birla-sun-life-insurance.doc

TRANSCRIPT

1

INSURANCE

The meaning of insurance: Insurance is a policy from a large financial institution that offers a

person, company, or other entity reimbursement or financial protection against possible future

losses or damages.

A simple example will make the meaning of insurance easy to understand. A biker is always

subjected to the risk of head injury. But it is not certain that the accident causing him the head

injury would definitely occur. Still, people riding bikes cover their heads with helmets. This

helmet in such cases acts as insurance by protecting him/her from any possible danger. The

price paid was the possible inconvenience or act of wearing the helmet; this i.e. equivalent to the

insurance premiums paid.

Major types of insurances are as mentioned below:

Life insurance: Descendant’s family receives financial benefits. Life insurances also

offer paid proceeds to the beneficiary.

Automobile insurance: Usually automobile insurances cover damages and legal

financial expenditures of the automobile driver.

Health insurance: Health insurance covers the expenditures associated to treatment and

medical expenditures.

Credit insurance: Borrowers often fail to repay debts, loans and mortgages due to

certain unavoidable circumstances, credit insurances can be of great help during such

crisis.

Property insurance: Property protection insurance provides protection from risks

associated to theft, fire, floods etc.

Life insurance

Life insurance or life assurance is a contract between the policy owner and the insurer, where

the insurer agrees to pay a sum of money upon the occurrence of the insured individual's or

2

individuals' death or other event, such as terminal illness or critical illness. In return, the policy

owner agrees to pay a stipulated amount called a premium at regular intervals or in lump sums.

How life insurance works

There are three parties in a life insurance transaction; the insurer, the insured, and the owner of

the policy (policyholder), although the owner and the insured are often the same person. For

example, if Mr. Rajan buys a policy on his own life, he is both the owner and the insured. But if

Mrs. Anita, his wife, buys a policy on Rajan’s life, she is the owner and he is the insured. The

owner of the policy is called the grantee (he or she will be the person who will pay for the

policy). Another important person involved is the beneficiary. The beneficiary is the person or

persons who will receive the policy proceeds upon the death of the insured. The beneficiary is

not a party to the policy, but is designated by the owner, who may change the beneficiary unless

the policy has an irrevocable beneficiary designation. With an irrevocable beneficiary, that

beneficiary must agree to changes in beneficiary, policy assignment, or borrowing of cash value.

The policy, like all insurance policies, is a legal contract specifying the terms and conditions of

the risk assumed. Special provisions apply, including a suicide clause wherein the policy

becomes null if the insured commits suicide within a specified time for the policy date (usually

two years). Any misrepresentation by the owner or insured on the application is also grounds for

nullification. Most contracts have a contestability period, also usually a two-year period; if the

insured dies within this period, the insurer has a legal right to contest the claim and request

additional information before deciding to pay or deny the claim.

The face amount of the policy is normally the amount paid when the policy matures, although

policies can provide for greater or lesser amounts. The policy matures when the insured dies or

reaches a specified age. The most common reason to buy a life insurance policy is to protect the

financial interests of the owner of the policy in the event of the insured's demise. The insurance

proceeds would pay for funeral and other death costs or be invested to provide income replacing

the deceased's wages. Other reasons include estate planning and retirement. The owner (if not the

insured) must have an insurable interest in the insured, i.e. a legitimate reason for insuring

another person’s life. The insurer (the life insurance company) calculates the policy prices with

an intent to recover claims to be paid and administrative costs, and to make a profit.

3

MAJOR PLAYERS OF INDIA IN INSURANCE

Reliance Life Insurance is a part of the Reliance group. It is one of the partners of Reliance

Capital Ltd which is a Anil Dhirubhai Ambani Group. Reliance Capital is one India's most

dominant private sector financial services companies. They offer insurance products which help

you with savings as well as give you protection.

Canara HSBC Life is a joint venture of Canara Bank, HSBC Insurance (Asia pacific) &

Oriental bank of Commerce. The Company got its approval from IRDA in June 2008 and from

that commencing its business. They have more than 4100 branches all over India.

DLF pramerica Life Insurance Company Ltd. is a joint venture between DLF Limited &

Prudential International Insurance Holdings Limited. DLF Pramerica believes in delivering a

secure & enrich life to there customers.

MetLife One of the fastest growing insurance company in India is MetLife. The company started

its operations in between 2000-2001. They have a range of various products to offer.

ICICI Prudential ICICI Bank with Prudential plc, both well known & strong financial

institutions came together in December 2000 to form an insurance company - ICICI Prudential

Life Insurance.

Max New York Life Max India’s leading multi business corporation & New York Life joined

there hands in 2000.The company started there operations in 2001. The company is involved in

Life & health products.

Bajaj Allianz Bajaj who are into iron & steel, finance, insurance & etc and Allianz who

provides financial services when came together they formed Bajaj Allianz Life Insurance

Company.

Bharti AXA Bharti AXA Life Insurance is a joint venture between Bharti & AXA. The

company started its functionality in December 2006 and they always believe to be a strong

financial institute.

4

HDFC Standard Life HDFC Standard Life Insurance is a joint venture between Housing

Development Finance Corporation Limited & a Group of Standard Life Plc.The Company

started commencing its business in December 2000.

AEGON Religare AEGON Religare Life Insurance Company Ltd is a joint venture with

AEGON, Religare and Bennett, Coleman & Company a part of Times Group. AEGON Religare

Life Insurance company was launched in July 2008.

Kotak Mahindra A joint venture of Kotak Mahindra group & Old Mutual plc is known as

Kotak Mahindra Old Mutual Funds. The Company started commencing its business in 2001. The

company aim is to help customers in making there financial decisions.

Future Generali Life Future Generali is a joint venture between Future Group of India & Italy

based Generali Group.Future Generali in India is into both Life & Non Life businesses in India.

The company wants to provide a financial security to all.

SBI Life SBI Life Insurance Company Limited is a joint venture between State Bank of India

and BNP Paribas Assurance. It is present in more than 41 countries across the world. SBI Life

offers a variety of plans in life insurance and pension.

Shriram Life Shriram Life Insurance Company is a joint venture between Shriram Group and

Sanlam Group.Shriram Group is one of India’s most esteemed financial services & Sanlam

Group is one of the largest life insurance providers of South Africa.

TATA AIG The TATA Group and American International Group Inc together formed Tata AIG

Life Insurance Co. Ltd.Tata Group holds 74% stake in the insurance venture with AIG holding

the balance 26%. They started their operations in April 2001

Aviva Aviva, one of UK's largest insurance company and world's 5th largest insurance group. It

was one of the first international insurance company to set up its office in India in the year 1995.

They introduced the concept of banc assurance in India.

5

IDBI Fortis IDBI Fortis Life Insurance Co. Ltd is a joint venture between three financial

institutes; they are IDBI Bank, Federal Bank and Fortis. They introduced there plans in March

2008. IDBI owns 48% equity while Federal Bank and Fortis own 26% equity each.

Sahara The Sahara Pariwar stepped into the insurance business by launching Sahara India Life

Insurance Co. Ltd. They received the IRDA license in February 2004 and started their operations

in October 2004. They are the first solely owned private sector insurance company in India.

ING VYSYA ING Life was established in 2001 as a joint venture between ING Insurance

International B.V. (INGI), ING Vysya Bank Limited and GMR Industries Limited. At present,

INGI, Exide Industries Limited, Ambuja Cement Ltd, Enam Group are the joint venture partners.

Star Union Star Union Dai-ichi Life Insurance Co.Ltd. is formed by three various financial

institutions. Bank of India, Union Bank of India and Dai-ichi Mutual Life Insurance Company

This firm was incorporated in the year 2007 and got their IRDA license on the 26th Dec 2008.

Some of the important milestones in the life insurance business in India are:

1818: Oriental Life Insurance Company, the first life insurance company on Indian soil started

functioning.

1870: Bombay Mutual Life Assurance Society, the first Indian life insurance company started its

business.

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate the life

insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the objective of

protecting the interests of the insuring public.

6

1956: 245 Indian and foreign insurers and provident societies are taken over by the central

government and nationalised. LIC formed by an Act of Parliament, viz. LIC Act, 1956, with a

capital contribution of Rs. 5 crore from the Government of India.

7

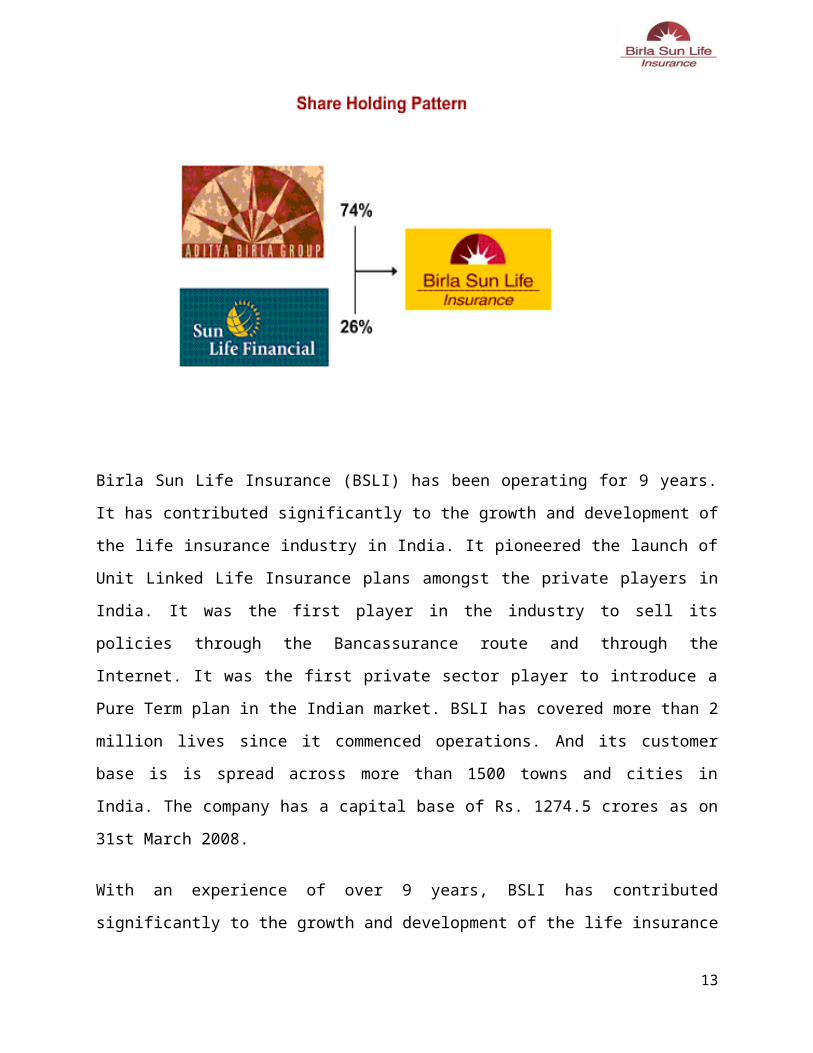

Birla Sun Life Insurance Company Limited is a joint venture between The Aditya Birla

Group, one of the largest business houses in India and Sun Life Financial Inc., a leading

international financial services organisation. The local knowledge of the Aditya Birla Group

combined with the expertise of Sun Life Financial Inc., offers a formidable protection for your

future.

The Aditya Birla Group has a turnover of close to Rs. 119000 crores, with a market

capitalisation of Rs. 133875 crores (as on 31st March 2008). It has over 100,000 employees

across all its units worldwide. It is led by its Chairman - Mr. Kumar Mangalam Birla. Some of its

key companies are Hindalco, Grasim and Aditya Birla Nuvo.

Sun Life Financial

Sun life financial –based in Canada-started in 1865.

It operates in all the important markets of the world like Canada, the United States, the United

Kingdom, Hong Kong, the Philippines, Japan, Indonesia, India, China and Bermuda.

8

Sun Life Financial Inc. has assets under management of over US$404.7 billion (as on 31st

March, 2008). It is a leading performer in the life insurance market in Canada.

Brands Of Aditya Birla Group

9

Birla Sun Life Insurance (BSLI) has been operating for 9 years. It has contributed significantly to

the growth and development of the life insurance industry in India. It pioneered the launch of

Unit Linked Life Insurance plans amongst the private players in India. It was the first player in

the industry to sell its policies through the Bancassurance route and through the Internet. It was

the first private sector player to introduce a Pure Term plan in the Indian market. BSLI has

covered more than 2 million lives since it commenced operations. And its customer base is is

spread across more than 1500 towns and cities in India. The company has a capital base of Rs.

1274.5 crores as on 31st March 2008.

With an experience of over 9 years, BSLI has contributed significantly to the growth and

development of the life insurance industry in India and currently ranks amongst the top 5 private

life insurance companies in the country.

Known for its innovation and creating industry benchmarks, BSLI has several firsts to its credit.

It was the first Indian Insurance Company to introduce “Free Look Period” and the same was

made mandatory by IRDA for all other life insurance companies. Additionally, BSLI pioneered

the launch of Unit Linked Life Insurance plans amongst the private players in India. To establish

credibility and further transparency, BSLI also enjoys the prestige to be the originator of practice

10

to disclose portfolio on monthly basis. These category development initiatives have helped BSLI

be closer to its policy holders’ expectations, which gets further accentuated by the complete

bouquet of insurance products (viz. pure term plan, life stage products, health plan and

retirement plan) that the company offers.

Add to this, the extensive reach through its network of 600 branches and 1,75, 000 empanelled

advisors. This impressive combination of domain expertise, product range, reach and ears on

ground, helped BSLI cover more than 2 million lives since it commenced operations and

establish a customer base spread across more than 1500 towns and cities in India. To ensure that

our customers have an impeccable experience, BSLI has ensured that it has lowest outstanding

claims ratio of 0.00% for FY 2008-09. Additionally, BSLI has the best Turn around Time

according to LOMA on all claims Parameters. Such services are well supported by sound

financials that the Company has. The AUM of BSLI stood at Rs. 8165 crs as on February 28,

2009, while as on March 31, 2009, the company has a robust capital base of Rs. 2000 crs.

Achievements of BSLI

1st to introduce ULIP fund options.

1st to launch illustrations so that customers understand the products better before they

buy.

1st to issue NAVs of funds for better transparency.

1st to disclose portfolio on a monthly basis.

1st to introduce “Free Look Period” and the same was made mandatory by IRDA for all

other Life Insurance Companies.

11

12

13

SWOT ANALYSIS OF BSLI

STRENGTH:

Multi-channel distribution and one of the largest distribution networks in India.

1 Million Policies sold within 3 and half years.

Training process of the company is very strong.

According to the change in surrounding environment like changes in customer

requirement.

WEAKNESS:

Company does not penetrate on the rural market at a time.

There is no plan for the low income group.

Fees for the advisor is high than the other companies.

OPPORTUNITY:

Insurance market is very big, where company can expand its business easily.

It has many ULIP plans so it can grow in near future.

THREATS:

‘OLD HABITS DIE HARD’: Its still difficult task to win the confidence of public

towards private company.

The company is facing major threats from LIC etc. -which is an government company.

Plans for all income groups are not available which can create adverse effect later on the

market share of the company.

14

MAJOR COMPETITOR AT A GLANCE LIC (LIFE INSURACE

CORPORATION)

LIC had 5 zonal offices, 33 divisional offices and 212 branch offices, apart from its corporate

office in the year 1956. Since life insurance contracts are long term contracts and during the

currency of the policy it requires a variety of services need was felt in the later years to expand

the operations and place a branch office at each district headquarter. re-organization of LIC took

place and large numbers of new branch offices were opened. As a result of re-organisation

servicing functions were transferred to the branches, and branches were made accounting units.

It worked wonders with the performance of the corporation. It may be seen that from about

200.00 crores of New Business in 1957 the corporation crossed 1000.00 crores only in the year

1969-70, and it took another 10 years for LIC to cross 2000.00 crore mark of new business. But

with re-organisation happening in the early eighties, by 1985-86 LIC had already crossed

7000.00 crore Sum Assured on new policies.

Today LIC functions with 2048 fully computerized branch offices, 100 divisional offices, 7

zonal offices and the Corporate office. LIC’s Wide Area Network covers 100 divisional

offices and connects all the branches through a Metro Area Network. LIC has tied up with some

Banks and Service providers to offer on-line premium collection facility in selected cities. LIC’s

ECS and ATM premium payment facility is an addition to customer convenience. Apart from

on-line Kiosks and IVRS, Info Centres have been commissioned at Mumbai, Ahmedabad,

Bangalore, Chennai, Hyderabad, Kolkata, New Delhi, Pune and many other cities. With a vision

of providing easy access to its policyholders, LIC has launched its SATELLITE SAMPARK

offices. The satellite offices are smaller, leaner and closer to the customer. The digitalized

records of the satellite offices will facilitate anywhere servicing and many other conveniences in

the future.

LIC continues to be the dominant life insurer even in the liberalized scenario of Indian insurance

and is moving fast on a new growth trajectory surpassing its own past records. LIC has issued

over one crore policies during the current year. It has crossed milestone of issuing

15

1,01,32,955 new policies by 15th Oct, 2005, posting a healthy growth rate of 16.67% over the

corresponding period of the previous year.

From then to now, LIC has crossed many milestones and has set unprecedented performance

records in various aspects of life insurance business.

Birla Sun Life Insurance Co. Ltd

Following are the Life Insurance plans that Birla Sun life Insurance Company Ltd.

1.)Birla Sun Life Insurance Term Plan - This plan can take care of your financial

commitments of yours towards your family by providing large cover at low cost. Minimum

age of entry for this plan is 18-55 and maximum maturity age is 70 years.

2. Birla Sun Life Insurance Premium Back Term Plan - This is a low cost life cover

promises you to refund the entire premium on maturity or death. Two options are also there

to choose 100% premium back or 125% premium back. Maximum term period for this plan

is 20 years.

3. Birla Sun Life Insurance Guaranteed Bachat Plan - It’s an non participating

endowment plan offers you guaranteed returns and chance to earn survival benefit from the

3rd year onwards. You can withdraw this benefit each tear or can use it as to pay the

premium dues.

4. Birla Sun Life Insurance Money Back Plus Plan - This is also a non-participating

endowment plan, which gives you maturity and survival both benefits. One remarkable point

is that on every policy anniversary it increases your cover by an equal amount of your base

premium.

5. Birla Sun Life Insurance Gold-Plus II - It’s an investment plan offering nine-funding

option to choose and 100% equity fund option also. Free unlimited switches are given to you

to manage your investments. This plan offers good liquidity to you.

16

6. Birla Sun life insurance Platinum Plus - It is a unit linked, non participating insurance

plan. In this plan, the investment risk is borne by the policyholder but not if this policy is

detained till maturity.

7. Birla Sun Life Insurance Saral Jeevan Plan - In today’s fast life it’s really easy to buy

an insurance plan, which you immediately can purchase just by providing three health

statements to the company. Bsli Saral Jeevan is the best option to go for.

8. Birla Sun Life Insurance Supreme-Life - It’s a unit linked non-participating plan

providing 8-fund options to choose. It gives a choice of two death benefits.

9. Birla Sun Life Insurance Dream Plan - It’s a unit-linked policy, which provides you

guaranteed returns, 0% allocation charges, and option to double or triple the guaranteed

maturity.

10. Birla Sun Life Insurance ClassicLife Premier - It will give you guaranteed additions in

the form of guaranteed units and a good choice of 8 investment funds are also there. You are

free to choose the term period of 10,20,30 or whole life.

11. Birla Sun Life Insurance SimplyLife - It ensures a lifetime of tax-free investments to

fulfill the needs of your dear ones. It’s a market related plan provides you a good death

benefit amount.

12. Birla Sun Life Insurance PrimeLife Premier - It’s a single time investment with top up

options. It keeps you hassle free and provides you guaranteed returns at regular intervals.

13. Birla Sun Life Insurance PrimeLife - It is a single premium policy gives you the

benefit of life insurance and investments as well. It’s a non-participating ULIP policy.

14. Birla Sun Life Insurance Flexi Cash Flow - For this policy you can pay lump sum

17

premium payment at regular intervals. It will give you 3% guaranteed returns on net policy

charges.

15. Birla Sun Life Insurance Flexi Save Plus - This plan will give you the choices of 3

fund options, maturity ages & guaranteed returns of 3%.

16. Birla Sun Life Insurance Flexi Life Line - This would provide you a life long cover till

100 years of age and will give you the option of tax-free partial withdrawals.

17. Birla Sun Life Insurance Single Premium Bond - This plan gives you the opportunity

to make one time investment with no medical tests and will also gives you the facility of high

entry age. It’s a short term investment plan provides you the option of 5 years or 10 years

term period.

18. Birla Sun Life Insurance Freedom 58 - It’s a non- participating ulip plan. It helps you

accumulate your premiums and the investment return there of into a corpus of your

retirement.

19. Birla Sun Life Insurance Flexi Secure Life Retirement Plan II - This will provide you

the option to take a life cover or not. You can choose your retirement age yourself whether

you want to prepone/postpone it.

20. Birla Sun Life Insurance Children's Dream Plan - It’s a unit-linked policy, which

provides you guaranteed returns, 0% allocation charges, and option to double or triple the

guaranteed maturity.

18

Various Plans offered by LIC are as follows :

Endowment Assurance Plans

1. Jeevan Amrit : This plan is designed for a higher cover at a lower cost. In this plan premium

payment is limited to 3 or 4 or 5 years and the premium payable during the first year is higher

than the premiums payable in subsequent years.

2. New Janaraksha Plan : Is an Endowment Assurance plan that provides financial protection

against death throughout the term of plan. It pays the maturity amount on survival to the end of

the term.

3. Jeevan Mitra(Double Cover Endowment Plan) : Is an endowment plan which takes care of

the financial needs even if death of the policyholder for the whole term of the plan.

4. Jeevan Mitra (Triple Cover Endowment Plan) : Is an endowment plan where thrice the

Sum Assured plus all bonuses on the basic sum assured to date is payable in a lump sum upon

the death of the life assured.

5. The Endowment Assurance Policy : This policy has a provisions for the family of the Life

Assured in event of his early death and also assures a lump sum at a desired age.

6. The Endowment Assurance Policy-Limited Payment : In this policy the payment of

premium can be limited either to a single payment or to a term shorter than the policy.

Children Plans

1. Jeevan Anurag : Is plan designed for the children educational requirements . This plan can be

taken on the parent’s life. The basic sum assured is given immediately on the death of the life

assured during the term of the policy.

2. Jeevan Kishore : Is a plan which can be availed by the parent or grand parents of the

children. It is an endowment assurance plan for children of less than 12 years of age.

3. Jeevan Chhaya : It is a plan where financial protection is given against death during the term

of the plan. It is an Endowment Assurance plan. Besides this benefit one-fourth of Sum Assured

19

is payable at the end of each of last four years of policy term irrespective if the life assured dies

or survives the duration of the policy.

4. Komal Jeevan : Is a Money Back Plan which can be bought by the parent or grand parent for

their child from the age of 0-10years. This plan gives financial protection against death during

the duration of the plan with periodic payments on survival at specified durations.

5. Child Future Plan : A policy where the future needs like education, marriage and other

requirements are taken care of. This plan provides a benefit which not only takes care of the risk

cover of the child during the policy but also after 7 years of the policy being expired.

6. Child Career Plan : A plan to meet the educational and other needs of the child. It provides

the risk cover on the life of child during the policy term as well as 7 years after the policy has

expired. There are also Survival benefits given to the life assured at the end of a specific

duration.

7. Child Fortune Plan : Is a unit linked plan which offers long term capital appreciation.

8. Marriage Endowment Or Educational Annuity Plan : This is an Endowment Assurance

plan that provides for benefits on or from the selected maturity date to meet the

Marriage/Educational expenses of the named child.

Money Back Plan

1. Bima Bachat : Is a money-back policy which offers financial security and assurance to the

policy holder and his family. The policy holder has to pay only one premium.

2. Money Back-20 years : Is an endowment plan where periodic payments of partial survival

benefits are paid during the term of the policy till the policy holder is alive.As the policy name

goes this plan 20% of the sum assured is payable after 5,10,15 years and the balance 40%

accrued bonus is payable at the 20th year.

3. Money Back 25 years : Is the same as the above plan only in this plan the 40% accrued bonus

is payable at the 25th year.

20

Pension plans

1. New Jeevan Dhara - I : is a Deferred Annuity plans that allows the policyholder to make

provision for regular income after the selected term.

2. New Jeevan Suraksha - I : Is a deferred annuity plan.

3. Jeevan Nidhi : Is a deferred annuity plan with profits.

4. Jeevan Akshay - VI : By paying a lump sum amount this immediate annuity plan can be

bought.

Unit Plans

1. Child Fortune Plus : Is a plan for children and to meet their educational needs. Its a unit

linked plan with long term capital appreciation.

2. Fortune Plus : It is a unit linked assurance plan where premium payment term (PPT) is 5

years and the premium payable in the first year will be 50% of total premium payable under the

policy.

3. Market Plus : Is a unit linked pension plan where after a specific period the pension is paid.

4. Money Plus - I : Is a unit linked Endowment plan which has investment plus insurance during

the term and you can pay regular premiums.

5. Profit Plus : It is a unit linked Endowment plan where the premium payment term (PPT) is

limited to single lump sum, or uniformly over 3, 4 or 5 years.

Whole Life Plans

1. Jeevan Anand : Is a combination of two plans- Endowment Assurance and Whole Life plan.

2. Jeevan Tarang : This is a with-profits whole of life plan which provides for annual survival

benefit at a rate of 5½ % of the Sum Assured after the chosen Accumulation Period.

21

3. The Whole Life Policy : Is a plan mainly to provide for payment of sum assured plus bonuses

on the death of the policyholder.

Golden Jubliee Plan

New Bima Gold : Where the premiums are paid back during the policy term in installments ,

besides that life insurance cover is given during the also at the extended term of the plan.

Some main Plans of BSLI:

(1) Birla Sun life insurance Platinum Plus - It is a unit linked, non participating insurance plan.

In this plan, the investment risk is borne by the policyholder but not if this policy is detained till

maturity.

Policy parameters

Entry age 18-70

Minimum annual premium Rs. 50000

Minimum sum assured 5*annual premium

Policy term 10 years

Premium paying term 3 years

Premium and sum assured

You can pay your policy premium annually, half-yearly, quarterly or monthly, subject to a

minimum installment premium of:

Rs. 50,000 per annum

Rs. 25,000 half-yearly

Rs. 15,000 quarterly; or

Rs. 10,000 per month (3 monthly installments required at issue)

You choose your Sum Assured (minimum 5 x annual premium).

22

Risk profile

0-40% in money market & cash

0-100% in debt instruments & derivatives

0-100% in equities & equity related securities.

Maturity Benefit

On maturity, your Fund Value will be paid to you.

In addition, we will pay an amount equal to:

the number of units under your policy at that time; times

the excess, if any, of the Guaranteed Maturity Unit Price over the then prevailing unit

price

Death Benefit

In the unfortunate event of the death of the life insured prior to the maturity date of the

policy, we will pay to the nominee the greater of (a) the Fund Value or (b) the Sum Assured

reduced for partial withdrawals as follows:

Before the life insured attains the age of 60, the Sum Assured payable on death is

reduced by partial withdrawals made in the preceding two years.

Once the life insured attains the age of 60, the Sum Assured payable on death is

reduced by all partial withdrawals made from age 58 onwards.

Partial withdraw

Partial withdraw after 3 complete policy years.

Minimum partial withdraw rs.5000

Policy surrender After 3 policy years and you will get 100% fund value at that time.

23

(2) Birla Sun Life Insurance children’s Dream Plan –

Policy parameters

Entry AgesLife Insured (parent): 18 years – 60 years

Nominee (child) : 30 days – 13 years

Term 18 years less the age of child at entry

Premium paying

frequency

Regular policy premiums can be paid yearly, half-yearly,

quarterly or monthly (for ECS only)

Addition of riders Accidental Death & Dismemberment Benefit (ADD)

The annual policy premium is based on:

The guaranteed maturity benefit and option you choose.

The enhanced sum assured you desire.

The plan term and your gender and age at entry.

Guaranteed Fund

Value

Equals all premiums paid, less charges and guaranteed maturity

benefit(s), accumulated at 3% per annum

Partial

WithdrawalsAllowed after 3 complete policy years

Investment Funds Protector, Builder, Enhancer

24

AT Death

Benefit

The sum assured is paid to the nominee upon the death of the life insured (parent)

The new life insured is the child and new owner is appointed as per your wishes.

The policy is continued as usual except:

•All riders and risk charges will cease

•Only the policy administration charge and fund management charge continue,

and

•BSLI will start paying the Maturity Continuation Benefit on a monthly basis

until the policy matures.

In case of death of the new life insured (child) prior to the end of the Term, higher

of 105% of the Fund Value or the Guaranteed Fund Value will be paid and the

policy will be terminated.

Charges of policy

Premium allocation charges

Fund management charges

Mortality charges

Surrender charges etc.

(3) Birla Sun Life Insurance Saral Jeevan Plan – The saral jeevan plan provides the dual

benefit of protection and investment. So it is the ideal policy if you want to secure your life and

build wealth at the same time.

Poicy parameters

Entry age 18-55

Policy term 10, 15, and 20 years

Age at maturity 65 or less

Mode of Premium Payment - Annual, Semi Annual, Quarterly, Monthly.

25

Maturity Benefit

Maturity benefit will be sum assured plus fund value at the end of maturity time.

Death Benefit – Your nominee will receive both sum assured and fund value in the unfortunate

event of death.

Investment Funds

Protector

Builder

Enhancer

Charges of Policy

Premium Allocation Charge- Nil (This means all of your policy premium will be

invested in the investment funds of your choice).

Fund Management Charge

Mortality charges

Surrender charges etc.

(4) Birla Sun Life Universal Health Plan-

The universal health plan is in addition to the benefit amount payable under each health benefit.

This unique benefit helps you and your family with out of pocket health related expenses.

Policy parameters

Entry Ages 18 years – 65 years

Term 3 years

Premium paying frequency

policy premiums can be paid yearly, half-yearly, quarterly or monthly

Premium According to age of the insured person. (e.g. for 25 – Rs. 4756 p.a., for 45- Rs. 6725 p.a., for 55- Rs. 9724 p.a.).

26

Benefits –

1. BSLI pay a fixed benefit amount of Rs. 1000 per day in Hospital plus Rs. 1000 per day in

Intensive Care Unit (ICU).

In case of an admission for surgical management :

2. if the surgery is listed in covered surgeries: BSLI pay a fixed benefit amount based on the

grade of the covered surgery-Rs. 100000, Rs. 50000, Rs. 25000, Rs. 15000 and Rs. 10000

for grade 1(major) to 5(minor) respectively.

3. if the surgery is not listed in the covered surgeries: BSLI pay a fixed benefit amount of

Rs. 2000 per day in hospital plus Rs. 1000 per day in ICU.

Tax benefit

The premium paid by you up to 15000 (Rs.20000 for senior citizens) p.a. to insure yourself

and/or your family, is eligible for tax benefit under section 80D of the income Tax Act, 1961,

which is subject to amendments from to time.

Death/Maturity benefit

This plan has no death benefit or maturity benefit. Furthermore, this plan provides for no

cash surrender value nor any policy loans.

(5) Birla Sun Life Retirement plan

Policy parameters

Entry Ages18 years – 80 years

Term

Premium paying frequencypolicy premiums can be paid yearly, half-yearly, quarterly or monthly

27

Premium Minimum Rs. 9600 p.a.(premium should be multiple of Rs. 1200)

Benefits

In the unfortunate event of death of the policyholder the nominee will receive the higher of:

75% of the base premium and all renewal base premiums paid. OR the surrender value at the

time plus all accumulated survival benefits.

Tax benefits

Under section 80CCC and 10(10A)

Partially withdraw

You can do partially withdraw min. Rs.5000

Some main plans of LIC

(1) Marriage Endowment Or Educational Annuity Plan : This is an Endowment Assurance

plan that provides for benefits on or from the selected maturity date to meet the

Marriage/Educational expenses of the named child.

Entry age 18 (min.) 60(max)

Sum assured 50000 (min) no limit (max)

Term 5 (min) 25 (max)

Mode of payment monthly, qtly, half yrly, yly,

FEATURES

The Marriage Endowment/ Educational annuity plan provides a sum assured to be kept aside for

the expenses of marriage or higher education of the policyholder's children. Premiums payable

28

for selected term or till death of the life Assured. Benefits will be given only after the selected

term.

Maturity benefits

Sum Assured + Bonus

Accident:

Accident benefit equivalent to basic sum assured would be available by paying appropriate

additional premiums in that behalf. An amount equivalent to Sum Assured become payable

immediately.

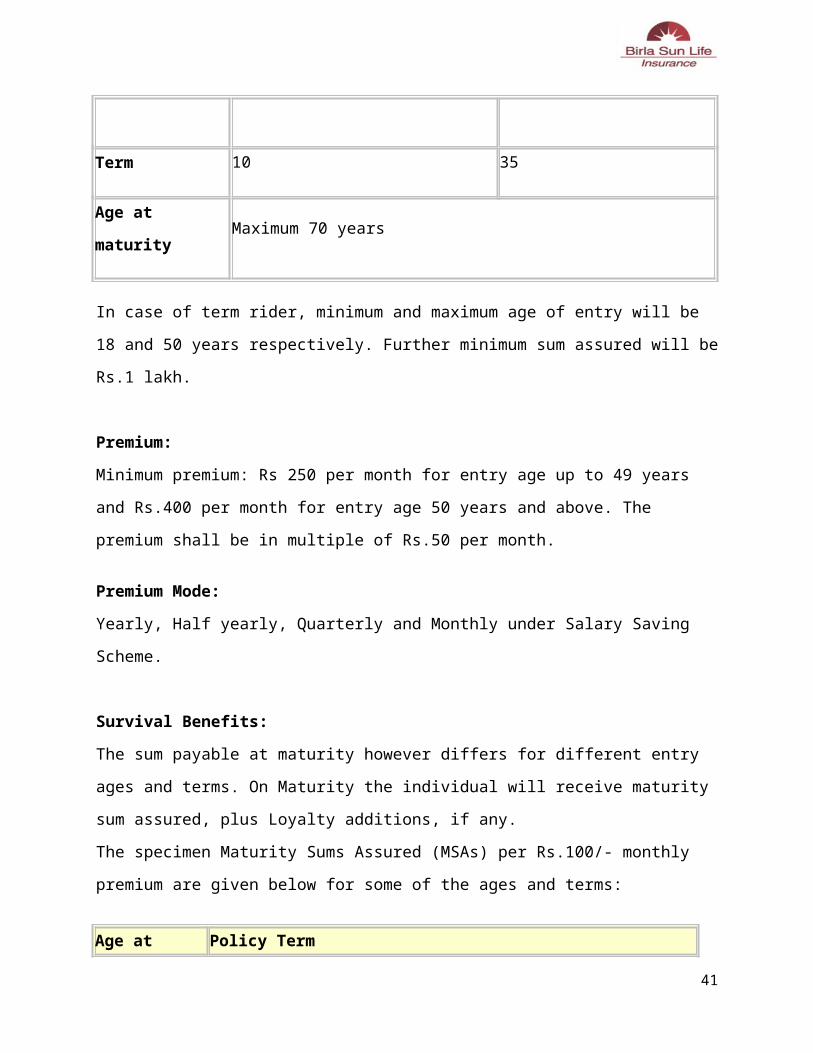

(2) Jeevan saral plan of LIC

Plan Details: This plan is appropriate for employees seeking life cover through Salary Savings

Schemes.

Eligibility:

Minimum Maximum

Age 12 Yrs (completed) 60 Nearest Birthday

Term 10 35

Age at maturity Maximum 70 years

In case of term rider, minimum and maximum age of entry will be 18 and 50 years respectively.

Further minimum sum assured will be Rs.1 lakh.

Premium:

29

Minimum premium: Rs 250 per month for entry age up to 49 years and Rs.400 per month for

entry age 50 years and above. The premium shall be in multiple of Rs.50 per month.

Premium Mode:

Yearly, Half yearly, Quarterly and Monthly under Salary Saving Scheme.

Survival Benefits:

The sum payable at maturity however differs for different entry ages and terms. On Maturity the

individual will receive maturity sum assured, plus Loyalty additions, if any.

The specimen Maturity Sums Assured (MSAs) per Rs.100/- monthly premium are given

below for some of the ages and terms:

Age at

EntryPolicy Term

10 yrs 15 yrs 20 yrs 25 yrs

20 11,156 19,628 28,039 36,839

40 10,431 17,839 24,598 30,854

50 8,442 13,444 16,164

Death Benefits:

Under this plan death cover will be same irrespective of age at entry and term. On death the

nominee will receive 250 times the monthly premium, plus return of premiums excluding

extra/rider premium premium.

(3) New Jeevan Suraksha Plan

This pension plan is a vehicle for planning a life long pension and is also tax deferred. Not only

can you plan a pension for life with the help of these annuities but these schemes also help you

reduce your tax liability.

30

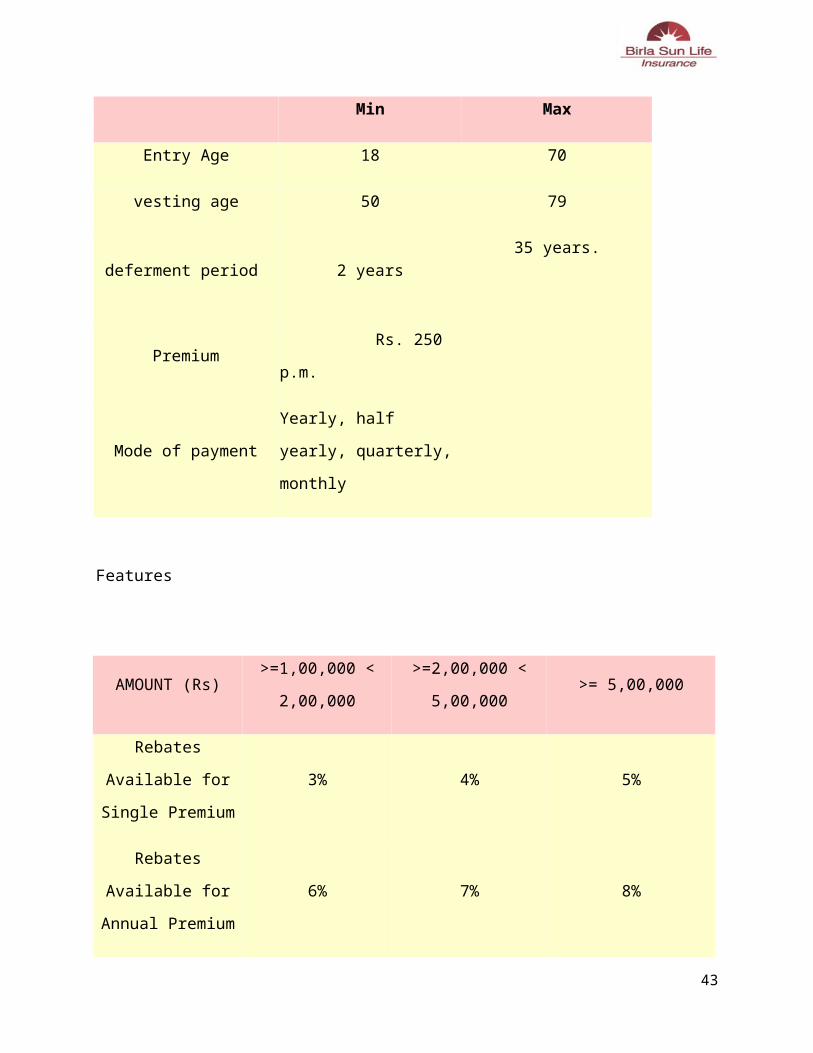

POLICY PARAMETERS

Min Max

Entry Age 18 70

vesting age 50 79

deferment period 2 years35 years.

Premium Rs. 250 p.m.

Mode of paymentYearly, half yearly,

quarterly, monthly

Features

AMOUNT (Rs) >=1,00,000 < 2,00,000 >=2,00,000 < 5,00,000 >= 5,00,000

Rebates Available for

Single Premium 3% 4% 5%

Rebates Available for

Annual Premium 6% 7% 8%

31

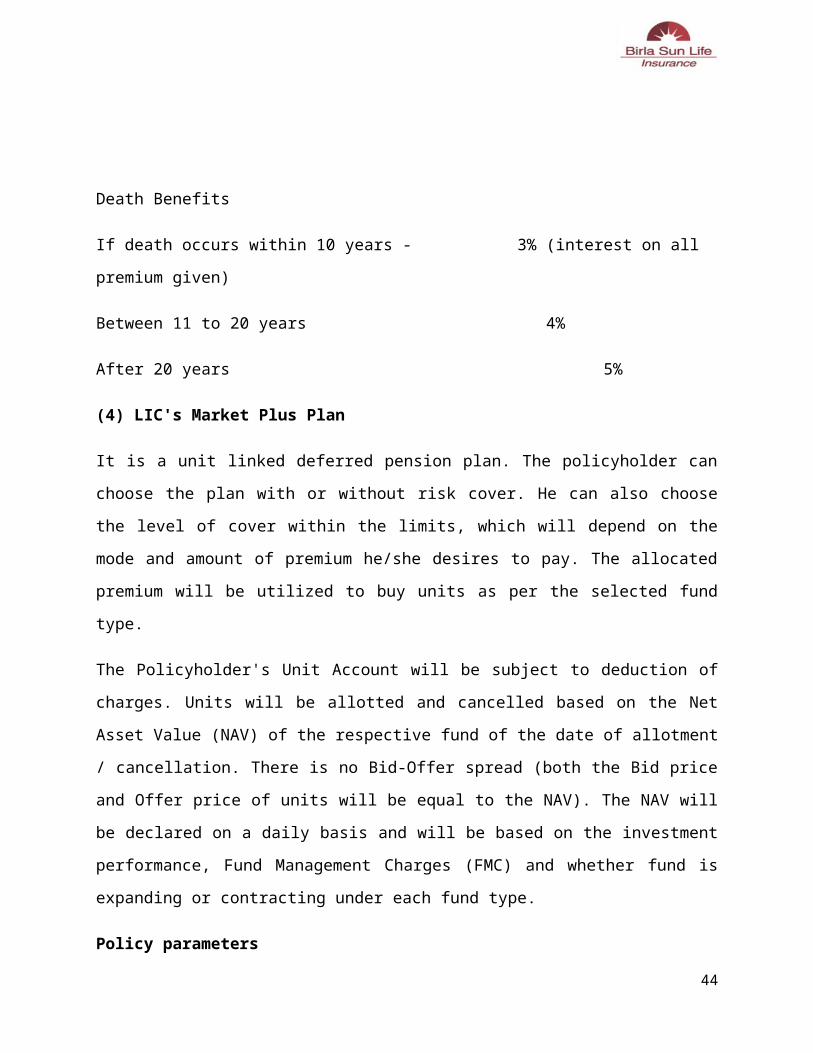

Death Benefits

If death occurs within 10 years - 3% (interest on all premium given)

Between 11 to 20 years 4%

After 20 years 5%

(4) LIC's Market Plus Plan

It is a unit linked deferred pension plan. The policyholder can choose the plan with or without

risk cover. He can also choose the level of cover within the limits, which will depend on the

mode and amount of premium he/she desires to pay. The allocated premium will be utilized to

buy units as per the selected fund type.

The Policyholder's Unit Account will be subject to deduction of charges. Units will be allotted

and cancelled based on the Net Asset Value (NAV) of the respective fund of the date of

allotment / cancellation. There is no Bid-Offer spread (both the Bid price and Offer price of units

will be equal to the NAV). The NAV will be declared on a daily basis and will be based on the

investment performance, Fund Management Charges (FMC) and whether fund is expanding or

contracting under each fund type.

Policy parameters

Entry age 18-70

Premium (Min) Rs. 5,000 p.a. for Regular premium and Rs. 10,000 for Single premium

(Max) No limit

Vesting age 40-75

Sum Assured (min) NIL- (when no life cover is opted) Rs. 25,000 for Single premium, Rs.

50,000 for Regular premium (When life cover is opted)

(Max) Regular Premium - 20 times of the annualized premium.

32

Minimum Deferment period 5 years

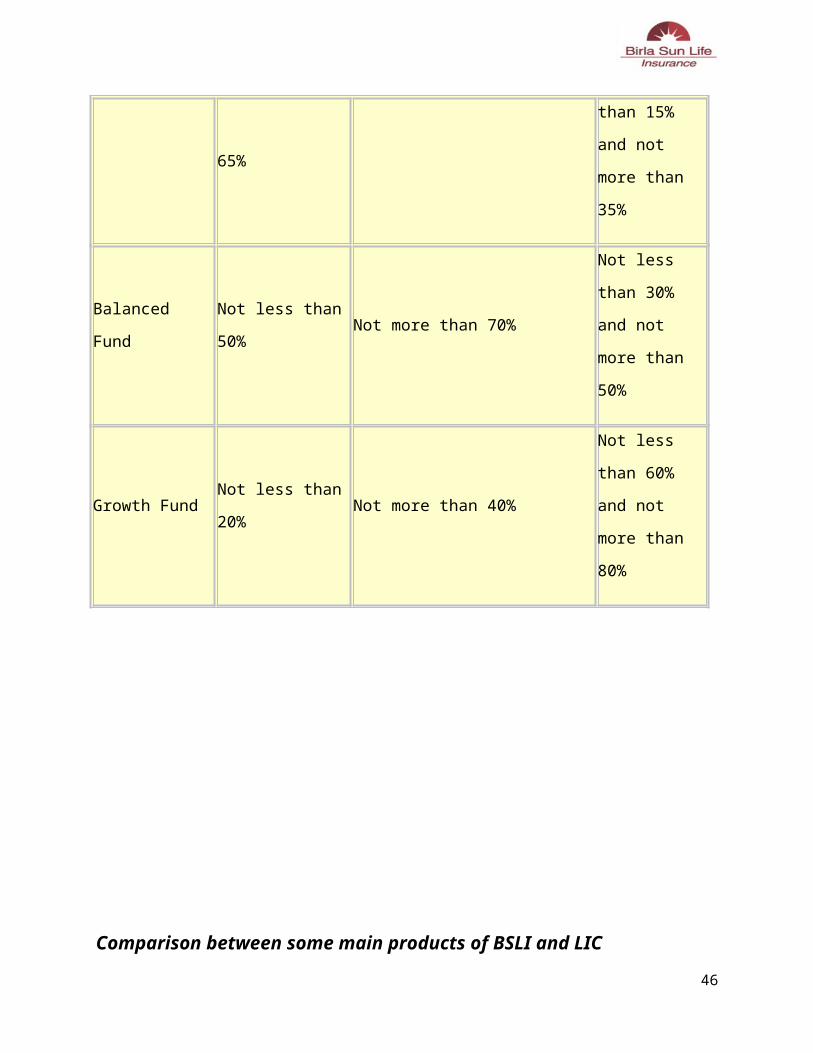

Investment fund types:

Fund Type

Investment in

Govt. / Govt.

Guaranteed

Securities /

Corporate Debt

Short-term investments such as

money market

instruments(Including Govt.

Securities & Corporate Debt)

Investment in

Listed Equity

Shares

Bond Fund Not less than 80% 100% NIL

Secured Fund Not less than 65% Not more than 85%

Not less than

15% and not

more than 35%

Balanced Fund Not less than 50% Not more than 70%

Not less than

30% and not

more than 50%

Growth Fund Not less than 20% Not more than 40%

Not less than

60% and not

more than 80%

33

Comparison between some main products of BSLI and LIC

1) Comparison between BSLI’s Children dream plan and LIC’s Marriage Endowment Or

Educational Annuity Plan:

In BSLI plan policy term is 18 years less the age of child at entry.

But in LIC plan policy term is 5-25 years.

Premium paying frequency is almost same i.e yearly , half yearly, quarterly, monthly.

In case of death benefit: in BSLI plan the sum assured is paid to the nominee upon the

death of the life insured (parent). The new life insured is the child and new owner is

appointed as per your wishes.

In LIC plan if death occurs due to accident then basic sum assured is payable on death

immediately and further premiums are not payable.after expiry of the term again basic sum

assured + bonus is payable.

In BSLI fund value is guaranteed.

o In LIC plan fund value is not guaranteed.

2) Comparison between BSLI’s Saral jeevan plan and LIC’s Jeevan saral plan

In BSLI plan entry age is 18-55 years

In LIC plan entry age is 12-60 years

In BSLI policy term is 10, 15, and 20 years.

In LIC policy term is 10-35 years.

In BSLI plan max. Maturity age is 65 years

In LIC plan max. Maturity age is 70 years.

In BSLI min. premium is 10000 p.a.

In LIC plan min. premium is 5000p.a.

34

3) Comparison between BSLI’s Retirement plan and LIC’s New Jeevan Suraksha plan.

In BSLI plan entry age is 18-80 years

In LIC plan entry age is 18-70 yrs.

In BSLI plan vesting age is 10-40 yrs from entry age (Max. 90yrs.)

In LIC plan vesting age is 50-79 yrs.

In BSLI plan min. premium is 9600 p.a.

In LIC plan min. premium is 3000 p.a.

Premium paying frequency is same i.e yearly, half yearly, quarterly, and monthly

Death Benefits:

In BSLI plan the unfortunate event of death of the policyholder the nominee will receive

the higher of:

75% of the base premium and all renewal base premiums paid. OR the surrender value at

the time plus all accumulated survival benefits.

In LIC plan

If death occurs within 10 years - 3% (interest on all premium given)

Between 11 to 20 years 4%

After 20 years 5%

35

4) Comparison between BSLI Platinum plus plan and LIC Market plus plan

Entry age in BSLI and LIC is same i.e. 18-70 years.

In BSLI min. annual premium is 50000p.a.

In LIC plan premium is 10000p.a.

In BSLI plan maturity benefit is guaranteed

In LIC plan maturity benefit is not

guaranteed

36

OBJECTIVES OF STUDY

To determine and analyze the Market Potential of the Birla Sun Life Insurance Company

in Ludhiana City.

To study and determine the competitor (LIC) position in the market.

To analyze market share of Birla Sun Life Insurance products in Ludhiana city.

To analyze the customer satisfaction regarding LIC and BSLI.

37

RESEARCH METHODOLOGY

MEANING OF RESEARCH-

Before understanding Research Methodology, we should understand the meaning of

research. Research in common parlance refers to a search for knowledge. One can also define

Research as a scientific and systematic search for pertinence information on a specific topic. In

fact, research is an art of scientific investigation.

DEFINITION OF RESEARCH-

Research is a systematized effort to gain new knowledge”

Redmann & Mory

MEANING OF RESEARCH METHODOLOGY-

Research Methodology, it is a way to systematically solve the research Problem. It may be

understood as a science of studying how research is done scientifically. In it we study the various

steps that are generally adopted by the researcher in studying his research problem along with the

logic behind them. It is necessary for the researcher to know not only the research.

Data Collection: - The objectives of the project are such that both primary and secondary data is

required to achieve them. So both primary and secondary data was used for the project. The

mode of collecting primary data is questionnaire mode and sources of secondary data are various

magazines, books, newspapers, & websites etc.

Primary data

The primary data are those data which are collected afresh and for the first time, and thus happen

to be original in character.

38

Secondary data

The secondary data on the other hand, are those which have already been collected by someone

else and which have already been passing through the statistical process.

Sample size –

100 people of Ludhiana City were selected

Research ----- Purposive research

39

40

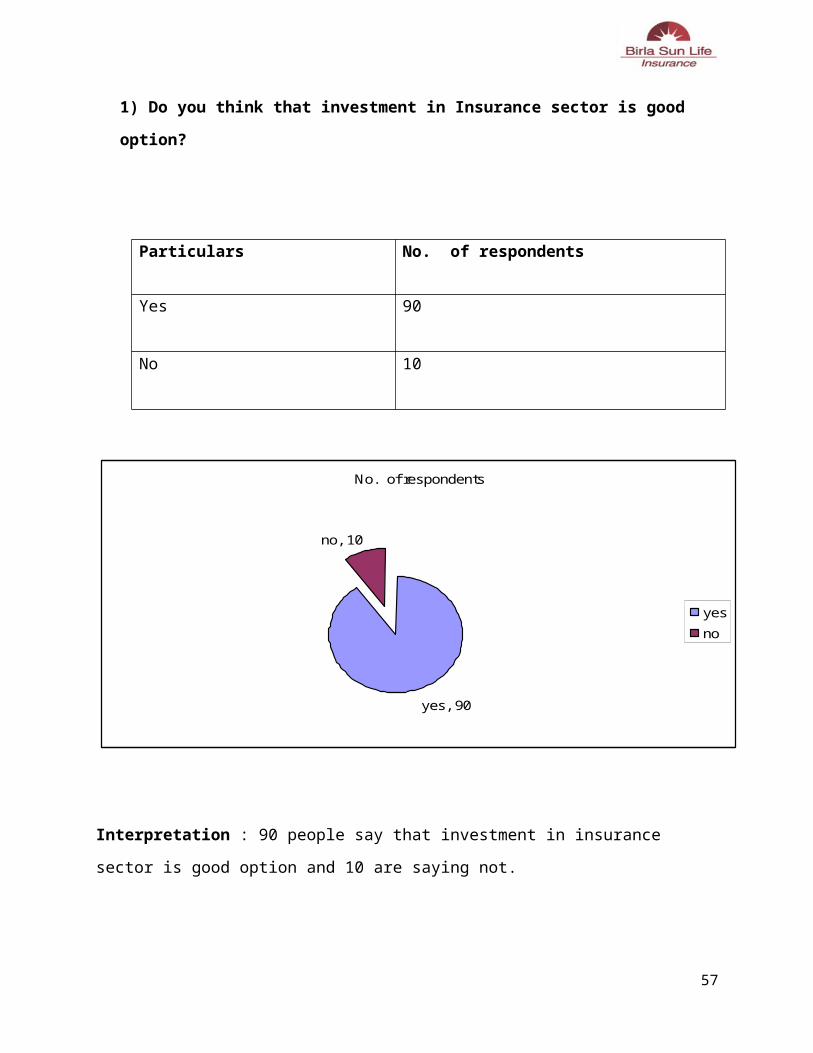

1) Do you think that investment in Insurance sector is good option?

Particulars No. of respondents

Yes 90

No 10

No. of respondents

yes, 90

no, 10

yes

no

Interpretation : 90 people say that investment in insurance sector is good option and 10 are

saying not.

41

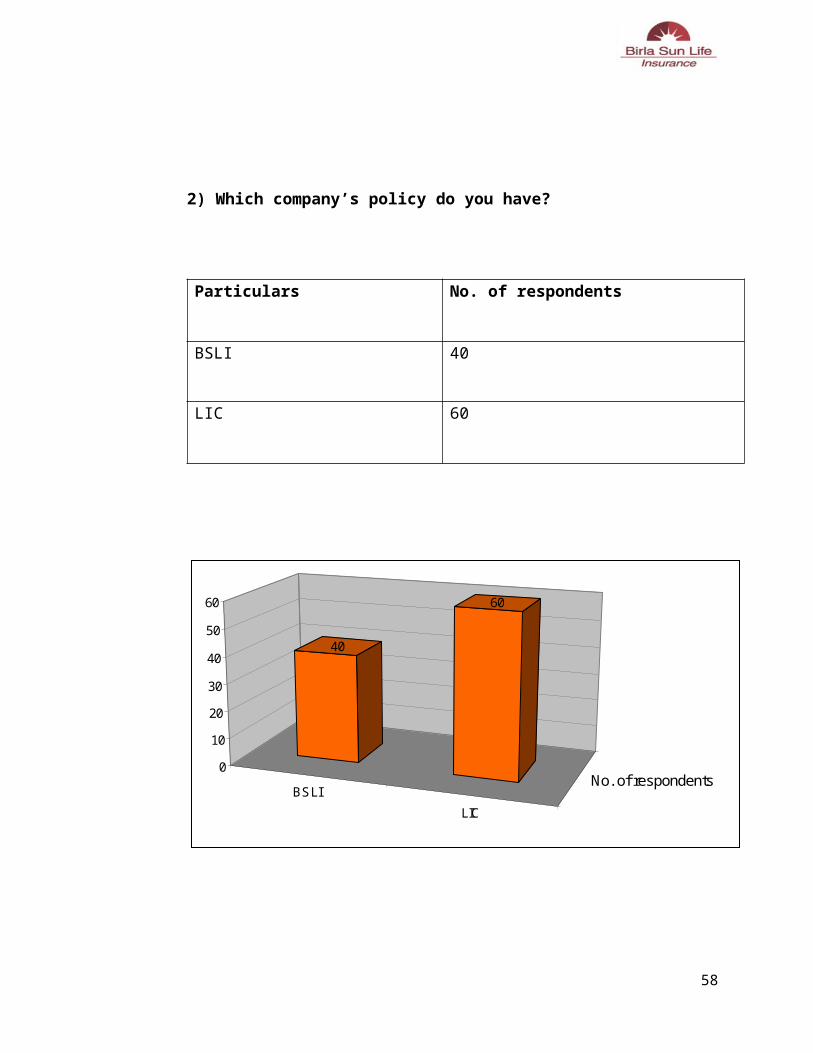

2) Which company’s policy do you have?

Particulars No. of respondents

BSLI 40

LIC 60

BSLI

LIC

No. of respondents

40

60

0

10

20

30

40

50

60

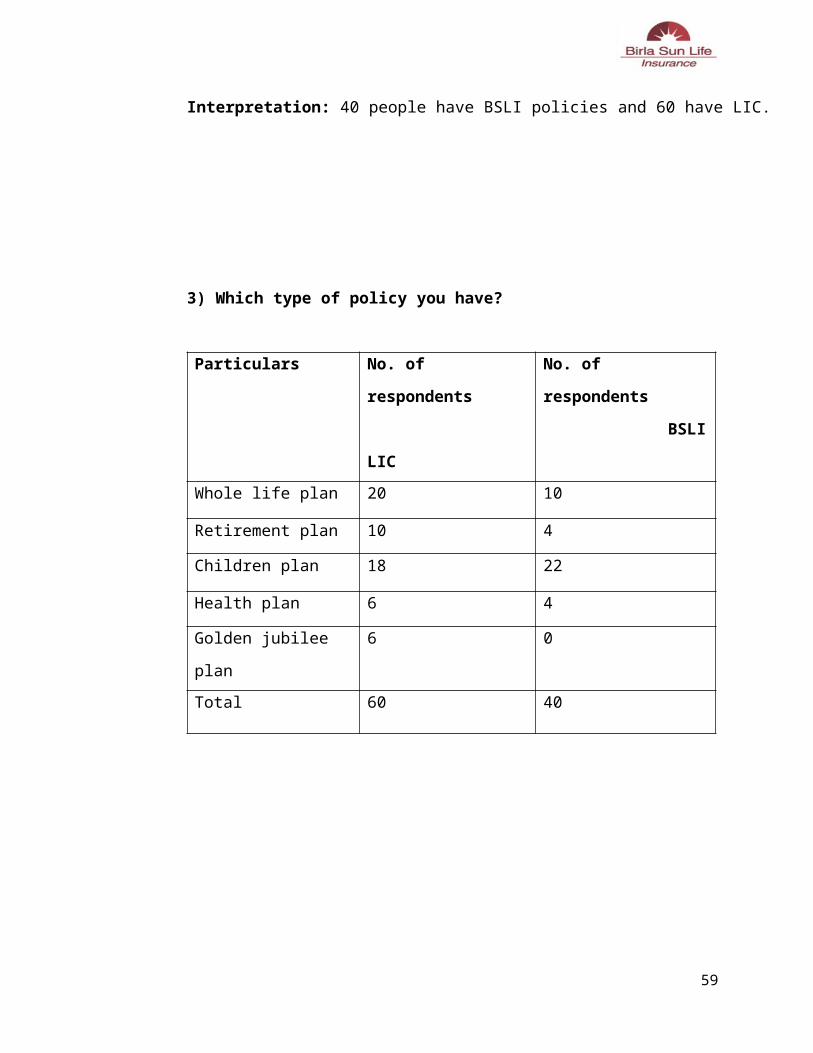

Interpretation: 40 people have BSLI policies and 60 have LIC.

42

3) Which type of policy you have?

Particulars No. of respondents

LIC

No. of respondents

BSLI

Whole life plan 20 10

Retirement plan 10 4

Children plan 18 22

Health plan 6 4

Golden jubilee plan 6 0

Total 60 40

20

10

18

6 6

10

4

22

4

00

5

10

15

20

25

No. of respondents LIC

No. of respondents BSLI

Interpretation: 20 people of LIC and 10 of Birla have whole life plan, 18 people of LIC and 22 of birla have

Children plan.

43

4) What percentage of interest you get from it?

Particulars No. of respondents

LIC

No. of respondents

BSLI

Below 5 % 0 0

5-8 % 14 6

8-12 % 42 28

Above12 % 4 6

0 0

14

6

42

28

46

0

5

10

15

20

25

30

35

40

45

Below 5 % 5-8 % 8-12 % Above12 %

No. of respondents LIC

No. of respondents BSLI

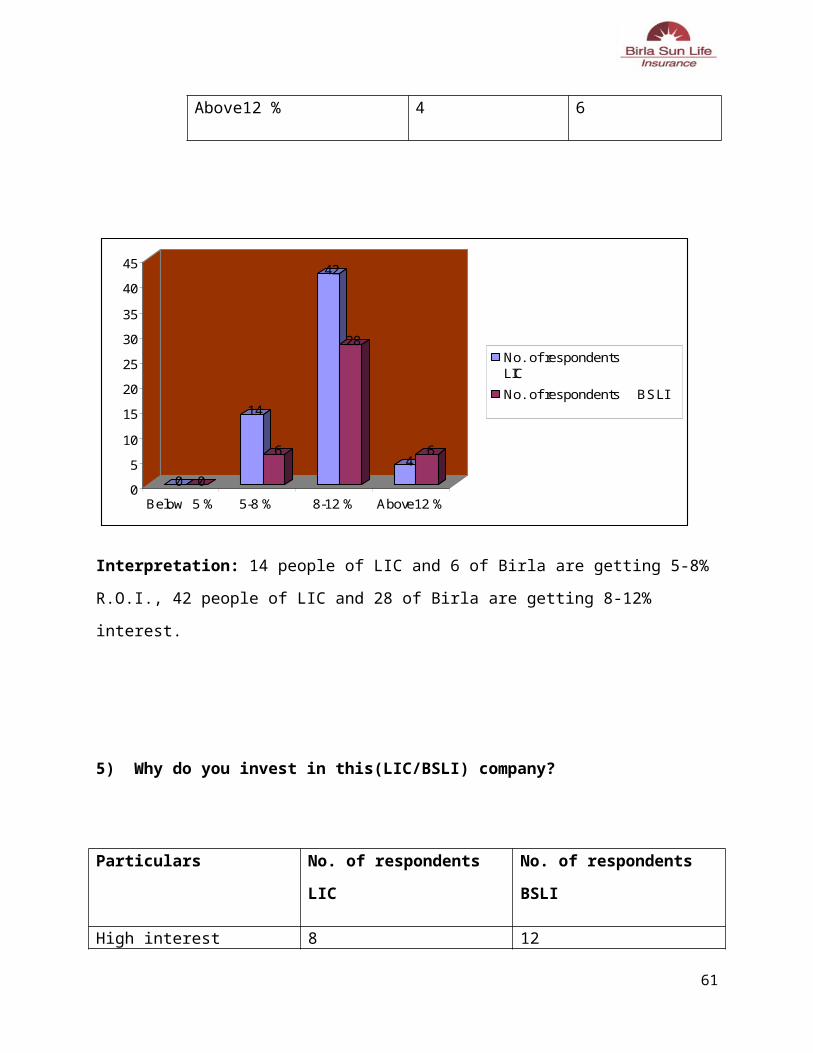

Interpretation: 14 people of LIC and 6 of Birla are getting 5-8% R.O.I., 42 people of LIC and

28 of Birla are getting 8-12% interest.

44

5) Why do you invest in this(LIC/BSLI) company?

Particulars No. of respondents

LIC

No. of respondents

BSLI

High interest 8 12

Good image of CO. 12 4

Growth of the CO. 18 12

Annual premium is reasonable 10 4

Maturity benefits 12 8

8

12

18

10

12

12

4

12

4

8

0 5 10 15 20

High interest

Good image of CO.

Growth of the CO.

Annual premium isreasonable

Maturity benefits

45

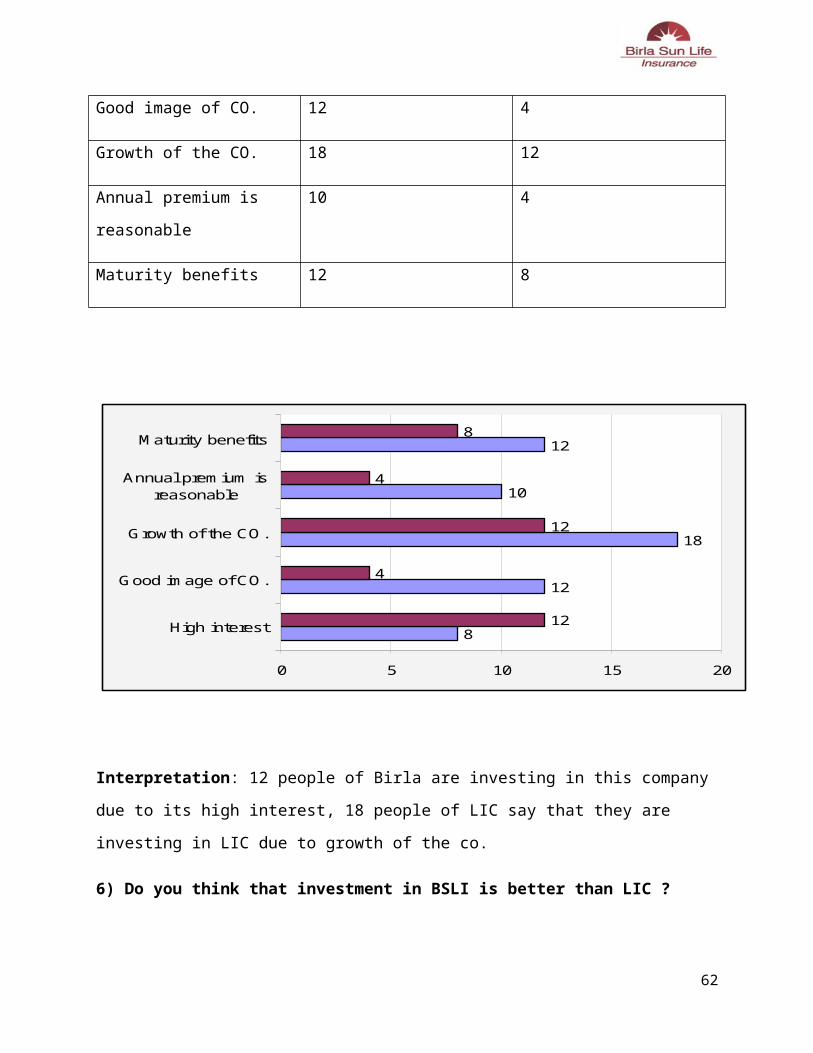

Interpretation: 12 people of Birla are investing in this company due to its high interest, 18

people of LIC say that they are investing in LIC due to growth of the co.

6) Do you think that investment in BSLI is better than LIC ?

Particulars No. of respondents

Yes 44

No 56

Interpretation: 44 people are saying that investment in BSLI is better than LIC, but 56 are

saying no.

(If NO then go to Q.N. 8 otherwise Q.N. 7)

46

7) If yes, then why?

Particulars No. of respondents

Guaranteed F.V. at maturity 10

Growth rate 16

More ULIP plan 8

Risk covered 4

All above 6

No. of respondents

10

16

8

4

6 Guaranteed F.V. atmaturity

Growth rate

More ULIP plan

Risk covered

All above

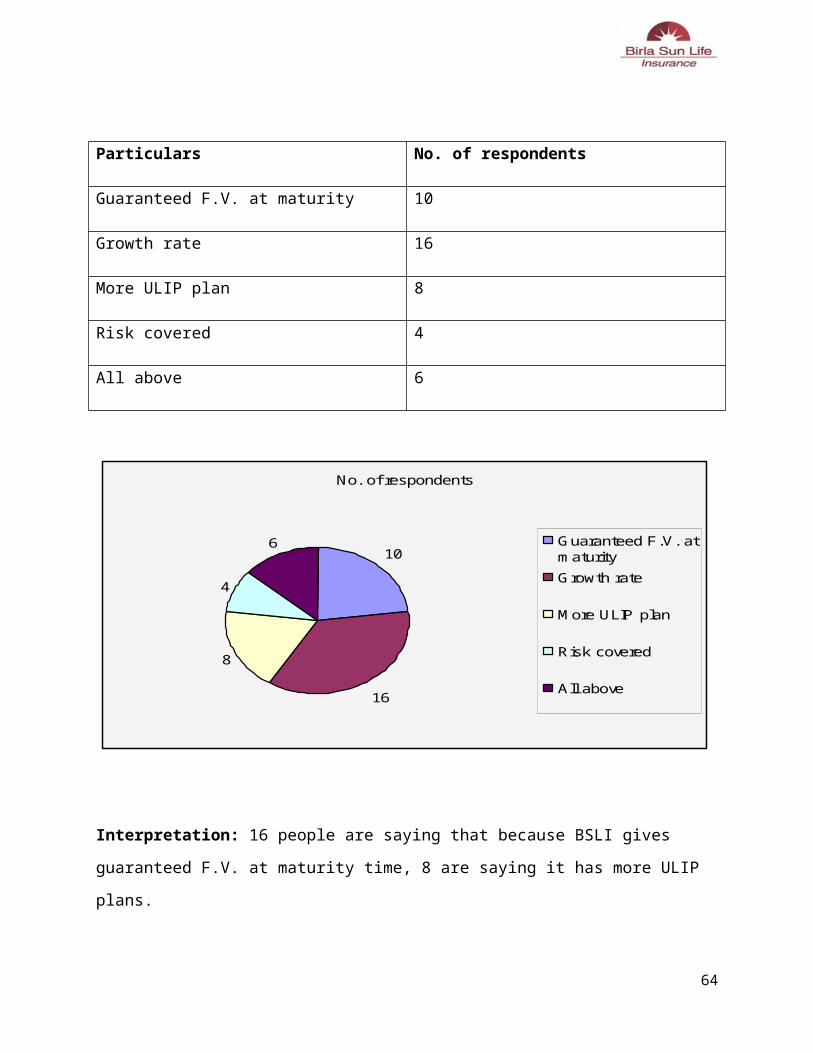

Interpretation: 16 people are saying that because BSLI gives guaranteed F.V. at maturity time,

8 are saying it has more ULIP plans.

47

8) If no, then why?

Particulars No. of respondents

LIC have govt. stake 24

Brand loyalty of LIC 14

Low A.P. than BSLI 12

High return 6

LIC have govt. stake, 24

Brand loyalty of LIC, 14

Low A.P. than BSLI, 12

High return, 6

LIC have govt. stake

Brand loyalty of LIC

Low A.P. than BSLI

High return

48

Interpretation: 24 people are saying that investment in LIC is better it has govt. stake, 14 are

saying it has brand loyalty.

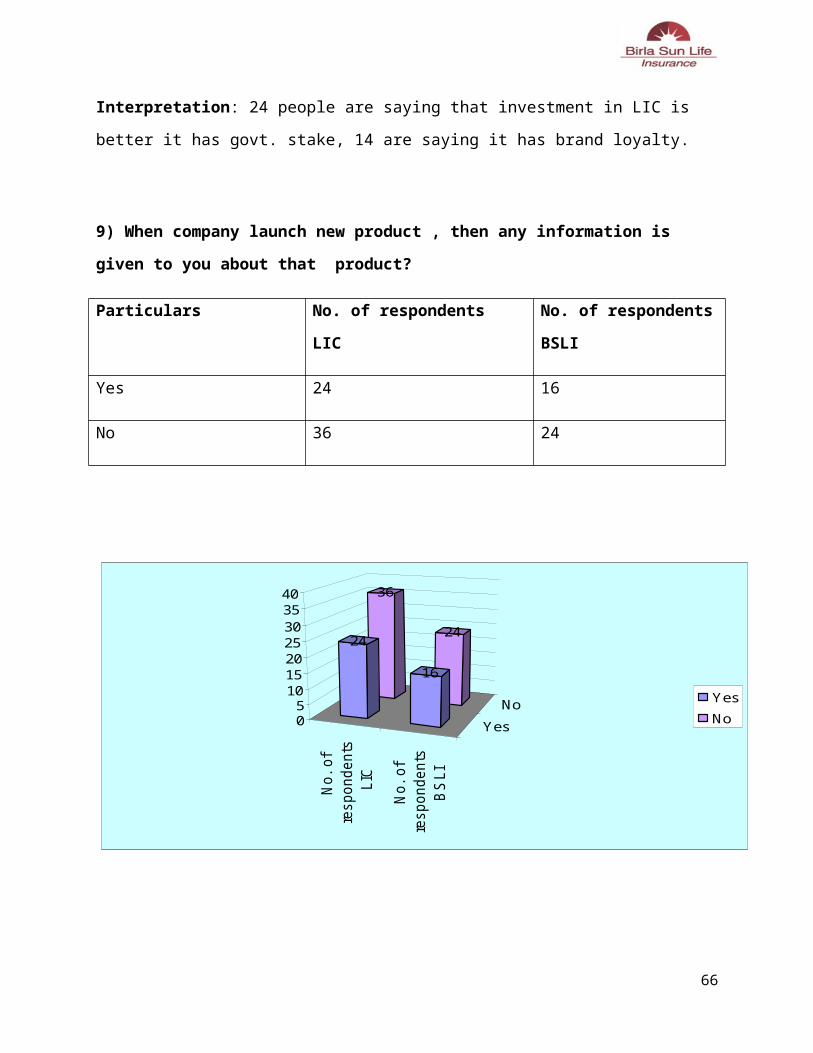

9) When company launch new product , then any information is given to you about that

product?

Particulars No. of respondents

LIC

No. of respondents

BSLI

Yes 24 16

No 36 24

No.

of

respondents

LIC

No.

of

respondents

BS

LI

Yes

No

36

2424

16

05

10152025303540

Yes

No

Interpretation: 24 people of LIC are saying yes and 36 are saying no, 16 people of BSLI are

saying yes and 24 are saying no about providing information.

49

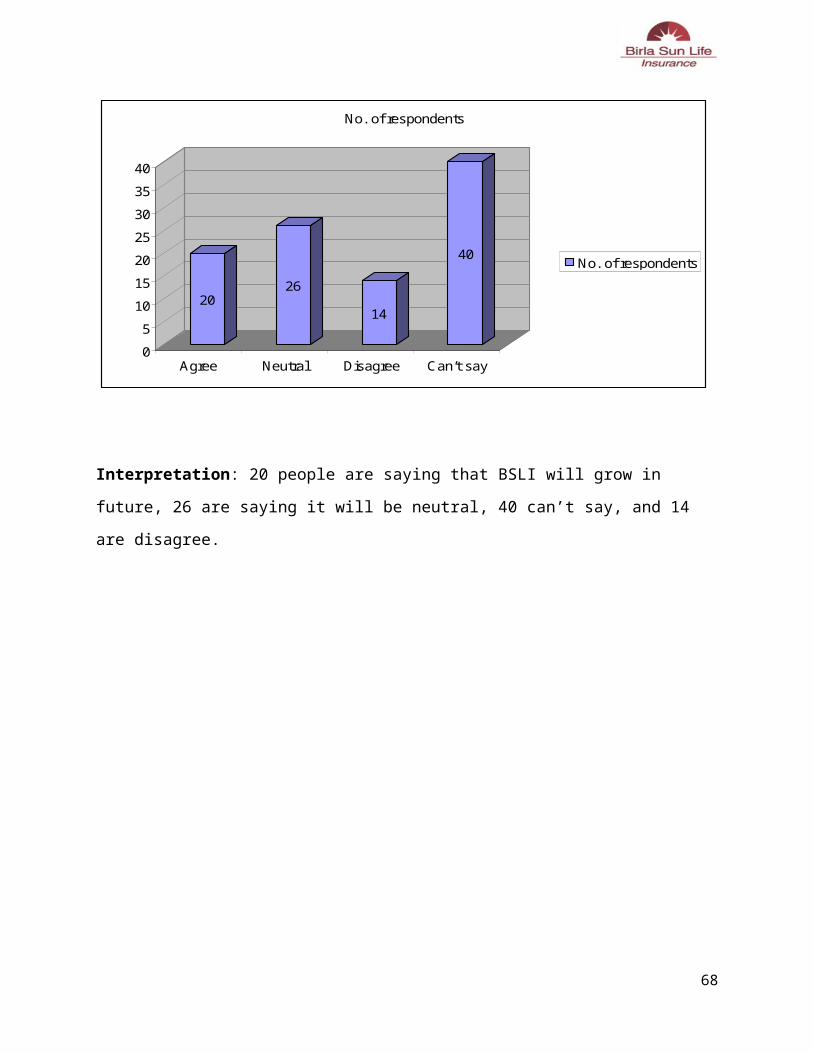

10) In near future, do you think BSLI will have high growth rate?

Particulars No. of respondents

Agree 20

Neutral 26

Disagree 14

Can’t say 40

2026

14

40

0

5

10

15

20

25

30

35

40

Agree Neutral Disagree Can’t say

No. of respondents

No. of respondents

Interpretation: 20 people are saying that BSLI will grow in future, 26 are saying it will be

neutral, 40 can’t say, and 14 are disagree.

50

51

FINDINGS

90 people saying that investment in insurance sector is good option and 10 are saying no.

40 people have BSLI policies and 60 have of LIC.

10 people of BSLI have Whole life plan, 4 have retirement plan, 22 have children plan, 4

have health plan.

56 people are saying that investment in LIC is better than BSLI, 44 are saying investment

in BSLI is better.

Most of the people of both LIC and BSLI are getting rate of interest 8-12%

Most of the people have children plan of BSLI.

Most of the people invest due to high interest of the policy in BSLI

People have more faith in govt. Companies than the private.

14 people invest in LIC due to its brand loyalty.

26 people saying that BSLI growth will be neutral in near future.

52

53

SUGGESTIONS

1) Information regarding new product should be provided to the customers.

2) The company should find out the no. of people who are not having any of the insurance

plans through an intensive market research and motivate them to get insured.

3) At some level Company should provide information to the customers about the

charges of the policy.

4) Company should target each and every class of the society.

5) Charges should be low of the policies.

6) Annual premium should be reasonable.

7) BSLI Company should work in systematic way.

54

55

LIMITATIONS

Some of the respondents were not cooperative.

There are chances of biased information provided by the respondents.

As the sample size is small compared to the total population, therefore there

can’t be full accuracy.

The time was limited.

Area was limited.

56

57

CONCLUSION

Here in this study we see that people have more policies of LIC in comparison to BSLI. People

have more faith in govt. companies than private. So it is necessary for BSLI Co. that it should

give more attention to that points or that areas where it lacks for further future growth. Insurance

sector is very wide and co. can grow in future.

58

59

BIBLIOGRAPHY

www.birlasunlife.com

www.licindia.com

www.google.com

Newspapers

60

61

ANNEXURE

NOTE: The information that you will provide will be kept confidential and will be used

only for academic Purpose.

Our questionnaire will be to those persons who have plans of BSLI or LIC.

GENERAL

Name __________________________________________________________________

Addres_________________________________________________________________

Gender_________Age ________Contact No. __________________________________

1. Do you think that investment in insurance sector is good option

(a) Yes (b) No

2. Which company’s policy do you have?

(a) Birla Sun Life Insurance (b) LIC

3. Which type of policy you have?

(a)Whole Life Plan (b) Retirement Plan (c) Children Plan (d) Health Plan

(e) Golden jubilee plan (f) any other please specify___________________

4. What percentage of interest you get from it?

(a) Below 5% (b) 5-8% (c) 8-12% (d) Above 12%

5. Why do you invest in this company?

(a) High interest (b) good image (c) Company growth

(d) Annual premium is reasonable (e) due to maturity benefits

(f) Any other please specify ______________________________

62

6. Do you think that investment in BSLI is better than LIC?

(a) Yes (b) No

( If your answer is no then jump to question no. 8)

7. if yes then why?

(a) Because BSLI gives guaranteed fund value at maturity time

(b) Growth rate of company is high (c) BSLI has more ULIP plans than LIC

(d) Risk factor is covered properly (e) all above

(f) Any other (please specify)_____________

8. If no then why?

(a) Because LIC is having government stake. (b) Brand loyalty of LIC

(c) It has low premium plans than BSLI (d) Investment return is higher than BSLI

(e) Any other (please specify)__________________________

9. Whenever company launch new product, then any information is given to you about that

product?

(a) Yes (b) No

10. In near future BSLI is having high growth rate.

(a) Agree (b) neutral (c) disagree (d) can’t say

Any suggestions __________________________________________________

63

SUMMER TRAINING REPORT

ON

“PERFORMANCE EVALUATION OF BIRLA SUN LIFE

INSURANCE PRODUCTS IN COMPARISON WITH LIFE

INSURANCE CORPORATION (LIC)”

A report submitted to Panjab University, ChandigarhIn partial fulfillment of the requirement

For the degree of

MASTER OF COMMERCE(Session: 2013-14)

SUPERVISED BY: SUBMITTED BY:Prof. (Mrs.) Harpreet Kaur Jaskiranjeet Kaur

H.O.D. (Commerce) M.Com. (2nd Sem)

Roll No.6158

SWAMI GANGA GIRI JANTA GIRLS COLLEGE

64

RAIKOT (LUDHIANA)

PREFACE

To achieve partial and concrete results, it is necessary that theoretical

knowledge must be supplemented with practical environment.

Keeping this view in mind, I have completed my research work regarding

“Performance evaluation of Birla Sun Life Insurance products in

comparison with Life Insurance Corporation (LIC)” By doing this

research work I have learnt a lot of things which would be really helpful for

me in future. This experience in decision making and practical application of

knowledge has contributed greatly to my growth.

JASKIRANJEET KAUR

65

DECLARATION

I Jaskiranjeet Kaur, hereby declare that the project entitled ““Performance

evaluation of Birla Sun Life Insurance products in comparison with Life

Insurance Corporation (LIC)” submitted for partial fulfillment for the award of

degree of MASTER OF COMMERCE (M.COM) is entirely original and has not

been submitted earlier by any one for any Degree or Diploma.

Date:

Place: Signature

66

ACKNOWLEDGEMENT

I deem it a great privilege to thank all those people who helped me to complete

this project work. I express my sincere thanks to the management of the

SWAMI GANGA GIRI JANTA GIRLS COLLEGE RAIKOT and our

respected Head of the Department Prof. Harpreet Kaur for giving me this

opportunity to undertake the project work.

I express my profound thanks to Mr. Munish Sharma, Birla Sun Life for

giving me valuable advice and guidance and sparing valuable time in

clarifying various points raised by me.

JASKIRANJEET KAUR

67

INDEX

Serial No. Particulars Page No.

1 Introduction to Insurance 1-6

2. Company profile 7-11

3. SWOT Analysis 12-13

4. Major competitor LIC 14-17

5. Various life insurance plans 18-35

6. Objectives 36

7. Research Methodology 37-38

8. Data Analysis 39-49

9. Findings 50-51

10. Suggestions 52-53

11. Limitations 54-55

12. Conclusion 56-57

13. Bibliography 58-59

Annexure 60-62

68