biopharma discovery and development contract services – indiana

TRANSCRIPT

Biopharma Discovery and Development Contract Services –Indiana Market Opportunities and Funding Options

An analysis of the pharmaceutical and biotech development and manufacturing sector

January 2008

65760 Covers 1/15/08 9:11 AM Page 2

Biopharma Discovery and Development Contract Services –

Indiana Market Opportunities and Funding Options

An analysis of the pharmaceutical and biotech development and manufacturing sector

January 2008

Copyright © 2007, BioCrossroads - BC Initiative, Inc./CICP Foundation

1

Table of Contents

I. EXECUTIVE SUMMARY ...................................................................................................... 3

II. PURPOSE AND OBJECTIVE................................................................................................. 6

III. OVERVIEW OF PHARMACEUTICAL AND BIOTECH MARKET FORCES................................. 7

Convergence of outsourcing activities for pharmaceutical and biotechnology companies ...................................................................................................................... 7

Defining and characterizing the outsourcing market space ........................................10

Contract Service Provider Scope of Services Map .......................................................10

IV. RESULTING CSP MARKET TRENDS...................................................................................11

(A) Size and Scale.........................................................................................................11

(B) Consolidation and Fragmentation .........................................................................12

(C) Framework for Emerging Opportunities................................................................13

(D) Challenges to Outsourcing.....................................................................................14

(1) Sponsor Transitional Issues ..........................................................................14

(2) Offshoring vs. Domestic Outsourcing. ..........................................................14

(3) Instructive Examples . ...................................................................................17

V. SPECIFIC GROWTH OPPORTUNITIES FOR INDIANA IN THE U.S. CONTRACT SERVICES MARKET ...............................................................................................................................18

1. Discovery (non-GLP) Services ................................................................................18

2. Analytical Chemistry Services................................................................................19

3. Pre-clinical Services ...............................................................................................20

4. Contract Manufacturing........................................................................................21

5. Business Services...................................................................................................23

VI. CAPITAL MARKET INTEREST IN SERVICE VENTURES .......................................................24

Opportunities for private equity and venture capital markets ..................................24

Private Equity and Venture Capital activity in contract services................................25

VII. FINDING, FORMING AND FUNDING SUCCESSFUL SERVICE VENTURES ..........................26

Pure startup CSPs ........................................................................................................26

Local Expansion of an Existing CSP..............................................................................27

Spinout of a Large Pharmaceutical Company .............................................................27

2

VIII. CONCLUSIONS................................................................................................................28

As Outsourcing Increases, Underserved Markets are Bringing Increased Opportunities for Capital Investment in CSPs ....................................................................................28

APPENDIX I: Biopharma Development and Manufacturing in Indiana – A representative list of companies, activities and employment ...............................................................30

Appendix II: Medco Headline and Article from Indianapolis Star ............................................31

Appendix III: CASE STUDIES OF SUCCESSFUL SERVICE COMPANY VENTURES ..........................34

Quintiles Transnational Corp......................................................................................34

Althea Technologies ...................................................................................................35

Aptuit..........................................................................................................................35

BioStorage Technologies, Inc......................................................................................36

Ricerca ................................................................................................................. 37

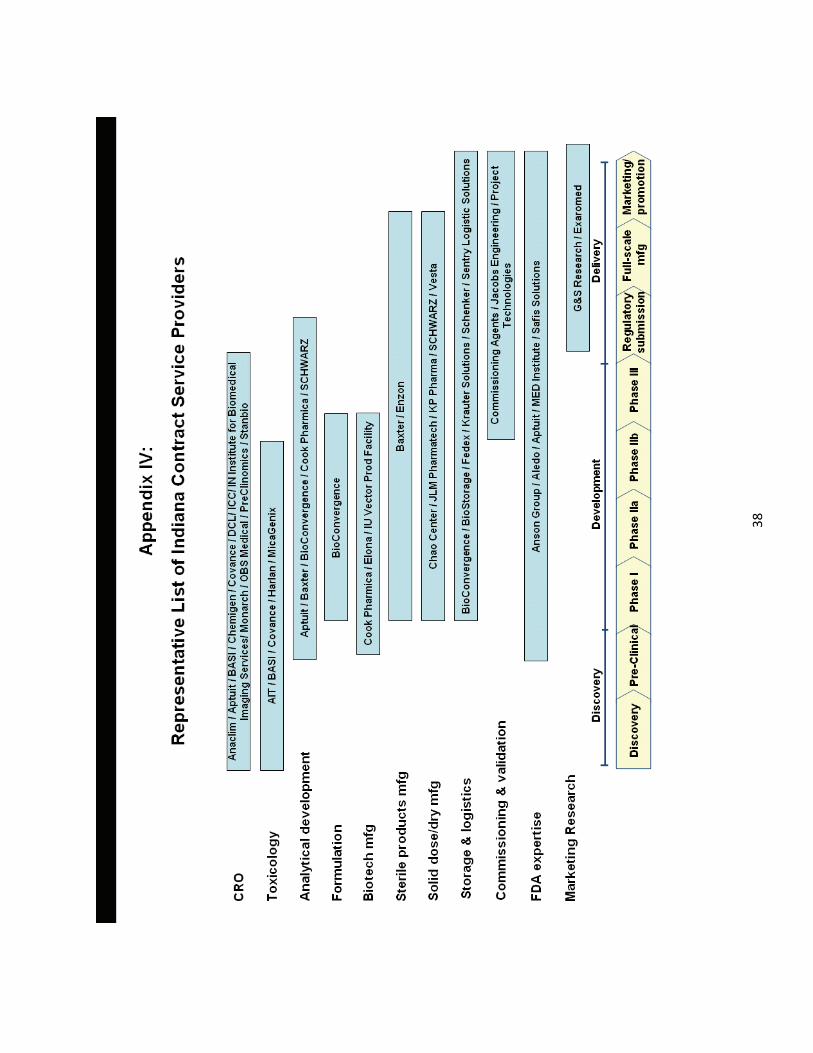

Appendix IV: Representative List of Indiana Contract Service Providers..................................38

Appendix V: Private Equity and Venture Capital Activity in Contract Services: Underlying Data ...................................................................................................39

Appendix VI: GLOSSARY OF ABBREVIATIONS............................................................................41

3

I. EXECUTIVE SUMMARY

As the pharmaceutical and biotechnology industries face a series of convergent financial and regulatory pressures, strategic utilization of third party vendors to perform essential, but non-core functions is increasing at unprecedented rates. The contract service providers (CSPs) that serve as partners in this emerging “networked” model of drug development are consequently experiencing record growth of 14 – 16% industry wide - - exceeding 20% in certain service segments. As these trends continue, regions already rich with talent and resources serving biopharmaceutical development will be able to further capitalize on existing assets and facilitate the increased services that the market is demanding.

Factors such as increasing regulatory roadblocks, payor consolidation and demands for greater transparency; pending patent expirations; risks from early and evolving science; increased development expenses; escalating market and investor impatience; and growing needs for more flexible business models moving from fixed to variable cost outlays are all familiar to fully integrated pharmaceutical and mature biotechnology companies (“FIPCOs”). In the present environment, FIPCOs need to become more nimble and flexible FIPNETS (fully integrated pharmaceutical networks) by increasing focus on core competencies while looking to outside service providers and strategic partners for assistance in validating, developing and bringing products to market through a virtual network of business relationships.

The outsourcing forces that are facing pharmaceutical and large biotech companies are parallel and convergent with those facing early-stage biotechnology companies. Here, the pressures come from the private venture capital markets that have fueled their growth. As the economics of the venture market have changed and the average price of the biotech IPO has stagnated and dropped, venture investors are betting on an early sale or strategic acquisition by a larger biopharma company to maximize return. As a result, biotech startups are operating as virtual companies that rely almost exclusively on CSPs to advance product development to the point of optimal exit or sale.

From discovery through development and commercialization, the current range of CSP services is both comprehensive and specialized, including clinical trial management, central laboratory services, product development and formulation, FDA regulatory services and other complementary services. The overall CSP market, comprised of approximately 1,100 individual CSPs, is valued at approximately $14 billion and growing at 14 – 16% annually. As smaller niche and mid-size regional CSPs consolidate with larger CSPs to meet the increased demand resulting from preferred provider relationships within the biopharmaceutical industry, biotech companies are finding themselves with lengthy lead times that could jeopardize product development and milestones imposed by venture investors. At the same time, the number of early stage development candidates is increasing and more emphasis is being placed on proving (or disproving) safety and efficacy as quickly and cost-effectively as possible. This all leads to a

4

marketplace of discovery and development service providers that will not be able to meet the mounting demand for service.

Services experiencing especially high demand in this market are early phase activities such as analytical chemistry, toxicology and other pre-clinical services as well as Phase I clinical services. Analyst reports describe the pre-clinical services industry as growing at 15 – 20% annually with lead time for expanding capacity of approximately 2 – 4 years. Such substantial growth and long lead times will only increase the reported backlogs of up to six months in study scheduling.

Outsourcing in the biopharmaceutical industry is not without its challenges. Many FIPCOs have an institutionalized aversion to relinquishing control necessary for maximizing outsourcing potential and managing relationships with CSPs.

The threat of offshoring presents a challenge to domestic outsourcing, but there are commonly identified barriers for all pharmaceutical and biotechnology companies when considering offshore alternatives, especially in India and China. These include well-documented concerns over intellectual property protection, language barriers (China), clinical study quality and integrity in remote locales, and perceived problems of delay around multiple layers of foreign regulatory approvals.

As central laboratory services presented a promising opportunity 25 years ago that led ultimately to the development of a major Covance facility near Indianapolis International Airport, specific growth opportunities are apparent today for Indiana in the U.S. contract services market. As pharmaceutical and biotechnology companies expand targets and pipelines, capacity shortages are arising among many late-stage discovery and early-stage development service providers. Analyst and industry reports cite backlogs in study scheduling in these areas and demand growing for pre-clinical, Phase I, bioanalytical and analytical chemistry services as well as biologics manufacturing. This report highlights five service opportunities:

• Non-GLP discovery services, such as pharmacokinetics/pharmacodynamics, in vitro ADME (absorption, distribution, metabolism and excretion), in vitro toxicology

• Analytical chemistry services

• Pre-clinical services such as toxicology, bioanalytical and large animal study services

• Contract manufacturing

• Post-launch activities such as adverse event reporting

5

These services offer strong growth opportunities generally and demand skills and training already present in abundance in the Indiana market.

The capital markets are also taking notice of the contract services sector and diverse sources of private equity and other capital are becoming increasingly available for the growth of service providers in the pharmaceutical and biotechnology industries. Equity investors are attracted to this sector because of its short time to revenue, relatively low capital requirements, and proprietary service offerings protected by IP. The funding market for these types of investments is still not efficiently organized and early capital for startup CSPs remains in short supply. Still, as the market coheres and matures and opportunities become clearer, more investors are likely to emerge and, in the process, gain greater comfort. Venture dollars are sporadically appearing in companies offering services earlier up the value chain, while private equity remains active in build-up investments in existing CSPs. Funding for service companies is especially challenging for first-time start-ups, but more readily available for expanding or consolidating existing CSP participants or spin-outs of new CSP offerings from larger pharmaceutical parents.

For Indiana, the time is right for emerging CSPs in an appealing range of growth areas. Key assets can indeed be productively assembled to pursue new ventures with the highest prospects for success in accessing the capital markets, building the regional economy and enhancing our signature strength as a national center for the development and manufacturing of innovation.

6

II. PURPOSE AND OBJECTIVE

As a business model of growing “disaggregation” (specialization in high value competencies, outsourcing others) becomes a new standard for fully integrated pharmaceutical and large biotechnology companies, demand is escalating for high quality contract service providers. This demand results not only from a series of pressures upon pharmaceutical and large biotechnology companies, but also from the trend of biotechnology start-up enterprises operating in a virtual model as an alternative to adding fixed-costs and infrastructure. Outsourcing activity is accelerating. Backlogs, caused by capacity shortages, are currently commonplace in certain service segments. The biopharma contract services industry is experiencing double digit growth.

Based on our extended research, BioCrossroads believes this growth rate will not only be sustained, but increase as the number of outsourced services rises. The contract services industry, in our view, is disorganized and marked by (seemingly contradictory) movements toward both consolidation of global, full service providers, and also continued fragmentation of hundreds of regional and niche service providers serving other specialized market segments.

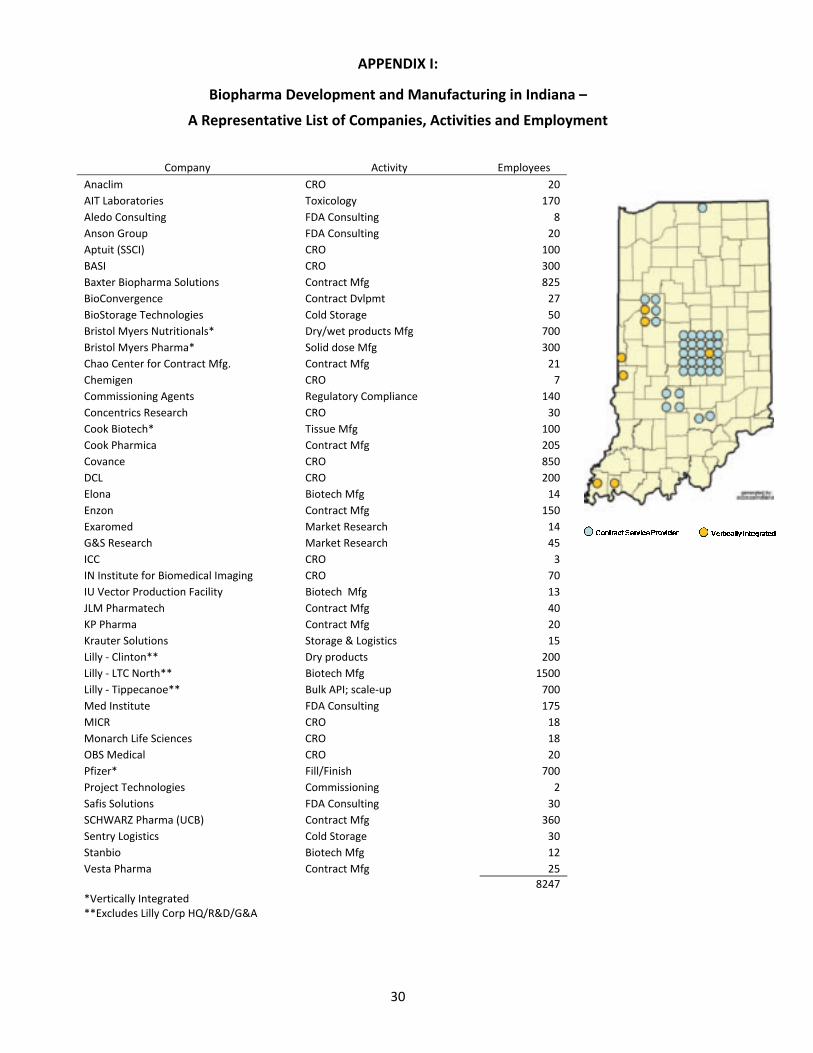

Indiana is one of only a limited number of U.S. locations having large pools of skilled employees experienced in the FDA compliant environment of drug discovery and development. In this region, opportunities exist to capitalize on rising demand throughout the contract services market and to build upon established industry infrastructure and assets. To illustrate this capacity, BioCrossroads has cataloged Indiana’s current assets on a map depicting the concentration of biopharmaceutical manufacturing and development facilities already representing more than 8,000 jobs within the state. That asset map is included as Appendix I to this report.

This report will define the growing impact of the contract services industry, address funding issues faced by emerging service companies and identify specific market opportunities as industry disaggregation and outsourcing accelerate amid rising research and development expenditures. Substantial data is readily available addressing trends, outlooks and strategies of the contract services industry and research and development functions of pharmaceutical companies. Our research seeks to utilize that data as a resource and translate it for application in the current market.

This report is the product of primary and secondary research conducted through the aggregation and synthesis of industry reports, in-person analyst consultations, and private conversations with both company and funding participants in the pharmaceutical and biotechnology industries. For convenience, a glossary of certain technical terms and abbreviations used in this report is set forth in Appendix VI.

7

For Indiana’s purposes, by identifying optimal emerging opportunities, utilizing existing business and workforce assets, and developing a strategy to facilitate early stage access to capital, a thriving biopharma contract services market – serving both pharmaceutical and biotechnology customers – presents compelling possibilities.

III. OVERVIEW OF PHARMACEUTICAL AND BIOTECH MARKET FORCES

Increasing costs and decreasing efficiencies are leading to a convergence of outsourcing activities for both pharmaceutical and biotechnology companies

The pharmaceutical industry today is a world of well-documented and increasing pressures. Topline factors, such as increasing regulatory roadblocks; payor consolidation and demands for greater transparency; pending patent expirations; risks from early and evolving science; increased development expenses; escalating market and investor impatience; and growing needs for more flexible business models moving from fixed to variable cost outlays, are all familiar facts of life for fully integrated pharmaceutical and mature biotechnology companies (“FIPCOs”). In this environment, FIPCOs will indeed become more nimble and flexible fully integrated pharmaceutical networks (FIPNETS) by increasing focus on core competencies while looking to outside service providers and strategic partners for assistance in validating, developing and bringing products to market through a far more virtual network of business relationships. Contract Research Organizations (CROs), independent drug discovery and development firms, Contract Manufacturing Organizations (CMOs), Contract Sales Organizations (CSOs), and other contract service providers will thus all become even more important partners in an era of constant change. As partnering continues and more work is shifted from FIPCOs to contract service providers, future job growth in the biopharmaceutical industry will see a similar shift as well.

Alison Sahoo, in a 2007 Business Insights report (“Optimizing Partnerships with Contract Organizations”) identifies the most important drivers of outsourcing in the biopharmaceutical industry as:

• Greater number of clinical trials;

• Increased complexity of clinical trials and regulatory submissions;

• Greater amount of data required from clinical trials;

• Rising cost pressures on pharmaceutical companies;

• Growing pressures to bring drugs to market more quickly; and

• Improved image of CROs.

8

As summarized in the Pharmaceutical Researchers and Manufacturers of America (PhRMA) 2007 Industry Profile, R&D spending in the pharmaceutical industry reached $55.2 billion in 2006 and is projected to grow to $75 billion by 2008. This growth is fueled by an increase in scope of research resulting in larger and lengthier studies, and is also influenced by a shift in focus both on the type and number of drugs under development.

While arguably some approval process improvements have been made on the regulatory front, including the added resources for new product review resulting from the Prescription Drug User Fee Act (PDUFA), the overall time to market for a new drug has not decreased. The average duration of clinical trials has risen by approximately 1.5 years since 2001, bringing the time to take a drug through clinical development and approval to 8.5 years. This increased time frame also fuels cost pressures and magnifies the importance of R&D efficiency.

Rising cost pressures and increased time to market are further intensified by key patent expirations and increased generic competition. A recent article in the Wall Street Journal (“Big Pharma Faces Grim Prognosis”, December 6, 2007) cites analyst forecasts to the effect that over the next five years, patents will expire on more than three dozen brand-name drugs accounting for $70 billion in annual U.S. sales – roughly half of the companies’ total combined U.S. sales for 2007.

Many large pharmaceutical companies are implementing measures to spread risk and focus on core competencies. AstraZeneca, for example, announced plans in September 2007 to outsource all drug manufacturing activities within ten years. The company’s leadership stated that manufacturing is no longer viewed internally as a core activity, and the company is implementing actions aimed at becoming a pure research, development and marketing organization while spreading risk and utilizing variable cost contracting for services that do not fit within a narrowing focus. This announcement is part of an overall cost-cutting initiative, including 7,600 announced job cuts, as AstraZeneca faces several patent expirations over the next several years.

Similarly, in December 2007, Bristol-Myers Squibb announced it would cut approximately 4,300 employees in a restructuring of operations that will include sale or closure of half of the company’s 27 manufacturing facilities worldwide, outsourcing additional manufacturing, and winnowing of the BMS portfolio of 500 products by 60%.

In addition to pure outsourcing arrangements, pharmaceutical companies are establishing strategic alliances and making innovative internal changes to boost R&D productivity. For example, Pfizer announced in October 2007 the appointment of a new head of R&D concurrent with the launch of an independent biotech R&D center in San Francisco. These announcements

9

follow the announcement earlier this year establishing the Pfizer Incubator in La Jolla, California with capacity to house up to eight start-ups for potential in-licensing candidates. All of these moves are intended to increase productivity, decrease time to market and intensively focus on building a world class biotherapeutics pipeline.

Similarly, Novartis has implemented an innovative variation on its internal venture capital fund by recently creating the $200 million Novartis Option Fund. This new fund is structured on an experimental investment strategy that makes seed investments to help start-up companies get from idea to proof of concept. In addition to the traditional seed investment, which in itself is in scant supply in today's market, an option fee allows Novartis to exercise licensing agreements if certain milestones are met. This option fee is separate from and does not dilute equity in the start-up. The success of this structure is yet to be proven, but Novartis is seeking a platform to enable early access to innovative technologies. According to a recent published statement of Novartis Chairman Daniel Vasella, moves like this are necessary in an environment in which “[we] must rethink assumptions, from innovation to markets to sales to promotion”.

Pharma is not alone in addressing change. Less frequently acknowledged are the parallel and convergent pressures toward disaggregation driving the development of the expanding early-stage biotechnology business. Here, such pressures come less from public markets, or regulatory authorities, than from the private venture capital markets that have traditionally fueled most of the growth of new biotechnology companies. While venture investments in this sector continue to skyrocket - $3.2 billion was invested in the sector during 2006 according to an industry leader participating in the Indiana Life Sciences Forum in October 2007 - the nature of these investments has evolved considerably over the past decade.

For example, according to 2006 data supplied by DowJones VentureWire, an average venture investment of $48 million in a biotechnology company in 2000 yielded an average exit through an initial public offering of $280 million over a relatively short (2-4 years) cycle of investment. Today, the average venture investment in a pre-IPO biotechnology company has risen to $103 million – and the average biotech IPO has plummeted to an average $110 million. Thus, the economics of the venture market are urging an increasing strategy of an earlier sale or strategic acquisition by a larger biotechnology or pharmaceutical partner, as an alternative to a later or lower-value IPO. And with this strategy comes a disincentive for the venture investors to promote – or even tolerate -- true and full biotech company formation when value is earliest and most profitably demonstrated through validating the underlying science, rather than building a successful new business.

Consequently, FIPCOs become FIPNETs through a process of outsourcing and disaggregation, while venture economics lead biotech companies to the same result from the opposite

10

direction by ensuring that these enterprises avoid vertical integration from the beginning. More and more, venture-backed biotech companies will be utilizing variable-cost contracting for services with high quality service providers rather than adding the fixed costs of infrastructure and internal development functions to largely virtual enterprises. As a result of these convergent trends, CSPs are experiencing substantial employment growth. According to a senior industry analyst, the sector experienced a 12% increase in headcount in 2006, following an 18% increase in 2005. As illustrated by Medco’s November 2007 decision to locate the world’s largest automated pharmacy in Central Indiana, over 20 competing locations and create 1,300 jobs; access to a skilled workforce is a determining factor in expansion in the biopharmaceutical industry. Just as access to two top-tier university pharmacy programs drove much of Medco’s decision (see Appendix II), Indiana has a breadth of talent both within industry and higher education (including the nation’s second largest medical school and two of the nation’s top five analytical chemistry programs) that will be able to meet the expanding workforce needs of contract service providers (CSPs) as outsourcing accelerates.

This point, and the opportunities for Indiana-based discovery contract services providers to fill resulting needs, has been reiterated to BioCrossroads time and again over the course of two years of extended contact with multiple biotechnology companies (and strategy organizations such as CONNECT) in San Diego. Other contacts we have explored in other biotechnology centers, such as San Francisco and Boston, underscore the fact that substantial outsourcing for discovery and development services is increasingly the norm for emerging biotechnology companies, irrespective of geography.

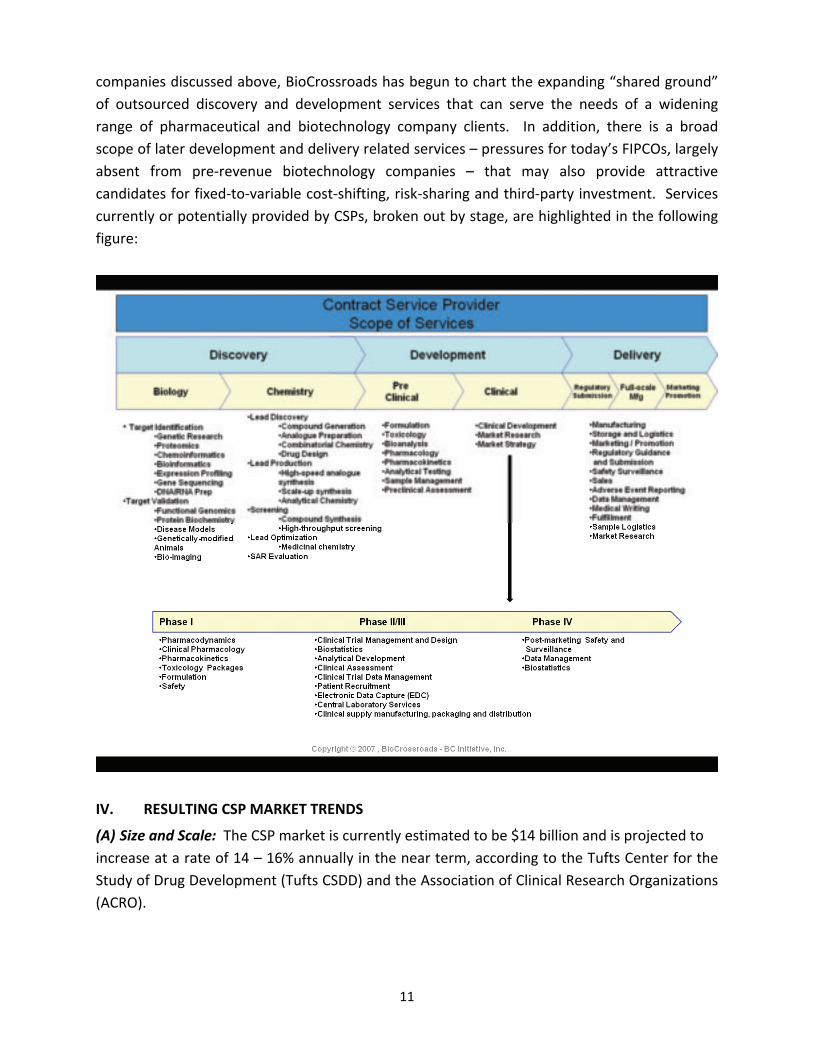

Defining and characterizing the outsourcing market space Contract Research Organizations are commonly defined as organizations that offer clients a wide range of pharmaceutical research services, including many specific clinical/pre-clinical activities. These services include: clinical trial management, central laboratory services, product development and formulation, FDA regulatory services and other complementary services necessary to move a new drug or biologic from discovery to FDA marketing approval. Industry data categorizes the drug discovery and development services market under the general “CRO” heading, with differentiations made between large-scale, full-service global CROs, and specialty regional or niche service CROs. In practice, key service providers in the pharmaceutical and biotechnology industry fall in various places along the spectrum of independent drug discovery and development firms, and CROs, CMOs and CSOs are rarely tracked independently. For purposes of this discussion, we refer to this entire array of third-party organizations as “Contract Service Providers” (CSPs). The CSP landscape from discovery through development and commercialization is vast and specialized. But, based on the converging trends for outsourcing by both pharma and biotech

11

companies discussed above, BioCrossroads has begun to chart the expanding “shared ground” of outsourced discovery and development services that can serve the needs of a widening range of pharmaceutical and biotechnology company clients. In addition, there is a broad scope of later development and delivery related services – pressures for today’s FIPCOs, largely absent from pre-revenue biotechnology companies – that may also provide attractive candidates for fixed-to-variable cost-shifting, risk-sharing and third-party investment. Services currently or potentially provided by CSPs, broken out by stage, are highlighted in the following figure:

IV. RESULTING CSP MARKET TRENDS

(A) Size and Scale: The CSP market is currently estimated to be $14 billion and is projected to increase at a rate of 14 – 16% annually in the near term, according to the Tufts Center for the Study of Drug Development (Tufts CSDD) and the Association of Clinical Research Organizations (ACRO).

12

Today’s market is comprised of an estimated 1,100 CSPs worldwide with significant levels of differentiation and scale. Only the top ten (most of which are located in the U.S.) contract providers are truly global, full-service CSPs well equipped to vie for the bulk of the pharmaceutical industry’s increasing needs. Approximately 100 other CSPs can be categorized as full-service providers, but do not operate on a global scale. These are regionally focused competitors for a different clientele, namely smaller pharmaceutical and biotechnology companies. The remaining CSPs are niche providers focused on more specialized service offerings, often based on nascent technologies. According to a 2007 Business Insights report (“The CRO Market Outlook: Emerging markets, leading players and future trends”), what niche providers lack in breadth they make up through depth of knowledge in their specialty fields.

(B) Consolidation and Fragmentation: The global CSP market is consolidating through mergers and acquisitions of smaller niche and mid-size regional CSPs, in response to capacity shortages caused by increased outsourcing by the pharmaceutical industry. However, as consolidation serves as a response to pressures from preferred provider relationships within the pharmaceutical industry, a void results elsewhere in the market serving venture-backed biotechnology firms. Because the larger, consolidated CSPs give preference to their larger pharmaceutical customers, biotech companies are finding themselves at the “back of the line” for these same services even though timing and reliable scheduling are acutely important to a biotechnology company’s venture capital investors. Thus, as the pharmaceutical industry increases reliance on a shrinking number of preferred provider relationships, biotechnology firms (and their investors) will struggle to identify their own preferred providers who offer high quality service without lengthy lead times, jeopardizing product development. A whole new sector of smaller, more responsive, high quality providers will likely be needed to serve these companies. A recent article by Jim Miller, in BioPharm International (“Outsourcing Insights: Booming Biopharma Pipeline Straining CRO Capacity”, May 1, 2007), finds capacity shortages for biotechs causing lengthy lead times and annual price increases of up to 5%. These smaller, high quality providers are beginning to organize as an industry and are increasingly forming alliances to enhance each other’s service offerings. An industry organization, the Pharmaceutical Industry Contract Research Association (PICRA), aids this process by creating a forum to share information and explore opportunities. In a 2007 Business Insights report (“Optimizing Partnerships with Contract Organizations”), Alison Sahoo provides an Indiana example of PICRA members formalizing a contract research partnership. Indiana-based MicaGenix is a pre-clinical service provider specializing in mutagenicity, histopathology and regulatory preparation and Bioanalytical Systems (BASi), also based in Indiana, provides complementary services such as pharmacokinetics (PK), pharmacodynamics (PD) and toxicology. The two entered into an alliance to market each other’s services in order to increase market penetration and strengthen client relationships. Concurrently, BASi also

13

entered into an alliance with Indiana-based INCAPS (now Monarch Life Sciences) to promote proteomics and protein characterization studies as an additional capability. Overall, with the volume of early stage development candidates continuing to grow and the pharmaceutical industry conducting more extensive early-stage testing on a wider range of targets, emphasis is being placed on the need to prove safety and efficacy as quickly and cost-effectively as possible with defined benchmarks along the way. The current marketplace of discovery and development service providers will not be able to meet the mounting demand for services.

(C) Framework for Emerging Opportunities: In this environment, demand is especially high for bioanalytical and analytical chemistry, pre-clinical, Phase I and other early phase services once perceived as core functions of integrated pharmaceutical and biotech companies. (“The CRO Market Outlook: Emerging markets, leading players and future trends” Business Insights 2007) Services such as in vitro ADME (absorption, distribution, metabolism and excretion) and toxicology are becoming attractive outsourcing candidates. For example, a 2005 report from Cambridge Healthtech Advisors (“Successful Outsourcing of Pharmaceutical R&D: Trends and Strategies”) found that nearly all pharmaceutical companies plan to outsource at least 20% of ADME services over the next three years, with similar plans from most of the surveyed biotechnology companies, to outsource at least 20% of early development operations during the same period. Moreover, analyst reports resulting from the Society of Toxicology annual meeting, held in March 2007, describe a preclinical services industry that is growing at the rate of 15 - 20% per year. However, these reports further find that it would take two to four years for any expanded capacity to come online. Due to the rising demand for early-phase services, companies attending the conference reported backlogs of up to six months in study scheduling.

In the current market, attractive outsourcing functions generally have similar characteristics. Access to a high quality service provider that can provide the requisite service is essential, and a value proposition consisting of increased speed and/or decreased cost provides the incentive for undertaking the disruptive action that outsourcing can represent.

Functions that are process-oriented or can be otherwise seen as commoditized services are especially conducive to conversion to variable costs, thereby extending company resources available to focus on core functions. In contrast, core business functions such as strategic planning and lead discovery that are highly specialized, conducted with proprietary methods

14

and holding potential for IP creation, present particularly high “barriers” to becoming feasible outsourcing candidates. The following table illustrates this distinction:

(D) Challenges to Outsourcing

(1) Sponsor Transitional Issues: It is worth noting that, for many traditional FIPCOs, cost-effective outsourcing remains an evolutionary process. A widely noticed aversion to relinquishing control by pharmaceutical clients is inhibiting the realization of the full benefits of outsourcing. In some cases, outsourcing actually leads to increased costs due to a lack of clearly defined objectives, vague standards for demonstrating equivalent quality, and inadequate staff training. According to reports from the “Partnerships with CROs” conference sponsored by the Institute for International Research in April 2007, large pharmaceutical companies have generally demonstrated a clear strategic vision to maximize outsourcing potential, but have not yet developed the necessary infrastructure to support effective implementation and management of outsourcing relationships. Still, the very fact that pharmaceutical company utilization of outsourcing continues to increase only underscores the significance, beyond pure considerations of cost, of other outsourcing advantages – including productive concentration of outside expert resources, risk sharing, and shifting from fixed to variable-contract expenses for accounting purposes.

(2) Offshoring vs. Domestic Outsourcing: Particularly for the industrial Midwest, “outsourcing” and “offshoring” often appear to be two sides of an unfortunate coin. To succeed in a strategy seeking to build a credible next generation of service businesses close to home, many fear that there is also an undeniable challenge in erecting sufficient “barriers to exit” to keep the resulting companies from going the way of steel and

15

automotive supply chains in migrating to lower-cost, rising-skill Asian and other offshore labor markets. For the moment, the CSP sector is one of U.S. and European dominance. Of the total 1,100 CSPs worldwide, approximately 900 are based in North America and Europe. Nevertheless, the CSP industry is increasing rapidly in Asia, with marked and substantial growth in both China and India. Prospects for achieving lower costs without sacrificing quality or speed; increasingly sophisticated scientific and technical workforces; access to new communities of “treatment-naïve” patients; and favorable tax climates are all contributing to the expansion of established CSPs and, on a smaller scale, the establishment of new stand alone CSPs in Asia.

For an Indiana-based strategy, two sets of factors make offshoring of services and product development arguably less of an immediate “threat” in the biopharma services sector than in other areas of traditional manufacturing and production.

First, there are commonly identified challenges for all pharmaceutical and biotechnology companies when considering offshore alternatives, especially in India and China. These include well-documented concerns over intellectual property protection, language barriers (China), clinical study quality and integrity in remote locales, and perceived problems of delay around multiple layers of foreign regulatory approvals. Additionally, as offshoring continues for technology-intensive industries, the “labor arbitrage” between the costs for skilled employees in U.S. vs. Asian markets will inevitably begin to close. For example, a Wall Street Journal article from July 2007 (“Some in Silicon Valley Begin to Sour on India”) identified rising labor costs, as well as hidden time and geographic outsourcing costs, as drivers for some companies to begin looking for alternatives for overseas operations.

Beyond this first set of general challenges to biopharma offshoring, there are inherently differing vantage points for pharmaceutical companies and biotechnology companies when assessing the feasibility of maintaining a virtual business structure encompassing offshore components. Pharmaceutical companies often have strong and deep management and administrative resources, global sales forces and markets, and multiple needs for access to new populations of “treatment-naïve” patients throughout the world. For these sophisticated organizations, offshore service providers in Asia – especially for clinical services – are simply one more major, but manageable, coordination challenge. Furthermore, for many of these large pharmaceutical companies, that coordination challenge may be mitigated considerably by the presence of familiar and preferred U.S. CSPs, such as Quintiles or Covance, and on the

16

international scene in substantial and growing Indian, Chinese and other offshore operations of their own.

However, for many biotechnology companies, particularly early-stage companies with a limited number of products under development, no international workforce, and scant administrative and management resources, the attractions of offshoring are arguably very different. For these smaller biotechnology companies, service provider proximity, and more easily enforceable intellectual property protection are often necessary ingredients to assure reliability and manage outsourcing risks with only a minimum of project management (or any other) infrastructure. Once again, this point on the value of proximate U.S. discovery and development contract service providers has literally been “brought home” to BioCrossroads time and again in our consultations with small biotechnology companies and their sponsors in San Diego and other U.S. discovery centers.

Some service segments present more attractive candidates than others as biopharmaceutical companies do look offshore for outsourcing partners. As noted above, clinical trials are an example of a subject and administrator-intensive service that may benefit from looking offshore for expanded capacity. Conversely, segments such as pre-clinical services or contract manufacturing present specific barriers to achieving goals of matched quality and cost savings. Pre-clinical services, for example, rely on advanced facilities and equipment and a small number of highly trained scientists to drive value. According to Business Insights (“Partnering with Contract Organizations,” November 2007), India, China, Latin America and Eastern Europe currently lack the pre-clinical infrastructure (and provider presence) of the U.S. and Western Europe, and contract manufacturing, in lower-cost countries, also often has unclear cost advantages. For similar reasons as the pre-clinical sector, manufacturing is less labor intensive and has a high fixed-cost component of equipment that inhibit the level of savings that may be achieved.

Thus, though not without risk, an outsourcing strategy contemplating a significant (though not exclusive) ongoing role for U.S.-based CSPs seems warranted for Indiana, especially in light of our prospects for involving biotechnology as well as pharmaceutical company consumers of these services. Particularly for biotechnology companies, and especially in the immediate term, sponsors are very likely to look first to U.S.-based providers to set the standard of service. Ultimately, quality, proximity, and the absence of cultural barriers should allow reliable and high-skilled U.S. CSPs to continue to enjoy a significant share of the growing CSP market, even as that market inevitably becomes more global and more competitive.

17

(3) A Need for Instructive Examples: Outsourcing is a well understood and documented trend in other technology-intensive industries, including information technology and telecommunications, but, for many, it is still regarded as a relatively new development in the pharma and biotech sectors. In truth, outsourcing here is also not a new concept and has been broadly utilized by the pharmaceutical industry as a short-term, tactical solution to address capacity issues. A highly instructive example of this fact can be found very close to home at the Indianapolis-based North American central laboratory operations of Covance. Less than 25 years ago, a centralized method for efficiently and accurately collecting and reporting data from clinical trials did not exist. Central laboratory functions were housed and performed within every large pharmaceutical company, but industry standards were lacking to ensure efficient access and accuracy of data. By the 1980’s, there was a clearly identified need for these central laboratory services as a standardized, scalable business function. From that identification grew what is today a $2 billion central laboratory services industry.

In 1986, the world’s first central laboratory opened in Indianapolis, under the name SciCor; known today as the Central Laboratory Services division of Covance, Inc. At the time SciCor was the only company that could report timely clinical data (within 48 hours) using the same clinical trial methodology. With an error rate of less than 2%, SciCor/Covance is now the industry standard for what has become a 100% outsourced market.

Building upon the infrastructure and talent pool of locally-based Eli Lilly and Company, a strategic acquisition, and the prospect of a key contract with Lilly, SciCor was able to secure venture funding from CID Equity Partners (established and supported by the State of Indiana) to develop a quickly successful business. In 1991, SciCor was acquired by Corning, yielding sizable returns for its investors and providing the platform for a world-class contract service provider. Along with SciCor, Corning acquired Hazelton Laboratories (biological testing and development services) and G.H. Besselaar Associates (clinical trials, market support services) to build the foundations of a full-service, global CRO.

Spun out of Corning in 1997, Covance today is the global leader in central laboratory and toxicology services and the second largest drug development services company in the world. Operating 33 offices in 18 countries, Covance provides drug development services from discovery through commercialization as a high-quality comprehensive service provider and partner for the pharmaceutical industry.

18

SciCor/Covance was ahead of its time, and represented a high-risk venture at its founding. SciCor’s founders, however, identified an opportunity to create a variable cost for Lilly while commoditizing a service that could be offered to the pharmaceutical industry as a whole. Today, after 25 years of expanded service and continued profitability, Covance provides a helpful lesson for defining opportunity in an environment of increasing external sourcing of R&D activities and escalating need for allocating resources and risks. And SciCor/Covance is clearly not an isolated example. Other brief case studies of both established and emerging CSPs in other service segments are included as Appendix III of this report; and even in Indiana, there are clearly a variety of CSPs already in successful operation all along the discovery – development – delivery cycle for pharmaceutical and biotechnology products (see Appendix IV).

V. SPECIFIC GROWTH OPPORTUNITIES FOR INDIANA IN THE U.S. CONTRACT SERVICES MARKET

With pharmaceutical and biotechnology companies expanding targets and pipelines, capacity shortages are arising among many late-stage discovery and early-stage development service providers. Ksenija Jakovcic, in a 2007 Business Insights report (“The CRO Market Outlook: Emerging markets, leading players and future trends”), cites backlogs in study scheduling of up to six months as a key indicator of mounting demand causing capacity shortages. Consequently, later discovery and early development services present particularly attractive growth opportunities. The same report also finds the demand particularly strong for preclinical (ADME and toxicology), Phase I, bioanalytical and analytical chemistry services. Also, as the industry expands its focus on biologics, timely and cost effective manufacturing options that can bring products to market become increasingly important and represent an attractive long-term growth sector despite some short-term challenges.

Highlighted below are five service segments that offer strong growth opportunities in the U.S. market generally. Each of these segments also involves skills and services that are especially attractive and plausible to be sourced from the Indiana market. This is not an exhaustive list, and our research continues to identify and target opportunities to leverage current assets for growth.

1. Discovery (non-GLP) Services

Primary research gathered from private conversations with pharmaceutical companies, biotechnology companies and service providers forecasts increasing opportunities for CSPs to serve as comprehensive discovery facilitators providing early, non-GLP (good laboratory practice) services such as PK/PD (pharmacokinetics/pharmacodynamics), in

19

vitro ADME, in vitro toxicology, and other related services. Currently, cost competitive, integrated discovery CSPs capable of handling large quantities of samples with efficient turnaround times are in scant supply. Pre-clinical and specialty service CSPs have the capabilities to provide such services, but their customarily GLP-compliant processes, facilities and methods do not provide cost-effective solutions for either startups or research-based institutions to reach proof of concept and attract market interest.

Furthermore, capacity within the preclinical service sector is being strained by the large number of new drug candidates and the larger and longer safety testing that has become standard in the post-Vioxx era. These trends lead to increased cost of preclinical services and further reduce economies of outsourcing non-GLP discovery services to existing GLP-compliant providers. Few academic institutions have the expertise and capacity to perform these services at a competitive cost, and academic bureaucracy and IP ownership issues, real or perceived, have been identified as major impediments to effective turnaround time and overall quality of service from these sources.

Non-GLP discovery services are crucial to traversing what has becoming known in the industry as the “valley of death” confronted early and urgently in the biopharmaceutical discovery and development process. As described by Duane Roth, CEO of CONNECT, a globally recognized organization fostering entrepreneurship and growth in technology of the life sciences, the “valley of death” is the crucial period between initial discovery and reaching proof of concept, the point that value is created and becomes measurable by outside investors. This barrier is faced by both industry and academic institutions and is impeding innovation due to lack of access to required expertise. A highly regarded researcher from the Indiana School of Medicine stated, at the 2007 Indiana Life Sciences Forum, that innovation is “hitting a wall because scientists don’t know where to go to get the expertise to take a lead forward.”

While the market appears strong for non-GLP discovery services, it is not evident if a standalone non-GLP service provider, without more, can represent a viable business model. Non-GLP studies are shorter and smaller in scope and therefore are typically priced less than GLP studies (an established service sector). As an alternative to a stand-alone company, a large-scale, non-GLP service platform may be better suited to provide a unique point of differentiation within a larger and more comprehensive discovery and early development CSP.

2. Analytical Chemistry Services

Analytical chemistry services provide an example of non-core, process-oriented functions that are outsourced by small pharmaceutical and biotech companies out of

20

necessity and could be strategically outsourced by their larger counterparts to lower drug development costs and reduce capital expenditures. Further analysis is warranted, but it appears (and Business Insight’s “The CRO Market Outlook” report confirms) that demand is especially strong for companies providing analytical chemistry services.

Analytical methods and instrumentation are critical in PK, PD, ADME, and other early development studies (areas that are seeing the greatest demand and backlogs caused by capacity shortages). Our analysis points to growth in analytical chemistry functions based on the cited increasing demand for early development services reliant on analytical chemistry and its broader application in high growth areas such as proteomics and biomarker research.

The expertise and technical capabilities to enable proteomics and biomarker research and discovery both overlap and complement the methods and instrumentation instrumental to analytical chemistry. By building upon a robust talent pool from within industry, Indiana has the raw materials to pursue this nascent area. Talent can be drawn from Indiana University and Purdue University’s top tier analytical chemistry programs and by potentially utilizing an existing broadly collaborative CRO (Monarch Life Sciences, formerly INCAPS) that has already established a leadership position in discovery-service proteomics and biomarker development.

Analytical chemistry fits squarely within the category of “Outsourcing Candidates” in the table found on page five of this report. Such capabilities are essential to the drug discovery and development process, but do not represent the type of core, “drug hunting” activity that biopharmaceutical companies insist upon retaining in-house even in today’s resource-constrained environment. Highly specialized, expensive equipment, and the staff to run the analysis can be contracted for on a variable cost, fee for service basis. Currently, a number of CSPs appear to offer some aspects of analytical chemistry services. However, a dedicated, specialized, full-service analytical chemistry provider remains a gap to be filled in this market.

3. Pre-clinical Services

Pre-clinical services, such as outside toxicology, bio-analytical, and large animal study services are all in shortening supply as the quantity of early drug candidates increases and pharmaceutical companies increasingly look to outsource these functions. According to a senior industry analyst, toxicology and bio-analytical services comprise a $12 billion market – of which only 15% is outsourced today. As part of a pre-clinical services market that is growing at 15 – 20% per year, opportunities will steadily increase for high quality service providers that can quickly scale-up operations. As mentioned earlier in this report, expansion capacity is contemplated within the current CSP pipeline, but this capacity will likely be quickly consumed by current demand and

21

exhausted if even a single large pharmaceutical company makes a strategic decision for entirely outsourcing these functions.

As an indication of the direction of the overall market, it is instructive to look at how the largest worldwide providers of pre-clinical services (Covance and Charles River) are performing and what they are planning for the future. Both Covance and Charles River are seeing substantial growth in year-over-year revenues and backlogs. Covance, in its third quarter earnings report (October 25, 2007) noted a 19.2% increase in early development (pre-clinical) revenues compared to the same period last year. For comparison, late stage development services net revenue grew at a rate of 12.9%. Covance’s early development services (pre-clinical) comprised in excess of 50% of total revenues for the quarter and backlogs increased 26.5% signaling a shortage in capacity. Charles River experienced similar increases in the second quarter of 2007 reporting net pre-clinical services revenues up 19.4% to $163.6 million.

Growth in both earnings and backlogs will likely only increase as greater emphasis is placed on early safety testing to screen out inappropriate candidates at the earliest stage to avoid significant development costs for drugs with high potential for failure. Business Insights estimates (“Partnering with Contract Organizations”, November 2007) that 25% of the $1 billion+ now required to bring each new drug to market could be saved through better pre-clinical testing to identify failures early.

Pre-clinical service providers require greater expertise and are critically dependent on specialized equipment and highly trained personnel. These factors add to the overall capital investment required to operate pre-clinical service companies and increase competition for top-tier toxicologists and pathologists who can run the studies. Alison Sahoo, in a 2007 Business Insights Report (“Optimizing Partnerships with Contract Organizations”), cites such “relatively high barriers to entry and scarcity of resources” as compelling reasons for biopharmaceutical companies to look increasingly to high quality outsourcing partners for these services.

4. Contract Manufacturing

In line with the overall CSP market, the market for contract manufacturing services is projected to continue enjoying double digit growth. The contract manufacturing market was valued at $31.5 billion in 2005 and is predicted to approach $50 billion by 2010. The primary reason for outsourcing manufacturing is evident: costs associated with manufacturing account for up to 16% of the total costs of sales of the average drug company according to Business Insights (“Optimizing Partnerships with Contract Organizations”, November 2007).

22

The main growth driver in contract manufacturing has historically involved large scale, small molecule API (active pharmaceutical ingredient) manufacturing. That trend appears to be shifting. Existing capacity of full scale manufacturing for small molecule APIs appears to be meeting or exceeding demand for the foreseeable future and assets appear to be moving from the U.S. to tax advantaged locations and markets with lower labor costs. Consequently, the projected growth in contract manufacturing will be derived primarily from the growth of biologics manufacturing, including biologics clinical trial material manufacturing, instead of small molecule API production.

A key indicator of these trends in the contract manufacturing market is the sales data for existing facilities. A recent article by Jim Miller in Pharmaceutical Technology (“CMOs Join Facility Swap Meet”, September 2007) analyzes facilities currently on the market and recent facility sales. CMOs have traditionally been built through acquisition of excess supply of facilities owned by large pharmaceutical companies. In a shifting trend, CMOs are now becoming common sellers of facilities to divest underperforming assets. Of the facilities that are on the market, small-molecule API facilities are the most difficult to sell unless they have high-containment capabilities.

As demand for manufacturing shifts from traditional high volume solid dose production to new formulations and dosages requiring greater expertise and different equipment, many facilities that are currently manufacturing patent protected blockbusters face the possibility of obsolescence as generic competition rises and patents expire. As a result, many pharmaceutical companies are beginning to outsource their own excess capacity. Alison Sahoo, in a 2007 Business Insights Report (“Optimizing Partnerships with Contract Organizations”) points out that Abbott, Alpharma, Alza, Bayer, GlaxoSmithKilne, Pfizer, Sanofi-Aventis and Shering all offer CMO services today.

Large molecules present a different story. According to Business Insights (“Partnering with Contract Organizations,” November 2007), there are currently 650 biotech drugs in development. Many of these are monoclonal antibody therapeutics which are very expensive to produce and offer a substantial revenue opportunity for CMOs. Attractive market opportunities include biologic capabilities in general, and especially injectables manufacturing and/or the capacity to manufacture high-potency APIs.

The complex structures of biological drugs require an extremely precise manufacturing process. And especially for biotech companies, navigating this process is challenging, since the FDA requires that material used in Phase III studies for biopharmaceuticals must be produced through employing the final manufacturing process in the final manufacturing site for commercial production. Biomanufacturing facilities require large capital investments and incur significant operating expenses. The lean, virtual structure

23

of biotechnology drug developers is not conducive to asset ownership of manufacturing facilities, enhancing the cost variability of outsourcing biologics manufacturing and creating an attractive market for GMP biomanufacturing CSPs.

Additionally, by outsourcing manufacturing functions, biopharmaceutical companies can achieve cost variability and spread risk to manufacturing partners. Business Insights recently quoted the cost of building a commercial manufacturing facility at $400 million (“Biomanufacturing Strategies: Market drivers, build-vs.-buy decisions and opportunities in contract relationship management”, September 2007). In the post-Vioxx era of heightened safety regulation and increased post-launch studies, biopharmaceutical companies can hedge risk by contracting for service and spreading exposure to third parties rather than undertaking large capital investments prior to establishing a market for their new products.

5. Business Services

Opportunities also exist to achieve the convergent objectives of pharmaceutical and biotechnology companies through disaggregation further down the value chain in processes that support products post-launch. For example, adverse event reporting, data management and medical writing are all functions likely to attract market attention as disaggregation continues. Adverse event (AE) reporting provides a particularly interesting example of a function performed almost entirely in-house by large pharmaceutical companies today, but involving process-oriented services even more segregable and scalable for third-party investment than many other traditionally outsourced development services. Combined with the product support functions and infrastructure of an in-bound call center, an opportunity exists to leverage expertise of the regulatory process found within the ranks of FIPCOs. By shifting labor, facility and infrastructure costs from fixed to variable, this essential, but non-core function offers cost saving potential for a critical service demanding rigorous standards and procedures and a high-quality talent pool. AE reporting and call center outsourcing has already begun and is a sector with strong growth potential. AE reports, for example, have grown at a 25% compound annual growth rate (CAGR) for the past decade and a senior industry analyst predicts that PDUFA IV that was approved in September 2007 will lead to a substantial increase in AE monitoring. Two firms of note are currently active providers: Telerx Healthcare and PPD, Inc. Telerx is a privately held company with call center functions as its core operation. Telerx was spun-out from Merck’s call center operation and is currently a wholly owned

24

subsidiary of Merck. Telerx has a dedicated healthcare and pharmaceuticals practice that provides expertise in regulatory requirements (AE reporting), medical education, and clinical trial recruitment. Telerx is privately held and therefore an analysis of financial performance and market penetration is unavailable. PPD is a publicly traded global CSP providing discovery, development and post-approval services to the pharmaceutical and biotechnology industries. PPD’s Medical Information and Professional Contact Center (MIPCC) division provides adverse event reporting and call center services to its clients. The MIPCC division and Telerx would be both instructive examples and key competitors to any new venture in this still new and largely unorganized market sector that provides compelling strategic outsourcing opportunities.

VI. CAPITAL MARKET INTEREST IN SERVICE VENTURES

To what extent are the opportunities identified in the previous section IV attractive to the private equity and venture capital markets?

Service companies offer convincing attributes, even in comparison to therapeutic and other product-based companies in the pharmaceutical and biotechnology sectors. Compared to product-based companies, service companies require a relatively low capital investment and often possess a clearer and quicker path to revenue. While sales cycles may be long in penetrating the large pharmaceutical market, such cycles generally represent a fraction of the time that it takes to bring a drug to market and are often supplemented through revenue opportunities presented by smaller biotech companies. From an investor standpoint, service ventures also possess strong assets and create barriers to entry through IP held on proprietary methods that can create real value. CSP growth has been strong and steady across most sectors. Returns continue to be impressive in comparison with other investments.

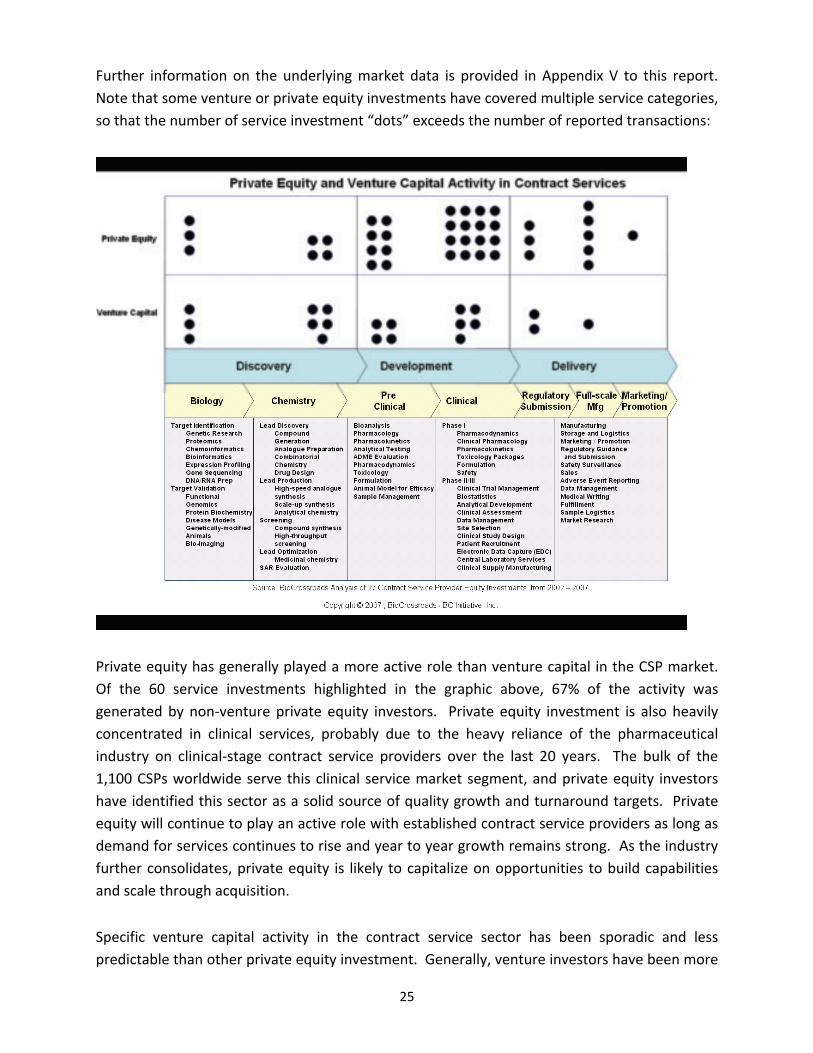

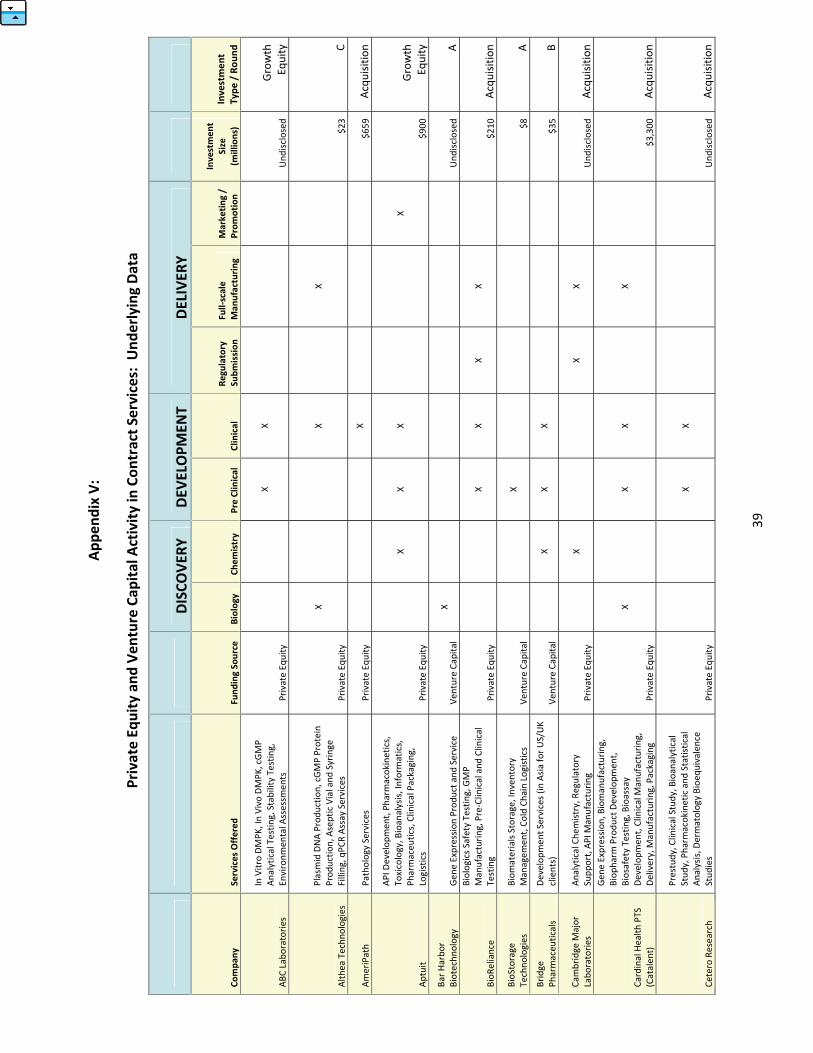

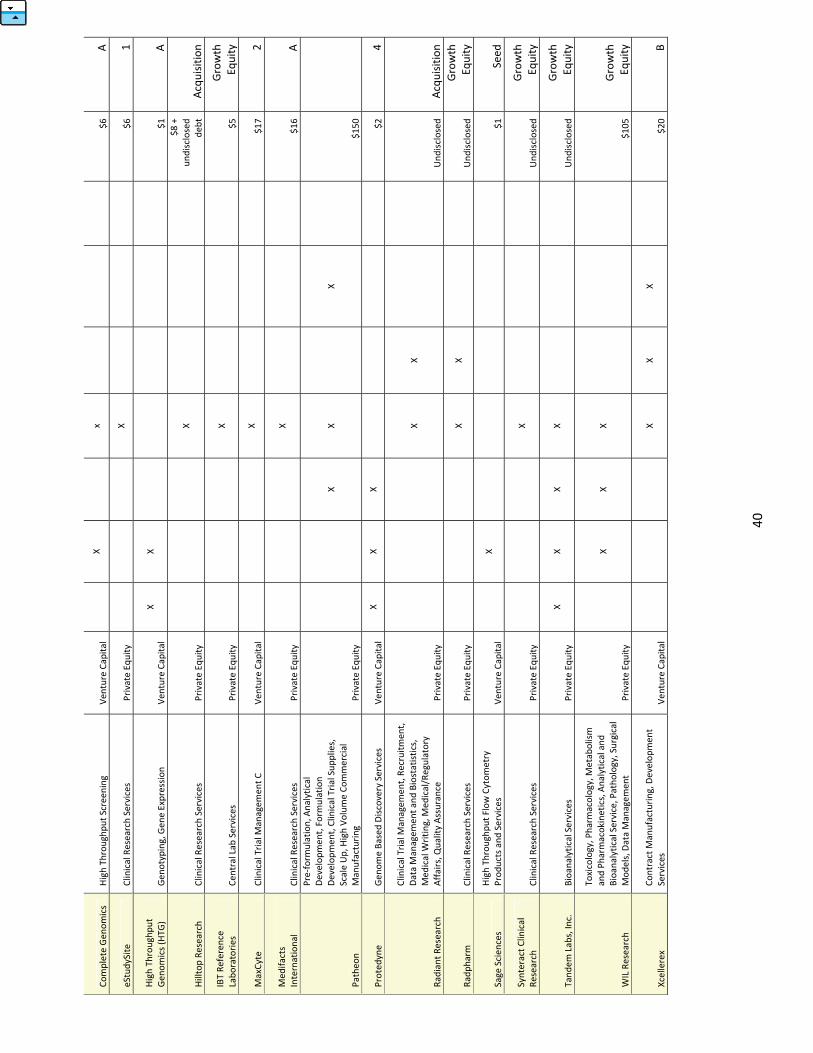

Despite these “investable” characteristics, only limited data is available regarding current investment activity in the contract services industry. Because of the shortage of organized market information, BioCrossroads has compiled its own initial survey of funding activity in the contract services sector. This is not an exhaustive list of recent market activity, but represents a substantial sampling that casts what we believe to be a helpful light on overall industry trends. The graphic below depicts disclosed venture capital and private equity activity in CSP financing (both Indiana and non-Indiana based companies) over the past five years and identifies both the type of investment and type of service.

25

Further information on the underlying market data is provided in Appendix V to this report. Note that some venture or private equity investments have covered multiple service categories, so that the number of service investment “dots” exceeds the number of reported transactions:

Private equity has generally played a more active role than venture capital in the CSP market. Of the 60 service investments highlighted in the graphic above, 67% of the activity was generated by non-venture private equity investors. Private equity investment is also heavily concentrated in clinical services, probably due to the heavy reliance of the pharmaceutical industry on clinical-stage contract service providers over the last 20 years. The bulk of the 1,100 CSPs worldwide serve this clinical service market segment, and private equity investors have identified this sector as a solid source of quality growth and turnaround targets. Private equity will continue to play an active role with established contract service providers as long as demand for services continues to rise and year to year growth remains strong. As the industry further consolidates, private equity is likely to capitalize on opportunities to build capabilities and scale through acquisition.

Specific venture capital activity in the contract service sector has been sporadic and less predictable than other private equity investment. Generally, venture investors have been more

26

attracted to companies providing later stage discovery and early development services, with 60% of reported venture investment funding discovery and pre-clinical work. Further, certain venture investors may have a unique perspective on (and added incentive to invest in) this segment of the market, if they have also made investments in biotechnology and other product-focused companies for which these services are in high demand.

VII. FINDING, FORMING AND FUNDING SUCCESSFUL SERVICE VENTURES

Service Company Formation and Capital Resources

Given the most promising areas for new investment, and the current trends for financing CSPs within the capital markets, what are the best ways to organize new CSP opportunities in Indiana to maximize the potential for third-party investment? There are three general models for new company formation in the contract services industry. Each of those three models presents unique attributes and challenges for both venture investors (attracted to growth through new venture creation) and private equity investors (attracted to investments that establish new opportunities for revenue expansion).

Pure startup CSPs are likely to have the greatest challenges. Such entities, seeking to form new companies without a large pharmaceutical company or other credible CSP-sponsoring “parent,” will have limited access to the capital markets. The long sales cycle into large pharmaceutical companies (2 – 3 years has been a standard experience) provides a barrier to entry to many start-ups. Patient investors at seed stages and throughout the ramp up sales cycle will be both rare and crucial to the survival of new CSPs entering the market. Members of the investment community participating in BioCrossroads Service Venture Funding Discussion in May 2007 concluded that start-up service ventures face particularly high barriers to early stage funding due to unclear exits, significant variable costs and a perceived lack of specialized markets that make many IP-based product companies attractive to investors. While the start-up CSP may target biotech companies with typically shorter sales cycles, the time to establish a portfolio of biotech clients that can provide a revenue stream comparable in size and reliability to that of a large pharmaceutical client would probably be significant and discouraging to venture and private equity investors alike. The leadership of the new CSP would likely need to deploy personal capital and attract funds from angel investors and grants to commence operations and growth before venture dollars become accessible.

Smaller companies and start-ups face exposure to project cancellations and cash flow shortfalls making their operations extremely vulnerable. Alison Sahoo, in a 2007 Business Insights report (“Optimizing Partnerships with Contract Organizations”) states that “this vulnerability has been a driving force behind the number of research site closures, as well as several highly publicized CRO bankruptcies, such as that of aaiPharma in 2005.” This volatility has led biopharmaceutical companies to significantly increase their diligence processes prior to selecting outsourcing

27

partners. In short, start-up CSPs are an obvious, but generally not the best, option for new CSP formation in this market.

A local expansion of an existing CSP is a more promising model for forming a new service offering. By identifying assets in a market such as a skilled workforce and a demand for an expanded service offering, an established CSP can be well positioned to enter into, or expand its presence, in emerging markets. Strong historical growth in the industry and the solid revenue base of established CSPs should readily attract suitable capital to an expansion effort. For global CSPs that are generally large, publicly traded and enjoying ready access to credit, there are a variety of debt and equity alternatives to finance expansion into new markets. For regional/niche sector CSPs with an existing revenue stream, customer base, and an identified growth strategy, the financing options are fewer, but venture investors may still look positively on expansions into emergent service offerings and geographic regions with demonstrated demand. As noted earlier, certain venture investors may also have the special strategic opportunity to achieve dual goals through potentially high-yielding investments in CSPs that may in addition be able to provide critical and cost-effective services for the development of other biotechnology product companies in the VC’s portfolio.

A spinout of a large pharmaceutical company offers an especially attractive model for forming a new CSP. Access to talent, assurance of key leadership, and an industry sponsor offering the prospect of early and sizable contract revenues are all benefits of this model. In addition to know-how, the sponsor can provide access to key personnel for leadership, physical assets and start-up capital. Venture investors will be able to see a clear path to revenue with an experienced business team and structure that is likely to surmount and surpass the rigorous procurement hurdles of large pharmaceutical companies. These attributes will all likely reduce the long sales cycles that otherwise present significant challenges to emerging CSPs. Private equity investors implementing a build-up or roll-up strategy could be attracted for similar reasons as VCs and would likely display interest in a pharma spin-out if the outsourced function offered demonstrably complementary (and supportive) services for the investor’s other portfolio companies.

It is worth noting that experience with corporate spin-outs in Indiana and elsewhere underscores certain inherent challenges in considering this model. First, to the extent that a spin-out carries with it existing (often, senior) “rebadged” employees from the sponsoring entity, these employees typically come with higher expectations and resultant costs for salary and benefits than others who might be hired from a presumably more competitive external marketplace. Ultimately, the ability of these transitioning employees to share in the upside equity potential of a successful new business should lead to greater openness to risk and higher tolerance for financial flexibility. Still, the challenges of such transition will be substantial and

28

should be taken into account both as likely additional start-up expenses and also as factors to consider and address when identifying and recruiting these key transitioning employees.

Second, as is clear from the longer tradition of outsourcing within the information technology industry, the transition to a more virtual structure implies a variety of new roles and expectations. Change is substantial not only for those employees who are rebadged, but also for those employees who are retained within the sponsoring company and suddenly responsible for managing (without replicating) the performance of their recently outsourced counterparts and other new company personnel (see Thompson and Arian, Towers Perrin, “Three Keys to Outsourcing Success: People. People. And People.” EDS, June 25, 2007)

“As corporations shift [IT] operational arrangements to a vendor, the day-to-day job responsibilities of the retained [IT] organization change markedly. The hands-on project management style familiar to most employees must be replaced by supplier management skills. Instead of dealing directly with their line clients, employees must now act alongside their outsourcer as part of a two-party team to address clients’ needs. And as clients’ needs change, employees must repress the urge to intercede directly with clients and instead communicate those changes to the outsourcer for handling. Perhaps most important, employees need to be strong advocates for change within their organizations.”

This lesson would not appear to be limited to one industry and, again, underscores the importance of developing an effective human resources strategy as well as effective business planning and investment strategies to ensure the success of any spin-out venture.

VIII. CONCLUSIONS

As Outsourcing Increases, Underserved Markets are Bringing Increased Opportunities for Capital Investment in CSPs

The contract services sector is growing at historic rates. All signs point to such growth continuing for the foreseeable future. The scope of service candidates for outsourcing is also growing. Services earlier up the value chain are beginning to be outsourced as large pharmaceutical and biotechnology companies narrow the definition of which functions must remain in-house. More specifically for Indiana, discovery and pre-clinical services, analytical chemistry discovery and development services, and biopharmaceutical and high-potency API manufacturing are all key market segments that will see mounting demand for outside providers in the near term. These services are critical to the development process and have a low probability of being offshored for out-sourcing in the near term. Especially for the biotechnology companies, proximity, demonstrated experience and quality, and IP security

29

concerns put U.S.-based CSPs at an advantage in meeting the growing demand for these service segments. Diverse sources of private equity and other capital are becoming increasingly available for the growth of service providers in the pharmaceutical and biotechnology industries. Attributes such as consistently seeking greater performance, short time to revenue, relatively low capital requirements, and proprietary service offerings protected by IP are attracting equity investors to this market and providing a balance to traditional product-based portfolio investments. The funding market for these types of investments is still not efficiently organized and early capital for start-up CSPs remains in short supply. Still, as the market coheres and matures and opportunities become clearer, more investors are likely to emerge and, in the process, gain greater comfort. Private equity and venture investors have been active in the contract services market, but traditionally not in the market spaces identified in this report as growth sectors, and not in start-up entities. Still, venture dollars are sporadically appearing in companies offering services earlier up the value chain. As this market gains definition, investment activity is poised to increase. Revenue-positive CSPs in emerging service sectors will ultimately provide private equity investors with attractive targets for growth through expansion of revenues, process improvements, build-ups and roll-ups. For Indiana, the time is ripe for emerging CSPs in an appealing range of growth areas. Key assets can indeed be productively assembled to pursue new ventures with the highest prospects for success in accessing the capital markets, building the regional economy and enhancing our signature strength as a national center for the development and manufacturing of innovation.

30

APPENDIX I:

Biopharma Development and Manufacturing in Indiana –

A Representative List of Companies, Activities and Employment

Company Activity Employees

Anaclim CRO 20 AIT Laboratories Toxicology 170 Aledo Consulting FDA Consulting 8 Anson Group FDA Consulting 20 Aptuit (SSCI) CRO 100 BASI CRO 300 Baxter Biopharma Solutions Contract Mfg 825 BioConvergence Contract Dvlpmt 27 BioStorage Technologies Cold Storage 50 Bristol Myers Nutritionals* Dry/wet products Mfg 700 Bristol Myers Pharma* Solid dose Mfg 300 Chao Center for Contract Mfg. Contract Mfg 21 Chemigen CRO 7 Commissioning Agents Regulatory Compliance 140 Concentrics Research CRO 30 Cook Biotech* Tissue Mfg 100 Cook Pharmica Contract Mfg 205 Covance CRO 850 DCL CRO 200 Elona Biotech Mfg 14 Enzon Contract Mfg 150 Exaromed Market Research 14 G&S Research Market Research 45 ICC CRO 3 IN Institute for Biomedical Imaging CRO 70 IU Vector Production Facility Biotech Mfg 13 JLM Pharmatech Contract Mfg 40 KP Pharma Contract Mfg 20 Krauter Solutions Storage & Logistics 15 Lilly - Clinton** Dry products 200 Lilly - LTC North** Biotech Mfg 1500 Lilly - Tippecanoe** Bulk API; scale-up 700 Med Institute FDA Consulting 175 MICR CRO 18 Monarch Life Sciences CRO 18 OBS Medical CRO 20 Pfizer* Fill/Finish 700 Project Technologies Commissioning 2 Safis Solutions FDA Consulting 30 SCHWARZ Pharma (UCB) Contract Mfg 360 Sentry Logistics Cold Storage 30 Stanbio Biotech Mfg 12 Vesta Pharma Contract Mfg 25 8247 *Vertically Integrated **Excludes Lilly Corp HQ/R&D/G&A

31

Appendix II:

Medco Headline and Article from Indianapolis Star

32

November 13, 2007

Region's skilled workers key to Medco deal By John Russell [email protected] November 13, 2007