brazilian sugarcane sector: recent developments and the ... · 23/02/2018 · brazilian sugarcane...

TRANSCRIPT

Brazilian Sugarcane Sector: Recent Developments and the Path Ahead

Leticia PhillipsRepresentative - North America

USDA’s 94th Annual Agriculultural Outlook Forum

Arlington, February 23, 2018

About UNICA

The Brazilian Sugarcane Industry Association (UNICA) is the leading sugarcane industry association in Brazil. Its more than 120 membercompanies, voluntarily engaged, represent over 50% of the ethanol and 60% of the sugar produced in Brazil.

Representing the sector with public entities in Brazil and abroad, establishing a constructive dialogue with stakeholders, monitoring(and influencing) legislation related to biofuels, sugar and bioelectricity, promoting the Brazilian ethanol image as a clean and renewableand sustainable energy abroad.

It has offices in four locations: São Paulo (headquarters), Brasília, Washington DC and Brussels

8 billion gallons2nd world largest producer:25% of production and 20%of world exports

15 million MWh4% of Brazilian electricity consumption

40 million tonsLargest producer and exporter in the world: 20% of global production and more than 40% of exports

Breakdown of Sugarcane’s Energy

Energy equivalent of 1 ton of sugarcane

= 1.2 oil barrel

Source: UNICA

Exportação de açúcar pela região Centro-SulSugarcane in Brazil

Source: NIPE-Unicamp, IBGE and CTC. Elaboration: UNICA

90% of national production

Sugarcane

The Brazilian Sugar Market:

An overview

0

10

20

30

40

1989

/90

1990

/91

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

ProductionExportsDomestic consumption + stocks

Source: UNICA, MAPA and Brazilian Foreign Trade secretariat (SECEX). Note: * geometric growth rate

Production, exports and consumption (million tonnes)

Evolution of the Brazilian sugar market

0%

15%

30%

45%

60%19

59/1

960

1963

/196

4

1967

/196

8

1971

/197

2

1975

/197

6

1979

/198

0

1983

/198

4

1987

/198

8

1991

/199

2

1995

/199

6

1999

/200

0

2003

/200

4

2007

/200

8

2011

/201

2

2015

/201

6

Brazilian market-share in the world market

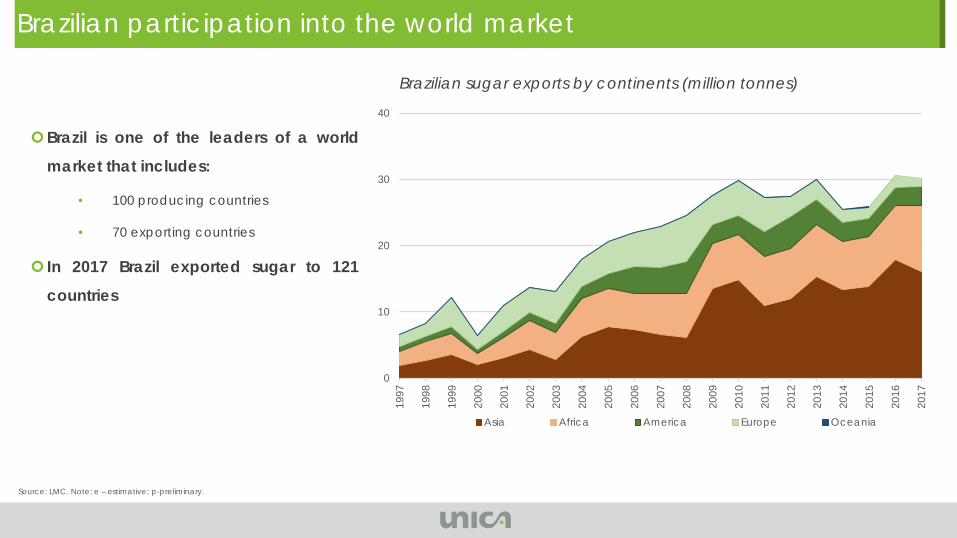

Source: LMC. Note: e – estimative; p-preliminary.

0

10

20

30

40

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Asia Africa America Europe Oceania

Brazilian participation into the world market

Brazil is one of the leaders of a world

market that includes:

• 100 producing countries

• 70 exporting countries

In 2017 Brazil exported sugar to 121

countries

Brazilian sugar exports by continents (million tonnes)

Challenges for the sugar industry

IstoÉ

-20

15

Stigmatization of sugar consumption

The Economist – 2016

Protectionist and distortive sugar policies across the globe

Thailand, India, China, United States and European Union

Região Centro-Sul: produtividade agrícola média na safraChallenges: Trade Issues

As of January 15th, 2018 the Thai government adopted a new regime, as a result of achallenge by Brazil. Brazilian government is analyzing the changes to ensure that it iscompliant with WTO rules

Brazil will defend its interest with respect to the safeguard measures promoted byChina - Brazil represented 60% of Chinese imports, Brazil the most affected country.

Continuous monitoring of potentially distortive public policies, by sugar producingcountries.

Brazil’s sugar quota in the US is smaller than DR’s

Quota established based on trade flows in the 80s

US sugar TRQ represents 0.5% of BR exports

The Brazilian Ethanol Market:

An overview

0

10

20

30

40

73/7

4

75/7

6

77/7

8

79/8

0

81/8

2

83/8

4

85/8

6

87/8

8

89/9

0

91/9

2

93/9

4

95/9

6

97/9

8

99/0

0

01/0

2

03/0

4

05/0

6

07/0

8

09/1

0

11/1

2

13/1

4

15/1

6

17/1

8

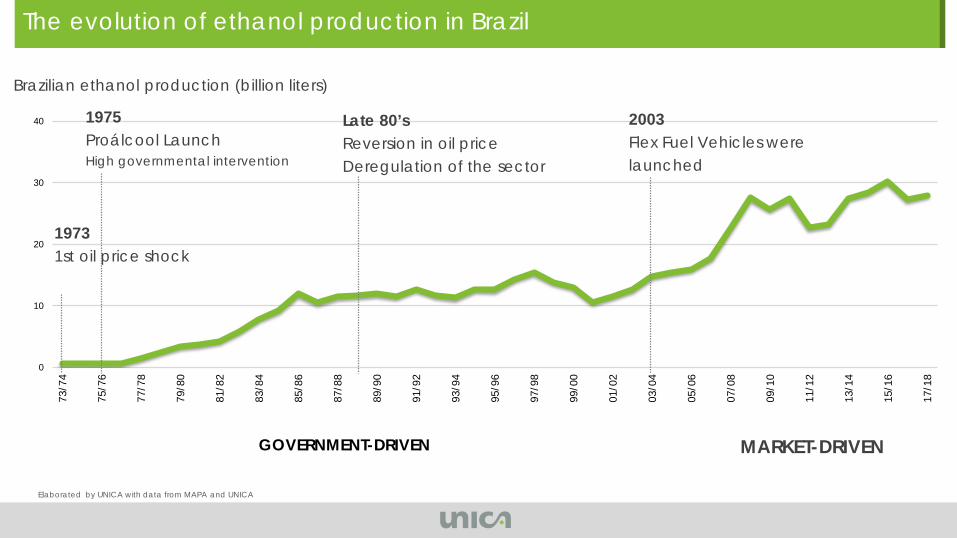

GOVERNMENT-DRIVEN

Elaborated by UNICA with data from MAPA and UNICA

19731st oil price shock

1975Proálcool LaunchHigh governmental intervention

Late 80’sReversion in oil priceDeregulation of the sector

2003Flex Fuel Vehicles were launched

MARKET-DRIVEN

The evolution of ethanol production in Brazil

Brazilian ethanol production (billion liters)

2,000

3,000

4,000

5,000

6,000

7,000

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

Historical productivity data in Brazil (liters of hydrous ethanol per hectare - moving average)

Expansion based on efficiency and productivity GAINS

In this period, ethanol yields

more than double

Up to the 2000’s, productivity

raised on average 3.5% p.y.

Productivity gains were even

more significant depending

on the region

With the RIGHT INCENTIVES, from both public policies and from the market, the

sugarcane sector responded POSITIVELY and TIMELY

Flex Fuel technology

Federal tax differential between fossil and renewable fuels

Reduction of VAT over hydrous ethanol

Rising oil prices

Competitive production costs

Global interest on biofuels and emission reduction alternatives

How did we get there?

What lays ahead?

2018/2019 Harvest

• UNICA still analyzing data to do a forecast

•Harvest update will be published in April, coinciding with the beginning of our harvest

•What we know so far?

•Harvest will favor ethanol production

•Sugar production will likely decrease

Recent Policy Changes

Trade Policy - Ethanol Tariff Rate Quota

• China and EU closed their markets to the US ethanol making Brazil the only market available to receive excess ethanol supplies

• US exported 660 MG to Brazil in 2017, three times more than 2016 exports (220MG) and five-times more than 2015 exports (135MG)

• UNICA acted to moderate the positions in the industry and produce a fair compromise -maintaining ethanol in MERCOSUR’s exception list

• August 2017 Brazilian government approved an import tariff of 20% on any import volume exceeding 158.5MG/year - quota is average annual import volume from 2014 - 2016

• Brazil’s TRQ represents about 16% of US ethanol exports.

• Tariff is valid for 2 years, starting September 2017. Temporary solution to what we hope is a temporary problem

• In Brazil sugar and ethanol are the same industry - NE producers are the most affected by lack of access to larger sugar quotas in markets like US and by imports of ethanol!

RenovaBio

Program promoted by the Department of Biofuels (DBIO)

of the Ministry of Mines and Energy (MME)

Highly important initiative to ensure emissions reduction

through the sustainable expansion of biofuels supply in

the country, guaranteeing the fulfillment of the

commitments signed in the Paris Climate Agreement and

increasing the guarantee of supply

43% reduction of GHG emissions by 2030 when

compared to 2005 levels

Mandate to reduce emissions

Today 2030

g CO2eq/MJ

Maximum level of GHG EMISSION BY ENERGY UNIT commercialized in

the form of fuels for the Brazilian fleet“x” grams of CO2eq. per

MegajouleGuarantee of supply

and in a sustainable manner

Establishment of PERIODIC DECARBONIZATION TARGETS for the fuel

sector

PREVISIBILITYand CLEAR RULES

Vital to promote INVESTIMENTS in the production and for development of other

government programs

How will decarbonization targets be met?

Each fuel will have a specificlevel of emissions, defined fromits LIFE CYCLE

Gasoline

Imported Ethanol

Brazilian Sugarcane Ethanol

Cellulosic Ethanol

Guarantee of incentives for the search for the highest

environmental and economic EFFICIENCY

g CO2eq. /MJCompetition between sources in meeting decarbonization targets

+

-

Incr

easin

g Le

vel o

f Em

issio

ns

How the RenovaBio works

Producer

Trade of CBio via Stock Exchange

Distributor Fueling Stations Consumer

Ethanol Gallons Ethanol Gallons Ethanol Gallons

MarketEmmission of Cbio 1 Cbio = reduction 1 t CO2eq

Acquisition of CBio

Individual TargetgCO2eq/MJ converted into the number of Cbios to be

acquired per unit of fossil fuel sold

Brazil’s Decarbonization

Target (gCO2eq/MJ)

� Next Steps

� Up to 6 months after sanction (June 2018): definition of targets

� 18 months after definition of targets: regulatory completion

� Effective from the beginning of 2020

Next Steps