bookkeeping - u.s. career...

TRANSCRIPT

Explore the possibilities

BookkeepingInstruction Pack 1 Lessons 1-6

0201202LB01B-64

Bookkeeping

Instruction Pack 1

Lesson 1: Getting Started: Course Introduction and Overview

Lesson 2: Bookkeeping ExplainedLesson 3: Bookkeeping EquationsLesson 4: The Accounting CycleLesson 5: The Journal and Entry SystemsLesson 6: The Ledger

No part of this document may be reproduced or transmitted in any form or by any means, electronic or mechanical, for any purpose, without the express written permission of U.S. Career Institute.

Copyright © 2014, Weston Distance Learning, Inc. All Rights Reserved. 0201202LB01B-64

AcknowledgmentsAuthorsRobert James

Editorial StaffKimberly FieldsChristine DunlapElizabeth MunsonBrian KaufmanCarolina TownsendKaryn Madison

Design/LayoutConnie HunsaderSandy PetersenJessica Babb-Raymundo

U.S. Career InstituteFort Collins, CO 80525

www.uscareerinstitute.edu

0201202LB01B-64 III

Table of Contents

Lesson 1: Getting Started: Course Introduction and OverviewStep 1: Learning Objectives for Lesson 1...................................................................................................................... 1Step 2: Lesson Preview.................................................................................................................................................... 1Step 3: Where You Can Work ........................................................................................................................................ 2Step 4: The Importance of Bookkeeping ...................................................................................................................... 2Step 5: A Career in Bookkeeping .................................................................................................................................. 3Step 6: U.S. Career Institute’s Bookkeeping Course ...........................................................................................................5Step 7: Practice Exercise 1-1 ........................................................................................................................................... 6Step 8: Review Practice Exercise 1-1 ............................................................................................................................. 6Step 9: Lesson Summary ................................................................................................................................................. 6Step 10: Quiz 1 ................................................................................................................................................................. 6

Lesson 2: Bookkeeping ExplainedStep 1: Learning Objectives for Lesson 2...................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 2Step 4: Record of Transaction ........................................................................................................................................ 2

The Journal—Debits and Credits ................................................................................................................... 3Two Financial Statements ................................................................................................................................ 4

Step 5: Practice Exercise 2-1 ........................................................................................................................................... 7Step 6: Review Practice Exercise 2-1 ............................................................................................................................. 7Step 7: Define Some Common Terms .......................................................................................................................... 8

Classifying Assets ............................................................................................................................................. 8Classifying Liabilities ....................................................................................................................................... 9

Step 8: Practice Exercise 2-2 ......................................................................................................................................... 10Step 9: Review Practice Exercise 2-2 ........................................................................................................................... 10Step 10: Lesson Summary ............................................................................................................................................. 10Step 11: Quiz 2 ............................................................................................................................................................... 11

0201202LB01B-64

Bookkeeping

IV

Lesson 3: Bookkeeping EquationsStep 1: Learning Objectives for Lesson 3...................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 1Step 4: Accounting Equation.......................................................................................................................................... 2Step 5: Balance Sheets ..................................................................................................................................................... 4Step 6: Practice Exercise 3-1 ........................................................................................................................................... 5

About Forms for Practice Exercises ............................................................................................................... 6Step 7: Review Practice Exercise 3-1 ............................................................................................................................. 6Step 8: Net Income Equation ......................................................................................................................................... 6Step 9: Practice Exercise 3-2 ........................................................................................................................................... 7Step 10: Review Practice Exercise 3-2 ........................................................................................................................... 7Step 11: Income Statement ............................................................................................................................................. 8Step 12: Practice Exercise 3-3 ........................................................................................................................................ 9Step 13: Review Practice Exercise 3-3 ........................................................................................................................... 9Step 14: Lesson Summary ............................................................................................................................................... 9Step 15: Quiz 3 ............................................................................................................................................................... 10

Lesson 4: The Accounting CycleStep 1: Learning Objectives for Lesson 4...................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 1Step 4: Eight Parts of the Accounting Cycle ................................................................................................................. 2

The Transaction ................................................................................................................................................ 4The Journal ........................................................................................................................................................ 4

Step 5: Practice Exercise 4-1 ........................................................................................................................................... 5Step 6: Review Practice Exercise 4-1 ............................................................................................................................. 5Step 7: The Double-entry System .................................................................................................................................. 6Step 8: Practice Exercise 4-2 ......................................................................................................................................... 10Step 9: Review Practice Exercise 4-2 ........................................................................................................................... 11Step 10: The Ledger ....................................................................................................................................................... 11

Posting and the Ledger .................................................................................................................................. 12Step 11: Practice Exercise 4-3 ...................................................................................................................................... 13Step 12: Review Practice Exercise 4-3 ......................................................................................................................... 14Step 13: Trial Balance .................................................................................................................................................... 14

0201202LB01B-64

Table of Contents

V

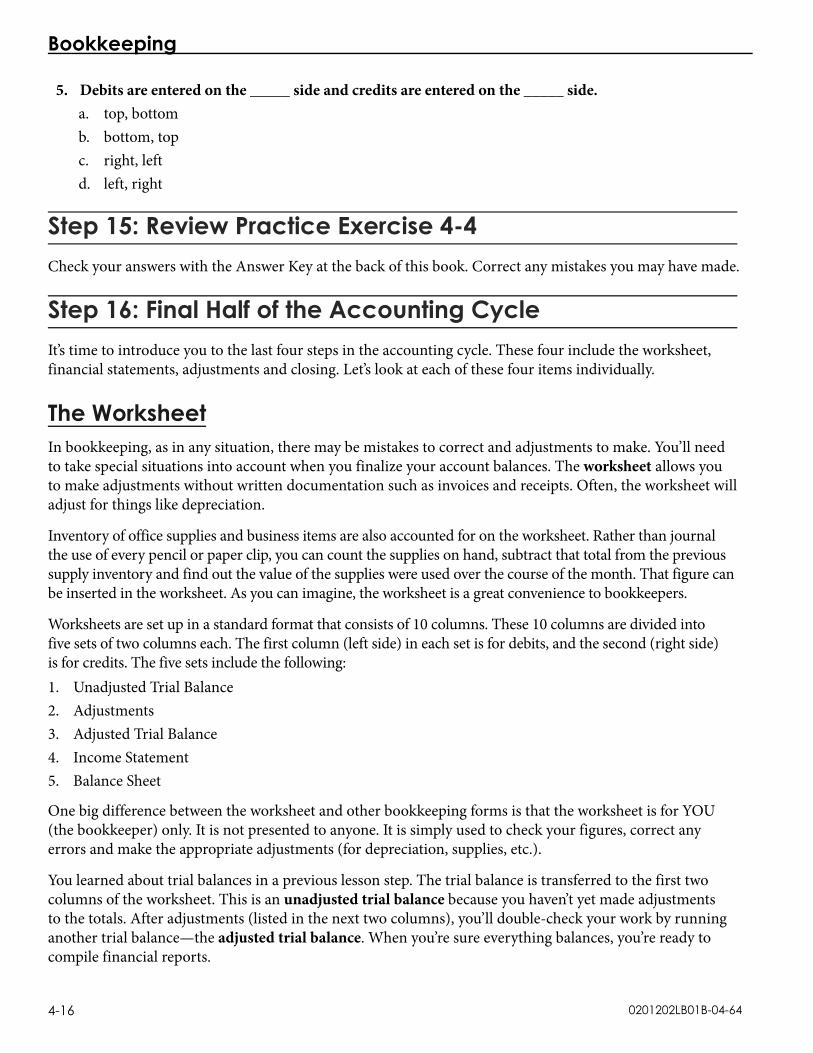

Step 14: Practice Exercise 4-4 ...................................................................................................................................... 15Step 15: Review Practice Exercise 4-4 ......................................................................................................................... 16Step 16: Final Half of the Accounting Cycle .............................................................................................................. 16

The Worksheet ................................................................................................................................................ 16Financial Statements ...................................................................................................................................... 17Adjustments..................................................................................................................................................... 17Closing the Books ........................................................................................................................................... 17

Step 17: Practice Exercise 4-5 ...................................................................................................................................... 18Step 18: Review Practice Exercise 4-5 ......................................................................................................................... 19Step 19: Lesson Summary ............................................................................................................................................. 19Step 20: Quiz 4 ............................................................................................................................................................... 19

Lesson 5: The Journal and Entry SystemsStep 1: Learning Objectives for Lesson 5...................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Need to Know .................................................................................................................................. 1Step 4: Book of Original Entry ...................................................................................................................................... 2

Constructing the Journal ................................................................................................................................. 2Debits and Credits ............................................................................................................................................ 3

Step 5: Practice Exercise 5-1 ........................................................................................................................................... 5Step 6: Review Practice Exercise 5-1 ............................................................................................................................. 5Step 7: Normal Account Balances ................................................................................................................................. 6Step 8: Practice Exercise 5-2 ........................................................................................................................................... 6Step 9: Review Practice Exercise 5-2 ............................................................................................................................. 6Step 10: Double-entry System of Accounting .............................................................................................................. 7Step 11: Practice Exercise 5-3 ...................................................................................................................................... 14Step 12: Review Practice Exercise 5-3 ......................................................................................................................... 15Step 13: Journalizing ..................................................................................................................................................... 15Step 14: Practice Exercise 5-4 ...................................................................................................................................... 18Step 15: Review Practice Exercise 5-4 ......................................................................................................................... 19Step 16: Lesson Summary ............................................................................................................................................. 19Step 17: Quiz 5 ............................................................................................................................................................... 19

Lesson 6: The LedgerStep 1: Learning Objectives for Lesson 6...................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 1

0201202LB01B-64

Bookkeeping

VI

Step 4: Comparing the Ledger and Journal .................................................................................................................. 2The Ledger Format ........................................................................................................................................... 2Constructing the Ledger .................................................................................................................................. 2

Step 5: Practice Exercise 6-1 ........................................................................................................................................... 4Step 6: Review Practice Exercise 6-1 ............................................................................................................................. 4Step 7: Account Numbers and Titles ............................................................................................................................. 5

Numbers ............................................................................................................................................................ 5Titles ................................................................................................................................................................... 6

Step 8: Practice Exercise 6-2 ........................................................................................................................................... 6Step 9: Review Practice Exercise 6-2 ............................................................................................................................. 6Step 10: Practice Exercise 6-3 ........................................................................................................................................ 7Step 11: Review Practice Exercise 6-3 ........................................................................................................................... 7Step 12: Posting and Referencing .................................................................................................................................. 8Step 13: Practice Exercise 6-4 ...................................................................................................................................... 11Step 14: Review Practice Exercise 6-4 ......................................................................................................................... 13Step 15: Trial Balance .................................................................................................................................................... 13Step 16: Practice Exercise 6-5 ...................................................................................................................................... 15Step 17: Review Practice Exercise 6-5 ......................................................................................................................... 15Step 18: Practice Exercise 6-6 ...................................................................................................................................... 15Step 19: Review Practice Exercise 6-6 ......................................................................................................................... 16Step 20: Finding and Correcting Errors ..................................................................................................................... 16Step 21: Practice Exercise 6-7 ...................................................................................................................................... 17Step 22: Review Practice Exercise 6-7 ......................................................................................................................... 17Step 23: Lesson Summary ............................................................................................................................................. 17Step 24: Quiz 6 ............................................................................................................................................................... 17

Answer KeyLesson 1 ............................................................................................................................................................................ 1

Practice Exercise 1-1 ........................................................................................................................................ 1Lesson 2 ............................................................................................................................................................................ 1

Practice Exercise 2-1 ........................................................................................................................................ 1Practice Exercise 2-2 ........................................................................................................................................ 2

Lesson 3 ............................................................................................................................................................................ 3Practice Exercise 3-1 ........................................................................................................................................ 3Practice Exercise 3-2 ........................................................................................................................................ 4Practice Exercise 3-3 ........................................................................................................................................ 4

0201202LB01B-64

Table of Contents

VII

Lesson 4 ............................................................................................................................................................................ 5Practice Exercise 4-1 ........................................................................................................................................ 5Practice Exercise 4-2 ........................................................................................................................................ 5Practice Exercise 4-3 ........................................................................................................................................ 6Practice Exercise 4-4 ........................................................................................................................................ 6Practice Exercise 4-5 ........................................................................................................................................ 6

Lesson 5 ............................................................................................................................................................................ 7Practice Exercise 5-1 ........................................................................................................................................ 7Practice Exercise 5-2 ........................................................................................................................................ 8Practice Exercise 5-3 ........................................................................................................................................ 8Practice Exercise 5-4 ........................................................................................................................................ 9

Lesson 6 .......................................................................................................................................................................... 11Practice Exercise 6-1 ...................................................................................................................................... 11Practice Exercise 6-2 ...................................................................................................................................... 11Practice Exercise 6-3 ...................................................................................................................................... 11Practice Exercise 6-4 ...................................................................................................................................... 12Practice Exercise 6-4 Continued .................................................................................................................. 13Practice Exercise 6-4 Continued .................................................................................................................. 14Practice Exercise 6-4 Continued .................................................................................................................. 15Practice Exercise 6-4 Continued .................................................................................................................. 16Practice Exercise 6-4 Continued .................................................................................................................. 17Practice Exercise 6-4 Continued .................................................................................................................. 18Practice Exercise 6-4 Continued .................................................................................................................. 19Practice Exercise 6-5 ...................................................................................................................................... 20Practice Exercise 6-5 Continued .................................................................................................................. 21Practice Exercise 6-5 Continued .................................................................................................................. 22Practice Exercise 6-5 Continued .................................................................................................................. 23Practice Exercise 6-5 Continued .................................................................................................................. 24Practice Exercise 6-5 Continued .................................................................................................................. 25Practice Exercise 6-5 Continued .................................................................................................................. 26Practice Exercise 6-5 Continued .................................................................................................................. 27Practice Exercise 6-6 ...................................................................................................................................... 28Practice Exercise 6-7 ...................................................................................................................................... 28

0201202LB01B-64

Bookkeeping

VIII

Course ObjectivesThe Bookkeeping Course prepares a student for an entry-level position in an accounting department or firm while enabling the student to effectively manage individual finances. Students learn the basic elements and concepts of maintaining journals and ledgers, as well as how to maintain and process the steps in the accounting cycle, including basic elements of accounts payable, accounts receivable and financial report preparation. Additionally, students learn about computerized bookkeeping and computerized personal finance.

This course trains students to:

● Manage individual finances.

● Perform competent, entry-level bookkeeping skills.

● Set up and manage a home-based bookkeeping.

Lesson 1 Getting Started:

Course Introduction and Overview

Welcome to U.S. Career Institute’s Bookkeeping Course! Congratulations on your decision to become a professional bookkeeper. As a professional bookkeeper, you’ll possess valuable skills that are very much in demand. This course will show you the ins and outs of bookkeeping and will give you the skills you need to work as a professional bookkeeper in a business or—if you choose—to establish and market your own bookkeeping business.

We make your course work easy to follow. Work through each lesson at your own pace by following the step-by-step instructions. And remember, if you have any questions, be sure to call our student support line. Our students are the most important asset we have.

Step 1: Learning Objectives for Lesson 1After completing the instruction in this lesson, you will be trained to do the following:

● Describe situations where bookkeeping skills are needed.

● Explain how U.S. Career Institute’s Bookeeping Course works and what you can expect in every lesson. (For example, the format of each lesson will be the same, step-by-step instruction.)

● Determine the skills you will need to begin working as a professional bookkeeper.

● Identify employment and business opportunities for a professional bookkeeper.

Step 2: Lesson PreviewWhat is bookkeeping? It is a skill needed by many—small business persons and individuals at home all need to know how much money they have. You will begin your journey toward the mastery of these skills here in Lesson 1. It is a lesson designed to show you the big picture of bookkeeping—from an introduction to people who need bookkeeping to an overview of the skills you will need to be a successful professional bookkeeper.

0201202LB01B-01-64

Bookkeeping

1-2

Step 3: Where You Can WorkYour career as a professional bookkeeper means that you can work for a wide variety of businesses. Your local ice cream store, doggie daycare and hair salons all have employees. That means they need you to handle their payroll.

Who pays taxes? Everyone! You’ve heard the saying that the only certain things in life are death and taxes? And everyone hates doing their own taxes, so they’ll love it when you show up at their door with the right skills.

Do you want to work in a business? If you are someone who likes variety, you could become a bookkeeping professional who gets different jobs through temporary agencies. Or you could work in the corporate offices of a chain of sub sandwich shops.

What about keeping sales and purchase records for a nail salon, small restaurant or coffee shop? The gas station, bookstore or kitchenware store?

Maybe you want to stay home, see the kids off to school, settle in for a second cup of coffee, and tackle the accounts of different clients.

If you don’t want to work for a business, advertise yourself to individuals. Maybe you have a desire to help a certain group of people? You can advertise your services at a discount rate for low-income, senior citizens who need help doing their income taxes.

It’s up to you! This course will provide you with the basic skills to begin your career in a wide choice of settings. Congratulations on making a great choice to improve your future!

Step 4: The Importance of BookkeepingDo you like to eat out in nice restaurants? Ever wonder why some restaurants succeed and others fail? You may have watched a favorite restaurant go out of business and wondered how great food and service didn’t result in long-term success. As a future bookkeeping professional, you might be pleased to learn that the difference-maker is often the bookkeeper!

Picture the owner of a small restaurant. This owner knows food. She knows the most scrumptious ways to prepare beef and potatoes. She knows the best supplier with the freshest ingredients. She also knows she is not an expert in finances. Because she is a smart businessperson, she brings in someone who is a bookkeeping professional. She makes her money by being a great cook, and she pays out a little of that money to a professional bookkeeper, who keeps track of the finances for her. Because she doesn’t have to worry about calculations, she can concentrate on making her scrumptious beef dishes.

The restaurant owner’s bookkeeper performs many important tasks. She keeps track of the payroll records (how much each employee earned). She tabulates expenses (which keeps the beef supplier happy!). She records daily, monthly and yearly income. And she compiles and submits tax records so that the restaurant owner—and the Internal Revenue Service (IRS)—are satisfied.

And after all these records are put together, this bookkeeping professional presents the restaurant owner a year-end report that reveals the bottom line: what her business is worth. This enables the owner to plan for the next year.

0201202LB01B-01-64

Getting Started: Course Introduction and Overivew

1-3

Now consider the restaurant across the street—a gourmet Italian place with wonderful pasta and cannoli. The cook is terrific. The atmosphere is grand. But the books are shambles! You see, this restaurant owner knows the best ways to cook linguine, but he “doesn’t know noodles” about keeping accurate records! Instead of paying a professional bookkeeper, the restaurant owner tried to save a few dollars by keeping his own records. Now, his suppliers are mad because they haven’t been paid. His employees are confused because their tax forms (you’ll learn about Form W-2 later) are inaccurate. Worse, the Internal Revenue Service is planning an audit of the restaurant, and the owner can’t produce accurate records of his accounts.

The first restaurant owner recognized the value of a good bookkeeper. The second restaurant owner made the mistake many people do. He tried to do a job he didn’t know enough about. If he had taken this course, he would have known about the importance of bookkeeping and the services available to him through a bookkeeping professional.

This course will not show you the most scrumptious ways to cook beef or make you an excellent Italian cook, but it will certainly teach you the necessary skills to keep the businessperson satisfied that his or her records are accurate.

Business people are not the only ones who need a good bookkeeper. Many individuals find it difficult to keep track of finances. Some have mortgages and even rental property they must keep track of. Others would gladly pay someone just to balance their checkbook or reconcile bank accounts for them. As a professional bookkeeper, you can offer your services to virtually anyone who handles money or other assets.

Step 5: A Career in BookkeepingSo what do professional bookkeepers do exactly? Bookkeepers keep track of “the books”—the financial records for a business. In short, they prepare and examine financial records. They take raw information like sales receipts and time cards and turn that information into data that organizations can use to make smart business decisions.

The duties of a bookkeeper include the following:

● Inspect account books and systems for efficiency and for proper accepted procedures.

● Organize and maintain financial records.

● Examine financial statements for accuracy and for compliance with the law.

● Prepare tax liability information and tax forms in a timely fashion.

Bookkeeping is often a full-time profession, with nearly a fifth of the work force working more than 40 hours per week. Bookkeeping is somewhat seasonal—the end of the business year requires a large number of additional forms and reports, which means that the bookkeeper has her hands full!

What kind of person makes a good bookkeeper? Probably the single most important attribute of a successful professional bookkeeper is attention to detail. You’ll soon discover that bookkeeping is built on accuracy. Imagine a builder who erects a five-story building. Now imagine that the bottom floor was poorly constructed. It doesn’t matter how well-built the next four floors are. If the bottom floor is structurally weak, the whole building is in danger.

Like the builder, a bookkeeper depends on accurate work to ensure that the reports that are created out of that work aren’t built on “shaky ground.” Bookkeepers are fanatics for detail and precision.

0201202LB01B-01-64

Bookkeeping

1-4

Bookkeepers are good at analytical thinking. Are you logical? Can you analyze a problem and come to a reasonable decision? If so, then bookkeeping might be perfect for you!

Bookkeeping professionals are independent. Bookkeeping is a job that’s done without much supervision. The job requires developing one’s own methods and routines. If you like the responsibility of being self-directed, you may love bookkeeping!

And bookkeeping requires integrity. Businesses need honest, ethical evaluations of their situations and practices.

Another way of looking at a career in bookkeeping is to spend a day with a real-world bookkeeper. Judith is a bookkeeper for a Colorado oil drilling firm with offices in several other states. How does she spend her time?

“I start with e-mails,” she notes. With oil wells in Colorado, Montana, Wyoming and the Dakotas, Judith has to keep track of operations and employees hundreds of miles away. Luckily, computer technology allows her to keep in touch in several ways, including the phone, fax and computer.

Early in her daily routine, Judith addresses invoices that arrive in the mail. “Invoices have to be journalized,” she explains. (Journalizing is something you’ll learn about in Lesson 2.) Not every letter has an invoice—some contain checks! “I code the checks and log them in the ledger” (something else you’ll learn early in your course). “Then I run a report to see what bills need to be paid. I cut checks, have them signed by the operations manager and then head to the post office and the bank.”

Because oil drilling is a rough job, Judith’s company has a lot of employee turnover. New hires have to be processed. Terminated employees need to have their paperwork brought up to date and closed. The oil company sends employees from state to state, depending on which rig needs help the most. Each rig has its own paperwork. Payroll is a complicated job! Luckily, Judith is detail-oriented, and able to keep up with the job’s demands.

Sometime during the day, Judith prints off a general ledger account to see how the month is shaping up. She has a logical mind, and she understands what she’s looking at, so if there’s a mistake anywhere, she spots it. The combination of proper training, a little experience and an analytical mind all come into play as she scans for errors that might haunt her later if she doesn’t catch them right away!

The end of the month is approaching. The company’s accountant reviews that information and compiles it in monthly reports. Judith has to do the preparatory work to help her compile those reports. Doing a little bit of work every day helps keep her from suffering a monthly time-crunch!

Just as Judith is about to take a lunch break, the boss pokes his head in her office and asks for a certain report. He’s trying to evaluate the company’s gas credit policies, and wonders how many credit cards are in use and which employee has which card. If Judith had been casual in her approach to the day, this request might have thrown her off schedule. Luckily, Judith is self-directed, and allows extra time for management requests. In her business, she’s learned that those requests are the rule, rather than the exception!

When running the report, she realizes that some of the credit cards are unaccounted for. This is a security issue, and she’s quick to report the situation to her boss. Because bookkeepers handle the company’s money, they are very sensitive to issues that involve ethics or security.

0201202LB01B-01-64

Getting Started: Course Introduction and Overivew

1-5

Judith’s afternoon is taken up with inventory concerns. The oil company has dozens of work vehicles, from fuel trucks to heavy equipment. Some are in use. Others are “in the shop” for maintenance and repairs. Keeping track of everything is a major endeavor. Luckily, Judith had a hand in selecting inventory management software, and she understands how to get the most out of the company’s tracking efforts. She sends an e-mail to the Montana supervisor, listing two trucks that are overdue for engine maintenance.

And so Judith finishes her day as it began—on the computer with her e-mails. A number of late hires have been reported. She notes that tomorrow will begin with new hire paperwork. And she’ll want to get her accounts receivable and accounts payable ledgers up-to-date. It seems that a bookkeeper’s work is never done. That’s just fine with Judith—a busy day is a challenging day! “I just love coming to work,” Judith explains. “It’s never dull, never the same and what I do makes a difference for everyone who works for my company.”

Can you see yourself in an office position, helping to determine the financial fate of a company? Perhaps you see yourself working from home, with a number of interesting clients. Either way, a career in bookkeeping may be your path to fulfilling success!

Step 6: U.S. Career Institute’s Bookkeeping CourseYou will be glad you decided to enroll in U.S. Career Institute’s Bookkeeping Course. We are the home study experts with more than 30 years of experience!

Some courses simply give you a book about the subject, but we walk you through each new lesson, one step at a time. This course is designed by both experienced educators and accounting experts so that you get the best of both worlds—a wealth of up-to-date bookkeeping knowledge presented in a fun, easy-to-understand format. If you have any questions, answers are just a phone call away. Use the student support line to reach our knowledgeable staff and get all the one-on-one help you need.

Numbers are the core of the bookkeeping profession. Because of that, we’ve included a math supplement with this course that will help you brush up on the skills you need.

As you move through the lessons in this Bookkeeping Course, you will find yourself becoming knowledgeable about every aspect of bookkeeping. You will be able to read and use the ledger and journal. The concepts of assets and capital will become second nature to you, as will checking accounts and the reconciliation process. You’ll understand the difference between debits and credits, and you’ll learn how to use these items. You’ll learn how to calculate payroll, handle tax issues, create balance sheets, and much more!

When you have completed this course, you will be ready to begin work as a professional bookkeeper, either in a company or organization, or by starting your own bookkeeping business from your home. If you decide to begin your own at-home business, this course will teach you how to get started, obtain clients and put you on the road to success.

Each lesson uses the same, step-by-step instruction so you don’t have to learn everything at once. Work at your own pace. Take the Practice Exercises to gauge your progress. Most importantly, dive in and have fun!

When most people think of numbers, they think of confusing scribbles on a blackboard. But professional bookkeepers see numbers differently. Numbers tell stories—stories of transactions, stories of businesses, stories of wealth. Some of the greatest success stories in history are written in numbers and pretty soon, not only will you be able to read those stories, you’re going to help write them!

0201202LB01B-01-64

Bookkeeping

1-6

Once again, congratulations on taking this first step toward an exciting, new career. You are on your way to becoming a qualified professional bookkeeper.

Step 7: Practice Exercise 1-1Read the following statements. For each statement below, write True or False on scratch paper.

1. Professional bookkeepers are independent and must have integrity.

2. Businesses such as restaurants can benefit from having an accurate bookkeeper.

3. Tax records and payroll records are NOT kept by a professional bookkeeper.

4. Accurate records are essential to the success of a business.

5. Individuals rarely have any use for a professional bookkeeper.

Step 8: Review Practice Exercise 1-1Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

Step 9: Lesson SummaryThis lesson introduced you to bookkeeping—both the career and your course. You discovered the kinds of businesses that need bookkeeping, including nearly every business in the marketplace! You learned that you will have a choice between working for a company as a professional bookkeeper, or setting up your own home business to provide bookkeeping services to small businesses, from bookstores to gas stations. And you learned just how important bookkeeping is. Without the information and regulatory assistance provided by bookkeepers, organizations would not be able to make good, solid business decisions.

You explored the characteristics that successful bookkeeping professionals have, and then followed Judith—a real-world bookkeeper for an oil company—through her busy workday. Along the way, you had a chance to see those success characteristics in action. As a professional bookkeeper, you will face your own fast-paced challenges.

In the next lesson, we’ll dive right into bookkeeping. You’ll be introduced to the journal and two of the most important financial reports. But first, test your understanding of the material so far by taking your first graded Quiz.

Step 10: Quiz 1Once you’ve mastered the course content, locate this Quiz in your Assignment Pack. Read and follow the Quiz instructions carefully.

Lesson 2Bookkeeping Explained

Step 1: Learning Objectives for Lesson 2After completing the instruction in this lesson, you will be trained to do the following:

● Explain what the record of transaction is and how it relates to bookkeeping.

● Distinguish between assets and liabilities, and explain how each one fits into the record of transaction.

● Define many of the most common terms used in bookkeeping.

Step 2: Lesson PreviewOne hundred years ago, in a small general store, bookkeeping simply meant writing down what was sold each day and counting the cash in the drawer. Today, a business’ finances are far more complex, requiring an expert to handle them—a professional bookkeeper. Taken as a whole, managing a business’ books may seem daunting at first, but by focusing on small, easy-to-master steps, you’ll soon become an expert. The secret to handling complicated financial matters as a professional bookkeeper is the consistent, careful, and diligent use of basic accounting principles.

In this lesson, you will begin to understand these principles—the foundation of your successful career in bookkeeping. A word of caution: You will be introduced to many new phrases and terms in this lesson. However, you do not have to have them all perfectly memorized or be able to completely understand how they all fit together. This will come with practice in later lessons. For now, focus on the big picture!

0201202LB01B-02-64

Bookkeeping

2-2

Step 3: Terms You Will Need to KnowHere are the bookkeeping terms you will learn about in this lesson:

● accounts

● accounts payable

● accounts receivable

● assets

● balance sheet

● buildings

● capital

● cash

● credit (Cr)

● current assets

● current liabilities

● debit (Dr)

● double-entry accounting

● equipment

● equity

● expenses

● financial reports

● fixed assets

● general ledger

● income statement

● journal

● land

● liquidity

● long-term liabilities

● net income

● net loss

● net worth

● posting

● prepaid expenses

● revenue

● supplies

● transaction

Step 4: Record of TransactionAny business dealing that involves money is called a transaction. As a professional bookkeeper, you will be responsible for keeping track of the transactions your clients conduct. You will keep the record of transaction. There are many examples of transactions in business.

● When a restaurant owner pays for supplies, that is a transaction.

● When an employee collects a paycheck, that is a transaction.

● Consumers make transactions by purchasing goods and services.

Transactions are recorded in a journal. The journal is the starting point for a bookkeeping system.

Suppose that you have a pile of loose coins—some pennies, nickels, dimes and quarters. You might sort those coins into a tray, putting pennies with pennies and nickels with nickels. When you were finished, you might write down the amount of each denomination. That written report would tell you how much money you had altogether.

0201202LB01B-02-64

Bookkeeping Explained

2-3

The journal is like that pile of unsorted coins; only the journal has unsorted transactions of all types. Like sorting coins into a tray, the bookkeeper transfers information from the journal to accounts in the general ledger. This sorting and recording process is called posting. Then, the bookkeeper uses the accounts to compile financial reports that tell business owners how much money they have altogether.

JOURNAL ACCOUNTS REPORTS

Let’s take a closer look at the first step in bookkeeping: the journal.

The Journal—Debits and CreditsAlthough we will cover the journal in more detail in a future lesson, there are some components to the journal you need to know now. First, there are Debits and Credits. Actually, debits and credits are essential to nearly all parts of the bookkeeping process, but the first time you will use these two items is in the journal. Every bookkeeping entry will be either a debit or credit. A debit is always entered in the left-hand column and a credit is in the right-hand column (Figure 2-1).

Company NameGeneral Journal

1 2Date Description P/R Dr Cr

12345

Figure 2-1: General Journal

At the top of the journal page, you’ll find the name of the company. You’ll also find a column for the Date and a space for the Description of each transaction you record. For example, suppose the restaurant you work for bought a supply of steaks from a purveyor. You would list the date of the invoice and list the specific accounts that were affected by the transaction in the description space.

The column marked 1 is the left-hand column, reserved for debits. (Dr is the accepted abbreviation for debits.) The column marked 2 is the right-hand column, reserved for credits. (Cr is the accepted abbreviation for credits.)

You might wonder, what’s the difference between debits and credits? Why split transactions into debits and credits anyway? All modern accounting is called double-entry accounting. An easy way to understand double-entry is to imagine that you own a lemonade stand. Suppose you sell a glass of lemonade to a passerby. Two things happen from that single transaction. First, your total sales go up. And, your total cash-on-hand goes up. Two accounts (Revenue and Cash) are affected by one transaction. The tricky part is this—one entry must be a credit, and one must be a debit to keep your accounts in balance.

0201202LB01B-02-64

Bookkeeping

2-4

Confused? Don’t worry. You’ll learn all you need to know about credits and debits in future lessons. For now, understand that each transaction is listed in the journal twice—once as a debit and once as a credit. From there, the information will be transferred into accounts in the general ledger. Finally, the information will be processed into financial reports. Those financial reports will provide a summary of the financial condition of the business.

Two Financial StatementsAfter you post to the accounts the information in your journal, you use this information to prepare various financial statements or reports. The first two kinds we will talk about are the balance sheet and the income statement.

The balance sheet is a summary of the business’ assets, liabilities and equity. Assets are what the business owns, such as vehicles and inventory. Liabilities include what the business owes, such as loans and accounts payable. Equity consists of what would remain of the assets if all the liabilities were paid.

Look at the balance sheet example of Jerry’s TV Repair (figure 2-2). Jerry Silver owns his own television repair shop. His assets include a delivery van, his repair tools, five televisions he has for sale (inventory), the spare parts in his shop and the money in the cash register and the bank. He also has an accounts receivable (people who owe him money) set-up that is also an asset. The breakdown of assets is as follows:

Cash $ 1,000Accounts Rec. 250Van 12,500Tools 1,500Televisions 1,500Parts 800Total: $17,550

Now, the TV repair shop also has some liabilities. Jerry buys parts from a local supplier. The supplier allows Jerry to buy the parts he needs and then bills Jerry later for his purchases. This arrangement is known as accounts payable. The money that is owed to the supplier is a liability. The company also owes the bank for a loan on the van. Basically, the company’s liabilities break down like this:

Notes Payable: 10,400Accounts Payable: 1,400Total: $11,800

0201202LB01B-02-64

Bookkeeping Explained

2-5

Jerry’s Computer Repair Balance Sheet July 31, 20XX

ASSETS LIABILITIES

CURRENT ASSETS SHORT-TERM LIABILITIES Cash $1,000 Accounts Payable $1,400 Accounts Rec. 250 Total Short-Term Liabilities $1,400 Inventory 1,500 Parts 800 LONG-TERM LIABILITIES Total Current Assets $3,550 Notes Payable $10,400 Total Long-Term Liabilities $10,400FIXED ASSETS Van $12,500 Tools 1,500 TOTAL LIABILITIES $11,800 Total Fixed Assets $14,000 EQUITY Owner’s Equity $5,750 Total Capital $5,750

TOTAL ASSETS $17,550 TOTAL LIABILITIES AND CAPITAL $17,550

Figure 2-2: Balance Sheet

If we look at these numbers, we can determine the equity in Jerry’s TV Repair. The formula for equity is Assets – Liabilities = Equity. Equity is sometimes called capital or net worth. For now, we will refer to it as equity. So, let’s figure the equity Jerry has in his business. Take his assets ($17,550) and subtract his liabilities ($11,800). What is the answer? Jerry has $5,750 worth of equity in his business. Or another way of saying this is Jerry’s TV Repair has a net worth of $5,750.

Overall, a business’ assets include such things as:

● buildings, land, equipment, tools, cash (both on hand and in the bank), accounts receivable, inventories, materials and spare parts.

Liabilities include:

● accounts payable (money owed to suppliers), payroll due (what the company owes its employees), loans and mortgage payments.

You will learn how to prepare a balance sheet in a future lesson. You will also learn how to create an operating statement. The income statement (also called a profit-and-loss statement) shows expenses subtracted from income for a specific length of time (a month or year, for example). This statement shows whether or not a business is turning a profit.

0201202LB01B-02-64

Bookkeeping

2-6

You just learned that the balance sheet is a summary of assets, liabilities and capital. An income statement is a summary of a company’s revenues, expenses and net income. Revenue is the process of collecting monies in exchange for goods and services. Expenses include those items that are used or needed to produce revenue. Net income consists of what’s left over after the expenses have been subtracted from the revenue. If for some reason expenses are greater than revenue, then the company has a net loss—that is, the company lost money.

Let’s look at an example of an operating statement, so you can see how these terms and concepts fit together. Jerry’s Computer Repair is a small, one-man operation. Jerry fixes computers (a service). He also sells refurbished computers (goods). Because Jerry sells goods as well as services, he has two revenue accounts. They are as follows:

Sales Revenue: $2,000Service Revenue: 1,000Total: $3,000

Jerry also has several expense accounts. They are as follows:Advertising Expense: $100Fuel Expense: 200Salary Expense: 500Utilities Expense: 50Total: $850

In simple terms, Jerry took in more money than he spent. That is, his revenues were greater than his expenses. So, Jerry made a profit—his net income was $2,150.

Jerry’s Computer Repair

Income Statement

July 31, 20XX

REVENUESSales Revenue $2,000Service Revenue 1,000 Total Revenues $3,000

EXPENSESAdvertising Expense $100Fuel Expense 200Salary Expense 500Utilities Expense 50 Total Expenses $850

NET INCOME $2,150

Figure 2-3: Income Statement

0201202LB01B-02-64

Bookkeeping Explained

2-7

Step 5: Practice Exercise 2-1Select the best single answer for the following items. Write your answers on scratch paper.

1. As a professional bookkeeper, you keep track of your client’s transactions. The first place these are recorded are in the _____.a. profit-and-loss statementb. journalc. balance sheetd. income statement

2. Debits are always entered in the _____ column while credits are entered in the _____ column.a. left-hand/right-handb. right-hand/left-handc. bottom/topd. top/bottom

3. “Posting” refers to _____.a. figuring a company’s net worthb. balancing debits and creditsc. transferring journal information to the correct accountsd. creating the operating statement

For the following questions, identify the following items as either assets or liabilities. Write your answers on scratch paper.

Joan’s Trucking has the following items as assets and liabilities. Classify them accordingly. Write assets for question 4 and liabilities for question 5.

15 delivery trucks Mortgage for warehouse Warehouse

Wages owned to drivers 35 spare tires Forklift

$20,000 in the bank Two computers Loan balance on 15 trucks

$50 owed to suppliers $200 owed to credit card company

Step 6: Review Practice Exercise 2-1Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

0201202LB01B-02-64

Bookkeeping

2-8

Step 7: Define Some Common TermsNow let’s talk a little more about assets and liabilities. You’ve already learned what those two terms mean, but here you’ll learn the different classifications of assets and liabilities.

Classifying AssetsAssets, as you learned earlier in this lesson, are what the business owns. They can be classified into two categories: Current Assets and Fixed Assets.

Current AssetsCurrent assets are assets that constantly change. On the balance sheet, list them according to how fast they can be converted to cash. This conversion is called liquidity. So, logically, the first current asset a company has is its cash. From there, it descends according to an asset’s liquidity. Overall, current assets are items that will either become cash soon (they are intended for sale), or they will be used by the business within a year. Here is an example list of current assets.

● Cash: This is the company’s total of dollars, coins, money orders, checks, letters of credit and bank drafts that it has on hand or in accessible bank accounts. Examples of accessible bank accounts (also called demand accounts) include checking and a normal savings account. Certificates of deposit and mutual funds typically are NOT demand accounts.

● Accounts Receivable: The amount of money customers owe the company for goods or services purchased but not yet paid for.

● Inventory: The dollar value of goods a company has in stock (for sale).

● Supplies: Materials used in the daily conducting of business. These include office supplies and store supplies.

● Prepaid Expenses: Items the company has purchased and paid for, but not received yet (insurance, for example).

Now that you have an idea what current assets are, let’s look at the second type of assets: Fixed Assets.

Fixed AssetsFixed assets are what the business uses to produce its product or service. This includes everything from a computer system for producing invoices to a truck used to transport the finished product. Basically, if an item puts the product together, transports the product or is used by people producing the product, it is considered a fixed asset.

0201202LB01B-02-64

Bookkeeping Explained

2-9

Fixed Assets include the following items:

● Land: The value of land owned by the company (figured at actual purchase price).

● Buildings: The purchase price or construction costs of all structures owned by the company. This includes permit fees, engineering fees and surveys.

● Equipment: Machines and vehicles along with interior structures, such as shelving and office furniture.

Like assets, liabilities are also classified into different categories.

Classifying LiabilitiesLiabilities are put into one of two categories: current and long-term. Current liabilities must be paid within the current year. Long-term liabilities are, logically, those liabilities to be paid after the current year.

Payroll, the company’s accounts payable (to creditors for supplies, for example) and short-term loans are examples of current liabilities.

Long-term liabilities include mortgage payments and long-term loans.

BookkeepingImagine a jar, full to the top with loose change. How much money is in there? To guess the total, take a random sample of coins to see how many are pennies, nickels, dimes, quarters or halves. Then calculate the total volume of coinage by multiplying the jar’s circumference by the height of the jar. (Of course, some of the space is taken up by air. You can fill the jar with water, dump the water out and measure it separately and then subtract the water volume from the total volume to get pure “coin volume.”) Worse, each coin denomination is a different size. You’d have to set up a ratio that accounts for the coin denomination’s size versus its relative presence in the jar. Armed with that information, you could multiply the estimate of the total number of each coin type by that coin’s value and then total the values.

Or you could count the money. Bookkeepers count.

Bookkeeping professionals make sense of financial information for clients. They do this by recording and organizing transactions. They examine assets and liabilities. Armed with this complex information, they deliver their findings in useful, easy-to-understand reports. And grateful clients are spared having to “guess” how their business is doing!

Before we wrap up this lesson, let’s pause for a Practice Exercise.

0201202LB01B-02-64

Bookkeeping

2-10

Step 8: Practice Exercise 2-2Match the account with the proper classification. Write your answers on scratch paper.

1. Cash a. Current assetb. Fixed assetc. Current liabilityd. Long-term liability

2. Accounts Payable

3. Equipment

4. Inventory

5. Mortgage Payable (30 years)

6. Accounts Receivable

7. Land

8. Payroll

9. Loan Payable (less than 1 year)

10. Prepaid Insurance

11. Building

Step 9: Review Practice Exercise 2-2Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

Step 10: Lesson SummaryThis lesson introduced you to the transaction—the starting point for all bookkeeping activity. You learned that bookkeeping is a process of recording and interpreting all of the transactions that a company makes. Recording transactions happens in the journal. You were introduced to debits and credits—a way of ordering transaction information. Interpreting transactions happens in financial reports. You were introduced to two of them—the income statement and the balance sheet. The income statement tells a business what their net income was for a given period of time. The balance sheet is a financial “snapshot” of a business, including assets (what the business owns), liabilities (what the company owes) and owner’s equity (the actual value of the business.)

0201202LB01B-02-64

Bookkeeping Explained

2-11

Then, you took a deeper look at assets and liabilities. You differentiated current and long-term liabilities. You learned about different kinds of assets, including fixed assets and current assets. And, you had a chance to practice making the proper asset and liability classifications.

Along the way, you were introduced to a number of terms that you will find useful in your journey to a career in accounting.

In the next lesson, you’re going to learn about the accounting equation, the foundation for everything you’ll do as an accountant. But first, take the graded Quiz to see how well you understand the material so far.

Step 11: Quiz 2Once you’ve mastered the course content, locate this Quiz in your Assignment Pack. Read and follow the Quiz instructions carefully.

0201202LB01B-02-64

Bookkeeping

2-12

Lesson 3Bookkeeping Equations

Step 1: Learning Objectives for Lesson 3After completing the instruction in this lesson, you will be trained to do the following:

● Define and use the accounting equation.

● Fill out balance sheets.

● Define and use the net income equation.

● Prepare income statements.

Step 2: Lesson PreviewIn this lesson, you’ll learn all about the accounting equation. This single equation is the foundation of modern bookkeping—the starting point for everything you’re going to learn in this course. Sound intimidating? Don’t worry—the equation is simple and easy to remember.

The accounting equation has to do with the relationship between assets, liabilities and capital. From this relationship, double-entry accounting was created. (You received a brief introduction to double-entry accounting in the last lesson.) And, certain financial statements are based directly on the same accounting equation.

What’s the best way to learn? By doing! Roll up your sleeves because you’re about to crunch your first set of numbers. You’re going to use the accounting equation to prepare simple balance sheets and operating statements. This lesson marks the beginning of your career as a professional bookkeeper!

Step 3: Terms You Will Need to KnowHere are the accounting services terms you will learn about in this lesson:

● accounting equation

● initial capital

● net income equation

● sales revenue

● service revenue

0201202LB01B-03-64

Bookkeeping

3-2

Step 4: Accounting EquationThe accounting equation is the basis of all bookkeeping activity. This equation shows the relationship between assets, liability and equity. Assets, you remember from Lesson 2, are what a business owns. (For example, restaurants own ovens, grills, refrigerators and food.) Liabilities consist of what the business owes. (For example, our restaurant owes for utilities and the labor it uses, as well as loans on the building and equipment.) And equity is the ownership in any asset after all debts associated with the asset are paid off. (For example, suppose the restaurant has a delivery truck worth $15,000. If you still owe $10,000, then your equity in the truck is $5,000.)

These principles establish the accounting equation:

Assets = Liabilities + Equity

Or

A = L + E

In the example of the delivery truck, the equation reads like this:

Truck Value ($15,000) = Amount Still Owed ($10,000) + Equity ($5,000)

Like any equation, the accounting equation can be switched around to solve for other variables. For example, in Lesson 2 you learned that equity equals asset value minus liabilities:

Equity = Assets – Liabilities

Or

E = A – L

This is just a restatement of the accounting equation. In the case of the delivery truck, suppose you want to know how much equity you have. The equation says you have $5,000 equity in the truck because the truck is worth $15,000, but you still owe $10,000.

Here’s another form of the same equation:

Liabilities = Assets – Equity

Or

L = A – E

Suppose you know the truck is worth $15,000. Your bookkeeper says you have $5,000 equity in the truck. How much do you still owe? According to the equation, you still owe another $10,000 (because assets minus equity is $15,000 - $5,000).

As you can see, these are all forms of the same basic equation. If you want to learn one form right away, memorize A = L + E. Knowing this form of the accounting equation will help you understand double-entry accounting, especially debits and credits.

0201202LB01B-03-64

Bookkeeping Equations

3-3

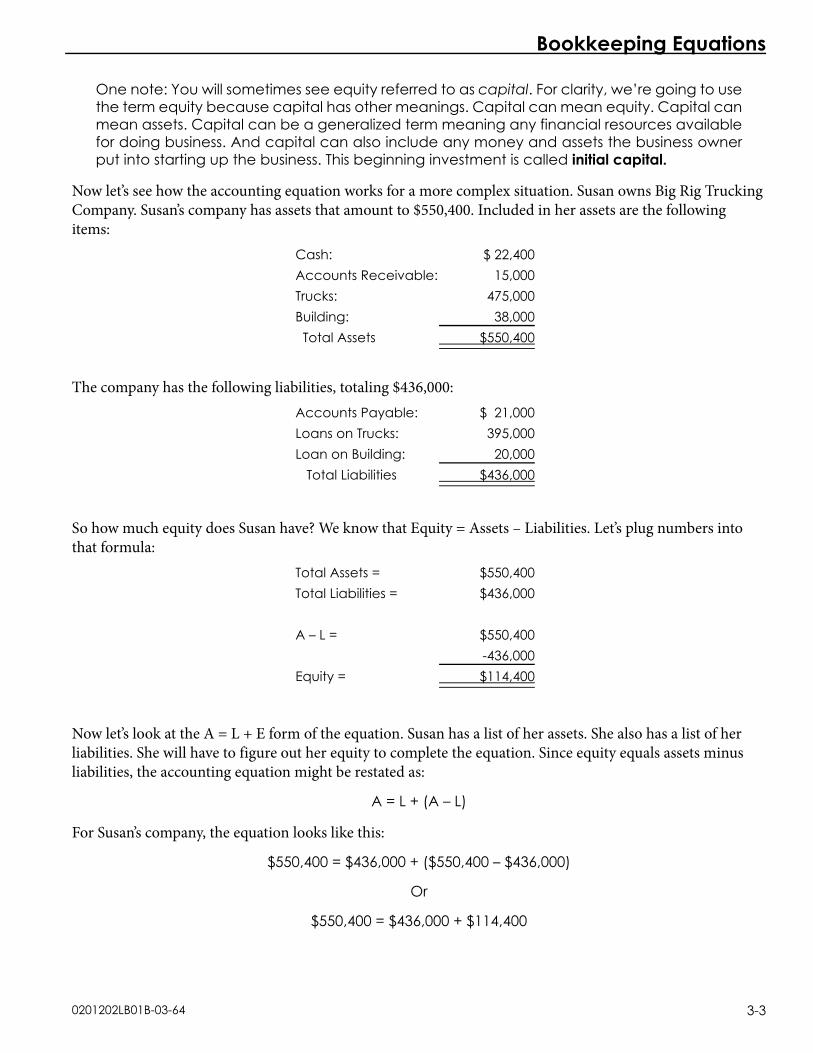

One note: You will sometimes see equity referred to as capital. For clarity, we’re going to use the term equity because capital has other meanings. Capital can mean equity. Capital can mean assets. Capital can be a generalized term meaning any financial resources available for doing business. And capital can also include any money and assets the business owner put into starting up the business. This beginning investment is called initial capital.

Now let’s see how the accounting equation works for a more complex situation. Susan owns Big Rig Trucking Company. Susan’s company has assets that amount to $550,400. Included in her assets are the following items:

Cash: $ 22,400Accounts Receivable: 15,000Trucks: 475,000Building: 38,000 Total Assets $550,400

The company has the following liabilities, totaling $436,000:Accounts Payable: $ 21,000Loans on Trucks: 395,000Loan on Building: 20,000 Total Liabilities $436,000

So how much equity does Susan have? We know that Equity = Assets – Liabilities. Let’s plug numbers into that formula:

Total Assets = $550,400Total Liabilities = $436,000

A – L = $550,400 -436,000Equity = $114,400

Now let’s look at the A = L + E form of the equation. Susan has a list of her assets. She also has a list of her liabilities. She will have to figure out her equity to complete the equation. Since equity equals assets minus liabilities, the accounting equation might be restated as:

A = L + (A – L)

For Susan’s company, the equation looks like this:

$550,400 = $436,000 + ($550,400 – $436,000)

Or

$550,400 = $436,000 + $114,400

0201202LB01B-03-64

Bookkeeping

3-4

The accounting equation will help you check for errors, since the equation must be in balance. If the numbers don’t balance, then you may have made an error when tabulating assets and liabilities.

Let’s see if our trucking company’s accounting equation balances. $550,400 = $436,000 + $114,400$550,400 = $550,400

Yes, it does.

What does that tell us? It tells us we have accurately figured the company’s assets, liabilities and capital. Once we have established that, we can take the next step in bookkeeping: filling out a balance sheet.

Step 5: Balance SheetsThe balance sheet summarizes assets, liabilities and equity in a standard format. The report is organized in the same way every time you use it. Assets go in the left column. Liabilities and capital go in the right column. This left-right format mirrors the accounting equation. Look at this example from Billy Bob’s Donut Shoppe (Figure 3-1).

Billy Bob’s Donut Shoppe Balance Sheet July 31, 20XX

ASSETS LIABILITIES

CURRENT ASSETS SHORT-TERM LIABILITIES Cash $22,500 Accnts Payable $7,900 Inventory 3,000 Wages Payable 4,000 Accnts Rec. 950 Notes Payable 5,750 Insurance 500 Total Current Liabilities $17,650 Total Current Assets $26,950 FIXED ASSETS LONG-TERM LIABILITIES Building $25,000 Mortgage $16,500 Van 17,000 Van Loan 8,000 Donut Oven 2,500 Total Long-Term Liabilities $24,500 Display Cases 1,000 Total Liabilities $42,150 Total Fixed Assets $45,500 EQUITY Owner’s Equity $30,300 Total Equity $30,300

TOTAL ASSETS $72,450 TOTAL LIABILITIES and EQUITY $72,450

Figure 3-1: Balance Sheet

0201202LB01B-03-64

Bookkeeping Equations

3-5

As you can see, the asset side of the balance sheet is equal to the liabilities and equity side. That’s why this particular report is called a “balance sheet”—as with the equation, the left side must equal the right side. If the assets balance with the liabilities and equity, you are well on your way to keeping accurate books.

Assets = Liabilities + Equity

Initial capital can be handled as both an asset and as equity. How can it be both? Let’s see how this works. Suppose your first step in starting the company is to put a check for $10,000 in the company bank account. According to the equation, you have an asset worth $10,000. You have no liabilities. And, your equity is $10,000. So, our equation balances:

A = L + E

$10,000 = $0 + $10,000

Did you notice that the capital deposit is listed twice? That’s the basis of double-entry accounting. One transaction—entered twice to keep the equation in balance. You’ll learn more about this in a future lesson!

$14,000 = $0 + $14,000

Use the following Practice Exercise to sharpen your accounting equation and balance sheet skills.

Step 6: Practice Exercise 3-1Set up and complete the balance sheet for Jill’s Stained Glass (Figure 3-2).

Jill’s Stained Glass has the following items. Classify them in the appropriate place on the balance sheet and then complete the balance sheet. (You can find the balance sheet in your Forms for Practice Exercies under Practice Exercise 3-1.)

Building: $40,500 Accounts Receivable: $250 Cash: $2,750 Accounts Payable: $14,750 Mortgage: $22,500

0201202LB01B-03-64

Bookkeeping

3-6

Jill s Stained Glass has the following items. Classify them in the appropriate place on the balance sheet and then complete the balance sheet.

Building: $40,500Accounts Receivable: $250Cash: $2,750Accounts Payable: $14,750Mortgage: $22,500

Jill’s Stained GlassBalance SheetJuly 31, 20XX

ASSETS LIABILITIES

CURRENT ASSETS CURRENT LIABILITIES (1) _________________ $_________ (7) ____________________ $______ (2) _________________ _________ Total Current Liabilities (8) $ ______ Inventory 2,500 Total Current Assets (3) $_______

FIXED ASSETS LONG-TERM LIABILITIES (4) _________________ $_________ (9) ____________________ $______ Equipment 1,250 Total Long-Term Liabilities (10) ______ Total Fixed Assets (5) $_______ _______ Total Liabilities (11) ______

EQUITY Owner’s Equity $10,000 Total Equity $10,000

TOTAL ASSETS (6) $_______ TOTAL LIABILITIES and EQUITY (12) $______

Figure 3-2: Practice Exercise 3-1 Balance SheetFigure 3-2: Balance Sheet

About Forms for Practice ExercisesThe completion of some Practice Exercises requires special forms. You will find a packet of required forms called Forms for Practice Exercises in your original course shipment. You can also find a downloadable, PDF version on the Student Web Site. The first form in the packet is a chart you’ll need for Practice Exercise 3-1!

Step 7: Review Practice Exercise 3-1Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

Balance sheets may vary slightly depending on the type of business you keep books for. If it is a sales business (a retail store, for example), the balance sheet might be a little different than if it is a service business.

Step 8: Net Income EquationImagine being a business person. What’s the most important thing to know about your business? Is it where your competition is? Maybe. But most likely, the most important thing about your business is the profit: How much money is the company making? The net income equation is the way to find out how much money a business is making.

0201202LB01B-03-64

Bookkeeping Equations

3-7

Very simply, the net income equation states that Revenue – Expenses = Net Income. Revenue refers to what money a business makes—the earnings of a company. The revenue can come from selling merchandise or from selling time and talent. When you sell a product, it is referred to as sales revenue. When you sell a talent or time, that is called service revenue.

Expenses are the cost of doing business. Salaries, rent, commissions and even gasoline for the company’s fleet of cars all qualify as expenses. In fact, anything purchased for use by the business in a business-related manner is considered an expense.

When you subtract expenses from revenue, you are left with the net income for a company. Net income is not exactly the same as profit. Profit could be either gross profit or net profit (something you’ll learn about in a future lesson). Net income is just that—net. Net income is what’s left after all expenses have been paid. It is sometimes called “the bottom line” because net income appears on the bottom of the page on an income report.

Let’s look at a simple example. Susan’s trucking company had service revenue of $18,000 last month. And, she had sales revenue of $2,000. Her total revenue for the month was $20,000.

Susan’s expenses included rent ($2,000), fuel ($4,000), salaries ($9,000) and office expenses ($1,000). Her total expenses were $16,000.

So, her net income was $4,000 (revenue minus expenses; $20,000 - $16,000).

Try a couple examples of this equation in the following Practice Exercise.

Step 9: Practice Exercise 3-2Answer the following questions on a sheet of scratch paper.

1. If Jon’s Tree Service needs $5,250 to operate each week and it brings in $12,250 each week, what is the company’s net income?

2. Harold’s Hardware pays out $22,350 in expenses every month. The company brings in $14,000 in service revenue and $50,000 in sales revenue during the same amount of time. What is Harold’s Hardware’s net income?

3. Rondell’s Thrift Shop makes $22,000 each month, but it costs Rondell $16,000 each month to keep the shop open. Now, if Rondell’s salaries in April cause his expenses to rise to $19,000, what is his shop’s net income for that month? What is his net income during each of the other 11 months of the year?

4. Sharon owns a beauty shop. The shop cuts through its competition and makes $35,000 each month. It is located in a popular mall, and it costs Sharon $27,000 each month to keep the shop open. What is Sharon’s net income?

Step 10: Review Practice Exercise 3-2Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

0201202LB01B-03-64

Bookkeeping

3-8