branch workforce optimization driven by analytics:

TRANSCRIPT

Branch Workforce Optimization Driven By Analytics:The Evolution of the Workforce through Advanced AnalyticsSecond Annual Survey of Banking Executives

INTELLIGENT BRANCH TRANSFORMATION®

© 2016 Kiran Analytics, Inc. All rights reserved.

Branch Workforce Optimization Driven By Analytics 2

3 Executive SummaryKiran Analytics conducted a second annual online survey of retail banks to gain insights on top branch workforce challenges and optimization strategies using advanced analytics.

4 Key Findings

5The Role of the Branch in Omni-Channel DeliveryThe branch is alive and well. Banks are evolving their role to deepen customer relationships, acquire new accounts, and generate referrals.

6 Top Branch Transformation InitiativesWorkforce optimization remains a top branch transformation priority.

7 Workforce Optimization For Revenue GrowthWorkforce optimization priorities have shifted focus from last year.

8Branch Workforce Planning Inability to align selling capacity with market opportunity limits revenue growth. Excess capacity and high turnover increases operational expenses.

9 Branch Workforce Requirements and StrategiesA widely popular strategy is the adoption of the universal banker staffing model.

11Advanced Analytics for Optimizing the WorkforceAs the pace of branch transformation accelerates, so does the adoption of advanced analytics for workforce decisions.

12 Key Takeaways

Table of Contents

Branch Workforce Optimization Driven By Analytics 3

© 2016 Kiran Analytics, Inc. All rights reserved.

Between March and June of 2016, Kiran Analytics conducted a second annual survey of banking leaders digging deeper into their branch transformation initiatives, workforce optimization strategies, and workforce analytics maturity. This included participants from 50 retail banks in North America to gain insights on:

• The role of the branch in omni-channel distribution strategy

• Branch transformation initiatives for delivering exceptional customer experience

• Branch workforce challenges

• Priorities for optimizing the branch workforce

• Branch staffing strategies

• Applications of advanced analytics for workforce optimization

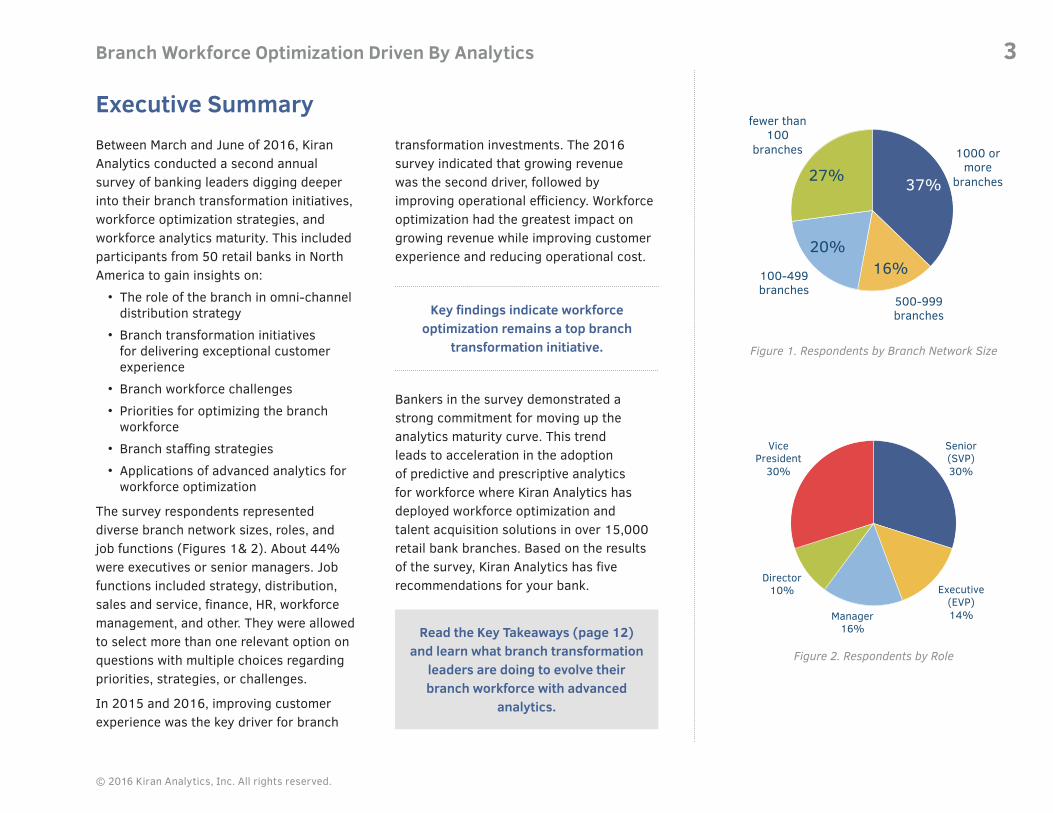

The survey respondents represented diverse branch network sizes, roles, and job functions (Figures 1& 2). About 44% were executives or senior managers. Job functions included strategy, distribution, sales and service, finance, HR, workforce management, and other. They were allowed to select more than one relevant option on questions with multiple choices regarding priorities, strategies, or challenges.

In 2015 and 2016, improving customer experience was the key driver for branch

transformation investments. The 2016 survey indicated that growing revenue was the second driver, followed by improving operational efficiency. Workforce optimization had the greatest impact on growing revenue while improving customer experience and reducing operational cost.

Executive Summary

Figure 1. Respondents by Branch Network Size

1000 or more

branches

500-999 branches

100-499 branches

fewer than 100

branches

Senior (SVP) 30%

Executive (EVP) 14% Manager

16%

Director 10%

Vice President

30%

Key findings indicate workforce optimization remains a top branch

transformation initiative.

Figure 2. Respondents by Role

Bankers in the survey demonstrated a strong commitment for moving up the analytics maturity curve. This trend leads to acceleration in the adoption of predictive and prescriptive analytics for workforce where Kiran Analytics has deployed workforce optimization and talent acquisition solutions in over 15,000 retail bank branches. Based on the results of the survey, Kiran Analytics has five recommendations for your bank.

Read the Key Takeaways (page 12) and learn what branch transformation

leaders are doing to evolve their branch workforce with advanced

analytics.

37%

16% 20%

27%

Branch Workforce Optimization Driven By Analytics 4

© 2016 Kiran Analytics, Inc. All rights reserved.

The branch is alive and well. Face-to-face interactions, new account openings, and convenient access to bankers are top reasons why banking leaders think the branch is a key component of their omni-channel delivery strategy.

Retail banks are continuing to transform their branches. The top four initiatives for branch transformation are:

1. Workforce optimization2. Customer migration to digital channels3. Network optimization4. In-branch technology deployment

Workforce optimization priorities are shifting to growth-oriented ones.

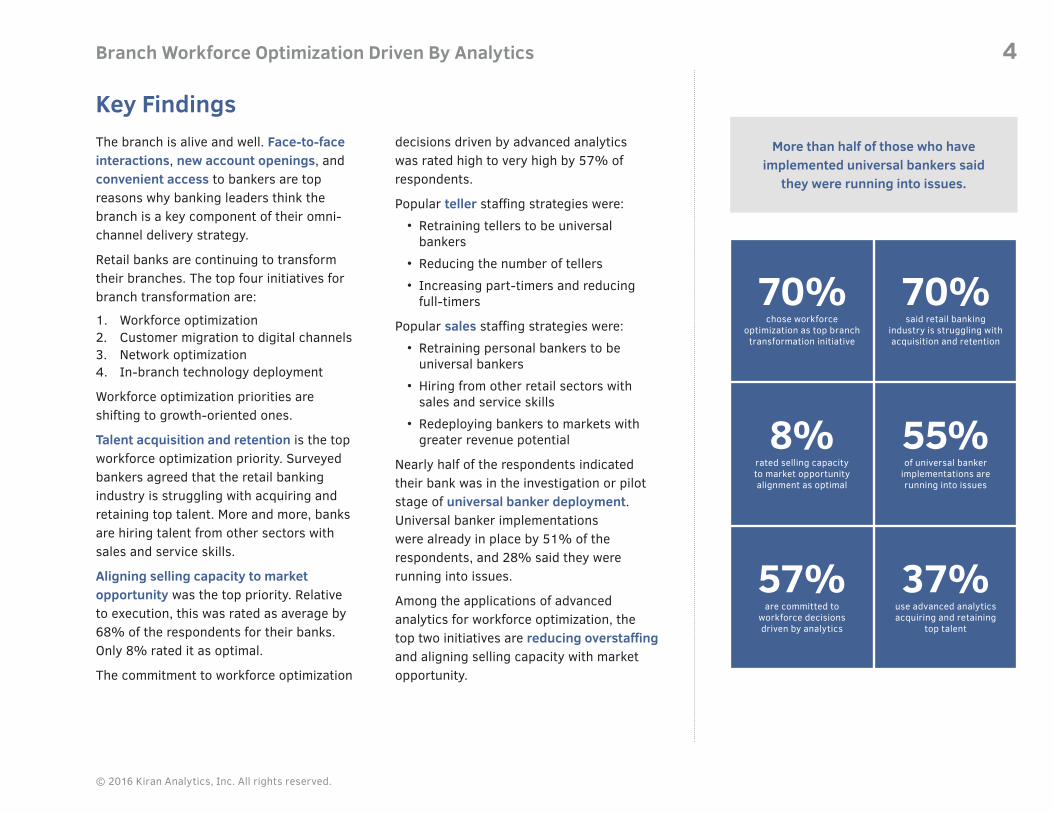

Talent acquisition and retention is the top workforce optimization priority. Surveyed bankers agreed that the retail banking industry is struggling with acquiring and retaining top talent. More and more, banks are hiring talent from other sectors with sales and service skills.

Aligning selling capacity to market opportunity was the top priority. Relative to execution, this was rated as average by 68% of the respondents for their banks. Only 8% rated it as optimal.

The commitment to workforce optimization

decisions driven by advanced analytics was rated high to very high by 57% of respondents.

Popular teller staffing strategies were:

• Retraining tellers to be universal bankers

• Reducing the number of tellers

• Increasing part-timers and reducing full-timers

Popular sales staffing strategies were:

• Retraining personal bankers to be universal bankers

• Hiring from other retail sectors with sales and service skills

• Redeploying bankers to markets with greater revenue potential

Nearly half of the respondents indicated their bank was in the investigation or pilot stage of universal banker deployment. Universal banker implementations were already in place by 51% of the respondents, and 28% said they were running into issues.

Among the applications of advanced analytics for workforce optimization, the top two initiatives are reducing overstaffing and aligning selling capacity with market opportunity.

Key Findings

8%rated selling capacity to market opportunity alignment as optimal

55%of universal banker

implementations are running into issues

57%are committed to

workforce decisionsdriven by analytics

37%use advanced analytics acquiring and retaining

top talent

70%chose workforce

optimization as top branch transformation initiative

70%said retail banking

industry is struggling with acquisition and retention

More than half of those who have implemented universal bankers said

they were running into issues.

Branch Workforce Optimization Driven By Analytics 5

© 2016 Kiran Analytics, Inc. All rights reserved.

Customers want to interact with the bank when, where, and how they want. Yes, customer visits and transactions in the branch are declining and the use of mobile devices is increasing; yet, consumers (even millennials) still prefer face-to-face interactions in the branches, especially for complex financial transactions.

To capitalize on consumer preferences, some banks are turning to initiatives which convert branches into advisory centers with smaller physical footprints instead of closing branch locations.1

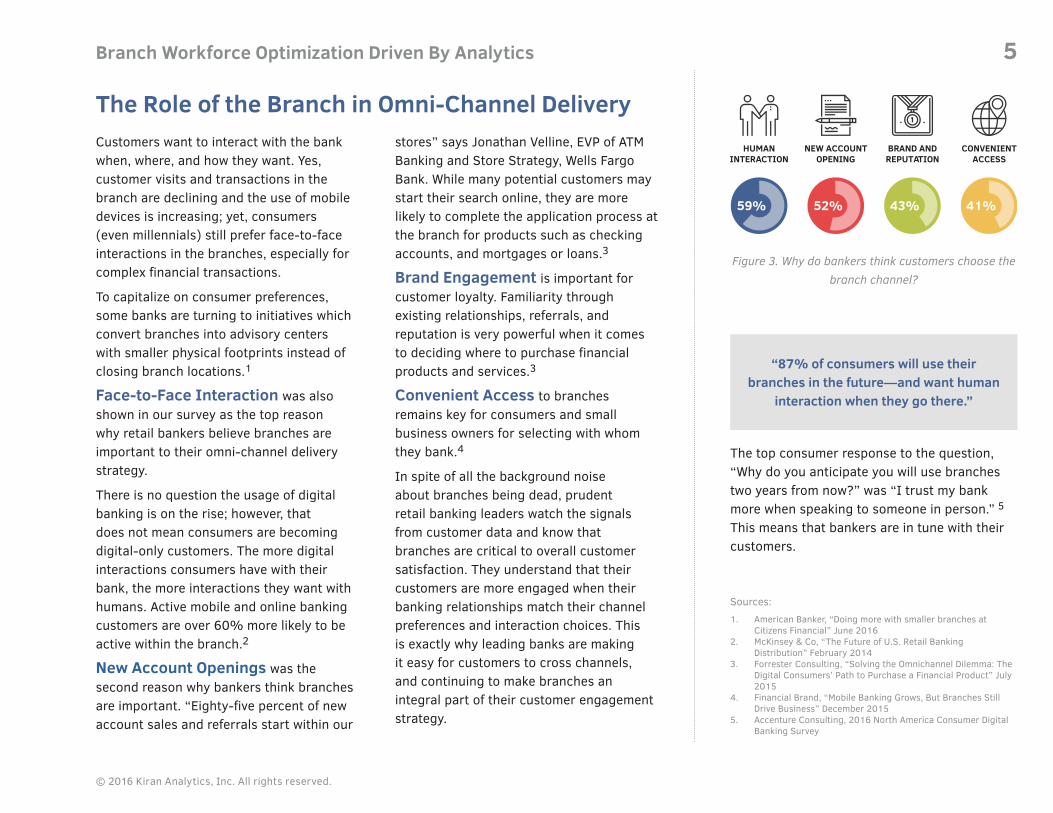

Face-to-Face Interaction was also shown in our survey as the top reason why retail bankers believe branches are important to their omni-channel delivery strategy.

There is no question the usage of digital banking is on the rise; however, that does not mean consumers are becoming digital-only customers. The more digital interactions consumers have with their bank, the more interactions they want with humans. Active mobile and online banking customers are over 60% more likely to be active within the branch.2

New Account Openings was the second reason why bankers think branches are important. “Eighty-five percent of new account sales and referrals start within our

stores” says Jonathan Velline, EVP of ATM Banking and Store Strategy, Wells Fargo Bank. While many potential customers may start their search online, they are more likely to complete the application process at the branch for products such as checking accounts, and mortgages or loans.3

Brand Engagement is important for customer loyalty. Familiarity through existing relationships, referrals, and reputation is very powerful when it comes to deciding where to purchase financial products and services.3

Convenient Access to branches remains key for consumers and small business owners for selecting with whom they bank.4

In spite of all the background noise about branches being dead, prudent retail banking leaders watch the signals from customer data and know that branches are critical to overall customer satisfaction. They understand that their customers are more engaged when their banking relationships match their channel preferences and interaction choices. This is exactly why leading banks are making it easy for customers to cross channels, and continuing to make branches an integral part of their customer engagement strategy.

The Role of the Branch in Omni-Channel Delivery

Figure 3. Why do bankers think customers choose the branch channel?

Sources: 1. American Banker, “Doing more with smaller branches at

Citizens Financial” June 20162. McKinsey & Co, “The Future of U.S. Retail Banking

Distribution” February 20143. Forrester Consulting, “Solving the Omnichannel Dilemma: The

Digital Consumers’ Path to Purchase a Financial Product” July 2015

4. Financial Brand, “Mobile Banking Grows, But Branches Still Drive Business” December 2015

5. Accenture Consulting, 2016 North America Consumer Digital Banking Survey

HUMANINTERACTION

NEW ACCOUNTOPENING

BRAND AND REPUTATION

CONVENIENT ACCESS

“87% of consumers will use their branches in the future—and want human

interaction when they go there.”

The top consumer response to the question, “Why do you anticipate you will use branches two years from now?” was “I trust my bank more when speaking to someone in person.” 5

This means that bankers are in tune with their customers.

Branch Workforce Optimization Driven By Analytics 6

© 2016 Kiran Analytics, Inc. All rights reserved.

The top branch transformation initiatives are focused on improving customer experience while growing revenue and lowering operating costs:

• Evolving workforce skills and capacity to meet the changing nature of consumer interactions in the branches.

• Migrating customers to digital channels for routine transactions such as making payments, depositing checks, or checking account balances.

• Empowering customers with in-branch technologies such as self-service, banker and video-assisted services.

• Aligning branch network locations and formats with market opportunities.

• Redesigning or upgrading the facilities to meet the changing nature of customer interactions.

Workforce Optimization was still the top initiative. Why? Because about 25% of the total cost of operating a retail bank is in branch staffing (Figure 5). First, it is important from an operational efficiency perspective. Customers do not go to the branch to see the facility. They go there to see a banker. When customer interactions with the bank involve the branch staff, the opportunity for deepening relationships and increasing revenue is improved. Workforce optimization was also selected as having the greatest impact on growing revenue (38%).

Channel Migration was the second most important initiative of 2016. It has become a high priority because consumer use of digital channels for simple transactions has grown rapidly, and banks have significantly improved the usability and functionality of their mobile applications. Banks must become increasingly agile to meet the demands of customer expectations and the accelerated use of mobile.1

Network Optimization, the alignment of the branch network with the needs of micro-markets and trade areas, continues to be a high transformation priority. Whenever possible, banks reduce the footprint of existing branches and in areas with slow demand, they close facilities or avoid investments. They upgrade facilities or open smaller branches in areas with growth potential.2

Deploying technology had the most significant change, dropping 17% from second to fourth place.

Top Branch Transformation Initiatives 70%

60%

59%

46%

35%

70%

52%

63%

41%

Optimizing the workforce

Migrating to digital channels

Optimize branch locations

Deploy technology

Redesign branch formats

2016 2015

Figure 4. Top Initiatives from 2016 and 2015

Sources: 1. Forrester Consulting, “Solving the Omnichannel Dilemma: The

Digital Consumers’ Path to Purchase a Financial Product” July 2015

2. IDC Financial Insights, “End-to-End Benefits of a Transformed Branch Network” July 2014

“While there have been tremendous innovations around mobile banking... the branch remains the center of that

relationship... with our customers.”

Barry Sommers, CEO of Chase’s Consumer Bank

25%Branch Staffing

Figure 5. 54% of the branch network cost is in branch staffing

Branch Workforce Optimization Driven By Analytics 7

© 2016 Kiran Analytics, Inc. All rights reserved.

The top five critical priorities for workforce optimization (Figure 6) were:

• Acquiring and retaining top talent

• Aligning selling capacity to market opportunity

• Providing sales training and incentives

• Deploying universal banker

• Reducing over-staffing

Acquisition and Retention is still the Achilles heel for branch staffing with over two-thirds of surveyed bankers agreeing that retail banking as an industry is struggling with it.

Retention was chosen by 54% of the respondents as one of the biggest workforce challenges (Figure 6). In the 2015 survey, 67% indicated that turnover was the number one challenge.

Slow adoption of analytics in human resources is a contributing factor to high turnover and performance variability. High employee turnover results in increased hiring and training costs. Increased performance variability adversely impacts service quality and branch productivity.

Recruiting was the second highest workforce challenge and was chosen by 46%. Similarly, quality of new hires

was ranked second in 2015 at 49%. It comes as no surprise then that acquiring and retaining top talent was the highest workforce optimization priority at 71% (Figure 7). In 2015, only 59% of those surveyed chose acquisition as a top priority, which means it moved up to first place.

Alignment of Selling Capacityof their banks to market opportunity was rated as average by 68% of the bankers (Figure 8). Only 8% rated it as optimal. This explains why it has moved up to second place as a priority and implies that bankers believe they have a significant opportunity to better deploy their sales resources.

Sales Training and Incentives is still within the top three priorities, but it has dropped from 64% to 54% from the previous year.

Universal Banker Deployment was the fourth priority which has become a very popular workforce strategy.

Branch Staff Reduction was the fifth priority which is focused on improving operational efficiency. It was also the top reason banks are using advanced analytics for workforce decisions.

Workforce Optimization For Revenue Growth

Figure 7. Critical priorities for optimizing workforce

71%

64%

54%

49%

48%

Acquiring and retaining top talent

Aligning selling capacity to market opportunity

Providing sales training and incentives

Deploying universal banker

Reducing over-staffing

Below average

5%

Average 68%

Suboptimal 18%

Optimal 8%

Figure 8. Surveyed bankers rated the alignment of selling capacity to market opportunity of their banks

54%

46%

67%

49%

Retention

Recruiting

2016 2015

Figure 6. Top two workforce challenges

Branch Workforce Optimization Driven By Analytics 8

© 2016 Kiran Analytics, Inc. All rights reserved.

There are several factors contributing to the challenges of workforce planning.

Migration to Digital Channels Banks are pushing for increased customer use of digital channels for routine transactions and branch visits are declining, but it does not completely eliminate them. Branch staff still needs to be available to handle these transactions.

Changing Operating Hours Some banks are reducing the number of branches in an area, but increasing the number of open hours for the remaining branches. This strategy inevitably impacts full time, part-time, and peak-time staffing. For branches with longer open hours, more flexible capacity is needed, which means the ratio of part-time to full-time needs to be higher in those branches.

Capacity Planning Branches should be staffed in a holistic manner to provide day-to-day staffing matched to customer demand, customer demographics, and market opportunity.

Pooling Staff ResourcesTo minimize staff overhead, some banks are employing branch managers who manage more than one branch. Other resources are

shared through the use of new technology such as video. Some banks are also creating resource pools to more effectively manage absences and vacancies. Pooled resources provide flexibility and cost savings, and can benefit the bank, its employees, and customers.

Environmental and Facility ChangesRedesigning branch formats was one of the top five initiatives at 35% (Figure 4, page 6). Instead of reducing the number of branches and negatively impacting the ubiquity of their brand, banks have turned to converting locations into different formats to meet changing customer demands. This also impacts the staffing required to maintain these locations.

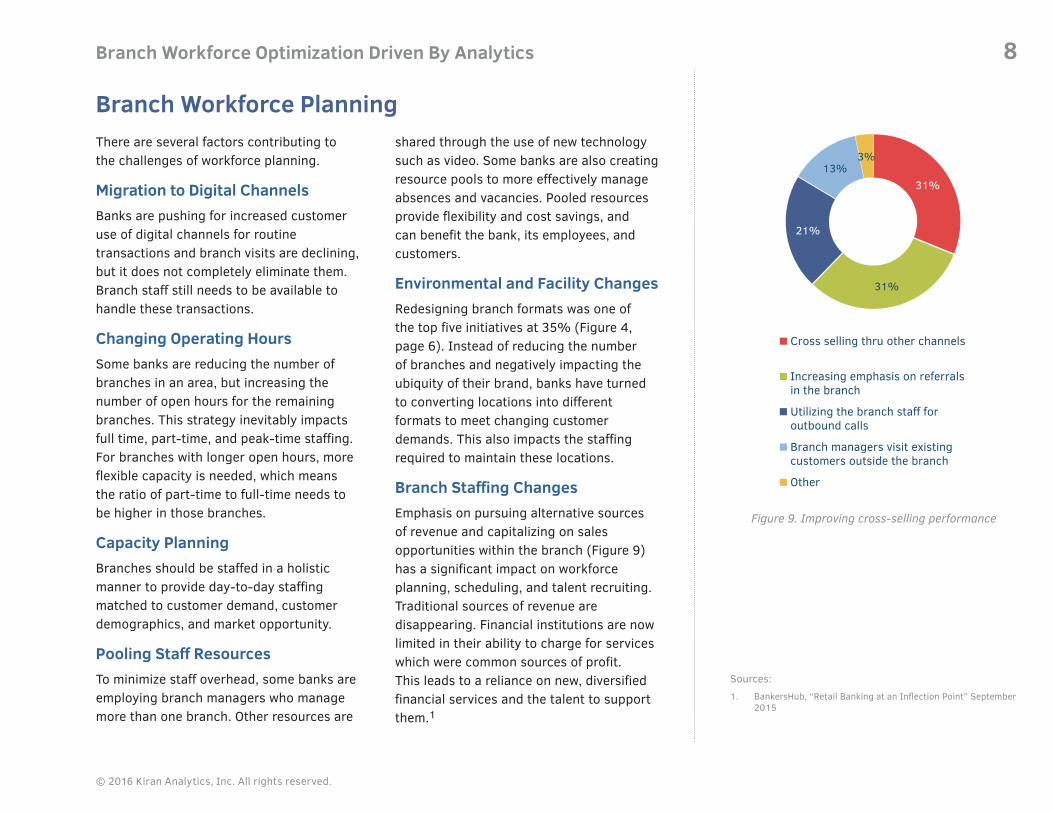

Branch Staffing ChangesEmphasis on pursuing alternative sources of revenue and capitalizing on sales opportunities within the branch (Figure 9) has a significant impact on workforce planning, scheduling, and talent recruiting.Traditional sources of revenue are disappearing. Financial institutions are now limited in their ability to charge for services which were common sources of profit. This leads to a reliance on new, diversified financial services and the talent to support them.1

Branch Workforce Planning

Sources: 1. BankersHub, “Retail Banking at an Inflection Point” September

2015

31%

31%

21%

13% 3%

Cross selling thru other channels

Increasing emphasis on referrals in the branch

Utilizing the branch staff for outbound calls

Branch managers visit existing customers outside the branch

Other

Figure 9. Improving cross-selling performance

31%

31%

21%

13% 3%

Cross selling thru other channels

Increasing emphasis on referrals in the branch

Utilizing the branch staff for outbound calls

Branch managers visit existing customers outside the branch

Other

Branch Workforce Optimization Driven By Analytics 9

© 2016 Kiran Analytics, Inc. All rights reserved.

In the face of pressure to cut labor costs and migrate consumers to less expensive digital channels, most banks are struggling with what to do about evolving and optimizing their branch workforce. Along with the changing role of the branch, customer-facing branch staffing requirements have also changed.

Requirements• Generalization—not just good at

account openings and loans, but also mobile banking and financial advice

• Increased need for engagement, relationship growth, and consultative selling skills

• Complex service delivery and issue resolution skills

• Tech savvy and digital native bankers

To maintain high levels of customer satisfaction with fewer branches and staff,

branch personnel must change what they do and how they do it. Customers still want to interact with them, but not for the same reasons as in the past.

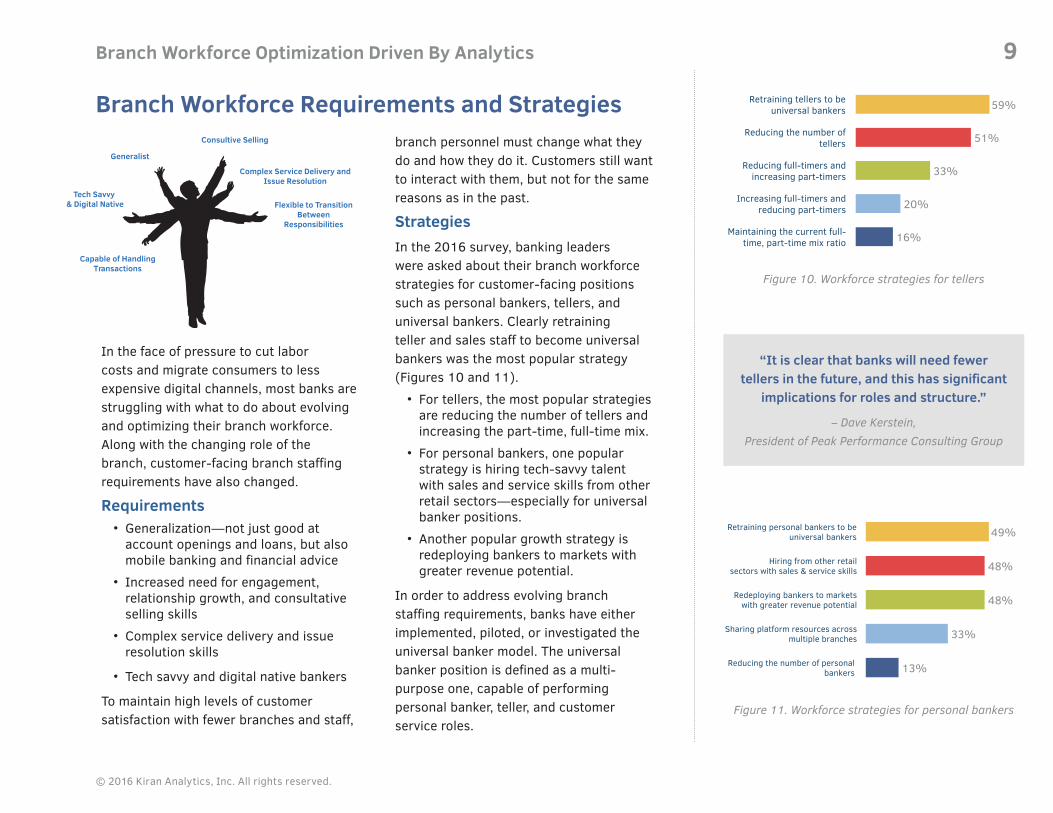

StrategiesIn the 2016 survey, banking leaders were asked about their branch workforce strategies for customer-facing positions such as personal bankers, tellers, and universal bankers. Clearly retraining teller and sales staff to become universal bankers was the most popular strategy (Figures 10 and 11).

• For tellers, the most popular strategies are reducing the number of tellers and increasing the part-time, full-time mix.

• For personal bankers, one popular strategy is hiring tech-savvy talent with sales and service skills from other retail sectors—especially for universal banker positions.

• Another popular growth strategy is redeploying bankers to markets with greater revenue potential.

In order to address evolving branch staffing requirements, banks have either implemented, piloted, or investigated the universal banker model. The universal banker position is defined as a multi-purpose one, capable of performing personal banker, teller, and customer service roles.

Branch Workforce Requirements and Strategies

Figure 11. Workforce strategies for personal bankers

59%

51%

33%

20%

16%

Retraining tellers to be universal bankers

Reducing the number of tellers

Reducing full-timers and increasing part-timers

Increasing full-timers and reducing part-timers

Maintaining the current full-time, part-time mix ratio

Figure 10. Workforce strategies for tellers

Generalist

Tech Savvy & Digital Native

Capable of HandlingTransactions

Flexible to TransitionBetween

Responsibilities

Consultive Selling

Complex Service Delivery andIssue Resolution

49%

48%

48%

33%

13%

Retraining personal bankers to be universal bankers

Hiring from other retail sectors with sales & service skills

Redeploying bankers to markets with greater revenue potential

Sharing platform resources across multiple branches

Reducing the number of personal bankers

“It is clear that banks will need fewer tellers in the future, and this has significant

implications for roles and structure.”

– Dave Kerstein, President of Peak Performance Consulting Group

Branch Workforce Optimization Driven By Analytics 10

© 2016 Kiran Analytics, Inc. All rights reserved.

Dave Martin, President of Bancmechanics, says, “The concept of a universal banker is not a new one. In-store bankers have been fulfilling the roles of universal bankers for a few decades. It’s making more sense to incorporate the universal banker model in all branch formats going forward.”

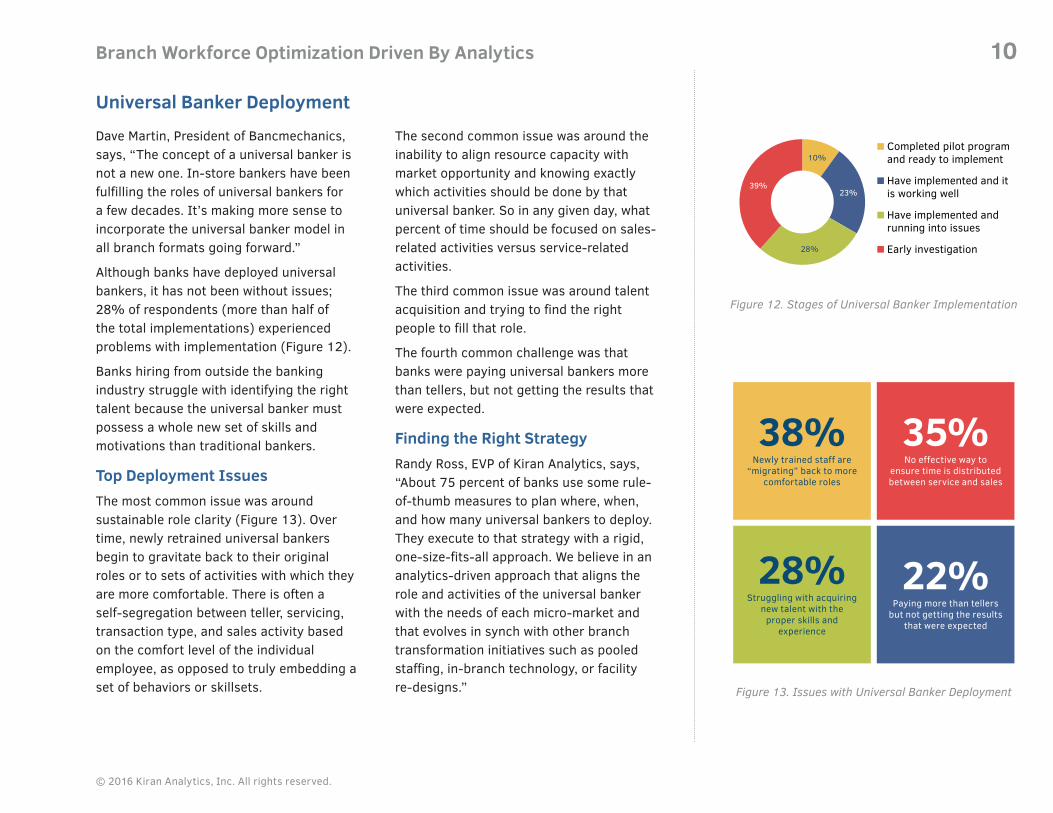

Although banks have deployed universal bankers, it has not been without issues; 28% of respondents (more than half of the total implementations) experienced problems with implementation (Figure 12).

Banks hiring from outside the banking industry struggle with identifying the right talent because the universal banker must possess a whole new set of skills and motivations than traditional bankers.

Top Deployment IssuesThe most common issue was around sustainable role clarity (Figure 13). Over time, newly retrained universal bankers begin to gravitate back to their original roles or to sets of activities with which they are more comfortable. There is often a self-segregation between teller, servicing, transaction type, and sales activity based on the comfort level of the individual employee, as opposed to truly embedding a set of behaviors or skillsets.

The second common issue was around the inability to align resource capacity with market opportunity and knowing exactly which activities should be done by that universal banker. So in any given day, what percent of time should be focused on sales-related activities versus service-related activities.

The third common issue was around talent acquisition and trying to find the right people to fill that role.

The fourth common challenge was that banks were paying universal bankers more than tellers, but not getting the results that were expected.

Finding the Right StrategyRandy Ross, EVP of Kiran Analytics, says, “About 75 percent of banks use some rule-of-thumb measures to plan where, when, and how many universal bankers to deploy. They execute to that strategy with a rigid, one-size-fits-all approach. We believe in an analytics-driven approach that aligns the role and activities of the universal banker with the needs of each micro-market and that evolves in synch with other branch transformation initiatives such as pooled staffing, in-branch technology, or facility re-designs.” Figure 13. Issues with Universal Banker Deployment

10%

23%

28%

39%

Completed pilot program and ready to implement

Have implemented and it is working well

Have implemented and running into issues

Early investigation

Figure 12. Stages of Universal Banker Implementation

38%Newly trained staff are

“migrating” back to more comfortable roles

35%No effective way to

ensure time is distributed between service and sales

28%Struggling with acquiring

new talent with the proper skills and

experience

22%Paying more than tellers

but not getting the results that were expected

Universal Banker Deployment

Branch Workforce Optimization Driven By Analytics 11

© 2016 Kiran Analytics, Inc. All rights reserved.

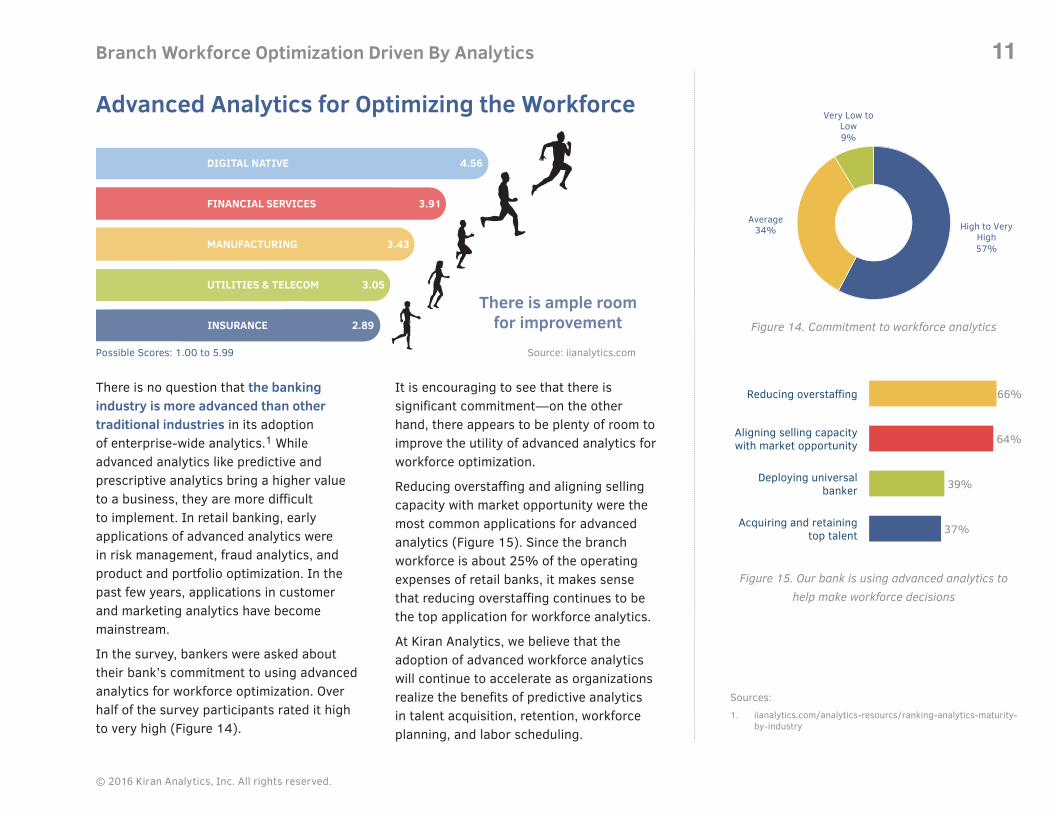

There is no question that the banking industry is more advanced than other traditional industries in its adoption of enterprise-wide analytics.1 While advanced analytics like predictive and prescriptive analytics bring a higher value to a business, they are more difficult to implement. In retail banking, early applications of advanced analytics were in risk management, fraud analytics, and product and portfolio optimization. In the past few years, applications in customer and marketing analytics have become mainstream.

In the survey, bankers were asked about their bank’s commitment to using advanced analytics for workforce optimization. Over half of the survey participants rated it high to very high (Figure 14).

It is encouraging to see that there is significant commitment—on the other hand, there appears to be plenty of room to improve the utility of advanced analytics for workforce optimization.

Reducing overstaffing and aligning selling capacity with market opportunity were the most common applications for advanced analytics (Figure 15). Since the branch workforce is about 25% of the operating expenses of retail banks, it makes sense that reducing overstaffing continues to be the top application for workforce analytics.

At Kiran Analytics, we believe that the adoption of advanced workforce analytics will continue to accelerate as organizations realize the benefits of predictive analytics in talent acquisition, retention, workforce planning, and labor scheduling.

Advanced Analytics for Optimizing the Workforce

66%

64%

39%

37%

Reducing overstaffing

Aligning selling capacity with market opportunity

Deploying universal banker

Acquiring and retaining top talent

Figure 15. Our bank is using advanced analytics to help make workforce decisions

High to Very High 57%

Average 34%

Very Low to Low 9%

Figure 14. Commitment to workforce analytics

Possible Scores: 1.00 to 5.99 Source: iianalytics.com

Sources: 1. iianalytics.com/analytics-resourcs/ranking-analytics-maturity-

by-industry

Branch Workforce Optimization Driven By Analytics 12

© 2016 Kiran Analytics, Inc. All rights reserved.

Face-to-face interactions and new account openings in bank branches provide the best opportunities to deepen customer relationships and build trust critical to customer loyalty and revenue generation. The quality of these interactions heavily depends on having the right staff in front of the customer at the right time and place. Retail banking leaders are keenly aware of this. That is why workforce optimization remains a top branch transformation priority.

The first wave of workforce strategies focused on expense reduction. The second wave has focused on strategies for growing revenue while simultaneously improving operational efficiency. Leaders in the next stage of banking transformation view their branch workforce as under-utilized assets and have been accelerating the use of advanced analytics to maximize value.

The following recommendations are based on the second annual survey of banking executives by Kiran Analytics and experience in deploying workforce optimization and talent acquisition solutions for leading retail banks in over 15,000 branches.

Evolve your workforce planning capabilities continuously with data and advanced analytics. Changes in

customer behaviors, market opportunities, new products, and branch technologies are inevitable. So are bank mergers, branch closures, openings, and redesigns. All of these changes impact daily staffing requirements which are different for each and every branch in the network. Intuition and one-size-fits-all approaches simply do not work.

Use predictive analytics to improve quality of universal banker hires. While 70% of bankers chose acquisition and

retention as a top workforce challenge, only 37% said their bank is using advanced analytics to tackle it. Since deploying universal bankers is a popular workforce strategy, and nearly half the banks are still investigating it, there is a significant opportunity to use predictive analytics for identifying and retaining top talent for universal bankers.

Key Takeaways

1

2

59%said human interactions was the top reason for customer branch visits

70% made workforce

optimization a top branch transformation initiative

70%chose acquisition and

retention as a top workforce challenge

37%are using advanced

analytics for acquisitionand retention

Branch Workforce Optimization Driven By Analytics 13

© 2016 Kiran Analytics, Inc. All rights reserved.

Align selling capacity to market opportunity to avoid under or overstaffing. Bankers ranked this as the second most

important workforce optimization priority. Only 8% rated it as optimal at their bank. When a branch is understaffed, sales opportunities are lost and service levels are compromised; when overstaffed, profitability is sacrificed. Use advanced analytics to resource the branches with just-right staffing levels and skill sets in order to meet sales and service targets.

Choose a workforce optimization solution that will help you stay ahead of the changes. Workforce decisions

based on simplistic or outdated software solutions cannot keep up with the change of pace in retail banking. Banks need modern workforce optimization software to make better workforce decisions faster. Select a solution that is easy-to-use for banking managers, easy-to-deploy and to

update in the field. For central workforce management teams, key considerations are high-fidelity, flexibility, and high-performance analytics. Key considerations for IT and compliance teams are solutions and applications made available through a secure, reliable, and highly available SaaS platform.

Partner with experts in workforce optimization for retail banks. Every industry has unique challenges, systems,

and solution requirements. Retail banking is quite different from other retail and service industries. Additionally, each and every bank is unique. Finally, within banks, there are significant differences between the requirements of branch workforce and contact center workforce optimization. Choose a workforce optimization partner that specializes in retail banking, understands the unique requirements of your bank, and the unique operational aspects of your line of business.

Key Takeaways continued

3

4

566%are using advanced analytics to address

overstaffing

68% rated their alignment of

selling capacity to market opportunity as average

31%are cross-selling through other channels to improve

performance

51%have implementeduniversal banker

staffing

© 2016 Kiran Analytics, Inc. All rights reserved.

Branch Workforce Optimization Driven By Analytics 14

INTELLIGENT BRANCH TRANSFORMATION®

Kiran Analytics drives intelligent branch transformation for retail banks through the application of predictive analytics.

Kiran’s solutions have been deployed in over 15,000 branches helping to forecast optimal branch staff levels accurately, hire better people faster, and to plan and schedule resources efficiently. As a result, retail banks increase sales and customer service while reducing operational costs. Our customers have saved tens of millions of dollars annually by transforming their recruiting, resource capacity planning, and branch staff optimization processes.

LaborScheduling

ResourceAlignment

TalentAcquisition

WorkforcePlanning

BranchTransformation

withPredictiveAnalytics

+1 858.270.9950