book presentation: excess returns: a comparative study of the methods of the world's greatest...

TRANSCRIPT

Book Presentation:

Excess returns –A comparative study of the methods of the world’s greatest investors

Frederik Vanhaverbeke

Topics:The investment philosophy;

Finding bargains; Fundamental business analysis;

Valuation; Common process mistakes;

How to buy and sell intelligently;Risk versus return;

The intelligent investor

Books/articles/ interviews

about/by top investors

Books stock market behavior

Business literature(best practices) Behavioral finance

Book Excess Returns

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

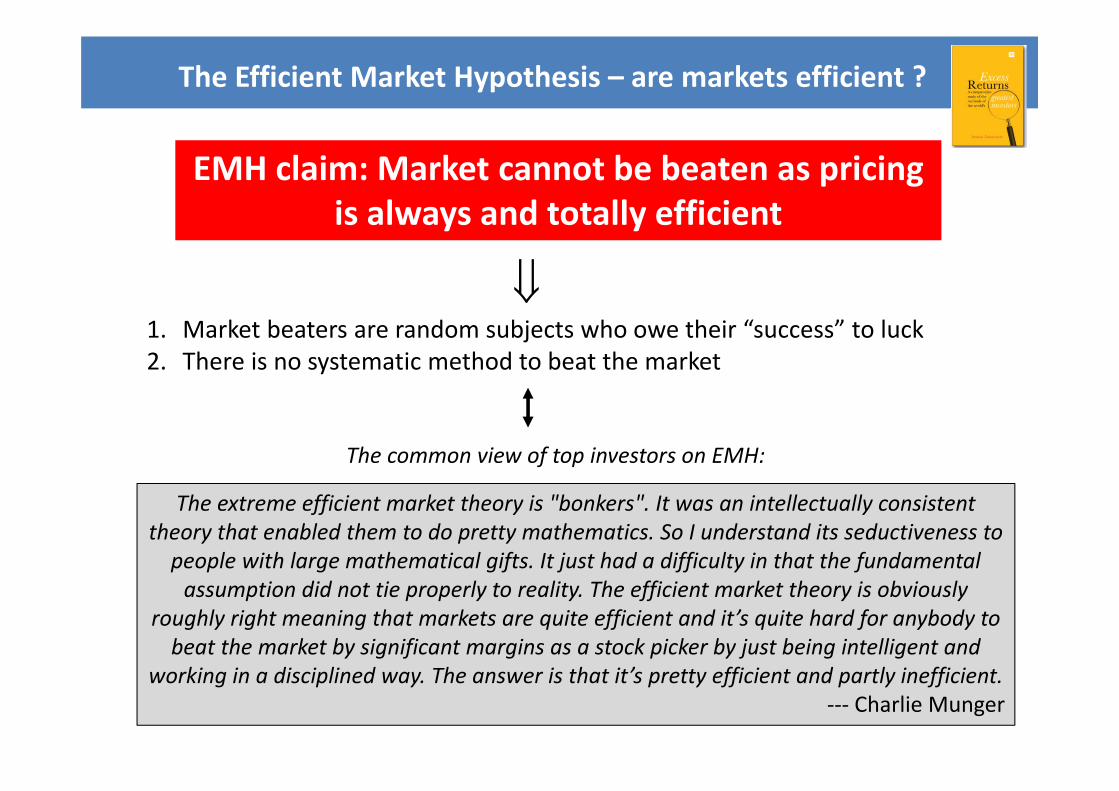

The Efficient Market Hypothesis – are markets efficient ?

EMH claim: Market cannot be beaten as pricing is always and totally efficient

1. Market beaters are random subjects who owe their “success” to luck2. There is no systematic method to beat the market

The extreme efficient market theory is "bonkers". It was an intellectually consistent theory that enabled them to do pretty mathematics. So I understand its seductiveness to people with large mathematical gifts. It just had a difficulty in that the fundamental assumption did not tie properly to reality. The efficient market theory is obviously

roughly right meaning that markets are quite efficient and it’s quite hard for anybody to beat the market by significant margins as a stock picker by just being intelligent and

working in a disciplined way. The answer is that it’s pretty efficient and partly inefficient.‐‐‐ Charlie Munger

The common view of top investors on EMH:

The Efficient Market Hypothesis –Challenge 1: Momentum trading

Jesse Livermore (first decades of 1900s): spiritual father of momentum trading

Turtle tradersOtherRichard Dennis:

1) 15 years (70s, 80s): $400 → $200 million2) 1994 → 1998: 63% annually

Annual compound return

Number of years (track record)

Tom Shanks 29.7% 22

Paul Rabar 25.5% 23

Liz Cheval 23.1% 21

H. Seidler 22.8% 23

Jerry Parker 22.2% 23

S. Abraham 21.7% 19

William Eckhardt:1978→ 1991: 60% annually

Turtle experiment

William O’Neil (CANSLIM):40% annually over 25 years

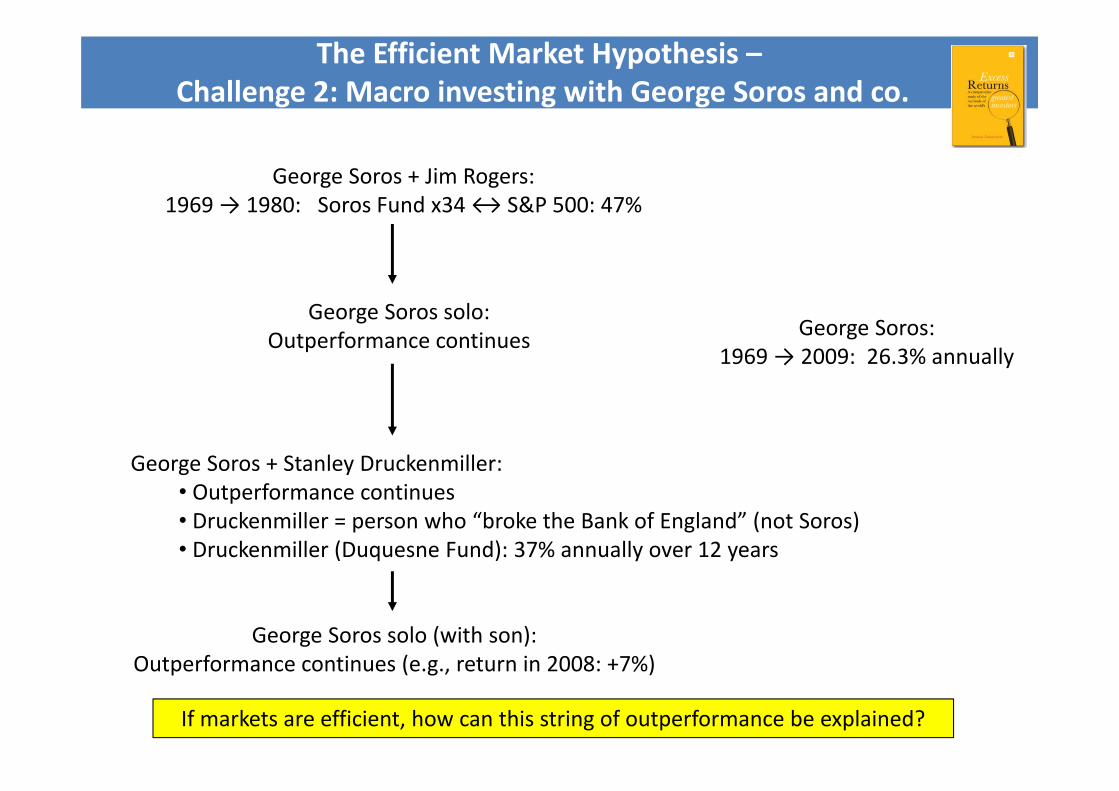

The Efficient Market Hypothesis –Challenge 2: Macro investing with George Soros and co.

George Soros:1969 → 2009: 26.3% annually

George Soros + Stanley Druckenmiller:• Outperformance continues• Druckenmiller = person who “broke the Bank of England” (not Soros)• Druckenmiller (Duquesne Fund): 37% annually over 12 years

If markets are efficient, how can this string of outperformance be explained?

George Soros solo:Outperformance continues

George Soros solo (with son):Outperformance continues (e.g., return in 2008: +7%)

George Soros + Jim Rogers:1969 → 1980: Soros Fund x34 ↔ S&P 500: 47%

The Efficient Market Hypothesis – Challenge 3

Edward Thorp, Mathematics professor:

• Derived the Black‐and‐Scholes option pricing model a few years before Black and Scholes but decided to keep it secret (to make money)

• 1969 → 1988: return Princeton Newton Partners: 19.1% annually

• Princeton Newton Partners: positive performance in 227 out of 230 months !!!→ probability of this kind of consistency or be er 6.1E‐46

(number of atoms on earth 1E50)

Can this be explained by luck?

The Efficient Market Hypothesis – Challenge 4: The Superinvestors of Graham‐and‐Doddsville and like minded

Annual compound return

Number of years (track record)

Benjamin Graham 21% 20

Walter Schloss 20% 49

Tom Knapp 20% 16

Bill Ruane 18% 14

Warren Buffet 22% 57

Annual compound return

Number of years (track record)

Joel Greenblatt 40% 20

Rick Guerin 33% 19

Eddie Lampert 29% 16

Charles Munger 20% 14

PremWatsa 22% 28

Pupils of Benjamin Graham

Warren Buffet adepts

“Superinvestors of Graham‐and‐Doddsville”: Walter Schloss, Tom Knapp, Rick Guerin, Bill Ruane, StanPerlmeter, Charles Munger: identified as exceptional investors by Buffett when they had no track

record!!!

The Efficient Market Hypothesis – Excess returns (over S&P 500) of top investors

The Efficient Market Hypothesis – Excess returns and the power of compounding

Warren Buffet, Jan 1957 – Jan 2013 (57 years): annual compound return = 22.29%(= 12.4% annually above return of S&P 500 including dividends)

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

The Investment Philosophy – Market Philosophy

Success in the market starts with a sound market philosophy…

Effective market philosophy• Explains drivers behind the market• Explains how these drivers create inefficiencies• Shows how one can take advantage of pricing inefficiencies

Effective market method Practical and proprietary implementation of the philosophy

Common for all market operators of same “school”

Different for each market operator, dependent on:• Personal preferences• Fit with personality

There is nothing new on Wall Street or in stock speculation. What has happened in the past will happen again and again and again. This is because human nature does not change, and it is human emotion

that always gets in the way of human intelligence.‐‐‐ Jesse Livermore

Market philosophies are timeless:

The Investment Philosophy – Examples

Investing versus momentum trading

INVESTING MOMENTUM TRADING

Drivers of stock prices

• Cognitive biases: herding, extrapolation, asymmetric loss aversion, etc…• Different market styles: investing, trading, speculating, etc…• Different objectives among market operators (e.g., quick win vs. long term)

Basic premise Over long term stock prices revert to their (true) intrinsic value

There is price momentum in stocks that tends to persist over some time

Basic approach• Determine intrinsic value of stocks• Buy at discount to intrinsic value• Sell when price reaches intrinsic value

• Closely track price action• Buy (sell short) stocks with strong (weak) price action

• Get out when trend reverses

Investing methods

Find stocks below intrinsic value+

Buy/ sell intelligently

→ take cues from most success-ful investors in the world

Focus of the book

The Investment Philosophy

BUY

SELL

Stock price (value)

Time

Intrinsic value

Stock price: quasi‐random walk around intrinsic value

Buy when stock trades at significant discount

Sell close to or above intrinsic value

The Investment Philosophy – remarks

It is extraordinary to me that the idea of buying dollar bills for 40 cents takes immediately topeople or it doesn’t take at all. It’s like an inoculation. If it doesn’t grab a person right away,

I find that you can talk to him for years and show him records, and it doesn’t make any difference. They just don’t seem able to grasp the concept, as simple as it is.

‐‐‐Warren Buffet

Fully endorse investment philosophy (“fit with personal beliefs”)

Apply a method that fits their personality and preferences

Have the right psychological mindset (e.g., patience, independence, emotional detachment, etc.)

Successful investors

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

The Investment Philosophy – consistency of outperformance, 1

Let’s first get a myth out of the world: outperformance in every single year is not of this world !!!

The Investment Philosophy – consistency of outperformance, 2

Joel Greenblatt: one of the most impressive track records in the hedge fund industry!!!

1995‐2005, Joel Greenblatt on his own: 30% a year (20% better

than the market)!!!

1985‐2005Greenblatt: $1,000 → $840,000S&P 500: $1,000 → $12,000

The Investment Philosophy – consistency of outperformance, 3

Even over multi‐year periods many top investors regularly underperform versus the market…

Their goal = outperformance over an entire (bull‐bear) cycle

The Investment Philosophy – consistency of outperformance, 4

Let’s look at Seth Klarman, one of the few hedge fund managers that Buffett would entrust his money to…

In spite of long period of under‐performance, track record

over 26 years is exceptional !!!

The Investment Philosophy – common sense on track records, 1

Hence, for all those who are still not convinced, answer the following question:

Investing = statistical process because stocks move along a quasi‐random walk over which the investor has no control !!!!

In a game where two dice throwers must throw a green surface, does someone

who throws a dice with 4 green and 2

red surfaces alwayswin from someone with a dice that has 3 green and 3 red

surfaces ?

The Investment Philosophy – common sense on track records, 2

→ Although the odds are stacked in favor of the first

dice thrower (i.e., he competes with an edge

versus the other player), statistics says that only over the long run (i.e., a sufficient number of games) the first dice thrower is (very likely)

to come out ahead.

The Investment Philosophy – common sense on track records, 3

Common sense on track records

Investing = statistical process:(*) Investor performance = quasi‐random walk versus market return (with other

expected return);(*) Every year is like one throw of the dice; investor with edge will not win every year

but is very likely to come out ahead over sufficient number of years;(*) Track records not easy to interpret, not even over multi‐year periods; those looking

exclusively at track records don’t count the number of green surfaces of the dice.

Evaluation investment method indispensable in evaluation track record (Buffet downplays importance of track records in his search for portfolio managers of his investment float; focuses on personality, philosophy and process instead)

So, ditch a top investor who temporarily underperforms at your own peril!!

The Investment Philosophy – common sense on track records, 4

Why should the time required for a planet to circle the sun synchronize precisely with the time required for business actions to pay off? While I

much prefer a five‐year test, I feel three years is an absolute minimum for judging performance. It is a certainty that we will have years when the

partnership performance is poorer, perhaps substantially so, than the Dow. If any three‐year or longer period produces poor results, we all should start looking around for other places to have our money. An exception to the

latter statement would be three years covering a speculative explosion in a bull market.

‐‐‐Warren Buffet

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

The Investment Chain ‐ Overview

Finding potentialbargains

Due DiligenceQualitative analysis

Quantitative analysis

Valuation

Focus: stocks with above‐average probability of being undervalued

Ignore: stocks that are unlikely to be bargains

Buy/stay away/ hold/ sell/sell short

Continuous follow‐up of existing positions

Preference for wrong types of stocks

Biased analysis

Irrational trades

Succesfullycoping with biases

THE INTELLIGENT INVESTOR

Superior process & execution

PSYCHOLOGICAL

BIASES

“Investment Process”

The Investment Process ‐ Finding Bargains ‐ 1

What stocks tend to be

undervalued?

What stocks tend to be overvalued?

Drivers of over/under valuation

Sentiment Cognitive biases

Number of investors looking at idea

Incentives to buy/sell

Information among investors about company

Top investors focus efforts on most promising ideas

Huge stock universe + due diligence of single idea very time‐consuming

Select for further scrutiny

Deselect

Tip‐offs

Well‐informed buyers/sellers

Well‐informed admirers

Choosing individual stocks without any idea of what you’re looking for is like running through a

dynamite factory with a burning match. You may live, but you’re

still an idiot.‐‐‐ Joel Greenblatt

The Investment Process – Finding bargains ‐ 2

Stocks in the spotlight Ignored stocks(dull, unfashionable, complex, small)

Positive sentiment stocks(hot, widely admired, high‐growth)

Negative sentiment stocks(despised, troubled, lousy industry)

People are always asking me where the outlook is good, but that’s the wrong question. The right question is: Where is the outlook most miserable?

‐‐‐ John Templeton

The Investment Process – Finding bargains –Jeffries’ Finest Moment

Jeffries, global investment bank; several nominations of "Best place to work“; Excellent track record in its industry up until 2011

Leucadia merges with Jeffries

The Investment Process – Finding bargains ‐ 2 ‐ examples

Companies with “buzz” around them are seldom good investments !!! – Belgium

The Investment Process – Finding bargains

IPOs Spin‐offs

Example, Belgian spin‐off out of Omega Pharma:

Any time you read about a spinoff being

accomplished through a rights offering, stop

whatever you’re doing and take a look.

‐‐‐ Joel Greenblatt

The new issue market is ruled by controlling stockholders and

corporations who can usually select the timing

of offerings. Understandably, these sellers are not going to offer any bargains.

‐‐‐Warren Buffet

The Investment Process – Finding bargains ‐ Summary

Odds stacked against undervaluation

Don’t waste your time on these!!!(does not exclude that there can be

an ocassional winner here)

Above‐average probability of undervaluation

Take a closer look (don’t buy blindly!!)

Hot stocks

Ignored stocks

IPOsSpecial situation

stocks

Hated stocks

Stocks hitting

new lows

Greenblatt’smagic formula

stocks

Stocks added to an index

Stocks removed from index

Underappreciated beneficiaries of new trends

Post‐bankruptcy stocks

Stocks of pioneering businesses

Businesses without earnings track

record

Insider buying

Not necessarily good short ideas (see next slide)!!!

The Investment Process – What do top investors short?

Poor fundamentals Management issues: dishonesty, greed,

exuberance, rubberstamping of boards Poor financials: weak balance sheet, low ROE

and low ROIC, poor cash flow generation Flawed business model Growth saturation Weak industry

Good stock characteristics Overinflated price High float Popular among professionals Middle-sized short interest

Triggers Insider sales Resignation key people Change in auditors Late filings Rumors that something is wrong

Do not short stocks with good stock characteristics that are

fundamentally OK

Avoid technology stocks

Avoid beaten-down stocks

Good Short candidates

Shorting is not for the faint of heart + stock selection requires a very specific approach…

The Investment Process – Finding bargains in emerging markets

Compelling valuations

Attractive country

Primary beneficiaries of emergence of the country

+

+

Economic reforms, hands‐off government, infrastructure,

savings mentality, etc.Successful investing in emerging markets

Financials, consumer products, media, excellently‐run players,

etc.

The Investment Process –How Top Investors analyze businesses

In evaluating people you look for three qualities: integrity, intelligence, and energy. If you don’t have the first, the

other two will kill you.‐‐‐Warren Buffet

Quantitative analysis

Income statement Earnings track record Dividend history Profit margins ROIC, ROE

Balance sheet Liquidity Solvency Z-score, H-score

Cash flows Operating cash flow Free cash flow

Qualitative business analysis

Industry Barriers to entry Competitive pressure Threat substitutes Capital intensity Rate of change

Business model Simplicity ↔ complexity Track record: scalability,

profitability, market share

Competitive position Power versus customers,

suppliers, internal competitors

Pillars: culture, HR, structure, processes, marketing, R&D, innovation, operations

Control over destiny Government interference Dependence on R&D,

fashion or critical decisions Operational/financial

leverage Diversification of customer

base and geography Impact weather or economy

Growth Decent growth prospects Track record Growth management Risk of growth saturation?

Management

Personality Integrity Modesty Non-complacency Independence

Experience & skill Track record Capital allocation: tight

ship, focus on opportunities, little leverage, no empire building

Strategy: unique + based on core competencies

Values Promotion values Consistently enforced Management = example

Ownership & allegiance Insider holdings Long tenures Fair compensation Long-term thinking Focus on company not on

personal cult

Energy and passion Love for the job Fascination for industry Motivated by challenge

and contents

Board of directors

Skills, savvy, experience Skin in the game Devotion to their duties Independence: willingness to

challenge CEO, small board, low compensation, no family ties,…

Insider sales? Earnings management?

Late filings?

Resignation key people? Auditor turnover?

Footnotes?

Due diligence characterized by:• Independence •Thoroughness (“going the extra mile”)• Scuttlebutt• Looking at subtle things that other investors overlook

• Skipping businesses that are toocomplex

• Critical view on leverage• Focus on one’s circle of competence

The Investment Process – How Top Investors value businesses

DCF

Multiples –income statement: P/E (trailing + normalized) P/FCF: for mature companies P/S: companies without or with unstable earnings

Multiples –balance sheet: P/BV: capital-intensive, no economic goodwill P/Liquidation value: decline/near bankrupt P/Replacement value: stable, low-growth

Multiples –income statement+balance sheet:EV/EBIT(DA), EV/S, EV/FCF

Sum-of-the-parts Value on a deal basis (with discount)

Graham and Dodd EPV: business with moat Full growth value: franchise

with substantial growth

Conservatism (margin of safety)

KISS (simple models)

Triangulation Comparison with peers/historical valuation

Skepticism Quality at fair price

Restrict number of parameters

Preference for balance sheet multiples

Normalize + use trailing values

Be skeptical of moats and growth

Avoid DCF when possible

As long as you are consistent in how you value businesses, your

degree of inaccuracy, if it is replicated through

consistency, will lead to a great model for relative valuations. So if your valuation model is not sophisticated, does not take into account six

dozens variables, well, as long as you are applying it the same way to every company and you are

looking at a lot of different companies, you will have a useful model for relative valuation which can lead to very superior investment

returns.‐‐‐ Charlie Munger

The Investment Process – Common Process mistakes ‐1

1. Incoherent investment approach• Investing trading

(e.g., Buffet: “stop losses is like buying a house for $1 million and telling yourbroker to sell when he/she gets a bid for $800,000.”)

• Investing speculation based on hunches/rumours

2. Lack of independence: markets are quite efficient so one must do one’s own thoroughdue diligence (what most others know is already in the stock price)

3. Biased analysis:• Mindless extrapolation of stock price performance/financial results• Cherry‐picking of information about companies• Sympathy and home bias: e.g., Kirk Kerkorian invested in GM right before its

bankruptcy due to his passion for cars.• Illusion of familiarity: e.g., people invest substantial amounts in stock of employer

even though they don’t know its financials well.

What is already known and published by others has already been acted upon. Assume you are always the last to know.

‐‐‐ Charles Kirk

The Investment Process – Common Process mistakes ‐2

4. Focus on wrong factors: economy (too challenging for most investors), short‐term “catalysts” (or lack thereof), etc.

Charlie and I continue to believe that short‐term market forecasts are poison and should be kept locked up in a safe place, away from children and also

from grown‐ups who behave in the market like children.‐‐‐Warren Buffet

5. Price instead of value: • Anchoring to purchase price as measure of cheap/expensive• Price action as element in fair value analysis

6. No attention to quality‐price tradeoff: buying cheap “crap” & overpaying for quality

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

Buying/Holding/Selling – Advice of top investors on how to trade different stock types

AVOID TRADEACTIVELY

BUY‐AND‐HOLD BUY‐AND‐WAIT

Emergingbusinesses

X ‐ ‐ ‐

Fast growers Undisciplinedwith leverage

‐ Buy late and sell early

‐

Stalwarts ‐ Buy cheap and sellafter 50% return

Decent market‐beating returns

‐

Slow growers X ‐ ‐ Special situations & turnarounds

Cyclicals Most investors X ‐ ‐

Turnarounds ‐ ‐ After turnaround if business great

X

Asset plays ‐ ‐ After asset realization if business great

X

Special situations

‐ ‐ After special situation priced in if business

great

X

Most top investors focus on limited number of stock types and avoid others (determined by personality and style)

Buying/Holding/Selling – Advice of top investors on how to trade different stock types

Textbook case of a turnaround – Thomas Cook

Distress, high uncertainty

Hopeful signs

Peter Lynch:• Wait when uncertainty too high

• Pounce when “hopefulsigns” line up

Source share prices: Yahoo finance

Buying/Holding/Selling – Advice of top investors on how to trade different stock types

Will Blackberry be PremWatsa’s turnaround story of then next few years?

Buying/Holding/Selling – General approach of top investors

Buying• High selectivity

• Patience• Gradual buying• Average down

Selling• Thesis invalidated

• Business not well understood• Price reaches fair value

• Replace with better bargain (dangerous!)• Gradual selling

Short selling• Are you up to the task?

• Proper risk management: stop losses & limit sizes• High selectivity

Buying/Holding/Selling – General approach of top investors

Example, International Coal (Prem Watsa)

Buying/Holding/Selling – Market cycles ‐Depression

Brutal market action of the Dow Jones between 1929 and 1932:

Only one in hundred survived the debacle of 1929‐1932 if one was not bearish in 1925.

‐‐‐Benjamin Graham

Buying/Holding/Selling – Market cycles ‐Depression

Buying/Holding/Selling – Market cycles ‐2008‐2009

Portrait of a smart and disciplined investor – PremWatsa

Watsa – not a a one hit wonder:(*) Annual compound growth in book value per share 1986‐2005: 28%(*) Successfully navigated market bubbles (Japan, technology crisis) prior to 2005

In 2007, a major U.S. bank CEO famously said ‘as long as the music is playing you have to get up and dance.’ After the Lehman bankruptcy in 2008, this same bank needed $45 billion from the U.S. government to continue in business. Expensive dance! We prefer to wait for the music to stop and

not depend on the kindness of strangers to be in business.‐‐‐PremWatsa

Buying/Holding/Selling – Market cycles ‐2008‐2009

Portrait of a smart and disciplined investor – PremWatsa – a detailed look

As an aside: Does this look like “déjà vu all over again” ? – PremWatsa

Buying/Holding/Selling – Market cycles ‐2008‐2009

Observations:• Economic growth since 2009 far below historical average in USA and Europe• Inflation steadily came down over past few years in Europe and USA; Europe close to deflation• Stock prices in USA at historically high valuations (in Shiller PE terms)

As they say, it is better to be wrong, wrong, wrong and then right than the other way

around!‐‐PremWatsa

Buying/Holding/Selling – Market cycles – 1970s

Stocks go nowhere; sentiment drifts down; inflation high (so real returns even negative); valuations move from expensive to extremely cheap

Buying/Holding/Selling – Market cycles – 1970s

How did the Superinvestors of Graham‐and‐Doddsville fare over the period ?

Buying/Holding/Selling – Market cycles – 1970s

Example, Warren Buffet:• 1969: could find no bargains in the market and therefore wound down his

investment partnership (kept only one deep‐value stock: textile company Berkshire Hathaway)

• 1974: around market bottom: “I feel like an oversexed man in a whorehouse”

How did they do it?

Focus on bargains (cheap stocks)

Ignore the sentiment of the

moment

Stay away from hot Nifty‐Fifty

stocks

Build cash in frothy markets

Get cash to work in bear markets

An investor should put money to work amidst the throes of a bear market, appreciating that things will likely get worse before they

get better.‐‐Seth Klarman

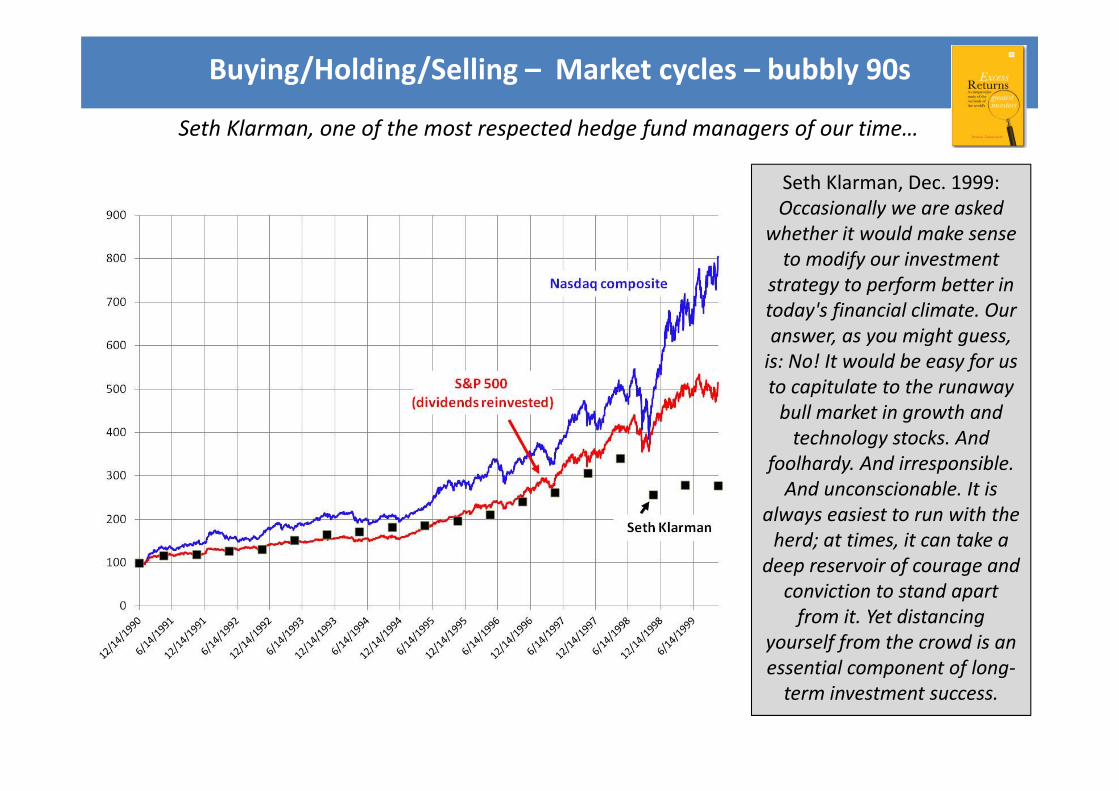

Buying/Holding/Selling – Market cycles – bubbly 90s

Buying/Holding/Selling – Market cycles – bubbly 90s

Would you entrust your money to these underperformers ???

Top investors refuse to participate in market folly and actually protect themselves against collapse:• Buffet: refuses to invest in technology stocks• Seth Klarman: hedges portfolio + moves into cheap small caps

Buying/Holding/Selling – Market cycles – bubbly 90s

Seth Klarman, one of the most respected hedge fund managers of our time…

Seth Klarman, Dec. 1999:Occasionally we are asked

whether it would make sense to modify our investment

strategy to perform better in today's financial climate. Our answer, as you might guess, is: No! It would be easy for us to capitulate to the runaway bull market in growth and technology stocks. And

foolhardy. And irresponsible. And unconscionable. It is

always easiest to run with the herd; at times, it can take a

deep reservoir of courage and conviction to stand apart from it. Yet distancing

yourself from the crowd is an essential component of long‐term investment success.

Buying/Holding/Selling – Market cycles – bubbly 90s

Well, you better would…

Top investors roar back with a vengeance and actually have positive performance throughout the collapse of the Nasdaq and S&P 500 !!!

Indicators for market turns:market sentiment + valuations

→ They are NOT afraid to underperform a few years and reap the profits a erwards

Top investors don’t try to time the market, often anticipate market turns years in advance…

Buying/Holding/Selling – Dealing with market cycles

Common Buying and Selling mistakes‐ some examples

Common practices among investors

Top Investors

Constantly trying to anticipate the moves of the

market

Far more money has been lost by investors preparing for correctionsor trying to anticipate corrections than has been lost in the

corrections themselves.‐‐‐Peter Lynch

Constantly trading in an attempt to take advantage of the market’s movements

Inactivity strikes us as intelligent behavior.‐‐‐Warren Buffet

Nobody has gone broke taking a profit.

Can you imagine a CEO using this phrase to urge his board to sell a star subsidiary?

‐‐‐Warren Buffet

Selling winners and hangingon to losing stocks

Selling winning stocks and hanging on to losing stocks is like cutting the flowers and watering the weeds.

‐‐‐Peter Lynch

Buying and selling based on emotion.

While enthusiasm may be necessary for great accomplishmentselsewhere on Wall Street it almost invariably leads to disaster.

‐Benjamin Graham

The economy as a first consideration

The way you lose money in the stock market is to start off with an economic picture. All these great heavy‐thinking deals kill you.

‐‐‐Peter Lynch

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

Risk versus return

Top investors deride academic view on risk, have unconventional view on risk:(*) volatility = opportunity to buy cheap(*) diversification = protection against ignorance(*) risk = lack of knowledge

To invest successfully, you need not understand beta, efficient markets, modern portfolio theory, option pricing or emerging markets. You may, in fact, be better off knowing nothing of these. Graham & Dodd investors, needless to say, do not discuss beta, the capital asset pricing model, or covariance in returns among securities. These are not subjects of any interest to them. In fact, most of them would have difficulty defining those terms. The investors simply focus on two variables: price

and value.‐‐‐Warren Buffet

Do not trust financial market risk models. Reality is always too complex to be accurately modeled. Attention to risk must be a 24/7/365 obsession, with people –not computers – assessing and reassessing the risk environment in real time. Despite the predilection of some analysts to model the financial markets using sophisticated mathematics, the markets are governed by behavioral science, not physical science.

‐‐‐Seth Klarman

Risk versus return – Basic tenets of top investors

The ten commandments of intelligent risk management

1) Do not participate in market folly – not even under the pressure of clients2) Be patient and tolerant of temporary underperformance3) Have the courage to accumulate cash when you can’t find bargains4) Have the courage to get cash to work when the market is in a tailspin5) Always insist on a margin of safety (i.e., buy cheap and sell when something is dear)6) Know what you hold (very) well7) First look at a stock’s downside (e.g., balance sheet); the upside will take care of itself8) Always be prepared for the unexpected (e.g., black swans)9) Use leverage sparingly (if at all)10) Always remember “If something is too good to be true, it probably isn’t.”

For people who do not adhere to these tenets:(*) diversification makes sense(*) volatility = risk(*) don’t ever think that you are investing !!!!

Risk versus return

Top investors exhibit excellent risk‐return ratios

Risk versus return – top investors protect against the downside

Limited number of down years + usually outperform when S&P 500 negative

Risk versus return – deviations from benchmark

Although they use the S&P 500 as a yardstick, they only compare themselves with that benchmark over several years (and take large annual deviations in their stride)

Risk versus return – deviations from benchmark

Let’s see how Buffett did versus the S&P 500 over his career:

Definitely no benchmark hugging here …

Risk versus return ‐ concentration

Example: Warren Buffet said in 2009 that if he would have been allowed by regulators he would

have seriously considered to go “all in” on Wells Fargo (a company he knows extremely well)in the depth of the credit crisis…

We agree with Mae West: “Too much of good thing can be

wonderful.”‐‐‐Warren Buffet

It is unwise to spread one’s funds over too many

different securities. Time and energy are required to come to a sound judgment of an investment and to keep abreast of the forces that may change the value

of a security. ‐‐‐Bernard Baruch

Not the first time:• 1951: bulk of Buffet’s portfolio in GEICO

• 1964: 40% of Buffet’s portfolio in American Express

• Challenge to the Efficent Market Hypothesis• The Investment Philosophy• Effectiveness of sound investing• The Investment Process

(*) Finding Bargains(*) Due Diligence(*) Common mistakes

• Buying and selling(*) Stock types(*) Market cycles(*) Common mistakes

• Risk versus return• The intelligent investor

Overview

The intelligent investor

Newton lost a time‐adjusted $3 million in the South Sea bubble; After this traumatizingexperience, he forbade anyone to speak the words “South Sea” in his presence…

Are smart people automatically intelligent investors ?

Newton: probably the greatest genius that ever

lived…

The Intelligent Investor

What does it take to be a successful investor ?

Right mental setup

Hard work

Passion

Right Attitude

+

+

+

Investor Intelligence

A winning combination: Warren Buffet

Without Investor Intelligence

Newton

Intellectual Intelligence (IQ)

Let me emphasize that it does not take a genius or even superior talent to be successful as a value analyst. What it needs first is, reasonable

intelligence; second, sound principles of operation; third, and most

important, firmness of character.‐‐‐ Benjamin Graham

I have heard many men talk intelligently, even brilliantly, about something – only to see them proven powerless when it comes to acting on what they believe. Investors must act in time.

‐‐‐ Bernard Baruch

Edward Thorpe, 1991: review of the Maddoff hedge fund for client

The intelligent investor ‐ Example

His findings: • Returns inconsistent with trading strategy

• Suspicious:(*) Trade confirmation statements: friend of Madoff(*) Information technology: brother of Madoff; Edward not alllowed to visit premises

• Ghost option trades:(*) Many options didn’t trade on transaction dates(*) Option prices on statements impossible (different from actual trade prices)

• Madoff’s organization could not be identified as counterparty to purported trades

Edward Thorpe exposed the Ponzi scheme 18 years before its self‐destruction by going the extra mile…

→ Advises client to get out (doesn’t bother to inform the SEC as they showed little interest in fraud cases at that time)