bp p.l.c. group results fourth quarter and full year …financial results the replacement cost...

TRANSCRIPT

1

BP p.l.c.

Group results

Fourth quarter and full year 2015

FOR IMMEDIATE RELEASE London 2 February 2016

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(4,407) 46 (3,307) Profit (loss) for the period(a) (6,482) 3,780

3,438 1,188 1,074 Inventory holding (gains) losses*, net of tax 1,320 4,293

(969) 1,234 (2,233) Replacement cost profit (loss)* (5,162) 8,073

Net (favourable) unfavourable impact of

non-operating items* and fair value

3,208 585 2,429 accounting effects*, net of tax 11,067 4,063

2,239 1,819 196 Underlying replacement cost profit* 5,905 12,136

Replacement cost profit (loss)

(5.32) 6.73 (12.16) per ordinary share (cents) (28.18) 43.90

(0.32) 0.40 (0.73) per ADS (dollars) (1.69) 2.63

Underlying replacement cost profit

12.28 9.92 1.06 per ordinary share (cents) 32.22 66.00

0.74 0.60 0.06 per ADS (dollars) 1.93 3.96

BP’s fourth-quarter replacement cost (RC) loss was $2,233 million, compared with a loss of $969 million a year ago. After

adjusting for a net charge for non-operating items of $2,617 million and net favourable fair value accounting effects of

$188 million (both on a post-tax basis), underlying RC profit for the fourth quarter was $196 million, compared with

$2,239 million for the same period in 2014. The net charge for non-operating items mainly relates to impairment charges in

the Upstream segment and also reflects $450 million of restructuring charges for the group. The lower underlying result was

mainly due to the Upstream segment which reported an underlying replacement cost loss of $728 million for the quarter.

Cumulative restructuring charges from the beginning of the fourth quarter 2014 totalled $1.5 billion by the end of 2015. A

further $1.0 billion of restructuring charges are expected to be incurred in 2016.

For the full year, RC loss was $5,162 million, compared with a profit of $8,073 million a year ago. After adjusting for a net

charge for non-operating items of $11,272 million and net favourable fair value accounting effects of $205 million (both on a

post-tax basis), underlying RC profit for the full year was $5,905 million, compared with $12,136 million for the same period in

2014. RC profit or loss for the group, underlying RC profit or loss and fair value accounting effects are non-GAAP measures

and further information is provided on pages 3 and 29.

All amounts relating to the Gulf of Mexico oil spill have been treated as non-operating items, with a net pre-tax charge of

$443 million for the fourth quarter and $11,956 million for the full year. For further information on the Gulf of Mexico oil spill

and its consequences see page 10 and Note 2 on page 16. See also Legal proceedings on page 33.

Including the impact of the Gulf of Mexico oil spill, net cash provided by operating activities for the fourth quarter and full year

was $5.8 billion and $19.1 billion respectively, compared with $7.2 billion and $32.8 billion for the same periods in 2014.

Excluding amounts related to the Gulf of Mexico oil spill, net cash provided by operating activities for the fourth quarter and

full year was $5.9 billion and $20.3 billion respectively, compared with $6.9 billion and $32.8 billion for the same periods in

2014.

Net debt* at 31 December 2015 was $27.2 billion, compared with $22.6 billion a year ago. The net debt ratio* at

31 December 2015 was 21.6%, compared with 16.7% a year ago. Net debt and the net debt ratio are non-GAAP measures.

See page 25 for more information. We aim to maintain the net debt ratio, with some flexibility, at around 20%. We expect the

net debt ratio to be above 20% whilst oil prices remain weak.

The reserves replacement ratio* on a combined basis of subsidiaries and equity-accounted entities was estimated at 61%(b)

for the year, excluding the impact of acquisitions and disposals.

BP today announced a quarterly dividend of 10.00 cents per ordinary share ($0.600 per ADS), which is expected to be paid on

24 March 2016. The corresponding amount in sterling will be announced on 14 March 2016. See page 24 for further

information.

*

For items marked with an asterisk throughout this document, definitions are provided in the Glossary on page 31.

(a) Profit attributable to BP shareholders.

(b) Includes estimated reserves data for Rosneft. The reserves replacement ratio will be finalized and reported in BP Annual Report and

Form 20-F 2015 which is scheduled to be published in early March 2016.

The commentaries above and following should be read in conjunction with the cautionary statement on page 34.

2

Group headlines (continued)

Total capital expenditure on an accruals basis for the fourth quarter was $6.1 billion, of which organic capital expenditure*

was $5.5 billion, compared with $6.7 billion for the same period in 2014, of which organic capital expenditure was $6.6 billion.

For the full year, total capital expenditure on an accruals basis was $19.5 billion, of which organic capital expenditure was

$18.7 billion, compared with $23.8 billion for the same period in 2014, of which organic capital expenditure was $22.9 billion.

See page 27 for further information. In 2016, we expect organic capital expenditure to be at the lower end of the range of

$17-19 billion.

BP has now completed the $10-billion divestment programme that was announced in October 2013. Disposal proceeds were

$0.2 billion for the fourth quarter and $2.8 billion for the full year. The full-year amount for disposal proceeds includes amounts

received from our Toledo refinery partner, Husky Energy, in place of capital commitments relating to the original divestment

transaction that have not been subsequently sanctioned.

The effective tax rate (ETR) on RC profit or loss for the fourth quarter and full year was 12% and 34% respectively, compared

with 70% and 26% for the same periods in 2014. Excluding the one-off deferred tax adjustment in the first quarter 2015 as a

result of the reduction in the UK North Sea supplementary charge, the ETR for the year was 22%. Adjusting for non-operating

items, fair value accounting effects and the North Sea adjustment, the underlying ETR for the fourth quarter and full year was

-20% and 31% respectively, compared with 38% and 36% for the same periods in 2014. The underlying ETR for the fourth

quarter reflects tax credits associated with losses in the Upstream segment offsetting tax charges arising elsewhere. The full-

year underlying ETR is lower than a year ago mainly due to changes in the geographical mix of profits. In the current

environment, and with our existing portfolio of assets, the ETR in 2016 is expected to be lower than 2015 due to the

anticipated mix of profits moving away from relatively high tax Upstream jurisdictions.

Finance costs and net finance expense relating to pensions and other post-retirement benefits were a charge of $457 million

for the fourth quarter, compared with $381 million for the same period in 2014. For the full year, the respective amounts were

$1,653 million and $1,462 million.

Reported production for the fourth quarter, including BP’s share of Rosneft’s production, was 3,397 thousand barrels of oil

equivalent per day (mboe/d), compared with 3,214mboe/d for the same period in 2014 (see Upstream on page 4 and Rosneft

on page 8). Reported production for the full year, including BP’s share of Rosneft’s production, was 3,277mboe/d, compared

with 3,151mboe/d in 2014.

The charge for depreciation, depletion and amortization was $15.2 billion in 2015, the same as 2014. In 2016, we expect the

charge to be similar to 2015.

Definitive agreements were signed in January 2016 to dissolve BP’s refining joint operation with Rosneft in Germany (see

Note 3 for further information).

3

Analysis of RC profit (loss) before interest and tax

and reconciliation to profit (loss) for the period

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

RC profit (loss) before interest and tax*

(3,085) 743 (2,280) Upstream (937) 8,934

780 2,562 838 Downstream

7,111 3,738

451 382 235 Rosneft

1,310 2,100

(647) (378) (627) Other businesses and corporate

(1,768) (2,010)

(468) (311) (328) Gulf of Mexico oil spill response(a)

(11,709) (781)

257 67 65 Consolidation adjustment – UPII*

(36) 641

(2,712) 3,065 (2,097) RC profit (loss) before interest and tax

(6,029) 12,622

Finance costs and net finance expense relating

(381) (474) (457) to pensions and other post-retirement benefits

(1,653) (1,462)

2,158 (1,347) 304 Taxation on a RC basis

2,602 (2,864)

(34) (10) 17 Non-controlling interests

(82) (223)

(969) 1,234 (2,233) RC profit (loss) attributable to BP shareholders

(5,162) 8,073

(4,985) (1,726) (1,546) Inventory holding gains (losses)

(1,889) (6,210)

Taxation (charge) credit on inventory holding

1,547 538 472 gains and losses 569 1,917

Profit (loss) for the period attributable to

(4,407) 46 (3,307) BP shareholders (6,482) 3,780

(a) See Note 2 on page 16 for further information on the accounting for the Gulf of Mexico oil spill response.

Analysis of underlying RC profit before interest and tax

Fourth Third Fourth

quarter quarter quarter

Year Year

2014 2015 2015 $ million

2015 2014

Underlying RC profit before interest and tax*

2,246 823 (728) Upstream 1,193 15,201

1,213 2,302 1,218 Downstream 7,545 4,441

470 382 235 Rosneft

1,310 1,875

(120) (231) (299) Other businesses and corporate

(1,221) (1,340)

257 67 65 Consolidation adjustment - UPII

(36) 641

4,066 3,343 491 Underlying RC profit before interest and tax

8,791 20,818

Finance costs and net finance expense relating to

(372) (359) (342) pensions and other post-retirement benefits (1,406) (1,424)

(1,421) (1,155) 30 Taxation on an underlying RC basis

(1,398) (7,035)

(34) (10) 17 Non-controlling interests

(82) (223)

2,239 1,819 196 Underlying RC profit attributable to BP shareholders 5,905 12,136

Reconciliations of underlying RC profit or loss to the nearest equivalent IFRS measure are provided on page 1 for the group and

on pages 4-9 for the segments.

4

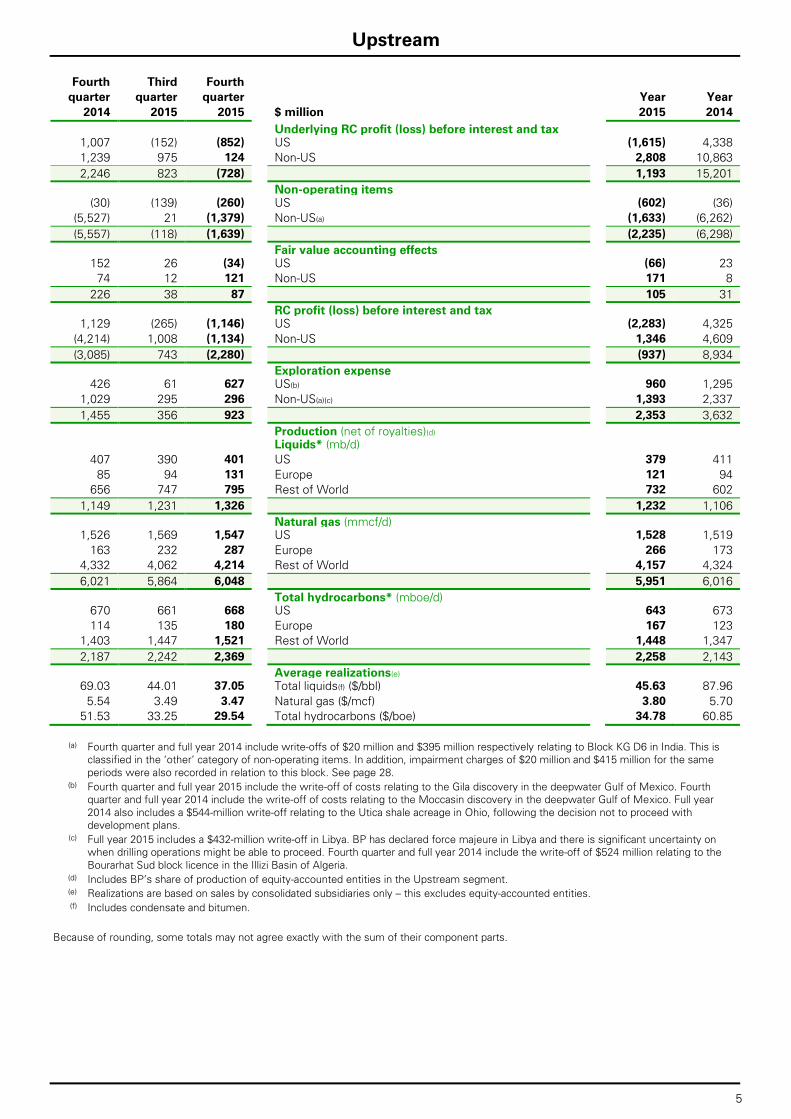

Upstream

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(3,165) 716 (2,298) Profit (loss) before interest and tax (967) 8,848

80 27 18 Inventory holding (gains) losses* 30 86

(3,085) 743 (2,280) RC profit (loss) before interest and tax (937) 8,934

Net (favourable) unfavourable impact of

non-operating items* and fair value

5,331 80 1,552 accounting effects* 2,130 6,267

2,246 823 (728) Underlying RC profit (loss) before interest and tax*(a) 1,193 15,201

(a) See page 5 for a reconciliation to segment RC profit before interest and tax by region.

Financial results

The replacement cost result before interest and tax for the fourth quarter and full year was a loss of $2,280 million and

$937 million respectively, compared with a loss of $3,085 million and a profit of $8,934 million for the same periods in 2014. The

fourth quarter and full year included a net non-operating charge of $1,639 million and $2,235 million respectively, compared with a

net non-operating charge of $5,557 million and $6,298 million for the same periods a year ago. The net non-operating charge for

the quarter relates mainly to a net impairment charge recorded in relation to a number of assets following a further fall in oil and

gas prices in the quarter and changes to other assumptions. See Note 4 Impairment of fixed assets on page 21 for further

information. Fair value accounting effects in the fourth quarter and full year had favourable impacts of $87 million and $105 million

respectively, compared with favourable impacts of $226 million and $31 million in the same periods of 2014.

After adjusting for non-operating items and fair value accounting effects, the underlying replacement cost result before interest

and tax for the fourth quarter and full year was a loss of $728 million and a profit of $1,193 million respectively, compared with a

profit of $2,246 million and $15,201 million for the same periods in 2014. The result for the fourth quarter reflected significantly

lower liquids and gas realizations and lower gas marketing and trading results partly offset by lower costs, including lower

exploration write-offs and benefits from simplification and efficiency activities. The result for the full year reflected significantly

lower liquids and gas realizations, rig cancellation charges and lower gas marketing and trading results partly offset by lower costs

including benefits from simplification and efficiency activities and lower exploration write-offs, and higher production.

Production

Production for the quarter was 2,369mboe/d, 8.3% higher than the fourth quarter of 2014. Underlying production* for the quarter

increased by 1.7%, mainly due to improved operating efficiency, wellwork delivery and major project start-ups partly offset by

planned maintenance activity. For the full year, production was 2,258mboe/d, 5.4% higher than in 2014. Underlying production for

the full year was flat versus 2014.

Key events

In November, BP signed a Heads of Agreement with the Egyptian Minister of Petroleum regarding the acceleration of the

development of the recent Atoll gas discovery. The Atoll discovery (BP 100%) in the North Damietta Offshore Concession in the

East Nile Delta, offshore Egypt was announced in March 2015. Development of Atoll will be executed and operated by Pharaonic

Petroleum Co. (PhPC), BP’s joint venture with EGAS and Eni.

Also in November, BP completed a transaction to acquire a 20% participatory interest in Taas-Yuryakh Neftegazodobycha LLC, a

Rosneft subsidiary that will further develop the Srednebotuobinskoye oil and gas condensate field in Eastern Siberia.

In December, BP announced the completion of its acquisition of 22.75% in the North Alexandria Concession and 2.75% in the

West Mediterranean Deep Water Concession from DEA Deutsche Erdoel AG. The acquisition will bring BP’s working interest in

both concessions of the West Nile Delta project in Egypt to 82.75%.

The new Glen Lyon floating production storage and offload (FPSO) vessel has completed sea trials and sailed away from South

Korea on 25 December. Glen Lyon is currently in tow to Norway for pre-installation works before travelling to the West of

Shetlands for installation and future start of production. The new FPSO is the centrepiece to the Quad 204 project, which is

redeveloping the Schiehallion and Loyal fields.

BP’s US Lower 48 Onshore business expanded its San Juan basin operations in December by acquiring all of Devon Energy’s

assets in the region. The bulk of the acquired assets, which span northern New Mexico and southern Colorado, consist of

Devon’s operated interest in the Northeast Blanco Unit. BP anticipates taking over operations of the unit’s 480 wells spread

across 33,000 gross acres at the end of the first quarter of 2016, after receiving required government agency approvals.

Outlook

We expect full-year 2016 underlying production to be broadly flat with 2015. The actual reported outcome will depend on the

exact timing of project start-ups, divestments, OPEC quotas and entitlement impacts in our production-sharing agreements*. We

expect first-quarter 2016 reported production to be broadly flat with the fourth quarter 2015. Oil prices continue to be challenging

in the near term.

The commentary above contains forward-looking statements and should be read in conjunction with the cautionary statement on page 34.

5

Upstream

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Underlying RC profit (loss) before interest and tax

1,007 (152) (852) US (1,615) 4,338

1,239 975 124 Non-US 2,808 10,863

2,246 823 (728) 1,193 15,201

Non-operating items

(30) (139) (260) US (602) (36)

(5,527) 21 (1,379) Non-US(a) (1,633) (6,262)

(5,557) (118) (1,639) (2,235) (6,298)

Fair value accounting effects

152 26 (34) US (66) 23

74 12 121 Non-US 171 8

226 38 87 105 31

RC profit (loss) before interest and tax

1,129 (265) (1,146) US (2,283) 4,325

(4,214) 1,008 (1,134) Non-US 1,346 4,609

(3,085) 743 (2,280) (937) 8,934

Exploration expense

426 61 627 US(b) 960 1,295

1,029 295 296 Non-US(a)(c) 1,393 2,337

1,455 356 923 2,353 3,632

Production (net of royalties)(d)

Liquids* (mb/d)

407 390 401 US 379 411

85 94 131 Europe 121 94

656 747 795 Rest of World 732 602

1,149 1,231 1,326 1,232 1,106

Natural gas (mmcf/d)

1,526 1,569 1,547 US 1,528 1,519

163 232 287 Europe 266 173

4,332 4,062 4,214 Rest of World 4,157 4,324

6,021 5,864 6,048 5,951 6,016

Total hydrocarbons* (mboe/d)

670 661 668 US 643 673

114 135 180 Europe 167 123

1,403 1,447 1,521 Rest of World 1,448 1,347

2,187 2,242 2,369 2,258 2,143

Average realizations(e)

69.03 44.01 37.05 Total liquids(f) ($/bbl) 45.63 87.96

5.54 3.49 3.47 Natural gas ($/mcf) 3.80 5.70

51.53 33.25 29.54 Total hydrocarbons ($/boe) 34.78 60.85

(a) Fourth quarter and full year 2014 include write-offs of $20 million and $395 million respectively relating to Block KG D6 in India. This is

classified in the ‘other’ category of non-operating items. In addition, impairment charges of $20 million and $415 million for the same

periods were also recorded in relation to this block. See page 28.

(b) Fourth quarter and full year 2015 include the write-off of costs relating to the Gila discovery in the deepwater Gulf of Mexico. Fourth

quarter and full year 2014 include the write-off of costs relating to the Moccasin discovery in the deepwater Gulf of Mexico. Full year

2014 also includes a $544-million write-off relating to the Utica shale acreage in Ohio, following the decision not to proceed with

development plans.

(c) Full year 2015 includes a $432-million write-off in Libya. BP has declared force majeure in Libya and there is significant uncertainty on

when drilling operations might be able to proceed. Fourth quarter and full year 2014 include the write-off of $524 million relating to the

Bourarhat Sud block licence in the Illizi Basin of Algeria.

(d) Includes BP’s share of production of equity-accounted entities in the Upstream segment.

(e) Realizations are based on sales by consolidated subsidiaries only – this excludes equity-accounted entities.

(f) Includes condensate and bitumen.

Because of rounding, some totals may not agree exactly with the sum of their component parts.

6

Downstream

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(4,064) 875 (644) Profit (loss) before interest and tax 5,248 (2,362)

4,844 1,687 1,482 Inventory holding (gains) losses* 1,863 6,100

780 2,562 838 RC profit before interest and tax 7,111 3,738

Net (favourable) unfavourable impact of

non-operating items* and fair value

433 (260) 380 accounting effects* 434 703

1,213 2,302 1,218 Underlying RC profit before interest and tax*(a) 7,545 4,441

(a) See page 7 for a reconciliation to segment RC profit before interest and tax by region and by business.

Financial results

The replacement cost profit before interest and tax for the fourth quarter and full year was $838 million and $7,111 million

respectively, compared with $780 million and $3,738 million for the same periods in 2014.

The 2015 results include a net non-operating charge of $548 million for the fourth quarter and a net non-operating charge of $590

million for the full year, compared with net non-operating charges of $790 million and $1,570 million for the same periods in 2014

(see pages 7 and 28 for further information on non-operating items). Fair value accounting effects had favourable impacts of $168

million for the fourth quarter and $156 million for the full year, compared with favourable impacts of $357 million and $867 million

in the same periods of 2014.

After adjusting for non-operating items and fair value accounting effects, the underlying replacement cost profit before interest

and tax for the fourth quarter and full year was $1,218 million and $7,545 million respectively, compared with $1,213 million and

$4,441 million for the same periods in 2014. The full-year result is a record for Downstream.

Replacement cost profit before interest and tax for the fuels, lubricants and petrochemicals businesses is set out on page 7.

Fuels business

The fuels business reported an underlying replacement cost profit before interest and tax of $888 million for the fourth quarter

and $5,995 million for the full year, compared with $925 million and $3,219 million for the same periods in 2014. The result for the

full year reflects a strong refining environment, improved refining margin optimization and operations, and lower costs from

simplification and efficiency programmes. The result for the quarter reflects lower costs from simplification and efficiency

programmes, offset by a weak supply and trading result.

On 15 January 2016 we announced that we had signed definitive agreements to dissolve our German refining joint operation with

our partner Rosneft, which will refocus our refining business in the heart of Europe.

Lubricants business

The lubricants business reported an underlying replacement cost profit before interest and tax of $294 million in the fourth quarter

and $1,384 million in the full year, compared with $313 million and $1,271 million for the same periods in 2014. The result for the

quarter reflects continued strong margins offset by adverse foreign exchange impacts. The result for the full year reflects strong

performance in growth markets and premium brands and lower costs from simplification and efficiency programmes. These full-

year factors contributed to around a 20% growth in the underlying replacement cost profit before interest and tax, which was

partially offset by adverse foreign exchange impacts.

Petrochemicals business

The petrochemicals business reported an underlying replacement cost profit before interest and tax of $36 million in the fourth

quarter and $166 million in the full year, compared with a loss of $25 million and a loss of $49 million for the same periods in

2014. The results for the quarter and full year reflect improved operational performance and benefits from our simplification and

efficiency programmes leading to lower costs.

Following a review of our petrochemicals portfolio to refocus our global business for long-term growth, on 6 January 2016 we

announced the agreement to sell our Decatur petrochemicals complex in Alabama, US.

Outlook

Looking ahead, refining margins in the first quarter are expected to be lower than the fourth quarter.

The commentary above contains forward-looking statements and should be read in conjunction with the cautionary statement on page 34.

7

Downstream

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Underlying RC profit before interest and tax -

by region

338 885 477 US 2,599 1,684

875 1,417 741 Non-US 4,946 2,757

1,213 2,302 1,218 7,545 4,441

Non-operating items

(337) 51 (196) US (86) (339)

(453) (8) (352) Non-US (504) (1,231)

(790) 43 (548) (590) (1,570)

Fair value accounting effects

379 153 124 US 102 914

(22) 64 44 Non-US 54 (47)

357 217 168 156 867

RC profit before interest and tax

380 1,089 405 US 2,615 2,259

400 1,473 433 Non-US 4,496

1,479

780 2,562 838 7,111 3,738

Underlying RC profit (loss) before interest

and tax - by business(a)(b)

925 1,917 888 Fuels 5,995 3,219

313 348 294 Lubricants 1,384 1,271

(25) 37 36 Petrochemicals 166 (49)

1,213 2,302 1,218 7,545 4,441

Non-operating items and fair value accounting

effects(c)

(383) 295 (220) Fuels (137) (389)

(45) (25) (17) Lubricants (143) 136

(5) (10) (143) Petrochemicals (154) (450)

(433) 260

(380) (434) (703)

RC profit (loss) before interest and tax(a)(b)

542 2,212 668 Fuels 5,858 2,830

268 323 277 Lubricants 1,241 1,407

(30) 27 (107) Petrochemicals 12 (499)

780 2,562 838 7,111 3,738

13.0 20.0 13.2 BP average refining marker margin (RMM)* ($/bbl) 17.0 14.4

Refinery throughputs (mb/d)

657 681 700 US 657 642

807 785 776 Europe 794 782

318 230 238 Rest of World 254 297

1,782 1,696 1,714 1,705 1,721

94.8 94.9 95.5 Refining availability* (%) 94.7 94.9

Marketing sales of refined products (mb/d)

1,166 1,121 1,267 US 1,158 1,166

1,173 1,272 1,188 Europe 1,199 1,177

534 479 476 Rest of World(d) 478 529

2,873 2,872 2,931 2,835 2,872

2,470 2,781 2,883 Trading/supply sales of refined products(d) 2,770 2,448

5,343 5,653 5,814 Total sales volumes of refined products 5,605 5,320

Petrochemicals production (kte)

872 877 938 US 3,666 3,844

937 976 727 Europe 3,527 3,851

1,719 2,004 2,002 Rest of World 7,567 6,319

3,528 3,857 3,667 14,760 14,014

(a) Segment-level overhead expenses are included in the fuels business result.

(b) BP’s share of income from petrochemicals at our Gelsenkirchen and Mülheim sites in Germany is reported in the fuels business.

(c) For Downstream, fair value accounting effects arise solely in the fuels business.

(d) Third quarter 2015 includes a minor reclassification between Marketing sales in Rest of World and Trading/supply sales of refined

products.

8

Rosneft

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015(a) $ million 2015(a) 2014

390 370 189 Profit before interest and tax(b) 1,314 2,076

61 12 46 Inventory holding (gains) losses* (4) 24

451 382 235 RC profit before interest and tax 1,310 2,100

19 – – Net charge (credit) for non-operating items* – (225)

470 382 235 Underlying RC profit before interest and tax* 1,310 1,875

Replacement cost profit before interest and tax for the fourth quarter and full year was $235 million and $1,310 million

respectively, compared with $451 million and $2,100 million for the same periods in 2014.

There were no non-operating items in the fourth quarter and full year 2015, compared with a non-operating charge of $19 million

and a gain of $225 million for the same periods in 2014.

After adjusting for non-operating items, the underlying replacement cost profit before interest and tax for the fourth quarter and

full year was $235 million and $1,310 million respectively, compared with $470 million and $1,875 million for the same periods in

2014. Compared with the same periods last year, the results for the fourth quarter and full year were primarily affected by lower

oil prices, foreign exchange, and comparatively favourable duty lag effects.

See also Group statement of comprehensive income – Share of items relating to equity-accounted entities, net of tax, and

footnote (a), on page 12 for other foreign exchange effects.

In June, Rosneft’s Annual General Meeting of Shareholders approved the distribution of a dividend of 8.21 roubles per share. We

received our share of this dividend in July 2015, which amounted to $271 million after the deduction of withholding tax.

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015(a) 2015(a) 2014

Production (net of royalties) (BP share)

819 810 811 Liquids* (mb/d) 813 821

1,203 1,125 1,261 Natural gas (mmcf/d) 1,195 1,084

1,027 1,003 1,028 Total hydrocarbons* (mboe/d) 1,019 1,008

(a) The operational and financial information of the Rosneft segment for the fourth quarter and full year is based on preliminary operational

and financial results of Rosneft for the full year ended 31 December 2015. Actual results may differ from these amounts.

(b) The Rosneft segment result includes equity-accounted earnings arising from BP’s 19.75% shareholding in Rosneft as adjusted for the

accounting required under IFRS relating to BP’s purchase of its interest in Rosneft and the amortization of the deferred gain relating to

the disposal of BP’s interest in TNK-BP. These adjustments have increased the reported profit before interest and tax for the fourth

quarter and full year 2015, as shown in the table above, compared with the equivalent amount in Russian roubles that we expect

Rosneft to report in its own financial statements under IFRS. BP’s share of Rosneft’s profit before interest and tax for each year-to-date

period is calculated by translating the amounts reported in Russian roubles into US dollars using the average exchange rate for the year

to date. BP's share of Rosneft’s earnings after finance costs, taxation and non-controlling interests, as adjusted, is included in the BP

group income statement within profit before interest and taxation.

9

Other businesses and corporate

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(647) (378) (627) Profit (loss) before interest and tax (1,768) (2,010)

– – – Inventory holding (gains) losses* – –

(647) (378) (627) RC profit (loss) before interest and tax (1,768) (2,010)

527 147 328 Net charge (credit) for non-operating items* 547 670

(120) (231) (299) Underlying RC profit (loss) before interest and tax* (1,221) (1,340)

Underlying RC profit (loss) before interest and tax

(167) (126) (107) US (439) (594)

47 (105) (192) Non-US (782) (746)

(120) (231) (299) (1,221) (1,340)

Non-operating items

(219) (127) (296) US (434) (360)

(308) (20) (32) Non-US (113) (310)

(527) (147) (328) (547) (670)

RC profit (loss) before interest and tax

(386) (253) (403) US (873) (954)

(261) (125) (224) Non-US (895) (1,056)

(647) (378) (627) (1,768) (2,010)

Other businesses and corporate comprises biofuels and wind businesses, shipping, treasury (which includes interest income on

the group's cash and cash equivalents), and corporate activities including centralized functions.

Financial results

The replacement cost loss before interest and tax for the fourth quarter and full year was $627 million and $1,768 million

respectively, compared with $647 million and $2,010 million for the same periods in 2014.

The fourth-quarter result included a net non-operating charge of $328 million, primarily relating to impairments, compared with a

net charge of $527 million a year ago, which related to restructuring provisions and impairments. For the full year, the net non-

operating charge was $547 million, compared with a net charge of $670 million in 2014.

After adjusting for non-operating items, the underlying replacement cost loss before interest and tax for the fourth quarter was

$299 million, compared with $120 million for the same period in 2014. The underlying charge in the fourth quarter was higher than

2014 mainly due to a number of one-off credits in the fourth quarter 2014. For the full year, the underlying replacement cost loss

before interest and tax was $1,221 million compared with $1,340 million in 2014.

Biofuels

The net ethanol-equivalent production (which includes ethanol and sugar) for the fourth quarter and full year was 189 million litres

and 795 million litres respectively, compared with 242 million litres and 653 million litres for the same periods in 2014.

Wind

Net wind generation capacity*(a) was 1,588MW at 31 December 2015, the same as at 31 December 2014. BP’s net share of wind

generation for the fourth quarter and full year was 1,253GWh and 4,424GWh respectively, compared with 1,240GWh and

4,617GWh for the same periods in 2014.

Outlook

In 2016, Other businesses and corporate average quarterly charges, excluding non-operating items, are expected to be around

$300 million although this will fluctuate from quarter to quarter.

(a) Capacity figures include 32MW in the Netherlands managed by our Downstream segment.

The commentary above contains forward-looking statements and should be read in conjunction with the cautionary statement on page 34.

10

Gulf of Mexico oil spill

We announced on 2 July 2015 that BP Exploration & Production Inc. reached agreements in principle with the US federal

government and five Gulf states to settle all outstanding federal and state claims arising from the Deepwater Horizon oil spill

along with more than 400 local government claims. On 5 October 2015, the United States lodged with the district court in MDL

2179 a proposed Consent Decree between the United States, the Gulf states and BP to fully and finally resolve any and all natural

resource damages (NRD) claims of the United States, the Gulf states, and their respective natural resource trustees and all Clean

Water Act (CWA) penalty claims, and certain other claims of the United States and the Gulf states. A hearing has been scheduled

by the court to consider approval of the proposed Consent Decree in March 2016.

For further details see Note 2 on page 16.

Financial update

The replacement cost loss before interest and tax for the fourth quarter and full year was $328 million and $11,709 million

respectively, compared with $468 million and $781 million for the same periods last year. The fourth-quarter loss reflects

additional business economic loss claims under the Plaintiffs’ Steering Committee settlements and the ongoing costs of the Gu lf

Coast Restoration Organization, partially offset by adjustments to provisions due to discounting effects. The loss for the full year

also includes amounts provided for the agreements described above, and additional increases in the provision for business

economic loss claims, associated claims administration costs and other items. The cumulative pre-tax charge recognized to date

amounts to $55.5 billion.

The cumulative income statement charge does not include amounts for obligations that BP currently considers are not possible to

measure reliably. The total amounts that will ultimately be paid by BP in relation to the incident will be dependent on many

factors, as discussed under Provisions and contingent liabilities in Note 2 on page 16. These could have a material impact on our

consolidated financial position, results and cash flows.

11

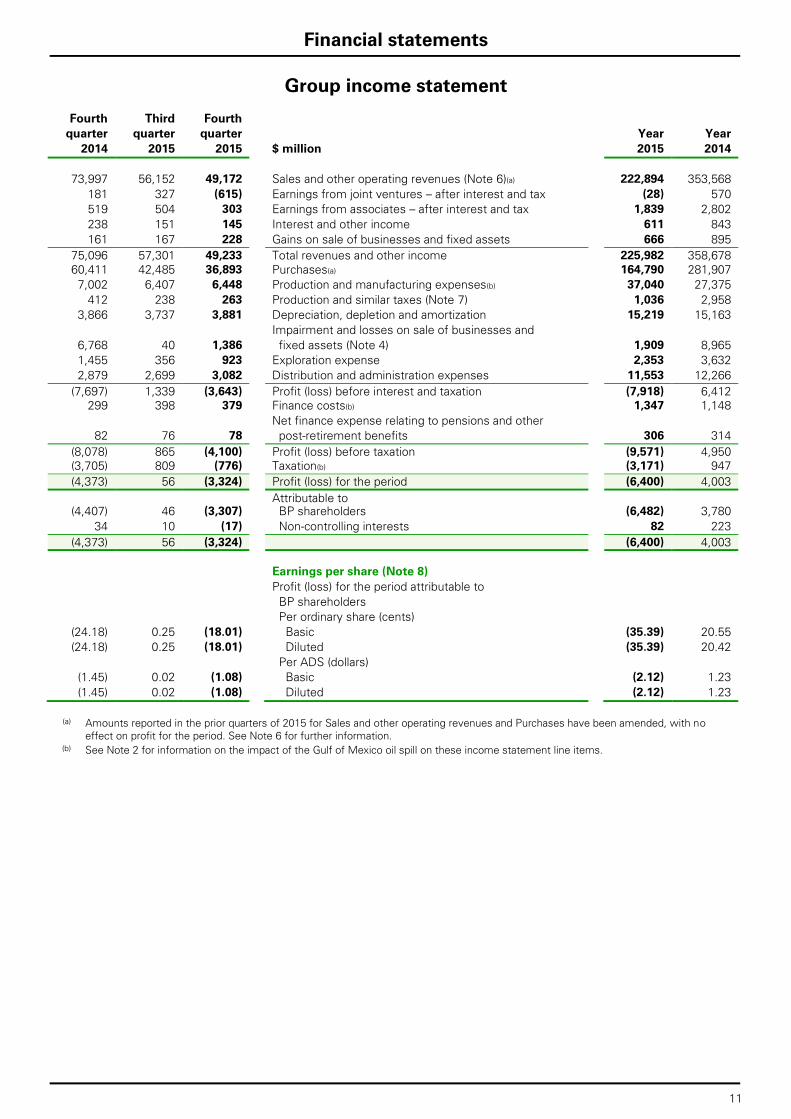

Financial statements

Group income statement

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

73,997 56,152 49,172 Sales and other operating revenues (Note 6)(a) 222,894 353,568

181 327 (615) Earnings from joint ventures – after interest and tax (28) 570

519 504 303 Earnings from associates – after interest and tax 1,839 2,802

238 151 145 Interest and other income 611 843

161 167 228 Gains on sale of businesses and fixed assets 666 895

75,096 57,301 49,233 Total revenues and other income 225,982 358,678

60,411 42,485 36,893 Purchases(a) 164,790 281,907

7,002 6,407 6,448 Production and manufacturing expenses(b) 37,040 27,375

412 238 263 Production and similar taxes (Note 7) 1,036 2,958

3,866 3,737 3,881 Depreciation, depletion and amortization 15,219 15,163

Impairment and losses on sale of businesses and

6,768 40 1,386 fixed assets (Note 4) 1,909 8,965

1,455 356 923 Exploration expense 2,353 3,632

2,879 2,699 3,082 Distribution and administration expenses 11,553 12,266

(7,697) 1,339 (3,643) Profit (loss) before interest and taxation (7,918) 6,412

299 398 379 Finance costs(b) 1,347 1,148

Net finance expense relating to pensions and other

82 76 78 post-retirement benefits 306 314

(8,078) 865 (4,100) Profit (loss) before taxation (9,571) 4,950

(3,705) 809 (776) Taxation(b) (3,171) 947

(4,373) 56 (3,324) Profit (loss) for the period (6,400) 4,003

Attributable to

(4,407) 46 (3,307) BP shareholders (6,482) 3,780

34 10 (17) Non-controlling interests 82 223

(4,373) 56 (3,324) (6,400) 4,003

Earnings per share (Note 8)

Profit (loss) for the period attributable to

BP shareholders

Per ordinary share (cents)

(24.18) 0.25 (18.01) Basic (35.39) 20.55

(24.18) 0.25 (18.01) Diluted (35.39) 20.42

Per ADS (dollars)

(1.45) 0.02 (1.08) Basic (2.12) 1.23

(1.45) 0.02 (1.08) Diluted (2.12) 1.23

(a) Amounts reported in the prior quarters of 2015 for Sales and other operating revenues and Purchases have been amended, with no

effect on profit for the period. See Note 6 for further information.

(b) See Note 2 for information on the impact of the Gulf of Mexico oil spill on these income statement line items.

12

Financial statements (continued)

Group statement of comprehensive income

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(4,373) 56 (3,324) Profit (loss) for the period (6,400) 4,003

Other comprehensive income

Items that may be reclassified subsequently to

profit or loss

(3,496) (2,247) (958) Currency translation differences (4,119) (6,838)

Exchange gains (losses) on translation of foreign

operations reclassified to gain or loss on sale of

54 7 – business and fixed assets 23 51

– – – Available-for-sale investments 1 –

(111) (70) (24) Cash flow hedges marked to market (178) (155)

Cash flow hedges reclassified to the

17 65 29 income statement 249 (73)

– 7 6 Cash flow hedges reclassified to the balance sheet 22 (11)

Share of items relating to equity-accounted

(2,418) (830) (233) entities, net of tax(a) (814) (2,584)

151 268 (43) Income tax relating to items that may be reclassified 257 147

(5,803) (2,800) (1,223) (4,559) (9,463)

Items that will not be reclassified to profit or loss

Remeasurements of the net pension and other

(2,825) (551) 2,570 post-retirement benefit liability or asset 4,139 (4,590)

Share of items relating to equity-accounted

(1) (1) – entities, net of tax (1) 4

Income tax relating to items that will not be

856 80 (881) reclassified (1,397) 1,334

(1,970) (472) 1,689 2,741 (3,252)

(7,773) (3,272) 466 Other comprehensive income (1,818) (12,715)

(12,146) (3,216) (2,858) Total comprehensive income (8,218) (8,712)

Attributable to

(12,155) (3,204) (2,836) BP shareholders (8,259) (8,903)

9 (12) (22) Non-controlling interests 41 191

(12,146) (3,216) (2,858) (8,218) (8,712)

(a) Includes the effects of hedge accounting adopted by Rosneft from 1 October 2014 in relation to a portion of future export revenue

denominated in US dollars. For further information see BP Annual Report and Form 20-F 2014 – Financial statements – Note 15.

13

Financial statements (continued)

Group statement of changes in equity

BP

shareholders’ Non-controlling Total

$ million equity interests equity

At 1 January 2015 111,441 1,201 112,642

Total comprehensive income (8,259) 41 (8,218)

Dividends (6,659) (91) (6,750)

Share-based payments, net of tax 656 – 656

Share of equity-accounted entities’ changes in equity,

net of tax 40 – 40

Transactions involving non-controlling interests (3) 20 17

At 31 December 2015 97,216 1,171 98,387

BP

shareholders’ Non-controlling Total

$ million equity interests equity

At 1 January 2014 129,302 1,105 130,407

Total comprehensive income (8,903) 191 (8,712)

Dividends (5,850) (255) (6,105)

Repurchases of ordinary share capital (3,366) – (3,366)

Share-based payments, net of tax 185 – 185

Share of equity-accounted entities’ changes in equity,

net of tax 73 – 73

Transactions involving non-controlling interests – 160 160

At 31 December 2014 111,441 1,201 112,642

14

Financial statements (continued)

Group balance sheet

31 December 31 December

$ million 2015 2014

Non-current assets

Property, plant and equipment 129,758 130,692

Goodwill 11,627 11,868

Intangible assets 18,660 20,907

Investments in joint ventures 8,412 8,753

Investments in associates 9,422 10,403

Other investments 1,002 1,228

Fixed assets 178,881 183,851

Loans 529 659

Trade and other receivables 2,216 4,787

Derivative financial instruments 4,409 4,442

Prepayments 1,003 964

Deferred tax assets 1,545 2,309

Defined benefit pension plan surpluses 2,647 31

191,230 197,043

Current assets

Loans 272 333

Inventories 14,142 18,373

Trade and other receivables 22,323 31,038

Derivative financial instruments 4,242 5,165

Prepayments 1,838 1,424

Current tax receivable 599 837

Other investments 219 329

Cash and cash equivalents 26,389 29,763

70,024 87,262

Assets classified as held for sale (Note 3) 578 –

70,602 87,262

Total assets 261,832 284,305

Current liabilities

Trade and other payables 31,949 40,118

Derivative financial instruments 3,239 3,689

Accruals 6,261 7,102

Finance debt 6,944 6,877

Current tax payable 1,080 2,011

Provisions 5,154 3,818

54,627 63,615

Liabilities directly associated with assets classified as held for sale (Note 3) 97 –

54,724 63,615

Non-current liabilities

Other payables 2,910 3,587

Derivative financial instruments 4,283 3,199

Accruals 890 861

Finance debt 46,224 45,977

Deferred tax liabilities 9,599 13,893

Provisions 35,960 29,080

Defined benefit pension plan and other post-retirement benefit plan deficits 8,855 11,451

108,721 108,048

Total liabilities 163,445 171,663

Net assets 98,387 112,642

Equity

BP shareholders’ equity 97,216 111,441

Non-controlling interests 1,171 1,201

98,387 112,642

15

Financial statements (continued)

Condensed group cash flow statement

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Operating activities

(8,078) 865 (4,100) Profit (loss) before taxation (9,571) 4,950

Adjustments to reconcile profit (loss) before taxation

to net cash provided by operating activities

Depreciation, depletion and amortization and

5,215 3,971 4,578 exploration expenditure written off 17,048 18,192

Impairment and (gain) loss on sale of businesses

6,607 (127) 1,158 and fixed assets 1,243 8,070

Earnings from equity-accounted entities, less

(224) (295) 1,028 dividends received (197) (1,461)

Net charge for interest and other finance expense,

49 196 164 less net interest paid 502 330

(58) 137 167 Share-based payments 321 379

Net operating charge for pensions and other post-

retirement benefits, less contributions and benefit

(664) (41) (464) payments for unfunded plans (592) (963)

551 113 591 Net charge for provisions, less payments 11,792 1,119

Movements in inventories and other current and

4,842 1,231 2,978 non-current assets and liabilities 843 6,925

(993) (867) (294) Income taxes paid (2,256) (4,787)

7,247 5,183 5,806 Net cash provided by operating activities 19,133 32,754

Investing activities

(5,900) (4,357) (5,126) Capital expenditure (18,648) (22,546)

(118) 33 (10) Acquisitions, net of cash acquired 23 (131)

(65) (55) (87) Investment in joint ventures (265) (179)

(128) (119) (888) Investment in associates (1,312) (336)

224 88 17 Proceeds from disposal of fixed assets 1,066 1,820

Proceeds from disposal of businesses, net of

880 200 215 cash disposed 1,726 1,671

48 61 1 Proceeds from loan repayments 110 127

(5,059) (4,149) (5,878) Net cash used in investing activities (17,300) (19,574)

Financing activities

(793) – – Net repurchase of shares – (4,589)

2,779 117 185 Proceeds from long-term financing 8,173 12,394

(2,937) (18) (3,559) Repayments of long-term financing (6,426) (6,282)

(186) (115) (124) Net increase (decrease) in short-term debt 473 (693)

9 – (5) Net increase (decrease) in non-controlling interests

(5) 9

(1,729) (1,718) (1,541) Dividends paid – BP shareholders (6,659) (5,850)

(40) (29) (20) – non-controlling interests (91) (255)

(2,897) (1,763) (5,064) Net cash provided by (used in) financing activities (4,535) (5,266)

Currency translation differences relating to cash

(257) (158) (177) and cash equivalents (672) (671)

(966) (887) (5,313) Increase (decrease) in cash and cash equivalents (3,374) 7,243

30,729 32,589 31,702 Cash and cash equivalents at beginning of period 29,763 22,520

29,763 31,702 26,389 Cash and cash equivalents at end of period 26,389 29,763

16

Financial statements (continued)

Notes

1. Basis of preparation

The results for the interim periods and for the year ended 31 December 2015 are unaudited and, in the opinion of

management, include all adjustments necessary for a fair presentation of the results for each period. All such

adjustments are of a normal recurring nature. This report should be read in conjunction with the consolidated financial

statements and related notes for the year ended 31 December 2014 included in the BP Annual Report and Form 20-F

2014.

BP prepares its consolidated financial statements included within BP Annual Report and Form 20-F on the basis of

International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB), IFRS

as adopted by the European Union (EU) and in accordance with the provisions of the UK Companies Act 2006. IFRS as

adopted by the EU differs in certain respects from IFRS as issued by the IASB. The differences have no impact on the

group’s consolidated financial statements for the periods presented.

The financial information presented herein has been prepared in accordance with the accounting policies expected to be

used in preparing BP Annual Report and Form 20-F 2015, which do not differ significantly from those used in BP Annual

Report and Form 20-F 2014.

In BP Annual Report and Form 20-F 2014 we disclosed a significant estimate or judgement relating to the recoverability

of asset carrying values, including the discount rates applied to estimates of future cash flows to determine the

recoverable amount of assets when performing impairment tests. During the fourth quarter 2015 the discount rates used

by the group in assessments of impairment were reviewed. The post-tax discount rate applied to cash flow analyses

used to calculate fair value less costs of disposal in the fourth quarter was 7%. For value-in-use calculations, the pre-tax

discount rate applied in the fourth quarter was 11%. For both calculations a premium of 2% continues to be added for

assets located in higher risk countries. The group’s assumptions for long-term oil and gas prices were also revised

downwards slightly for impairment tests in which the recoverable amount of Upstream assets is determined on the

basis of fair value less costs of disposal. Impairment tests continue to utilize market-based forward prices for the first

five years. Further details will be provided in BP Annual Report and Form 20-F 2015 which is expected to be published in

early March 2016.

2. Gulf of Mexico oil spill

(a) Overview

As a consequence of the Gulf of Mexico oil spill, BP continues to incur various costs and has also recognized liabilities for

future costs. The information presented in this note should be read in conjunction with BP Annual Report and Form 20-F

2014 – Financial statements – Note 2 and Legal proceedings on page 228 and on page 33 of this report.

The group income statement includes a pre-tax charge of $443 million for the fourth quarter and $11,956 million for the

full year in relation to the Gulf of Mexico oil spill. The fourth-quarter charge reflects additional business economic loss

claims under the Plaintiffs’ Steering Committee (PSC) settlement, finance costs and the ongoing costs of the Gulf Coast

Restoration Organization, partially offset by adjustments to provisions due to discounting effects. The cumulative pre-tax

income statement charge since the incident, in April 2010, amounts to $55,451 million.

The cumulative income statement charge does not include amounts for obligations that BP considers are not possible, at

this time, to measure reliably. For further information, see Provisions and contingent liabilities below.

The agreements in principle signed on 2 July 2015 to settle all federal and state claims and claims made by more than

400 local government entities were subject to execution of definitive agreements, including a Consent Decree with the

United States and Gulf states with respect to the Clean Water Act penalty and natural resource damages and other

claims, a Settlement Agreement with five Gulf states with respect to state claims for economic loss, property damage

and other claims, and resolution to BP’s satisfaction of the economic loss, property damage and other claims with more

than 400 local government entities. The proposed Consent Decree between the United States, the Gulf states and BP

was available for public comment until early December 2015 and is subject to final court approval. The Consent Decree

and Settlement Agreement with the five Gulf states are conditional upon each other and neither will become effective

unless there is final court approval of the Consent Decree; a hearing has been scheduled by the court to consider

approval of the proposed Consent Decree in March 2016. During the third quarter 2015, the Settlement Agreement with

the five Gulf states was executed. BP has accepted releases received from the vast majority of local government entities

and payments required under those releases were made during the third quarter. For more information on the proposed

Consent Decree and Settlement Agreement see Legal proceedings on pages 32-34 of BP Third Quarter and nine months

results 2015.

The agreements described above (the Agreements) significantly reduce the uncertainties faced by BP following the Gulf

of Mexico oil spill in 2010. There continues to be uncertainty regarding the outcome or resolution of current or future

litigation and the extent and timing of costs relating to the incident not covered by the Agreements. The total amounts

17

Financial statements (continued)

Notes

2. Gulf of Mexico oil spill (continued)

that will ultimately be paid by BP in relation to the incident will be dependent on many factors, as discussed under

Provisions and contingent liabilities below, including in relation to any new information or future developments. These

uncertainties could have a material impact on our consolidated financial position, results and cash flows.

The amounts set out below reflect the impacts on the financial statements of the Gulf of Mexico oil spill for the periods

presented. The income statement, balance sheet and cash flow statement impacts are included within the relevant line

items in those statements as set out below.

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Income statement

468 311 328 Production and manufacturing expenses 11,709 781

(468) (311) (328) Profit (loss) before interest and taxation (11,709) (781)

9 115 115 Finance costs 247 38

(477) (426) (443) Profit (loss) before taxation (11,956) (819)

163 (87) (134) Taxation 3,492 262

(314) (513) (577) Profit (loss) for the period (8,464) (557)

31 December 31 December

$ million 2015 2014

Balance sheet

Current assets

Trade and other receivables 686 1,154

Current liabilities

Trade and other payables (693) (655)

Accruals (40) –

Provisions (3,076) (1,702)

Net current assets (liabilities) (3,123) (1,203)

Non-current assets

Trade and other receivables – 2,701

Non-current liabilities

Other payables (2,057) (2,412)

Accruals (186) (169)

Provisions (13,431) (6,903)

Deferred tax 5,200 1,723

Net non-current assets (liabilities) (10,474) (5,060)

Net assets (liabilities) (13,597) (6,263)

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Cash flow statement - Operating activities

(477) (426) (443) Profit (loss) before taxation (11,956) (819)

Adjustments to reconcile profit (loss) before

taxation to net cash provided by

operating activities

Net charge for interest and other finance

9 115 115 expense, less net interest paid 247 38

334 235 227 Net charge for provisions, less payments 11,296 939

Movements in inventories and other current

3 (135) (36) and non-current assets and liabilities (732) (1,454)

(131) (211) (137) Pre-tax cash flows (1,145) (1,296)

Net cash from operating activities relating to the Gulf of Mexico oil spill, on a post-tax basis, amounted to an outflow of

$137 million and an outflow of $1,130 million in the fourth quarter and full year of 2015 respectively. For the same

periods in 2014, the amounts were an inflow of $304 million and an outflow of $9 million respectively.

18

Financial statements (continued)

Notes

2. Gulf of Mexico oil spill (continued)

Trust fund

BP established the Deepwater Horizon Oil Spill Trust (the Trust), funded in the amount of $20 billion, to satisfy legitimate

individual and business claims, state and local government claims resolved by BP, final judgments and settlements, state

and local response costs, and natural resource damages and related costs. Fines and penalties are not covered by the

trust fund.

The funding of the Trust was completed in 2012. The obligation to fund the $20-billion trust fund, adjusted to take

account of the time value of money, was recognized in full in 2010 and charged to the income statement. An asset has

been recognized representing BP’s right to receive reimbursement from the trust fund. This is the portion of the

estimated future expenditure provided for that will be settled by payments from the trust fund. During 2014, cumulative

charges to be paid by the Trust reached $20 billion. Subsequent additional costs, over and above those provided within

the $20 billion, are expensed to the income statement as incurred.

At 31 December 2015, $686 million of the provisions and payables are eligible to be paid from the Trust. The

reimbursement asset is recorded within Trade and other receivables on the balance sheet, all of which is classified as

current, as payment of all amounts covered by the remaining reimbursement asset may be requested during 2016.

During 2015, $3,022 million of provisions and $147 million of payables were paid from the Trust.

At 31 December 2015, the remaining cash in the Trust not allocated for specific purposes was $25 million. This

unallocated amount was exhausted in January 2016 and BP commenced paying claims and other costs not covered by

the specific-purpose cash balances. The total cash remaining in the Trust and associated qualifying settlement funds,

amounting to $1.4 billion, includes $0.7 billion in the seafood compensation fund, $0.2 billion held for natural resource

damage early restoration projects and $0.5 billion held in relation to certain other specified costs under the PSC

settlement.

(b) Provisions and contingent liabilities

BP has recorded certain provisions and disclosed certain contingent liabilities as a consequence of the Gulf of Mexico oil

spill. These are described below and in more detail in BP Annual Report and Form 20-F 2014 – Financial statements –

Note 2.

Provisions

BP has recorded provisions relating to the Gulf of Mexico oil spill in relation to environmental expenditure, litigation and

claims, and Clean Water Act penalties. Movements in each class of provision during the fourth quarter and full year are

presented in the table below.

Litigation Clean

and Water Act

$ million Environmental claims penalties Total

At 1 October 2015 6,004 6,644 4,179 16,827

Net increase (decrease) in provision (9) 575 – 566

Unwinding of discount 47 25 34 106

Change in discount rate (115) (59) (84) (258)

Utilization – paid by BP (1) (80) – (81)

– paid by the trust fund (7) (646) – (653)

At 31 December 2015 5,919 6,459 4,129 16,507

Of which – current 227 2,849 – 3,076

– non-current 5,692 3,610 4,129 13,431

Litigation Clean

and Water Act

Environmental claims penalties Total

$ million

At 1 January 2015 1,141 3,954 3,510 8,605

Net increase (decrease) in provision 5,393 5,832 661 11,886

Unwinding of discount 94 50 68 212

Change in discount rate (149) (74) (110) (333)

Reclassified to other payables (459) (125) – (584)

Utilization – paid by BP (23) (234) – (257)

– paid by the trust fund (78) (2,944) – (3,022)

At 31 December 2015 5,919 6,459 4,129 16,507

19

Financial statements (continued)

Notes

2. Gulf of Mexico oil spill (continued)

Environmental

The environmental provision includes amounts payable for natural resource damage costs under the proposed Consent

Decree. These amounts are payable in instalments over 16 years commencing one year after the court approves the

Consent Decree; the majority of the unpaid balance of this natural resource damages settlement accrues interest at a

fixed rate. Amounts payable under the $1-billion early restoration framework agreement with natural resource trustees

for the US and five Gulf states, that are not yet allocated to specific projects, are also included in environmental

provisions.

Litigation and claims

The litigation and claims provision includes amounts that can be estimated reliably for the future cost of settling claims

by individuals and businesses for damage to real or personal property, lost profits or impairment of earning capacity and

loss of subsistence use of natural resources (Individual and Business Claims), and amounts provided under the

Agreements in relation to state claims that have not yet been paid. Claims administration costs and legal costs have also

been provided for. Amounts that cannot be measured reliably and which have therefore not been provided for are

described under Contingent liabilities below.

Litigation and claims – PSC settlement

BP has provided for its best estimate of the cost associated with the 2012 PSC settlement agreements with the

exception of the cost of business economic loss claims, except where an eligibility notice has been issued and is not

subject to appeal by BP within the claims facility. See BP Annual Report and Form 20-F 2014 – Financial statements –

Note 2 and Legal proceedings on pages 228-237 for further details on the settlements with the PSC and related matters.

Management believes that no reliable estimate can currently be made of any business economic loss claims not yet

processed or processed but not yet paid, except where an eligibility notice has been issued and is not subject to appeal

by BP within the claims facility.

The submission deadline for business economic loss claims passed on 8 June 2015; no further claims may be submitted.

A significant number of business economic loss claims have been received but have not yet been processed and it is not

possible to quantify the total value of the claims.

A revised policy for the matching of revenue and expenses for business economic loss claims was introduced in May

2014 and, of the claims assessable under the revised policy, the majority have not yet been determined at this time.

Uncertainties regarding the proper application of the revised policy to particular claims and categories of claims continue

to arise as the claims administrator has applied the revised policy. Only a small proportion of claim determinations have

been made under some of the specialized frameworks that have been put in place for particular industries, namely

construction, agriculture, professional services and education, and so determinations to date may not be representative

of the total population of claims. In addition, although some pre-determination data has been provided to BP, detailed

data on the majority of pre-determination claims is not available due to a court order to protect claimant confidentiality.

Therefore there is an insufficient level of detail to enable a complete or clear understanding of the composition of the

underlying claims population.

There is insufficient data available to build up a track record of claims determinations under the policies and protocols

that are now being applied following resolution of the matching and causation issues. We are unable to reliably estimate

future trends of the number and proportion of claims that will be determined to be eligible, nor can we reliably estimate

the value of such claims. A provision for such business economic loss claims will be established when these

uncertainties are resolved and a reliable estimate can be made of the liability.

The current estimate for the total cost of those elements of the PSC settlement that BP considers can be reliably

estimated, including amounts already paid, is $12.4 billion. The Deepwater Horizon Court Supervised Settlement

Program (DHCSSP) has issued eligibility notices, many of which are disputed by BP, in respect of business economic

loss claims of approximately $402 million which have not been provided for. The total cost of the PSC settlement is likely

to be significantly higher than the amount recognized to date of $12.4 billion because the current estimate does not

reflect business economic loss claims not yet processed or processed but not yet paid, except where an eligibility notice

has been issued and is not subject to appeal by BP within the claims facility.

20

Financial statements (continued)

Notes

2. Gulf of Mexico oil spill (continued)

There continues to be a high level of uncertainty with regards to the amounts that ultimately will be paid in relation to

current claims as described above and the outcomes of any further litigation including by parties excluded from, or

parties who opted out of, the PSC settlement. There is also uncertainty as to the cost of administering the claims

process under the DHCSSP and in relation to future legal costs. The timing of payment of provisions related to the PSC

settlement is dependent upon ongoing claims facility activity and is therefore also uncertain.

Litigation and claims – other claims

The provision recognized for litigation and claims includes amounts agreed under the Agreements in relation to state

claims. The amount provided in respect of state claims is payable over 18 years from the date the court approves the

Consent Decree, of which $1 billion is due following the court approval of the Consent Decree. The vast majority of local

government entities who filed claims have issued releases, which were accepted by BP; amounts due under those

releases were paid during the third quarter of 2015.

Clean Water Act penalties

A provision has been recognized for penalties under Section 311 of the Clean Water Act, as determined in the

Agreements. The amount is payable in instalments over 15 years, commencing one year after the court approves the

Consent Decree. The unpaid balance of this penalty accrues interest at a fixed rate.

Provision movements and analysis of income statement charge

A net increase in provisions of $566 million and $11,886 million was recognized for the fourth quarter and full year

respectively. The fourth-quarter net increase arises primarily due to an increase in the litigation and claims provision for

business economic loss claims. The remainder of the income statement charge mainly relates to finance costs, offset by

adjustments to provisions due to discounting effects. The net increase for the full year also includes amounts provided

for the Agreements, and additional increases in the litigation and claims provision for business economic loss claims,

associated claims administration costs and other items. The following table shows an analysis of the income statement

charge.

Fourth Cumulative

quarter Year since the

$ million 2015 2015 incident

Environmental costs (124) 5,303 8,526

Spill response costs – – 14,304

Litigation and claims costs 516 5,758 32,538

Clean Water Act penalties – amount provided (84) 551 4,061

Other costs charged directly to the income statement 20 97 1,354

Recoveries credited to the income statement – – (5,681)

Charge (credit) related to the trust fund – – (137)

Other costs of the trust fund – – 8

Loss before interest and taxation 328 11,709 54,973

Finance costs – related to the trust funds – – 137

– not related to the trust funds 115 247 341

Loss before taxation 443 11,956 55,451

Further information on provisions is provided in BP Annual Report and Form 20-F 2014 – Financial statements – Note 2.

21

Financial statements (continued)

Notes

2. Gulf of Mexico oil spill (continued)

Contingent liabilities

BP currently considers that it is not possible to measure reliably other obligations arising from the incident, including:

Claims asserted in civil litigation, including any further litigation by parties excluded from, or parties who opted out

of, the PSC settlement, including as set out in Legal proceedings on pages 228-237 of BP Annual Report and Form

20-F 2014, except for claims covered by the Agreements.

The cost of business economic loss claims under the PSC settlement not yet processed or processed but not yet

paid (except where an eligibility notice has been issued and is not subject to appeal by BP within the claims facility).

Any obligation that may arise from securities-related litigation.

Any obligation in relation to other potential private or non-US government litigation or claims (except for those items

provided for as described above under Provisions).

It is not practicable to estimate the magnitude or possible timing of payment of these contingent liabilities.

As a result of the Agreements, contingent liabilities are no longer disclosed in relation to Clean Water Act penalties,

natural resource damages and state claims and the vast majority of local government entity claims. See additional

information on the Agreements above.

The magnitude and timing of all possible obligations in relation to the Gulf of Mexico oil spill continue to be subject to

uncertainty.

See also BP Annual Report and Form 20-F 2014 – Financial statements – Note 2.

3. Non-current assets held for sale

On 15 January 2016 BP and Rosneft announced that they had signed definitive agreements to dissolve the German

refining joint operation Ruhr Oel GmbH (ROG). The restructuring, which is expected to be completed in 2016, will result

in Rosneft taking ownership of ROG’s interests in the Bayernoil, MiRO Karlsruhe and PCK Schwedt refineries. In

exchange, BP will take sole ownership of the Gelsenkirchen refinery and the solvent production facility DHC Solvent

Chemie. Assets and associated liabilities relating to BP’s share of ROG’s interests in the Bayernoil, MiRO Karlsruhe and

PCK Schwedt refineries have been classified as held for sale in the group balance sheet at 31 December 2015.

4. Impairment of fixed assets

The net impairment loss for the fourth quarter and full year is $2,014 million and $2,357 million respectively. Of this total

amount, $1,303 million and $1,646 million respectively is included within the line item in the income statement for

Impairment and losses on sale of businesses and fixed assets. The remaining $711 million in the fourth quarter and full

year relates to BP’s share of impairment charges recognized by equity-accounted entities included in the income

statement line item Earnings from joint ventures – after interest and tax.

The fourth-quarter net impairment loss comprised $1,579 million in Upstream, $156 million in Downstream, and

$279 million in Other businesses and corporate. The full-year net impairment loss comprised $1,960 million in Upstream,

$87 million in Downstream, and $310 million in Other businesses and corporate.

The net impairment loss in Upstream, including BP’s share of impairment charges recognized by equity-accounted

entities, comprised impairment losses of $2,572 million and $3,040 million for the fourth quarter and full year

respectively, and impairment reversals of $993 million and $1,080 million for the same periods. Impairment losses have

been recorded in a number of regions with the largest charge arising in Angola, a significant element of which relates to

the Angola LNG plant. Impairment losses also included charges in relation to assets in the North Sea but these were

more than offset by impairment reversals in relation to other assets in the region.

The impairment losses primarily arose as a result of a lower price environment, technical reserves revisions, and

increases in decommissioning cost estimates for certain assets. The impairment reversals arose mainly as a result of

decreases in cost estimates and a reduction in the discount rate applied, offsetting the impact of lower prices.

22

Financial statements (continued)

Notes

5. Analysis of replacement cost profit (loss) before interest and tax and reconciliation

to profit (loss) before taxation

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

(3,085) 743 (2,280) Upstream (937) 8,934

780 2,562 838 Downstream 7,111 3,738 451 382 235 Rosneft 1,310 2,100 (647) (378) (627) Other businesses and corporate (1,768) (2,010) (2,501) 3,309 (1,834) 5,716 12,762 (468) (311) (328) Gulf of Mexico oil spill response (11,709) (781) 257 67 65 Consolidation adjustment – UPII* (36) 641 (2,712) 3,065 (2,097) RC profit (loss) before interest and tax (6,029) 12,622 Inventory holding gains (losses)* (80) (27) (18) Upstream (30) (86) (4,844) (1,687) (1,482) Downstream (1,863) (6,100) (61) (12) (46) Rosneft (net of tax) 4 (24) (7,697) 1,339 (3,643) Profit (loss) before interest and tax (7,918) 6,412 299 398 379 Finance costs 1,347 1,148 Net finance expense relating to pensions 82 76 78 and other post-retirement benefits 306 314 (8,078) 865 (4,100) Profit (loss) before taxation (9,571) 4,950 RC profit (loss) before interest and tax* 683 324 (1,429) US (12,243) 5,251 (3,395) 2,741 (668) Non-US 6,214 7,371 (2,712) 3,065 (2,097) (6,029) 12,622

23

Financial statements (continued)

Notes

6. Sales and other operating revenues

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

By segment

15,800 10,357 10,212 Upstream 43,235 65,424

65,249 50,921 43,463 Downstream(a) 200,569 323,486

616 552 556 Other businesses and corporate 2,048 1,989

81,665 61,830 54,231 245,852 390,899

Less: sales and other operating revenues

between segments

8,270 5,809 4,987 Upstream 21,949 36,643

(814) (377) (133) Downstream 68 (173)

212 246 205 Other businesses and corporate 941 861

7,668 5,678 5,059 22,958 37,331

Third party sales and other operating revenues

7,530 4,548 5,225 Upstream 21,286 28,781

66,063 51,298 43,596 Downstream(a) 200,501 323,659

404 306 351 Other businesses and corporate 1,107 1,128

73,997 56,152 49,172 Total sales and other operating revenues 222,894 353,568

By geographical area

27,300 20,680 16,936 US 78,281 132,310

51,933 39,200 34,773 Non-US(a) 158,519 251,943

79,233 59,880 51,709 236,800 384,253

Less: sales and other operating revenues

5,236 3,728 2,537 between areas 13,906 30,685

73,997 56,152 49,172 222,894 353,568

(a) Amounts reported in the prior quarters of 2015 for Downstream and Total sales and other operating revenues have been

amended. Amended Total sales and other operating revenues are $55,519 million for the first quarter 2015, $62,051 million

for the second quarter 2015 and $56,152 million for the third quarter 2015. The previously reported amounts for Total sales

and other operating revenues were $54,196 million, $60,646 million and $54,730 million respectively. Purchases have been

amended by the same amounts and therefore there is no impact on reported profit.

7. Production and similar taxes

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

56 30 118 US 215 690

356 208 145 Non-US 821 2,268

412 238 263 1,036 2,958

8. Earnings per share and shares in issue

Basic earnings per ordinary share (EpS) amounts are calculated by dividing the profit for the period attributable to ordinary

shareholders by the weighted average number of ordinary shares outstanding during the period.

The calculation of EpS is performed separately for each discrete quarterly period, and for the year-to-date period. As a

result, the sum of the discrete quarterly EpS amounts in any particular year-to-date period may not be equal to the EpS

amount for the year-to-date period.

24

Financial statements (continued)

Notes

8. Earnings per share and shares in issue (continued)

For the diluted EpS calculation the weighted average number of shares outstanding during the period is adjusted for the

number of shares that are potentially issuable in connection with employee share-based payment plans using the

treasury stock method.

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 $ million 2015 2014

Results for the period

Profit (loss) for the period attributable

(4,407) 46 (3,307) to BP shareholders (6,482) 3,780

1 – 1 Less: preference dividend 2 2

Profit (loss) attributable to BP

(4,408) 46 (3,308) ordinary shareholders (6,484) 3,778

Number of shares (thousand)(a)(b)

Basic weighted average number

18,232,147 18,329,701 18,369,064 of shares outstanding 18,323,646 18,385,458

3,038,691 3,054,950 3,061,510 ADS equivalent 3,053,941 3,064,243

Weighted average number of

shares outstanding used to

18,232,147 18,371,656 18,369,064 calculate diluted earnings per share 18,323,646 18,497,294

3,038,691 3,061,942 3,061,510 ADS equivalent 3,053,941 3,082,882

18,199,882 18,349,963 18,412,392 Shares in issue at period-end 18,412,392 18,199,882

3,033,313 3,058,327 3,068,732 ADS equivalent 3,068,732 3,033,313

(a) Excludes treasury shares and includes certain shares that will be issued in the future under employee share-based payment

plans.

(b) If the inclusion of potentially issuable shares would decrease loss per share, the potentially issuable shares are excluded from

the weighted average number of shares outstanding used to calculate diluted earnings per share.

9. Dividends

Dividends payable

BP today announced an interim dividend of 10.00 cents per ordinary share which is expected to be paid on 24 March

2016 to shareholders and American Depositary Share (ADS) holders on the register on 12 February 2016. The

corresponding amount in sterling is due to be announced on 14 March 2016, calculated based on the average of the

market exchange rates for the four dealing days commencing on 8 March 2016. Holders of ADSs are expected to receive

$0.600 per ADS (less applicable fees). A scrip dividend alternative is available, allowing shareholders to elect to receive

their dividend in the form of new ordinary shares and ADS holders in the form of new ADSs. Details of the fourth-quarter

dividend and timetable are available at bp.com/dividends and details of the scrip dividend programme are available at

bp.com/scrip.

Dividends paid

Fourth Third Fourth

quarter quarter quarter Year Year

2014 2015 2015 2015 2014

Dividends paid per ordinary share

10.000 10.000 10.000 cents 40.000 39.000