board member’s guide...governmental accounting government-wide financial statements...

TRANSCRIPT

Board Member’s Guideto Governmental Accounting and ReportingS E P T E M B E R 1 9 , 2 0 1 9

P R E S E N T E D BY:

C H R I S T I N A G R I G G S

G E M S B O K C O N S U LT I N G , I N C .

1

Overview• Government Financial Statements• Budgeting and Reporting• Monthly Board Reports

2

Governmental AccountingGovernment-wide Financial Statements◦ Statement of Net Position◦ Statement of Activities

Statement of Net Position (Balance Sheet) Reports on the District’s assets, liabilities and committed funds for future expenses and future expected income. Fiduciary activities such as employee and volunteer pension plans are not included in the government-wide statements since theseassets are not available to fund District programs.

Statement of Activities: Outlines what caused a changed in the Net Position over the past 12 months. An important purpose of the design of the statement ofactivities is to show the financial reliance of the District’s distinct activities or functions on revenues provided by the District’s taxpayers.

3

Governmental AccountingGovernment-wide Statements What to look for:◦ Overall Fiscal Health of District

◦ Increasing or decreasing Net Position◦ Aged Capital Assets◦ Reduced Tax Revenue (1 year)◦ Trends ◦ Why?

◦ Long-Term View

4

Governmental AccountingFund Statements:Reports on Resources and Expenses segregated for specific activities

◦ General Fund◦ Enterprise Fund◦ Special Revenue Fund◦ Pension Fund

◦ Short-Term View

5

Governmental AccountingFund StatementsWhat to look for:◦ Year-Over-Year ◦ Revenue Trends◦ Operating Surplus/Deficit◦ Large buckets of expenses and the trends

6

Statement of Net Position

Questions to Ask:- How much do we owe in the future (beyond 1 year)?- How much do we owe in the next year?- Does the Unrestricted value exceed the amount owed?- Do Assets exceed Liabilities?- Does Cash and Investments exceed Liabilities?

7

Statement of Activities

Identifies how much tax revenue is needed by the District as a whole to sustain current operating costs

- What to look for:- How much non-recurring revenue was received and percentage of the operating

costs did it cover?- Were there charges for services and how much of the costs did it cover?- If grants and contributions were received, would the expenses they were used

for have been purchased regardless of external funds?- If the Change in Net Position was negative, was this planned for (in the budget)?

If so, what caused it?

- Additional insights:- Which Fund or Funds impacted the Change in Net Position- Was there a decrease in funding or an increase in expenses or both

8

Statement of Net PositionSingle Fund

- Identify trends you want to “watch”- Changes to Debt- Changes to Accrued Wages- Changes to Cash and Investments- Tax Revenue Historical and future trends

9

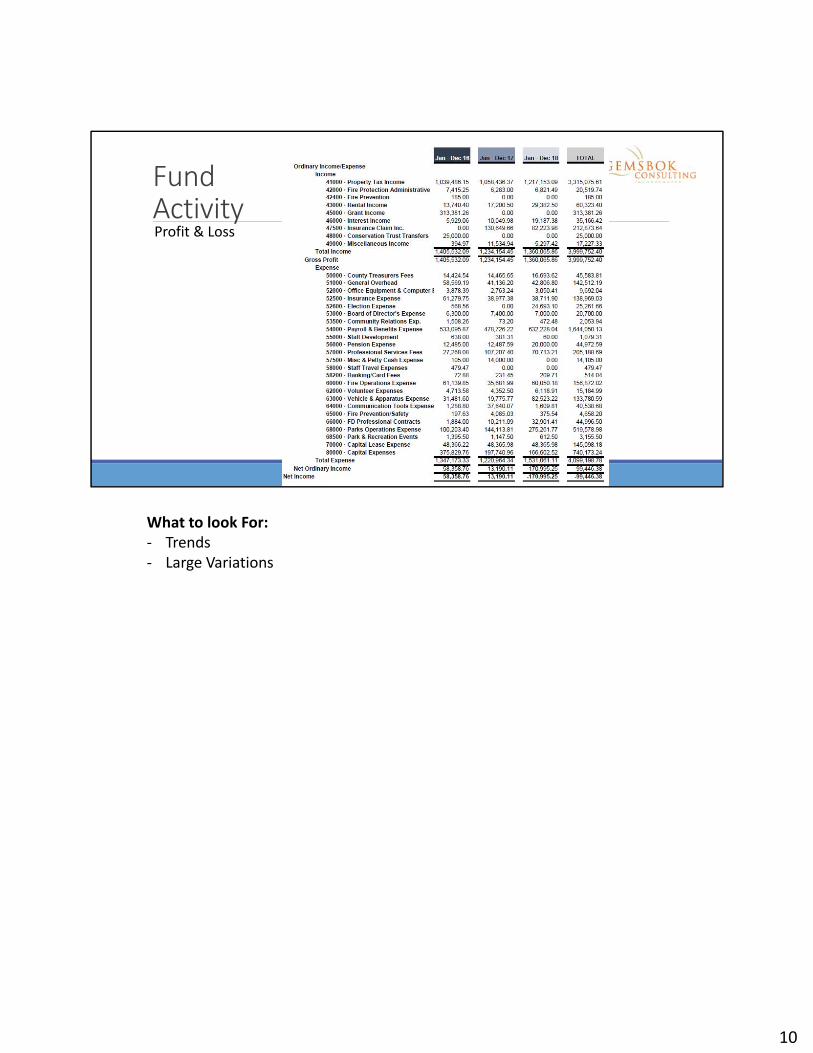

Fund ActivityProfit & Loss

What to look For:- Trends- Large Variations

10

BudgetingComponents of a BudgetData neededWorking from a Budget

11

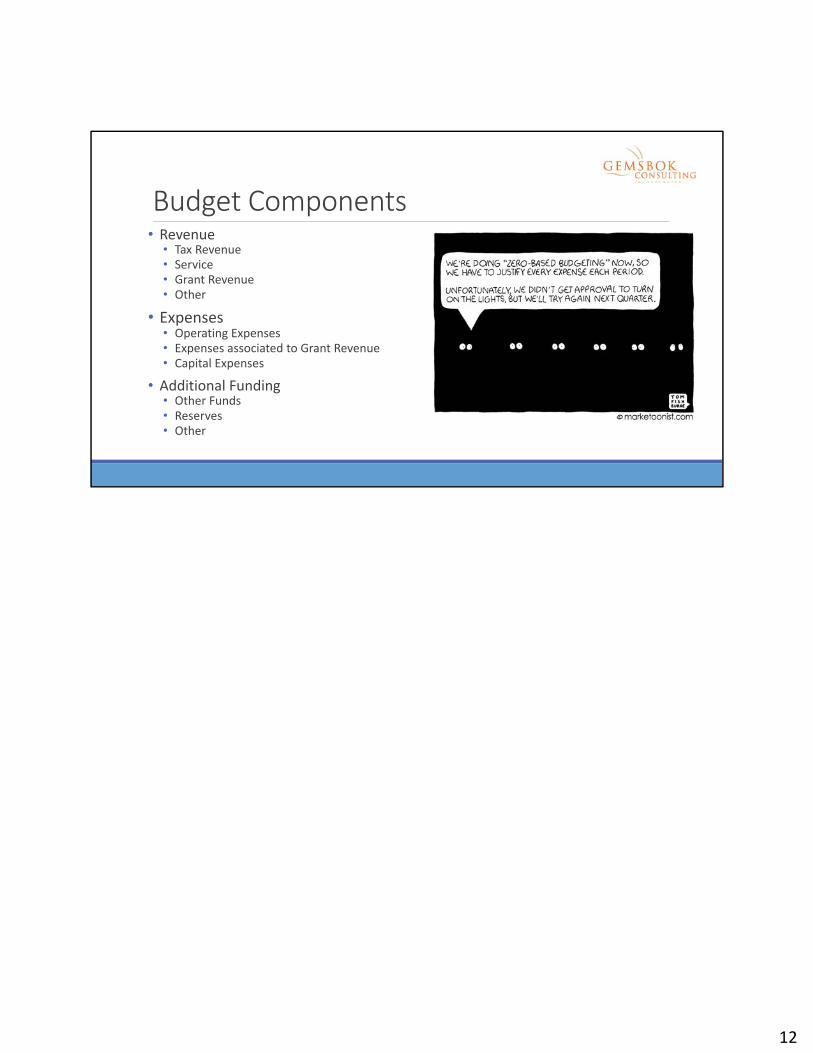

Budget Components• Revenue• Tax Revenue• Service • Grant Revenue• Other

• Expenses• Operating Expenses• Expenses associated to Grant Revenue• Capital Expenses

• Additional Funding• Other Funds• Reserves• Other

12

Budgeting: Before You StartHistorical DataForecast

13

Budgeting: Forecast

14

Budget ReportingPeriod Actual vs. BudgetYear-to-Date Actual vs. BudgetYear-to-Date vs. Annual Budget

15

Appropriations• Why?• What should they include• How does a detailed budget support

this process?

16

Board Reports• What’s the Goal• What should they include

17

Board Reports: Goal• Fiduciary Responsibility• Explain the Why• Guides Decision Making

18

Board Reports• Executive Summary• Tell the story• Provide high-level insights and key information• Key fiscal and non-fiscal data• What occurred and what’s the forecast• Identify obstacles and key decisions to be made

• Detailed Reports• Provide comparisons• Benchmarks• Budget to actual details

19

Questions

20