Market Data

Figure 47: Evolution of production capacities for Polyvinyl Chloride 2011-2020 48

Figure 48: Polyvinyl Chloride (PVC): Capacities, 2011-2020, America (South) in kt/a 49

Figure 49: World‘s total capacity of Polyvinyl Chloride 2011 and 2020 49

Figure 50: Evolution of production capacities for Starch Blends 2011-2020 50

Figure 51: Actual volume of produced Starch Blends and name plate capacities for 2011 in the dif-ferent regions 51

Figure 52: Starch Blends: Capacities, 2011-2020, America (North) in kt/a 51

Figure 53: Starch Blends: Capacities, 2011-2020, America (South) in kt/a 52

Figure 54: Starch Blends: Capacities, 2011-2020, Asia in kt/a 52

Figure 55: Starch Blends: Capacities, 2011-2020, Europe in kt/a 53

Figure 56: Starch Blends: Capacities, 2011-2020, Oceania in kt/a 53

Figure 57: World‘s total capacity of Starch Blends 2011 and 2020 54

Figure 58: Application sectors for Starch Blends 2011; C: construction polymer, F: functional po-lymer 54

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

68 Policies impacting bioplastics market development

5 Policies impacting bioplastics market development

Dirk Carrez, Clever Consult, Belgium

Lara Dammer, Michael Carus, nova-Institut GmbH, Germany

5.1. Introduction 665.2. Stimulatin market demand 66

5.2.1. Dedicated policies promoting bio-based products and bioplastics 675.2.2. Mandates 715.2.3. Public procurement policies 71

5.3. Overcoming investment barriers: Taxes and Subsidies 735.3.1. US 735.3.2. Brazil 735.3.3. China 745.3.4. Thailand 745.3.5. Malaysia 74

5.4. Productspecificpolicies 745.5. Research and Innovation policies focussing on bio-based products 76

5.5.1. Europe 765.5.2. US 775.5.3. Japan 785.5.4. China 785.5.5. Brazil 795.5.6. South Korea 79

5.6. Non-dedicated policies impacting bioplastics 805.6.1. Europe 805.6.2. Brazil 81

5.7. Other 815.7.1. Feedstock-related policies 815.7.2. Bioenergy related policies 83

5.8. General Bioeconomy Strategies and Policies 885.8.1. Some examples 88

5.9. List of tables 935.10. Listoffigures 935.11. References 94

103Jan Ravenstijn

Bio-based polymers, a revolutionary change

6 Bio-based polymers, a revolutionary change

Jan Ravenstijn, Jan Ravenstijn Consulting, Netherlands

6.1. Introduction 1016.2. Market trends 1026.3. Technology trends 1036.4. Environmental trends 1056.5. Selected biopolymer families 109

6.5.1. Polyhydroxyalkanoates (PHA) 1096.5.2. Polybutylenesuccinates (PBS) 1136.5.3. Natural Oil Polyols and CO2-based polyols for polyurethanes (PUR) 1206.5.4. Polyamides (PA): 126

6.6. Customer views 1316.7. New business concepts 133

6.7.1. PharmafilterBV(TheNetherlands). 1336.7.2. AvantiumTechnologiesB.V.(TheNetherlands). 134

6.8. New value chain 1346.9. Listoffigures 136

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

140 Asian markets for bio-based resins

7 Asian markets for bio-based resins

Wolfgang Baltus, National Innovation Agency (NIA), Thailand

7.1. Introduction 1387.2. Asian markets for bio-based resins 1387.3. Asia-Pacific region in numbers 1427.4. Feedstock – Key to success in Asia-Pacific 144

7.4.1. Sugarcane 1477.4.2. Cassava 1487.4.3. Threats 1507.4.4. Other feedstock and cost considerations 150

7.5. Policy Development 1517.5.1. Stimulation of investment 1517.5.2. End-of-life policy 152

7.6. Market growth factors 1537.6.1. Environmental factors 1537.6.2. Financial factors 1537.6.3. Technical factors 154

7.7. Selected biopolymer families – limitations, challenges and chances in Asia Pacific 1547.7.1. Polylactic acid (PLA) 1547.7.2. Polybutylenesuccinate (PBS) 1607.7.3. Bio-PE/Bio-PET 1617.7.4. PHA 1637.7.5. Polyamide 163

7.8. Case Study: The National Bioplastics Roadmap in Thailand – Situation and outlook after 4 years in operation 1647.9. List of tables 1667.10. List of figures 166

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

170 Asian markets for bio-based resins

7.9 List of tables

Table 1: Global and Asian production capacities of selected bio-based polymers 2011 and 2020 142

Table 2: GDP data, population and stage of development for selected countries in Asia-Pacific 145

Table 3: Available Feedstock in Asian regions 148

Table 4: Available Biomass equivalents in Asia 149

Table 5: Main regions of cassava production, total yield and yield per hectare 153

7.10 List of figures

Figure 1: Value chain from PLA/PBS plants (in millions of euros) 141

Figure 2: Municipal waste generation in selected AP countries in 2025. Size of bubble = population size 146

Figure 3: Plastic consumption per capita in selected AP countries versus gross net income per capita in 2010. Size of bubble = population size 146

Figure 4: Polymer value chain in Thailand, 2011 (PTIT 2012) 147

Figure 5: Benchmarking of different feedstocks for PLA in Thailand 148

Figure 6: Available Biomass Simulation (based on APEC, 2008) 149

Figure 7: Value Chain of PLA compared for different biomass input 150

Figure 8: Sugarcane production and yields for selected countries 151

Figure 9: Sugarcane price development 1980 – 2012 in Thailand 151

Figure 10: Prices of Thai domestic cassava compared to crude oil 152

Figure 11: Estimation of PLA demand in Asia 2012 (t/yr) - 2011. Total amount ~ 39,000 t/yr, import ratio for PLA: 71 % 159

Figure 12: NatureWorks LLC dominates the PLA market. 159

Figure 13: The collapse of the local PLA resin production in China 2007-2012. Source: CCM, China 160

Figure 14: Bioplastics market in Japan, 2007 and 2011 (Adapted from JSBI, 2012) 163

Figure 15: Ethylene prices and bio-PE price projections 165

Figure 16: Present PET value chain 166

171Roland Essel and Michael Carus

Environmental evaluation of bio-based polymers and plastics

8 Environmental evaluation of bio-based polymers and plastics

Roland Essel and Michael Carus nova-institut GmbH, Hürth, Germany

8.1. Introduction 1698.2. Results from recent life cycle assessments 169

8.2.1. CO2 emissions and fossil resource depletion 1698.2.2. Other environmental impact categories 173

8.3. Feedstock supply and use of by-products 1748.4. Geneticallymodifiedorganisms 1758.5. Biodiversity 1768.6. Land use 177

8.6.1. Land use change 1788.6.2. Landuseefficiency 180

8.7. Conclusion 1838.8. List of tables 1858.9. Listoffigures 185

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

188 Environmental evaluation of bio-based polymers and plastics

8.8 List of tables

Table 1: Comparison of non-renewable energy use and greenhouse gas emissions of petrochemical and bio-based polymers 175

8.9 List of figures

Figure 1: Environmental impacts of different polymers in two impact categories: climate change and fossil resource depletion 173

Figure 2: Savings of fossil resources due to the production of bio-based polymers. 174

Figure 3: Reduction of greenhouse gas emissions through production of bio-based polymers. 175

Figure 4: Relative changes in the eco-profile of Ingeo PLA. 176

Figure 5: Average product-specific environmental impacts of bio-based materials in comparison to conventional materials 177

Figure 6: Comparison of greenhouse gas emissions and fossil resource depletion in the production of PHA from different feedstocks (Kim & Dale 2005, Harding et al. 2007) 178

Figure 7: Implications of biodiversity loss 180

Figure 8: Worldwide use of agricultural biomass harvested in 2008 181

Figure 9: Illustration of direct and indirect land-use changes 182

Figure 10: Land use per tonne of bio-based PLA, bio-based PE and bioethanol from five crops valid for both current agricultural practice and if all residues/co-products are used. 183

Figure 11: Avoided NREU per hectare of land for the various bio-based products relative to their fossil based counterparts 184

Figure 12: Annual sugar/starch yield for selected feedstocks. 185

Figure 13: Land use efficiency of photovoltaic panels compared to biofuels 186

189

Green Premium within the value chain from chemicals to bioplastics

Janpeter Beckmann

9 Green Premium within the value chain from chemicals to bioplastics

Janpeter Beckmann and Michael Carus nova-Institut GmbH, Germany

9.1. Introduction 1879.2. GreenPremium-Useanddefinition 187

9.2.1. Introductory market observations 1879.2.2. TypesofperformanceanddefinitionofGreenPremium 1909.2.3. Green Premium market overview 193

9.3. Understanding the reasons for Green Premium prices 1999.3.1. Explanations and individual expert opinions 1999.3.2. Drivers 201

9.4. Summary and conclusions 2029.5. List of tables 2039.6. Listoffigures 2039.7. References 204

209

Brands: Sustainability Strategies and Bioplastics - Information from the fast moving consumer goods industries (focus packaging)

Harald Kaeb

10 Brands: Sustainability Strategies and Bioplastics - Information from the fast moving consumer goods industries (focus packaging)

Harald Kaeb, narocon InnovationConsulting, Germany

10.1. Introduction – Why read this 20610.2. Summary – what strikes the eye 20810.3. List of Drivers – Brand Motivation (not weighed or prioritized) 209

10.3.1. Sustainability targets in general & strategic 20910.3.2.Specificdriversforincreaseduseofbioplastics(additional) 209

10.4. Company-specificaspects 20910.4.1. Coca-Cola 21010.4.2. Danone 21110.4.3. Friesland-Campina 21410.4.4. Henkel 21410.4.5. Nestlé 21610.4.6. Proctor & Gamble 21810.4.7. Unilever 219

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

224

11 Company Profiles

Table of Content

8.1 Acetati S.p.A. 228

8.2 Amyris 229

8.3 Anhui COFCO Biochemical & GALACTIC Lactic Acid Co., Ltd. 230

8.4 Anellotech Inc. 231

8.5 Anqing Hexing Chemical Co., Ltd. 232

8.6 Arizona Chemical 233

8.7 Arkema SA 234

8.8 Avantium Chemicals BV 236

8.9 BASF SE 237

8.10 Bayer MaterialScience 239

8.11 Bio-On Srl 240

8.12 BioAmber 241

8.13 BioBased Technologies LLC 243

8.14 BioMatera Inc. 244

8.15 Biomer 245

8.16 Biop Biopolymer Technologies AG 246

8.17 Bioplastech 247

8.18 BIOTEC Biologische Naturverpackungen GmbH & Co. KG 248

8.19 Braskem 249

8.20 Cardia Bioplastics Limited 250

8.21 Cargill Inc. 251

8.22 Cathay Industrial Biotech 252

8.23 Casda Biomaterials Co., LTD 253

8.24 Celanese Acetate LLC 254

8.25 Cereplast Inc. 255

8.26 Cerestech Inc. 256

8.27 Chemplast Sanmar Limited 257

8.28 Chengdu Dikang Biomedical Co., Ltd. 258

8.29 China New Materials Holding 259

349

Company product index

Company product index

1,3-Propanediol

DuPont

METabolic EXplorer (METEX)

1,4-Butanediol

BioAmber

China New Materials Holding

Genomatica

Global Bio-Chem

Novamont SpA

Adipic acid

DSM N.V.

Rennovia

Verdezyne

Bio-paraxylene (bioPX)

Anellotech Inc.

Gevo

Global Bioenergies

Honeywell UOP

M&G Group (Gruppo Mossi & Ghisolfi)

Virent

Butanol

Cathay Industrial Biotech

Cellulose acetate

Acetati S.p.A.

Celanese Acetate LLC

Clarifoil

Daicel Chemicals Industries Ltd.

Eastman Chemical Company

Rhodia Acetow

WinGram Industry Co. Ltd. (Great River Qin Xin Plastic Manufacturer Co. Ltd.)

Market study on „Bio-based Polymers in the World“ © nova-Institut 2013

358 List of Acronyms

List of Acronyms

AA Adipic Acid

ABS Acrylonitrile Butadiene Styrene polymer

ADM Archer Daniels Midland

ACHEMA Ausstellungstagung für chemisches Apparatewesen

AG Aktien Gesellschaft

ARD Agro-industrie Recherches et Developpement

ASTM American Society for Testing & Materials

B2B Business to business

BASF Badische Anilin und Soda Fabrik

BCAP Biomass Crop Assistance Programme

BCG Biotechnology Commercialization Grant

BDO Butanediol

BMC Bulk moulding compound

BMBF Bundesministerium für Bildung und Forschung

BMELV Bundesministerium für Ernährung, Landwirtschaft und Verbraucherschutz

BMW Bayerische Motoren Werke

BNDES Brazilian Development Bank

CA Cellulose Acetate

CAP Common Agricultural Policy

CCC Commodity Credit Corporation

CEN European Committee for Standardization

CLIB2021 Cluster Industrielle Biotechnologie e.V.

CO2 Carbon dioxide

DAB Diaminobutane

DG Directorate-General

DMC Double Metal Cyanides (catalyst)

DNP Diversified Natural Products

DOE United States Department of Energy

Drop-in A bio-based polymer with a chemical structure identical to that of its petro-based counterpart

DS Degree of substitution

DSM Dutch State Mines