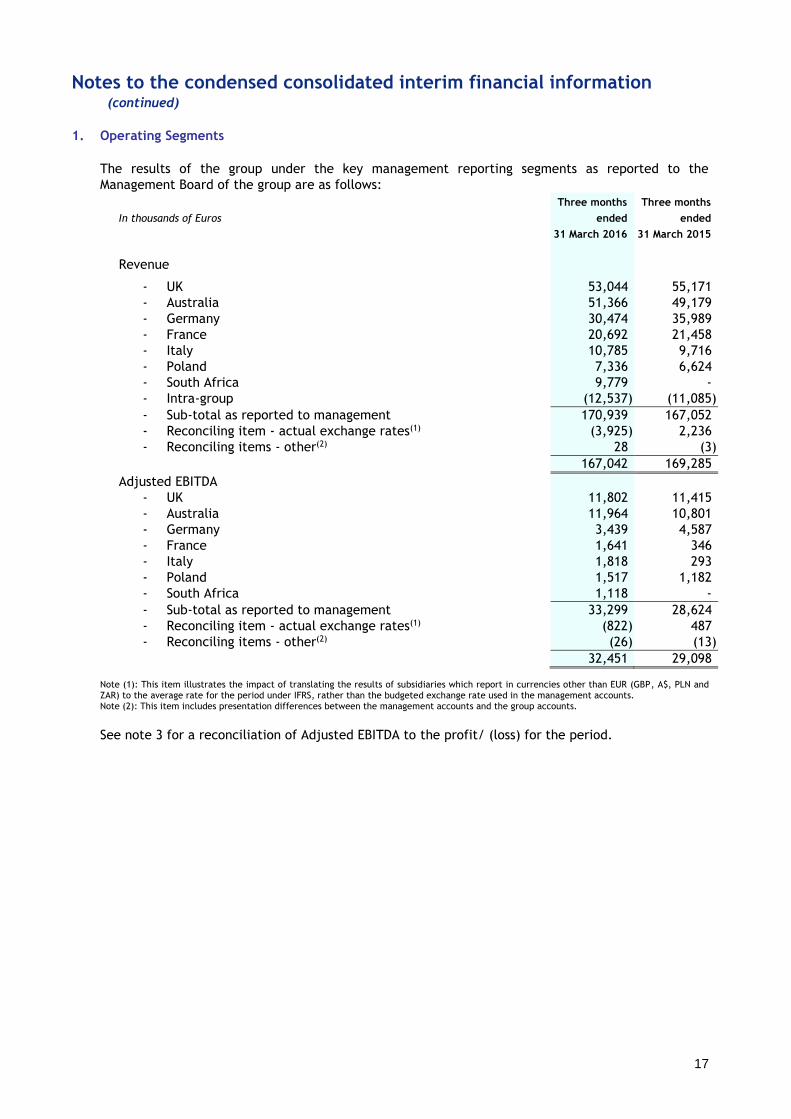

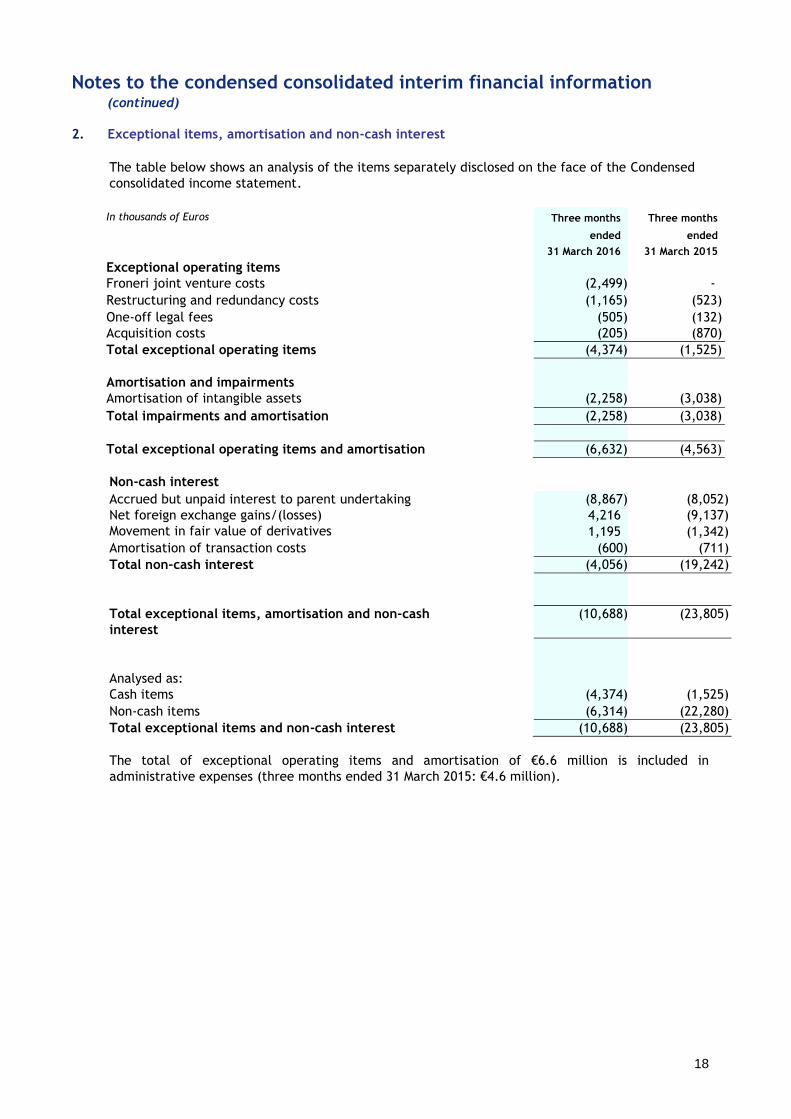

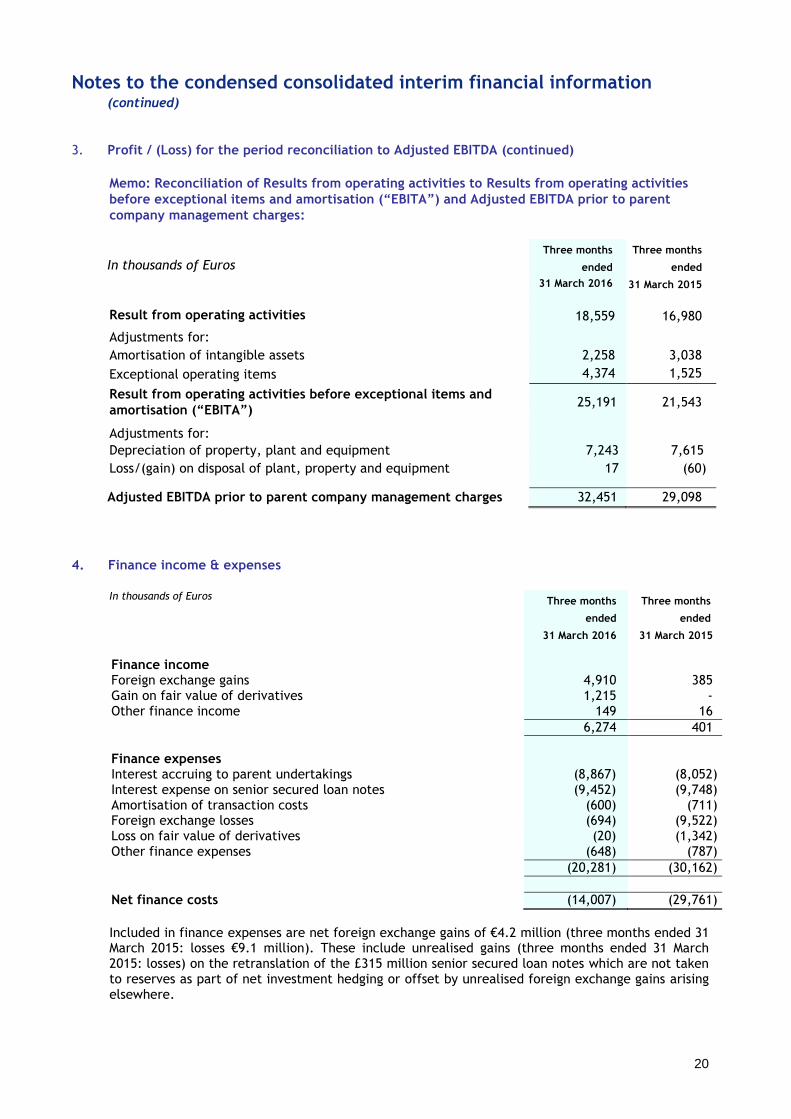

bondholder information pack quarter 1 2016 - r&r ice cream · on management’s current ... -...

TRANSCRIPT

1

Bondholder information pack Quarter 1 2016

Contents

Business highlights

Operating and financial review

R&R Ice Cream plc consolidated financial information

2

FORWARD-LOOKING STATEMENTS

This Bondholder Information Pack includes “forward-looking statements” within the meaning of the U.S. securities laws and

the laws of certain other jurisdictions, which are based on our current expectations and projections about future events. All

statements other than statements of historical facts included in this Bondholder Information Pack including, without limitation,

statements regarding our future financial position, risks and uncertainties related to our business, strategy, capital expenditure,

projected costs and our plans and objectives for future operations, may be deemed to be forward-looking statements. Words such

as “believe,” “expect,” “anticipate,” “may,” “assume,” “plan,” “intend,” “will,” “should,” “estimate,” “risk,” and similar

expressions or the negatives of these expressions are intended to identify forward-looking statements. These statements are based

on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause

actual results, performance or events to differ materially from those anticipated by such statements. Factors that could cause such

differences in actual results include:

our inability to address significant changes in consumer preferences;

increased price, or decreased availability, of commodities we use to produce our products;

adverse changes in general economic conditions and/or reductions in consumer spending;

our ability to accurately predict demand for our summer selling season;

inclement weather in the regions in which our ice cream is sold;

our inability to effectively compete in our highly competitive industry;

the size and sophistication of our customers;

the loss of any of our major customers;

our dependence on the value and perception of our brands;

our reliance on licences from third parties;

increased shipping prices or disrupted shipping services;

significant damage to any of our factories;

significant charges incurred due to the closing or divesting of all or a portion of a manufacturing plant or facility;

the shipment of contaminated products or lawsuits relating to product liability;

health concerns which may cause a decreased demand for our products;

the damaged image or reputation of our customers, which could adversely affect the sales of our products;

our failure to comply with existing or future government regulations;

costs and liabilities imposed by environmental regulations;

our inability to retain or attract key personnel;

detrimental fluctuations in currency exchange rates;

our inability to adequately protect our confidential information due to the absence of patent protection;

our inability to successfully integrate our recently acquired businesses;

our inability to maintain adequate infrastructure and resources to support any future growth;

adverse economic, social or political conditions in any of the several different countries in which we operate; and

disruptions in our information technology systems.

We disclose important factors that could cause our actual results to differ materially from our expectations under the

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” section in this Bondholder

Information Pack. Other sections of this Bondholder Information Pack describe additional factors that could adversely affect

our business, financial condition or results of operations. Moreover, we operate in a very competitive and rapidly changing

environment. New risk factors emerge from time to time and it is not possible for us to predict all such risk factors, nor can we

assess the impact of all such risk factors on our business or the extent to which any factor, or combination of factors, may

cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and

uncertainties, you should not place undue reliance on forward-looking statements as a prediction of actual results.

3

BUSINESS HIGHLIGHTS FOR THE THREE MONTHS ENDED MARCH 31, 2016

Froneri joint venture with Nestlé

- On April 27, 2016 we announced an agreement with Nestlé to set up the Froneri joint venture

- Combined sales of approximately €2.5 billion, in 20 countries and employing about 15,000 people

- Headquartered in the UK, operating primarily in Europe, the Middle East (excluding Israel), Argentina,

Australia, Brazil, the Philippines and South Africa

- Froneri will combine:

- R&R’s and Nestlé’s ice cream activities in the relevant countries

- Nestlé’s European frozen food business (excluding pizza and retail frozen food in Italy), as well as

its chilled dairy business in the Philippines

- Compelling rationale for the joint venture

- R&R’s competitive manufacturing model and significant presence in retail

- Nestlé’s strong and successful brands and experience in ‘out-of-home’ distribution

- The transaction is subject to employee consultations and the approval of regulatory authorities

- Subject to these approvals, the transaction is anticipated to close later this year

- Nestlé and PAI will have equal equity interests in the joint venture

Record Q1 2016 for R&R

- Branded share of revenue up 3% to 56%

- Geographical diversification working well with strong performance from Australia and South Africa as the

peak season ends in the southern hemisphere

- Year-on-year NPD growth: up to 10.5% of Q1 2016 revenue, versus 8.2% in Q1 2015

- Operational improvements continue to drive efficiency and margin improvement

Revenue of €167.0 million for the three months ended March 31, 2016

- Strong southern hemisphere performance: €12.1 million of growth from South Africa and Australia

- The European business is marginally down year-on-year, ahead of the key trading season

- Revenue adversely effected by unfavourable exchange rates which contributed to a €5.3 million reduction

in revenues year-on-year

Adjusted EBITDA of €32.5 million increased €3.4 million (+11.5%) for the three

months ended March 31, 2016

- South Africa contributed €1.0 million Adjusted EBITDA in the three months ended March 31, 2016

- €3.5 million of underlying growth at constant exchange rates (+ 12.2%), including €2.5 million like-for-

like growth from Australia

- €1.2 million adverse effect due to unfavourable exchange rates

LTM EBITDA of €191.1 million is up €3.4 million (+1.8%) from December 31, 2015

Net debt position at quarter end of €621.9m

- Senior leverage: 3.25x LTM EBITDA

- €63.2 million of cash and cash equivalent balances

Notes: 1 Data presented here at actual average exchange rates. 2 Adjusted EBITDA is presented here before parent company or investor management charges. 3 LTM EBITDA represents Adjusted EBITDA of the group for the last twelve months to March 31, 2016 including the post-acquisition results

of R&R South Africa. There is no pro forma adjustment to the performance of R&R South Africa. 4 Net debt figure excludes parent company loan and any debt issued by parent companies.

4

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion in conjunction with the audited financial statements and related notes

thereto and other financial information included with this document. The statements in this discussion regarding

industry outlook, our expectations regarding our future performance, liquidity and capital resources and other non-

historical statements in this discussion are forward-looking statements. These forward-looking statements are

subject to numerous risks and uncertainties, including, but not limited to, the risks and uncertainties described in

the “Forward-Looking Statements” section of this document. Our actual results may differ materially from those

contained in or implied by any forward-looking statements.

Overview

R&R Ice Cream plc (“R&R”) is the third largest global manufacturer of ice cream products and the largest private

label manufacturer in the world. R&R is the second largest take-home ice cream manufacturer in Europe, with leading

market shares in each of the United Kingdom, German, French and Italian ice cream markets. We also have a leading

market share in Australia and South Africa following the acquisition of Peters Food Group Limited (‘Peters’) in June

2014 and the acquisition of Nestlé South Africa’s ice cream business (‘R&R South Africa’) in May 2015.

R&R offers a broad product range of branded and private label ice cream products. We primarily produce take-

home ice cream products, including ice cream tubs and multi-packs of ice cream cones, ice lollies, ice cream sticks

and ice cream desserts, and impulse products, which individuals buy on impulse for immediate consumption. Our

scale, focus on large, stable take-home markets and highly efficient manufacturing operations provide us with key

advantages over our competitors and have allowed us to continue to generate stable earnings and significant free cash

flow through various economic cycles. We believe our broad product range allows us to maintain strong sales volumes

as consumer demand shifts between branded and private label products.

For R&R’s most recent year end, the year ended December 31, 2015, we generated Adjusted EBITDA of

€187.7 million, revenue of €991.6 million and free cash flow before acquisitions and exceptional operating items

of €113.4 million.

R&R operates eleven plants located in seven countries, on three continents. Eight of these plants are in the four

largest ice cream markets in Europe (the UK, Germany, France and Italy), which allows us to supply our customers

quickly and efficiently in these key markets. Our manufacturing platform benefits from many years of significant

capital investment and footprint rationalisation. Our plants have also benefited from sharing and implementation of

best practices and procedures across our group in order to leverage technological expertise. We believe that our scale

and manufacturing footprint provides us with a competitive advantage over most of our competitors, which are

generally smaller and only offer regional distribution.

With the acquisition of the South African business, we now have a production footprint to serve ice cream markets

in sub-Saharan Africa. Following an acquisition, we make capital investments and implement our best practices in

order to bring such facilities in line with our group-wide standards.

We benefit from a variety of licensed and owned brands, and we have exclusive ice cream product licences with

the world’s largest food company (Nestlé), the world’s largest confectionary company (Mondelēz, formerly Kraft

Foods), and the world’s largest entertainment company (Disney). Strong private label relationships with our customers

provide us with strong opportunities to cross sell our branded products.

In the UK, we produce under licence a number of products under Nestlé’s prominent confectionary brand names,

including Smarties, KitKat, Rolo, Milky Bar and Lion Bar. We have an exclusive licence agreement with Mondelēz

to produce and sell in the UK ice cream products under the Cadbury brands that include Dairy Milk, Crunchie, Cadbury

Caramel and Marvellous Creations (which is a range of super-premium products).

Across Europe, our exclusive licence agreement with Mondelēz enables us to produce and sell ice cream products

under established brand names including Milka, Oreo, Toblerone, Philadelphia and Daim. We also have non-exclusive

access to various Disney licences such as Mickey Mouse, Minnie Mouse and Cars.

In Australia, we have, amongst others, the iconic Drumstick, Connoisseur, and Peters Original brands. In South

Africa, we have incorporated a number of similarly iconic brands (predominantly on an owned basis, rather than

licenced) in South Africa and across sub-Saharan Africa, such as Dairy Maid, Country Fresh, Tin Roof, King Cone,

Jive, and KitKat.

5

Comparing results for the three months ended March 31, 2016 and the three months ended March 31, 2015

We acquired Nestlé South Africa’s ice cream business (“R&R South Africa”) in May 2015. The results of R&R

South Africa have been consolidated into the results of R&R Group for the three months ended 31 March 2016, but

not included in the results for the three months ended March 31, 2015. Direct comparability of the results of the two

periods is therefore impacted by this difference. The R&R South Africa’s balance sheet has been fully consolidated

into the consolidated statement of financial position at March 31, 2016.

Comparing the three months ended March 31, 2016 to the three months ended March 31, 2015 is also affected

by the average exchange rates used to translate the UK and Australia business performance. In 2016, the three month

average rate was 1.2986 EUR: 1 GBP and 0.6544 EURO: 1 AUD, whilst in 2015 the rates were 1.3457 EUR: 1 GBP

and 0.6987 EURO: 1 AUD. The Adjusted EBITDA for the three months ended March 31, 2016 was adversely

impacted by €1.2 million as a result of exchange rate difference when compared to the three months ended March

31, 2015.

Overview for the year-to-date

Adjusted EBITDA was €32.5 million at March 31, 2016 compared to €29.1 million at March 31, 2015, an increase

of €3.4 million. This is a record performance for the first quarter and includes €1.0 million of Adjusted EBITDA

contributed by R&R South Africa and €2.5 million of Adjusted EBITDA growth by R&R Australia, year-on-year (at

constant exchange rates). Our European businesses contributed €1.1 million of Adjusted EBITDA growth (at constant

exchange rates).

Adjusted EBITDA margin increased 2.2 percentage points from 17.2% in the three months ended 31 March

2015 to 19.4% in the three months ended March 31, 2016. This increase is due to improvements in gross margin

and overhead savings.

The Q1 YTD headlines are as follows:

Figures are €000 Three months ended

March 31, 2016

Three months ended

March 31, 2015 Year-on-year % Year-on-year

Consolidated revenue 167,042 169,285 (2,243) (1.3%)

Adjusted EBITDA 32,451 29,098 3,353 11.5%

Adjusted EBITDA% 19.4% 17.2% 2.2% -

Free cash flow(1) (40,780) (14,398) (26,382) (283%)

Note (1): defined as net cash flows from operating activities and investing activities, before acquisitions of subsidiaries and exceptional operating items

Source: consolidated interim financial information

Consolidated revenues have reduced €2.2 million or 1.3% year-on-year. On a like-for-like basis, and at constant

exchange rates, revenue has fallen by €5.9 million. The impact of average exchange rates, year-on-year has

impacted revenue by a further €5.3 million. The Australian business has grown by €2.2 million, year-on-year, and

at constant exchange rates.

The decline in the revenue of the European business, year-on-year, is largely the effect of exiting less profitable

contracts in our German business, which has declined €5.5 million. During 2015, we exited a number of less

profitable contracts in our German business, which generally run from April to March each year. The effect of

exiting these contracts impacts on the first quarter results for 2016, and the comparison year-on-year.

The UK showed a decline of €2.2 million, on revenue of €53.1 million, as slow market conditions and timing

of promotions affected the start of the season.

Our gross margin (before exceptional items) increased 4.7 percentage points from 34.2% in the three months

ended March 31, 2015 to 38.9% in the three months ended March 31, 2016. The gross margin contributed by R&R

South Africa for the three months ended March 31, 2016 positively impacted the gross margin of the group by 0.8

percentage points; though the majority of the increases were due to the exiting of less profitable contracts in our

German business, the growth in new product development (which has a positive effect on our gross margin), the

growth of our branded share in the sales mix, and the positive effects of capital expenditure projects on our

operational efficiency.

Free cash flow has been impacted by the acquisition of R&R South Africa, which has driven an increase in

debtors versus the comparative period in 2015 (effect: €6.5 million in the three months ended March 2016; €nil in

6

the three months ended March 2015), and also by a build-up of inventory earlier in the European season than in

2015, which has impacted our inventory position by €8.8 million, year-on-year. The rationale for the inventory

build-up is to improve service levels through the European peak season and to accommodate new business in Italy,

in particular. Capital expenditure is also €4.7 million higher in the first quarter of 2016, compared to the first quarter

of 2015, which is a result of continued investment in our manufacturing capability and IT systems, in particular.

Factors Affecting our Business

Various factors affect our operating results during each period, including:

Seasonality. Our business is seasonal, and a large percentage of our sales are generated between the months of

April and September of each year. As a result of our seasonality, our sales fluctuate from quarter to quarter, which

often affects the comparability of our results between quarterly periods. Sales in certain of our markets are more

seasonal than others, based on factors such as weather patterns and consumer preference. Our Australian and South

African businesses reduce the seasonality of the business, as the summer selling season in both Australia and South

Africa occurs during a period of historically lower sales in our European markets, and moreover the seasons in both

geographical markets are more consistent than in the rest of the Group. In 2014, the second and third quarters

represented approximately 66% of our revenue. In 2015, the second and third quarters have accounted for 63% of

our revenues on a last twelve months’ revenue basis.

We generally produce most of our products prior to and during our summer selling season, as it is impossible for

us to produce upon receipt of orders for all customers during the primary selling season. Our inventory levels peak at

the end of May, as we generally build our inventory with what we expect to sell in the following three to five weeks,

based on forecast sales, working closely with our customers. We generally produce in advance a higher percentage of

our branded inventory than our private label products as these are not as dependent on the satisfactory conclusion of

the annual contracts prevalent in mainland Europe. If demand levels fluctuate, we can generally increase or decrease

production to bring our stock to our desired levels within approximately three weeks. During our peak production

periods, we purchase large amounts of raw materials, hire additional workers at our facilities as temporary workers

and incur many other costs of our operations that we consider to be variable.

We finance our working capital needs through cash and cash equivalents, revolving credit borrowings and

factoring facilities. Our working capital requirements are typically higher in the first half of each year due to our

build-up of inventory for the summer selling period in Europe. As a result, our revolving credit and factoring

borrowings typically increase from January to May. In June, as we begin to generate cash from early summer season

sales of our ice cream products, we begin to repay our borrowings. In 2012, we put factoring facilities in place in

the UK and France, in 2013 in Germany and in 2014 in Australia, to supplement our Revolving Credit Facility and

cash on hand. This financing better matches the seasonality of our working capital cycle. Aside from renewing

facilities before they became due for repayment or renewal, we have not entered into any new significant credit

facilities since that time. We are currently in the process of implementing local credit facilities for R&R South

Africa, though this is outside of the restricted group.

Changes in Prices of Raw Materials. Raw materials used as ingredients and for packaging account for a

significant portion of our cost of sales. The principal raw materials we use to manufacture our products are cream,

milk, whey protein, sugar, glucose, cocoa, butter, coconut oil and palm oil. Many of the raw materials we use in

our manufacturing processes are commodities and are subject to significant price volatility. Changes in the price of

oil has also had a significant impact on our results each year as it has an impact on the cost of packaging, freight

and the cost of other components that we use in our manufacturing process, such as plastic.

We continue to take actions to reduce overall materials expense and exposure to price fluctuations. At present,

we see raw material cost pressures in the sugar market, for example, and the futures market indicates a persistence

of this trend. However, we continue to take measures to reduce our exposures to these and other cost pressures,

where possible. Since 2007, we have increased the amount of raw materials that we purchase pursuant to fixed price

contracts which set prices for our raw material sales for that year. We enter into these arrangements when we believe

that we can secure favourable prices for our raw materials for specified future periods. We fix a substantial

proportion of the annual cost of our raw materials used for ingredients and packaging through fixed-price contracts,

with the proportion fixed as at December 31, 2015, representing approximately 64% of our expected raw materials

expenditure for 2016.

Dairy products represented 12% of our cost of sales in 2015. Fixed-price contracts do not generally exist for

dairy products. We have previously reduced the amount of dairy fat and increased the amount of vegetable fat in

our ice cream products in order to reduce the effects of volatility in dairy prices on our business. However,

increasing demand for premium ice cream products across all markets is now leading to an increased requirement

for dairy fats.

7

Weather Trends. Sales of ice cream are generally positively impacted by warm, sunny, dry weather and are

negatively impacted by cool, overcast or rainy weather. Hours of sunshine, temperature and rainfall are the three

most important weather factors during the summer selling season. Our 2015 results in the UK, in particular, were

adversely affected because of unseasonal weather, though our Italian business benefitted from a prolonged period

of warm and dry weather over the 2015 summer. However, our recent acquisitions in the southern hemisphere

spread our risk related to weather trends.

The majority of our business is in take-home ice cream markets, rather than impulse markets. The only

significant parts of our business involving impulse are the “route” business in Australia (which was acquired in June

2014), and smaller elements of the business in the UK, Poland and South Africa. Trends in take-home ice cream,

such as the introduction of premium products and indulgent flavours (which frequently contain enhancements such

as pieces of confectionery or biscuits), and the resulting increase in home consumption have made ice cream sales

less dependent on warm, sunny, dry weather, as consumers increasingly purchase ice cream as part of their weekly

grocery shopping as opposed to an item purchased on impulse. This is particularly important in countries where the

summer months do not always guarantee warm, sunny or dry weather, such as the UK. Our acquisitions of Eskigel

in Italy, Peters in Australia and Nestlé’s South African ice cream business mean that we are now less dependent on

weather patterns in Northern Europe.

We are able to take steps to control our costs during the summer season if we expect weather trends to be

adverse. For example, a portion of our factory workforce across our enterprise is employed on a seasonal basis. We

are able to shorten the work period for our seasonal workers if our product requirements do not meet our projections.

Competition and Market Trends. The ice cream industry is highly competitive, and our products compete based

on a variety of factors, including design, quality, price, customer service and rate of innovation. Levels of

competition and the ability of our competitors to more accurately address consumer tastes, predict trends and

otherwise attract customers through competitive pricing or other factors impact our results of operations. Our

competitors’ ability to identify and encourage changes in consumer trends may impact our decision regarding what

types of ice cream to develop and sell.

Certain actions by our competitors may impact our operating results, such as changes in their pricing or

marketing or levels of promotional sales, which may cause us to take certain actions that impact our profitability,

such as reductions in our prices or increases in our marketing expenditures. Some of our competitors from time to

time reduce their prices significantly in order to enhance their brand recognition. In addition, during more difficult

economic conditions the level and frequency of promotional activity required to stimulate sales is typically greater

than in less difficult economic conditions. The levels at which we are able to price our products are influenced by a

variety of factors, including the quality of the product, cost of production for those products, prices at which our

competitors are selling similar items, price points of products and willingness of our customers to pay for higher

priced items. These factors may limit our ability to respond to such price changes. We have also sought to enhance

our competitive position by increasing our scale, diversifying our products and enhancing and acquiring brands and

brand licences. We have also sought to address the growing trend towards premiumisation of ice cream products, in

both the branded and private label markets, through new product development.

Foreign Currency Exchange Rates. As a result of our operations in various countries, we generate a significant

portion of our sales and incur a significant portion of our expenses in currencies other than the Euro, including the

British Pound, Australian Dollar, the Polish Zloty and the South African Rand. During 2015, 54% of our reported

revenue was derived from subsidiaries whose functional currency is not the Euro, largely the British Pound and

Australian Dollar. Typically, our costs and the corresponding sales are denominated in the same currency. Sometimes,

however, we are unable to match sales received in foreign currencies with costs paid in the same currency, and our

results of operations are consequently impacted by currency exchange rate fluctuations. Therefore, as and when we

determine it is appropriate and advisable to do so, we seek to mitigate the effect of exchange rate fluctuations through

the use of derivative financial instruments. These are typically less than 12 months in duration, and “vanilla” contracts

such as forward foreign exchange transactions and short-term swaps.

We present our consolidated financial statements in Euro. As a result, we must translate the assets, liabilities,

revenue and expenses of all of our operations with a functional currency other than the Euro into Euro at then-

applicable exchange rates. Consequently, increases or decreases in the value of the Euro may affect the value of these

items with respect to our non-Euro businesses in our consolidated financial statements, even if their value has not

changed in their original currency. For example, a stronger Euro will negatively affect the reported results of operations

of the non- Euro businesses and conversely a weaker Euro will improve the reported results of operations of the non-

Euro businesses. These translations could significantly affect the comparability of our results between financial

periods and/or result in significant changes to the carrying value of our assets, liabilities and shareholders’ equity.

We record the effects of these translations in our consolidated statement of comprehensive income and expense as

exchange differences on retranslation of foreign operations. During the three months ended March 31, 2016 the

8

Euro to British Pound exchange rate averaged 1.2986 to 1 (three months ended March 31, 2015: average of 1.3457

to 1); and during the three months ended March 31, 2016 the Euro averaged 0.6544 to 1 Australian Dollar (three

months ended March 31, 2015: average of 0.6987 to 1). During the three months ended March 31, 2016 the Euro

to South African Rand exchange rate averaged 0.0573 to 1.

A summary of the EUR: GBP exchange rates during the three months ended March 31, 2016 and 2015 is shown

below: Three months ended March 31, 2016 Three months ended March 31, 2015

Average for the period 1.2986 1.3457

Opening balance sheet rate 1.3570 1.2841

Closing balance sheet rate 1.2652 1.3821

A summary of the EUR: Australian Dollar exchange rates during the three months ended March 31, 2016 and

2015 is shown below: Three months ended March 31, 2016 Three months ended March 31, 2015

Average for the period 0.6544 0.6987

Opening balance sheet rate 0.6693 0.6756

Closing balance sheet rate 0.6752 0.7098

A summary of the EUR: South African Rand exchange rates during the three months ended March 31, 2016

and 2015 is shown below:

Three months ended March 31, 2016 Three months ended March 31, 2015

Average for the period 0.0573 Not applicable

Opening balance sheet rate 0.0591 Not applicable

Closing balance sheet rate 0.0593 Not applicable

Acquisitions of Complementary Businesses. We continue to evaluate acquisition opportunities that may

improve our market share and product offerings, reduce costs, or allow us to enter new geographic markets. We

have completed 11 acquisitions since 2007. Following any acquisition, our results of operations will be impacted

by the results of the newly acquired business, debt incurred to acquire the business and expenditures made to

integrate the newly acquired business into our company. In general, when looking to integrate and improve a newly

acquired business, we look to several main areas: (i) reviewing current prices and product engineering or changing

recipes to achieve acceptable margins on products sold; (ii) researching ways to enhance our purchasing to benefit

from economies of scale; (iii) reducing duplicated overhead; (iv) moving production to the most efficient locations,

subject to geography and logistics; (v) sharing knowledge and experience; (vi) creating synergies with and benefits

to the existing businesses; and (vii) improving management of working capital. Many of these integration measures

require expenditure. When acquiring a business, we believe that the best results are achieved by reviewing the

existing business over the first year and identifying the strengths and weaknesses of that business. During this period

we look to implement the R&R management reporting and key performance indicators to provide reliable,

standardised information. Additionally, we seek to achieve certain improvements, for example, from the purchase

of ingredients at better prices. After a period of observation and understanding, we determine the extent of capital

expenditure required to improve the business, potential further synergies that we believe can be extracted, how we

can sell more, staffing resources we believe may enhance the business and any identifiable savings we believe can

be achieved.

In May 2015, we completed the acquisition of Nestlé South Africa’s ice cream business. The consideration

paid was €8.6 million, which included separate sums for the trade and assets of the business, and certain intellectual

property (such as brand trademarks, patents and domain names). The trading business (known as R&R Ice Cream

South Africa Pty Limited) is outside of the restricted group for security purposes, though its direct holding company

(R&R Ice Cream South Africa Holdings Limited, registered in the UK, and owner of certain of the intellectual

property related to R&R Ice Cream South Africa’s trading business) is part of the restricted group. In the three

months ended 31 March 2016, the business achieved €9.0 million of sales and Adjusted EBITDA of €1.0 million.

In addition, certain acquisitions have resulted in, and future acquisitions may result in, efficiencies of scale and

therefore provide cost savings across the company. When integrating a newly acquired business, we review the key

9

production facilities and processes gained with that business to determine if they are duplicative of our current

facilities and production capabilities. Through this review and the resulting combination of duplicative processes,

we are often able to streamline our operations, reduce costs and recognise synergies across our operations.

On 5 October 2015, we announced that R&R was in advanced discussions with Nestlé to set up a new joint

venture covering ice cream based mainly in Europe and Africa. On April 27, 2016 we made a further announcement

setting out our agreement with Nestlé to set up Froneri, a joint venture with sales of approximately €2.5 billion in

over 20 countries, employing about 15,000 people. Froneri will be headquartered in the UK and will operate

primarily in Europe, the Middle East (excluding Israel), Argentina, Australia, Brazil, the Philippines and South

Africa. The new company will combine Nestlé and R&R’s ice cream activities in the relevant countries and will

include Nestlé’s European frozen food business (excluding pizza and retail frozen food in Italy), as well as its

chilled dairy business in the Philippines. The transaction is subject to employee consultations and the approval of

regulatory authorities. Financial details were not disclosed. There has been no effect of this joint venture on the

accompanying condensed consolidated interim financial information.

Retailer Customer and Consumer Preferences. Our revenues are also impacted by our ability to continue to

produce ice cream that is desired by our retailer customers. Retailer customers purchase our private label ice cream

primarily based on price, quality and ability to deliver products which meet margin targets, ability to deliver our

products on a timely basis and ability to manufacture various types of ice cream in large volumes. Our ability to

meet these demands impacts our ability to sell to new and existing private label customers. In addition, our ability

to effectively sell our branded products to our customers is driven by consumer demand for our products, as a result

of, among other things, our marketing campaigns and the taste and quality of our products.

Impact of Acquisitions

Impact of the acquisition of Nestlé South Africa’s ice cream business. In May 2015, we completed the

acquisition of Nestlé South Africa’s ice cream business. The consideration paid was €8.6 million, which included

separate sums for the trade and assets of the business, and certain intellectual property (such as brand trademarks,

patents and domain names). The trading business (known as R&R Ice Cream South Africa Pty Limited) is outside

of the restricted group for security purposes, though its direct holding company (R&R Ice Cream South Africa

Holdings Limited, registered in the UK, and owner of certain of the intellectual property related to R&R Ice Cream

South Africa’s trading business) is part of the restricted group. In the three months ended 31 March 2016, the

business achieved €9.0 million of sales and Adjusted EBITDA of €1.0 million, illustrating the continued strong

performance in the latter part of the South African peak season.

Acquisition Accounting

We have accounted for the acquisition of R&R South Africa using the acquisition method of accounting. As a

result, the purchase price for R&R South Africa has been allocated to the tangible and intangible assets acquired and

liabilities assumed based upon their respective fair values as of the date of the acquisition.

The allocation of the purchase price of the assets acquired has been determined, where appropriate, by external

experts. Under applicable accounting guidance, we are permitted to continue to make fair value adjustments until 12

months after the acquisition date. We have evaluated the remaining depreciable lives of the manufacturing assets to

reflect the estimated useful lives for purposes of calculating periodic depreciation, and we will continue to amortise

the intangible assets over their estimated useful lives, unless the intangible assets are determined to have indefinite

lives.

Components of Revenue and Expenses

Note that the information provided in this section for the three months ended March 31 2016 includes three months

post-acquisition for R&R South Africa, but that the information for the three months ended March 31, 2015 does not

include R&R South Africa as it was before the business was acquired.

Revenue

We generate revenue from the sale of ice cream and related products. We generate sales under contracts with

retailers, and by individual orders through sales personnel and independent brokers. In the UK, we generally enter

into purchase orders or other contracts for sale that have a rolling thirteen-week term. In Germany and France we

generally enter into longer-term contracts, typically for twelve months. In many cases, subject to certain exceptions,

the contracts have fixed prices for products but do not specify volumes. Rather, the contract terms govern individual

purchase orders to be delivered to us as required by the retailer. In our contracts for sale of goods in Germany, certain

of our prices for our goods vary based on our costs of raw materials, allowing us to pass some of our increased costs

10

through to consumers. In Poland, we typically enter into contracts with distributors and retailers early in the calendar

year, fixing pricing and retrospective rebate levels for the coming summer season. In Italy, relationships with

customers are regulated by framework contracts setting quality standards and payment terms, while other metrics

(such as prices, discounts, promotional campaigns and new products) are negotiated annually. In Australia, there

are generally long standing arrangements with grocery customers. These arrangements are reviewed annually,

including the range of products and fixed pricing. Volumes are not specified, however agreed promotional and

marketing activity is undertaken to drive growth with additional incentives provided to the retailer based on achieving

stepped volume growth thresholds. In South Africa, there are generally long standing arrangements with grocery

customers and with distributors. In similar arrangements to Australia, these arrangements are reviewed annually,

including the range of products and fixed pricing, though volumes are not specified.

Revenues include sales of products less allowances, trade discounts and volume rebates. Revenue from sales

of products is recognised when the significant risks of ownership have been transferred to the buyer (which is

typically when the goods are dispatched). Our relationships with our retailer customers do not include a right of

return for unsold merchandise.

In the three months ended March 31, 2016, our ten largest customers by revenue, represented 43.4% (three

months ended March 31, 2015: 46.9%) of our revenue. Transactions with our largest customer accounted for 5.8%

of our total revenue in the three months ended March 31, 2016 (three months ended March 31, 2015: 6.5%).

Expenses

Cost of Sales. Cost of sales includes directly attributable costs such as material, labour, energy, product-specific

research and development, maintenance and consumables. Our costs of sales are primarily variable in nature based

on the amount of products we are selling at a given time.

Our raw material costs are the primary driver of our cost of sales, accounting for approximately 66% of our

cost of sales (excluding R&R South Africa) for the three months ended March 31, 2016, compared to 65% of our

cost of sales for the three months ended March 31, 2015. Personnel expenses, which are salaries and wages, paid to

our officers and employees, also significantly impact our cost of sales, accounting for approximately 13.5% of our

cost of sales (excluding R&R South Africa) for the three months ended March 31, 2016 (three months ended March

31, 2015: 13.8%). Our raw material costs and personnel expenses are expected to continue to be key components

of our operating expenses in the future.

Distribution Expenses. Distribution expenses represent the costs associated with the storage and shipping of

our products. These costs include freight, storage and other related distribution costs.

Administrative Expenses. Administrative expenses represent overheads including sales and marketing but also

those costs associated with support functions, such as finance, human resources, IT, professional fees (legal and

accounting) and senior management, and also include costs relating to impairment and amortisation of intangibles.

Typically, costs of these support functions are salaries and benefits, systems costs, insurance costs and costs of

professional services. Administrative costs are relatively fixed in nature and were 16.8% of our revenue for the

three months ended March 31, 2016 compared to 14.1% of revenue for the three months ended March 31, 2015.

The change in the ratio of administrative expenses to revenue is largely a result of the cost structure of R&R South

Africa business, which is similar to our Australian businesses, being branded and carries higher overheads in

servicing larger land masses. In addition, in the three months ended March 31, 2016 there are €6.6 million of

exceptional operating expenses and amortisation included in administrative expenses compared to €4.6 million in

the three months ended March 31, 2015.

Finance Expenses. Finance expense consists primarily of cash interest expense on financial debt, interest rate

derivative instruments, capital lease and other financing obligations, non-cash interest on loans from our

shareholders and unrealised foreign exchange gains or losses on financial liabilities denominated in currencies other

than Euros (except to the extent covered by net investment hedging).

Income Tax Expenses. Our income tax expense includes UK and non-UK income taxes and is based on pre-tax

income or loss. The effective rate may be higher or lower than the income tax rate in our countries of operation largely

because of the non-deductibility of certain of our interest expense, unrealized foreign exchange losses and the (non-

cash) effect of movements in deferred tax balances.

Adjusted EBITDA. Adjusted EBITDA is defined as profit/(loss) for the period before income tax

(credit)/charge, net finance expenses, depreciation and amortisation, plus certain additional supplemental

adjustments as described in note 3 to our financial statements. Adjusted EBITDA for 2015 and 2016 is stated prior

to any parent company or investor management charges. For further details of the calculation of Adjusted EBITDA,

see note 3 to our financial statements.

11

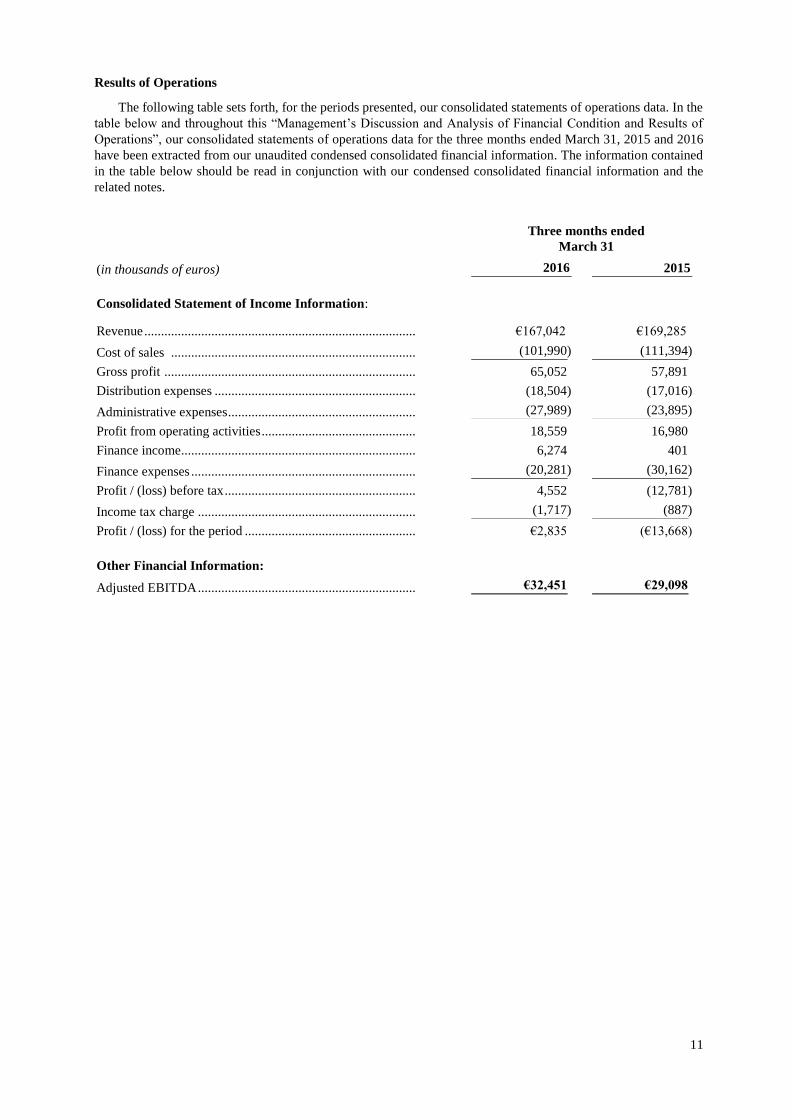

Results of Operations

The following table sets forth, for the periods presented, our consolidated statements of operations data. In the

table below and throughout this “Management’s Discussion and Analysis of Financial Condition and Results of

Operations”, our consolidated statements of operations data for the three months ended March 31, 2015 and 2016

have been extracted from our unaudited condensed consolidated financial information. The information contained

in the table below should be read in conjunction with our condensed consolidated financial information and the

related notes.

Three months ended

March 31

(in thousands of euros) 2016 2015

Consolidated Statement of Income Information:

Revenue ................................................................................. €167,042 €169,285

Cost of sales ......................................................................... (101,990) (111,394)

Gross profit ........................................................................... 65,052 57,891

Distribution expenses ............................................................ (18,504) (17,016)

Administrative expenses ........................................................ (27,989) (23,895)

Profit from operating activities .............................................. 18,559 16,980

Finance income...................................................................... 6,274 401

Finance expenses ................................................................... (20,281) (30,162)

Profit / (loss) before tax ......................................................... 4,552 (12,781)

Income tax charge ................................................................. (1,717) (887)

Profit / (loss) for the period ................................................... €2,835 (€13,668)

Other Financial Information:

Adjusted EBITDA ................................................................. €32,451 €29,098

12

The table below also sets forth consolidated statement of income data expressed as a percentage of

revenues for the periods indicated:

Three months ended

March 31

(in percentages of revenue) 2016 2015

Consolidated Statement of Income Information:

Revenue ................................................................................. 100.0% 100.0%

Cost of sales .......................................................................... (61.1) (65.8)

Gross profit ............................................................................ 38.9 34.2

Distribution expenses ............................................................ (11.1) (10.1)

Administrative expenses ........................................................ (16.8) (14.1)

Profit from operating activities .............................................. 11.1 10.0

Finance income ...................................................................... 3.8 0.2

Finance expenses ................................................................... (12.1) (17.8)

Profit / (loss) before tax ......................................................... 2.7 (7.5)

Income tax charge .................................................................. (1.0) (0.5)

Profit / (loss) for the period ................................................... 1.7% (8.1%)

Other Financial Information:

Adjusted EBITDA ................................................................. 19.4% 17.2%

Discussion and Analysis of our Results of Operations

The tables and discussions set forth below provide a separate analysis of each of the line items that comprise our

statement of income for each of the periods described below. In each case, the tables present (i) the amounts reported

by us for the comparative periods, (ii) the Euro change and the percentage change from period to period and (iii) the

percentage change from period to period after removing the effects of changes in foreign exchange rates (“FX”).

Changes in foreign currency rates have had a significant translation impact on our reported operating results in the

periods presented below, since a significant portion of our operations have functional currencies other than the euro.

As a result, we have included the percentage change net of exchange rates in order to present operational and other

changes and factors in addition to FX that affected our business during the applicable periods. We have removed the

effects of FX changes in each discussion by identifying the exchange rate used to translate the earlier period’s non-

Euro denominated results and re-translating the later period’s non-Euro denominated results using that same rate.

For the 2016 versus 2015 comparison, the British Pound figures for the three months ended March 31, 2016 have

been retranslated at €1.3457: 1 GBP (that is, the average exchange rate that applied in the three months ended March

31, 2015). Similarly, for the 2016 versus 2015 comparison, the Australian Dollar figures for the three months ended

March 31, 2016 have been retranslated at €0.6987: 1 AUD (that is, the average exchange rate that applied in the three

months ended March 31, 2015).

We have not adjusted the numbers for the impact of the Polish Zloty as this is not considered to be significant.

For the three months ended March 31, 2016, the South African Rand balances have been retranslated at ZAR 0.0573:

€1.00.

13

Three months ended March 31, 2016 compared to the three months ended March 31, 2015

The table below presents consolidated statement of income data, including the amount and percentage changes

for the periods indicated:

Three months ended

March 31

Amount of

Change

Percent

Change

Percent

Change

Excluding

GBP/AUS

FX (in thousands of euros) 2016 2015

Consolidated Statement of

Income Information:

Revenue ....................................................... €167,042 €169,285 (€2,243) (1.3)% 1.8%

Cost of sales ................................................. (101,990) (111,394) 9,404 (8.4)% (5.7)%

Gross profit ................................................... 65,052 57,891 7,161 12.4% 16.2%

Distribution expenses .................................. (18,504) (17,016) (1,488) 8.7% 11.3%

Administrative expenses .............................. (27,989) (23,895) (4,094) 17.1% 20.5%

Profit from operating activities ..................... 18,559 16,980 1,579 9.3% 14.9%

Finance income ............................................ 6,274 401 5,873 1,464.6% 1,478.9%

Finance expenses .......................................... (20,281) (30,162) 9,881 (32.8)% (31.6)%

Profit / (Loss) before tax .............................. 4,552 (12,781) 17,333 (135.6)% 2.0%

Income tax charge ........................................ (1,717) (887) (830) 93.6% 105.7%

Profit / (Loss) for the period ......................... €2,835 (€13,668) €16,503 (120.7)% (124.8)%

Other Financial Information:

Adjusted EBITDA ........................................ €32,451 €29,098 €3,353 11.5% 15.7%

Revenue

Consolidated revenues have reduced €2.2 million or 1.3% year-on-year. On a like-for-like basis, and at constant exchange rates, revenue has fallen by €5.9 million. The impact of average exchange rates, year-on-year has impacted revenue by a further €5.3 million. The Australian business has grown by €2.2 million, year-on-year, and at constant exchange rates.

The decline in the revenue of the European business, year-on-year, is largely the effect of exiting less profitable contracts in our German business, which has declined €5.5 million. During 2015, we exited a number of less profitable contracts in our German business, which generally run from April to March each year. The effect of exiting these contracts impacts on the first quarter results for 2016, and the comparison year-on-year.

The UK showed a decline of €2.2 million, on revenue of €53.1 million, as slow market conditions and timing of promotions affected the start of the season.

By geographical segment, based on our operating segment analysis in the Q1 2016 Condensed consolidated interim financial information, except as stated otherwise:

Using constant exchange rates, UK revenues decreased by €2.1 million. Market conditions have been

difficult with a weaker performance in retail sales, whilst there has been growth in sales to discounters. The

market has seen the effects of price promotions from our largest competitor, which has driven some marginal

volume growth in the market (up 1.0%, year-on-year, to the end of March 2016), but with a similar effect

on pricing, such that the market (in value terms) has been broadly flat over the same period. The UK business

has not sought to buy volumes, but has offered incremental promotions, particularly in the retail channel.

Using constant exchange rates for each period, Australian revenues have increased €2.2m in the three

months ended March 31, 2016 compared to the three months ended March 31, 2015, which is a strong

performance at the end of the summer season in Australia, despite a challenging market in Q1 2016.

German revenues showed a decline of €5.5 million in the three months ended March 31, 2016 compared to

the three months ended March 31, 2015. This was largely a result of exiting of less profitable contracts from

April 2015. There is also a notable change in mix within the German business, with owned and licensed

brands contributing 17.4% of external revenues, compared to 15.6% in the three months ended March 31,

2015.

French revenues have shown a slight decrease of €0.8 million compared to the prior period due to market

14

conditions although there has been a €0.3 million increase in branded sales. Branded sales as a proportion

of total sales continues to increase year on year.

Italian revenues increased €1.1 million in the three months ended March 31, 2016 compared to the prior

period, mainly due to intercompany sales, but also a €0.3 million increase in sales to discounters.

Polish revenues have increased €0.7 million compared to the prior period, an increase of 11% year on year.

This is mainly as a result of strong branded sales.

South Africa contributed revenues of €9.0 million at the average exchange rate for the three months ended

March 31, 2016, and like Australia this period represents the end to the main selling season. Performance

has benefitted from post-acquisition initiatives to grow sales and market share, in what is a growing market.

Cost of Sales

Cost of sales (including exceptional items) reduced by €9.4 million or 8.4% to €102.0 million for the three months ended March 31, 2016 as compared to €111.4 million for the three months ended March 31, 2015. This reduction would grow to €12.2 million on a like-for-like basis (excluding the impact of acquisitions and FX). The reduction in cost of sales is attributable to the exiting of less profitable contracts in our German business, the growth in new product development (which has a positive effect on our gross margin), the growth of our branded share in the sales mix, and the positive effects of capital expenditure projects on our operational efficiency.

Distribution Expenses

Distribution expenses increased by €1.5 million or 8.7% to €18.5 million for the three months ended March 31, 2016 as compared to €17.0 million for the three months ended March 31, 2015. Excluding the effects of FX, distribution expenses increased €1.9 million, or 11.3%. The increase is largely attributable to the impact of R&R South Africa which has added €2.4 million to distribution costs in 2016 compared to 2015. Excluding one-off effects, distribution costs reduced by €0.9 million including the effects of FX, or by €0.4 million excluding the effects of FX.

Administrative Expenses

Administrative expenses increased €4.1 million or 17.1% to €28.0 million for the three months ended March 31, 2016 as compared to €23.9 million for the three months ended March 31, 2015. Excluding the effects of FX, our administrative expenses increased €4.9 million, or 20.5%. The increase is mainly due to the impact of R&R South Africa which has added €1.8 million to administrative expenses in 2016 compared to 2015 and a €2.1 million increase in exceptional operating expenses and amortisation, which includes €2.5 million of costs related to the proposed joint venture with Nestlé.

Finance Expenses

Net finance expenses decreased €15.8 million or 52.9% to €14.0 million for the three months ended March 31, 2016 as compared to €29.8 million for the three months ended March 31, 2015. This decrease is substantially due to a decrease in net foreign exchange losses of €13.4 million (non-cash item) together with an increase of €2.5 million of gains on the revaluation to fair value of derivative financial instruments (also non-cash). Offsetting these effects, compounding (higher) interest in the amount of €0.8 million with respect to our subordinated shareholder loans.

Of the €14.0 million net finance charges (three months ended March 31, 2015: €29.8 million), €8.9 million (March 30 2015: €8.1 million) relates to non-cash interest on the subordinated shareholder loan.

Income Tax Charge

Income tax charge increased €0.8 million to a €1.7 million charge for the three months ended March 31, 2016 as compared to a €0.9 million charge for the three months ended March 31, 2015. Excluding FX, our income tax charge increased €0.9 million.

Adjusted EBITDA

Adjusted EBITDA increased €3.4 million in the three months ended March 31, 2016 to €32.5 million

compared to €29.1 million in the three months ended March 31, 2015. This is a record performance despite an

adverse impact from unfavourable FX rates of €1.2 million which is offset by a €1.0m EBITDA contribution

from R&R South Africa. Adjusted EBITDA increased 2.2 percentage points from 17.2% in the three months

ended 31 March 2015 to 19.4% in the three months ended March 31, 2016. The benefits from the increase in

gross margin and overhead savings contributing to the improved Adjusted EBITDA percentage.

15

Cash Flows

The following summarises our primary sources of cash flow in the periods presented:

Three months ended

March 31 Change to Net

Cash Flow

Amount (in thousands of euros) 2016 2015

Cash generated used in:

Operating activities ............................................... (€29,286) (€9,697) (€19,589)

Investing activities ................................................ (11,070) (8,205) (2,865)

Financing activities ............................................... (3,338) (389) (2,949)

Total ........................................................................ (€43,694) (€18,291) (€25,403)

Free cash flow before financing, acquisitions

and exceptional operating items: (€40,780) (€14,398) (€26,382)

Operating Activities

Cash generated from operating activities reduced €19.6 million to an outflow of €29.3 million for the three months

ended March 31, 2016 as compared to an outflow of €9.7 million for the three months ended March 31, 2015. This is

mainly due to a €17.4 million increase in working capital within operating activities as a result of the start of stock

building ahead of the European summer, with inventories increasing €8.8 million year-on-year, compared to the

closing year end positions. The rationale for the inventory build-up is to improve service levels through the

European peak season and to accommodate new business in Italy, in particular. In addition, cash flow has been

impacted by the acquisition of R&R South Africa, which has driven an increase in debtors versus the comparative

period in 2015 (effect: €6.5 million in the three months ended March 2016; €nil in the three months ended March

2015), and also the effect of settlement of a number of exceptional costs that were accrued at the 2015 year end

(combined effect: €2.9 million, year-on-year).

Investing Activities

Cash used in investing activities increased by €2.9 million to an outflow of €11.1 million for the three

months ended March 31, 2016 as compared to an outflow of €8.2 million for the three months ended March 31,

2015. This increase is mainly due to an increase in capex spend of €4.2 million as a result of continued

capital investment in our factories. The same period in 2015 also included a €1.7 million deferred

consideration payment related to a historic acquisition.

Financing Activities

Cash used in financing activities increased by €2.9 million to a net outflow of €3.3 million for the three

months ended March 31, 2016 as compared to a €0.4 million inflow for the three months ended March 31, 2015.

This related to a loan to a parent undertaking in the three months ended March 31, 2016.

Free cash flow before financing, acquisitions and exceptional operating items

Free cash flow before financing, acquisitions and exceptional operating items worsened by €26.4 million to

an outflow of €40.8 million for the three months ended March 31, 2016 as compared to a €14.4 million outflow

for the comparative period. This is largely driven by the increase in working capital and capital expenditure

year-on-year, offset by a €3.4 million improved EBITDA performance in the first quarter.

R&R Ice Cream plc

Registered No. 05777981

Condensed consolidated interim financial information

(unaudited) for the three months ended

31 March 2016

2

Contents

Page

Condensed consolidated interim financial information

Condensed consolidated income statement 3

Condensed consolidated statement of comprehensive income 4

Condensed consolidated statement of changes in equity 5

Condensed consolidated statement of financial position 6

Condensed consolidated statement of cash flows 7

Notes to the condensed consolidated interim financial information 8

Condensed consolidated income statement

3

For the three months ended 31 March 2016

In thousands of Euros

Note

Before exceptional

items, amortisation and non-cash

interest

Exceptional items,

amortisation and non-cash

interest(1)

Three months ended

31 March 2016 Total

Before exceptional

items, amortisation and non-cash

interest

Exceptional items,

amortisation and non-cash

interest(1)

Three months ended 31

March 2015 Total

Revenue 1 167,042 - 167,042

169,285 - 169,285

Cost of sales (101,990) - (101,990)

(111,394) - (111,394)

Gross profit 65,052 - 65,052

57,891 - 57,891

Distribution expenses (18,504) - (18,504)

(17,016) - (17,016)

Administrative expenses (21,357) (6,632) (27,989)

(19,332) (4,563) (23,895)

Results from operating activities 25,191 (6,632) 18,559 21,543 (4,563) 16,980

Finance income 4 149 6,125 6,274

16 385 401

Finance expenses 4 (10,100) (10,181) (20,281)

(10,535) (19,627) (30,162)

Net finance costs 4 (9,951) (4,056) (14,007)

(10,519) (19,242) (29,761)

Profit / (Loss) before income tax 15,240 (10,688) 4,552 11,024 (23,805) (12,781)

Income tax charge 5 (1,717)

(887)

Profit / (Loss) from continuing operations

2,835 (13,668)

Attributable to:

Equity holders of the Company 2,835 (13,668)

Note (1): in order to aid understanding of the financial results, the Directors have presented additional analysis prior to the effect of exceptional items, amortisation of intangible assets and non-cash interest income/ (charges). These items are analysed in detail in note 2.

The notes on pages 8 to 27 are an integral part of this condensed consolidated interim financial information.

All operations are continuing.

Condensed consolidated statement of comprehensive income

4

For the three months ended 31 March 2016

In thousands of Euros

Note

Three months

ended

31 March 2016

Three months

ended

31 March 2015

Profit / (Loss) for the period 2,835 (13,668)

Other comprehensive income / (expense)

Items that are or may be reclassified to profit or loss

Exchange differences on retranslation of foreign operations 6 (12,744) 31,169

Net investment hedging 6 14,919 (17,220)

2,175 13,949

Total comprehensive income for the period 5,010 281

Condensed consolidated statement of changes in equity

5

For the three months ended 31 March 2016

In thousands of Euros

Share

capital

Currency

translation

Accumulated

loss

Total

equity

Balance at 1 January 2016 50,886 (21,276) (193,079) (163,469)

Profit for the period - - 2,835 2,835

Exchange difference on retranslation of

foreign operations - (12,744) - (12,744)

Net investment hedging - 14,919 - 14,919

Total comprehensive income for the period - 2,175 2,835 5,010

Balance at 31 March 2016 50,886 (19,101) (190,244) (158,459)

Balance at 1 January 2015 50,886 (17,141) (226,472) (192,727)

Loss for the period - - (13,668) (13,668)

Exchange difference on retranslation of

foreign operations - 31,169 - 31,169

Net investment hedging - (17,220) - (17,220)

Total comprehensive income/ (expense) for

the period - 13,949 (13,668) 281

Balance at 31 March 2015 50,886 (3,192) (240,140) (192,446)

Condensed consolidated statement of financial position

6

As at 31 March 2016

In thousands of Euros

Assets

Note

31 March

2016

31 March

2015

31 December

2015

Non-current assets

Property, plant and equipment 200,368 208,889 202,339

Intangible assets 591,092 635,431 607,612

Deferred tax assets 23,900 18,830 21,270

Total non-current assets 815,360 863,150 831,221

Current assets

Inventories 172,230 156,978 94,618

Current tax assets 742 4,041 780

Trade and other receivables 192,161 150,669 168,488

Cash and cash equivalents 63,216 28,203 108,676

428,349 339,891 372,562

Assets classified as held for sale 428 414 428

Total current assets 428,777 340,305 372,990

Total assets 1,244,137 1,203,455 1,204,211

Equity and liabilities

Equity

Share capital 6 50,886 50,886 50,886

Currency translation reserve 6 (19,101) (3,192) (21,276)

Accumulated loss 6 (190,244) (240,140) (193,079)

Total equity (158,459) (192,446) (163,469)

Non-current liabilities

Financial liabilities 7 1,066,378 1,073,195 1,084,799

Deferred tax liabilities 19,036 20,428 17,479

Provisions 8 4,897 4,168 4,741

Total non-current liabilities 1,090,311 1,097,791 1,107,019

Current liabilities

Financial liabilities 7 14,831 26,199 5,543

Trade and other payables 285,418 264,674 244,555

Current tax liabilities 5,227 74 3,914

Provisions 8 6,809 7,163 6,649

Total current liabilities 312,285 298,110 260,661

Total liabilities 1,402,596 1,395,901 1,367,680

Total equity and liabilities 1,244,137 1,203,455 1,204,211

These financial statements were approved by the Board of Directors on 27 May 2016 and were signed on its behalf by:

Ibrahim Najafi Director

Condensed consolidated statement of cash flows

7

For the three months ended 31 March 2016

In thousands of Euros

Note Three months

ended

31 March 2016

Three months

ended

31 March 2015

Cash flows from operating activities

Adjusted EBITDA 3 32,451 29,098

Adjustments for exceptional items (4,374) (1,525)

Operating cash flow before changes in working

capital and provisions 28,077 27,573

Increase in inventories (77,612) (68,773)

Increase in trade and other receivables (20,337) (18,770)

Increase in trade and other payables 41,736 53,934

Increase/(decrease) in provisions 248 (1,054)

Cash used in operations (27,888) (7,090)

Interest paid (618) (942)

Income tax paid (780) (1,665)

Net cash used in operating activities (29,286) (9,697)

Cash flows from investing activities

Interest received 145 16

Proceeds from sale of property, plant and equipment 4 60

Acquisition of subsidiary, net of cash acquired - (1,746)

Acquisition of property, plant and equipment (10,697) (6,514)

Acquisition of intangible assets (522) (21)

Net cash used in investing activities (11,070) (8,205)

Net cash outflow from operating and investing activities (40,356) (17,902)

Cash flows from financing activities

Loan to parent undertaking 9 (3,336) -

Repayment of finance lease liabilities (2) (338)

Transaction costs relating to refinancing - (51)

Net cash outflow from financing activities (3,338) (389)

Net decrease in cash and cash equivalents (43,694) (18,291)

Cash and cash equivalents at 1 January 108,676 36,012

Effect of exchange rate fluctuations on cash held (1,766) 1,482

Prepaid transaction costs deducted from revolving credit facility - 226

Cash and cash equivalents at 31 March 63,216 19,429

Closing cash and cash equivalents reconciled by:

Cash 63,216 28,203

Revolving credit facility - (8,774)

Cash and cash equivalents at 31March 63,216 19,429

Memorandum:

Net cash flow from operating and investing activities (43,692) (17,902)

Acquisition of subsidiaries, net of cash acquired - 1,746

Exceptional operating items – cash flows 2,912 1,758

Free cash flow before financing, acquisitions and exceptional

operating items

(40,780) (14,398)

The notes on pages 8 to 27 are an integral part of this condensed consolidated interim financial information.

Notes to the condensed consolidated interim financial information

R&R Ice Cream plc Annual Report 8

Basis of preparation

This condensed consolidated interim financial information presents the consolidated financial records for the three months ended 31 March 2016 of R&R Ice Cream plc and its subsidiaries. The condensed consolidated interim financial information for the three months ended 31 March 2016 has been prepared in accordance with the International Accounting Standard (“IAS”) 34 ‘Interim financial reporting’ as adopted by the European Union. The condensed consolidated interim financial information for the three months ended 31 March 2016 does not constitute statutory financial statements under the definition of Section 434 of Part 15, chapter 7 of the Companies Act 2006, and does not include all of the information and disclosures required for full annual financial statements. It should be read in conjunction with the consolidated report and financial statements for the group for the year ended 31 December 2015. The condensed consolidated interim financial information has not been audited. The comparative figures for the financial year ended 31 December 2015 are not the Company’s statutory accounts for that financial year. Those accounts have been reported on by the Company’s auditors and delivered to the registrar of companies. The auditor’s report on those financial statements was (i) unqualified, (ii) did not include a reference to any matters to which the auditors drew attention by way of emphasis without qualifying their report and (iii) did not contain a statement under section 498 (2) or (3) of the Companies Act 2006. We have changed the presentation of the condensed consolidated statement of cash flows to re-present working capital movements within cash used in operating activities. This change does not impact any totals presented from the comparative period. Going concern At 31 March 2016, the group has consolidated net liabilities of €158.5 million (31 March 2015: €192.4 million). Net liabilities are typical in private equity backed businesses largely due to the financing structure adopted and the rolling up of non-cash interest on parent company loans, which is not payable until 2110 at the earliest. In 2014, the business refinanced, securing loan notes providing absolute certainty over future interest charges until 2020. The Directors believe that the rates are competitive and reduce the exposure of the business to increases in interest rates for the medium term. This gives the Board further comfort as to the going concern status, understanding the related cash requirements and the lack of additional unknown risk. The Directors have considered this position, together with the group’s budgets and positive net current assets position, and after making appropriate enquiries, the Directors consider that the group has adequate resources to continue in operational existence for the foreseeable future and therefore continue to adopt the going concern basis for the preparation of this condensed consolidated interim financial information. Seasonality This condensed consolidated interim financial information was approved for issue on 27 May 2016. Except as described below, the basis of preparation and accounting policies applied in this condensed consolidated interim financial information for the three months ended 31 March 2016 is consistent with those of the annual financial information for the year ended 31 December 2015, as described in that annual financial information. For the purposes of this condensed consolidated interim financial information, it should be noted that the group’s sales are subject to significant monthly fluctuations as a result of the seasonal weather patterns experienced in our core geographical markets. As a result of these seasonal fluctuations, the group has historically made the majority of its revenue and profits in the second and third quarters of the year. However this has now reduced following the acquisition of businesses in Australia and South Africa. In the year ended 31 December 2015, we generated 63% of our sales between April 1 and September 30 (2014: 70%). The balances of inventories, trade debtors and trade creditors at 31 March each year are also higher than at the financial year end as a result of seasonal fluctuations.

Notes to the condensed consolidated interim financial information (continued)

9

Basis of measurement The consolidated financial statements have been prepared on the historical cost basis except for the revaluation of certain financial instruments. The methods used to measure fair values are discussed further below. Use of estimates and judgements

The preparation of financial statements requires management to make judgements, estimates and assumptions

that affect the reported values of assets, liabilities, revenues and expenses. The estimates and associated

assumptions are based on historical experience and other judgements reasonable under the circumstances, the

results of which form the basis of making the judgements about carrying values of assets and liabilities that are

not readily apparent from other sources. Actual results may differ from those estimates. Significant areas of

estimates and judgement for the group are:

Measurement of fair value assets and liabilities acquired as part of business combinations.

Historically, on the acquisition of businesses, significant judgements are required in respect of

the fair value of intangible assets, such as brands and customer relationships, the fair value of

Property, plant and equipment and other assets.

Discount factors and future cash flow projections used in testing for impairment of assets, in

particular in respect of brands and goodwill which have indefinite useful economic lives and are

tested annually for impairment. The impairment testing is based on value-in-use calculations,

which include estimates and assumptions in respect of future cash flows of the group, in

particular in respect of future sales, costs, growth rates and terminal values. Judgements are

also involved in the calculation of discount factors by country and for the group.

Measurement and recognition of current and deferred tax assets and provisions. The group is

subject to income tax in numerous jurisdictions. Significant judgement is required in determining

current tax liabilities and in the recognition of deferred tax assets and liabilities; and this

includes reassessing judgements formed in previous periods when circumstances change, such as

changes in legislation, dialogue with tax authorities or other factors. Where this is the case, the

judgement exercised in these matters may cause the group to alter balances from the amount

initially recognised, and such differences will impact the current and deferred income tax assets/

liabilities and credit/ charge in the period of determination. Judgement is also required in