biscuits t.y.b.b.a ppr

TRANSCRIPT

APRODUCT PROJECT

REPORTON

: PREPARED BY :

RAJESH H. MER: CLASS :

T.Y.B.B.A.

: COLLEGE :

SMT. M.T. DHAMSANIA COLLEGE RAJKOT

: ACADEMIC YEAR :

2011 – 2012

ROLL NO. – 30 SEAT NO. –

: SUBMITTED TO :

SAURASHTRA UNIVERSITY.

: GUIDED BY:

Prof. B.L.SARDHARA

1

DECLARATIONI RAJESH H. MER undersigned a student of T.Y.B.B.A.

here by declare that the project work presented in this report is my

own work and has been carried out under the supervision of Prof.

B.L.SARDHARA of SMT. M.T. DHAMSANIA COLLEGE

RAJKOT

This report has not been previously submitted to any other

University your any examination.

DATE:

PLACE: RAJKOT (RAJESH H. MER.)

2

PREFACEThe B.B.A. is a professional course which helps the students

to develop the knowledge for business field and industry in

T.Y.B.B.A. the product project report is the part of our syllabus.

The product project report shows us actually what

difficulties is new entrepreneur of small business faces while

starting his unit. A product project report plays a significant role

for small business specially for financial arrangement that’s why

proper care should be taken in preparing this report.

3

ACKNOWLEDGEMENTI glad to present Product Project Report on BISCUIT

MIXTURE to the Saurashtra University.

In this reference, I am heartly thankful to Prof.

B.L.SARDHARA for support and guidance provided by her.

I am also thankful to all those person who have helped me in

every aspects for preparing the project.

DATE:

PLACE: RAJKOT (RAJESH H. MER.)

4

INDEXNo. Particular

1 Introduction of Product.

2 Project at a Glance.

3 Partner’s Background.

4 Location.

5 Market Potential.

6 Raw material.

7 Basis and Presumption.

8 Implementation Schedule.

9 Manufacturing Process.

10 Production Capacity.

11 Financial Details of Project.

(A) Details of lord and Building.

(B) Machinery & Equipments.

(C) Other Fixed Assets.

12 Working Capital.

(A) Personnel.

(B) Raw material.

(C) Utilities.

5

(D) Other Contingent Express.

13 Project Cost.

14 Sources of Funds.

15 Depreciation.

16 Financial Analysis.

(A) Cost of Production.

(B) Turnover.

(C) Return on Investment.

(D) Profitability Analysis.

(E) Break Even Analysis.

(F) Balance Sheet.

17 Suppliers of Machinery.

18 Future Prospects.

19 Risk Factors.

6

Introduction Of Product

Biscuits constitute an important item of bakery industry.

Today Biscuits become a common item of consumption among all

classes of people with tea or coffee, Biscuits make a tasty

nutritious shake. Biscuits has become here and more popular as a

convenient food with the changes taking place in the economic life

of masses, the consumption of Biscuit has been increasing over the

years, and this envisages the scope for setting up of Biscuit

Mixture units.

People started manufacturing Biscuits of their own taste by

using baking ovens very popular in the market now-a-days. To

made it more convenient there is a need of Biscuit Mixture which

will be ready mix and after adding water, the dough will be ready

mix hour on commercial scale saves times, labour and is

sometimes ever cheap to the housewives.

7

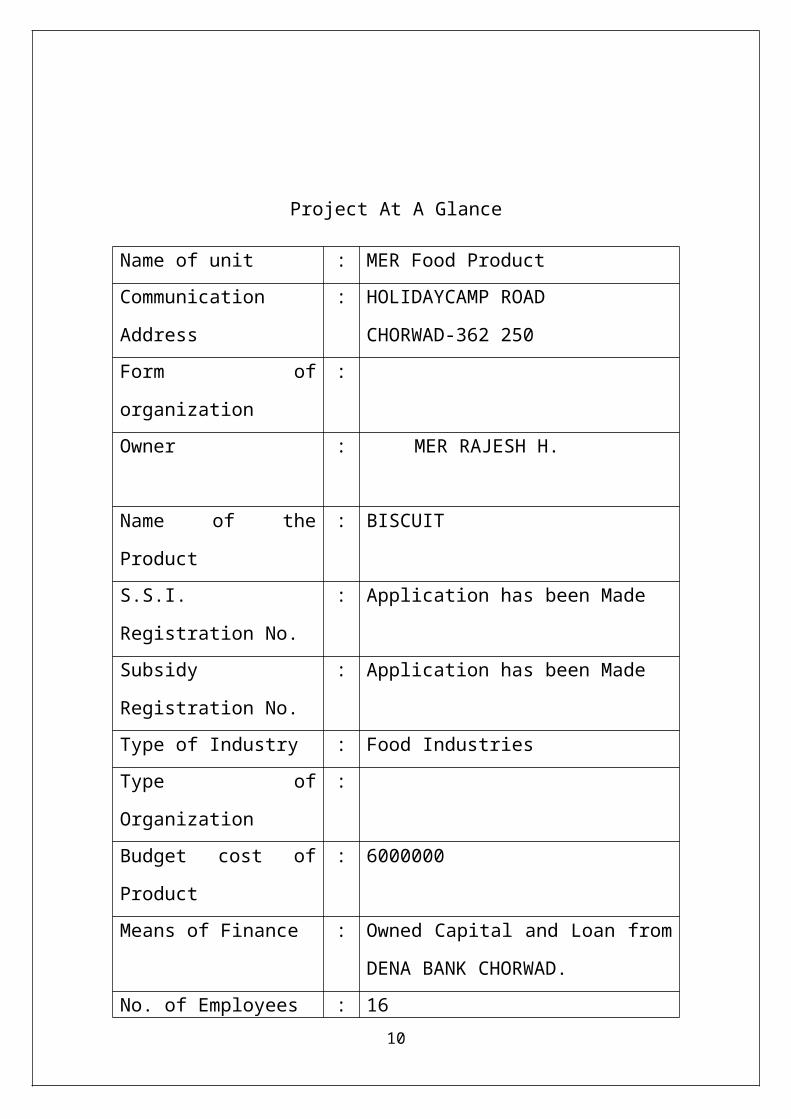

Project At A Glance

Name of unit : MER Food Product

Communication Address : HOLIDAYCAMP ROAD

CHORWAD-362 250

Form of organization :

Owner : MER RAJESH H.

Name of the Product : BISCUIT

S.S.I. Registration No. : Application has been Made

Subsidy Registration No. : Application has been Made

Type of Industry : Food Industries

Type of Organization :

Budget cost of Product : 6000000

Means of Finance : Owned Capital and Loan from DENA

BANK CHORWAD.

No. of Employees : 16

Plant Installed Capacity : 100 %

8

Owner’s Background

Name : MER RAJESH H.

Age : 20 Years.

Education : B.B.A. with Advance Marketing

Management.

Address : Near water tank chorwad.

Financial Contribution : 20,00,000

Duties and Responsibilities : Marketing and Production Department.

9

Location

To choose the proper location is first step for establishment

of unit. True selection of location helps unit for better growth,

while selecting the site of location the factors should be considered

are as follows:

1. Availability of Raw material.

2. Cheaper Manpower.

3. Transport Facilities.

4. Availability of Energy sources.

I shall start Biscuits industry in chorwad at holidaycamp

road chorwad because Raw material and labour are the main

factors in this industry which is early available at this place.

10

Market Potential

The consumption of Biscuit has been increasing over the

years. The finding of survey indicates that nearly 47% of Biscuits

are consumed in the rural and semi-urban areas which constitutes

bulk of our population. Looking at such a demand this ready mix

can definitely be a popular item particularly in rural and urban

areas.

So, we can class by whole Biscuit market into there

categories based on area:

1. Urban Market.

2. Semi-Urban Market.

3. Rural Market.

11

Raw Material

The main raw material used in Biscuit Mixture are as

follows:

1. Wheat Flour.

2. Sugar.

3. Vegetable Fat.

4. Miscellaneous Items.

(A) Milk Powder.

(B) Chemical.

(C) Colour Flavor.

(D) Coco Vit Fat.

(E) Glucose Etc.

5. Packing Material.

Above all raw materials are easily available from local

market. So, there is no difficulty to get raw material. So, there is

less of transportation. All the materials are available from local

market.

12

Basis And Presumption

1. The scheme is based on single shift 300 working days per

annul.

2. For the first 2 years the utilisation capacity will be 65.71% from

the third year onwards it will run at its full capacity.

3. Labour wages as per the rate prevailing in the area.

13

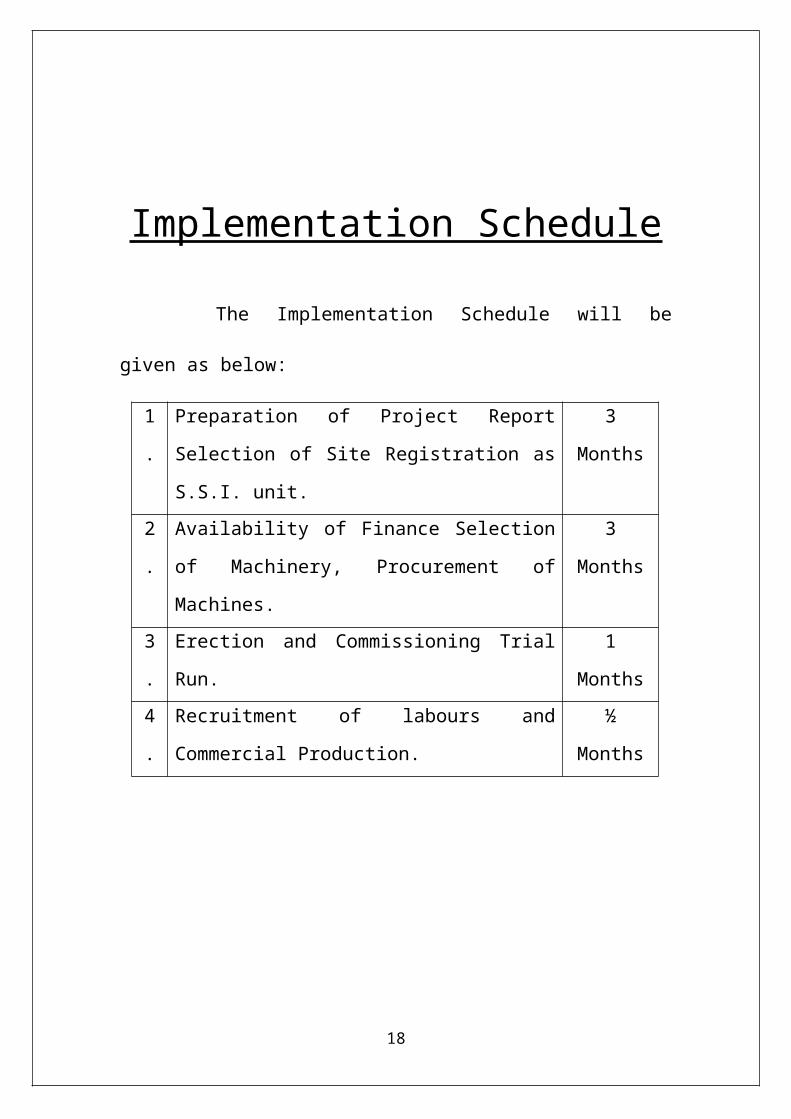

Implementation Schedule

The Implementation Schedule will be given as below:

1. Preparation of Project Report Selection of Site

Registration as S.S.I. unit.

3 Months

2. Availability of Finance Selection of Machinery,

Procurement of Machines.

3 Months

3. Erection and Commissioning Trial Run. 1 Months

4. Recruitment of labours and Commercial

Production.

½ Months

14

Manufacturing Process

The ingredients normally used are Maida, Sugar, Vanaspati

or Bakery Fat, Backing powder, Milk powder, Essence and

Chemicals. The ingredients as per formulation except Vanaspati

bakery fat are dried to desired moisture content before grinding if

required. They are then weighed, mixed and blended thoroughly.

The product thus obtained is packed in polythene bags of suitable

size paper box and then kept in big cartoons for storing and

transportation. The fat is to be added at the fire of preparation of

the mixture for baking by the consumer.

Quality Specification: -

It is a new product and therefore the quality specifications

about Moisture content and bacteriological count etc. are required

to be looked into.

15

Production Capacity

No. Particulars Quantity

1. Biscuit Mixture 500

g.m. Packet

1,00,000

2 Biscuit Mixture 250

g.m. Packet

1,00,000

3 Biscuit Mixture 100

g.m. Packet

1,50,000

4 Biscuit Mixture 50

g.m. Packet

2,00,000

The total production capacity at 100% is 2,00,000 packets of

50 gm & 1,50,000 packets of 100 gm. & 1,00,000 packets of 250

gm& 1,00,000 packet of 500 gm.

16

Financial Aspect

(I) Details of Lard & Building

No. Details Area [sq. Ht] PSM Rate Total Valve

1. Lard & Building 500 5,000 25,00,000

(II) Machinery & Equipment

No. Details No. of

Machines

Amount

1. Shifter Fitted with 3 Hp Motor 1 85,000

2. Micropuluerser complete with Motor 1 65,000

3. Cabinet model electrically operated

oven with 48 trays each 32" × 16" × 1"

with thermostatic control & other

accustoms

1 2,00,000

4. Weighing machine

a. Platform Type capacity 100

kg.

b. Table model.

1

1

55,000

35,000

5. Polythene Bag sealing machine (5,000

each)

2 40,000

6. Miscellaneous equipments tools, trays, 85,000

17

bells etc.

Total Machinery & Equipment 5,65,000

(III) Other Fixed Assets

No. Details Amount

1. Electricity & Installation 54,500

2. Office Furniture & Other Equipment 1,24,500

1,79,000

Total Fixed Cost = 25,00,000 + 5,65,000 + 1,79,000

= 32,44,000

18

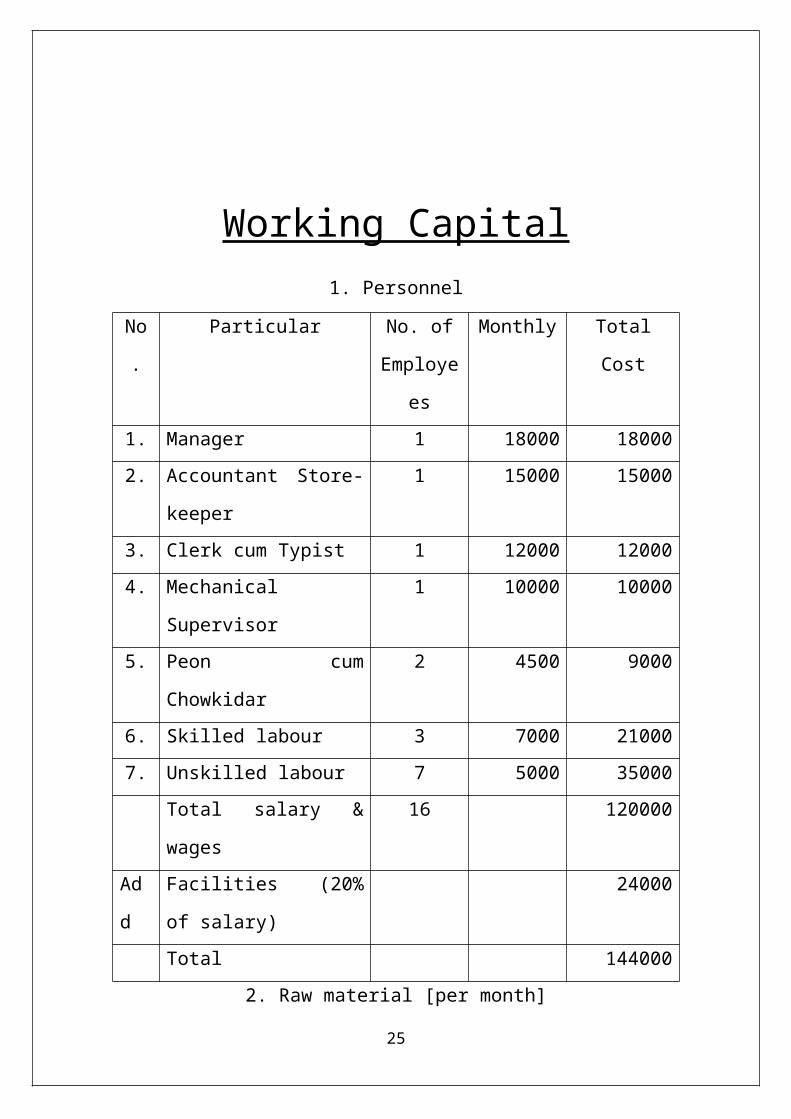

Working Capital1. Personnel

No. Particular No. of

Employees

Monthly Total Cost

1. Manager 1 18000 18000

2. Accountant Store-keeper 1 15000 15000

3. Clerk cum Typist 1 12000 12000

4. Mechanical Supervisor 1 10000 10000

5. Peon cum Chowkidar 2 4500 9000

6. Skilled labour 3 7000 21000

7. Unskilled labour 7 5000 35000

Total salary & wages 16 120000

Add Facilities (20% of salary) 24000

Total 144000

2. Raw material [per month]

No. Particular Quantity (14 Kg)

Rate [perkg.]

Value

1. Wheat Flour 4,200 18 75,600

2. Sugar 1,300 30 39,000

3. Vegetable Fat 750 80 60,000

4. Miscellaneous items Milk Powder, Chemicals, Colour, Flavor, Coco, Vit, Fat, Glucose, etc.

35,600

5. Packing Material 52,000

Total 2,62,200

19

3. Utilities [per month]

No. Particular Amount

1. Power 8,000

2. Water 12,000

Total 20,000

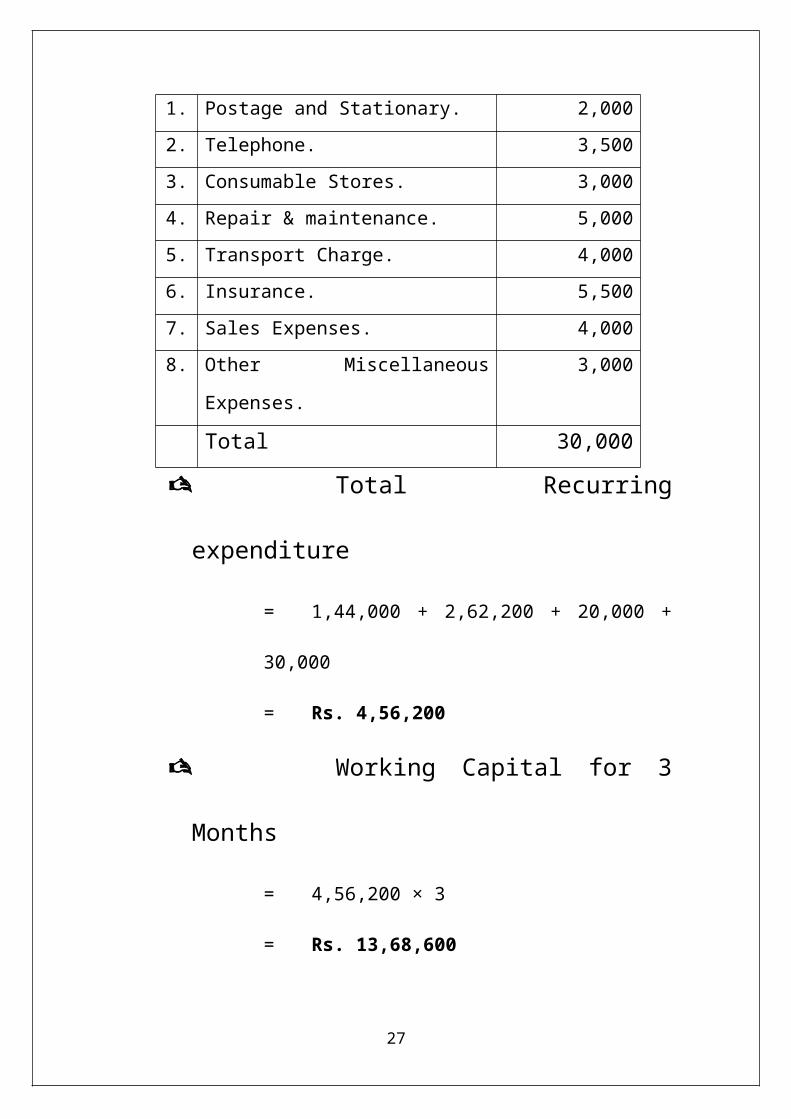

4. Other Contingent Expenses [per month]

No. Particular’s Amount

1. Postage and Stationary. 2,000

2. Telephone. 3,500

3. Consumable Stores. 3,000

4. Repair & maintenance. 5,000

5. Transport Charge. 4,000

6. Insurance. 5,500

7. Sales Expenses. 4,000

8. Other Miscellaneous Expenses. 3,000

Total 30,000

Total Recurring expenditure

= 1,44,000 + 2,62,200 + 20,000 + 30,000

= Rs. 4,56,200

Working Capital for 3 Months

= 4,56,200 × 3

= Rs. 13,68,600

Project Cost20

1. Fixed Capital

No. Particular Amount

1. Land and Building 25,00,000

2. Machinery & Equipment 5,65,000

3. Other Fixed & Installation

a. Electricity & Installation

b. Office Function & other Equipment

46,500

1,32,500

Total 32,44,000

2. Working Capital

No. Particular Amount

1. Personnel (Wages & Salary) 1,44,000

2. Raw Material 2,62,200

3. Utility of Power & Water 20,000

4. Other contingent Expenses 30,000

Total 4,56,200

Total capital investment: -

Fixed Capital Investment 32,44,000

Working Capital for 13,68,600

(4,56,200 × 3)

Total Project Cost 46,12,600

Sources of Funds: -

No. Description Amount

21

1. Owned Capital 23,03,300

2. Borrowed Capital 23,03,300

46,12,600

Owners Capital: -

No. Description Amount

1. RAJESH H. MER 23,03,300

23,03,300

Borrowed Capital: -

No. Description Amount

1. DENA BANK CHORWAD 23,03,300

23,03,300

Interest on Fund: -

No. Description Rate Amount

1. Owned Capital 10% 2,30,330

22

2. Borrowed Capital 12% 2,76,396

5,06,726

Depreciation: -

No. Description Rate Amount

1. Depreciation on Machinery 25% 1,41,250

2. Depreciation on L&B 15% 3,75,000

3. Depreciation on Other 12% 21,480

Assets

5,37,730

Cost of Production

23

No. Particulars Amount

1. Total recurring cost per year (4,) 54,74,400

2. Total Depreciation 5,37,730

Total cost of Production 6012130

Turnover

24

No. Particulars Rate per packet Quantity Value

1. Biscuit Mixture 500

g.m. Packet

39.5 1,00,000 3950000

2 Biscuit Mixture 250

g.m. Packet

19.5 1,00,000 1950000

3 Biscuit Mixture 100

g.m. Packet

9.5 1,50,000 1425000

4 Biscuit Mixture 50

g.m. Packet

4.5 2,00,000 900000

Annual Turnover 8225000

25

Return on Investment

ROI = EBIT × 100

Cost of Project

= 1705544× 100

4612600

= 36.97%

Cost Of Capital

Interest on Owned Capital 10 %

Interest on Borrowed Capital 12 %

COC = 10 + 12

2

= 11 %

Thus, ROI > COC

26

Profitability Analysis

Sales 8225000

Less: Cost of Production 6012130

EBIT 2212670

Less: Interest 506726

EBT 1706144

Less: Tax 35 % 597150

PAT 1108994

Profit Volume Ratio:

PVR = Contribution × 100

Sales

= 2212670× 100

8225000

= 26.90%

Net Profit Ratio:

Net Profit Ratio = Net Profit × 100

Sales

= 1108994 × 100

8225000

= 13.48%

27

Break Even Analysis

For the calculation of B.E.P., we have to calculate fixed cost

& variable cost

Fixed Cost:

Total Depreciation 537730

40% of Salary & Wages 691200

40% of other Contingent Expenses 144000

Interest on Total Investment 506726

1879656

Variable Cost:

60% of Salary & Wages 1036800

60% of other Contingent Expenses 216000

Raw Materials 3146400

Utilities 1,20,000

4519200

28

Contribution:

Contribution = Sales – Variable Cost

= 8225000 – 4519200

= 3705800

BREAK EVEN POINT:

B.E.P. (in %) = Fixed Cost × Utilized Capacity

Contribution

= 1879656× 65.71

3705800

= 33.33%

29

Trading & P&L Acc.

Particulars Amount Particulars Amount

Purchase 3146400 Sales 8225000

Utility 240000

Gross Profit 4838600

8225000 8225000

Wages &Salary 1728000 Gross Profit 4838600

Depreciation 537730

Interest 506726

Other Contingent 360000

Expenses

EBT 1706144

Less: Tax 597150

Net Profit 1108994

4838600 4838600

30

Balance Sheet

Capabilities Amount Assets Amount

Capital: L & B

Owned: 2303300 2500000

– Dep.: 375000 2125000

Machine& Equip.

Borrowed: 2303300 565000

– Dep.: 141250 423750

Interest 506726

Other Assets

Net Profit 1108994 179000

– Dep.: 21480 157520

6222320 Cash & Bank 3516050

6222320

31

Suppliers of Machinery

Address of Machines and

Equipment Suppliers:

(i) M/s. Nagpal Brothers,

2789 Zorawar Singh Marg, Delhi.

(ii) M/s. Nagpal Engg. Works,

Loharogate, Patiala.

(iii) M/s. Baltiboi & co. (p) Ltd.,

P.B. No. 1904 – Fort, Bombay – 400 001.

(iv) M/s. Novel Engineers Pvt. Limited,

4th Floor, Sambhava Chambers,

Sir Phirozshah Mehta Road,

Bombay – 400 001.

(v) M/s. Narang Corporation,

P –24 Cop naught place,

New Delhi – 110 002.

Address of raw material Suppliers:

32

Locally Available

Future Prospects

Every units airs at its growth and development in future at

the time of establishment. The future development of any unit

shows its success in the market. Future development may be get

through the increasing installed capacity or utilizing the existing

resources of the unit to the full extend.

So far as our unit is concern we have to utilize folly the

available resources of our unit and by increasing production

capacity we want to cover none market share with maintenance of

good quality.

There are so many varieties of Biscuits in the market. The

consumption of Biscuits has been increasing over the year. We

wants to cover more market in rural as well as in urban areas.

Looking to this good prospect I select the product of Biscuit.

It is for medium clays people as well as poor class people also.

33

Risk Factors

In each and every business activity there is some risk in the

some way our unit is also having some risk factory, which are as

follows:

As our product is under the list of food items so if license not

provided by government authority within a specific time it is

difficult to start the production.

There is also possibility for non-receipt or less receipt of loan

from government.

At present there is minimum competition in the market but in

the future then may be cut-throat competition and it may be

difficult to continue the business at the time of competition.

It is also possible that all the factory may suitable for production

and finance but the marketing of our products may not enough

so there is every possibility of failure or close-down the unit.

34