books & records in the audit...

TRANSCRIPT

The Devil is in the Details:Books & Records in the Audit Context

Presented by:

James Santivañez

JMS Advisory Group, LLC

Troy Wangen

True Partners Consulting LLC

UPPO Presentation Disclaimer

Use of the Unclaimed Property Professionals Organization, Inc., (UPPO) name of copyrighted materials in this presentation does not constitute an endorsement by UPPO of a member, vendor, product or service. The content represents the opinions of the author and not necessarily those of UPPO. This information is not intended as legal advice and should not be used to replace the advice of legal counsel.

UPPO Antitrust Statement

UPPO has a policy of strict compliance with U.S. federal antitrust laws.

UPPO members and/or meeting attendees cannot come to understandings, make agreements, or otherwise concur on positions or understandings, make agreements, or otherwise concur on positions or activities that in any way tend to raise, lower or stabilize prices or fees. Members and/or attendees can discuss pricing models, methods, systems, and applications, as well as certain cost matters that do not lead to an agreement or consensus on prices or fees to be charged. However, there can be no discussion as to what constitutes a reasonable, fair or appropriate price or fee to charge for any service or product.

Information may be presented with regard to historical pricing activities so long as such information is general in nature and does not include data on current prices or fees being charged in any trade area. Any discussion of current or future prices, fees, discounting, and other terms and conditions of sale, which may lead to an agreement or consensus on prices or fees to be charged, is strictly prohibited.

Today’s Agenda

• Why are records important?

• Typical Audit Requests

• What should a holder consider for “COMPLETE” records?

– General Ledger, Disbursements, A/R

• Current Estimation Methodology

• The Proof is in the Lawsuits

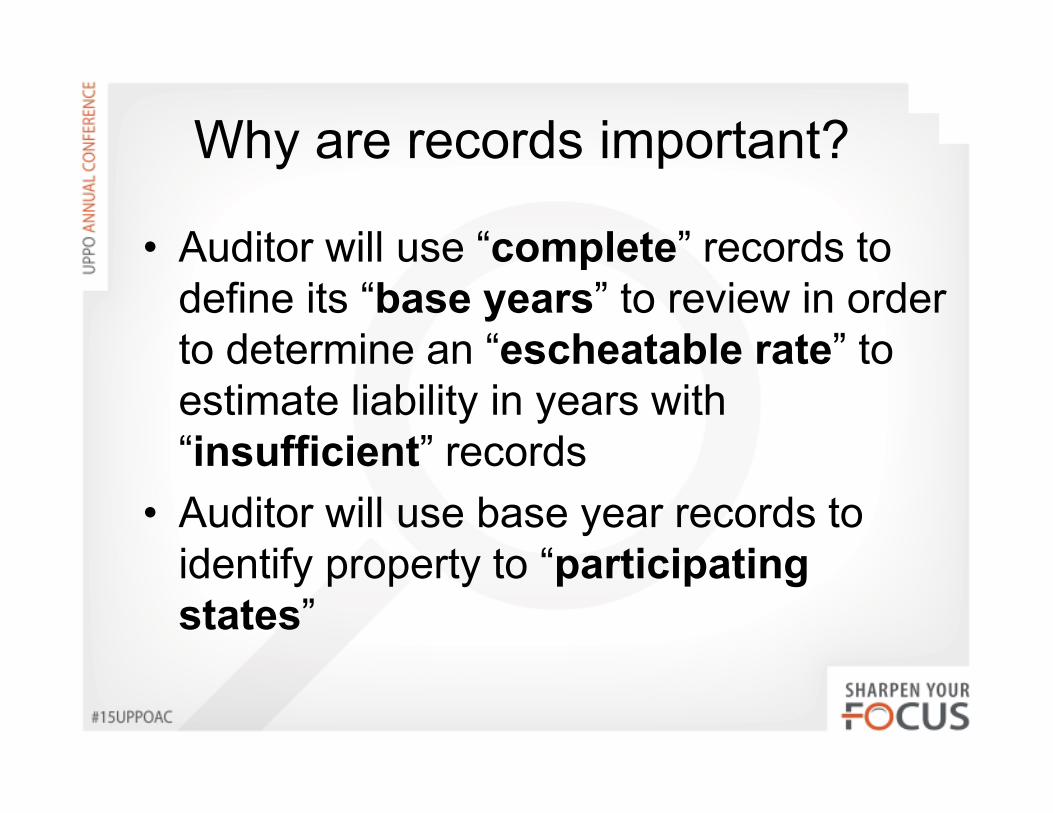

Why are records important?

• Auditor will use “complete” records to define its “base years” to review in order to determine an “escheatable rate” to estimate liability in years with “insufficient” records

• Auditor will use base year records to identify property to “participating states”

Why are records important?

• Burden of Proof rests with the HOLDER

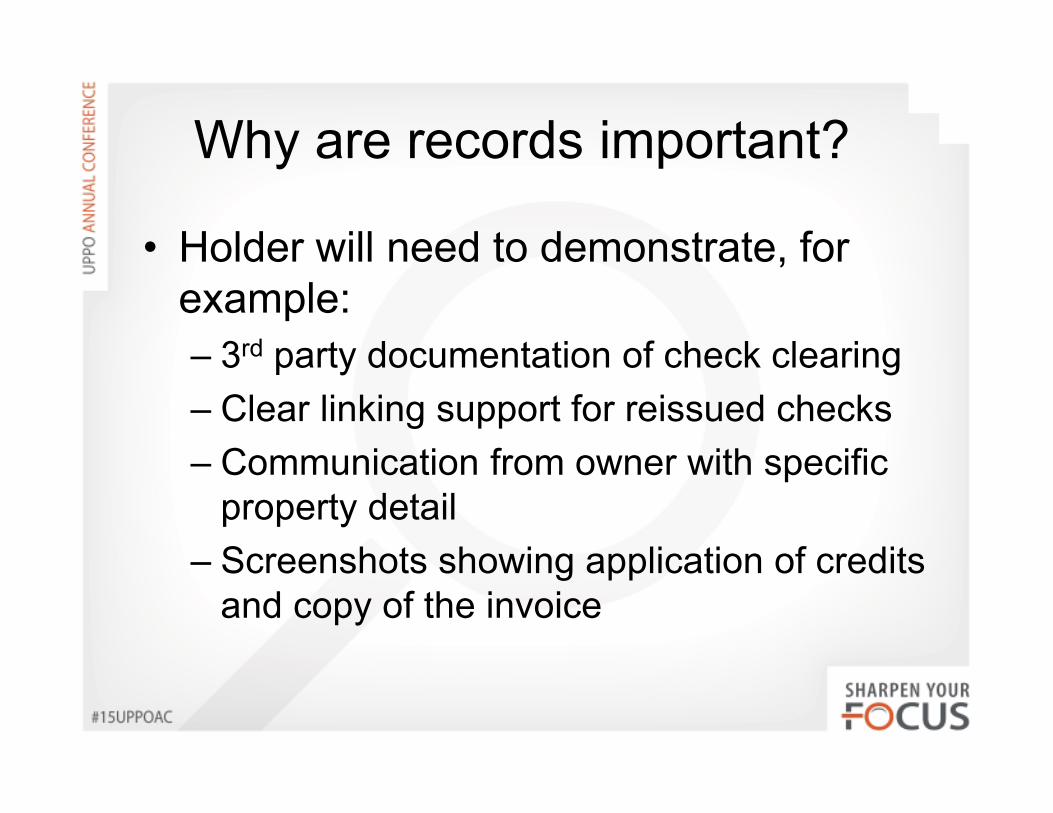

Why are records important?

• Holder will need to demonstrate, for example:

– 3rd party documentation of check clearing

– Clear linking support for reissued checks

– Communication from owner with specific property detail

– Screenshots showing application of credits and copy of the invoice

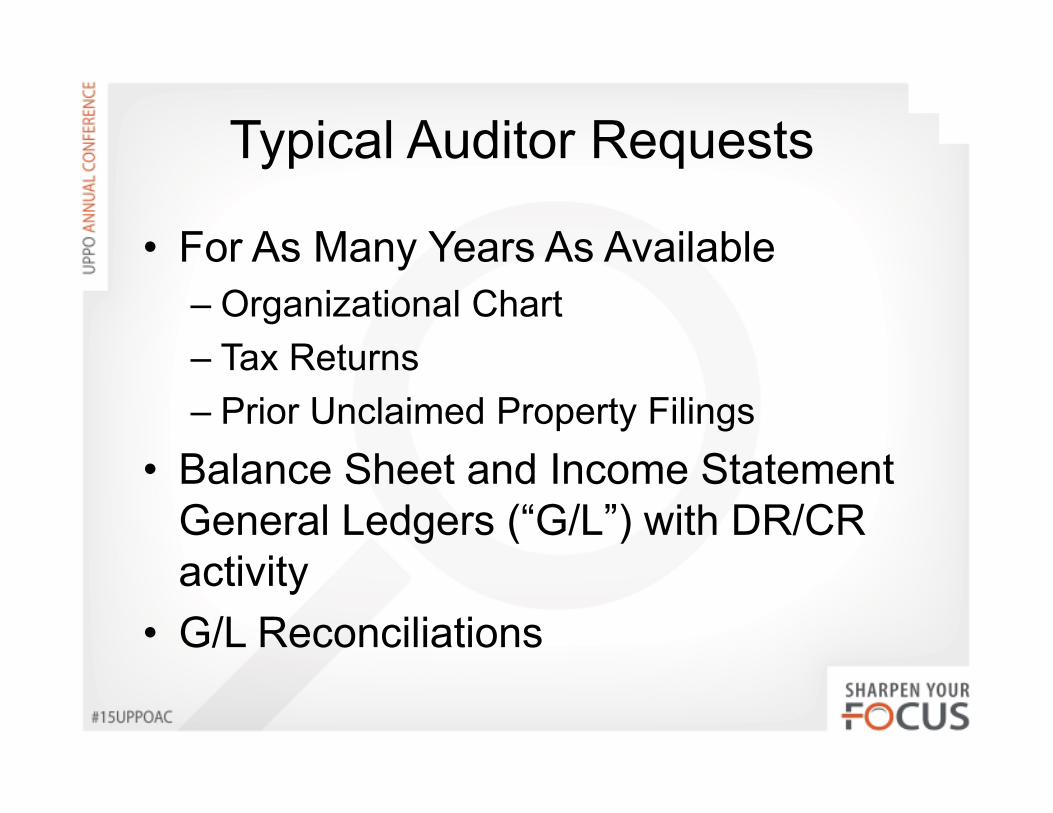

Typical Auditor Requests

• For As Many Years As Available

– Organizational Chart

– Tax Returns

– Prior Unclaimed Property Filings

• Balance Sheet and Income Statement General Ledgers (“G/L”) with DR/CR activity

• G/L Reconciliations

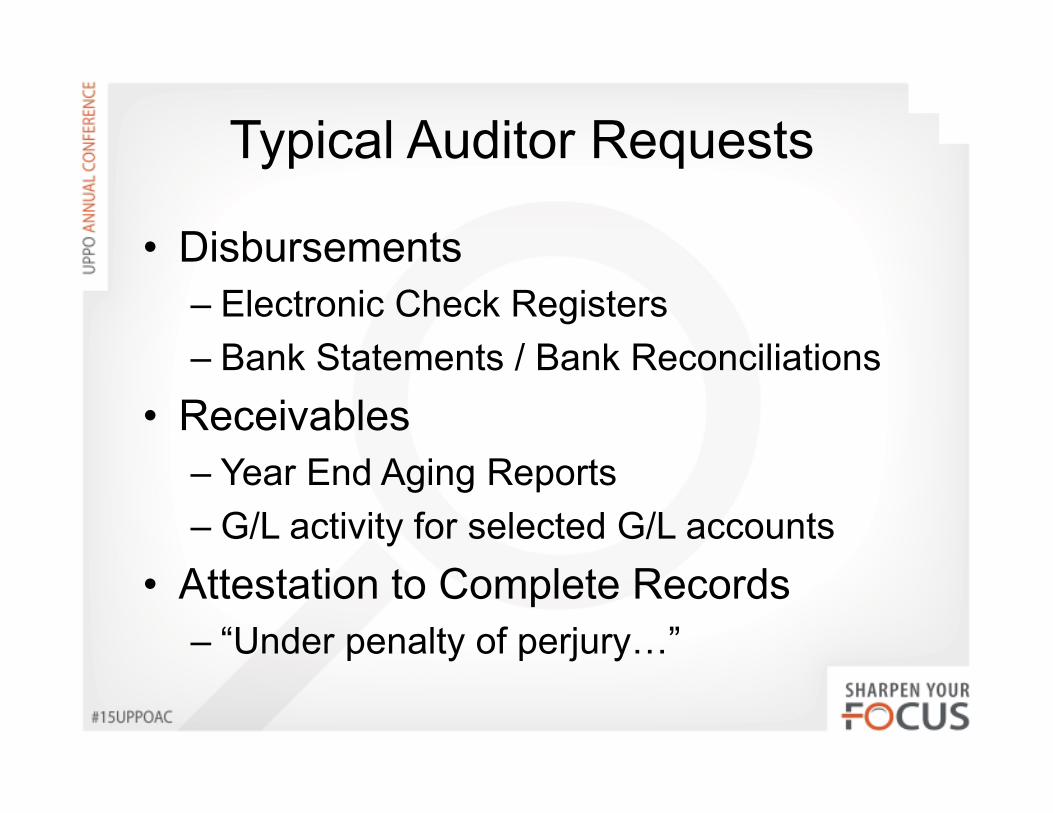

Typical Auditor Requests

• Disbursements

– Electronic Check Registers

– Bank Statements / Bank Reconciliations

• Receivables

– Year End Aging Reports

– G/L activity for selected G/L accounts

• Attestation to Complete Records

– “Under penalty of perjury?”

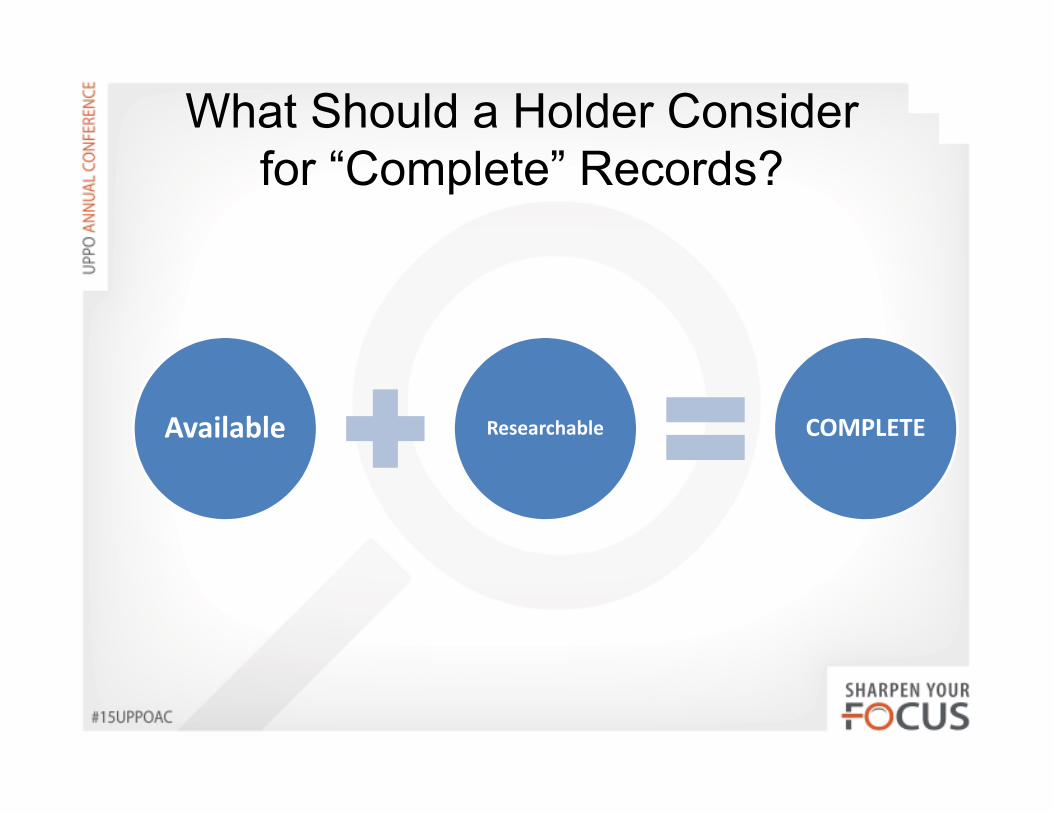

What Should a Holder Consider for “Complete” Records?

Available Researchable COMPLETE

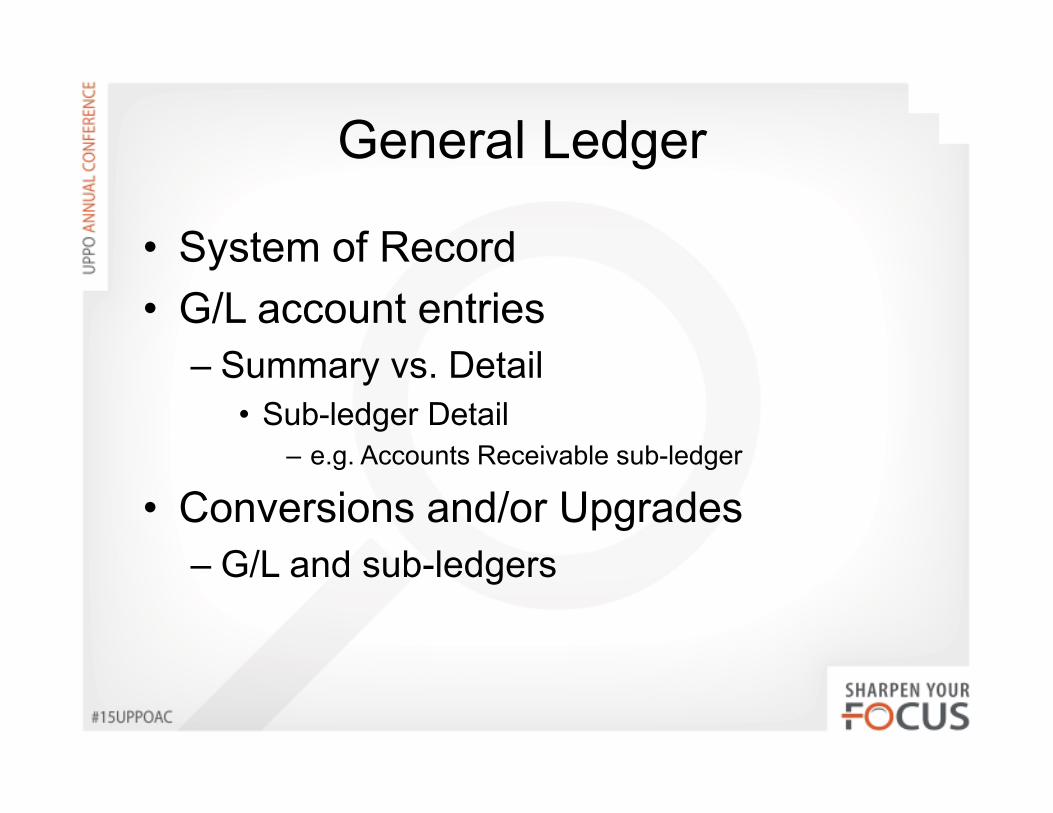

General Ledger

• System of Record

• G/L account entries

– Summary vs. Detail

• Sub-ledger Detail– e.g. Accounts Receivable sub-ledger

• Conversions and/or Upgrades

– G/L and sub-ledgers

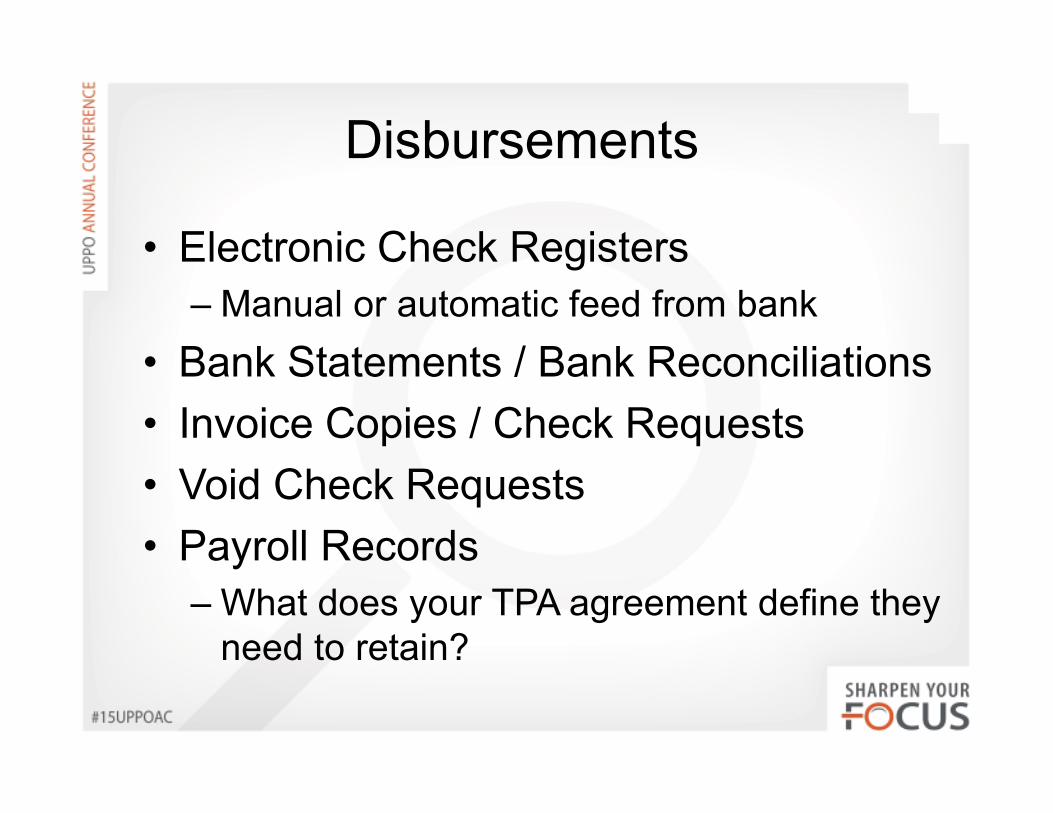

Disbursements

• Electronic Check Registers

– Manual or automatic feed from bank

• Bank Statements / Bank Reconciliations

• Invoice Copies / Check Requests

• Void Check Requests

• Payroll Records

– What does your TPA agreement define they need to retain?

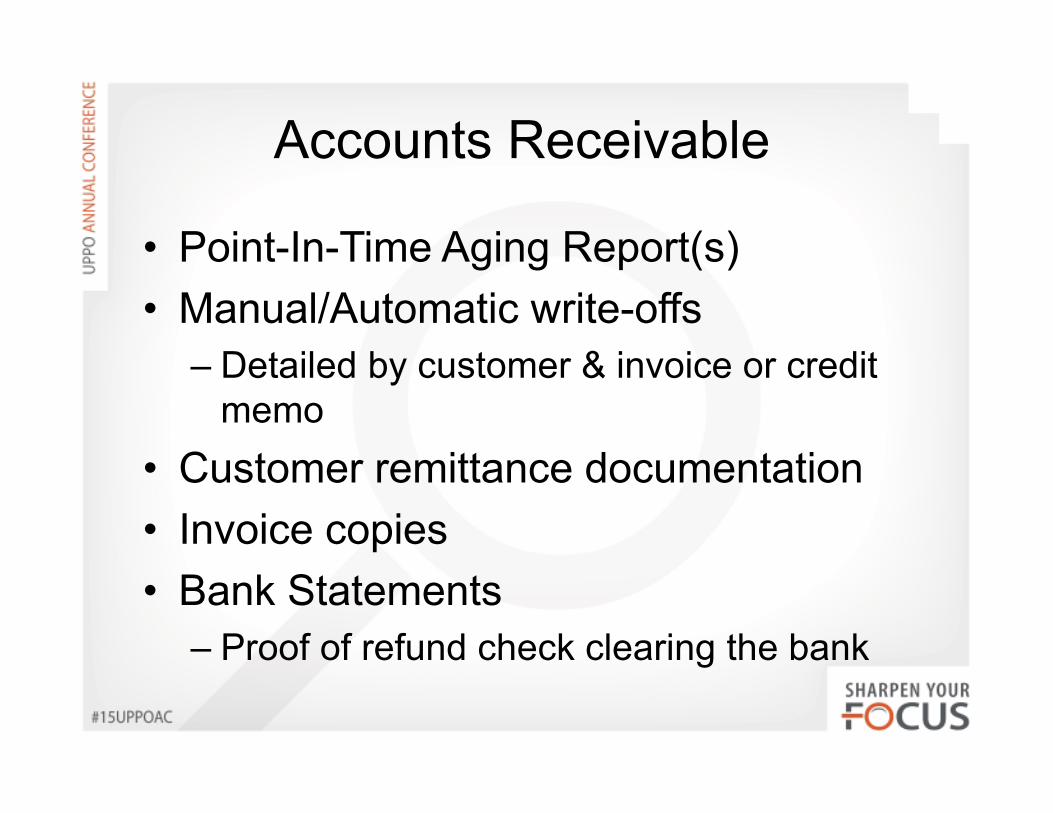

Accounts Receivable

• Point-In-Time Aging Report(s)

• Manual/Automatic write-offs

– Detailed by customer & invoice or credit memo

• Customer remittance documentation

• Invoice copies

• Bank Statements

– Proof of refund check clearing the bank

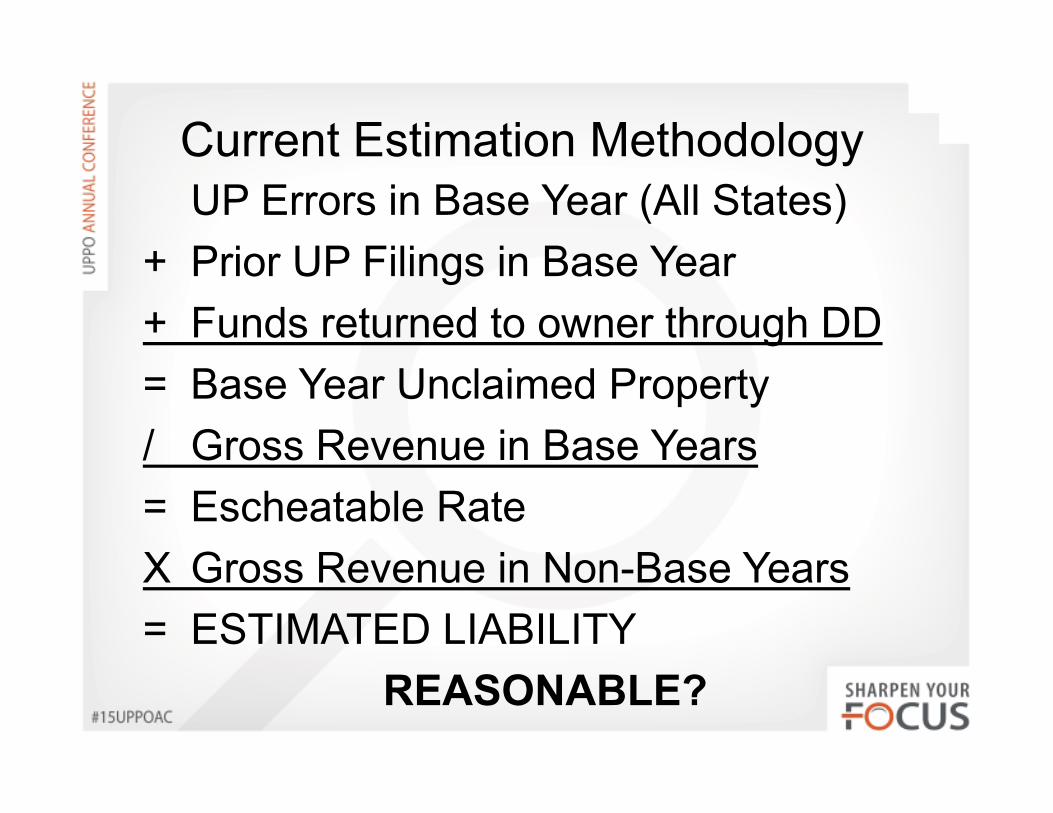

Current Estimation MethodologyUP Errors in Base Year (All States)

+ Prior UP Filings in Base Year

+ Funds returned to owner through DD

= Base Year Unclaimed Property

/ Gross Revenue in Base Years

= Escheatable Rate

X Gross Revenue in Non-Base Years

= ESTIMATED LIABILITY

REASONABLE?

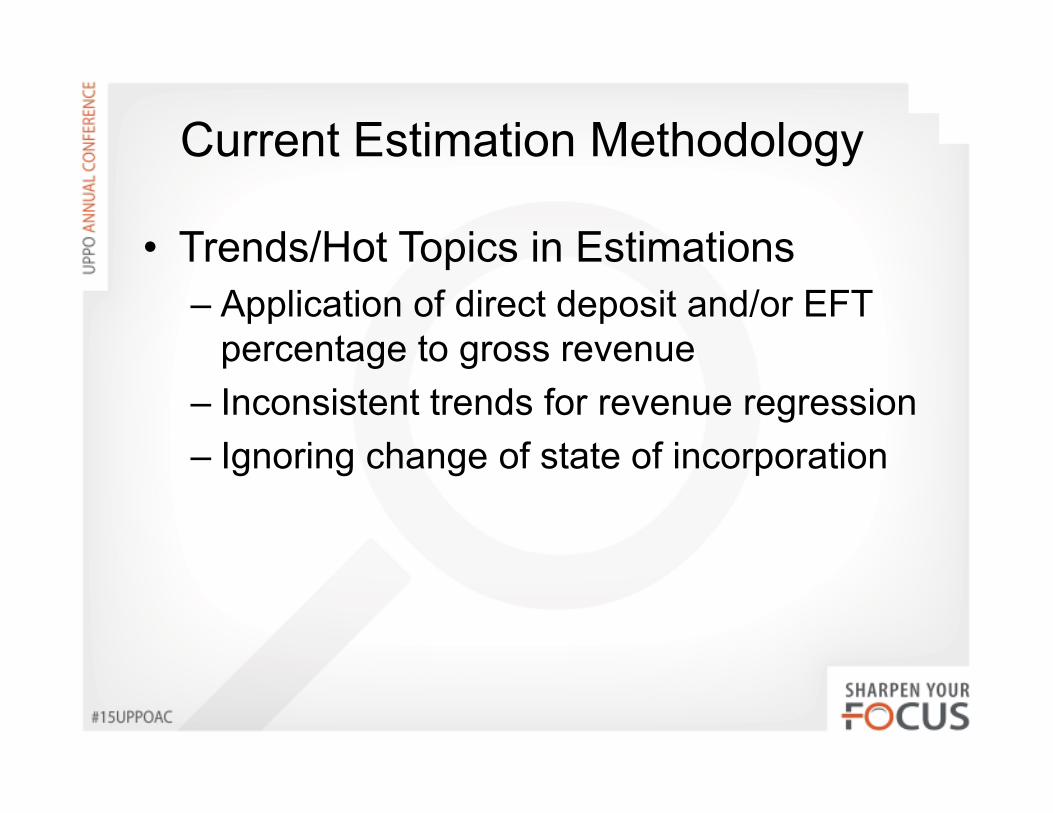

Current Estimation Methodology

• Trends/Hot Topics in Estimations

– Application of direct deposit and/or EFT percentage to gross revenue

– Inconsistent trends for revenue regression

– Ignoring change of state of incorporation

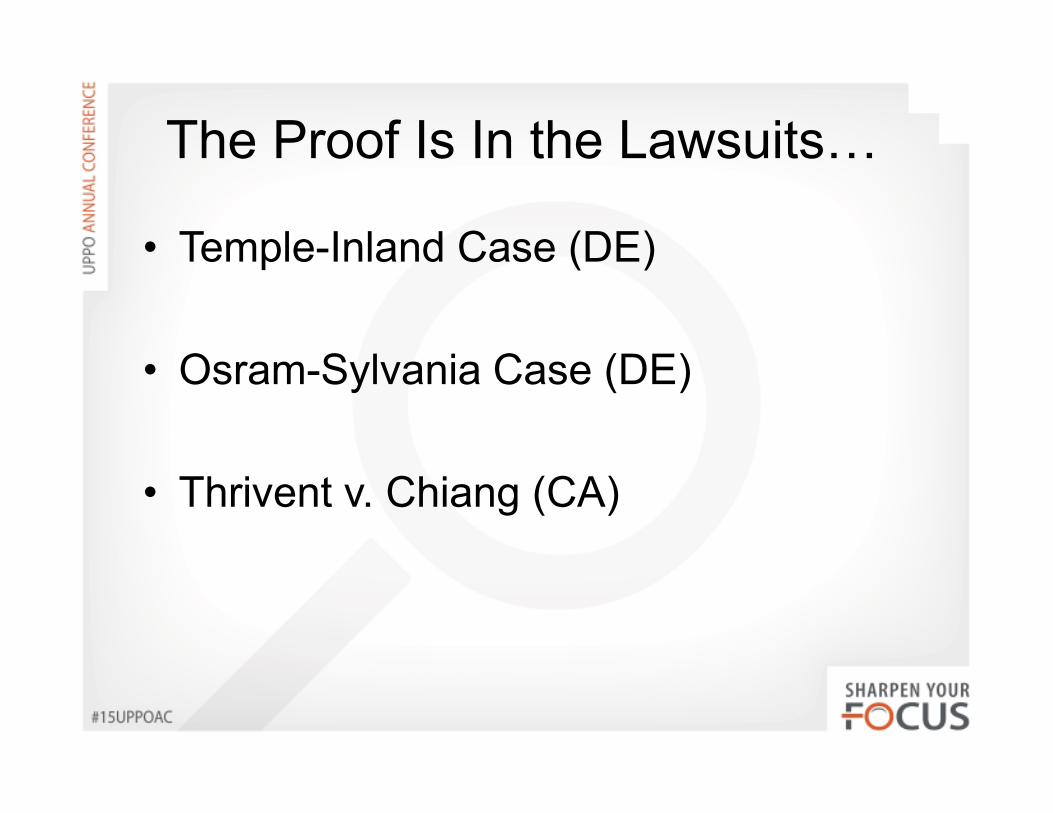

The Proof Is In the Lawsuits?

• Temple-Inland Case (DE)

• Osram-Sylvania Case (DE)

• Thrivent v. Chiang (CA)

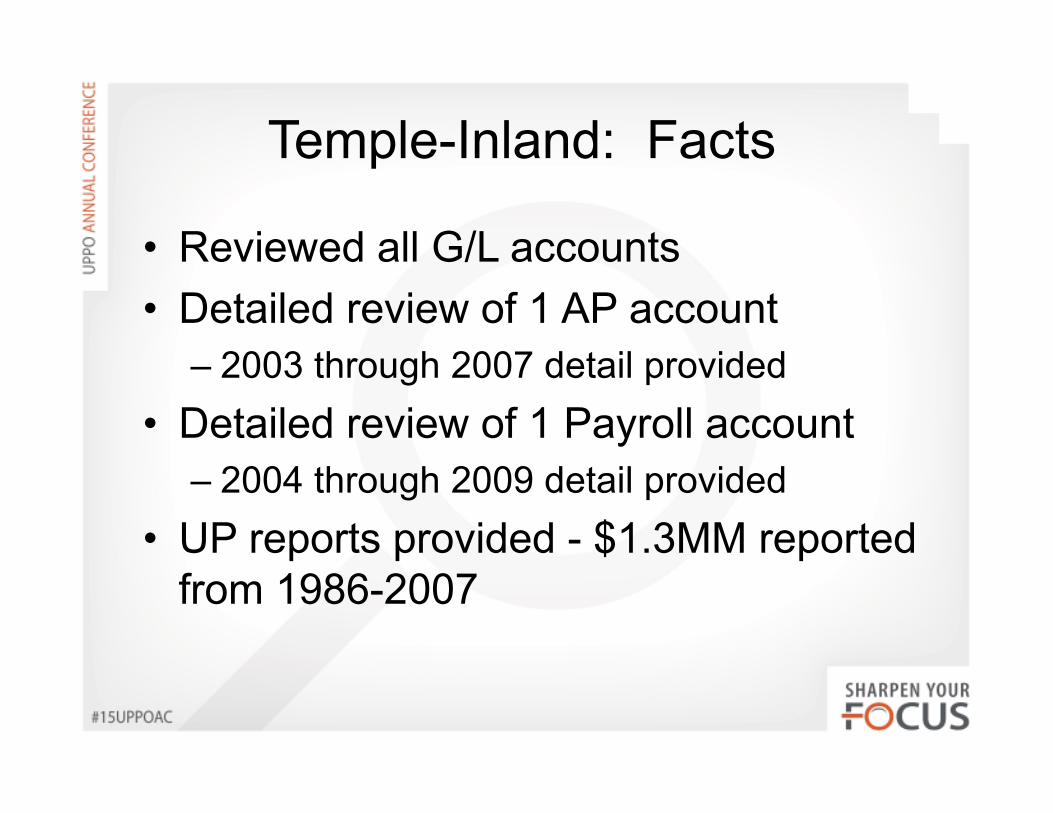

Temple-Inland: Facts

• Reviewed all G/L accounts

• Detailed review of 1 AP account

– 2003 through 2007 detail provided

• Detailed review of 1 Payroll account

– 2004 through 2009 detail provided

• UP reports provided - $1.3MM reported from 1986-2007

Temple-Inland: Facts

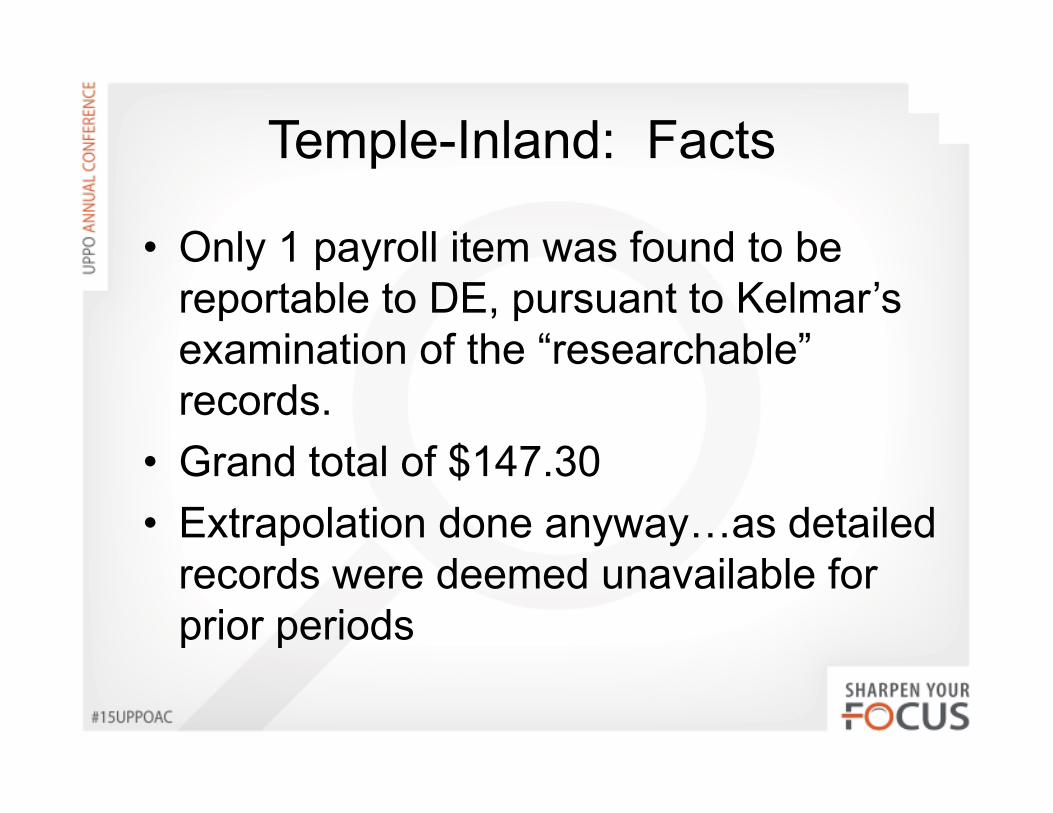

• Only 1 payroll item was found to be reportable to DE, pursuant to Kelmar’s examination of the “researchable” records.

• Grand total of $147.30

• Extrapolation done anyway?as detailed records were deemed unavailable for prior periods

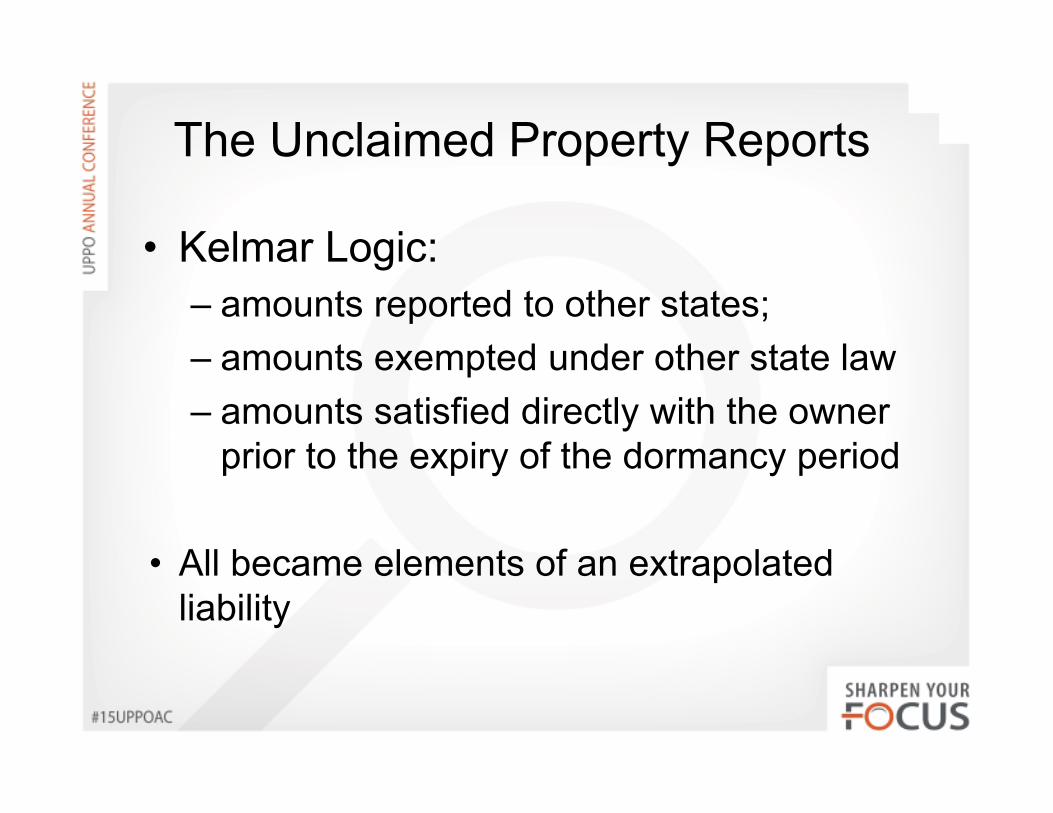

The Unclaimed Property Reports

• Kelmar Logic:

– amounts reported to other states;

– amounts exempted under other state law

– amounts satisfied directly with the owner prior to the expiry of the dormancy period

• All became elements of an extrapolated liability

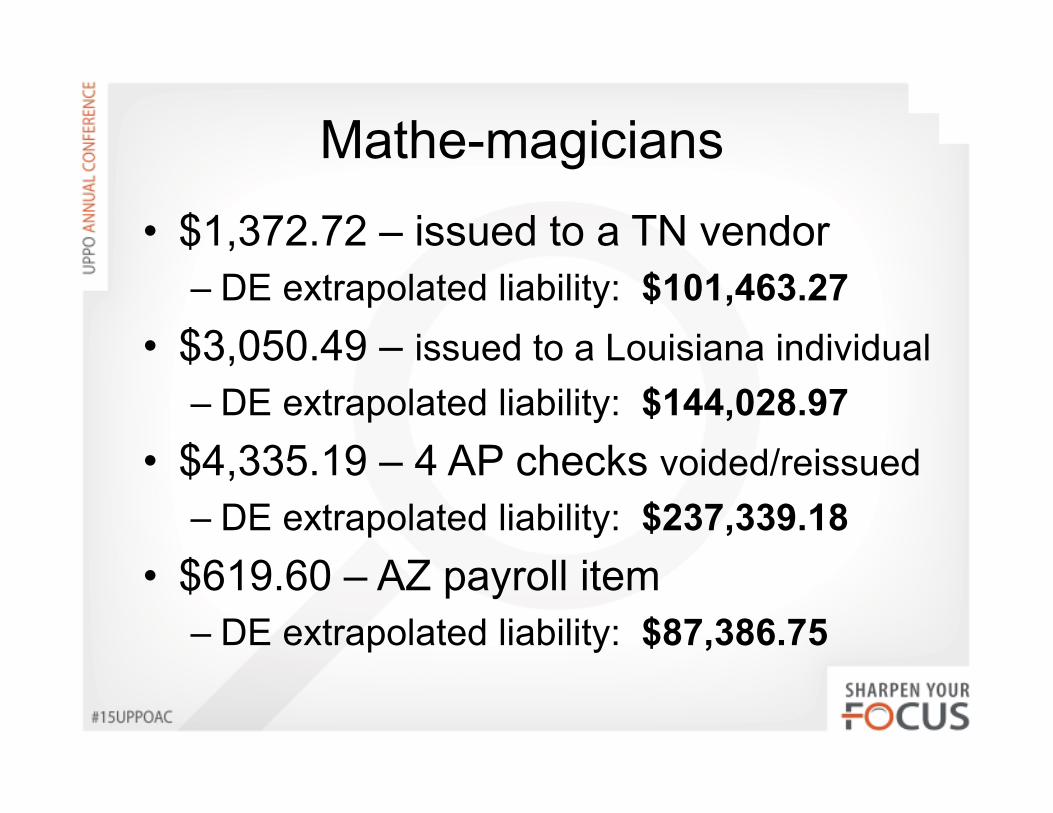

Mathe-magicians

• $1,372.72 – issued to a TN vendor

– DE extrapolated liability: $101,463.27

• $3,050.49 – issued to a Louisiana individual

– DE extrapolated liability: $144,028.97

• $4,335.19 – 4 AP checks voided/reissued

– DE extrapolated liability: $237,339.18

• $619.60 – AZ payroll item

– DE extrapolated liability: $87,386.75

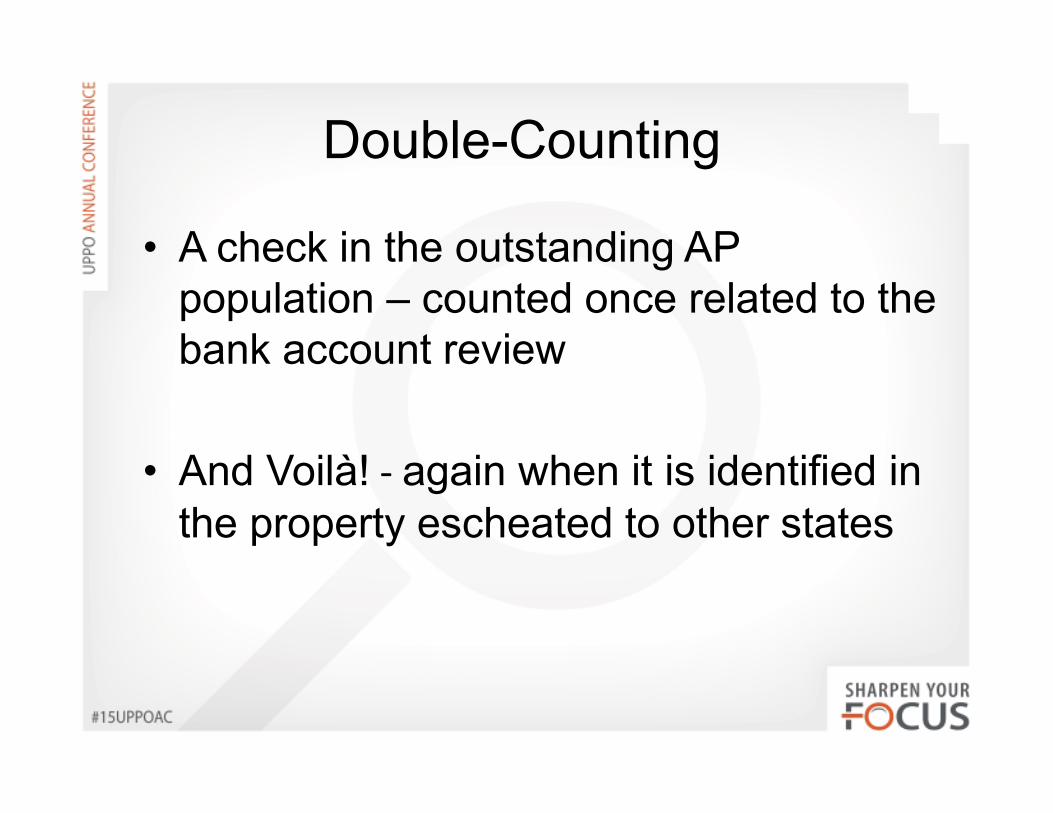

Double-Counting

• A check in the outstanding AP population – counted once related to the bank account review

• And Voilà! - again when it is identified in the property escheated to other states

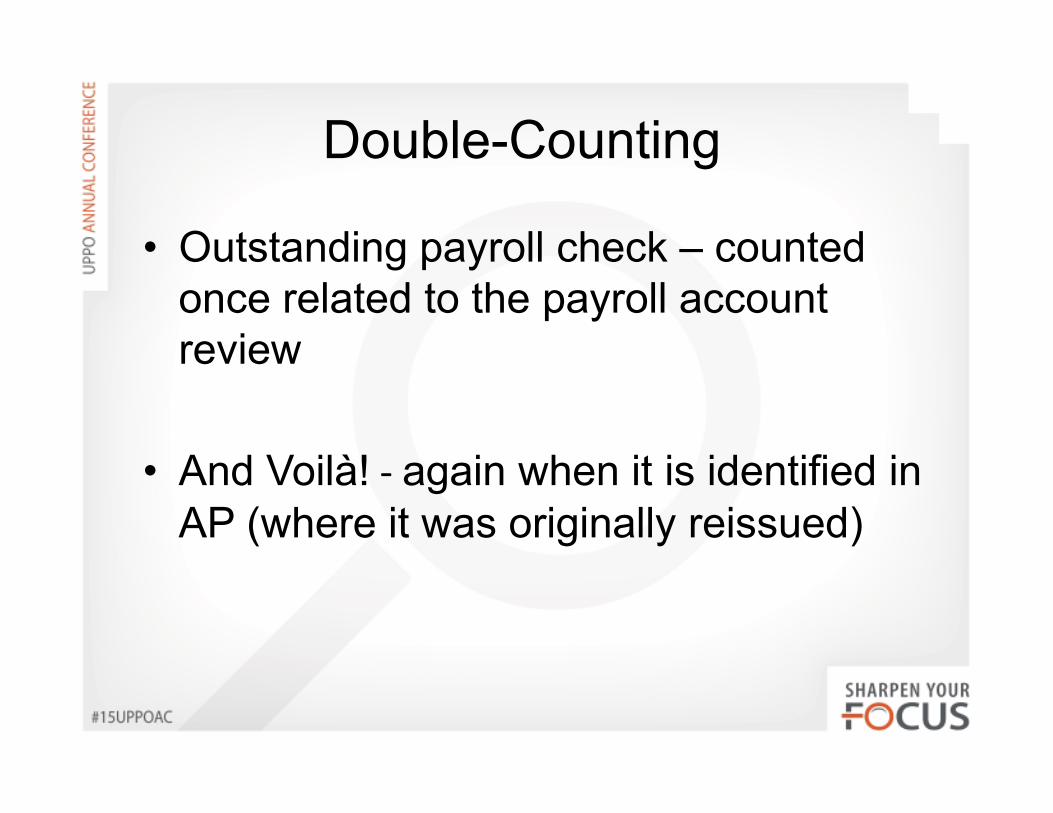

Double-Counting

• Outstanding payroll check – counted once related to the payroll account review

• And Voilà! - again when it is identified in AP (where it was originally reissued)

Osram-Sylvania

• Did not go through the Admin. Appeals process

• Extremely interesting information about how Kelmar gets paid

• Kelmar’s “proprietary” methodology highlighted again

Thrivent v. Chiang

“You’re asking for everything, millions of things, when what you need are a very circumspect group of things. You need death — in instances where there is a death certificate or there is a policy, or you have an insured and their projected statistical date of death by actuarial standards has passed, and then there is a — with three years passed.

What I’m hearing here, and which was in the warp and woof of your papers? is that the Government gets what they want, when they want, how they want it, and the way they want it. And the Constitution, as I read it in those cases, doesn’t say that.”

What Do These Cases Tell Us?

• Road maps for first line defenses

• Advocates must collectively hold Kelmar to the standards enumerated by these holder’s arguments

• Cooperative, yet judicious with what you provide to the auditors

• A final recommendation?

Questions?

James SantivañezJMS Advisory Group, LLC

(404) 474-7733

Troy WangenTrue Partners Consulting LLC

(312) 588-3430